Embed Size (px)

Citation preview

8/6/2019 Market Haven Monthly Newsletter - July 2011

http://slidepdf.com/reader/full/market-haven-monthly-newsletter-july-2011 1/11

MARKET HAVEN MONTHLYPAGE 1

T he market is showing some price volatility

centered around month end, the last days of

QE2, and the Greece bailout. For all the fanfare

of the -7% price drop in the S&P from the end of

April through the latter part of June, the VIX

never showed any real signs of fear.

In the end, the stock market remains somewhat

overvalued. I know there are traders who can’t

stand to miss a single second of a trading

session and there are high frequency trading

programs that endeavor to trade every

picosecond. I’m sorry, I just don’t see that much

changing in that short of a time span. In fact, the

world has been in a slow motion transition for a

couple of years now. There are legitimate

reasons phrases like “kick the can down the

road” and “extend and pretend” have been used.

There is a lot of forecasting (i.e., guessing) going

on about what is going to happen next. Inflation.

No, deflation. Perhaps hyperinflation, as

everybody grabs their guns and begin to shoot

each other. The collapse of our currency. The

collapse of the euro. A crash in China. I have less

of an issue with these types of speculative macro

outlooks than I do with such particulars as next

quarter’s earnings or interest rates over the next

six months.

Once we stop and admit that it’s all speculation,

we can get on with the business of trying to

make a rational decision about how to invest

based on what we can observe. Sure, there are

some events that seem more probable than

others. But we really don’t know until they

happen. And when we don’t know the future

(and I never have), we must rely on the most

rational observations we can. Now, if you have

some kind of competitive advantage because

you’re David Einhorn, Jim Simons or Pau

Tudor Jones, you may clearly dismiss me as a

mere mortal and I will take no offense at that.

For those of you who are human and are

interested in understanding how in the world

you can outperform the market witho

traveling the same path as the likes of Raj

Rajaratnam, we have really one main variable to

which to moor ourselves. That is price. When

you can’t tell the future, you buy as cheaply as

you can and then wait for things to play out.

Market Haven Monthly

2011

JULY

8/6/2019 Market Haven Monthly Newsletter - July 2011

http://slidepdf.com/reader/full/market-haven-monthly-newsletter-july-2011 2/11

MARKET HAVEN MONTHLYPAGE 2

Where’s the Va lue?

Stocks

Our Static Model is an easy way to hedge out

much of the market risk in an unemotional way.

Through regular rebalancing and a fairly

conservative asset allocation, the portfolio has

done a good job of dampening volatility risk.

The beta of our long portfolio has historically

been about 1.3 allowing investors to get full

market exposure while leaving some cash on the

sidelines. Net long exposure for the Static Model

is +50%. Our Timing Model, on the other hand,

factors in market valuations and adjusts market

exposure regularly. Net long exposure currently

is -30%.

Strategy StaticModel

TimingModel

Long Exposure +80% 0%

Short Exposure -30% -30%

Net Exposure +50% -30%

At 1320, market p/e’s finished the quarter at

16.8x. This is an optimistic valuation. It suggests

that the markets feel all warm and fuzzy aboutthe future. But that sure isn’t what I see in the

economic data. We continue to believe that

there is limited upside and lots of downside

potential from here. The Fed’s low interest rate

policy is the primary factor levitating the market

at these levels. QE2 is now finished and the Fed,

which supplied 70% of the Treasury purchases

up until month end will only be buying bonds to

roll over maturities. If they make good on this

promise to limit their involvement in the bond

market, then we believe weak demand should

drive up yields on Treasuries, thereby

dampening the return of stocks.

As expected, earnings have continued to move

away from trend. They are currently at +15%and rising. We expect this to continue for a few

more quarters, which could contribute to stock

gains. Eventually, that will change. We usually

see earnings reverse direction once they have

exceeded trend earnings by about +25%. A note

here: stock prices don’t always coincide with

downturns in earnings.

The rising yield environment has temporarily

flipped from rising to falling. Actually, this is a

positive for stocks. We’ll wait to see if that

continues now that QE2 has finished. Corporate

spreads have widened recently and are still in

the 80th percentile, which is not good for stock

returns.

Even though the markets could continue to

rally, it’s not worth the risk in our minds. We

believe investors at these levels would buying

based on sentiment or greed rather than sound

8/6/2019 Market Haven Monthly Newsletter - July 2011

http://slidepdf.com/reader/full/market-haven-monthly-newsletter-july-2011 3/11

MARKET HAVEN MONTHLYPAGE 3

rational valuation levels. When the music stops

someone will not have a chair. We’ll go ahead

and grab ours now, thank you.

