Embed Size (px)

Citation preview

September Investment Newsletter THE LTI WEBSITE LAUNCH

On Monday August 20th I had the pleasure of launching the LTI

website featuring a blog, resources, investing tips and more. There are

many more features and content I plan to add in the future but I am

very pleased with what we have created thus far. The website will be an

evolutionary process, continually improving and growing over time.

As of Sept 8th, the LTI website has had 294 visitors and 1132

page views. The blog and newsletter sections of the website are by far

the most popular. I highly recommend bookmarking the blog

(http://ltinvesting.com/blog/) under your favorites as I will continuously

post economic data and various other information that will help you

make an informed decision on the global economic conditions and your

investing strategy.

September Newsletter

Written by Alain Roy

CEO LTI – Long Term Investing

September 11, 2012

www.ltinvesting.com

In this issue: • The Website Launch

• Dollar Cost Averaging – A Bad

Strategy

• Stock Screening – The LTI

Macroscreening Tool

• Aaron’s RESP - Summary

• Stock Market Update

• Global Economy Update

• Summary

“Printing money has never

solved anyone’s problems.

Maybe sometimes in the

short term..but anyone who

has studied history or

economics knows that

printing money in the longer

term doesn’t work. Maybe

this time it’s different, but I

doubt it”

Jim Rogers Legendary Investor Millionaire

DOLLAR COST AVERAGING – A BAD STRATEGY

I decided to put another nail in the coffin of mutual funds and test the theory of

dollar cost averaging which is ever so popular with financial advisors. Most folks will invest

a certain amount of money, every month, in mutual funds via their financial planner. The

monthly contributions are then immediately used to purchase more mutual funds shares

ignoring all market conditions. This approach is often called Dollar Cost Averaging. For

example, you invest $500 per month, continuously over time, and your money is then

invested into your mutual fund holdings. Because you are buying in equal periods, every

month, you are dollar cost averaging, meaning you are buying high, buying low and buying

in the middle.

I completed a 10 year scenario where you would invest $500 every month into the

S&P 500, the benchmark for all investments, using SPY exchange traded fund prices. If you

started investing in 2000, using dollar cost averaging, your total return after 12 years would

be a whopping 3.3% after dividends and paying the Management Expense Ratio.

Cummulative Inevstment Returns in a Mutual Fund using Dollar Cost Averaging

(S&P 500 was the model, dividends and MER included)

-3.9%

-6.7%

-9.0%

0.8%

2.2%

3.2%

4.9%

3.5%

-2.2%

0.2%

2.3%2.6%

3.3%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Date

Return (%)

3.3% return after 10 years of being invested! I would be outraged. You often hear of the

lost decade and in reality this is true for most folks. If you would have used a dollar cost

averaging approach where you invested $500 per month every month since 2000, in the US

stock markets (using the S&P 500 as the benchmark), you would only have a return of

3.3% after all dividends and after paying the mutual fund company and your financial

planner 2.25% along the way. Here is the actual breakdown of the graph above in a table.

The next question is why? Just by the definition you are ensuring AVERAGE results because

of DOLLAR COST AVERAGING. Then on top of that tack on -2.25% due to the management

expense ratio. Even in the years that you lost money such as 2000-2002 and 2008 your

financial planner still received around 1% and the mutual fund company received the other

1.5% (roughly).

How do you ever expect to achieve great results if you are buying at market highs?

It is nearly impossible to buy low and sell high, when you are buying high, average and low.

Sometimes you are buying low when a crash occurs but as I have shown in past

newsletters, crashes only last a short period of time. The number of days that a market

crash lasts is 33 days, using the average from historical crashes. Yet market tops tend to

roll along like small mountains. Therefore you are likely buying high and average way more

than buying low and the end result is horrible returns.

