Embed Size (px)

Citation preview

GASB UpdatePrepared by:

Debbie Harper

Brandon Young

Ryan Domino

www.lslcpas.com

• June 30, 2019 Fiscal Year– GASB 83: Certain Asset Retirement Obligations

– GASB 88: Certain Disclosures Related to Debt, including DirectBorrowings and Direct Placements

• June 30, 2020 Fiscal Year– GASB 89: Accounting for interest cost incurred before the end of

a construction period

– GASB 84: Fiduciary Activities

• June 30, 2021 Fiscal Year– GASB 87: Leases

1

www.lslcpas.com

On The Horizon Update

• Financial Reporting Model– Public Hearings Held in March 2019

– Exposure Draft estimated for June 2020

• Conduit Debt Statement– Exposure Draft Issued April 2019

– Final Expected May 2019

• Deferred Compensation Statement– Added April 2019

FISCAL YEAR ENDING

JUNE 30, 2019

2

www.lslcpas.com

GASB 83

CERTAIN ASSET RETIREMENT OBLIGATIONS

www.lslcpas.com

Asset Retirement Obligation (AROs)

• Legal obligation to perform future asset retirement activities related to tangible capital assets.

• External laws, regulations, contracts, or court judgements together with occurrence of internal event that obligates a government.

• Example: Decommissioning nuclear reactors; dismantling and removing sewage treatment plants;

• Internal events: contamination, tangible asset that is required to be retired; abandoning a tangible capital asset before in operation.

3

www.lslcpas.com

Financial Reporting

• Recognize liability and deferred outflows for AssetRetirement Obligation in full accrual statements.

• Amortize deferred outflow to expense over the estimatedremaining life of the asset.

www.lslcpas.com

GASB 88

CERTAIN DISCLOSURES RELATED TO DEBT, INCLUDING DIRECT BORROWINGS AND

DIRECT PLACEMENTS

4

www.lslcpas.com

GASB 88Certain Disclosures Related to Debt,

including Direct Borrowings and Direct Placements

• Clarifies which liabilities governments should include when disclosing debt information.

• Defines debt and disclosures resulting from a contractual obligation with a set fixed amount and date.

• Other disclosure requirements related to debt:– Unused credit lines

– Assets pledged as collateral for debt

– Terms related to significant events of default

– Significant termination events

– Significant subjective acceleration clauses

www.lslcpas.com

Clarifies which liabilities governments should include when disclosing debt information

• Direct Borrowings– Loan Agreements with lenders

• Direct Placements– Debt Security directly to an investor

• Direct Borrowings and Direct Placements– Negotiated directly with the investor or lender

– Not offered for public sale

5

www.lslcpas.com

Defines debt and disclosures resulting from a contractual obligation with a set fixed amount and date

• Fixed Amount– Variable Rate Interest

– Capital Appreciation Bonds

• Do not preclude the amount to be settled from being considered fixed.

www.lslcpas.com

Other disclosure requirements related to debt

• Amounts of unused lines of credit

• Assets pledged as collateral for debt

• Terms specified in debt agreements related to significant– Events of default

– Termination events

– Subjective acceleration clauses

• Separate direct borrows and direct placements from other debt

6

www.lslcpas.com

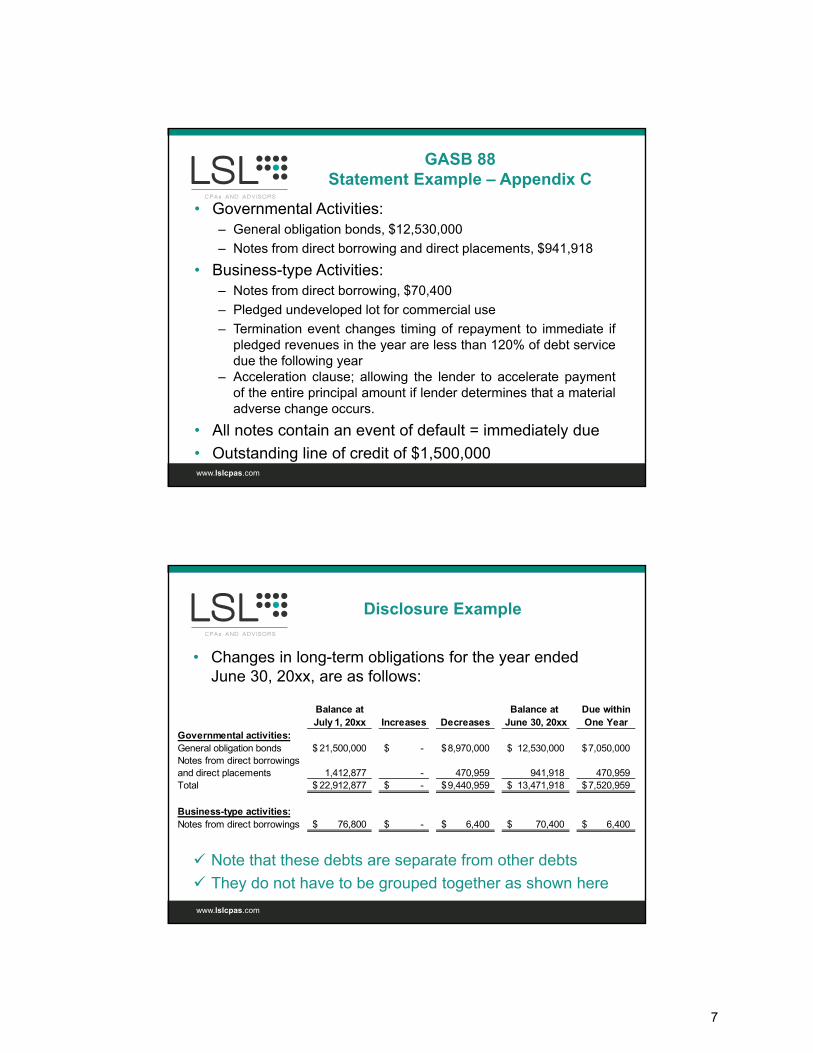

GASB 88 Statement Example – Appendix C

• Governmental Activities:– General obligation bonds, $12,530,000

– Notes from direct borrowing and direct placements, $941,918

• Business-type Activities:– Notes from direct borrowing, $70,400

– Pledged undeveloped lot for commercial use

– Termination event changes timing of repayment to immediate ifpledged revenues in the year are less than 120% of debt servicedue the following year

– Acceleration clause; allowing the lender to accelerate paymentof the entire principal amount if lender determines that a materialadverse change occurs.

