Embed Size (px)

Citation preview

1

M&A Accounting and Firm Valuation Paul Healy

Harvard Business School

Introduction

For many companies, mergers and acquisitions are important investments

that are sources of growth and transformation. In 2014 alone, their global value

amounted to $3.2 trillion. Many of these deals are “bet the farm” investments for

acquirers with potential to transform their firms and even their industries. But prior

research indicates many fail to add value for acquiring shareholders (see Healy,

Palepu and Ruback, 1997). Given their economic significance, it is important that

M&A reporting standards provide timely information on which acquisitions have

added value and which have not.

Pooling of interests accounting failed to meet this objective. It valued an

acquisition at its book value reported on the target firm's books prior to the

acquisition. This made it challenging for investors to compare the post-acquisition

earnings generated by the combined firm with the actual cost of the net assets

acquired. In contrast, by recognizing the cost of assets acquired at their fair values

at the date of acquisition, purchase accounting enables investors to judge whether

the net assets acquired have generated an attractive book return.

Yet purchase accounting raises a number of important questions for standard

setters. How should the difference between the purchase price of the business and

the fair value of separable tangible net assets be reported? Should the acquirer be

required to separately value identifiable intangibles, such as brands and in-process

R&D for the target? Should goodwill (the residual) be allocated across divisions?

2

Should intangible assets be amortized after an acquisition, or should they be

retained at cost and subject to an impairment test?

FAS 141 eliminated the pooling option and required that all combinations be

accounted for under the purchase (or acquisition) method, with identifiable

intangibles acquired reported at their fair values at date of purchase. Identifiable

intangibles with finite lives, such as patents and copyrights, are amortized over their

useful lives unless they are deemed impaired, in which event they are written down

to their estimated fair value. In contrast, identifiable intangibles with indefinite lives

are reported at fair value at date of purchase and subject to an annual impairment

test. Any residual value, which reflects the value of intangibles that cannot be

separately identified, is recorded as goodwill and allocated across firms’ business

units. FAS 142 required that, since it has an indefinite life, goodwill is not amortized

but subject to regular impairment tests.

Advocates for current M&A rules argue that they provide investors with

information needed to judge whether an acquisition has been successful on a timely

basis. Opponents counter that these rules provide managers with too much latitude

in reporting for difficult to value intangibles. They note that given the evidence that

many acquisitions fail to add value for acquiring shareholders, much of the goodwill

reported is bad will and that managers have incentives to fail to recognize these

losses on a timely basis (see Holthausen and Watts, 2001; Watts, 2003).

Considerable evidence has been compiled in the academic literature on the

impact of merger accounting standards. The findings suggest that impairment

charges under FAS 142 provide new information to investors (Chambers, 2007;

3

Chen, Kohlbeck and Warfield, 2008; Bens, Heltzer and Segal, 2011; and Li, Shroff,

Venkataraman and Zhang, 2011). However, there is also evidence that managers

take advantage of the judgment provided them under the latest accounting

standards to: (a) overstate goodwill, which since it is unamortized increases future

earnings (see Shalev, Zhang and Zhang, 2013; and Paugam, Astolfi and Ramond,

2015), and (b) delay recognizing impairments on intangibles, leading stocks to be

temporarily be mispriced (Ramanna and Watts, 2012; Li and Sloan, 2015).

In this paper I revisit questions on M&A accounting using data for one of the

largest acquisitions in history, the Time Warner acquisition of AOL. The acquisition

was widely viewed as one of the worst in history, providing ample opportunity to

better understand at a micro level how the acquisition was initially reported, when

impairment tests were reported, and how the market interpreted the reporting. In

the spirit of the conference, given this field evidence, I conclude with some

reflections on accounting research and M&A reporting standards.

