Embed Size (px)

Citation preview

Contributions to Management Science

Managerial Discretion and Performance in China

Towards Resolving the Discretion Puzzle for Chinese Companies and Multinationals

Bearbeitet vonHagen Wülferth

1. Auflage 2013. Buch. xxiii, 534 S. HardcoverISBN 978 3 642 35836 4

Format (B x L): 15,5 x 23,5 cmGewicht: 997 g

Wirtschaft > Management > Unternehmensführung

Zu Inhaltsverzeichnis

schnell und portofrei erhältlich bei

Die Online-Fachbuchhandlung beck-shop.de ist spezialisiert auf Fachbücher, insbesondere Recht, Steuern und Wirtschaft.Im Sortiment finden Sie alle Medien (Bücher, Zeitschriften, CDs, eBooks, etc.) aller Verlage. Ergänzt wird das Programmdurch Services wie Neuerscheinungsdienst oder Zusammenstellungen von Büchern zu Sonderpreisen. Der Shop führt mehr

als 8 Millionen Produkte.

Literature Review and Hypotheses 2

This chapter conducts a thorough, in-depth review of both the empirical and the

theoretical literature on the impact of managerial discretion on performance.

The literature review is used for fulfilling four purposes within the present study:

1. Deriving the research gap and research objective (see Sect. 1.1 and 1.2).

2. Formulating the postulate and hypotheses (see Sects. 2.4.2 and 2.4.3).

3. Selecting the unit of analysis (see Chap. 3).4. Developing the study’s new discretion model (see Chap. 4).

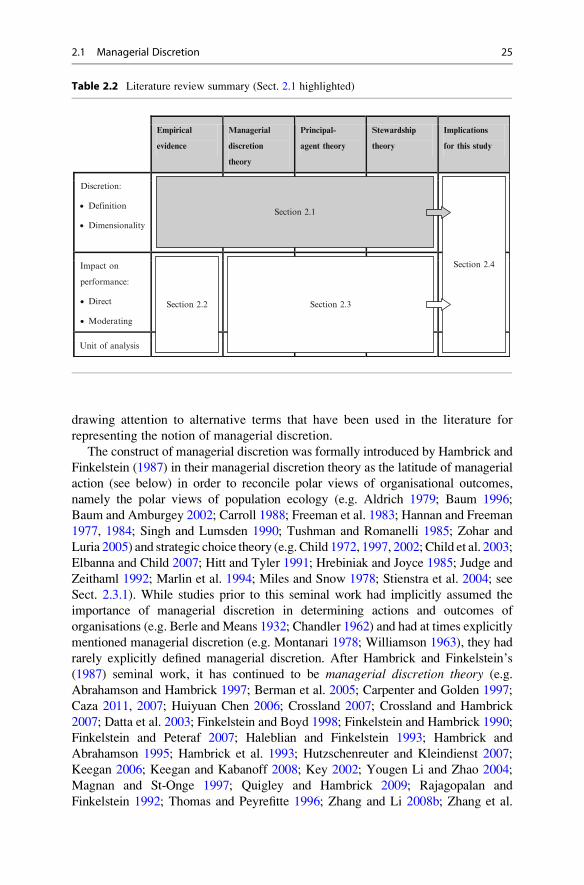

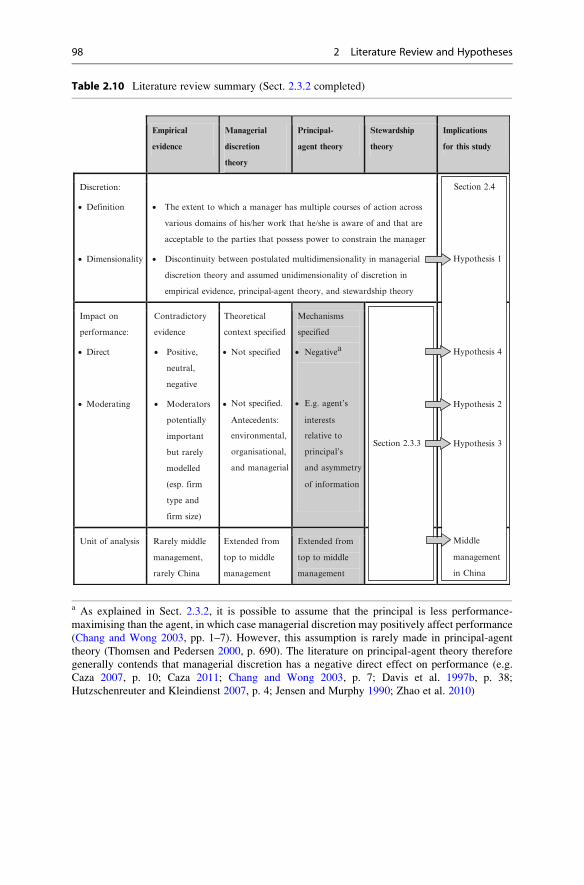

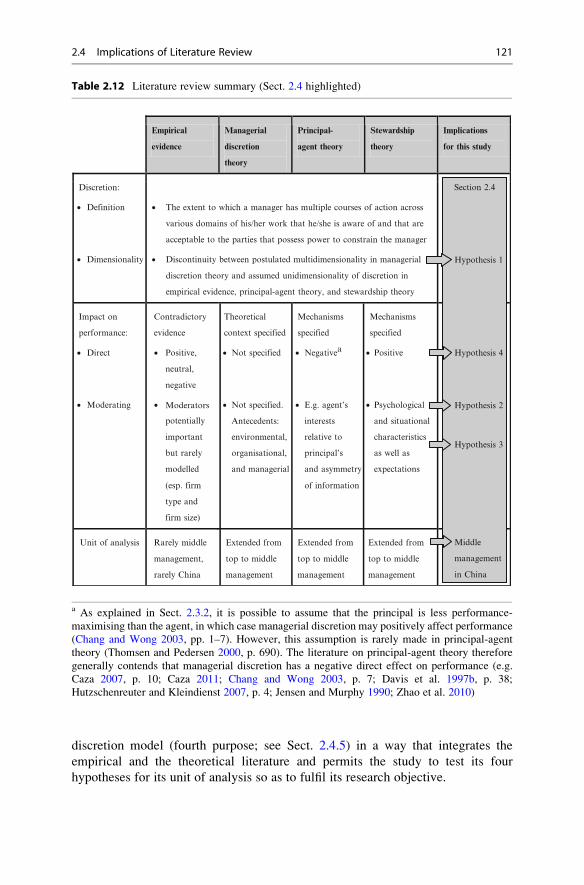

The literature review is structured according to Table 2.1. As indicated by the

rows in Table 2.1, the topics reviewed cover managerial discretion as such (i.e. its

definition and dimensionality), the impact of managerial discretion on performance

(i.e. its direct effect and moderating effects), and the unit of analysis. For each topic,

both the empirical and the theoretical literature are utilised, as represented by the

columns in Table 2.1. The table is completed throughout this chapter in the

following sequence:

• Section 2.1 discusses both the empirical and the theoretical literature for mana-

gerial discretion as such (i.e. its definition and dimensionality).

• Section 2.2 reviews the empirical literature on the impact of managerial discre-

tion on performance, including which units of analysis have been used.

• Section 2.3 reviews the theoretical literature on the impact of managerial

discretion on performance (managerial discretion theory, principal-agent theory,

and stewardship theory), including which units of analysis have been chosen.

• Section 2.4 synthesises the previous sections into implications for the present

study with a focus on formulating the study’s postulate and hypotheses. The other

three purposes are addressed only briefly, as they are further scrutinised in other

chapters (see Chap. 1 for the research gap and research objective, Chap. 3 for the

unit of analysis, and Chap. 4 for the study’s new model).

H. Wulferth, Managerial Discretion and Performance in China,Contributions to Management Science, DOI 10.1007/978-3-642-35837-1_2,# Springer-Verlag Berlin Heidelberg 2013

23

2.1 Managerial Discretion

As noted above, this section discusses both the empirical and the theoretical literature

on managerial discretion, since managerial discretion is the construct that lies at the

heart of the present study. First, Sect. 2.1.1 derives the definition of managerial

discretion from the literature, which forms the basis for measuring discretion in the

study’s empirical model in Chap. 4. Thereafter, Sect. 2.1.2 explores the literature with

respect to the dimensionality of managerial discretion, which again is important for

measuring discretion in the present study’s model and leads to the formulation of the

study’s first hypothesis. Applying the format of Table 2.1, Table 2.2 summarises that

this section reviews the empirical and theoretical literature on managerial discretion,

which generates implications for this study (such as the formulation of Hypothesis 1).

2.1.1 Definition of Managerial Discretion

The present section explores the literature on managerial discretion theory (see

Sect. 2.3.1), principal-agent theory (see Sect. 2.3.2), and stewardship theory (see

Sect. 2.3.3) in an effort to provide a sound definition of managerial discretion. This

forms the basis for measuring discretion in the study’s empirical model in Chap. 4.

The section begins by briefly reviewing the origins of the literature on discretion

before turning to its definition. Discretion is defined in general terms and as applied

to the study’s unit of analysis. This section concludes by explaining why manage-

