Embed Size (px)

Citation preview

Kayne Anderson Capital Advisors, L.P.

www.kaynecapital.com Confidential

KAYNE ANDERSON ENERGY FUNDS AUGUST 2017

2 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

Overview Kayne Anderson Capital Advisors

A Leading Alternative Investment Manager Since 1984

• Approximately $26 billion in assets under management

• Diversified investor base

• Over 300 employees (approximately 140 investment professionals)

• Substantial principal commitment; employee capital represents ~6% of firm assets

ATTACK NICHES • Identify underserved investment classes and unique opportunities where inefficiencies exist

• Field best-in-class teams to focus on market segments whose size or complexity serve as a barrier to entry

KNOWLEDGE AND SOURCING

ADVANTAGE

• Develop knowledge and sourcing advantages to mitigate and reduce risk

• Extensive network of deep relationships within industries alongside a strong reputation

FOCUS ON ENERGY

INVESTING

• $19 billion (over 75%) of firm assets invested in energy companies

• One of the largest MLP investors in the industry

• Large and seasoned, 60-person investment team dedicated to energy

• Energy investments throughout capital structure including debt, public equity and private equity

Differentiated Investment Philosophy

As of March 31, 2017.

3 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

Kayne Anderson Energy Funds Investment approach

Note: As of July 2017. % distributed represents total distributions / total contributed capital. The target IRR set forth herein is provided as an indicator as to how KAEF VIII will be managed and is not intended to be viewed as an indicator of likely performance returns to investors. The target return is based on estimates and assumptions that potential investments will yield a return equal to or greater than the General Partner’s return targets, however, there can be no assurance that KAEF VIII’s return objectives will be realized or that the General Partner will be successful in finding investment opportunities that meet these anticipated return parameters.

• Early stage middle-market investments in private North American oil and gas companies

• Engineering centric approach to capital allocation, value creation

• Growth equity model; 15-20 companies per fund

• High concentration of successful repeat management teams

• Value-added partner to management through knowledge integration and technology transfer

STRATEGY STRUCTURE

• Investment size of $50 to $300 million

• Returns from capital appreciation

• Targeted gross ROI of 2.0x+ and gross IRR of 25%+

• Typical holding period of three to five years

• Active investor (with majority control)

• Typically common equity investments through LLCs

Kayne Anderson

Capital Advisors, L.P.

Energy Fund I $112,500,000

Realized August 1998

Energy Fund V $820,000,000 Fully Invested

96% Distributed May 2009

Energy Fund II $240,000,000

Realized December 2002

Energy Fund VI $1,600,000,000

83% Invested 88% Distributed December 2012

Energy Fund III $550,000,000

Realized November 2004

Energy Fund VII $2,051,450,000

63% Invested 31% Distributed

September 2016

Energy Fund IV $950,000,000

Realized November 2006

Energy Fund VIII $2,000,000,000

Targeting Q4 2017 First Close

Kayne Anderson

Capital Advisors, L.P.

Kayne Anderson

Capital Advisors, L.P.

Kayne Anderson

Capital Advisors, L.P.

Kayne Anderson

Capital Advisors, L.P.

Kayne Anderson

Capital Advisors, L.P.

Kayne Anderson

Capital Advisors, L.P.

Kayne Anderson

Capital Advisors, L.P.

4 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

Kayne Anderson Energy Funds Capitalizing on engineering technology transfer

Ability to Quickly and Effectively Apply New Technology Across Basins is KAEF’s Main Competitive Advantages • Focus on early-stage assets in the middle market

• Utilize technical expertise to corroborate both current and historical learnings from over 100 resource plays

UNIQUE INSIGHTS PROVIDE COMPELLING OPPORTUNITIES

EXPLORATORY WELLS

ENHANCED COMPLETIONS

CORE EXPANSION FULL DEVELOPMENT

Limited success

Unknown type curve

Infancy Phase Delineation Proven Maturity Phase

Acreage Multiples

Information

Producing asset

Type curves are de-risked

Acquire assets for development

Wall Street fully values potential

Typical KAEF Investment

Typical KAEF Sale

Apply knowledge from analogous plays

Process initial results

Prove up type curve

Exploit efficiencies

Expand economic / geologic limits

Delineate key locations

Prove - Up Development

5 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

POWDER RIVER BASIN

BALIDOR

Kayne Anderson Energy Funds Transferring engineering technology across basins

SCOOP / STACK CASILLAS TRIUMPH

CORLENA III BEACON II CANYON II

LEARNINGS FROM 25+ CURRENT AND

80+ PRIOR PORTFOLIO COMPANIES

We see the industry and technology evolving in

“real time”

