Embed Size (px)

Citation preview

MAR 2011MEGAMORPHOSIS II - MUMBAI

CORE ISSUES & FUTURE GROWTH

VISION & CONCEPT OPTIONS

THE REGIONAL CONCEPT PLAN

THE REGIONAL CONCEPT PLAN

PROJECT MILESTONE

Phase 0

Investigation

Phase 1

Planning Strategy & Structure Development

Phase 2Draft

Regional Plan Phase 3

Final Regional Plan

Jun 2010

Jun 2011

Jul 2011

Phase 4

Local Plan & Urban Design

Mar 2010

Sep 2010

Project Duration of 66 weeks

From March 2010 to July 2011

Phase 5

Implementation Strategy

Phase 6

Final Submission

Steering Committee / Stakeholders Meetings

Draft/ Final Report Submission

Apr 2010

Nov 2010

Apr 2011

Current Project Status

• Vibrancy & Density

• Efficient but not sufficient public transport

• Magnificent but untapped heritage

• Slums & super luxury properties

• National Park, mangroves & polluted air

• Scenic waterfront & polluted water

• Resilient & Innovative

The exciting Mumbai

EXPANDING ECONOMY & POPULATION

Overall Demographic Profile:

• Expanding population from 25mil in 2008 to between 38 mil and 44 mil by 2052

• Labour market rising to between 20.4 mil and 23.2 mil

Growth Rate & Centre:

• CAGR-basis projection => GDP growth taken for entire block of years up to 2052

• Anticipated faster growth rate in RoMMR than GM

• Increasing contribution to MMR GDP from RoMMR with more new developments

• GDP per capita rising to Rs 1mil by 2052Scenarios GDP Growth Rate GM to MMR Ratio

MMR GM RoMMR 2008 2032 2052

Moderated Case

7% 6.3% 7.7% 0.6 0.5 0.45

Base Case 7.4% 7% 7.9% 0.6 0.55 0.5

Stretched Case

9% 8% 10% 0.6 0.45 0.4

RISING DEMAND FOR WORK SPACES

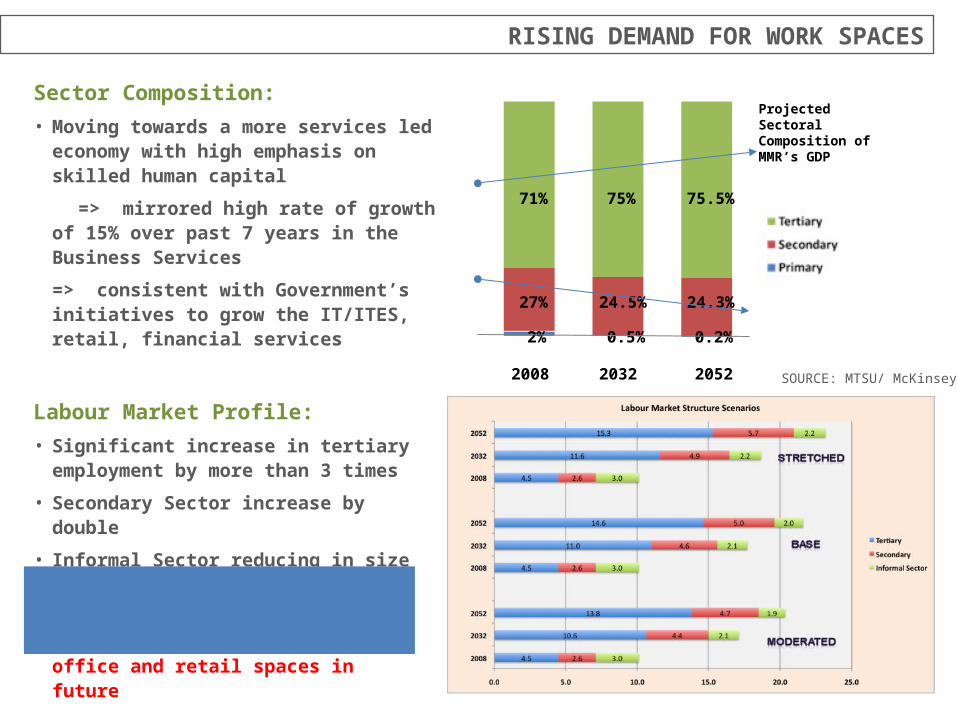

Sector Composition:

