Embed Size (px)

Citation preview

J P M O R G A N H V A C C O N F E R E N C E

M A Y 31, 2 0 0 7

2007 outlook & long-term objectives

Business strategy

Company review

Appendix

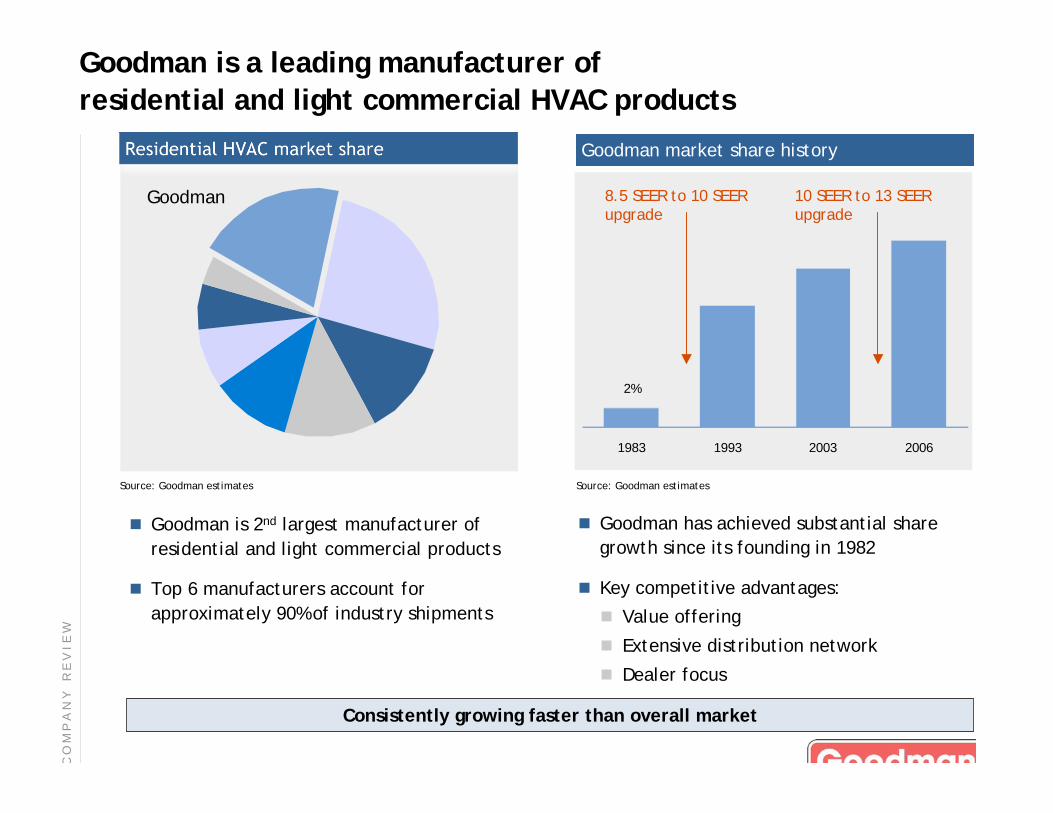

Goodman is a leading manufacturer of

residential and light commercial HVAC products

C O

M P

A N

Y R

E V

I E

W

Residential HVAC market share

Goodman

Source: Goodman estimates

Goodman market share history

2%

1983 1993 2003 2006

Source: Goodman estimates

Consistently growing faster than overall market

Goodman is 2nd largest manufacturer of

residential and light commercial products

Top 6 manufacturers account for

approximately 90% of industry shipments

Goodman has achieved substantial share

growth since its founding in 1982

Key competitive advantages:

