Embed Size (px)

Citation preview

Maintaining Financial Stabilityin an Open Economy:

Sweden in the Global Crisis and Beyond

Ralph C. BryantDale W. Henderson

Torbjörn Becker

November 21, 2011

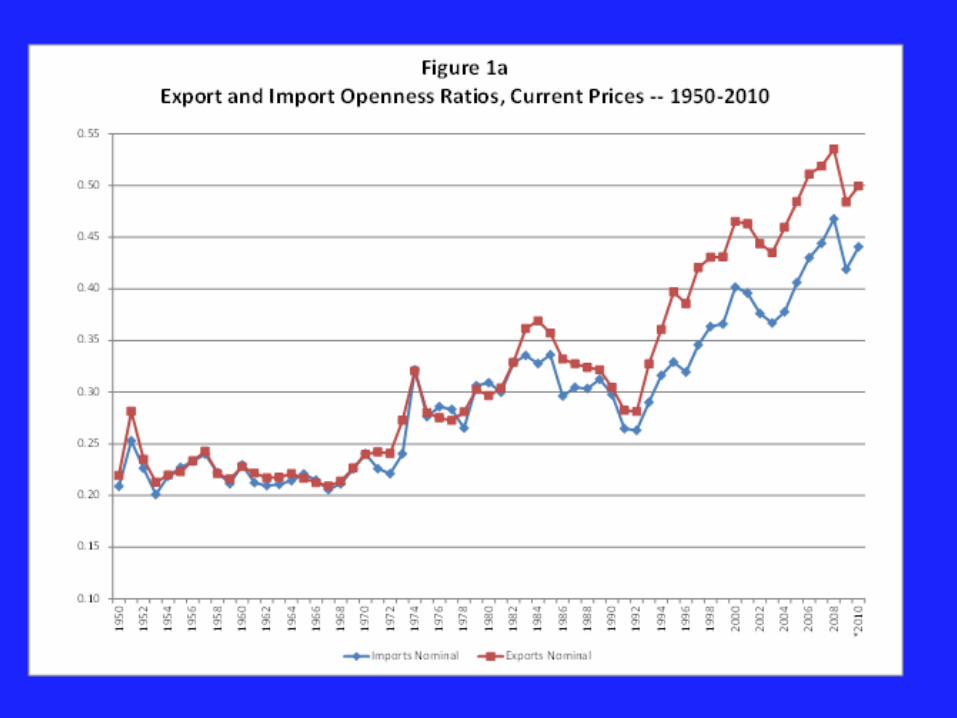

Sweden is highly open to the rest of the world, dependent on extensive cross-border transactions in goods, services, and financial assets and liabilities.

• The openness for goods and services has substantially increased during recent decades.

• The financial dimensions of openness have increased still more rapidly.

