Embed Size (px)

Citation preview

BBUS 361INTERMEDIATE ACCOUNTING I

LECTURE NOTES

Fall 2013Professor Valerie Li

1

THE ROLE OF ACCOUNTING IN BUSINESS

What is accounting?Financial information for decision makers to make decisionsFor investors, creditors, any external usersManagers prepare the info for external usersTo know how the company is runningA system to identify, measure, report the financial info to external parties for decision making

Who are the primary users of financial accounting?

Others?

Creditors and investors

Why do they need this information?ReturnsRisk

Theoretical value of the firm:Based on market capStock price * shares outstanding

=present value of future cash flows, determines stock price

2

STANDARD SETTING

Why do we need standards?Conflict in interestCompare companiesConsistent reporting system

Historical background:

Who sets the standards in the U.S.? FASB – private sector to set standardsSEC authority of US to oversee standards

Former big 4 accountants, creditors, government (SEC), investors, money managers, risk metrics, professor, CFO

Accounting Standards Codification (ASC)Database of rules

Example: Accounting for Research and Development

Previously: R&D SFAS #2

Codification: 730-10-25

How are standards set?Political processDue process, very open

3

Everyone can give their opinions as comments on proposals

Example: Accounting for Employee Stock OptionsCant record 0 for ESO because ESO has value so it is an expense for the company to give stock options

Advantages: more insights from multiple parties Disadvantages: takes too long, bias, go with not the best

solution

How do we know standards are followed?AuditorsSEC enforcementsInternal control/auditorsCEO/CFO certifies financial statement after 2002The board

International Financial Reporting Standards (IFRS)

Reasons for global accounting standards: Comparability of financial statements

Difficulties/Drawbacks:CostlyHard to have one size fits all

Current Status: Still debating

4

5

CONCEPTUAL FRAMEWORK

Original Framework:

Purpose: To set forth fundamentals on which financial reporting standards are based.

Statement of financial accounting concepts SFAC #8 Objectives of Financial Reporting

SFAC #8 Qualitative Characteristics of Accounting Information

SFAC #6 Elements of Financial Statements

SFAC #5 & #7 Recognition and Measurement in Financial Statements

Current Conceptual Framework Project:

Purpose: To develop an improved common conceptual framework that provides a sound foundation for developing future accounting standards (joint project with IASB)

Eight phases:

Objectives and Qualitative Characteristics Elements and Recognition Measurement Reporting Entity Presentation and Disclosure …

6

Objectives of Financial Reporting (based on revised framework)

Provide useful information to capital providers-Helps assess amounts, timing and uncertainty about future cash flows- Clearly portrays the economic resources of an enterprise

Qualitative Characteristics of Accounting Information (based on revised framework)

GRAPHIC 1-7 Hierarchy of Qualitative Characteristics of

Financial Information

7

Fundamental Characteristics:

Relevance: Capable of making a difference in a decision

Predictive valueCan predict future outcome

Confirmatory valueConfirms prediction, change previous expectations depending on real outcomeProvide feedback about previous evaluation

Materiality In specific context

Faithful Representation: Depicts the economic phenomena it purports to represent

Completeness Can’t hide any info, tell everything

Neutrality (rejection of conservatism) Without bias

Free from material error

Enhancing Characteristics:

ComparabilityCompare different firm’s financial statementsCompare across timeConsistency

Verifiability CredibilityCan prove

8

Timeliness Have info ready in time and influence decisions

UnderstandabilityEasy to understand

9

Key Constraints Cost Effectiveness

Provide info if benefit of info is more than cost to prepare the info

Elements of Financial Statements (based on SFAC #6)

Assets Liabilities Equity (or net assets = A – L) Investment by owners Distributions to owners (dividends) Comprehensive income Revenues Expenses Gains Losses

Assets – Probable future economic benefit obtained or

controlled by a particular entity as a result of past transactions

Liabilities – Probable future sacrifice of economic benefit resulting from a present obligation of a particular entity as a result of past transactions.

Equity – Residual ownership interest (Assets less Liabilities)

Transactions with ownersTwo types: investment by owner’s like stock issuanceDistribution to owners

10

Like Dividends and stock buy back

Comprehensive Income

Comp Inc. = NI + Other Compr. Income

Revenue – Expenses + Gains – Losses

o Revenues:Inflow of assets or settlements of liabilities from on-going business

o Gains:Inflow of assets or settlements of liabilities not from on-going business

o Expenses: R&D should be assets but it is shown as an expenseOutflow of assets for incurrence of liabilities from on-going business

o Losses: Outflow of assets for incurrence of liabilities not from on-going business

11

Recognition and Measurement (based on SFAC #5&7)

Recognition: The process of recording an item in the financial statements

What are the alternatives to recognition? Disclose in the footnotes

Criteria for recognition:

Definitions – The item meets the definition of an element of financial statements

Measurability – The item has an attribute you can measure

Relevance – The attribute is relevant

Reliability – The attribute is reliable

Revenue recognition: Realization (after miderm will talk about this)

Realization principle:o The earnings process is complete or virtually

complete;o There is reasonable certainty as to the collectability

of the asset to be received. Expense recognition: Matching

12

Measurement: Five different attributes currently used in practice:

1. Historical Cost:

2. Current Cost: how much you have to spend to replace it

3. Net realizable value : net amount you collect and then end (A/R)

4. Present value of future cash flows: bonds

5. Fair value (market cost): you uwb much you can send it for?

Which measurement is the most common for recognition?

Why? 3 level floor valueLevel 1 : active fitLevel 2: similion marketLevel 3: estimation

Debate over Fair Value Accounting

13

Evolving GAAP: (articulation of financial statements) Balance sheet approach: revalue all assets I have at end and

then at beginning and find the difference = net income

Income statement approach

14

THE ACCOUNTING PROCESS

Review of Accounting Basics

Four Main Financial Statements:

• Balance Sheet

• Income Statement

• Statement of Cash Flows

• Statement of Stockholders’ Equity

Accounting Equation

Relationship among Financial StatementsIncome statement and balance sheet: Change in RE = net income - dividends

Cash flows and

15

Accounting Equation -- Examples An increase to one side of the equation must result in either:

- Decrease to the same side

or

- Increase to the other side

Accounting CycleA complete description of the accounting cycle is given in figure 2-3 of your book (page 56)

Recording Journal EntriesThree components to a journal entry:

16

• If debits = credits equation is always balanced• BUT…this does not mean that the journal entry is correct!• Also note:

– Revenues increase S/E so an increase in revenues is a ___credit___

– Expenses decrease S/E so an increase in expense is a ___debit____

17

Top McQueen Espresso Practice Problem

McQueen loves coffee and has decided to open an espresso stand. She plans to call it “Top McQueen Espresso”. She enters into several transactions during June 2005, the first month of operations. For each transaction described below, write out the appropriate journal entry.

1) McQueen contributes $20,000 to start-up the business.Cash…………………………..20,000

Owner’s equity……………………20,000

2) The company takes out a three-year loan from the bank in the amount of $10,000. [Ignore interest payments for now]

Cash…………………………..10,000Note payable……………………10,000

3) The company purchases an espresso machine and cart for $28,000.

Espresso machine and cart…………………..28,000Cash………….……………………………………28,000

4) The company purchases 100 lbs of coffee beans for $1100. The purchase was made “on account”, meaning the amount will be paid in 30 days.

Inventory……..……………..1,100A/P……………………………1,100

18

5) The company purchases other miscellaneous supplies such as cups, milk, napkins, etc. continuously throughout the month. Total supplies purchased during the month were $400. All purchases were made for cash.

Supplies……………………..400Cash…………………..……400

6) The company pays a monthly rental fee for the space on which the cart is located. The rental fee is $200/month.

Rent expense……………………..200Cash………………………………200

7) During the first month of operations, cash sales totaled $4,800.

Cash…………………………..4,800Revenue………………………4,800

8) In addition, the company sold pre-paid “coffee cards”. Customers can purchase these cards in advance and redeem them at the time of purchase. Coffee card purchases totaled $400 during the month.

Cash…………………………………....400Unearned revenue……………….……400

19

9) Since business was better than expected, McQueen hired a part-time barista to help out. Wages paid to the part-time barista were $320.

Salary expense……………….…..320Cash……………………..320

Posting -- T-account methodCreate T-accounts and post the above journal entries.

20

Adjusting EntriesSome events that need to be recorded are not the result of transactions with external parties. These events require “adjusting entries” at the end of the reporting period.

Adjustments can be classified as:

Prepayments: cash before recognition. Cash is paid or received before expenses or revenue is recognized

Example: prepaid expense, unearned revenue

Accruals: cash after recognition. Cash has not been paid or received when revenue or expense has incurred

Example:

Prepayment AccrualRevenues

InitiallyDebit CashCredit Unearned revenue

Adjusting entryDebit LiabilityCredit Revenue

InitiallyDebit ReceivableCredit Revenue

Adjusting entryDebit CashCredit Receivable

Expenses

InitiallyDebit Prepaid expenseCredit Cash

Adjusting entry

InitiallyDebit ExpenseCredit Payable

Adjusting entry

21

Debit ExpenseCredit Prepaid expense

Debit PayableCredit Cash

22

Example: Fiscal period is 1 month here1) Prepaymentsa. Prepaid expenses

1/18 Paid $30,000 for 3 months rentPrepaid rent………….30,000

Cash…………………………….30,000

1/31 AdjustmentRent expense…………………..10,000

Prepaid rent……………………….10,000

b. Pre-collected revenue

1/10 Collect gift card $500Cash………………………………………………….500

Unearned revenue……………………………500

1/31 $200 yet to redeemUnearned revenue…………………………300

Revenue………………………………………………300

23

Alternative approach to record prepayments: to record initial cash directly into expense or revenue account. The adjusting entry then records the unexpired prepaid expense (asset) or unearned revenue (liabilities) as of the end of the period.

