Embed Size (px)

Citation preview

EGMP-38 – Macroeconomics Assignment

Name of the Student – Rahul Chandrashekar

EGMP Batch - 38

Roll Number - EGMP38047

Subject - Macro Economics

Table of Contents Analyze the impact of BrExit on the global economy? ..................................................................................................................... 2

Background .................................................................................................................................................................................. 2

UK Economy & Impact due to BrExit ............................................................................................................................................ 5

Foreign Direct Investment .................................................................................................................................................. 5

Trade, Current Accounts & External Debt .......................................................................................................................... 6

Foreign Exchange & Reserves Depletion ............................................................................................................................ 8

Education ........................................................................................................................................................................... 8

Indicators for increase in Labor Cost .................................................................................................................................. 9

Indicators for Deflation (and) hyperinflation ..................................................................................................................... 9

Industries impacted .......................................................................................................................................................... 10

Impact to Global Economy ......................................................................................................................................................... 12

Articles from Newspaper ........................................................................................................................................................... 15

Discuss FCNR deposits and the impact that its maturing will have on the exchange rate? ............................................................ 16

Overview .................................................................................................................................................................................... 17

Background ................................................................................................................................................................................ 18

Current Accounts and Reserves ................................................................................................................................................. 18

Impact to Exchange rate ............................................................................................................................................................ 19

Impact to Economy .................................................................................................................................................................... 20

Solutions & Opportunities .......................................................................................................................................................... 20

Articles from Newspaper ............................................................................................................................................................ 21

Write a short note on NPA’s in the banking sector and transmission of monetary policy? ........................................................... 22

How did the problem worsen? .................................................................................................................................................. 24

Burden on the fiscal System ....................................................................................................................................................... 25

Transmission of monetary policy ............................................................................................................................................... 25

EGMP-38 – Macroeconomics Assignment

Analyze the impact of BrExit on the global economy?

This write-up gives overview of the background of BrExit with its impact to UK and global market.

Background

The European Union is a system of international institutions, the first of which originated in 1957, which now

represents 27 European countries through the following bodies:

– European Parliament: elected by citizens of member countries

– Council of the European Union: appointed by governments

of the member countries

– European Commission: executive body

– Court of Justice: interprets EU law

– European Central Bank, which conducts monetary policy through a system of member country

banks called the European System of Central Banks

For a country to be a member of the EU, it should -

– Have low barriers that limit trade and flows of financial assets

– Adopt common rules for emigration and immigration to ease the movement of people

– Establish common workplace safety and consumer protection rules

– Establish certain political and legal institutions that are consistent with the EU’s definition of

liberal democracy.

EGMP-38 – Macroeconomics Assignment

Fig -1 : European Union

Key data (EU VS UK)

Objectives of EU

Oneness

– Promotion of peace and the well-being of the

Union´s citizens.

– An area of freedom, security and justice without

internal frontiers

Economy

– Sustainable development based on balanced

economic growth and social justice

– Social market economy - highly competitive and

aiming at full employment and social progress

– Free single market

0 200,000,000 400,000,000 600,000,000

Population

UK 65,110,000

EU 510,056,011

0 1,000,000 2,000,000 3,000,000 4,000,000 5,000,000

Area (sq-km)

UK 242,495

EU 4,324,782

0 5 10 15 20 25

GDP (Trillion $)

UK 2.849

EU 19.205

0 10,000 20,000 30,000 40,000 50,000

GDP / Capita ($)

UK 43,771

EU 31,918

EGMP-38 – Macroeconomics Assignment

BrExit is the withdrawal of the United Kingdom (UK) from the European Union (EU). UK joined the European

Economic Community (EEC), the predecessor of the EU, in 1973. Continued membership of the EEC was approved

in a 1975 referendum by 67% of voters. In the June 2016 referendum on EU membership, 52% voted to leave,

resulting in the complex process of withdrawal being initiated and political and economic changes in the UK and

other countries.

Reference - Wikipedia

52%48%

United Kingdom European Union membership referendum, 2016

Leave Remain

67%

33%

United Kingdom European Community (Common Market) Membership Referendum 1975

Yes No

Note

As of August 2016, the UK has not yet initiated

the formal withdrawal procedure, and will not

leave the EU until either two years after they

notify the European Council of their decision

to withdraw, or on the coming into force of a

withdrawal agreement.

Fig -2 : Referendum BrExit

Fig -3 : Voting pattern Referendum BrExit

EGMP-38 – Macroeconomics Assignment

UK Economy & Impact due to BrExit

UK has been one the biggest benefactor from the access of common market, due to the fact that it’s GDP has

grown at an exponential rate after becoming a member of EU – due to the fact that EU has tested Britain’s

economy by unleashing greater competition. Access of single market has provided unique opportunity for UK to

expand its boundaries by accessing resources, new technology, opportunity cost (access to low cost labor) etc.

Being one of the largest markets within the union, UK offered gateway for commerce for established companies in

UK (pre-1973).

Fig -4: GPD grown UK

Foreign Direct Investment UK is also the largest recipient of FDI in EU due to its competency and high financial services, healthcare services,

manufacturing services. However, BrExit will have huge out flux of capital from UK which could have consequences

to its industry, there are trends which witnesses the domino effect in UK post-BrExit - The Purchasing Managers'

Index (PMI) is an indicator of the economic health of the manufacturing sector has come down in UK.