• All notes contain an event of default = immediately due

• Outstanding line of credit of $1,500,000

www.lslcpas.com

Disclosure Example

• Changes in long-term obligations for the year ended June 30, 20xx, are as follows:

Note that these debts are separate from other debts

They do not have to be grouped together as shown here

Balance at Balance at Due withinJuly 1, 20xx Increases Decreases June 30, 20xx One Year

Governmental activities:General obligation bonds 21,500,000$ -$ 8,970,000$ 12,530,000$ 7,050,000$ Notes from direct borrowings and direct placements 1,412,877 - 470,959 941,918 470,959 Total 22,912,877$ -$ 9,440,959$ 13,471,918$ 7,520,959$

Business-type activities:Notes from direct borrowings 76,800$ -$ 6,400$ 70,400$ 6,400$

7

www.lslcpas.com

Consider Segregating on Face of Financial Statements

LIABILITIES

Current Liabilities:

Accounts payable 5,864,825$

Accrued liabilities 2,543,254

Accrued interest 1,325,465

Compensated absences due within one year 5,132,546

Claims payable due within one year 4,213,585

Long-term obligations due within one year 7,520,959

Total current liabilities 26,600,634$

Non-current liabilities:

Compensated absences due in more than one year 2,312,580$

Claims payable due in more than one year 18,325,012

Net OPEB liability 10,564,258

Net pension liability 272,586,152

Long-term obligations due in more than one year 5,950,959

Total non-current liabilities 309,738,961$

www.lslcpas.com

Disclosure Example

• The Government’s outstanding notes from directborrowings and direct placements related to governmentactivities of $941,918 contain a provision that in an eventof default, outstanding amounts become immediatelydue if the Government is unable to make payment.

8

www.lslcpas.com

Disclosure Example

• The Government’s outstanding notes from directborrowings relate to business-type activities of $70,400 aresecured with collateral of an undeveloped lot zoned forcommercial use. In addition they contain (1) a provisionthat in an event of default, the timing of repayment ofoutstanding amounts become immediately due if pledgedrevenues during the year are less than 120% of debtservice coverage due in the following year and (2) aprovision if that Government is unable to make payment,outstanding amounts are due immediately. As well as anacceleration clause that allows the lender to acceleratepayment of the entire principal amount outstanding if thelender determines that a material adverse change occurs.

www.lslcpas.com

Disclosure Example

• The Government also has an unused line of credit in theamount of $1,500,000.

Debt service requirements on long-term debt atJune 30, 20xx, are as follows:

Show debt services schedules here as usualShow debt services schedules here as usual

9

FISCAL YEAR ENDING

JUNE 30, 2020

www.lslcpas.com

GASB 89

ACCOUNTING FOR INTEREST COST INCURRED BEFORE THE END OF A

CONSTRUCTION PERIOD

10

www.lslcpas.com

GASB 89Accounting for Interest Cost Incurred

before the End of a Construction Period

• Changes accounting requirements for interest costincurred before the end of a construction period.

• Including such interest cost that previously was accountedfor in accordance with GASB 62.

• Resulting in interest cost incurred before the end of aconstruction period to be recognized as an expense andNOT to be included in the historical cost of a capital asset.

www.lslcpas.com

Accounting for Interest Cost

• This is a prospective application.

• Earlier application is encouraged.

• CIP, interest cost incurred in the fiscal year of implementation should NOT be capitalized.

11

www.lslcpas.com

Key take away• Include Prepaid Insurance when calculating gains/losses

• Review Current Debt Disclosures for:– Unused credit lines

– Assets pledged as collateral

– Terms related to significant events if default

– Significant termination events

– Significant subjective acceleration clauses

• Talk with all departments that currently capitalize interest costs– Prepare to stop capitalizing by 20/21 or stop now if project won’t

be completed by then.

www.lslcpas.com

GASB 84

FIDUCIARY ACTIVITIES

12

www.lslcpas.com

Fiduciary Activities Needed clarification

• Large variances in the use of fiduciary funds in practice– Some reported as governmental funds

– Some a fiduciary funds

– Some not reported at all

www.lslcpas.com

Identifying Fiduciary Activities

• Fiduciary Component Units– Meets Statement 14 as amended as a component unit AND is

one of the following arrangements: An irrevocable trust of a pension plan

An irrevocable trust of an OPEB plan

Non employer assets accumulated for a pension plan

Non employer assets accumulated for an OPEB plan

13

www.lslcpas.com

Component Unit Flowchart

Does the PG hold the PCU’s

corporate Powers?(15)

Does the PG hold the PCU’s

corporate Powers?(15)

Not part of this PGNot part of this PGIs the PCU legally

separate?(15)

Is the PCU legally separate?

(15)

Does the PG appoint a voting majority of the PCU’s Board?

(22-24)

Does the PG appoint a voting majority of the PCU’s Board?

(22-24)

Is the PG able to impose its will on

the PCU?(25-26)

Is the PG able to impose its will on

the PCU?(25-26)

Is there a financial benefit/burden relationship?

(27-33)

Is there a financial benefit/burden relationship?

