Embed Size (px)

Citation preview

TECHNICAL REPORTUCED 2000/01-02

LEGAL AND ECONOMIC CONSIDERATIONS FOR

INCORPORATION OF NEVADA TOWNS

UNIVERSITY OF NEVADA, RENO

LEGAL AND ECONOMIC CONSIDERATIONS FOR

INCORPORATION OF NEVADA TOWNS

Prepared By:

George W. Borden

and

Thomas R. Harris

Nevada Cooperative ExtensionCenter For Economic Development

University of Nevada, Reno

George W. Borden is a Community Development Specialist, Nevada Cooperative Extension. Heis located in Las Vegas, Nevada.

Thomas R. Harris is a Professor in the Department of Applied Economics and Director of theUniversity Center for Economic Development at the University of Nevada, Reno.

August 2000

UNIVERSITYOF NEVADA

RENO

The University of Nevada, Reno is an Equal Opportunity/Affirmative Action employer and does not discriminate on the basisof race, color, religion, sex, age, creed, national origin, veteran status, physical or mental disability, and in accordance withuniversity policy, sexual orientation, in any program or activity it operates. The University of Nevada employs only UnitedStates citizens and aliens lawfully authorized to work in the United States.

This publication, Legal and Economic Considerations forIncorporation of Nevada Towns was published by the UniversityCenter for Economic Development in the Department of AppliedEconomics and Statistics at the University of Nevada, Reno.Funds for this publication were provided by the United StatesDepartment of Commerce Economic DevelopmentAdministration under University Centers Program contract #07-66-04742. This publication's statements, conclusions,recommendations, and/or data represent solely the findings andviews of the authors and do not necessarily represent the viewsof the U.S. Department of Commerce, the EconomicDevelopment Administration, the University of Nevada, Reno,or any reference sources used or quoted by this study. Referenceto research projects, programs, books, magazines, or newspaperarticles does not imply an endorsement or recommendation bythe authors unless otherwise stated. Correspondence regardingthis document should be sent to:

Thomas R. Harris, DirectorUniversity Center for Economic Development

University of Nevada, RenoDepartment of Applied Economics and Statistics

Mail Stop 204Reno, Nevada 89557-0105

UCEDUniversity of Nevada, Reno

Nevada Cooperative Extension

I. Introduction

Communities organize to provide services that residents cannot provide for themselvesindividually. To pay for these services, communities must have access to financial resources.The State of Nevada offers communities various options for managing their affairs. Three areaddressed in this paper: General Improvement Districts, Unincorporated Towns, andIncorporated Cities.

This paper is intended for use by any member of the public interested in learning more aboutoptions available to Nevada communities. The Nevada Revised Statutes are used as the primarysource of information. The interested reader will also want to refer to decisions by the NevadaSupreme Court regarding these statutes, the Nevada Administrative Code, the Nevada AttorneyGeneral and their district or city attorney.

II. General Improvement DistrictsA General Improvement District (GID) is created pursuant to NRS Chapter 318. These districts“serve a public use and will promote the health, safety, prosperity, security and general welfare”of their inhabitants. Their projects must be in the public interest. Each district is a “bodycorporate and politic and a quasi-municipal corporation. (NRS 318.015) Furthermore, the boardthat manages a GID has “all rights and powers necessary or incidental to or implied from thespecific powers granted” and “specific powers shall not be considered as a limitation upon anypower necessary or appropriate to carry out [its] purposes. . .” GIDs are included in this paperbecause they provide means of organizing a community’s resources that is similar toincorporation.

The board of county commissioners is in any county in Nevada has the “jurisdiction, power andauthority to create districts within the county it serves.” (NRS 318.050) The board ofcommissioners may adopt a resolution or consider a petition by a proposed property owner toinitiate the formation of a district. (NRS 318.050) Once the initiating ordinance has beenadopted, the property owners of the proposed district are notified and given the opportunity toprotest the formation of the district. If after considering the protests and determining that thedistrict is “required by public convenience and necessity” and that the creation of the district is“economically sound and feasible” the board of commissioners can adopt an ordinance creatingthe district. (NRS 318.055 to 318.075) The board of commissioners establishes the accountingand auditing practices and procedures for the district, a budget and management standards for thedistrict. In counties of fewer than 400,000 people, it has the option of appointing five people toserve as the first board of trustees for the district. These positions will be filled through generalelections hereafter. The board also has the option of serving as the ex officio board of trustees incounties with fewer than 400,000 people. In counties of more than 400,000 people, the board ofcommissioners is the ex officio board of trustees of the district.” (NRS 318.080 to NRS318.09533)

A. Powers of General Improvement DistrictsThere are twenty basic powers granted to general improvement districts. According to NRS318.116 “Any one, all or any combination of the following basic powers may be granted to adistrict . . .” These twenty powers are enumerated below. Please note that GIDs do not have theauthority to provide for police, planning, or zoning.

1. Furnishing electric light and power2. Extermination and abatement of mosquitoes, flies, other insects, rats, and liver fluke or

fasciola hepatica.3. Furnishing facilities or services for public cemeteries.4. Furnishing facilities for swimming polls.5. Furnishing facilities for television.6. Furnishing facilities for FM radio.7. Furnishing streets and alleys.8. Furnishing curb, gutter and sidewalks.9. Furnishing sidewalks.10. Furnishing facilities for storm drainage or flood control.11. Furnishing sanitary facilities for sewerage.12. Furnishing facilities for lighting streets.13. Furnishing facilities for the collection and disposal of garbage and refuse.14. Furnishing recreational facilities.15. Furnishing facilities for water.16. Furnishing fencing.17. Furnishing facilities for protection from fire.18. Furnishing energy for heating.19. Furnishing emergency medical services.20. Control and eradication of noxious weeds.

B. Access to RevenuesDepending on the specific purposes of the GID, the board may have the power to levy a generalad valorem tax, special assessments, establish tolls, rates and other service charges. The GIDmay also be able to borrow money and issue short-term notes, warrants, interim debentures,general obligation bonds, revenue bonds, and special assessment bonds. The ability of the boardto utilize debt will depend on the population and purpose of the district. (NRS 318) A districtmay be eligible for distributions from the state government if it provides two of the following:fire protection, road repair, maintenance and construction, or parks and recreation. (NRS360.740)

As mentioned previously, the total ad valorem tax levy for all public purposes must not exceed$3.64 on each $100 of assessed valuation. This also has implications for a GID, as any givenpiece of taxable property within its boundaries may be subject to tax by the state, county, town,other special districts, or school district. If a GID is being considered as one means of localorganization and ad valorem taxes are being considered as one source of possible revenue, thenthe $3.64 limit needs to be taken into consideration. It can be especially difficult for GIDs withlow assessed valuation of taxable property. To generate sufficient revenues, the GID in thissituation may have to levy higher ad valorem taxes than a local government with high assessed

valuation of taxable property. Once the statutory limit of $3.64 is reached, generating additionalrevenue can be difficult. Local governments may find themselves feuding. Disputes that cannotbe resolved by the local governments themselves will be resolved by the Tax Commission. (NRS361.455)

C. Cooperative AgreementsA GID may not find it financially feasible to pay for all of the services it would like to provide.According to NRS 277.045, counties, incorporated cities, unincorporated towns, school districts,and other special districts may into enter cooperative agreements to provide governmentalfunctions. These agreements may involve use of property, equipment or personnel. A GID maynot have to make the capital expenditures necessary to build new structure, purchase equipmentor hire additional staff. It may be able to reach an agreement with the county to use existingstructures, equipment, and staff as necessary for a fee.