Prepaid Expense Unearned RevenueInitially Debit Rent expense

Credit CashDebit Cash 500 Credit Revenue 500 (instead of Unearned revenue)

Adjustment

Debit Prepaid RentCredit Rent expense

Debit Revenue 200Credit Unearned revenue 200

Previous Examples:

2) Prepaymentsc. Prepaid expenses

1/18 Paid $30,000 for 3 months rent

1/31 Adjustment

d. Pre-collected revenue

1/10 Collect gift card $500

24

1/31 $200 yet to redeem

25

3) Accrualsa. Accrued expenses

1/15 Wages accrued $400Wages expense………………400

Wages payable…………….400

1/20 Paid wages $400Wages payable……………….400

Cash……………………………….400

b. Sales on account

1/15 credit sale of $1000Account receivable…….1000

Sales Revenue…………………1000

1/20 collect cash $1000Cash………..1000

A/R………………..1000

26

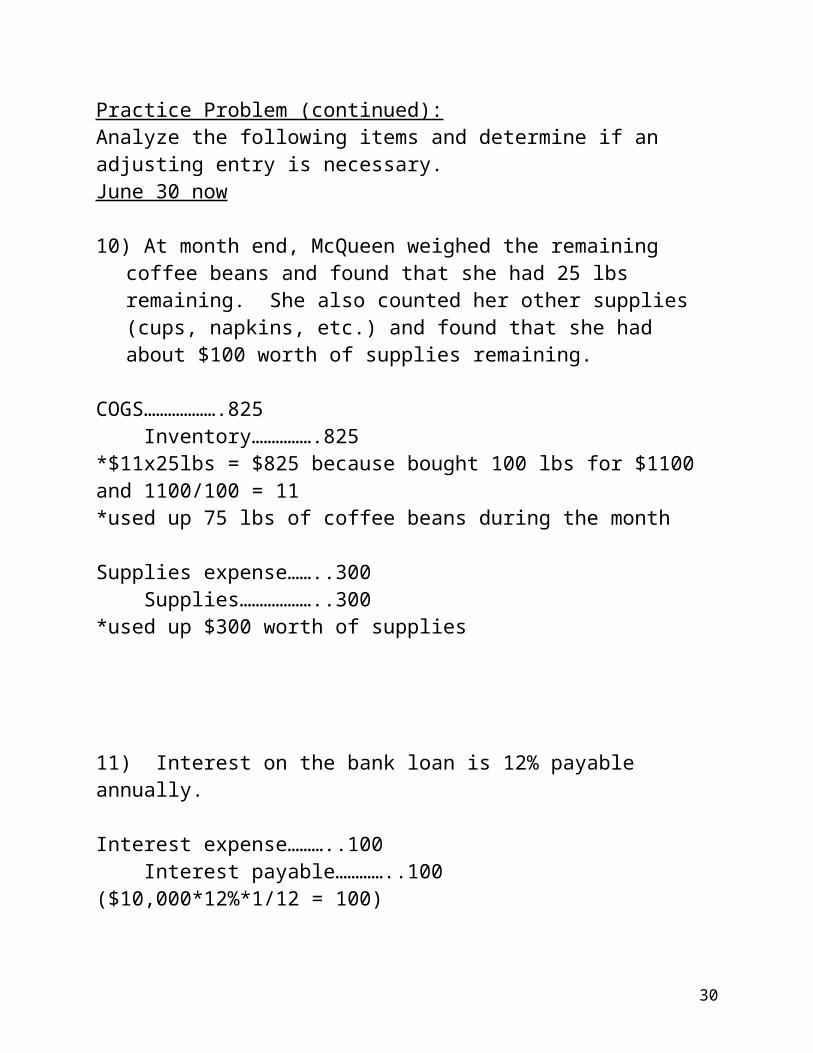

Practice Problem (continued):Analyze the following items and determine if an adjusting entry is necessary.June 30 now

10) At month end, McQueen weighed the remaining coffee beans and found that she had 25 lbs remaining. She also counted her other supplies (cups, napkins, etc.) and found that she had about $100 worth of supplies remaining.

COGS……………….825Inventory…………….825

*$11x25lbs = $825 because bought 100 lbs for $1100 and 1100/100 = 11*used up 75 lbs of coffee beans during the month

Supplies expense……..300Supplies………………..300

*used up $300 worth of supplies

11) Interest on the bank loan is 12% payable annually.

Interest expense………..100Interest payable…………..100

($10,000*12%*1/12 = 100)

12) The espresso machine and cart are expected to last 5 years.Depreciation expense……………..467

Accumulated Depreciation………467($28,000/5 * 1/12= $466) or (28000/60)

For this class, always straight line depreciation************

27

13) By the end of July, $150 worth of cards were redeemed.Unearned revenue……………….150

Revenue…………………………...150Because originally 400, 150 was redeemed

Financial Statement Preparation and Closing Entries

The financial statements can now be prepared from the ending balances in each T-account. Recall however that revenues and expenses DO NOT appear on the balance sheet but do affect the balance sheet through their effect on retained earnings. In order to prepare the balance sheet, we need to transfer the revenues and expenses to the retained earnings account. This method of transferring the revenues and expenses to retained earnings is known as the closing process.

Closing process:1) Close revenues and expenses to income summary account.2) Close income summary account to retained earnings.3) Close dividends to retained earnings.

What does it mean to “close” an account?To make it to zero balance

Practice Problem (continued)Prepare the closing entry for “Top McQueen Espresso” for the month of June:

28

Prepare the income statement, balance sheet, and statement of stockholders’ equity for “Top McQueen Espresso” on the following pages.

Top McQueen EspressoIncome Statement

For the month ended June 30, 2001

Top McQueen EspressoStatement of Stockholders’ Equity

For the month ended June 30, 2001

29

Top McQueen EspressoBalance SheetJune 30, 2001

To prepare the cash flow statement, we must return to the Cash T-account and examine the transactions that affected the account throughout the period. First, classify each transaction as operating, investing, or financing and then prepare the statement of cash flows on the next page.

30

Top McQueen EspressoStatement of Cash Flows

For the month ended June 30, 2001

31

Notice that Cash from Operation DOES NOT equal Net Income.

32

ACCRUAL VS. CASH FLOWS CONCEPTSCash flows from operations is a distinctly different concept from net income (accrual accounting):

1. Cash Flow Accounting - benefits and efforts are measured in terms of cash inflows and cash outflows.

2. Accrual Accounting - benefits and efforts are measured in terms of revenues and expenses. Revenues are inflows of assets (or decreases in liabilities) and Expenses are outflows of assets (or creation of liabilities). Cash is just one type of asset!

Very generally:a) Revenues are recognized when earned.

b) Expenses are recognized when the “effort” (or resources) is expended to generate revenue (matching principle)

Examples of differences in timing:

Revenue ExamplesRevenue earned

before cash received

Sales on AccountDebit ARCredit Sales Rev

Later Cash collectionDebit CashCredit AR

33

Cash received before revenue earned.

Cash collectionDebit CashCredit Unearned Rev

LaterDebit Unearned RevCredit Rev

Expense ExamplesExpense occurs

before cash paid.

Interest expenses incurredDebit Interest expenseCredit Interest payable Later paymentDebit Interest payableCredit Cash

Cash paid before expense occurs

Prepaid rentDebit prepaid rentCredit Cash

LaterDebit Rent expenseCredit Prepaid rent

Note that in each case, an asset or liability “holds” the timing difference between net income and cash flows from operations.

34

Which measure is more important?NI is more important for investorThe measure with more correlation to stock price is more important

Don’t know for creditors

35

Dechow, P., 1994, “Accounting Earnings and Cash Flows as Measures of Firm Performance: The Role of Accounting Accruals,” Journal of Accounting and Economics 18:3-42

36

Recall that in our “Top McQueen Espresso” example, Net Income for June did not equal Cash Flows from Operations. Why?

Let’s compare the Net Income and Cash Flows from Operations of Top McQueen Espresso:

37

Income Statement Statement of Cash Flows DiffRevenue: 4950 Cash collections from Sales:

5200 250Expenses: Cost of Goods Sold: (825)

Cash paid for inventory: 0 825

Supplies Expense: (300)

Cash paid for supplies: (400) 100

Rent Expense: 200

Cash paid for rent: (200) 0

Wage Expense: 320

Cash paid for wages: (320) 0

Interest Expense: 100

Cash paid for interest: 0 100

Depreciation Exp: 467

Cash paid for depreciation: 0 467

NET INCOME: 2738 Cash flows from operations: 4280 1542

Notice: All else held constant1) Revenues do not equal Cash Collections from Sales. Why?5200 is cash revenue collectedCash revenue is higher by 250 that means CFO will be higher than

NI by $250Cash revenue is greater than the accrued revenue by 250

because unearned revenue is 250 (goes up by 250)

Change CL goes up (cause unearned) CFO > NI

2) Cost of Goods Sold (cost of coffee beans used) does not equal cash paid for inventory. What are the differences?

COGS > cash paid for inventory by $825Bought more inventory than you soldNI > CFO by 275 (on inventory T account)Look at Accounts Payable since didn’t pay for the inventory in

cash yet

38

AP goes up by 1100Change in AP $1100 …. NI< CFO by $1100 because haven’t used

cash to pay yet----Change CA up and Inventory up which means CFO < NIIf inventory is up then means you bought more than you sold,

and so cash expenses is higherChange in CL up………so CFO > NI

3) Supplies Expense does not equal Cash Paid for Supplies. What are the differences

CFO rev is 400 and CFO expense is 300 so = 100So NI > CFO by 100 cause supplies expense went up and cash income goes down (bought more than you used)Supplies account goes up by 100Change in CA goes up 100

4) Interest Expense does not equal Cash Paid for Interest. What are the differences?