rial discretion is important—which derives directly from its definition—and by

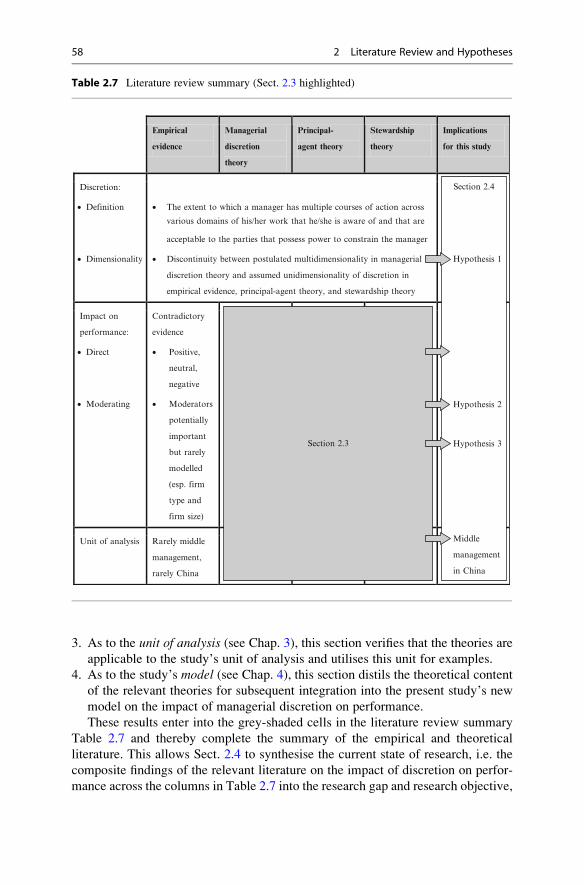

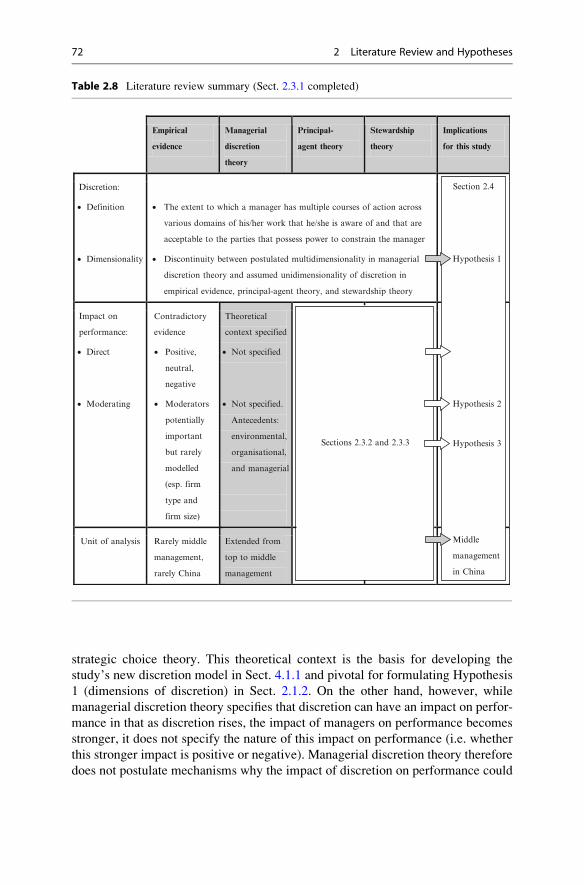

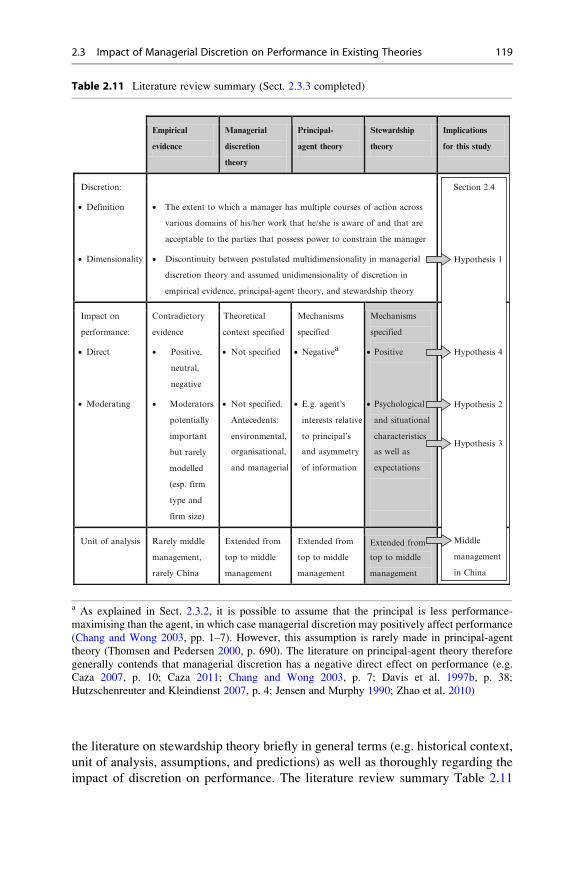

Table 2.1 Literature review summary (blank)

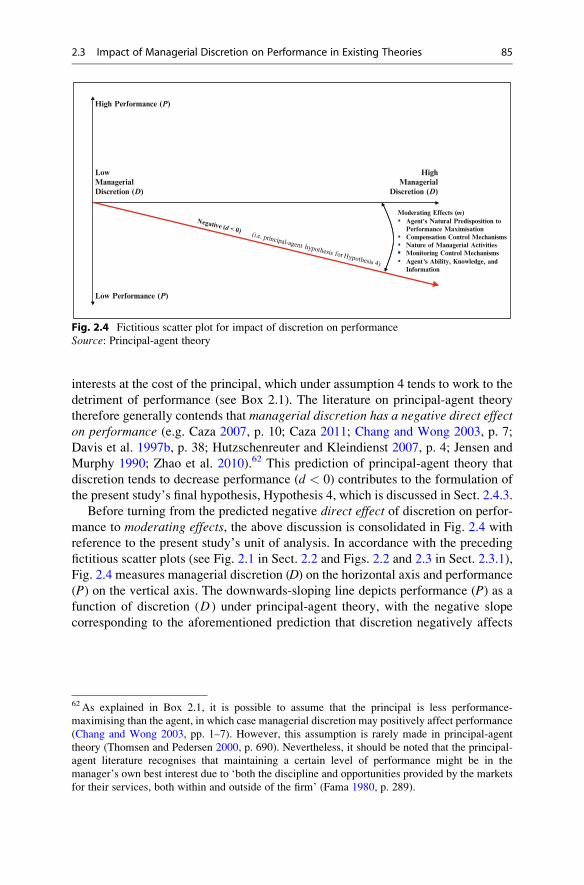

Empirical

evidence

Managerial

discretion

theory

Principal-

agent theory

Stewardship

theory

Implications

for this study

Discretion:

• Definition

• Dimensionality

Impact on

performance:

• Direct

• Moderating

Unit of analysis

Section 2.1

Section 2.2 Section 2.3

Section 2.4

24 2 Literature Review and Hypotheses

drawing attention to alternative terms that have been used in the literature for

representing the notion of managerial discretion.

The construct of managerial discretion was formally introduced by Hambrick and

Finkelstein (1987) in their managerial discretion theory as the latitude of managerial

action (see below) in order to reconcile polar views of organisational outcomes,

namely the polar views of population ecology (e.g. Aldrich 1979; Baum 1996;

Baum and Amburgey 2002; Carroll 1988; Freeman et al. 1983; Hannan and Freeman

1977, 1984; Singh and Lumsden 1990; Tushman and Romanelli 1985; Zohar and

Luria 2005) and strategic choice theory (e.g. Child 1972, 1997, 2002;Child et al. 2003;

Elbanna and Child 2007; Hitt and Tyler 1991; Hrebiniak and Joyce 1985; Judge and

Zeithaml 1992; Marlin et al. 1994; Miles and Snow 1978; Stienstra et al. 2004; see

Sect. 2.3.1). While studies prior to this seminal work had implicitly assumed the

importance of managerial discretion in determining actions and outcomes of

organisations (e.g. Berle and Means 1932; Chandler 1962) and had at times explicitly

mentioned managerial discretion (e.g. Montanari 1978; Williamson 1963), they had

rarely explicitly defined managerial discretion. After Hambrick and Finkelstein’s

(1987) seminal work, it has continued to be managerial discretion theory (e.g.

Abrahamson and Hambrick 1997; Berman et al. 2005; Carpenter and Golden 1997;

Caza 2011, 2007; Huiyuan Chen 2006; Crossland 2007; Crossland and Hambrick

2007; Datta et al. 2003; Finkelstein and Boyd 1998; Finkelstein and Hambrick 1990;

Finkelstein and Peteraf 2007; Haleblian and Finkelstein 1993; Hambrick and

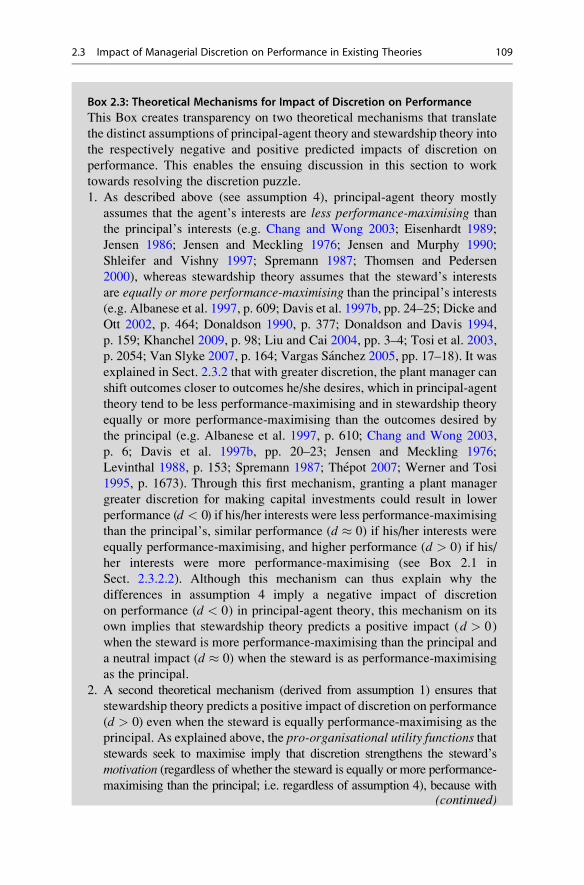

Abrahamson 1995; Hambrick et al. 1993; Hutzschenreuter and Kleindienst 2007;

Keegan 2006; Keegan and Kabanoff 2008; Key 2002; Yougen Li and Zhao 2004;

Magnan and St-Onge 1997; Quigley and Hambrick 2009; Rajagopalan and

Finkelstein 1992; Thomas and Peyrefitte 1996; Zhang and Li 2008b; Zhang et al.

Table 2.2 Literature review summary (Sect. 2.1 highlighted)

Empirical

evidence

Managerial

discretion

theory

Principal-

agent theory

Stewardship

theory

Implications

for this study

Discretion:

• Definition

• Dimensionality

Impact on

performance:

• Direct

• Moderating

Unit of analysis

Section 2.1

Section 2.2 Section 2.3

Section 2.4

2.1 Managerial Discretion 25

2006a, b) rather than principal-agent theory (e.g. Agrawal and Knoeber 1996;

Baysinger and Butler 1985; Berger et al. 1997; Brush et al. 2000; Chang and Wong

2003; Childs and Mauer 2008; Denis et al. 1997; Eisenhardt 1989; Fama 1980;

Fama and Jensen 1983a, b; He et al. 2009; Jensen 1986; Jensen and Meckling 1976;

Jensen and Murphy 1990; Jensen and Ruback 1983; Laffont and Martimort 2002;

Lang et al. 1995; Levinthal 1988; Ongore 2011; Shleifer and Vishny 1997;

Spremann 1987; Thepot 2007; Thomsen and Pedersen 2000; Walters 1995;

Wang et al. 2008; Weidenbaum and Jensen 1993; Werner and Tosi 1995, p. 1673;

Xu et al. 2005; Zou 1989) or stewardship theory (e.g. Albanese et al. 1997;Arthurs andBusenitz 2003; Corbetta and Salvato 2004; Davis et al. 1997a, b; Dicke and Ott 2002;

Donaldson 1990; Donaldson andDavis 1989, 1991, 1993, 1994, p. 159; Eddleston and

Kellermanns 2007; Fox and Hamilton 1994; Lane et al. 1999; Liu and Cai 2004;

Miller and Le Breton-Miller 2006; Mills and Keast 2009; Muth and Donaldson 1998;

Salvato 2002; Tian and Lau 2001; Tosi et al. 2003; Van Slyke 2007; Vargas Sanchez

2001, 2004, 2005; Zahra 2003) that has paid the most attention to defining discretion.

Nevertheless, while the definition of discretion in this study therefore derives mainly

from managerial discretion theory, it is consistent with the definitions implicitly used

in principal-agent theory and stewardship theory:

• Contributions to principal-agent theory (e.g. Burkart et al. 1997; Childs and

Mauer 2008; He et al. 2009; Lang et al. 1995) have tended not to explicitly define

managerial discretion, which continues a tendency from new institutional eco-

nomics (Williamson 1963) to pay relatively limited attention to defining the

construct of managerial discretion. This is exemplified by Williamson’s (1963)

paper, which despite carrying the title ‘Managerial Discretion and Business

Behavior’ shies away from explicitly defining discretion. Nevertheless,

Williamson’s (1963) implicit definition of managerial discretion as the latitude

of managers to pursue their own (non-profit-maximising) objectives1 is consis-

tent with the seminal definition by Hambrick and Finkelstein (1987,

pp. 371–378) discussed below. Similarly, more recent studies on principal-

agent theory (e.g. Burkart et al. 1997; Childs and Mauer 2008; He et al. 2009;

Khanchel 2009, p. 97; Lang et al. 1995; Spremann 1987, p. 10) employ the term

managerial discretion—often without explicitly defining it—with an implicit

meaning that concurs with managerial discretion theory.2

1Although Williamson (1963) embeds managerial discretion in an economic theory of the firm

using the notion of expense preference, he does not offer a definition of the term. However, it is

implicit in his work that managerial discretion is viewed as the latitude of managers to pursue their

own (non-profit-maximising) objectives, particularly in terms of channelling the firm’s monopoly

profits to discretionary expenses that benefit the management, such as top management compen-

sation. Williamson (1963) finds some empirical evidence that is consistent with this view, i.e. that

given opportunities for high discretion (e.g. high entry barriers and high internal representation on

the board of directors), discretionary expenses tend to be higher.2 Some studies on principal-agent theory explicitly mention discretion and define it in a way

consistent with Hambrick and Finkelstein’s (1987, pp. 371–378) definition, such as defining

discretion ‘as managers’ decision-making latitude’ (Chang and Wong 2003, p. 2) or as

‘control rights’ (Shleifer and Vishny 1997, p. 742).