DELAWARE BASIN SILVER HILL I & II

PANTHER INVICTUS BEACON II

IN-HOUSE ENGINEERS WITH EXPERIENCE IN OVER 100 RESOURCE

PLAYS

KAYNE ANDERSON ENERGY FUNDS

INDUSTRY ACTIVITY

Constantly monitoring industry activity in

established and emerging plays

Significant knowledge and experience across

multiple basins to identify calling cards of

resource plays

WILLISTON BASIN KRAKEN I & II

Leveraged experience in the Midland Basin to

identify potential in the Delaware

KAEF continues to identify new areas

that can benefit from new technology

Recognized the impact of new technology to

underwrite transactions in STACK & SCOOP

6 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

Kayne Anderson Energy Funds Significant presence in core areas of the STACK & SCOOP plays

KEY STACK & SCOOP HIGHLIGHTS KAEF STACK / SCOOP MAP

KAEF VII portfolio companies have acquired nearly 100,000 net acres in the STACK and SCOOP to date

• The STACK/SCOOP play is now the second most actively developed play with 82 active rigs, behind only the Permian with 296 active rigs

• Characterized by multiple stacked-pay zones with attractive drilling economics at current commodity prices

• Significant potential upside through further optimized completions, down-spacing, extended laterals and additional prospective formations

• Large public operators continue to consolidate smaller operators to high-grade and grow inventory

• Canyon Midstream II recently announced plans to build a midstream system to provide capacity for the significant resource potential of the STACK

• Anchored by two KAEF portfolio company acreage dedications

STACK (55,000 NET ACRES)

BEACON II CORLENA OIL COMPANY III

TRIUMPH ENERGY

SCOOP (45,000 NET ACRES)

CASILLAS PETROLEUM

STACK MIDSTREAM SYSTEM

CANYON MIDSTREAM II

7 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

Kayne Anderson Energy Funds Expanding the core of the Williston Basin

WILLISTON BASIN MAP

WILLISTON BASIN (85,000+ NET ACRES)

KRAKEN OIL & GAS I & II

INVESTMENT THEMES

In September 2016, Kraken II acquired 80,000 net acres and 2,800 boe/d of net production for $222 million

• Negotiated middle-market acquisition from capital-constrained public company

• Knowledge and technology transfer through enhanced completions proven at Kraken I

• Expanding the core of a major basin

• Engineering data indicating well-measured downside and competitive economics

• Asset with appeal to broad buyer universe due to scale and attractive single well returns

• Unique engineering insights framed underwriting thesis

UNDERWRITING THESIS

- 5

10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95

100 105

- 200 400 600 800 1,000 1,200 1,400 1,600

EUR

bbl/

ft

Proppant lb/ft

Open Hole Completion

Cemented Liner Only

Leading-Edge Design

Gen 1 Completions

Gen 2 Completions Base Case

Gen 3 Completions Upside Case

OPPORTUNITY SET

Any projections, targets, or estimates used in this presentation are forward looking statements and are based on KAEF’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Investors should seek financial advice regarding the appropriateness of an investment in the Fund.

9 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

Kayne Anderson Energy Funds Technology impact

Source: RS Energy Group.

The technical innovations experienced over the past two years will continue to expand the economic limits of today’s plays

MIDLAND BASIN (2011-2012) MIDLAND BASIN (2012-2013) MIDLAND BASIN (2014-2016)

• Initial development in the Midland Basin was focused in the southeastern portion of the basin in 2011 and 2012

• EURs averaged 70 boe/1,000 ft

• During 2012 and 2013, operators moved north into the heart of the Midland Basin

• EURs averaged >100 boe/1,000 ft

• From 2014 to 2016 the existing core of the Midland Basin was rapidly expanded by the use of laterals >7,500 ft and proppant >1,500 lbs/ft

• EURs averaged >150 boe/1,000 ft

Expanded Core

New Core

Original Core

0% 50% 100%

Change in EUR% (2014-2016)

10 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

$5.0 $5.5 $7.1

$4.9 $4.4 $2.9

$1.7

$7.8 $7.0 $5.3

$1.7 $1.6

$0.6 $0.5

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

2010 2011 2012 2013 2014 2015 2016

$B

Total Proved Capital Total Unproved Capital (Early Stage Assets)

Divested $2.5B of Assets

CHESAPEAKE ENERGY CAPITAL BUDGET

Kayne Anderson Energy Funds Compelling market for early stage oil and gas assets

Large number of assets currently in market or expected to come to market in near-term

• Industry participants continue to sell assets to fund development capital budgets

• Over 100 assets across North American basins

• Does not include off-market transactions

Public company budgets remained focused on delineated assets with minimal capacity for early stage assets

• Limited competition for early stage assets

• Industry remains largely capital constrained

Permian Deals: 23

Mid-Continent: 20

Eagle Ford: 11

Rockies: 13 Appalachia: 15

ARK-LA-TEX: 6

Bakken: 8

ASSETS IN MARKET

Source: BMO Capital Markets, Chesapeake Energy public filings – Total Proved Capital represents proved property acquisitions and development costs. Total Unproved Capital represents unproved property acquisitions and exploratory costs.

