Embed Size (px)

Citation preview

Country Profile 2006

Malaysia This Country Profile is a reference work, analysing the country�s history, politics, infrastructure and economy. It is revised and updated annually. The Economist Intelligence Unit�s Country Reports analyse current trends and provide a two-year forecast.

The full publishing schedule for Country Profiles is now available on our website at www.eiu.com/schedule The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For over 50 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where the latest analysis is updated daily; through printed subscription products ranging from newsletters to annual reference works; through research reports; and by organising seminars and presentations. The firm is a member of The Economist Group.

London The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom Tel: (44.20) 7576 8000 Fax: (44.20) 7576 8500 E-mail: [email protected]

New York The Economist Intelligence Unit The Economist Building 111 West 57th Street New York NY 10019, US Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 E-mail: [email protected]

Hong Kong The Economist Intelligence Unit 60/F, Central Plaza 18 Harbour Road Wanchai Hong Kong Tel: (852) 2585 3888 Fax: (852) 2802 7638 E-mail: [email protected]

Website: www.eiu.com

Electronic delivery This publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, online databases and as direct feeds to corporate intranets. For further information, please contact your nearest Economist Intelligence Unit office

Copyright © 2006 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, the Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 1741-0096

Symbols for tables �n/a� means not available; ��� means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

Ten

om

Ko

ta K

inab

alu

San

dak

anR

anu

Ran

uR

anu

Lah

ad D

atu Ta

wau

Sem

po

rna

Ku

dat

Bala

mba

ngan

Ba

ngg

iB

an

ggi

Ba

ngg

iB

an

ggi

Bea

ufo

rtB

eau

fort

Bea

ufo

rtLa

bua

n I

s. Bru

nei

Ba

y

Mir

i

BBin

tulu

Sib

u Sim

anSi

man

gg

ang

gg

ang

Sim

ang

gan

g

Ku

chin

g

Sem

atan

BR

UN

EI

IND

ON

ES

IA

SA

RA

WA

K

SA

BA

H

Cro

cker

Range

Cro

cker

Range

SOU

TH C

HIN

ASE

A

SULU

SEA

CELE

BES

SEA

Ba

lab

ac

Stra

itB

ala

ba

cSt

rait

Ba

lab

ac

Stra

it

THEPHILIP

PINES

Ipo

hIp

oh

Ku

ala

Lip

isK

ual

a Li

pis

Tap

ahTa

pah

Tem

erlo

hTe

mer

loh

KU

ALA

LU

MP

UR

KU

ALA

LU

MP

UR

aya

aya

KU

ALA

LU

MP

UR

Ku

ala

Tere

ng

gan

u

Ipo

h

Joh

or

Bah

aru

Pu

traj

aya

Pu

traj

aya

Pu

traj

aya

Pet

alin

g J

aya

Geo

rget

ow

n

Ko

ta B

ahar

u

Ku

ala

Ker

aiK

ual

a K

erai

Ku

ala

Ker

ai

Du

ng

un

Chu

kai

Ku

anta

n

Tum

pat

Tum

pat

Tum

pat

Mel

aka

Mel

aka

Klu

ang

Klu

ang

JOH

OR

JOH

OR

Mer

sin

g

Tio

ma

n I

s.

Klu

ang

Sere

mb

anSe

rem

ban

Seg

amat

Seg

amat

Sere

mb

an

Ku

ala

Lip

isTa

pah

Tem

erlo

h

Seg

amat

Mu

ar

Bat

u P

ahat

Kel

ang

Bag

an D

atu

kTe

luk

An

son

Bat

u G

ajah

Pari

t B

un

tai

Alu

r Se

tar Ta

ipin

g

Pera

iPe

rai

PE

RA

KP

ER

AK

KE

LA

NTA

NK

EL

AN

TAN

Pera

i

Kan

gar

Kan

gar

Kan

gar

MA

LA

YS

IAM

AL

AY

SIA

MA

LA

YS

IA

THA

ILA

ND

IND

ON

ES

IA

SIN

GA

PO

RE

SOU

TH C

HIN

A

SEA

Stra

it o

f M

ala

cca

TER

EN

GG

AN

UTE

RE

NG

GA

NU

TER

EN

GG

AN

U

PA

HA

NG

PE

RA

K NG

OR

NG

OR

SE

LA

NG

OR

AN

AN

NE

GE

RI

SE

MB

ILA

N

MA

LA

CC

AJO

HO

R

KE

DA

H

PE

RL

IS

PE

NA

NG

KE

LA

NTA

N

Mel

aka

0 k

m10

02

00

0 m

iles

100

150

50

0 k

m10

02

00

30

0

0 m

iles

100

150

50

Oct

obe

r 2

00

6

Mai

n r

ailw

ay

Mai

n r

oad

Inte

rnat

ion

al b

ou

nd

ary

Ad

min

istr

ativ

e b

ou

nd

ary

Mai

n a

irp

ort

Cap

ital

Maj

or

tow

n

Oth

er t

ow

n

© T

he

Eco

no

mis

t In

tell

igen

ce U

nit

Lim

ited

20

06

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

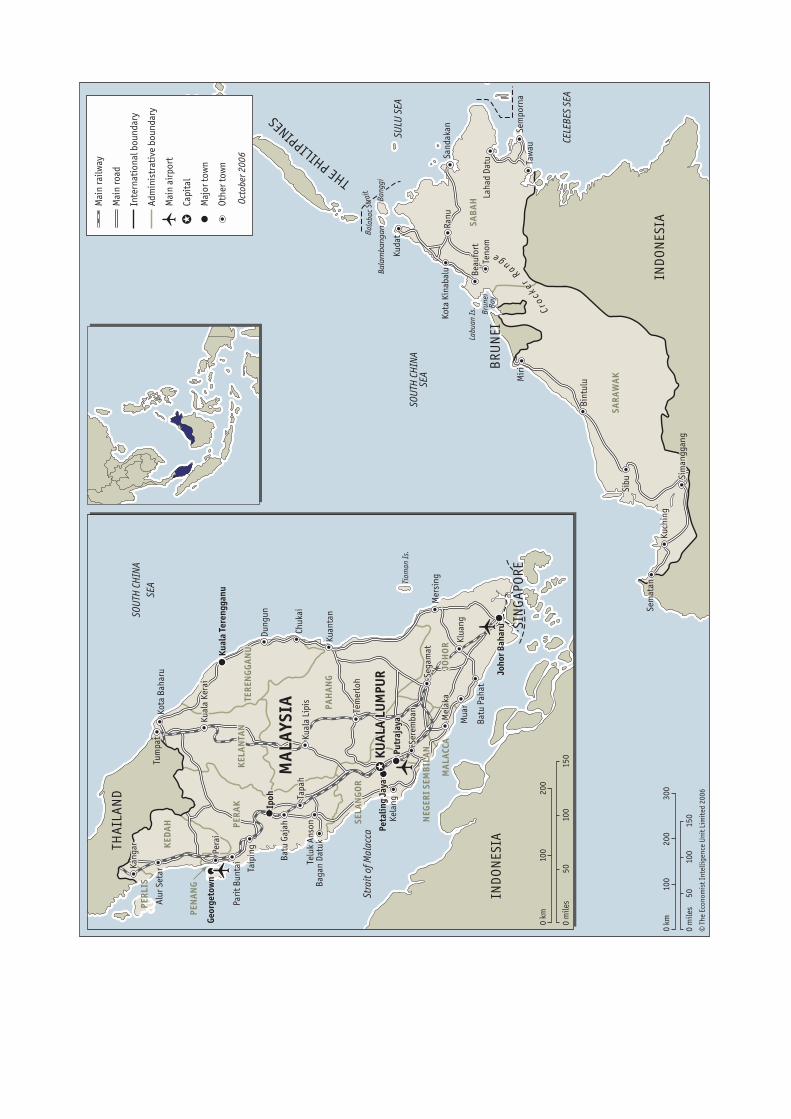

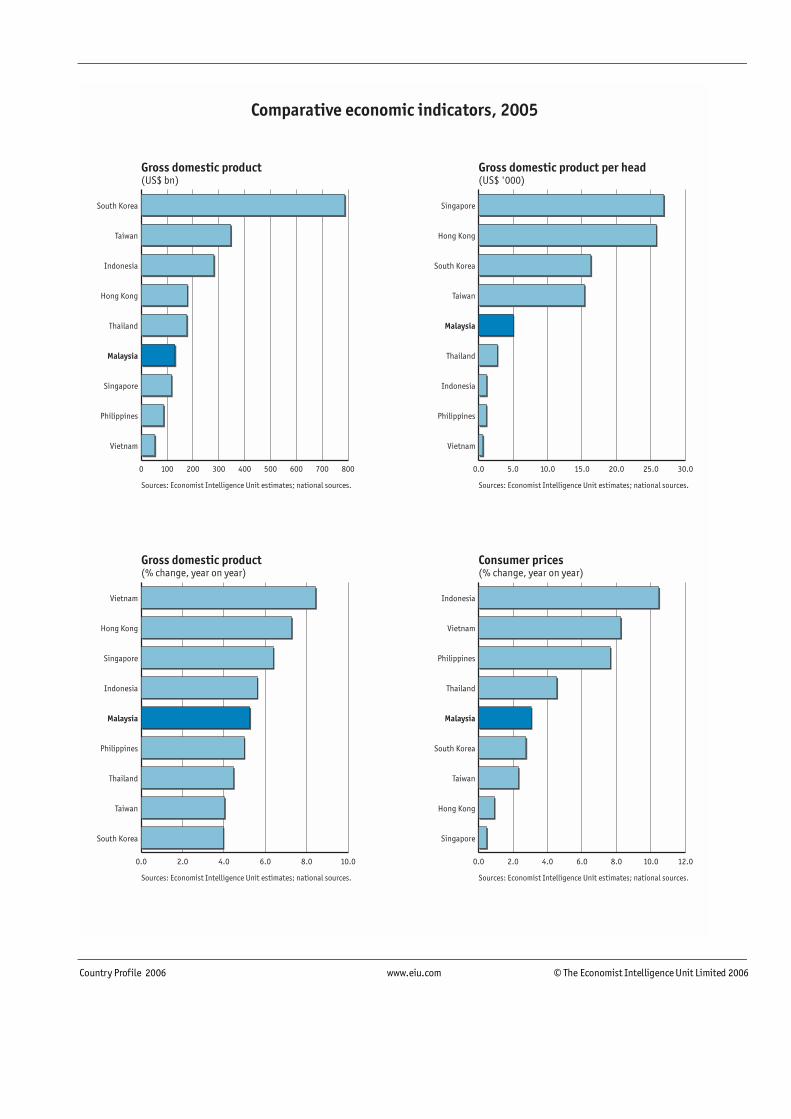

Comparative economic indicators, 2005

Gross domestic product(US$ bn)

Sources: Economist Intelligence Unit estimates; national sources.

Gross domestic product(% change, year on year)

Sources: Economist Intelligence Unit estimates; national sources.

Consumer prices(% change, year on year)

Sources: Economist Intelligence Unit estimates; national sources.

Gross domestic product per head(US$ '000)

Sources: Economist Intelligence Unit estimates; national sources.

