Embed Size (px)

Citation preview

Market Entry and Company Incorporation

October 9, 2012

♣

presented byAjay Sethi FCA – Managing Partner, ASA & Associates

Mathias Niehaus CPA – Partner, optegra:hhkl

1www.asa.in

PRESENTATION OUTLINE

Segment I

India Tour

Location Search in India

Indian Partner – Why? How?

Avoiding Pitfalls

Segment II

Understanding Regulatory Compliance

FDI Norms – an Overview

Investment Strategy

Policy Framework22

www.asa.in

INDIA TOURSome Facts

33www.asa.in

Our Current Concerns

Growth Rate (Projected 9.0% v/s Outlook 5.5%)

Rising Inflation (touching double digits)

Dip in FDI (78 % dip in June ‘12 YOY)

Reforms in Slow Motion (resistance from coalition partners)

4www.asa.in

4Source – Department of Industrial Policy and Promotion as on September 2012 5

GDP

The Growth Story

www.asa.in

6

Inflation

www.asa.inSource – Department of Industrial Policy and Promotion as on September 2012

FDI INFLOWS (Top Ten Countries) (in USD million)

Rank Country 2010‐2011 2011‐12 Cumulative Inflows(Apr ‘00 – June ‘12)

% of total Inflows

1 Mauritius 6987 9942 65608 38

2 Singapore 1705 5257 17555 10

3 UK 755 9257 16314 9

4 Japan 1562 2972 12663 7

5 USA 1170 1115 10710 6

6 Netherlands 1213 1409 7652 4

7 Cyprus 913 1587 6603 4

8 Germany 200 1622 4880 3

9 France 734 663 2988 2

10 UAE 341 353 2301 1

7

Foreign Direct Investment – Country wise

www.asa.inSource – Department of Industrial Policy and Promotion as on September 2012

figures in US$ millionCumulative Inflows (April ‘00 – June ‘12)

8

Foreign Direct Investment – Sector wise

www.asa.inSource – Department of Industrial Policy and Promotion

Subsidy on diesel reduced

Bank rates increased

Multi brand retail allowed

Civil Aviation opened

Broadcasting (DTH) opened

9

Reforms Aimed at Accelerating Foreign Direct Investment (Sept 2012)

www.asa.in

21

Direct Tax Code (April 1, 2013 - doubtful)

New Companies Bill (awaited)

Indirect Taxes - Goods & Services Tax (April 1, 2013 - doubtful)

International Financial Reporting Standards (deferred)

10

Policy Framework – On the Horizon

www.asa.in

LOCATION SEARCH

11www.asa.in

Key Index

Port

Automobile

Chemicals

ITMumbai

Bengaluru

Chennai

GUJARAT

UTTAR PRADESH

KARNATAKA

RAJASTHAN

MAHARASHTRA

TAMIL NADU

City

KERALA

ANDHRA PRADESH

Delhi /Gurgaon/Noida

Pune

HARYANA

12

Identifying a Good Location

www.asa.in

13

Key Index

Mumbai - Chennai Freight Corridor (Approved)

Delhi – Kolkata Freight Corridor Delhi – Mumbai Industrial Corridor

Dedicated Freight Corridors

www.asa.in

State

Important Industrial

Area(Dealing

Authority)

Approx Cost

(in € / sq mts)

Ease of Acquiring Land Key Factors

Haryana(North)

Udyog ViharManesarKundli(HSIDC)

440160100

Involves liaisoning. Authorities are vested with high discretionary powersLow Availability

• Fully developed industrial belt

• Auto components in close vicinity

Rajasthan(North)

NeemranaKhushkhera(RIICO)

35

Defined documentation and regular follow-ups required High Availability

• Semi developed industrial belt

• Within easy reach of Haryana i.e. an alternate

HSIDC - Haryana State Industrial & Infrastructure Development Corporation LtdRIICO - Rajasthan State Industrial Development & Industrial Corporation€ 1 = INR 70 (approx)

14

Industrial Areas – Sample study

www.asa.in

State

Important Industrial

Area(Dealing

Authority)

Approx Cost

(in € / sq mts)

Ease of Acquiring Land Key Factors

Tamil Nadu(South)

Orgadam, Sriperambadur, Hosur(SIPCOT, TIDCO)

29 and above

Land allotment discretionary, involves active liaisoningMedium Availability

• 3 key ports within radius• Facing South East Asia

(Thailand)• Some areas developed.