100 because haven’t paid for the interest yetAccrued expense is higher than cash expense so NI < CFOWhat account is holding this difference? = Interest payableIP will go up by 100

So, we could reconcile Net Income to CFO as follows:Indirect method Statement of Cash FlowsStart with NIAdd back noncash items like dep, bad debt expense

39

Dep bad del expense (adjust for change in CA and change in L)

CF from operating activitiesNI 2738+depreciation 467+unearned revenue 250+supplies (100)+AP 1100+inventory (275)+interest 100

CFO 4280

40

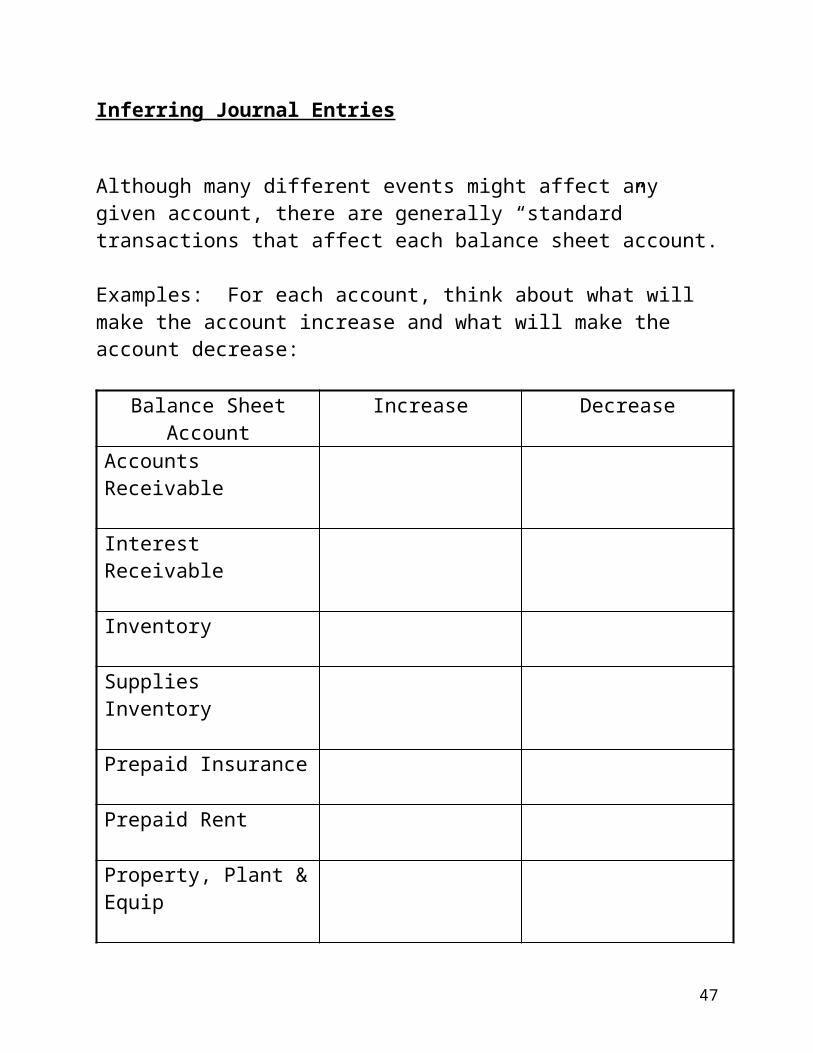

Inferring Journal Entries

Although many different events might affect any given account, there are generally “standard” transactions that affect each balance sheet account.

Examples: For each account, think about what will make the account increase and what will make the account decrease:

Balance Sheet Account

Increase Decrease

Accounts Receivable

Interest Receivable

Inventory

Supplies Inventory

Prepaid Insurance

Prepaid Rent

Property, Plant & Equip

Accounts Payable

Wages Payable

Interest Payable

Unearned Revenue

41

Therefore, if you know the change in a balance sheet account from the beginning of a period to the end of a period (the net increase or decrease in the account), AND you know one reason for the change you can infer the other reason for the change. Practice Problem:Following is selected balance sheet information from Koa’s Kitty Food, Inc. for the years ended December 31, 2004 and 2005.

Account 12/31/04 12/31/05Accounts Receivable 8,500 9,000Merchandise Inventory 10,100 9,600Prepaid Rent 2,400 2,000Accounts Payable 8,900 7,900Wages Payable 1,900 2,000

In addition, the following information for the year ended 12/31/05 is provided to you:

Accrual sales $24,500Cash paid to suppliers for inventory purchased on account 13,700Rent Expense 3,400Cash paid for wages 4,700

Using this information, compute the following (NOTE: Assume that accounts payable relates entirely to merchandise inventory):

a) Cash collected from customers $________________

b) Cash paid for rent expense $________________

42

c) Cost of goods sold $________________

d) Wage expense $________________

This inference process is difficult but very useful. We will use it throughout the quarter and you will see again in BBUS 363 when you cover the Statement of Cash Flows.

43

INCOME STATEMENT PRESENTATIONTypical Income Statement Format: Multi-step

44

Alternative: Single Step Format

Does it matter?

Valuation Implications:

45

Types of irregular items:

1. Economic events

a. Discontinued operations (SFAS #144, ASC 205-20): Component of a company 1) that has or will be eliminated from the operations of the company and 2) that the company will not have any significant continuing involvement in after disposal

Proposed changes:(based on Exposure draft of a new ASU) : Component of a company 1) that has been disposed or 2) is classified as held for sale, and represents one of the following:1) An operating segment

2) A business

Why does it matter?

Two components: - When the component has been sold: 1) Income/Loss from operation of discontinued segment from the beginning of the reporting period to the disposal date, 2) Gain or loss on disposal of discontinued segment

- When the component is considered held for sale: If decision has been made in the current period to discontinue operation but not yet discontinued (eg by sale) need to 1. separately report the income/loss on this operation

46

2. if FV of assets < book value, recognize the expected loss on sale (an impairment loss) But if FV > book value, do NOT recognize the gain til actually sell the operations.

Example: Company disposes of a segment that had operating losses for the year of $40,000 and that resulted in loss of $10,000 on disposal. Tax rate is 40% and income from continuing operations is $200,000.

47

Example of discontinued operations from Target Corp 10-KCONSOLIDATED RESULTS OF OPERATIONS (millions, except per share data) 2004 2003 2002 Sales $45,682 $ 40,928 $ 36,519 Net credit card revenues 1,157 1,097 891

Total revenues 46,839 42,025 37,410 Cost of sales 31,445 28,389 25,498 Selling, general and administrative expense 9,797 8,657 7,505 Credit card expense 737 722 629 Depreciation and amortization 1,259 1,098 967 Earnings from continuing operations before

interest expense and income taxes 3,601 3,159 2,811 Net interest expense 570 556 584 Earnings from continuing operations before

income taxes 3,031 2,603 2,227 Provision for income taxes 1,146 984 851 Earnings from continuing operations $ 1,885 $ 1,619 $ 1,376 Earnings from discontinued operations, net

of $46, $116 and $152 tax $ 75 $ 190 $ 247 Gain on disposal of discontinued

operations, net of $761 tax $ 1,238 $ — $ — Net earnings $ 3,198 $ 1,809 $ 1,623 Basic earnings per share

Continuing operations $ 2.09 $ 1.78 $ 1.52 Discontinued operations $ 0.08 $ 0.21 $ 0.27 Gain from discontinued operations $ 1.37 $ — $ —

Basic earnings per share $ 3.54 $ 1.99 $ 1.79 Diluted earnings per share

Continuing operations $ 2.07 $ 1.76 $ 1.51 Discontinued operations $ 0.08 $ 0.21 $ 0.27 Gain from discontinued operations $ 1.36 $ — $ —

Diluted earnings per share $ 3.51 $ 1.97 $ 1.78 Weighted average common shares

outstanding: Basic 903.8 911.0 908.0 Diluted 912.1 919.2 914.3

See Notes to Consolidated Financial Statements throughout pages 28-37.

48

b. Extraordinary items: Income items that are unusual and infrequent

c. Other unusual/irregular items: Income items that are unusual or infrequent (but not both)

Restructuring charges

- Recognize when “incurred” not necessarily paid. - Fair value the liability

a. Based on expected termination/severance payments to employees

b. Are estimates. So could be too high or low

Are they part of permanent earnings?

49

Pro forma earnings- Street earnings: managers (and analysts) exclude items

from earnings

Some people refer to as excluding the “bad stuff”:

50

51

1. Turns out pro forma earnings are more highly correlated with stock returns than reported earnings meaning (in an efficient capital market) ….

2. SOX Section 401. If firms report pro forma in a press release or elsewhere, they must reconcile to reported earnings

What are managers’ incentives for reporting these items?