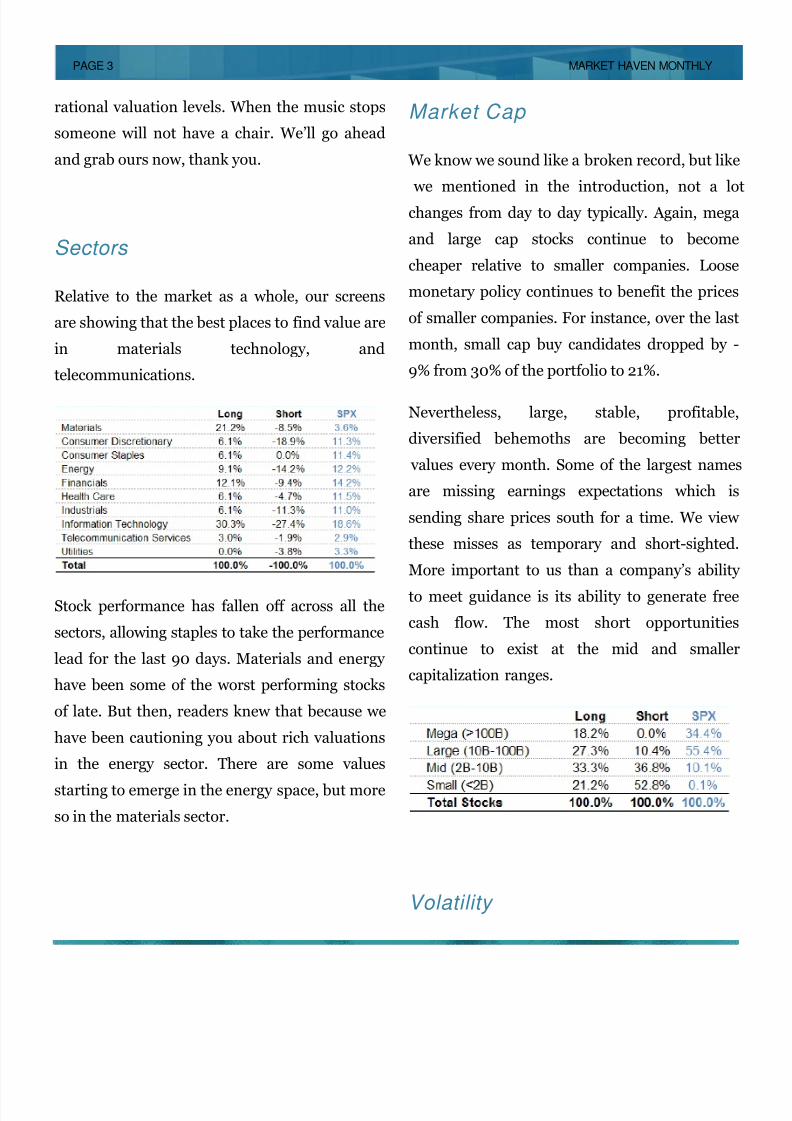

Sectors

Relative to the market as a whole, our screens

are showing that the best places to find value are

in materials technology, and

telecommunications.

Stock performance has fallen off across all the

sectors, allowing staples to take the performance

lead for the last 90 days. Materials and energy

have been some of the worst performing stocks

of late. But then, readers knew that because we

have been cautioning you about rich valuations

in the energy sector. There are some values

starting to emerge in the energy space, but more

so in the materials sector.

Market Cap

We know we sound like a broken record, but like

we mentioned in the introduction, not a lot

changes from day to day typically. Again, mega

and large cap stocks continue to become

cheaper relative to smaller companies. Loose

monetary policy continues to benefit the prices

of smaller companies. For instance, over the last

month, small cap buy candidates dropped by -

9% from 30% of the portfolio to 21%.

Nevertheless, large, stable, profitable,

diversified behemoths are becoming better

values every month. Some of the largest names

are missing earnings expectations which is

sending share prices south for a time. We view

these misses as temporary and short-sighted.

More important to us than a company’s ability

to meet guidance is its ability to generate free

cash flow. The most short opportunities

continue to exist at the mid and smaller

capitalization ranges.

