Embed Size (px)

Citation preview

ME 101: High Mix/Low Volume Manufacturing

Lecture 5 - September 6, 2012

• Announcements•Prof. McMains was called in for jury duty today

•She will unlikely be back for office hours this afternoon•The ME 101 discussion section classroom has been assigned:

•Friday 11:00 AM VALLEY LSB Room 2066

•Guest lecture by Prof. Dornfeld

ME 101: High Mix/Low Volume Manufacturing

Manufacturing Productivity

Source: USA Today, June 15, 2001, p. 2B

ME 101: High Mix/Low Volume Manufacturing

Now, consider the problems the Japanese faced more recently with

the fluctuation of the value of the Yen!

Over the last 10 years or so the yen has increased in value almost

two to one vs. the dollar. (More recently this has gotten a bit better-

what is the Yen/$ conversion today?)

So 1 Yen buys twice as much in the US now compared to before

(or, by contrast, 1 US$ buys about half as much as it did before.)

This makes Japanese good very expensive in the US and US goods

cheap in Japan.

Uphill Battle - Dollar and Exchange Rates

ME 101: High Mix/Low Volume Manufacturing

EXCHANGE RATES: Yen per $1

http://finance.yahoo.com/

ME 101: High Mix/Low Volume Manufacturing

Quick £ook at some production economic$? ¥es!

We need a basis for evaluating alternatives - a logical basis for comparison - so we look at the value of the alternatives

For common methods:- payback period (how long will it take to get our

money back?)- present worth (what is the value of this long term

investment today?)- uniform annual cash flow (what can this yield yearly?)- rate of return (how does this compare to other investment

opportunities?)

Usually use one (or more) of these to compare alternatives.

Let’s look at each method and how it is applied.

ME 101: High Mix/Low Volume Manufacturing

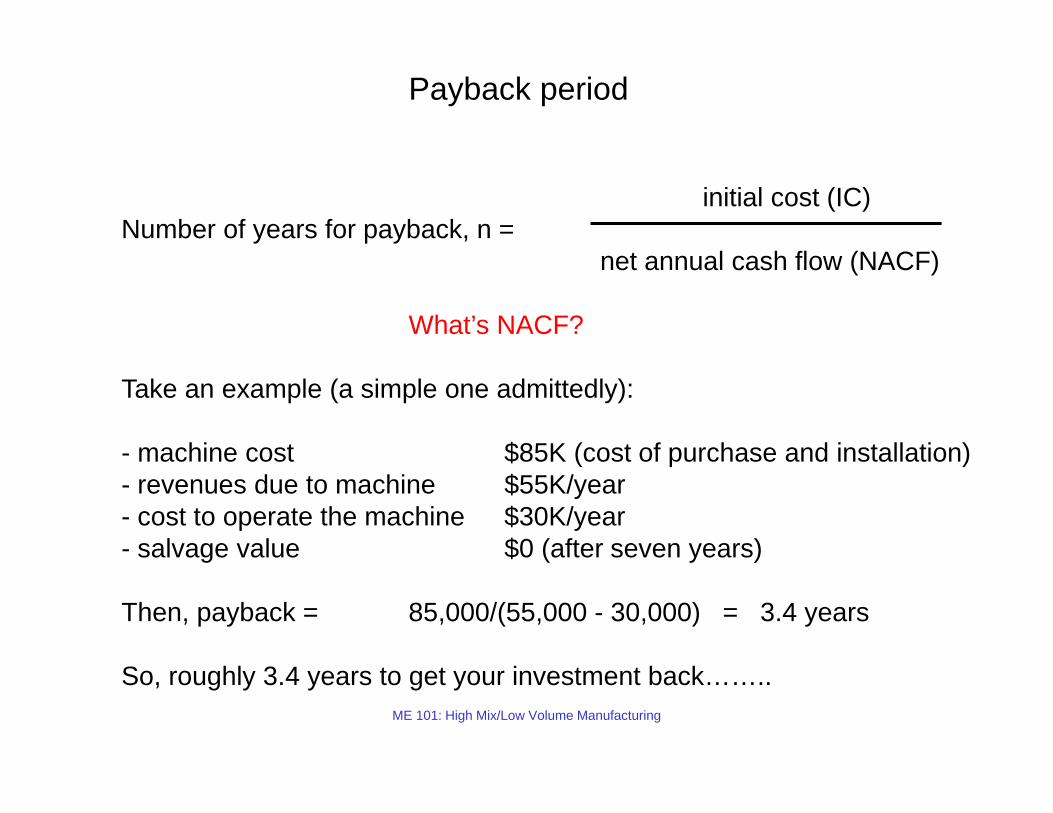

Payback period

initial cost (IC)Number of years for payback, n =

net annual cash flow (NACF)

What’s NACF?

