Embed Size (px)

Citation preview

Report

Key trends in R&D in relation to food, beverages, nutrition & healthWhat these trends mean for NZ

Julian MellentinJune 2011

Presented by

NEW NUTRITION BUSINESS

Julian Mellentin is director of a company dedicated solely, since 1995, to providing strategic and market insights into the business of food and health, globally.

Offices in London, New Zealand, affiliate companies in Finland and Japan.

Publishes New Nutrition Business, world’s leading food and health insight service.

Julian is also co-author of Functional Foods Revolution, the best-selling (54,000 copies sold) and first-ever book on the business of functional foods, now translated into Japanese. He is also co-author of the The Food & Health Marketing Handbook.

Our credentials

NEW NUTRITION BUSINESS

Our exclusive focus gives us an unrivalled knowledge of food and health globally. Our customers appreciate our ability to explain what is happening and what it means to them, and our ability to help them use our insights to create additional sales and higher profit margins.

Health & nutrition trends analysis: What we do better than anyone else. We constantly monitor consumer research, supermarket sales data and every year we interview 450 industry executives – giving our customers clear, actionable insights, tailored to individual companies’specific areas of interest.

Innovation and commercialising science: we help some of the world’s biggest food and beverage companies identify innovations and how to take them to market. We help companies turn market information into R&D strategy.

Global leadership: from Australia to America to Europe, businesses use our unrivalled competence to inform their strategy and guide the direction of product development. We work with some of the world’s leading companies as well as entrepreneurial start-ups. Client references are available on request.

Unrivalled expertise

NEW NUTRITION BUSINESS

1. Deliver clarity on the R&D trends and areas of R&D focus in foods, beverages, nutrition and health (supplements will also be included). The trends will be ranked and the industry rationale for each one explained, along with detail about the current market size and dynamics relating to each research area and any relevant consumer insights.

2. The trends are identified separately for consumer goods companies and for ingredient suppliers, as there are different research priorities at different points in the value chain.

3. Where possible, we have used case studies of actual companies to illustrate the trend.

Objectives & content

NEW NUTRITION BUSINESS

4. The report describes the nutrition science commercialisation life-cycle and the key success factors for bringing new science to market.

5. A special section is devoted to a focus on trends among Japanese companies.

6. The report summarises the points that are – we believe – most relevant to New Zealand and the strategy formulation challenge that government faces, and sets out potential options and steps for New Zealand.

Objectives & content (cont.)

NEW NUTRITION BUSINESS

Each year we interview more than 450 senior executives, worldwide, in foods, beverages, supplements and ingredients.

We also work closely with some of the world’s largest companies (and some of the smallest) to identify innovations and new directions for research.

Taken together these give us unrivalled knowledge in the health and nutrition arena which we have drawn on to create this report.

In support of this project we have additionally conducted confidential interviews with senior Innovation and R&D executives at:•Danone•PepsiCo•Nestlé•General Mills•DSM

Methodology and sources…1

NEW NUTRITION BUSINESS

Our customers all make use of our searchable database of information on the business of food, nutrition and health.

Around 850 companies make thousands of individual searches each year.

We are able to see exactly what each company’s R&D group is searching for and this over the past 10 years has provided both a good sample and accurate indicator of the key areas of interest for R&D and innovation.

While we cannot disclose individual companies’ data, we can say that this report is informed by the R&D strategy of Yoplait, Unilever, Nestlé, George Weston, Danone, PepsiCo…..and many, many others.

Methodology and sources…2

NEW NUTRITION BUSINESS

Summary

16

NEW NUTRITION BUSINESS

Research agendas are most strongly driven by the following….

NUTRITION NEEDS

CATEGORIES

Fruits & Veg

Grains

SYSTEMSBENEFITS

Services

Digestive Weight Management

Energy

AntioxidantsDiabetes

Mobility

Cognitive

Dairy Seniors

Sports Nutrition

Packaging

NEW NUTRITION BUSINESS

Selection criteria driving R&D strategy

Accessibility Science to developGeneric science currently available or medium or long term development needed?

RegulatoryApproved for use? Are claims possible?

IngredientsClearly defined to be able to deliver the benefit. Easy to integrate into a food or beverage form.

OwnabilityProprietary technology or patent?

Opportunity Food CategoryCan be executed in current categories? Providesopportunities to move into new categories? Is the benefit and the ingredient logical and acceptable to consumers in a food/beverage form?

RelevanceIs there any public health need?

CompetitionDoes this provide the opportunity to fill a gap in the market or to create a new category?

Consumer InterestAt what level is consumer awarenessof this benefit? What is the credibility?

These are some of the actual criteria which many companies take into account in deciding whether to pursue a particular direction in R&D and product development. Short-term financial pressures increasingly mean that companies are under pressure to focus on near-term, low-risk opportunities.

NEW NUTRITION BUSINESS

It should be noted that many of the areas defined on Slide 9 have a significant number of overlaps and these overlaps will be seen again and again in this report.

The consumer goods companies, because they are closest to the consumer, are the biggest driver of the R&D agenda throughout the industry. It should be noted that many of the areas under research by ingredient companies –who are upstream from the consumer – are not on the chart and play little role in the corporate R&D strategies of consumer goods companies.

Oral health, for example, is an area of R&D interest to some ingredient companies – such as the Danisco operation of DuPont – but it is of limited interest to food and beverage companies since the market opportunity is limited. As one senior food company executive noted: “It is such a small niche that we would struggle to justify to our chairman why we would put any efforts into it.”

11

Key issues

NEW NUTRITION BUSINESS

Consumer goods companies’ innovation and research focus is driven by a mixture of “technology push” and “consumer pull”.

Technology push in this context means what their access to technologies, patents and production facilities enables them to do in terms of creating new products, while consumer pull means the preferences of consumers –which may be very different from what technology can deliver.

Ingredient companies, by contrast, are still very strongly “technology push”oriented. This isn’t surprising as they are upstream from the consumer and own no consumer brands of their own, and they are grounded in science and technology.

Ingredient companies often (usually) place thinking about the consumer and how to deliver their technology to the consumer at the end point of their R&D efforts - while by contrast consumer goods companies try to balance consumer needs and technology at every stage in the development process.

12

Key issues

NEW NUTRITION BUSINESS

As a result ingredient company activities have a very high failure rate. Danisco, see below, may have introduced a new sterol for heart health, but it is late into an established market and brings no new point of difference.

13

Key issues

NEW NUTRITION BUSINESS

Key issues

14

• Science and functional claims have become a commodity: there are hundreds of universities and research organisations offering their services as research partners to the food and beverage industry.

• Companies have a marked preference for collaborating with individual researchers who have specific expertise rather than focusing on the institution of which they are part.

• Companies are also drawn to researchers whose work can be – and preferably already is –patented or in some other way can become proprietary intellectual property that can be used to create unique products.

• Geographical proximity is also important.

• Research partnerships and services increasingly provided by ingredient suppliers, who are called upon to undertake R&D work for client companies (or potential clients).

• Ingredient companies are more and more becoming gatekeepers for research to get to the mass of the medium and small food companies.

NEW NUTRITION BUSINESS

1. R&D trends – consumer goods companies

16

NEW NUTRITION BUSINESS

Consumer goods companies’ innovation and research focus is driven by a mixture of “technology push” and “consumer pull”.

Technology push in this context means what their access to technologies, patents and production facilities enables them to do in terms of creating new products, while consumer pull means the preferences of consumers –which may be very different from what technology can deliver.

Balancing these two is a continuous process and there are no easy solutions.

Over the last 15 years most companies have learnt that allowing technology push to dictate their activities has resulted in products that fail in the marketplace – and around 80% of all new foods and beverages with health benefits are withdrawn within two years of launch.

Balancing technology push with consumer pull is key

16

NEW NUTRITION BUSINESS

Ingredient companies, by contrast, are still very strongly “technology push”oriented. This isn’t surprising as they are upstream from the consumer and own no consumer brands of their own, and they are grounded in science and technology – in fact senior executives often have no direct experience of business-to-consumer markets.

The approach of these companies can be summarised as creating or acquiring technologies, developing them and then trying to find or create markets for them.

Ingredient companies often (usually) place thinking about the consumer and how to deliver their technology to the consumer at the end point of their R&D efforts - while by contrast consumer goods companies try to balance consumer needs and technology at every stage in the development process.

Balancing technology push with consumer pull is key

17

NEW NUTRITION BUSINESS

Ingredient companies’ “technology push” approach has contributed to the high rate of failure as they “push” technology into the consumer market before:

a) establishing how it should best be commercialised; or b) whether it meets any real consumer need; or c) how the consumer can best be educated about its benefits.

One example of this technology push approach is the way in which ingredient companies pushed marine-source omega-3 (DHA/EPA) to consumer goods companies, encouraging them to prematurely launch omega-3 fortified foods and beverages (before consumer issues with omega-3 had been properly resolved). As a result most omega-3 foods and beverages have failed in the marketplace, with companies such as Danone and Mueller Dairy removing omega-3 from many brands’ formulations.

Balancing technology push with consumer pull is key

18

NEW NUTRITION BUSINESS

The top consumer health concerns (things that affect them personally)

19

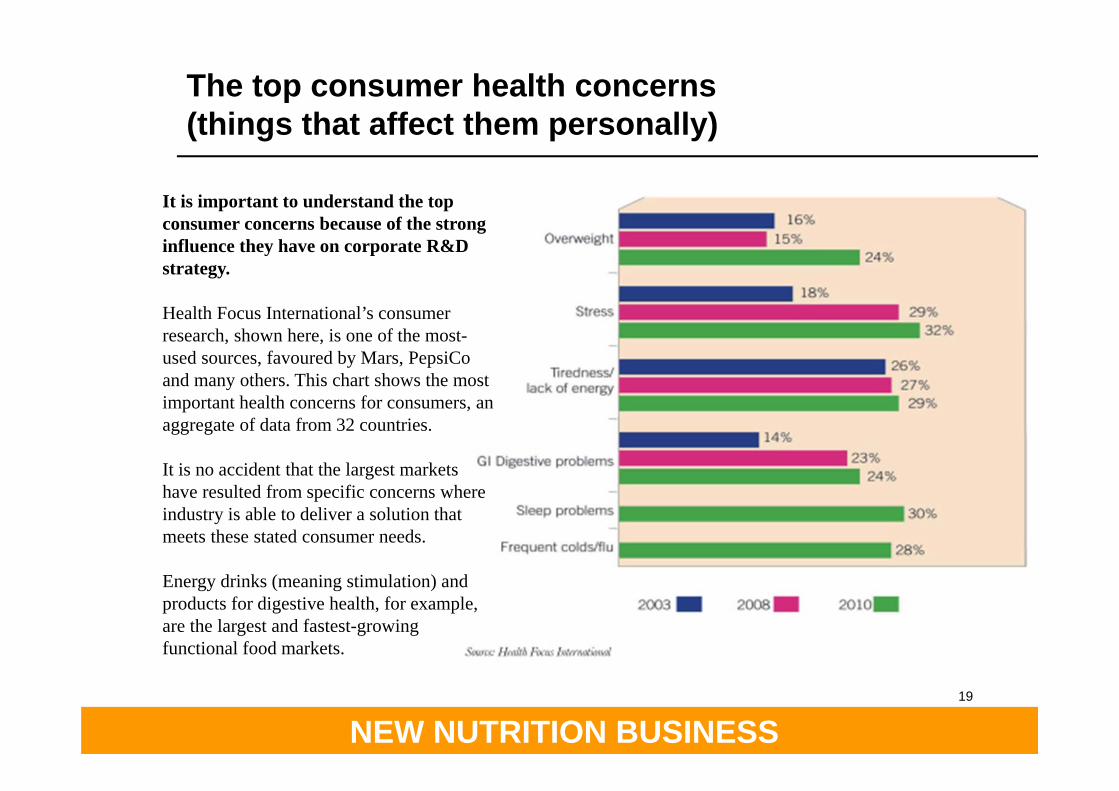

It is important to understand the top consumer concerns because of the strong influence they have on corporate R&D strategy.

Health Focus International’s consumer research, shown here, is one of the most-used sources, favoured by Mars, PepsiCo and many others. This chart shows the most important health concerns for consumers, an aggregate of data from 32 countries.