Value offering

Extensive distribution network

Dealer focus

8.5 SEER to 10 SEERupgrade

10 SEER to 13 SEERupgrade

Source: Goodman estimates

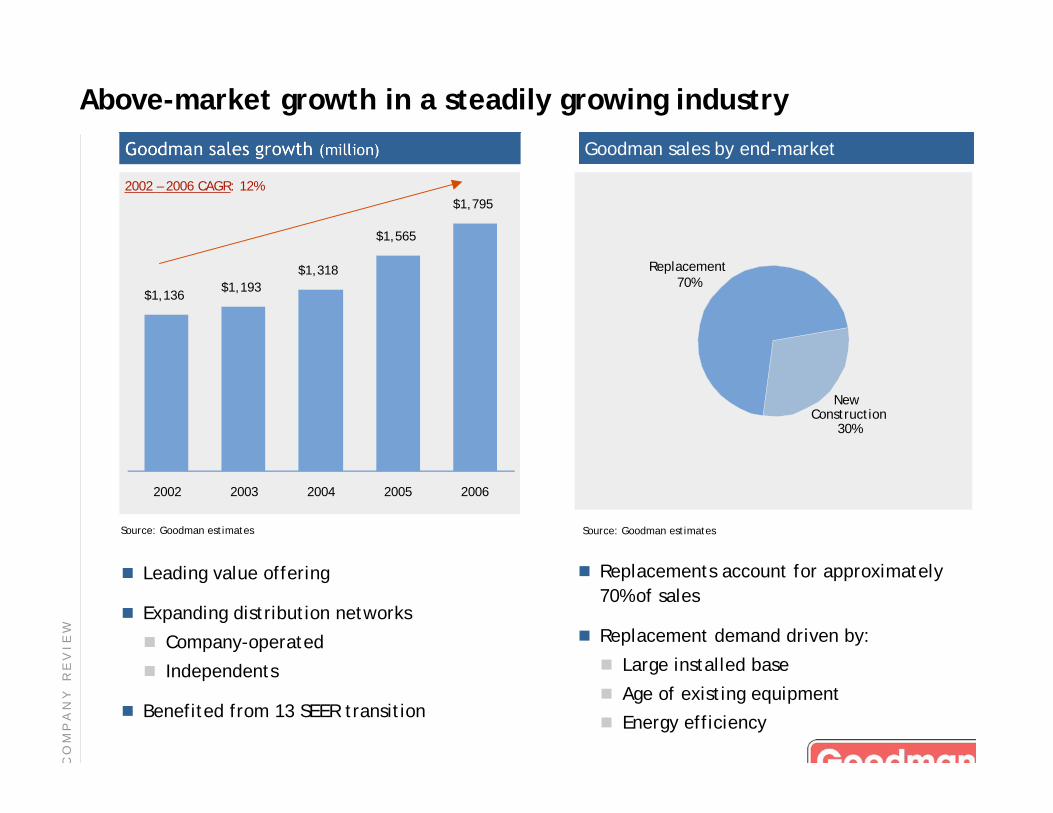

Goodman sales growth (million) Goodman sales by end-market

$1,136$1,193

$1,565

$1,795

$1,318

2002 2003 2004 2005 2006

Replacement70%

New Construction

30%

Source: Goodman estimates

2002 – 2006 CAGR: 12%

Above-market growth in a steadily growing industry

C O

M P

A N

Y R

E V

I E

W

Replacements account for approximately

70% of sales

Replacement demand driven by:

Large installed base

Age of existing equipment

Energy efficiency

Leading value offering

Expanding distribution networks

Company-operated

Independents

Benefited from 13 SEER transition

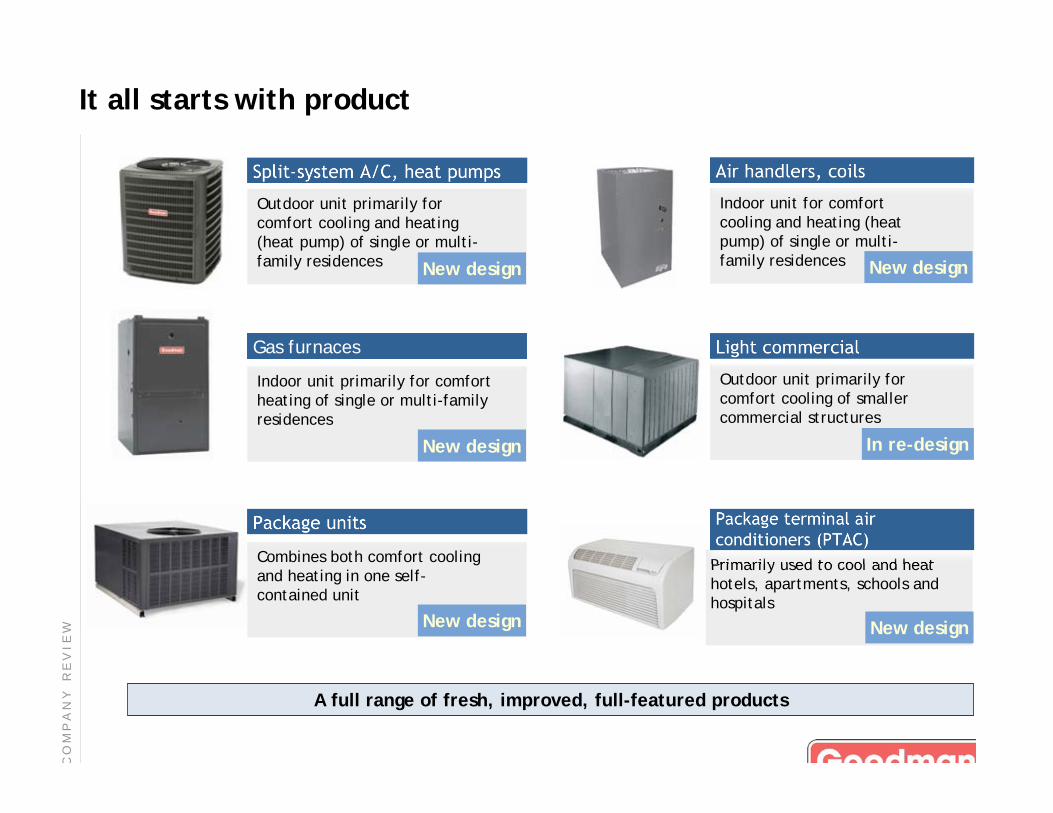

Primarily used to cool and heathotels, apartments, schools andhospitals

Indoor unit for comfortcooling and heating (heatpump) of single or multi-family residences

It all starts with product

Package Units

A full range of fresh, improved, full-featured products

Outdoor unit primarily forcomfort cooling of smallercommercial structures

Combines both comfort coolingand heating in one self-contained unit

Indoor unit primarily for comfortheating of single or multi-familyresidences

Split-system A/C, heat pumps

Outdoor unit primarily forcomfort cooling and heating(heat pump) of single or multi-family residences

Package terminal airconditioners (PTAC)