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Vietnam

Philippines

Indonesia

Thailand

Malaysia

Taiwan

South Korea

Hong Kong

Singapore

0 100 200 300 400 500 600 700 800

Vietnam

Philippines

Singapore

Malaysia

Thailand

Hong Kong

Indonesia

Taiwan

South Korea

0.0 2.0 4.0 6.0 8.0 10.0 12.0

Singapore

Hong Kong

Taiwan

South Korea

Malaysia

Thailand

Philippines

Vietnam

Indonesia

0.0 2.0 4.0 6.0 8.0 10.0

South Korea

Taiwan

Thailand

Philippines

Malaysia

Indonesia

Singapore

Hong Kong

Vietnam

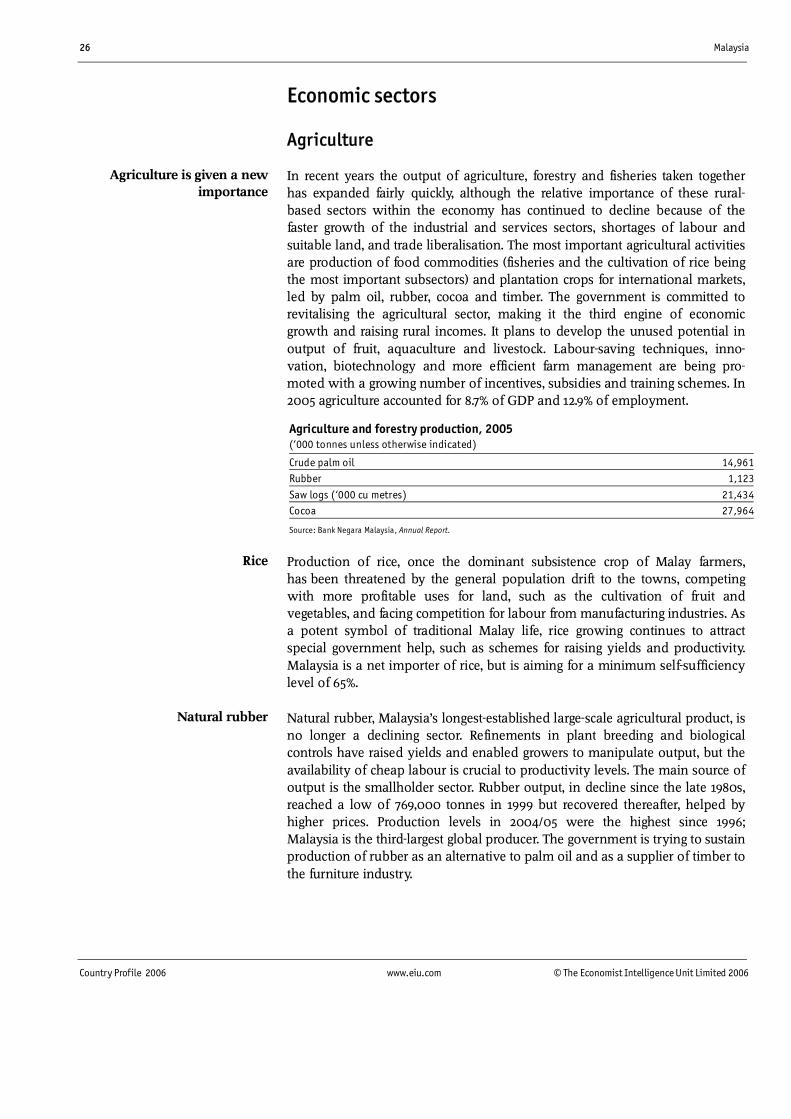

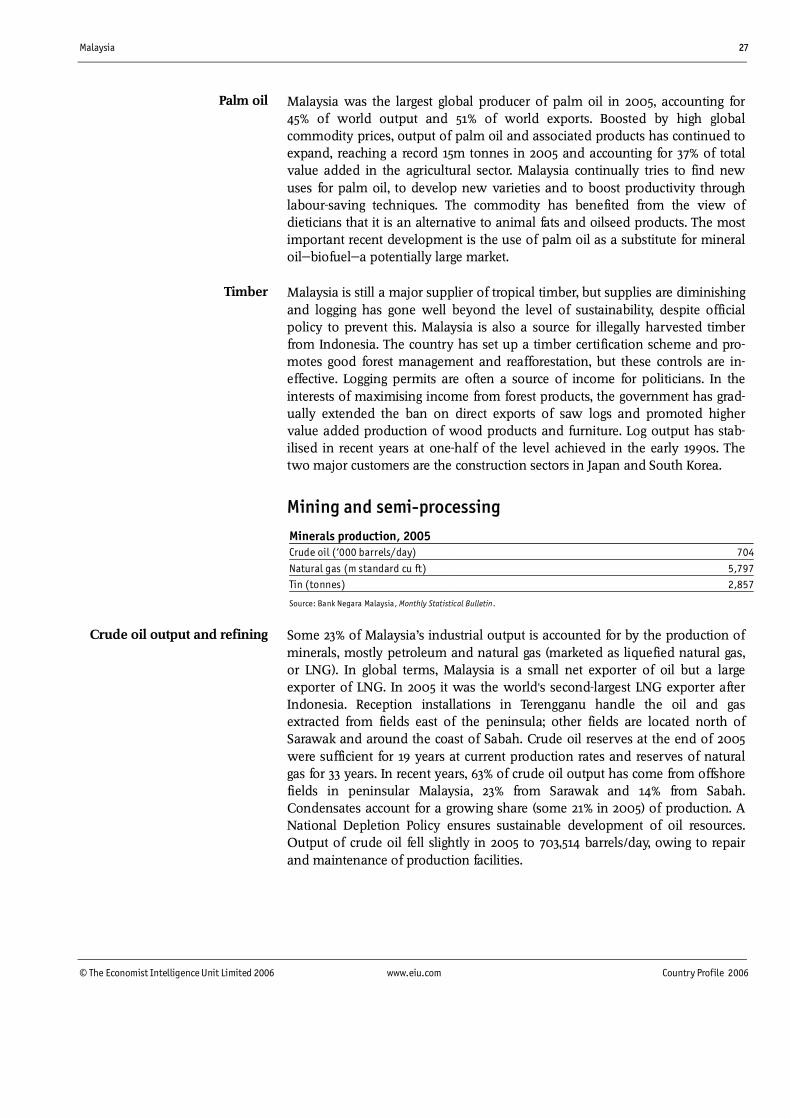

Malaysia 1

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Contents

Malaysia

3 Basic data

4 Politics 4 Political background 6 Recent political developments 9 Constitution, institutions and administration 10 Political forces 12 International relations and defence

15 Resources and infrastructure 15 Population 16 Education 16 Health 17 Natural resources and the environment 18 Transport, communications and the Internet 19 Energy provision

20 The economy 20 Economic structure 21 Economic policy 23 Economic performance 25 Regional trends

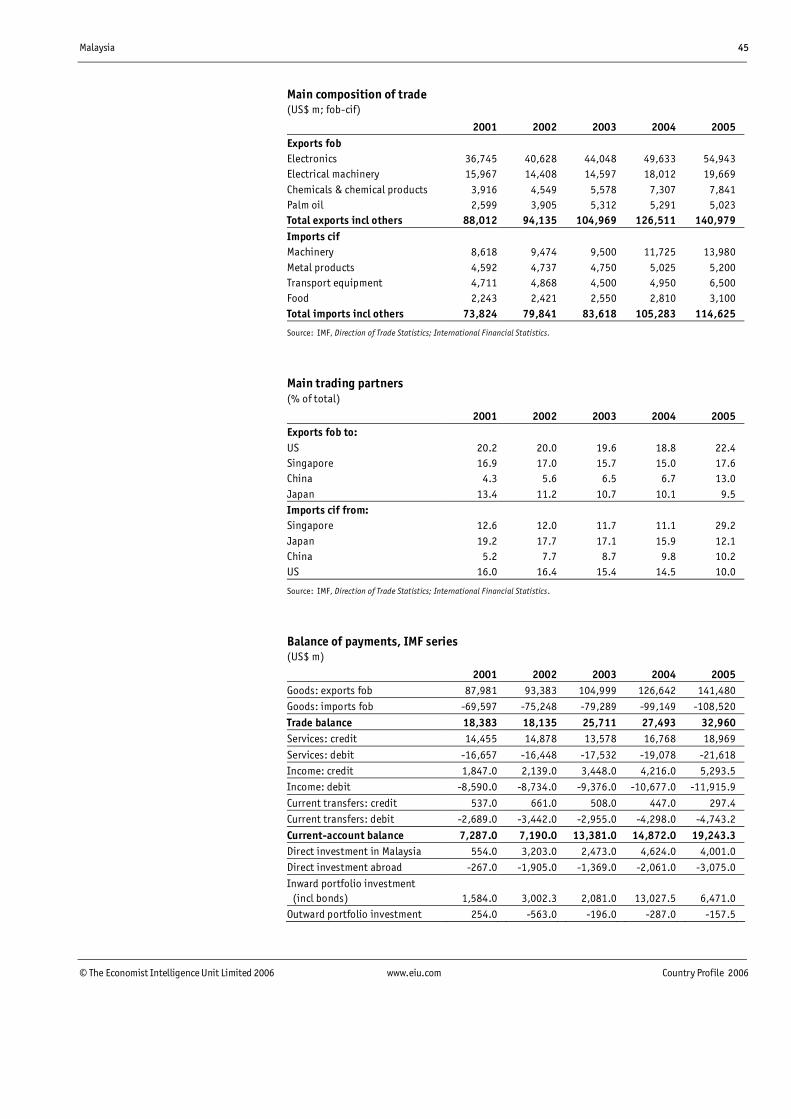

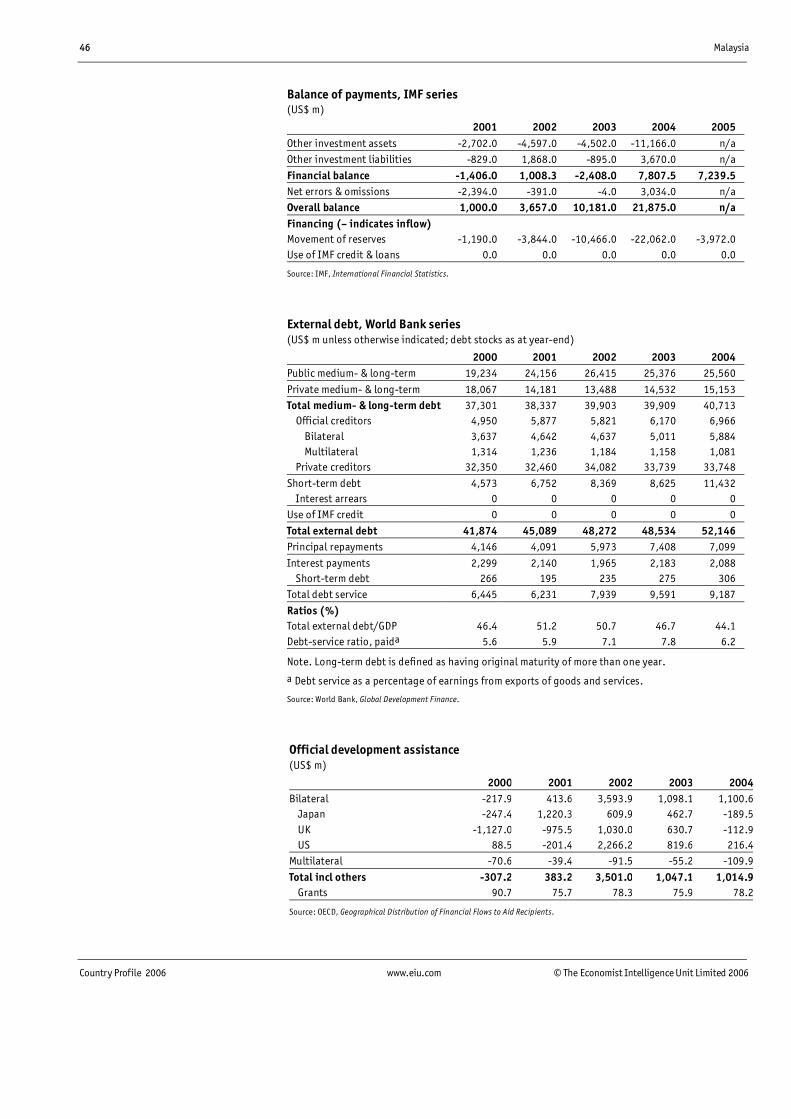

26 Economic sectors 26 Agriculture 27 Mining and semi-processing 28 Manufacturing 29 Construction 30 Financial services 31 Other services

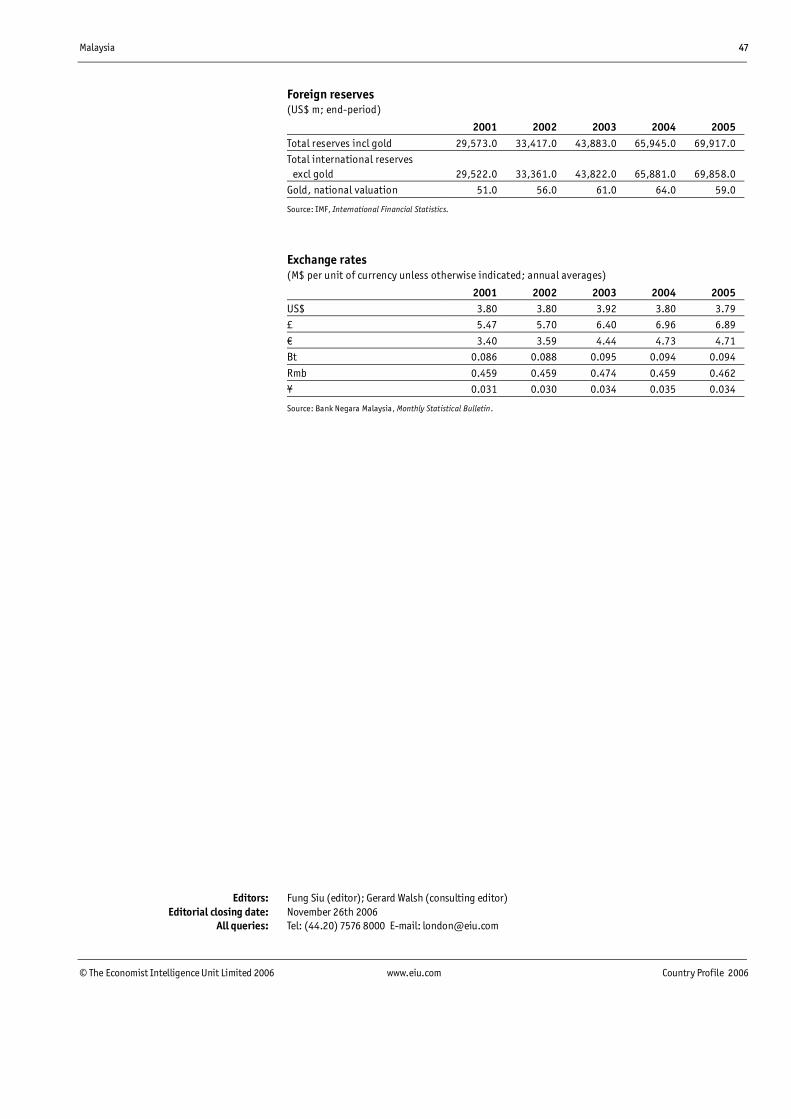

32 The external sector 32 Trade in goods 34 Invisibles and the current account 34 Capital flows and foreign debt 35 Foreign reserves and the exchange rate

36 Regional overview 36 Membership of organisations

38 Appendices 38 Sources of information 39 Reference tables 39 Population 39 Labour force 40 Transport statistics 40 Energy production