Other Areas: 17

11 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

Kayne Anderson Energy Funds Compelling market for early stage oil and gas assets

Highest potential for value creation and equity returns

• Asymmetric risk/return through application of engineering technology transfer

• Measured approach limits capital exposure during prove-up phase

• Investments resilient to downward moves in commodities prices

Limited competition

• Industry is largely capital constrained

• Focus and capital investment limited to more delineated plays

• Industry participants continue to sell existing early stage assets rather than incubate new project areas

Vast opportunity set

• Oil field technical innovation has grown exponentially since the downturn creating new tools to develop assets

• Other factors beyond “rock quality” drove the concentration of investment

• Substantial high-quality resource exists beyond the “15 counties”

12 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

Kayne Anderson Energy Funds Early stage assets are resilient to commodity price movements

Early stage assets are resilient to movements in commodities prices • Production weighted investment outcomes often correlated to changes in commodity prices

REDUCTION IN SERVICE COSTS

REDUCTION IN SERVICE COSTS AND

IMPROVED EUR

2014 Single Well Economics ($50/bbl & $2.75/mmbtu)

2016 Single Well Economics ($50/bbl & $2.75/mmbtu)

2014 Single Well Economics ($85/bbl & $4.00/mmbtu)

Hz Wolfcamp A - Single Well Economics

EUR (mbo): 720

D&C Cost ($mm): $9.0

IRR: 76%

Hz Wolfcamp A - Single Well Economics

EUR (mbo): 720

D&C Cost ($mm): $6.5

IRR: 38%

Hz Wolfcamp A - Single Well Economics

EUR (mbo): 986

D&C Cost ($mm): $6.5

IRR: 65%

Throughout KAEF’s experience, resource plays continue to improve over time with operational efficiencies, optimizations and improved reserve recoveries

Note: Based on Silver Hill’s lower Wolfcamp A type curve estimates. Does not represent a guaranteed investment return to investors.

13 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

Kayne Anderson Energy Funds KAEF activity map

Source: RS Energy Group research. Note: * recent exit or under PSA.

Bakken Kraken I (EF V)

Kraken II (EF VII)

Powder River Balidor (EF VII)

SCOOP/STACK Beacon II (EF VII) Casillas (EF VI/VII) Corlena III (EF VII) Triumph (EF VII)

DJ *HRM II (EF VI)

East Texas Treadstone II (EF VI)

Canada Newton (EF IV/V)

Delaware Basin Beacon II (EF VII) Invictus (EF VII)

*Panther II (EF VI) *Silver Hill I (EF VI) *Silver Hill II (EF VII)

Other Permian Basin Adventure III (EF V) *KA Henry I (EF V) Monadnock (EF VII)

PAK (EF VI)

Diversified Canyon I (EF V/VI) Canyon II (EF VII) Haymaker (EF VI)

Haymaker II (EF VII) :Historical KAEF portfolio company activity

Midland Basin Adventure III (EF VII)

Amistad (EF VII) Grenadier II (EF VI) KA Henry II (EF VI)

PT Petroleum (EF VI) *RB Permian (EF VI) RB Permian II (EF VII)

APPENDIX CASE STUDIES

The following case studies have been included to illustrate the opportunity-rich environment within the onshore North American middle-market and the competitive strengths of the Kayne Anderson Energy Funds team. Any projected returns provided herein should not be considered as a guarantee of returns to limited partners.

15 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

KAEF Portfolio Update Case study: Silver Hill Energy Partners I (KAEF VI)

Leased ~25,000 net acres in Loving and

Winkler Counties, TX at ~$3,000/acre

Drilled 20 horizontal wells across multiple horizons (total of 47

producing wells including Silver Hill II, KAEF VII company)

Sold upstream assets to RSP

Permian for $2.4B

Initial Single Well Economics (2014)EUR (Mbo): 530D&C Costs ($MM): $9.0IRR 1 : 33%(1) Assumes $85/bbl and $4.00/MMbtu pricing.