52

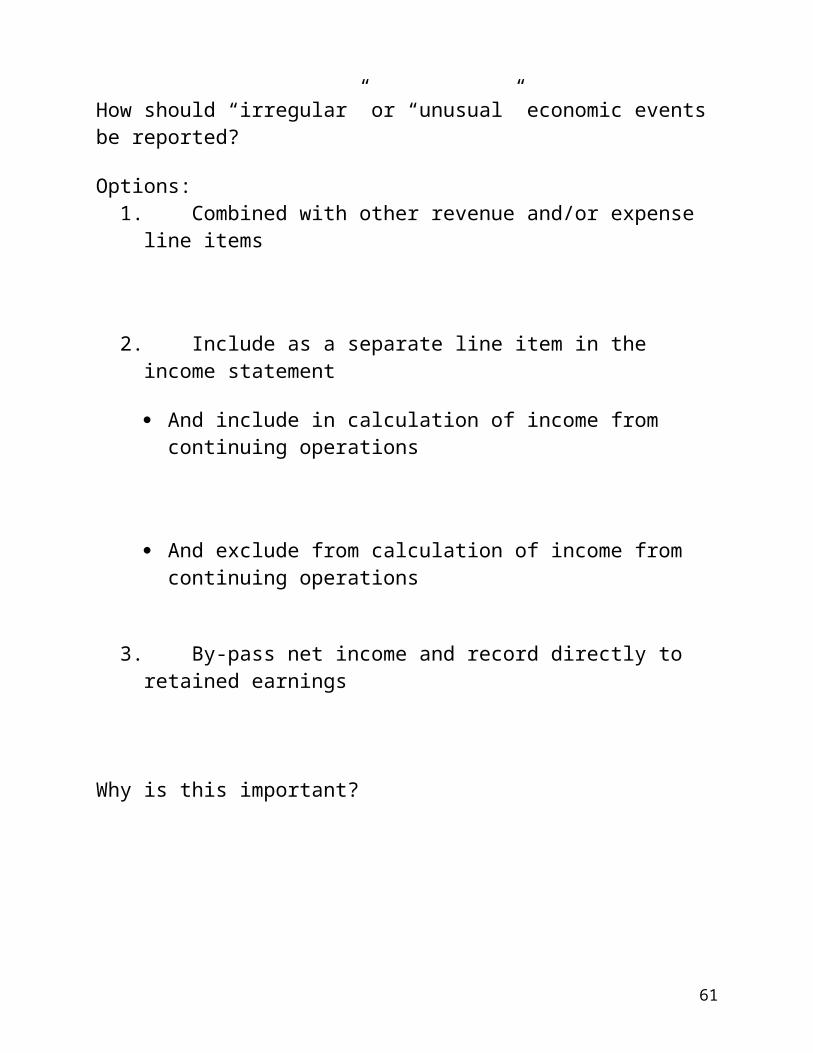

How should “irregular” or “unusual” economic events be reported? Options:

1. Combined with other revenue and/or expense line items

2. Include as a separate line item in the income statement

And include in calculation of income from continuing operations

And exclude from calculation of income from continuing operations

3. By-pass net income and record directly to retained earnings

Why is this important?

53

Example: Coca-Cola Enterprises

Examine the following Statement of Income and excerpts from the Notes to the Consolidated Financial Statements (next page).

Did CCE have any unusual or irregular items during 2005?

54

55

Practice ProblemShepard Industries is a manufacturer of medical devices. During 2004, several unusual events occurred at Shepard Industries:

The company sold a subsidiary, Shepard Financing, that provided financing to customers to assist them in purchasing some of the more expensive items in the company’s product line. The company no longer offers financing directly but provides customers with referrals to financing companies that provide such services. Prior to the sale, Shepard Financing incurred a loss of $200,000. The sale of the subsidiary resulted in a gain of $50,000.

The company incurred damage to one of their production facilities in Arizona, resulting from a tornado. Tornados are highly unusual occurrences in the area. The damage sustained to the buildings, equipment, and inventory totaled $80,000

Due to poor performance, the company announced a restructuring plan to reorganize its business units and streamline production. The restructuring plan included layoffs of 2,000 personnel and the disposal of non-productive assets and inventory from underperforming product lines. The cost of the restructuring was $130,000.

Excluding these items, the company had revenues of $1,000,000, Cost of Goods Sold of $600,000, and Selling, General and Administrative Expenses of $180,000.

The company’s income tax rate is 30%.

The company has (and always had) 100,000 shares of common stock outstanding and no preferred stock.

Prepare an income statement for Shepard Industries for the year ended December 31, 2004, in good form (space available on next page).

56

Shepard IndustriesStatement of Income

For the Year Ended 12/31/2004

57

2. Accounting related (SFAS #154, effective from January 1,

2006)a. Corrections of errors: Error in financial statement

resulting from mistake, misapplication of GAAP or misuse of facts

b. Changes in accounting principles: - A change from one allowable method under GAAP to

another (voluntary change) Ex:

- or as a result of a rule change (mandatory change)

c. Changes in accounting estimates: Normal, recurring corrections/ adjustments to estimates in the financial statements

58

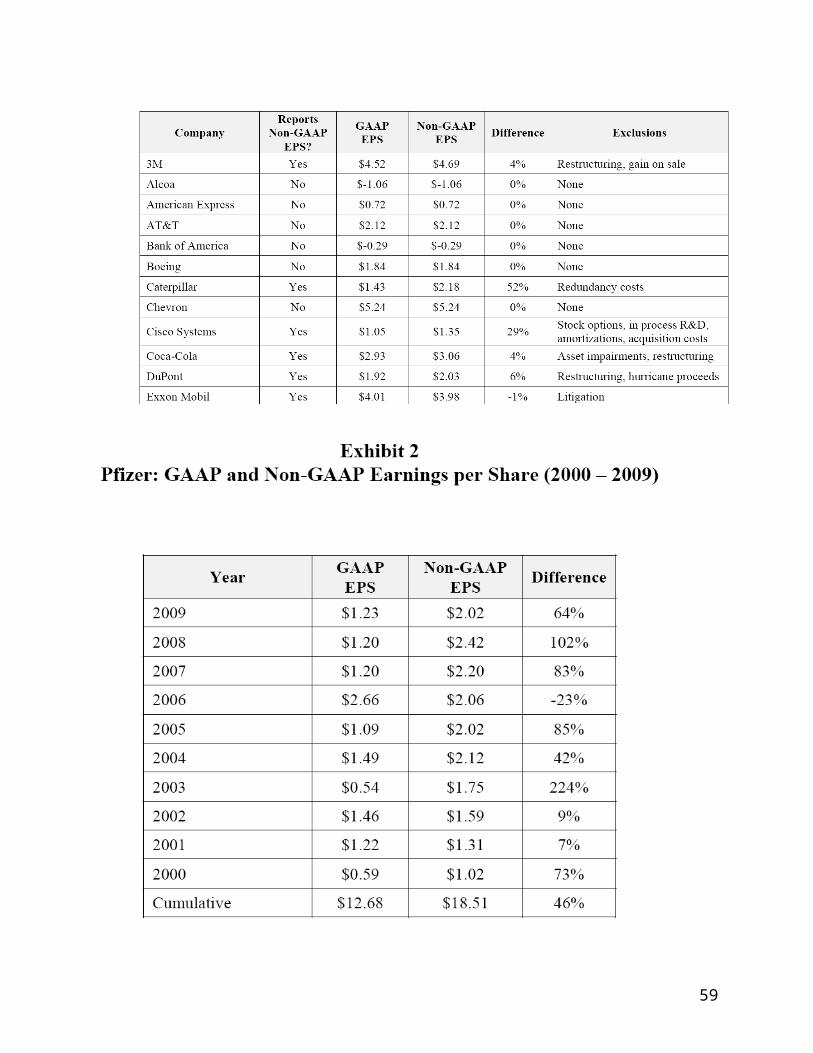

Earnings Per Shareis the amount of income earned expressed on a per share basis.

In the income statement, firms must disclose:EPS for (a) income before any separately reported items, (b) each separately reported item (3) net income

Basic EPS = (Net Income – Preferred Dividends) / # of common stocks outstanding.

($ in thousands, except per share data) 2010Loss from continuing operations before extraordinary item $ (77,962) Loss from discontinued operations, net of tax _ Extraordinary item, net of tax -- Net loss $ (77,962)

Basic earnings (loss) per shareLoss from continuing operations before extraordinary item $ (.67)Loss from discontinued operations --Extraordinary item --Net loss $ (.67)

59

COMPREHENSIVE INCOME (SFAS #30)All changes in equity except those resulting from investments by or distributions to owners

Comprehensive income = NI +Other Comprehensive Income (OCI)

Common items in OCI:

Impetus for this standard:

Presentation:

1. Separate statement

2. Combined statement

Accumulated Other Comprehensive Income (Accumulated OCI)- Reported in balance sheet