26 2 Literature Review and Hypotheses

• Stewardship theory has likewise placed little emphasis on defining the construct

of managerial discretion and in this regard resembles principal-agent theory

rather than managerial discretion theory. Nevertheless, although stewardship

theory therefore makes no substantial contribution to defining the construct of

discretion, it does mention discretion and uses it in a way consistent with the

definition of managerial discretion provided below (see Sect. 2.3.3; e.g. Davis

et al. 1997b, pp. 25–26; Fox and Hamilton 1994, pp. 70–74; Hambrick and

Finkelstein 1987, pp. 371–378; Mills and Keast 2009, pp. 14–15; Van Slyke

2007, pp. 165–167; Vargas Sanchez 2005, p. 19).

According to the widely-accepted definition by Hambrick and Finkelstein (1987,

pp. 371–378), managerial discretion (or simply discretion)3 is defined as the ‘latitude

of managerial action’, namely the extent to which a manager has multiple courses ofaction (or choices or decisions) across various domains of his/her work that he/sheis aware of and that are acceptable to the parties that possess power to constrain themanager. For instance, the managerial discretion of a plant manager (i.e. the unit of

analysis) measures the extent to which the plant manager has multiple choices across

such domains as making capital investments or hiring workers that he/she is

aware of and that are acceptable to corporate headquarters in China. In particular,

a plant manager with the discretion to undertake small and large capital investments

without prior authorisation from corporate headquarters in China has greater

latitude of action (i.e. discretion) in the domain of making capital investments

than a plant manager who is constrained to making only small capital investments.

As this definition of managerial discretion has been widely accepted in the literature

(e.g. Abrahamson and Hambrick 1997, p. 513; Carpenter and Golden 1997, p. 187;

Caza 2007, p. 27; Chang and Wong 2003, p. 2; Crossland 2007, p. 1; Crossland and

Hambrick 2007, p. 767; Finkelstein and Boyd 1998, p. 179; Finkelstein and

Hambrick 1990, p. 484; Hambrick and Abrahamson 1995, p. 1427; Hambrick and

Finkelstein 1987, pp. 371–378; Rajagopalan and Finkelstein 1992, p. 32), it is

employed in the present study for defining managerial discretion. For this purpose,

the definition of discretion is further scrutinised below in four parts:

• The first part of the definition reads ‘the extent to which a manager has multiplecourses of action (or choices or decisions)’. A manager may have many possible

courses of action within a given domain of his/her work. For instance, within the

domain of making capital investments, a plant manager could potentially choose

between a vast number of alternative investments, such as alternative machinery

or equipment. Although it has been suggested in the literature that one may

attempt to create a complete list of all possible actions that a manager might

take in relevant situations (Hambrick and Finkelstein 1987, p. 401; Yougen Li and

Zhao 2003, pp. 4–5), the approach is generally ruled out on practical grounds,

for even within a given domain, the multiple courses of action available to a

3Managerial discretion is sometimes abbreviated by the term ‘discretion’ in the present study.

The term ‘middle management discretion’ used herein therefore refers to the managerial discretion

of middle management.

2.1 Managerial Discretion 27

manager may be vast and impractical to enumerate (Caza 2007, p. 39; March and

Shapira 1987, p. 1412). The ‘latitude of managerial action’ within a given domain

is therefore commonly specified as the extent to which the manager can autono-

mously decide on his/her courses of action relative to the parties that possess

power to constrain the manager (e.g. Acemoglu et al. 2007; Caza 2007; Chang and

Wong 2003; Cheng et al. 2006; Colombo and Delmastro 2004; Glaister et al.

2003; Marin and Verdier 2006). As described in Sect. 4.2.2, the measurement of

managerial discretion in the present study precisely follows this approach.

• The second part of the definition adds ‘across various domains of his/her work’.A manager can possess multiple courses of action in different areas or domains

of his/her work. While Hambrick and Finkelstein (1987, pp. 371–372) do not

exhaustively postulate an array of domains of managerial action, they provide

examples of domains such as resource allocation, staffing, product market

selection, and competitive initiatives. Similarly, in the present study the domains

of managerial action measured for the plant manager are making capital

investments, hiring workers, introducing new products, and sales and marketing

activities. This selection of domains measured in the present study is shown in

Sect. 4.2.2 to be consistent with the literature (e.g. Acemoglu et al. 2007;

Caza 2007; Chang and Wong 2003; Cheng et al. 2006; Colombo and Delmastro

2004; Glaister et al. 2003; Marin and Verdier 2006).

• The third part refines the definition by specifying ‘that he/she is aware of’.In order for a manager’s multiple courses of action across the domains of his/her

work to count towards his/her level of managerial discretion, a manager must be

aware of these potential choices (Hambrick and Finkelstein 1987, p. 378).

Seminal work has postulated and empirically confirmed that it is thus the

discretion a manager perceives rather than some objective degree of discretion

awarded that matters for predicting managerial behaviour (e.g. Carpenter and

Golden 1997, p. 202; Caza 2007; 2011; Galavan 2005; Galavan et al. 2009;

Glaister et al. 2003; Hambrick and Finkelstein 1987, p. 373; Key 2002;

Walters 1995; Zhao et al. 2010).4 For instance, a plant manager that has been

granted complete authority for hiring a full-time permanent shop floor worker

but erroneously feels that he must involve top management at corporate head-

quarters in the decision process is likely to act subject to this constraint despite a

high degree of objective discretion. As explained in Sect. 4.2.2, the present study

measures discretion based on 467 interviews with plant managers, which allows

the study to evaluate perceived rather than objective managerial discretion of

middle managers.

4 Glaister et al. (2003) find empirical evidence that the managerial discretion a manager perceives

for himself/herself may differ from the discretion that his/her superiors perceive. In particular, in

their sample of UK-European joint ventures, perceptions of managerial discretion of the joint

venture management differ between the joint venture management itself and the parent firms as

well as between each of the parent firms.

28 2 Literature Review and Hypotheses

• The fourth part of the definition qualifies ‘and that are acceptable to the partiesthat possess power to constrain the manager’. Hambrick and Finkelstein (1987,

p. 378) explain that in order to represent managerial discretion, the multiple

courses of action across the domains that the manager is aware of must ‘lie

within the zone of acceptance of powerful parties’.5 For example, a powerful

party potentially constraining the managerial actions of a chief executive officer

(CEO) is the board of directors (Hambrick and Finkelstein 1987, p. 401),

whereas the powerful party relevant for the plant manager in the present study

is the top management at corporate headquarters in China (see Fig. 1.1 in Sect.

1.3). Hambrick and Finkelstein (1987, p. 401) suggest measuring a CEO’s

managerial discretion as ‘the explicit dollar limits that most firms place on the

CEO’s discretion to commit resources without board approval’ (the board being

the powerful party). In the same sense, the present study measures the plant

manager’s discretion in the domain of making capital investments as the explicit

monetary limit on the maximum capital investment that the plant manager can

undertake without prior authorisation from corporate headquarters in China (i.e.

the relevant powerful party). As demonstrated in Sect. 4.2.2 (see Fig. 4.10), this

study measures the plant manager’s discretion in each of the four domains

assessed relative to the relevant powerful party (i.e. to corporate headquarters

in China). Consequently, the above discussion implies that discretion in the

present study matches each of the four parts of the definition of managerial

discretion.

Summarising the definition, managerial discretion is defined as the extent to

which a manager has multiple courses of action across various domains of his/her

work that he/she is aware of and that are acceptable to the parties that possess power

to constrain the manager (Abrahamson and Hambrick 1997, p. 513; Carpenter and

Golden 1997, p. 187; Caza 2007, p. 27; Chang and Wong 2003, p. 2; Crossland

2007, p. 1; Crossland and Hambrick 2007, p. 767; Finkelstein and Boyd 1998,

p. 179; Finkelstein and Hambrick 1990, p. 484; Hambrick and Abrahamson 1995,

p. 1427; Hambrick and Finkelstein 1987, pp. 371–378; Rajagopalan and Finkelstein

1992, p. 32). By taking the four parts of this definition in turn, it has been shown that

for the unit of analysis of the present study, managerial discretion measures the

5As explained in Sects. 2.3.1 and 2.3.2, Finkelstein and Peteraf (2007, pp. 237–243) incorporate

the assumption of post-contractual asymmetric information (i.e. hidden action) from principal-

agent theory (e.g. Eisenhardt 1989, p. 59; Jensen and Murphy 1990, p. 226; Khanchel 2009, p. 97;

Levinthal 1988, p. 153; Spremann 1987, p. 3; Van Slyke 2007, p. 162; Werner and Tosi 1995,

p. 1673) into managerial discretion theory. They argue that different characteristics of managerial

activities affect the ability of key stakeholders (i.e. the powerful parties) to pre-specify and monitor

the manager’s work, thus creating or constraining discretion. Asymmetric information (i.e. the

inability to monitor the manager’s actions) therefore widens the ‘zone of acceptance of powerful

parties’ (Hambrick and Finkelstein 1987, p. 378). E.g. if top management at corporate headquar-

ters in China could not properly monitor the plant manager’s actions, the plant manager might

undertake capital investments out of self-serving interests that reduced performance, which top

management might have to accept due to their inability to monitor the plant manager’s action

(Spremann 1987, p. 10).

2.1 Managerial Discretion 29

extent to which the plant manager has multiple choices across domains such as

making capital investments, hiring workers, introducing new products, and sales

and marketing activities that he/she is aware of and that are acceptable to corporate

headquarters in China—which is precisely what is measured empirically in the

present study (see Sect. 4.2.2).

The potential importance of managerial discretion in terms of affecting perfor-

mance follows directly from this definition. Defined as the ‘latitude of managerial

action’, managerial discretion measures the leeway of a manager to take action

which might impact on performance (Hambrick and Finkelstein 1987, p. 371).

In fact, as put by Caza (2007, p. 1), ‘[i]ndividuals can only influence organizations

through discretion’ and discretion is thus ‘a fundamental aspect of organized

behavior’ and ‘the key to understanding agency in organizations.’ With the extent

of managerial discretion potentially improving or reducing performance according

to stewardship theory (see Sect. 2.3.3) and principal-agent theory (see Sect. 2.3.2),

respectively, adjusting the discretion granted to middle managers is thus a potential

success factor for the top management of Chinese firms and multinationals in China

when used to optimise the company’s performance along the value chain (e.g.