It is no accident that the largest markets have resulted from specific concerns where industry is able to deliver a solution that meets these stated consumer needs.

Energy drinks (meaning stimulation) and products for digestive health, for example, are the largest and fastest-growing functional food markets.

NEW NUTRITION BUSINESS

Selection criteria driving R&D strategy

Accessibility Science to developGeneric science currently available or medium or long term development needed?

RegulatoryApproved for use? Are claims possible?

IngredientsClearly defined to be able to deliver the benefit. Easy to integrate into a food or beverage form.

OwnabilityProprietary technology or patent?

Opportunity Food CategoryCan be executed in current categories? Providesopportunities to move into new categories? Is the benefit and the ingredient logical and acceptable to consumers in a food/beverage form?

RelevanceIs there any public health need?

CompetitionDoes this provide the opportunity to fill a gap in the market or to create a new category?

Consumer InterestAt what level is consumer awarenessof this benefit? What is the credibility?

These are some of the actual criteria which many companies take into account in deciding whether to pursue a particular direction in R&D and product development. Short-term financial pressures increasingly mean that companies are under pressure to focus on near-term, low-risk opportunities.

NEW NUTRITION BUSINESS

A key issue: science is a commodity

21

“Science and functional claims have become a commodity.”

“Science is not a point of difference – but it gives you the platform to create a point of difference from the way you use branding and marketing to commercialise the science”

Source: interviews with senior innovation executives in multinational food companies.

•There are tens, perhaps hundreds, of universities and research organisations offering their services as research partners to the food and beverage industry.

•Increasingly companies collaborate with a wide range of third party researchers to conduct research that would in the past have been conducted in-house.

•These alliances are fluid, with companies conducting research wherever there are researchers who are recognised in the the field.

NEW NUTRITION BUSINESS

A key issue: science is a commodity

22

• Enduring partnerships between companies and research organisations seem to be few.

• Companies have a marked preference for collaborating with individual researchers who have specific expertise rather than focusing on the institution of which they are part.

• Companies are also drawn to researchers whose work can be – and preferably already is –patented or in some other way can become proprietary intellectual property that can be used to create unique products. An example is Danone Medical Nutrition’s partnership with MIT Massachusetts (which is driven by a particular researcher’s competence), which will see Danone bring to market a beverage clinically proven to reverse the symptoms of Alzheimers (see Slide 66). The technology is covered by a patent which belongs to MIT.

• Geographical proximity is also important – MIT is just 3 hours drive from Danone’s North American innovation team.

NEW NUTRITION BUSINESS

Expertise plus geographical proximity

23

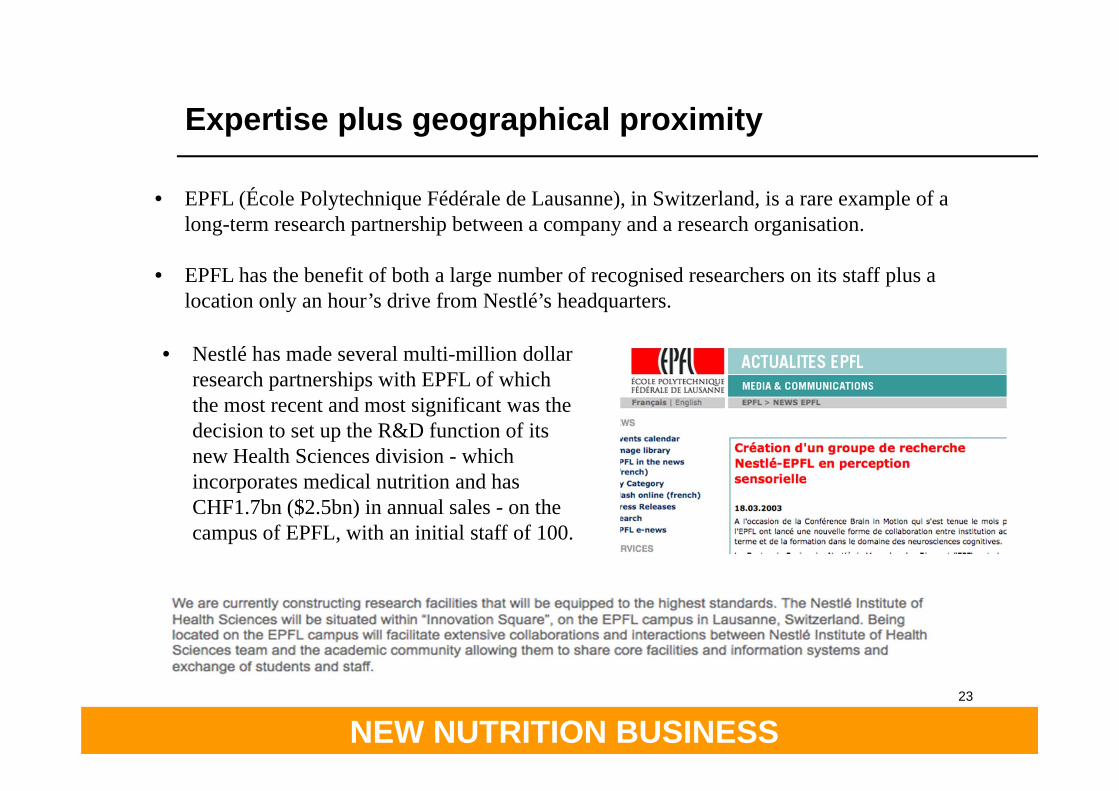

• EPFL (École Polytechnique Fédérale de Lausanne), in Switzerland, is a rare example of a long-term research partnership between a company and a research organisation.

• EPFL has the benefit of both a large number of recognised researchers on its staff plus a location only an hour’s drive from Nestlé’s headquarters.

• Nestlé has made several multi-million dollar research partnerships with EPFL of which the most recent and most significant was the decision to set up the R&D function of its new Health Sciences division - which incorporates medical nutrition and has CHF1.7bn ($2.5bn) in annual sales - on the campus of EPFL, with an initial staff of 100.

NEW NUTRITION BUSINESS

Research is now an ingredient supplier service

24

Research partnerships and services are also increasingly provided by ingredient suppliers, who are called upon to undertake R&D work for client companies (or potential clients).

Many medium sized companies – and almost all small ones – increasingly leave R&D up to the ingredient companies who supply them and they expect these companies to supply a total package which includes ingredients, proof of efficacy and validity of claims, final product concepts and formulations, regulatory advice and labelling.

In fact far-sighted companies are deliberately setting out to bind their clients – the consumer goods companies – closer to them by offering such total packages, which include R&D strategy.

Companies such as DSM (a diversified ingredients group), Beneo (the world’s biggest supplier of dietary fibres) and Carbery (an Irish supplier of dairy proteins) are all actively pursing such a strategy, with Beneo even having set up a stand-alone consultancy company specifically to provide these services even to companies who are not clients for its fibres.

Ingredient companies are more and more becoming gatekeepers for research to get to the mass of the medium and small food companies.

NEW NUTRITION BUSINESS

Research is now an ingredient supplier service

25

Ingredients giant Beneo, based in Belgium, has set up a stand-alone consultancy company specifically to provide consultancy services even to companies who are not clients for its fibres.

NEW NUTRITION BUSINESS

Research agendas are most strongly driven by the following….

NUTRITION NEEDS

CATEGORIES

Fruits & Veg

Grains

SYSTEMSBENEFITS

Services

Digestive Weight Management

Energy

AntioxidantsDiabetes

Mobility

Cognitive

Dairy Seniors

Sports Nutrition

Packaging

NEW NUTRITION BUSINESS

The term “natural” is not used in a technical sense, rather it is usedas a consumer definition, to mean foods that are “free-from”artificial colours, preservatives or additives.

In most western markets, delivering foods that meet this “natural”perception has become a basic requirement and influences researchagendas.

There are still many Asian markets – such as Thailand – where thistrend has yet to develop.

Foods that are “as natural as possible” - now a basic requirement

The “natural” trend is illustrated by the proliferationof “natural” sweeteners – Lo Han, Stevia and manyothers – which are expected to re-define thesweetener market over the next decade.

NEW NUTRITION BUSINESS

Only the very largest food companies – such as Nestlé, Danone, Unilever and PepsiCo – have the resources to invest significantly in areas such as nutrigenomics and metabolomics.

Despite the many claims made for the future potential of these technologies it is very clear from the companies whom we interview and from our customers’ own priority lists that the insights from this research are many years from being commercially available, except perhaps in a few medical foods.

Many senior executives describe this type of research as “speculative science”. With the exception of a very small number of companies of the size of Nestlé and Unilever, speculative science is losing favour among the senior managements of consumer goods companies, who in recent years have seen millions invested in such research with little commercial success to show for it.

Hence we have focused in this report only on the areas which have been clearly identified by companies as targets for commercialisation within the next 3-5 years.

Where is nutrigenomics on this list?

28

NEW NUTRITION BUSINESS

Seniors – the key “Nutrition Need”

29

NEW NUTRITION BUSINESS

It’s worth beginning by focusing on the broad Nutrition Need “seniors” (see Slide 9) because it is arguably the most important both in terms of its influence on R&D strategy and also in terms of its market impact.

The consumer need is clear and the opportunity is growing with the ageing population.

“Senior nutrition” is a term that encompasses a wide array of health benefits –and in fact almost every benefit area we identify in this report (see Slide 9) is one in which “seniors” form a large (even dominant) part of the potential target market.

What has also emerged very strongly is that seniors (taking as many companies do a definition of people over the age of 50) already are the single-largest group of buyers of products with health benefits.

In fact…

Finding a place in “senior” nutrition is the aim of every major food company

30

NEW NUTRITION BUSINESS

“Functional foods” = mature and senior consumers

31

NEW NUTRITION BUSINESS

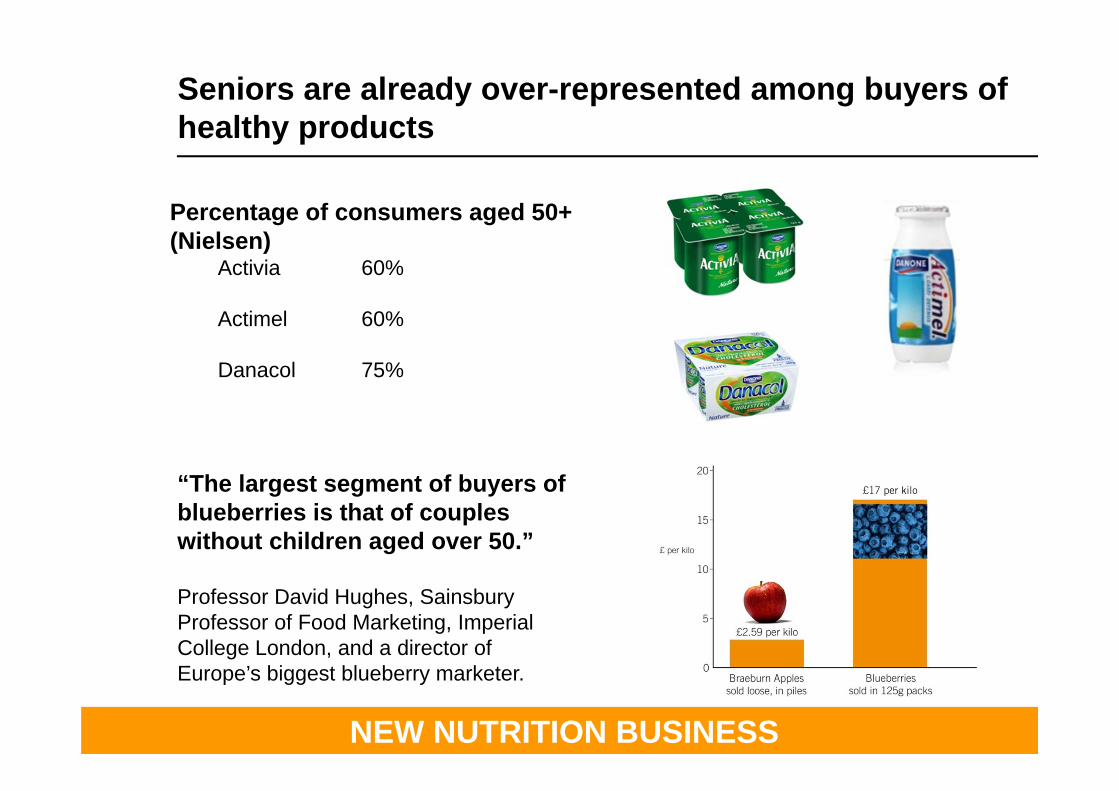

Percentage of consumers aged 50+ (Nielsen)

Activia 60%

Actimel 60%

Danacol 75%

Seniors are already over-represented among buyers of healthy products

“The largest segment of buyers of blueberries is that of couples without children aged over 50.”