(27-33)

Related organization note

disclosure(68)

Related organization note

disclosure(68)

Part of this PG(15)

Part of this PG(15)

Does the fiscal dependency

Criterion apply?(21b)

Does the fiscal dependency

Criterion apply?(21b)

See Note belowSee Note below

Would it be misleading to exclude the PCU

because of its relationship with the

PG? (39-41)

Would it be misleading to exclude the PCU

because of its relationship with the

PG? (39-41)

Are the two boards substantively the

same? (53)

Are the two boards substantively the

same? (53)

Does the CU provide services entirely or

almost entirely to the PG? (53)

Does the CU provide services entirely or

almost entirely to the PG? (53)

DiscretePresentation

(44-51)

DiscretePresentation

(44-51)

The PCU is not a CU of this reporting entity (see JV reporting

requirements) (69-78)

The PCU is not a CU of this reporting entity (see JV reporting

requirements) (69-78)

Blend (52-54)Blend (52-54)

Blend (52-54)Blend (52-54)

YESYES

YESYES

YESYES

YESYES

A A

A

YESYES

YESYES

YESYES

YESYESYESYES

NONO NONO

NONO NONO NONO

NONO

NONO NONO

NONO

www.lslcpas.com

Does your component unit fall underFiduciary Activities? (3 options)

• Fiduciary Component Units– Assets are:

• Administered through a trust agreement or equivalent arrangement in which the government itself is not a beneficiary,

• Dedicated to providing benefits to recipients in accordance with the benefit terms, and

• Legally protected from the creditors of the government

14

www.lslcpas.com

Does your component unit fall underFiduciary Activities? (3 options)

• Fiduciary Component Units– Assets are

• for the benefit of individuals, and

• the government does not have administrative involvement with the assets or direct financial involvement with the assets.

• In addition, the assets are not derived from the government’s provision of goods or services to those individuals.

www.lslcpas.com

So what is considered Administrative Involvement or Direct Financial Involvement?

• Administrative involvement– If government monitors compliance with the requirements of the

activity that are established by the government or by a resourceprovider that does not receive the direct benefits of the activity.

– If government determines eligible expenditures that areestablished by the government or by a resource provider thatdoes not receive the direct benefits of the activity.

– If government has the ability to exercise discretion in how assetsare allocated.

15

www.lslcpas.com

So what is considered Administrative Involvement or Direct Financial Involvement?

• Direct Financial Involvement– If government provides matching resources for the activities.

www.lslcpas.com

Does your component unit fall underFiduciary Activities? (3 options)

• Fiduciary Component Units– Assets are

• For the benefit of organizations or other governments that are not part of the financial reporting entity.

• In addition, the assets are not derived from the government’s provision of goods or services to those organizations or other governments.

16

www.lslcpas.com

Identifying Fiduciary Activities

• Pension and OPEB Arrangements that are NOT component units and government controls assets– A pension plan that is administered through an irrevocable trust.

(see paragraph 3 of Statement 67)

– An OPEB plan that is administered through an irrevocable trust. (see paragraph 3 of Statement 74)

– A circumstance in which assets from entities that are NOT part of the reporting entity are accumulated for pensions.

(see paragraph 116 of Statement 73)

– A circumstance in which assets from entities that are NOT part of the reporting entity are accumulated for OPEB.

(see paragraph 59 of Statement 74)

www.lslcpas.com

Control of Assets not considered in determining component unit is a fiduciary component unit

• Control of Assets– If the government holds the assets or

– Has the ability to direct the use, exchange, or employment of the assets in a manner that provides benefits to the specified or intended recipients.

– Restrictions from legal or other external restraints that stipulate the assets can be used only for a specific purpose do not negate a government’s control of the assets.

17

www.lslcpas.com

Identifying Fiduciary Activities

• Other Fiduciary Activities if all three of the following:1) The government has control over the assets

2) Those assets are NOT derived either:• Solely from the government’s own-source revenues (i.e. Sewer and

water charges, investment earnings, sales taxes, property taxes)

• From the government mandated nonexchange transactions or voluntary nonexchange transactions with the exception of pass-through grants and for which the government does not have administrative or direct financial involvement

www.lslcpas.com

Identifying Fiduciary Activities

• Other Fiduciary Activities if all three of the following:3) The assets associated with the activity has one or more of the

following characteristics:a) The assets are

1) administered through a trust in which the government itself isNOT a beneficiary,

2) Dedicated to providing benefits to recipients in accordancewith the benefit terms, and

3) Legally protected from the creditors of the government

b) The assets are for the benefit of individuals and the governmentdoes NOT have administrative involvement with the assets ordirect financial involvement with the assets and NOT derived fromgovernment.

18

www.lslcpas.com

Identifying Fiduciary Activities

• Other Fiduciary Activities if all three of the following:3) The assets associated with the activity has one or more of the

following characteristics (continued):c) The assets are for the benefit of organizations or other

governments that are NOT part of the financial reporting entity AND assets are NOT derived from the government.

www.lslcpas.com

How to report Identified Fiduciary Activities

• Pension (and other employee benefit) trust funds– Pension plans and OPEB plans that are administered through

irrevocable trusts. (see paragraph 3 of Statement 67 and/or 74)

– Other employee benefit plans for which (1) resources are held ina trust fund AND (2) contributions to the trust and earnings onthose contributions are irrevocable.

19

www.lslcpas.com

Look for additional breakdown of investments

Combine here, break‐out in back

Break‐out here

www.lslcpas.com

How to report Identified Fiduciary Activities

• Investment trust funds– Used to report fiduciary activities from the external portion of

investment pools and individual investment accounts that areheld in a trust when government is not a beneficiary and assetsare dedicated to providing benefits to recipients in accordancewith benefit terms where assets are legally protected fromgovernment creditors.

20

www.lslcpas.com

www.lslcpas.com

How to report Identified Fiduciary Activities

• Private-Purpose Trust Funds– Used to report all fiduciary activities that are NOT:

• pension (and other employee benefit) trust funds or

• investment trust funds AND

– Held in a trust

– Government is not a beneficiary

– Assets provide benefits to recipients in accordance with benefitterms where assets are legally protected from governmentcreditors.

