Embed Size (px)

Citation preview

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 1/70

1

CHAPTER 1-

INTRODUCTION

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 2/70

2

1. INDUSTRY PROFILE

1.1 INTRODUCTION TO BANKING

In the modern age, Banking constitutes the fundamental basis of economic growth and life blood

of any business. The term Bank is being used since long time but there is no clear conception

regarding its beginning. Origin of the word Bank belongs to the word Banchi or to the Greek

word Banque. Both these words refer to some kind of banking. In simple words Bank refers to an

institution that deals with money. This institution accepts money from the people and gives loan

to those who are in need. But now there are not only dealing with money but also performing

various other functions.

According to Indian Banking Companies Act 1949, “Banking company is one which transacts

the business of Banking which means the accepting for the purpose of lending or investment of

deposits of money from the public repayable on demand or otherwise and withdraw able by

cheque, draft or otherwise.”

With stiff competition and advancement of technology, the services provided by bank have

become more easy and convenient. Earlier people had to wait for hours before they could

withdraw cash from their accounts. Similarly, cheque clearance used to take months from north

to south of country. Nowadays banking deals with the latest discoveries in the banking

instruments along with the polished version of their old systems.

The Indian Banking has finally worked up to the competitive dynamics of the “new” Indian

market and is addressing the relevant issues to take on the multifarious challenges of

globalization. Banks that employ IT solutions are perceived to be „futuristic‟ and proactive

players capable of meeting the multifarious requirements of the large customer base. The

unleashing of products and services through the internet has galvanized players at all levels of

the banking and financial institutions. It has compelled to look anew at reorienting their

strategies using the internet as a medium. The internet has emerged as new and challenging

frontier of marketing with the conventional ways being just as applicable like in any other

marketing medium the Indian banking has come a long way from being a sleepy business to a

highly proactive and dynamic entity.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 3/70

3

This transformation has been largely brought about by the large dose liberalization and economic

reforms that allowed banks to explore new business opportunities rather than generating

revenues from conventional streams (i.e. borrowing and lending)

1.1.1 Banking in India

The Reserve Bank of India acts as a centralized body, monitoring any discrepancies and

shortcoming in the system. It is the foremost monitoring body in the Indian Financial Sector. For

the past three decades India‟s banking system has several outstanding achievements to its credit.

The most striking is its extensive reach. It is no longer confined to only metropolitans or

cosmopolitans in India. In fact, Indian Banking system has reached even to the remote corners of

the country. This is one of the main reasons of India‟s growth process. The liberal government

policies for Indian banks since 1969 have paid rich dividends . Not long ago, an account holder

had to wait for hours at the bank counters for getting a draft or for withdrawing his own money.

Gone are the days when the most efficient bank transformed money from one branch to the other

in two days. Now it is as simple as instant messaging. The first bank in India, though

conservative, was established in 1786. From 1786 till today, the journey of Indian banking

System can be segregated into three distinct phases.

The Phases were:

Phase I:-

During the first phase the growth was very slow and banks also experienced periodic failures

between 1913 and 1948. There were approximately 1100 banks, mostly small . To streamline the

functioning and activities of commercial banks , the Government of India came up with the

Banking Companies Act, 1949 which was later changed to Banking Regulation Act 1949 as per

amending Act of 1965(Act no. 23 of 1965). Reserve Bank of India was vested with extensive

powers for the supervision of the banking in India as the Central Banking Authority. During

those days confidence in banks was low. As an aftermath deposit mobilization was slow. Abreast

of its savings bank facility provided by the Postal department was comparatively safer.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 4/70

4

PhaseII:

Government took major steps in this Indian Banking Sector Reform after independence. In 1955,

it nationalized Imperial Bank of India with extensive banking facilities on a large scale especially

in rural and semi-urban areas. It formed State Bank of India to act as the principal agent of RBI

and to handle banking transactions of the Union and State Governments all over the country.

Seven banks forming subsidiary of State Bank of India was nationalized in 1960 on 19 th

July,1969, major process of nationalization was carried out. It was the effort of the then Prime

Minister of India, Mrs. Indira Gandhi. 14 major commercial banks in the country were

nationalized. Second phase of nationalization of Indian Banking Sector Reform was carried out

in 1980 with seven more banks. This step brought 80% of the banking segment in India under

Government ownership. The following are the steps taken by the Government of India to

Regulate Banking Institutions in the Country:

1949: Enactment of Banking Regulation Act.

1955: Nationalization of State Bank of India.

1959: Nationalization of SBI subsidiaries.

1961: Insurance cover extended to deposists.

1969: Nationalization of 14 major banks.

1971: Creation of credit guarantee corporation.

1975: Creation of regional banks.

1980: Nationalization of seven banks with deposits over 200 crore.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 5/70

5

Banking in the sunshine of the Government ownership gave the public implicit faith and

immense confidence about the sustainability of these institutions.

Phase III:-

The liberalize policy of Government of India permitted entry to private sector in the banking

industry as a result of a new industrial policy of 1991 in which emphasis was laid on

privatization, globalization, and liberalization. The major differentiating parameter that

distinguishes private banks from all the nationalized banks in the Indian banking is the level of

service that is offered to the customer. The private sector banks have generally been established

by promoters of repute or by „high value‟ domestic financial institutions. The popularity of these

banks can be gauged by the fact that in a short span of time, these banks have gained

considerable customer confidence and consequently have shown impressive growth rates. With

efficiency being the major focus, these banks have leveraged on their strengths and competencies

along with management and operational efficiency. Private banks have also superior product

positioning and higher employee productivity skills. The private bank with their focused

business and service portfolio have a reputation of being niche players in the industry.

This phase has introduced many more products and facilities in the banking sector in its reforms

measure. In 1991, under the chairmanship of M Narasimha, a committee was set up by his name

which worked for the liberalization of banking practices. The country is now flooded with

foreign banks and their ATM stations. Efforts are being put to give a satisfactory service to

customers. Phone banking and net banking is introduced. The entire system became more

convenient and swift. Time is now given more importance. The financial system of India has

shown a great deal of resilience. It is sheltered from any crisis triggered by any external

macroeconomics shock as other East Asian Countries suffered this is all due to a flexible

exchange rate regime, the foreign reserves are high, the capital account is not yet fully

convertible, and banks and their customers have limited foreign exchange exposure.

1.1.2 Banking structure in India

In India the banks are being segregated in different groups. Each group has their own benefits

and limitations in operating in India. Each has their own dedicated target market.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 6/70

6

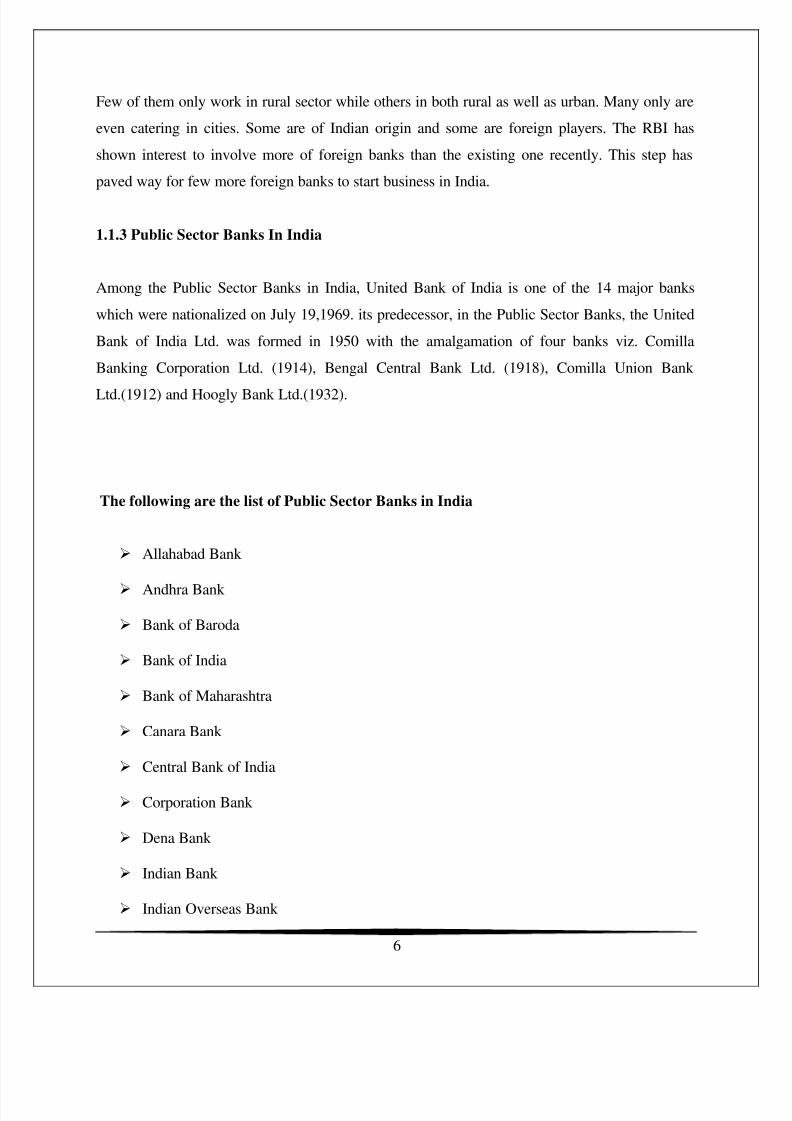

Few of them only work in rural sector while others in both rural as well as urban. Many only are

even catering in cities. Some are of Indian origin and some are foreign players. The RBI has

shown interest to involve more of foreign banks than the existing one recently. This step has

paved way for few more foreign banks to start business in India.

1.1.3 Public Sector Banks In India

Among the Public Sector Banks in India, United Bank of India is one of the 14 major banks

which were nationalized on July 19,1969. its predecessor, in the Public Sector Banks, the United

Bank of India Ltd. was formed in 1950 with the amalgamation of four banks viz. Comilla

Banking Corporation Ltd. (1914), Bengal Central Bank Ltd. (1918), Comilla Union Bank

Ltd.(1912) and Hoogly Bank Ltd.(1932).

The following are the list of Public Sector Banks in India

Allahabad Bank

Andhra Bank

Bank of Baroda

Bank of India

Bank of Maharashtra

Canara Bank

Central Bank of India

Corporation Bank

Dena Bank

Indian Bank

Indian Overseas Bank

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 7/70

7

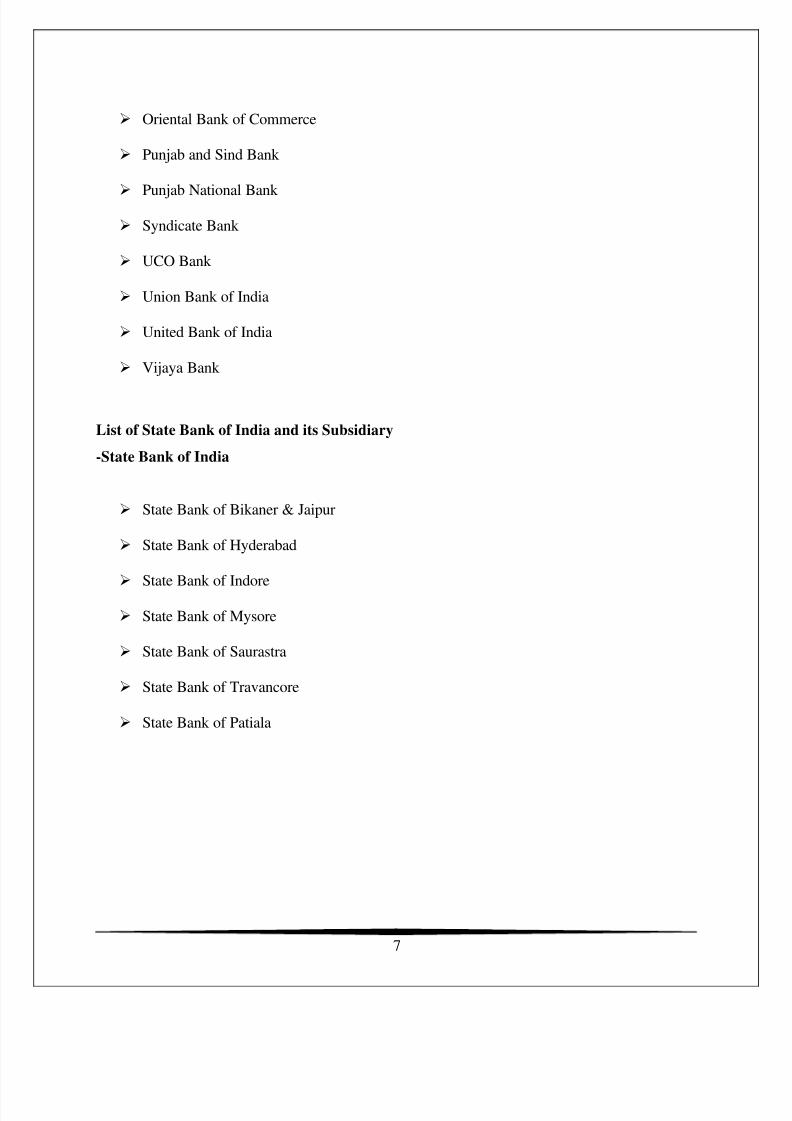

Oriental Bank of Commerce

Punjab and Sind Bank

Punjab National Bank

Syndicate Bank

UCO Bank

Union Bank of India

United Bank of India

Vijaya Bank

List of State Bank of India and its Subsidiary

-State Bank of India

State Bank of Bikaner & Jaipur

State Bank of Hyderabad

State Bank of Indore

State Bank of Mysore

State Bank of Saurastra

State Bank of Travancore

State Bank of Patiala

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 8/70

8

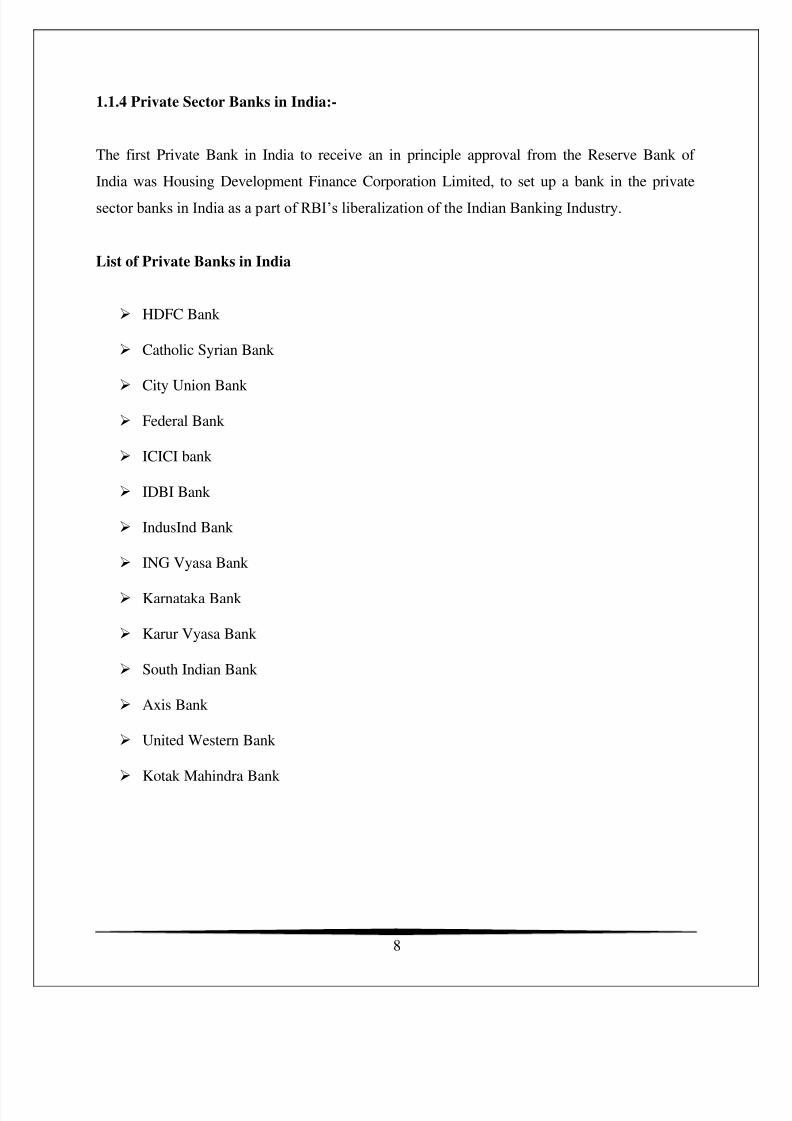

1.1.4 Private Sector Banks in India:-

The first Private Bank in India to receive an in principle approval from the Reserve Bank of

India was Housing Development Finance Corporation Limited, to set up a bank in the private

sector banks in India as a part of RBI‟s liberalization of the Indian Banking Industry.