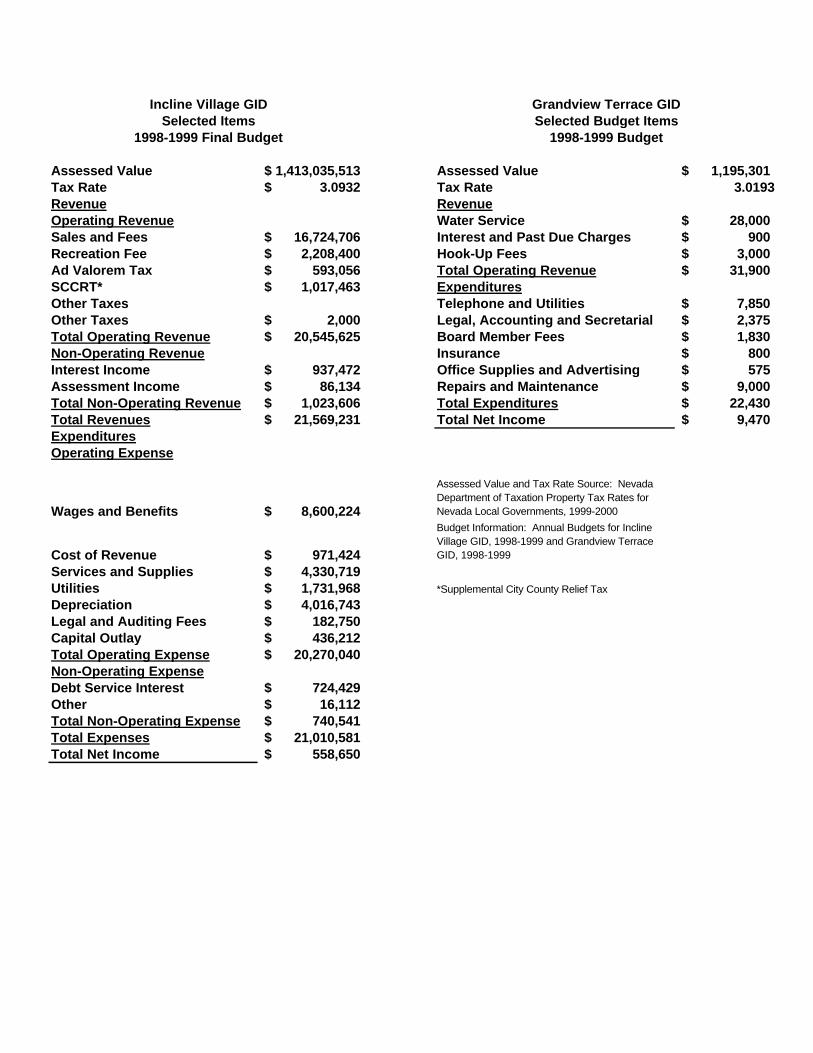

D. Budget Examples for Selected General Improvement DistrictsSelected budget items from two General Improvement Districts are presented below to show thevariety of services that GIDs offer as well as their means of paying for them. Incline Village isorganized as a GID and offers an extensive array of services with an equally extensive means offinancing those activities. Grandview Terrace is a small GID organized to provide water serviceto its residents. Its revenues consist mainly of user fees.

Any community considering forming a GID should carefully consider the services it wants toprovide as a GID as well as the most appropriate means of financing those services. Asmentioned above, sources of revenue may include property taxes, special assessments, tolls,rates, services charges, intergovernmental revenues from the state, and grants. If a GID plans touse property tax as a means of generating revenue, it must also be concerned about the NevadaRevised Statute limit of $3.64 of total property tax for every $100 of assessed value. There maybe complications that arise with the county and other political entities, such as towns, cities, andother districts, as they all vie for right to levy property tax within that limit.

Incline Village GID Grandview Terrace GIDSelected Items Selected Budget Items

1998-1999 Final Budget 1998-1999 Budget

Assessed Value 1,413,035,513$ Assessed Value 1,195,301$ Tax Rate 3.0932$ Tax Rate 3.0193Revenue RevenueOperating Revenue Water Service 28,000$ Sales and Fees 16,724,706$ Interest and Past Due Charges 900$ Recreation Fee 2,208,400$ Hook-Up Fees 3,000$ Ad Valorem Tax 593,056$ Total Operating Revenue 31,900$ SCCRT* 1,017,463$ ExpendituresOther Taxes Telephone and Utilities 7,850$ Other Taxes 2,000$ Legal, Accounting and Secretarial 2,375$ Total Operating Revenue 20,545,625$ Board Member Fees 1,830$ Non-Operating Revenue Insurance 800$ Interest Income 937,472$ Office Supplies and Advertising 575$ Assessment Income 86,134$ Repairs and Maintenance 9,000$ Total Non-Operating Revenue 1,023,606$ Total Expenditures 22,430$ Total Revenues 21,569,231$ Total Net Income 9,470$ ExpendituresOperating Expense

Wages and Benefits 8,600,224$

Assessed Value and Tax Rate Source: Nevada Department of Taxation Property Tax Rates for Nevada Local Governments, 1999-2000

Cost of Revenue 971,424$

Budget Information: Annual Budgets for Incline Village GID, 1998-1999 and Grandview Terrace GID, 1998-1999

Services and Supplies 4,330,719$ Utilities 1,731,968$ *Supplemental City County Relief Tax

Depreciation 4,016,743$ Legal and Auditing Fees 182,750$ Capital Outlay 436,212$ Total Operating Expense 20,270,040$ Non-Operating ExpenseDebt Service Interest 724,429$ Other 16,112$ Total Non-Operating Expense 740,541$ Total Expenses 21,010,581$ Total Net Income 558,650$

III. Unincorporated TownsNRS Chapters 269 and 244 contain the statutes providing for and limiting the power of board ofcounty commissioners and other boards to manage the affairs of and provide for unincorporatedtowns. The county and any other boards that may participate in the management of the town’saffairs are limited to those powers stated or inferred from these statutes.

As provided for in NRS 269, the board of county commissioners may oversee the affairs of anyunincorporated town. However, the citizens of those towns have the option of more specificcontrol. A discussion of these three options follows.

A. Town Board Form of GovernmentNRS 269.016 to 269.022 provides for the creation town boards. Any unincorporated town mayestablish a town board form of government according to these statutes. (NRS 269.016)According to NRS 269.0165, the residents of a town may submit a petition requesting a townboard form of government to the board of county commissioners. The board of countycommissioners may either adopt the proposal or submit the proposal to the electors for theirapproval. If the town board form of government is adopted, then the commissioners will appointfive residents and qualified electors to serve on the board until the next general election when thetown will elect the next five members (NRS 269.017) The town board can be discontinued whenthe board of county commissioners puts that question on the ballot in a general election (NRS269.022)

A town board may adopt all ordinances, rules, and regulations and perform all other actsnecessary for the execution of the powers and jurisdiction conferred NRS Chapter 269 (NRS269.155) as well as revise and codify those ordinances into a town code. (NRS 269.166 to269.169) It can punish breaches of ordinances. (NRS 269.160)

The town board may provide the following for the unincorporated town. The board of countycommissioners may also provide these.

1. Fire Protection (NRS 269.250 to 269.270)2. Police Protection (NRS 269.235 to 269.247)3. Public Works (NRS 269.400 to 269.470).4. Television or FM radio broadcast translator signals (NRS 269.127 and NRS 269.575)5. Manage, use and sell property (NRS 269.125)6. Limit competition by providing or franchising for the following (NRS 269.128 and

269.129)a. Ambulance Serviceb. Public transportation or taxi cabsc. Waste disposald. Operations at an airport (excluding police and fire protection but may include car

rental and concession stands)

e. Water and Sewage Treatment (unless regulated in that town by an agency of thestate)

f. Concessions on property owned or leased by the towng. Landfills

7. Business licenses (NRS 269.170)8. Regulate vehicle traffic (NRS 269.185)9. Board of Health (NRS 269.190)10. Keeping of animals (NRS 269.195 TO 269.200 and 269.227)11. Nuisances (NRS 269.205 to 269.210)12. Loitering and prowling (NRS 269.217)13. Disorderly Conduct (NRS 269.215)14. Regulation of storage of explosive and combustible materials (NRS 269.220)15. Regulate discharge of firearms (NRS 269.222)

B. Town Advisory BoardAn unincorporated town may also be managed in part by a Town Advisory Board. The residentsof an unincorporated area of a county can either petition the board of county commissioners tobegin the process or placed directly on a ballot providing that certain criteria are met. (NRS269.540 and 269.545) If the petition is brought to the board and meets the necessary criteria, theboard may pass an ordinance thus forming the unincorporated town (NRS 550). The board ofcounty commissioners also has the option of putting the question to the voters in the nextprimary or general election. (NRS 269.550) If the voters approve the question, the board canproceed with the formation of the unincorporated town by ordinance. This ordinance mustcontain the “boundaries, a listing of the services to be provided, and the number of members tobe on the town advisory board.” (NRS 269.560) This original ordinance may be amended laterto adjust the list of services provided. (NRS 269.570) NRS Chapter 269.575 provides a list ofpossible services that may be provided by an unincorporated town. These include the following:

1. Cemetery2. Dump stations and sites3. Fire protection4. Flood control and drainage5. Garbage collection6. Police7. Parks8. Recreation9. Sewage collection10. Streets11. Street lights12. Swimming pools13. Television translator14. Water distribution15. Acquisition, maintenance and improvement of town property.