Light commercial

Air handlers, coils

Package units

Gas furnaces

New design

New design

New design New design

In re-design

New design

C O

M P

A N

Y R

E V

I E

W

Goodman value: reliable performance and a better price

1992: First in industry to offer 5-year parts warranty on all products

2004: First in industry to offer lifetime compressor warranty on highefficiency products

2007: First in industry to offer 10-year parts warranty on all products

2004 2005 2006 2007F

Supplier defects (per million)

0.2%

2004 2005 2006 2007F

Service incident rate

1.0%

2004 – 2006: 25% improvement2007: Equivalent to 6 results

C O

M P

A N

Y R

E V

I E

W

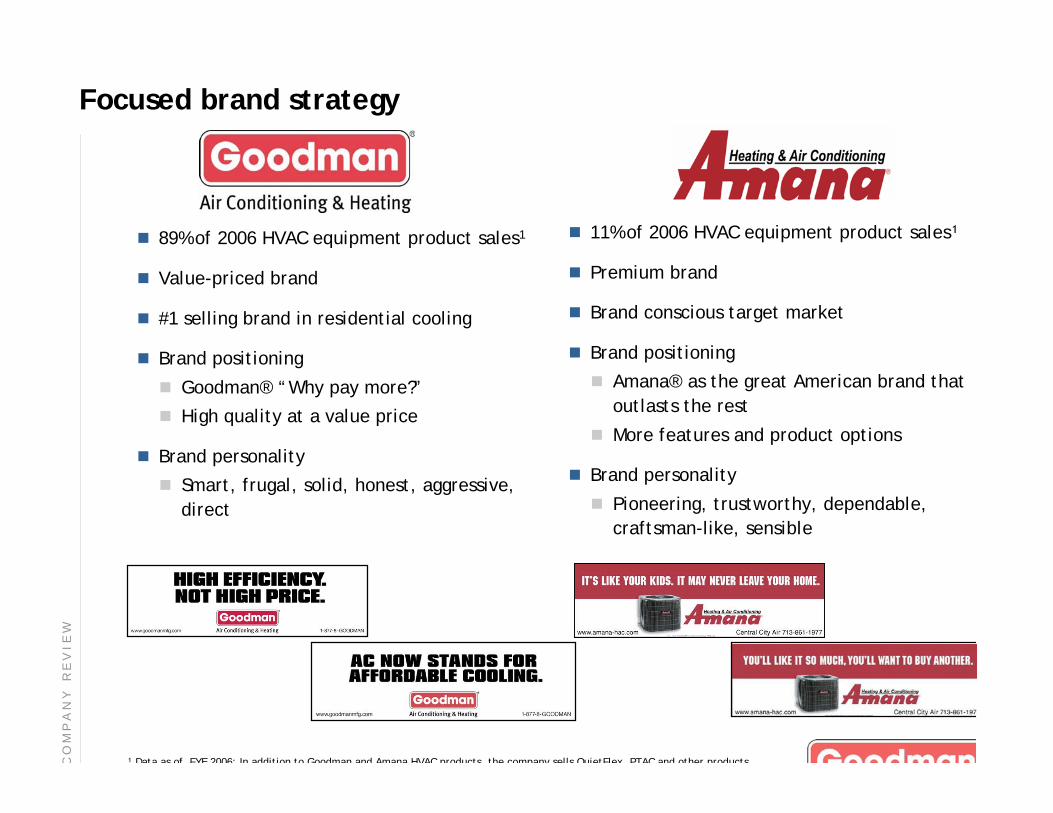

Focused brand strategy

89% of 2006 HVAC equipment product sales1

Value-priced brand

#1 selling brand in residential cooling

Brand positioning

Goodman® “Why pay more?”

High quality at a value price

Brand personality

Smart, frugal, solid, honest, aggressive,

direct

11% of 2006 HVAC equipment product sales

Premium brand

Brand conscious target market

Brand positioning

Amana® as the great American brand that

outlasts the rest

More features and product options

Brand personality

Pioneering, trustworthy, dependable,

craftsman-like, sensible

Data as of FYE 2006; In addition to Goodman and Amana HVAC products the company sells QuietFlex PTAC and other productsC O