2 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

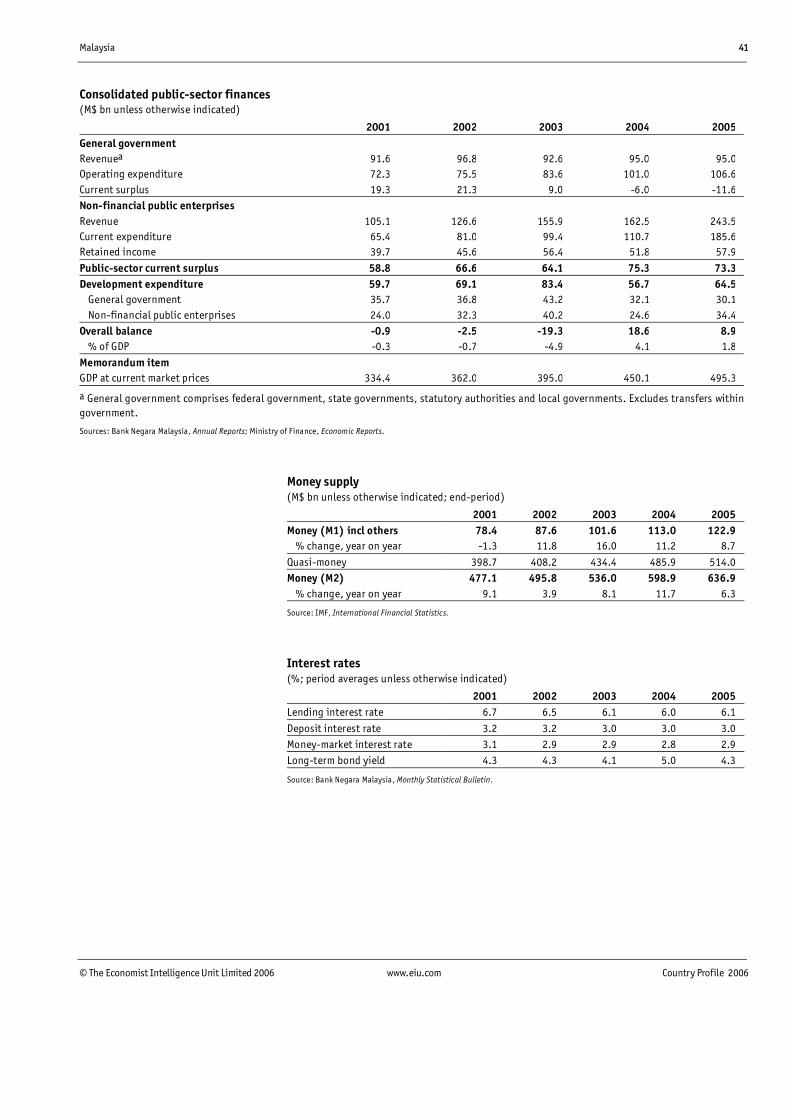

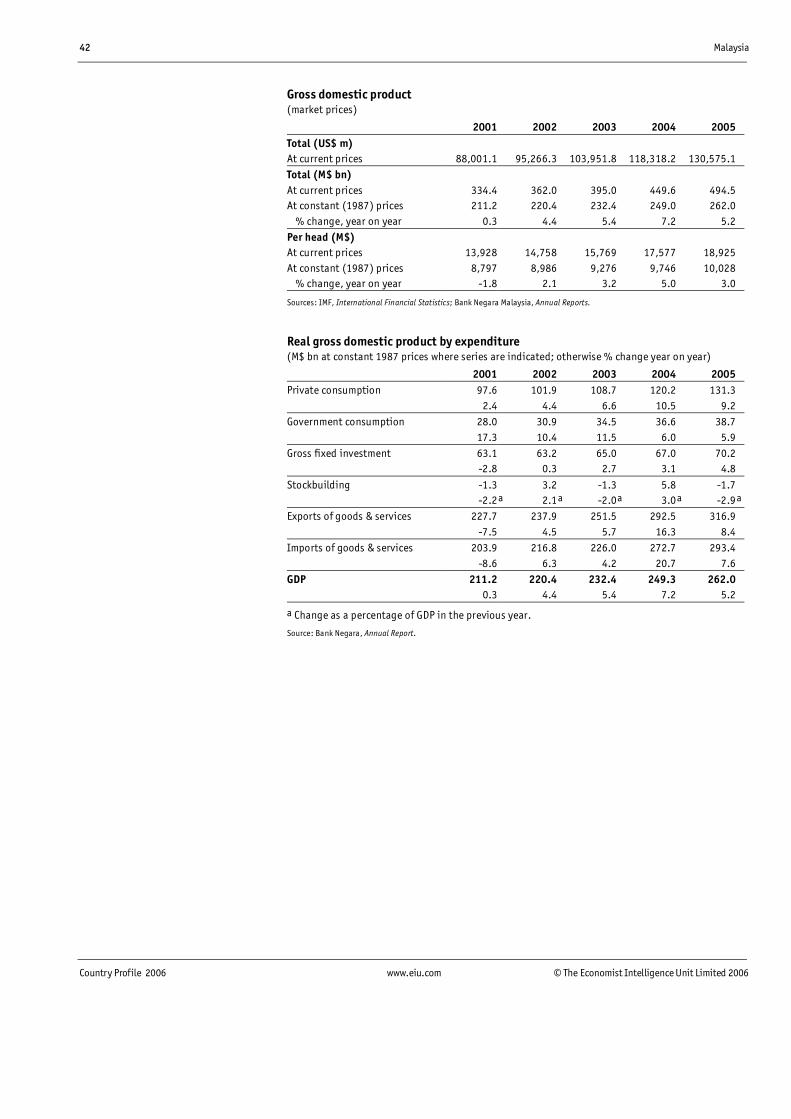

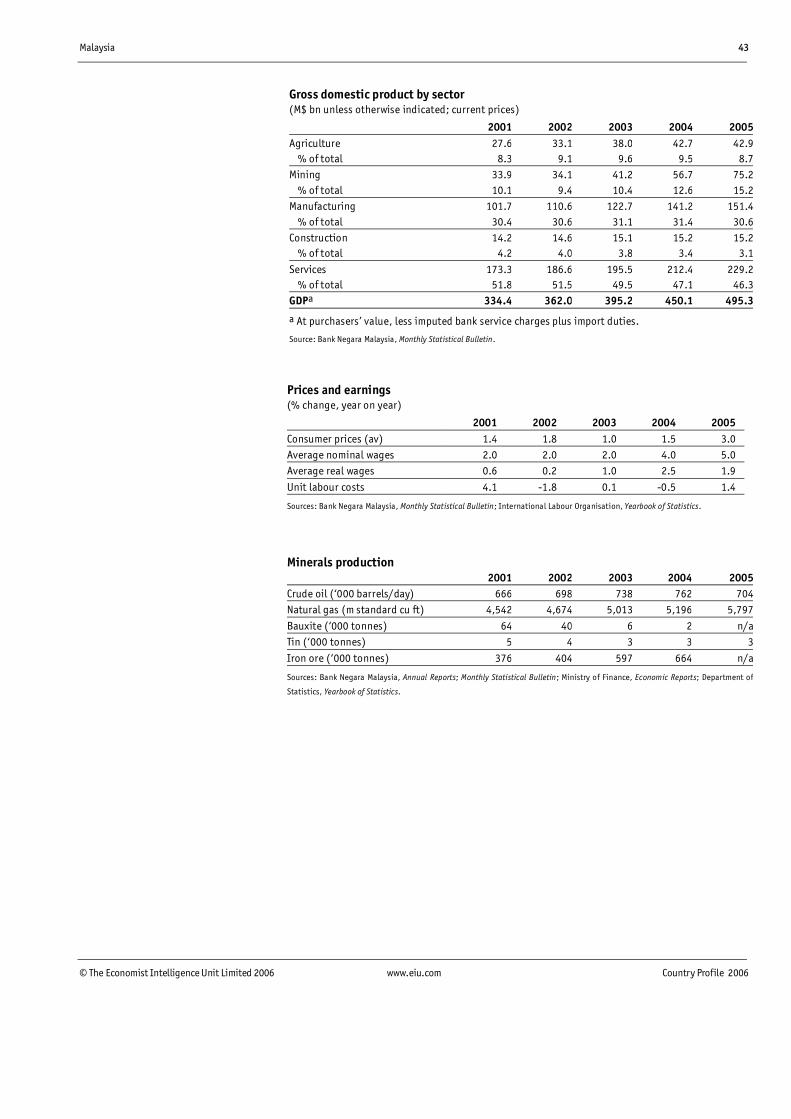

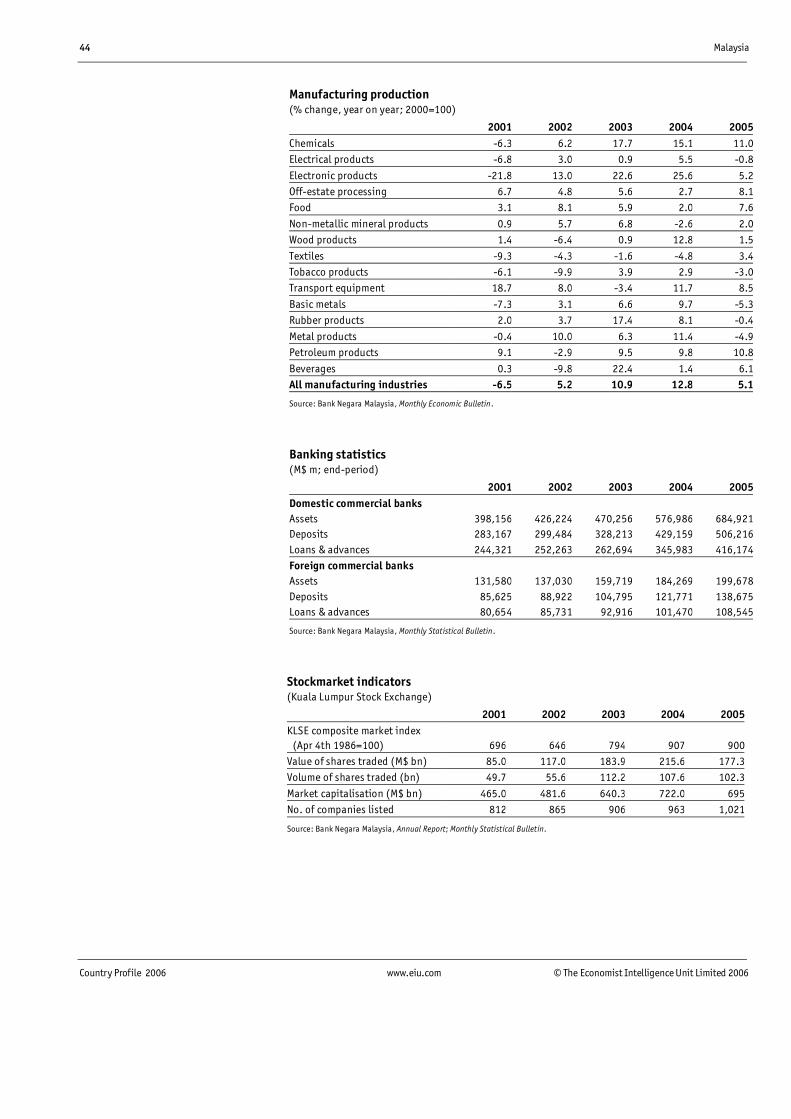

41 Consolidated public-sector finances 41 Money supply 41 Interest rates 42 Gross domestic product 42 Real gross domestic product by expenditure 43 Gross domestic product by sector 43 Prices and earnings 43 Minerals production 44 Manufacturing production 44 Banking statistics 44 Stockmarket indicators 45 Main composition of trade 45 Main trading partners 45 Balance of payments, IMF series 46 External debt, World Bank series 46 Official development assistance 47 Foreign reserves 47 Exchange rates

Malaysia 3

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Malaysia

Basic data

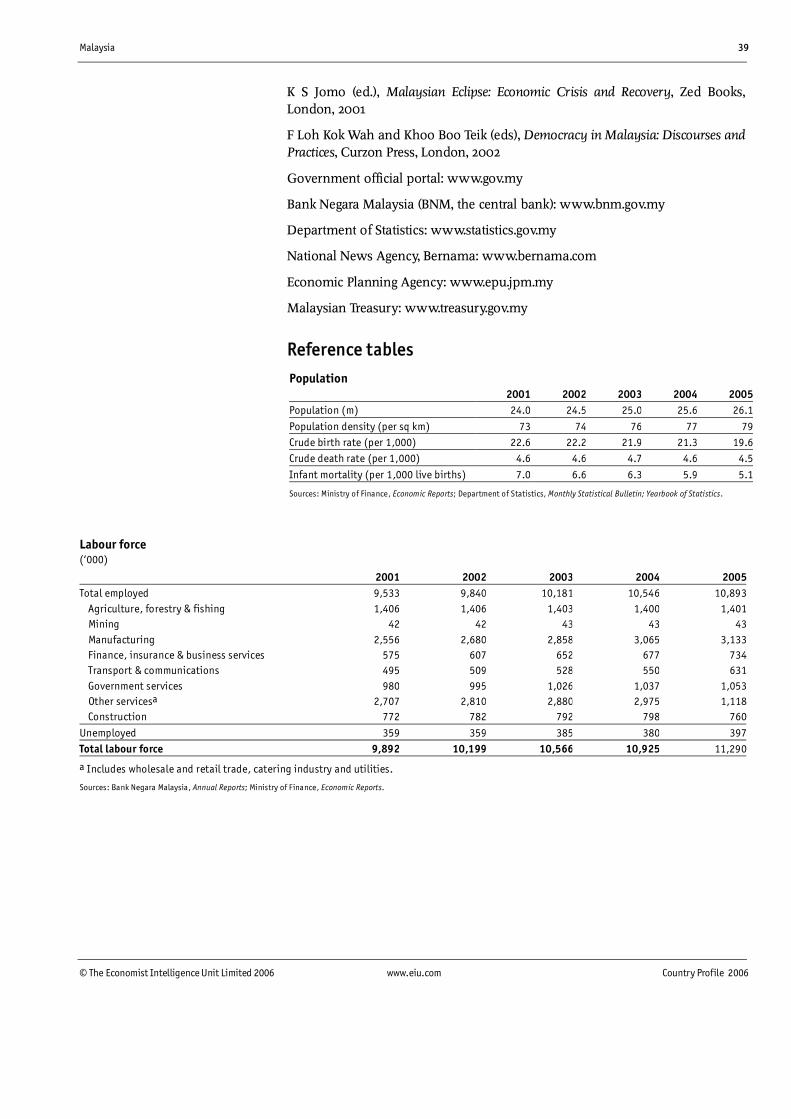

330,113 sq km

26.1m

Population in �000 (2002)

Kuala Lumpur (capital) 1,367 Johor Baharu 724 Klang 632 Ipoh 601 Petaling Jaya 460

Tropical

Hottest months, April and May, 23-33°C (average daily minimum and maximum); coldest month, December, 22-32°C; driest month, July, 99 mm average rainfall; wettest month, April, 292 mm average rainfall

Malay (the official language); main other languages: Chinese (Min Nan, Hakka, Mandarin and Min Dong), English, Tamil, Iban (in Sarawak), Banjar (in Sabah). There are 140 languages spoken in Malaysia (peninsular Malaysia 40, Sabah 54, Sarawak 46)

Malaysia uses the metric system but some British weights and measures are still in use. Local measures include:

1 pikul=25 gantang=100 katis=60.48 kg 1 koyan=40 pikul=2.419 tonnes

Ringgit or Malaysian dollar (M$, or RM)=100 sen (cents). Average exchange rates in 2005: M$3.79:US$1; M$6.89:£1. On July 21st 2005 the central bank abandoned the fixed exchange-rate system, which pegged the ringgit to the US dollar at M$3.8:US$1, for a managed float against a trade-weighted basket of currencies. Exchange rates on November 3rd 2006: M$3.64:US$1; M$6.93:£1

Peninsula: 7 hours ahead of GMT; Sabah and Sarawak: 8 hours ahead of GMT

January 1st (New Year!s Day); January 10th (Eid Al-Adha); January 29th-30th (Chinese New Year); January 31st (Islamic New Year); April 11th (the Prophet Mohammed�s birthday); May 1st (Labour Day); May 12th (Vesak day); June 3rd (the king�s birthday); August 31st (National Day); October 21st (Deepavali); October 23rd (Eid Al-Fitr, the end of Ramadan); December 25th (Christmas Day); December 31st (Hari Raya Qurban)

Total area

Climate

Weather in Kuala Lumpur (altitude 39 metres)

Languages

Measures

Currency

Time

Public holidays, 2006

Population

Main towns

4 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Politics

Political background

Fundamental to the understanding of Malaysia�s political development is an appreciation of its geographical, ethnic and cultural diversity. Political parties are largely based on ethnicity, locality or religion. Basic themes of post-war political history are the maintenance of racial harmony, positive discrimination in favour of the bumiputera (�sons of the soil�"ethnic Malays and other indi-genous peoples) and friction between Islamic parties and the government. Since independence in 1957, Malaysia has been ruled by coalition governments dominated by the principal Malay party, the United Malays National Organisation (UMNO).