• Moving towards a more services led economy with high emphasis on skilled human capital

=> mirrored high rate of growth of 15% over past 7 years in the Business Services

=> consistent with Government’s initiatives to grow the IT/ITES, retail, financial services

SOURCE: MTSU/ McKinsey

71%

27%

2%

75%

24.5%

0.5%

75.5%

24.3%

0.2%

2008 2032 2052

Projected Sectoral Composition of MMR’s GDP

Labour Market Profile:

• Significant increase in tertiary employment by more than 3 times

• Secondary Sector increase by double

• Informal Sector reducing in size but still remaining

• Pointing to a consistent and high demand for commercial office and retail spaces in future

MORE AFFORDABLE HOUSING NEEDED

HOUSEHOLD INCOME PER ANNUM, INR

NUMBER OF HOUSEHOLDS IN MILLIONS

2010 2020 2032 2052Less than 90,000 0.7 0.41 0.06 090,000 - 200,000 2.53 1.61 0.51 0.04200,000 - 500,000 2.79 4.35 6.22 0.76500,000 - 1,000,000 0.12 1.34 2.8 6.621,000,000 - 1,500,000 0.03 0.21 0.41 4.441,500,000 - 2,500,000 0.06 0.13 0.21 2.22Above 2,500,000 0.03 0.06 0.1 0.74Total households 6.34 8.11 10.36 14.81

REGIONS2010 2020 2032 2052

Prevailing rates

Growth Scenario

Projected rates

Growth Scenario

Projected rates

Growth Scenario

Projected rates

Cluster 1South Mumbai 65,000

High201,500

Moderate566,215

Low1,024,849

Central Mumbai 25,000 77,500 217,775 394,173Western Mumbai 35,000 108,500 304,885 551,842

Cluster 2East Mumbai & Thane 10,000

High 31,000 High 120,900 High 1,160,640Navi Mumbai 8,500 26,350 102,765 986,544

Cluster 3Vasai-Virar 3,200

High 9,920 High 38,688 Moderate 216,653Mira Bhayandar 4,500 13,950 54,405 304,668

Cluster 4Kalyan 3,400

High10,540

High41,106

Moderate230,194

Karjat-Khopoli 1,700 5,270 20,553 115,097Pen-Alibaug 1,500 4,650 18,135 101,556

Note: All rates are in Rs/ sq. ft. Rise in property rates is based on a high growth assumption for MMR

NEED FOR COMPREHENSIVE TRANSPORTATION SYSTEM

• Public transport mode remains high at 78%

• Total trips in future will be almost 1.7 times to 2 times of the trip volume recorded in 2005