Year Cummulative Return MER Div. YieldTotal Cummulative Return, after MER and Dividends

2000 -2.9% -2.25% 1.3% -3.9%2001 -5.7% -2.25% 1.3% -6.7%2002 -8.3% -2.25% 1.6% -9.0%2003 1.3% -2.25% 1.8% 0.8%2004 2.1% -2.25% 2.4% 2.2%2005 3.1% -2.25% 2.3% 3.2%2006 4.7% -2.25% 2.5% 4.9%2007 3.1% -2.25% 2.7% 3.5%2008 -2.6% -2.25% 2.7% -2.2%2009 0.3% -2.25% 2.2% 0.2%2010 2.2% -2.25% 2.3% 2.3%2011 2.3% -2.25% 2.5% 2.6%2012 2.90% -2.25% 2.7% 3.3%

Here is the graph showing the daily prices of the SPY which is an ETF mirroring the S&P

500. You can see how quick crashes occur and how much longer increases and tops occur

versus a crash. Therefore, with Dollar Cost Averaging, you never get the chance to buy low

that often. You are doomed to average, if not below average returns.

If you are currently investing in mutual funds you will achieve below average results

due to:

• the management expense ratio

• level of diversification (diworsification!!) leading to average results

• not participating in the dividend growth the same way you would owning the

most solid companies in that mutual fund but as individual stock

On top of the three reasons above, if you are invested in a mutual fund AND are using a

Dollar Cost Averaging approach, well good luck with that. You’re doomed to the poor

house!! Next I will show you an example of the results that you could have achieved

following the Market Buying Opportunity Indicators and the LTI Investing Rules.

In the last newsletter, I summarized the main Buying Opportunity Indicators I use to help

guide the timing of my stock purchases. Here is a brief summary from the last newsletter

as a reminder:

There are dozens of indicators I use to help me determine when to buy stocks. One

category of indicators I use is Market Indicators available from StockCharts.com. The table

below summarizes the main Market Indicators I use, which can be obtained by entering the

ticker symbols at: http://stockcharts.com/h-sc/ui

Note: Never use one indictor alone. Look at all of the above indicators prior to buying

equities, in addition to other indicators such as Put to Call Ratio, Rydex ratio, AAII

Investors, Sentiment, etc.

My favorite of the group is the $OEXA200r, the % of S&P 100 stocks above their 200 day

moving average. Here is a trend of this indicator since 2002.

Ticker

Potential

Buying

Opportunity

Great

Buying

Opportunity

Index Name

$OEXA200r <30 <15 % of S&P 100 Stocks above their 200 day

moving average

$BPCOMPQ <45 <30 NASDAQ Composite Bullish Percent Index

$RHNYA <15 <5 NYSE High-Low Index

$NYSI <-300 < - 600 McClellan NASDAQ Summation Index

$NAHL < -200 < -600 NASDAQ New High - New Lows Ratio

$SPXHILO <25 <10 S&P500 High-Low Index

Using these indicators great buying opportunities occurred in:

• Sept-Oct 2002

• March 2009

Potentially great buying opportunities occurred in:

• Oct-Nov 2008

• July 2010

• Aug 2012

I did not buy any equities in Oct-Nov 2008 as I felt that the wheels were just starting to fall

off. However, I did buy in March 2009, July 2010 and Aug 2012 and if I would have been

managing my money, like today, I would have bought in Sept-Oct 2002.

Now let’s go back to the original example and assume since 2000 we would want to invest

$500 per month in the S&P 500. But instead of buying into a mutual fund we would place

that money into our self-directed investing account and buy the SPY, S&P 500 ETF, where

we can buy and sell stocks at our leisure. For this example I assumed the monthly money

was sitting in the account receiving 0%, building up, until the buying opportunity occurred.

In reality you would have invested in something like xcb.to paying you monthly dividends

but since xcb.to was not around back then I ignored the 4% annual yield and assumed you

let it sit there getting 0%. Here are the results you would have achieved if you would have

followed the Market Buying Opportunities and the LTI Investing Rules and bought in 2002,

2009, 2010 and 2011 at the above-mentioned opportune times:

• Total return of 26.8% as of Sept 2012

• Dividend yield of 3.5% is included in the

26.8%

• Dollar cost Averaging in a Mutual Fund

Return: 3.3%

It is truly alarming how pitiful the results are in

the mutual fund with the dollar cost averaging approach. My cumulative weighted portfolio

average return was roughly 26% at the start of 2012 therefore I am proof that it is possible.