Optimized Single Well Economics EUR (Mbo): 980D&C Costs ($MM): $7.0IRR 1 : 35%(1) Assumes strip pricing as of 2/5/16.

Premium valuation received in sales process reflects Silver Hill I’s contiguous, core acreage position with multiple prospective horizons within one of the most highly economic basins in North America

16 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

KAEF Portfolio Update Case study: Panther Energy Company II (KAEF VI)

Leased ~15,000 net acres in Reeves and Culberson Counties, TX for

~$3,000/acre before selling down a 49% non-op WI at a promoted price

Sold assets to WPX and a private

company for $863mm

Premium valuation achieved is a direct reflection of Panther II’s ability to identify, assemble and delineate a core Delaware Basin acreage position with highly economic drilling locations throughout multiple benches

Drilled 17 horizontal wells across multiple horizons and grew production to 7,500 boe/d. Grew position to ~18,000 net acres through bolt-on acquisitions

primarily in Reeves and Loving Counties

Initial Single Well Economics (2014)Reeves WCA EUR (Mboe): 533D&C Costs ($MM): $8.4IRR 1 : 31%(1) Assumes strip capped at $85/bbl flat pricing.

Optimized Single Well Economics (2016)Reeves WCA EUR (Mboe): 1,174D&C Costs ($MM): $6.5IRR 1 : 49%(1) Assumes strip pricing as of 4/28/16.

17 Common Philosophy | Shared Resources | Niche Expertise

Kayne Anderson Capital Advisors, L.P.

Disclosures and Legal Disclaimer

Investment in Kayne Anderson Energy Funds (together, the “Partnerships” or the “Funds”, and each individually, the “Partnership” or “Fund”) involves a high degree of risk. There can be no assurance that the Partnership’s investment objectives can be achieved, or that a Limited Partner will receive a return of capital. In addition, there may be occasions when the General Partner of the respective Partnership and its affiliates encounter potential conflicts of interest in connection with the Partnership. For a more detailed explanation of the risks of the Partnerships, please review the Partnership’s Confidential Private Placement Memorandum.

In addition to historical information, this presentation contains "forward-looking statements". The words "forecast", "estimate", "project", "intend", "expect", "should", "believe" and similar expressions are intended to identify forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties, assumptions and other factors, including those discussed in the Memorandum, which may cause the Fund’s actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. In addition, new risks and uncertainties may arise from time to time. Accordingly, all forward-looking statements should be evaluated with an understanding of their inherent uncertainty. Except as required by law, we assume no obligation to publicly update or revise these forward-looking statements for any reason, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future.

Certain economic and market information contained herein has been obtained from published sources prepared by third parties or KACALP and in certain cases has not been updated through the date hereof. While such sources are believed to be reliable, neither the Fund, nor its respective affiliates or employees assume any responsibility for the accuracy or completeness of such information.

Information contained herein may include information respecting prior investment performance including gross and net returns. Information respecting prior performance, while a useful tool in evaluating an investment, is not necessarily indicative of actual results to be achieved for unrealized investments, the realization of which is dependent upon many factors, many of which are beyond the control of the Fund or KACALP.

No representation or warranty, express or implied, is given by or on behalf of the Fund, KACALP, or any of such persons' directors, officers or employees or any other person as to (a) the accuracy or completeness of the information or (b) the opinions contained in this document and no liability is accepted for any such information or opinions. Unless otherwise stated in this document, the information contained herein is based on the Fund's information and estimates. The information and opinions contained in this presentation are provided as of the date of this document and are subject to change without notice.

This confidential presentation (this “Presentation”) is qualified in its entirety by reference to the respective Memorandum and the Limited Partnership Agreement of each of the Funds, as may be amended and/or modified from time to time and the subscription agreement related thereto, copies of which will be made available upon request and should be reviewed before purchasing a limited partnership interest in the Funds. The purchase of interests in the Funds will be suitable only for sophisticated investors for whom an investment in the Fund does not constitute a complete investment program and who fully understand and are willing to assume the risks involved in the Funds’ investment program. Statements in this Presentation are made as of December 2016 unless stated otherwise, and neither the delivery of this Presentation at any time nor any sale of the limited partnership interests described herein shall under any circumstances create an implication that the information contained herein is correct as of any time after such date. This Presentation is not intended to be relied upon as the basis for an investment decision, and is not, and should not be assumed to be, complete. The contents herein are not to be construed as legal, business, or tax advice, and each prospective investor should consult its own attorney, business advisor, and tax advisor as to legal, business, and tax advice. In considering any performance information contained herein, prospective investors should bear in mind that past performance is not necessarily indicative of future results, and there can be no assurance that the Fund will achieve comparable results.