The Town Advisory Board may have three to five members. Its duties are to “assist the board ofcounty commissioners in governing the unincorporated town by acting as liaison between theresidents of the town and the board of county commissioners” and “advise the board of countycommissioners on matters of importance to the unincorporated town and its residents.” (NRS269.576 and 269.577) Additionally, the board of county commissioners of any county maydesignate one or more of the town services to be “within the power of a town advisory board tomanage.” (NRS 269.580) The board of county commissioners is obligated to “solicit the adviceof the town advisory board in preparation of the tentative budget for the town affected” and“allow towns to recommend their own ordinances and codes.” (NRS 269.590) The board ofcounty commissioners may also allow the town advisory board to “control any expenditureswhich are a part of a county-approved budget.” (NRS 269.590) The Town Advisory Board mayalso be given control of unappropriated money available through the county for town purposes to“be expended at [its] discretion.” (NRS 269.595)

C. Citizens’ Advisory CouncilIf the board of county commissioners is the governing body of an unincorporated town, the boardcan create a Citizens’ Advisory Council (NRS 269.024). The council consists of three to fivemembers who are residents and qualified electors in the town. It shall “assist the board of countycommissioners in governing the town by acting as liaison between the residents of the town andthe board.” The council cannot expend or contract any town money for any purpose. Itsmembers serve without compensation. The existence of a Citizens’ Advisory Council in no wayaffects the responsibilities of the board of commissioners. (NRS 269.024 to NRS 269.0248)

D. Cooperative AgreementsAn unincorporated town may not find it financially feasible to pay for all of the services it wouldlike to provide. According to NRS 277.045, counties, incorporated cities, unincorporated towns,school districts, and other special districts may into enter cooperative agreements to providegovernmental functions. These agreements may involve use of property, equipment orpersonnel. For example, an unincorporated town may not the funds necessary to make thecapital expenditures necessary to build new structures, purchase equipment or hire additionalstaff. It may be able to reach an agreement with the county to use existing structures, equipment,and staff as necessary for a fee.

E. Sources of Revenue Available to Unincorporated Towns

1. Property TaxProperty tax, also referred to as the Ad Valorem Tax, is an important source of revenue for localgovernments. Real and personal property in Nevada can be assessed for taxation. There areexceptions, but generally property subject to taxation must be assessed at 35% of its taxablevalue. Furthermore, the total ad valorem tax levy for all public purposes must not exceed $3.64on each $100 of assessed valuation. This has serious implications for local government. Forexample, any given piece of taxable property may be subject to tax by the state, county, town,special district, or school district. A local government seeking to levy a new ad valorem tax will

need to take this limit into consideration. It can be especially difficult for local governmentswith low assessed valuation of taxable property. To generate sufficient revenues, the localgovernment in this situation may have to levy higher ad valorem taxes than a local governmentwith high assessed valuation of taxable property. Once the statutory limit of $3.64 is reached,generating additional revenue can be difficult. Local governments may find themselves feuding.Disputes that cannot be resolved by the local governments themselves will be resolved by theTax Commission. (NRS 361.455)

According to NRS 269.120 the board of county commissioners “assess, fix, and designate theamount of taxes that should be levied and collected for city or town purposes on all real andpersonal property assessable for state or county purposes within any town or city in theircounty.” In practice, as part of the budgeting process, the town board would submit theirrequest(s) for taxes to be levied to the county commissioners. Towns have access to the fundsset aside for them pursuant to NRS 269.095. For example, if a general ad valorem tax isassessed on a particular unincorporated town, that money is to be used solely for the benefit ofthat town by the governing body of that town, e.g., the town board.

The board of county commissioners can levy and collect taxes on assessable real and personalproperty within any town or city within their county (NRS 269.120.) There are exceptions, butgenerally the board of county commissioners “shall levy a tax, not exceeding 1.5% per annum”upon the assessed value of all real and personal property situated in any unincorporated town” intheir respective county (NRS 269.115)

2. Intergovernment Revenues/Consolidated Tax DistributionIn 1997, the State Legislature created the Local Government Tax Distribution Fund. Thisrevenue is distributed to local governments as Consolidated Tax Distributions. This fund iscomprised of Revenues from the following taxes:

1. Supplemental City-County Relief Tax (SCCRT) 1.75% of all taxable sales and taxableitems of use. Ninety-nine percent of total collections returned to local governmentsthrough the Consolidated Tax Program.

2. Basic City-County Relief Tax (BCCRT) One-half of 1% of all taxable sales and taxableitems of use. Ninety-nine percent of in-state collections returned to eligible localgovernments through the Consolidated Tax Program.

3. Cigarette Tax: 17.5 mills per cigarette or 30% of manufacturers’ wholesale price of othertobacco. Five mills per cigarette for distribution to eligible local governments throughthe Consolidated Tax Program, less administrative fees.

4. Liquor Tax: Various rates and licenses. 50cents per gallon of collections on over 22%alcohol allocated for distribution to eligible local governments through the ConsolidatedTax Program.

5. Motor Vehicle Privilege Tax:6. Real Property Transfer Tax (RPTT)

An unincorporated town can receive intergovernmental transfers from the state government.(NRS 360.660). To be eligible the town must have received some distribution before July 1,1998 (NRS 360.670). If a local government is created after July 1, 1998 and that body offers

police protection and fire protection, construction, maintenance, road repair, or parks andcreation, then the new local government can request to the executive director of the Nevada taxcommission to receive intergovernmental transfers (NRS 360.740)

An unincorporated town may also receive funds from the county.

3. Licenses, Permits, and Franchise FeesUnincorporated towns may collect revenue through licenses, permits, and franchise fees.Examples include business licenses and animal fees. liquor licenses, gaming licenses, andbuilding permits. If an unincorporated town offers a franchise to a particular business to providea service for the town, e.g., ambulance service, then the town will also collect a franchise fee forgiving that business the exclusive right to provide that service in the town.

4. Charges for servicesTowns may charge for the use of town property. Examples of charges in this area include feescollected at a swimming pool or cemetery.

5. Proprietary/Enterprise FundsThe unincorporated town may provide certain services for fees. These operate in a mannersimilar to private businesses. The cost of providing the goods or services is covered primarilythrough user charges. Examples of these services might include water and sewer, solid wastedisposal, and electricity.

6. GrantsUnincorporated towns may also receive grants. Grants may be available from the state and/orthe federal governments. Typically, grant money must be spent according to the specific termsof the grant proposal and the city must match all or part of the grant funds with its own money.An example of a grant a town might receive is a community development block grant. A grantwill probably be included as intergovernmental revenue in the fiscal budget.

7. Capital RevenuesCapital revenues include the sale of bonds and interest earned on town investments. Towns mayacquire debt through the sale of bonds with certain limitations. For example, according to NRS269.425, a town cannot become indebted for public works projects for an amount exceeding 25%of the total last assessed valuation of the taxable property of the town. Refer to the severalreferences in the NRS for more information on bonds.

F. Budget ExpendituresThe following are budget expense items typical to unincorporated towns in Nevada (Townbudgets for Tonopah, Pahrump, Minden, and Gardnerville)

1. General Government: Town Board, Administration, Buildings and Grounds2. Public Safety3. Public Works4. Culture and Recreation

5. Community Support6. Cemetery7. Capital Projects8. Highways and Streets9. Television10. Debt Service

IV. Incorporated CitiesThe Nevada Constitution provides the authority for the creation of municipal corporations inArticle 8 section 8. For the purposes of this paper, a municipal corporation is the same as anincorporated city. An incorporated city is a legal, political, and economic entity. A cityexercises its legal, political, and economic authority for the public good of the citizens whoreside within its boundaries. It passes and enforces laws, provides services, and raises money topay for the costs of civil government. A city is the creation of the state, as are counties andschool districts. Cities are not subordinate to counties. (Povolny, 1981)

A. Incorporating Under NRS 266The legislature has provided for the specific means of organizing an incorporated city in theNevada Revised Statutes (NRS) Chapter 266.005 to 266.050. It is an extensive process. A noticeto organize an incorporated city must be filed with the county clerk (NRS 266.018). A petition isthen circulated and verified and reviewed by the county clerk, board of county commissioners,committee on local government finance, department of taxation, and any “state, county, orregional planning commission or agency that exercises planning authority over any part of thearea proposed to be incorporated and to every other local government within the county.”(NRS266.0261) There must be public hearings. According to NRS 266.0285 the board of countycommissioners must take into account a number of factors for the incorporation of the proposedcity including:

1. Population and density of population2. Land area, uses, topography, natural boundaries and drainage basin3. Use of area by agriculture and mineral production4. Extent of commercial and industrial development5. Extent and age of residential development6. Comparative size and assessed value of subdivided and unsubdivided land7. Current and potential issues regarding transportation8. Past expansion of population and construction9. Likelihood of significant growth in the area and in adjacent incorporated and

unincorporated areas during the next 10 years10. Present cost, method and adequacy of regulatory controls and governmental service, e.g.,

water and sewer service, fire rating and protection, police protection, improvement andmaintenance of streets, administrative services and recreational facilities and the futureneed for such services and controls.