Adams et al. 2005; Caza 2007; 2011; Chang and Wong 2003; Corbetta and

Salvato 2004; Crossland and Hambrick 2007; Davis et al. 1997b; Donaldson and

Davis 1991; Eddleston and Kellermanns 2007; Finkelstein and Hambrick 1990;

Hambrick and Finkelstein 1987; Hutzschenreuter and Kleindienst 2007; Jensen and

Murphy 1990; Khanchel 2009; Liu and Cai 2004; Mills and Keast 2009;

Misangyi 2002; Quigley and Hambrick 2009; Tang 2008; Tosi et al. 2003;

Van Slyke 2007; Vargas Sanchez 2004; Zhao et al. 2010).6

Finally, it is worth noting that alternative terms have been used in the literature

at times to describe phenomena identical or similar to managerial discretion.

For example, some scholars have employed such terms as managerial autonomyand decision-making autonomy, often synonymously with managerial discretion

(e.g. Cheng et al. 2006; Gammelgaard et al. 2010; Glaister et al. 2003; Groves et al.

1994; Heinecke 2011; Li 2007; Lopez-Navarro and Camison-Zornoza 2003;

Oh 2002; Perrone et al. 2003; Venaik 1999; Verhoest 2003; Wang et al. 2008;

Xu et al. 2005). Other scholars have written about the delegation of authority or

decision rights in terms of decentralisation (e.g. Aghion and Tirole 1997;

Burkart et al. 1997; Colombo and Delmastro 2004; Jensen 1998; Marin and Verdier

2006; Zhang 1997). Certain studies have used autonomy and decentralisation

6 In addition to discretion having a potentially important impact on performance (see above), it has

been empirically demonstrated that discretion may significantly affect managerial power

(Carpenter and Golden 1997), managerial compensation (Finkelstein and Boyd 1998; Magnan and

St-Onge 1997; Rajagopalan and Finkelstein 1992; Werner and Tosi 1995; Wright and Kroll 2002;

Zhang and Xie 2008), workers’ incentives (Groves et al. 1994), a successor chief executive officer’s

age (Wang 2009), top management team tenure, trust (Perrone et al. 2003), strategic attention

(Abrahamson and Hambrick 1997), environmental commitment (Aragon-Correa et al. 2004), pricing

(Cameron 2000), organisational knowledge creation (Oh 2002), and research and development

(Zhang et al. 2006a, b).

30 2 Literature Review and Hypotheses

interchangeably (e.g. Acemoglu et al. 2007; Bloom et al. 2008), while other studies

have differentiated the two concepts. For example, Barnabas and Mekoth (2010,

pp. 330–336) define autonomy consistently with managerial discretion as the extent

of a manager’s freedom in decision making and decentralisation as the extent to

which this decision-making authority is diffused throughout the organisation. They

therefore argue that autonomy and decentralisation are comparable at lower levels

of operation (e.g. middle management), which they empirically confirm for retail

bank branch managers in India. For the middle managers analysed in the present

study (i.e. plant managers in China; see Chap. 3), managerial discretion, autonomy,

and decentralisation are therefore closely related (e.g. Barnabas and Mekoth 2010,

p. 334; Caza 2007, p. 61), thus allowing the present study to draw on a broader

literature base while keeping given differences in mind.7

2.1.2 Dimensionality of Managerial Discretion

The definition of managerial discretion in the previous section based on Hambrick

and Finkelstein (1987, pp. 371–378) implies that a manager’s discretion

(i.e. ‘latitude of managerial action’) spans various domains of his/her work. In

particular, the domains of managerial action in which a given plant manager can

possess discretion include making capital investments, hiring workers, introducing

new products, and sales and marketing activities in the present study (e.g. Acemoglu

et al. 2007; Caza 2007; Chang and Wong 2003; Cheng et al. 2006; Colombo and

Delmastro 2004; Glaister et al. 2003; Marin and Verdier 2006). However, the

definition of discretion leaves it open whether discretion awarded in one domain

of the manager’s work (e.g. making capital investments) impacts on performance in

a similar way as discretion awarded in another domain of the manager’s work (e.g.

hiring workers)—in which case discretion would be unidimensional—or impacts

on performance in a different way than in different domains—in which case

discretion would be multidimensional. As explained below, whether discretion

can be viewed as unidimensional or multidimensional has important implications

for how to model managerial discretion:

• Unidimensional. If granting the plant manager discretion in one domain of his/

her work (e.g. making capital investments) impacts on performance in a similar

way as granting discretion in any other domain of his/her work (e.g. hiring

workers, introducing new products or sales and marketing activities), then

7Decentralisation of decisions rights from top management at corporate headquarters in China to

the plant manager of the present study is related to the extent to which the plant manager possesses

decision rights (and thus multiple courses of action) across various domains that are acceptable to

top management (i.e. powerful parties). While decentralisation is therefore closely related to

managerial discretion and autonomy in the present study, it tends to emphasise the objective

delegation of decision rights to the plant manager rather than the perceived latitude of managerial

action that defines the managerial discretion of the plant manager.

2.1 Managerial Discretion 31

managerial discretion is unidimensional in its impact on performance. In this

case, measures of a manager’s discretion in different domains can be combined

into a single construct of discretion, which will then, ceteris paribus, rise

whenever discretion increases in any of the measured domains.

• Multidimensional. If, in contrast, granting the plant manager discretion in one

domain of his/her work (e.g. making capital investments) impacts on perfor-

mance in a differently-signed way than granting discretion in another domain of

his/her work, then managerial discretion is multidimensional in its impact on

performance. For example, the plant manager might use discretion for capital

investments in ways that increase performance but use discretion for hiring

workers in ways that decrease performance. If this is this case, then measures

of discretion in different domains cannot meaningfully be combined into a single

(i.e. unidimensional) discretion construct: As a unidimensional construct of

discretion is restricted to impact on performance in a single way (i.e. positive,

neutral or negative), it is not possible for the construct to be increasing in each

discretion measure and still reveal the true, differently-signed impacts of discre-

tion on performance in each domain. Instead, if discretion in different domains

affects performance in distinct ways, then discretion is multidimensional in its

impact on performance and needs to be measured by multiple constructs of

discretion rather than a single, unidimensional construct spanning the various

domains of the manager’s work.

Despite the potential importance of whether discretion is unidimensional or

multidimensional (which motivates the present study’s postulate; see Sects. 1.2

and 2.4), the theoretical and empirical literature to date have not provided a

conclusive answer as to whether discretion should be treated as unidimensional or

as multidimensional (i.e. whether or not managerial discretion has distinct impacts

in different domains). In particular, there seems to be a discontinuity between

managerial discretion theory on the one hand, which postulates the multidimen-

sionality of discretion, and many empirical studies as well as principal-agent theory

and stewardship theory on the other hand, which implicitly tend to assume the

unidimensionality of discretion:8

• On the one hand, both early and recent theoretical studies grounded mostly in

managerial discretion theory (see Sect. 2.3.1) have posited on qualitative groundsthat managerial discretion consists of several types, i.e. is multidimensional (e.g.

Barnabas and Mekoth 2010; Carpenter and Golden 1997, p. 195; Caza 2007, pp.

26–82; Chen 2006; Finkelstein and Peteraf 2007, p. 245; Groves et al. 1994, p. 190;

Hambrick and Abrahamson 1995, p. 1439; Hambrick and Finkelstein 1987, pp.

371–402;Hambrick et al. 1993, p. 409;March and Simon 1958; Perrone et al. 2003,

pp. 422–423). In particular, Hambrick and Finkelstein (1987, pp. 371–402) contend

that managers vary significantly ‘in the number of domains in which they have

8 This discontinuity motivates the study’s first hypothesis (see below) and the integration of the

various existing theories into a new single model for the impact of managerial discretion on

performance (see Chap. 4).

32 2 Literature Review and Hypotheses

discretion’ and thus ‘have some domains of high discretion and others of low

discretion’. They expect that this ‘type of mixed discretion lead[s] to consequences

that differ from simply thinking about moderate discretion’ (1987, p. 402). More-

over, they posit that each different combination of causes of discretion ‘may lead to

its own set of accompanying organizational factors’, including performance (1987,

p. 389). Applied to the unit of analysis of the present study, managerial discretion

theory therefore implies that a plant manager might have different degrees of

discretion in different domains of his/her work, and a plant manager with high

discretion for making capital investments and low discretion for hiring workers

might produce different results than a plant manager with moderate discretion for

bothmaking capital investments and hiringworkers. In other words, it is implicit in

managerial discretion theory that discretion in different domains might lead to

distinct impacts and in this sense might be a multidimensional construct.

• On the other hand, as explained in the preceding section, neither principal-agenttheory (see Sect. 2.3.2) nor stewardship theory (see Sect. 2.3.3) have placed

much emphasis on the nature of the construct of discretion. When referring to

discretion, both theories tend to treat discretion as a single (unidimensional)

construct with a particular positive (in stewardship theory) or negative (in

principal-agent theory) impact on performance (e.g. Chang and Wong 2003;

Dicke and Ott 2002, p. 468; Fox and Hamilton 1994, p. 74; He et al. 2009;

Spremann 1987, p. 18; Vargas Sanchez 2005, p. 19; Xu et al. 2005). Moreover,

despite the postulated multidimensionality in qualitative studies of managerial

discretion theory (see above), quantitative empirical studies have frequently

made the simplifying assumption in their research designs that discretion is

unidimensional. In particular, among studies attempting to measure discretion

directly, scholars have frequently gauged a manager’s discretion in different

areas of his/her work and combined these indicators into a single unidimensional

discretion construct (e.g. Barnabas and Mekoth 2010; Bloom et al. 2008;

Caza 2007; 2011; Chang and Wong 2003; Cheng et al. 2006; Gammelgaard

et al. 2010; Marin and Verdier 2006). Moreover, among the many empirical

studies resorting to proxy measures for gauging managerial discretion, discretion

has prevalently been modelled as unidimensional as well.9 Compared to this

prevalent assumption of unidimensionality in the empirical literature, only a

9 Empirical studies have modelled unidimensional discretion constructs by measuring one or

several proxies related to e.g. ratings of managerial power, internal representation on the board

of directors, managerial stock ownership, and financial ratios (e.g. Huiyuan Chen 2006;

Khanchel 2009; Yougen Li and Zhao 2004; Zhang and Li 2008b; Zhang et al. 2006a, b) as well

as multiple antecedents drawn from mostly the task environment (e.g. Agarwal et al. 2009;

Berman et al. 2005; Cameron 2000; Finkelstein and Boyd 1998; Finkelstein and Hambrick

1990; He et al. 2009; Magnan and St-Onge 1997; Rajagopalan and Finkelstein 1992;

Williamson 1963). In addition, industry-level discretion has been frequently proxied in existing

studies (e.g. Abrahamson and Hambrick 1997; Datta et al. 2003; Finkelstein and Hambrick 1990;

Hambrick and Abrahamson 1995; Hambrick et al. 1993; Keegan 2006; Keegan and Kabanoff

2008; Thomas and Peyrefitte 1996).

2.1 Managerial Discretion 33

small minority of studies have differentiated managerial discretion according to

multiple dimensions of the manager’s work and these studies have often

analysed phenomena other than the impact of managerial discretion on perfor-

mance (e.g. Colombo and Delmastro 2004; Glaister et al. 2003; Groves et al.

1994; Xiaoyang Li 2007; Perrone et al. 2003).