List of Private Banks in India

HDFC Bank

Catholic Syrian Bank

City Union Bank

Federal Bank

ICICI bank

IDBI Bank

IndusInd Bank

ING Vyasa Bank

Karnataka Bank

Karur Vyasa Bank

South Indian Bank

Axis Bank

United Western Bank

Kotak Mahindra Bank

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 9/70

9

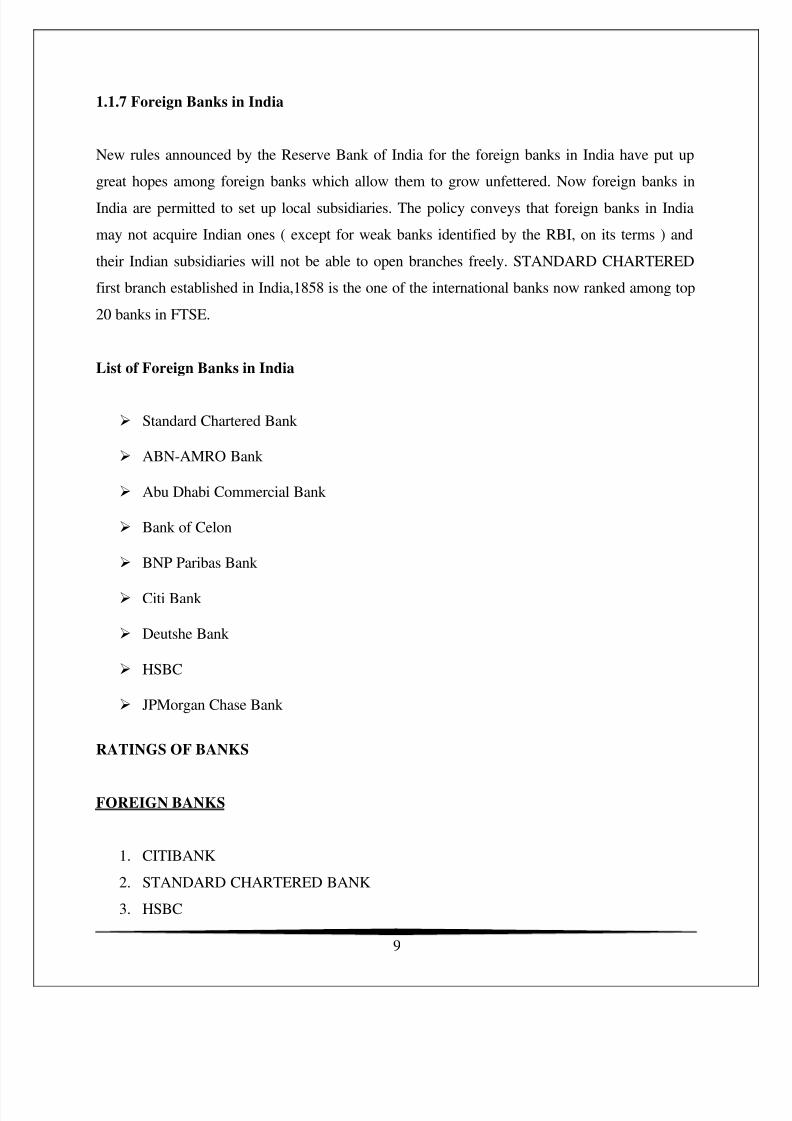

1.1.7 Foreign Banks in India

New rules announced by the Reserve Bank of India for the foreign banks in India have put up

great hopes among foreign banks which allow them to grow unfettered. Now foreign banks in

India are permitted to set up local subsidiaries. The policy conveys that foreign banks in India

may not acquire Indian ones ( except for weak banks identified by the RBI, on its terms ) and

their Indian subsidiaries will not be able to open branches freely. STANDARD CHARTERED

first branch established in India,1858 is the one of the international banks now ranked among top

20 banks in FTSE.

List of Foreign Banks in India

Standard Chartered Bank

ABN-AMRO Bank

Abu Dhabi Commercial Bank

Bank of Celon

BNP Paribas Bank

Citi Bank

Deutshe Bank

HSBC

JPMorgan Chase Bank

RATINGS OF BANKS

FOREIGN BANKS

1. CITIBANK

2. STANDARD CHARTERED BANK

3. HSBC

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 10/70

10

4. ABN-AMRO BANK

5. AMERICAN EXPRESS

6. DEUTSCHE BANK

PRIVATE BANKS

1. ICICI BANK

2. HDFC BANK

3. AXIS BANK

4. KOTAK MAHINDRA BANK

1.2 Customer Satisfaction in Retail Banking

Customer satisfaction is an abstract concept and the actual manifestation of the state of

satisfaction will vary from person to person and product/service to product/service. The

state of satisfaction depends on a number of both psychological and physical variables which

correlate with satisfaction behaviors such as return and recommend rate. The level of

satisfaction can also vary depending on other factors the customer, such as other products

against which the customer can compare the organization's products.

In a competitive marketplace where businesses compete for customers, customer

satisfaction is seen as a key differentiator and increasingly has become a key element of

business strategy.

However, the importance of customer satisfaction diminishes when a firm has

increased bargaining power. For example, cell phone plan providers, such

as AT&T and Verizon, participate in an industry that is an oligopoly, where only a few

suppliers of a certain product or service exist. As such, many cell phone plan contracts

have a lot of fine print with provisions that they would never get away if there were, say,

a hundred cell phone plan providers, because customer satisfaction would be way too

low, and customers would easily have the option of leaving for a better contract offer.

There is a substantial body of empirical literature that establishes the benefits of customer

satisfaction for firms.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 11/70

11

Savings & Banking Services- At Standard Chartered we offer a wide choice of savings

accounts with competitive interest rates and the option to save in local or foreign

currencies.

Savings accounts-You also have the added convenience of our international network,

giving you easy access to your money when you're abroad.Here are just a few of the

savings accounts you can open with us.

MyDreamAccount-Save for your children's future with a special account that's easier for

parents to manage.

PayrollAccount-A one-stop banking solution for companies and their employees that

improves the way salary payments are managed. The account offers bank-wide range of

benefits to employees and salary process convenience to the employer.

Women'Account-Choose a bank account designed specifically to meet the financial

needs of women.

Saver-Manage your money anytime, anywhere - and watch your savings grow faster with

our most competitive interest rate.

Marathon Survey account-Enjoy an interest rate that is as attractive as that of time

deposits while enjoying the transaction convenience to your account and withdraw

flexibility to your money at anytime.

Foreign Currency Account-Start saving your money in multiple foreign currencies! It's

easy with Standard Chartered Bank and it comes with a high interest rate as well.

Banking services-From demand drafts and foreign exchange services to safe deposit

boxes and telegraphic transfers, Standard Chartered's banking services are designed to

make managing your finances easier, wherever you are in the world.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 12/70

12

“To help you manage your wealth and plan for the future, we offer a comprehensive range

of advisory services.”

Investment Advisory Services

From financial reviews and health checks to evaluating your risk profile and customising an asset

allocation plan that suits your individual objectives.

Retail FX products

If you're looking to capitalise on opportunities in the currency markets, Standard Chartered can

offer you a number of easy and flexible ways to invest in foreign currencies.

These include:

FX Margin Trading

Currency Trading

Premium Currency Deposits

Principal Protected Currency Deposits

Mutual Funds

Our fund families offer a broad range of mutual funds designed to match your risk tolerance andmanagement style.

Our Funds include highly diversified portfolios that:

Actively allocate across a full range of major asset classes and geographic markets.

Offer absolute returns, with potentially higher yields than a typical liquidity portfolio, while

managing short-term risk. Provide consistent return and capital appreciation, regardless of

market direction, but with greater emphasis on returns superior to those offered by traditional

cash offerings.

Loans & Mortgages

Our personal loans and award-winning mortgages are helping people realise their aspirations in

countries across the world.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 13/70

13

1. Personal loans

Whether you're planning a vacation, redecorating your home or supporting your child through

college, a personal loan from Standard Chartered will give you the extra funds you need. You

can even use it as a standby line of credit for unforeseen expenses.

Depending on your specific credit needs, you can take out an Installment Loan or a Revolving

Loan without any guarantee or collateral. Whichever option you choose, we'll help you stay in

control of your finances and make the most of life's opportunities and experiences.

2.

Mortgages

Are you about to buy your first home or move to a new place? Maybe you're investing in

property or looking to switch to a better deal. Wherever you are on the property ladder, we can

help you choose the right mortgage for you.

By combining award-winning mortgages with local and international experience, Standard

Chartered is in a strong position to help homebuyers and property investors across the world. In

fact, we've won awards as a leading Mortgage Bank in most of the countries in which we dobusiness.

Credit Cards

Designed to give greater flexibility and round-the-clock convenience, Standard Chartered credit

cards are accepted at outlets across the world.

Promotional statement by Standard Charterd Bank

“Whether you're looking for extended repayment terms, special cardholder privileges or an

attractive rewards programme, we have the ideal credit card to suit you and your lifestyle.”

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 14/70

14

Insurance

The insurance agency market serves more than six million people, giving an opportunity for

banks to sell insurance products from their banking halls in a hybrid called bankassurance.

Standard Chartered Insurance solutions include:

Life Insurance

Savings and Retirement Planning Insurance

Health and Medical Insurance

Home Insurance

Motor Insurance

1.2.1 RETAIL BANKING IN INDIA

Retail banking refers to provision of banking services to individuals and small business where

the financial institutions are dealing with large number of low value transactions. This is in

contrast to wholesale banking where the customers are large, often multinational companies,

governments and government enterprise, and the financial institution deal in small numbers of

high value transactions.

The concept is not new to banks but is now viewed as an important and attractive market

segment that offers opportunities for growth and profits. Retail banking and retail lending are

often used as synonyms but in fact, the later is just the part of retail banking. In retail banking all

the needs of individual customers are taken care of in a well-integrated manner.

Today‟s retail banking sector is characterized by three basic characteristics:

· Multiple products (deposits, credit cards, insurance, investments and securities);

· Multiple channels of distribution (call center, branch, internet) and

· Multiple customer groups (consumer, small business, and corporate).

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 15/70

15

1.2.3 NATURE OF RETAIL BANKING

Retail banking has been described as “hotter than vindaloo”. Considering the fact that vindaloo,

the Indian-English innovative curry in umpteen numbers of restaurants of London, is very hot

and spicy, it seems that retail banking is perceived to be the in-thing in today‟s world of banking.

It is however broad in nature.

1.2.4 BANKS CHANGING TO RETAIL BANKING

Banks are awash with liquidity. Prime corporates do not borrow from banks except at sub-PLR

rates. Banks do not favor other corporates. Suddenly there is a great change in attitude of banks.

The name of the game is no longer „Lending to big corporates, huge amoun ts to create loan

assets‟. Banks invest their resources in government paper to the hilt and then scout for hitherto

neglected retail borrowers for lending. Retail credit is now welcomed even from RBI‟s

perspective. There are no longer any regulatory hurdles. Consumer credit is no longer considered

as unproductive, as it triggers demand for consumer products, which in turn help manufacturers

in a period of economic slowdown. Retail to project credit stands to a ratio of 3: 1. While the

rates of interest on consumer credit have still fallen, there is a scope for further reduction.

Perhaps, competition will further bring down the interest rates.

Fixed interest rates on housing loan have sharply fallen, but not the floating rates, which are

linked to medium and long-term PLRs. Banks, refuse to reduce these rates, which appears rather

unfair. But then the consumers still needs innovative products like graduated payment mortgages

etc., in place of standalone EMI structures.

SME sector borrowers still appear to be suffering from inadequate and delayed credit delivery

this sector has immense potential for growth and banks have to devise innovative strategies to

fund their ventures on the principle of entrepreneurship and bankabilty rather than mere

collateral securities.

Micro finance, another area of retail credit, has unfortunately become a so-called priority sector

credit. Perhaps it will be a great idea if it is delinked from the obnoxious priority tag and thereby

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 16/70

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 17/70

17

Second, changing consumer demographics indicate vast potential for growth in consumption

both qualitatively and quantitatively. India is one of the countries having highest proportion

(70%) of the population below 35 years of age (young population). The BRIC report of the

Goldman-Sachs, which predicted a bright future for Brazil, Russia, India and China, mentioned

Indian demographic advantage as an important positive factor for India.

Third, technological factors played a major role. Convenience banking in the form of debit

cards, internet and phone-banking, anywhere and anytime banking has attracted many new

customers into the banking field. Technological innovations relating to increasing use of credit /

debit cards, ATMs, direct debits and phone banking has contributed to the growth of retail

banking in India.

