Embed Size (px)

Citation preview

Long term macro-

economics assessment of

Latin America

Sarah Hunter

Oxford Economics

Page 2

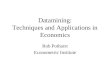

Economic forecasts

Household projections

Risk

•Oxford Economics’ Global Economic Model

•Econometric analysis to decompose population into income groups and model consumption by product & service

•Based on Economic & Political Risk Evaluator

•WEF’s World Competitiveness Report

Methodology

Macro

Forecasts

Macroeconomic analysis was completed in three stages, with each stage leveraging quantitative tools

built by the Oxford Economics team

Page 3

Market Influencers

Growth has slowed in most Latam countries as the region has been buffeted by weak commodity prices,

with many countries having limited scope for policy response

Key drivers of the near-term economic growth prospect are:

Commodity prices – countries such as Bolivia, Colombia, Guatemala and Paraguay have been hit by weak commodity

prices. However, there has been a boost to commodity importers such as El Salvador and Honduras;

US growth – the US is important for trade and remittances for Costa Rica, El Salvador and Honduras and these

countries will benefit as the US recovery strengthens;

Inflation and deficits – these are critical for determining the amount of policy support an economy can expect. Fiscal

policy in Bolivia and Costa Rica is constrained while inflation has pushed up interest rates in Colombia.

Exports

(% of GDP)

Commodities

(% of exports)

Current

account

(% of GDP)

Workers

remittances

(% GDP)

InflationInterest rate

(lending)

Government

balance

(% of GDP)

Population

(16-26 CAGR)

Bolivia 20.5% 82% -8.3% 3.6% 4.5% 8.4% -6.3% 1.4%

Colombia 11.6% 73% -6.0% 1.1% 7.6% 14.3% -3.9% 0.7%

Costa Rica 19.1% 26% -3.5% 1.2% 1.3% 14.2% -6.2% 0.9%

El Salvador 16.8% 18% -3.1% 16.8% 1.6% 6.2% -2.3% 0.3%

Guatemala 18.1% 49% 0.1% 9.9% 4.5% 13.2% -1.3% 1.9%

Honduras 28.3% 28% -6.9% 17.4% 2.9% 20.7% -3.2% 1.3%

Paraguay 42.6% 62% -1.2% 1.6% 4.7% 18.5% -2.5% 1.2%

External Factors Domestic factors

Page 4

Bolivia and Honduras have the most favorable medium-term growth outlooks, whereas El Salvador has

weaker underlying fundamentals that limits growth

Macroeconomic Outlook

Macro Outlook

Domestic and institutional factors are more

important in determining outlook for investment

and productivity, which are key to explaining

long run growth. In particular:

Business environment – challenging

across all countries, although Costa Rica

and Paraguay have relatively business

friendly policies that should be more

supportive of investment;

Political stability/corruption – these

factors increase the cost of doing

business across Latam;

Security – security is a major concern in

El Salvador, Guatemala, and Honduras

and this severely hampers private

enterprise.Bolivia Colombia Costa Rica El Salvador Guatemala Honduras Paraguay

0

5

10

15

20

25

30

% o

f G

DP

Other FDI

Source: Oxford Economics

Investment

Page 5

Outlook for Households

Costa Rica, Colombia, El Salvador, Guatemala, and Paraguay are all expected to have average incomes

approaching or above US$20,000 by 2026

Consumer spending

The outlook for average incomes is largely

determined by overall economic growth and

therefore we expect to see the strongest income

growth in Bolivia and Honduras.

The poorest households in the study are

Bolivia and Honduras. Average incomes are

only over US$20,000 in Costa Rica and

Colombia suggesting limited discretionary

spending across the countries in this study.

“Middle class” households – countries with

relatively high starting income levels and those

likely to see robust economic growth should see

the largest rise in the number of households

with income >US$20,000. These are Costa Rica

and Colombia. The smallest increases occur in

Bolivia and Guatemala.