Fig 5 : FDI flow EuroZone Fig 6 : UK Manufacturing PMI

EGMP-38 – Macroeconomics Assignment

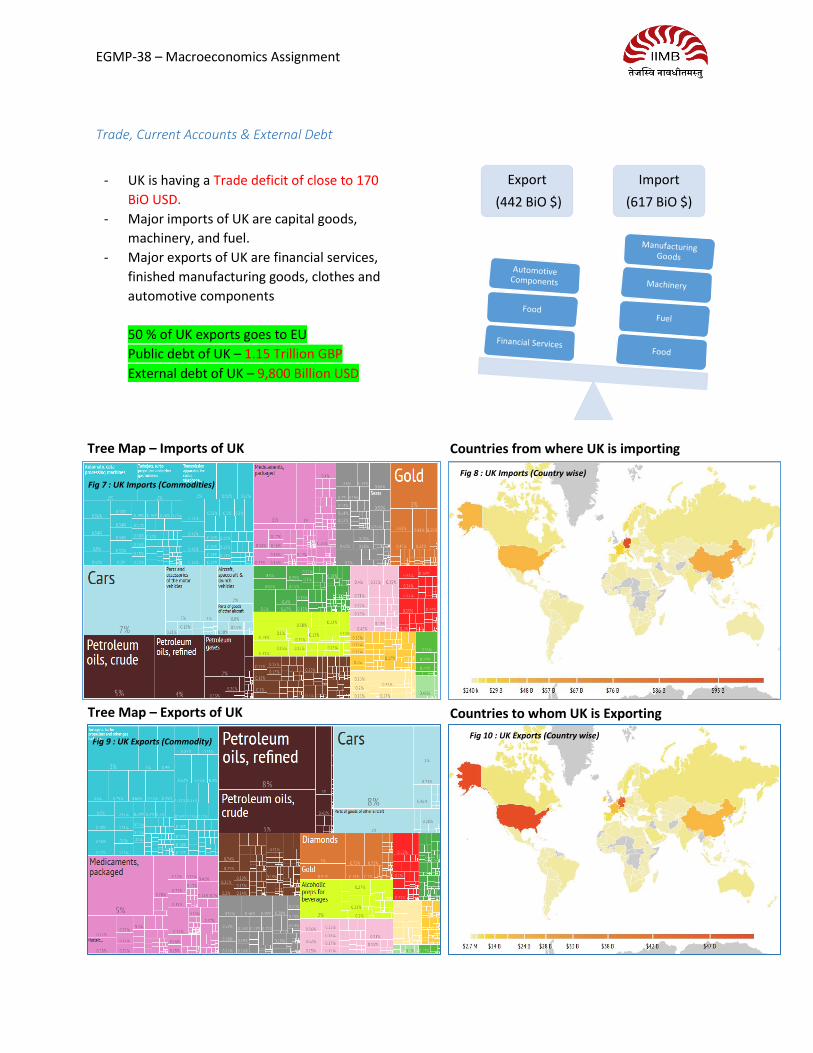

Trade, Current Accounts & External Debt

Export

(442 BiO $)

Import

(617 BiO $)

- UK is having a Trade deficit of close to 170

BiO USD.

- Major imports of UK are capital goods,

machinery, and fuel.

- Major exports of UK are financial services,

finished manufacturing goods, clothes and

automotive components

50 % of UK exports goes to EU

Public debt of UK – 1.15 Trillion GBP

External debt of UK – 9,800 Billion USD

Tree Map – Imports of UK Countries from where UK is importing

Tree Map – Exports of UK Countries to whom UK is Exporting

Fig 7 : UK Imports (Commodities)

Fig 8 : UK Imports (Country wise)

Fig 10 : UK Exports (Country wise) Fig 9 : UK Exports (Commodity)

EGMP-38 – Macroeconomics Assignment

- BrExit will have impact of UK exports as it is a

market 50% of its exports are consumed by EU.

- Exports of UK (to EU) - ~ 250 BiO $

- Exit from BrExit could mean that the manufacturing

will be shifted to countries like Ireland and financial

services will be shifted to countries like Luxemburg.

- Reduction in demand of UK exports could translate

in reduction in production, reduction in

employment which will result from economic

slowdown to economic recession.

- Labor cost will become more expensive due to less

flow of labor from EU which could have negative

impact in the economy. This is irrespective of

depreciation of UK currency.

- Possibility of using cash reserves and reduction of

interest rate will benefit economy (short-term

shocks) but due to possibility of fall in demand of

UK exports, reduced access to free market – it does

not provide the vital signs of employment.

- Education industry could have an impact due as UK

attracts thousands of students (primarily in China,

India) – new ideation will have impact.

- Reduction in employment will result in other socio-

economic issues.

- Reduction in employment will result in reduced

consumption which will result in falling prices –

possibility of deflation

- Balance of trade gap could raise making imports

dearer due to depreciation of UK currency – if no

economic activity does not happen it could result in

hyperinflation

- Public debt of UK is 85% of GDP which will

magnitude recession.

Fig 11 : UK Exports & Imports (within EU)

Fig 12 : UK Interest Rate

Fig 13 : UK Government Debt

EGMP-38 – Macroeconomics Assignment

Foreign Exchange & Reserves Depletion

Education

- Post BrExit has caused depreciation of UK

pound against US dollar and EU euro.

- Though depreciation of UK pound benefits

exports, it would make imports dearer and with

limited access to free market it could result in

recession.

- UK has foreign exchange reserves of 160 BiO

USD. This will help is handling of short-term

shocks and volatility

- UK attracts approx. 200,000 plus students

worldwide yearly.

- BrExit will reduce the attractiveness to students

of foreign origin due to reduced job

opportunities.

Fig 14 : UK GBP Vs USD

Fig 15 : UK Foreign Reserves Fig 16 : UK GBP Vs EURO

Fig 17 : UK Student inflow

EGMP-38 – Macroeconomics Assignment

Indicators for increase in Labor Cost

Indicators for Deflation (and) hyperinflation

Short-term Effect – Inflation followed by Deflation

- BrExit will increase the labor cost due to

o Limited access to low labor cost

o Payment of borrowings

- High labor cost will provide option for shifting

production and services from UK to emerging

and EU countries (like Ireland, Spain, etc –

which are looking for filling the UK void).

- BrExit will cause inflation in commodities due

to speculation.

- BrExit could result in reduction of consumption

/ demand of commodities.

- Reduction in commodities could result in price

reduction which results in Deflation.

- Markets with deflation does not attract

business as the market does not offer any

opportunity.

- Deflation causes a negative spiral to the

economy and makes activities worse.