British colonial policy was the major formative influence on Malaysia. From the late 18th century, British influence was gradually extended across the Malay peninsula and North Borneo. The colonial administration encouraged (and sponsored) the arrival of immigrants from southern China and southern India to work in tin mines and on rubber plantations. As the region developed into a commodity exporter, it remained administratively fragmented, with internal government largely under local control. By the 1930s, �Malaysia� consisted of the Straits Settlements (Malacca, Penang and Singapore), the Federated Malay States (Selangor, Perak, Negeri Sembilan and Pahang) and the unfederated states (Kedah, Perlis, Kelantan, Terengganu and Johor), as well as North Borneo (Sabah) and Sarawak.

After the second world war, the restored British colonial system sought to create a more integrated territory, a more cohesive society and a stronger central government. The ethnic Chinese were in the majority on the Malayan peninsula, including Singapore. The new Malayan Union (1946-48) soon collapsed as a result of opposition from the Malay rulers to a loss of sovereignty and proposed citizenship for non-Malays. Relations between the different ethnic groups, especially between the Malays and the Chinese, have remained a highly sensitive issue in Malaysian political life.

After the second world war, many of the ethnic Chinese sympathised with the communist revolution in China. A guerrilla war was started by the largely ethnic-Chinese Malayan Communist Party, leading to the declaration of a State of Emergency in 1948, which did not officially come to an end until 1960. One of the measures used by the colonial regime to suppress the insurrection was detention without trial, a practice that successive Malaysian governments have continued to employ. The Emergency was to cast a long shadow over Malaysian politics.

Rapid progress towards full independence"which was proclaimed in 1957"and the establishment of democracy in a pluralist society formed part of the anti-insurgency strategy. The successor of the Malayan Union, the Federation of Malaya (1948-63), passed some powers back to the states. Singapore, with its largely Chinese population, was excluded from both arrangements. The

Independence was proclaimed in 1957

Malaysia under British influence

Malaysia 5

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

political framework that emerged reflected Malaysia�s ethnic variety. UMNO was formed in 1946, and the Malaysian Chinese Association and the Malayan Indian Congress were founded in 1949. These three parties formed the Alliance in 1952 and have remained the core of post-independence governments.

British decolonisation policy continued to shape the country after independ-ence. Sarawak, Sabah and Singapore were added to the peninsula-based federation in 1963 to form a new Federation of Malaysia, with the North Borneo territories offsetting the preponderance of ethnic-Chinese citizens resulting from Singapore�s membership. Brunei refused to join the federation because of a disagreement over the position of the sultan and the control of oil resources. When Singapore withdrew from the federation in 1965, there was a decisive switch in political power towards the ethnic Malays and the central government in Kuala Lumpur.

Losses for UMNO in the 1969 general election stirred up anti-Chinese sentiment and provoked serious race riots, in which many Chinese were killed. The riots were a political and economic turning point. In the crisis that followed, parlia-mentary government was suspended for 21 months. The Alliance that had ruled since independence was replaced by a broader-based coalition, the Barisan Nasional (BN, National Front). With minor changes in its composition, the BN has ruled Malaysia ever since. After the riots the BN government instituted a 20-year New Economic Policy (NEP), a programme of positive dis-crimination aimed at reducing interracial tensions by improving the incomes and economic weight of the bumiputera. The National Development Policy (NDP), which followed the NEP after 1990, relaxed some of the positive dis-crimination measures that favoured the bumiputera. An extended period of strong economic growth until 1998 made it possible to raise the status of the bumiputera and avoid serious intercommunal conflict.

A decisive shift towards more authoritarian government occurred in 1987, when there was a serious split in UMNO in which Mahathir Mohamad, who had been party president and prime minister since 1981, nearly lost power. Dr Mahathir responded by consolidating his power within UMNO and making it difficult to challenge an incumbent leader. In response to the government losing a number of cases in the High Court, the constitution was changed, and by 1988 the judiciary had been stripped of much of its independence, leaving little check on the government�s exercise of power. Decision-making became highly concentrated around Dr Mahathir and an expanded prime minister!s department.

The 1997-98 Asian financial crisis plunged Malaysia into a severe economic downturn, but also exposed corruption within UMNO. Calls for political reform and a change in leadership intensified, especially among younger UMNO politicians. The deputy prime minister, Anwar Ibrahim, became the focal point of the reformasi (reform) movement. In September 1998 Mr Anwar was dismissed from the government, expelled from UMNO and later jailed for a total of 15 years on charges of obstruction of justice, sodomy and corruption. The dubious treatment of Dr Mahathir�s heir-apparent upset UMNO�s

The Federation of Malaysia was formed in 1963

The 1969 race riots were a political watershed

The 1997-98 Asian crisis leads to calls for political reform

6 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

traditional supporters. In the November 1999 general election, UMNO lost its Malay majority but the BN nonetheless retained its two-thirds majority in parliament, owing to the continued support of the ethnic Chinese. The main beneficiary was the conservative Malay-based Islamic party, Parti Islam sa-Malaysia (PAS), which gained control in Terengganu while retaining the neighbouring state of Kelantan, and made strong inroads in other northern states dominated by Malays.

Under Dr Mahathir, UMNO stepped up its policy of favouring and promoting Islam to counteract the influence of PAS. The position that only sharia courts can decide about Islamic issues was enshrined in the constitution in 1988. To counter the pledge made by PAS that it would set up an Islamic state should it win power, Dr Mahathir declared in September 2001 that Malaysia was already an Islamic state. The constitution only gives Islam the status of official religion and grants freedom to practise one!s religion. Sharia law continued to steadily encroach upon the civil area, upsetting non-Muslims, who form some 40% of the population, and many progressive Malays. The September 11th 2001 terrorist attacks on the US discredited Islamic fundamentalism and led to a crackdown on Islamist extremists.

Recent political developments

Dr Mahathir retired in October 2003, after 22 years of strong leadership as prime minister and UMNO president. His successor, Abdullah Badawi, called an election on March 21st 2004. The polls were preceded by anti-corruption measures and promises of further action that attracted strong public approval. Mr Abdullah, who is an Islamic scholar and is not linked to any known scandals, campaigned with his own agenda of moderate Islam. The BN gained a spectacular election victory, winning nine-tenths of the available 219 parliamentary seats, the coalition�s best-ever result. UMNO recovered the majority support of Malay voters, while PAS lost control of Terengganu.

Mr Abdullah failed to build a strong power base after his election victory. His anti-corruption campaign proved to be more about establishing rules for ethical government than prosecuting corrupt politicians and civil servants. The September 2004 UMNO party elections were heavily tainted by bribes and many of Mr Abdullah!s candidates were defeated. In another sign of Mr Abdullah�s weakness, the UMNO annual congress in July 2005 voted to strengthen the bumiputera policies, to the alarm of the Chinese parties in the ruling BN. These policies, which aim to increase the economic participation of the Malay population, had been gradually de-emphasised after the Asian financial crisis.

Without Dr Mahathir�s charisma and strong power base, Mr Abdullah had diffi-culty changing economic and social policies without arousing accusations of corruption and favouritism. While more tolerant of dissent and criticism, Mr Abdullah could not control the religious and racial tensions that had be-come increasingly evident. Creeping Islamisation, religious intolerance and

Creeping Islamisation begins to divide the nation

Mr Abdullah fails to build a strong power base

Religious and racial tensions rise

Malaysia 7

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

racial prejudice alarmed non-Muslim ministers in the BN cabinet to such an extent that in January 2006"in an unprecedented move"they presented a memorandum to the prime minister to defend the rights of the religious min-orities. They hurriedly withdrew their request after loud protests from Malay and Islamic organisations and newspapers. In July 2006 the government forbade public discussion of the status of Islam and threatened to tighten press controls.

Dr Mahathir!s mounting dissatisfaction with his successor finally led in August 2006 to a call for his replacement. Dr Mahathir complained of broken promises, wrong decisions, government corruption and the undermining of national interest, but he also appeared to be motivated by hurt pride and a loss of in-fluence on policy and the distribution of government contracts. Divisions deep-ened as scandals from the Mahathir era re-emerged. Dr Mahathir!s challenge threw UMNO into disarray and Mr Abdullah!s position looked vulnerable.

Parliamentary forces (no. of seats)

1995 1999 2004Barisan Nasional (BN, National Front) 162 148 198 United Malays National Organisation (UMNO) 88 71 109 Malaysian Chinese Association (MCA) 30 29 31 Malaysian Indian Congress (MIC) 6 7 9 Gerakan Rakyat Malaysia (GRM) 7 6 10 People�s Progressive Party (PPP) 0 0 1 Parti Pesaka Bumiputera Bersatu (PBB) 13 10 11 Sarawak United Peoples� Party (SUPP) 6 8 6 Parti Bansa Dayak Sarawak (PBDS) 4 6 6 Sabah Progressive Party (SAPP) 0 2 2 Parti Bersatu Sabah (PBS)a � � 4 Liberal Democratic Party (LDP) 0 1 � Parti Bersatu Rakyat Sabah (PBRS)b 1 Sarawak National Party (SNAP)c 4 4 � United Pasokmomogun Kadazandusan Murut Organisation (UPKO)b 4 3 4 Sarawak Progressive Democratic Party (SPDP)d 4 BN Direct 0 1 0Oppositione � 42 20 Parti Islam sa-Malaysia (PAS) 7 27 7 Keadilan PRMf � 5 1 Democratic Action Party (DAP) 9 10 12 Parti Bersatu Sabah (PBS)a 8 3 � Parti Melayu Semangat �46 (S46)g 6 � �Independent 0 0 1Total 192 193 219

a PBS rejoined the BN in 2001. b UPKO and PBRS are splinter parties of PBS, which left the BN in 1990. c SNAP was forced to leave the BN in 2002. d SPDP was formed by former SNAP members. e PAS, DAP and Keadilan contested the 1999 as a coalition, the Barisan Alternatif (BA); DAP left the BA inSeptember 2001. f The Parti Keadilan Nasional merged in December 2002 with Gerakan Rakyat Malaysia (GRM). g Reunited with UMNO in 1996.

Source: The Star.

8 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

The March 2004 election defeat had a devastating effect on the opposition alliance, the Barisan Alternatif (BA, Alternative Front), which consists of PAS and the Parti Keadilan Rakyat (Keadilan), the party led by Wan Azizah, the wife of Mr Anwar. The mainly ethnic-Chinese left-wing Democratic Action Party (DAP)"which left the BA in September 2001, protesting at the intention of PAS to found an Islamic state"became the largest opposition party. The release of Mr Anwar in September 2004, after his conviction for sodomy was overturned, gave new hope to a demoralised opposition. Mr Anwar used the greater leeway Mr Abdullah allowed the judiciary to rebuild his reputation and tried to prove that his downfall was the result of a conspiracy. It was often assumed that, if successful, he would rejoin UMNO, instead of becoming an opposition leader.

Important recent events

September 2001

Following the September 11th 2001 attacks on the US, the government tightens the already stringent security regulations. United Malays National Organisation (UMNO) gains support among Malay moderates by associating the opposition party, Parti Islam sa-Malaysia (PAS), with Islamist extremism. The prime minister, Mahathir Mohamad, declares that Malaysia is already an Islamic state and announces further Islamisation measures. The opposition coalition, Barisan Alternatif (BN, National Front), splits, as the Democratic Action Party (DAP) leaves over PAS!s Islamic agenda.

October 2003

Dr Mahathir retires and is succeeded by his deputy, Abdullah Badawi.

March 2004

The BN wins its largest-ever election victory with an anti-corruption agenda, thrashing PAS, which loses control of Terengganu, and reducing the Parti Keadilan Rakyat (Keadilan) to a single seat.

September 2004

The High Court overturns the conviction for sodomy of the former deputy prime minister, Anwar Ibrahim, who is set free after serving nearly six years for corruption. Corruption thrives at the UMNO party elections, in which many of Mr Abdullah!s candidates are defeated.

July 2005

UMNO�s annual congress votes to renew the system of Malay privileges; Mr Abdullah plays down its significance to his non-bumiputera coalition partners.

January 2006

Non-Muslim ministers in the BN cabinet call on Mr Abdullah to defend the rights of religious minorities.

August 2006

Dr Mahathir calls on UMNO to replace Mr Abdullah as party leader.

The opposition�s hopes are raised as Mr Anwar is freed

Malaysia 9

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Constitution, institutions and administration

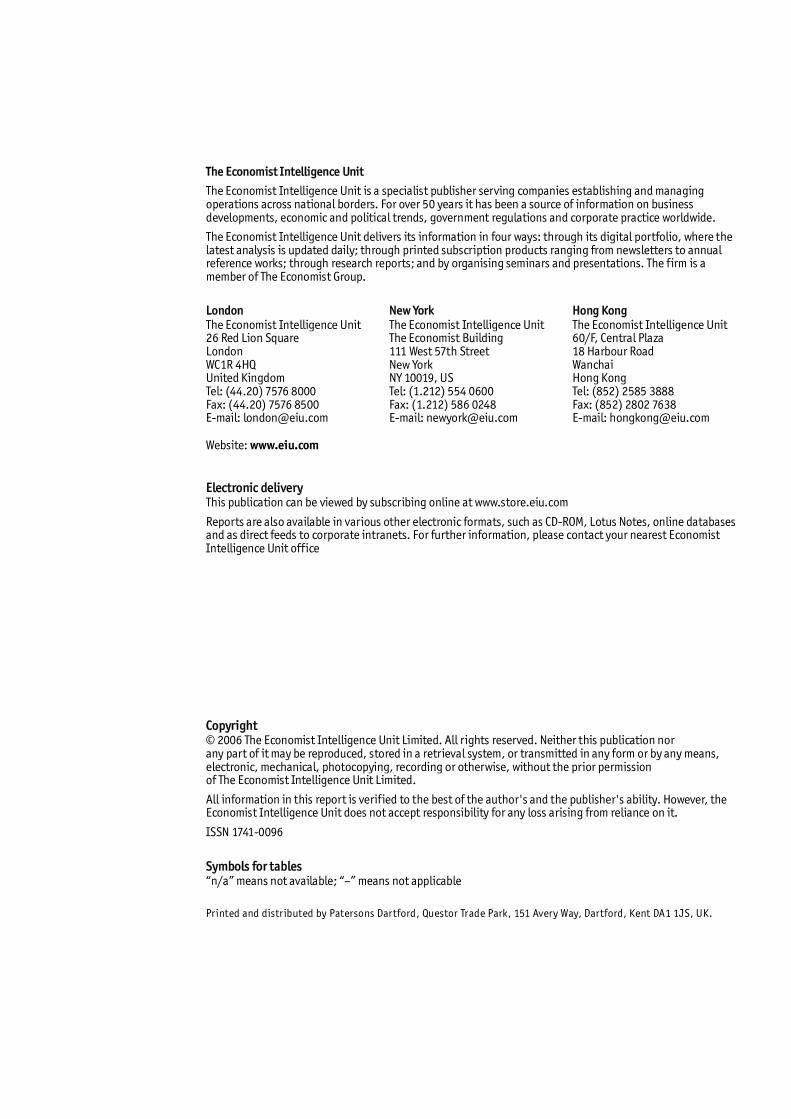

Malaysia is a federal, constitutional monarchy within the Commonwealth. The federation consists of 13 states (11 in peninsular Malaysia, plus Sarawak and Sabah); in addition there are three federal territories (Kuala Lumpur, Labuan island, and the federal administrative capital, Putrajaya).