21

www.lslcpas.com

www.lslcpas.com

How to Report identified Fiduciary Activities

• Custodial funds– Used to report fiduciary activities that are NOT held in trust

agreements or equivalent arrangements.

– The external portion of investments pools that are not held in atrust when government is not a beneficiary.

– Assets provide benefits to recipients in accordance with benefitterms where assets are legally protected from governmentcreditors.

– Should be reported in a separate external investment pool fundcolumn, under the custodial fund classification.

22

www.lslcpas.com

www.lslcpas.com

23

www.lslcpas.com

www.lslcpas.com

How to Report Identified Fiduciary Activities

• Business-type Stand Alone Statements– Resources expected to be held 3 months or less can be reported

in the statement of net position, with inflows and outflowsreported as operating cashflows in the statement of cashflows.

24

FISCAL YEAR ENDED

JUNE 30, 2021

www.lslcpas.com

Background

• FASB 13 guided our lease accounting (1976) through NCGA 5 – Accounting and Financial Reporting Principles for Lease Agreements of State and Local Governments

• Updates through GASB 13 – Accounting for Operating Leases

• Locked it in with GASB 62 –

codifying accounting and financial

reporting guidance with FASB

• FASB updates Lease Reporting…

25

www.lslcpas.com

Foundation

• Lease Transaction (Operating/Capital)

• Lessee– receives the legal right to use an underlying asset.

– promises to make payments over time for the right to use that underlying asset.

– Therefore, the Lessee has financed the acquisition of that legal right.

• Lessor– receives payments over time transferring the right to use that

underlying asset.

www.lslcpas.com

Objective

• Establish a single model for lease accounting based on the foundational principle that leases are financings of the right to use an underlying asset.

• Lessee is required to recognize the lease liability and the right to use lease asset.

• Lessor is required to recognize the lease receivable and a deferred inflow of resources.

26

www.lslcpas.com

Defined

• A contract that conveys control of the right to useanother entity’s nonfinancial asset as specified in thecontract for a period of time.

• Nonfinancial asset examples = buildings, land, vehicles,and equipment.

www.lslcpas.com

Exclusions

• Non-exchange transaction– Lease for $1/year (GASB 33)

– Lease for free (future GASB project – revenue/exp recognition)

• Contracts for rights to explore for natural resources

• Licensing Contracts (i.e. Computer software)

• Service Concession Arrangements (GASB 60)

• Intangible Assets, except for “right-to-use” as in Subleasing for an underlying asset

• Conduit Debt (Interpretation 2)

27

www.lslcpas.com

Exclusions

• Supply Contracts

• Leases of Inventory

www.lslcpas.com

BUT….. What about……..?

• Bargain purchase options – Still Lease Accounting

• Leases associated with COPs – Still Lease Accounting

• Historical works of art and assets under construction

28

www.lslcpas.com

Lease Term

• The period during which a lessee has a noncancelable right to use an underlying asset, plus the following periods, if applicable:– Option to extend the lease if reasonably certain to exercise

– Option to terminate if reasonably certain not to exercise

• Short-term Lease = maximum term of 12 months (or less) including options to extend regardless of probability

www.lslcpas.com

Financial Reporting - Recognition

• Recognize a liability and a lease asset– Lessee takes possession of the asset or gains access to use

• This creates the obligation

29

www.lslcpas.com

Financial Reporting – Lessee Measurement

• Liability = Present Value of payments expected to be made during the lease term (less any lease incentives).

• Present Value– Interest rate the lessor charges the lessee (implicit interest rate)

– Alternative – Estimated incremental borrowing rate is acceptable

www.lslcpas.com

Financial Reporting – Lessee Measurement

• Variable Payments– Dependent on index/rate – Use baseline and the current index/rate

to measure the future payments.

– Dependent on future performance – Don’t estimate performance• Use minimum guarantee amounts

• Variable payments that are fixed in substance and reliably measured

– Purchase Options/Residual Guarantees – include if reasonably certain those options will occur and are required.

30

www.lslcpas.com

Financial Reporting – Lessee Measurement

Asset

• Amount of initial measurement of the lease liability, plus any payments made to the lessor at or before the commencement of the lease term and certain direct costs.

• Include cost to place asset into service

• Include initial direct costs associated with lease – Structuring fees (legal and administrative costs)

www.lslcpas.com

Lessee Reporting Example – Facts & Assumptions

• Lease contract for equipment beginning July 1, 20X1 for 60 months

• Option to extend for 24 months; County unsure on exercising option

• Lease may continued month-to-month at end of term

• Base payment $1,000/month, includes 200 machine hours; $5 per excess hour

• Additional $80/month for repairs and maintenance

• Lease contract states 4% interest rate

• Separate $1,500 contract for delivery and installation

31

www.lslcpas.com

Lessee Reporting Example – Lease Term

• Noncancellable period of lease is 60 months

• County is not reasonably certain to exercise option to extend 24 months– Should NOT be included in lease term

• Potential month-to-month extensions– NOT included in lease term as not enforceable; either County or