M&A Accounting and AOL’s Acquisition of Time Warner

On January 10 2000, AOL announced the acquisition of Time Warner for

$162 billion. Despite revenues of only $4.8 billion, dwarfed by Time Warner’s $27.3

billion, AOL’s high stock valuation enabled its shareholders to end up owning 55%

of the combined company and Time Warner (TW) shareholders 45%.

TW had itself been forged out of the mergers of Warner Bros. movie studio

(which included HBO and Cinemax), Time magazine and its publishing business, and

Ted Turner’s TBS cable company (which included CNN). AOL, an internet service

4

provider, was itself no stranger to acquisitions having acquired Netscape and its

largest competitor, Compuserve.

The acquisition was intended to allow AOL to transition from being a pure

internet service provider into a media and entertainment giant. In anticipation of

the growth of broadband access to online content, AOL had sought access to the new

technology via deals with telecommunications, cable and satellite companies so that

it could provide its subscribers with faster access to the internet than phone lines.

The acquisition of TW was seen as a way to accelerate this process. In addition,

AOL‘s 22 million subscribers could be used to leverage TW’s television, movie, and

publishing content. The deal was also attractive to TW since it had unsuccessfully

sought to enter the online market to leverage its content.

In reflecting on the combination fifteen years later, McGrath (2015)

explained that at the time, “a lot of people thought that the merger was a brilliant

move and worried that their own companies would be left behind. … The whole

thing was “transformative”. Had [the] initial assumptions been borne out, we might

be talking today about what a visionary deal it was.”

Of course, with the benefit of hindsight, the deal is now seen as one of the

more spectacular merger failures in history. McGrath explained the problems.

Merging the cultures of the combined companies was problematic from the get go. Certainly the lawyers and professionals involved with the merger did the conventional due diligence on the numbers. What also needed to happen, and evidently didn’t, was due diligence on the culture. The aggressive and, many said, arrogant AOL people “horrified” the more staid and corporate Time Warner side. Cooperation and promised synergies failed to materialize as mutual disrespect came to color their relationships.

A few scant months after the deal closed, the dot com bubble burst and the economy went into recession. Advertising dollars evaporated, and AOL was

5

forced to take a goodwill write-off of nearly $99 billion in 2002, an astonishing sum that shook even the business-hardened writers of the Wall Street Journal. AOL was also losing subscribers and subscription revenue. The total value of AOL stock subsequently went from $226 billion to about $20 billion.

The acquisition is also noteworthy because it was one of the first to adopt

FAS 141 and 142. Given the visibility and intensive scrutiny of the acquisition, it

makes a potentially useful field study to investigate how the standards were

implemented and whether they provided timely information on the merged firm’s

performance.