Professor David Hughes, Sainsbury Professor of Food Marketing, Imperial College London, and a director of Europe’s biggest blueberry marketer.

NEW NUTRITION BUSINESS

Key learnings on Seniors

Life stage is key and the needs of seniors need to be carefully segmented. Here is an example of segmentation used by one company:

Boomers 50-60Young seniors 60-70Seniors 70-80Grand seniors 80+

Needs and attitudes are different at each stage:•Boomers – healthy and physically active•Young seniors and seniors – transitioning to more health issues•Grand seniors – fragile, illness

Most major companies’ research focus is on delivering more products – across a wide range of benefit platforms – that will appeal to one or more of the above segments.

In effect, seniors drive the food and health market and their needs to a large extent set the research agenda.

NEW NUTRITION BUSINESS

Source: Spire Research

Asia Pacific’s demographic transformation

22 2415

2330 30

16 1524 21 20

3746

24

50 5240

28 23

42 3831

4553

33

57 59

4337

30

48 4539>40

0102030405060708090

100

Japa

n

China

Sout

h Kor

ea

India

Sing

apor

eHon

gKon

gAus

tralia

Indo

nesia

Malays

ia Ta

iwan

Tha

iland

Total

Countries in Asia Pacific

Perc

enta

ge o

f pop

ulat

ion

aged

50

and

abov

e

2005 2030 2050

“Seniors” is no longer a future market: ageing populations are here now – even in Asia-Pacific

20% of Asia is >50 years old now, rising to 40% by 2030

NEW NUTRITION BUSINESS

Bringing together the best of medical nutrition with brand know-how

The 70-80+ age groups are an under-served opportunity and hence medical nutrition companies are increasing their focus on these segments, using the products and technologies they supply into the hospital and aged care home markets.

This is resulting in medicalised products moving into the pharmacy channel. An example is BeneVia, a range of nutritional drinks which is a joint venture between Danone Medical Nutrition and HealthSpan Solutions.

The range targets important health concerns for seniors, with each juice clinically proven to deliver active nutrients that help manage specific health issues: Strength & Energy, Heart Health, Memory & Focus, Immune Protect.

35

NEW NUTRITION BUSINESS

Cholesterol-lowering: brands now matter more than technologies

Many health benefit areas are already well-served and present few opportunities. One example is cardiovascular health.

Cholesterol-lowering and heart health is an example of a fairly mature and established market.

Effective technologies have been developed (there are around 10 suppliers of plant sterols/stanols to lower cholesterol for example) and the market’s development is now based on companies’ success with branding and distribution.

In Europe, for example, a €1 billion ($1.8 billion) market for cholesterol-lowering dairy products is controlled by just three brands – Danone’s Danacol, Unilever’s Pro.activ and Benecol – which between them have a 90% market share.

Market growth is limited – cholesterol-lowering is a niche concern – and hence most activity in the market is about fighting for market share. Growth comes from extending this niche proposition to new geographic markets, such as the launch of Benecol in Indonesia.

Brands and communications are what create points of difference – technology does not.

36

NEW NUTRITION BUSINESS

Cholesterol-lowering: brands matter more than technologies

An example is the performance in Italy – where 20% of the population is already over the age of 65 – of Danone’s Danacol cholesterol-lowering brand.

It earned €72.7 million ($120 million) in sales in 2009, a 28.8% increase (the Italian economy shrank 6%) and in 2010 grew another 10%.

This came despite being one of the most highly-priced items in the dairy cabinet.

37

NEW NUTRITION BUSINESS

Senior consumers dominate the health niches

Note that the core consumer for cholesterol-lowering brands such as Danacol is aged 55-64, with the second-biggest consumer group aged 65-74.

Attempts to widen the appeal of cardiovascular health groups to younger age groups have universally failed.

“The core consumer is 50+ with a very few in their forties. We have learnt over the last ten years that there is no interest in prevention among younger age groups.”Esther van Onselen, Marketing Manager, Benecol

MiniCol, a cholesterol-lowering cheese, marketed by Swiss dairy Emmi, also reports its consumers are mostly in the 55-64 age group and the second biggest group are 65-74. MiniCol has a repeat purchase rate of 86%.

NEW NUTRITION BUSINESS

Blood-pressure lowering: another niche

Beyond cholesterol-lowering, other benefit areas form even smaller niches.

An example is blood pressure lowering. The Evolus brand is based on patented technology that involves fermenting peptides with probiotics, developed by Valio of Finland and marketed there and also in Spain, Portugal, Switzerland and elsewhere by its partner Emmi Dairy. The technology is as effective as ACE inhibiting drugs.

Total sales of Evolus across four countries with a combined population of 65 million - €40 million ($71 million).

Core consumer is aged 65-74, second group 55-64.

Unilever entered this market in Europe and withdrew as salesvolumes were too low to be economic.

The Japanese market has stagnated for several years and is aniche led by Yakult.

Hence cardiovascular health is not high on most company’s R&D plans – it is a market of small niches which is already well-served.

39

NEW NUTRITION BUSINESS

Benefit platforms

40

NEW NUTRITION BUSINESS

1. Digestive

41

NEW NUTRITION BUSINESS

Digestive health

One of consumers’ top needs.

A huge and growing market – possibly the second-biggest functional market in the world. Mature in Europe, growth very strong in eastern Europe, Asia, South America.

Core consumer 40+ and may be older.

Probiotic dairy dominates (it is 100% of the figures shown here) and there is an embryonic effort to take probiotics into other categories (see Slide 99).

Biggest dairy brand is Danone Activia and 2nd-biggest Yakult (25% owned by Danone).

Fibre-fortified products are an emerging area, thanks to new technologies that have allowed higher dosages (>25% of the RDA) without taste and texture problems. .

2010 2011

€12bn ($21bn) €13.2bn ($23bn)

NEW NUTRITION BUSINESS

Over-40s (and particularly over-60s). Digestive health becomes a more important issue for people as they age. Bodily functions slow down with age and the digestive system is no exception.

Older people are five times more likely than younger people to develop constipation.

Around half of 70-year-old men struggle with constipation on a daily basis.

Look at demographics and the rapid aging of the baby-boomer cohort and it’s clear that the digestive health market will thrive as populations age.

The focus of many research programmes is a “more effective product” for older age groups.

The core consumers for digestive health

43

NEW NUTRITION BUSINESS

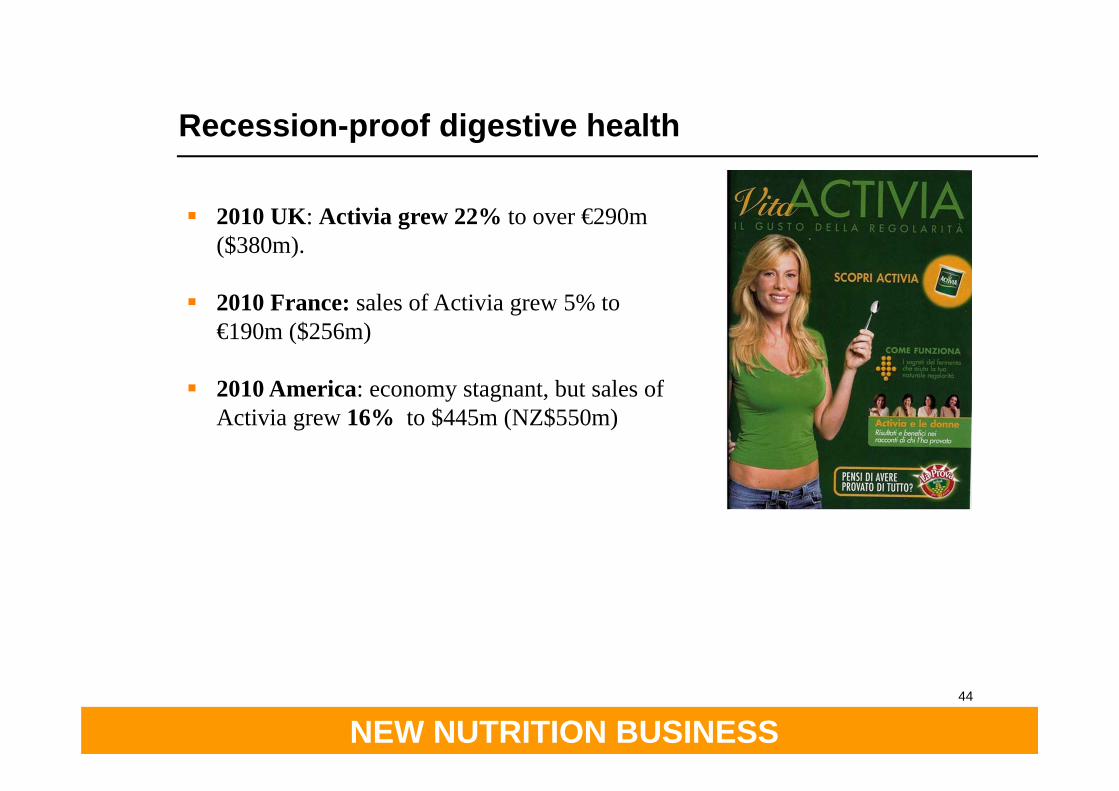

2010 UK: Activia grew 22% to over €290m ($380m).

2010 France: sales of Activia grew 5% to €190m ($256m)

2010 America: economy stagnant, but sales of Activia grew 16% to $445m (NZ$550m)

Recession-proof digestive health

44

NEW NUTRITION BUSINESS

Despite media attention to Danone Activia’s problems with its health claims, sales continue to increase, the result of a “feel the benefit” advantage, good taste and NPD – and its appeal to older consumers who have a real issue.

Recession proof digestive health

45

NEW NUTRITION BUSINESS

Not only probiotic brands have thrived. General Mills’ Fiber One brand is the “expert brand” in fibre – and despite a 50% price premium and America’s recession, in 2009 it grew 20% and in 2010 a further 10%.

Source: Infoscan Reviews, Information Resources, Inc. (IRI)

Digestive health – valuable to consumers even in a recession

46

NEW NUTRITION BUSINESS

2. Energy

47

NEW NUTRITION BUSINESS

Natural Energy

Energy is one of consumers’ top needs.

A huge and growing market – possibly the biggest ‘functional’ market in the world

Young and aggressive positioning dominates with the core consumer male aged 18-25 (80% of sales).

It is a white space opportunity for products which are more natural and/or aimed at older consumers and women.

The only major success in the white space has been in the US, where 5-Hour Energy, a single-serve 100ml energy shot for the over-35s, went from zero to $1bn in retail sales in four years. The brand is now more actively targeting the 60+ market.

2010 2011

€12.7bn ($22.4bn) €13.6bn ($24bn)

NEW NUTRITION BUSINESS

Natural Energy: the challenge

Research efforts are characterised by two approaches:

1. A dose that restores the status of vitamins and minerals linked to energy metabolism and/or tiredness.

2. A kick of stimulation – which is the primary consumer interest. But it is difficult to deliver the tangible effect without caffeine.

Many “natural” approaches that do not use caffeine have failed in the market, such as Ocean Spray’s Cranergy cranberry-based energy drink.

Hence some companies are now resorting to caffeine but in a “natural carrier”, such as fruit juice – an example is Nestlé’s Jamba Juice.

Creating an all-natural energy drink proposition is the “holy grail” of many beverage companies.

Note the cross-over with the “fruit and veg” category focus (see Slide 91).