M P

A N

Y R

E V

I E

W

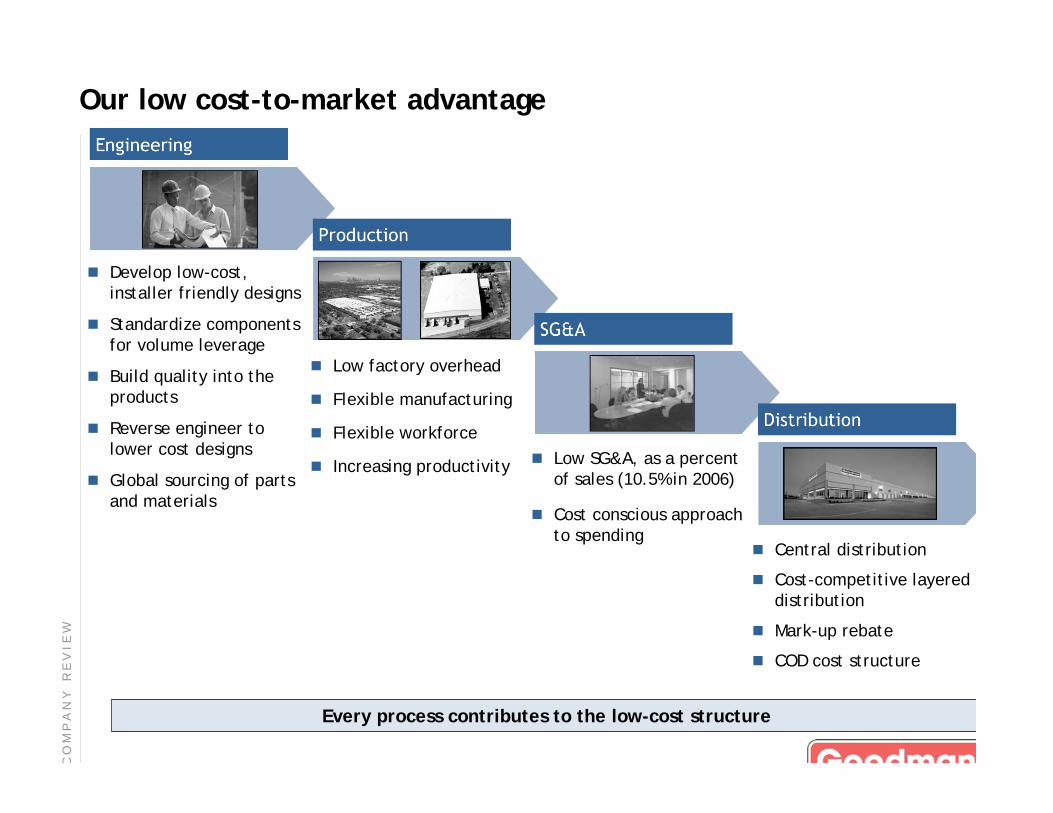

Production

Distribution

SG&A

Engineering

Our low cost-to-market advantage

Develop low-cost,installer friendly designs

Standardize componentsfor volume leverage

Build quality into theproducts

Reverse engineer tolower cost designs

Global sourcing of partsand materials

Low factory overhead

Flexible manufacturing

Flexible workforce

Increasing productivity Low SG&A, as a percentof sales (10.5% in 2006)

