Embed Size (px)

DESCRIPTION

Land & Energy Quarterly is all about oil, gas, real estate and life as we know it in Western Pennsylvania. The magazine is meant to teach you of the legal side of the laws of land and the boom of the oil and gas industry.

Citation preview

PREMIER ISSUE

LAND & ENERGYQUARTERLY

Energy – The Professional staff provides abstracting services and oil, gas, mineral, and coal Certified Title Opinions detailing own-ership/leasehold of surface and subsurface interests for multi-national corporations, regional and local gas exploration/production companies, real estate professionals, developers, investors, buyers, sellers, and lessors of land.

• Cost effective “curative” legal services removing defects in the chain of title.• Oil and gas valuations, family limited partnerships, corporations, limited liability companies, severance deeds, lease assign-

ments, and estate planning documents to reduce income taxes and minimize or eliminate inheritance taxes on subsurface interests.

• Negotiation services for Rights of Way and Easements for production distribution.• Representation for multi-million dollar sale of several hundred acre site and related assets for multiple well pad and

compression station.• Lease agreements between exploratory production companies and not for profit organizations [501 (C) (3) (6) (7)] forming

for profit entities as the depository of severed subsurface interests and related documentation to enable not-for-profits to receive unrelated business income (UBI) while maintaining non-profit and/or charitable tax status.

• Counsel to national midstream company for over the limit weight claims successfully reducing fines.

Real Estate – Legal services to local, regional, and national real estate companies, banks, investors, exploration and production companies, homeowners associations, third party employee relocation companies, buyers, and sellers.

• Representation of clients in over 10,000 residential, commercial, and relocation real estate transactions.• Counsel to developers for the acquisition, sale, and improvement of residential housing lots and condominium

developments.• Counsel for regional and national real estate brokerages involving oil, gas, mineral, and coal interests including quarterly

accredited continuing education for realtors and appraisers.

Litigation – Legal services in the areas of personal injury, insurance company bad faith, real property, landlord tenant, oil and gas contracts, and curatives.

• Twenty-five (25) years and over 50 jury trials of experience throughout state and federal courts in Pennsylvania and West Virginia.

• Received $1.6 million dollar verdict against a major insurance company for breach of contract and bad faith.• Negotiation for six figure settlements.• Successfully litigated products liability case to the Pennsylvania Superior and Supreme Courts.

Estate Planning – Administration, counsel clients on the importance of properly prepared estate plans to minimize inheritance taxes and direct assets after death.

• Preparation of hundreds of Estate Plans including Last Will and Testaments, Durable General and Health Care Powers of Attorney, living wills, revocable and irrevocable trusts.

• Representation in Orphan’s Court for probatable assets of testate and intestate decedents.• Preparation and filing of state and federal inheritance tax packages.• Counseling for wealth preservation.

Business, Tax, Accounting – Counsel and represent clients on selection of business entitles, income, and inheritance tax liabilities.

• Advise clients as to business entity selection for protection of personal and corporate assets.• Form limited liability partnerships, companies, and corporations.• Quick books reconciliation.• Preparation of personal tax returns and business tax returns.• Accounting and controller services.• Representation at IRS audits and before the United States Tax Court.

About the Firm…

Lawrence D. Brudy & Associates, Inc. is a regionally positioned Appalachian Basin Law Firm

comprised of Attorneys, Certified Public Accountants, Paralegals, Legal Assistants, Title

Examiners, Title Analysts, Licensed Title Insurance Agents, Real Estate Brokers, Marketing, and

Public Relations Personnel.

Practice Groups

TABLE OF CONTENTSWe are y

ou

r attorn

eys in

today's ever-changing w

orld

Summer 2013, Lawrence D. Brudy & Associates, Inc.,

was a proud sponsor of the Butler BlueSox.

“The way a team plays as a whole determines its success. You may have the greatest bunch

of individual stars in the world, but if they don't play together, the club won't be worth a

dime.” - Babe Ruth

Enhanced Title Insurance Policies…………………………………………………….

Oil, Gas and Mineral Rights Disclosure and Addendum…………………………….

What is “Title Washing”?……………………………………………………………..

2013 Pennsylvania Housing Market…………………………………………………..

Enhanced Title Opinions: The Use of Comprehensive Well Data Tools……………

The Oil and Gas Lease: Inside the Controversy……………………………………..

Oil & Gas Interests & Lease Negotiations…………………………………………….

How Oil and Gas Production Affects “Clean and Green” Properties……………….

Before you Sign… Tips for Pennsylvania Farmers…………………………………..

Pennsylvania Supreme Court Rules in Butler v. Charles Powers Estate

to Affirm Dunham Rule………………..……………………………………..………..

What is a Deed?……………………………………..………………………………….

The Use of Mapping Data Programs………………………………………………….

Page

Page

Page

Page

Page

Page

Page

Page

Page

Page

Page

Page

CLOSINGS • TITLE INSURANCE • LITIGATION

855.935.1400

www.ldbassoc.com

REAL ESTATE:

RESIDENTIAL • COMMERCIAL • RELOCATION

• TITLE INSURANCE • RIGHT OF WAY AGREEMENTS •

SURFACE/SUBSURFACE DEED PREPARATION

• ‘SIXTY YEAR’ TITLE SEARCHES • ASSIGNMENTS •

LAND AGREEMENTS • SALE / PURCHASE AGREEMENTS

DEED PLOT SURVEY PRINTS

Lawrence D. Brudy, a licensed Pennsylvania attorney, real estate bro-

ker, title insurance agent and notary public, has provided accredited

continuing education for the Education Development School of Real

Estate, Career Growth Real Estate Academy, Butler County Associa-

tion of Realtors, Appraisal Institute Pittsburgh Metropolitan Chapter

and the Institute for Paralegal Education. The focus of the continuing

education has been on oil, gas, coal and minerals and the affects on

buying, selling and financing all or a portion of subsurface interests in

tandem with the surface estate.

Very few buyers realize that, like other insurance

products, the title insurance industry has

insurance products that offer different coverage. An en-

hanced policy, which offers additional coverage from

the standard coverage, is available to the homeowner.

Although the enhanced policy premium is 10% higher

than the standard policy premium, the reality is a

minimal cost to the homeowner for the ability to

substantially reduce their risk and exposure on one of

the largest investments they will make in a lifetime.

Both the enhanced policy and the standard policy

include protection against any defect in title existing at

the time of purchase. Also included in a standard policy

is protection against prior instruments of record that

would be in a first lien position, title if vested in

someone other than the seller, the unmarketability of

title, and the right of pedestrian access to the property.

The enhanced policy, however, covers a number of other

issues that may arise, including building permit

violations, subdivision problems, and instances of for-

gery even after the policy is issued. Furthermore, the

enhanced policy includes automatic increases in

coverage for five years, to account for the increase of

value in your home.

Because of the added coverage and the low cost offered

by the enhanced policy, it is important that purchasers

are aware it exists. Buyers who decide to add this

coverage will be required to have a survey completed,

which should always be recommended as a precaution.

A buyer should be aware of what they are buying, since

again this is likely one of the biggest purchases they will

make in their lifetime.