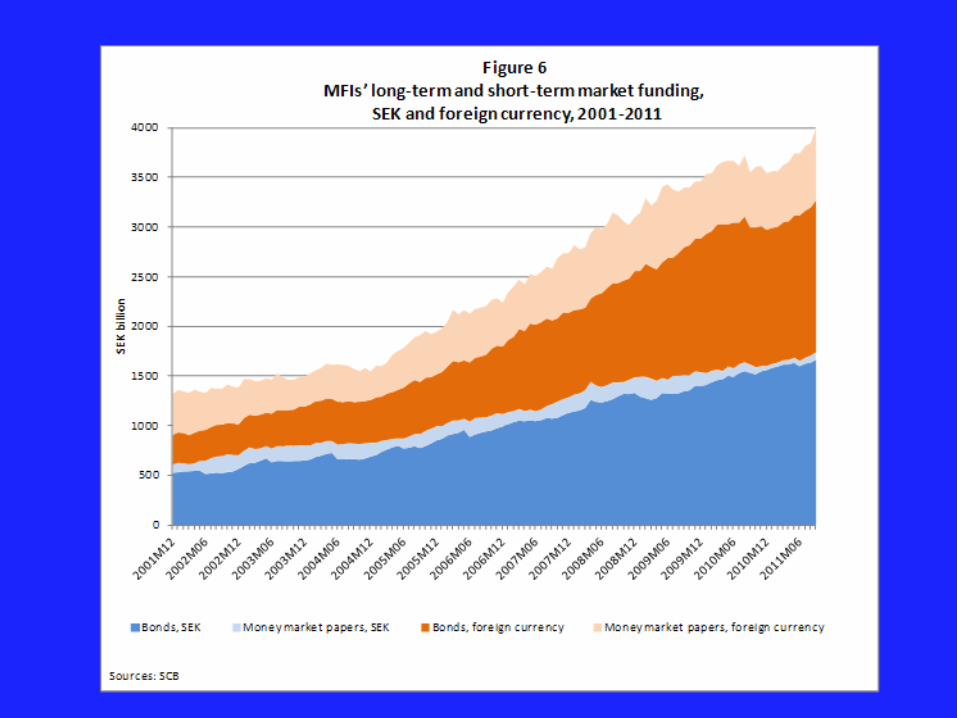

• Swedish financial institutions and markets are now pervasively linked to the rest of the global financial system.

Two key characteristics of the Swedish financial system:

- Swedish financial institutions rely heavily on borrowing and lending across the Swedish border, with many of the transactions and the resulting balance-sheet items denominated in foreign currencies. - The financial institutions depend significantly on wholesale market funding, arranged at shorter maturities, to finance their lending at longer maturities.

- The combination of these characteristics can be potentially hazardous in periods of global financial stress.

- Such vulnerabilities did suddenly surface in the fall of 2008.

The report discusses the entire broad range of collective-support activities taken by Swedish authorities during the 2008-2010 crisis period:

• emergency liquidity lending in dollars• emergency liquidity lending in kronor• emergency market support and extension of government guarantees • modification in government deposit guarantees• facilitating the orderly recapitalization or resolution of institutions coping with

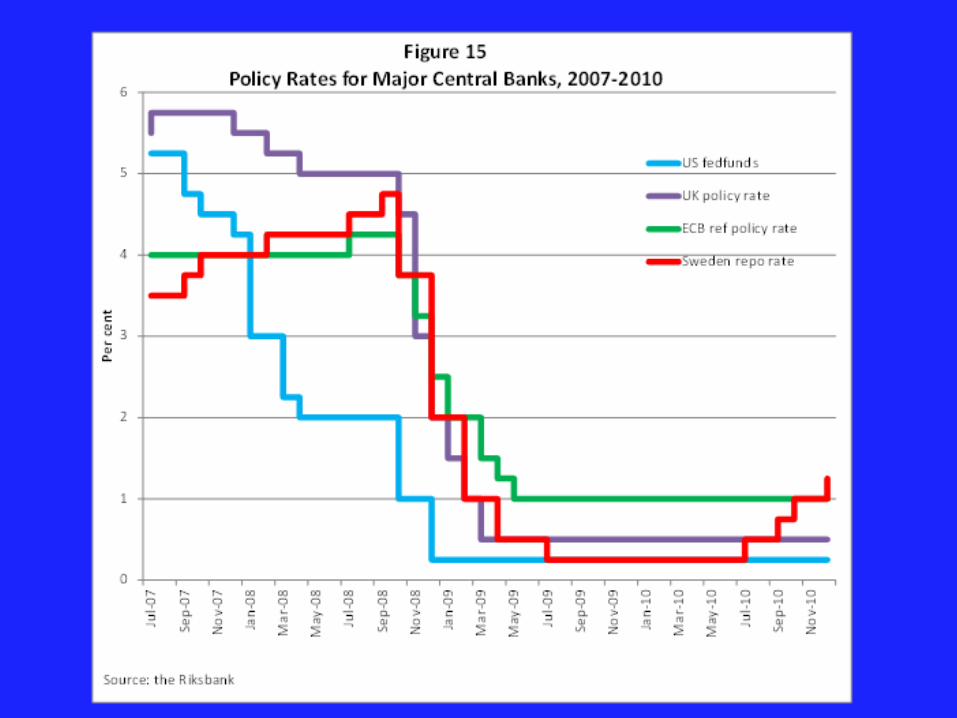

possible insolvency• in general the catalyzing of cooperative behavior to manage the crisis.• the crisis-period Riksbank decisions for the setting of the official policy interest

rate, the instrument of traditional monetary policy.

Swedish Emergency Financial Policies During the Global Crisis

All things considered, the Swedish crisis actions seem to us commendably prompt,

typically appropriate, and augur well for the management of

potential future crises.

Some Questions about Crisis Decisions Taken with the Traditional Instrument of Monetary Policy

Could the Riksbank have adopted a more accommodating posture for forward guidance about the repo rate during the crisis period?