Fig 18 : UK Labor cost

Fig 19 : Forecast economical pattern - Deflation

EGMP-38 – Macroeconomics Assignment

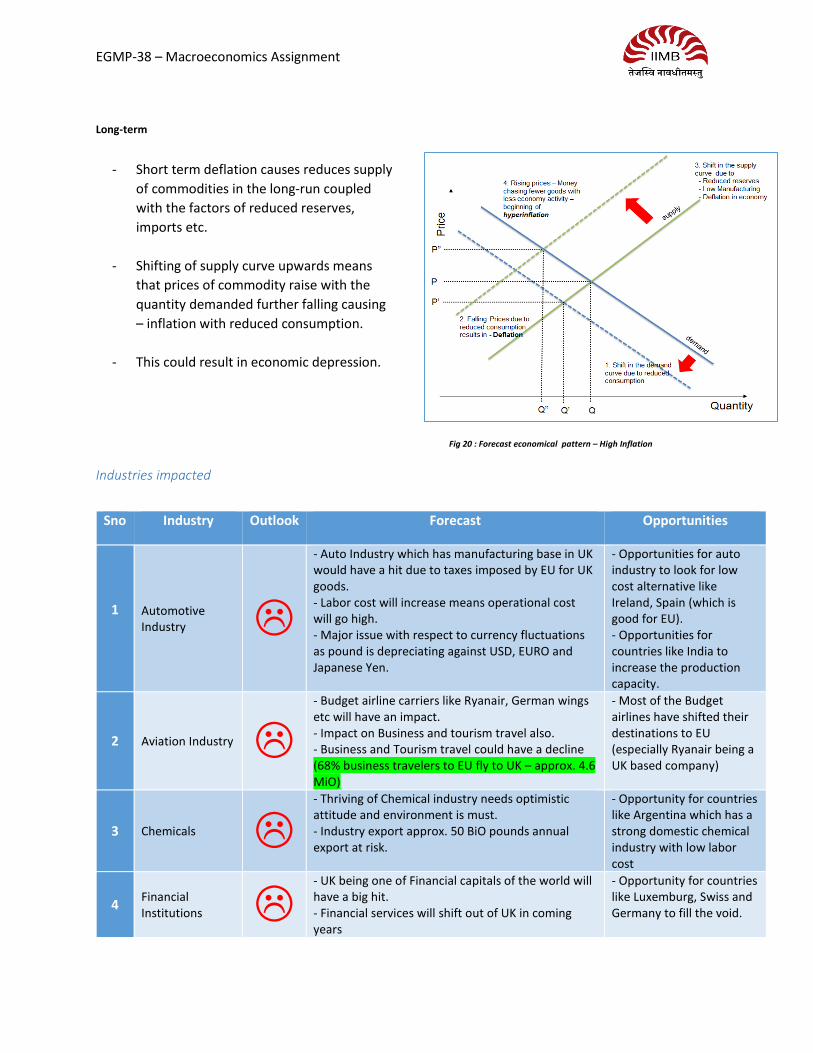

Long-term

Industries impacted

Sno Industry Outlook Forecast Opportunities

1

Automotive Industry

- Auto Industry which has manufacturing base in UK would have a hit due to taxes imposed by EU for UK goods. - Labor cost will increase means operational cost will go high. - Major issue with respect to currency fluctuations as pound is depreciating against USD, EURO and Japanese Yen.

- Opportunities for auto industry to look for low cost alternative like Ireland, Spain (which is good for EU). - Opportunities for countries like India to increase the production capacity.

2 Aviation Industry

- Budget airline carriers like Ryanair, German wings etc will have an impact. - Impact on Business and tourism travel also. - Business and Tourism travel could have a decline (68% business travelers to EU fly to UK – approx. 4.6 MiO)

- Most of the Budget airlines have shifted their destinations to EU (especially Ryanair being a UK based company)

3 Chemicals

- Thriving of Chemical industry needs optimistic attitude and environment is must. - Industry export approx. 50 BiO pounds annual export at risk.

- Opportunity for countries like Argentina which has a strong domestic chemical industry with low labor cost

4 Financial Institutions

- UK being one of Financial capitals of the world will have a big hit. - Financial services will shift out of UK in coming years

- Opportunity for countries like Luxemburg, Swiss and Germany to fill the void.

- Short term deflation causes reduces supply

of commodities in the long-run coupled

with the factors of reduced reserves,

imports etc.

- Shifting of supply curve upwards means

that prices of commodity raise with the

quantity demanded further falling causing

– inflation with reduced consumption.

- This could result in economic depression.

Fig 20 : Forecast economical pattern – High Inflation

EGMP-38 – Macroeconomics Assignment

Sno Industry Outlook Forecast Opportunities

5 Manufacturing (Light & Heavy)

- Manufacturing will have issues in long run in UK due to high labor cost and tax imposed to UK goods from EU - Reduced demand for UK goods could result in deflation which is a negative booster for any manufacturing economy. - Local Manufacturing will not be an option due to high price increase - Efficiency could be vital issue

- Opportunities for countries like Ireland, India to fill the void. - Opportunities for China import getting higher but will have to further reduce the price on imports

6 Oil Industry

- Oil analysts and traders were in agreement that this decline in price was likely to hold only for the short-term. - In the long-term, a greater question mark now looms over the prospects of the UK oil and gas industry, which was already seeing market challenges. Outside of the EU, the UK could see barriers to trade. There is no clear indication yet of what sort of movement and trade deals a non-EU UK would be able to establish with the European Union.

- Opportunities of new scientific quest. - Development of alternative low cost fuel energy source – like fuel cell

7 Pharma

- Pharma industry which just recovered from 2008 financial crisis will have a hit due to BrExit. - Prices of drugs will increase. - Choices for low cost manufacturers in the offing.

- Opportunity for low cost drug manufacturers to fill the void.

8 Real Estate

- Real estate projects are at bigger risk. - Access to low cost labor from EU no more an option. - Access to high cost local labor market adds pressure. - Delays in construction projects could add negative spiral.

- Opportunities for innovation like 3D printed road and bricks (currently used in Netherlands) - Opportunity for manufacturers from India, China to export low cost raw materials like steel, cement etc.

9 Retail

- Retail industry will have an immediate hit due to reduced demand of the products - Negative supply spiral could have drastic impact to the economy.

- Opportunities for low cost countries to export products to UK

10 Software Industry

- IT industry setup in UK will have a major hit. - Ramp-down of employment with pay cuts. - IT export countries like India will have a hit in profitability.

- Opportunities for countries like Ireland to fill the void.

11 Textiles - Textile imports could have an impact in UK which will have an impact to countries like India, Vietnam etc

- Opportunities for countries like Bangladesh, Sri lanka

12 Tourism

- Depreciation of Pound could have an impact on reduced airfares. However, with reduced frequency of destinations from flight carriers to UK, tourism industry could have a hit.

- Opportunities for countries like Greece to capitalize on tourism opportunity.

:-|

EGMP-38 – Macroeconomics Assignment

Impact to Global Economy

Legend

Sno Country Outlook Impact & Opportunity

1 African Union

- Africa’s export to UK represents about 5% of total Africa’s export. - Africa is more feared on slowdown in China than BrExit as China is its biggest trading partner. - Opportunities for countries like Nigeria, Ghana for providing services on energy and manufacturing. - Opportunities for countries like south Africa for providing better financial and healthcare services. - Opportunities for African union in providing low cost minerals and ores for manufacturing world.