Despite this discontinuity of postulated multidimensionality (in managerial

discretion theory) and implicitly assumed unidimensionality (in many empirical

studies as well as principal-agent theory and stewardship theory), empirical studies

have on occasion investigated the dimensionality of discretion explicitly. This has,

however, not always produced concurrent results and therefore warrants further

investigation. For example, Cheng et al. (2006, p. 348) experiment with separating

operational and strategic decisions but find that these two indices are sufficiently

correlated and correlate sufficiently with the overall index in order to support a

unidimensional measure for discretion. By contrast, Caza’s (2007, pp. 26–82)

factor analysis confirms that research and development (R&D) managers in Europe

perceive their discretion as multidimensional and his regression reveals that some

antecedents (or causes, determinants or sources of discretion; see Sect. 2.3.1) differ

between dimensions of discretion. Furthermore, Caza generalises the multidimen-

sionality of discretion on qualitative grounds by demonstrating its consistency with

the literature on various hierarchical levels in organisations from workers to top

management. However, when empirically investigating the impact of discretion on

performance, Caza (2007, pp. 14–16) does not allow for this multidimensionality,

implicitly treating discretion as unidimensional and thus modelling only a single

overall impact on performance.

The unresolved dimensionality of managerial discretion in the theoretical and

empirical literature (i.e. unidimensionality versus multidimensionality) motivates

the formulation of one of the four hypotheses of the present study (i.e. Hypothesis

1). As discussed above, although managerial discretion theory hints that discretion

may be multidimensional, both principal-agent theory and stewardship theory tend

to treat discretion as unidimensional and many existing empirical studies have

tended to make the simplifying assumption in their research designs that discretion

is unidimensional (see references above). Whether or not this assumption of

unidimensionality is universally tenable is examined by testing the null hypothesis

of unidimensionality (H01) against the alternative hypothesis of multidimensionality

(H11)—i.e. testing whether the impact of discretion on performance differs between

dimensions of discretion. If H01 cannot be rejected, the prevalent simplifying

assumption of a unidimensional construct of discretion in existing studies might

be justifiable. However, if H01 can be rejected in favour of H1

1 , this simplifying

assumption of unidimensionality is not universally tenable (since it is then not

tenable at least in the instance of this particular study) and instead more granular

research designs that allow for the potentially multidimensional nature of discretion

would be required in order to produce more meaningful results in future research.

34 2 Literature Review and Hypotheses

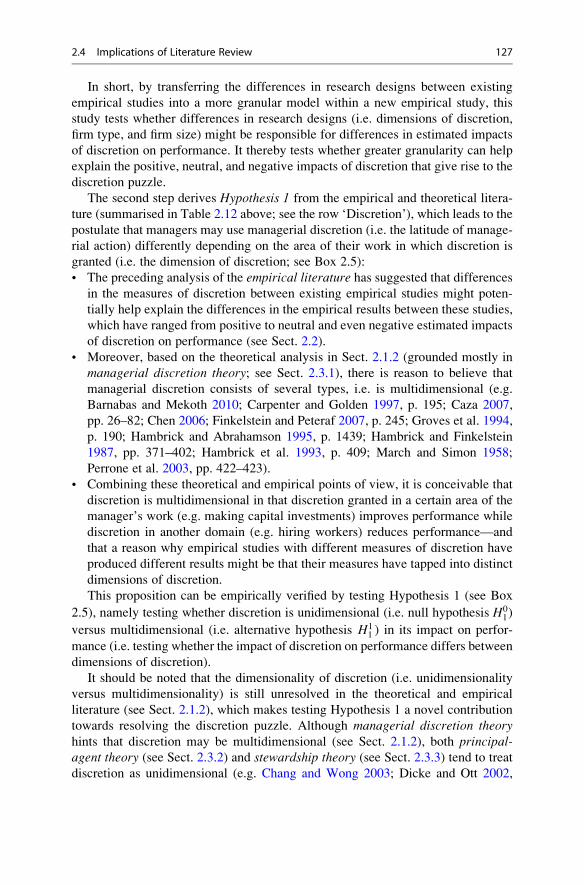

Hypothesis 1 (Dimensions of Discretion)

H01: Managerial discretion is unidimensional in its impact on performance.

H11: Managerial discretion is multidimensional in its impact on performance.

The importance of testing Hypothesis 1 in the present study derives from its

potential contribution towards resolving the discretion puzzle and thus towards

fulfilling the present study’s research objective (see Sect. 1.2). In particular, as is

explained in Chap. 7, erroneously treating discretion as unidimensional when it is in

fact multidimensional might produce misleading estimates of the impact of discre-

tion on performance that could potentially be a cause of the contradictory empirical

evidence that gives rise to the discretion puzzle. Therefore, empirically testing

Hypothesis 1 regarding the dimensions of managerial discretion in the present study

constitutes a vital step towards resolving the discretion puzzle.

Table 2.3 summarises the discussion on the definition and dimensionality of

discretion presented in this section (i.e. Sect. 2.1) using the literature review sum-

mary table introduced in the opening of Chap. 2 (see Table 2.1). As indicated by the

grey-shaded arrow in Table 2.3, the above discussion of the theoretical and empirical

literature leads to the formulation of Hypothesis 1 on the dimensionality of discre-

tion. The following sections complete the remaining cells in this table, which allows

Sect. 2.4 to eventually synthesise the theoretical and empirical literature into

implications for the present study, such as the study’s four research hypotheses.

2.2 Impact of Managerial Discretion on Performancein Existing Empirical Evidence

This section conducts a thorough, in-depth review of empirical studies10 on the

impact of managerial discretion on performance, which completes the grey-shaded

10 The present study reviews over 80 empirical studies on managerial discretion and related

phenomena, e.g. Abrahamson and Hambrick (1997), Acemoglu et al. (2007), Adams et al. (2005),

Agarwal et al. (2009), Agrawal and Knoeber (1996), Aragon-Correa et al. (2004), Barnabas and

Mekoth (2010), Baysinger and Butler (1985), Berger et al. (1997), Berman et al. (2005), Bloom et al.

(2008), Bowen et al. (2008), Brush et al. (2000), Burkart et al. (1997), Zhang and Li (2008b), Zhang

and Xie (2008), Zhang et al. (2006a, b), Cameron (2000), Carpenter and Golden (1997), Caza

(2007), Caza (2011), Chaganti et al. (1985), Chang and Wong (2003), Chang and Wong (2004),

Chen (2006), Cheng et al. (2006), Colombo and Delmastro (2004), Crossland and Hambrick (2007),

Datta et al. (2003), Demsetz and Lehn (1985), Denis and Denis (1993), Denis et al. (1997),

Donaldson and Davis (1991), Finkelstein and Boyd (1998), Finkelstein and Hambrick (1990),

Gammelgaard et al. (2010), Glaister et al. (2003), Groves et al. (1994), Wang (2009), Haleblian

and Finkelstein (1993), Hambrick and Abrahamson (1995), Hambrick et al. (1993), He et al. (2009),

Heinecke (2011), Hutzschenreuter and Kleindienst (2007), Kayhan (2008), Keegan and Kabanoff

(2008), Keegan (2006), Kesner (1987), Khanchel (2009), Lang et al. (1995), Lieberson and

O’Connor (1972), Lopez-Navarro and Camison-Zornoza (2003), Mackey (2008), Magnan and St-

Onge (1997), Manner (2010), Marin and Verdier (2006), Misangyi (2002), Oh (2002), Ongore

2.2 Impact of Managerial Discretion on Performance in Existing Empirical Evidence 35

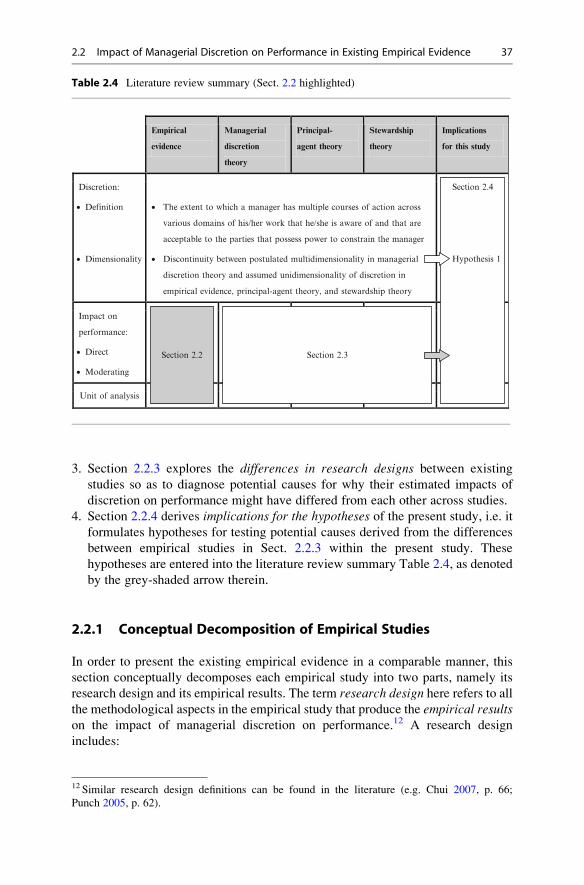

cells in the literature review summary Table 2.4.11 To this end, four steps are

pursued:

1. Section 2.2.1 conceptually decomposes each empirical study into two parts,

namely its research design and its empirical results, which paves the way for

scrutinising the existing empirical evidence in the remainder of this section.

2. Section 2.2.2 presents the differences in empirical results between existing

studies that give rise to the discretion puzzle (see Sect. 1.1), i.e. the positive,

neutral, and negative estimated impacts of discretion on performance.

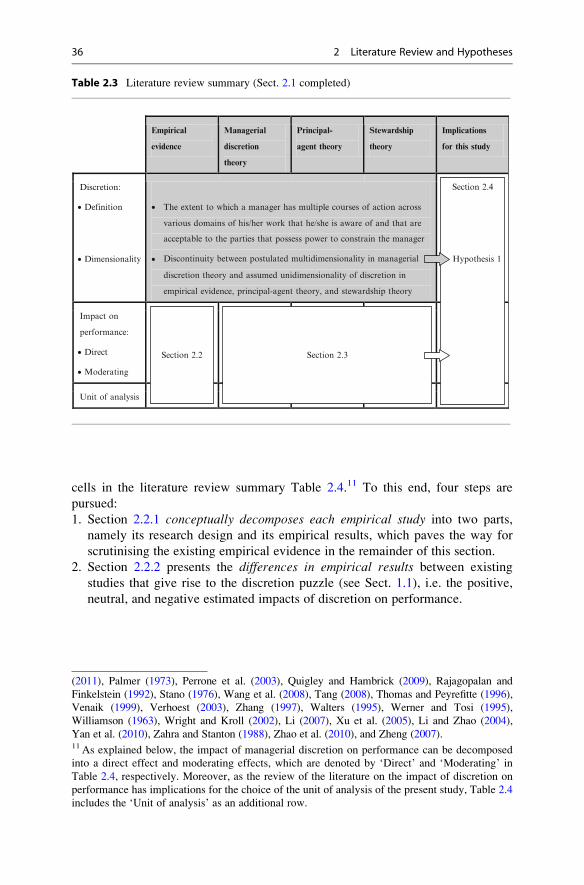

Table 2.3 Literature review summary (Sect. 2.1 completed)

Empirical

evidence

Managerial

discretion

theory

Principal-

agent theory

Stewardship

theory

Implications

for this study

Discretion:

• Definition

• Dimensionality

• The extent to which a manager has multiple courses of action across

various domains of his/her work that he/she is aware of and that are

acceptable to the parties that possess power to constrain the manager

• Discontinuity between postulated multidimensionality in managerial

discretion theory and assumed unidimensionality of discretion in

empirical evidence, principal-agent theory, and stewardship theory

Impact on

performance:

• Direct

• Moderating

Unit of analysis

Section 2.2 Section 2.3

Section 2.4

Hypothesis 1

(2011), Palmer (1973), Perrone et al. (2003), Quigley and Hambrick (2009), Rajagopalan and

Finkelstein (1992), Stano (1976), Wang et al. (2008), Tang (2008), Thomas and Peyrefitte (1996),

Venaik (1999), Verhoest (2003), Zhang (1997), Walters (1995), Werner and Tosi (1995),

Williamson (1963), Wright and Kroll (2002), Li (2007), Xu et al. (2005), Li and Zhao (2004),

Yan et al. (2010), Zahra and Stanton (1988), Zhao et al. (2010), and Zheng (2007).11 As explained below, the impact of managerial discretion on performance can be decomposed

into a direct effect and moderating effects, which are denoted by ‘Direct’ and ‘Moderating’ in

Table 2.4, respectively. Moreover, as the review of the literature on the impact of discretion on

performance has implications for the choice of the unit of analysis of the present study, Table 2.4

includes the ‘Unit of analysis’ as an additional row.