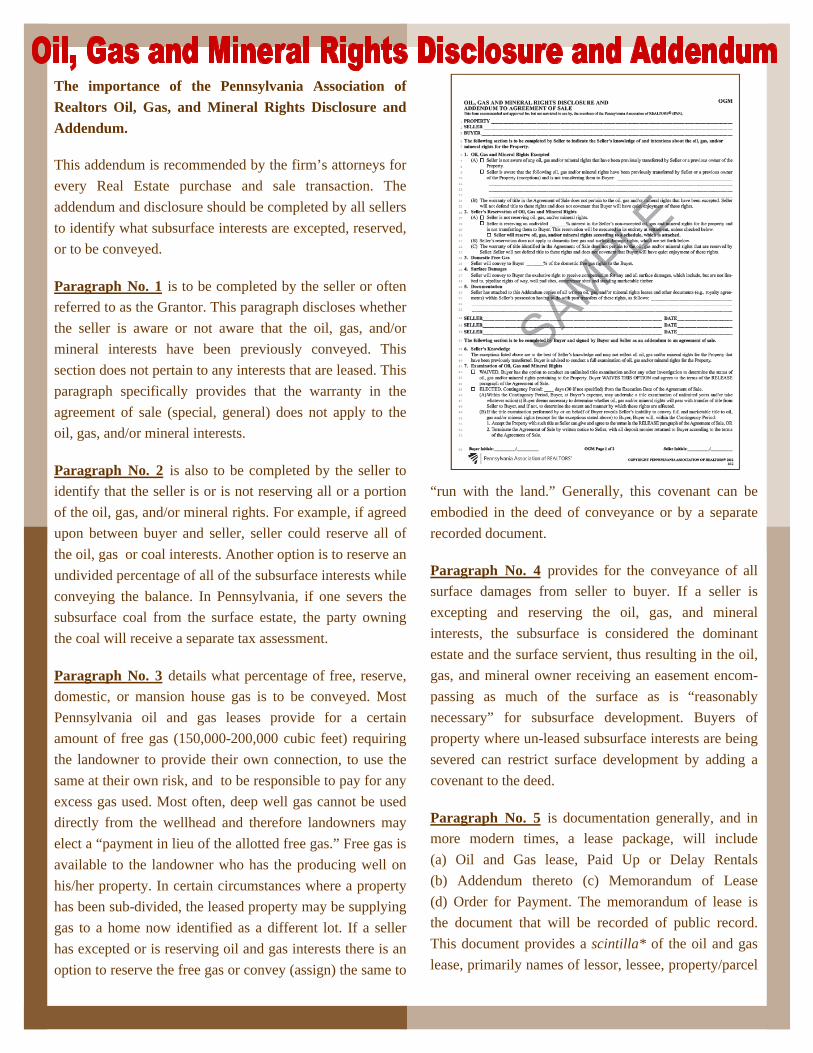

The importance of the Pennsylvania Association of

Realtors Oil, Gas, and Mineral Rights Disclosure and

Addendum.

This addendum is recommended by the firm’s attorneys for

every Real Estate purchase and sale transaction. The

addendum and disclosure should be completed by all sellers

to identify what subsurface interests are excepted, reserved,

or to be conveyed.

Paragraph No. 1 is to be completed by the seller or often

referred to as the Grantor. This paragraph discloses whether

the seller is aware or not aware that the oil, gas, and/or

mineral interests have been previously conveyed. This

section does not pertain to any interests that are leased. This

paragraph specifically provides that the warranty in the

agreement of sale (special, general) does not apply to the

oil, gas, and/or mineral interests.

Paragraph No. 2 is also to be completed by the seller to

identify that the seller is or is not reserving all or a portion

of the oil, gas, and/or mineral rights. For example, if agreed

upon between buyer and seller, seller could reserve all of

the oil, gas or coal interests. Another option is to reserve an

undivided percentage of all of the subsurface interests while

conveying the balance. In Pennsylvania, if one severs the

subsurface coal from the surface estate, the party owning

the coal will receive a separate tax assessment.

Paragraph No. 3 details what percentage of free, reserve,

domestic, or mansion house gas is to be conveyed. Most

Pennsylvania oil and gas leases provide for a certain

amount of free gas (150,000-200,000 cubic feet) requiring

the landowner to provide their own connection, to use the

same at their own risk, and to be responsible to pay for any

excess gas used. Most often, deep well gas cannot be used

directly from the wellhead and therefore landowners may

elect a “payment in lieu of the allotted free gas.” Free gas is

available to the landowner who has the producing well on

his/her property. In certain circumstances where a property

has been sub-divided, the leased property may be supplying

gas to a home now identified as a different lot. If a seller

has excepted or is reserving oil and gas interests there is an

option to reserve the free gas or convey (assign) the same to

“run with the land.” Generally, this covenant can be

embodied in the deed of conveyance or by a separate

recorded document.

Paragraph No. 4 provides for the conveyance of all

surface damages from seller to buyer. If a seller is

excepting and reserving the oil, gas, and mineral

interests, the subsurface is considered the dominant

estate and the surface servient, thus resulting in the oil,

gas, and mineral owner receiving an easement encom-

passing as much of the surface as is “reasonably

necessary” for subsurface development. Buyers of

property where un-leased subsurface interests are being

severed can restrict surface development by adding a

covenant to the deed.

Paragraph No. 5 is documentation generally, and in

more modern times, a lease package, will include

(a) Oil and Gas lease, Paid Up or Delay Rentals

(b) Addendum thereto (c) Memorandum of Lease

(d) Order for Payment. The memorandum of lease is

the document that will be recorded of public record.

This document provides a scintilla* of the oil and gas

lease, primarily names of lessor, lessee, property/parcel

identifier, and lease term. The most important docu-

ments to be reviewed are the oil and gas lease and the

addendum. The lease will outline the exploration and

production company’s terms and conditions for leas-

ing. The addendum modifies the boiler plate terms of

the lease pursuant to the negotiations between the

landowner and the exploration and production com-

pany.

Paragraph Nos. 6 & 7 provide the opportunity for the

buyer to conduct a title examination to determine the

status of the oil, gas, minerals, and coal. This exami-

nation should include an attorney’s certification

(interpretation of the public record search and

“curatives” to enable subsurface development of the

property). This process will take 30-45 days and costs

$5,000.00 or more. If a seller is conveying the subsur-

face interests, a Certified Title Opinion should be pre-

pared to verify the ownership and leasehold of all sub-

surface interests. Because a property is under lease,

this is not conclusive evidence that the lessor owns or

is entitled to royalties or subsurface interests.

Paragraph No. 8 is the area where by the seller is to

provide the “reservation” language (see paragraph No.

2) if the seller is reserving the non-excepted subsur-

face interests. The seller is to provide the buyer with

the reservation language to be incorporated into the

deed of conveyance.

Paragraph No. 9 provides for the review of the

seller’s reservation language. As with other para-

graphs of the PAR Agreement of Sale, both para-

graphs 8 and 9 default to a fifteen (15) day response.

In Western Pennsylvania it is customary practice for

the law firm or title insurance agency working for the

buyer or mortgage lender to prepare the deed on be-

half of the seller, at a charge to the seller. Our firm, as

part of the representation whether representing a buyer

or a seller, prefers to prepare the deed of conveyance

at a cost to our client to ensure our clients contractual

obligations are accurately memorialized in the

document(s).

The Firm’s Attorneys and Certified Public Accountants

involved in providing tax planning and the preparation of

estate plans for clients are often asked what items and/or

documents should be stored in a Safe Deposit Box.