The position of king (yang di-pertuan agung, meaning �supreme ruler�) is largely ceremonial and is rotated every five years. The nine-strong Conference of Rulers of the states of the peninsula, excluding Malacca and Penang (the sultans of Kedah, Perak, Johor, Selangor, Pahang, Terengganu and Kelantan; the yang di-pertuan besar, or supreme minister, of Negeri Sembilan; and the raja of Perlis) elects one of its number to serve as king. Each ruler is also the leader of the Islamic faith in his state.

The federal parliament consists of an upper chamber, the Senate or Dewan Negara (Council of the Nation), which has 70 members, 44 of whom are appointed by the king and 13 pairs are elected by the state legislatures, and a lower chamber, the House of Representatives or Dewan Rakyat (Council of the People), directly elected by universal suffrage, with 219 seats. The lower house has long been a rubber stamp for the BN, and little real debate on draft legislation or issues takes place there, but Mr Abdullah has introduced measures to stimulate parliamentary discussion and initiative.

Each of the 13 states in the Federation has an Executive Council dealing with non-federal matters under a menteri besar (chief minister), who is answerable to elected state assemblies. The constitutional head of each state government is either one of the traditional rulers or (in Penang, Malacca, Sabah and Sarawak) a state governor appointed by the king on the advice of the federal government. Federal territories are administered directly by the federal government.

The Malaysian judicial system still resembles the UK system inherited from the colonial period. The independence of the judiciary was effectively curbed by Dr Mahathir in 1987-88 in response to a court ruling declaring the April 1987 UMNO leadership elections invalid. The High Court was stripped of the power of judicial review and the separation of executive and judicial power was terminated. Judges were given a code of conduct, the breaching of which could result in dismissal. In the years that followed the powers of the executive were increased further. The legal framework leaves little room for the judiciary to reassert its independence. The acquittal by the High Court of Mr Anwar in September 2004 is widely viewed as a sign that Mr Abdullah will allow the judiciary greater independence, but there has been no sign of judicial reform.

In September 2001, to counter criticism from PAS, Dr Mahathir stated that Malaysia was �already� an Islamic state. This raised fear among the non-Muslim 40% of the population and remained a controversial subject. The constitution says that Islam is the official religion, but other religions are free to be practised. During the past two decades the government has actively

A federal constitutional monarchy

The federal parliament

The states� executive councils

Islam is the official religion

The independence of the judiciary has been curbed

10 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

promoted and favoured Islam. Islamic or sharia law is enforced at a state rather than federal level, and applies only to Muslims. Ethnic Malays are by definition Muslim. Apostasy or deviation from the established (Sunni) Muslim faith is likely to be punished by sharia courts. Continuing Islamisation means that conflicts between sharia law and human rights principles, enshrined in the federal constitution, are increasing.

After the May 1969 race riots, the government decided to marginalise Chinese and Indians in the civil and armed services. A few non-Malays have been promoted to high ranks of office, but the careers of the majority of non-Malays are strictly circumscribed unless they become Muslim.

Political forces

Race is the major defining feature of the political system: all major political parties are organised along racial lines. Malaysia has been ruled by coalition governments since independence, but in reality the BN coalition is totally dom-inated by UMNO and is unlikely to lose power. UMNO controls the Election Commission, which supervises elections and checks electoral rolls, and the redrawing of constituency boundaries. Because of rock-solid support for the BN in Sarawak and Sabah, the BN coalition seems almost impossible to dislodge.

UMNO, the party of Malay nationalists in the colonial period, remains the most important of the Malay parties. In the March 2004 election it regained the majority support of the Malay section of the population, which it had lost in the 1999 election. The president of UMNO invariably serves as the prime minister and UMNO members hold the deputy prime minister and key cabinet posts. Elections to the UMNO supreme council determine the leadership succession. The party voting system makes it difficult to challenge an incumbent leader but encourages bribery for other positions.

PAS is the alternative to UMNO for the Malay population; it is an ultra-conservative Islamic party and a haven for Malay protest votes, offering a greater devotion to Islam and possibly also a stronger commitment to Malay nationalism than UMNO. From its inception, PAS has intended to set up an Islamic state and introduce Islamic law. Its intention of creating an Islamic state presents a major obstacle to the building of a coalition of opposition forces.

UMNO!s position within the BN coalition is disproportionate to the number of votes it attracts. This reflects the subservient position of the Chinese parties (the Malaysian Chinese Association, or MCA, and the Parti Gerakan Rakyat Malaysia, or Gerakan) and the Indian party (Malaysian Indian Congress, or MIC), which goes back to the supposed acceptance by the immigrant community of a constitutional bargain at independence in 1957. Chinese and Indian community leaders accepted the notion of Malay special rights and the special status of Islam in exchange for citizenship.

The March 2004 election defeat had a devastating effect on the opposition alliance, the BA, which consists of PAS and the Parti Keadilan Rakyat (Keadilan), the party led by Wan Azizah, the wife of Mr Anwar. The left-of-centre, largely

Racial discrimination in administration

The BN coalition is dominated by UMNO

The opposition is weak and divided

Malaysia 11

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

ethnic-Chinese DAP"which left the BA in September 2001, protesting at the intention of PAS to found an Islamic state"became the largest opposition party. The release of Mr Anwar in September 2004, after his conviction for sodomy was overturned, gave new hope to a demoralised opposition.

The entitlement of the bumiputera to special rights is laid down in the constitution. UMNO regularly warns other parties not to question Malay special privileges, the position of Islam or relations between the different races; those who do will be accused of sedition. The political system has remained stuck in this mode for nearly 50 years. But the gap between the races has widened noticeably over the past decade. Residents continue to define themselves in the first place by race, rather than by a Malaysian identity.

Key political figures

Abdullah Ahmad Badawi

Malaysia�s prime minister and president of the United Malays National Organisation (UMNO). Mr Abdullah, an Islamic studies graduate, has had limited success in fighting corruption. Lacking the charisma and strong power base of his predecessor, Mahathir Mohamad, disappointment is growing over his ineffectiveness and failure to fulfil promises.

Najib Razak

Deputy prime minister and UMNO�s deputy president, defence minister and son of a former prime minister. As a rival to Mr Abdullah, he is expected to challenge the prime minister in the future.

Mahathir Mohamad

Prime minister and president of UMNO from July 1981 until November 2003. He is the principal architect of the economic advancement of the Malay community and the rapid industrial growth of Malaysia. Dr Mahathir dominated political life for two decades, and has become increasingly critical of his successor. In August 2006 he asked UMNO to replace Mr Abdullah.

Anwar Ibrahim

Former deputy prime minister, dismissed in 1998 and jailed for abuse of power and sodomy. Mr Anwar was released in September 2004 after his sodomy conviction was overturned by the High Court. He is trying to prove, in the courts, that he was the victim of a conspiracy by his rivals within UMNO. As an advocate of political reform and a possible bridge between UMNO and ultra-conservative Islam, he remains a powerful political influence and a possible future prime minister.

Khairy Jamaluddin

The son-in-law of the prime minister and deputy head of UMNO Youth, who is believed to control access to Mr Abdullah and the distribution of many government contracts. He became a focal point of Dr Mahathir!s criticism in 2005-06.

Political structure is fossilised

12 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

International relations and defence

Under Mr Abdullah, Malaysia�s diplomatic relations have begun to reflect economic interests more closely than under Dr Mahathir, who irritated some Western governments with his controversial opinions. Malaysia remains a champion of the interests of the developing world and a defender of the interests of the Islamic world. Membership of the Association of South-East Asian Nations (ASEAN) remains central to Malaysia�s foreign policy. Greater economic integration, through bilateral trade agreements, is also leading to closer relations with its largest trading partners.

Malaysia!s relations with Singapore, the US and Australia have warmed notably. Co-operation rather than constant bickering now characterises relations with Singapore, although several long-standing disagreements remain to be solved. Malaysia works closely with the US in the fight against international terrorism but remains critical of US intervention in Iraq. The strongest improvement is in relations with Australia (which Dr Mahathir refused to visit during his tenure as prime minister). In 2005 Malaysia entered into free-trade negotiations with Australia.

Relations with Indonesia, Malaysia!s largest provider of foreign labour, are generally good, despite Indonesia!s poor record of dealing with terrorist threats within its borders, illegal immigration and air pollution from forest fires. Islamic militancy among the 3m ethnic-Malays in southern Thailand, and the heavy-handed response of the Thai army, is souring relations between the two countries.

Given the proliferation of trade agreements concluded or being negotiated"either multilaterally in Asia or bilaterally, for instance the free-trade agreement with the US, Malaysia!s largest export market"economic diplomacy is playing a larger role. But growing competition for energy resources in Asia has increased the chances of territorial disputes. Malaysia has border disagreements with Indonesia, Singapore, the Philippines and China.

In 2002 Malaysia restarted the modernisation of the armed forces that was derailed by the Asian economic crisis. The intention is to develop an all-round modern conventional capability, with enhanced maritime security, from what was originally a counter-insurgency force. Malaysia, together with Singapore, the UK, Australia and New Zealand, is a member of the Five Power Defence Arrangement, which provides for co-operation and consultation in case of attack. Malaysia co-operates on border security with its neighbours. According to Mr Razak, Malaysia�s primary security threat is internal; counter-terrorism and urban warfare capabilities are being developed to deal with violent extremism. In 2004 Malaysia started a limited obligatory national service, although mainly as a nation-building exercise.

Defence spending is to remain high

Islamic militancy is souring relations with Thailand

Foreign relations have improved under Mr Abdullah

There is an increasing chance of territorial disputes

Malaysia 13

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

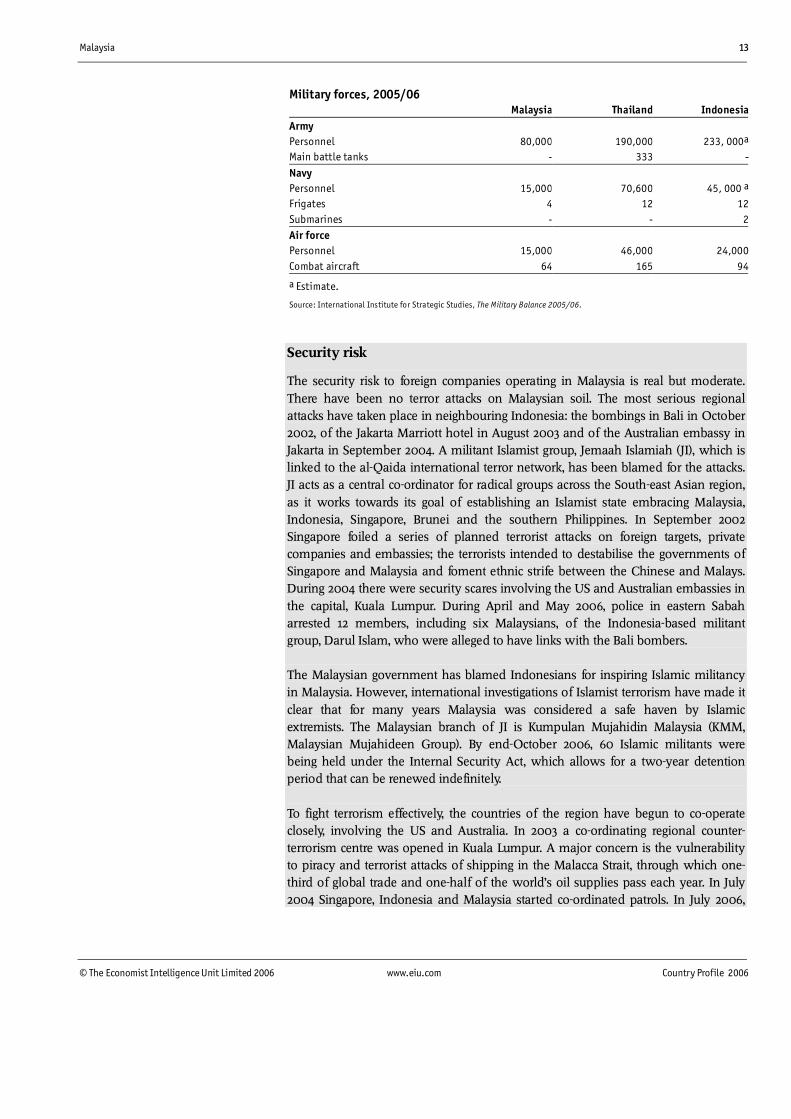

Military forces, 2005/06 Malaysia Thailand IndonesiaArmy Personnel 80,000 190,000 233, 000a

Main battle tanks - 333 -

Navy Personnel 15,000 70,600 45, 000 a

Frigates 4 12 12Submarines - - 2Air force Personnel 15,000 46,000 24,000Combat aircraft 64 165 94

a Estimate.

Source: International Institute for Strategic Studies, The Military Balance 2005/06.