36 2 Literature Review and Hypotheses

3. Section 2.2.3 explores the differences in research designs between existing

studies so as to diagnose potential causes for why their estimated impacts of

discretion on performance might have differed from each other across studies.

4. Section 2.2.4 derives implications for the hypotheses of the present study, i.e. itformulates hypotheses for testing potential causes derived from the differences

between empirical studies in Sect. 2.2.3 within the present study. These

hypotheses are entered into the literature review summary Table 2.4, as denoted

by the grey-shaded arrow therein.

2.2.1 Conceptual Decomposition of Empirical Studies

In order to present the existing empirical evidence in a comparable manner, this

section conceptually decomposes each empirical study into two parts, namely its

research design and its empirical results. The term research design here refers to allthe methodological aspects in the empirical study that produce the empirical resultson the impact of managerial discretion on performance.12 A research design

includes:

Table 2.4 Literature review summary (Sect. 2.2 highlighted)

Empirical

evidence

Managerial

discretion

theory

Principal-

agent theory

Stewardship

theory

Implications

for this study

Discretion:

• Definition

• Dimensionality

• The extent to which a manager has multiple courses of action across

various domains of his/her work that he/she is aware of and that are

acceptable to the parties that possess power to constrain the manager

• Discontinuity between postulated multidimensionality in managerial

discretion theory and assumed unidimensionality of discretion in

empirical evidence, principal-agent theory, and stewardship theory

Impact on

performance:

• Direct

• Moderating

Unit of analysis

Section 2.2 Section 2.3

Section 2.4

Hypothesis 1

12 Similar research design definitions can be found in the literature (e.g. Chui 2007, p. 66;

Punch 2005, p. 62).

2.2 Impact of Managerial Discretion on Performance in Existing Empirical Evidence 37

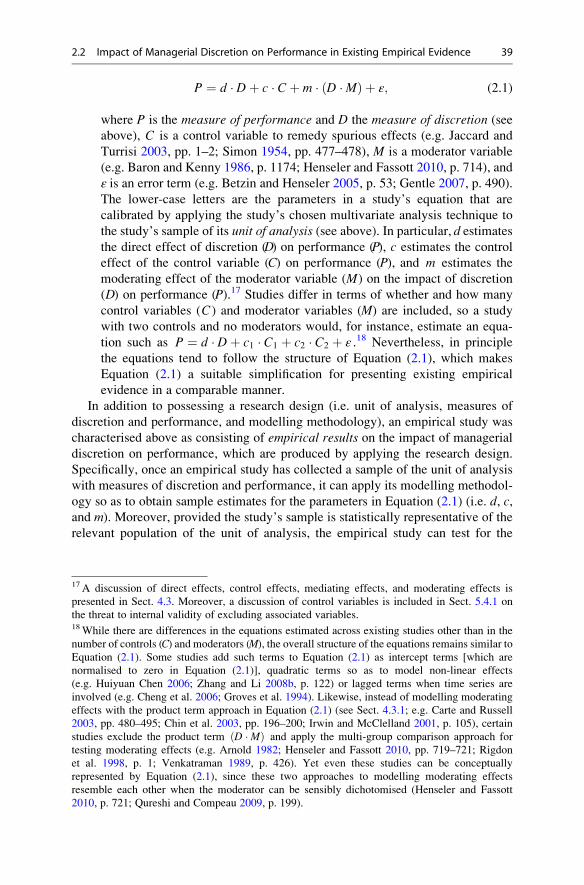

• A unit of analysis, which is ‘the entity about which one is trying to draw

conclusions’ (Johnson et al. 2007, p. 58) and in the studies reviewed below

generally refers to a manager whose managerial discretion is investigated

(e.g. top management in the United States).13 Most studies’ results are estimated

based on a sample drawn from the population that the unit of analysis defines

(Northrop and Arsenault 2007, p. 214).

• A measure of discretion and a measure of performance, which attempt to gauge

discretion and performance for the study’s chosen unit of analysis.14

• A modelling methodology for estimating the impact of the measure of discretion

on the measure of performance for the chosen unit of analysis. The modelling

methodology can be decomposed into the equations that are estimated for

inferring the impact of discretion on performance and the multivariate analysis

technique that is applied for estimating these equations.

– As to multivariate analysis techniques, existing studies typically adopt obser-vational cross-sectional designs (e.g. Caza 2007; 2011; Huiyuan Chen 2006;

Colombo and Delmastro 2004; Finkelstein and Boyd 1998; Glaister et al.

2003; Yougen Li and Zhao 2004; Marin and Verdier 2006; Oh 2002; Perrone

et al. 2003; Williamson 1963; Zhang and Li 2008b; Zhang et al. 2006a, b)

using first and second generation multivariate analyses, namely multiple

regressions (e.g. ordinary least squares multiple regressions) and structural

equation models (i.e. variance-based and covariance-based structural equa-

tion models; see Sect. 5.1.1; e.g. Bentler and Chou 1987; Bentler and Weeks

1980; Bollen 1989; Chin et al. 2003, p. 194; Fassott 2005; Fornell 1987;

Joreskog 1970, 1981; Joreskog and Sorbom 1982, 1988; Lohmoller 1987,

1989; Wold 1966, 1973, 1975, 1982, 1985, 1989).15

– In order to estimate the impact of managerial discretion on performance, the

chosen multivariate analysis technique in a given study then typically

estimates an equation that resembles Equation (2.1):16

13 The unit of analysis of the present study (i.e. the plant manager in China) is discussed in detail in

Chap. 3.14 The measures of discretion and performance in the present study are described in Sect. 4.2 and are

demonstrated to exhibit high reliability and construct validity in Sects. 5.2 and 5.3, respectively.15 A discussion of alternative multivariate analysis techniques is provided in Sect. 5.1.1, which

develops its own decision-tree logic for choosing an appropriate modelling methodology for the

present study.16 A more complete version of Equation (2.1) is developed from the literature in Sect. 4.3 as part of

the present study’s new empirical discretion model. This equation resembles Equation (2.1) when

expressed in vector/matrix notation (e.g. Gentle 2007, pp. 479–491; Harville 2008, pp. 1–10;

Knapp 2007, pp. xxi–xxiv), but it is sufficiently general that it can be disaggregated into an

arbitrary number of discretion dimensions, controls, and moderators. In contrast to the simplified

Equation (2.1), the equation in Sect. 4.3 fulfils the requirements of state-of-the-art methodological

research such as that all the components of the product term D �Mð Þ must be included in the

equation in direct form (Carte and Russell 2003, pp. 480–495; Cohen 1978; Cronbach 1987;

Henseler and Fassott 2010, pp. 718–719; Irwin and McClelland 2001, p. 105). Applying this

requirement to Equation (2.1), it would read P ¼ d � Dþ c � Cþ m � D �Mð Þ þ q �M þ ε . Theintercept term is normalised to zero.

38 2 Literature Review and Hypotheses

P ¼ d � Dþ c � Cþ m � D �Mð Þ þ ε; (2.1)

where P is the measure of performance and D the measure of discretion (see

above), C is a control variable to remedy spurious effects (e.g. Jaccard and

Turrisi 2003, pp. 1–2; Simon 1954, pp. 477–478), M is a moderator variable

(e.g. Baron and Kenny 1986, p. 1174; Henseler and Fassott 2010, p. 714), and

ε is an error term (e.g. Betzin and Henseler 2005, p. 53; Gentle 2007, p. 490).

The lower-case letters are the parameters in a study’s equation that are

calibrated by applying the study’s chosen multivariate analysis technique to

the study’s sample of its unit of analysis (see above). In particular, d estimates

the direct effect of discretion (D) on performance (P), c estimates the control

effect of the control variable (C) on performance (P), and m estimates the

moderating effect of the moderator variable (M) on the impact of discretion

(D) on performance (P).17 Studies differ in terms of whether and how many

control variables (C) and moderator variables (M) are included, so a study

with two controls and no moderators would, for instance, estimate an equa-

tion such as P ¼ d � Dþ c1 � C1 þ c2 � C2 þ ε .18 Nevertheless, in principle

the equations tend to follow the structure of Equation (2.1), which makes

Equation (2.1) a suitable simplification for presenting existing empirical

evidence in a comparable manner.

In addition to possessing a research design (i.e. unit of analysis, measures of

discretion and performance, and modelling methodology), an empirical study was

characterised above as consisting of empirical results on the impact of managerial

discretion on performance, which are produced by applying the research design.

Specifically, once an empirical study has collected a sample of the unit of analysis

with measures of discretion and performance, it can apply its modelling methodol-

ogy so as to obtain sample estimates for the parameters in Equation (2.1) (i.e. d, c,and m). Moreover, provided the study’s sample is statistically representative of the

relevant population of the unit of analysis, the empirical study can test for the

17A discussion of direct effects, control effects, mediating effects, and moderating effects is

presented in Sect. 4.3. Moreover, a discussion of control variables is included in Sect. 5.4.1 on

the threat to internal validity of excluding associated variables.18While there are differences in the equations estimated across existing studies other than in the

number of controls (C) and moderators (M), the overall structure of the equations remains similar to

Equation (2.1). Some studies add such terms to Equation (2.1) as intercept terms [which are

normalised to zero in Equation (2.1)], quadratic terms so as to model non-linear effects

(e.g. Huiyuan Chen 2006; Zhang and Li 2008b, p. 122) or lagged terms when time series are

involved (e.g. Cheng et al. 2006; Groves et al. 1994). Likewise, instead of modelling moderating

effects with the product term approach in Equation (2.1) (see Sect. 4.3.1; e.g. Carte and Russell

2003, pp. 480–495; Chin et al. 2003, pp. 196–200; Irwin and McClelland 2001, p. 105), certain

studies exclude the product term D �Mð Þ and apply the multi-group comparison approach for

testing moderating effects (e.g. Arnold 1982; Henseler and Fassott 2010, pp. 719–721; Rigdon

et al. 1998, p. 1; Venkatraman 1989, p. 426). Yet even these studies can be conceptually

represented by Equation (2.1), since these two approaches to modelling moderating effects

resemble each other when the moderator can be sensibly dichotomised (Henseler and Fassott

2010, p. 721; Qureshi and Compeau 2009, p. 199).

2.2 Impact of Managerial Discretion on Performance in Existing Empirical Evidence 39

significance of the parameters in Equation (2.1) (see Sects. 4.3.3 and 5.5; e.g. Fogiel

2000, pp. 158–190; Garson 2002, pp. 139–196; Gliner and Morgan 2000, p. 148;

Greene 2003, pp. 892–896; Gujarati 2004, pp. 119–139; Hayashi 2000, pp. 33–45;

Salvatore and Reagle 2002, pp. 87–95; Spanos 1986, pp. 213–311; Wooldridge

2002, pp. 116–299).