Lessor can cancel

• Lease term = 60 months

www.lslcpas.com

Lessee Reporting Example – Initial Measurement of Asset and Liability

• Base Payment = $54,480 – $1,000/month X 60 months X Discounted at 4%

• Excess Use Charge = $0– Variable based on future usage/performance EXCLUDED

• Repair & Maintenance = $0– EXCLUDED unless not practical

• Delivery and Installation = $1,500– Initial direct costs included in asset

• Initial Value of Leased Asset = $55,980

32

www.lslcpas.com

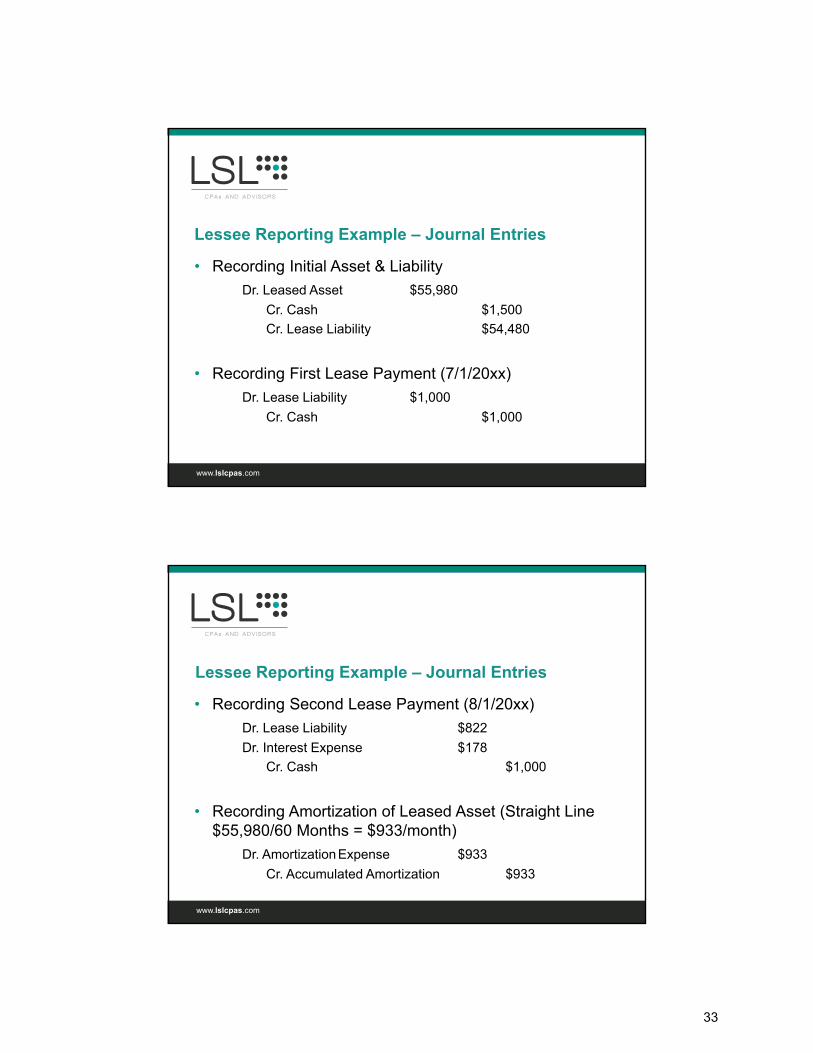

Lessee Reporting Example – Journal Entries

• Recording Initial Asset & Liability

Dr. Leased Asset $55,980

Cr. Cash $1,500

Cr. Lease Liability $54,480

• Recording First Lease Payment (7/1/20xx)

Dr. Lease Liability $1,000

Cr. Cash $1,000

www.lslcpas.com

Lessee Reporting Example – Journal Entries

• Recording Second Lease Payment (8/1/20xx)

Dr. Lease Liability $822

Dr. Interest Expense $178

Cr. Cash $1,000

• Recording Amortization of Leased Asset (Straight Line $55,980/60 Months = $933/month)

Dr. AmortizationExpense $933

Cr. Accumulated Amortization $933

33

www.lslcpas.com

Financial Reporting – Investment Asset

• Special Circumstances for Assets that meet investmentdefinition (lease is entered into for the purpose ofsubleasing solely for profit)– Lease Receivable would meet investment measurement

• (GASB 72)

YourSpecial

www.lslcpas.com

Financial Reporting – Lessor Measurement

• Lease Receivable– Present Value of future lease payment

(fixed payments, variable payments that depend on index/rate,

variable payments that are fixed in substance)