• Hence, much more comprehensive road & rail networks are expected

• Domestic air travel demand could increase to 35mil passengers

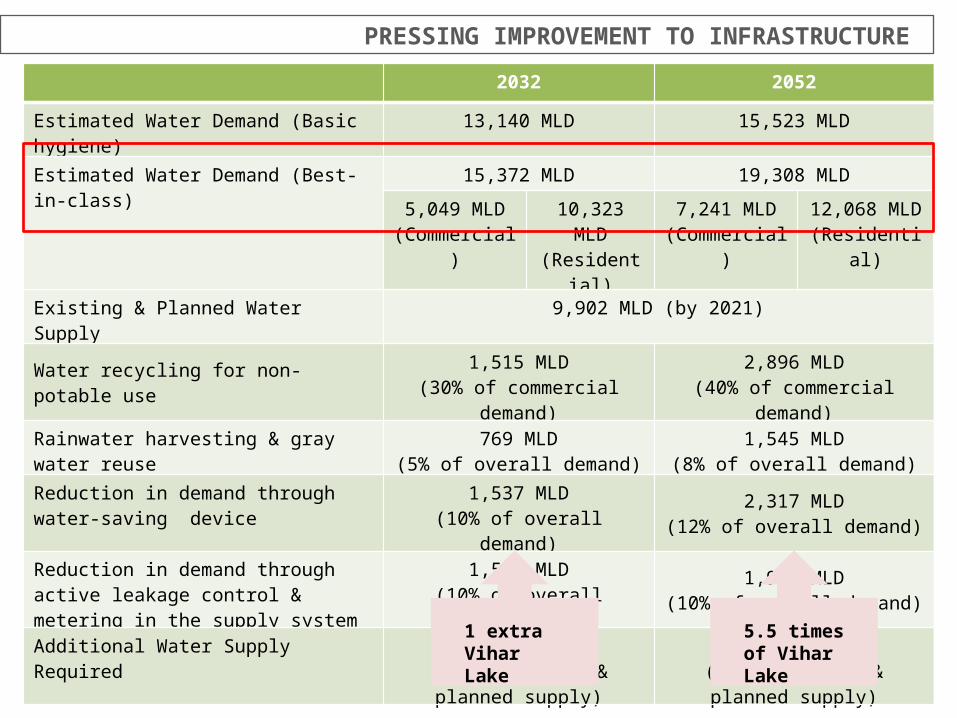

PRESSING IMPROVEMENT TO INFRASTRUCTURE

2032 2052

Estimated Water Demand (Basic hygiene) 13,140 MLD 15,523 MLD

Estimated Water Demand (Best-in-class) 15,372 MLD 19,308 MLD

5,049 MLD (Commercial)

10,323 MLD (Residential)

7,241 MLD(Commercial)

12,068 MLD(Residential)

Existing & Planned Water Supply 9,902 MLD (by 2021)

Water recycling for non-potable use 1,515 MLD(30% of commercial demand)

2,896 MLD(40% of commercial demand)

Rainwater harvesting & gray water reuse 769 MLD(5% of overall demand)

1,545 MLD(8% of overall demand)

Reduction in demand through water-saving device

1,537 MLD(10% of overall demand)

2,317 MLD(12% of overall demand)

Reduction in demand through active leakage control & metering in the supply system

1,537 MLD(10% of overall demand)

1,931 MLD(10% of overall demand)

Additional Water Supply Required 112 MLD(1.1% of ext’g & planned supply)

605 MLD(6.1% of ext’g & planned supply)

1 extra Vihar Lake

5.5 times of Vihar Lake

PRESSING IMPROVEMENT TO INFRASTRUCTURE

Sewerage

Solid Waste

OVERALL BROAD LAND AREA REQUIREMENTS

Existing 2032 2052 Remarks

Forest/wetland & water body

31%1,350 sqkm

31% 31% Forest , wetland and water body to be retained

Agriculture/ waste /scrubland

54%2,350 sqkm

39% 29%

Urbanized area (%)AreaDensity (ppl/sqkm)

15%650 sqkm40,000

<30%1300 sqkm27,000

<40%1734 sqkm23,000 Shanghai City : 24,000

Housing & facilities 40% 520 sqkm

40%694 sqkm

Industries, Logistics, Commercial & mix use space

20%260 sqkm

20%346 sqkm

European cities: 30%US cities: 10%Singapore : 19% (future goal)

Parkland (main recreational parks)

10%130 sqkm

12%208 sqkm

Singapore : 20% (future goal)

Infra/utilities

25%325 sqkm

23%399 sqkm

European cities: 18 %US cities: 36 %Singapore :22% (future goal)

Special use (military & other special uses)