11. Present and projected revenues for the county and proposed city12. Probable effect of incorporation and of any alternatives to incorporation on the social,

economic and government structure of the affected county and the proposed city.

13. The probably effect of incorporation on revenues and services in the county and localgovernments in adjacent areas.

14. The probably effect of the proposed incorporation and of any alternatives to incorporationon the availability and requirement of water and other natural resources

15. Any determination by a governmental agency that the area is suitable for residential,commercial or industrial development, or that the area will be opened to privateacquisition.

16. The recommendations of any commission, agency, district or member of the public whosubmits a written report.

17. Testimony from any person who testifies at a hearing18. Existing petitions for annexation of any part of the area.

If the proposed city is located within five miles of an existing city, the board of countycommissioners must also take into consideration:

1. The size and population of the existing city2. Growth in population and commercial and industrial development in the existing city

during the past 10 years.3. Any extension of the boundaries of the existing city during the past 10 years.4. The probability of growth of the existing city toward the area proposed to be incorporated

in the next 10 years, considering natural barriers and other factors that might influencesuch growth.

5. The willingness of the existing city to annex the area proposed for incorporation and toprovide services to the area.

The board of county commissioners will issue its opinion in writing considering and advisabilityof incorporating and the feasibility of that proposed city and will make arrangements for anelection (NRS 266.029). If the ballot question passes, another election is held to elect theofficers of the city (NRS 266.036.) Once the officers are elected, Articles of Incorporation mustbe filed, and a budget must be prepared, ordinances adopted, and property tax levied. Theofficers must also negotiate equitable apportionment of the fixed assets of the county, contractsfor employment of personnel, services, and the purchase of equipment, materials and supplies(NRS 266.039 to 266.041)

NRS 266.034 provides for the liability of the costs of incorporation. Generally speaking, if thecity is not incorporated, these costs are a charge against the county. If the city is incorporated,these costs are a charge against the newly incorporated city. These expenses can include thecosts of certifying the petition, publishing notices, requesting the report on items 1-18 and 1-5above, conducting the public hearing and election, the mailing of sample ballots and any appealspermitted by NRS 266.0265.

Once incorporated, a city is classified as first, second, and third class according to NRS 266.055.First class cities have more than 20,000 residents. Second class cities have more than 5,000 andfewer than 20,000 inhabitants. All cities with fewer than 5,000 residents are classified as thirdclass. As provided for in NRS 266.095, first class cities are further organized into 8 wards of thesame approximate population and compact formation. Second and third class cities have the

option of further organizing into wards and may organize into 3 or 5 wards, depending on theirordinances.

Cities organized under NRS Chapter 266 are managed by a mayor and council. The mayor is thechief executive of the city. The mayor’s office, general powers and duties, and authority andprovided for specifically in NRS 266.165 through NRS 266.200. Generally speaking, the mayorsupervises the affairs of the city and provides information and makes recommendations to thecouncil. The mayor is the presiding officer of the council, has the right to veto matters passed bythe council, and approve all resolutions and ordinances.

City councils are discussed specifically in NRS 266. In first class cities, there are 9 councilmembers with one member elected from each ward and one elected by the city at large. In citieswith 3 or 5 wards, one councilmen is elected from each ward. If a city is not divided into wards,the councilmen are elected by the voters of the city at large. NRS 266.105 gives city councils thepower to “make and pass all ordinances, resolutions and orders, . . .. necessary for the municipalgovernment and the management of the city affairs, for the execution of all powers vested in thecity” and to “enforce obedience to such ordinances.”

B. Incorporating Under NRS 267A city may also exercise the option of adopting the commission form of government instead ofthe mayor-council government provided for in NRS Chapter 266. One of the main differencesbetween cities organized under 267, is that the voters do not elect a mayor. In the city’s charter,the number of commissioners, their terms of office, duties, and compensation are determined.The commission handles all affairs of the city.

C. Incorporating With A Special CharterA third option for incorporating involves presenting a draft city charter to the county’slegislators, the assemblymen and senators. The legislators can have the charter introduced as abill at the next meeting of the legislature. The legislature may approve or not approve thecharter. It may also decide to amend the charter before approving it. The mayor and council ofthe newly created city have their powers conferred upon them by the legislature. (Povolny, 1981)This method of incorporating may seem simpler; however, the same level of research andplanning as required by NRS 266 should be completed to help ensure the success of the city.

At the present time, there are 18 cities incorporated in Nevada. These cities are listed in Table 1.

Table 1. Incorporated Cities in NevadaBoulder City Gabbs SparksCaliente Henderson WellsCarlin Las Vegas YeringtonCarson City North Las Vegas FallonElko Reno MesquiteEly Lovelock Winnemucca

Italics denote city organized by special charter.

D. Authority of Incorporated CitiesThrough the Nevada Constitution, Article VIII, Sections 1 and 8, the legislature has the power toregulate municipal corporations. Cities have the authority to make and pass ordinances for theirgeneral welfare. They are not limited by statute, as are counties and unincorporated towns. Forexample, the city council of cities incorporated under NRS Chapter 266 have “the power to makeand pass all ordinances, resolutions and orders . . . necessary for the municipal government andthe management of the city affairs, for the execution of all powers vested in the city . . .” (NRS265.105) The commissioners of a city organized under NRS Chapter 267 have similar power inthat they have “. . .all of the powers which are now or may hereafter be conferred uponincorporated cities. . .” (NRS 267.120)

Cities chartered through the state legislature have similar wording included in their charters. Forexample, the preamble for the charter for the City of Elko states, “In order to provide for theorderly government of the City of Elko and the general welfare of its citizens the legislaturehereby establishes this charter for the government of the City of Elko. Furthermore, theircharter states that the “board of supervisors may make and pass all ordinances, resolutions, andorders . . . necessary for the municipal government and the management of the affairs of the cityand for the execution of all the powers vested in the city.”

Although cities are able to pass and enforce ordinances for their general welfare, the statutes doprovide for specific issues they may also control. A list of these is included below.

1. Community Development (NRS 268.745 to 268.761)2. 911 Emergency Service Phone Number (NRS 268.765 to NRS 268.777)3. Redevelopment or Urban Renewal (NRS Chapter 279 and NRS Chapter 268.780 to

268.785 and NRS 268.79 to NRS 268.795)4. Central Business Area (268.801 to 268.808)5. Pedestrian Malls (NRS 268.810 to 268.823)6. Public Works (NRS 266.261 to 266.263)7. Control City Property (NRS 266.265 to 266.267)8. Condemn property for public uses (NRS 266.270)9. Streets, sidewalks, parks, and public grounds (NRS 266.275)10. Traffic and parking (NRS 266.277 and 266.280)11. Utilities (266.285, 266.290)12. Railroads and railways (NRS 266.295)13. Franchises for public purposes (NRS 266.300)14. Fire Department (NRS 266.310)15. Cemeteries (NRS 266.316)16. Police (NRS 266.321)17. Control of Animals (NRS 266.325)18. Public health (NRS 266.330)19. Nuisances (NRS 266.335)20. Regulate and license professions, trades and businesses (NRS 266.355 to NRS 366.368)21. Sell and lease city-owned electric light and power systems (NRS 266.386 to 266.3867)

22. Establish offices and officers for the city, including city attorney, city clerk, city auditorcity treasurer, and chief of police (NRS 266.390 to 266.530)

23. Municipal Courts (266.550 to 266.595)

As provided for in NRS 266.600, the city council controls the finances of the city. It canappropriate money for city purposes and provide for the expenses of the city and the city’s debt.It can levy taxes, fees, and fines, and issue debt.