Take an example (a simple one admittedly):

- machine cost $85K (cost of purchase and installation)- revenues due to machine $55K/year- cost to operate the machine $30K/year- salvage value $0 (after seven years)

Then, payback = 85,000/(55,000 - 30,000) = 3.4 years

So, roughly 3.4 years to get your investment back……..

ME 101: High Mix/Low Volume Manufacturing

Payback period, cont’d

Income+

Expense-

After 3.4 years, revenues = expenses

1 2 3 4 5years

85K

30K/year

55K/year

3.4 years

revenues

expenses

0

purchasemachine

ME 101: High Mix/Low Volume Manufacturing

Payback period, cont’d

If the net annual cash flow varies year to year…….

How would that happen?

Thenn

initial cost, IC = (NACFj)j=1

and then determine n

ME 101: High Mix/Low Volume Manufacturing

Present worth

Present worth (PW): Determine the equivalent present value of all current and future cash flows

But…….future cash flow value based on the interest rate in the future!

positive PW GOOD

negative PW BAD

We will need interest rate charts to help determine this

What effect does interest rate have on this calculation?

That is……i% gives better/worse PW?

ME 101: High Mix/Low Volume Manufacturing

Cash flow diagram

Income+

Expense-

1 2 3 4 5years

85K

30K/year

55K/year

0

future revenues

future expenses

ME 101: High Mix/Low Volume Manufacturing

F final payment; P present worth; A annual payment (expense); i interest; n years

ME 101: High Mix/Low Volume Manufacturing

PW = - machine cost + future revenues/year (P/A, i%, n) - cost/year (P/A, i%, n)

= - 85K + 55K (P/A, 10%, 7) - 30K (P/A, 10%, 7)

= -85K + 55K (4.8684) - 30K (4.8684)

= $36,700 +

Present worth, cont’d

UAC example

ME 101: High Mix/Low Volume Manufacturing

Uniform annual cost, UACThis represents the current and future cash flow as an equivalent annual cost

The initial costs, such as equipment, must be expressed as annual cost; the annual operating expenses and revenue are already annualized

For this example,

UAC = -85K (A/P, I%, 7) + 55K - 30K

= -85K (.2054) + 25K

-17,459 (see interest rate chart)= 7, 541 +

Hence, the investment exceeds the 10% rate of return (if it was exactly 10% rate of return UAC would be zero)

ME 101: High Mix/Low Volume Manufacturing

Rate of return (return on investment ROI)

Here we calculate the ROI of an investment using either PW or UAC

For our example, using UAC

UAC = 0

= -85K (A/P, i%, 7) + 55K - 30K

(A/P, i%, 7) = 25K/85K= 0.2941

Interpolate in interest rate charts for varying interest ratesalong n =7 for matching interest rate factor

ME 101: High Mix/Low Volume Manufacturing

Rate of return (return on investment ROI)

Here we calculate the ROI of an investment using either PW or UAC

For our example, using UAC

UAC = 0

= -85K (A/P, i%, 7) + 55K - 30K

(A/P, i%, 7) = 25K/85K= 0.2941

Interpolate in interest rate charts for varying interest ratesalong n =7 for matching interest rate factor

Here, i = 22.15% the “true” rate of return

ME 101: High Mix/Low Volume Manufacturing

Various costsSome definitions...- direct labor cost: the sum of wages paid to

those who operate the machines for processing and assembly

- material cost: cost of all “raw” materials- overhead cost: all “other” costs associated

with running the factory- factory overhead: all factory costs other

than direct labor and materials(see lecture 2)

- corporate overhead: costs other than manufacturing activities (see lecture 2)

ME 101: High Mix/Low Volume Manufacturing

Costs in manufacturing

Fixed and variable costs

- fixed: constant for any level of productionproperty taxfactory buildinginsurancecost of production equipment

- variable: scales with level of productiondirect labor costs (plus fringe benefits)raw materialspower and other consumables

ME 101: High Mix/Low Volume Manufacturing

Breakdown of costs for a manufactured product

Source: Skinner, W., “The focused factory,” Harvard Business Review, May-June 1974, pp. 113-121 ≈ 50%