Last Will and Testaments, Powers of Attorney and Liv-

ing Wills are not filed or recorded in Pennsylvania,

[generally] with the exception of a real property convey-

ance or death [probate]. Our Attorneys prepare estate

planning documents, in triplicate originals (Last Will and

Testaments, Powers of Attorney and Living Wills). We

suggest a set remains with the client, a set with the Ex-

ecutor/Executrix and the last kept in the file or place

where all of the “important papers” are kept. In the event

changes need to be made to the documents, we recom-

mend those changes be through our office as the docu-

ments are retained on our computer systems.

These are items or documents we do not recommend you

keep in a Safe Deposit Box: Last Will and Testament;

Durable General and Health Care Powers of

Attorney; Intervivos and Testamentary Trusts; Living

Wills; Funeral / Burial Arrangements; Financial docu-

ments including computer logins, pass-

words and usernames; and, Cash.

These are items or documents we do recommend you

keep in a Safe Deposit Box: Sentimental or heirloom

items; Impossible to replace photographs; Rare coins

and stamps; Military medals; and Inventory of all home

items (lists, video, DVD) including the combination of

home safe.

Most important is to provide your person of trust with

the information, direction and location of where the

“important papers” can be found.

Many consider the drilling of

Edwin Drake’s oil well in

1859 the beginning of what

we know today as the oil and

gas industry in this country. In the years thereafter,

subsurface interests began to be severed from sur-

face ownership. What also followed were attempts

to recover those interests by subsequent owners in

title. One such method in the early 20th Century was

the practice of “title washing.” A reading of the

pertinent sections of Pennsylvania Oil and Gas

Law and Practice (First Edition, George T. Bisel

Co., Inc. 2012) provides the following as to the

practice’s concept:

To understand the manner in which a parcel of land

is to be taxed, it must first be determined how the

property in question is assessed. Local assessors

have traditionally divided real property into two

distinct classes of property, Seated Land and Un-

seated Land (See 72 P.S. §5511.21). Seated Land

applied to those parcels of real estate that were im-

proved through building, cultivation or otherwise,

while Unseated Land was that which was unim-

proved or wild, typically consisting of unimproved

forest land. The difference in distinctions created a

good deal of litigation, as could be expected, with

the state legislature ultimately validating all tax

sales regardless of classification.

The importance of the distinction between seated

and unseated lies in the underlying premise that

taxes on unseated land constitute a tax against the

land itself, i.e., in rem, and conversely taxes on

seated land constitute a tax against the owner, i.e.,

in personam. As such there is no personal liability

for taxes on unseated land. Historically then, no-

tice requirements varied between the two classifi-

cations, with personal notice not being required for

unseated land.

In Mullane v. Central Hanover Bank and Trust,

339 U.S. 306 (1950), the Supreme Court held that

the distinction between “in personam” and “in rem”

jurisdiction is not the basis for difference in notice

procedures (“Notice by publication cannot simply

bear the normative weight expected of it. Chance

alone brings to the attention of even a local resident

an advertisement in small type inserted in the back

pages of a newspaper, and if he makes his home out-

side the area of the newspaper’s normal circulation

the odds that the information will never reach him are

large indeed”).

Early case law has held that a tax sale of unseated

land, as it is a tax against the land itself and not any

particular identified owner, carries with it all estates

within the unseated parcel that have not been sepa-

rately assessed. Hutchison v. Kline 199 Pa. 564

(1901); F.H. Rockwell & Co. v. Warren County, 228

Pa. 430 (1910). Thus, an unseated parcel of land that

was subject to a prior severance of the surface and

subsurface interests could be sold at a tax sale and the

buyer would take title to the parcel in fee, in spite of

the prior different ownership of the surface and sub-

surface. This transformation of prior split estate

ownership into a single fee ownership has been

termed by commentators as the unique Pennsylvania

“Title Wash.”

The practice of title washing was popularly employed

by large lumber companies in north-central Pennsyl-

vania beginning at the turn of the 20thcentury. Com-

panies such as the Central Pennsylvania Lumber

Company (CPL) held vast holdings of primarily un-

seated land in Elk, Potter, Sullivan and Lycoming

Counties, among others. It’s been estimated that

these companies controlled hundreds of thousands of

acres in Pennsylvania’s timber lands.

A review of tax sale records in any of the counties in

which CPL operated reveals that most of their hold-

ings were exposed to tax sales as a result of the non-

payment of taxes due thereon. Often, a related indi-

vidual (officer, attorney, etc.) would purchase the

lands at tax sale, hold the divestible title for the two-

year redemption period, and then convey whatever

interest was obtained as a result of the sale back to CPL

(or any other timber company employing the same tactic)

upon the expiration of the two-year redemption pe-

riod. As much of the lands owned by CPL and similar

companies were surface parcels subject to prior reserva-

tions of subsurface rights, the tax sales against the un-

seated parcels would arguably extinguish the rights of

those holding under prior reservations.

As the 20th Century progressed, owners (or their heirs) of

lost subsurface interests argued principally that the al-

leged tax sale was made under such attendant circum-

stances to render inequitable or actually fraudulent any

claim of divestiture of the subsurface interests. As case

history progressed, courts began to view subsurface inter-

ests as being something apart from the surface interests

and their attendant tax sales. In Day v. Johnson, 31 Pa.

D. & C.3d. 556 (1983), the Judge reasoned that an assess-

ment of unproduced oil and gas would be an act of

“clairvoyance” and held that the tax sale of unseated land

had no effect on the severed subsurface oil and gas inter-

est irrespective of its classification as unseated land.

Today, title washing is not possible due to changes in tax

sale statutes that prohibit owners from purchasing their

own property and the current advances in the due process

notice requirements needed for the divestiture of liens

and other interest holders brought into the tax-sale statu-

tory schemes as a result of recent United States Supreme

Court rulings. Presently, 72 P.S. §5860.609 pertaining to

UpsetTax Sales provides:

72 P.S. §5860.609. Nondivestiture of liens.

Every such sale shall convey title to the property under

and subject to the lien of every recorded obligation,

claim, lien, estate, mortgage…with which said property

may have or shall become charged or for which it may

become liable. [emphasis added]

A properly noticed Judicial Sale under 72 P.S.

§5860.610 could divest a severed mineral interest owner

if the owner received actual notice of the pending judicial

sale.

Should I have a survey done prior to

buying my new home?Attorneys always recommend having a “staked survey”

done prior to the closing of the purchase. It is not uncom-

mon that neighboring driveways, tree lines or gardens

encroach on the subject property, or outbuildings, wood

piles, doghouses have been located on the new buyers

property. In many situations relocating the misplaced

structure or a recorded easement can solve the issue prior

to closing.

My husband, who recently passed away,

and I owned our home as “tenants by the

entireties.” Do I need to have a new deed

prepared and recorded?

No. Property held as “tenants by the entireties” is a form

of ownership by husband and wife, whereby each owns

the entire property. In the event of death of one of the

tenants, the survivor owns the property by operation of

law without the necessity of probate.

I own oil and gas interests that have been

severed from the surface estate of land.

Can I leave those assets to my children

and grandchildren in my Will?

Yes. Those interests can be left in percentage assign-

ments as “in kind” distributions as a specific devise or in

the residuary clause of the Will. These oil and gas assets

are taxable for Inheritance tax purposes. Additionally, if

the interests are producing royalties, you will need to

contact the Lessee for an assignment, ratification and di-

vision agreement to receive the royalties.

According to the February residential real estate report from the West Penn Multi-List, Inc., the Southwestern Pennsylvania market strengthened for those selling their homes.