Cost conscious approachto spending

Central distribution

Cost-competitive layereddistribution

Mark-up rebate

COD cost structure

Every process contributes to the low-cost structure

C O

M P

A N

Y R

E V

I E

W

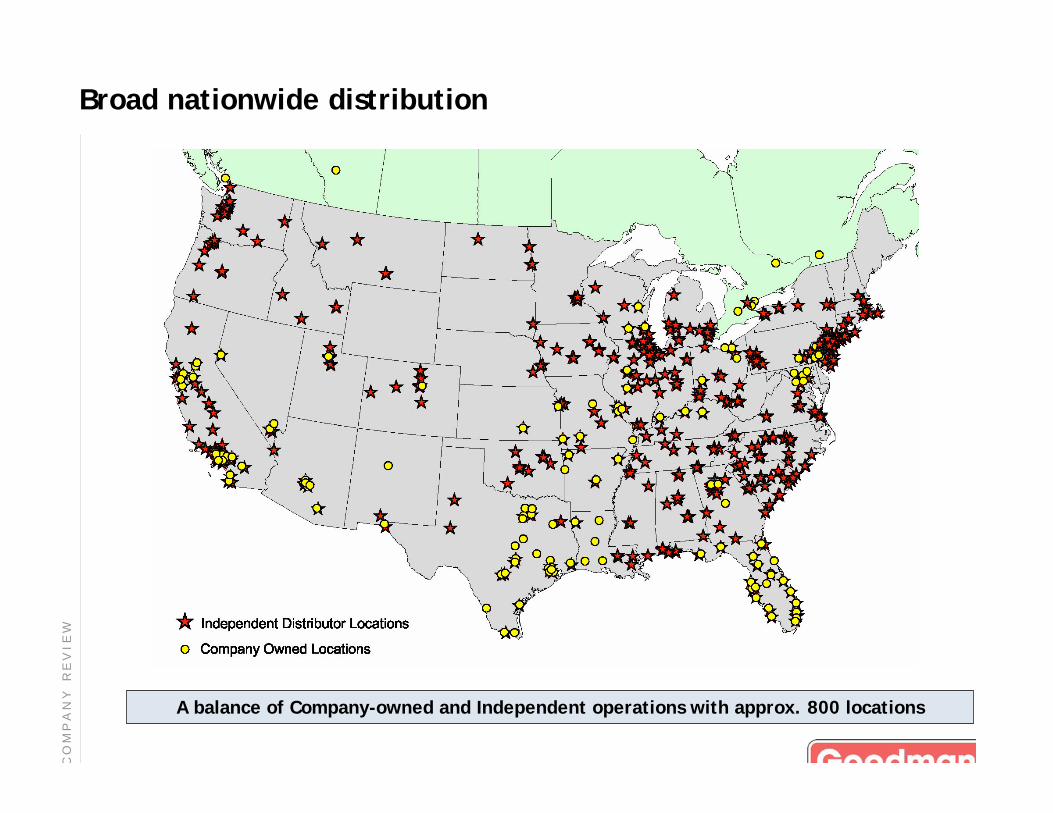

Broad nationwide distribution

A balance of Company-owned and Independent operations with approx. 800 locations

C O

M P

A N

Y R

E V

I E

W

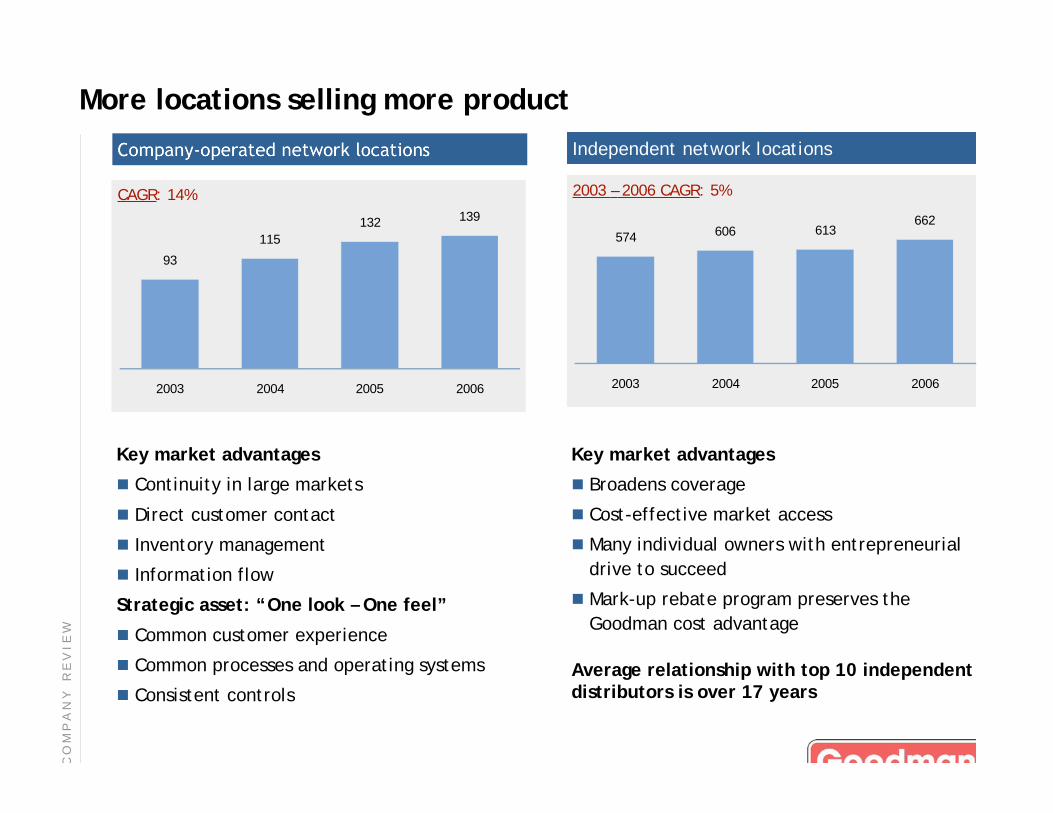

More locations selling more product

93

115

139132

2003 2004 2005 2006

Company-operated network locations

CAGR: 14%

Independent network locations

574606

662613

2003 2004 2005 2006

2003 – 2006 CAGR: 5%

Key market advantages

Continuity in large markets

Direct customer contact

Inventory management

Information flow

Strategic asset: “One look – One feel”