Valuation of Intangibles

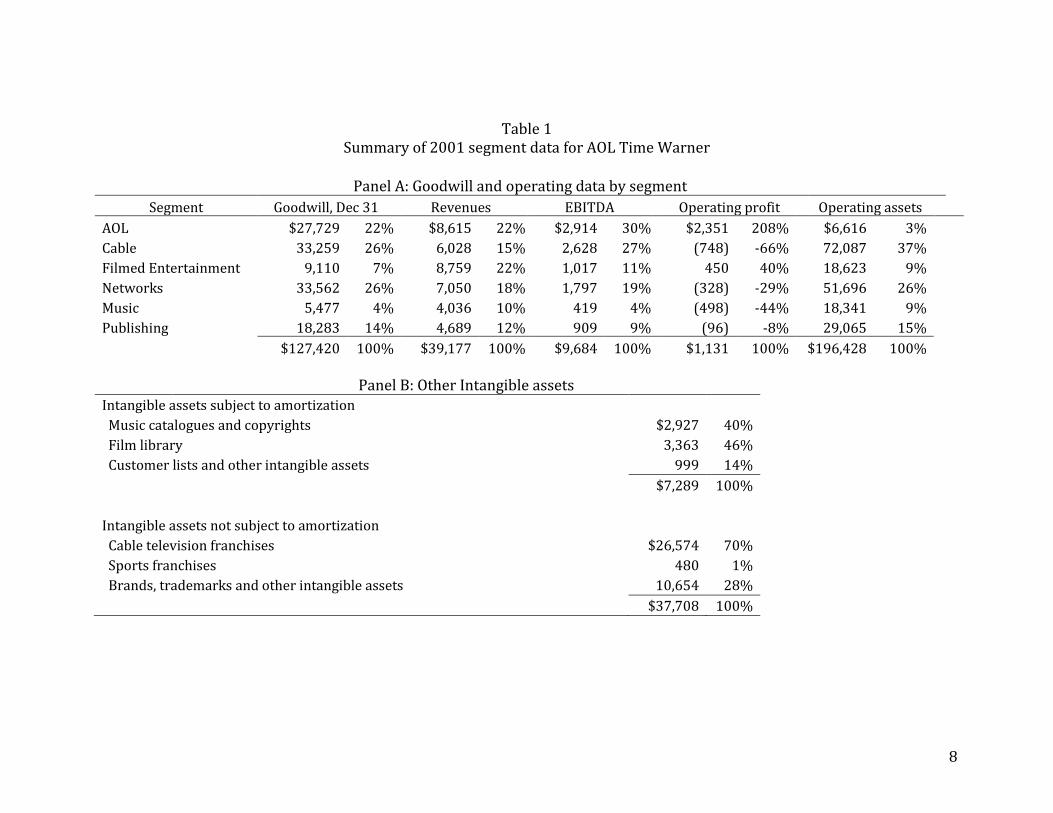

As reported in Table 1, AOL Time Warner recognized $7.3 billion on

intangible assets subject to amortization (primarily for TW’s music and film rights)

and $37.7 billion for intangibles not subject to amortization (notably TW’s cable and

sports franchises, and brands and trademarks). These assets reflected the stand-

alone value of TW’s identifiable intangibles. On its December 31, 1999 balance

sheet, TW valued its music and film right intangibles at $0.8 billion, and the cable

television and sports franchise intangibles at $8.5 billion, indicating under

acquisitions accounting AOL Time Warner was able to revalue these assets

significantly.

In addition, AOL Time Warner reported goodwill for $127.4 billion. This

reflected (a) the pre-acquisition value of goodwill for TW as a stand-alone business

(since TW alone was worth than the sum of its parts); (b) the incremental value of

goodwill arising as a result of the merger, presumably reflecting expected merger

synergies; and (c) any overpayment by AOL made to acquire TW. Prior to the

6

acquisition, on December 31, 1999, TW had reported goodwill of $15.5 billion.

However, the standalone value of TW’s goodwill would have been substantially

higher than this amount. How much, though, is unclear.

After the acquisition was completed, as required by FAS 141, AOL Time

Warner allocated goodwill across its business segments. The allocation, reported in

Table 1, apportions the majority of the goodwill to the AOL, cable and networks

segments. What is less clear, however, is how one would make such an allocation.

After all, goodwill represents the value of assets that cannot be separately identified;

it depends on the interactions between the segments that generate value for the

firm.

As noted above, some of this goodwill arises from the pre-acquisition value of

TW’s goodwill, which reflects any synergies between its business units prior to

combining with AOL. For example, there may be synergies between the cable and

film businesses, which were also brought together under a merger. Yet it is not

straightforward to allocate any such goodwill between these units. I suspect that it

would have been useful to investors to understand how much of the $127 billion of

goodwill reported by AOL Time Warner represented its valuation of goodwill for

TW as a stand-alone business.