2 ASEAN

- ASEAN countries are the largest importers of UK products - Brunei 680 MiO USD imports from UK vs 48 MiO USD exports to UK - Cambodia 25 MiO USD imports from UK vs 1.2 BiO USD exports to UK - Indonesia 1 BiO USD imports from UK vs 2.2 BiO USD exports to UK - Philippines 600 MiO USD imports from UK vs 650 MiO USD exports to UK - Singapore 6 BiO USD imports from UK vs 2 BiO USD exports to UK - Malaysia 2 BiO USD imports from UK vs 2.2 BiO USD exports to UK - Vietnam 700 MiO USD imports from UK vs 4.8 BiO USD exports to UK - Thailand 1.8 BiO USD imports from UK vs 3.6 BiO USD exports to UK

- Brunei, Singapore could be hit in a big way due to BrExit due to increase in prices of imports from UK. - Opportunity for Singapore to fill void of financial services of UK. - Opportunity for Malaysia, Indonesia, Vietnam in providing low cost manufacturing.

3 Australia

- Australia is also least affected by BrExit as approximately less than 4 % of its exports goes to UK - Majority of Australia exports (75%) goes to emerging markets. - In spite of the short term shocks, Australia will emerge as a gainer in the long-run. - Having huge amount of resources, it can also provide support in terms of attracting investments.

4 Brazil

- Brazil will also be able to survive short-term and long-terms shocks due to BrExit. - Brazil 4.2 BiO USD imports from UK vs 4 BiO USD exports to UK - Brazil with resources and low labor cost will be attracted by EU as an alternative to China / UK

5 Canada

- United Kingdom is Canada’s third largest merchandise export destination, after the United States and China. - Canada might actually negotiate a slightly better trade deal than the comprehensive economic and trade agreement forged with EU. - Telecommunications, manufacturing will have boost.

6 China - China being an export oriented economy will have issue due to BrExit.

- China manufacturing is expected to reach saturation by 2025 and BrExit has range of saturation.

good bad neutral

EGMP-38 – Macroeconomics Assignment

- Expects economic slowdown, deflation in long run, however UK will still have to import goods and services from China – as UK labor cost will be higher. - China has approx. more than 1 Trillion USD in reserves and will be able to survive the shock.

7 EU

- Even though EU has short-term volatility due to BrExit, there are potential opportunities in the offing. - Ireland, Dutch, can fill the void of being the next manufacturing and IT services from Britain. - Luxembourg has potential for filling the void of financial services from Britain, - Labor cost is predicted to come down, which will boost the economy of EU in long run. - Major cause of concern could be on the ageing population and stability of Euro against USD

8 Germany

- Germany is one of the largest exporter and importer from UK. - Germany is also the largest economy in EU and a powerhouse. - BrExit poses potential opportunity and threat to Germany. - Threat (primarily short-run) is falling GBP could have issues for the German automotive and manufacturing sectors. - Ageing population could be a challenging aspect.

9 India

- India being a domestically driven economy (Consumption) is insulated for any shocks from BrExit - India has foreign reserves of approx. 350plus Billion USD and will expect to handle any short terms shocks. - Since the world is looking for a stable economy, India will attract more FDI / capital inflow. - IT industry and Textiles could have a short term hit due to volatility/ uncertainty. - Since the decision on BrExit will take at least 2 more years, India will not have a big

hit. - 7 to 14% of IT revenues depend on UK programs, out of with there could be a reduction of 3 to 6% in revenue. - Textile contribute to approx. 24% of Indian export which could be in radar however will not have an impact due to low cost production compared to UK. - Manufacturing will be a huge boost due to low labor cost with access of labor pool. - Making labor skill ready could be a potential challenge. - Demographic dividend will be a key aspect in promoting growth

10 Japan

- Raising Yen and falling GBP has negative affect to Japan. - Japan which is currently in lost decade due to housing bubble will have major challenges with its manufacturing and automotive centers located in UK - Depreciating GBP will have consequences in profitability an operational. - Ageing population also adds magnitude to negative spike.

11 Latin America

- BrExit will cause further decline in Latin American commodity prices – which has fallen substantially in last four years. - Major resources (minerals, oil, raw materials) from Latin America is consumed by UK. - Falling demand will have negative impact causing already existing food inflation in Latin America causing chaos and instability. - Reduced investments from UK means that Latin America will not have reserves for global trade.

12 Mexico - Mexico peso had a depreciation with BrExit and expects austerity and budget

cuts.

EGMP-38 – Macroeconomics Assignment

- Mexico being one of the emerging markets poses potential on manufacturing and technology services - Mexico also has potential of being nearshored to USA providing services and resources to North America and EU

13 Russia

- Russia is one of the biggest gainer due to the energy rich resources. - Post BrExit , most of EU nations will ease sanctions in favor of Russia - However, Russia poses threat on global oil prices possible can come down due to reduction in world trade - Russia low cost labor will appreciate economy by boosting opportunities in manufacturing.

14 South Korea

- Asia's fourth-largest economy intends to bet big on innovation to mitigate any potential economic damage. - "We will pre-emptively respond to the BrExit impact through creative endeavors for

innovation," Prime Minister Hwang Kyo-Ahn announced at the World Economic Forum

- Structural reforms in sectors including education, labor and finance will help Korea ride the wave of the fourth industrial revolution

15 Turkey

- Turkey being a growing economy places will experience good cycles due to BrExit. - Turkey which has always tried to be a member of EU and exit of UK will pose opportunity for Turkey membership. - Low labor cost will boost manufacturing services - Political climate needs to be monitored.

16 USA

- US could have short term volatility as most of it financial and Automotive companies have manufacturing headquarters in UK - Strengthening of USD against is good boost for the economy however its assets in UK could have impact. - A strong dollar makes product commodities more expensive outside US which could have impact to its commodities and export. - Possibility of movement of manufacturing to Ireland is in offing for tapping EU market in long-run. - Possibility of movement of Financial services to EU from UK in the offing. - No visible long-term volatility