Common customer experience

Common processes and operating systems

Consistent controls

Key market advantages

Broadens coverage

Cost-effective market access

Many individual owners with entrepreneurial

drive to succeed

Mark-up rebate program preserves the

Goodman cost advantage

Average relationship with top 10 independentdistributors is over 17 years

C O

M P

A N

Y R

E V

I E

W

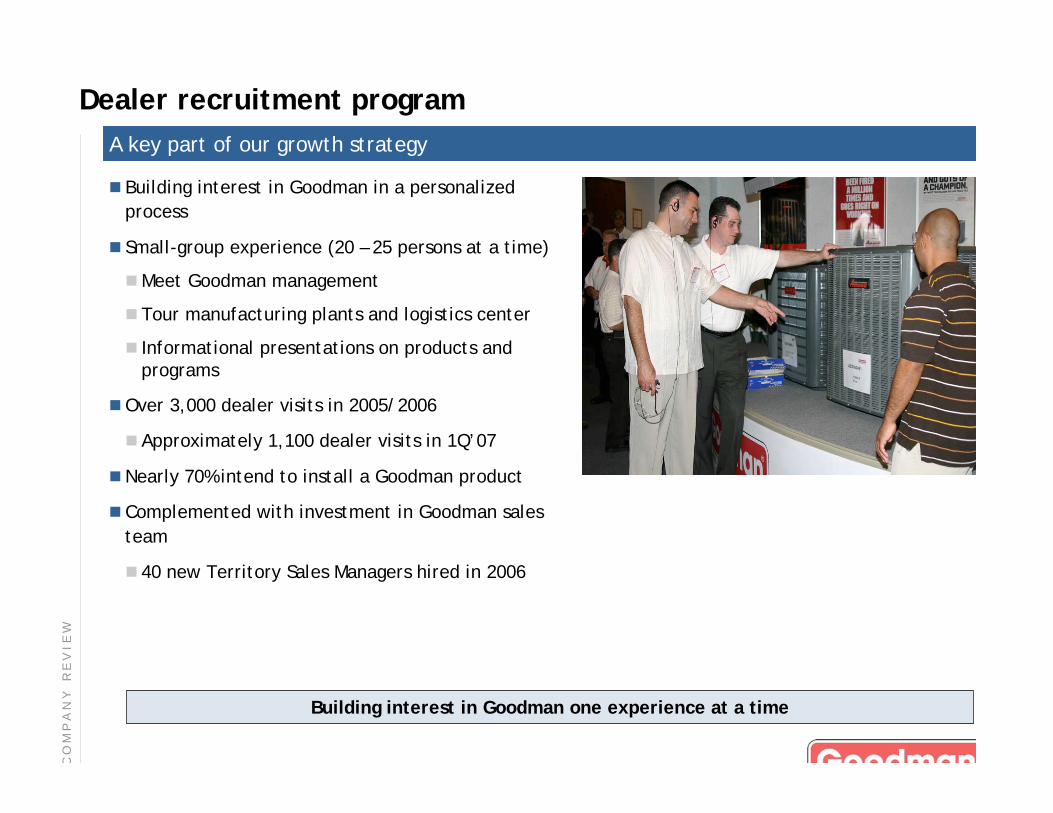

Dealer recruitment program

A key part of our growth strategy

Building interest in Goodman in a personalized

process

Small-group experience (20 – 25 persons at a time)

Meet Goodman management

Tour manufacturing plants and logistics center

Informational presentations on products andprograms

Over 3,000 dealer visits in 2005/2006

Approximately 1,100 dealer visits in 1Q’07

Nearly 70% intend to install a Goodman product

Complemented with investment in Goodman sales

team

40 new Territory Sales Managers hired in 2006

Building interest in Goodman one experience at a time

C O

M P

A N

Y R

E V

I E

W

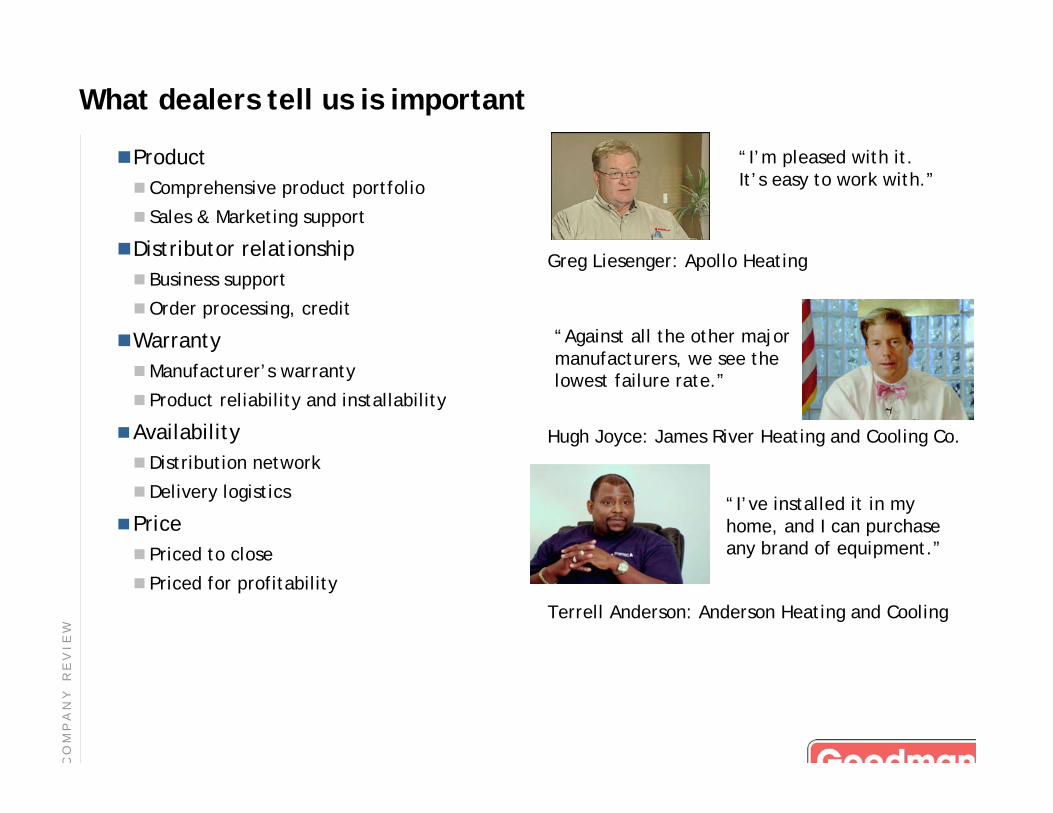

Product

Comprehensive product portfolio

Sales & Marketing support

Distributor relationship

Business support

Order processing, credit

Warranty

Manufacturer’s warranty

Product reliability and installability

Availability

Distribution network

Delivery logistics

Price

Priced to close

Priced for profitability

What dealers tell us is important

Greg Liesenger: Apollo Heating

“I’m pleased with it.It’s easy to work with.”

Hugh Joyce: James River Heating and Cooling Co.

“Against all the other majormanufacturers, we see thelowest failure rate.”

“I’ve installed it in myhome, and I can purchaseany brand of equipment.”