Fourth, the Treasury income of the banks, which had strengthened the bottom lines of banks

for the past few years, has been on the decline during the last two years. In such a scenario, retail

business provides a good vehicle of profit maximisation. Considering the fact that retail‟s share

in impaired assets is far lower than the overall bank loans and advances, retail loans have put

comparatively less provisioning burden on banks apart from diversifying their income streams.

Fifth, decline in interest rates have also contributed to the growth of retail credit by generating

demand for such credit.

1.2.6 ROLE OF CUSTOMER RELATIONSHIP MANAGEMENT IN RETAIL BANKING

Retail banks are facing greater challenges than ever before in executing their customer

management strategies. Intensifying competition, proliferating customer contact channels,

escalating attacks on customer information, rising customer expectations and capitalizing on new

market opportunities are at the top of every bank executive‟s agenda.

In looking for ways to drive growth, banks need to evaluate their customer management strategy.

Do they currently have a CRM solution that is capable of delivering:

• Consistent and cost-effective customer service?

• Customer -aligned products and services?

• Enhanced customer loyalty and long-term value?

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 18/70

18

2.6 A)CRM IN RETAIL BANKING: CURRENT TRENDS AND DYNAMICS

Today, more than ever before, the ability to maximize customer loyalty through close and

durable relationships is critical to retail banks‟ ability to grow their businesses. As banks strive to

create and manage customer relationships, several emerging trends affect the approach and tools

banks employ to achieve sustainable growth. These trends reflect a fundamental change in the

way banks interact with the customers they have - and those they want to acquire.

1) Trend: Focusing on organic growth

How can a retail bank drive growth? Traditionally, banks have grown through an aggressive

strategy of acquiring direct competitors and taking over their branch networks. Today, thatstrategy is no longer sufficient, since it doesn‟t create organic growth for the financial institution.

To build stronger customer loyalty, banks need improved customer knowledge to develop

products and deliver services targeted at specific market segments; resulting in more directed

marketing, sales and service tactics. This is not to say M&As will not continue to be an effective

way to expand product offerings and service capabilities. However, retail banks will focus on

acquiring businesses that have essential products or capabilities to complete the bank‟s portfolio

of offerings. The goal? To gain greater wallet share of current customers and support their

organic growth. A recent example of this is the acquisition of Providian by Washington Mutual

that expanded its credit card offering for both banking and mortgage customers.

2) Trend: seeking out and better serving emerging customer segments

One of the ways banks can achieve improved organic growth is by focusing on new markets.

Emerging demographic segments represent untapped revenue streams that can fuel a bank‟s

growth. In the U.S., the Hispanic market represents a major opportunity. This fast-growing and

underserved customer segment offers new potential revenue for retail banks. The need every

bank has is how to respond quickly and at low cost. And this need is increasing all the time.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 19/70

19

3) Trend: creating deep business insight into customer Preferences

Customer loyalty that drives organic growth can only be built through a consistent customer

experience. This means understanding each individual customer‟s needs and preferences. One of

the largest challenges banks faceis how to better understand their customers and provide

personalized customer service.

A “one-size-fits-all” customer strategy no longer works. Banks need to serve the rapidly

diverging needs of all markets: aging baby-boomers, time-stressed mid-lifers and younger

technophiles (i.e., Gen-X and Gen-Y). Banks must move out of their “comfort zone” and develop

services and products that address the specific needs of different market segments.

It is clear that financial service providers can no longer sustain growth and profitability targets

through mass direct mail campaigns that deliver less than 1 percent response rates. Those that do

will lose out to competitors implementing personalized communications that target the right

customer, at the right time, with the right product or service. To optimize customer relationships

and loyalty, banks need to integrate processes and technologies that enable them to build – and

then act upon – a detailed view of what each customer wants. This will require highly skilled

customer service professionals, with the right combination of linguistic, culturally aligned and

financial services skills, as well as the ability to deploy customer service strategies quickly,

efficiently and cost-effectively.

4) Trend: Responding to intensifying competition through revitalized offerings

The need to revitalize a company‟s portfolio of offerings happens in every industry. Examples in

high-tech manufacturing, consumer industries and transportation show how important new

offerings are in order to stay competitive as products and services become more

“commoditized.” The

same is true in the financial services industry. Today‟s retail banks face a relentless stream of

new competitors, eager to take a share of the market‟s revenues.

Three major competitors offering differentiated products, services or distribution models have

emerged over the past decade: Brokerage and insurance firms, expand ing their offering •

portfolios into banking products beyond their traditional product sets.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 20/70

20

Nontraditional players such as PayPal (expanding through technology-led channels of services)

or telecommunications companies (expanding by bundling of payments for “like” services) are

growing by becoming payment aggregators. Nonbanking companies looking to (if not already)

enter • the market by offering banking products and services. The entry of nontraditional players

will not only affect bank growth rates as they compete for consumers, but will also place

downward pressure on operating margins and profitability created through their nonbanking

business models.

Renewing and reinvigorating product offerings and customer service strategies are essential

ways to stay competitive in a changing marketplace. Proactive banks will respond to market

opportunities and competitive threats by launching new products, entering new markets and

acquiring new customer segments. A proactive CRM solution is the foundation that can help

support this without disrupting current services that would put existing clients at risk.

5. Trend: Improving distribution and channel Management

How are retail banks responding to intensified market competition? To take themselves to the

next level of improved sales and service, banks are focusing on developing, implementing and

integrating their channels more rapidly and efficiently. Their goal is to meet three objectives:

Improved and more consistent service based on a full customer view

Increased revenue through adoption of new products

Improved profitability through lower product development and service costs

Forward-looking banks will simultaneously improve customer service quality and profitability

by deploying an integrated CRM strategy. Deepening relationships with their customers means

that banks must offer their products and services through appropriate delivery channels that

appeal to their customers. Deploying multiple channels and integrating them at the enterprise

level give banks a consistent and full view of the customer. To be successful, this must include

all service channels – both physical and virtual – including, call center, Web, branch, kiosk,

ATM, phone and mobile devices.

To achieve this, banks need to develop technology, operational processes and customer strategies

to make their channels more effective in reaching and serving their customers. By tailoring

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 21/70

21

products or services to specific customers or market segments, banks will be able to increase

their product adoption rate, revenues and return on investment (ROI) for new

Product development.

6. Trend: safeguarding customer information

Adding to this complexity, customer privacy and information security are under attack as never

before. The threats come from many quarters – including increasingly sophisticated identity

thieves, constant phishing expeditions by criminals seeking to trap unwary customers, and even

“inside jobs” where staff sell customer data to criminals. Expanding legislative and industry

requirements for customer security are also increasing costs for financial services companies.

Compliance with customer information

regulations is becoming increasingly complex as regulations are growing at all operating levels:

At the global level – The Payment Card Industry • (PCI) Act requires a single set of information

security standards and requirements

for all payment organizations.

At the national level – The Gramm-Leach-Bliley Act not • only requires that financial

institutions ensure the security and confidentiality of customer records and information but also

requires companies to protect against anticipated threats and unauthorized access, which could

result in substantial harm or inconvenience to a customer.

At the state level – The California Information Practice • Act requires businesses in California

to disclose any security breach that occurs to any California resident whose unencrypted personal

information was, or is reasonably believed to have been, acquired by an unauthorized person.

Against this ever-expanding background, it is vital that banks ensure their customer data is

secure from both internal and external threats. The following are three key reasons why this is so

important:

If a bank loses a customer‟s information, it invariably loses the customer as well.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 22/70

22

A security breach has an immense negative impact on the value of the bank‟s brand and

reputation, hindering the bank‟s ability to acquire new customers.

Under Basel II, banks without required client data security as a part of their risk

management program must maintain higher levels of capital reserves – reducing the

amount of funds available to invest in the marketplace and generate revenue.

By preventing security breaches and avoiding losses, banks can actually realize a ROI from

investing in security. This makes protecting customer data a prerequisite for competing

effectively in the retail financial services market. Banks must balance the cost of security against

the need to share information and service the customer, while at the same time finding ways to

secure vital customer and financial data for the purposes of risk management planning.

1.2.7 BENEFITS

1.Reaping the benefits of a CRM solution

Faced with these numerous and varied trends, retail banks are reshaping the way they must

interact with their customers. A fully integrated, enterprise wide CRM platform ensures bankshave the core capabilities to take full advantage of their customer relationships and capitalize on

these market dynamics, rather than losing out because of them.

2.Gaining Sales Momentum

In today‟s increasingly competitive environment, where maximizing organic growth is a bank‟s

priority, sales momentum is essential. To build this momentum, banks need to focus

simultaneously on:

Increasing acquisition rates of new and emerging customer segments, such as the

Hispanic population in the U.S.

Improving retention of existing customers and saving “at risk” customers

Increasing profitability of customer relationships, either at the top-line through increased

sales, or at the bottom-line through more cost-effective service

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 23/70

23

Improving integrated channel distribution strategies to get the right product, to the right

client, at the moment the customer has the need

Maximizing the value and return from CRM investments that have already been made

3.Increasing Acquisition Of New Customers

A CRM solution should help a bank target customers based on the “value” they bring to the

bank, now and throughout the life of the customer (and beyond through “next generation”

marketing). Banks need to ensure that their value propositions have traction with the right market

segments. This will enable the bank to identify, target and capture new customers. Clearly,

customer insight and strategy are the core differentiators for the bank. CRM solutions (people,

applications, systems and processes) must support these strategies to get the right products and

services to the right customers.

4.Improving Retention Of Existing Customers

Customer retention can be achieved by enhancing customer satisfaction and loyalty, improving

problem resolution, and creating the ability to identify and save “at-risk” customers. In fact, an

“at-risk” customer actually represents a major opportunity for additional revenue – if handled

correctly.

However, the greatest danger for banks is either not identifying “at risk” customers or not havingthe capabilities to do anything to recover them.

For example, a customer makes a large withdrawal from his or her account. This may signal that

the customer is switching funds to another bank. Or the customer may be buying a house, a boat,

or paying college tuition, in which

case there are clear opportunities to sell additional products or investments. The identification

and treatment of this customer should reflect his or her lifetime value. CRM-driven techniques

will help retain customers and can migrate mere “account holders” into loyal, long -term,

profitable customers.

5.Increasing The Profitability Of Customer Relationships

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 24/70

24

Boosting revenues requires improving the product pipeline and close rates, while reducing sales

and service costs. On the revenue side, the bank‟s CRM solution should use customer

intelligence to target specific offers and manage marketing campaigns for a high likelihood of

acceptance. Customer treatment strategies should be fully integrated with a CRM platform and

the processes to support them. On the cost side, better channel management, CRM automation

and integration will help increase the efficiency and effectiveness of sales and service.

6.Improving Distribution And Channel Management

To win profitable customers and build long-term relationships with them, banks need to have the

right insight, products and services for the right customer at the lowest possible cost. From call

centers to Web sites, every one of a bank‟s multiple channels must be scalable, flexible, low-cost

and

fully integrated with all the other channels. This is the only way to consolidate customer

information and provide consistent treatment across the enterprise. Each of the bank‟s channels

must also be able to accommodate change and adapt to future trends in the marketplace.

7.Maximizing The Value Of Past CRM Investments

As new technologies and channels emerge, the need to control costs and maximize the ROI from

existing CRM investments raises many questions:

How can a bank lower its operational cost structure while leveraging the newest

technologies – such as interactive voice recognition-based routing – to improve service

quality and customer experience?

How can it manage its customer service/call center workforce more efficiently and

effectively – in an era when a major call center has to handle tens of million of calls a

year from a vastly diverse spectrum of customers?

How can the bank‟s investment in customer care be refocused to create a permanently

lower and more flexible cost base – perhaps through use of a common platform,

technologies and processes?

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 25/70

25

1.3 ABOUT STANDARD CHARTERED: A Brief History of Standard

Chartered

Standard Chartered is the world's leading emerging markets bank being headquartered in

London. Its businesses however, have always been overwhelmingly international. Standard

Chartered Bank Limited (Standard Chartered) is the 52nd largest bank in the world. It is

registered in the United Kingdom, but conducts most of its business overseas. It was formed in

1969 as Standard and Chartered Banking group to effect the merger of two British overseas

banks, The Chartered Bank and The Standard

Royal Charter incorporated the Chartered Bank in 1853 to provide banking facilities in India,

Australia and China. During the second half of the nineteenth century branches were opened in

many centers in India and the Far East. After 1945 the bank grew rapidly

The Chartered Bank opened its first overseas branch in India, at Kolkata, on 12 April 1858 .

Eight years later the Kolkata agent described the Bank's credit locally as splendid and its

business as flourishing, particularly the substantial turnover in rice bills with the leading Arab

firms. When The Chartered Bank first established itself in India, Kolkata was the most

important commercial city, and was the center of the jute and indigo trades. With the growth of

the cotton trade and the opening of the Suez Canal in 1869, Bombay took over from Kolkata as

India's main trade center. Today the Bank's branches and sub-branches in India are directed and

administered from Mumbai (Bombay) with Kolkata remaining an important trading and banking

center.

The early years

Standard Chartered is named after two banks, which merged in 1969. They were originally

known as the Standard Bank of British South Africa and the Chartered Bank of India, Australia

and China. Of the two banks, the Chartered Bank is the older having been founded in 1853

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 26/70

26

following the grant of a Royal Charter from Queen Victoria. The moving force behind the

Chartered Bank was a Scot, James Wilson.

James Wilson went on to start The Economist, still one of the world's pre-eminent publications.

Nine years later, in 1862, the Standard Bank was founded by a group of businessmen led by

another Scot, John Paterson, who had emigrated to the Cape Province in South Africa and had

become a successful merchant. Both banks were keen to capitalize on the huge expansion of

trade between Europe, Asia and Africa and to reap the handsome profits to be made from

financing that trade. The Chartered Bank opened its first branches in 1858 in Calcutta and

Mumbai. A branch opened in Shanghai that summer beginning Standard Chartered unbroken

presence in China. The following year the Chartered Bank opened a branch in Hong Kong and

an agency was opened in Singapore.

The Standard Bank opened for business in Port Elizabeth, South Africa, in 1863. It pursued a

policy of expansion and soon amalgamated with several other banks including the Commercial

Bank of Port Elizabeth, the Colesberg Bank, the British Kaffarian Bank and the Fauresmith

Bank. The Standard Bank was prominent in the financing and development of the diamond fields

of Kimberly in 1867 and later extended its network further north to the new town of

Johannesburg when gold was discovered there in 1885.