5 %65 sqkm

5 %87 sqkm

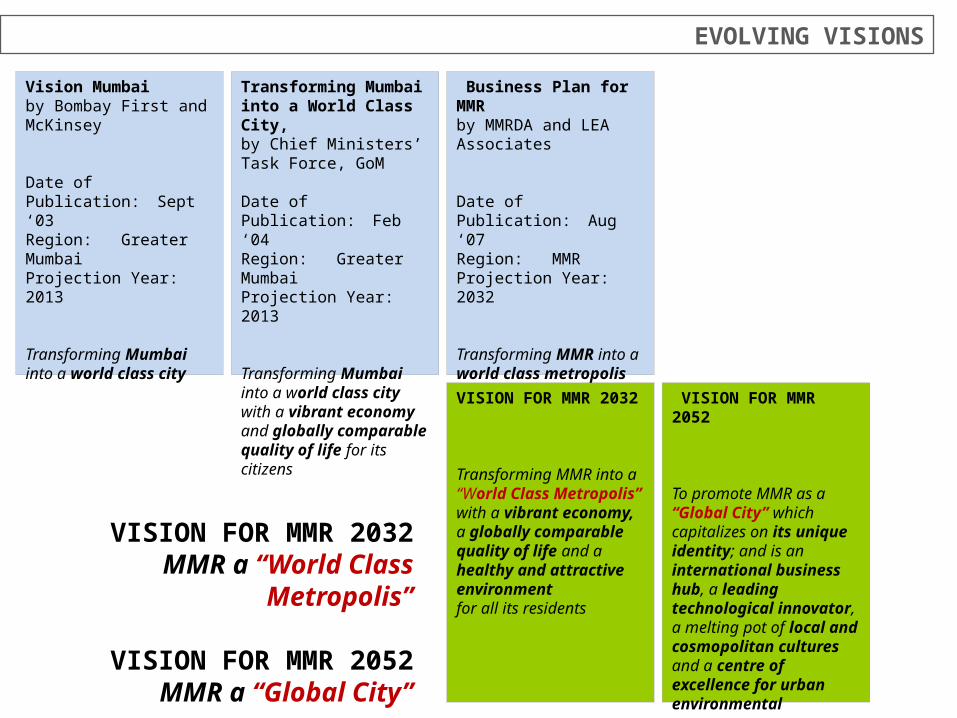

EVOLVING VISIONS

Vision Mumbai by Bombay First and McKinsey

Date of Publication: Sept ‘03

Region: Greater Mumbai Projection Year: 2013

Transforming Mumbai into a world class city

Transforming Mumbai into a World Class City, by Chief Ministers’ Task Force, GoM

Date of Publication: Feb ‘04

Region: Greater Mumbai Projection Year: 2013

Transforming Mumbai into a world class city with a vibrant economy and globally comparable quality of life for its citizens

Business Plan for MMRby MMRDA and LEA Associates

Date of Publication: Aug ‘07

Region: MMRProjection Year: 2032

Transforming MMR into a world class metropolis with a vibrant economy and globally comparable quality of life for all its citizens

VISION FOR MMR 2032

Transforming MMR into a “World Class Metropolis” with a vibrant economy, a globally comparable quality of life and a healthy and attractive environmentfor all its residents

VISION FOR MMR 2052

To promote MMR as a “Global City” which capitalizes on its unique identity; and is an international business hub, a leading technological innovator, a melting pot of local and cosmopolitan cultures and a centre of excellence for urban environmental management.

VISION FOR MMR 2032MMR a “World Class Metropolis”

VISION FOR MMR 2052MMR a “Global City”

* The Concept Plan for Mumbai Metropolitan Region is Voluminous.

For Further Information Contact

Bombay First

Email: [email protected] Contact: 022 22810070/71

![Untitled-1 [spaceforte.com]LTD. OFFICE IN MUMBAI, DESIGNED BY AR. SUNDEEP KARKHANIS. Navi Mumbai 20 Mar 2014 Text: Keshia D'souza Photographs: Prashant Bhat lines and rich anishes](https://img.dokumen.tips/doc/110x75/60095dcd74fb2f6e27503c84/untitled-1-ltd-office-in-mumbai-designed-by-ar-sundeep-karkhanis-navi-mumbai.jpg)