EGMP-38 – Macroeconomics Assignment

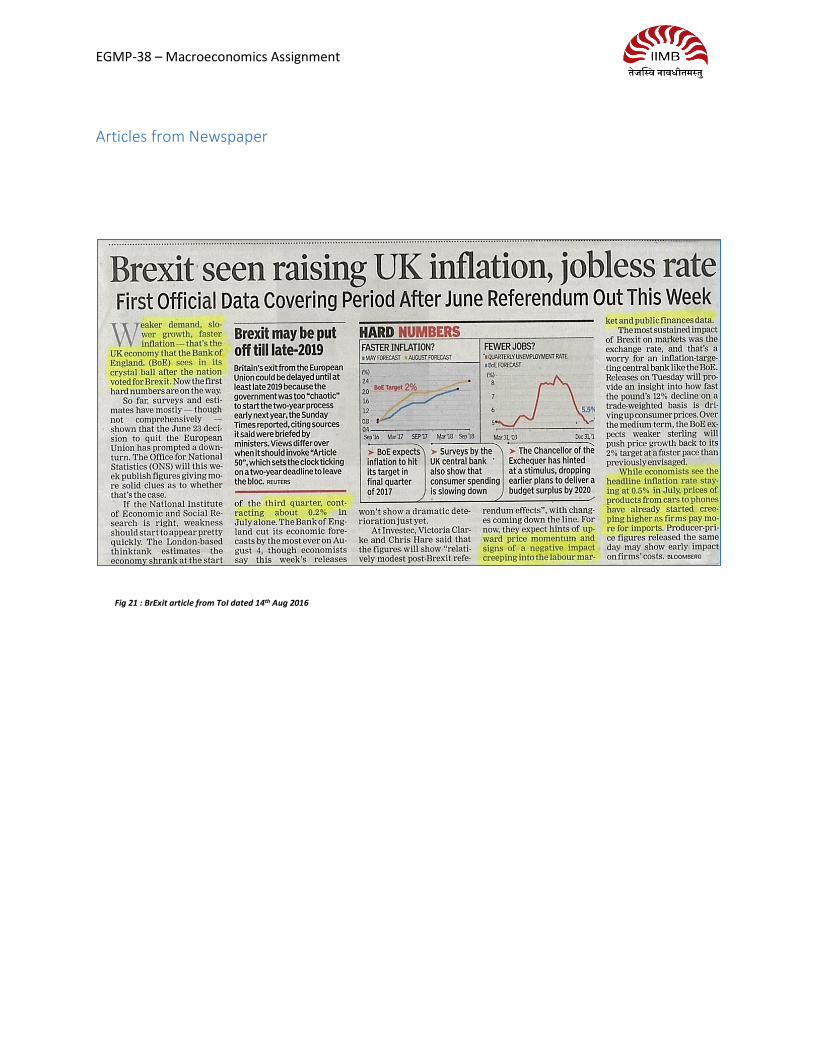

Articles from Newspaper

Fig 21 : BrExit article from ToI dated 14th Aug 2016

EGMP-38 – Macroeconomics Assignment

Fig 22 : BrExit article from FE dated 18th Aug 2016

EGMP-38 – Macroeconomics Assignment

Discuss FCNR deposits and the impact that its maturing will have on the

exchange rate?

Overview

- FCNR (B) deposit is abbreviated as Foreign Currency Non-Resident (B), is a term deposit which can

be opened by NRI (Indian residents, who are in employment, studying and staying permanently abroad and foreign nationals -with their origin in India (except of Pakistan and Bangladesh). Students proceeding abroad for higher studies are treated as Non-residents).

- FCNR(B) Term Deposit have maturity of minimum 1 year & maximum 5 years and depositors can open the deposit using – Pound Sterling, United States Dollar, Euro , Australian Dollar, Japanese Yen and Canadian Dollar.

o Foreign Currency Travelers Cheque / Notes may be accepted during temporary visits of the NRI, for credit to account.

o Minimum Balance requirements 1000 USD 500 GBP 1000 Euros 1000 CAD 1000 AUD 110,000 Yen

- FCNR (B) deposits are not taxable under wealth tax and Interest from FCNR (B) accounts are exempted from Income tax rules and these accounts can be opened as per depositor’s choice, in any of the permitted currencies, with / out of the funds received as foreign inward remittances in convertible currency through normal banking channel.

- As per RBI guidelines – banks can grant loans and overdraft facilities to the deposit holders.

- Interest rates on FCNR (B) deposits are regulated by RBI and are the same across all the banks. The biggest advantage of FCNR deposits is that there is no currency risk, i.e. if a depositor invests in USD, he/she will receive USD on maturity.

- The disadvantage of FCNR deposits is the low interest rate – approx. 2.7% for term of 1-2 years (for USD). However to address the low interest rates, RBI introduced forward cover to increase the yield of FCNR deposits.

- Forward contract locks the Rupee returns on the deposits and future movements in currency markets cannot affect returns – thus protecting the depositor from fluctuations in the exchange rate. Combining the interest rates and forward cover the return on yield is increased from 2.7% to 8-9%.

EGMP-38 – Macroeconomics Assignment

Background

Current Accounts and Reserves

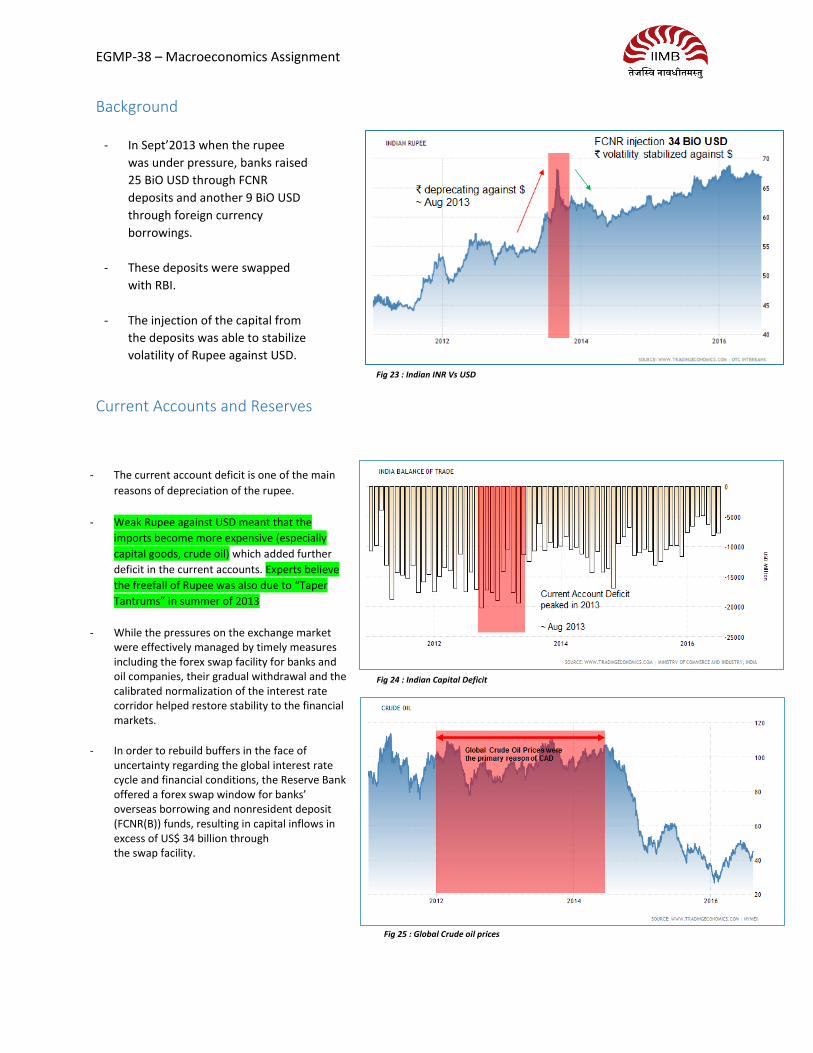

- In Sept’2013 when the rupee

was under pressure, banks raised

25 BiO USD through FCNR

deposits and another 9 BiO USD

through foreign currency

borrowings.