ME 101: High Mix/Low Volume Manufacturing

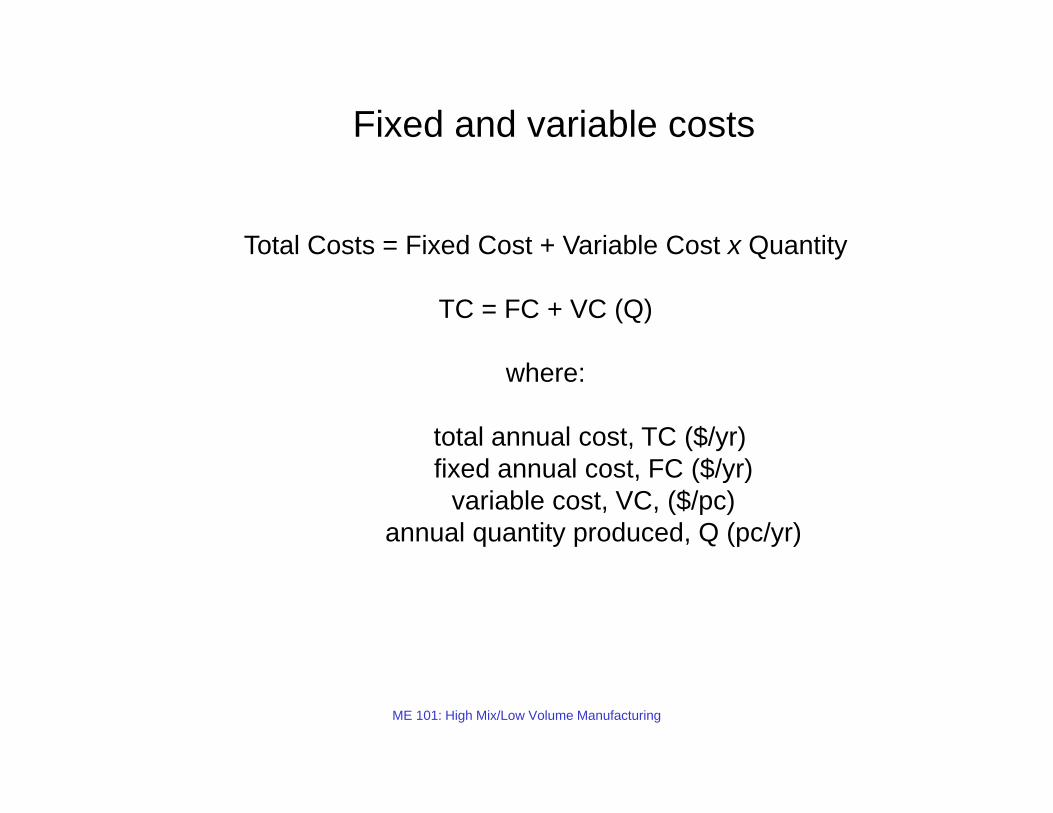

Fixed and variable costs

Total Costs = Fixed Cost + Variable Cost x Quantity

TC = FC + VC (Q)

where:

total annual cost, TC ($/yr) fixed annual cost, FC ($/yr)

variable cost, VC, ($/pc)annual quantity produced, Q (pc/yr)

ME 101: High Mix/Low Volume Manufacturing

Fixed and variable costs

Production output

Cost

Fixed costs

Variable costs

ME 101: High Mix/Low Volume Manufacturing

Real costs

Typical factory OH rates, FOHR, can be severaltimes the cost of direct labor calculated as

total cost of operating a plantdirect labor costs

Corporate OH rates, COHR, (including cost ofmanagement, engineering, accounting, personnel) are

cost of managementdirect labor costs

ME 101: High Mix/Low Volume Manufacturing

Real costs, cont’d

Cost of equipment usage

Machine cost is the capital cost of the machineapportioned over the life of the asset at the appropriate rate of return used by a firm

expressed as $/hour

Also have machine overhead which includes thecost of power to operate, floor space, maintenanceand repair including consumables, etc.

ME 101: High Mix/Low Volume Manufacturing

Cost rate for a work center

Total cost rate for a work center is sum of labor and machine costs

CO = CL (1 + FOHRL) + Cm (1 + FOHRm)

CO = hourly rate to operate work center ($/hr)CL = direct labor wage rate ($/hr)FOHRL= factory OH rate for laborCm = machine hourly rate ($/hr)FOHRm= factory OH rate for machines

Corporate OH rates not included since, for comparison of alternatives,those costs will be present in any alternative.