Security risk

The security risk to foreign companies operating in Malaysia is real but moderate. There have been no terror attacks on Malaysian soil. The most serious regional attacks have taken place in neighbouring Indonesia: the bombings in Bali in October 2002, of the Jakarta Marriott hotel in August 2003 and of the Australian embassy in Jakarta in September 2004. A militant Islamist group, Jemaah Islamiah (JI), which is linked to the al-Qaida international terror network, has been blamed for the attacks. JI acts as a central co-ordinator for radical groups across the South-east Asian region, as it works towards its goal of establishing an Islamist state embracing Malaysia, Indonesia, Singapore, Brunei and the southern Philippines. In September 2002 Singapore foiled a series of planned terrorist attacks on foreign targets, private companies and embassies; the terrorists intended to destabilise the governments of Singapore and Malaysia and foment ethnic strife between the Chinese and Malays. During 2004 there were security scares involving the US and Australian embassies in the capital, Kuala Lumpur. During April and May 2006, police in eastern Sabah arrested 12 members, including six Malaysians, of the Indonesia-based militant group, Darul Islam, who were alleged to have links with the Bali bombers. The Malaysian government has blamed Indonesians for inspiring Islamic militancy in Malaysia. However, international investigations of Islamist terrorism have made it clear that for many years Malaysia was considered a safe haven by Islamic extremists. The Malaysian branch of JI is Kumpulan Mujahidin Malaysia (KMM, Malaysian Mujahideen Group). By end-October 2006, 60 Islamic militants were being held under the Internal Security Act, which allows for a two-year detention period that can be renewed indefinitely. To fight terrorism effectively, the countries of the region have begun to co-operate closely, involving the US and Australia. In 2003 a co-ordinating regional counter-terrorism centre was opened in Kuala Lumpur. A major concern is the vulnerability to piracy and terrorist attacks of shipping in the Malacca Strait, through which one-third of global trade and one-half of the world�s oil supplies pass each year. In July 2004 Singapore, Indonesia and Malaysia started co-ordinated patrols. In July 2006,

14 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Malaysia signed a mutual legal assistance treaty with the United States, to ease criminal investigations, including into corruption and terrorism.

Social unrest

The major long-term risk to business comes from a return of economic and political conditions that could lead to an outbreak of racial violence. Tensions persist below the surface between the majority Malays on one hand and the minority ethnic Chinese and Indian populations on the other. In the most serious post-war racial conflict, in 1969, divisions within the Malay majority led to the scapegoating of the ethnic Chinese, hundreds of whom were killed in riots. Any attempt to reduce the privileges of the bumiputera (ethnic Malays and other indigenous peoples) could stoke Malay resentment. An even more sensitive issue is religion; a growing feeling on the part of Muslims that the position of Islam is being undermined may cause unrest. Nonetheless, the short-term risk of large-scale racial violence appears low. Large-scale demonstrations against the government and the ruling United Malays National Organisation (UMNO) were last held in 1998, when the deposed deputy prime minister, Anwar Ibrahim, led reformasi (reform) demonstrations. Although Mr Anwar was released from prison in September 2004, a revival of large-scale public protests looks unlikely under the reform-minded Mr Abdullah, even though most traditional means of protest remain blocked. There is widespread awareness within Malaysia that it is heavily dependent on foreign direct investment, and the opposition is unlikely to target foreign businesses specifically.

Armed conflict

The risk of armed conflict affecting business is low. Sporadic Islamist violence has occurred during the past few years. In 2001 KMM members were arrested and accused of involvement in bank robberies, the murder of a state assembly representative, and the bombing of a church and a temple. There are no �no-go areas� in Malaysia, and the government remains very much in control of the country. It is unlikely that Islamist extremists could develop the ability to stage an armed conflict. Islamic militancy in southern Thailand, where the population is mainly of Malay origin, poses no direct threat to Malaysian security but strains relations with Thailand.

Organised crime

Malaysia is, in general, a fairly safe country. Violent crime, kidnapping and extortion are rare, although they have attracted more publicity in recent years. Organised crime is seldom a threat to foreign business. Foreigners are, however, often the target of pickpockets, burglars, car break-ins and purse-snatching. Credit-card fraud is a growing problem. Chinese criminal gangs, or triads, do operate in Malaysia but their activities do not usually attract much publicity. Illegal activities by organised Malaysian groups that are most frequently mentioned by law-enforcement agencies are piracy"the illegal copying and distribution of CDs and DVDs"as well as credit-card counterfeiting and drug trafficking.

Malaysia 15

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Resources and infrastructure

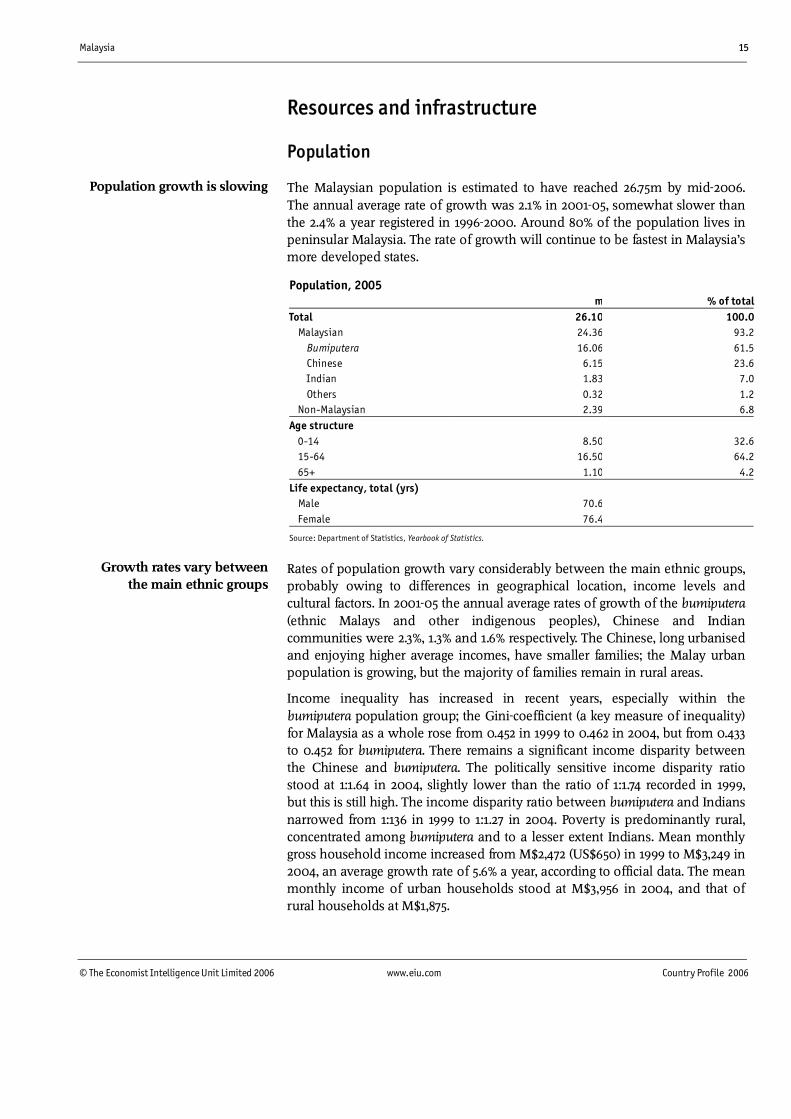

Population

The Malaysian population is estimated to have reached 26.75m by mid-2006. The annual average rate of growth was 2.1% in 2001-05, somewhat slower than the 2.4% a year registered in 1996-2000. Around 80% of the population lives in peninsular Malaysia. The rate of growth will continue to be fastest in Malaysia�s more developed states.

Population, 2005 m % of totalTotal 26.10 100.0 Malaysian 24.36 93.2 Bumiputera 16.06 61.5 Chinese 6.15 23.6 Indian 1.83 7.0 Others 0.32 1.2 Non-Malaysian 2.39 6.8Age structure 0-14 8.50 32.6 15-64 16.50 64.2 65+ 1.10 4.2Life expectancy, total (yrs) Male 70.6 Female 76.4

Source: Department of Statistics, Yearbook of Statistics.

Rates of population growth vary considerably between the main ethnic groups, probably owing to differences in geographical location, income levels and cultural factors. In 2001-05 the annual average rates of growth of the bumiputera (ethnic Malays and other indigenous peoples), Chinese and Indian communities were 2.3%, 1.3% and 1.6% respectively. The Chinese, long urbanised and enjoying higher average incomes, have smaller families; the Malay urban population is growing, but the majority of families remain in rural areas.

Income inequality has increased in recent years, especially within the bumiputera population group; the Gini-coefficient (a key measure of inequality) for Malaysia as a whole rose from 0.452 in 1999 to 0.462 in 2004, but from 0.433 to 0.452 for bumiputera. There remains a significant income disparity between the Chinese and bumiputera. The politically sensitive income disparity ratio stood at 1:1.64 in 2004, slightly lower than the ratio of 1:1.74 recorded in 1999, but this is still high. The income disparity ratio between bumiputera and Indians narrowed from 1:136 in 1999 to 1:1.27 in 2004. Poverty is predominantly rural, concentrated among bumiputera and to a lesser extent Indians. Mean monthly gross household income increased from M$2,472 (US$650) in 1999 to M$3,249 in 2004, an average growth rate of 5.6% a year, according to official data. The mean monthly income of urban households stood at M$3,956 in 2004, and that of rural households at M$1,875.

Growth rates vary between the main ethnic groups

Population growth is slowing

16 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

Malaysia has, throughout its history, been a country of immigrants. In 2005 the legal foreign residents numbered about 2.4m or 8.9% of the population, but there were probably another 1m illegal immigrants, attracted to Malaysia by the availability of work. The government, believing illegal immigrants are a threat to public order, organises regular campaigns to expel them. Given Malaysia!s porous borders, corruption among officials and high unemployment, the campaigns have little effect on deterring this type of migration and often cause economic disruption. Official plans to reduce the economy!s dependence on low-skilled labour may have more effect in the longer term.

Education

The government places great emphasis on education, which is the largest item in the federal budget. The aim is to provide a �world-class quality education system�. Primary education is compulsory for all Malaysian children. Primary and secondary education is free for students aged 7-17 in the public school system (which includes national-type schools teaching in Mandarin and Tamil). Malaysia has a literacy rate of 93%. Over 97% of seven-year-olds are enrolled in the public school system. The private fee-paying sector plays an important role only in higher education. There are public examinations at the end of the primary level (at age 12), the lower secondary level (usually at 17) and the higher secondary level (at 19). Malay and English are compulsory subjects. The matriculation exam at the end of the higher secondary level gives access to Malaysian public universities.

In 2003 there were around 271,000 students, including 15,000 international students, enrolled at 690 private colleges, 14 private universities and four foreign university branch campuses, which teach in English. This compares with 80,000 students at the 16 public universities, which use Malay as a medium of instruction. The international rating of Malaysian universities has declined in recent years. Sending pupils abroad was especially popular before the Asian financial crisis, but the need to do so has been reduced by twinning arrangements with foreign universities. There is also a large number of private and public colleges offering vocational and skill-based education and training. State assistance mostly takes the form of soft loans, repayable when students graduate and take paid employment. University entrance is in theory based on merit but is in practice biased towards the children of bumiputera. Employers frequently complain about the low quality of Malay graduates. With this in mind, science and mathematics have been taught in English since 2003. After independence in 1957 the role of English was systematically reduced for Malay-nationalist reasons.

Health

Malaysia provides an integrated and comprehensive system of public and private healthcare services but the system is under serious strain. For many years the government has underfunded public healthcare, which is suffering from long waiting lists and an outflow of senior staff, largely because of low

Malaysia continues to attract immigrant workers

Public healthcare system is under strain

Education is given a high priority

Malaysia 17

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

remuneration. The private sector has filled the gap. With greater prosperity and increased demand for medical services, health policy is shifting towards more preventative medicine, tighter cost controls and higher private contributions. The government is considering setting up a national health fund with contributions linked to different levels of services, while maintaining free access to medical services for the poor, especially in rural areas.

There is an extensive network of primary healthcare services, which in 2004 was supported by more than 3,000 health clinics and 2,900 dental units as well as 124 public hospitals with more than 34,000 beds. Clean water, safe food and sanitary disposal of waste are generally available. But there are wide geographical variations: health indicators for Sabah, Sarawak and some pre-dominantly rural states on the Malayan peninsula are well below average. The 218 private hospitals are generally smaller and better equipped, providing around one-quarter of total beds. Given an acute shortage of manpower, the government is advocating electronic medical services and greater use of the services offered by general practitioners.

According to national statistics, Malaysia is estimated to have spent around 4.5% of GDP in 2004 on healthcare, divided roughly equally between the govern-ment and the private sector. This is low compared with the World Health Organisation!s recommendation of 5-8% of GDP. Growth in government healthcare spending has continued to trail overall public spending. The 2007 healthcare budget showed increases of only 1.6% for operating expenditure and 3.6% for development spending, not enough to keep up with rising costs, according to the Malaysian Medical Association. Rather than building more hospitals and clinics, the government will be upgrading and enhancing existing services and facilities under the Ninth Malaysia Plan 2006-10 (9MP).

Natural resources and the environment

Malaysia has a tropical climate. Its economic development was dominated by the cultivation of plantation crops, such as natural rubber and palm oil, as well as by tin mining. Malaysia remains an important centre of tin refining, supplementing its declining domestic mine output with imported concentrates. Malaysia is the world!s third-largest natural rubber producer, after Thailand and Indonesia. High commodity prices have bolstered production in the last three years. Malaysia is one of the world�s largest producers of palm oil; output continues to expand as international demand grows for dietary reasons and, in recent years especially, as a substitute for mineral oil.

More than half of Malaysia is still covered in tropical forest and swamps. Malaysia remains one of the world�s leading producers of tropical saw logs. Controls on tree-felling by loggers continue to be flouted, but output is grad-ually declining. Controls are now linked to replanting, usually with commercial crops, and forestry resources are, at least in theory, managed on a sustainable basis. The diversity and complexity of Malaysia!s ecosystem is particularly rich. Nonetheless, there has been serious environmental degradation as a result of uncontrolled logging, industrial development and urbanisation. A regular

Plantation crops still have an important economic role

18 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

annual occurrence and threat to public health is haze, which is caused by forest fires in Indonesia.