60

61

62

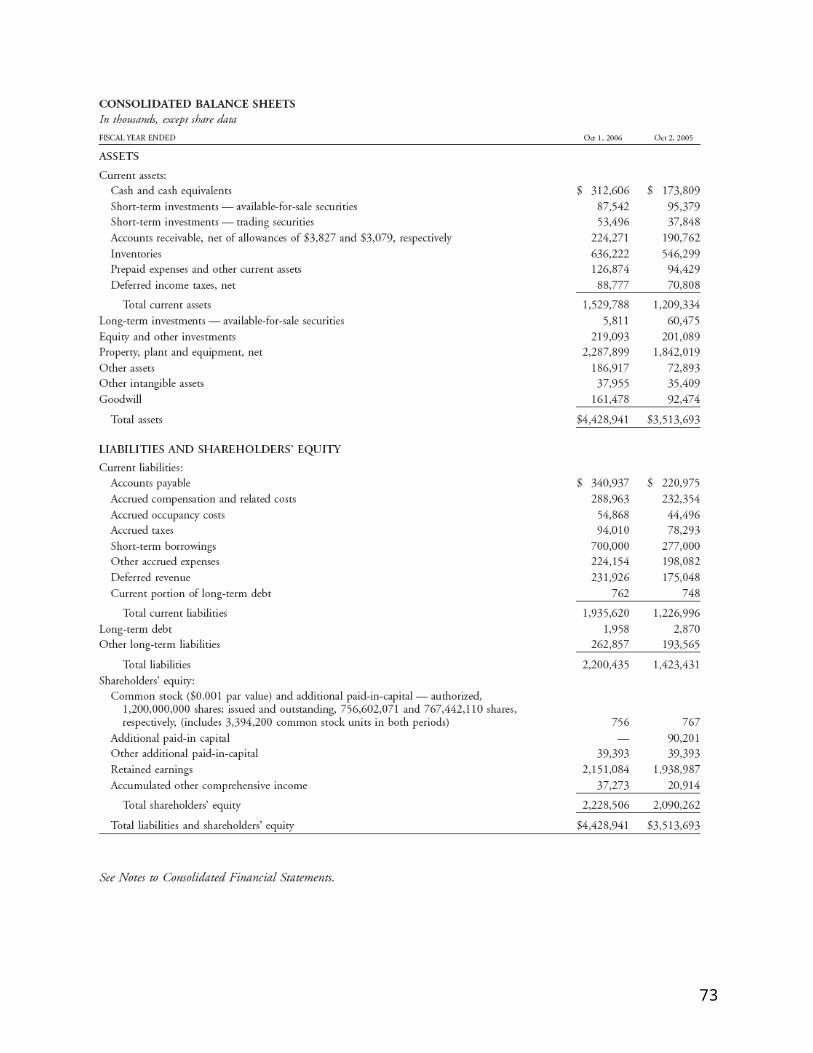

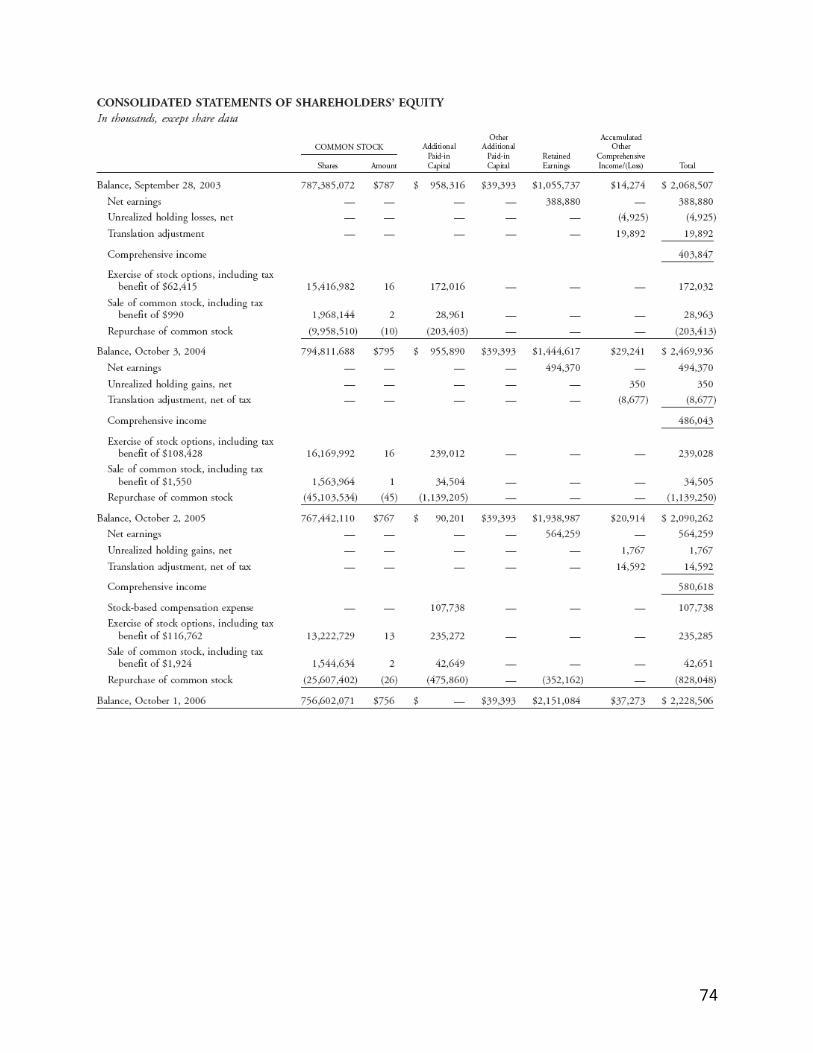

BALANCE SHEET AND DISCLOSURES

Purpose:

Typical Format:

63

What are assets?Assets Classified how:

Operating cycle: define

Limitations:

Classifications:

64

Cash and Cash Equivalents

Example: Dell (from the text)Note 1—Description of Business and Summary of Significant Accounting PoliciesCash and Cash EquivalentsAll highly liquid investments, including credit card receivables, due from banks, with original maturities of three months or less at date of purchase are carried at cost and are considered to be cash equivalents. All other investments not considered to be cash equivalents are separately categorized as investments.

Short-term investments : temporary investment or short-term marketable securities. The company has the intend and ability to sell within a year or operating cycle.

o

PROPERTY, PLANT, AND EQUIPMENT. What are liabilities?

probable future sacrifices of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events.

Shareholders’ EquityResidual ownership interest (assets less liabilities)

65

Other Important Disclosures/Elements of Financial Statements:

Notes to the financial statements

Summary of Significant Accounting Polices pp 56-66 (11

pages!!)

Subsequent Events

What are they?

Walmart: 14. Subsequent Events (in part) On March 5, 2009, the Company's Board of Directors approved an increase in the annual dividends for fiscal 2010 to $1.09 per share. The annual dividend will be paid in four quarterly installments on April 6, 2009, June 1, 2009, September 8, 2009, and January 4, 2010, to holders of record on March 13, May 15, August 14, and December 11, 2009, respectively. On March 27, 2009, the Company issued and sold $1.0 billion of 5.625% Notes Due 2034 at an issue price equal to 98.981% of the notes' aggregate principal amount.

Related Party transactions

66

What are they?

Why disclose?

Note M: Related Party Transactions (in part)On May 16, 2008, we completed two transactions relating to our corporate aircraft. First, we sold our Bombardier Global Express airplane for approximately $46,787,000 in cash (a net after-tax cash benefit of approximately $29,000,000) to an unrelated third party. This resulted in a gain on sale of asset of approximately $16,000,000 in the second quarter of fiscal 2008. Second, we entered into an Aircraft Lease Agreement (the “Lease Agreement”) with a limited liability company (the “LLC”) owned by W. Howard Lester, our Chief Executive Officer and Chairman of the Board of Directors, for use of a Bombardier Global 5000 owned by the LLC. These transactions were approved by our Board of Directors.

Management Discussion and Analysis

Auditors’ ReportExternal auditor – attest to the fairness of the financial statements

1. Unqualified :

2. Qualified:

3. Adverse 4. Disclaimer

Compensation of directors and top executives

67

FINANCIAL STATEMENT ANALYSIS

General principles:

Scaling: Numbers need to be scaled to be economically meaningful

o Common size financial statements

I/S: Express all line items as a % of

B/S: Express all line items as a % of

o Ratios – Divide line items in economically meaningful way

Benchmarks: Need to compare to something to be useful

Common ratios: Liquidity: Ability to pay debts as they come due in the

short-term

Current ratio: CA/ CL

Quick Ratio:

Solvency: Ability to pay debts when they come due in

the long-term

68

Debt to equity:

Times interest earned:

Activity: Effectiveness of asset use

Receivables turnover

Inventory turnover

Asset turnover

Profitability: Ability to generate wealth in the long-term

Profit margin

Return on Assets (ROA)

69

Return on Equity (ROE)ROE = Profit Margin Asset turnover (1+Leverage)

Example: Nordstrom vs. CostcoNordstrom and Costco are both retailing giants but they have very different business models.

Which ratios discussed above, would you expect to differ between the two companies?

The following are selected data from Nordstrom and Costco for 2003:

Nordstrom CostcoSales 6,491,673 42,545,552COGS 4,213,955 37,235,383Net Income 242,841 721,000Receivables 594,900 556,090Inventory 901,623 3,339,428Current Assets 2,455,430 5,711,538Total Assets 4,465,688 12,709,383Current Liabilities 1,049,549 4,528,802Shareholders’ Equity 1,634,009 6,554,980

Were your intuitions correct?

70

REVENUE RECOGNITION

Issue: What amount of revenue should a company report in a given period?

General Principle: Revenue is recognized when it is both:

Earned

Realized or realizable

How easy is this to apply?

Start of End of Sale/ Start of End of Production Productiondelivery Cash Cash

of AssetCollection Collection

Examples:

Merchandise sales at Nordstrom?

Upfront “activation” fees associated with cellular service?

Sale of an iphone?-

Why is applying principle difficult?

71

- Why is it important?

Excerpt from Kravet, T. and T. Shevlin, 2010 “Accounting Restatements and Information Risk,” Review of Accounting Studies 15:264-294

72

Staff Accounting Bulletin (SAB) 104 (previously 101):

Reason behind the issuance of SAB 101

Is this GAAP?

According to SAB 104, revenue is realized or realizable and earned when the following criteria are met:

Persuasive evidence of an arrangement exists

Delivery has occurred or services has been rendered

1) “Bill-and-hold” arrangements- Facts : Company A receives purchase orders for products it

manufactures. At the end of its fiscal quarters, customers may not yet be ready to take delivery of the products for various reasons. These reasons may include, but are not limited to, a lack of available space for inventory, having more than sufficient inventory in their distribution channel, or delays in customers' production schedules.

- Question : o May Company A recognize revenue for the sale of its

products once it has completed manufacturing if it segregates the inventory of the products in its own warehouse from its own products?

o May Company A recognize revenue for the sale if it ships the products to a third-party warehouse but (1) Company A retains title to the product and (2) payment by the customer is dependent upon ultimate delivery to a customer-specified site?