New under process

Gujarat(West)

Sanand, Mehsana(GIDC)

Upto 29

Transparent process; strict adherence to conditions High Availability

• Important future port on 2 freight corridors

• Facing Middle East & Europe market

• Industrial area under development

SPICOT - State Industries Promotion Corporation of Tamil Nadu LtdTIDCO - Tamil Nadu Industrial Development Corporation LtdGIDC - Gujarat Industrial Development Corporation€ 1 = INR 70 (approx) 15

Industrial Areas – Sample study

www.asa.in

Demand-Supply scenario, Competition analysis, Distribution networks?

Quality of Infrastructure (water, power, land, roads, quality of labor)?

Logistics and easy access to resources taken into consideration?

If land is required, have you considered future expansion plans?

Have you considered various Municipal Level Taxes?

Have you considered effect of Social Security Schemes?

16

Initial Feasibility & Location Study

www.asa.in

Retail

Logistics

Healthcare

Food Processing

Defence Supplies

Real Estate Development

17

A Few Promising Sectors

www.asa.in

INDIAN PARTNER

18www.asa.in

Pros

Operating Infrastructure

Ready Distribution Channel

Government Dealing

Labor Management

Cons

Management and Control

Dilution of Profits

Protection of Technology, Trademarks and Trade

Names

2919

Why an Indian Partner?

www.asa.in

Indian partner looks at a business horizon of 3-5 years to measure the

returns on investment

The Indian partner will aim at faster turnaround in negotiations, basically, a

‘top-down’ management approach

You should discuss in detail, management control issues viz. appointment

to the board of directors, chairman of the board, appointment of CEO, MD

and CFO, issues arising from future change of control, non-compete, etc.