ME 101: High Mix/Low Volume Manufacturing

Breakeven analysis

Breakeven analysis done for- profit analysis (effect of changes in

output on costs and revenues)breakeven is when costs = revenues

- production method cost comparison(effect of changes in output on two or more methods of production)

breakeven is when costs for the two production methods are equal

ME 101: High Mix/Low Volume Manufacturing

Profit breakeven analysis

fixed costs

ME 101: High Mix/Low Volume Manufacturing

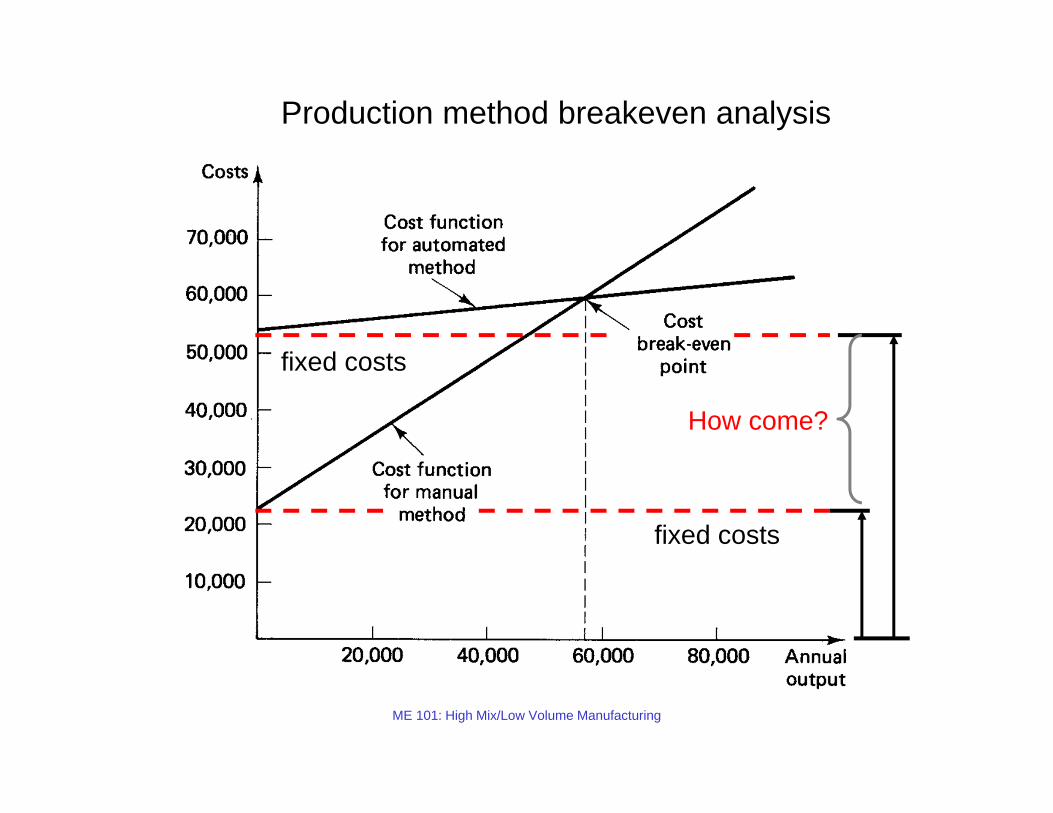

Production method breakeven analysis

fixed costs

fixed costs

How come?

ME 101: High Mix/Low Volume Manufacturing

Review:another important financial metric…“Working Capital”

Source: S. Tully, “Raiding a company’s hidden cash,” Fortune, Aug. 12, 1994, p.82.

Working capital consists of inventories — raw materials, WIP and finished goods — as well as a companies receivables (what other companies owe it) minus its payables (what it owes other companies).

On the average (circa ‘94) Fortune 500 companies use 20¢ of working capital for each dollar of sales.

ME 101: High Mix/Low Volume Manufacturing

Review:“Working Capital” cont’d

Source: S. Tully, “Raiding a company’s hidden cash,” Fortune, Aug. 12, 1994, p.82.

Reducing working capital has a big effect:

first - it improves the financial picture (a dollar saved is a dollarearned……)

second - it forces companies to produce and deliver faster than the competition, enabling them to win new business and charge premium prices for filling rush orders. Costs decrease (lower inventory, fewer warehouses, lower labor costs (aka fewer workers)

ME 101: High Mix/Low Volume Manufacturing

This promotes HMLV manufacturing

Premium on:- rapid movement of order and part- product manufactured “to order”…..Burger King!- finished goods move from line to delivery truck- suppliers pushed to cut inventories…deliver “just

in time” since minimal stock translates into lower raw material prices (Deere story)

As velocity increases…..inventory (working capital) decreases

What does this say about the production line….availability? defect rates? WIP to handle the occasional line failure?