Return from each

buying opportunity2,002 9.2%2,009 29.6%

2,010 21.3%2,011 23.8%

Weighted Average

Cummulative Return

(dividends included)

26.8%

STOCK SCREENING – THE LTI MACROSCREENING TOOL

Choosing a company to invest your money in is a very difficult task. In my

experience most individual investors need a strong mechanical, non-emotional, system

when it comes time to choosing the companies to invest their hard earned money in. Your

first step is to determine your investment goals. However, regardless of your goals, you

should be investing in the best companies in the given sector, not the 5th best or 6th best.

My investment goals are fairly simple:

1. Invest in the best companies in their respective sector with strong fundamentals and

a strong dividend growth rate

2. Buy the company stock at a reasonable price; usually a low price

3. If the company continues to be financially strong then hold for the long term and

allow the dividends to continue growing over time. This will result in double digit

dividend yields over time and likely a very handsome stock price appreciation.

After screening over 7500 companies, I noticed over and over again there were certain

parameters consistent amongst the very best companies. That was when the LTI

Macroscreening Tool was born and simplified into four screening criteria as shown below:

The four screening parameters are:

1. Earning per share growth over time

2. Return on Equity > 12%

3. Consistent Net Profit Margins and/or increasing over time

4. Retained Earnings growth over time

Earnings per share growth over time

1. Go to http://money.msn.com/

2. Type in the stock ticker symbol or name in the top left box and hit enter

3. On the left hand side click on “10-Year Summary”

Look for EPS growth over time. Also look for share buybacks by looking at “Shares

Outstanding” in the bottom right. Share buybacks are another sign of strength.

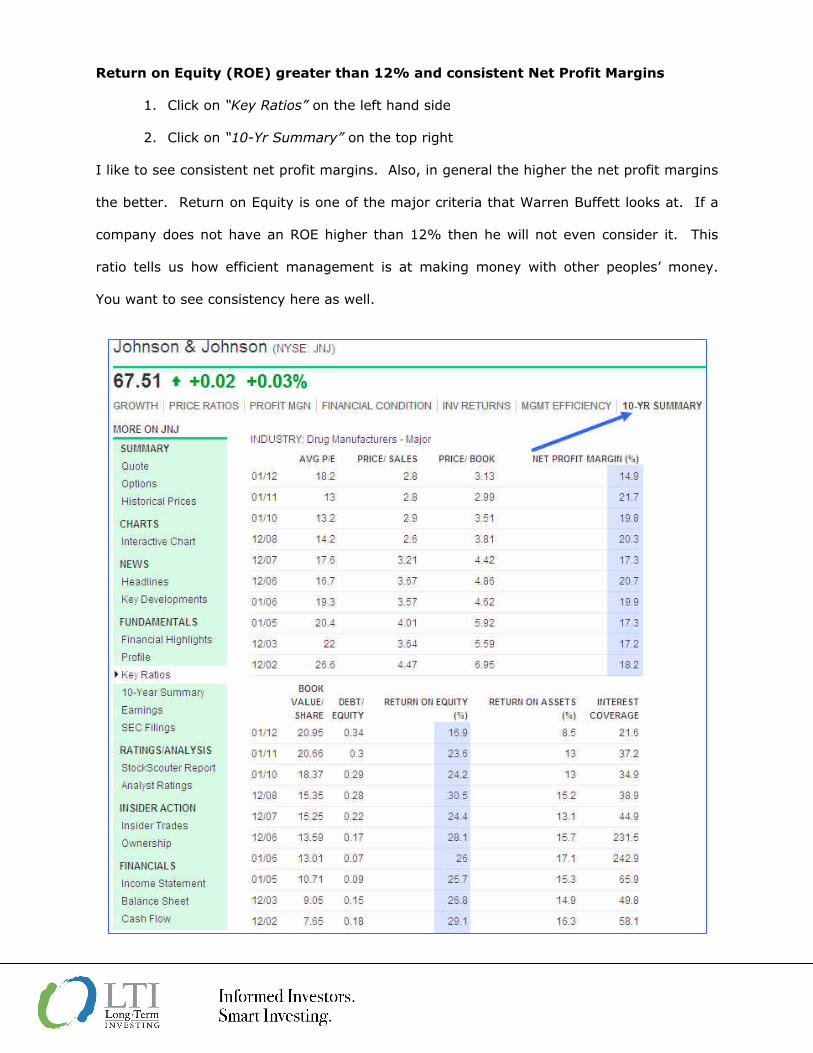

Return on Equity (ROE) greater than 12% and consistent Net Profit Margins

1. Click on “Key Ratios” on the left hand side

2. Click on “10-Yr Summary” on the top right

I like to see consistent net profit margins. Also, in general the higher the net profit margins

the better. Return on Equity is one of the major criteria that Warren Buffett looks at. If a

company does not have an ROE higher than 12% then he will not even consider it. This

ratio tells us how efficient management is at making money with other peoples’ money.