The way in which these empirical results on the parameters in Equation (2.1)

(i.e. d , c , and m) relate to the impact of managerial discretion on performance

can be seen by partially differentiating performance (P ) in Equation (2.1) with

respect to discretion (D) so as to obtain an equation of discretion’s total impact

on performance:

@P

@D¼ d þ m �M (2.2)

Equation (2.2) reveals that the total estimated ceteris paribus impact of manage-

rial discretion (D) on performance (P) is the sum of the direct effect of discretion on

performance (here d) and the moderating effect of the moderator variable (here m)multiplied by the value of the moderator variable (M). If variables are centred to

means of zero, then when the moderator variable reaches its mean value (i.e. zero),

the total impact of discretion on performance measures the direct effect of discre-

tion on performance (see Sect. 4.3.2 on comparative statics; e.g. Aiken and West

1991, p. 37; Dowling 2000, pp. 284–291; Finney et al. 1984; Henseler and Fassott

2010, p. 728; Hirschey 2009, p. 99). Consequently, Equation (2.2) implies that the

total impact of discretion on performance is equal to the direct effect of discretion

on performance (d) when the moderator variable is zero (e.g. at its average level)

and is adjusted upwards or downwards to the extent that the moderator diverges

from zero. For example, if the moderator measures firm size, with M ¼ 0

representing an average-sized firm and M ¼ 1 a large firm, then the total impact

of discretion on performance is d þ m for a large firm, i.e. it exceeds the impact of

discretion in an average-sized firm (d) by the moderating effect of firm size (m).Given that the existing empirical studies on the impact of discretion on perfor-

mance have differed from each other as to whether and which moderators were

included (with most studies not modelling any moderators; see Sect. 2.2.4), only the

direct effects of discretion on performance (d) are fully comparable across studies.

Hence, when setting moderators, where included, to zero (i.e. settingM ¼ 0, which

reduces Equation (2.2) to d ), the total impact of discretion on performance in

existing studies can be inferred from the estimated direct effect of discretion on

performance (d):• If the direct effect is significantly greater than zero (d > 0 ), then discretion

is estimated as having a positive impact on performance, meaning granting a

manager more managerial discretion might increase performance.

• If the direct effect is significantly smaller than zero (d < 0), then discretion is

estimated as having a negative impact on performance, meaning granting a

manager more managerial discretion might reduce performance.

40 2 Literature Review and Hypotheses

• If the direct effect is insignificantly different from zero (d � 0), then discretion is

found to have an insignificant or neutral impact on performance, meaning

granting a manager more managerial discretion might not alter performance.

It should be noted, however, that an insignificant direct effect (d � 0) does not

prove discretion to have no impact on performance, since there might be a non-

zero impact on performance in the population, but e.g. the study’s sample might

be too small to provide significant evidence (Betton 1985, p. 3; Doehring 1988,

p. 104; Zhuravskaya 2000, p. 143).

Having conceptually decomposed empirical studies into their research designs

and empirical results, the next two sections review the extant literature with respect

to differences in empirical results (e.g. positive versus neutral versus negative

impacts on performance, d ; see Sect. 2.2.2) and differences in research designs

(e.g. unit of analysis, measures of discretion and performance, and modelling

methodology; see Sect. 2.2.3) in an effort to work towards resolving the discretion

puzzle.

2.2.2 Differences in Empirical Results

Drawing on the methodological discussion in the previous section (see Sect. 2.2.1),

this section compares and contrasts the empirical results on the impact of discretion

on performance in the extant literature in terms of the studies’ estimated directeffects of discretion on performance ( d in Equations (2.1) and (2.2) above).19

Consistently finding a positive (d > 0), neutral (d � 0) or negative (d < 0) direct

effect throughout existing studies would demonstrate that managerial discretion

tended to improve, not alter or reduce performance, respectively. However, the

review reveals that there is abundant contradictory evidence on discretion’s

impact on performance, ranging from positive (d > 0) to neutral (d � 0) and

negative (d < 0). It is therefore unclear whether additional discretion can be

expected to improve, not alter or reduce performance and this gives rise to the

discretion puzzle discussed in Sect. 1.1:20

• A number of scholars have found significant evidence that the direct effect of

discretion on performance is positive (d > 0), i.e. that granting a manager more

managerial discretion might increase performance (e.g. Agarwal et al. 2009;

Barnabas and Mekoth 2010; Chang and Wong 2003; Gammelgaard et al. 2010;

Khanchel 2009). These references demonstrate that empirical evidence of a

positive impact of discretion on performance spans different levels of

19 As explained in Sect. 2.2.1, when moderators deviate from zero, the impact of discretion on

performance deviates from the direct effect of discretion (d ) by moderating effects, which are

reviewed in Sect. 2.2.4.20 In order to achieve a broad coverage of existing empirical evidence, studies are also included if

they denote managerial discretion by alternative comparable terms, such as managerial autonomy

(see Sect. 2.1.1).

2.2 Impact of Managerial Discretion on Performance in Existing Empirical Evidence 41

management and geographies, e.g. hedge fund managers worldwide (Agarwal

et al. 2009), retail bank branch managers in India (Barnabas and Mekoth 2010),

top management in China (Chang and Wong 2003), management of foreign-

owned subsidiaries of multinationals in Europe (Gammelgaard et al. 2010), and

top management in Tunisia (Khanchel 2009).

• However, various scholars have also found significant evidence that the direct

effect of discretion on performance is negative (d < 0), i.e. that granting a

manager more managerial discretion might reduce performance (e.g. He et al.

2009; Heinecke 2011; Stano 1976; Williamson 1963; Xu et al. 2005).

Again, these studies exemplify that discretion might harm performance for

various levels of management and geographies, e.g. top management in the

United States (He et al. 2009; Stano 1976; Williamson 1963), regional manage-

ment of multinationals worldwide (Heinecke 2011), and top management in

China (Xu et al. 2005).

• Finally, scholars have found the direct effect of discretion on performance to be

insignificant (d � 0), meaning granting a manager more managerial discretion

might not alter performance (e.g. Caza 2011; Groves et al. 1994; Yougen Li and

Zhao 2004; Lopez-Navarro and Camison-Zornoza 2003; Venaik 1999). This

evidence on discretion not significantly altering performance likewise covers

multiple levels of management and geographies, e.g. managers of research and

development (R&D) units in Europe (Caza 2011), factory managers in China

(Groves et al. 1994), top management in China (Yougen Li and Zhao 2004),

general managers of Spanish export joint ventures (Lopez-Navarro and

Camison-Zornoza 2003), and marketing managers of subsidiaries of

multinationals worldwide (Venaik 1999).

While this contradictory evidence21 on the impact of discretion therefore spans

different levels of management and different geographies, it should be noted that

even for a given level of management in a given country, empirical studies have

estimated positive, neutral, and negative impacts of discretion on performance. This

is exemplified by top management in China, where Chang and Wong (2003, 2004)

and Zhang (1997) find a positive, Li and Zhao (2004) find a neutral, and Xu et al.

(2005) find a negative direct effect of managerial discretion on performance.

In short, there is an abundance of coexisting empirical evidence that managerial

discretion has a positive, neutral, and even negative impact on performance.

21 It should further be noted that in addition to empirical studies that explicitly aim to measure

managerial discretion or autonomy (exemplified by the references above), the contradictory

evidence extends to studies that implicitly measure constructs potentially related to discretion,

such as diffusion of ownership, managerial stock ownership, internal representation on the board,

and other measures of board composition. Chang and Wong (2003, p. 7) view such studies as

evidence of an inconclusive relationship between discretion and performance, with the empirical

findings of e.g. Donaldson and Davis (1991) and Kesner (1987) supporting a positive, those of

Chaganti et al. (1985), Demsetz and Lehn (1985), and Zahra and Stanton (1988) supporting a

neutral, and those of Baysinger and Butler (1985) and Palmer (1973) supporting a negative

relationship.

42 2 Literature Review and Hypotheses

Section 1.1 coined the term discretion puzzle for this ostensible paradox that accordingto empirical evidence, discretion increases, does not affect, and decreases performance,

which remains unexplained by the existing theories (i.e. managerial discretion theory,

principal-agent theory, and stewardship theory; see Sects. 1.1 and 2.3).