NEW NUTRITION BUSINESS

3. Weight management

50

NEW NUTRITION BUSINESS

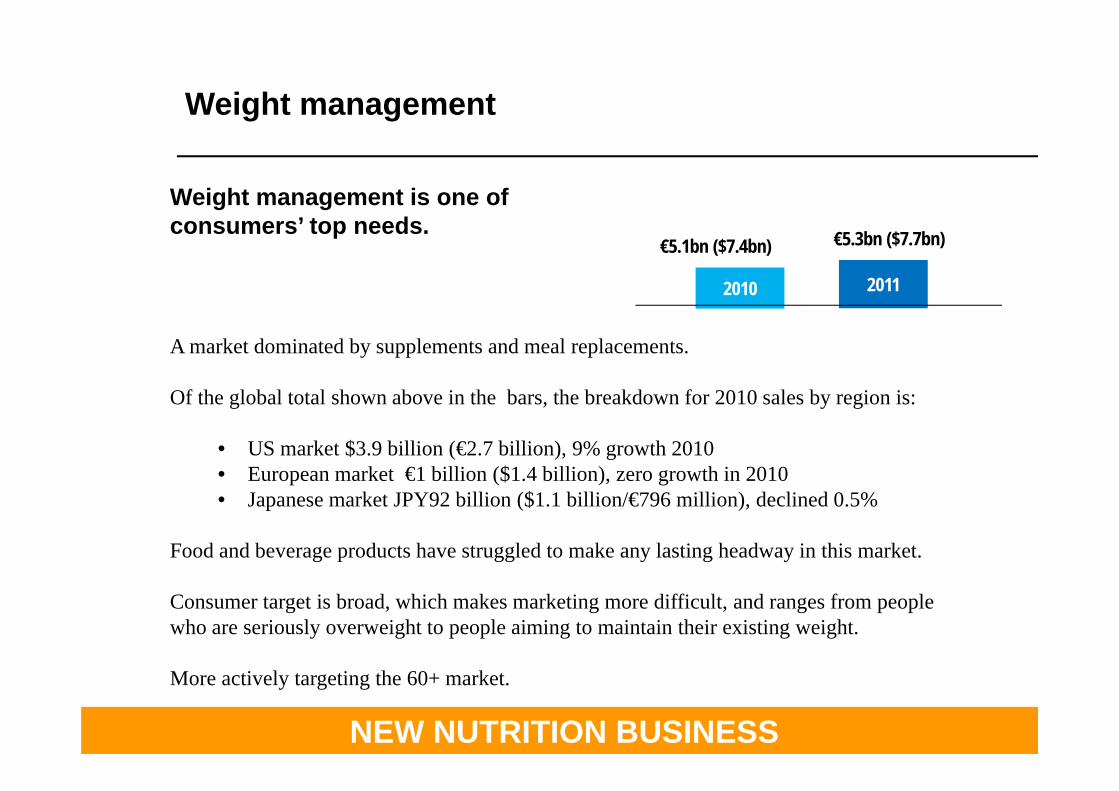

Weight management

Weight management is one of consumers’ top needs.

A market dominated by supplements and meal replacements.

Of the global total shown above in the bars, the breakdown for 2010 sales by region is:

• US market $3.9 billion (€2.7 billion), 9% growth 2010• European market €1 billion ($1.4 billion), zero growth in 2010• Japanese market JPY92 billion ($1.1 billion/€796 million), declined 0.5%

Food and beverage products have struggled to make any lasting headway in this market.

Consumer target is broad, which makes marketing more difficult, and ranges from people who are seriously overweight to people aiming to maintain their existing weight.

More actively targeting the 60+ market.

2010 2011

€5.1bn ($7.4bn) €5.3bn ($7.7bn)

NEW NUTRITION BUSINESS

The world’s most-successful weight management brand

Kellogg’s Special K is not the product of science or R&D but of marketing innovation.

Its “drop a jeans size” and “drop a bikini size” introduced in the US and France in 2001 are not clever grains, but clever positioning of the benefit.

Since rolled out to 33 countries: brand has grown from $300m (NZ$370m) in 2001 to $1.5bn (NZ$1.85bn) in retail sales by 2010. 52

NEW NUTRITION BUSINESS

The dairy industry’s favoured strategy of fibre+whey protein combinations for weight management (from satiety) has failed.

Spain: one of Europe’s most-active weight management markets, Danone Vital Vitalinea SatisfAcción 0% fat yoghurt stalled at €7m (NZ$12.4m) despite a clear “helps to control the appetite for longer” claim and marketing spend of €5m (NZ$8.8m).Elsewhere brand withdrawn.

US: Kellogg Special K dairy satiety drink “providing protein and fiber to satisfy hunger for longer” stalled.

Slim-Fast hunger shot (protein and fibre) withdrawn.

Weight management dairy brands have mostly failed…

53

NEW NUTRITION BUSINESS

Most dairy satiety brands that have been launched in Europe and US have been withdrawn or linger in niches.

Partly because protein and fibre products as presently formulated do not enable people to “feel the benefit” sufficiently.

The lessons: major companies realise that a single product on the shelf is not enough consumers are skeptical about a single-product, “magic-bullet” approach people want service and support

Researchers are faced with the question of how to address this problem. So where to look for inspiration?

Why is dairy in weight management not doing well?

54

NEW NUTRITION BUSINESS

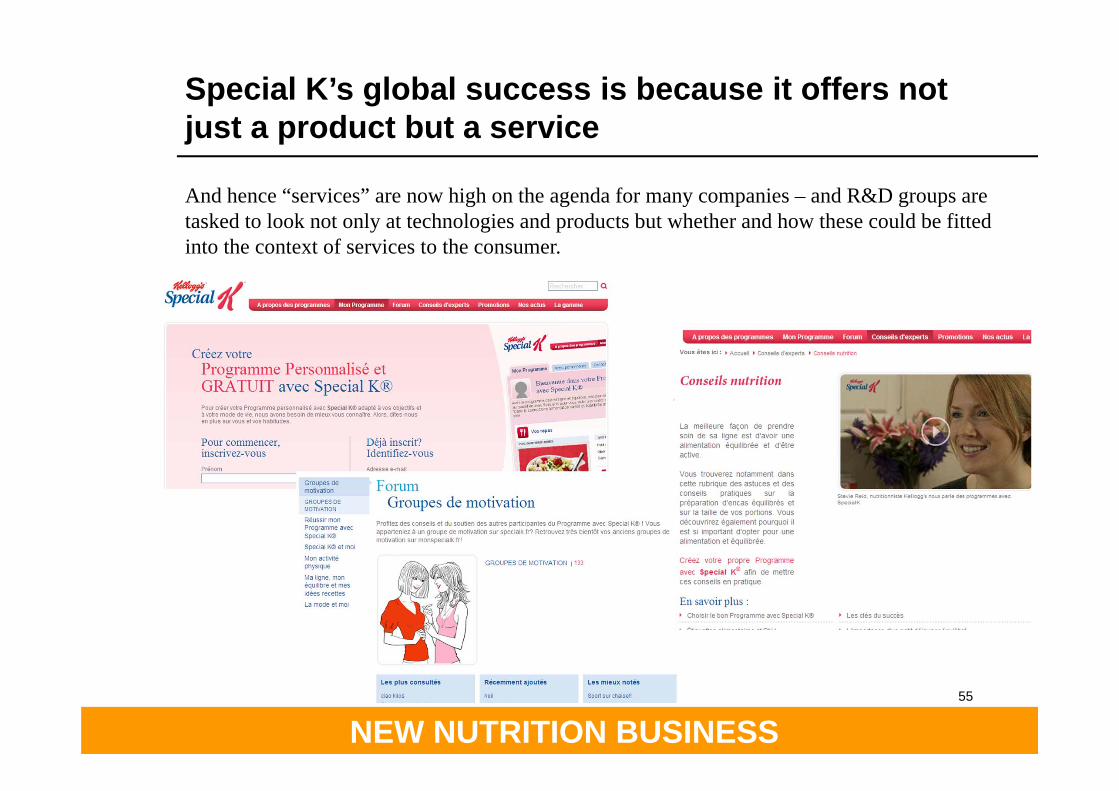

Special K’s global success is because it offers not just a product but a service

55

And hence “services” are now high on the agenda for many companies – and R&D groups are tasked to look not only at technologies and products but whether and how these could be fitted into the context of services to the consumer.

NEW NUTRITION BUSINESS

No accident that Nestlé acquired Jenny Craig– a service with products

Elements of weight management service

Smart devices and tools –enable people to stay connected and get help anywhere anytime

Community – sharing the experience with others

Coaching - help me as an individual

Help me track progress

Customised to my needs and lifestyle

Make eating pleasurable

NEW NUTRITION BUSINESS

4. Mobility

57

NEW NUTRITION BUSINESS

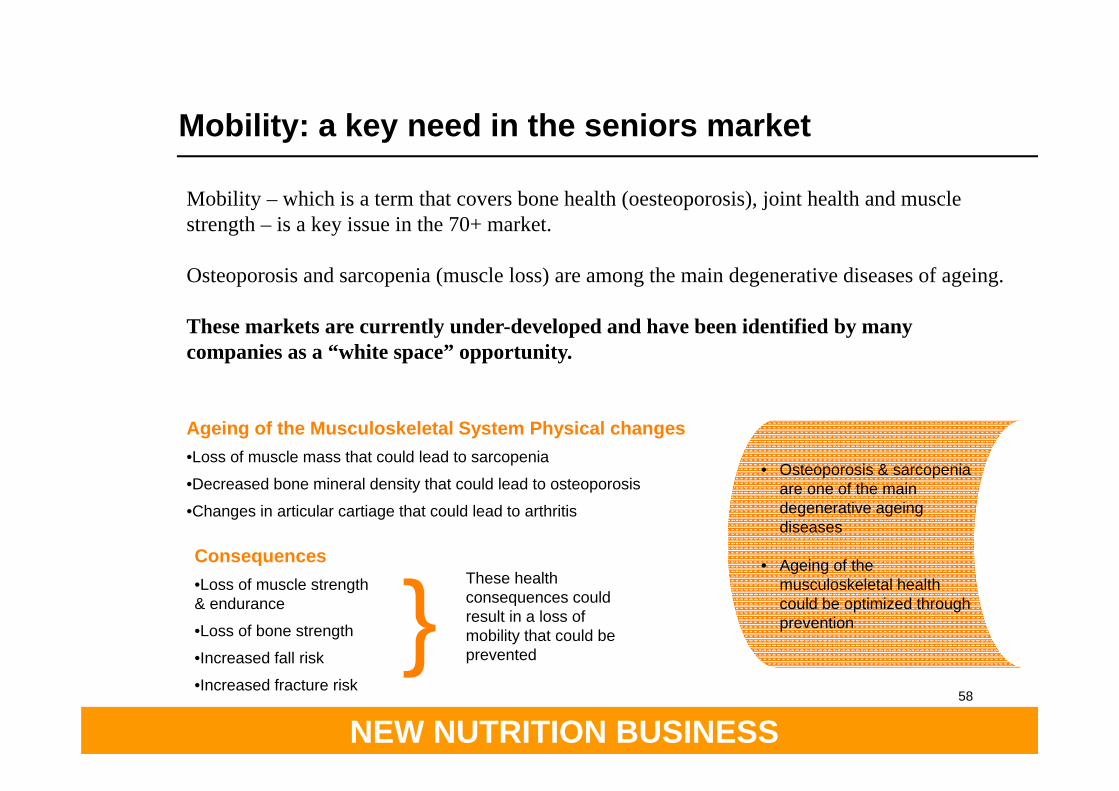

Mobility – which is a term that covers bone health (oesteoporosis), joint health and muscle strength – is a key issue in the 70+ market.

Osteoporosis and sarcopenia (muscle loss) are among the main degenerative diseases of ageing.

These markets are currently under-developed and have been identified by many companies as a “white space” opportunity.

Mobility: a key need in the seniors market

58

Ageing of the Musculoskeletal System Physical changes•Loss of muscle mass that could lead to sarcopenia

•Decreased bone mineral density that could lead to osteoporosis

•Changes in articular cartiage that could lead to arthritis

Consequences•Loss of muscle strength & endurance

•Loss of bone strength

•Increased fall risk

•Increased fracture risk

}These health consequences could result in a loss of mobility that could be prevented

• Osteoporosis & sarcopeniaare one of the main degenerative ageing diseases

• Ageing of the musculoskeletal health could be optimized through prevention

NEW NUTRITION BUSINESS59

Sarcopenia – or muscle wastage – is a condition that affects everybody to a greater or lesser extent as they age.