20

Understanding Your Indian Partner

www.asa.in

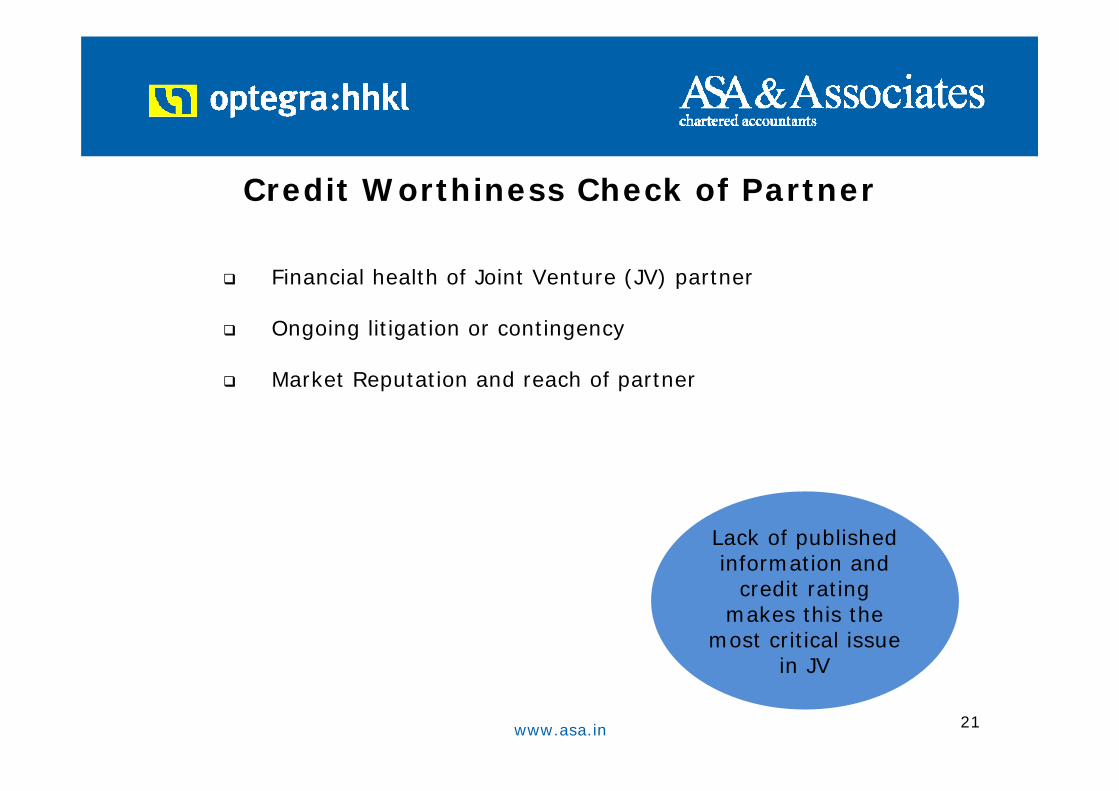

Financial health of Joint Venture (JV) partner

Ongoing litigation or contingency

Market Reputation and reach of partner

30

Lack of published information and

credit rating makes this the

most critical issue in JV

21

Credit Worthiness Check of Partner

www.asa.in

3122

Sources

www.asa.in

Median EBITDA Multiples (All Sectors)

Source: Mergermarket

Source: Capital IQ

23

Rationalising Valuations

www.asa.in

Source: Mergermarket

Announced Date Target Company Bidder Company Stake Acquired

Deal Value EBITDAUSD (mn) Multiple

SELECTED DEALS 2011 & 2012 01-09-2012 JSW Ispat Steel JSW Steel 53.30% 1,350 7.2401-08-2012 Genpact Bain Capital 30.50% 1,004 10.8510-01-2011 Patni Computer Systems iGate Corporation 83.60% 1,213 7.4821-03-2012 Mahindra Satyam Tech Mahindra 57.40% 921 9.1021-05-2012 Thomas Cook Fairbridge Capital 77.00% 141 11.7923-11-2011 Neo Structo Construction Bilfinger Berger NA 80 8.3607-01-2011 APW President Systems Schneider Electric 75.00% 19 6.6201-08-2012 PVR L Capital Eco 11.10% 10 6.54

SELECTED DEALS 2006 28-08-2006 Matrix Laboratories Mylan Inc 71.50% 723 401-12-2006 Gemini TV Sun TV Network NA 603 23.0130-01-2006 Ambuja Cements Holcim 20.00% 564 14.6404-04-2006 MphasiS BFL Electronic Data Systems Corp. 51.70% 342 21.7910-03-2006 Spice Communications Axiata Group Berhad 49.00% 179 12.2814-05-2006 Zuari Cement Ciments Francais 50.00% 54 18.6222-11-2006 Geojit Financial Services BNP Paribas SA 33.40% 46 16.6614-09-2006 GPI Textiles Avenue Capital Group 40.00% 33 15.5004-12-2006 Adani Retail Reliance Industries NA 22 30.6107-09-2006 Capgemini Business Services Capgemini 51.00% 11 30.98

24

Rationalising Valuations

www.asa.in

3225

Joint Venture - Documentation

www.asa.in

Term Sheet – Some Key Guidelines

3326www.asa.in

Shareholding structure has a major bearing on the quality of management, its ability to decide and respond to business dynamics.

The law broadly recognizes the following power thresholds for shareholders:

3427

Shareholding Structure

www.asa.in

10 Per Cent & Above - Minority Control

Calling an extraordinary general meeting on requisition - Section 169

Demand for Poll during voting - Section 179

Investigation of affairs of company - Section 235

Prevention of oppression of minority shareholders and to preventmismanagement of the company - Section 399

35

Less than 10 per cent

deprives the above rights

28

Shareholding Structure

www.asa.in

51 Per Cent & Above - Simple Majority

Section 79 – Issue of shares at a discount specifying the maximum rate, subject to sanction of Company Law Board

Section 81(4) - Issue of further shares with Government’s consent where special resolution is not passed