Any investment in the Funds is subject to various risks, some of which are outlined herein. A complete description of certain risks involved with an investment in the Funds can be found in the respective Memorandum; such risks should be carefully considered by prospective investors before they make any investment decision.

This Presentation does not constitute an offer or solicitation in any state or other jurisdiction to subscribe for or purchase any limited partnership interests described herein. KACALP and its affiliates reserve the right to modify any of the terms of the offering and the limited partnership interests described herein.

Recipients of this Presentation agree that KACALP, its affiliates and their respective partners, members, employees, officers, directors, agents, and representatives shall have no liability for any misstatement or omission of fact or any opinion expressed herein. The Presentation is not intended for any general distribution or publication and is strictly confidential. This Presentation and the information contained herein consists of confidential proprietary information and is the sole property of the Funds. Each recipient further agrees that it will (i) not copy, reproduce, or distribute this Presentation, in whole or in part, to any person or party (including any employee of the recipient other than an employee directly involved in evaluating an investment in the Fund) without the prior written consent of KACALP; and (ii) keep permanently confidential all information contained herein that is not already public.

Past performance is no guarantee of future results. An investment in the Partnership could suffer loss.

8/10/2017

2017 EnerCom Oil and Gas Conference

August 2017

Tailwater Capital

2

• Middle-market private equity focused exclusively on the energy industry

• History of creating solutions oriented, value-added partnerships

• Well-established track record, having executed more than 65 transactions

representing $16.6 billion in value over the last 19 years

• Invest growth equity across the midstream and upstream sectors

• Currently manage over $2.1 billion across five distinct funds of capital

Growth Mindset, Partnership Oriented

Tailwater Capital EnerCom Oil and Gas Conference – August 2017

Midstream Strategy

3

Partnership Alignment

Vast Midstream Industry

Transaction Structure Creativity

• Most critical element of our strategy

• Focused on developing long-term, repeat partnerships

• Diversify through projects, not teams

• Recognize and trust team’s industry expertise

• Interest / experience across midstream industry

- Gathering

- Disposal

- Treating

- Compression

- Processing

- Transportation

- Storage

- Fractionation

• Interest / experience across transaction structures

- Anchored greenfield

- Acquisitions

- Joint ventures

• Flexible in terms of project size

• Differentiated upstream investing promotes midstream investing

Tailwater Capital EnerCom Oil and Gas Conference – August 2017

Midstream Strategy in Practice

4Tailwater Capital

• Gas gathering & processing

• East Texas, North Louisiana

• CEO: Fritz Brinkman

• Solids waste disposal

• Permian and Eagle Ford

• CEO: George Wommack

• Crude oil transportation

• South Texas• CEO: Phil

Mezey

• Spent lubes processing

• Baytown, TX• CEO: Jim Lelio

• Integrated Midstream

• Eagle Ford and Mississippi / Alabama

• CEO: Bruce Williamson

• Water gathering and disposal

• Bakken, Permian

• CEO: Patrick Walker

• Gas gathering & processing

• Permian• CEO: Jim Bryant

• Gas gathering & processing

• DJ Basin• CEO: Charlie

Beecherl

• Oil / gas gathering & gas processing

• Mid-Continent• CEO: Brandon

Webster

• Gas gathering, compression & treating

• Appalachia• CEO: Robert

Stiles

EnerCom Oil and Gas Conference – August 2017

Upstream Strategy

5

Proven Operators in the Core of Proven

BasinsBasins of Interest

Transaction Structure Creativity

• Emphasize operator expertise and track-record

• Delineated basins in the “core”

• Tailwater currently has positions in the following basins

- Anadarko

- Appalachian

- DJ

- Delaware

- Williston

• Interest/ experience across non-operated structures

- Primary leasing

- Acreage acquisitions

- Wellbore purchases

- Joint ventures

Tailwater Capital EnerCom Oil and Gas Conference – August 2017

Upstream Strategy in Practice

6Tailwater Capital

Tailwater UpstreamBasins of Interest

EnerCom Oil and Gas Conference – August 2017

Midstream Private Equity Outlook

Current Market Perspectives and Tailwater Approach

8Tailwater Capital

• High competition in certain basins across the United States (ex. Permian Basin)

• Reinvigorated transaction volume in certain basins, but large deals are expensive

• Ability to purchase non-core assets from poorly capitalized MLPs and upstream operators still

exists

• Opportunities outside of the Permian and SCOOP / STACK still exist

Current Market Perspectives

• Middle-market approach to midstream lessens competitive intensity

• Open to non-traditional midstream opportunities such as water, landfills, and downstream

adjacent projects

• Focus on a variety of basins by using both anchored greenfield and non-core acquisition

transaction structures

• Back new management teams and invest growth capital in established platforms or joint ventures