Terrell Anderson: Anderson Heating and Cooling

C O

M P

A N

Y R

E V

I E

W

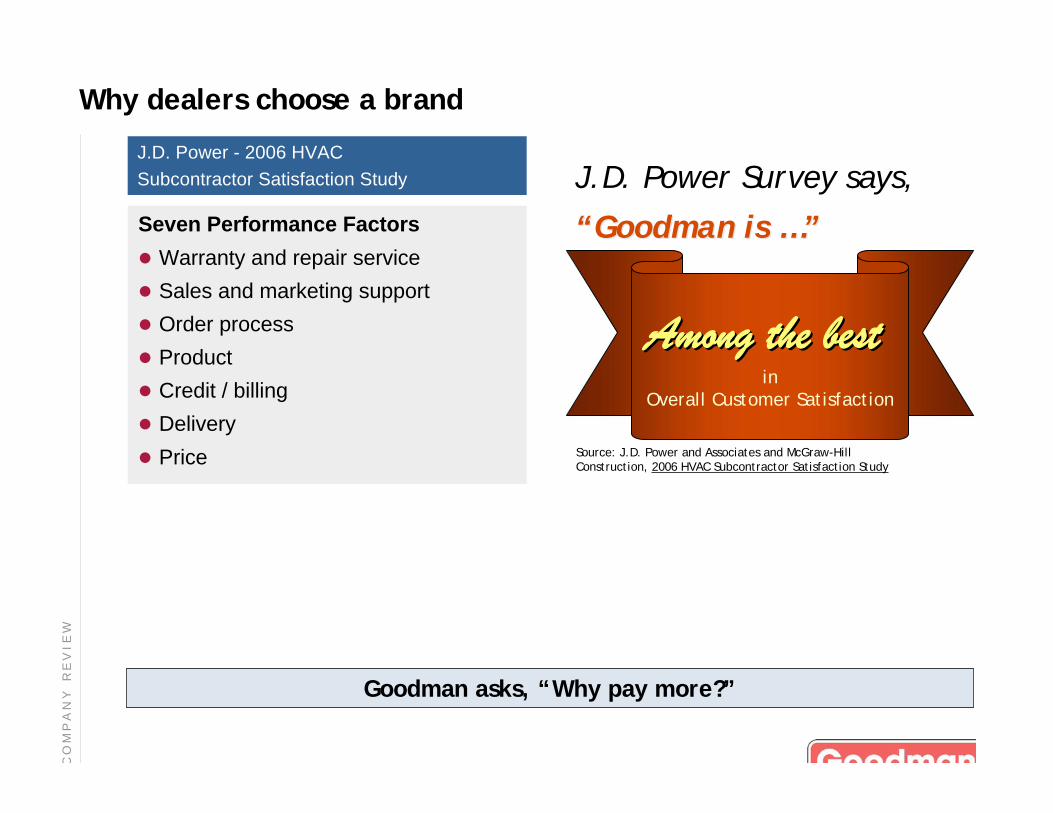

Why dealers choose a brand

Source: J.D. Power and Associates and McGraw-HillConstruction, 2006 HVAC Subcontractor Satisfaction Study

Among the bestAmong the best in

Overall Customer Satisfaction

J.D. Power - 2006 HVAC

Subcontractor Satisfaction Study

Seven Performance Factors

Warranty and repair service

Sales and marketing support

Order process

Product

Credit / billing

Delivery

Price

J.D. Power Survey says,

““Goodman is Goodman is …”…”

Goodman asks, “Why pay more?”