You want to see consistency here as well.

Retained Earnings Growth over time

1. Click on “Balance Sheet” on the left hand side near the bottom

2. Click the “Annual” button near the top

3. Retained earnings are shown near the bottom of the page.

In my opinion, Retained earnings growth is the single most useful measure of the strength

of a company. If I was told to invest millions of dollars into a company but I had only one

item to look at, it would be historical retained earnings.

Let’s go through some examples:

Bank of Nova Scotia (BNS) versus Manulife Financial

• EPS for BNS is much more consistent

• ROE is above 12% for BNS and higher than Manulife

• Net Profit Margins for Manulife is negative recently, a sign that they cannot withstand

tough economic difficulties unlike BNS who continue to produce high net profit margins.

Even in the good years BNS had higher net profit margins than Manulife.

• BNS has growing retained earnings and Manulife has decreasing retained earnings.

When retained earnings are not growing this is a warning sign.

Bank of Nova Scotia is the clear winner here. This is a clear case of a great company to

invest (BNS) versus a company that does not even make my Watch List (Manulife). If you

see a company with no retained earnings growth this is a sign of weakness in my mind. If

a company passes the above mentioned 4 criteria they proceed to the Financial Statement

Analysis step: http://ltinvesting.com/financial-statement-analysis/

With these four simple parameters you are able to very effectively and efficiently

weed out the good from the bad and be left with the best of the best. The Financial

Statement Analysis further refines the search until you are left with the very best, cream of

the crop type companies in your watch list. This is part of Risk Management: invest in the

BEST companies.

•

Manulife Financial Bank of Nova Scotia

EPS

Return on

Equity

(%)

Net Profit

Margin

(%)

Retained

Earnings EPS

Return on

Equity

(%)

Net Profit

Margin

(%)

Retained

Earnings

2011 -0.02 0.9 0.1 2501 2011 4.65 15.8 26.7 24662

2010 -1 -6.5 -4.7 3393 2010 3.87 15.1 23.7 21932

2009 1.89 10.9 7.7 15870 2009 2.97 12.8 15.9 19916

2008 -0.54 -2.9 -2.5 12796 2008 3.1 14.6 13.8 18549

2007 2.15 13.3 9.3 14388 2007 4.01 21.4 19 17460

2006 2.03 12.4 9.3 2006 3.56 20.3 20.1

2005 2.15 14.5 10.6 2005 3.23 20.3 23.7

2004 1.88 11.4 9.8 2004 2.97 20.3 25

2003 1.69 16.9 9.6 2003 2.64 18.8 20.5

2002 1.03 11.1 6 2002 1.16 8.6 8.3

Sometimes it is not as clear and you need to do some more digging. Let’s have a

look at Coke vs. Pepsi:

• Both have increasing Earnings per Share over time

• Coke seems to have a more stable Return on Equity

• Coke has higher net profit margins

• Both companies have strong retained earnings

• Both companies are buying back shares

In this case both companies would pass onto the Financial Statement Analysis step for

further analysis. As it turns out Coke made my ‘A’ list and Pepsi made my ‘B’ list.

Therefore I would invest in Coke before investing in Pepsi as Coke is the more

fundamentally solid company. However, should Pepsi fall to a low enough price, I would be

happy buying their shares but I would first look at Coke.

Sometimes the company looks good but one item of the four is not good. The two most

important items in my experience are retained earnings growth and Return on Equity. If a

company has good EPS growth and good net profit margins but does not have growing

retained earnings right away they are off my list. It’s that simple. I only want the best of

the best in my list. Walmart vs. Target is a good example of keeping only the best.