Could the repo rate have fallen all the way to zero? Might more flexibility about the “zero lower bound” have been feasible and helpful?

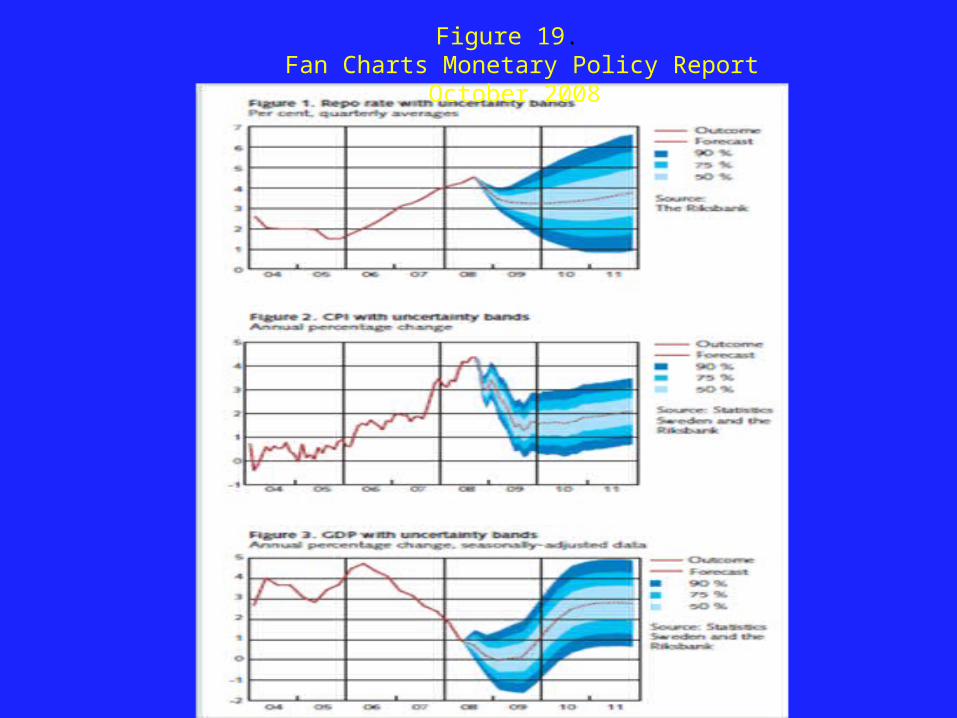

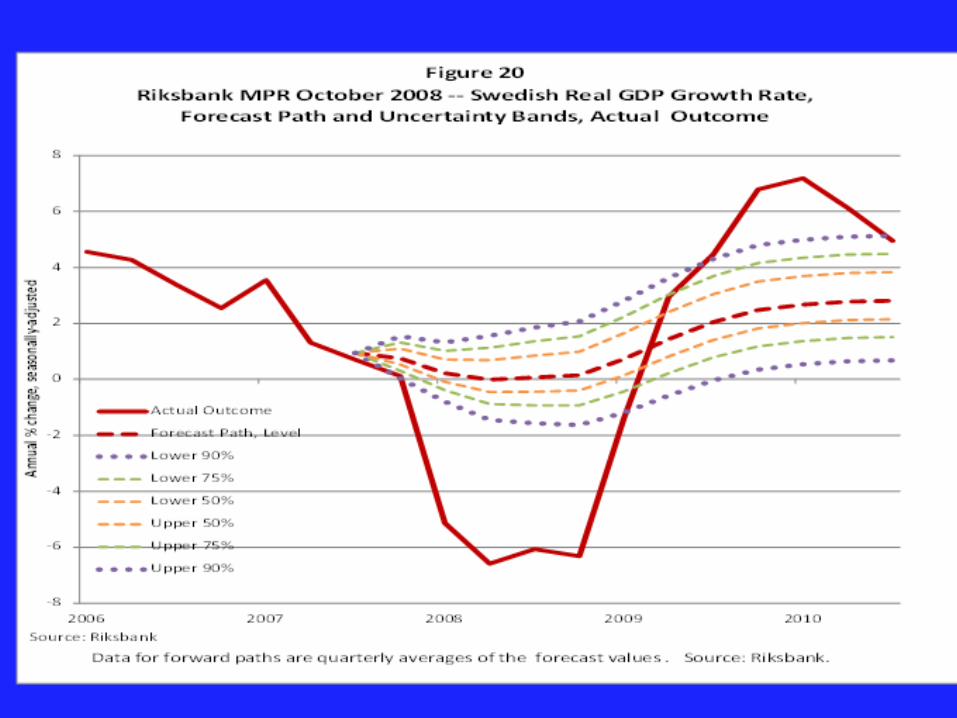

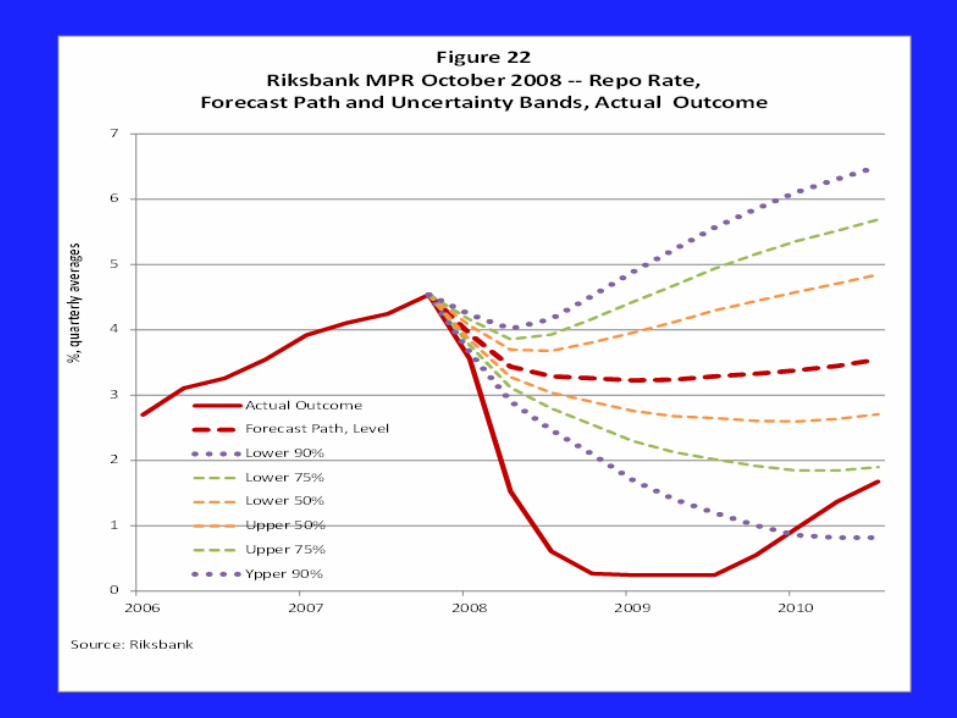

Could forward guidance have constructively given greater emphasis to uncertainty? Might there be a marginally different approach to the fan charts and their uncertainty bands?

Figure 24. February 2009 Figure 25. April 2009

Figure 26. July 2009

Figure 19. Fan Charts Monetary Policy Report October 2008

Could forward guidance have constructively given greater emphasis to uncertainty? Might there be a marginally different approach to the fan charts and their uncertainty bands?

- All central banks struggling with the issue

- Uncertainty in severe crises is especially great.

- Example of how the conventional uncertainty bands were very wide of the mark in the crisis.

Modifications or Refinements to Procedures for Handling Uncertainty

- Move away from the calculation of uncertainty bands dependent only on historical forecast errors. Experiment with a temporary abandonment of the customary procedures, introducing elements of discretionary judgment and contemporaneous conditions?

- Prepare uncertainty bands not only for the main scenario but also for the alternative scenarios?

- a temporary shortening of the time horizon over which forecast levels and uncertainty bands are to be presented.?

- consider abandoning – temporarily, and perhaps even permanently – the presentation of bands that are symmetric about a forecast path?

- consider an enhancement of the textual discussion of uncertainties in Monetary Policy Reports and Updates.

Exiting from Crisis Conditions in 2010-2011

- Recent period has been characterized by a debate within the Riksbank about the most appropriate stance and communication techniques for forward guidance for the repo rate.- What explains the differences in analytical approach between the majority and minority views?

- The current differences of view between the Board majority and Board minority about the substance of forward guidance are a first-order issue.

- Might it be helpful to give the public a more explicit discussion of the differences in analytical approach between the different views? Tailor that discussion to handling of uncertainty in communication of forward guidance?