Loss of muscle strength and endurance•Tire more quickly•Loss of bone strength•Increased fall risk

A health problem that threatens to reach epidemic proportions. Sarcopenia afflicts:•15% of men aged 70, 25% of women aged 70•20% of men aged 75, 33% of women•More than 50% of people over the age of 80

Your ability to assimilate protein shrinks markedly after the age of 50. Someone in their 20s, if they eat whey protein or beef protein, will get as much benefit from either. Someone in their 60s will get almost 100% of the protein from whey protein, because it’s easily absorbed. But they’ll probably get only about 60% of the benefit of eating the protein from beef.

Sarcopenia – muscle strength and independence

NEW NUTRITION BUSINESS60

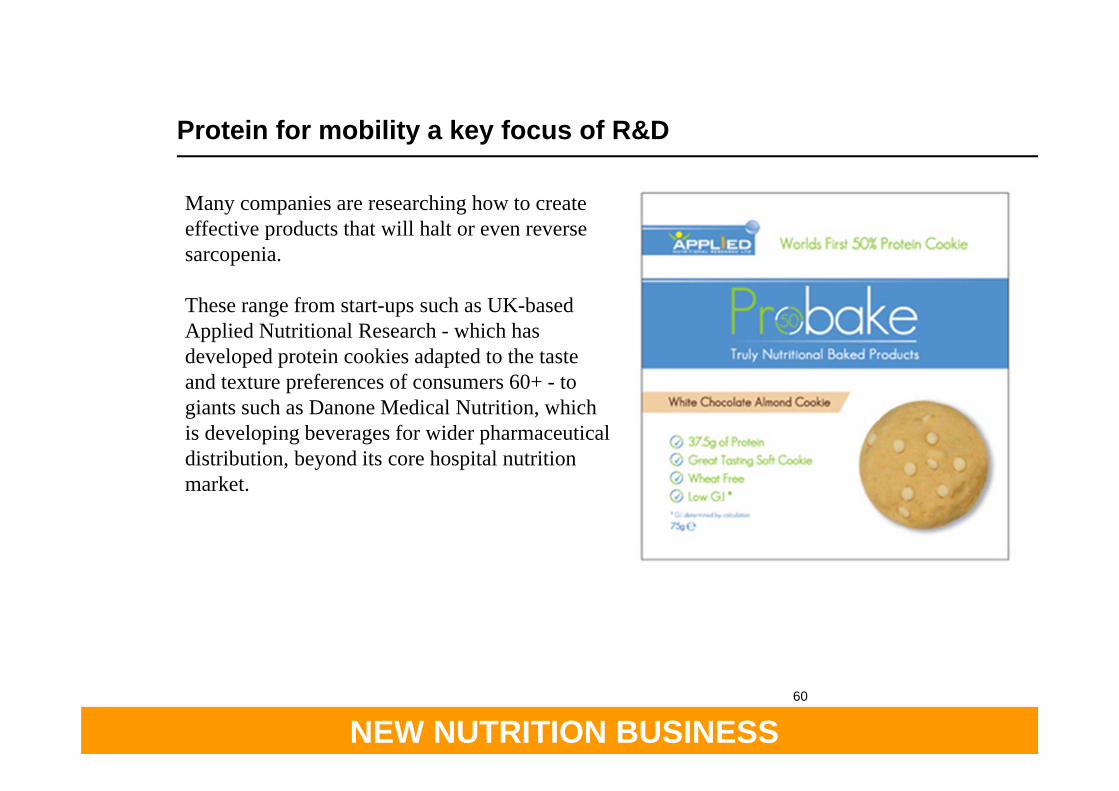

Protein for mobility a key focus of R&D

Many companies are researching how to create effective products that will halt or even reverse sarcopenia.

These range from start-ups such as UK-based Applied Nutritional Research - which has developed protein cookies adapted to the taste and texture preferences of consumers 60+ - to giants such as Danone Medical Nutrition, which is developing beverages for wider pharmaceutical distribution, beyond its core hospital nutrition market.

NEW NUTRITION BUSINESS

The bone health segment of “mobility”

Fonterra’s Anlene brand (which offers 4x as much calcium per serve as regular milk) specifically targets “movement”as its benefit.

Focused on a bone health=active lifestyle message, with clinical studies to prove the benefit, Anlene targets women 40+ (biggest consumers 50+).

It is the number one bone health brand in Asia, with market share of 70% in Malaysia, 50% in Indonesia and elsewhere.

NEW NUTRITION BUSINESS

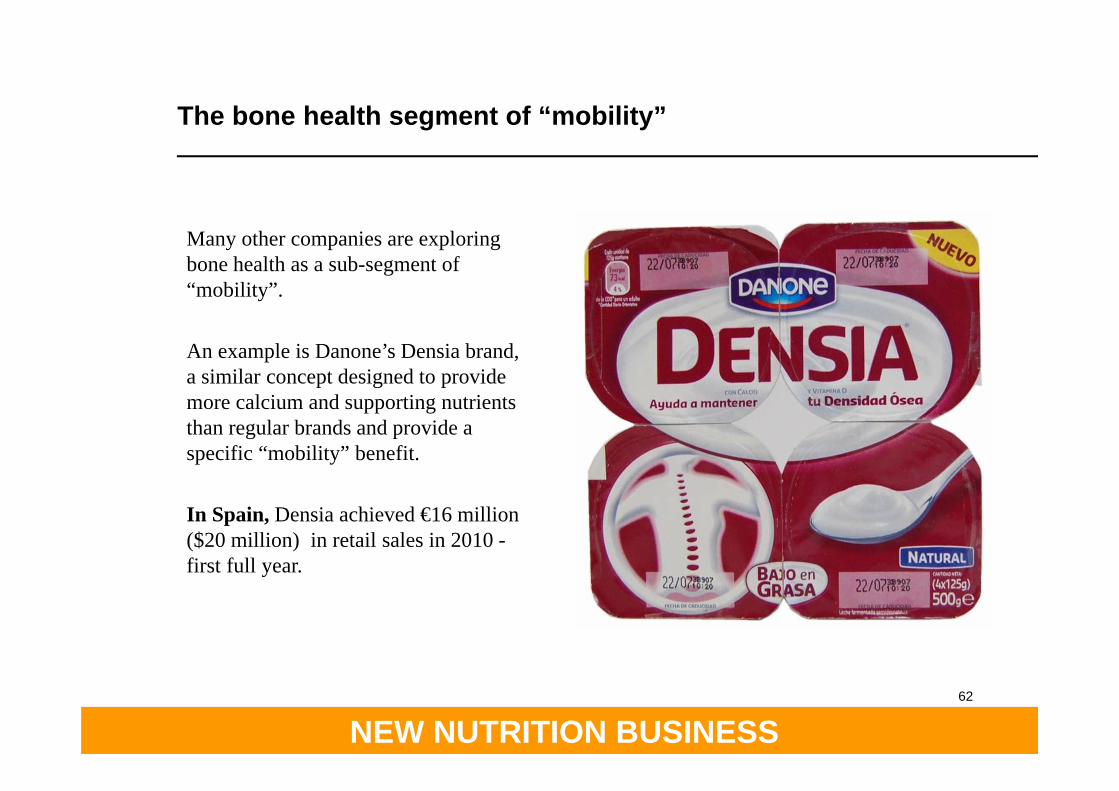

Many other companies are exploring bone health as a sub-segment of “mobility”.

An example is Danone’s Densia brand, a similar concept designed to provide more calcium and supporting nutrients than regular brands and provide a specific “mobility” benefit.

In Spain, Densia achieved €16 million ($20 million) in retail sales in 2010 -first full year.

62

The bone health segment of “mobility”

NEW NUTRITION BUSINESS

Joint health – based on ingredients such as glucosamine and chondroitin – is another important sub-segment of mobility.

Beverage formats account for 15% of the US joint health supplement business overall - retail sales of supplement pills are valued at $900 million ($1.1bn).

“One hundred per cent of the growth in this broad category in 2009 came from beverages.”

Elations is the leading beverage, with sales of $85 million ($105 million) in 2010. Its advantage, according to VP of marketing Mike Burton, is that:

Boomers don’t like to take pills – that’s something that always has been associated with getting old and sick, and they don’t want to feel old or sick, especially when they’re only in their 40s and 50s. They view themselves as much more active and able to continue with their lives than people of their age a few generations ago, and a beverage fits better into their overall lifestyle.

Elations is a beverage sold under supplement regulation in the US and based on a technology originally developed by Procter & Gamble.

The joint health segment of mobility: and a supplement/beverage cross-over

63

NEW NUTRITION BUSINESS

5. Cognitive

64

NEW NUTRITION BUSINESS

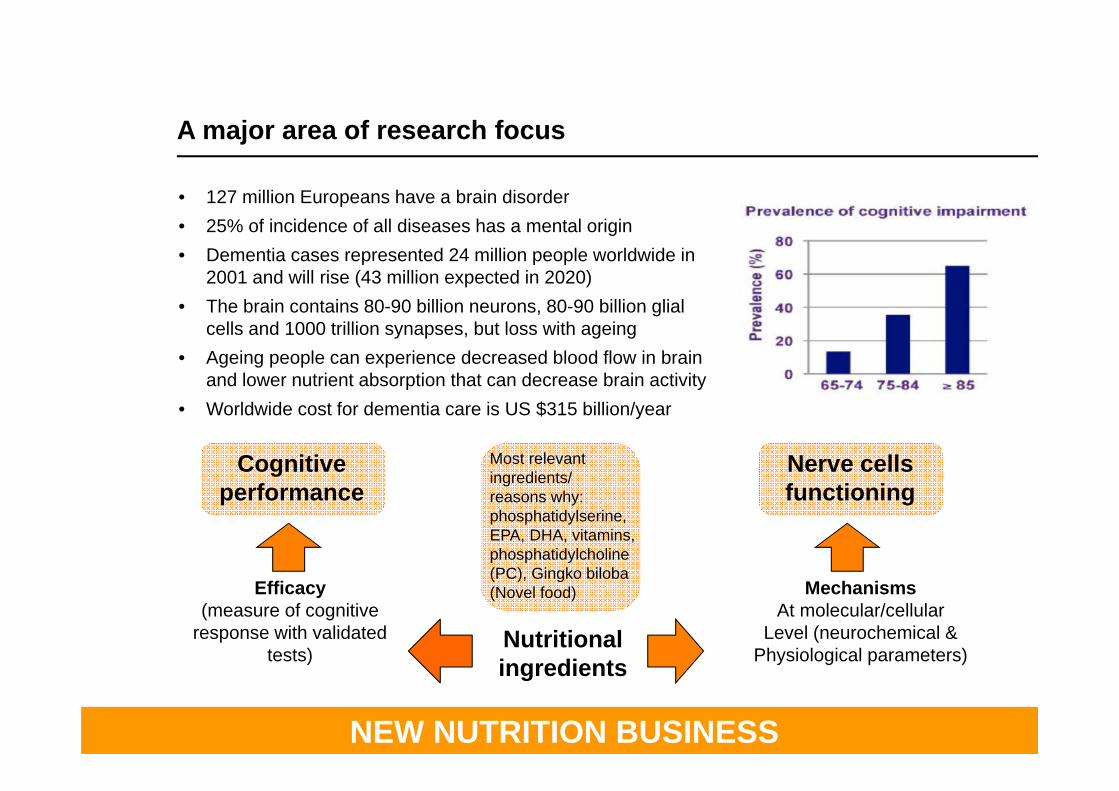

A major area of research focus

• 127 million Europeans have a brain disorder• 25% of incidence of all diseases has a mental origin• Dementia cases represented 24 million people worldwide in

2001 and will rise (43 million expected in 2020)• The brain contains 80-90 billion neurons, 80-90 billion glial

cells and 1000 trillion synapses, but loss with ageing• Ageing people can experience decreased blood flow in brain

and lower nutrient absorption that can decrease brain activity• Worldwide cost for dementia care is US $315 billion/year

Cognitiveperformance

Efficacy(measure of cognitive

response with validated tests)

Most relevant ingredients/ reasons why: phosphatidylserine, EPA, DHA, vitamins, phosphatidylcholine (PC), Gingko biloba (Novel food)

Nutritionalingredients

Nerve cellsfunctioning

MechanismsAt molecular/cellular

Level (neurochemical &Physiological parameters)

NEW NUTRITION BUSINESS66

A white space opportunity

Cognitive health is still in its early stages with no credible products currently on the market and it is seen as a “white space” opportunity.