“It’s a spring for selling in our region. Compared to last year at this time, we now are seeing fewer homes listed for sale, coupled with a significant increase in the number of homes being sold, which is depleting our housing inventory faster than it’s being replen-ished,” said George Hackett , current president of the West Penn Multi-List, Inc. and president of Coldwell Banker Real Estate Services, Pittsburgh. “This is help-ing homes sell more quickly and for a higher average price than they did last year at this time.”

A comparison of February 2012 to February 2013 data for the 13-county region the West Penn Multi-List serves shows new listings decreased 6.96 percent (2,746 homes versus 2,555), and residential homes placed under agreement increased 18.23 percent (2,633 homes versus 3,113). For the same time period, average home sale price increased 6.08 percent ($140,861 to$149,424), and average days on market decreased 10.62 percent (113 versus 101 days).

“People are taking advantage of the continued low interest rates and entering the housing market,” Hack-ett said. “We hope to see more sellers following suit in the coming months. Working with a professional real estate sales associate can really help people price their homes to sell quickly in today’s market.”

These numbers represent the 13-county area serviced by the West Penn Multi-List, Inc., the definitive source for real estate information for its service area –Allegheny, Armstrong, Beaver, Butler, Washington, Westmoreland, Fayette, Greene, Clarion, Lawrence, Mercer, Somerset and Indiana Counties.

According to RealtyPIN (¨Philadelphia Real Estate Outlook for Spring 2013,¨ Feb. 8, 2013), Philadelphia

real estate professionals eagerly awaited spring of 2013. Here are the reasons why:

Sales prices are on the riseAccording to recently-released data, the median sales price for a home in the Philadelphia area during the fourth quarter of 2012 was $137,450. That’s a 16.1 percent increase from the same time period in 2011. Like other metropolitan areas, Philadelphia is starting to see consumer confidence in the housing market return, meaning more prospective buyers are now actively searching to purchase a home. The result? Steadily increasing home prices. The higher demand means sellers can charge more for their homes, essentially creating bidding wars between buyers, and that’s always good news for homeowners and their realtors!

Listing Prices are holding steadyOftentimes, a homeowner’s listing price and the actual sale price of the home can be very different. This is especially true in a market that is flooded with distressed properties due to foreclosure and short sales. Basically what happens is that the distressed properties end up selling for prices well below what the homes are actually worth, and in an effort to compete, “normal” sellers have to drop their prices, too. In the end, the value of every home on the market is affected because no one wants their home viewed as “overpriced” by prospective buyers. In Philadelphia, the average listing price last week was $213,135. That number has stayed relatively the same throughout the Winter, which is when home sales tend to drop off. The fact that we are seeing listing prices hold steady during the real estate market’s slow period means sellers are confident that they can get the price they are asking for when sales pick back up in the Spring – which is, typically, the busiest time of year for homebuyers.

Homes in all price ranges are sellingNo matter how much your home is worth, if it’s located in Philadelphia, someone may be interested in purchasing it! If you take a look at the five most popular

2013 Pennsylvania Housing Market

By housingpredictor.com

neighborhoods for home sales in the area, both Rittenhouse Square and Manayunk make the list. That’s significant when you compare the average listing price of homes in those two communities. Real estate statistics show that the average listing price in Rittenhouse Square was $1,068,422 last week, which is almost four times higher than the average listing price in Manayunk ($273,982). Because both of these neighborhoods are among the most popular with buyers, it proves that a well-maintained home in good condition will sell, regardless of its size and/or price.

More listingsMany homeowners are leery of listing their homes during the winter months because they know there are fewer buyers actively searching the market for a home during that time of year. When spring rolls around, many of those same homeowners decide to list their home, and experts expect even more inventory this year since sellers know that buyer confidence is on the rise.

Here are brief summaries of real estate market conditions in March, 2013, in several Pennsylvania cities, courtesy of Movoto:

- Lancaster’s home resale inventories increased, with a 50 percent increase since March 2013. Distressed properties such as foreclosures and short sales increased as a percentage of the total market in April. The median listing price in Lancaster went down from March to April. There were a total of 0 price increases and 4 price decreases.

- Philadelphia’s home resale inventories stayed the same, with a 0 percent change since March 2013. Distressed properties such as foreclosures and short sales remained the same as a percentage of the total market in April. The median listing price in Philadelphia went up from March to April. There were a total of 111 price increases and 1056 price decreases.

- West Chester’s home resale inventories increased, with a 8 percent increase since March 2013. Distressed properties such as foreclosures and short sales increased as a percentage of the total market in April. The median listing price in West Chester went down from March to April. There were a total of 16 price increases and 76 price decreases.

With the increasing awareness of

Marcellus Shale and natural gas

activity - often described as no less than

a “boom” - has come an increasing need

for information, and nowhere is this

more apparent than in the real estate

field.

Accordingly, Lawrence D. Brudy, Esq.,

President of Lawrence D. Brudy &

Associates, Inc., has been called on to

explain the complexities of buying,

selling and leasing real estate in what is

becoming the Natural Gas Age.

Mr. Brudy, who is also a licensed

Pennsylvania Real Estate Broker, has

lectured on Marcellus Shale drilling at

Realtor Continuing Education classes for

the Educational Development School of

Real Estate. He explained the use of the

disclosure and addendum used in con-

junction with the Pennsylvania Associa-

tion of Realtors Agreement of Sale, em-

phasizing the importance of using it on

every real estate transaction identifying

the estates in land to be “sold,”

“excepted,” and “reserved.”

Recognizing the need for understanding

in this relatively new field, the firm’s

attorneys and certified public

accountants are available to speak at

organizations, company or realtor

meetings on the development of oil, gas

and mineral interests, the determination

of subsurface ownership, the valuation

of oil and gas interests, buying and sell-

ing land, estate and tax planning

involving oil, gas and coal interests.

TITLE • DUE DILIGENCE • VALUATIONS • LITIGATION

855.935.1400

ENERGY PRACTICE

OIL & GAS / MINERAL VALUATIONS

• CERTIFIED TITLE OPINIONS •SUBSURFACE SALES / PURCHASES

• SEVERENCE DEEDS • LEASE AGREEMENTS •ADDENDUMS • RATIFICATIONS • ASSIGNMENTS

• LEASE AGREEMENTS • ADDENDUMS •TITLE ABSTRACTING AND CURATIVES

• RATIFICATIONS • ASSIGNMENTS •BUSINESS ENTITY PARTNERSHIPS

• LITIGATION • RIGHT OF WAYS •

www.ldbassoc.com

Often in title opinions the Firm’s attorneys find older oil

and gas leases that have expired by primary term, but

have no surrender or release of record. This is particu-

larly evident in the leases from the late 1800’s and early

1900’s. There are several reasons why a release or Sur-

render may never have been recorded with the Recorder

of Deeds in the county where the land is located; per-

haps the Lessee is deceased, or the operating company

went out of business. Whatever the reason, an unre-

leased oil and gas lease represents the looming possibil-

ity of an unknown well holding an older oil and gas

lease by production.

One of the ways to confront this potential problem is the

use of a resource providing a comprehensive and inte-

grated database of land, well mapping and production

information. With the use of a comprehensive well map-

ping tool, such as drillinginfo, our attorneys are able to

locate the site of any recorded well location in relation

to any parcel of land. We are then able to view the infor-

mation on record for a well that may affect a particular

parcel of land, including the Lessor name, well operator,

well American Petroleum Institute number and name,

permits, unitization declarations, depth of the well, and

production figures for oil and gas.