In Asia the Chartered Bank expanded opening offices in, Myanmar in 1862, what is now

Pakistan and Indonesia in 1863, the Philippines in 1872, Malaysia in 1875, Japan in 1880 and

Thailand in 1894 industries. During 1904 a branch opened in Vietnam. Both the Chartered and

the Standard Bank opened offices in New York and Hamburg in the early 1900s. The Chartered

Bank gaining the first branch license to be issued to a foreign bank in New York

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 27/70

27

The impact of war:

Even the First World War offered opportunities for expansion when the Standard Bank set up a

branch in Tanzania shortly after British troops occupied the formerly German administered Dar

es Salaam in September 1916. Both banks survived the inter-war years.

but the world trade slump led to the closure of operations in the Canary Islands, Liberia, the

Netherlands, and Equatorial Guinea. Disaster struck the Chartered Bank's office in Yokohama,

Japan, when an earthquake in 1923

The post war years

After the Second World War many countries in Asia and Africa gained their independence. This

led to local incorporation in some countries, particularly in Africa.

In 1948 the Chartered Bank opened in Bangladesh and during 1957 it acquired the Eastern Bank.

The Eastern Bank gave the Chartered Bank a network of branches including Aden, Bahrain,

Beirut, Cyprus, Lebanon, Qatar and the United Arab Emirates. The Chartered Bank also entered

into a joint venture to form the Iran-British Bank, which opened for business in 1959. The bank

grew rapidly and had 24 branches when it was nationalized in 1981. By the mid 1950s the

Standard Bank had around 600 offices in Southern, Central and Eastern Africa. Its network grew

substantially in 1965 when it merged with the former Bank of British West Africa, which had

some 60 branches in Nigeria, 40 branches in Ghana and eleven branches in Sierra Leone in

addition to operations in Cameroon and Gambia.

Both viewed the future with some trepidation as the need to protect themselves from acquisition

became ever more apparent. In 1969 the decision was made by the Standard Bank and the

Chartered Bank to undergo a friendly merger thus forming Standard Chartered PLC.

Standard Chartered subsequently acquired the UK based Hodge Group, in which it already had a

minority shareholding, and the Wallace Brothers Group. The Hodge Group brought to Standard

Chartered an extensive network of UK offices specializing in installment credit and industrial

leasing, and after a period of rationalization its name was changed to Chartered Trust Limited.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 28/70

28

Standard Chartered decided, after the merger, to expand the Group outside its traditional

markets. In Europe a number of offices were opened including Austria, Belgium, Denmark,

Ireland, Spain and Sweden as well as several major cities in the UK. Standard Chartered also

opened offices in Argentina, Canada, Colombia, the Falkland Islands, Panama and Nepal. In the

USA three banks were acquired. These included the Union Bank of California, which gave

Standard Chartered a presence in Brazil and Venezuela.

Standard Chartered reviewed its operations and decided to focus on its core strengths of

Consumer Banking, Corporate & Institutional banking and Treasury in its well-established

operations in Asia, Africa and the Middle East. This led to a series of divestments notably in

Europe, the United States and Africa. During this time staff numbers were reduced; businesses

not considered core were sold or closed; associate holdings disposed of; unprofitable branches

closed and back office functions consolidated. In addition expensive buildings were sold with the

proceeds reinvested in the business, and the senior management team was radically changed and

strengthened.

Standard Chartered in the 1990s

Even within this period of apparent retrenchment Standard Chartered expanded its network, re-

opening in Vietnam in 1990, Cambodia and Iran in 1992, Tanzania in 1993 and Myanmar in

1995. With the opening of branches in Macao and Taiwan in 1983 and 1985 plus a representative

office in Laos (1996), Standard Chartered now has an office in every country in the Asia Pacific

Region with the exception of North Korea. Standard Chartered now offers full banking services

in Colombia, Peru and Venezuela. In 1999, Standard Chartered acquired the global trade finance

business of Union Bank of Switzerland. This acquisition makes Standard Chartered one of the

leading clearers of dollar payments in the USA.

Today Standard Chartered is the world's leading emerging markets bank employing 30,000

people in over 500 offices in more than 50 countries primarily in countries in the Asia Pacific

Region, South Asia, the Middle East, Africa and the Americas.

The new millennium has brought with it two of the largest acquisitions in the history of the bank

with the purchase of Grindlays Bank from the ANZ Group and the acquisition of the Chase

Consumer banking operations in Hong Kong in 2000.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 29/70

29

These acquisitions demonstrate Standard Chartered firm committed to the emerging markets,

where they have a strong and established presence and where they see future growth.

Standard Chartered has maintained a long local presence, since 1858, with particular emphasis

on relationship banking. Significant networks have been established with vendors and financial-

related organizations to enable them offer their customers a comprehensive range of flexible

financial services, with special focus on transactional banking products.

Supported by state-of-the-art operations, Standard Chartered is pro-active in improving every

part of services. Electronic Delivery system has been put in place to ensure that transactions are

handled speedily. They have Cash Product Specialists and dedicated Customer Service Centers

to provide customers with effective solutions.

Standard Chartered in India deals in:

Personal Banking: It includes issuance of debit cards, credit cards. Loans that may be in

form of car loans, home loans, loans against the car, unsecured loans, loans against

property. Insurance includes both general insurance and life insurance in which it has tie

up with Bajaj Allianz. In Investments from traditional Fixed Deposits to Mutual Funds,

RBI Bonds and also more contemporary and sophisticated products like Principalprotected products, Funds of Funds, Derivatives and Offshore investment products; the

Bank offers an the entire range of investment options available to Indian investors.

Services: Include Net Banking, ATM network, phone banking, Electronic clearing

system

Commercial Banking

Online Treasury

Internet Banking

SME‟s

Corporate Responsibility:

Corporate Responsibility is seen as an opportunity to make the brand stand out. It is about

making sure that, in pursuing business goals; it helps in identifying and addressing

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 30/70

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 31/70

31

Standard Chartered believes it is important to work with suppliers that take their responsibilities

towards the environment and community. Social and environmental considerations form an

integral part in evaluating and selecting suppliers.

1.3.1 DIFFERENT PRODUCT AND SERVICES OF STANDARD CHARTERED BANK

IN RETAIL BANKING

Wide range of retail banking products and services are offered by the banks, which cover both

Depository and Advances to suit various segments of customer like salaried persons,

businessmen, traders, professionals, pensioners etc.

1. INTERNAL BANKING includes the following:-

A. PERSONAL BANKING

Saving accounts

Current accounts

Demat accounts

Corporate salary account

Term deposits

B. EXCEL BANKING

The customer who quaterly average balance of 5 lac are given the excel banking services which

include some unique features than yhe other customer i.e

wealth management solutions

exclusive privileges

personal relationship manager

priority banking

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 32/70

32

investment and financial planning

C. CREDIT BANKING

Personal loans

Housing loans

Vehicle or automobile loans

Loan for consumer goods

Credit and debit cards – global and International

Loan for holidays

Education loans

Gold loans

Event loans

Overdraft

D . INVESTMENTS

INSURANCES (tie up with bajaj allianz)

Mutual funds

Different investment structures

Forex exchange

E. NRI ACCOUNTS

The present menu of bank accounts for Non-Resident Indians (NRIs) has three categories:

1. Non-Resident (External) Rupee Accounts (NRE)

2. Non-Resident (Ordinary) Rupee Accounts (NRO)

3. Foreign Currency Non-Resident (Banks) Accounts FCNR (B)

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 33/70

33

Banks are coming out with more features to add value to retail banking products and services.

These are called VALUE ADDED PRODUCTS AND SERVICES. These include the following:

-

· Free collection of specified number of outstation instruments per month.

· Instant credit of outstation cheque.

· Concession in commission, exchange for issuance of pay orders and demand drafts.

· Issuance of free chequebooks.

· Issuance of free ATM cards.

· Interest rate options (fixed or floating)

· Waiver of credit card issuance fees.

· Free issuance of Add On cards to the members of the cardholders.

· Accident insurance cover.

· Arranging for insurance cover on the lockers in the bank.

· Reducing the fees charged on locker facilities.

· Free execution of standing instructions of customers.

· Free investment advisory services.

· Legal services for documentation

· Services to senior citizens

Other services include: -

· Payment of utility bills like electricity bills, telephone bills and water bills etc. on due date.

· Payment of monthly or quarterly education fee for children.

· Payment of insurance premium on or before due dates.

· Demating of shares, debentures and bonds.

· Making payments at doorsteps.

2. EXTERNAL BANKING includes following:-

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 34/70

34

A. Phone or Mobile banking

B. Net banking

C. Atm services

D. Sms service

E. NEFT(national electronic fund transfer)

F. RTGS(real time gross settlement)

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 35/70

35

CHAPTER 2

LITERATURE REVIEW

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 36/70

36

Ha.H & John. J (2010) “Role of customer orientation in an integrative model of brand

loyalty in services” The Service Industries Journal Jul 2010. Vol. 30, Iss. 7; pg. 1025

This study attempts to model the development of brand loyalty by examining the simultaneous

effects of customer orientation, perceived quality, brand associations, and satisfaction on brand

loyalty. Data are used from retail banking and discount store retailing services to examine thedirect and indirect effects of customer perceptions of customer orientation and quality on brand

loyalty. It was found that customer orientation has a direct effect on brand loyalty and indirect

effects through customer satisfaction, perceived quality, and brand associations as mediators.Further, perceived quality has a direct effect on brand loyalty as well as an indirect effect with

satisfaction as a mediator. The results suggest that effective management of brand loyalty would

require tracking of customer perceptions of a firm's customer orientation, quality and brand, inaddition to measuring customer satisfaction.

Anon (2010) “BankAtlantic Ranks Highest in Customer Satisfaction in Florida” Business

Wire Headquartered in Westlake Village, Calif., J.D. Power and Associates is a global marketing

information services company operating in key business sectors including market research,

forecasting, performance improvement, training and customer satisfaction.

Anon(2010) “Customer Satisfaction with Online Banking Slips, But Still Significantly Beats

Offline Banking” Michigan Banker Vol. 22, Iss. 6; pg. 20, 2 pgs

According to the 2010 Online Financial Services Study from ForeSee Results andForbes.com, customer satisfaction with online banking fell two points in 2010, from 83 in 2009

to 81 (on a 100 point scale). While a statistically significant drop, that number remains high (80is considered the threshold for excellence) and, in fact, is far superior to offline banking and mostother online industries. The five largest banks in the country (Bank of America, Citibank, Chase,

PNC, and Wells Fargo) scored the lowest in the study, on average, while credit unions tend to

have the highest online customer satisfaction scores. However, with all bank categories scoringhigher than 80, online banking (81) is clearly providing superior satisfaction to

offline banking (75).

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 37/70

37

Anon (2010) “Independent Bank Receives Top Ranking in Customer Satisfaction” Michigan

Banker Jun 2010. Vol. 22, Iss. 6; pg. 61, 2 pgsIn a recent J.D. Power and Associates 2010 Retail Banking Satisfaction Study, Independent Bank

was one of two banks that received a perfect "five" Power Circle Rating for customer service.

Anon (2010) “StanChart offers 'Cash Back' for credit cardholders” The Financial Express

Dhaka: Aug 25, 2010.

During Ramadan, Standard Chartered Bank has introduced a 3.0 per cent Cash Back offer for itscredit cardholders, said a press release.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 38/70

38

CHAPTER 3

RESEARCH

METHODOLOGY

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 39/70

39

Objectives of the study

This initiative was taken by Standard Chartered Bank, Ludhiana which is in the Retail Banking

Business. This bank offers retails banking solutions to customers and has unique products

This project deals with the customer satisfaction in retail banking of Standard Chartered Bank

Ltd.

The main objectives of the study are:

Study the customer know how about the services provided by Foreign Private Banks.

Study the Customer Relationship Management.

To know whether customers feel safe to invest in foreign banks or not.

To know the satisfaction level of customers with the services being offered to them.

To know whether the Retail Banking helps in upbringing the present economic situation.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 40/70

40

RESEARCH PROCESS:-

DIFFERENT STEPS ARE TO BE FOLLOWED IN THE RESEARCH PROCESS AND THEY ARE EXPLAINED AS

BELOW:

1. PROBLEM SOLVING

This is the basic step in the research process. IT IS WELL SAID, “A PROBLEM WELL DEFINED IS

HALF SOLVED” HERE THE PROBLEM IS “ Studing the customer satisfaction in retail banking through

the services being provided to consumers residing in Ludhiana”

2. RESEARCH DESIGN

Descriptive

3. UNIVERSE OF THE STUDY

People residing in Ludhiana

4. SAMPLING DESIGN

SAMPLE SIZE:- Sample size of 100 respondent

SAMPLE UNIT:-The Ludhiana from Feroze Gandhi market

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 41/70

41

5. DATA COLLECTION:- The data used in this report is primary as well as secondary.

(i)The primary data has been collected by using Questionnaire.

(ii)The secondary information has been gathered from different books, magazines and

internet.

Scope of the study

Scope of the study was limited to people residing in Ludhiana. Data was collected from 100

respondents which was the sample size through questionnaires.

Banks upon which study was conducted were private banks both Indian and Foreign. Bankstaken into consideration were SCB, HDFC, HSBC, ICICI and others. Research done was to

know how much the customers are satisfied with the services being provided by these banks.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 42/70

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 43/70

43

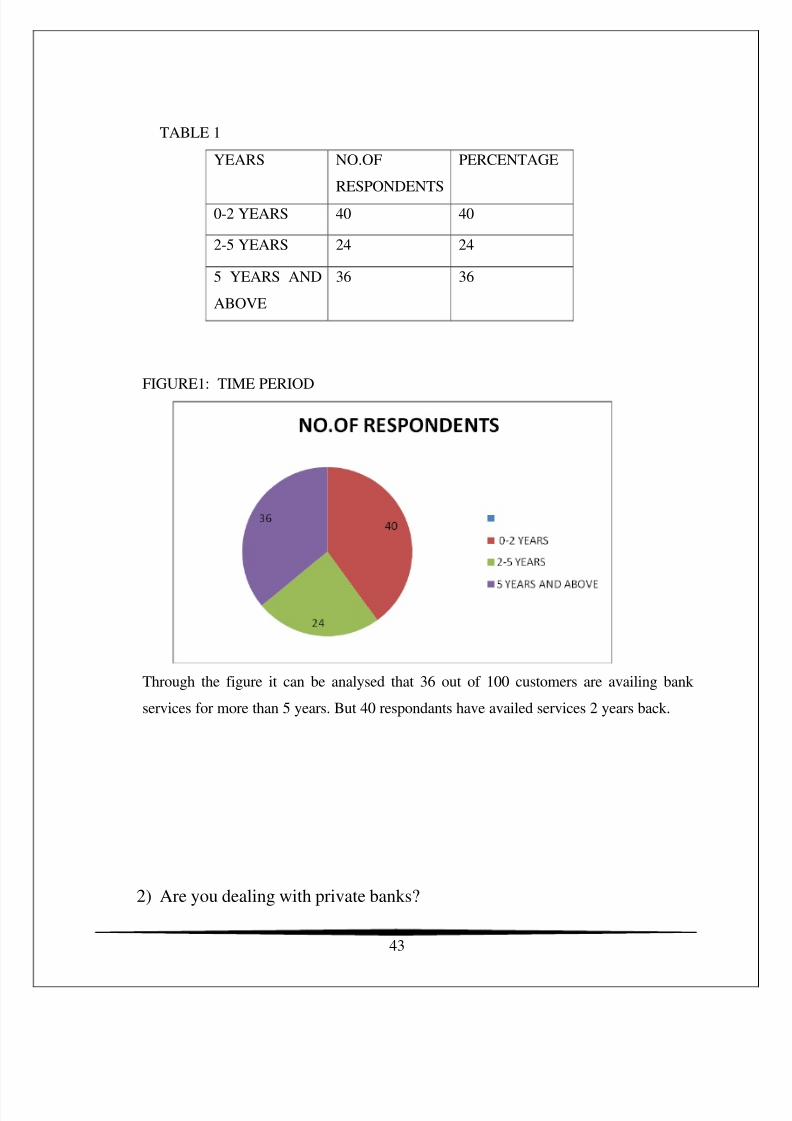

TABLE 1

YEARS NO.OF

RESPONDENTS

PERCENTAGE

0-2 YEARS 40 40

2-5 YEARS 24 24

5 YEARS AND

ABOVE

36 36

FIGURE1: TIME PERIOD

Through the figure it can be analysed that 36 out of 100 customers are availing bank

services for more than 5 years. But 40 respondants have availed services 2 years back.