Many companies are focused on trying to create technology which is effective and, when delivered in a food or beverage format, is credible to consumers.

Medical nutrition companies such as Nestlé, Novartis, Abbott and Danone are all investing in this area and are likely to create the market through their access to pharmaceutical distribution.

Danone is likely to be first to market, with a brand called Souvenaid, which is based on a patented combination of ingredients developed at MIT, Massachussets and which has been clinically shown to reverse the symptoms of Alzheimers disease.

NEW NUTRITION BUSINESS

6. Diabetes

67

NEW NUTRITION BUSINESS

As with cognitive health it is a “white space” market opportunity with no credible products to help people with diabetes in mass market distribution.

Diabetes is a major public health concern:•More than 300 million people worldwide have pre-diabetes•More than 280 million people worldwide have diabetes•380 million people are expected to have diabetes by 2025

The factors that are driving its increase are:•An ageing population•Sedentary lifestyles•Dietary choices•Overweight and obesity

Diabetics have a higher incidence of heart attacks and stroke.

Approaches such as low GI/GL have proven to have limited appeal to the medical community or consumers except in Australia.

Why diabetes?

NEW NUTRITION BUSINESS

3. The daily struggle of Blood Sugar Management

2. Nutrition is part of the therapy1. Chronic disease with long term complications

c

Why diabetes?

NEW NUTRITION BUSINESS

7. Antioxidants

70

NEW NUTRITION BUSINESS71

A challenging area

• Not quite a benefit: strictly speaking, we should not categoriseantioxidants as a “benefit”, since they are not a benefit sought by consumers in the same sense as “weight management”or “digestive health”. However, consumers infer a “protection” benefit from the presence of antioxidants and because antioxidants and their potential protection benefits are high on most companies’ research agenda, we have included antioxidants here.

• An implied benefit: The high antioxidant content marketing message is not a direct benefit message but an ingredient statement, with the benefits implied. Consumers are free to interpret this as meaning what they want it to mean to them, individually. It has worked because consumers perceive antioxidants as something healthy to include in the diet and the many possible benefits of antioxidants are being actively communicated by the media.

• Research driven by regulation threat: fuelled by the often questionable science underpinning the usage of antioxidant marketing messages, regulators in Europe and the US are training their guns on antioxidants. Europe’s rigorous new health claims system has rejected every antioxidant-based claim that has come before it. The need to better substantiate benefits has become a driver of R&D activity.

NEW NUTRITION BUSINESS72

Liz Read, company nutritionist at Nestlé, which markets the Nescafé Green Blend antioxidant-rich coffee brand said she was not surprised by the raft of negative opinions issued:

“It was likely to happen because of the state that general antioxidant research is in at the moment. The research we’ve got for the epidemiological effects of foods that contain antioxidants is really good, but we probably need another 10 years to get it into the state of, say, polyunsaturates and fibre.”

Proving the benefits of antioxidants in the body will be a challenge, Read adds:

“You have to show first of all that it is absorbed by the body so it’s bio-available, secondly that it is then having an effect on the cells in the body, and thirdly that these are definitely antioxidant effects. It’s a case of joining the dots.”

Regulators’ sights set on antioxdants

NEW NUTRITION BUSINESS73

Many marketers love the term “antioxidants”.

Recent years have seen a frenzy of interest in using terms such as “high in antioxidants” on product labels and in advertising.

However, the antioxidant frenzy seems to have passed its peak – and with marketing, regulatory and scientific challenges mounting, the use of the marketing term “antioxidants”will only be effective only in niches where it is delivered by innovative products supported by excellent marketing execution and by strong science.

Nestlé’s high antioxidant green coffee is a perfect example of successful brand creation in the antioxidant space. It provides a health benefit in a natural and convenient form – in some countries advertising emphasizes that “we’ve returned to nature”; provides a first-in-its-category product that offers a healthy alternative to green tea; it’s delivered in an eye-catching package that’s unlike anything else on the coffee shelf, and it retails at a premium price.

A message loved by marketers

NEW NUTRITION BUSINESS74

Pom Wonderful pomegranate juice’s success rested on: leveraging the benefits and healthy image of fruit; offering a previously inconvenient fruit in a convenient-and-natural form; delivering a premium product in innovative packaging. Pom’s appeal, like that of many “high antioxidant” products, has been niche not mass.

“Antioxidants” success has been driven by more factors than most marketers realise

NEW NUTRITION BUSINESS75

Read says one way to avoid the ‘antioxidants’conundrum would be to use the term ‘polyphenols’instead – and indeed Nestlé does do so in advertising and labelling for Nescafé Green Blend. But she admits: “We could say polyphenols but consumers don’t yet understand what polyphenols are. The word antioxidants is well understood by consumers.”

Nestlé, as one of the world’s biggest food companies, has deep pockets and can well afford to conduct the necessary proprietary research.

Smaller companies may not be in such a fortunate position and it is possible that the term “antioxidant” might become one that only the largest companies can afford to use.

Regulators’ sights set on antioxdants

NEW NUTRITION BUSINESS76

Research into individual food component’s benefits tend to be driven by the companies with the biggest commercial interest in that food component.

Cocoa’s flavonol content and benefits, for example, have been extensively researched by both Mars and Hershey, as well as by Barry Callebaut, the biggest supplier of cocoa as an ingredient.

Research agendas driven by specific competences

Mars has made the biggest investment and the company experiments with new product forms (supplements and beverages and snacks), new ways of delivering benefits and new brands. Many of Mars’ test concepts may have been withdrawn, but it is clear that they are providing the company with a wealth of lessons that it can apply successfully in the future.

NEW NUTRITION BUSINESS77

Confectionery giant Hershey has also attempted to leverage the antioxidant-rich qualities of cocoa in a number of forms, including a protein-based sports beverage called “reGen.” The brand is currently on test-market in 26 sporting goods stores in Hershey’s home state of Pennsylvania.

Efforts to create more acceptance: cocoa + protein

NEW NUTRITION BUSINESS

Nutrition needs

78

NEW NUTRITION BUSINESS

Sports

79

NEW NUTRITION BUSINESS

Sports Nutrition

In addition to the “seniors” opportunity already discussed, the area of “sports nutrition”is high on many companies’ research agendas, with a particular focus on exploring how to broaden its appeal from a niche market.

Currently the sports area is a sizeable market with two segments:

1. Protein/carbohydrate-based products:- Global market value: $4.2 bn ($5.2bn)- Biggest market US: $2.5 bn ($3.1bn)

2. Hydration (water-based products):- Gatorade global sales €3.75 bn ($6.7bn)- European sports drinks > €1.75 bn ($3bn)- Leaders: Lucozade (GSK), Powerade (Coca Cola), Gatorade (PepsiCo).

The sports nutrition segment currently is very male-focused and the opportunities that have been identified are to increase the appeal to women and to take sports products to a more “healthy lifestyle” positioning.

The market also lacks natural solutions.

NEW NUTRITION BUSINESS

“The typical tired approach from male-led brands looking to appeal to women is ‘change the portion size and put pink on the label.’ Women are the undermet need in the market-place. The number of women who work out is greater than that of men, and all of the products catering to them are afterthoughts or re-positionings from an ill-fitting male parent brand.”Source: Anthony Almada, Genr8, sports nutrition formulation house

“Many women feel patronised by products which are labelled “for women” and feature pink in the design. They are also alienated by very male products which pretend to be female –they are ‘transvestite brands’.”Source: consumer researcher

The “muscle image” is wrong for the target market

NEW NUTRITION BUSINESS

“You’ve got retailers requesting that we help take products off the shelf featuring very veiny guys and replace them with products that are more natural and approachable, especially for women.

“Veiny guys are only 2% of the population, and existing sports-nutrition products aren’t meant for the mainstream markets that retailers are trying to attract.”

Opportunity 1: Women

Companies are focusing on creating:

•Products that can be used before, during and after sport.•Delivering doses of vitamins and minerals through fruits & dairy•Delivering doses of protein•Products that are low in fat and calories

NEW NUTRITION BUSINESS

“Natural flavours and colours in products are key for European consumers if sports products are to make any headway in the wider lifestyle market.”

In US and Europe Gatorade now offers “natural” versions of its products with natural colours, flavours and ingredients.

“And we have removed high-fructose corn syrup from all products because it is a barrier to purchase for some athletes and also some sideline mothers buying for their kids.”

Source: Gatorade

Opportunity 2. Natural

NEW NUTRITION BUSINESS

There is also a significant overlap with the fruits and vegetables category (see Slide 91) – either as carriers for sports benefits (as an alternative to dairy) or ideally to provide intrinsic and all-natural sports benefits.

Marketing the intrinsic health benefit of beetroot. Studies published in the Journal of Applied Physiology showed for the first time that drinking beetroot juice can boost stamina, allowing an individual to exercise for up to 16% longer.

Name - Beet It Stamina Shot - intended to appeal to sports market.

“We’re now supplying international rugby teams, premiership football teams and athletes as well as ballet and dance schools. Word of mouth has been very powerful.”

Opportunity 2. Natural

NEW NUTRITION BUSINESS

Categories

85

NEW NUTRITION BUSINESS86

The three categories of strategic growth focus

Source: PepsiCo

There seems to be a consensus on which categories provide the best platforms for health benefits and these are neatly summarised in the strategy focus statement (below) from PepsiCo, which has made these three the pillars of its future growth.

Few companies operate in more than one of these categories. A few, such as Danone, have recently extended to operating in two of them.

NEW NUTRITION BUSINESS87

The three categories of strategic growth focus

Fruits and vegetables are seen as the highest-growth opportunity – not fresh products but juices, snacks and other convenient forms. There are still many opportunities to create new brands and new segments of the market with fruit and vegetable-based products.

Dairy still has significant growth potential, both for ingredients and for new brands.

Whole grains are seen as the lowest-growth opportunity of the three – largely because of the difficulty in delivering grain benefits in forms that are both good-tasting and convenient. Most innovation in this area is connected to renovating existing products rather than creating new brands.

NEW NUTRITION BUSINESS

Dairy

88

NEW NUTRITION BUSINESS89

Dairy has become, in most markets, the category which consumers accept most as a carrier for health benefits.

This has been driven by:

Thirty years of R&D by the dairy industry to understand every component of dairy and its health benefits and what can be added to dairy to deliver a health benefit. The dairy industry’s R&D investment overshadows that of any other category.

Vigorous marketing worldwide of dairy products with health benefits has helped create some high-profile brands and has built consumer identification of dairy with health benefits.

Dairy has a “naturally healthy” and “natural” image.

Dairy’s dominance

NEW NUTRITION BUSINESS90

In some areas dairy now “owns” certain benefits – such as probiotics for digestive health and cholesterol-lowering – meaning that the category’s association with those benefits is strongest in the mind of the consumer, making it difficult for any other category to mount a credible challenge.

As a result even companies such as PepsiCo have realised that it needs to make dairy – an area where that company has no historic competence of any kind – a key part of its strategy.

Dairy’s dominance

NEW NUTRITION BUSINESS

Fruits and vegetables

91

NEW NUTRITION BUSINESS92

In all categories, strong trend towards consumers wanting health benefits that are as natural as possible.

Fruit’s advantages:Seen by health-conscious consumers as one of the few things they can eat as an indulgence without feeling any guilt.

Has a halo of health, made brighter all the time by media eager for simple and positive stories about healthy eating.

Scientific research into the benefits of fruit is at an early stage. The science of fruit is today where the science of dairy nutrition was 20 years ago.

Fruit’s natural advantage

NEW NUTRITION BUSINESS

93

Plus vegetables

Vegetables in convenient formats are also getting more attention

Adding vegetables to beverages, for example, can reduce the number of calories without sacrificing texture or taste. Adding vegetables to fruit juice can significantly lower calorific value.

“A helping of food that was either 15% or 25% vegetable by weight, although the vegetables could not be seen or tasted, those who were eating the altered foods saw their calorie intake drop substantially—as much as 360 calories a day—at the same time their vegetable intake rose. The researchers concluded that “this strategy can lead to substantial reductions in energy intakes and increases in vegetable intakes.”