ME 101: High Mix/Low Volume ManufacturingRef. Fortune, Nov. 14, 1994, p. 158

Increasing Efficiency at Boeing

Boeing is making leaps in all phases of manufacturing, such as parts production and final assembly - building big

sections of the plane in parallel rather than in sequence, for example. One source of innovation is the Sheet Metal

Center, a unit making 100,000 different parts a year, including the skins and frames that form the shell of an aircraft. Until recently, Sheet Metal supplied door parts

in big bins and workers would spend hours sorting through the bins before doors could be built. Now, the Center

delivers the doors in ready-to-assemble kits directly to the assembly bays, totally bypassing warehouses.

Producing kits for entire modules shows how stretch targets draw the best ideas from the plant floor. Since 1993, Sheet Metal has cut stocks awaiting assembly

from $270 Million to $130 Million. Now Boeing is extendingthe kit concept to wing assemblies and other sections.

ME 101: High Mix/Low Volume Manufacturing

Working capital costs

What are the costs in a warehouse?

- units x value per unit

- warehouse space $/sq. ft.

- labor $/hour

- equipment

- insurance, utilities

- other overhead ….managers

- and …..

ME 101: High Mix/Low Volume Manufacturing

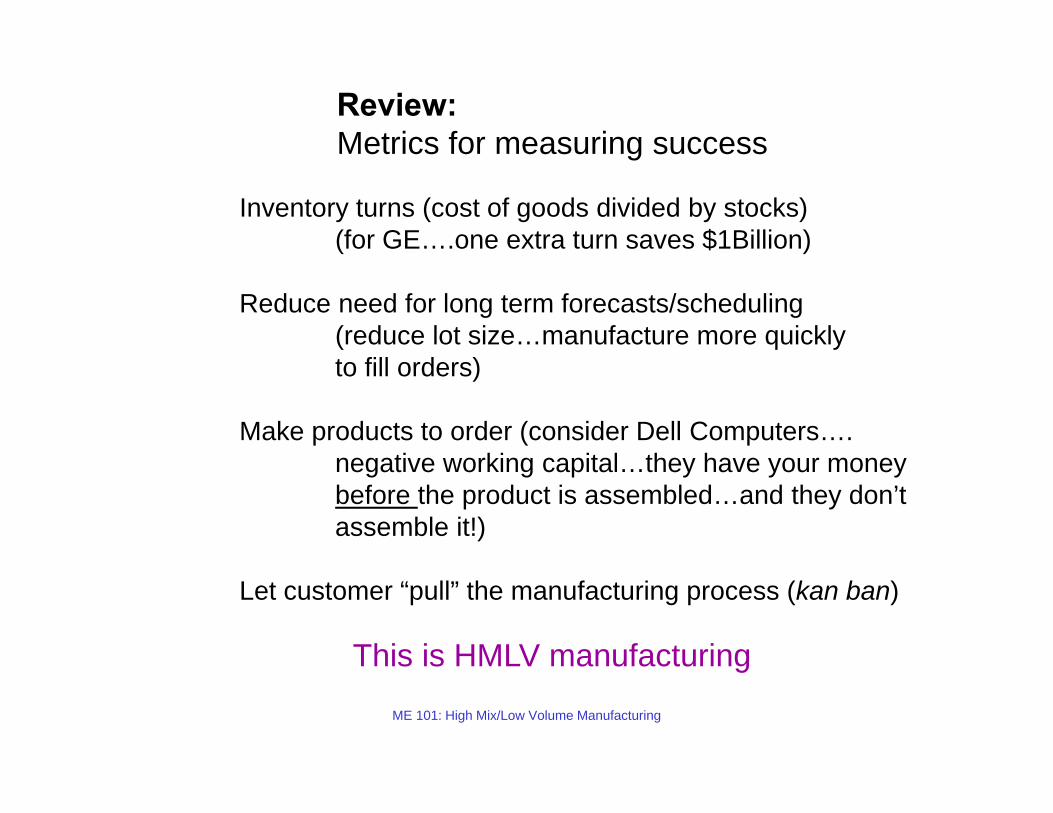

Review: Metrics for measuring success

Inventory turns (cost of goods divided by stocks)(for GE….one extra turn saves $1Billion)

Reduce need for long term forecasts/scheduling(reduce lot size…manufacture more quickly to fill orders)

Make products to order (consider Dell Computers….negative working capital…they have your moneybefore the product is assembled…and they don’t assemble it!)

Let customer “pull” the manufacturing process (kan ban)

This is HMLV manufacturing