Coke Pepsi

EPS

Return on

Equity

(%)

Net Profit

Margin

(%)

Retained

Earnings EPS

Return on

Equity

(%)

Net Profit

Margin

(%)

Retained

Earnings

2011 1.85 27.1 18.4 53,550 2011 4.03 31.3 9.7 40,316

2010 2.53 38.1 33.6 49,278 2010 3.92 29.9 10.9 37,090

2009 1.47 27.5 22 41,537 2009 3.77 35.4 13.7 33,805

2008 1.24 28.4 18.2 38,513 2008 3.21 42.5 11.9 30,638

2007 1.28 27.5 20.7 36,235 2007 3.43 33 14.4 28,184

2006 1.08 30 21.1 2006 3.34 26.7 16

2005 1.02 29.8 21.1 2005 2.39 28.6 12.5

2004 1 30.4 22.3 2004 2.41 30.9 14.2

2003 0.88 30.9 20.8 2003 2.04 30 13.2

2002 0.8 33.7 20.3 2002 1.67 31.5 11.8

Walmart vs. Target

• Both have increasing EPS, good ROE and consistent net profit margins

• However Target has no retained earnings growth whereas Walmart does

• After performing a Financial Statement Analysis on each company, guess which

company made my ‘A’ Watch List: Walmart. The retained earnings growth over time in

my experience of analyzing thousands of companies has been one of the best measures

of how fundamentally strong the company is. After further analysis, Target did not even

make my list. If retained earnings are not growing or are decreasing, I do not consider

them for investment.

Another example is Translalta. The stock price has dropped big time lately making their

dividend yield attractive. However their EPS are stagnant, the ROE is under 12% and

erratic and their retained earnings are going down. Contrast this to Canadian Utilities.

Walmart Target

EPS

Return on

Equity

(%)

Net Profit

Margin

(%)

Retained

Earnings EPS

Return on

Equity

(%)

Net Profit

Margin

(%)

Retained

Earnings

2011 4.54 22.1 3.5 68,691 2011 4.28 18.5 4.2 12,959

2010 4.18 22.4 3.6 63,967 2010 4 18.9 4.3 12,6982009 3.73 20.5 3.5 66,357 2009 3.3 16.2 3.8 12,947

2008 3.35 20.3 3.3 63,660 2008 2.86 16.1 3.4 11,4432007 3.16 19.9 3.4 57,319 2007 3.35 18.6 4.5 12,7612006 2.92 19.8 3.5 2006 3.21 17.8 4.7

2005 2.72 21.5 3.7 2005 2.71 17 4.62004 2.46 21.2 3.7 2004 2.07 14.5 4

2003 2.03 20.3 3.4 2003 1.76 14.5 3.92002 1.76 19.8 3.4 2002 1.5 14.5 3.7

Transalta Canadian Utilities

EPS

Return on

Equity

(%)

Net Profit

Margin

(%)

Retained

Earnings EPS

Return on

Equity

(%)

Net Profit

Margin

(%)

Retained

Earnings

2011 1.33 9.3 11.1 527 2011 3.72 12.3 15.8 2,507

2010 1.19 8.2 9.7 431 2010 3.28 12 15.3 2,3662009 0.66 4.5 4.8 634 2009 3.78 13.2 18.4 2,568

2008 1.18 9.2 7.5 688 2008 3.36 13.3 15.2 2,2792007 1.53 13.2 11.2 763 2007 3.13 13.4 16.4 2,0362006 0.21 1.7 1.6 2006 2.61 12.1 13.6

2005 0.93 7.2 6.9 2005 2.12 10.5 10.82004 0.79 6 6.4 2004 2.47 12.5 10.5

2003 1.55 11.5 12.4 2003 2.07 11.3 7.12002 1.06 8.5 10.5 2002 2.44 14 10.4

AARON’S RESP PORTFOLIO SUMMARY

The RESP is truly a great way to save for your child’s education. The government

will give you 20% of whatever you put into the RESP to a max of $500 per year. This

means you can invest $2500 in an RESP and the government will give you $500; in a

calendar year. Therefore, without placing the money in any investment you are achieving a

20% risk free return. I say risk free because you can have this money invested in nothing

inside the RESP but the government will still give you 20%. How amazing is that? Try

getting a 20% return on your investment risk free...doesn’t exist other than this. Naturally

it makes sense to do everything we can as parents to ensure we max out the RESP every

year in order receive $500 of free money from the government. In June 2012, I bought

Santander Preferred shares which pay quarterly dividends at an annual yield of 10.2% (at

my purchase price of $25.09). In addition, I also bought some xcb.to shares which have a

4.2% annual yield in the form of monthly dividends. So Aaron’s RESP looks like this so far:

• Total Portfolio yield of 7.2% per annum

• Weighted Portfolio return in 2012 (as of Sept 7): 12.6% (not including gov. match )

• This is a solid and very safe portfolio for the little guy so far.