Section 94(2) - Alteration of share capital

contd

3629

Shareholding Structure

www.asa.in

51 Per Cent & Above - Simple Majority

Declaration of Dividend - Section 205

Adoption of Annual Accounts & Director’s report - Section 210

Appointment of external auditor - Section 224

Appointment of Director, Managing Director – Section 256, Section 269

37

Shareholding 50:50– High Chances of deadlock in case of

disagreement amongst the partners; all of

above powers compromised. 30

Shareholding Structure

www.asa.in

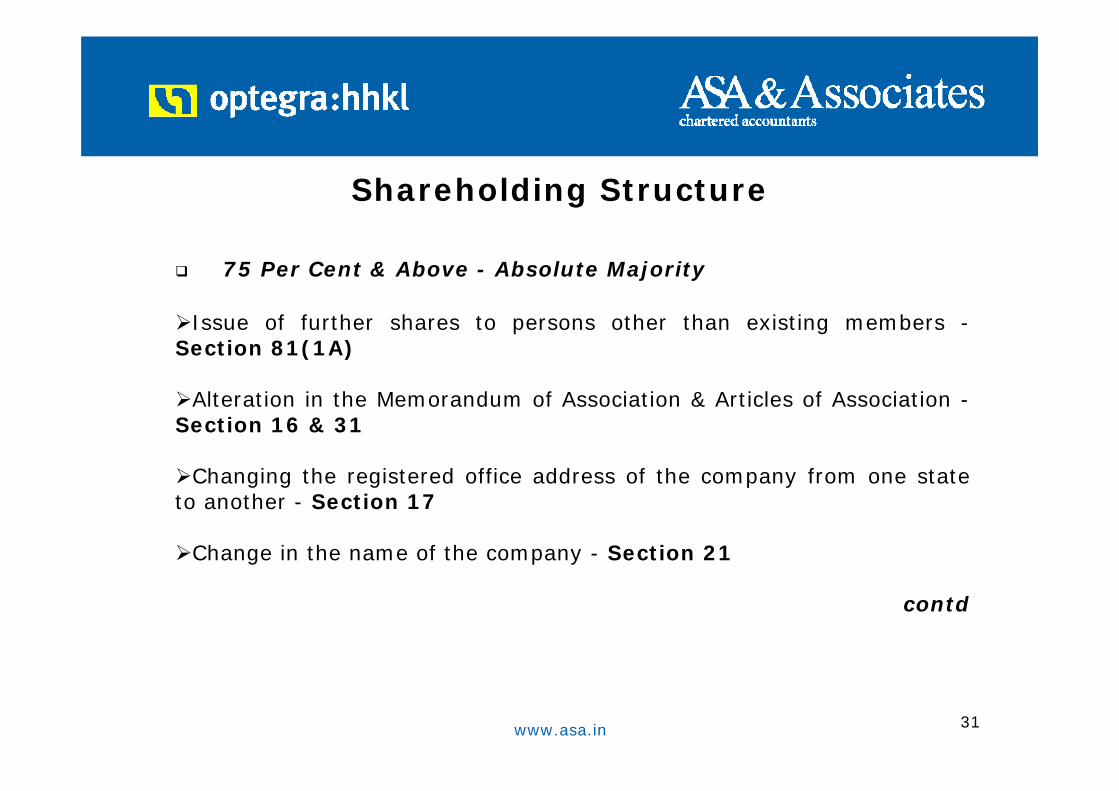

75 Per Cent & Above - Absolute Majority

Issue of further shares to persons other than existing members -Section 81(1A)

Alteration in the Memorandum of Association & Articles of Association -Section 16 & 31

Changing the registered office address of the company from one state to another - Section 17

Change in the name of the company - Section 21

contd

3831

Shareholding Structure

www.asa.in

75 Per Cent - Absolute Majority

Buy-back of shares - Section 77A

Reduction of share capital - Section 100

Winding up a company by Court - Section 433(a)

Voluntary Winding up a company - Section 484(1) (b)

39

Virtual control of the company; suitable for

technology providers or where customers have

global commitments and firm order available

32

Shareholding Structure

www.asa.in

AVOIDING PITFALLS

33www.asa.in

Reserved Matters – An important tool

Alteration of the structure of issued capital

Issue of shares and other securities

Transfer of shares

Change in constitution of the Board of Directors

Hiring key Managers

Declaration of any dividend, other distribution

4034

Shareholding Structure

www.asa.in

• Arms’ Length price (ALP) - Any income arising from an international transaction between associated parties to be computed having regard to ALP. ALP means the price which is applied in a transaction between persons other than associated enterprises

• Associated Enterprise (AE) - Participation in management or control or capital of other enterprise. Directly through intermediaries

35

TRANSFER PRICING - Ensuring that transactions between group companies are at market price?

www.asa.in

Germany payment? supply of goods

India

servicingwarranty etc.