E. Cooperative AgreementsCities may not find it financially feasible to pay for all of the services they would like to provide.For example, a city may not be able to afford to build a new structure to house its municipalcourt system or even to employ an entire staff to manage that system. NRS Chapter 277 allowsfor some alternatives. According to NRS 277.045, counties, incorporated cities, unincorporatedtowns, school districts, and other special districts may into enter cooperative agreements toprovide governmental functions. These agreements may involve use of property, equipment orpersonnel. A city may not have to make the capital expenditures necessary to build a newstructure or hire a full-time staff. It may be able to reach an agreement with the county to use itscourtroom and staff as necessary for a fee.

F. Access to financial resources

1. Property TaxAccording to NRS 269.120 the board of county commissioners “assess, fix, and designate theamount of taxes that should be levied and collected for city or town purposes on all real andpersonal property assessable for state or county purposes within any town or city in theircounty.” In practice, as part of the budgeting process, the city council or city commissionerswould submit their request(s) for taxes to be levied to the county commissioners. Cities haveaccess to the funds set aside for them pursuant to NRS 269.095. For example, if a general advalorem tax is assessed on a particular city, that money is to be used solely for the benefit of thatcity by the governing body of that city, e.g., the city councilor city commissioners.

A city may levy and collect taxes within the city on real and person property. NRS 266.650limits the levy to taxes annually to not exceed 3% of the assessed value of all taxable real estateand personal property within the city. There are exceptions, but generally property subject totaxation must be assessed at 35% of its taxable value. Furthermore, the total ad valorem tax levyfor all public purposes must not exceed $3.64 on each $100 of assessed valuation. This hasserious implications for local government. For example, any given piece of taxable propertymay be subject to tax by the state, county, city, special district, or school district. A localgovernment seeking to levy a new ad valorem tax will need to take this limit into consideration.It can be especially difficult for local governments with low assessed valuation of taxableproperty. To generate sufficient revenues, the local government in this situation may have tolevy higher ad valorem taxes than a local government with high assessed valuation of taxableproperty. Once the statutory limit of $3.64 is reached, generating additional revenue can be

difficult. Local governments may find themselves feuding. Disputes that cannot be resolved bythe local governments themselves will be resolved by the Tax Commission. (NRS 361.455)

2. Intergovernment Revenues – Consolidated TaxIn 1997, the State Legislature created the Local Government Tax Distribution Fund. Thisrevenue is distributed back to local governments as Consolidated Tax Distribution. This fund iscomprised of Revenues from the following taxes:

1. Supplemental City-County Relief Tax (SCCRT) 1.75% of all taxable sales and taxableitems of use. Ninety-nine percent of total collections returned to local governmentsthrough the Consolidated Tax Program.

2. Basic City-County Relief Tax (BCCRT) One-half of 1% of all taxable sales and taxableitems of use. Ninety-nine percent of in-state collections returned to eligible localgovernments through the Consolidated Tax Program.

3. Cigarette Tax: 17.5 mills per cigarette or 30% of manufacturers’ wholesale price of othertobacco. Five mills per cigarette for distribution to eligible local governments throughthe Consolidated Tax Program, less administrative fees.

4. Liquor Tax: Various rates and licenses. 50cents per gallon of collections on over 22%alcohol allocated for distribution to eligible local governments through the ConsolidatedTax Program.

5. Motor Vehicle Privilege Tax:6. Real Property Transfer Tax (RPTT)

A city can receive intergovernmental transfers from the state government. (NRS 360.660). Tobe eligible the city must have received some distribution before July 1, 1998 (NRS 360.670). Ifa local government is created after July 1, 1998 and that body provides police protection andeither fire protection, construction, maintenance, and road repair, or parks and creation, then thenew local government can request to the executive director of the Nevada tax commission toreceive intergovernmental transfers (NRS 360.740)

The city council may also request funds from the county commissioners for roads (NRS255.610).

3. Licenses, Permits, and Franchise FeesCities may collect revenue through licenses, permits, and franchise fees. Examples includebusiness licenses, liquor licenses, gaming licenses, and building permits. If a city offers afranchise to a particular business to provide a service for the city, e.g., concessions at the airport,then the city will also collect a franchise fee for giving that business the right to do business atthe city airport.

4. Charges for servicesCities may charge for the use of city property. Examples of charges in this area include feescollected at a golf course, swimming pool, cemetery, or civic center.

5. Proprietary Funds/Enterprise DistrictsCities may establish enterprise districts. These operate in a manner similar to private businesses.The cost of providing the goods or services is covered primarily through user charges. Examplesof enterprise funds include water works, sewer, solid waste disposal, and electricity.

6. Fines/ForfeituresFines imposed by the municipal court, as well, as bail bond fee, are revenue for cities.

7. GrantsCities may also receive grants. Grants may be available from the state and/or the federalgovernment. Typically, grant money must be spent according to the specific terms of the grantproposal and the city must match all or part of the grant funds with its own money. As a budgetitem, grants are usually included as intergovernmental revenues.

8. Capital RevenuesCapital revenues include the sale of bonds and interest earned on city money. The city mayborrow money; however, except for the procurement of water supplies, the city cannot haveoutstanding bonds exceeding 30% of the total assess valuation of the taxable property of the city.It cannot have warrants, certificates, scrip or other debt, except bonded indebtedness, in excess of20% of assessed valuation (NRS 266.600). There are several statutes regarding bondingincluding NRS Chapters 268, 271, and 350. (Povolny, 1981)

G. Municipal ExpendituresThe following are budget expense categories typical to cities in Nevada (City Budgets of Elko,Lovelock, Carlin, and Yerington)

1. General Government Functions: Administration, Clerk, Personnel, Information Systems,Finance, Insurance, Planning, Zoning

2. Municipal Court3. Public Safety: Dispatch, Police, Fire4. Public Works: Streets, Engineering, Fleet Maintenance, Building Department, Facilities

Maintenance,5. Health Function: Animal Shelter, Other Health, Cemetery6. Community Services7. Airport8. Recreation9. Capital Construction10. Debt Service11. Water Service12. Sewer13. Landfill

V. Budget Comparisons for Incorporated Cities and UnincorporatedTownsSelected budget items from four incorporated cities and four unincorporated towns ofcomparable populations have been included. Revenues and expenditures from their FY 1998-1999 budgets have been included. Money transfers in and out of funds with surpluses anddeficits were not included in these figures. Consequently, the some of the budgets show thecommunities operating with revenues exceeding expenditures. Information on enterprise funds,or proprietary funds as they are also referred, was included when it was available. The assessedproperty values, tax rates, and populations of the communities are provided for additionalcomparisons.

A. The City of Carlin and the Town of MindenThe City of Carlin and the Town of Minden are two communities of similar size. Carlin’spopulation is estimated to be 2680 and Minden’s population is approximately 2400. As a city,Carlin received more money from the Consolidated Tax Distribution (CTD) ($864,903) thandoes than did the Town of Minden ($254,239). Carlin’s share of the CTD was also a muchlarger percentage of its budget (49%) than was Minden’s share (13%). Despite these differences,Carlin and Minden had budgets of similar size, $1,779, 459 and $1,910,755 respectively.Minden did not receive as much in CTD, but it did take in more revenue in property tax($419,757) than did Carlin ($243,904). Minden also collected more revenue through proprietaryfunds for the services it provides. For example, Minden collected $476,484 for providing waterwhile Carlin collected only $182,912. Minden collected $380,602 in trash fees while Carlincollected only $62,022 for its garbage utility.

Carlin and Minden had similar expenditures, $2,172,750 and $2,130,827 respectively. Carlinsplits its largest budget expenditures between expenses for its Proprietary Funds (30%), PublicSafety (23%) General Government (20%) and Public Works (18%). Minden’s biggest budgetexpenditure is for General Government (45%) followed by expenses for its Proprietary Funds(32%) and Community Support (20%).

Only the residents of these communities can know for certain if their local governments aremeeting their needs. This comparison provides an excellent example of how two communities ofsimilar size can have budgets of comparable amounts yet have markedly different sources ofrevenue and choose very different uses for those revenues.