Aaron's RESP Portfolio Summary

Santander

Preferred Share

10% Div. Yield

Xcb.to

(Corp Bond ETF,

4.2% Div. Yield)

Santander Preferred Share

Xcb.to (Corp Bond ETF)

For any parents or grandparents reading this newsletter I highly encourage you to open an

RESP for your child or children and do your very best to put away $2500 per year per child

in order to receive $500 per year of free money from the government. You can put more

than $2500 away in a given year, you just won’t get any more money from the government.

The most they will give you per year is $500, hence why it makes the most sense for most

parents to put $2500 per year.

STOCK MARKET UPDATE

The stock markets have been advancing lately on various central bank

announcements such as the ECB bond buying program, some Chinese easing and other

easing strategies. This has helped to lift stock markets to a 3 year high. The future

direction of the markets is always unknown. However, there are some indicators an

investor can use to determine what position the markets are in: overbought, oversold or

neutral.

Last week I posted, http://ltinvesting.com/markets/rydex-bulls-to-bear-ratio-continues-

its-ascent/, that the Rydex ratio was showing signs of the equity market either at a top or in

the topping process.

The volatility index is currently very low versus the last five years. Periods of calm in the

markets may go on for some time but at some point something occurs to jolt the markets,

fear and uncertainty rises and volatility increases. Therefore when the waters are too calm,

especially in today’s economy I tend to get cautious: http://ltinvesting.com/markets/the-

volatility-index-vix/

The ratio of utility stocks to the S&P 500 is a good indicator I like to use to determine

whether equities are in the oversold, neutral or overbought category. The graph below

shows that equities are entering the overbought stage.

The surge in equities has caused the xcb.to bond fund to drop in price and fall below its 50

day moving average recently. I took this opportunity to put roughly 50% of my cash into

xcb.to. This is a great place to store your cash while you wait for a buying opportunity. It

pays roughly 4.2% in yield via monthly dividends. In addition, when markets drop, the

value of xcb.to goes up. This ETF is a great way to achieve a decent return while you wait

for an equity buying opportunity in a relatively safe manner. You can make this strategy

even safer by implementing a Stop Limit close to your purchase price to protect yourself

further from any unforeseen events. The graph below shows where I bought xcb.to. If it

drops under its 50 day moving average again I will continue to buy more. There were many

folks in the LTI network who moved some of their cash into this fund via my direction. I

estimate that the LTI network invested between $125K and $200K in xcb.to during the

period highlighted in green. I am hoping it drops below this level again so I can move

another large chunk of my cash into this fund.

GLOBAL ECONOMIC UPDATE

Fundamentally the global economy is weak and is slowing in many parts of the

world. Central banks continue to print more money, buy bonds in order to back stop major

risks and continue to kick the can down the road further. Meanwhile stock markets continue

to climb.

France continues to struggle

according to their Total Production

Index.

France’s Producer Price Index year

over year is on the decline.

Germany’s business

climate is deteriorating.

Germany’s production is

starting to stagnate and the

year over year is turning

negative.

China’s economy is

showing continued

signs of weakness.

US Velocity of M2 Money Stock has

been decelerating; a sign of

economic weakness.

US Velocity of M2 Money Stock

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

Jan-

70

Jan-

73

Jan-

76

Jan-

79

Jan-

82

Jan-

85

Jan-

88

Jan-

91

Jan-

94

Jan-

97

Jan-

00

Jan-

03

Jan-

06

Jan-

09

Jan-

12

Ratio

Source: FREDltinvesting.com

Velocity of M1 Money

Supply is also showing the

same trend as the larger

M2 money supply.