Holding Company

Wholly Owned

SubsidiaryCustomer

Transfer Pricing Issue – what should be the

profit margin of the Wholly

Owned Subsidiary?

Advanced Pricing

Agreements

36

TRANSFER PRICING - Determining the appropriate pricing for group companies transactions

www.asa.in

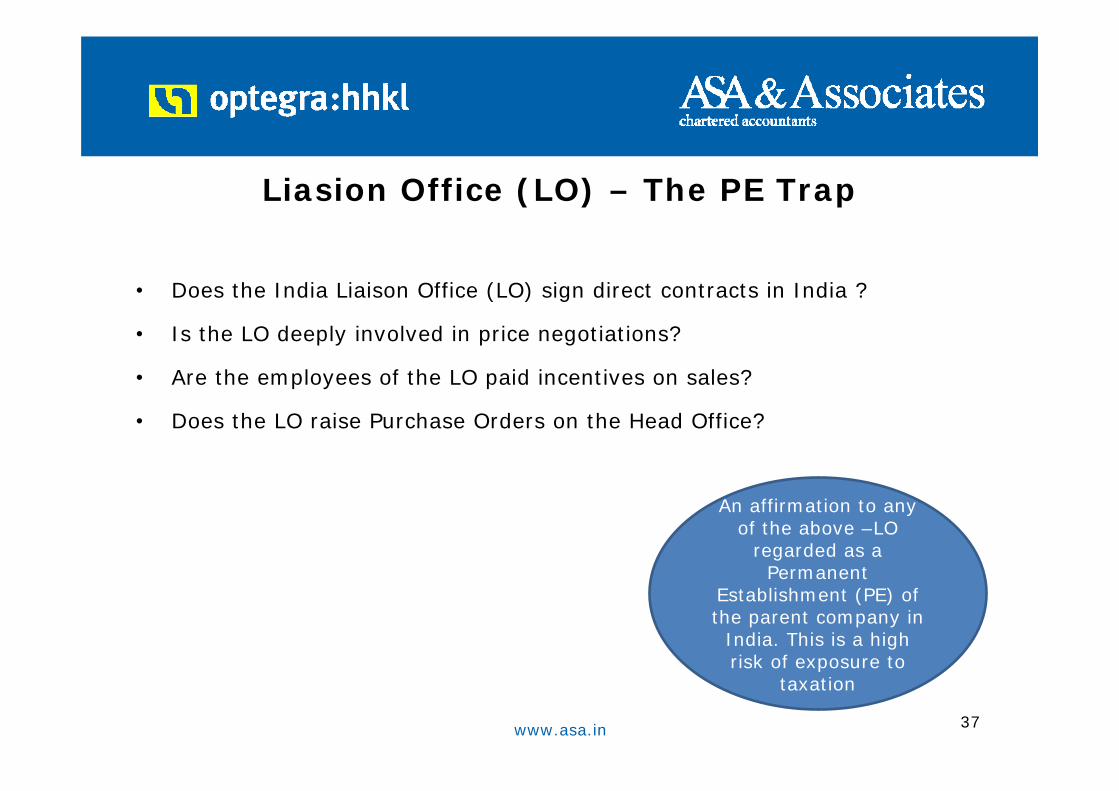

• Does the India Liaison Office (LO) sign direct contracts in India ?

• Is the LO deeply involved in price negotiations?

• Are the employees of the LO paid incentives on sales?

• Does the LO raise Purchase Orders on the Head Office?

An affirmation to any of the above –LO

regarded as a Permanent

Establishment (PE) of the parent company in

India. This is a high risk of exposure to

taxation

37

Liasion Office (LO) – The PE Trap

www.asa.in

Whether the credit in respect of

Dividend Distribution Tax

(DDT) of INR 17 is available in the Parent Country?