2) Are you dealing with private banks?

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 44/70

44

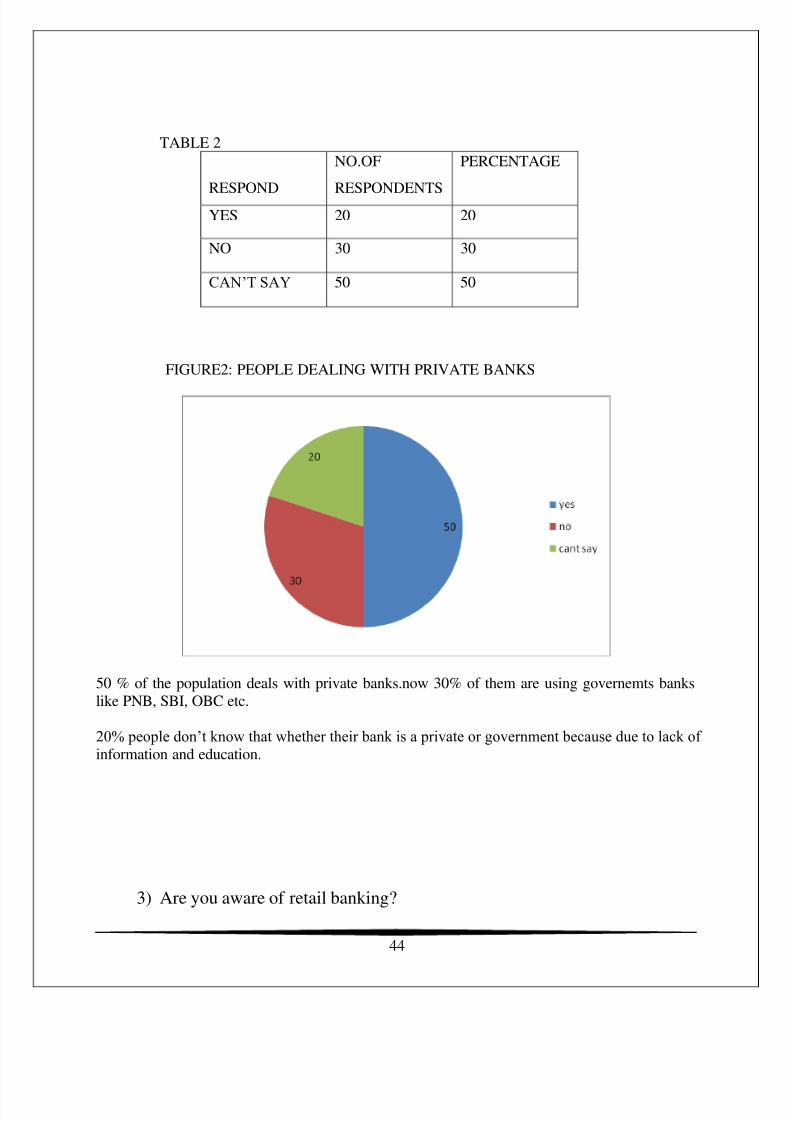

TABLE 2

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

YES 20 20

NO 30 30

CAN‟T SAY 50 50

FIGURE2: PEOPLE DEALING WITH PRIVATE BANKS

50 % of the population deals with private banks.now 30% of them are using governemts banks

like PNB, SBI, OBC etc.

20% people don‟t know that whether their bank is a private or government because due to lack of information and education.

3) Are you aware of retail banking?

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 45/70

45

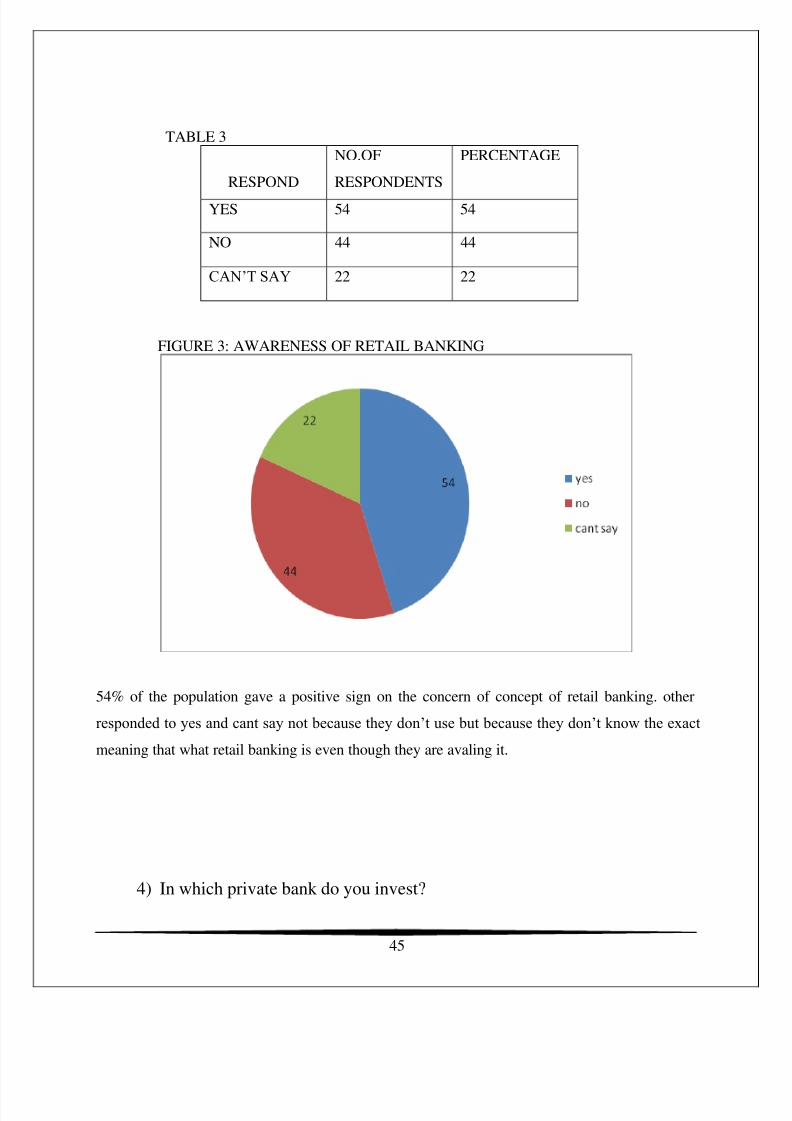

TABLE 3

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

YES 54 54

NO 44 44

CAN‟T SAY 22 22

FIGURE 3: AWARENESS OF RETAIL BANKING

54% of the population gave a positive sign on the concern of concept of retail banking. other

responded to yes and cant say not because they don‟t use but because they don‟t know the exact

meaning that what retail banking is even though they are avaling it.

4) In which private bank do you invest?

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 46/70

46

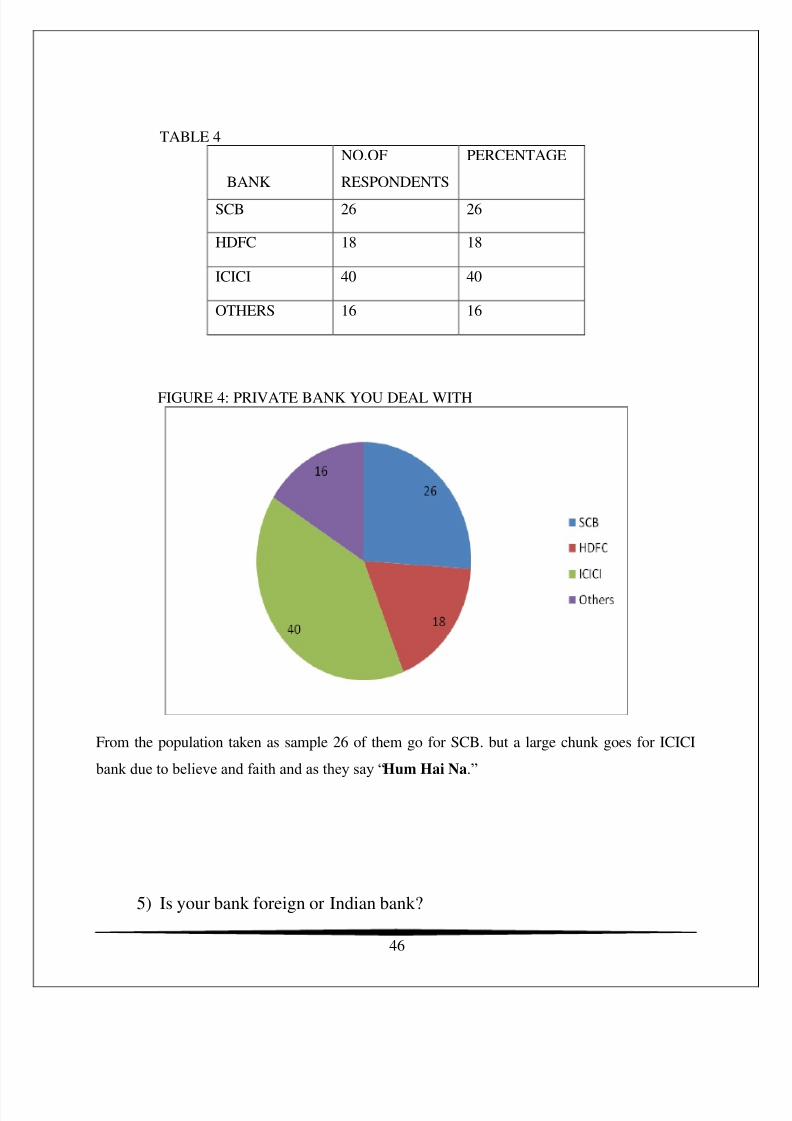

TABLE 4

BANK

NO.OF

RESPONDENTS

PERCENTAGE

SCB 26 26

HDFC 18 18

ICICI 40 40

OTHERS 16 16

FIGURE 4: PRIVATE BANK YOU DEAL WITH

From the population taken as sample 26 of them go for SCB. but a large chunk goes for ICICI

bank due to believe and faith and as they say “Hum Hai Na.”

5) Is your bank foreign or Indian bank?

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 47/70

47

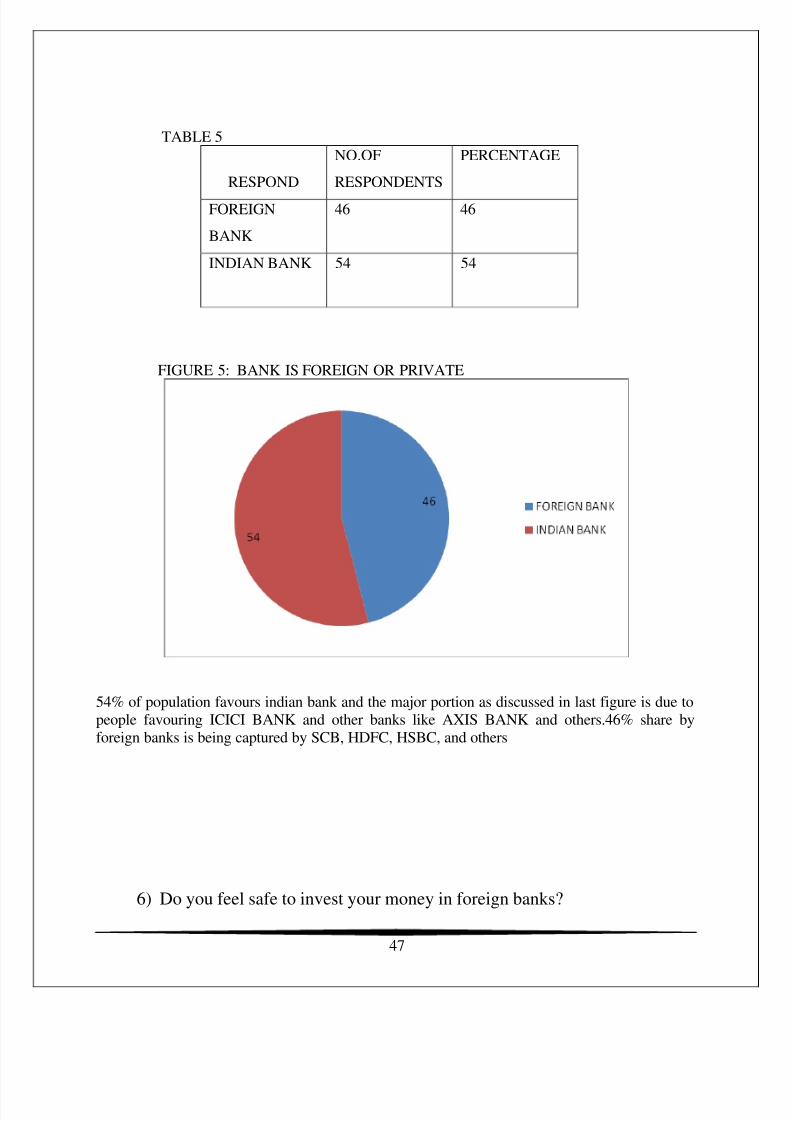

TABLE 5

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

FOREIGN

BANK

46 46

INDIAN BANK 54 54

FIGURE 5: BANK IS FOREIGN OR PRIVATE

54% of population favours indian bank and the major portion as discussed in last figure is due to

people favouring ICICI BANK and other banks like AXIS BANK and others.46% share by

foreign banks is being captured by SCB, HDFC, HSBC, and others

6) Do you feel safe to invest your money in foreign banks?