The second goodwill component arises from any projected synergies for the

combination of AOL and TW. At the time of the acquisition, industry experts argued

that the merged firm could generate synergies by using AOL’s network of

subscribers to leverage Time Warner’s cable and entertainment businesses, and by

providing AOL’s subscribers with faster broadband access to the internet. But if

7

such is the case, it is unclear whether the related goodwill should be attributed to

the AOL business segment, to the Cable, or to the Entertainment segments. If these

business units were strictly independent, it would be straightforward to separately

estimate the value of goodwill for each. But given the businesses were combined

precisely because management expected that they would create synergies, leading

the whole to exceed the sum of the parts, any such allocation seems arbitrary.

Intangible Impairment

FAS 142 requires that goodwill be carried on the books at its fair value at

purchase, and not subject to periodic amortization. Instead, each year its current

assessed fair value is compared to its book value to decide whether an impairment

charge should be recorded. In contrast, under the former standard, FAS 121,

impairments were recognized when the undiscounted estimated future cash flows

attributable to goodwill fell below book value, a less stringent standard that the

FASB recognized might happen rarely for an indefinite lived asset.

AOL Time Warner’s goodwill was materially impacted by the new standard

for impairment. In early 2002, the company reported that as a result of applying the

fair value benchmark for write-downs under FAS 142, rather than the undiscounted

cash flow benchmark, it would have to write down goodwill by $54.2 billion. As

reported in Table 2, this charge was taken against the goodwill allocations to TW

business units. Consistent with the findings of Beatty and Weber (2006), AOL Time

Warner opted to report the impact of the adoption of FAS 142 by showing the

impairment charge as the effect of an accounting change, reported “below the line”.

8

Table 1 Summary of 2001 segment data for AOL Time Warner

Panel A: Goodwill and operating data by segment

Segment Goodwill, Dec 31 Revenues EBITDA Operating profit Operating assets

AOL $27,729 22% $8,615 22% $2,914 30% $2,351 208% $6,616 3%

Cable 33,259 26% 6,028 15% 2,628 27% (748) -66% 72,087 37%

Filmed Entertainment 9,110 7% 8,759 22% 1,017 11% 450 40% 18,623 9%

Networks 33,562 26% 7,050 18% 1,797 19% (328) -29% 51,696 26%

Music 5,477 4% 4,036 10% 419 4% (498) -44% 18,341 9%

Publishing 18,283 14% 4,689 12% 909 9% (96) -8% 29,065 15%

$127,420 100% $39,177 100% $9,684 100% $1,131 100% $196,428 100%

Panel B: Other Intangible assets

Intangible assets subject to amortization Music catalogues and copyrights $2,927 40%

Film library 3,363 46%

Customer lists and other intangible assets 999 14%

$7,289 100%

Intangible assets not subject to amortization

Cable television franchises $26,574 70%

Sports franchises 480 1%

Brands, trademarks and other intangible assets 10,654 28%

$37,708 100%

9

Table 2 Changes in AOL Time Warner goodwill in 2002

Dec. 31, 2001 Additions

Impact of accounting

change

Fourth quarter

impairment Dec. 31,

2002

AOL $27,729 $8,536 $0 $(33,489) $2,776 Cable 33,259 267 (22,976) (10,550) 0 Filmed Entertainment 9,110 (71) (4,091) 0 4,948 Networks 33,562 (4) (13,077) 0 20,481 Music 5,477 (35) (4,796) (646) 0 Publishing 18,283 (243) (9,259) 0 8,781

$127,420 $8,803 $(54,199) $(44,685) $36,986

In addition, at the end of the fourth quarter, AOL Time Warner announced

that it would have to take a further $44.7 billion charge for goodwill impairment,

primarily against the AOL unit’s allocation. These impairments ($98.9 billion)

resulted in the complete write-down of goodwill in the cable and music businesses,

and reduced goodwill for the AOL unit by 93%.

Given the challenges in valuing the goodwill for each business unit, one has

to wonder how these impairment allocations were generated. Why did the $54.2

billion impairment affect only the allocations to TW’s segments and not those of

AOL, particularly given concerns about the decline in the online subscription

business with the collapse of the dot com market? Consistent with this concern, the

company’s 2002 performance, reported in table 3, showed a 38% decline in EBITDA

for the AOL business unit, whereas the cable unit grew by 5% and Networks by

13%.