Cross referencing the information available from the

Department of Environmental Protection with the chain

of title, we have been able to enhance the quality of our

title opinions. With this resource, and the depth of in-

formation it provides, we are able to better determine

the current leasehold status of a parcel of land and also

provide a more definitive determination as to the unre-

leased oil and gas leases in a title opinion.

The Oil and Gas Lease Act: Inside the Controversy

On September 7th, Act 66 will officially become

effective; yet questions, controversy, and even out-

rage will remain. Exactly what is Act 66, how does

it affect my oil and gas lease, and why all the con-

troversy, are just a few of the questions being asked

by thousands of landowners.

Act 66, or “The Oil and Gas Lease Act” was in-

tended to create more transparency for landowners

regarding the royalties from oil and gas leases, and

the deductions that were being taken from the royal-

ties. Companies must now affix a check stub, or

financial record, to the royalty checks. The check

stubs will include financial information such as the

total barrels of crude oil or number of one-thousand

cubic feet (Mcf) of gas or volume of natural gas

liquids sold, the price the company received per

barrel, Mcf, or gallon, the net value of total sales

from the property less taxes and deductions, the

royalty owner’s interest, the owner’s share of the

total value of sales, etc.

The source of the controversy, however, comes

from Section 2.1 entitled “Apportionment,” which

reads: “Where an operator has the right to develop

multiple contiguous leases separately, the operator

may develop those leases jointly by horizontal drill-

ing unless expressly prohibited by a lease. In deter-

mining the royalty where multiple contiguous leases

are developed, in the absence of an agreement by

all affected royalty owners, the production shall be

allocated to each lease in such proportion as the

operator reasonably determines to be attributable

to each lease.”

Opponents to the Act raise as arguments that this lan-

guage creates a “forced pooling” statute, that it takes

away a landowner’s ability to renegotiate older leases,

and that the provision was not properly vetted. It is

important to distinguish the difference between

“pooling” and “forced pooling.” Besides the obvious

that forced pooling is done without one’s authoriza-

tion, forced pooling is including an owner’s property

without a lease into a well unit, and extracting oil and

gas that may lie underneath their property, for which

landowners would still receive a royalty. Forced pool-

ing must be approved by the state, and some states re-

quire an overwhelming majority of landowners in fa-

vor of drilling before such forced pooling can be au-

thorized. The reasoning behind forced pooling is that

the will of the vast majority to develop the oil and gas

they own should not be hindered by a small minority

of holdouts. Currently, Pennsylvania allows forced

pooling only for shallow wells, or a depth of about

3,800 feet below the surface. In 2009, an unsuccessful

attempt was made to allow forced pooling pertaining to

wells that penetrate the Marcellus Shale horizon. Gov-

ernor Tom Corbett has said publicly that he would not

sign any legislation that allowed forced pooling.

Pooling is condensing multiple leases into one well

unit. Most current oil and gas leases contain a unitiza-

tion clause, which expressly allows the Lessee to com-

bine the leased lands into much larger units. One of the

largest advantages to pooling is that companies are

able to drill fewer wells, which greatly reduces the en-

vironmental impact of the surface. Prior to the hydrau-

lic fracturing method of drilling, well units were much

smaller because wells were vertical, not horizontal. A

leased, and that the Lessee already has the right to drill

each land independently, “Where an operator has the

right to develop multiple contiguous leases sepa-

rately…” The owners have already entered into an oil

and gas lease, and the Lessee has the right to drill.

Pennsylvania State Senator Gene Yaw, who introduced

the bill said, “There is nothing that forces any land-

owner who doesn’t have a current lease to do so.”

Pooling also has environmental advantages. “All leases

must be held by the same company, and that company

could drill a separate well on each property under its

existing leases,” Yaw said. “The provision is pro-

environment in an attempt to have less wells, but the

same opportunities for those who have elected to

lease.” The controversy occurs because landowners

who missed out on the enormous bonus payments and

higher royalty interests by signing leases before the

Marcellus and Utica gas boom want to renegotiate the

lease.

Act 66 does not pertain to a lease that expressly pro-

hibits unitization or pooling, or establishes a maximum

unit size. Leases that contain such limitations would

need to be renegotiated before that property could be

pooled into a unit. The Act also does not apply to

leases that contain depth restrictions, where only rights

to drill shallow wells were leased. The lack of depth

restrictions is also a source of contention, because it

was not known that future drilling technology would

allow for drilling to such depths. As the leases simply

state “all the oil and gas underlying the parcel…” it is

presumed that what is leased is all quantities of oil/gas

from the surface of the earth to the center of the earth.

Opponents of the Act feel that a lack of a unitization or

pooling clause should allow the landowner to renegoti-

ate the terms of the lease, demanding a higher royalty

amount or bonus payment. Even though Act 66 may

thwart any attempts in renegotiation, the landowners

still stand to see a significant increases in royalty pay-

ments as a much larger volume of gas will be ex-

tracted.

typical well unit was 40 or 80 acres. Today, a well

unit can be well over 640 acres.

That is where the controversy begins. When older

leases were signed, both the landowners and the oil

and gas companies could not anticipate current

drilling technology and capability. Thus, as well

units were smaller, many leases were silent as to

pooling and unitization. Older leases are still rele-

vant today. This is because, generally, oil and gas

leases contain two terms of duration in which the

lease will remain in effect: The “primary term” and

the “secondary term.” The primary term is the

term that most people understand the lease to be:

one year, three years, five-years, etc. The secon-

dary term contains something to the effect of “and

so much longer as oil, gas, or either of them is pro-

duced in paying quantities.” Leases that have ex-

pired primary terms, but continue to produce are

leases that are “held by production.” This means

that an oil and gas lease signed in 1875, with a one

-year primary term, can still be in effect, given that

the well has been producing oil and/or gas. Fur-

thermore, the amount of production may be of little

consequence. A Washington County case recently

decided that even free gas supplied to the land-

owner was enough to satisfy the secondary term.

Another term that can be found in secondary terms

is the Storage Clause. The Storage Clause allows

the Lessee to store oil and gas on the property; as

long as oil and / or gas is stored on the premises,

the lease will remain in effect.

It is primarily the older leases that remain held by

production that are affected by Apportionment

Clause of Act 66. As noted earlier, most modern

leases contain unitization or pooling clauses in the

lease that allows the Lessee to merge lands into

larger well units. One of the most highlighted

points made by proponents of Act 66 is that the

Act only applies to lands that have already been

Oil and Gas Lease Negotiations generally begin with the

landowner being contacted by a “landman” – an agent

representing a gas exploration/development company, and

presenting a lease. There are multiple paragraphs and

clauses embodied within the lease. This article’s focus will

be limited to the forms and types of payments to the

landowner. The Landowner is referred to as the “Lessor”

and is the party who owns the oil, gas and mineral inter-

ests. The exploration/development company is referred to

as the “Lessee,” the party that is leasing the interests and

responsible for the development of the land. Development

includes but is not limited to exploring, drilling, extracting,

conducting seismic tests and installing production equip-

ment such as compressing, gathering, treating, dehydrating

and separating stations.

The standard boiler plate lease agreements typically

contain provisions for Lessor payments all of which are

negotiable.