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 48/70

48

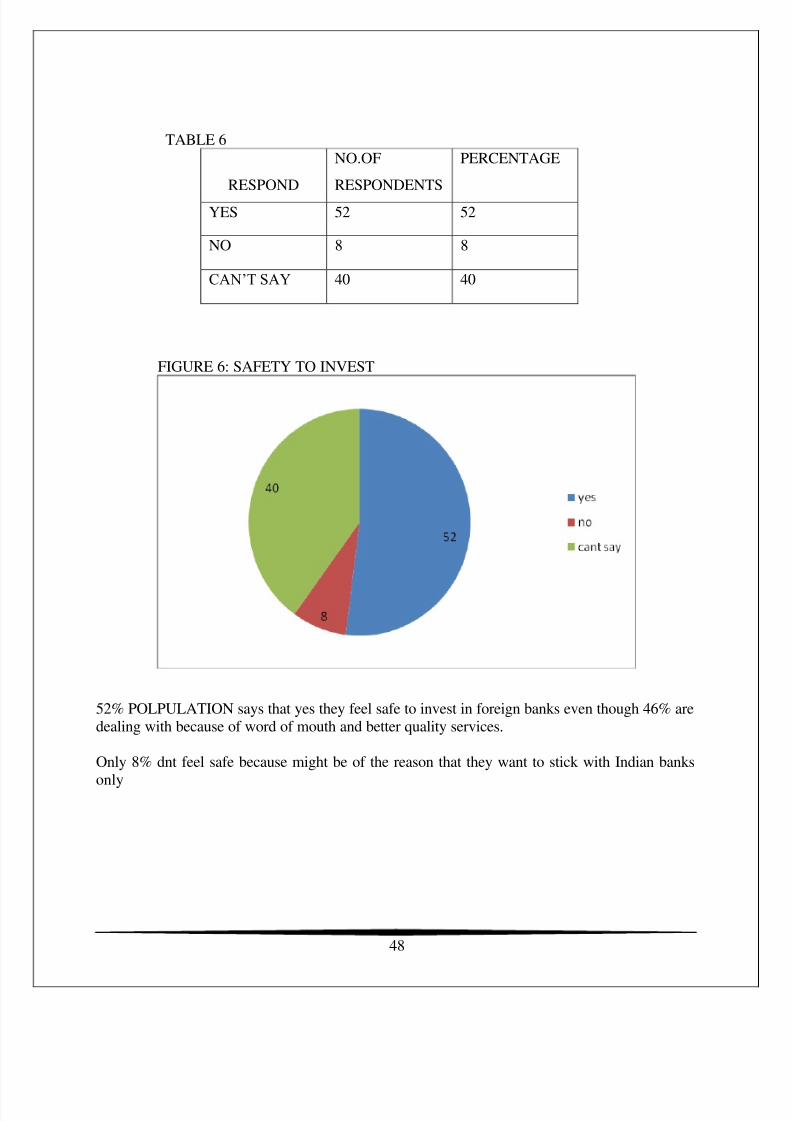

TABLE 6

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

YES 52 52

NO 8 8

CAN‟T SAY 40 40

FIGURE 6: SAFETY TO INVEST

52% POLPULATION says that yes they feel safe to invest in foreign banks even though 46% are

dealing with because of word of mouth and better quality services.

Only 8% dnt feel safe because might be of the reason that they want to stick with Indian banks

only

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 49/70

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 50/70

50

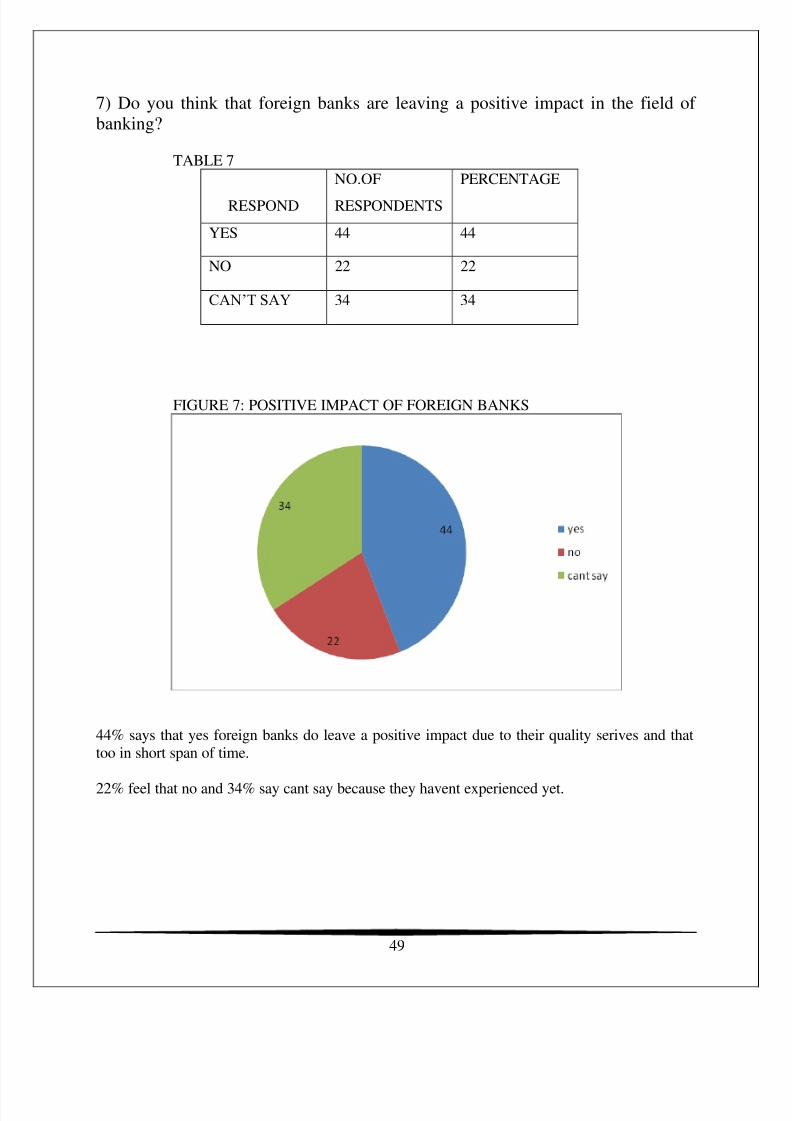

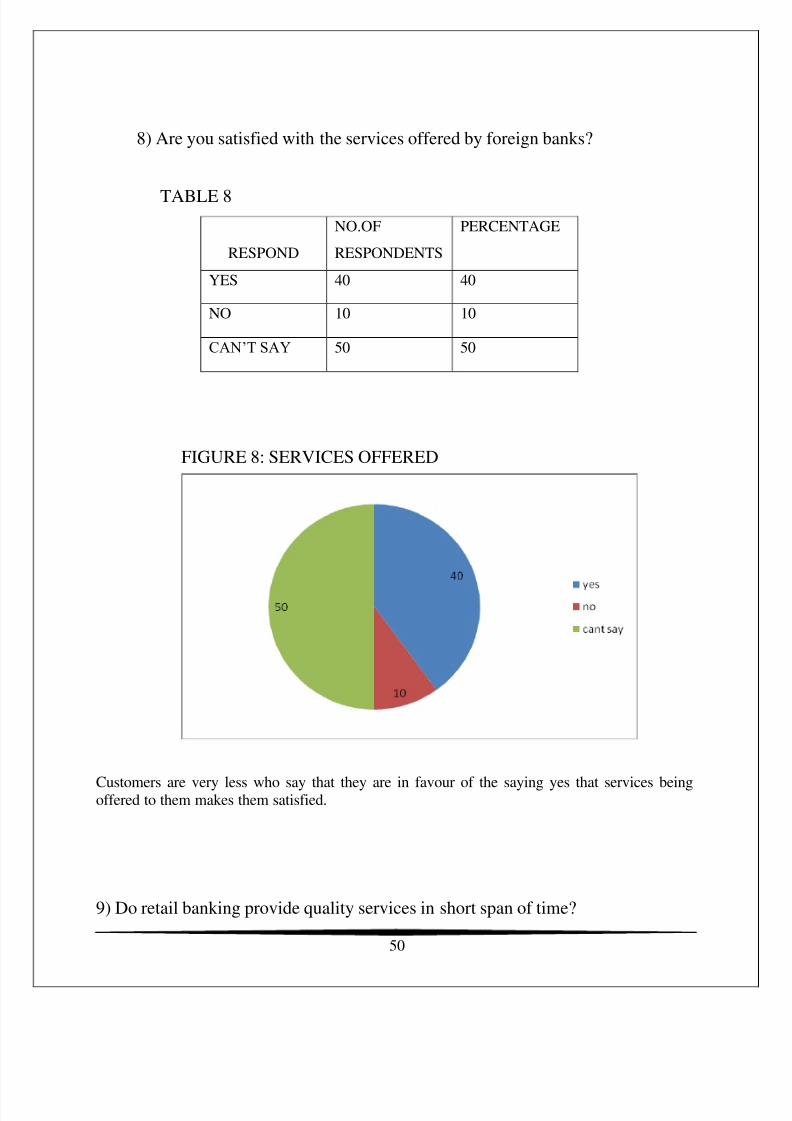

8) Are you satisfied with the services offered by foreign banks?

TABLE 8

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

YES 40 40

NO 10 10

CAN‟T SAY 50 50

FIGURE 8: SERVICES OFFERED

Customers are very less who say that they are in favour of the saying yes that services beingoffered to them makes them satisfied.

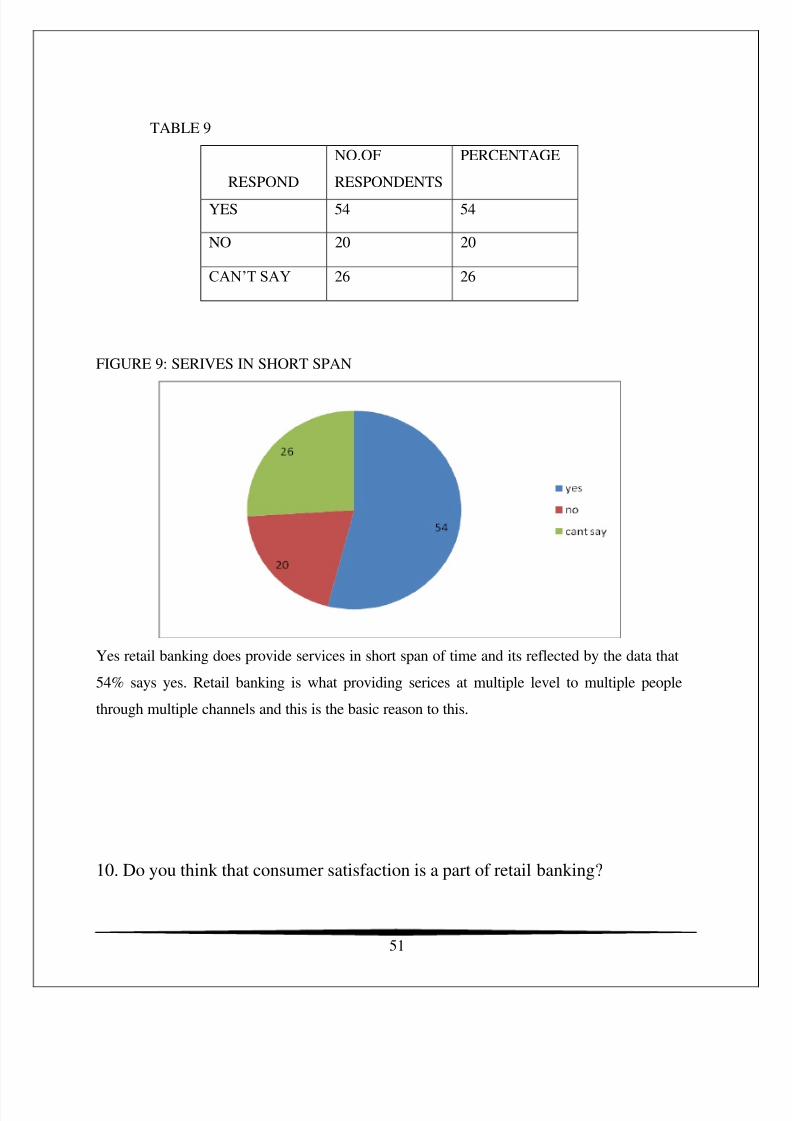

9) Do retail banking provide quality services in short span of time?

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 51/70

51

TABLE 9

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

YES 54 54

NO 20 20

CAN‟T SAY 26 26

FIGURE 9: SERIVES IN SHORT SPAN

Yes retail banking does provide services in short span of time and its reflected by the data that

54% says yes. Retail banking is what providing serices at multiple level to multiple people

through multiple channels and this is the basic reason to this.