10

Table 3 Segment revenues and EBITDA for AOL Time Warner in 2002

Revenues EBITDA

2001 2002

Percent change 2001 2002

Percent change

AOL $8,615 $ 9,094 6% $2,914 $1,798 -38% Cable 6,028 7,035 17% 2,628 2,766 5% Filmed Entertainment 8,759 10,040 15% 1,017 1,232 21% Networks 7,050 7,655 9% 1,797 2,032 13% Music 4,036 4,205 4% 419 482 15% Publishing 4,689 5,422 16% 909 1,155 27%

$39,177 $43,451

$9,684 $9,465

Timeliness of Impairments

How timely were AOL Time Warner’s impairments? To help answer this

question, I conducted three analyses. The first examined stock price changes around

the public announcements by the company of the impairments. The second

examined the performance of AOL Time Warner subsequent to the impairments to

determine whether its reported book returns exceeded its cost of capital. And the

third examined the timing of the impairments relative to changes in the value of the

company’s stock.

AOL Time Warner’s public announcements of the impairment charges were

made on January 7, 2002 (when it disclosed that the new accounting standard

would require an impairment of between $40 billion and $60 billion), April 24, 2002

(when it reported the actual impairment under the accounting change of $54.2

billion), and January 29, 2003 (when it reported the additional $44.7 billion

impairment).

11

The market reactions to the first two announcements were 0.2% and 2.0%

respectively (versus -0.2% and -1.0% for the Nasdaq index), suggesting that the

market had either anticipated the impact of the accounting change/impairment or

did not view it as economically significant. Only the announcement of the $44.7

additional impairment elicited much reaction, with the company’s stock dropping

12.1% (versus -1.5% for the Nasdaq), reflecting negative news conveyed by the

impairment charge and AOL Time Warner’s revenue and operating earnings news.

Relative to the fourth quarter of 2001, AOL Time Warner’s Q4 2002 revenues

declined by 25% and its operating earnings by 52%.

If the impairment charges taken by AOL Time Warner represented an

unbiased assessment of the decline in fair value of aggregate goodwill, one might

anticipate that in subsequent years the company would be able to earn a book

return on assets that at least equaled its cost of capital. Table 4 reports book returns

on beginning net operating assets from 2002 to 2009, the year the AOL business

was spun off. Despite the large goodwill impairment charge in 2002, AOL Time

Warner reported ROAs ranging from -15.4% to 6.2%, with an average of 0.4%. After

excluding 2008, when the company took another large impairment, the average ROA

was only 3%, consistently lower than any plausible cost of capital. AOL Time

Warner, therefore, continued to underperform following the large impairment in

2002, indicating that its assets (and intangibles in particular) continued to be

overvalued.

In 2008, AOL Time Warner formally recognized that its intangible assets

were overvalued, and took a $2.2 billion impairment on AOL goodwill, a $7.1 billion

12

charge for the impairment of publishing goodwill and identifiable intangible assets,

and a $14.8 billion impairment of cable franchise rights. The impairment of the cable

franchise is noteworthy because its value reflected the revaluation at the time of the

AOL deal.

Table 4 Operating ROA for AOL Time Warner

ROA

Intangible assets Total net

operating assets 2001 -135.2% 169,058 177,783 2002 -56.5% 81,192 83,644 2003 1.6% 83,639 85,644 2004 2.7% 83,215 83,871 2005 2.4% 83,940 84,609 2006 6.2% 92,903 98,147 2007 2.9% 91,692 98,772 2008 -15.4% 68,278 79,008 2009 2.2% 38,935 44,927

ROA is defined as net operating profit after tax divided by beginning of year net operating assets. Net operating profit after tax is net income plus the after-tax cost of net interest. Net operating assets are working capital plus long-term assets less non-interest bearing long term debt.