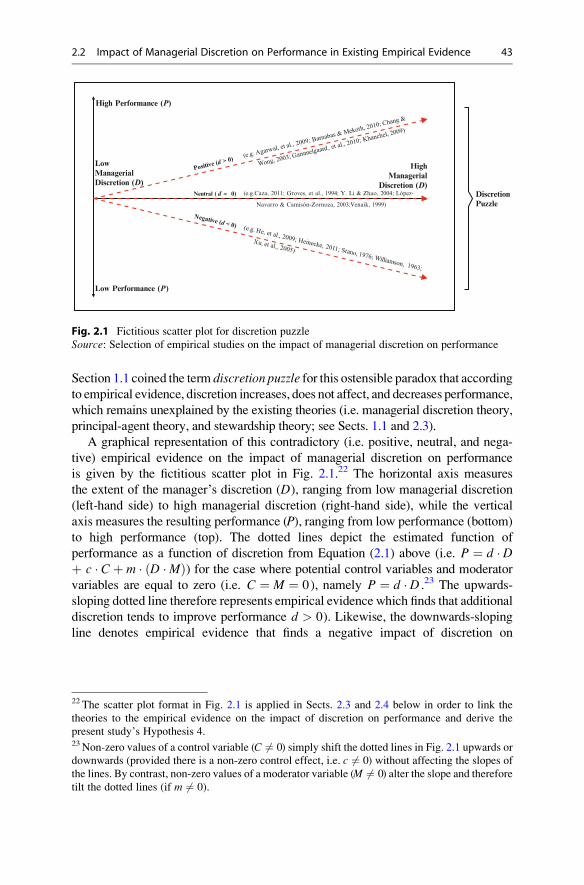

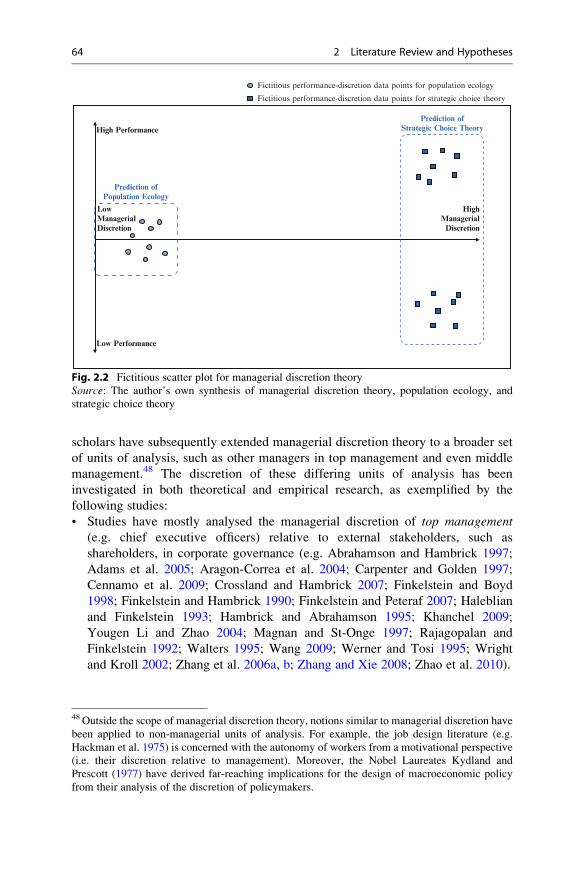

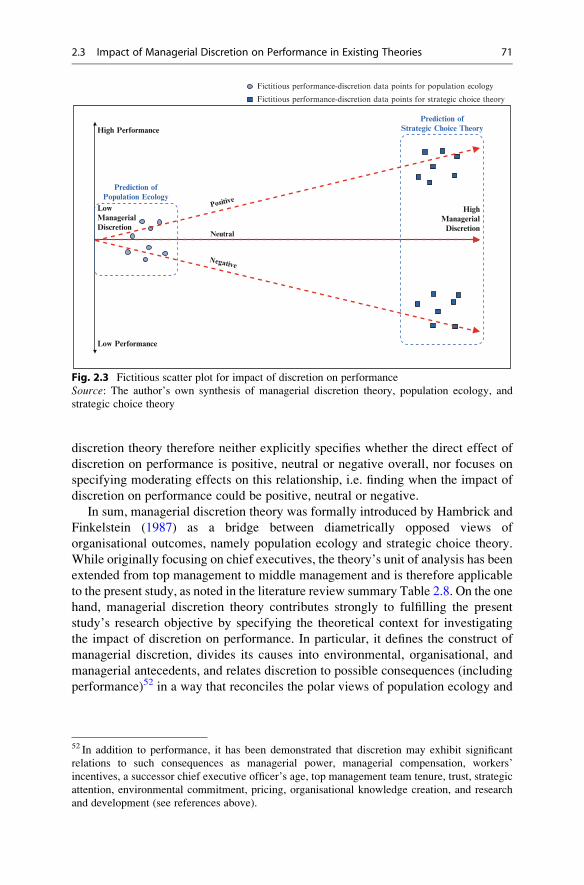

A graphical representation of this contradictory (i.e. positive, neutral, and nega-

tive) empirical evidence on the impact of managerial discretion on performance

is given by the fictitious scatter plot in Fig. 2.1.22 The horizontal axis measures

the extent of the manager’s discretion (D), ranging from low managerial discretion

(left-hand side) to high managerial discretion (right-hand side), while the vertical

axis measures the resulting performance (P), ranging from low performance (bottom)

to high performance (top). The dotted lines depict the estimated function of

performance as a function of discretion from Equation (2.1) above (i.e. P ¼ d � Dþ c � Cþ m � D �Mð Þ) for the case where potential control variables and moderator

variables are equal to zero (i.e. C ¼ M ¼ 0), namely P ¼ d � D .23 The upwards-

sloping dotted line therefore represents empirical evidence which finds that additional

discretion tends to improve performance d > 0). Likewise, the downwards-sloping

line denotes empirical evidence that finds a negative impact of discretion on

High Performance (P)

LowManagerialDiscretion (D)

HighManagerial

Discretion (D)

Low Performance (P)

DiscretionPuzzle

Neutral ( d ≈ 0) (e.g.Caza, 2011; Groves, et al., 1994; Y. Li & Zhao, 2004; López-

Navarro & Camisón-Zornoza, 2003;Venaik, 1999)

Fig. 2.1 Fictitious scatter plot for discretion puzzle

Source: Selection of empirical studies on the impact of managerial discretion on performance

22 The scatter plot format in Fig. 2.1 is applied in Sects. 2.3 and 2.4 below in order to link the

theories to the empirical evidence on the impact of discretion on performance and derive the

present study’s Hypothesis 4.23 Non-zero values of a control variable (C 6¼ 0) simply shift the dotted lines in Fig. 2.1 upwards or

downwards (provided there is a non-zero control effect, i.e. c 6¼ 0) without affecting the slopes of

the lines. By contrast, non-zero values of a moderator variable (M 6¼ 0) alter the slope and therefore

tilt the dotted lines (if m 6¼ 0).

2.2 Impact of Managerial Discretion on Performance in Existing Empirical Evidence 43

performance (d < 0). Finally, the flat line depicts empirical evidence that finds an

insignificant (or neutral) impact of discretion on performance (d � 0). This fictitious

scatter plot therefore reveals that when treating existing empirical evidence at an

aggregate level in terms of their estimated impact of managerial discretion on

performance, their results are divergent, ranging from positive to neutral and even

negative. These contradictory results give rise to the discretion puzzle, as indicated in

Fig. 2.1.24 In order to work towards resolving the discretion puzzle, the next section

explores differences in the research designs of existing studies as potential causes for

their widely differing estimated impacts of discretion on performance.

2.2.3 Differences in Research Designs

In order to work towards resolving the discretion puzzle (i.e. the research objective;

see Sect. 1.2), this section turns to diagnosing potential causes for why existing

empirical studies might have produced such divergent empirical results as shown in

Fig. 2.1 in Sect. 2.2.2. As Sect. 2.2.1 has defined a study’s research design as all

methodological aspects that produce a study’s particular empirical results, differences

in research designs between existing studies could be potential causes for differences

in empirical results between existing studies (i.e. differences in d). In particular, the

differences in the chosen unit of analysis, measures of discretion and performance,

and modelling methodology between existing studies might be able to explain the

positive, neutral, and negative estimated impacts of managerial discretion on perfor-

mance across studies and thereby help resolve the discretion puzzle.25

Yet it is first of all necessary to identify the differences in aspects of the research

designs underlying the existing studies under review before maintaining that such

aspects can at least in part explain disparities in the empirical results of those

studies. This section therefore explores whether and which research design aspects

have differed between studies, thus diagnosing whether they could be potential

causes for the observed differences in empirical results. It is found that empirical

studies have indeed varied strongly in their research designs, enforcing the notion

that the differences in research designs might help explain the differences in the

estimated results for the impact of discretion (i.e. positive, neutral, and negative):

24 It should be noted that due to their observational cross-sectional designs, the existing empirical studies

cannot unequivocally demonstrate that additional discretion causes an increase or decrease in perfor-

mance but rather only make statements regarding association that may be consistent with causality

(e.g. Caza 2007, p. 46; Finkelstein and Hambrick 1990, p. 500; Granger 1969; Sanchez 2008, p. 5;

Simon 1954, pp. 477–478; Wagner 2002, pp. 287–292; see Sect. 5.4.1).25 For example, if two different studies adopt two different measures of discretion, each of which

taps into a distinct dimension of discretion, then one study might find a positive and the other a

negative impact of discretion on performance, provided the distinct discretion dimensions have

different performance impacts.

44 2 Literature Review and Hypotheses

• The unit of analysis (i.e. manager whose discretion is analysed) has varied across

studies on the impact of discretion in a number of ways, including with respect to

geography, level of management, firm type, and firm size:

– Geography. Empirical studies have analysedmanagers worldwide (e.g. Agarwal

et al. 2009; Crossland and Hambrick 2007; Venaik 1999), in the United States

(e.g. He et al. 2009; Stano 1976; Tang 2008), in European countries (e.g. Caza

2011; Gammelgaard et al. 2010), in Asian countries (e.g. Barnabas and Mekoth

2010; Yougen Li and Zhao 2004), and in African countries (e.g. Khanchel 2009;

Ongore 2011).

– Level of management. Most studies have focused on top management as the

unit of analysis (e.g. Chang and Wong 2003, 2004; Xiaoyang Li 2007;

Walters 1995; Zhao et al. 2010) although individual studies have investigated

the discretion of middle management (e.g. Caza 2007).

– Firm type. Empirical studies have combined firms to various (partly

overlapping) aggregates, such as listed firms (e.g. Huiyuan Chen 2006;

Zhang and Li 2008b; Zhang and Xie 2008), multinational corporations

(e.g. Heinecke 2011; Thomas and Peyrefitte 1996; Wang et al. 2008), inter-

national joint ventures (e.g. Lopez-Navarro and Camison-Zornoza 2003; Yan

et al. 2010), and state-owned enterprises (e.g. Groves et al. 1994; Xu et al.

2005; Zhang 1997).

– Firm size. Units of analysis in studies have ranged from small firms with a

few hundred employees (e.g. Cheng et al. 2006) to large firms with tens of

thousands of employees (e.g. Adams et al. 2005; Werner and Tosi 1995;

Williamson 1963) or combinations of smaller and larger firms.

– In addition to these examples of differences in the unit of analysis, the

managers investigated in the empirical literature have varied in a number of

other ways, such as in terms of industry and time-related aspects.26

Before exploring differences in the next aspect of the research design, the

above review of differences in the unit of analysis between existing studies is

utilised to derive implications for the unit of analysis of the present study. While

the literature review has shown that there have been individual studies for

middle management and China, compared to the total amount of studies, evi-

dence on the impact of discretion on performance has remained particularly

scarce for both middle management (see Caza 2007, p. 1) and for China (see

Yougen Li and Zhao 2003, p. 6; Zhang and Li 2008a, pp. 37–38). It follows that

given the abundance of middle managers in organisations27 and the importance

of China for domestic Chinese firms and foreign multinationals (Aminpour and

Woetzel 2006, p. 41; Grant 2006, p. 25; Hexter 2006, p. 1; Hoover 2006, p. 92;

26 As noted in Chap. 3, a unit of analysis is also defined in terms of time (Northrop and Arsenault

2007, p. 214).27 As explained in Chap. 3, there are tens of thousands of plant managers in China alone (Guojia

tongji ju [National Bureau of Statistics] 2007, 14–1, 14–2, 14–18). With plant managers being but

one example of middle managers, this translates into an even larger number of middle managers in

organisations worldwide.

2.2 Impact of Managerial Discretion on Performance in Existing Empirical Evidence 45

Kaufmann et al. 2005, p. 21; McGregor 2005, pp. 2, 272; Pascha 1998, p. 57;

Taube 2008, p. 186; Tian 2007, pp. 7–8), this limited evidence on the impact of

discretion motivates the choice of middle management in China as the unit of

analysis (see Sect. 2.4.4 and Chap. 3). In addition, the differences between

existing studies in the unit of analysis’ firm type and firm size lead to the

formulation of Hypotheses 2 and 3—as discussed below in Sect. 2.2.4.

• As with the unit of analysis, the measure of discretion and the measure ofperformance have also varied strongly across existing studies, confirming

differences in these measures as potential causes for the observed differences

in empirical results between studies. The breadth of different discretion

measures employed is exemplified in Table 2.5, which segments different

measures of discretion according to their implicit assumptions regarding the

dimensions of discretion (which have been discussed in Sect. 2.1.2).28 The threerows in Table 2.5 correspond to studies that assume managerial discretion to be

unidimensional (first row) or multidimensional (second row) or that make no

assumption regarding discretion’s dimensionality (third row):

– Unidimensional. As explained in Sect. 2.1.2, most empirical studies have

assumed thatmanagerial discretion is unidimensional in the sense that discretion

(across multiple areas of the manager’s work) can be measured overall by a

single construct (which then is expected to either increase, not alter or decrease

performance). Among these studies, however, there has been considerable

variation in terms of how the assumed unidimensional construct of discretion

is measured. Table 2.5 shows that one possibility is to measure a manager’s

discretion in a single dimension of his/her work and to take this to represent

discretion overall (e.g. Acemoglu et al. 2007).29Another possibility is to gauge a

manager’s discretion across several dimensions of his/her work and combine

these indicators into a single construct of discretion (e.g. Barnabas and Mekoth

2010;Caza 2007;Chang andWong2003;Cheng et al. 2006;Gammelgaard et al.

2010).30 A third possibility is to gauge a single construct of discretion not by

direct measures of the manager’s discretion but rather by proxy measures that

are expected to be empirically related to discretion overall (e.g. Agarwal et al.