Page 6

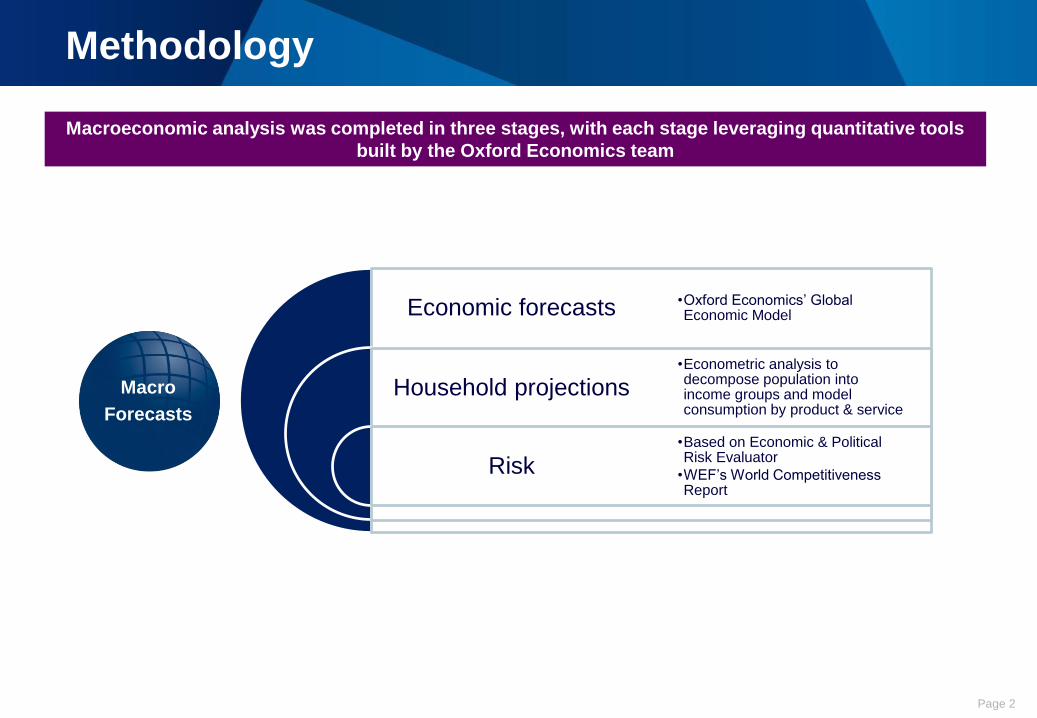

Exchange Rate

We expect to see a gradual depreciation in the currencies of Bolivia, Colombia, Costa Rica, Guatemala,

Honduras, and Paraguay against the US$

Exchange Rate

Volatility can be managed with some form of

exchange rates control and El Salvador is

dollarized.

The robustness of pegs depend largely on a

country’s reserves (relative to size of imports

and short-term debt). Bolivia has a significant

buffer while Costa Rica and Honduras are

more vulnerable should the markets turn

against them.

Most countries will see a real appreciation of

the exchange rate over the forecast period.

Colombia (Oil), Guatemala (Agriculture) and

Paraguay (Soya) are exposed to

commodities and uncertainty over the outlook

for commodity prices means that volatility over

the next few years may be higher than normal.

2015 2021

Depreciation

(CAGR 2015-21) 2026

Depreciation

(CAGR 2021-26)

Bolivia 6.9 7.2 0.6% 7.7 1.4%

Colombia 2741 2900 0.9% 2956 0.4%

Costa Rica 535 642 3.1% 723 2.4%

El Salvador

Guatemala 7.7 8.5 1.7% 9.3 1.8%

Honduras 22.0 25.3 2.4% 29.7 3.3%

Paraguay 5205 5859 2.0% 6362 1.7%

Exchange rate

Page 7

Latam Market Potential

Note: The size of the bubble indicates number of households with income >US$20,000

Honduras and Bolivia offer strong growth potential, while Colombia and Guatemala are the largest

markets

2011-16 2016-21 2021-26

Bolivia 4.9 4.4 5.0

Colombia 3.8 3.6 3.5

Costa Rica 3.8 4.0 3.4

El Salvador 2.0 2.1 2.1

Guatemala 3.6 3.5 3.4

Honduras 3.4 4.0 4.6

Paraguay 4.4 3.8 3.2

Source: Oxford Economics/Haver Analytics

GDP growth (%)

Page 8

Bolivia Macro Outlook

Market Outlook

Risk

Bolivia has been hit by the slump in commodity prices but the economy should benefit from the recovery in oil

and gas prices. While growth should outperform Latam as whole, income levels are relatively low