To further examine the timeliness of the 2008 intangible impairment I

examine the market valuation of AOL Time Warner. Table 5 reports quarterly

multiples of the company’s enterprise value (EV) to book capital,1 intangible assets,

and intangible assets to book capital from 2001/Q1 (when the merger was first

reported) to 2009/Q4. Throughout this period, intangibles ranged from 80-95% of

total capital, signifying their economic significance. The EV-book capital multiple fell

below one in the fourth quarter of 2001, suggesting that the market perceived that

the company’s intangibles were impaired. AOL Time Warner implicitly

1 Enterprise value is the market capitalization of equity plus the book value of net debt. Book capital is the book value of equity plus net debt.

13

acknowledged this one year later (2002/Q4) when it took the $44.6 billion write-off.

The EV-book capital multiple remained above one until the fourth quarter of 2007,

when it fell to 0.99, and declined steadily throughout 2008. This appeared to prompt

the third significant impairment of $25.1 billion. However, even this appears to have

been insufficient, since the multiple continued to be less than one until the first

quarter of 2012.

Overall, AOL Time Warner’s recognition and impairment of intangibles maps

into many of the findings in the academic literature. The company initially took a

significant $55 billion impairment as a result of the change in accounting standards,

reporting the change below the line. This announcement met with little market

response. In contrast, the fourth quarter 2002 impairment of $44.6 billion,

presumably in response to the decline in AOL’s subscriber base, was accompanied

by a material 12% drop in stock price, signifying that either the impairment and/or

declines in quarterly revenues and operating earnings were surprises to investors.

Finally, there is also evidence consistent with the company delaying further

write-downs despite reporting ROAs well below the cost of capital for five

consecutive years. In 2008, after one year of EC-book capital multiples below one, it

opted to take another write-down for $25.1 billion, but even this appears to be too

little to late, since the multiple continued to be well below one.

14

Table 4 History of AOL Time Warner valuation and intangibles

Yr/Qtr EV/ Book capital

multiple Intangibles Intangibles as % book

capital 2001/1 1.37 169,503 94.1% 2001/2 1.10 167,939 93.3% 2001/3 1.08 167,898 94.0% 2001/4 0.75 169,058 94.7% 2002/1 0.83 125,325 95.8% 2002/2 0.62 125,262 95.7% 2002/3 0.76 127,150 96.9% 2002/4 0.96 81,192 95.1% 2003/1 1.07 87,096 95.9% 2003/2 1.15 86,370 98.6% 2003/3 1.17 86,657 98.6% 2003/4 1.17 83,639 94.3% 2004/1 1.14 83,222 93.6% 2004/2 1.13 83,170 93.0% 2004/3 1.11 83,552 92.9% 2004/4 1.15 83,215 92.3% 2005/1 1.11 83,226 91.5% 2005/2 1.12 83,132 93.6% 2005/3 1.14 83,545 93.4% 2005/4 1.12 83,940 94.5% 2006/1 1.10 83,464 94.4% 2006/2 1.08 84,428 95.0% 2006/3 1.16 93,046 93.6% 2006/4 1.21 92,903 93.2% 2007/1 1.18 93,100 93.5% 2007/2 1.09 93,264 93.6% 2007/3 1.04 93,431 93.6% 2007/4 0.99 91,692 91.4% 2008/1 0.93 94,081 94.5% 2008/2 0.89 94,836 91.3% 2008/3 0.73 94,570 92.0% 2008/4 0.74 68,278 79.7% 2009/1 0.69 43,572 80.8% 2009/2 0.78 43,390 80.3% 2009/3 0.85 41,422 76.7% 2009/4 0.91 38,935 79.2%

15

Discussion and Summary

So what can we learn from the accounting for the AOL Time Warner merger?