– Symmetrical with lease liability

34

www.lslcpas.com

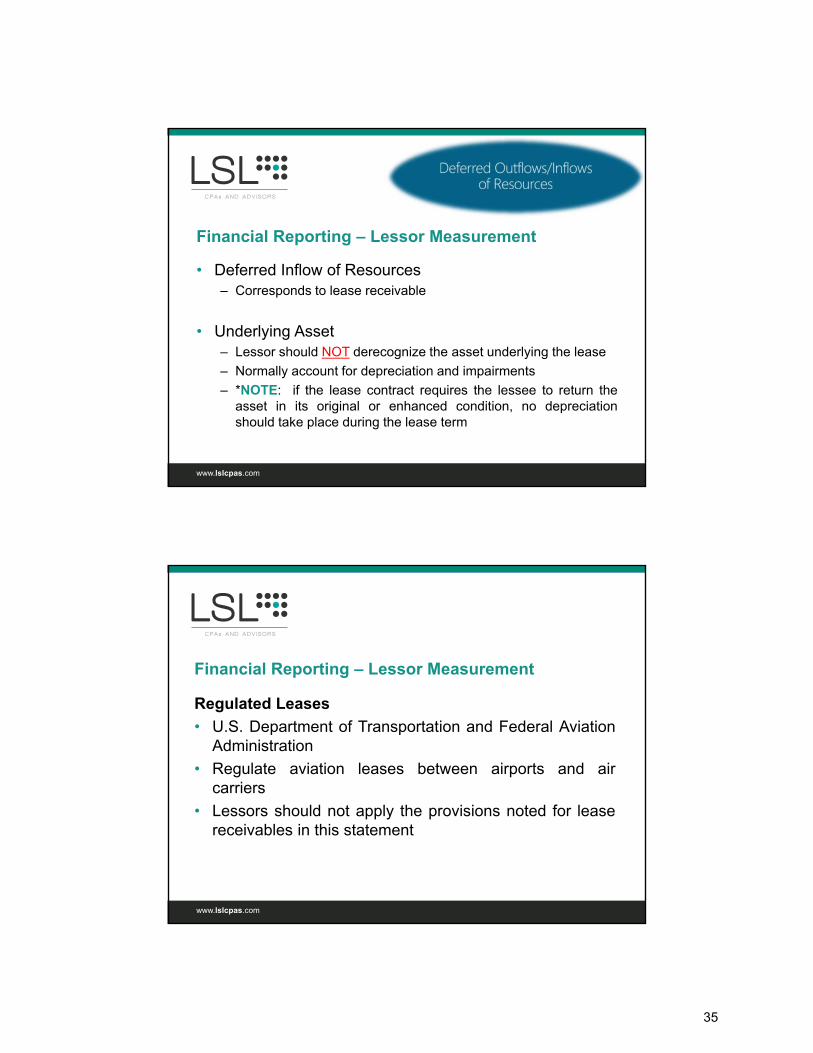

• Deferred Inflow of Resources– Corresponds to lease receivable

• Underlying Asset– Lessor should NOT derecognize the asset underlying the lease

– Normally account for depreciation and impairments

– *NOTE: if the lease contract requires the lessee to return theasset in its original or enhanced condition, no depreciationshould take place during the lease term

Financial Reporting – Lessor Measurement

www.lslcpas.com

Financial Reporting – Lessor Measurement

Regulated Leases

• U.S. Department of Transportation and Federal AviationAdministration

• Regulate aviation leases between airports and aircarriers

• Lessors should not apply the provisions noted for leasereceivables in this statement

35

www.lslcpas.com

Financial Reporting – Lessor Measurement

Regulated Leases

• Must meet these requirements:– Lease rates cannot exceed a reasonable amount

• (reasonable is determined by an external regulator)

– Lease rates should be similar for lessees that are similarly situated

– Lessor cannot deny potential lessees the right to enter into leases if facilities are available

• (provided that the lessee’s use of facility complies with restrictions)

www.lslcpas.com

Financial Reporting – Lessor Measurement

• Recognize the revenues based on the payment provisions of the lease contract

36

www.lslcpas.com

Lessor Reporting Example – Facts & Assumptions

• Lease contract for equipment beginning July 1, 20xx for 60 months

• Option to extend for 24 months; Lessee unsure on exercising option

• Lease may continued month-to-month at end of term

• Base payment $1,000/month, includes 200 machine hours; $5 per excess hour

• Additional $80/month for repairs and maintenance

• Lease contract states 4% interest rate

• Separate $1,500 contract for delivery and installation

www.lslcpas.com

Lessor Reporting Example – Lease Term

• Noncancellable period of lease is 60 months

• Lessee is not reasonably certain to exercise option to extend 24 months– Should NOT be included in lease term

• Potential month-to-month extensions– NOT included in lease term as not enforceable; either Lessee or

County can cancel

• Lease Term = 60 months

37

www.lslcpas.com

Lessor Reporting Example –Measurement of Lease Receivable

• Base Payment = $54,480 – $1,000/month X 60 months X Discounted at 4%

• Excess Use Charge = $0– Variable based on future usage/performance EXCLUDED

• Repair & Maintenance = $0– EXCLUDED unless not practical

• Initial Value of Lease Receivable = $54,480

www.lslcpas.com

Lessor Reporting Example –Journal Entries

• Recording Initial Receivable & Deferred Inflow

Dr. Lease Receivable $54,480

Dr. Cash $1,500

Cr. Deferred Inflow $54,480

Cr. Lease Revenue $1,500

• Recording First Lease Payment (7/1/20X1)

Dr. Cash $1,000

Cr. Lease Receivable $1,000

38

www.lslcpas.com

Lessor Reporting Example –Journal Entries

• Recording Second Lease Payment (8/1/20X1)

Dr. Cash $1,000

Cr. Lease Receivable $822

Cr. Interest Revenue $178

• Recording Amortization of Deferred Inflow (Straight Line $54,480/60 Months = $908/month)

Dr. Deferred Inflows $908

Cr. Lease Amortization Revenue $908

www.lslcpas.com

Remeasurement – Liability

• Certain circumstances require a relook

• Changes in the lease contract

• Estimates incorporated into the liability measurementchanged (probability to exercise option)– Change in index/rate alone does NOT require remeasurement

• Contingent rentals becoming noncontingent– Lessor requires a nominal payment the first year and fixed

payments in subsequent years are based on a percentage offirst-year sales.

39

www.lslcpas.com

Remeasurement - Asset

• If liability is remeasured then adjust the same dollar for lease asset.

• UNLESS……– Adjustment causes a negative

– An Impairment

www.lslcpas.com

Expense Recognition

• Interest expense related to discount on the lease liability

• Amortization expense related to the lease asset– Decrease in right to use the asset over the lease term

40

www.lslcpas.com

Notes to Financial Statements - LESSEES

• General Description of Lease Arrangement– Variable payments

– Residual Value guarantees, not included in liability

• Total amount of Lease Asset– Related accumulated amortization

• Disclose Lease Asset by Major Classes– Separate from other Capital Assets

• Expenses recognized in the reporting period not previously included in liability

www.lslcpas.com

Notes to Financial Statements - LESSEES

• Debt Service Schedule

• Commitments under leases before end of lease term

• Components of any loss associated with an impairment

• Sublease transactions, if any

• Sale-leaseback transaction, if any

• Lease-leaseback transaction if any

41

www.lslcpas.com

Lessee Note Disclosure Example

“In July 20X1, the County entered into a lease agreement to obtainequipment at an interest rate of 4%, which includes delivery andinstallation costs of $1,500 due July 1, 20X1. The lease term is fiveyears with base monthly payments of $1,000 per month beginning onJuly 1, 20X1, plus $5 per every machine hour in excess of 200 permonth. In addition, the lease requires an $80 per month payment forrepairs and maintenance. As of June 30, 20X2, the lease liabilityoutstanding is $44,289, while the net leased asset value is $44,784,which includes accumulated amortization of $11,196. Expenses relatedto the excess usage charge and repairs and maintenance feerecognized during the year ended June 30, 20X2 amounted to $XXX.The remaining debt service schedule on the lease is as follows:

www.lslcpas.com

Lessee Note Disclosure Example

Year EndingJune 30, Principal Interest Total

20X3 10,418$ 1,582$ 12,000$ 20X4 10,843 1,157 12,000 20X5 11,284 716 12,000 20X6 11,744 256 12,000

Total 44,289$ 3,711$ 48,000$

42

www.lslcpas.com

Notes to Financial Statements - LESSOR

• General Description of Lease Arrangement– Variable payments

– Residual Value guarantees, not included in liability

• Total amount of Revenues (Lease, Interest, Other)