- These deposits were swapped

with RBI.

- The injection of the capital from

the deposits was able to stabilize

volatility of Rupee against USD.

- The current account deficit is one of the main

reasons of depreciation of the rupee.

- Weak Rupee against USD meant that the

imports become more expensive (especially

capital goods, crude oil) which added further

deficit in the current accounts. Experts believe

the freefall of Rupee was also due to “Taper

Tantrums” in summer of 2013

- While the pressures on the exchange market were effectively managed by timely measures including the forex swap facility for banks and oil companies, their gradual withdrawal and the calibrated normalization of the interest rate corridor helped restore stability to the financial markets.

- In order to rebuild buffers in the face of uncertainty regarding the global interest rate cycle and financial conditions, the Reserve Bank offered a forex swap window for banks’ overseas borrowing and nonresident deposit (FCNR(B)) funds, resulting in capital inflows in excess of US$ 34 billion through the swap facility.

Fig 23 : Indian INR Vs USD

Fig 24 : Indian Capital Deficit

Fig 25 : Global Crude oil prices

EGMP-38 – Macroeconomics Assignment

Impact to Exchange rate

- Foreign exchange reserves were coming down

due to rising fuel prices in world trade.

- Inflation in India also added worry reducing

aggregate demand of commodities

- Interest rates from the central bank was also

high which – not creating an environment to

boost aggregate demand

- FCNR not only proved to be timely in strengthening external resilience but also helped in easing domestic liquidity significantly.

- FCNR deposits are expected to get matured in

Sep’2016 which amounts is approx. 30 BiO USD.

- Deposits will be debited back in the currency

payed by the depositors at the time opening the

account.

- Outflow of capital from the deposits could

impact three segments - spot markets, forward

markets and money markets.

- Outflow of capital could further depreciate

Rupee against USD (70 Rs/$)

- Depreciation of Rupee means that we have to

spend more for the same quantity of items

purchased in the market.

- Imports will become dearer causing further

increase in CAD.

- Increase in commodity prices means that the

aggregate demand will reduce which could

cause economic slowdown.

Fig 26 : India foreign exchange reserves

Fig 27 : Forecast Impact on exchange rate

EGMP-38 – Macroeconomics Assignment

Impact to Economy

Solutions & Opportunities

- Reduction in the liquidity in the system will

result in Inflation which causes reduction of

demand due to increased prices of commodity.

- Reduction in aggregated demand causes

reduction in production which caused reduced

output from manufacturing sectors.

- Reduced output results in layoff of employees

(or) salary cuts which results in further

reduction in demand.

- Pay cuts (or) Layoffs magnitudes reduction in

demand resulting in prices falling causing

deflation.

- Manufacturers will not like to manufacture

products in an economy with deflation.

- Economic slowdown becomes recession which if

not solved could result in depression.

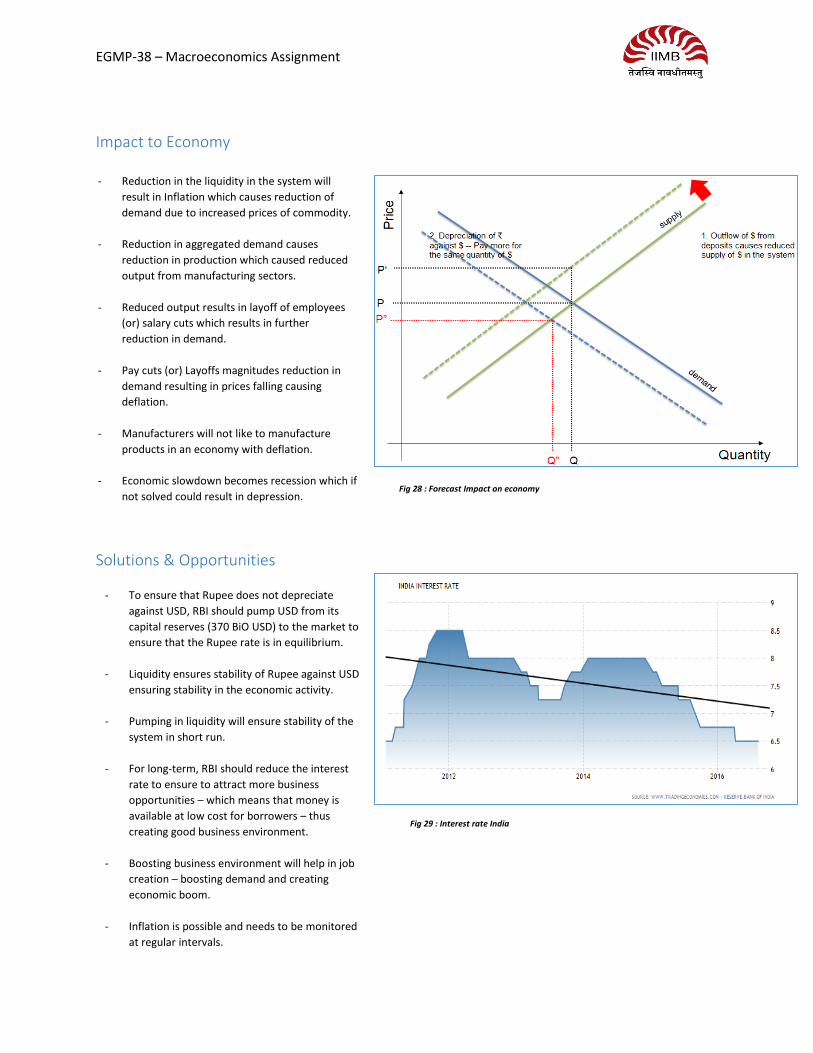

- To ensure that Rupee does not depreciate

against USD, RBI should pump USD from its

capital reserves (370 BiO USD) to the market to

ensure that the Rupee rate is in equilibrium.

- Liquidity ensures stability of Rupee against USD

ensuring stability in the economic activity.

- Pumping in liquidity will ensure stability of the

system in short run.

- For long-term, RBI should reduce the interest

rate to ensure to attract more business

opportunities – which means that money is

available at low cost for borrowers – thus

creating good business environment.

- Boosting business environment will help in job

creation – boosting demand and creating

economic boom.