- The Commission has set forth criteria to be met in order to recognize revenue when delivery has not occurred. These include:

1. The risks of ownership must have passed to the buyer;

73

2. The customer must have made a fixed commitment to purchase the goods, preferably in written documentation;

3. The buyer, not the seller, must request that the transaction be on a bill and hold basis. The buyer must have a substantial business purpose for ordering the goods on a bill and hold basis;

4. There must be a fixed schedule for delivery of the goods. The date for delivery must be reasonable and must be consistent with the buyer's business purpose (e.g., storage periods are customary in the industry);

5. The seller must not have retained any specific performance obligations such that the earning process is not complete;

6. The ordered goods must have been segregated from the seller's inventory and not be subject to being used to fill other orders; and

7. The equipment [product] must be complete and ready for shipment.

2) Customer acceptance provisions- Installation, (by whom), working to specifications3) Subsequent performance obligations

Inconsequential? 4) License fee revenue Delivery begins when license term begins5) Nonrefundable upfront fees

o A registrant sells a lifetime membership in a health club. After paying a nonrefundable "initiation fee," the customer is permitted to use the health club indefinitely, so long as the customer also pays an additional usage fee each month. The monthly usage fees collected from all customers are adequate to cover the operating costs of the health club.

A registrant requires a customer to pay a nonrefundable "activation fee" when entering into an arrangement to

74

provide telecommunications services. The terms of the arrangement require the customer to pay a monthly usage fee that is adequate to recover the registrant's operating costs. The costs incurred to activate the telecommunications service are nominal.

- Unless the up-front fee is in exchange for products delivered or services performed that represent the culmination of a separate earnings process, the deferral of revenue is appropriate.

- In the situations described above, the staff does not view the activities completed by the registrants (i.e., selling the membership, signing the contract, enrolling the customer, activating telecommunications services or providing initial set-up services) as discrete earnings events.

The seller’s price to the buyer is fixed or determinable

Collectibility is reasonably assured

75

Revenue Recognition after Delivery (i.e., during cash collection)If the collection of cash on a sale is not reasonably assured, the sale does not meet the “realized or realizable” criteria to recognize revenue. In this case, revenue (and the associated expense – i.e., COGS) is recognized over the period in which cash is collected.

Two methods: Installment method

o Record receivable, inventory reduction and deferred profit

o Compute average gross margin on sales for the year

o Recognize a portion of gross profit based on cash collected: gross profit % $ collected

Cost recovery method

o Same as above except recognize gross profit once cash received to date exceeds cost of sales

76

Practice ProblemGeorge Company sells washing machines and has a very lenient credit policy. As a result, the company has no basis for estimating uncollectible accounts. The company began operations in 2003. In the first two years of operations the company had:

2003 2004Installment Sales $250,000

(Sale A)$260,000

(Sale B)Cost of Installment Sales 150,000 169,000Cash Collections: On Installment Sales A 75,000 100,000On Installments Sales B 150,000

Prepare the appropriate journal entries assuming the company uses the installment method:

2003 2004

What if the company uses the cost recovery method?

77

Revenue Recognition before Delivery - Contract Accounting (ARB 45, ASC 605-35)When would recognition before delivery be a concern?

Two methods: Percentage-of-completion method

-

Completed-Contract method

Simple ExampleSeattle Grace Construction Company (SGCC) enters into a contract to build a new building for Addison Company. The contract price is $2,500,000, expected costs are $2,000,000, and the construction is expected to last 2 years. Cost incurred on the project are $1,200,000 in year 1 and $800,000 in year 2.

What percent of the project is completed at the end of year 1? How much of the revenue should be recorded in year 1 and year 2?

Percentage Completion

Completed Contract

Year 1 Year 2 Year 1 Year 2Revenues

Expenses

78

Net Income

Which provides “better” information?

Use percentage-of-completion when:1. Estimates of progress toward completion, revenues, and

costs are reasonably dependable.2. Contract specifies enforceable rights regarding goods or

services to be provided and received by the parties, the consideration to be exchanged, and the manner and terms of settlement

3. The buyer can be expected to satisfy all obligations under the contract

4. The contractor (seller) can be expected to perform the contractual obligations.

Accounting using Percentage-of-Completion Method

JE to record costs incurred on the project:

JE to record Revenue/COGS:

79

Progress Billings: Contractually agreed-upon amounts that the contractor (seller) is allowed to bill the buyer at set intervals. Only the amounts “billed” can be recorded in Accounts Receivable. Revenue “earned” in excess of amounts billed are kept in the Contracts in Progress (i.e., Inventory) account.

JE to record progress billings:

Why use a contra-account?

Contracts in Progress Billings on CIP A/R

80

Simple Example (con’t)Assume all construction costs are paid in cash, that the progress billings made by SGCC to Addison are $1,250,000 in years 1 and 2, and Addison pays that amount in each of the two years What journal entries would the company record if the company uses the percentage of completion method?

Year 1 Year 2

Net impact on Financial Statements?

Assets = Liabilities + S/E

81

Changes in estimates:The total estimated costs of the project could change over time. This is treated as a “change in estimate” and is treated prospectively – that is, no changes are made to prior net income but changes are made going forward.

Thus, calculations of revenues and expenses should be based on cumulative amounts less amounts recorded in prior periods.

Revenue recorded in CY = Revenue earned to date – Revenue recorded in PY

Expense recorded = Expense to date – Expense recorded in PY

Practice ProblemOn July 1, 2003, Scranton Construction contracted to build an office building for Scott Industries for a total contract price of $1,900,000. The building was completed on December 31, 2005. Additional data were:

2003 2004 2005Contract costs incurred during the year

$450,000 210,000 900,000

Estimated costs to complete as of 12/31

1,050,000 990,000 0

Billings to Scott Industries 300,000 700,000 900,000Collections from Scott Industries 300,000 700,000 900,000

82

Compute the amount of revenue and expenses that should be recorded in each year.

83

Prepare the journal entries that would be recorded in each of the three years

2003 2004 2005

What amounts would be reflected on the company’s financial statements?

2003 2004 2005Balance Sheet:

Income Statement:

84

EXCEPTION: If a change in the estimate of total costs will result in the contact becoming unprofitable, the company must recognize in the current period the entire expected loss – which includes reversing any gross profit recorded in the prior period.

Revenue recorded =

Expense recorded =

85

Practice Problem (con’t)Suppose that the estimated cost to complete as of December 31, 2004 were $1,340,000 and the estimated cost turns out to be correct:

2003 2004 2005Contract costs incurred during the year

$450,000

210,000 1,340,000

Estimated costs to complete as of 12/31

1,050,000

1,340,000

0

Billings to Scott Industries 300,000 700,000 900,000Collections from Scott Industries

300,000 600,000 1,000,000

Compute the amount of revenue and expenses that should be recorded in each year.

2003 2004 2005

86

IFRSIAS 11 governs accounting for long-term construction contracts.

Primary difference: Completed-contract vs. Zero-Profit methods

87

Multiple-deliverables (EITF 00-21, ASC 605-25)

Examples:

What are managers’ incentives with respect to accounting for multiple-deliverable items?

Originally, in arrangement with multiple “deliverables”, delivered item could be considered separate “unit of accounting” only if all the following conditions were met:

1) Delivered item has value to customer on stand-alone basis

2) There is objective evidence of fair value of undelivered item

3) If general right of return exists, delivery/performance of undelivered item considered probable and substantially under control of vendor

Recent changes:

Allocation of amounts (consideration) received should be based on relative selling prices, using:

Vendor-specific objective evidence Third-party evidence Best estimate of selling price

BUT: Limited to amount that is NOT contingent upon delivery of additional item

88

Example: CellularCo. (from EITF 00-21)CellularCo runs a promotion in which new customers who sign a two-year contract receive a “free” phone. The contract requires the customer to pay a cancellation fee of $300 if the customer cancels the contract. There is a on-time “activation fee” of $50 and a monthly fee of $40 for the ongoing service. The same monthly fee is charged by CellularCo regardless of whether a “free” phone is provided. The phone costs CelluarCo $100. Further, assume that CellularCo frequently sells the phone separately for $120. CellularCo is not required to refund any portion of the fees paid for any reason. CellularCo is sufficiently capitalized, experienced and profitably business and has no reason to believe that the two-year service requirement will not be met. CellularCo is considering whether 1) the phone and 2) the phone service (that is, the airtime) are separable deliverables in the arrangement. The activation fee is simply considered additional arrangement consideration to be allocated. The phone and activation are delivered first, followed by the phone service (which is provided over the two-year period of the arrangement).

1) Are these separate units of accounting? Why or why not?

2) If yes, how should the total consideration be divided between the two units?

89

90

Example of disclosure on revenue recognition for multiple elements (from the 10-K of Cellco Partnership, d/b/a Verizon Wireless, Notes to Consolidated Financial Statements):

Revenue Recognition

The Partnership earns revenue by providing access to the network (access revenue) and for usage of the network (airtime/usage revenue), which includes roaming and long distance revenue. In general, access revenue is billed one month in advance and is recognized when earned; the unearned portion is classified in advance billings. Airtime/usage revenue, roaming revenue and long distance revenue are recognized when service is rendered and included in unbilled revenue until billed. Equipment sales revenue associated with the sale of wireless handsets and accessories is recognized when the products are delivered to and accepted by the customer, as this is considered to be a separate earnings process from the sale of wireless services. Effective July 1, 2003, the Partnership adopted the provisions under Emerging Issues Task Force (“EITF”) Issue No. 00-21, “Revenue Arrangements with Multiple Deliverables.” Prior to the adoption, customer activation fees, along with the related costs up to but not exceeding the activation fees, were deferred and amortized over the customer relationship period. Subsequent to the adoption of EITF 00-21, customer activation fees are recognized as part of equipment revenue. The existing deferred balances, prior to the effective date, will continue to be amortized in the statement of operations.