X – India

Parent Company

X – German Company

Government Treasury

IndiaGermany

INR 17

INR 83

Net Profit 133

Tax on Profit 33

Distributable Profit 100

Amount in INR

38

Repatriating Profits – The issue of Dividend Distribution Tax

www.asa.in

Segment II

Mathias Niehaus Partner, optegra:hhkl

39www.asa.in

Most laws originate from British Laws

Procedure Driven

Failures to comply usually leads to penalty and sometimes prosecution

Stacked in favor of labor(blue collar staff)

Fine reading and interpretation is the norm

40

Understanding Regulatory Compliance

www.asa.in

13

Pre 1991

1991

1997

2000

2000-10

Allowed selectively up to 40%

Up to 74/51/50% in 112 sectors under theautomatic route 100% in some sectors

Up to 100% under automatic route in all sectors except a small negative list

More sectors opened, Equity caps raised in many other sectors, procedures simplified

FDI up to 51% allowed under the automatic route in 35 priority sectors

41

Evolving FDI Policy

www.asa.in

12

Social focus becomes high priority

Infrastructure becomes prime focus with guided government expenditure e.g.Delhi Mumbai Industrial Corridor

Streamlining archaic laws viz. Items reserved for Small Scale Industries (abolished) Fringe Benefit Tax (abolished) Goods and Services Tax (concept laid) Direct Tax Code (placed for public opinion) New Companies Bill (set in motion)

Look East Policy set in motion through Free Trade Agreement (FTA) with Korea, Thailand, etc

Stronger Corporate Governance – E-governance project of the Ministry of Corporate Affairs

YEARS 2006-2012

42

Aiming for Inclusive Growth

www.asa.in

FDI Norms – an Overview

43www.asa.in

Lotteries, gambling and betting

Atomic energy (but India likely to buy half a dozen nuclear plants in the near future)

Retail shops (but foreign companies can open single-brand shops)

Real Estate Business

Tobacco Products

44

Inbound Investments - Industry out of Bounds

www.asa.in

Banking, Insurance and Finance Companies

Defence, Mining and Strategic Industries

Air Transport Services

Telecommunication

Single Brand and Multi Brand retailing

Arms and military supplied

Media, Broadcasting, Satellite

Security Agencies

45

Inbound Investments – Industries where Government Permission is required

www.asa.in

Sector/ Activity FDI Cap/ Equity Entry Route

Civil Aviation 49% Automatic

Multi Brand Product Retail 51% Approval based

NBFC 100% Automatic

Broadcasting49% (FDI + FII)74% (FDI + FII)

AutomaticApproval based

Power Exchange 49% (FDI – 26% + FII – 23%)

FII – AutomaticFDI – Approval based

Defence 26% Approval based

46

Inbound Investments – Industries with Cap on Investments

www.asa.in

The rest of the field is open

47www.asa.in

There are thousands of firms in many industries

Family-owned enterprises often run into management crises, look for

saviors

The market for skilled personnel is at last getting organized

State governments compete to attract enterprises

Investing has become easier now

48

Investment Strategy – Why India

www.asa.in

Going alone makes more sense now

Government interference in industry has declined, so a partner is not

necessary as intermediary

The market for skilled personnel has become organized, so it is

possible to recruit management

It is also now possible to buy running companies

49

Investment Strategy – Subsidiary

www.asa.in

If you still prefer joint ventures

The top 100 Indian firms have more choice today and are more difficult to

attract

But there are thousands of mid-sized companies (technologically strong)

and smaller companies (mostly family-managed) which are still available

But put in place a management structure which gives you an effective

voice

50

Investment Strategy – Joint Venture

www.asa.in

INDIA

Head Office Representation

Local Subsidiary

DistributionChannel

Liaison Office

Project Office

Branch Office Wholly Owned Subsidiary

Joint Venture

Importer

C&F Agents

Franchisee

German Corporate

Limited Liability Partnership

1051

India Entry - Mode of Investment

www.asa.in

Corporate[CO]

Liaison Office[LO]

Project Office[PO]

Branch Office[BO]

Limited Liability Partnership (LLP)

Characteristics Share capital owned by parent company

No commercial activities allowed

Temporary site office, specific projects

Commercial activities allowed

Commercial activities allowed

Status Shareholders Foreign Company

Foreign Company

Foreign Company

Partnership

Tax Rate 30% + + Non Taxable 40% + + 40% + + 30% ++

Control Board of Directors

Parent Company

Parent Company

Parent Company

Partners

Set-up FIPB Approval / Automatic Route (8-12 weeks)