First, it reinforces the view that acquisitions are high-risk undertakings. Large

acquisitions can be particularly challenging to implement successfully. Planned

synergies can fail to materialize for a variety of reasons - conflicts in corporate

cultures, changing technologies that threaten industry leaders, responses of

competitors, etc. As a result, goodwill and the other intangible assets reported as a

result of an acquisition are highly risky and likely to trigger subsequent impairment

tests.

Second, the practice of decomposing goodwill into business unit allocations,

required by FAS 141, seems arbitrary given goodwill reflects the synergies from

combining the firm’s identifiable assets, and is not by itself a separable asset. For

AOL Time Warner, synergies could arise from combining AOL’s subscriber business

with TW’s cable and entertainment business, but it is difficult to identify which

particular unit generated the goodwill. In addition, stand-alone goodwill for TW

reflects synergies between its various business units. But again, the allocation of

goodwill from these sources to individual business units seems arbitrary.

Instead, it might be more useful for merging companies to report the share of

goodwill applicable to the target as a stand-alone entity, and the portion attributable

to projected synergies in the two businesses. The relative magnitude of these

amounts would allow financial statement users to better understand the risks from

an acquisition – either in realizing the projected synergies or in the assessing

whether the target was fairly valued as a stand-alone business. Given the difficulty

16

in separating these components after the merger has occurred, I suspect that it

makes little sense to track these allocations over time and to assign impairments to

specific mergers and these two goodwill components. Although, some companies do

track actual merger synergies over time to understand successes and failures of

merger investments.

Third, goodwill impairments are unlikely to be timely events. Stock markets

can respond quickly to new information on a firm’s prospects, whereas accountants

typically revalue intangibles once a year. As a result, investors are likely to

anticipate that intangible assets are impaired prior to their being reported by

management. Impairments are likely to confirm that reported poor performance is

due to failures to achieve anticipated merger synergies or from overpayment for the

target, rather than deteriorations in the acquiring firm’s business. As such they help

financial statements to reflect differences between successful and failed

acquisitions. But they may not provide much new information to financial markets

relative to more timely quarterly revenues and earnings that are used as inputs to

judge whether impairments are called for.

Fourth, the failure to impair intangibles after sustained poor performance, as

was the case for AOL Time Warner, is one indicator that managers are reluctant to

recognize the acquisition’s failure. Concern about such delays lead some to advocate

for systematically amortizing goodwill (also with impairment tests). This would

have forced AOL Time Warner to write-down its goodwill and identifiable

intangibles with indefinite lives between 2002 and 2008. Such a policy may be more

conservative, but it is difficult to understand how a mechanical write-down of

17

intangibles provides information that helps financial statements to reflect

differences between successful and failed acquisitions.

Proponents of amortization argue that, like fixed assets, intangibles get used

up over time and it is important to recognize their use as an expense. However,

there is an important distinction between fixed assets and intangibles. New fixed

asset outlays are reported as an asset, whereas outlays to preserve or enhance

intangibles, such as advertising or R&D, are typically expensed. As a result,

amortizing intangibles and simultaneously expensing outlays that preserve or grow

their value effectively double counts their expense. Unless we decide to permit the

capitalization of outlays that preserve and grow goodwill, which I would not

advocate, the current system will inevitably lead to an inconsistency in the reporting

of outlays for fixed assets and goodwill.

Fifth, although research findings demonstrate that managers exercise

judgment to delay impairments under FAS 142, it is worth remembering that

management exercised considerable judgment under the prior standards. They

could groom an acquisition to meet criteria for pooling of interests, which

eliminated the risk of having to recognize goodwill impairments from merger

failures. And managers of firms that used purchase accounting were subject to a less

stringent impairment test and could exercise considerable reporting judgment to

reduce the risk of impairments even when acquisitions had failed. Would AOL Time

Warner’s financial statements have reflected the merger’s failure on a more timely

basis had pooling been used? Or had purchase accounting been used but a less

stringent impairment test and management judgment were available to defer

18

recognizing any loss? Despite concerns about the delays in impairment discussed

above, I suspect the answer to both these questions would be no.