Source: American Journal of Clinical Nutrition

Vegetable taste issues can be overcome – hence the success of fruit and vegetable juice in Japan and V8 fruit plus vegetable drink in the US

NEW NUTRITION BUSINESS

Very little human clinical evidence for the benefits provided by individual fruit or vegetables or their components

Just 127 studies on more than 50 fruits out of 487 total studies. Many fruits have no human studies

Lots of ‘soft’ data based on in vitro and in vivo small animal trials

Scientific controversy about exactly how antioxidants work is not helpful

But the research needs are high

94

NEW NUTRITION BUSINESS

EATING FRUIT & VEG TOP ACTION CONSUMERS TAKE TO IMPROVE HEALTH

HEALTH

Why Fruits & Veg key for health?

CONVENIENCE IS A KEY DRIVERFRUIT & VEG = THE INHERENT HEALTH FOOD

WORLDWIDE DEFICIENCY IN FRUIT & VEG INTAKE

• European Fruits &Veg intake dropped by 14% 2004 – 2009

• 80% want to eat more, 20% do it !

SpecificWell Being

Antioxidant

CancerUrinary tract

Vitamins

EnergyWeight

NEW NUTRITION BUSINESS

Success is usually the result of bringing together good science and good marketing

Very few fruit or vegetables have made strong associations with particular health benefits – and the produce industry has not been responsible for any market successes or any significant R&D initiatives.

The strongest associations result from beverage marketers leveraging science:

Cranberry: Investment in science enabled Ocean Spray to understand its benefits in fighting urinary tract infections (health claim approved in France) and turn it into the original superfruit.

Pomegranate: Investment in science of its cardiovascular benefits enabled Paramount Farms to create the Pom Wonderful brand.

96

NEW NUTRITION BUSINESS

Consumers are very receptive to learning about new benefits that are natural and intrinsic to fruit

Consumers are very receptive to learning about new benefits and are willing to believe new, positive messages about natural and intrinsic health benefits.

Cherries and sports performance

Beetroot and blood pressure

Cranberry and urinary tract infections(new message in France in 2004)

You do not need to wait for consumers to tell you what benefits they want from which fruit or vegetables. The opportunity is to educate them about benefits.

97

NEW NUTRITION BUSINESS

PepsiCo has made “fruits and vegetables” one of its core platforms for growth (along with “dairy” and “whole grains”)

Danone has acquired global rights to the ProViva brand and technology.

Danone and Chiquita have formed a partnership to jointly build a new business in fruit drinks and fruit snacks.

Danone quietly acquiring fruit drink companies.

Nestlé working on making fruit a core business platform in selected markets.

Success of fruit and vegetable juices in Japan and Campbell’s V8 veg+fruit juice brand has prompted a move by many companies to also capitalise on vegetable’s halo of health.

Fruit and vegetable – increasingly a strategic focus

NEW NUTRITION BUSINESS

Faced with the fact that probiotic dairy for digestive health is now dominated by a few leading brands, some companies are looking to create new categories.

An example is how Danone is leveraging the intrinsically healthy image of fruit to create probiotic fruit juice

ProViva, launched in Sweden in 1994, has shown how successful probiotic fruit juice can be even in a country –Sweden – which has a very high per capita consumption of dairy products and in which lactose intolerance is rare.

Bacteria is L. plantarum 299v, very strong clinical evidence base.

Annual retail sales of 25 million litres, worth over $50m (NZ$62m), in a country with a population of just 9.1 million.

Fruit – a carrier for new health benefits

99

NEW NUTRITION BUSINESS

ProViva sales 1994-2009

100

NEW NUTRITION BUSINESS

Danone has signed a 10-year license agreement with Swedish probiotic science company Probi – which developed the active ingredient in ProViva – which allows Danone to use Probi’s technology in probiotic fruit drinks for digestive health.

Danone also acquired 51% of the ProViva brand – which sets the stage for a global roll-out of a brand which is one of the most innovative and successful of the past decade.

ProViva’s success factors:1.A clinically-proven digestive health benefit that you can quickly feel2.An innovative and truly differentiated product3.Taste so good that by itself it’s a reason for people to buy the product has attracted a huge following even in a country that’s traditionally highly dairy-focused. 4.A long-term view of building success

Juice: the next digestive health growth opportunity

101

NEW NUTRITION BUSINESS

Whole grains

102

NEW NUTRITION BUSINESS103

Grains: natural advantages but convenience challenge

Grains benefit from a perception of being “all-natural” and least-processed. As a result, even highly-processed grain-based foods, such as breakfast cereals, have a strong naturally healthy image in consumers’ minds in many markets.

While there has been significant investment in building a health benefit platform for some grains, such as oats, these efforts have not always been enduringly successful. Sales of oats, for example, are stagnant in the US market after a few years of growth in the early part of this decade. On the other hand, sales of oats are growing very strongly in Asian markets, where they have the advantage of being a “new and innovative” food.

Grains are a credible carrier for benefits such as digestive health and whole grains have created a positive association with heart health.

However, the delivery forms for grains’ benefits do not have the convenience advantages enjoyed by dairy and fruit drinks. Health-enhanced breads, for example, perform poorly in the market-place, while health-enhanced pastas have just a 5% share of the US pasta market (for example), which is the market where they have been most successful.

NEW NUTRITION BUSINESS

Systems

104

NEW NUTRITION BUSINESS

Asked to list his R&D priorities, the VP of R&D at one of the world’s largest companies replied: “Packaging has to be number one.”

The reason is that packaging innovation is increasingly recognised as core to many of the successes in the business of food and health.

Packaging makes it possible to:•deliver (and protect) new ingredients •create controlled doses (such as Yakult-style daily dose products)•achieve strong differentiation on the shelf (as the Pom Wonderful bottle demonstrates) which is essential for products wanting to be noticed by consumers in today’s crowded supermarket•achieve premium prices and higher margins

1. Packaging

105

NEW NUTRITION BUSINESS

As already discussed in the section on weight management, it has become clear to many companies that in areas such as weight management, diabetes, sports nutrition and senior nutrition, offering a service as well as a product is an opportunity for competitive advantage.

A wide variety of services are undergoing test-marketing. One example is Nestlé HomeCare, which operates in France, which provides at-home nutritional support for people who have come out of hospital, delivering foods direct to their homes, providing care by health professionals, etc.. If successful the concept will be rolled out to other markets.

2. Services

106

NEW NUTRITION BUSINESS

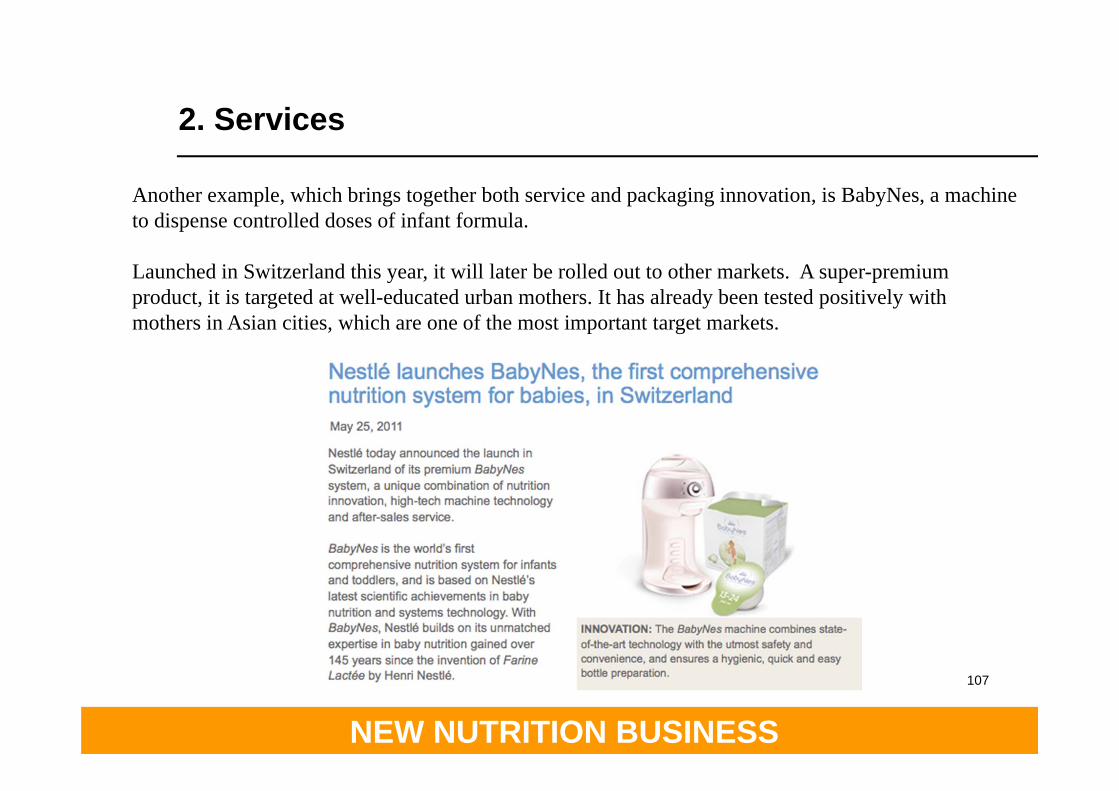

Another example, which brings together both service and packaging innovation, is BabyNes, a machine to dispense controlled doses of infant formula.

Launched in Switzerland this year, it will later be rolled out to other markets. A super-premium product, it is targeted at well-educated urban mothers. It has already been tested positively with mothers in Asian cities, which are one of the most important target markets.

2. Services

107

NEW NUTRITION BUSINESS

2. R&D trends – ingredient companies

16

NEW NUTRITION BUSINESS

The R&D agenda is broad

109

Research at the ingredient supplier level – a term we use here in a broad sense to cover both major diversified ingredient groups (such as DSM) as well as small start-ups investing in R&D around perhaps a singe ingredient or compound – is driven by a number of factors:

1. Success of their technologies is strongly determined by the R&D priorities of the consumer goods companies, who are their customers.

2. Yet many companies’ strategy is determined by “technology push” – which means identifying an active, building a basis of clinical evidence for it and then ”pushing” this active to the consumer goods companies for them to include in their products.

3. The benefit platform chosen for many actives is often – inevitably – the one that science can substantiate. It may not be one that either connects to consumer needs or to the main areas of interest of the consumer goods companies!

4. Hence the rate of failure at the level of commercialising ingredient science is very high.

NEW NUTRITION BUSINESS

The R&D agenda is broad

110

5. A few companies have altered their strategies to focus more heavily on supplying the dietary supplements market, where consumer acceptance of a wide range of benefits is much higher than for foods and beverages and there are no issues with taste, which is often a major obstacle to consumer acceptance of many new ingredients.

There are hundreds – perhaps thousands – of ingredient companies developing and attempting to commercialise hundreds of ingredients addressing every imaginable benefit area.

Some of these have become very successful in supplements, such as marine omega-3s, which lend themselves for a variety of reasons to supplements as the best delivery mechanism but food and beverages are not good delivery mechanisms for them.

Even where clinical science is robust and regulators approve health claims, this may be of no commercial value if the benefit is of limited consumer interest.

For example….

NEW NUTRITION BUSINESS

An example is Sirco, a patented technology which belongs to a science-based company called Provexis and which is marketed with a claim that it helps “maintain a healthy blood flow and benefits circulation”.

At launch, Provexis thought the appeal for its Sirco juice brand would be broad. They targeted consumers aged 40 but found its primary appeal was to: “Over 55s, with a lot of people who call us and write to us in the over-70 group”.

Sales flattened at $3m (NZ$3.7m) and did not grow “beyond the niche of healers”. The brand has been relaunched with an EU-approved claim – but sales are no better and the consumer niche is the same.

Provexis has licensed the technology to ingredient giant DSM to market to its customer base. This may yet prove successful – but it’s worth noting that: 1.Provexis has been in existence for 10 years and has yet to earn a profit. It earns almost zero revenue from Sirco. 2.None of the companies we interviewed sees a future for this technology other than as a super-niche medical food.

Health claim approval of little value to “technology push” products

111

NEW NUTRITION BUSINESS

The classic science commercialisation model

The problem is that every science-based ingredient company has a strategy statement that reads something like this….

NEW NUTRITION BUSINESS

Few technologies turn a profit

But for this model to work companies require deep pockets.

And the flaws in this model are more apparent than ever.

2001 on behalf of a client we reviewed 50 IP-based nutritional ingredient businesses in Europe and North America. Criteria included: must already have some commercial sales, must be established five years or more.