• Revenues recognized in the reporting period not previously included in receivable

• Existence, terms, conditions of options by the lessee to terminate the lease

• Or existence of debt issued secured by lease payments

www.lslcpas.com

Notes to Financial Statements - LESSOR

• Leases of assets that are investments, if any

• Certain regulated leases, if any

• Sublease transactions, if any

• Sale-leaseback transaction, if any

• Lease-leaseback transaction if any

• Lease schedule of future payments (principal and interest)– Five subsequent fiscal years

– Five-year increments thereafter

43

www.lslcpas.com

Sublease transaction considerations

• Originally the Lessee and also the Lessor

• Two separate Transaction

• Do not offset against each other (unless with blended component unit)

• Lessor transaction should be disclosed separately from the original lessee transaction

www.lslcpas.com

Sale-Leaseback transaction considerations

• Originally sells the underlying asset and leases the property back (see GASB 62 for qualifications)

• Two separate Transaction

• Do not offset against each other (unless with blended component unit)

• Lessor transaction should be disclosed separately from the original lessee transaction

44

www.lslcpas.com

Lease-Leaseback transaction considerations

• Asset leased by first party to another then leased back to first party (leasing back one floor of a building to the owner)

• Net Transactions

• Do not offset against each other (unless with blended component unit)

• Lessor transaction should be disclosed separately from the original lessee transaction

www.lslcpas.com

Regulated Leases

• General Description of agreement

• Extent of capital assets are subject to preferential orexclusive use under agreement, by major class of assetAND by counterparty.

• Total amount of Revenues in reporting period from thisagreement:– Lease revenue, interest revenues, etc.

• Schedule of expected future minimum payments:– Subsequent five years, then five-year increment thereafter

45

www.lslcpas.com

Regulated Leases

• Revenues recognized in reporting period for variablepayments not included in expected future minimumpayments

• Existence, terms, and conditions of options by the lesseeto terminate the lease or abate payments,

• IF the lessor has issued debt for which the debtpayments are secured by lease

www.lslcpas.com

KEEP CALM

• Retroactiveimplementation

• Earlyapplicationencouraged.

46

GASB Update

Consider yourself updated…….

Thank you!

47

48

THIS PAGE INTENTIONALLY LEFT BLANK

ERP Best PracticesPrepared by:

Bryan Gruber

Kirk Hamblin

www.lslcpas.com

ERP Best Practices

• About ERP

• Planning, Implementation, Approach

• Data Conversion, testing, and Going Live

• Challenges, Mistakes

• Moving forward with Technology

• Process Improvement

• Key Takeaways

49

www.lslcpas.com

Looking for Change?

• Common reasons you are looking for new system:– Outdated and unsupported systems

– Limited reporting capabilities

– Limited functionality

– Lack of key controls/access

– Lack of ability to integrate/communicate with other systems

www.lslcpas.com

Looking for Change?

• Resources Management– Cost / Efficiency

– Security / Controls

• Talent Market– Ability to attract and retain talent

– Future succession

• Attract new business and development– Improved customer experience and information

– Revenue generation and efficiency

– Innovation

50

www.lslcpas.com

Introduction to Enterprise Resource Planning (ERP)

• "ERP" stands for enterprise resource planning. It refers to a suite of software applications that organizations use to manage day-to-day activities.– A complete ERP suite also includes enterprise performance

management, software that helps to plan, budget, predict, and report on an organization’s financial results.

What is ERP?

www.lslcpas.com

What is ERP?

• Enterprise Resource Planning (ERP)– Integration of systems across departments and business

functions into a common database.

– Provides for greater efficiency and business process.

– Supports better and faster communication and informationthroughout the organization.

– Promotes data integrity and improved control.

– Movement to cloud platform.

51

www.lslcpas.com

Introduction to Enterprise Resource Planning (ERP)

• Applications under common database– Finance, Human Resources, Parks and Rec., GIS, Licensing,

Planning, Permits, Electronic Payments, Contract Management.

• Solutions– Cloud Based / SAAS

– On-Premises

– Hybrid

What is ERP?

www.lslcpas.com

To cloud or not to cloud, that is the question?

Cloud Based System (Off‐Site) On‐Site Local Server

No on‐site server to maintain. Physical Control of System with IT Dept.

Potential Costly Data Recovery No Third Party Access

Accessed over the internet Potential off‐site access through VPN / RD

May require software install, may just be accessed via internet browser

Typically is accessed with local install

Cloud Security is outsourced Security is an inhouse responsibility.

Control over updates may be limited.(forced downtime).

Updates are controlled by IT Dept.

Hardware replacement handled by third party.

Organization responsible for hardware server replacements, capital investment

52

www.lslcpas.com

Considering the cloud:

• Understand how updates, support, security, back-ups,recovery, and downtime are handled?

• What about Bandwidth?– What bandwidth is required for smooth system operation?

– Bandwidth testing

– ISP reliability, backup ISP?

www.lslcpas.com

• Strategic Planning – Developing Long Term– A new ERP by itself will not solve all problems

– To be transformative, must have a vision… not about the “bellsand whistles”

• Develop a clear understanding of the needs and goals ofyour organization– Programs, Services, Departments, and Functions

– Information and communication

– User experience (internal and external)

– Reliability and Controls

Planning

53

www.lslcpas.com

Embracing the Process of Change

• Opportunity of change and improvement!– Why transfer an inefficient process into a new ERP.