Tailwater Approach

EnerCom Oil and Gas Conference – August 2017

Contact Details

9

Jason DownieManaging Partner

Edward HerringManaging Partner

David CecerePrincipal

Billy DeArmanPrincipalUpstream

Joel FryPrincipal

2021 McKinney Ave | Suite 1250 |Dallas, TX 75201

Tailwater Capital EnerCom Oil and Gas Conference – August 2017

Questions

August 17, 2017

EnerCom Presentation

Private and Confidential

OFS Energy Fund Introduction

Formed the team in October 2008 to make investments in lower middle market energy service companies

OFS seeks to provide creative solutions for business owners in the form of buyouts, recapitalizations, and growth equity investments

First fund (“Fund I”) managed by the OFS principals at a predecessor entity named Dorado Energy Partners was closed in October 2008 with $46.5 million in total commitments

– 4.2x gross cash-on-cash and 200.0% gross IRR

Second fund (“Fund II”) was closed in September 2012 with $90.0 million in total commitments and had an add-on closing in November 2014 that raised total commitments to $130.0 million

– OFS principals and industry advisors personally committed $15.0 million

– To date, $96.6 million capital called relating to investments in eight platform companies

– Total capital called of $109.0 million

• Two exits, both completed in March 2014, represented returns of 4.1x gross cash-on-cash and 84.5% gross IRR

Third fund (“Fund III”) was closed in April 2014 with $175.0 million in total commitments

– To date, $85.7 million capital called related to investments in five portfolio companies

– Total capital called of $99.8 million

• One exit in August 2017, represented return of 3.6x gross cash-on-cash and the potential to increase to 4.6x with the earn-out

– Fund III targets investments of $15.0 million to $30.0 million in each portfolio company, but has the ability to invest larger amounts with co-investment from Fund III investors

Private and Confidential 2

EnerCom Presentation

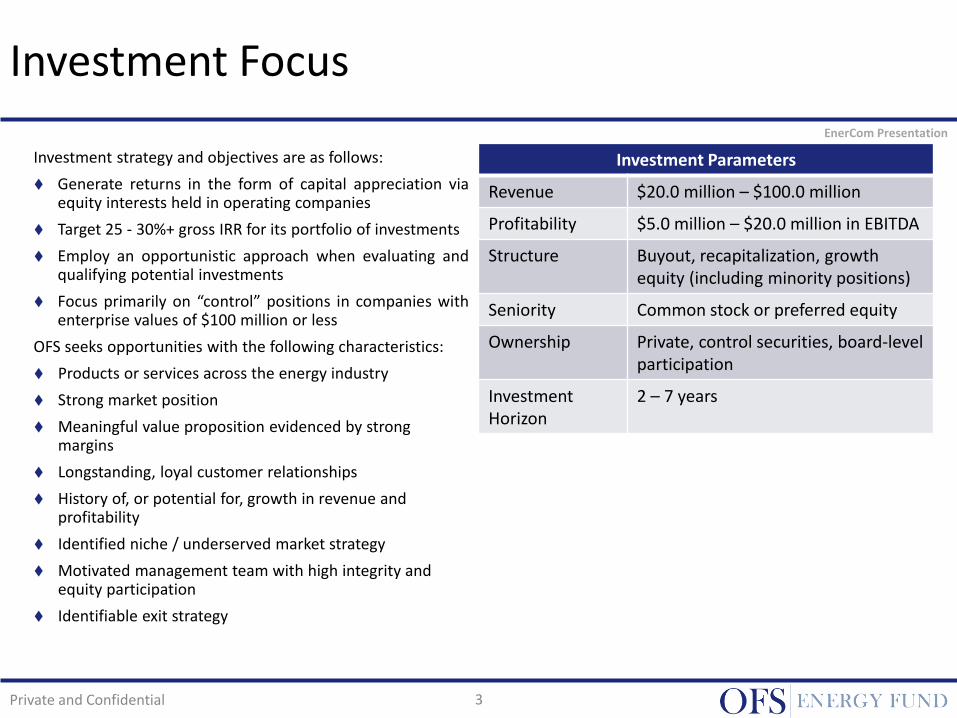

Investment Focus

Investment strategy and objectives are as follows:

Generate returns in the form of capital appreciation via equity interests held in operating companies

Target 25 - 30%+ gross IRR for its portfolio of investments

Employ an opportunistic approach when evaluating and qualifying potential investments