- Inflation is possible and needs to be monitored

at regular intervals.

Fig 28 : Forecast Impact on economy

Fig 29 : Interest rate India

EGMP-38 – Macroeconomics Assignment

Articles from Newspaper

Fig 30 : Article on FCNR account in ToI dated 13th Aug 2016

EGMP-38 – Macroeconomics Assignment

Write a short note on NPA’s in the banking sector and transmission of

monetary policy?

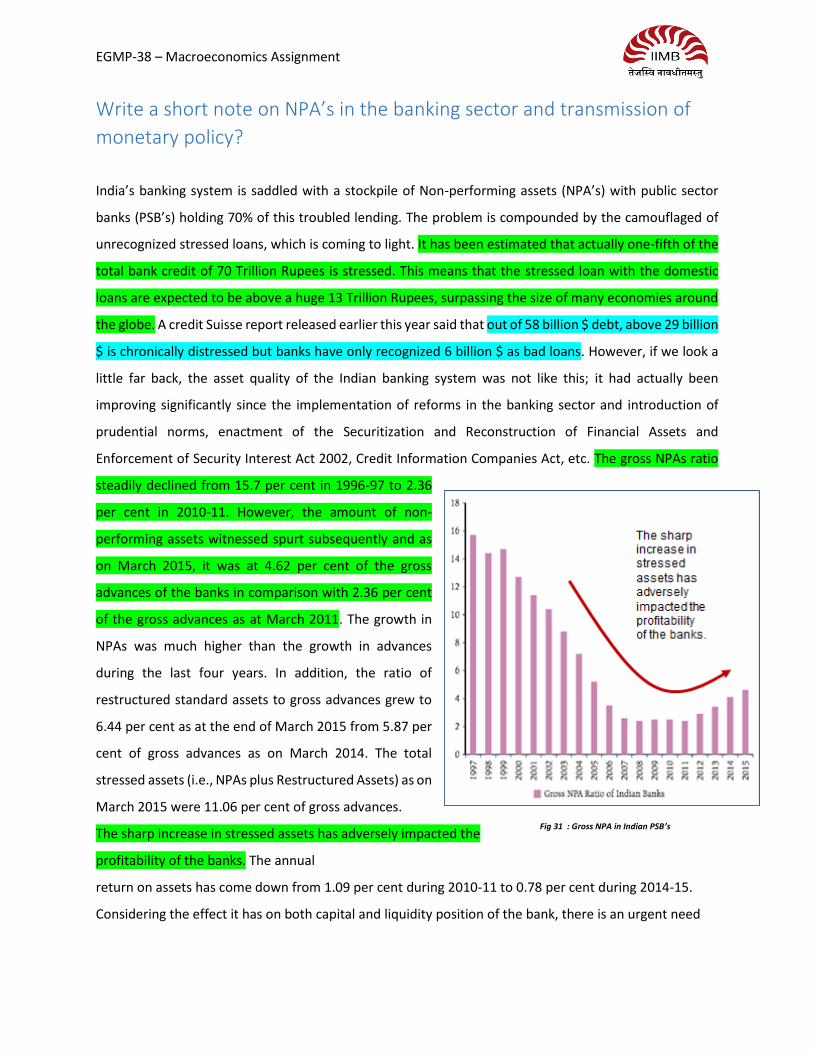

India’s banking system is saddled with a stockpile of Non-performing assets (NPA’s) with public sector

banks (PSB’s) holding 70% of this troubled lending. The problem is compounded by the camouflaged of

unrecognized stressed loans, which is coming to light. It has been estimated that actually one-fifth of the

total bank credit of 70 Trillion Rupees is stressed. This means that the stressed loan with the domestic

loans are expected to be above a huge 13 Trillion Rupees, surpassing the size of many economies around

the globe. A credit Suisse report released earlier this year said that out of 58 billion $ debt, above 29 billion

$ is chronically distressed but banks have only recognized 6 billion $ as bad loans. However, if we look a

little far back, the asset quality of the Indian banking system was not like this; it had actually been

improving significantly since the implementation of reforms in the banking sector and introduction of

prudential norms, enactment of the Securitization and Reconstruction of Financial Assets and

Enforcement of Security Interest Act 2002, Credit Information Companies Act, etc. The gross NPAs ratio

steadily declined from 15.7 per cent in 1996-97 to 2.36

per cent in 2010-11. However, the amount of non-

performing assets witnessed spurt subsequently and as

on March 2015, it was at 4.62 per cent of the gross

advances of the banks in comparison with 2.36 per cent

of the gross advances as at March 2011. The growth in

NPAs was much higher than the growth in advances

during the last four years. In addition, the ratio of

restructured standard assets to gross advances grew to

6.44 per cent as at the end of March 2015 from 5.87 per

cent of gross advances as on March 2014. The total

stressed assets (i.e., NPAs plus Restructured Assets) as on

March 2015 were 11.06 per cent of gross advances.

The sharp increase in stressed assets has adversely impacted the

profitability of the banks. The annual

return on assets has come down from 1.09 per cent during 2010-11 to 0.78 per cent during 2014-15.

Considering the effect it has on both capital and liquidity position of the bank, there is an urgent need

Fig 31 : Gross NPA in Indian PSB’s

EGMP-38 – Macroeconomics Assignment

for banks to reduce their stressed assets and clean up their balance sheets lest they become a drag on

the economy. The International Monetary fund has come out with a more conservative figure: Bad loans

made up around 5.9% of the total loans in

India. Even that’s more than twice as much

as the country with the second highest

amount of NPA’s – Thailand at 2.7%, China

which is often cited for its bad-debt

problems, has an NPA percentage of only

1.5%. Managing asset quality is always very

important and becomes a prominent

objective especially during a period of

economic downturn. Recognizing the

importance of effective asset quality

management, Reserve Bank has issued various guidelines

to banks, from time to time, on various aspects of asset quality management. At least three public

sector banks (PSBs), Central Bank of India, Allahabad Bank and Dena Bank posted huge losses in the

October-December quarter on account of a sharp increase in bad loans, while Punjab National Bank

(PNB), India’s second largest state-run bank, logged a significant fall in its profit. Bad loans are loans,

where recovery is overdue more than 90 days. PNB reported gross non-performing assets (NPAs) of 8.47

per cent for the December-quarter. This is the highest level of bad loans the bank has recorded at least

in 11 years. Central Bank of India logged a loss of INR 836.62 crore for October-December 2015-16,

against a profit of INR 137.65 crore in the third quarter of the previous fiscal with its GNPAs rising to

8.95 % of the gross advances during the quarter, as against 6.2 % year ago.