The Partnership’s revenue recognition policies are in accordance with the Securities and Exchange Commission’s (“SEC”) Staff Accounting Bulletin (“SAB”) No. 101, ‘‘Revenue Recognition in Financial Statements,” SAB No. 104, “Revenue Recognition,” and EITF Issue No. 00-21.

IFRSIAS 18 is the main standard related to revenue recognition and has similar requirements to SAB 104

BUT: more principles based vs. rules-based

91

Revenue Recognition Exposure Draft (November 2011)Purpose:

Core Principle: “Recognize revenue to depict the transfer of goods or services to customers in an amount that reflects the consideration received (or expected to be received)”Requirements:

Identify contracts with customers

Consider substance over form

Examples:

Identify separate performance obligations in the contract

Bundled goods: Separate performance obligation if good/service is “distinct”

Determine transaction price

amount of consideration expected to be entitled

Allocate transaction price to separate performance obligations

Based on relative standalone selling price basis

What if not sold separately?-Expected cost + margin approach-Expected market assessments approach

Recognize revenue when the entity satisfies each performance obligationWhen customer obtains control of good or service

92

CASH AND EQUIVALENTS

Cash

Cash equivalents short-term, highly liquid investments that are:

• easily converted into a known amount of cash.• close to maturity. – no longer than three months from

date of purchase• not sensitive to interest rate changes.

Cash and Cash equivalents usually combined and reported as the most liquid “current asset”.

Restricted cashcash that has been set aside for a particular use and is not available for paying current liabilities. Compensating Balance is some specified minimum amount that must be maintained on deposit with a bank that has made a loan to the company.

RECEIVABLESTwo main types of receivables:

Accounts receivable – short-term, oral promises to pay for goods or services sold

Notes receivable – short or long-term, written promises to pay a certain sum of money on specified future date(s)

93

Accounts ReceivableTwo main accounting issues:

1) Recognition (initial valuation)– record account receivable at face vaue less any trade discount and possibly and cash discount

2) Subsequent valuation – record account receivable (net) at net realizable value, using an allowance for returns and/or an allowance for uncollectibles as necessary.

Sales DiscountsOffered to encourage prompt payment.

Example of terminology: 2/10, n/30

2 /10, n/ 30# of days discount is available

Otherwise, net (or all) is due

CreditperiodDiscount

percent

94

Gross method (most common): Sales recorded at gross amount, discounts taken are recorded in a contra-revenue account called “Sales discounts”

Simple Example: ABC Company sells a widget to XYZ company for $5,000 on terms 2/10, n/30.

At time of sale:

If paid in 10 days:

Net method: Sales recorded at net amount, discounts NOT taken, recorded as additional income (perhaps as Interest Income).

At time of sale:

When discount period expires:

95

What is the cost of offering cash discounts?

In our simple example, what does the company earn if it doesn’t offer a discount?

What does it earn if it does offer the discount (suppose annual interest is 10%)?

ValuationAccounts receivable should be recorded at “net realizable value” – the net amount the company expects to receive in cash. Requires determination of whether accounts will be collected.

How do we know which accounts won’t be collected?-- Wait until specific accounts are known to be

uncollectible (direct write-off method).

-- Estimate amount of accounts receivables that will ultimately not be collected and record amount in the period in which revenue is generated (allowance method).

96

Accounting under Allowance Method:JE to record estimate of uncollectible accounts each period as bad debt expense:

JE to record specific accounts determined to be uncollectible:

- Two basic methods for estimating bad debt expense:

1) Percentage of sales method:

2) Percentage of receivables method

Practice ProblemThe following information is taken from the balance sheet of Mickey Company at 12/31/2004:

Accounts Receivable (net of allow. for doubtful accts of $10,000) $90,000

97

The following events occurred during 2005. Prepare the journal entries for each event:

1) Sold $1,000,000 on account

2) Collected $800,000 on A/R

3) Identified $20,000 of specific accounts which are deemed uncollectible

4) Estimated bad debt expense a. using the percentage of sales method (2.5%)

Compute the balances in each account at year end:

A/R Allow. for DA Bad Debt Exp.

98

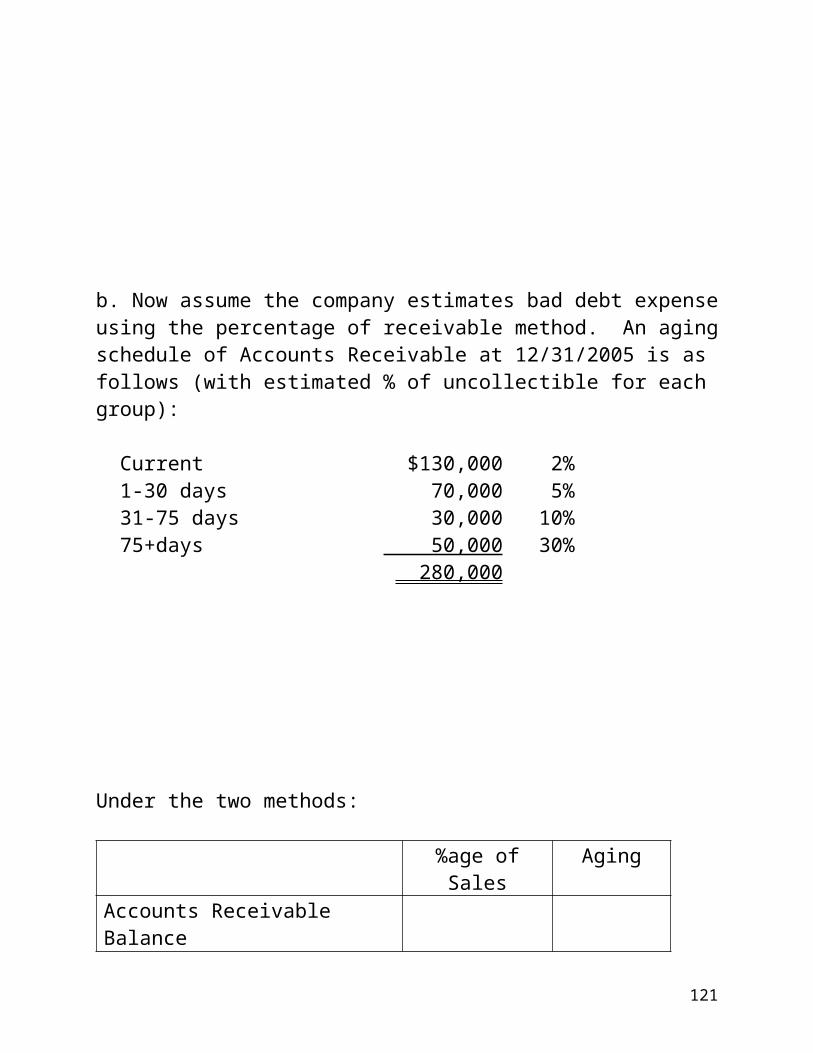

b. Now assume the company estimates bad debt expense using the percentage of receivable method. An aging schedule of Accounts Receivable at 12/31/2005 is as follows (with estimated % of uncollectible for each group):

Current $130,000 2%1-30 days 70,000 5%31-75 days 30,000 10%75+days 50,000 30%

280,000

Under the two methods:

%age of Sales

Aging

Accounts Receivable BalanceAllowance for Doubtful AcctsNet ReceivableBad Debt Expense

Why is bad debt expense and allowance balances different under these two methods?

99

Advantages/Disadvantages:

% of Sales

% of Receivables

Recoveries – Accounts that have been written off the books that are subsequently collected. Recoveries are accounted for by 1) reversing the write-off entry, 2) recording the collected cash.

100

Notes Receivable Notes receivable should be recorded at the present value of the cash expected to be collected.

Cash Flows:

Principles: amount to be received at the maturity Interest : periodic interest payment

Definition: written promises that will receive certain sum(s) of money at specified future date(s).

Short –term : Long – term :

Interest – Bearing Notes

Recognition: Record the face amount and recognize interest revenue

when it is earned;

EX: On October 1, 2012, McQueen Company sold car parts and accepted a $5,000, 90-day, 12% note from Mater Corp. Interest is payable at maturity. Mater paid all amounts due on December 31, 2012. Record the necessary journal entries.

1) First Scenario: McQueen’s FYE is 12/31

10/1/12

12/31/12

101

2) Second Scenario: McQueen’s FYE is 10/31

10/1/12

10/31/12

12/31/12

Non-Interest Bearing Notes

Recognition: using a discount account (essentially the same method as long-term notes)

EX: On October 1, 2012, McQueen Company sold car parts and accepted a $5,000, 90-day, non-interest-bearing note from Mater Corp. Mater paid all amounts due on December 31, 2012. Record the necessary journal entries.

102

1) First Scenario: McQueen’s FYE is 12/31

10/1/12

12/31/12

2) Second Scenario: McQueen’s FYE is 10/31

10/1/12

10/31/12

12/31/12

What is the effective rate?

Subsequent Valuation of Notes Receivable

103

Using an allowance account for uncollectibles : provisions for loan loss More important for long-term notes receivable

104

Financing with Accounts ReceivablesCompanies will sometimes transfer their receivables to another party.

Secured Borrowing – Borrowing money and using receivables as collateral

o Pledging –

o Assigning –

Practice Problem:On December 31, 2009, ABC Company assigns $100,000 of its accounts receivable to a finance company and signs a promissory note. The finance company advances 80% of the accounts receivable assigned less a finance fee of 1.6% of the accounts receivable assigned. Interest on the note at 12% is payable monthly.

105

December 31, 2009

During January 2010, ABC recorded cash collections of $58,000 and sales discounts (ABC uses the gross method) of $2,000 related to the assigned accounts receivable. At the end of January, ABC remitted the cash for the assigned accounts receivable collected plus accrued interest to the finance company.