City of CarlinSelected Budget Items, 1998-1999

Population 2680Assessed Value $ 20,816,391Property Tax Rate 3.5834Revenues PercentageProperty Taxes $ 243,904 14%Licenses and Permits $ 53,007 3%Intergovernmental Resources $ 939,362 53%Consolidated Tax Distribution $ 864,903 49%County Gaming License $ 9,278 1%MV Fuel Tax $ 62,861 4%Real Property Transfer Tax $ 1,263 0.1%Grants $ 1,057 0.1%Charges for Services $ 21,339 1%Water Utility $ 182,912 10%Garbage Utility $ 62,022 3%Sewer Utility $ 169,863 10%Street Light Fees $ 14,797 1%Fines and Forfeits $ 34,451 2%Miscellaneous $ 57,802 3%Total Revenues $ 1,779,459 100%ExpendituresGeneral Government $ 435,650 20%Public Safety $ 499,102 23%Public Works $ 395,733 18%Health $ 34,949 2%Culture and Recreation $ 72,242 3%Community Support $ 60,741 3%Utility Expenses Incl. Depreciation $ 642,717 30%Debt Service $ 31,616 1%Total Expenditures $ 2,172,750 100%Excess of Revenues Over (Under) Expenditures $ (393,291)

Population Source: Nevada Department of Taxation Annual Report, Fiscal 1998-1999

Assessed Value: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-2000

Property Tax Rate: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-20000

Budget Figures: City of Carlin Budget, 2000-2001

Town of MindenSelected Budget Items, 1998-1999

Population 2400Assessed Value 93,874,364Property Tax Rate 2.7864Revenues PercentageProperty Tax $ 419,757 22%Intergovernmental Revenue $ 486,029 25%Consolidated Tax Distribution $ 254,239 13%County Gaming License $ 58,613 3%Distribution from County $ 22,794 1%Community Development Block Grant $ 150,383 8%Charges for Services $ 17,332 1%Miscellaneous Revenue $ 130,551 7%Proprietary Fund: Trash Fees $ 380,602 20%Proprietary Fund: Water $ 476,484 25%Total Revenues $ 1,910,755 100% Expenditures General Government $ 949,971 45% Culture and Recreation $ 82,730 4% Community Support $ 415,826 20% Proprietary Fund: Trash Operating Expenses $ 280,983 13% Proprietary Fund: Water Operating Expenses $ 401,317 19%Total Expenditures $ 2,130,827 100% Revenues Over (Under) Expenditures $ (220,072)

Population Source: Nevada Department of Taxation Annual Report, Fiscal 1998-1999

Assessed Value: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-2000

Property Tax Rate: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-20000

Budget Figures: Town of Minden Budget, 2000-2001

B. The City of Lovelock and the Town of GardnervilleThe City of Lovelock and the Town of Gardnerville are similar in size, 2880 and 2780respectively. Their budgets are also similar in size. Lovelock’s revenues were $1,270,128 whileGardnerville’s revenues were $1,051,392. The sources of those revenues are considerablydifferent. Lovelock received 26% of its budget ($333,243) from the CTD while Gardnervillereceived 18% of its budget ($191,243) from the CTD. Gardnerville collected considerably morein Property Tax ($232,754 or 22% of its revenues) than did Lovelock ($102,997 or 8% of itsrevenues). Gardnerville also collected more in Proprietary Fund fees ($532,849 or 51% of itsrevenues) than did Lovelock ($328,250 or 26% of its revenues).

Proprietary Fund expenditures were sizable for both Lovelock and Gardnerville (31% and 39%respectively). Lovelock spent another 31% of its budget on Public Safety and 22% on GeneralGovernment. Gardnerville spent 41% of its budget on Public Works and 18% on GeneralGovernment.

The comparison of Lovelock and Gardnerville is another example of how two communities canhave different sources of revenues and similar uses for those funds. Both communities spent themajority of their revenues on expenditures for General Government and their Proprietary Funds.The biggest difference is that Lovelock spent 31% of its budget on Public Safety and only 8% forPublic Works. Gardnerville spent 41% of its budget on Public Works and made no classificationfor expenditures for Public Safety. Only the residents of these two communities can decide ifthese are appropriate sources and uses for their local government funds.

City of LovelockSelected Budget Items 1998-1999

Population 2880Assessed Value $ 18,402,273Property Tax Rate 3.6392Revenues PercentageProperty Tax $ 102,997 8%Other Taxes $ 23,300 2%Licenses and Permits $ 107,300 8%Intergovernmental Resources $ 626,805 49%Consolidated Tax Distribution $ 333,243 26%Housing Rehabilitation Grant $ 65,000 5%City Share of County Gaming Licenses $ 14,500 1%Other $ 214,062 17%Charges for Services $ - 0%Sewer Fees $ 220,000 17%Disposal Fees $ 108,250 9%Rental Income $ 500 0%Labor Income $ 1,000 0%Miscellaneous $ 700 0%Fines and Forfeits $ 27,200 2%Miscellaneous $ 52,076 4%Total Revenues $ 1,270,128 100%ExpendituresGeneral Government $ 299,602 22%Judicial $ 57,085 4%Public Safety $ 412,378 31%Public Works $ 103,700 8%Culture and Recreation $ 30,000 2%Proprietary Fund Operating Expenses (incl. Depreciation) $ 414,635 31%Intergovernmental Expenditures $ 16,900 1%Debt Principal $ - 0%Debt Interest $ - 0%Total Expenditures $ 1,334,300 100%Excess of Revenues over (under) Expenditures $ (64,172)

Population Source: Nevada Department of Taxation Annual Report, Fiscal 1998-1999

Assessed Value: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-2000

Property Tax Rate: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-2000

Budget Figures: City of Lovelock Budget, 1999-2000

Town of GardnervilleSelected Budget Items 1998-1999

Population 2780Assessed Value $ 75,722Property Tax Rate 2.6338Revenues PercentageProperty Tax $ 232,754 22%Intergovernmental Revenue $ 237,353 23%Consolidated Tax Distribution $ 191,243 18%County Gaming License Shared $ 22,410 2%Distribution from County $ 23,700 2%Other $ - 0%Charges for Service $ 16,770 2%Miscellaneous Revenue $ 31,666 3%Charges for Trash, Landfill, etc. $ 532,849 51%Total Revenues $ 1,051,392 100%ExpendituresGeneral Government $ 180,508 18%Public Works $ 410,921 41%Culture and Recreation $ 24,211 2%Expenditures for Trash, Landfill, Etc. $ 398,154 39%Total Expenditures $ 1,013,794 100%Excess of Revenues Over (under) Expenditures $ 37,598

Population Source: Nevada Department of Taxation Annual Report, Fiscal 1998-1999

Assessed Value: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-2000

Property Tax Rate: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-2000

Budget Figures: Town of Gardnerville Budget, 2000-2001

C. The City of Yerington and the Town of TonopahThe City of Yerington and the Town of Tonopah are two communities of similar population,2870 and 2760 respectively. Yerington’s revenues were almost twice that of Tonopah’srevenues ($2,520,523 vs. $1,455,740). Yerington received funding from the CTD, $231,916, butit is a relatively small percentage of its revenues, 9%. Yerington used a variety ofIntergovernmental Resources for revenues for this particular budget. Another large source ofrevenues was charges for services through Proprietary Funds (34%). Only 4% of its revenuescame from Property Tax. Tonopah relied more on the CTD as it accounted for 13% of itsrevenues. Tonopah also collected 36% of its revenues from charges for services through itsProprietary Fund. Approximately 8% of its budget came from the collection of Property Tax,although the amount was almost identical to that of Yerington’s ($108,090 and $108,899respectively.)

Expenditures through the Proprietary Funds were considerable for both Yerington and Tonopah,34% and 56% respectively. Yerington spent 23% of its expenditures on Public Safety whileTonopah spent 15%. Tonopah spent 20% of its budget on Culture and Recreation whileYerington spent only 2%. Yerington spent 17% of its budget on other IntergovernmentalExpenditures, an expense that had not been incurred in the two previous budget years. Nodetails on the expenditure were provided.