Fig 32 : Performance of Indian PSB’s

EGMP-38 – Macroeconomics Assignment

How did the problem worsen?

The NPAs on bank balance sheets didn’t happen overnight. There is a mix of factors including laxity in

apprising creditworthiness of a borrower for years on end, government’s directed lending through state-

run banks, using state-run banks for the

roll out of government’s populist schemes

and the misuse of banking system by

politically connected crony promoters to

their advantage. What we see today is a

result of all this. When banks went on a

lending spree in 2010-2013 period, the

assumption was there will be a sharp

economic recovery that will justify their

actions. But, that recovery hasn’t

happened yet, putting a whole lot of loans

at risk. In a recent article, it wouldn’t be an

exaggeration if one says that India’s state-run banks are on the

verge of a crisis. Over 90 per cent of the total bad loans of Indian banks (currently stands over INR 3,

00,000 crore) is on the balance sheets of these entities. Their restructured loan portfolio would be

nearly double this amount, if one goes by industry estimates. These two categories together, termed as

stressed assets, would constitute around 11-12 per cent of the total bank loans given.

Also, there is a risk of existing restructure loans turning bad if economy doesn’t do well as expected.

Many loans, especially in infrastructure sector, which bank conveniently pushed to the restructured

basket to avoid turning bad loans, might return to haunt in that case. This is one reason why RBI

governor, Raghuram Rajan, stipulated a deadline of March, 2017 for banks to clean up their bad loans

and state the problem today and do not postpone for tomorrow.

Though the Reserve Bank of India (RBI) and the finance ministry have consistently maintained that bad

loans in Indian banking system is not at an alarming level, the stress that is emerging from bank balance

sheets, especially that of state-run banks, is indeed a serious problem for finance minister, considering

Fig 33 : Gross NPA in %

EGMP-38 – Macroeconomics Assignment

its multiple implications on requirement of capital and banks’ ability to further lend that is critical for

economic growth.

Burden on the fiscal System

In turn, this would make allocation of capital to state-run banks a complex process for finance minister,

who has so far allocated Rs70,000 crore for state-run banks and has asked them to find funds from the

market for about Rs1.1 lakh crore. The consensus estimate of capital these banks would require in the

year to 2019 is at least Rs2.4 lakh crore when the Basel-III norms will take effect. Also, the capital

requirement can change if bad loans shoot up beyond estimates. For every Rs100 loan, banks need to

set aside Rs 15 if the loan turns bad.

The government, which owns majority stake in these banks, will have to work out ways to face this

‘capital’ shock in the years ahead or, at least, let these banks go private and fend for themselves. One

thing is sure.

Transmission of monetary policy

Transmission of monetary policy speaks about how central bank’s interest rate decision affect the

economy and inflation. The central bank conducts monetary policy to promote economic stability and

growth in the economy, experience has shown that the best way to achieve economic stability and

growth is by keeping inflation low, stable and predictable to ensure that the people save and invest with

confidence. The policy interest rate is the main tool to keep inflation on target. The central bank usually

changes this key interest rate 8 times a year and there are lot of factors considered to decide on changes

in the interest rate. A lot of research goes into the decision of changing the interest rate. The central

bank analyzes the economic developments and use forecasting models to determine the appropriate

interest rate to keep inflation rate in target. The economic projections are important as it takes time for

changes in policy interest rate to affect inflation, in deciding the policy interest rate for today, the

central bank has to look ahead the rate of inflation in the future. In order to keep inflation close to the

target, the central bank tries to keep the overall demand in balance with the overall supply.

EGMP-38 – Macroeconomics Assignment

Let’s consider an economy as illustrated in the

fig-34 where the overall supply balances the

overall demand ensuring that the it meets the

inflation target set by the central bank (in this

scenario 2.5 %), based on the future inflation

prediction the central bank has not changed the

policy interest rate (in this scenario 4%). The

central bank will try to forecast the future

inflation rate based on the supply and demand

scenario the policy interest rate

Fig-34 – Illustrated Scenario of an Economy

Let’s consider a scenario where due to some

activities in the economy the overall demand

within an economy exceeds compared to the

overall supply as represented in fig 35, this

causes raise in the inflation above the target set

by the central bank. In such a scenario, the

central bank increases the policy interest rate

and observes the changes in the inflation rate.

The increase in the interest rate makes money

borrowing expensive on both

consumer/business loans and dampens

spending and investment – but also raises

interest rate on bank deposits promoting

savings.

Fig-35 – Changes in the Policy interest rate due to increase Inflation in an

economy

EGMP-38 – Macroeconomics Assignment

Raising policy interest rate ensures that the

overall demand balances with the overall

supply in the long run thus bringing back

inflation on target as represented in fig 37. The

calibration of increase policy interest rate

continues by the central bank until the inflation

rate reaches the inflation target set by the

central bank. This is how the transmission of

monetary policy works in an economy with

growing inflation pressure.

Fig-36 – Appropriate level of increase in the policy interest rate brings back

inflation to target

Fig-38 – Changes in the Policy interest rate due to decrease of Inflation in an

economy

Let’s see how central bank transmission of

policy works when the overall supply of an

economy exceeds the overall demand of an

economy as illustrated in fig-38. Since the

overall supply exceeds the overall demand,

prices of commodities / products fall down

causing decreasing inflation below the target. In

order to balance the overall demand and

supply, the central bank will decrease policy

interest rate to an appropriate level – which

promotes investment and spending and

boosting overall demand.

EGMP-38 – Macroeconomics Assignment

Decreasing policy interest rate ensures that the

overall demand balances with the overall

supply in the long run thus bringing back

inflation on target as represented in fig 39. The

calibration of decrease policy interest rate

continues by the central bank until the inflation

rate reaches the inflation target set by the

central bank. This is how the transmission of

monetary policy works in an economy with

where supply exceeds demand.

Fig-39 – Appropriate level of increase in the policy interest rate brings back

inflation to target

While commercial interest rate are the most important means how the change in the bank’s policy rate

affects inflation rate, there is also another channels of how the change in the policy can affect the

inflation rate – which is the exchange rate. Raise in Indian interest rates compared to rates of other

countries boosts the Indian rupee compared to other global currencies which overtime makes imported

goods for Indian economy cheaper and exports of Indian goods more expensive to other expensive in

foreign market – this causes reduced demand of Indian goods in the market causing damper on

inflation. Drop of Indian interest rates compared to rates of other countries causes opposite affect – it

boosts demand in the economy and raising inflation. Occasionally when an economy is faced with major

shock (like global economic crisis 2008-2009), banks have flexibility to return inflation to target on

shorter (or) longer time frame.