• Key to Success is embracing the capabilities of the new technologyand forgetting the words “that’s how we’ve always done it”.

• Process is King

– Team Involvement is crucial, the day to day end users of eachdepartment will help identify key weaknesses and developsolutions to improve.

– Team members may fear change / resist. Plan for this and workfor the support. Sell the vision and the importance of progress.

Planning

www.lslcpas.com

Planning

• Develop a timeline and milestones including modules

• Assess staffing resources– How will daily operations and the extra hours required during the

transition be balanced?• Increased staffing?

• Overtime pay incentives?

– Consider an ERP Expert Consultant

– Develop expectations with ERP Company • Push for what you think is best for your organization’s success!

54

www.lslcpas.com

Preparing for the Unknown

• How do you prepare for unknown factors in yourimplementation?– Learn from others experiences who have implemented

– Ask questions vendor, consultants, and others

– Planning and preparation

– Prepare your organization anticipation, outlook and reactions.There will be challenges!

Planning

www.lslcpas.com

Challenges

• One organization focus as opposed to departments working autonomously. – No Individual preferences

– Requires greater collaboration and communication

– Lack of shared vision

– Resistance to change

• Organization accountability– Involvement Executive Management and IT

55

www.lslcpas.com

Data Conversion

• Develop estimated timeline required to convert data.– This may take longer than you anticipated.

• What will need to be converted.– No need to waste time and resources converting data that is no

longer useful.

• How long will the prior system be maintained on aserver? Include this in your strategic plan.

www.lslcpas.com

Data Conversion

• Chart of Accounts– Time to change? Consider:

• Feedback and involvement from users, budget, accounting, audit

• Promote efficiency, simplicity, effectiveness, compliance

• Don’t rush, get help

– Mapping

56

www.lslcpas.com

Parallel Tests & Going Live

• Utilize Dual Systems to Work out issues and errors withthe assistance of your implementation team.– Ensures reporting is accurately setup in the new system

– Examples, Payroll Information Reported to PERS• Ideally tasks such as this can be included in the implementation

plan from the beginning, however, incase something is missed, thiscan potentially be caught before you lose the support of yourimplementation team.

• This phase can be labor intensive, plan for efficiency.– Double the systems, double the work.

www.lslcpas.com

• Reporting considerations

• Establish an imported data checkpoint, verifying thatdata from the old system was imported successfully.– Limits the timeframe of error moving forward if differences arise

running dual systems

• Utilize your ERP Vendor Team to the fullest before theymove on to a new project when you go live.– Support after may not be personnel familiar with your system.

Parallel Tests & Going Live

57

www.lslcpas.com

ERP Implementation Mistakes –Avoiding the Headache

• Insufficient process planning and assessment

• Lack of leadership involvement / commitment

• Failure to include end-users/departments in the decisionmaking process and implementation– A Team that works together will SUCCEED together

– Department Buy-In and Support / Encouraging Change /Brainstorming Process Improvements

• Under estimating resources required

www.lslcpas.com

ERP Implementation Mistakes –Avoiding the Headache

• Lack of Training– Realize the full potential of your investment and its capabilities

consistent with your processes.

• Lack of accountability to make decisions / deadlines.

• Insufficient data cleansing.

• Over customization, increases cost.

• Lack of Testing / Rushed to Go-Live.

58

www.lslcpas.com

Moving Forward with Technology

www.lslcpas.com

Cloud?

• Efficiency / Accessibility

• Scalability and updates

• Security Considerations

• Infrastructure / Maintenance Cost

59

www.lslcpas.com

Integration

• Financial

• Utilities, taxes, permits, licensing, fees, charges forservices

• Asset Management

• Budgeting

• Human Resources / payroll

• Procurement

www.lslcpas.com

Electronic

• Approvals / documentation

• Paperless

• Mobile

• Real-time

• Data management and analytics (centralized data)– Timely and accurate data

– Business analytics better understand financial and operationaldata and correlation

60

www.lslcpas.com

Transparency / Communication

• Department information and communication

• Grant reporting / compliance

• Board information

• Public transparency

www.lslcpas.com

Mobile

• Internal – HR / timekeeping

– Bill payment

– mobile

• External – Online access and services / web payment services

61

www.lslcpas.com

Automation

• Reduce data entry – scan and auto populate

• Bots (digital assistants)

www.lslcpas.com

Smart Cities

• Cloud, mobile, internet of things

• Service, efficiencies, and value

• Real time data analytics

62

www.lslcpas.com

Process Improvement

• Lean Six Sigma Process

• Change Management

• Role of IT and innovation– Technology Roadmap – strategic plan

– Seat at the table

– Communication / skills

www.lslcpas.com

ERP Takeaways

63

www.lslcpas.com

Key Takeaways

• Obtain not only leadership support, but OrganizationalSupport. Team Involvement!

• Choose the right Project Manager for your Organizationsimplementation.– Point of view needs to be open for change, non-bias to their dept

– Communicative and Organized

– Respected by others, will be working with all depts. of the Org.

• Clear Strategic Plan and Goals

• Embracing Change, Positive Outlook for what’s ahead.

www.lslcpas.com

Key Takeaways

• Thorough Budget and Time Tables– Budget for unexpected delays

– Utilize your ERP Vendor’s experience for advice and beproactive.

– Consider use of consultants

• Plan for the Future and beyond.– Avoid an ERP that will not fit your needs shortly after.

– If a cloud system is not implemented, do you see this in thefuture, can your system be converted to cloud if desired?

64

www.lslcpas.com

Key Takeaways

• Understanding the security of your system– This may be outsourced, but still your data.

• Develop a system failure plan / back up plan.– How will you function if your system goes down.

Questions?

Thank you!

64