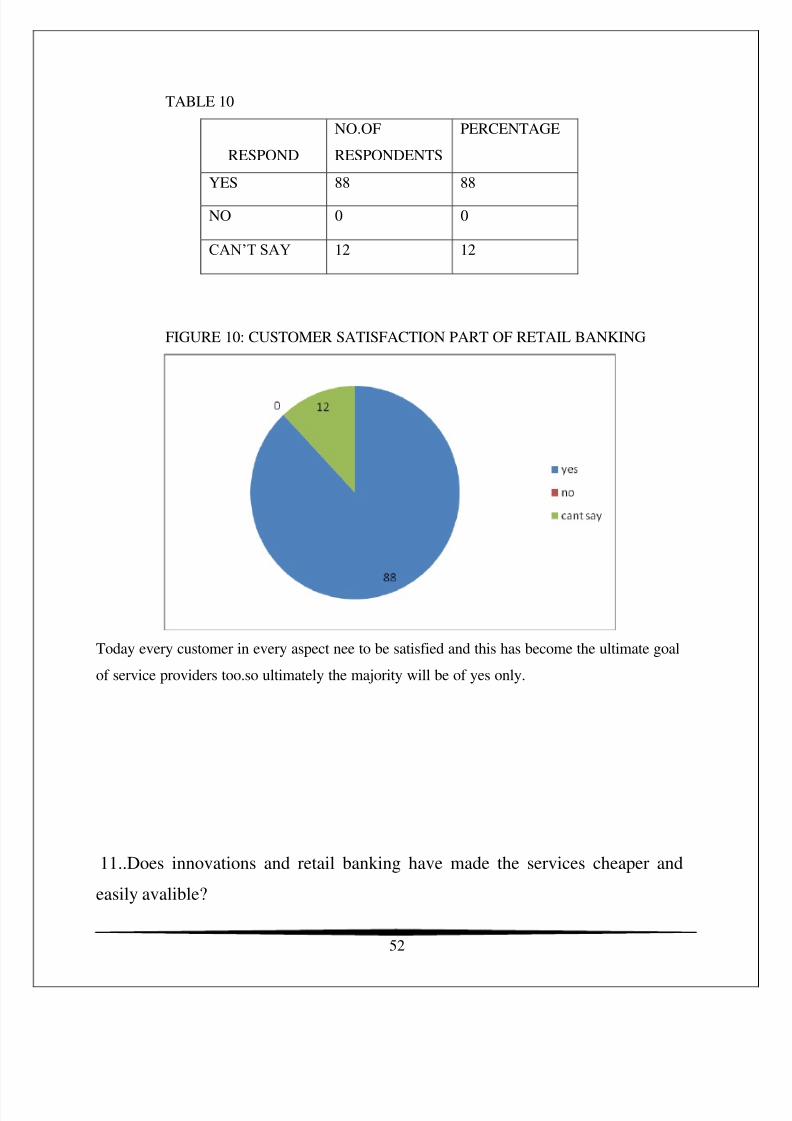

10. Do you think that consumer satisfaction is a part of retail banking?

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 52/70

52

TABLE 10

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

YES 88 88

NO 0 0

CAN‟T SAY 12 12

FIGURE 10: CUSTOMER SATISFACTION PART OF RETAIL BANKING

Today every customer in every aspect nee to be satisfied and this has become the ultimate goal

of service providers too.so ultimately the majority will be of yes only.

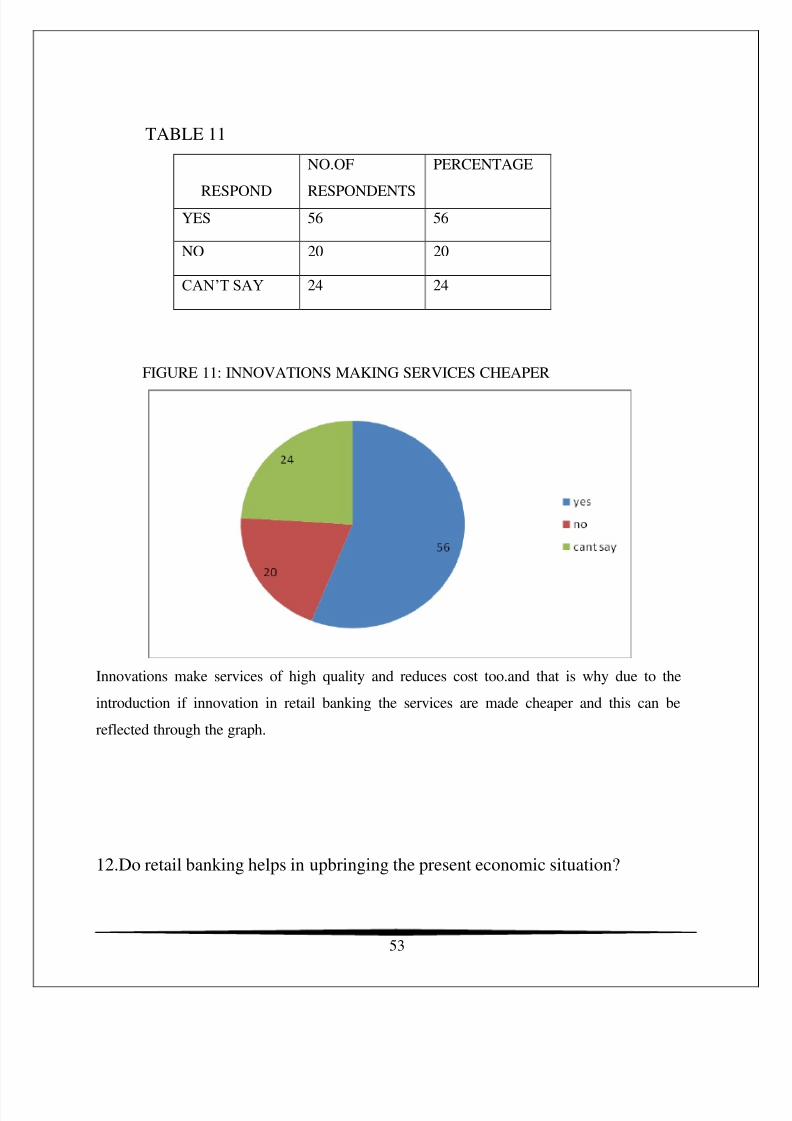

11..Does innovations and retail banking have made the services cheaper and

easily avalible?

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 53/70

53

TABLE 11

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

YES 56 56

NO 20 20

CAN‟T SAY 24 24

FIGURE 11: INNOVATIONS MAKING SERVICES CHEAPER

Innovations make services of high quality and reduces cost too.and that is why due to the

introduction if innovation in retail banking the services are made cheaper and this can be

reflected through the graph.

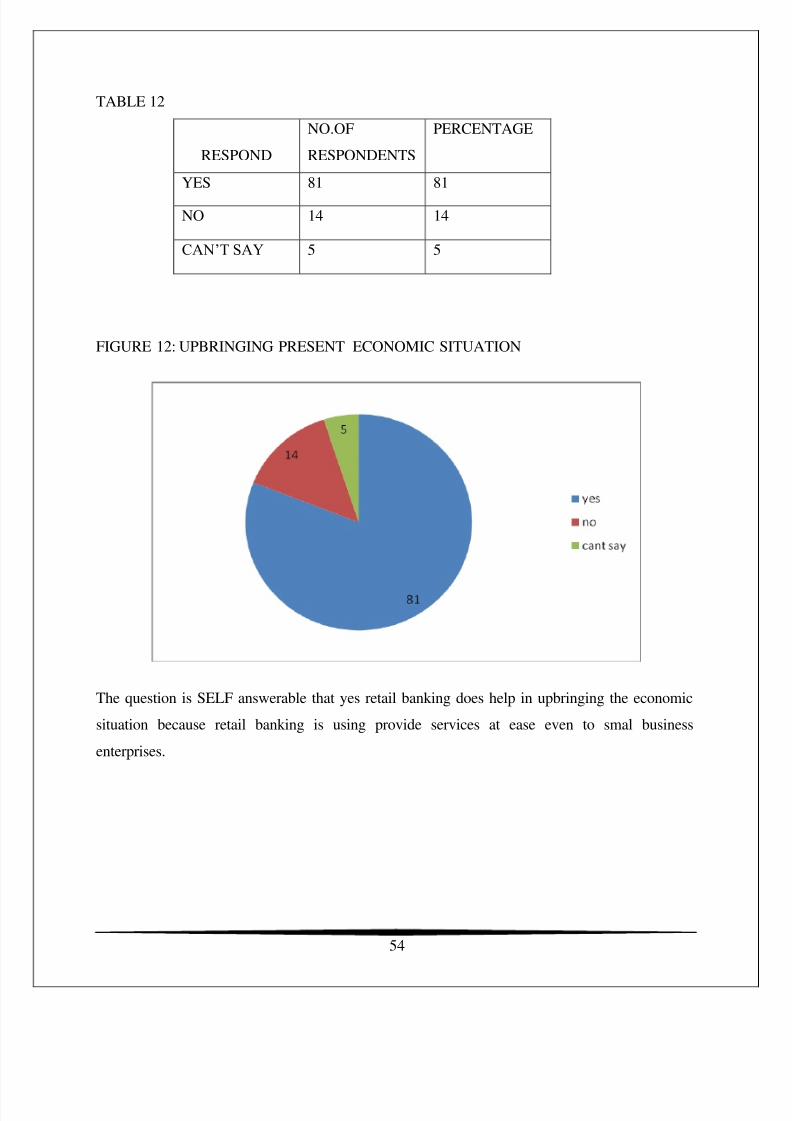

12.Do retail banking helps in upbringing the present economic situation?

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 54/70

54

TABLE 12

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

YES 81 81

NO 14 14

CAN‟T SAY 5 5

FIGURE 12: UPBRINGING PRESENT ECONOMIC SITUATION

The question is SELF answerable that yes retail banking does help in upbringing the economic

situation because retail banking is using provide services at ease even to smal business

enterprises.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 55/70

55

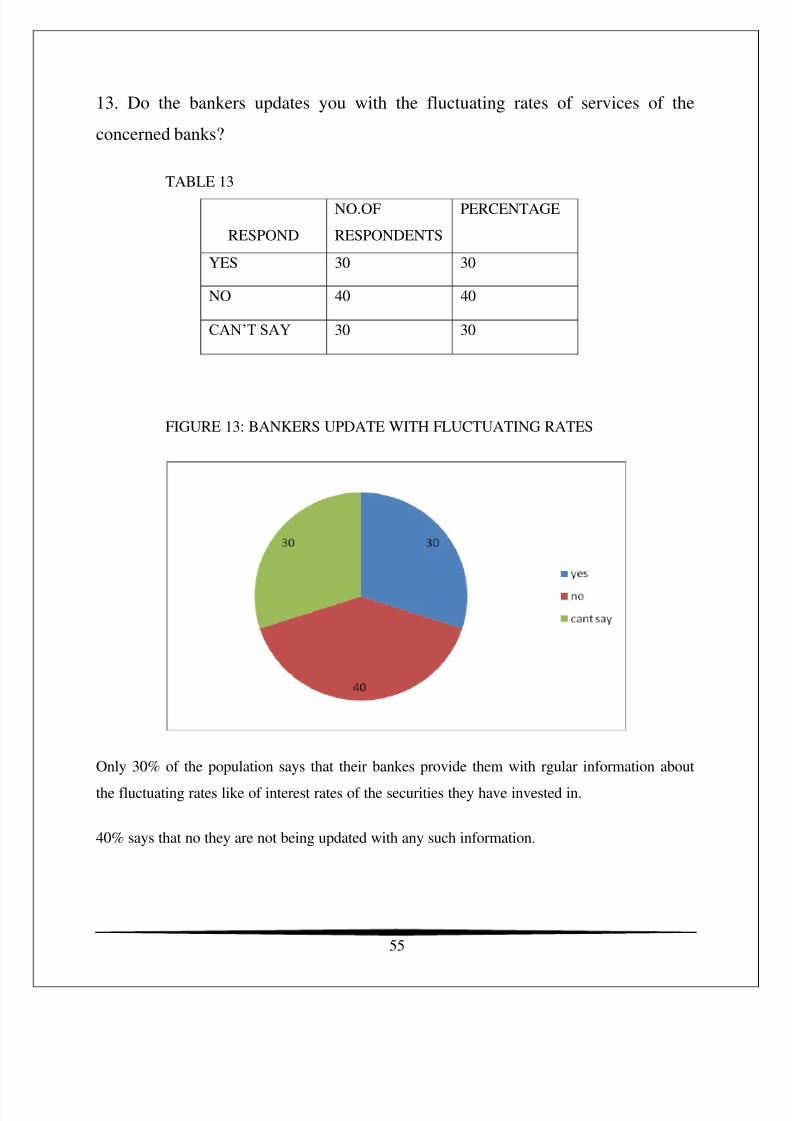

13. Do the bankers updates you with the fluctuating rates of services of the

concerned banks?

TABLE 13

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

YES 30 30

NO 40 40

CAN‟T SAY 30 30

FIGURE 13: BANKERS UPDATE WITH FLUCTUATING RATES

Only 30% of the population says that their bankes provide them with rgular information about

the fluctuating rates like of interest rates of the securities they have invested in.

40% says that no they are not being updated with any such information.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 56/70

56

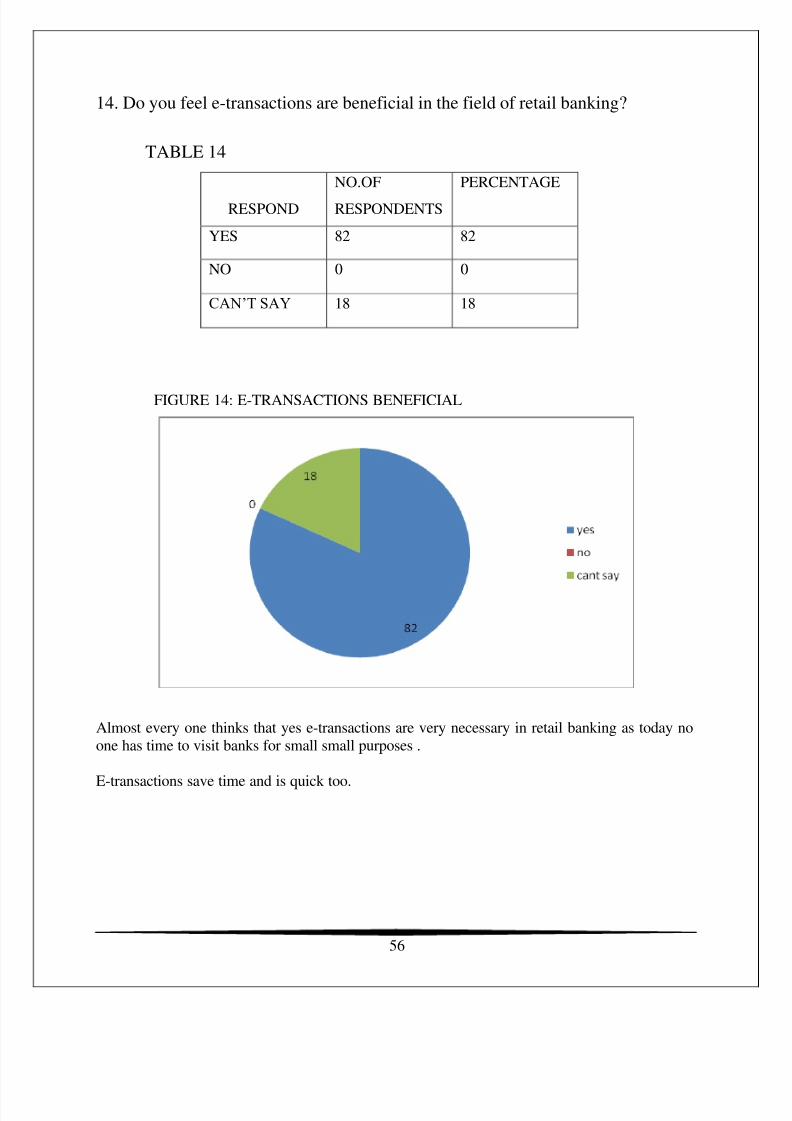

14. Do you feel e-transactions are beneficial in the field of retail banking?

TABLE 14

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

YES 82 82

NO 0 0

CAN‟T SAY 18 18

FIGURE 14: E-TRANSACTIONS BENEFICIAL

Almost every one thinks that yes e-transactions are very necessary in retail banking as today no

one has time to visit banks for small small purposes .