In conclusion, additional analysis seems to be essential before we can draw

strong conclusions about the effectiveness of FAS 141 and 142 in holding

management more accountable for acquisition outcomes. The following are some

questions that might be worth pursuing:

Are there fewer under-performing acquisitions post-FAS 141/142?

Are managers of under-performing acquisitions disciplined more promptly for poor decisions (through early retirement or termination, investor activism or takeovers) under FAS 141/142?

Do divestitures of failed acquisition targets take place more

frequently or more quickly after FAS 142?

Can field research allow us to better understand how managers justify deferring impairing intangibles for failed mergers?

Given limitations on the timeliness of impairments, how do investors

judge whether an acquisition has succeeded or failed on a timely basis?

19

References

Beatty, A., and J. Weber. 2006. Accounting Discretion in Fair Value Estimates: An Examination of SFAS 142 Goodwill Impairment. Journal of Accounting Research 44, 257-288. Bens, D., W. Heltzer, and B. Segal. 2011. The Information Content of Goodwill Impairments and SFAS 142. Journal of Accounting, Auditing and Finance 26, 527-555. Chambers, D. 2007. Has Goodwill Accounting Under SFAS 142 Improved Financial Reporting? Unpublished paper, University of Kentucky. Chen, C., M. Kohlbeck, and T. Warfield. 2008. Timeliness of Impairment Recognition: Evidence from the Initial Adoption of SFAS 142. Advances in Accounting 24, 72-81. Financial Accounting Standards Board (FASB). 1995. Statement of Financial Accounting Standards No. 121: Accounting for the Impairment of Long-Lived Assets and for Long-Lived Assets to Be Disposed Of. Norwalk, CT: FASB. Financial Accounting Standards Board (FASB). 2001. Statement of Financial Accounting Standards No. 141: Business Combinations. Norwalk, CT: FASB. Financial Accounting Standards Board (FASB). 2001. Statement of Financial Accounting Standards No. 142: Goodwill and Other Intangible Assets. Norwalk, CT: FASB. Hayn, C., and P. Hughes. 2006. Leading Indicators of Goodwill Impairment. Journal of Accounting, Auditing and Finance 21, 223–265. Healy, P., K. Palepu and R. Ruback. 1997. Which Mergers are Profitable: Strategic or Financial. Solan Management Review 38, 45-57. Holthausen, R., and R. Watts. 2001. The Relevance of Value-Relevance Literature for Financial Accounting Standard Setting. Journal of Accounting and Economics 31, 3-75. Li, Z., P. Shroff, R. Venkataraman, and X. Zhang. 2011. Causes and Consequences of Goodwill Impairment Losses. Review of Accounting Studies 16, 745-778. Li, K. and R. Sloan. 2015. Has Goodwill Accounting Gone Bad? Unpublished paper, University of California Berkeley. Paugam, I., P. Astolfi and O. Ramond. 2014. Accounting for Business Combinations: Do Purchase Allocations Matter? Journal of Accounting and Public Policy 34, 362-

20

391. Ramanna, K. 2008. The Implications of Unverifiable Fair-Value Accounting: Evidence from the Political Economy of Goodwill Accounting. Journal of Accounting and Economics 45, 253-281. Ramanna, K., and R. Watts. 2012. Evidence on the Use of Unverifiable Estimates in Required Goodwill Impairment. Review of Accounting Studies 17, 749-780. Shalev, R., I. Zhang and Y. Zhang. 2013.CEO Compensation and Fair Value Accounting: Evidence from Purchase Price Allocation. Journal of Accounting Research 51, 819-854. Watts, R. 2003. Conservatism in Accounting Part I: Explanation and Implications. Accounting Horizons 17, 207-221.