Paid-Up Lease Bonuses – Negotiated by the landman and

landowner or their Attorney, bonus payments vary from

county to county and depend upon the shale thickness of

the area, well production, and competition for the oil, gas

and mineral interests. Lease bonus payments are a dollar

amount per acre multiplied by the number of years for the

lease. For example, a five-year “paid up” lease at

$100.00 / acre / year for 100 acres would calculate as fol-

lows: $100.00 / acre x five-year term x 100 acres =

$50,000.00 paid-up bonus payment.

Delay Rental Payments – Payments made on an annual

basis calculated on dollar amount / acre x the number of

acres. For example, leasing of 100 acres at $100.00 / acre

for a five-year term. $100.00 x 100 acres x 1 year =

$10,000.00 annual payment. Unlike the Paid-Up Lease

Bonus, if a well is drilled or the lands are unitized and the

property owner begins receiving royalty payments before

the expiration of the lease primary term (i.e. five-years)

no other delay rental payments are required as the royalty

compensation will maintain the lease most often referred

to as being “held by production” (HBP).

Royalty Percentage Payments – These are the monthly

or quarterly payments to the landowner based upon well

production and unitization. Variables such as price /

thousand cubic feet of gas, unit size, well production and

royalty percentage with / without costs impact the pay-

ment. For example, using the following sample numbers

annual royalty payments would be as follows: Royalty

interest 15% without costs, $4.00 / thousand cubic feet of

gas, 100 acres of landowner property, 640-acre unit size,

2.5 million cubic feet of gas produced / day = annual

royalty payment of $85,546.88. Depending upon how the

royalty percentage has been negotiated is determinative

along with the other aforementioned variables of the an-

nual payments.

Paid-Up Lease Bonus, Delay Rental Payments and

Royalties may be treated differently for federal income

tax purposes, and questions should be referred to a tax

professional for answers.

Oil & Gas Interests & Lease Negotiations

The Pennsylvanian Department of Agriculture

reports that currently, over 9.3 million acres statewide are

enrolled in the Clean and Green Program [Pennsylvania

Farmland and Forest Land Assessment Act of 1974: Act

319]. The Clean and Green Program is a land conservation

program that gives preferential assessment values to

landowners who qualify for the program. In short, the

program is a tool that serves as an incentive to landowners

to preserve agricultural and forest land. In order to qualify,

generally a landowner must own 10 acres of land that are

used for either Agricultural Use, Agricultural Reserve, or

Forest Reserve. If a landowner uses their land for

agricultural use, but owns less than ten acres, he/she may

still qualify for the program if the landowner can show that

the land can produce at lease $2,000 annually in farm in-

come.

In 2010, The Clean and Green Act was amended to

allow for Clean and Green landowners to engage in oil and

gas exploration while maintaining their lands eligible for the

program and being subjected to limited roll-back tax

penalties. Typically, when a portion of Clean and Green

properties cease to be utilized for purposes other than the

program qualifying requirements, a split-off occurs and

the portion of the split-off ceases to receive the preferen-

tial assessment value and is assessed by its fair market

value, and that portion is subject to a roll-back tax. The roll

-back tax is the difference between the taxes paid based on

the Clean and Green assessment and the taxes that would

have been paid or payable had that land not been valued,

assessed and taxed under the program.

The Amended version of the Clean and Green Act

of 1974 provides that Clean and Green land may be used for

the exploration and removal of gas and oil, including the

extraction of coal bed methane. The portion of the lands

that are subject to roll-back taxes are those developed for

the exploration and removal of gas and oil, including the

development of appurtenant facilities, such as new roads,

bridges, pipelines, and other buildings or structures, and of

course, the well site itself. The restored well site and land

that are no longer capable of being immediately used for

the Clean and Green qualifying purposes will be subject to

the roll-back tax. The measurement of the restored well

site and land is taken from the well site restoration report

approved by the PA Department of Environmental

Protection.

The landowner is responsible for the roll-back tax

due upon the filing of the approved well site restoration

report with the county assessor. However, the landowner

is not responsible for the payment of the roll-back tax if the

oil and gas activities are conducted by other parties who

hold the oil and gas rights, as long as the transfer of the

rights occurred before the land was enrolled in the Clean

and Green program and before the Amendment took effect

in December, 2010. It is important to mention that oil and

gas exploration and drilling companies that lease Clean and

Green properties have no obligation in paying the roll-back

taxes unless specifically designated in the oil and gas lease.

Jonathan D. Hall, Esq. is a licensed attorney in Penn-

sylvania, where he was admitted in 2011 to the Pennsyl-

vania Bar Association. He earned his Bachelor’s degree

from Edinboro University of Pennsylvania with a double

concentration in Comprehensive Business Management

and Financial Services. He earned his Juris Doctor from

Duquesne University School of Law in Pittsburgh, where

he was awarded the CALI Award for Academic Excel-

lence in PA Civil Procedure. He is a member of the En-

ergy Practice Group, where his focus is on oil and gas,

coal, and subsurface evaluation. He is an active member

of the American Association of Professional Landmen

(AAPL).

References: PENNSYLVANIA FARMLAND AND FOREST LAND ASSESSMENT ACT OF 1974: ACT 319; PENNSYLVANIA FARMLAND AND FOREST LAND ASSESSMENT ACT - RESPONSIBILITIES OF COUNTY ASSESSORS, SPLIT-OFF, SEPARATION OR TRANSFER AND ROLL-BACK TAXES AND SPECIAL CIRCUMSTANCES; Act of Oct. 27, 2010, P.L. 866, No. 88 Session of 2010 No. 2010-88; PENNSYLVANIA DEPARTMENT OF ENERGY

about the AUTHOR

How Oil and Gas Production Affects

“Clean and Green” Properties

According to the Department of Agriculture,

Pennsylvania is made up of more than 7.8 million acres

of farmland. For many farmers who

experience financial setbacks or

devastating natural disasters, there are

appealing alternatives to commercial

credit lenders – Farm Loan Programs.

In 2010, the Farm Service Agency

(“FSA”) administered over $131.9 mil-

lion in loans for Pennsylvania farmers.

Farm Ownership Loans, designed to assist farm

purchasers, and sometimes Farm Operations Loans, are

secured by an interest in the land itself. For most

landowners this consideration has never registered as an

impediment to financing. Enter the Natural Gas Age.

Pennsylvania farmers and ranchers are warming up to the

idea of natural gas extraction, which has been, for many,

a real boost for putting money back into the farm for long

overdue improvements.

Farmers, with existing FSA loans, should take a

close look at their security instrument before signing any

oil and gas lease. The FSA security instruments contain

language that requires borrowers to obtain prior consent

from the Agency before entering into any transactions

that may affect the real estate security. (7 CFR 765.351).

In fact, the FSA regulates that for the “sale” of oil, gas,

coal or other minerals, the borrower must receive written

consent prior to engaging in such transactions (7. CFR

765.351(b)). Arguably, this includes the leasing of oil

and gas interests to a third party. What’s more, an even

closer inspection of the loan document (executed on or

after December 23, 1985) could reveal that the FSA

actually has a security interest in the oil, gas, coal or

other minerals if their valuation was included in the

appraisal. For loans executed before December 23, 1985

the FSA has a per se security interest in the oil and gas

underlying the farm.

With this in mind, a potential impediment exists for

the farmer who is in negotiations with a gas company.