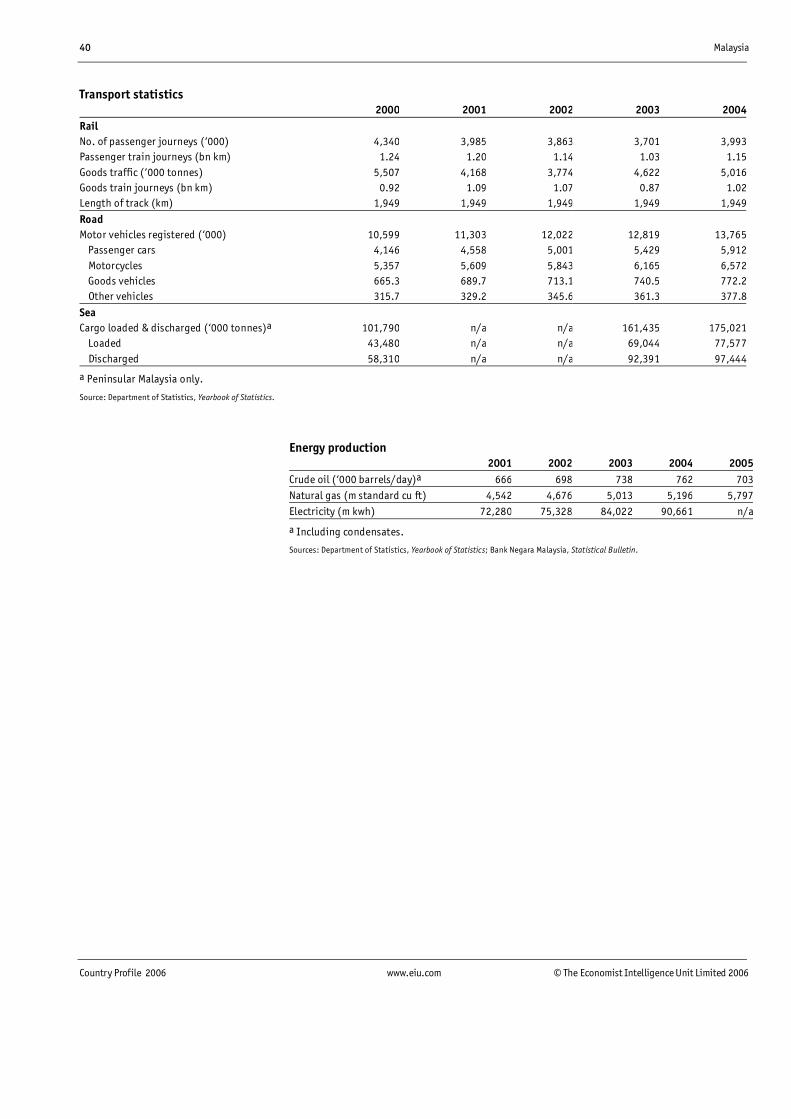

Crude oil and natural gas are the most important primary products. Both oil and natural gas are extracted from two main areas in the South China Sea, off Terengganu and Sabah. Malaysia is, by international standards, a small producer of crude oil but a large exporter of natural gas. In 2005 it was the world!s second-largest exporter of liquefied natural gas (LNG) after Indonesia. At current usage rates, reserves of crude oil will last for 19 years and natural gas 33 years. The other main minerals produced are copper, iron ore, bauxite, coal and gold. Industrial minerals mined are clay, kaolin, silica, limestone, barite, phosphates and stone.

Transport, communications and the Internet

Malaysia�s physical infrastructure compares favourably with that of most other countries in the region. Substantial investment during the boom years by the private and public sector was interrupted by the 1997-98 financial crisis, but investment has since resumed, albeit at a slower pace. By 2004 the national road network stood at 77,695 km. Malaysia has made considerable progress in the creation of a more integrated, efficient and reliable urban transport system. But traffic congestion is getting worse, especially in Kuala Lumpur, despite the promotion of public transport. An express railway links Kuala Lumpur to Kuala Lumpur International Airport (KLIA), connecting to an urban rail system and monorail network, which also serves the administrative capital, Putrajaya. KLIA, a spectacular modern airport, was opened in June 1998, with a capacity of 25m passengers a year. Malaysia is determined to become the regional hub for air transport, which has expanded strongly since the start of a budget airline, Air Asia. There are 117 regional airports, covering the whole of Malaysia, of which 38 have paved runways.

Malaysia�s ports handled 369m tonnes in 2005, up from 224m tonnes in 2000, an increase of 65% over the period. Growth was the result of a rise in containerised and liquid bulk cargo, but also of diversion of traffic from the Port of Singapore (POS). Strong expansion is continuing on the central west coast at Port Klang, as well as at the Port of Tanjung Pelepas (PTP) in Johor, in direct competition with POS. Planned port capacity by 2010 is 570m tonnes, a 29% rise compared with 2005, after a 36% increase in the preceding five years. Malaysia is determined to become the preferred regional transshipment point.

State-owned Telekom Malaysia plays a central role in telecommunications: it is the dominant provider in the (stagnating) market for fixed-line services and an important operator of mobile services; five companies compete in each market section. In 2005 there were 16.6 fixed-line telephones for every 100 people. Telekom is the central provider of the fibre-optic communications infrastructure. Cellular services have continued to grow rapidly. Tariff liberalisation boosted the number of mobile-phone users from 5.1m in 2000 to 19.5m in 2005 (a penetration rate of 74.1%), most of whom use prepaid services. The first auction

Malaysia still has large reserves of crude oil and gas

Investments in infrastructure have resumed

Aggressive expansion of port capacity continues

Telecommunications

Malaysia 19

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

of third-generation (3G) licences took place in 2005 and paved the way for the introduction of a full range of 3G mobile services in 2006.

Malaysia intends to position itself as a regional and even a global hub for information and communications technology (ICT) and multimedia. ICT is con-sidered a crucial element to achieve a competitive knowledge-based economy. The extension of the Multimedia Super Corridor (MSC; see Economic sectors: Manufacturing) plays an essential role in the fostering of local capabilities. But ICT usage remains relatively low by international comparison, with 5.7m personal computers installed by 2005, a penetration rate of 21.8 per 100 population. The number of Internet dial-up subscribers stood at 3.7m in 2005, a 13.9% penetration rate, while the penetration rate for broadband subscribers was just 2.4%. These rates were well below those of Singapore, Japan, South Korea and Taiwan. The government has set a target of 13% broadband penetration by 2010 and 35% for dial-up connections, although it will continue to keep a wary eye on Internet content, fearing uncensored criticism.

Energy provision

Malaysia is well endowed with energy resources. It is a net exporter of oil and gas, which are extracted from beneath the South China Sea. Reception install-ations in Terengganu handle the oil and gas extracted from fields east of the peninsula; other fields are located north of Sarawak and around the coast of Sabah. Oil reserves will last for another 19 years and natural gas for another 33 years at the current rate of usage. Half of the oil produced is exported. Large coal reserves are found in Sarawak and Sabah, but their low grade and difficulty of access have discouraged development. The high rainfall and rugged topography provide extensive scope for hydroelectric power. Completion of the 2,400-mw Bakun dam in Sarawak will more than double the country!s hydroelectric capacity.

Fuel used for electricity generation is mostly natural gas (two-thirds of total), followed by coal, hydroelectricity and oil; renewable energy (especially biomass, from palm oil and wood waste) will soon overtake oil. Coal will cover the bulk of the expanding demand for power, but gas will remain the main fuel for power generation.

Malaysia�s reserve margin"the difference between installed capacity and peak demand"stood at 39.5% at end-2005. The extraordinarily high margin was the result of a 1990s! privatisation policy, under which independent power producers (IPPs) built and operated thermal generating plants to supply the national grid. The IPPs produced 40% of peninsular Malaysia�s electricity in 2004; state-owned Tenaga Nasional (TNB) provided 60%. The unusually favourable supply contracts were being revised in 2006. Notwithstanding tariff increases in 2006, the average electricity selling price to industrial and commercial customers is among the lowest in ASEAN.

ICT is considered crucial for knowledge-based economy

There are substantial energy resources

Power generation is driven by gas and coal

20 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

The economy

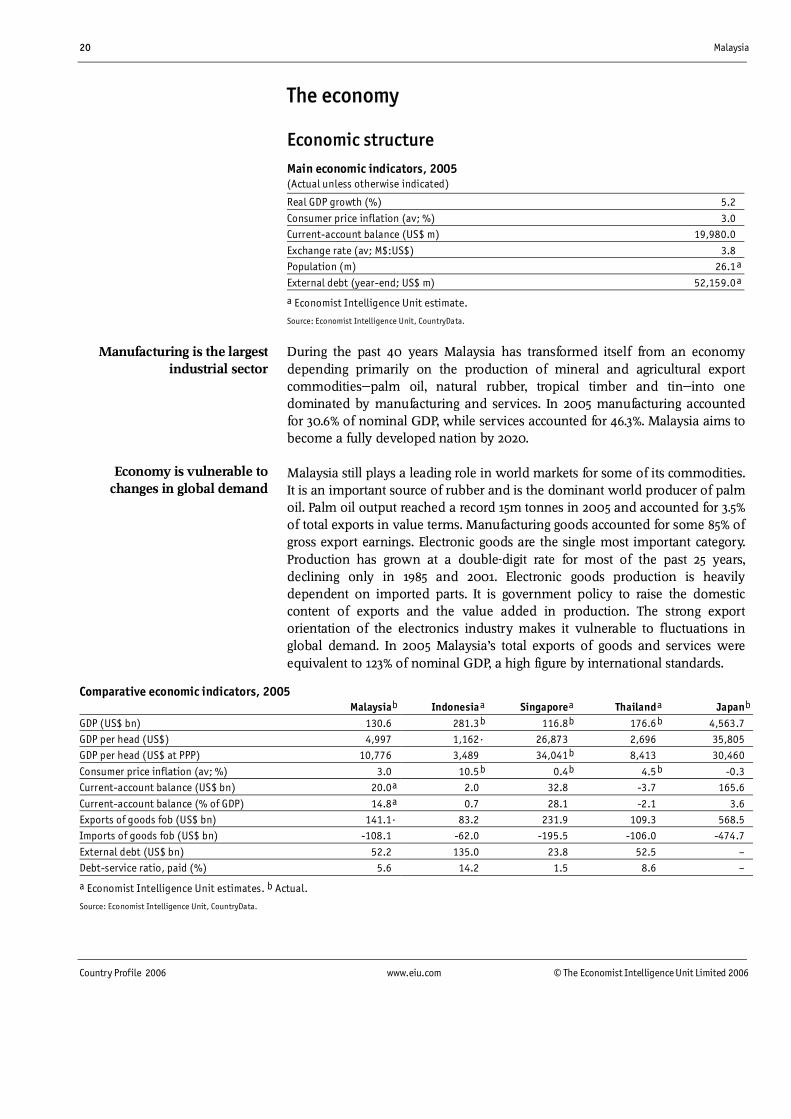

Economic structure Main economic indicators, 2005 (Actual unless otherwise indicated)

Real GDP growth (%) 5.2

Consumer price inflation (av; %) 3.0

Current-account balance (US$ m) 19,980.0

Exchange rate (av; M$:US$) 3.8

Population (m) 26.1a

External debt (year-end; US$ m) 52,159.0 a

a Economist Intelligence Unit estimate.

Source: Economist Intelligence Unit, CountryData.

During the past 40 years Malaysia has transformed itself from an economy depending primarily on the production of mineral and agricultural export commodities"palm oil, natural rubber, tropical timber and tin"into one dominated by manufacturing and services. In 2005 manufacturing accounted for 30.6% of nominal GDP, while services accounted for 46.3%. Malaysia aims to become a fully developed nation by 2020.

Malaysia still plays a leading role in world markets for some of its commodities. It is an important source of rubber and is the dominant world producer of palm oil. Palm oil output reached a record 15m tonnes in 2005 and accounted for 3.5% of total exports in value terms. Manufacturing goods accounted for some 85% of gross export earnings. Electronic goods are the single most important category. Production has grown at a double-digit rate for most of the past 25 years, declining only in 1985 and 2001. Electronic goods production is heavily dependent on imported parts. It is government policy to raise the domestic content of exports and the value added in production. The strong export orientation of the electronics industry makes it vulnerable to fluctuations in global demand. In 2005 Malaysia�s total exports of goods and services were equivalent to 123% of nominal GDP, a high figure by international standards.

Comparative economic indicators, 2005 Malaysiab Indonesiaa Singapore a Thailanda Japanb

GDP (US$ bn) 130.6 281.3b 116.8 b 176.6b 4,563.7

GDP per head (US$) 4,997 1,162. 26,873 2,696 35,805

GDP per head (US$ at PPP) 10,776 3,489 34,041 b 8,413 30,460

Consumer price inflation (av; %) 3.0 10.5b 0.4 b 4.5b -0.3

Current-account balance (US$ bn) 20.0a 2.0 32.8 -3.7 165.6

Current-account balance (% of GDP) 14.8a 0.7 28.1 -2.1 3.6

Exports of goods fob (US$ bn) 141.1. 83.2 231.9 109.3 568.5

Imports of goods fob (US$ bn) -108.1 -62.0 -195.5 -106.0 -474.7

External debt (US$ bn) 52.2 135.0 23.8 52.5 �

Debt-service ratio, paid (%) 5.6 14.2 1.5 8.6 �

a Economist Intelligence Unit estimates. b Actual.

Source: Economist Intelligence Unit, CountryData.

Manufacturing is the largest industrial sector

Economy is vulnerable to changes in global demand

Malaysia 21

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Economic policy

The new government of Abdullah Badawi began to tighten fiscal policy in 2004, following six years of budget deficits. Some large projects were cancelled and development spending (spending on facilities) was cut back but, owing to political resistance, the pace of budget consolidation slowed dramatically between 2005 and 2006. Fiscal plans during this period were also thrown into disarray by a sharp increase in international oil prices, which caused a surge in direct fuel subsidies. It led to several increases in domestic fuel prices and made the government more determined to phase out fuel subsidies.

Government spending began to accelerate in late 2006 ahead of new projects planned under the Ninth Malaysia Plan 2006-10 (9MP). The 2007 budget shows a clear shift towards greater stimulation, with measures aimed to boost private consumption and a cut in the corporate tax. Operating expenditure is scheduled to rise by 16.6% and development spending by 31%. Optimism about economic growth (6% in 2007) and high petroleum-related revenue (nearly 40% of revenue, or M$53.7bn/US$14.7bn) are expected to lead to an 11.8% increase in total revenue. As a result, the budget deficit is projected to drop to 3.4% of GDP from an estimated 3.5% in 2006.

The most important future taxation change is the introduction of a goods and services tax (GST)"a comprehensive value-added tax"originally planned for 2007 but delayed until a later date. It will achieve a long-planned shift from direct to indirect taxation, made necessary by the volatility of direct taxes and their failure to keep up with economic growth. The GST is expected to improve tax collection and provide a more stable source of revenue. The government has stated that it will cut corporate and individual income tax rates at the same time as introducing the GST. Malaysia�s 28% corporate tax rate may then be reduced to a level closer to Singapore�s 20%. In addition, the government aims to reduce or abolish subsidies, not just those connected with fuel.

Finding additional government revenue is also part of the reason for the reform of the government-linked corporations (GLCs). The 40 GLCs include some of Malaysia�s largest companies, such as the oil company, Petronas, and the energy company, Tenaga Nasional. Together, the companies account for some 36% of the capitalisation of the Malaysian stockmarket. The government intends to boost the return on its investments, with the likely aim of selling off part of its holdings later. The GLCs have been given guidelines and targets, and told to improve their efficiency and competitiveness, and make their management more accountable. The transformation of the government-owned sector is meant to have a powerful effect on the private sector and boost the efficiency of the whole economy.