January 2010

January 31, 2010

106

Selling Receivable – Transferring rights to collect receivables to a third party in exchange for cash

o Without recourse – purchaser bears risk of uncollectibility

o With recourse – seller bears the risk of uncollectibility

Why do firms do this?

Which would managers prefer?

Criteria for classification as “sale” (SFAS #140, ASC 860-10-40):

1. Transferred asset is isolated from transferor (beyond reach of transferor’s creditors)

2. Transferees can pledge or exchange the transferred asset

3. Transferor does not have effective control of asset through repurchase agreement

107

108

Practice Problem

On December 31, 2009, B Company sells $100,000 of accounts receivable to a factor. B receives cash equal to 90% of the factored accounts receivable. The factor retains the remaining 10% to cover its factoring fee (5% of the factored accounts receivable) and to provide a cushion against potential sales returns. B estimates that the fair value of the last 10% of receivables to be collected is $9,000 and that $3,000 of the factored accounts receivable will be uncollectible.

Without Recourse With Recourse

109

INVENTORYItems held for sale in the ordinary course of business. Three issues related to inventory: 1) Control, 2) acquisition/Production, 3) Cost Flow Assumption

ControlWhy are accurate, up-to-date records of inventory important?

-

Perpetual inventory system – tracks purchases and sales as they occur

Periodic inventory system – inventory physically counted periodically

What effect do errors in inventory counts have on the financial statements?

Recall: Beginning Inventory + Purchases – COGS = Ending Inventory

110

Balance Sheet

Income Statement

This Period This period

Next period

Overstated Inventory

Understated Inventory

Acquisition/Production of Inventory1) Items to include

Consigned goods

Goods in Transit

FOB Shipping point vs. FOB destination

Buyback arrangements

2) Cost to attachGeneral rule: All costs associated with manufacture, acquisition, storage or preparation.

Merchandising Company:

111

Manufacturing Company:

Cash Discounts Gross method: Record in inventory at gross amount,

reduce inventory if discounts taken

Net method: Record in inventory at net amount,

record Discounts Lost as other expense

112

Cost Flow AssumptionQuestion: How do we allocate the total cost of goods available for sale (beginning inventory + purchases) between COGS and ending inventory?

Beginning Inventory + Purchases = COGS + Ending Inventory

Four possibilities:1) Specific ID: Specifically identify which items were sold and

which are remaining.

2) FIFO – Assume items are sold in the order they are purchased.

COGS: First items purchased (oldest items) are the first items sold (FIFO)

End. Inv.:Last items purchased (newest items) stay in ending inv. (LISH)

3) LIFO – Assume most recent items purchased are sold first.

COGS: Last items purchased are the first items sold (LIFO)

End Inv: First items purchased stay in ending inv. (FISH)

4) Weighted Average: Items sold are valued at the weighted average cost of the goods available for sale

COGAS/total no. of units available for sale

IMPORTANT POINT: The method chosen need not represent the actual movement of inventory!! It is simply a method of assigning $ values to inventory items.

113

A company may use any of the above methods under either a periodic or a perpetual inventory system. The difference between, for example, LIFO periodic and LIFO perpetual, is in what you consider "available for sale" at the time of each sale.

For this class, we will assume a periodic inventory method for all computations of COGS.

Practice Problem:The following information relates to the Sunny Valley Corporation for the month of October:

Date Description Units Cost TotalBeginning 300 10October 5 Purchase 220 11October 12 Sale 260October 22 Purchase 150 12October 25 Sale 80TOTAL

Compute COGS and ending inventory assuming the company uses the FIFO cost flow assumption:

Compute COGS and ending inventory assuming the company uses the LIFO cost flow assumption:

114

Compute COGS and ending inventory assuming the company uses the Weighted Average cost flow assumption:

Notice that under each method COGS + EI = COGAS. Why?

FIFO LIFO WACOGSEnding Inv.COGAS

Which method provides the most current cost in Ending Inventory?

Which method provides the most current cost in COGS?

If prices rising: COGSLIFO COGSFIFONILIFO NIFIFOEILIFO EIFIFO

If prices falling COGSLIFOCOGSFIFO

NILIFO NIFIFO

115

EILIFO EIFIFO

These relations are true as long as the number of units purchased exceeds the number of units sold.

LIFO LiquidationsIf the number of units sold exceeds the number of units purchased, the company has essentially “sold” some of the beginning inventory units (which may have very old costs attached to them). This is called “liquidating LIFO layers”.

Practice Problem (con’t)Continue the Sunny Valley Corporation example. Suppose in the following year, the company has the following purchases and sales:

Units Cost TotalPurchases 200 13 2,600Sales 400

What is COGS under LIFO?

What is COGS under FIFO?

116

LIFO reserveThe difference between EI valued on a LIFO basis and EI valued on a FIFO basis is often referred to as the “LIFO reserve”. The LIFO reserve is a contra-account to Inventory.

Companies often maintain records on a FIFO basis and at the end of each period compute EI on a LIFO basis and adjust the reserve accordingly.

Practice ProblemMcCoy Industries is a manufacturer of small office equipment. The company values its inventories under the LIFO method. At 12/31/2004, the company reported the following:

Inventories (net of LIFO reserve of 25,000)125,000

During 2005, the company purchased $825,000 of inventory and determined COGS using FIFO to be $800,000. At 12/31/2005, inventories using LIFO would be valued at $140,000. Record the journal entry to adjust the LIFO reserve

FIFO or LIFO?Arguments in favor of LIFO Arguments in favor of FIFO

117

IFRSIAS 2 governs accounting for inventory.

Primary Difference: NO LIFO!

Dollar Value LIFOUsing the LIFO method discussed previously can be problematic because of 1) record-keeping and 2) LIFO liquidations.

An alternative is Dollar-value LIFO (DVL), which applies LIFO procedures to pools of similar goods based on dollars rather than units. Ending inventory is compared to beginning inventory, both measured in dollars adjusted for inflation.

Recall: Under unit LIFO,If units purchased > units sold(or units EI > units BI) LIFO layer addedIf units purchased < units sold(or units EI < units BI) LIFO layer liquidated

Under DVL, If $ purchased > $ sold(or $ EI >$ BI) LIFO layer

addedIf $ purchased < $ sold(or $ EI < $ BI) LIFO layer

liquidated

But, if tracking inventory in $’s and not units:

118

Inventory in $ = inventory in units x cost/unit

Inventory in $ could be due to in units or in cost/unit

Inventory in $ could be due to in units or in cost/unit

Therefore, to determine if LIFO layers are added or liquidated, we need to adjust the inventory in $’s to “take away” the effect of changes in cost/unit (i.e., “price level” changes).

How do we do that?1. Compute price change from “base year” prices (price

index) for the pool of inventory

Price index – a measure of the change in prices from a base year (the first year dollar value LIFO is adopted in this case) to the current year.

Price index = Ending inventory quantities x current end-of-year costs Ending inventory quantities x base end-of-year costs

(Mostly is given)

2. Divide the inventory value for the pool (based on current prices) by price index

The difference between the beginning inventory at base year prices and the ending inventory at base year prices indicates whether a layer has been added or taken away:

If EIBASE$ > BIBASE$ LIFO layer added

119

add LIFO layer at current year cost (multiply layer at base year prices and multiply by price index)

If EIBASE$ < BIBASE$ LIFO layer liquidated remove most recent layers added

120

Practice ProblemOn January 1, 2000, Deoxys Inc. changed from FIFO to dollar value LIFO. At that date, its beginning FIFO inventory was $100,000. The following information relates to the company’s inventory for the years ended 12/31/2000 through 12/31/2003:

Year-ended Ending inventory at current costs (or

FIFO)Year-end price

index12/31/2000 $124,800 1.212/31/2001 169,500 1.512/31/2002 144,200 1.412/31/2003 140,400 1.3

Compute ending inventory on a dollar value LIFO basis for each year:

121

If the company purchased $500,000 of goods during 2000, what would COGS be under FIFO and under LIFO?

122

INVENTORY – ADDITIONAL ISSUES

Lower of Cost or Market (LCM) ruleGAAP requires that inventories be reported at the lower of “cost” or “market”

What is “Cost”?

What is “Market”?

Under GAAP, “market” is defined as replacement cost (RC), except:

If RC > Net Realizable Value (NRV), use NRV

If RC < NRV less normal profit margin, use NRV less normal

profit margin

Note that the rule is “asymmetric” – inventory is reduced if market falls below cost but is NOT written up if market rises above cost.

The LCM rule can be applied to products individually or to groups of products. What is the advantage of grouping products?

Journal entry to record write-down:

What impact does the company’s choice of cost flow assumption have on the probability of an inventory write-down?

123

Practice ProblemThe following data relate to Zubat Inc. for the five different items it sells to its customers. Determine the appropriate “market” value for each of the five products.

Product A

Product B

Product C

Product D

Product E

Historical Cost $1,000 $2,000 $1,500 $1,125 $800Replacement Cost 550 1,300 675 1,000 900Estimated selling price 850 1800 1,200 1,875 1,400Estimated costs of disposal 250 600 300 375 240Normal Profit Margin 90 180 120 200 140“Market”

What value should be reported for ending inventory if the company applies the LCM, to individual products? Prepare any necessary journal entries to adjust inventory to LCM.

What is the value of ending inventory if the company applies LCM to the entire inventory? Prepare any necessary adjusting journal entries.

124

IFRSAnother difference between US GAAP and IAS 2 relates to LCM. Under IAS 2 market is always defined as NRV.

How would that change our previous analysis?

Also, write-downs can be subsequently reversed if market value increases BUT only up to the amount of the original write-down.

o

125