E-transactions save time and is quick too.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 57/70

57

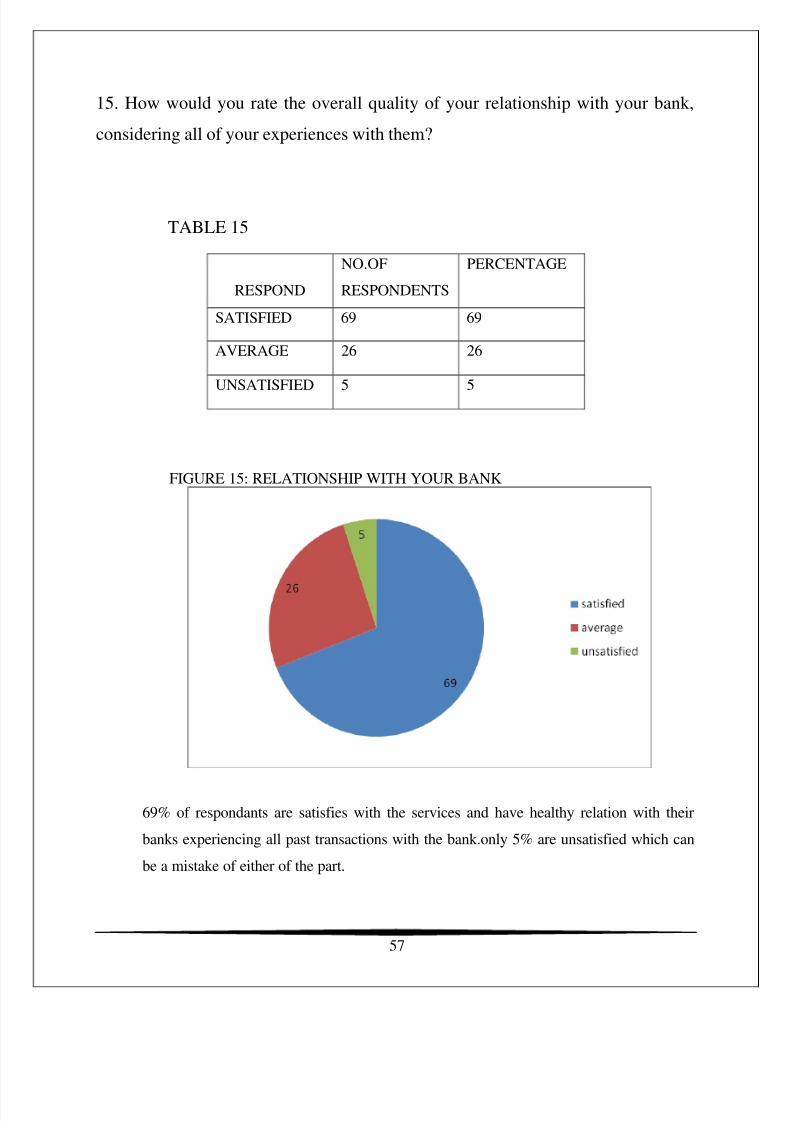

15. How would you rate the overall quality of your relationship with your bank,

considering all of your experiences with them?

TABLE 15

FIGURE 15: RELATIONSHIP WITH YOUR BANK

69% of respondants are satisfies with the services and have healthy relation with their

banks experiencing all past transactions with the bank.only 5% are unsatisfied which can

be a mistake of either of the part.

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

SATISFIED 69 69

AVERAGE 26 26

UNSATISFIED 5 5

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 58/70

58

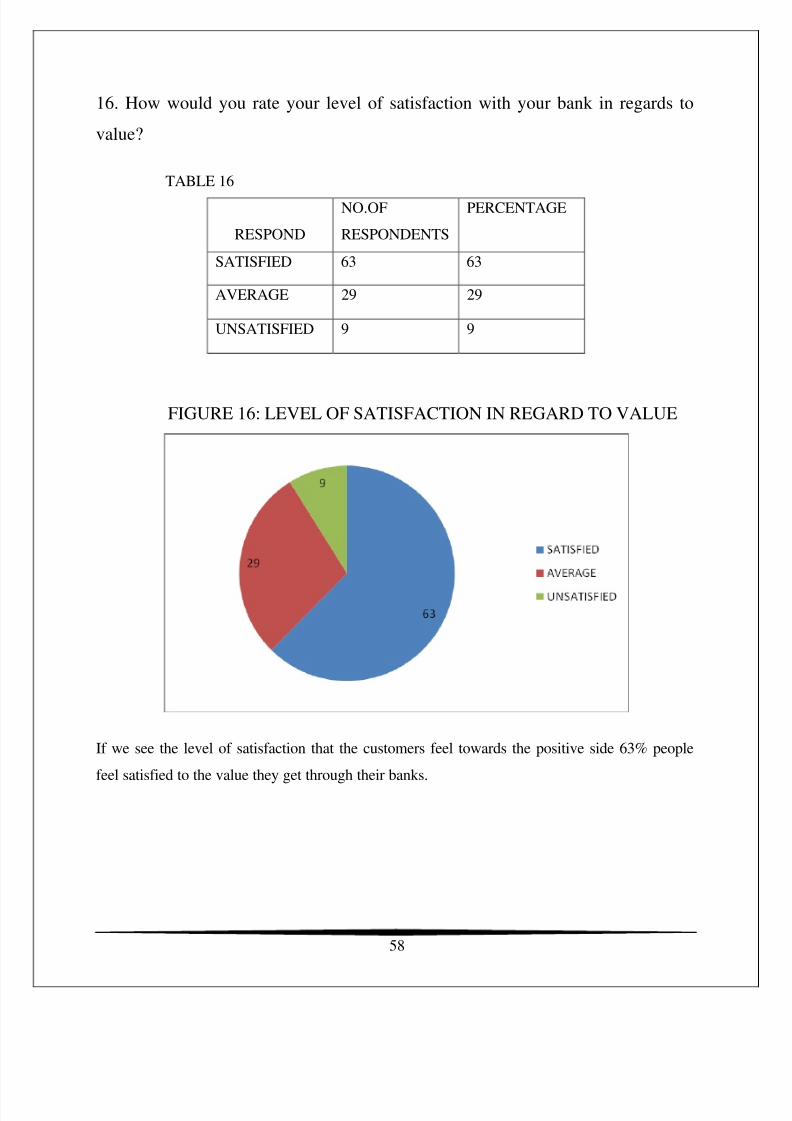

16. How would you rate your level of satisfaction with your bank in regards to

value?

TABLE 16

FIGURE 16: LEVEL OF SATISFACTION IN REGARD TO VALUE

If we see the level of satisfaction that the customers feel towards the positive side 63% people

feel satisfied to the value they get through their banks.

RESPOND

NO.OF

RESPONDENTS

PERCENTAGE

SATISFIED 63 63

AVERAGE 29 29

UNSATISFIED 9 9

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 59/70

59

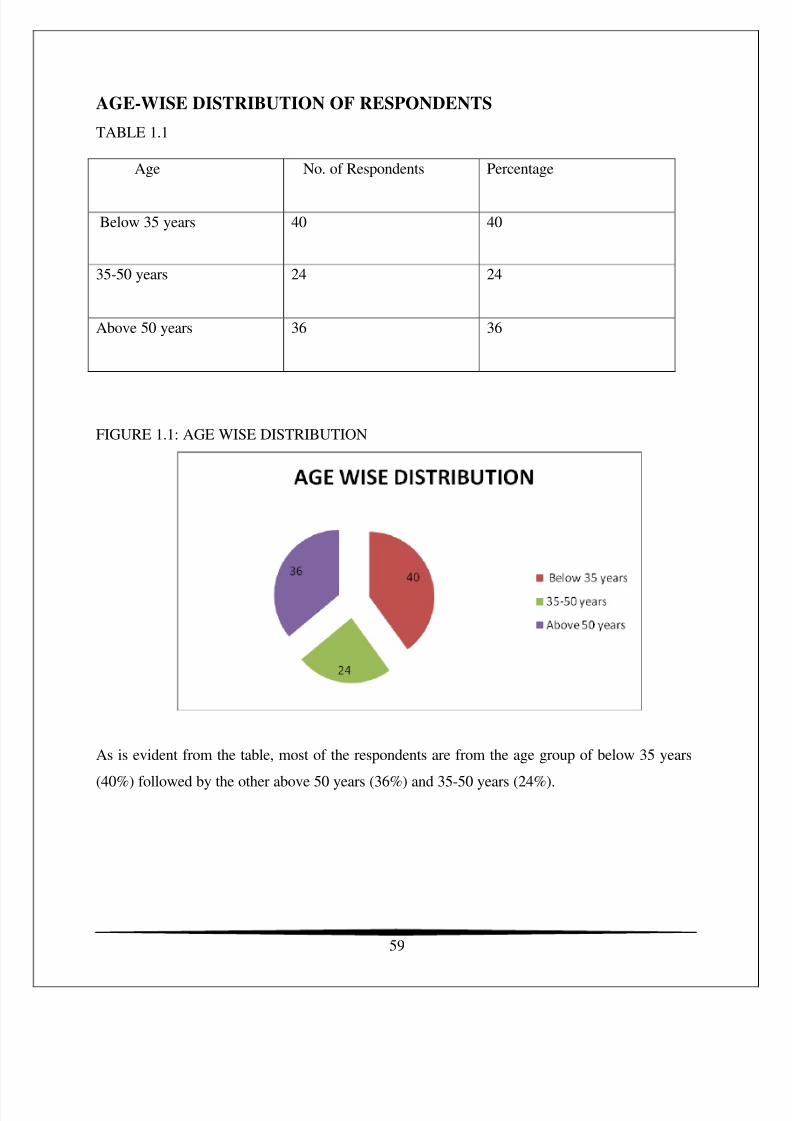

AGE-WISE DISTRIBUTION OF RESPONDENTS

TABLE 1.1

Age No. of Respondents Percentage

Below 35 years 40 40

35-50 years 24 24

Above 50 years 36 36

FIGURE 1.1: AGE WISE DISTRIBUTION

As is evident from the table, most of the respondents are from the age group of below 35 years

(40%) followed by the other above 50 years (36%) and 35-50 years (24%).

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 60/70

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 61/70

61

Findings:

The study allowed me get answers regarding the service awareness among people and the

problems it faces. The key findings and analysis of the survey showed the following:

46 out of 100 respondants said that their bank is a foreign private bank and only 50

respondants feel safe in investing money in foreign banks. This difference is due to the

word of mouth that is these four people would like to invest in foreign banks as they have

heard of good services and positive response fron those who do.

40 respondants say that they are satisfied with the serices being offered to them by

foreign banks. Fluctuation in this this could take place according to the situations.

Customer base of foreign banks is good but not that as of Indian private bank like ICICI

as taken to compare for our study because of the perception made in the mind of people

that ONE INDIAN CAN SERVE THE OTHER BETTER.

Only few respondants were aware of the net banking serives because even today many

are not aware of how to avail for or to use the services. so this are need to be improved

upon by private banks.

81% of respodants say that yes retail banking helps in upbringing the present economic

situations. In this is quite obvious because retail banking is all about providing multiple

services at multiple levels to multiple group . Even the small business are being

provided with provisions.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 62/70

62

Recommendations

I suggest following measures, which Standard chartered Bank could take so as to take

on heavy competition from HSBC, ICICI, HDFC banks as in Ludhiana:

To identify regions where promotions are required. SCB lacks visibility in Northern

region where as it is a well known name in western region. Even then, its promotional

campaign focuses on western region where as northern region is still waiting for

promotional campaigns.

SCB should contact with their clients regularly for knowing the problems faced by them.

This will help SCB in providing best services to customers.

Also a problem recognized is that still many customers are not updated with Hi-Tech

services like of how to use Net banking like online transactions, checking accounts. So I

think that banks should first give demo to there customers regarding this.

As security is a matter of concern for most of the customers SCB should rely on providing

customers with special managers like relationship managers so as to provide customers

feeling of faith.

It is been seen that the customers are really happy with the services being provided it can

be said tha customer relationship management is the core to this result and all foreign

private banks should maintain it in furure to retain its customers.

From fig. 5 it is seen that even today more INDIAN PRIVATE BANKS ARE BEING

GIVEN priority then the foreign banks even though their services are much better, foreignbanks like SCB and others should properly do the customer segmentation, know their

needs and then make proper marketing strategies.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 63/70

63

Conclusion

Throughout the whole study being conducted on 100 respondents of Ludhiana it is being

concluded that in this era the foreign banks are playing equally or even more part for

giving innovative services to their customers. Most of the customers are satisfied with the

services. The important field that customers feel that should be emphasized is giving

them security to the investment done by them because their might be a fraud cases too.

Banks are developing healthy relations with their customers to capture market share n

retain customers for long period of time.

But everything comes with some drawbacks too. It has been studied that some services

tht are highly innovative, the customers don‟t know how to avail them. So the banks

beforehand should make their customers educate regarding this. This could be like

similar to use of Net Banking services.

On a overall view point Retail Banking is a popular topic where all banks whether Indian

or Foreign are taking keen interest to capture market share.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 64/70

64

LIMITATIONS OF THE STUDY

Collection of data by questionnaire method can have the limitations of the inability and

unwillingness of respondents to provide information.

The findings of the study are based on the subjective opinion of the respondents. They

could not be verified.

The accuracy of the results is also limited by the reliability of the tools of investigation

and analysis of data.

The present study is confined to the city of Ludhiana only. The findings of the study may

not be applicable in other parts of the country because of social and cultural differences.

The behaviour of consumers is very dynamic in nature. There is every possibility that

findings of today may become invalid tomorrow.

The scope of the study is also limited.

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 65/70

8/8/2019 Khushboo Project

http://slidepdf.com/reader/full/khushboo-project 66/70

66

QUESTIONNAIRE

Dear Respondents,

I am a student of MBA (Sem III) of Lovely Profesional University.I am carrying out a project on

“Retail and Consumer Banking” on the basis of a study conducted at Standard Chartered Bank,

Ludhiana as a part of my Summer Training. I request you to kindly spare some of your valuable

time for filling up the following questionnaire. The information provided by you will be kept

confidential and used only for study purpose.

Thank You,

Khushboo Anand

1.For how long are you using banking?

(a)yes (b)no (c)2-5 yrs (d)above 5

2. Are you dealing with private banks?

(a) YES (b) NO (c) CAN‟T SAY

3. Are you aware of consumer and retail banking?

(a) YES (b) NO (c) CAN‟T SAY