Page 9

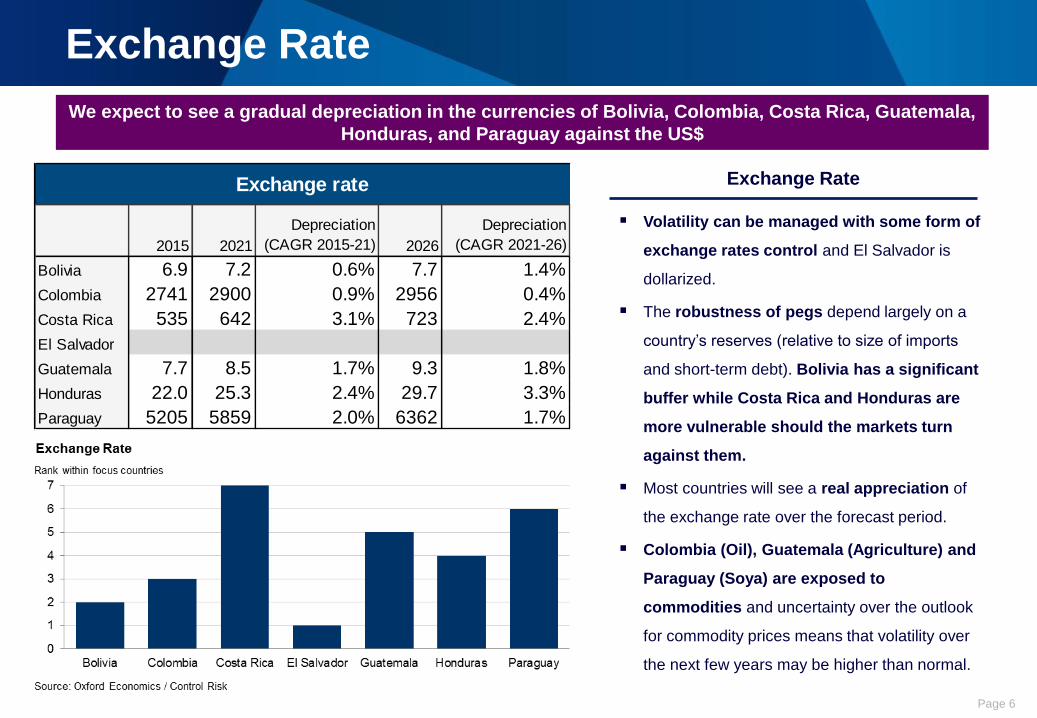

Colombia Macro Outlook

Market Outlook

Risk

The largest and second highest income market out of Millicom’s countries, but FX hit by commodity prices and

policy backdrop to remain tight. The situation with FARC and ELN has improved but remains a risk