RBI approval(8 weeks)

RBI approval(8 weeks)

RBI approval(8 weeks)

FIPB & ROLLP Approval

Closure ROC (12-15 months)

RBI(3-6 months)

RBI(3-6 months)

RBI(6-8 months)

(15-18 months)

RBI – Reserve Bank of IndiaFIPB – Foreign Investment Promotion BoardROC – Registrar of CompaniesROLLP – Registrar of Limited Liability Partnership

1152

India Entry – Alternate Entity Comparison

www.asa.in

Liaison Office (Companies exploring business opportunities in India)

Pro – Ease of setting-up and shutting-down

Con – Limited scope of operations

Branch Office (Research & development companies)

Pro – Simple structure with less compliances

Con – Approval is discretionary and taxability is high

53

Investment StrategyInbound Investments – Entry Options

(Unincorporated Entity)

www.asa.in

Project Office (Companies involved in one time turnkey or installation projects)

Pro – Ease of setting-up

Con – Applicable only in specific cases. Tax litigation possible

Limited Liablility Partnership (Corporate structure with benefit of limited

liability and flexibility of partnership)

Pro – A corporate structure without the Dividend Distribution Tax (DDT)

Con – Regulations Untested

54

Investment StrategyInbound Investments – Entry Options

(Unincorporated Entity)

www.asa.in

Forms of Corporate

Public Private

Minimum Capital (approx.) EURO 8,600 EURO 1,700

Members – MinimumMaximum

7 2

NA 50

Minimum Directors 3 2

Listing on stock exchange Permissible Not Permissible

Reporting requirements High Low

55

Investment StrategyInbound Investments – Entry Options

(Corporate)

www.asa.in

56

Company Incorporation

www.asa.in

AVOIDING PITFALLSWhile Setting-Up a Company

57www.asa.in

• Name should not resemble existing entity in India

• Similar names requires no objection certificate from pre-existing entities

• Specific words (such as ‘India’) have minimum prescribed government fee

• Name approval is valid for 60 days, reapplication thereafter

Future Litigation, risk of suspension of operations till the

requirements are met or the name is changed

58

Selecting a name for your Indian Company

www.asa.in

• State Stamp Duties must be considered while deciding the location

• The main object should be clear and specific to the main activity

• The Memorandum and Articles of Association must be drafted carefully, for

a Joint Venture (JV), the agreed terms must be incorporated therein

• Specific words have minimum prescribed government fee

• Name is reserved for 60 days, reapplication is required thereafter

Risk of JV Partner not abiding with the JV

Agreement!

59

Avoiding Common Errors

www.asa.in

Investments against issue of shares or convertible debentures or preference shares

Reporting to Reserve Bank Of India (RBI) must be done within 30 days from the date of remittance

Equity instruments should be issued within 180 days from the date of inward remittance else the amount should be refunded immediately

Non-compliance reckoned as a

contravention could attract penalty up to

3 times of the amount involved

60

Reporting to Exchange Control Authorities

www.asa.in

The shares or convertible debentures between resident to non resident Compliance with sectoral caps and relevant regulations Sales proceeds can be repatriated outside India, net of taxes

Pricing guidelines must be adhered to Listed companies –Securities Exchange Board of India (SEBI)

guidelines Unlisted companies - not less than fair value of shares determined by

a Merchant Banker or a Chartered Accountant as per the Discounted Free Cash Flow Method (DCF)

The Transfer should be reported to RBI within 60 days of

receipt of consideration

61

Acquisition of shares through a private arrangement

www.asa.in

Pre-incorporation expenses such as rent, feasibility study

Verification and certification by the statutory auditor

Foreign Inward Remittance Certificates of funds received from overseas promoters for the expenditure incurred must be arranged

The applications, complete in all respects, for capitalisation being made within the period of 180 days from the date of incorporation of the company

The applications, must be made

within 180 days from the date of incorporation of

the company

62

Pre-Incorporation Expenses

www.asa.in

THANK YOU

63www.asa.in