There are some alternatives available, He can negotiate

with the gas company for a payoff of the loan so that both

parties can proceed free and clear of the looming

“acceleration” clause in the loan document. The

borrower/farmer can submit to the

local FSA office a FSA-2060

application requesting a partial release

of the security interest (i.e. oil and

gas) and/or consent to enter into the

lease. The former alternative requires

a degree of finesse at the bargaining

table so as to ensure a fair but

profitable lease. The latter alternative

has some long standing implications. First, the

application requires you to calculate and disclose the

“anticipated proceeds” of the transaction. Next, it

requires applicant to identify what the proceeds will be

used for.

The first foreseeable problem is that calculating

projected earnings from royalty streams is a complex

task. Guesswork is not recommended nor will it serve

the applicant in the long run. Another problem an

applicant may have is trying to honestly disclose what the

proceeds will be used for. Obviously, perpetuating the

success of farm operations is number one on the list.

However, does the applicant have to disclose the

arguably superfluous purchases – grandson’s new truck,

the trip to Florida, or the new kitchen counter? What

level of detail is required? These are all important

questions for the applicant/borrow/potential Lessor.

What’s even more compelling is the notation on the very

bottom of the application which discretely discloses that

the information you put in the application “may be fur-

nished” to almost every federal, state or local agency you

can think of, including the Internal Revenue Service and

private individuals/entities. It does include the proviso

that information requested is “voluntary.” However,

failure to disclose could result in a rejection or delay.

The complexities of leasing encumbered farmland do

not outweigh the benefits. The most important step you

can take in protecting your assets and ensuring you are in

compliance with your pre-existing contractual

arrangements is to consult with professionals and get

educated.

Pennsylvania Supreme Court Rules in Butler v. Charles Powers Estate to Affirm Dunham Rule

On April 24, 2013, the Pennsylvania Supreme

Court issued an Opinion wherein it reversed

the Superior Court in the case of Butler v.

Powers Estate.

At issue was a deed dated back to 1881 which

conveyed 244 acres situated in Susquehanna

County. The deed reserved one-half of the oil

and mineral rights underlying the property to

the heirs of Charles Powers. The 244 acres are

currently owned by John and Josephine Butler,

who in 2010, filed an action to quiet title

claiming that they owned the oil and gas under

the property. The trial court, relying on the

“Dunham Rule,” agreed with the Butlers. The

Dunham Rule came into being in 1882 when

the Pennsylvania Supreme Court held that a

reservation of “minerals” without the explicit

mention of oil and gas created a rebuttable

presumption that the grantor did not intend to

convey oil and gas.

The heirs of the Powers Estate appealed to the

Supreme Court arguing that the Dunham Rule

was not applicable because Marcellus Shale

gas is an unconventional gas unlike other natu-

ral gas which is a conventional gas. The

appellants also argued that a previous case held

that if gas was present in coal, it belonged to

the owner of the coal. By the same logic, gas

found in Marcellus Shale should belong to the

owner of the shale, accordingly to appellants.

The Supreme Court agreed and reversed the

trial court.

However, the Supreme Court found that

neither the appellees nor the Superior Court

provided any justification for limiting or

overruling the Dunham Rule, and in the con-

text of a private deed conveyance the term

“minerals” does not include oil and gas. The

Supreme Court further held that the term

“natural gas” was not contained anywhere in the

plain language of the deed reservation.

Therefore, the burden was on appellees under

the Dunham Rule to present clear and

convincing evidence that it was the intent of the

parties when executing the deed in 1881 to also

include the natural gas. The Supreme Court

reiterated that the rule in Pennsylvania is that

natural gas and oil simply are not minerals

because they are not of metallic nature, as the

common person would understand minerals.

The Supreme Court also distinguished the Butler

case from the case which stated that natural gas

found in coal belongs to the owner of the coal,

U.S. Steel Corp. v. Hoge, 468 A.2d 1380 (Pa.

1983), stating, “We therefore find no merit in

any contention that because Marcellus Shale

natural gas is contained within shale rock,

regardless of whether shale rock is or is not a

mineral, such consequentially renders the natural

gas therein a mineral.

Accordingly, the Pennsylvania Supreme Court

reaffirmed the rule that natural gas is not

included in a deed reservation or grant without

either: (1) natural gas being explicitly contem-

plated within the reservation or grant; or (2)

clear and convincing parol evidence that the

parties intended for natural gas to be included

within the deed reservation or grant, despite only

a general reservation or grant of minerals.

Because neither existed, the court held that the

trial court correctly concluded that Marcellus

shale gas was not included in the deed

reservation.

A Deed is a written instrument which conveys

(transfers) ownership in all or a portion of an interest in

real property. The conveyed property can be described

by metes and bounds, landmarks, lot or parcel numbers,

or residual acreage less outsales. The person or entity

transferring the property is the “grantor” and the person

or entity receiving the property is the “grantee”. Deeds

are executed, witnessed, and notarized and recorded in

the deed records of the county where the property is

located. Pennsylvania is a “race-notice” jurisdiction

meaning if there are multiple purchasers who are not

aware of the others’ purchase, the first to record their

interest will have a valid purchase. In Pennsylvania, the

grantee does not need to sign a deed for the instrument

to be recorded. The most common types of deeds used

in real estate transactions are identified as General, Spe-

cial, Quit Claim, and Fiduciary.

• General Warranty Deeds convey the grantor’s

interest and warrants (guarantees) the interest

conveyed against any acts, omissions, or defects by

the grantor or any predecessor in the chain of title as

to the quality of title. A general warranty deed

provides a grantee with the most protection against

title defects and/or claims. Grantors can provide a

“general warranty” regardless of the warranty

previously conveyed.

• Special Warranty Deeds convey the grantor’s

interest and “warrants” (guarantees) the interest

conveyed against any acts, omissions, or defects by

the grantor for the period of time grantor has owned

the property but NOT for predecessors in the chain

of title. A special warranty can be conveyed

regardless of the warranty previously conveyed.

• Quit Claim Deeds carry or provide no warranty as

to the quality of the chain of title. Quit claim deeds

are often used to convey or relinquish whatever

interest the grantor possessed in the property. A quit

claim deed can be used to add or remove a spouse's

name to title as a result of a marriage or divorce.

• Fiduciary Deeds provide when an estate or trust is

conveying property. When a person dies, whether

testate (with a will) or intestate (without a will), and

an estate is opened to provide the appointment of an

executor or executrix, that person takes the

fiduciary oath to gather and protect the Estate’s as-

sets. This fiduciary can also be the trustee of a

“living,” “Inter vivos,” “revocable” or irrevocable

trust. Living, inter vivos, or revocable trusts become

irrevocable upon the death of the settler. A fiduciary

deed provides to the grantee that the property has

not been encumbered by the Estate. A grantee of a

Fiduciary Deed can convey any type of future

warranty deed.