Page 10

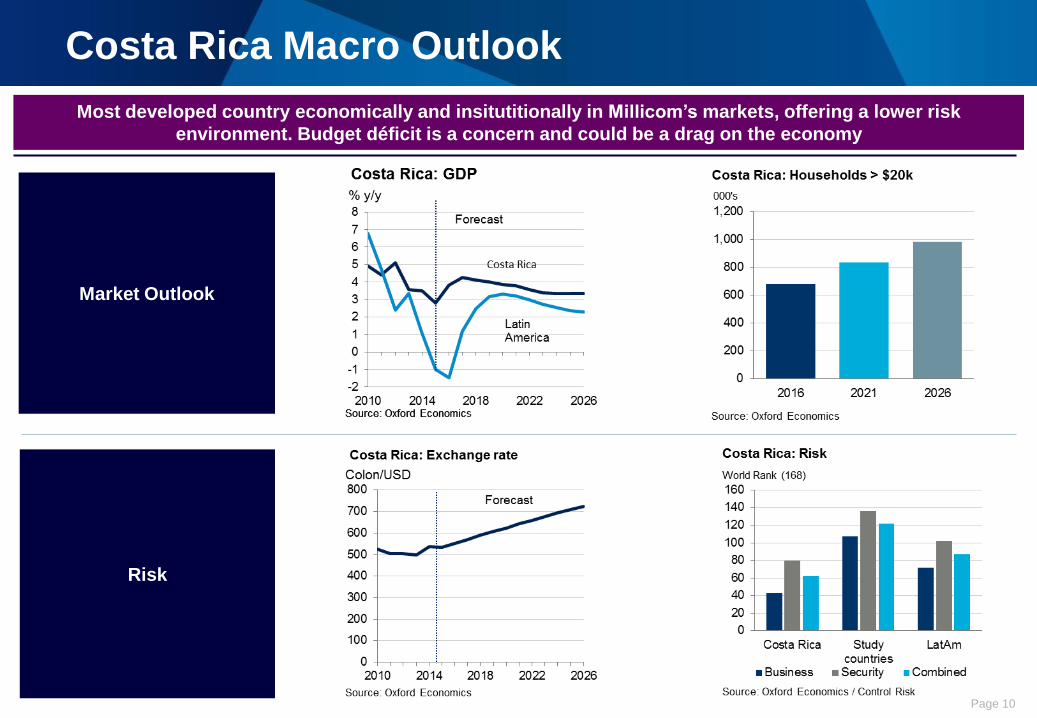

Costa Rica Macro Outlook

Market Outlook

Risk

Most developed country economically and insitutitionally in Millicom’s markets, offering a lower risk

environment. Budget déficit is a concern and could be a drag on the economy

Page 11

El Salvador Macro Outlook

Market Outlook

Risk

Security threat and criminality clouds the outlook and the weak political backdrop means progress to creating a

more business-friendly environment is likely to be slow

Page 12

Guatemala Macro Outlook

Market Outlook

Risk

Dependent on the US, especially for remittances, which should help growth over the next couple of years, while

rapid population growth should help medium term prospects. Security remains a risk to business, however

Page 13

Honduras Macro Outlook

Market Outlook

Risk

Growth set to accelerate, underpinned by recovery in US and solid fundamentals. Progress on reforms to

promote the business environment are needed

Page 14

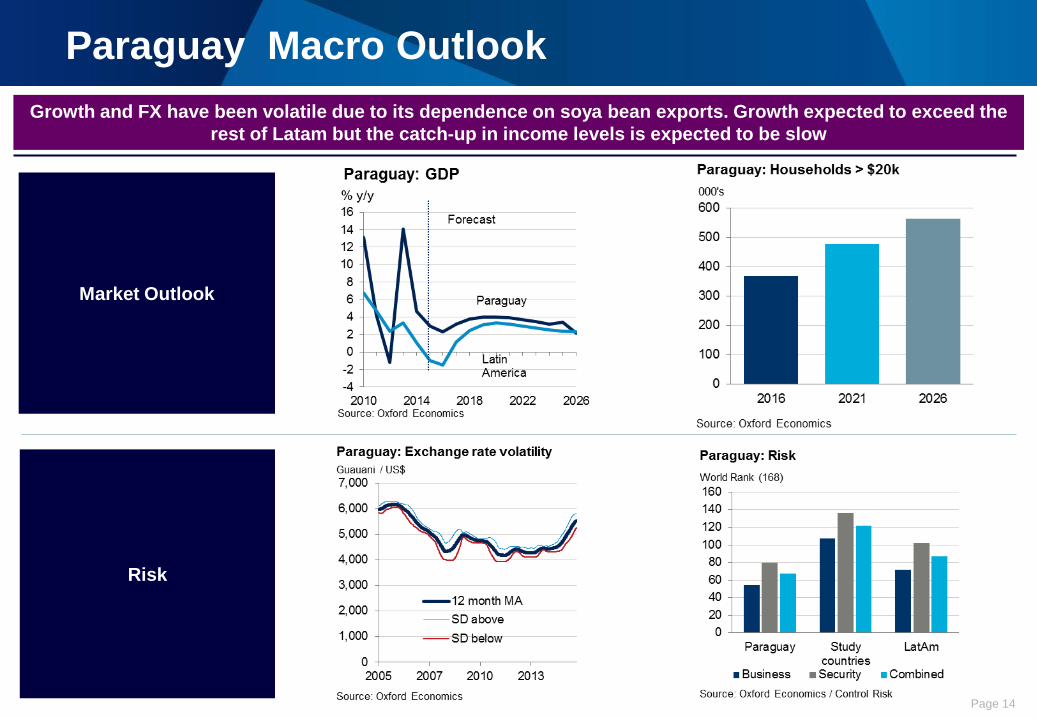

Paraguay Macro Outlook

Market Outlook

Risk

Growth and FX have been volatile due to its dependence on soya bean exports. Growth expected to exceed the