-

The Global Crisis and theDebate About Financial Policies

• View that monetary policy ought to put higher priority on financial stability taken more seriously.

• New urgency for improving prudential policies. • Recognition that monetary policy and prudential

policies related so probably better if coordinated. • Increased focus on allocation of responsibilities for

financial policies – among agencies in a country and among international institutions.

Monetary Policy and Financial Stability • Before • First, the Fed cannot reliably identify bubbles in asset prices.

Second, even if it could identify bubbles, monetary policy is far too blunt a tool for effective use against them. (Bernanke 2002)

• If prices of houses or other assets are partly driven by factors that are hard to explain and that are believed to give rise to inefficient allocations and risks of large fluctuations in real economic activity and inflation, such events will, in one way or another, find their way into our thinking about monetary policy. (Ingves September 2007)

• After • The diverse tools of financial regulation and supervision, … should

be, I believe, the first line of defense against the threat of financial instability. However, …the possibility that monetary policy could be used directly to support financial stability goals, at least on the margin, should not be ruled out. (Bernanke October 2011)

Monetary Policy and Financial Stability

• Conditions for using monetary policy to fight bubbles (Kohn 2006)– Must be able to identify bubbles with reasonable accuracy and

at an early stage to avoid taking actions that unnecessarily harm the economy.

– Must be a good chance of damping speculative activity with policy-rate increases that do not take too heavy a toll on the rest of the economy.

– Costs of ending the bubble early must be less than the costs of waiting to take action until after the crash.

• These conditions enunciated before the global crisis. The conviction that all three must hold appears to have softened.

• Growing sentiment that, in a highly uncertain world, the conditions might be satisfied more often than previously thought.

Prudential Policy InstrumentsIllustration of Possible Layering of Capital Requirements

Type of Requirement Reason for Imposition Percent of

Assets

Structural Capital too low (moral hazard) 7.0

Cross-sectional Foreign-affiliate loans exceed 25% 2.0

Cyclical Cost of and need for capital 2.5

SIFI Size & connectedness externalities 2.5

Maximum requirement 14.0

Maturity Mismatchs: General• “… Riksbank’s stress tests indicate that the banks …are taking

larger liquidity risks than many other European banks.” FSR 2011:1

• View echoed by IMF staff in their Financial Sector Stability Assessment for Sweden (July 2011)

• It is noteworthy that neither report stresses maturity mismatches in foreign currency.

• According to Finansinspectionen’s liquidity reporting regulations) “All amounts shall be…reported separately in SEK, EUR, USD and other currencies”. (FFFS 2011:37, Section 5)

• Large short-term uncovered dollar borrowing makes Sweden vulnerable to liquidity squeeze in dollars. Rough estimate is SEK 450 billion , 14% of GDP, by big four bank. (Nyberg 2011)

Foreign Currency Mismatch: Solution One• Require banks to reduce maturity mismatch in foreign currency. • Basel III minimum regulatory standard for Liquidity Coverage

Ratio (LCR) regardless of currency

• Basel III framework includes not as minimum regulatory standard but as a monitoring tool a LCR by significant currency. For the dollar

• Sweden free to set its own standard

Foreign Currency Mismatch: Solution 2

• Have Riksbank hold significant amount of dollar reserves and act as lender of last resort in dollars

• When is this solution efficient?– If dollar liquidity needs of banks uncorrelated,

Riksbank reserves can be low since only a few banks will need to borrow at any given time.

– But if dollar liquidity needs of banks very correlated, as they often have been, much less to gain.

– Might be cheaper because Riksbank (via SNDO) can borrow at a relatively low rate.

Foreign Currency Mismatch: Comparison

• What are the costs and who should pay them?– Difference between rate for long-term dollar borrowing

and short rate for liquid dollar investment.– Banks pay a fee for a credit line in dollars at the Riksbank

related to their short-term liabilities

• Difficulties with either solution – Level of liquidity ratio?– Amount of fee and relationship of credit line with Riksbank

to short-term liabilities?