Of the 50 only two were making a profit

Reviewed same group 2003, 2005, 2008.

Only six now making a profit, some had disappeared. Some absorbed by larger groups.

For example…

NEW NUTRITION BUSINESS

Few technologies turn a profit

An example of one of the many failures is Canadian-based Forbes Medi-Tech.

As the figures on the following page show, it brought to market a plant sterol-based cholesterol-lowering technology which was a “me-too” and which brought no point of difference to an over-supplied market.

As a result the company never met its sales targets. It made the common mistake of believing that by investing further in science and approved claims it could obtain success.

Faced with a disappointing performance in its first technology, it moved to another, attempting to create synergies between its sterols and marine omega-3s. This was both a large investment and reflected a total failure to understand the perspectives of consumer goods companies.

The company focused more on technology push than on attempting to understand consumer pull. As the figures show, founded in 1995, Forbes never made a profit.

In 2010 the company was put into liquidation.

NEW NUTRITION BUSINESS

Forbes Medi-Tech: What failed science commercialisation looks like

Total sales 98-08 C$62m (NZ$86.5m)Cumulative losses C$106.5m (NZ$148.5m)!Capital invested over C$100m (NZ$140m)!

NEW NUTRITION BUSINESS

Packaging innovation a driver of technology profitability

By contrast, Finland-based Raisio Group, makers of the Benecol cholesterol-lowering technology:

1.Were one of the first three companies to market with their technology2.By being one of the first to market they helped create a new segment of the market3.With its partners, particularly Swiss-based Emmi Dairy, Raisio used packaging innovation to create better consumer pull for products containing its technology, and this transformed the company’s fortunes.

The key lesson that the company says it learnt – as the figures on the next chart show – is that science is of no value unless other market-oriented innovations, such as packaging innovations, are connected to it.

NEW NUTRITION BUSINESS

Benecol: what successful science commercialisation looks like

Packaging is key: The roll-out from 2002 of the first-ever daily dose format for cholesterol-lowering drinks by one of its partners by itself transformed Benecol from an under-performing business into a consistently profitable one.

NEW NUTRITION BUSINESS

Recaldent is an example of taking a dairy-based innovation and making it successful in the consumer market by understanding the consumer.

Consumers are familiar with gum as a format that offered dental health benefits.

Recaldent offered the chance for the number 2 company in gums (Cadbury) to enter the dental health segment with a new benefit.

Worldwide retail sales of products made with Recaldent may already be over $200 million (NZ$247 m) a year.

In Japan, Recaldent gum holds the rank of the 9th-biggest FOSHU-approved functional food.

Successful ingredient companies find or create a genuine point of difference

NEW NUTRITION BUSINESS

Another key lesson from Recaldent is the long timescale of successful science commercialisation.

In 1989 Professor Eric Reynolds, School of Dental Science at University of Melbourne, embarked on a project to discover whether calcium and phosphate from cows milk could be delivered to teeth in a way that it could repair damaged tooth enamel.

1998 the first commercially manufactured batch of Recaldent produced.

Not until 2008 did Recaldent pass the tipping point commercially.

Recaldent: long timescales to market success

NEW NUTRITION BUSINESS

As Forbes, Benecol and Recaldent all found, key to success is to establish some genuine point of difference.

For example, there are over 20 suppliers of marine omega-3, with new entrants all the time.

How is each company to differentiate itself? They cannot.

In most markets there is usually only room for 2-3 leading players and perhaps one or two niche players. But if you are a niche player in a niche ingredient market you cannot survive.

Price will emerge as the main battleground for those trying to survive – as it has in other categories, such as fibre:

“There are many, many suppliers of dietary fibre, but essentially they all offer more or less the same thing supported by similar science. They all tell me they are unique or strongly based in science. But the truth is they are all the same. So when we buy fibres for use in functional foods we select on price now.”Interview with functional food ingredients buyer of major multinational

Find or create a genuine point of difference

NEW NUTRITION BUSINESS

Foods vs supplements?

Target the supplements markets as well as food and beverage

For companies producing me-too ingredients, such as marine omega-3s, and ingredients with limited opportunity in the food and beverage market, the much more fragmented dietary suplements markets offer a bigger opportunity.

Supplements (in pill form) have the advantage of not being expected to perform on taste -meaning higher doses of active ingredients can be used than could be formulated into many foods.

Often ingredient = the benefit – people with a health need often search for a specific ingredient that their own research says will “fix” their health concern

Less of a challenge matching benefit, format and brand

Traditionally a high margin business.

121

NEW NUTRITION BUSINESS

Food or supplement: many companies have now defined some benefit areas as only suitable for the supplements market

AREAS OF PRIMARY INTEREST FOR FOOD AND BEVERAGE

AREAS BETTER SERVED BY DIETARY SUPPLEMENTS

Vision

Skin / Hair / Nails

Allergy

HORMONAL WELL BEING

Fertility

PMS

SPECIALNUTRITION NEEDS

Pregnancy

Teenagers

COGNITIVE

METABOLIC DISORDERS

Blood Glucose

Weight Management

ENERGY

MOBILITY

CELL PROTECT

SPECIALNUTRITION NEEDS

Seniors

Sports

Source: confidentially provided by industry source for this study

Oral health

NEW NUTRITION BUSINESS

>$2.25 billion (NZ$2.8bn) and growing: retail sales of omega-3 dietary supplements in US and Europe

<$500 million (NZ$617m) and static: retail sales of omega-3 foods and beverages (excl. infant formula) in US and Europe.

The omega-3 companies live on supplements!

The supplement area is a good place to take early-stage science that would not pass food regulations for health claims.

Supplement sales still growing despite recession.

Biggest opportunities in Asia.

Example: a focus on supplements and Asia

NEW NUTRITION BUSINESS

BioGaia: re-thinking a commercialisation model

Company founded 1993 in Sweden to commercialise probiotic L. reuteri, companymade no profits for many years despite having its bug used in successfulbrands such as Stonyfield Farm.

To turn around situation owners decided to:• get closer to the consumer• become global, setting up offices in Japan and US• be a successful niche player in as many markets as possible• focus on supplements and regional (not global) partners.

Today: • products on sale in 40 countries.• 50% of sales from Asia – very little in Sweden. “Sweden is where our office is, it is not akey market.”

• 2008 sales up 36% over 2007 to SEK 145.2m (NZ$28.5m). • Operating profit SEK 25.8m (NZ$5m), a 200% increase over 2007

NEW NUTRITION BUSINESS

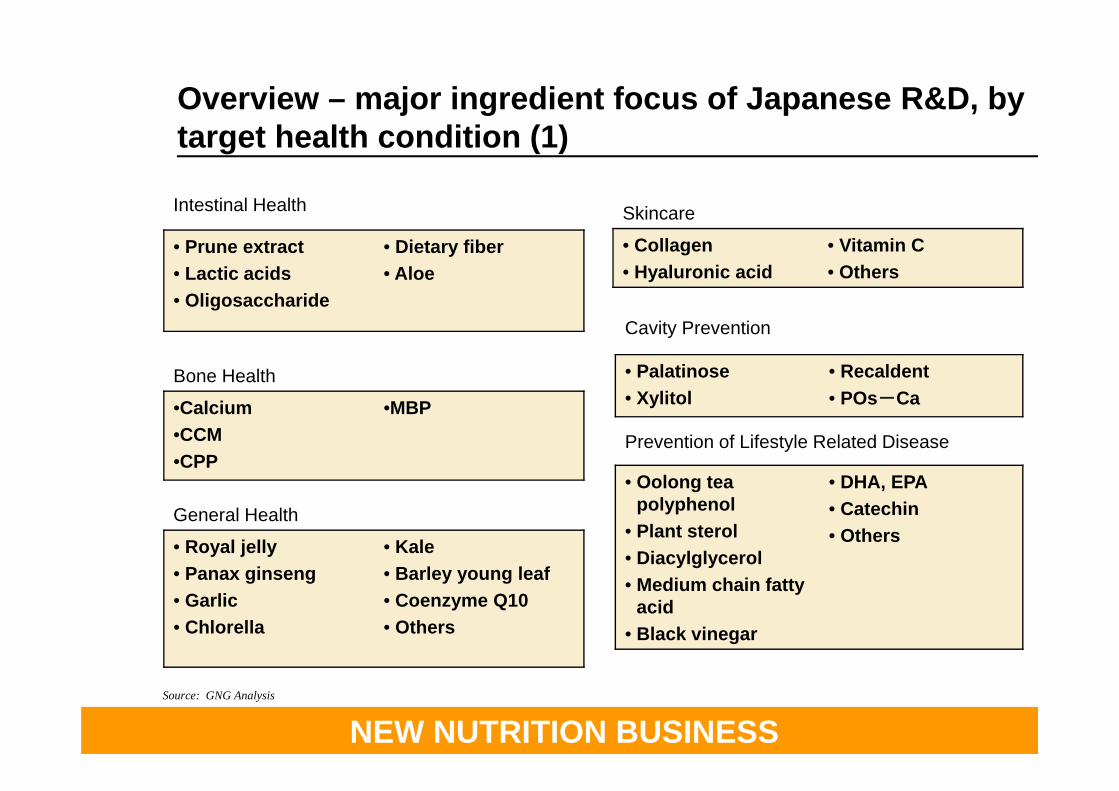

Japanese R&D trend overview

16

NEW NUTRITION BUSINESS

Summary

Source : Fuji Keizai, GNG Analysis

• Because of the Japanese food industry’s pioneering role in giving birth to the health and wellness market, hundreds of companies have conducted research into thousands of ingredient compounds.

• The market for digestive health products – from probiotics – is well-established and hence it does not have the R&D attention that it has in the West, other than for specific companies, such as Yakult Honsha and Meiji, who are working to add to the clinical support for their probiotics.

• Key R&D areas include: beauty, eye health, solving a shortage of vegetables in the diet, and energy.

• The good image of fruit has, as in the West, prompted intensified research into the functionalities of fruit in recent years and given the importance of fruits and vegetables to the R&D agenda – and given that this is a snapshot of the industry rather than a comprehensive description, we have used Japanese R&D efforts in fruits and vegetables as the primary examples in the following slides.

NEW NUTRITION BUSINESS

Cavity Prevention

• Palatinose• Xylitol

• Recaldent• POs-Ca

Prevention of Lifestyle Related Disease

• Oolong tea polyphenol

• Plant sterol • Diacylglycerol• Medium chain fatty

acid• Black vinegar

• DHA, EPA• Catechin• Others

Bone Health

•Calcium•CCM•CPP

•MBP

Intestinal Health

• Prune extract• Lactic acids• Oligosaccharide

• Dietary fiber• Aloe

General Health

• Royal jelly• Panax ginseng• Garlic• Chlorella

• Kale• Barley young leaf• Coenzyme Q10• Others

Skincare

• Collagen• Hyaluronic acid

• Vitamin C• Others

Overview – major ingredient focus of Japanese R&D, by target health condition (1)

Source: GNG Analysis

NEW NUTRITION BUSINESS

Breath Care

• Chlorophyll• Flavonoids

• Herbs

Eye Health

• Blueberry • Cassis

Multi Balance

• Multi vitamins • Amino acid

• Minerals

Weight Loss

• Dietary fiber• Protein• Garcinia Cambodia• Glucomannan• Gymnema• Amino acids

• Brewer's yeast• Catechin• New sweeteners• Others

Sore Throat

• Herbal extracts• Chinese quince

•Menthol

Source: GNG Analysis

Overview – major ingredient focus of Japanese R&D, by target health condition (2)

NEW NUTRITION BUSINESS

Size of markets for health ingredients derived from selected fruits

Fruits Active ingredient Health Platform Estimated Market Size 2010 (Raw Materials)

Bilberry Polyphenol (Anthocyanin) Eye Health, Skincare 7,300 million yen($91 million)

Cassis Polyphenol (Cassis Anthocyanin)

Eye Health, Skincare (Under-eye Circle, Dullness Skin)

2,500 million yen($31 million)

Pomegranate Ellagic Acid, Polyphenol (Punicalagin)

Anti-aging, Whitening, Easing Menopausal Discomfort

≦100 million yen($1.25m)

Apple Polyphenol Skincare, weight-loss, cholesterol-lowering

≦300 million yen($3.75m)