rest of Latam but the catch-up in income levels is expected to be slow

Page 15

Market Attractiveness

Costa Rica is least risky but biggest returns could be in Bolivia and Honduras

Market attractiveness

Note: The size of the bubble indicates total

consumption in a market

Note: Countries ranked by their score with a low rank meaning a country performs well. Economic growth is drawn from Oxford

Economics’ forecasts, exchange rate risk, security risk, political stability and social cohesion are taken from the Economic and

Political Risk Evaluator, and business environment, infrastructure and health & education are sourced from the World

Competitiveness Report from the World Economic Forum.

Costa Rica offers the least risky returns, although it is not the fastest growing nor largest market in the study.

Bolivia and Honduras are attractive from growth but risks are higher with infrastructure poor in both countries and security a

concern in Honduras.

Colombia and Guatemala are larger, more mature markets with some structural challenges and operational risks

Paraguay is relatively unattractive as a small market with very under developed infrastructure, a poor growth outlook and

volatile exchange rate. Poor security dominates the outlook in El Salvador.

Bolivia Colombia Costa Rica El Salvador Guatemala Honduras Paraguay

Economic Growth 1 4 3 7 5 2 6

Exchange Rate 2 3 7 1 5 4 6

Business environment 3 4 1 4 4 4 2

Security 1 4 1 7 5 5 17 15 12 19 19 15 15

Operational Environment 1 3 2 6 6 3 3

Infrastructure 6 4 2 1 3 5 7

Health and Education 6 4 1 3 5 2 7

Political 7 1 1 3 3 3 6

Social Cohesion 5 6 2 2 6 2 124 15 6 9 17 12 21

Structural Factors 7 4 1 2 5 3 6

Appendix

Page 17

GDP growth

-2

0

2

4

6

8

10

12

14

16

2010 2012 2014 2016 2018 2020 2022 2024 2026

Bolivia

Colombia

Paraguay

Source: Oxford Economics

% y/y

Forecast

South America GDP growth

0

1

2

3

4

5

6

2010 2012 2014 2016 2018 2020 2022 2024 2026

Costa Rica El Salvador

Guatemala Honduras

Source: Oxford Economics

% y/y

Forecast

Central America GDP growth

% y/y 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e 2024e 2025e 2026e

Bolivia 4.4 4.8 4.6 6.1 3.4 4.1 5.2 5.1 6.8 5.5 4.0 3.4 3.8 4.1 4.5 4.8 5.0 5.0 5.0 5.0 4.9 4.9

Colombia 4.7 6.7 6.9 3.5 1.7 4.0 6.6 4.0 4.9 4.4 3.1 2.6 3.0 3.7 3.7 3.7 3.7 3.5 3.5 3.5 3.3 3.3

Paraguay 2.3 4.7 5.5 6.2 -3.9 13.1 4.2 -1.2 14.0 4.7 2.9 2.3 3.2 3.8 4.0 4.0 3.9 3.7 3.5 3.2 3.4 2.2

Costa Rica 5.9 8.8 8.0 2.6 -0.9 4.9 4.4 5.1 3.6 3.5 2.8 3.8 4.2 4.1 4.0 3.9 3.8 3.6 3.4 3.4 3.4 3.4

El Salvador 3.6 3.9 3.8 1.3 -3.1 1.4 2.2 1.9 1.8 1.4 2.5 2.6 2.3 2.0 2.1 2.1 2.1 2.1 2.1 2.1 2.1 2.1

Guatemala 3.3 5.4 6.3 3.3 0.5 2.9 4.2 3.0 3.6 4.3 3.8 3.4 3.5 3.5 3.5 3.5 3.5 3.5 3.5 3.4 3.4 3.0

Honduras 6.0 6.6 6.2 4.2 -2.4 3.7 3.8 4.1 2.8 3.0 3.7 3.5 3.7 3.8 4.0 4.0 4.5 4.6 4.7 4.5 4.5 4.6