City of YeringtonSelected Budget Items 1998-1999

Population 2870Assessed Value 37,951,799$ Property Tax Rate 3.3396$ Revenues PercentageProperty Taxes 108,899$ 4%Other Taxes 0%Licenses and Permits 193,647$ 8%Intergovernmental Resources 1,202,027$ 48%Motor Vehicle 54,406$ 2%State Gaming Licenses 62,000$ 2%Municipal Special Assessments 900$ 0%Consolidated Tax Distribution 231,916$ 9%County Gaming Licenses 34,350$ 1%County Road Ad Valorem 90,000$ 4%Real Property Transfer Tax 12,000$ 0%Aviation Tax 2,000$ 0%RTC Shared Revenue 110,000$ 4%County General Ad Valorem 90,000$ 4%Parks Agreement 34,885$ 1%County Airport Tax 4,000$ 0%Other 475,570$ 19%Charges for Services 20,150$ 1%Charges for Sewer 425,000$ 17%Charges for Water 296,300$ 12%Charges for Mason Water 116,000$ 5%Fines and Forfeits 47,025$ 2%Miscellaneous 111,475$ 4%Total Revenues 2,520,523$ 100%ExpendituresGeneral Government 249,756$ 10%Judicial 42,577$ 2%Public Safety 591,785$ 23%Public Works 318,345$ 12%Culture and Recreation 50,062$ 2%Intergovernmental Expenditures 443,645$ 17%Contingencies 10,000$ 0%Utility Enterprises 869,011$ 34%Total Expenditures 2,575,181$ 100%Excess of Revenues over (under) Expenditures (54,658)$

Population Source: Nevada Department of Taxation Annual Report,Fiscal 1998-1999

Assessed Value: Nevada Department of Taxation Property TaxRates for Nevada Local Governments, 1999-2000

Property Tax Rate: Nevada Department of Taxation Property TaxRates for Nevada Local Governments, 1999-20000

Budget Figures: City of Yerington Budget, 1998-1999

Tonopah TownSelected Budget Items 1998-1999

Population 2760Assessed Value $ 27,505,044Property Tax Rate $ 3.64Revenue PercentageProperty Taxes $ 108,090 8%Other Taxes $ 195,662 14%Licenses and Permits $ 18,500 1%Intergovernmental Resources $ 321,088 23%Intergovernment Distribution $ 190,548.00 14%County Liquor License $ 2,400.00 0%County Gaming License $ 23,040.00 2%Gas $ 12,000.00 1%Other 93,100.00 7%Charges for Services $ 17,000 1%Charges for Utility $ 601,000.00 43%Non-Operating Revenue for Utility $ 47,012.00 3%Fines and Forfeits $ 25,000 2%Miscellaneous $ 62,500 4%Total Revenues $ 1,395,852 100%ExpendituresGeneral Government $ 69,291 4%Public Safety $ 261,915 14%Public Works $ 89,715 5%Culture and Recreation $ 356,460 19%Utility Expense $ 1,080,415.00 58%Total Expenditures $ 1,857,796 100%Excess of Revenues over (under) Expenditures $ (461,944.00)

Population Source: Nevada Department of Taxation Annual Report, Fiscal 1998-1999

Assessed Value: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-2000

Property Tax Rate: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-20000

Budget Figures: Town of Tonopah Budget, 1998-1999

D. City of Elko and Town of PahrumpThe City of Elko and the Town of Pahrump are two communities with similar population counts,19,670 and 18,970 respectively. Pahrump has considerably higher assessed value than Elko,($423,719,373 vs. $272,263,390) yet collects less in property tax for its budget than does Elko($702,375 vs. $1,213,961). This is due to the fact that the property tax rate levied by the City ofElko is .5388. The property tax rate levied by the Town of Pahrump is .1905. It is alsointeresting that the total property tax rate levied on all property in the City of Elko is 2.6465.The total property tax rate levied on all property in the Town of Pahrump is 3.3137. Theproperty in the town of Pahrump is considerably closer to the NRS property tax limit of 3.64 thanis the property in the City of Elko. This may present challenges if Pahrump were to decide itneeded additional property tax funding.

The City of Elko relied heavily upon the CTD as it accounted for 57% of its budget revenues.The Town of Pahrump received less ($451,157 vs. $6,138,169) and also relied less on the CTD.It accounted for only 23% of its budget revenues.

The largest expenditures for the City of Elko were Public Safety ($5,341,442 or 48% of its totalexpenditures), Public Works ($2,979,361 or 27% of its total expenditures), and GeneralGovernment ($1,299,983 or 12% of its total expenditures). Pahrump spent 43% of its budget onGeneral Government ($698,500), 27% on a Capital Project Fund ($438,000), and 19% on PublicSafety ($313,200).

City of ElkoSelected Budget Items, 1998-1999

Population 19670Assessed Value 272,263,390$ Property Tax Rate1 2.6465Revenues PercentageProperty Tax 1,213,961$ 11%Licenses/Permits 1,055,050$ 10%Intergovernmental Revenue 7,578,409$ 70%Consolidated Tax Distribution 2 6,138,169$ 57%Charges for Services 627,700$ 6%Fines/Forfeitures 177,000$ 2%Miscellaneous Revenues 151,333$ 1%Total Revenues 10,803,453$ 100%ExpendituresGeneral Government 1,299,983$ 12%Judicial Function 116,687$ 1%Public Safety 5,341,442$ 48%Public Works 2,979,361$ 27%Health Function 275,980$ 2%Recreation Function 1,084,962$ 10%Community Services 62,070$ 1%Total Expenditures 11,160,485$ 100%Excess of Revenues Over (Under) Expenditures (357,032)$

1Average of three tax districts for City of Elko

2Source: Nevada Department of Taxation Annual Report, 1998-1999

Not included: Proprietary Funds for Water, Sewer, and Landfill

Population Source: Nevada Department of Taxation Annual Report, Fiscal 1998-1999

Assessed Value: Nevada Department of Taxation Property Tax Rates for Nevada LocalGovernments, 1999-2000

Property Tax Rate: Nevada Department of Taxation Property Tax Rates for Nevada LocalGovernments, 1999-20000

Budget Figures: City of Elko Budget, 1998-1999

Town of PahrumpSelected Budget Items, 1998-1999

Population 18970Assessed Value $ 423,719,373Property Tax Rate 3.3137Revenues PercentageProperty Tax $ 702,375 35%Consolidated Tax Distribution $ 451,157 23%Licenses and Permits $ 128,000 6%Nye County Grant $ 20,000 1%Charges for services $ 8,000 0%Fines and Forfeitures $ 50,000 3%Miscellaneous $ 43,600 2%Other Revenues $ 593,500 30%Total Revenues $ 1,996,632 100%ExpendituresGeneral Government $ 698,500 43%Public Safety $ 313,200 19%Culture and Recreation $ 150,100 9%Community Support $ 2,400 0.1%Cemetery Fund $ 16,000 1%Capital Project Fund $ 438,000 27%Total Expenditures $ 1,618,200 100%Excess of Revenues Over (Under) Expenditures $ 378,432

Population Source: Nevada Department of Taxation Annual Report, Fiscal 1998-1999

Assessed Value: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-2000

Property Tax Rate: Nevada Department of Taxation Property Tax Rates for NevadaLocal Governments, 1999-20000

Budget Figures: Town of Pahrump Budget, 1998-1999

Not included: Proprietary Funds for Water, Sewer, and Landfill

VI. Discussion of City and Town BudgetsAs was discussed above, a community that is considering incorporating must follow the severalrequirements outlined in the Nevada Revised Statutes. This section attempts to give citizensinterested in incorporating their community an insight into some of the financial considerationsmanaging an incorporated city.

A. RevenuesIf a community is considering incorporating, it must consider the revenue it might generate tocover its potential expenditures.

1. Property TaxProperty tax is an important component of local budgets. For the unincorporated towns used inthese examples, property tax accounted for an average of 21% of their total revenues.Incorporated cities may rely less on property tax as property tax revenues account for an averageof only 9% of the total revenues of the four cities examined in this paper. Any communityconsidering incorporating should consider their assessed value, the property tax they would beable to levy as a city, and the total property tax already levied on their community with all of theoverlapping tax districts included.

All of these factors are important in estimating property tax revenue as an incorporated city, butthe total property tax rate levied including overlapping districts is especially critical because theNevada Revised Statutes limit the property tax levied on any piece of property to $3.64 per $100of assessed value. In the unincorporated town examples included, the property tax including theoverlapping tax districts averaged $3.09. Unincorporated towns with low assessed propertyvalues may have high tax rates and thus be closer to the $3.64 limit than communities withhigher assessed property values. This could make raising revenue through property tax difficult.

2. Intergovernmental Revenues

a) Consolidated Tax DistributionThe Consolidated Tax Distribution is probably the biggest source of intergovernmental

revenues for incorporated cities. Of the four incorporated cities used in these examples, itaccounted for an average of 35% of their revenues. Of the four unincorporated towns, itaccounted for almost 17% of their revenues. Any community considering incorporating willneed to contact the Executive Director of the Nevada Tax Commission to determine how muchthey would receive in the Consolidated Tax Distribution.

b) Other Intergovernmental RevenuesOther sources of Intergovernmental Revenues vary from city to city. Incorporated cities

may receive revenue from a number of governmental sources including the county for roads andgaming licenses, aviation taxes, transportation funds, and state and federal grants. Anycommunity considering incorporating should research what types of intergovernmental revenuesmight be available for the services they want to provide.