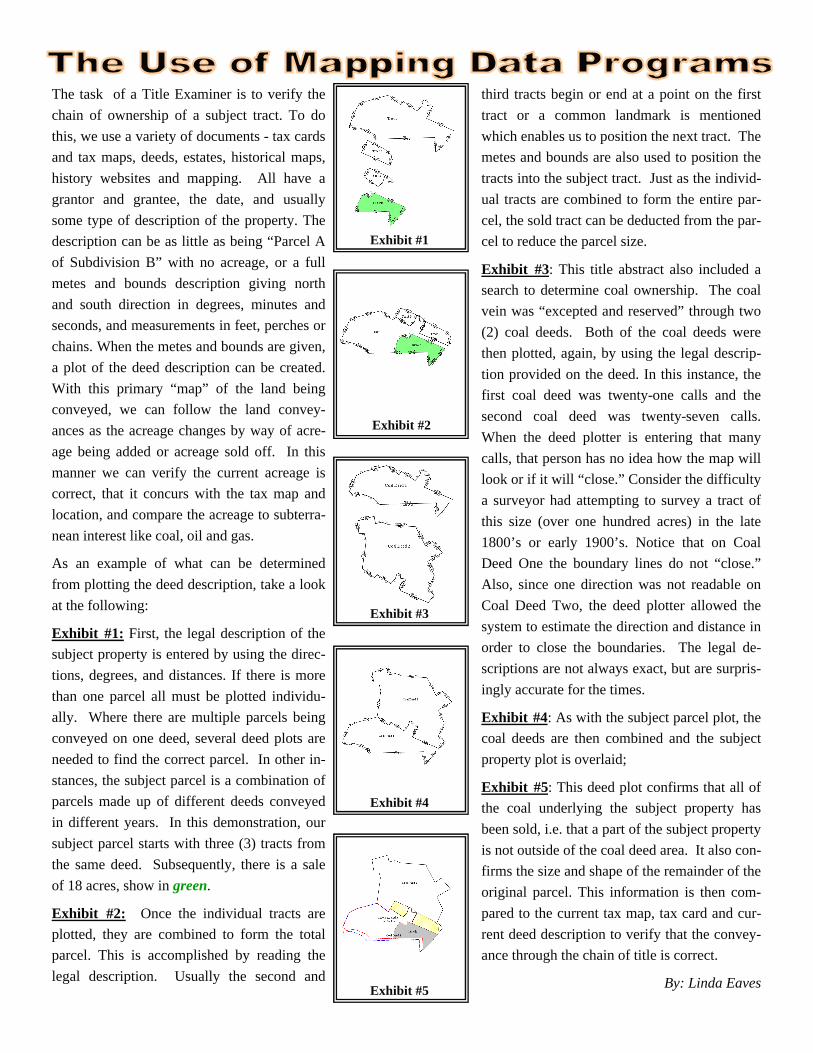

The task of a Title Examiner is to verify the

chain of ownership of a subject tract. To do

this, we use a variety of documents - tax cards

and tax maps, deeds, estates, historical maps,

history websites and mapping. All have a

grantor and grantee, the date, and usually

some type of description of the property. The

description can be as little as being “Parcel A

of Subdivision B” with no acreage, or a full

metes and bounds description giving north

and south direction in degrees, minutes and

seconds, and measurements in feet, perches or

chains. When the metes and bounds are given,

a plot of the deed description can be created.

With this primary “map” of the land being

conveyed, we can follow the land convey-

ances as the acreage changes by way of acre-

age being added or acreage sold off. In this

manner we can verify the current acreage is

correct, that it concurs with the tax map and

location, and compare the acreage to subterra-

nean interest like coal, oil and gas.

As an example of what can be determined

from plotting the deed description, take a look

at the following:

Exhibit #1: First, the legal description of the

subject property is entered by using the direc-

tions, degrees, and distances. If there is more

than one parcel all must be plotted individu-

ally. Where there are multiple parcels being

conveyed on one deed, several deed plots are

needed to find the correct parcel. In other in-

stances, the subject parcel is a combination of

parcels made up of different deeds conveyed

in different years. In this demonstration, our

subject parcel starts with three (3) tracts from

the same deed. Subsequently, there is a sale

of 18 acres, show in green.

Exhibit #2: Once the individual tracts are

plotted, they are combined to form the total

parcel. This is accomplished by reading the

legal description. Usually the second and

third tracts begin or end at a point on the first

tract or a common landmark is mentioned

which enables us to position the next tract. The

metes and bounds are also used to position the

tracts into the subject tract. Just as the individ-

ual tracts are combined to form the entire par-

cel, the sold tract can be deducted from the par-

cel to reduce the parcel size.

Exhibit #3: This title abstract also included a

search to determine coal ownership. The coal

vein was “excepted and reserved” through two

(2) coal deeds. Both of the coal deeds were

then plotted, again, by using the legal descrip-

tion provided on the deed. In this instance, the

first coal deed was twenty-one calls and the

second coal deed was twenty-seven calls.

When the deed plotter is entering that many

calls, that person has no idea how the map will

look or if it will “close.” Consider the difficulty

a surveyor had attempting to survey a tract of

this size (over one hundred acres) in the late

1800’s or early 1900’s. Notice that on Coal

Deed One the boundary lines do not “close.”

Also, since one direction was not readable on

Coal Deed Two, the deed plotter allowed the

system to estimate the direction and distance in

order to close the boundaries. The legal de-

scriptions are not always exact, but are surpris-

ingly accurate for the times.

Exhibit #4: As with the subject parcel plot, the

coal deeds are then combined and the subject

property plot is overlaid;

Exhibit #5: This deed plot confirms that all of

the coal underlying the subject property has

been sold, i.e. that a part of the subject property

is not outside of the coal deed area. It also con-

firms the size and shape of the remainder of the

original parcel. This information is then com-

pared to the current tax map, tax card and cur-

rent deed description to verify that the convey-

ance through the chain of title is correct.

By: Linda Eaves

Exhibit #1

Exhibit #2

Exhibit #3

Exhibit #4

Exhibit #5

LAWRENCE D. BRUDY & ASSOCIATES, INC. was a Bronze Sponsor of the NAPE East Expo Charity

Luncheon which Benefits the Wounded Warriors Project

Note: Former Pittsburgh Steelers running back and four-time

Super Bowl Champion, Rocky Bleier, was the keynote speaker at

the inaugural NAPE East Charities Industry Luncheon. Since 2007,

NAPE Charities has donated more than $2.5 million dollars to

benefit veterans.

1. According to trulia.com, Florida is known to have the most bathrooms per

bedroom, averaging 1.28.

2. Throughout history a red door has symbolized many things - in the early days

of America, it meant the home was a safe place for travelers to stop for the

night and in feng shui a red door invites positive energy into a home.

3. Pittsburg, Pittsburgh or Pittsbourgh? The town was named in 1758 by

Scotsman John Forbes, who was honoring William Pitt the Elder. Forbes sent

a letter to Pitt the same year to let him know that the city had been named for

him, and in the letter he spelled it "Pittsbourgh." Most experts agree that as a

Scotsman, Forbes probably pronounced it the same way we pronounce Edin-

burgh. It wasn't until 1769 that the "Pittsburgh" spelling first turned up on a

surveying document, but the real controversy came with the 1891 United

States Board on Geographic Names ruling that all towns with the spelling

"burgh" needed to drop the "h." Many people were outraged at the decision

and refused to follow the rules, even the Pittsburgh Gazette, the University of

Pittsburgh and the Pittsburgh Stock Exchange. In 1911, the Geographic Board

gave in and officially restored the "h" that was never really missing for most

people anyway.

LAWRENCE D. BRUDY & ASSOCIATES, INC.ATTORNEYS AT LAW

ENERGY • REAL ESTATE • TITLE • LITIGATION

(855) 935-1400

Your ENERGY Firm in the Natural Gas Age

What can these six words mean for you?

CONFIDENCE • EXPERIENCE • RELIABILITY

ACCURACY • KNOWLEDGE • INTEGRITY

For the answer, and more, visit us at:

www.ldbassoc.com/6words