Source: Oxford Economics

Page 18

Households and household income

Total households

(millions) 2010 2011 2012 2013 2014 2015 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e 2024e 2025e 2026e

Bolivia 2.6 2.6 2.7 2.8 2.8 2.9 3.0 3.0 3.1 3.2 3.3 3.3 3.4 3.5 3.6 3.7 3.7

Colombia 12.2 12.5 12.7 13.0 13.3 13.6 13.9 14.2 14.4 14.7 15.0 15.3 15.5 15.8 16.1 16.3 16.6

Paraguay 1.4 1.4 1.5 1.5 1.5 1.6 1.6 1.6 1.7 1.7 1.7 1.7 1.8 1.8 1.8 1.9 1.9

Costa Rica 1.3 1.3 1.4 1.4 1.4 1.4 1.5 1.5 1.5 1.5 1.6 1.6 1.6 1.6 1.7 1.7 1.7

El Salvador 1.5 1.5 1.5 1.5 1.5 1.6 1.6 1.6 1.6 1.6 1.7 1.7 1.7 1.7 1.7 1.7 1.7

Guatemala 2.9 2.9 3.0 3.1 3.2 3.3 3.4 3.5 3.5 3.6 3.7 3.8 3.9 4.0 4.1 4.2 4.3

Honduras 1.6 1.6 1.7 1.7 1.7 1.8 1.8 1.8 1.9 1.9 1.9 2.0 2.0 2.1 2.1 2.2 2.2

Average household personal disposable income ($US at 2012 prices)

($ ‘000) 2010 2011 2012 2013 2014 2015 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e 2024e 2025e 2026e

Bolivia 6.6 6.8 7.0 7.3 7.5 7.7 7.8 8.0 8.2 8.4 8.6 8.8 9.0 9.2 9.4 9.7 9.9

Colombia 19.9 20.6 21.0 21.4 21.8 22.0 22.2 22.5 22.9 23.3 23.8 24.3 24.8 25.2 25.7 26.2 26.7

Paraguay 13.7 13.9 14.6 14.9 15.2 15.3 15.4 15.7 16.1 16.4 16.8 17.1 17.3 17.5 17.7 17.9 18.0

Costa Rica 23.3 23.7 24.2 24.5 24.8 25.1 25.7 26.4 27.1 27.8 28.4 29.1 29.7 30.4 31.0 31.7 32.1

El Salvador 16.6 16.8 16.9 16.8 16.8 16.8 17.0 17.1 17.3 17.5 17.6 17.8 18.0 18.2 18.4 18.5 18.7

Guatemala 16.3 16.4 16.4 16.5 16.6 16.8 16.8 16.9 17.0 17.1 17.3 17.3 17.4 17.7 18.0 18.2 18.4

Honduras 9.8 9.9 10.0 10.1 10.2 10.2 10.3 10.5 10.7 10.9 11.1 11.3 11.6 11.8 12.1 12.4 12.6

Source: Oxford Economics

Source: Oxford Economics

Page 19

Exchange rates

Exchange rates (vs. US $)

2010 2011 2012 2013 2014 2015 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e 2024e 2025e 2026e

Bolivia Bolivianos7.02 6.94 6.91 6.91 6.91 6.91 6.91 6.91 7.01 7.08 7.15 7.21 7.26 7.32 7.37 7.52 7.66

Colombia Pesos1,899 1,848 1,797 1,869 2,002 2,742 3,300 3,200 3,100 3,000 2,950 2,900 2,903 2,902 2,900 2,928 2,956

Paraguay Guaranies4,735 4,191 4,425 4,321 4,462 5,205 5,658 5,670 5,698 5,732 5,784 5,859 5,947 6,042 6,145 6,253 6,362

Costa Rica Colones526 506 503 500 538 535 552 571 590 608 624 642 660 677 696 709 723

Guatemala Quetzales8.06 7.79 7.83 7.86 7.73 7.65 7.82 7.98 8.10 8.23 8.36 8.49 8.63 8.77 8.93 9.10 9.28

Honduras Lempiras18.90 18.92 19.50 20.36 21.02 21.98 22.90 23.36 23.83 24.31 24.79 25.34 26.00 26.83 27.74 28.70 29.69

Source: Oxford Economics