tf

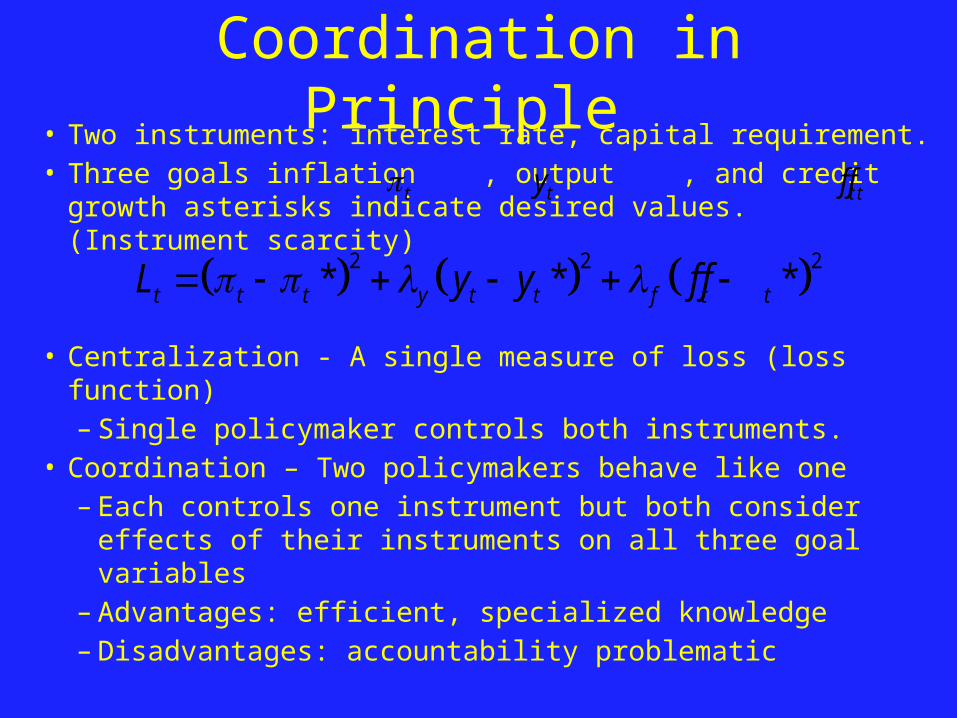

Coordination in Principle • Two instruments: interest rate, capital requirement.• Three goals inflation , output , and credit growth

asterisks indicate desired values. (Instrument scarcity)

• Centralization - A single measure of loss (loss function)– Single policymaker controls both instruments.

• Coordination – Two policymakers behave like one– Each controls one instrument but both consider effects of

their instruments on all three goal variables– Advantages: efficient, specialized knowledge– Disadvantages: accountability problematic

t ty

2 2 2* * *t t t y t t f t tL y y f f

tf

Coordination in Principle• Decentralization – Divide loss function up and have policymakers

consider only effects on parts they have been given when choosing their instruments.

– Advantages: accountability and specialized knowledge– Disadvantage: inefficient

• Degree of inefficiency depends on effects of each on the other’s goal• Different loss functions not so plausible.• Differences in model or information

2 2

, * *m t t t y t tL y y

2

, *p t f t tL f f

Coordination in Practice

Ministry ofFinance

National Debt Office

Finans-inspektionen

Riksbank

iFinancial Stability Council?

Is It Broke?• Memorandum of Understanding 2009 sets out the

responsibilities of a “consultation group” of same four agencies but– no formal rules for making sure advice considered – no way of confirming what happened at meetings.

• Apparent efficiency gains from merging Riksbank and FI• However, looks as though headed for continuation of

something like current division of responsibilities • Set up a “Financial Stability Council” with same agencies

but changes to remedy shortcomings– Comply or explain– Minutes made public with a lag.

Need for Better Models of Financial Behavior

• Models of the transmission of monetary policy through the financial system more inadequate than realized before crisis.

• Few models of effects of macroprudential policies including their possible time variation.

• Now intensification of research efforts to improve the modeling of financial behavior, including at the Riksbank.

• Efforts include integrating research on financial behavior into the larger, general-equilibrium models underpinning all types of macroeconomic and prudential policy actions.

![INDEX [] · 2005-10-25 · 5 Bryant, John F, 27 Bryant, Levi Clinton, Sr, 109 Bryant, Lillie S, 101 Bryant, Linster, 101 Bryant, Litha L, 109 Bryant, Louisa M, 111 Bryant, Mary, 101](https://img.dokumen.tips/doc/110x75/5f4498e1f4a6be5e1a48d4d2/index-2005-10-25-5-bryant-john-f-27-bryant-levi-clinton-sr-109-bryant.jpg)