Focus primarily on “control” positions in companies with enterprise values of $100 million or less

OFS seeks opportunities with the following characteristics:

Products or services across the energy industry

Strong market position

Meaningful value proposition evidenced by strong margins

Longstanding, loyal customer relationships

History of, or potential for, growth in revenue and profitability

Identified niche / underserved market strategy

Motivated management team with high integrity and equity participation

Identifiable exit strategy

Private and Confidential 3

Investment Parameters

Revenue $20.0 million – $100.0 million

Profitability $5.0 million – $20.0 million in EBITDA

Structure Buyout, recapitalization, growth equity (including minority positions)

Seniority Common stock or preferred equity

Ownership Private, control securities, board-level participation

Investment Horizon

2 – 7 years

EnerCom Presentation

OFS Investment Criteria

Energy Service and Midstream Focused

Upstream Services and Equipment (examples include)

– Aftermarket service and repair of “must-run” drilling, completion and production equipment

– Specialty manufacturing

– Downhole tool rental and repair

– Well service / production services

– Well testing / completion services

– Offshore services

– Corrosion control and specialty coatings

– Inspection and Testing NDE

– Drilling services

– Chemicals

Midstream opportunities

– Treating and processing equipment

– Gas gathering and field infrastructure services

– New well connections

– Right of way maintenance

– Compression-related equipment and aftermarket services

– Oilfield construction

– Chemicals

Downstream services

– Power and Plant related services and equipment

The Fund will not invest in pre-commercial technologies or make E&P investments

Early, Growth or Late Stage Event-Driven Opportunities

Buyouts and recapitalizations of seasoned companies with history of profitability

Equity investments in high-growth, less mature companies

Partnerships with proven management teams / executives to pursue “restart” opportunities

Business owners seeking liquidity for estate planning or wealth diversification

Generational transition for family-owned businesses

Partner / family buyout or recapitalization

Expansion opportunities with limited access to capital

Investing with the “Right” Partners

Emphasis placed on partnering with management teams and entrepreneurs with successful track records

Willing to consider minority position investments with the right partners

EnerCom Presentation

Private and Confidential 4

OFS Difference

Small Professionally-Managed Fund

One of few professionally-managed private equity funds focused exclusively on lower middle market energy service companies

Experienced and consistent team – investment professionals have worked together over the course of three funds since 2008

Ability to act quickly – small investment committee consisting of day-to-day investment professionals

Flexibility with regard to structuring transactions allows for opportunistic investing

History of developing strong working relationships with management teams as reflected by the fact that management from every realized investment has invested in subsequent funds

Significant Strategic Support

Principals have extensive financial and operational experience acquiring and growing energy service companies and a proven history of developing and implementing successful exit strategies

Investment team with its own industry relationships from previous funds, work experiences, and participation in numerous industry trade groups

Limited Partners include owners and executives of E&P and energy service companies as well as commercial banking executives who help provide support to portfolio company growth initiatives and deal referrals

Private and Confidential 5

EnerCom Presentation

OFS Market Position

Focus on transactions less than $100 million in Enterprise Value for the following reasons:

Increased market competition for transactions above $100 million

Traditional energy / oilfield service funds, now managing several hundred million to billions in equity, are focused on acquiring larger companies that are often competitively auctioned

Investment Banks primarily focused on advising larger clients with auction processes and not interested in smaller fees – limiting organized competition for smaller transactions

Large public strategic buyers searching for acquisitions that “move the needle”

Underserved market below $100 million with many appealing targets

Few professionally managed small energy service funds – competition is limited to small generalist funds and individual investors

Family offices may review investment opportunities in the $1 - $3 million range with traditional energy private equity firms reviewing opportunities greater than $20 million

Large funds and strategic buyers focus on consolidating large privately-owned companies

Recent and continuing public company consolidation will create additional new opportunities

Smaller companies are better suited for buy-and-build platforms

Commercial banks are hesitant to lend to small oil & gas services companies without equity sponsors

Principals provide unique capabilities to lower middle market investments

Operational experience growing and acquiring companies as well as extensive financial expertise

Pull through relationships to augment sales and sourcing / procurement opportunities

Maintain “bench” of oilfield professionals with focused knowledge and interested in new opportunities

Proven history of developing and implementing successful exit strategies

EnerCom Presentation

Private and Confidential 6

Market Dynamics

Growth in onshore activity driven by increased commodity prices and more efficient E&P operations

Oilfield service companies are starved for capital having survived 2015 and 2016

– Exhausted working capital levels

– Equipment fleets are in substantial state of deferred maintenance

No / very limited access to bank financing

Equity is the solution

Seller psychology shifting to more reasonable valuations and emphasis on “support for growth”

Capital markets activity – IPOs, 144A transactions, etc. based on forward EBITDA valuations for equity raises

Offshore energy service market is in fourth year of downcycle and has not hit bottom yet; may present interesting investment opportunities

Private and Confidential 7

EnerCom Presentation

Fund II Portfolio Summary – Active Investments

Private and Confidential 8

$ in millions EnerCom Presentation

Active InvestmentsOnshore /

OffshoreProducts/Services

Date of

Investment

Total

Investment

Fund

Ownership

2016 Rev.

2017(E) Rev.