3. Licenses, Permits, and Franchise FeesOf the four incorporated cities used in these examples, revenue from licenses, permits, andfranchise fees accounted for approximately 7% of their revenues. Two of the unincorporatedtowns did not provide a category for this type of revenue. For the remaining two that did, anaverage of 3% of their budgets came from licenses, permits, and franchise fees. If a communityis considering incorporating, they should determine which activities will require licenses, whatthe charges will be, and how much revenue will be generated. Similarly, they should determineif they are going to franchise any of the incorporated city’s services, such as landfill operations,and determine the revenue from those franchises.

4. Charges for servicesBoth incorporated cities and unincorporated towns may charge for use of city or town property.In the examples used, Charges for Services accounted for 2.7% of the city budgets and 1.25% ofthe town budgets. One city, Lovelock, did not include this category. If a community isconsidering incorporating, it should consider what revenues might be available for charging forservices. These revenues may offset some or all of the expense of providing these services.

5. Proprietary Funds and Enterprise DistrictsIncorporated cities and unincorporated towns alike may provide services through EnterpriseDistricts. These are also referred to as Proprietary Funds. These operate in a manner similar toprivate businesses. The cost of providing the goods or services is covered primarily through usercharges. Examples of enterprise funds include water works, sewer, solid waste disposal, andelectricity. In three cities surveyed for this paper, revenue from the proprietary funds accountedfor almost 28% of their available revenues. In three of the unincorporated towns, revenue fromthe proprietary funds accounted for approximately 44% of their available revenue. If acommunity is planning on providing services through an Enterprise District, it should estimatethe revenues available through charging for these services.

6. Fines and ForfeituresBoth unincorporated towns and incorporated cities may collect fines and forfeitures.Incorporated cities typically do so through their municipal court. Of the four incorporated citiesused in these examples, less than 2% of their revenues came from Fines and Forfeitures. Two ofthe unincorporated towns provided this budget category and an average of just over 2% of theirrevenues are generated from Fines and Forfeitures. A community considering incorporating willhave some cost associated with the operations of a municipal court. As such, it should estimatethe revenue available from the Fines and Forfeitures.

7. GrantsGrants may be available from the state and or federal government. Typically, grant money mustbe spent according to the specific terms of the grant proposal and the community must match all

or part of the grant funds with its own money. If a community is considering pursuing grants asa means of generating revenue, it should determine the financial impact of taking the grant aswell as the length of time that the grant money is available to be spent.

8. Capital RevenuesUnincorporated Towns and Incorporated Cities may earn interest on their money as well as issuebonds to raise revenue. While bonds initially provide a source of revenue, they must also beserviced with regular payments. A community should consider how much interest they can earnon their funds as well as the revenue generated from bond sales and the payments due on thebonds.

B. ExpendituresUnincorporated towns and incorporated cities tend to have similar budget categories includingGeneral Government, Proprietary Funds, Public Safety, Public Works, and Culture andRecreation. Incorporated cities have the additional expense of maintaining a municipal judicialsystem and police.

For both unincorporated towns and incorporated cities, large budgetary expenditures tend to bewithin the Proprietary Funds. Of the three incorporated cities that included Proprietary Funds intheir budget information, nearly 32% of their budgets are spent in this category. Approximately28% of their revenues are generated from the fees they charge for these services. For the threeunincorporated towns that included Proprietary Funds in their budget information, 42% of theirbudgets are spent in this category. Approximately 44% of their revenues are generated from feesthe towns charge for these services.

Public safety is another large budget category for incorporated cities because of the cost ofmaintaining their own police and fire protection. Of the four incorporated cities surveyed,approximately 31% of their annual budgets are spent on Public Safety. Three cities providedinformation for municipal courts. Their expenditures averaged just over 2% of their annualbudgets. Only two unincorporated towns surveyed include funding for Public Safety. Theirexpenditures average 17% of their annual budget expenditures.

The expenditures for general government functions are sizeable for both unincorporated townsand incorporated cities, but the actual expense for incorporated cities can be considerably higherbecause they tend to provide their own governmental functions for the administration, clerk,personnel, information systems, finance, insurance, planning, and zoning. Unincorporated townsmay rely on the county to provide for some of these functions. For the four incorporated citiessurveyed, General Government expenditures averaged 16% of their budgets. For the fourunincorporated towns, it averaged higher at approximately 27%.

Public works are another area of large expenditures for incorporated cities. Of the four surveyed,they spent an average of just over 16% on Public Works. Only two unincorporated towns spentmoney on public works. One community spent 5% and the other spent 41% of their annualbudget on Public works.

A community considering incorporating should carefully consider all costs, including additionalcosts that may be unique to operating as an incorporated city. As mentioned above these mayinclude the cost of a municipal court and police and fire protection. There may be additionalcosts as well depending on the services the incorporated city may offer.

VII. Questions to Answer When Considering A Change for aCommunityWhen a community is considering forming an unincorporated town, incorporated city, or GID,there are several factors that it must take into consideration. This paper has provided a generaloverview of characteristics of each. With this information, a community can begin to answer thefollowing questions for itself:

A. What type of authority does the community want to have in governingitself?

Incorporated cities have the highest degree of political autonomy. They are not limited byspecific statute, as are counties, unincorporated towns, and GIDs to the types of services they canprovide. The NRS provides that they can make and pass all lawful ordinances necessary tomanage their affairs.

An unincorporated town can have a great deal of local authority if organized with a town boardform of government; however, it does not possess the same degree of autonomy as anincorporated city. A GID offers additional local authority as they are considered to be corporate,political, and quasi-municipal bodies.

The powers of an incorporated city, unincorporated town, or GID, are subordinate to a RegionalPlanning Agency. An example of this type of agency is the Tahoe Regional Planning Agency.

B. What type of services does the community want to deliver?Because they are not limited by specific statute, incorporated cities have the ability to offer thebroadest range of services to its citizens. Through statutes, unincorporated towns have the abilityto provide several services to its residents. GIDs are limited to twenty services they can provide.The ability to provide police, zoning, and planning is not available to GIDs.

C. What type of control over local resources does the community want?Incorporated cities have the most control over local resources, as they are a legal entities notsubordinate to the county. Town boards can exercise considerable control over resources

available to them; however, they are limited by statute. GIDs are also able to manage theirresources with a fair amount of autonomy, but again they are limited by statute.

D. What financial resources does the community want to access?Incorporated cities, unincorporated towns, and GIDs have access to similar financial resources:Intergovernmental transfers, property tax, user fees, grants, and license and permit fees areexamples. The critical point is not necessarily the type of resource available, but rather theamount of money available from each of these sources.

E. Will there be sufficient revenues to cover the expenditures?Before a city can be incorporated, sufficient evidence must be gathered to show that the city can,among other things, generate enough revenues to cover its expenditures. A community willlikely need to contract with firms that specialize in municipal issues and accounting for help indetermining the financial feasibility as well as other issues critical to incorporating. Acommunity seeking to form a town or GID may also need to seek the assistance of professionalsin addition to the research they perform themselves to determine the financial feasibility of sucha pursuit.

VIII. ResourcesAttorney General100 N Carson StreetCarson City, NV 89701-4717775-684-1100

555 E Washington Avenue Suite 3900Las Vegas, NV 89101702-486-3420

District AttorneyNevada Revised StatutesNevada Administrative CodeNevada Department of TaxationNevada State Supreme Court DecisionsState of Nevada Home Pagewww.state.nv.usState of Nevada Legislature Home Pagewww.leg.state.nv.us

IX. ReferencesNevada Revised Statutes, Chapters 244, 244A, 265, 266, 267,268, 269,270, 271, 272, 274, 277,308, 309, 318, 360, 377

Nevada Department of Taxation Property Tax Rates for Nevada Local Governments Fiscal Year1999-2000

Nevada Department of Taxation Annual Report 1998-1999

City of Elko Budget FY 1998-1999

Incline Village GID Budget FY 1998-1999

Grandview Terrace GID Budget GY 1998-1999

City of Carlin Budget FY 2000-2001

Town of Minden Budget FY 2000-2001

Town of Gardnerville Budget FY 2000-2001

City of Yerington Budget FY 1998-1999

Town of Tonopah Budget FY 1999-2000

Town of Pahrump Budget FY 1998-1999

City of Lovelock Budget FY 1999-2000

An Introduction To Legal and Economic Considerations Regarding Incorporation of NevadaTowns, Povolny, Cynthia, January 1981.