Some of Mr Abdullah!s priorities are different from those of his predecessor, Mahathir Mohamad. This is especially the case with the promotion of agri-culture, which is intended to become the third engine of economic growth, after services and manufacturing. Linked to this are incentives to boost investment in agriculture and food production. The government intends to promote the

New tax will provide a stable revenue source

The GLCs are being transformed

Fiscal policy favours agriculture and SMEs

Fiscal consolidation stalls

22 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

biotechnology industry, which is expected to find uses and applications for the country!s unusually rich natural resource endowment. Another area singled out for special treatment are small and medium-sized enterprises (SMEs), which the government intends to develop into an internationally competitive small-company sector, to fill a gap in an economy that has been dominated by large, often foreign-owned, corporations.

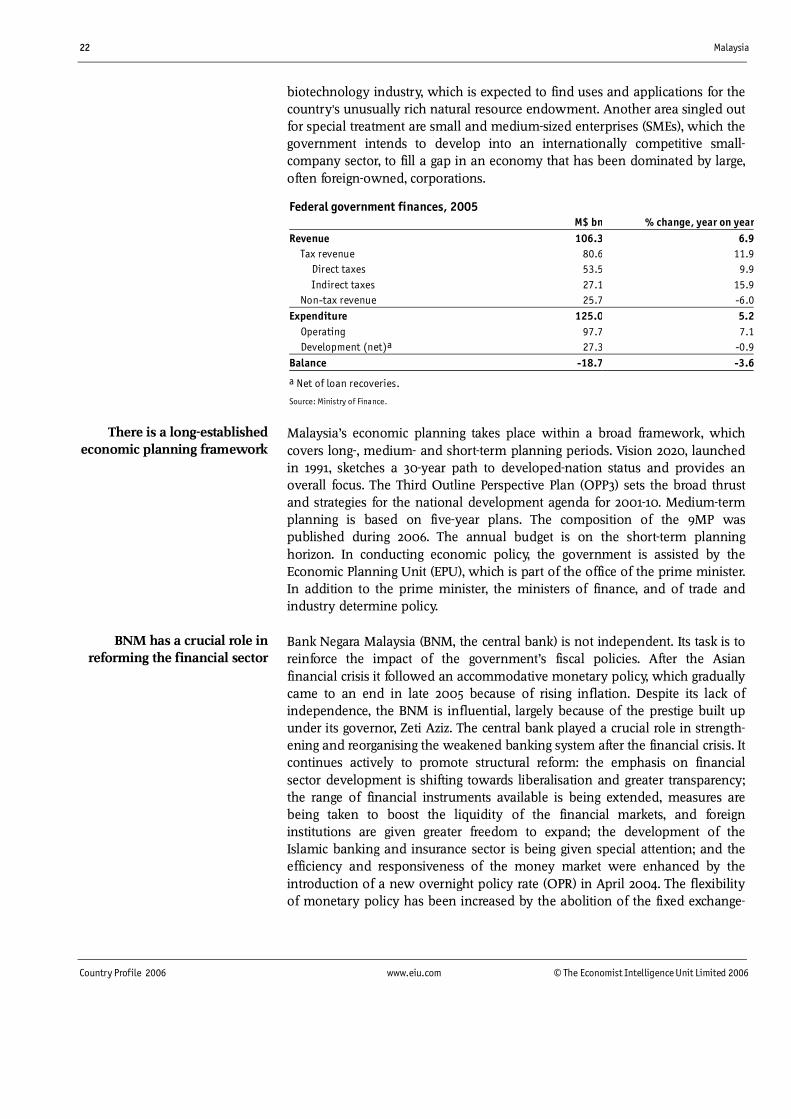

Federal government finances, 2005 M$ bn % change, year on yearRevenue 106.3 6.9 Tax revenue 80.6 11.9 Direct taxes 53.5 9.9 Indirect taxes 27.1 15.9 Non-tax revenue 25.7 -6.0Expenditure 125.0 5.2 Operating 97.7 7.1 Development (net)a 27.3 -0.9Balance -18.7 -3.6

a Net of loan recoveries.

Source: Ministry of Finance.

Malaysia�s economic planning takes place within a broad framework, which covers long-, medium- and short-term planning periods. Vision 2020, launched in 1991, sketches a 30-year path to developed-nation status and provides an overall focus. The Third Outline Perspective Plan (OPP3) sets the broad thrust and strategies for the national development agenda for 2001-10. Medium-term planning is based on five-year plans. The composition of the 9MP was published during 2006. The annual budget is on the short-term planning horizon. In conducting economic policy, the government is assisted by the Economic Planning Unit (EPU), which is part of the office of the prime minister. In addition to the prime minister, the ministers of finance, and of trade and industry determine policy.

Bank Negara Malaysia (BNM, the central bank) is not independent. Its task is to reinforce the impact of the government�s fiscal policies. After the Asian financial crisis it followed an accommodative monetary policy, which gradually came to an end in late 2005 because of rising inflation. Despite its lack of independence, the BNM is influential, largely because of the prestige built up under its governor, Zeti Aziz. The central bank played a crucial role in strength-ening and reorganising the weakened banking system after the financial crisis. It continues actively to promote structural reform: the emphasis on financial sector development is shifting towards liberalisation and greater transparency; the range of financial instruments available is being extended, measures are being taken to boost the liquidity of the financial markets, and foreign institutions are given greater freedom to expand; the development of the Islamic banking and insurance sector is being given special attention; and the efficiency and responsiveness of the money market were enhanced by the introduction of a new overnight policy rate (OPR) in April 2004. The flexibility of monetary policy has been increased by the abolition of the fixed exchange-

BNM has a crucial role in reforming the financial sector

There is a long-established economic planning framework

Malaysia 23

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

rate system in favour of a managed float against a trade-weighted index of currencies of Malaysia!s major trading partners in July 2005.

Economic performance

The most striking aspect of the performance of the Malaysian economy is its dependence on exports, particularly electronics and electrical goods, which made up 53% of exports in 2005. This means that economic growth is vulnerable to global fluctuations in the demand for these products. This dependence cannot be reduced quickly, and a shift to other sources of economic growth, which the government is promoting, may take a long time. In line with other countries in South-east Asia, Malaysia has suffered two recessions during the past nine years. The country enjoyed a decade of consistently fast growth, with economic expansion driven by manufacturing investment and exports, until the Asian financial crisis of 1997-98. Malaysia benefited from the surge in global demand for information and communication technology goods, which pulled the economy out of recession in 1999. But by 2001 it was hit by a downturn in global demand, which resulted in a plunge in exports and a sharp slowdown in GDP growth to only 0.3%. Growth resumed in 2002 and peaked at 7.2% in 2004; it dipped to 5.2% in 2005 and is estimated at 5.7% in 2006.

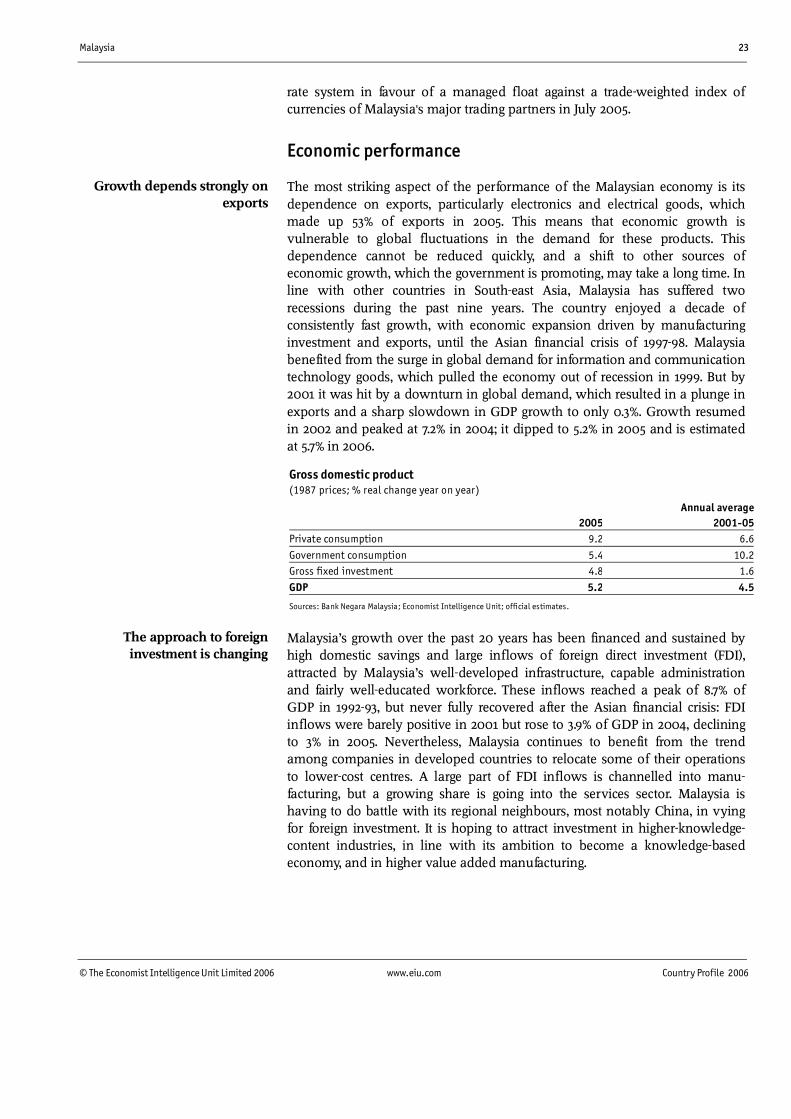

Gross domestic product (1987 prices; % real change year on year)

Annual average 2005 2001-05Private consumption 9.2 6.6

Government consumption 5.4 10.2Gross fixed investment 4.8 1.6

GDP 5.2 4.5

Sources: Bank Negara Malaysia; Economist Intelligence Unit; official estimates.

Malaysia�s growth over the past 20 years has been financed and sustained by high domestic savings and large inflows of foreign direct investment (FDI), attracted by Malaysia�s well-developed infrastructure, capable administration and fairly well-educated workforce. These inflows reached a peak of 8.7% of GDP in 1992-93, but never fully recovered after the Asian financial crisis: FDI inflows were barely positive in 2001 but rose to 3.9% of GDP in 2004, declining to 3% in 2005. Nevertheless, Malaysia continues to benefit from the trend among companies in developed countries to relocate some of their operations to lower-cost centres. A large part of FDI inflows is channelled into manu-facturing, but a growing share is going into the services sector. Malaysia is having to do battle with its regional neighbours, most notably China, in vying for foreign investment. It is hoping to attract investment in higher-knowledge-content industries, in line with its ambition to become a knowledge-based economy, and in higher value added manufacturing.

The approach to foreign investment is changing

Growth depends strongly on exports

24 Malaysia

Country Profile 2006 www.eiu.com © The Economist Intelligence Unit Limited 2006

According to the central bank, Malaysia!s potential output growth, determined by the expansion and non-inflationary utilisation of physical capital and the labour force, as well as by total factor productivity growth (TFP), stood at 5.7% in 2005. In the years before the Asian financial crisis, the Malaysian economy was growing at a rate that exceeded its potential growth. After the crisis, a gap opened between actual and potential production (more commonly referred to as the output gap)"largely owing to plunging capital investment"which did not disappear until 2004, when private investment recovered modestly. The biggest difference in the composition of economic growth after the Asian crisis is the significantly larger contribution made in recent years by TFP, which incorporates technological progress and greater efficiency. Capital is being used more efficiently, in part owing to past infrastructure investments and structural reforms. Government policy is aiming to boost productivity growth, for instance, by increasing the efficiency of the GLCs. The evidence on labour productivity is mixed: there are regular complaints about skill shortages and the low quality of Malay graduates. But the authorities have high hopes that the implementation of the Knowledge-Based Economy Master Plan, which includes large investments in education and training, will help to close the output gap.

The government seeks to control inflation by means of fiscal, monetary and industrial policies, and also intervenes directly to monitor and control prices. There are tight price controls on some 20 basic goods with a high weighting in the consumer price index. Inflationary pressures have increased with the surge in global oil prices during 2005/06 and a decline in the spare capacity of the Malaysian economy, although they have been partially offset by increased competition, as a result of falling trade barriers.

Inflation (% change)

Annual average 2005 2001-05Consumer price index (2000=100) 3.0 1.7

Source: Bank Negara Malaysia.

Malaysia has traditionally had a tight labour market. The unemployment rate averaged 3.5% in 2005, below the rate of 4% or less that the Malaysian authorities consider a full employment level. Malaysia attracts large numbers of foreign workers, especially from Indonesia, whom the government repatriates from time to time for economic or security reasons. In mid-2006 there were 1.8m legal foreign workers and at least half a million people working illegally. Manufacturing, plantation and construction as well as Malaysian households depend on"mainly unskilled"foreign workers. Over the past decade Malaysia has also experienced persistent shortages of skilled labour, which is being filled by controlled immigration from other Asian countries. As the country moves to become a knowledge-based economy, one of its greatest challenges is the need to equip workers with new skills.

Inflation is being kept in check

Raising efficiency determines the growth potential

Shortages of skilled labour continue

Malaysia 25

© The Economist Intelligence Unit Limited 2006 www.eiu.com Country Profile 2006

Malaysia�s relatively high wage levels (compared with some of its neighbours, such as Indonesia, for example) make the country a magnet for foreign labour but also lead to a steady loss of less-skilled jobs to surrounding countries, especially in recent years. Given the economy�s export dependence, it is not surprising that wages in the exposed sectors of the economy respond quickly to business cycle changes, in part also because of a lack of trade union bargaining power. Since 2001 the growth in salaries in the private non-manufacturing sector has exceeded that in manufacturing, reflecting a shift in the economy towards services.

Manufacturing sector real wages (% change)

Annual average 2005 2001-05Wages 0.8 2.1

Sources: Bank Negara Malaysia; Economist Intelligence Unit; official estimates.

Regional trends

Economic development is concentrated in the western states of the peninsula. Tin mining and plantation development began in the 19th century in Selangor, Perak and Johor"the areas that, together with Penang, still have the largest concentrations of manufacturing industry. Penang and the Klang Valley (in central Selangor, between the capital, Kuala Lumpur, and the coast) are the main locations of export-oriented manufacturing. Penang�s customs-free industrial zones have been the focus of investment by international electronics companies, whereas the Klang Valley has the largest and longest-established concentration of general manufacturing operations.

Successive five-year plans have fostered the location of industrial projects in new areas, still mainly in states on the west of the peninsula (Kedah, Negeri Sembilan and Malacca). In the predominantly rural states on the eastern coast of the peninsula (Kelantan, Terengganu and Pahang) and the two Borneo states (Sabah and Sarawak), industrial activity is mainly related to the processing of local raw materials. Timber processing has developed in all of these states.