Fund II

OnshoreManufacturer of production

equipment and meter runsSep-2012 $23.1 37%

$55.6

$87.1

OnshoreWorkover rigs, wireline,

chemical salesOct-2013 $21.3 65%

$13.5

$21.5

OffshoreHighly engineered handling

equipmentOct-2013 $2.5 50%

$0.3

$1.7

Onshore

Water transfer, water

recycling, water treatment,

and solids control

Oct-2013 $13.3 60%$23.6

$42.2

Onshore Production equipment rental Dec-2013 $11.3 75%$5.0

$9.3

Fund III Portfolio Summary – Active Investments

Private and Confidential 9

$ in millions EnerCom Presentation

Active InvestmentsOnshore /

OffshoreProducts/Services

Date of

Investment

Total

Investment

Fund

Ownership

2016 Rev.

2017(E) Rev.

Fund III

Onshore Coiled tubing services Aug-2014 $25.8 72%$66.5

$125.7

Onshore

Frac stack, wireline, surface

drilling, solids control, mixing

plant, torque and test

Sep-2014$34.5 (Fund)

$14.9 (Co-Inv)

1.7%

+ Profits

Interest

$42.1

$72.9

Onshore

Provides parts, repairs, and

services for industrial gas

turbines

Oct-2015 $10.9 80%$35.3

$43.4

Onshore Nitrogen services Mar-2017 $8.5 85%$0.5

$8.1

VanZandt Controls

Onshore Valve distribution and services May-2017 $6.0 69%$6.0

$12.8

Fund I Track Record

Private and Confidential 10

$ in millions

Fund I Investment Summary:

– Commenced operations in October 2008 with $46.5 million in Committed Capital

– Called a total of $16.7 million of which $13.8 was invested into 4 portfolio companies

– Fund I returned $47.3 million and was liquidated in August 2012 achieving a 4.2x cash-on-cash return and an IRR of 199%

Realized

Investments

Onshore /

OffshoreProducts/Services

Date of

Investment

Total

Investment

Fund

OwnershipDate of Exit Realized Value Multiple IRR

Fund II

OnshoreProvider of natural gas treating

equipmentAug-2009 $3.8 14% Sep-2010 $19.3 5.0x 263%

Offshore

Provider of riser repair and

inspection and industrial

coatings

Jul-2009 $8.0 100.0% Aug-2009 $26.3 3.3x 175.0%

Onshore Manufacture and rent IBCs May-2010 $0.3 6.0% Jan-2015 $11.1 36.1x 126.0%

Onshore

Develop gathering systems

and pipelines Jun-2010 $1.7 Mar-2011 $1.7 1.0x 2.0%

EnerCom Presentation

Past Deals: Lone Star Fasteners, LP

Company: Lone Star Fasteners, LP – fasteners and related parts to energy equipment OEMs

Investment Highlights:

– Bruce Ross and Beau Ross (with other shareholders) purchased operating subsidiaries of T3 Energy Services in February 2004 for $7.0 million; at the time Lone Star had approximately 300 employees

– Immediately reduced headcount by 50 people, selectively increased sale prices and expanded international supply chain

– Instituted lean manufacturing techniques and brought in new operating management

– For the years ended December 2003 and December 2005, respectively, Lone Star increased revenue from $20 million to $35 million and EBITDA from $1 million to $6 million

– Recapitalized in November 2005 with Trinity Hunt Partners – share value had increased over 20 times from 2004 to 2005

– After the recap, Lone Star acquired 5 operating companies and grew sales from $35 million to $140 million, and EBITDA from $7 million to $25 million during 2006 and 2007

EnerCom Presentation

$36,000,000(1)

recapitalized by

November 2005

Investment Summary

Investment $ 1.0 million Feb-04

Ownership 100%

Equity Value at Recap $ 28.0 million Nov-05

Gross IRR 571%

Cash-on-cash Return 28.0x

(1) – Includes sale price and working capital true-up

Private and Confidential 11