Volatility

8/6/2019 Market Haven Monthly Newsletter - July 2011

http://slidepdf.com/reader/full/market-haven-monthly-newsletter-july-2011 4/11

MARKET HAVEN MONTHLYPAGE 4

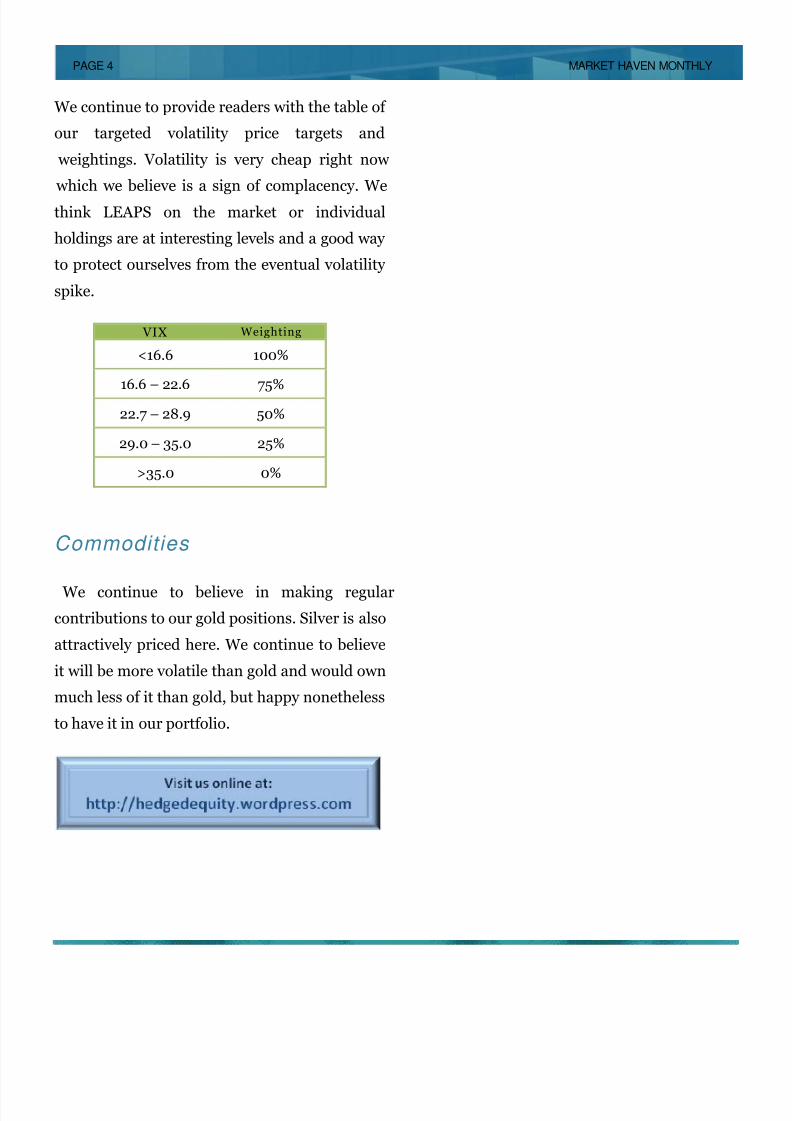

We continue to provide readers with the table of

our targeted volatility price targets and

weightings. Volatility is very cheap right now

which we believe is a sign of complacency. We

think LEAPS on the market or individual

holdings are at interesting levels and a good way

to protect ourselves from the eventual volatility

spike.

VIX Weighting

<16.6 100%

16.6 – 22.6 75%

22.7 – 28.9 50%

29.0 – 35.0 25%

>35.0 0%

Commodities

We continue to believe in making regular

contributions to our gold positions. Silver is also

attractively priced here. We continue to believe

it will be more volatile than gold and would own

much less of it than gold, but happy nonetheless

to have it in our portfolio.

8/6/2019 Market Haven Monthly Newsletter - July 2011

http://slidepdf.com/reader/full/market-haven-monthly-newsletter-july-2011 5/11

MARKET HAVEN MONTHLYPAGE 5

Some Investment Ideas

Here are a few names that have shown up

recently as potential investment ideas on our

screens. Some of these may appear in the

portfolios. Some may not simply because the

names currently in the portfolio haven’t worked

their way yet.

Diversification is an important part of our

investment process. We like to have north of 30

names in the long portfolio and 60 or more inour short portfolio. We let the ideas that are

working continue to run. Conversely, the ideas

that are not working become a smaller

proportion of the portfolio simply by the

diminishing market cap they exhibit. This also

lends to the comfort we have taking chances on

stocks that may have headline or operational

risk from time to time.

Don’t forget to do your own homework. We’re

not your financial advisor so we do not know

your specific financial situation and what

makes sense for you individually. Don’t take

anything we talk about as financial advice.

Freeport Mcmoran Copper & Gold

(FCX) - long

FCX is a $50 billion commodity company that

has operations all over the world. It is the

world’s second largest copper producer and is

also a major producer of gold and molybdenum.

Molybdenum is used in corrosion resistance and

has applications in steel production. For those

investors who are uncomfortable with pure gold

exposure, here is a way to leverage operational

exposure to commodities. FCX has an earnings

yield of 16% and a dividend yield of 2.8%. Cash

flow and return on equity is solid.