As part of my research I have hundreds of economic indicators from the major

economies around the world. The general 30,000 foot view shows a global economy that is

slowing down. Some areas are in a recession, others are contracting and others, such as

the US are growing very mildly. This is a natural cycle so we should not be too worried. In

fact, I get excited when I see global economic weakness because this means a potential

buying opportunity in equities may occur in the medium term. From a longer term

perspective this is not a time to be buying into equities. You should be moving your

portfolio to a more defensive strategy and protecting any gains that you have achieved.

Here are LTI blog links to more information, data and graphs for the areas mentioned

above:

http://ltinvesting.com/france-economy/france-economy-ppi-retail-trade-and-production/

http://ltinvesting.com/us-economy/us-velocity-of-money-not-looking-good/

http://ltinvesting.com/us-economy/us-government-social-benefits-above-historical-average/

http://ltinvesting.com/us-economy/us-yield-curve-showing-slight-sign-of-economic-weakness/

http://ltinvesting.com/markets/update-on-germany-production-inflation-and-business-climate-index/

http://ltinvesting.com/china-economy/chinas-economy-continues-to-cool-off-and-contract/

http://ltinvesting.com/uncategorized/world-exports-index-shows-signs-contraction/

US Velocity of M1 Money Stock

4

5

6

7

8

9

10

11

Jan-

70

Jan-

73

Jan-

76

Jan-

79

Jan-

82

Jan-

85

Jan-

88

Jan-

91

Jan-

94

Jan-

97

Jan-

00

Jan-

03

Jan-

06

Jan-

09

Jan-

12

Ratio

Source: FREDltinvesting.com

SUMMARY

Here are the key takeaways from this month’s newsletter:

1. The LTI MacroScreening Tool is an easy and efficient way to help in deciding whether a

company is worth investing in. Remember these rules:

o Do not invest in a company that does not have retained earnings growth

o Do not invest in a company that has a Return on Equity < 12%

o Do not invest in a company with erratic net profit margins

o Do not invest in a company with flat or declining EPS growth

2. Dollar Cost Averaging is an extremely bad investment strategy doomed to average or

below average returns. Combine this with investing in a Mutual Fund and you have the

worst investment strategy out there. Since 2000, using a Dollar Cost Averaging

approach investing in mutual funds (a typical strategy of many people), you would have

a return of 3.3% as of September 2012. Pitiful. Meanwhile I have enjoyed a 26%

return employing a patient and disciplined strategy of buying the best companies at low

prices and basking in the glory of increasing dividends over time and capital

appreciation.

3. An RESP for your child’s education is one of the best savings tools available to

Canadians. If you put $2500 per year away in an RESP you will receive $500 from the

government for a return of 20%. Truly amazing! If you have kids you should be doing

everything in your power to put $2500 in an RESP per child. Make the necessary

sacrifices for the future of your children. It will pay off in a huge way down the road.

4. Stock markets are climbing on irrational exuberance and are starting to show signs of

overbought and topping conditions. I would not be buying any equities at this time.

5. The global economy continues to remain weak. Investing in equities at this time is not

recommended. A more defensive portfolio is required in order to protect your capital

from future risks. Placing Stop Limits on any stocks of companies you do not plan to

own forever is prudent. Moving money over into the xcb.to bond fund as it drops below

its 50 day moving average is a good place to store your cash while you wait for the next

buying opportunity.

LTI BOOK OF THE MONTH

Mary Buffett’s book Interpretation of Financial Statements is very good supporting

material for the section on stock screening and what to look for in a company which I wrote

about early in this newsletter. I highly recommend this book for any individual investor

interested in taking their knowledge one step further. This is a fairly simplified book on this

subject and one I highly recommend.

• Warren Buffet and the Interpretation of Financial Statements

• $18.17 on Amazon.com

• http://www.amazon.ca/Warren-Buffett-Interpretation-Financial-

Statements/dp/1416573186

Alain Roy, P.Eng, MBA Candidate CEO of LTI – Long Term Investing www.ltinvesting.com

Disclaimer: The content of this newsletter is to increase your financial intelligence and is

intended as general information only. Any action that you take as a result of this

information and analysis is ultimately your responsibility. I will not be held responsible for

any negative outcomes of any kind as a result of this information. Please use this

information responsibly. Consult your financial advisor before making any investment

decisions.