ASML Hold ing NV (ASML) - long

ASML is the world’s third largest supplier o

semiconductor manufacturing equipment. They

are a $16 billion company based in the

Netherlands. It is in a very cyclical industry and

not for the faint-hearted. Its return on equity is

37% and the company has a p/e of 7.5x. There is

some risk in this stock.

Eli Lilly (LLY) - long

You are probably already familiar with this $43

billion pharmaceutical company. More popular

brand names include Zyprexa (schizophrenia),

Cymbalta (antidepressant), Alimta (cancer),

Gemzar (cancer), Humalog (diabetes), and

Cialis (erectile dysfunction). It has a 5.2% yield,

an enterprise value / EBITDA of 7x, and an ROE

of 32%. Like other drug makers, we believe the

stock is a cash cow that will eventually benefit

8/6/2019 Market Haven Monthly Newsletter - July 2011

http://slidepdf.com/reader/full/market-haven-monthly-newsletter-july-2011 6/11

MARKET HAVEN MONTHLYPAGE 6

from the increased demand of an aging

demographic.

KKR & Company LP (KKR) - long

KKR is a global asset manager with various

operations in three primary segments that

include the private, public, and capital markets.

The company has a good reputation and a global

presence which they plan to leverage in order to

make further inroads into Asian emerging

markets. The stock seems cheap at 6.5x earnings

and 2.3x book. It has a dividend yield of 5.1%.

Resea rch In Motion (RIMM) - long

We know that we recommended RIMM back in

November 2010. Since that time it has dropped -

48%. We don’t have any better visibility on the

company than anyone else. In fact, they may be

going the way of the dinosaur. Technology is a

hard space in which to invest. We recognize

that. What we do know is that the company has

a a solid balance sheet with no debt, a p/e of

5.3x, an EV/EBITDA of 2.7x, high ROEs and a

product that still has a solid presence. When the

sentiment is this negative on a company this

profitable, we believe it is worth an investment.

8/6/2019 Market Haven Monthly Newsletter - July 2011

http://slidepdf.com/reader/full/market-haven-monthly-newsletter-july-2011 7/11

MARKET HAVEN MONTHLYPAGE 7

Portfolio Changes Last Month

In the long portfolio we made no trades

during the month.

There were no trades in the short portfolio

for the month.

Previously Mentioned Ideas

Below are the investment ideas that we have

highlighted in past issues. Additionally, we have

updated the current model recommendation for

each stock.

May 2011

Power-One Inc. (PWER) – buy

Banco Macro (BMA) – buy

Innophos Holdings (IPHS) – buy

Tim Participacoes SA (TSU) – buy

LAM Research Corporation (LRCX) – buy

April 2011

Vale S.A. (VALE) – buy

Rio Tinto Plc (RIO) – buy

ON Semiconductor (ONNN) – buy

IBM (IBM) – buy

Par Pharmaceuticals (PRX) – buy

Marc h 2011

CNOOC Limited (CEO) – buy

Credicorp Limited (BAP) – buy

Abbott Laboratories (ABT) – buy

Newmont Mining Corp (NEM) – buy

Harris Corp (HRS) – buy

February 2011

LHC Group (LHCG) – buy

Compania Cervecerias Unidas SA (CCU) – hold

NetEase.com Inc (NTES) – hold

Aflac Inc. (AFL) – buy

Microsoft Corp. (MSFT) – buy

January 2011

Amedisys (AMED) – hold

Warnaco Group (WRC) – buy

Alliance Resource Parnters LP (ARLP) –buy

BHP Billiton ADR (BHP) – buy

8/6/2019 Market Haven Monthly Newsletter - July 2011

http://slidepdf.com/reader/full/market-haven-monthly-newsletter-july-2011 8/11

8/6/2019 Market Haven Monthly Newsletter - July 2011

http://slidepdf.com/reader/full/market-haven-monthly-newsletter-july-2011 9/11

MARKET HAVEN MONTHLYPAGE 9

Long Portfolio

Below is the long portfolio at month end. Anyone interested in viewing the short portfolio may contact us and we will be happy to provide the breakdown.

8/6/2019 Market Haven Monthly Newsletter - July 2011

http://slidepdf.com/reader/full/market-haven-monthly-newsletter-july-2011 10/11

MARKET HAVEN MONTHLYPAGE 10

Newsletter Portfolio Performanc e

8/6/2019 Market Haven Monthly Newsletter - July 2011

http://slidepdf.com/reader/full/market-haven-monthly-newsletter-july-2011 11/11

MARKET HAVEN MONTHLYPAGE 11

Newsletter Portfolio Performanc e