C O

M P

A N

Y R

E V

I E

W

2007 outlook & long-term objectives

Business strategy

Company review

Appendix

Business strategy

B U

S I N

E S

S S

T R

A T

E G

Y

Maintain low-cost and value

leadership

Expand and strengthen distribution

networks

Increase dealer base

Grow in selected markets

Develop and introduce new products

and new technologies

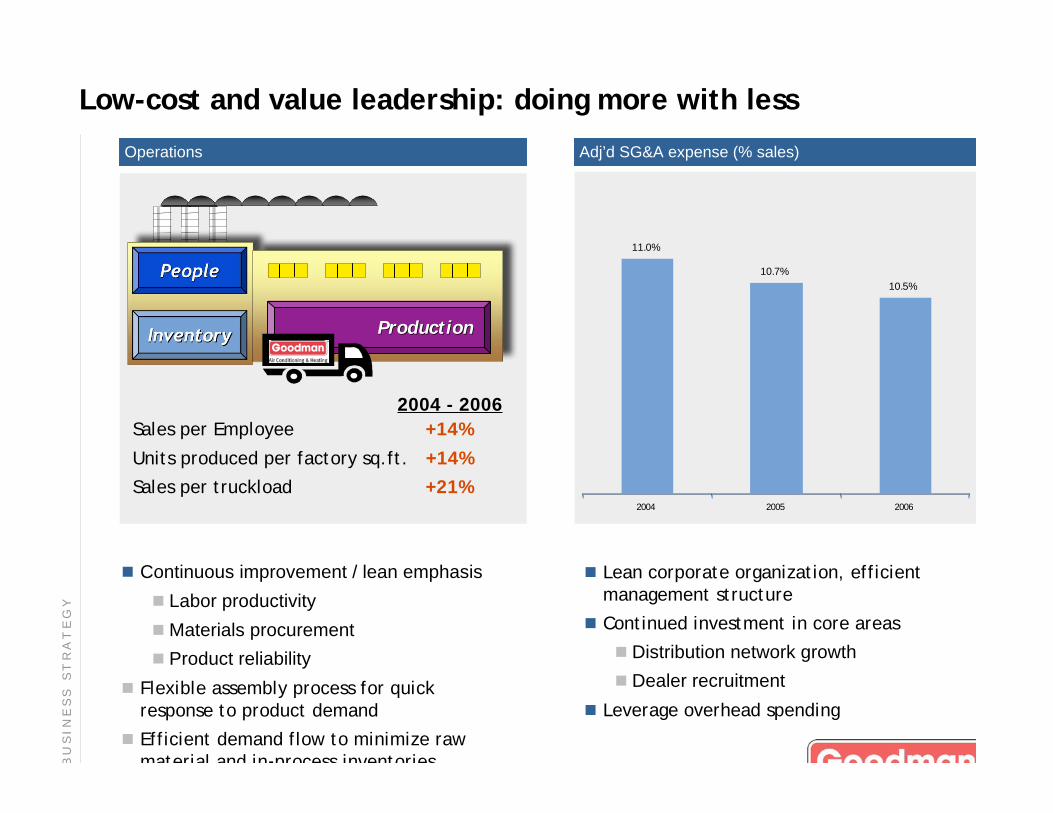

Low-cost and value leadership: doing more with less

B U

S I N

E S

S S

T R

A T

E G

Y

11.0%

10.7%

10.5%

2004 2005 2006

Adj’d SG&A expense (% sales)

Lean corporate organization, efficientmanagement structure

Continued investment in core areas

Distribution network growth

Dealer recruitment

Leverage overhead spending

PeoplePeople

InventoryInventory ProductionProduction

2004 - 2006

Operations

Sales per Employee +14%

Units produced per factory sq.ft. +14%

Sales per truckload +21%

Continuous improvement / lean emphasis

Labor productivity

Materials procurement

Product reliability

Flexible assembly process for quickresponse to product demand

Efficient demand flow to minimize rawmaterial and in process inventories

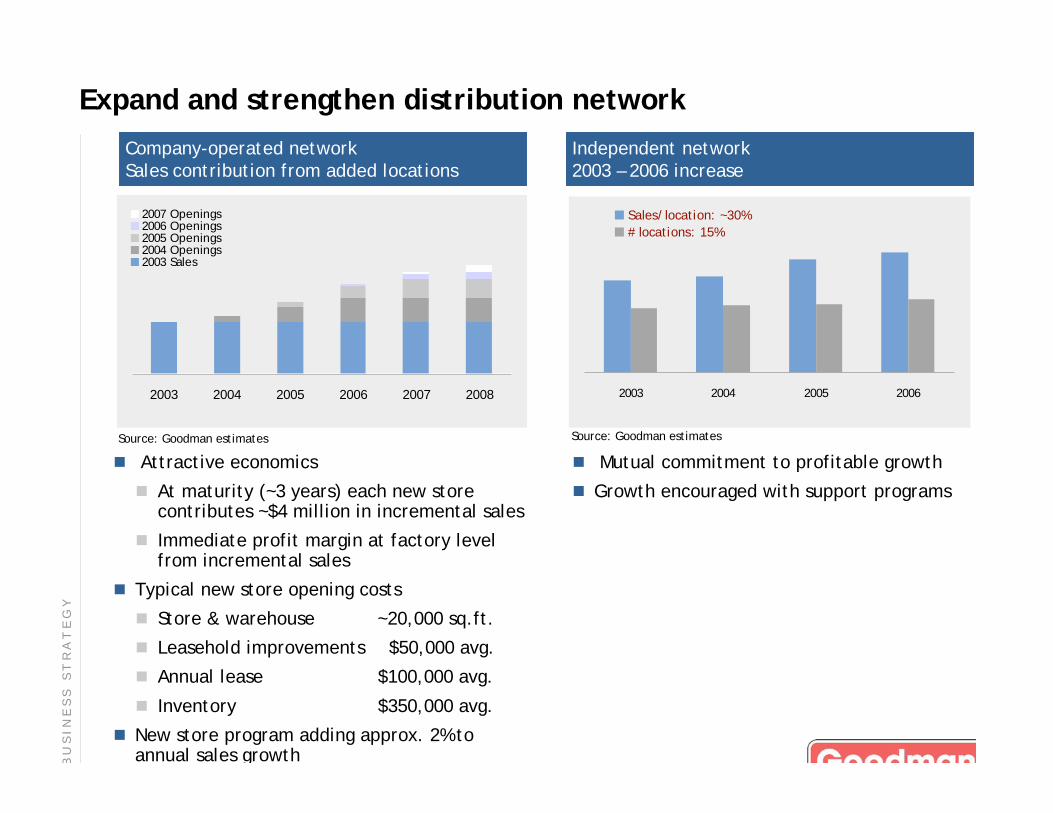

Expand and strengthen distribution network

2003 2004 2005 2006

Sales/location: ~30%

# locations: 15%

Attractive economics

At maturity (~3 years) each new storecontributes ~$4 million in incremental sales

Immediate profit margin at factory levelfrom incremental sales

Typical new store opening costs

Store & warehouse ~20,000 sq.ft.

Leasehold improvements $50,000 avg.

Annual lease $100,000 avg.

Inventory $350,000 avg.

New store program adding approx. 2% toannual sales growth

2003 2004 2005 2006 2007 2008

2007 Openings2006 Openings2005 Openings2004 Openings2003 Sales

Company-operated networkSales contribution from added locations

Independent network2003 – 2006 increase

Source: Goodman estimatesSource: Goodman estimates

Mutual commitment to profitable growth

Growth encouraged with support programs

B U

S I N

E S

S S

T R

A T

E G

Y

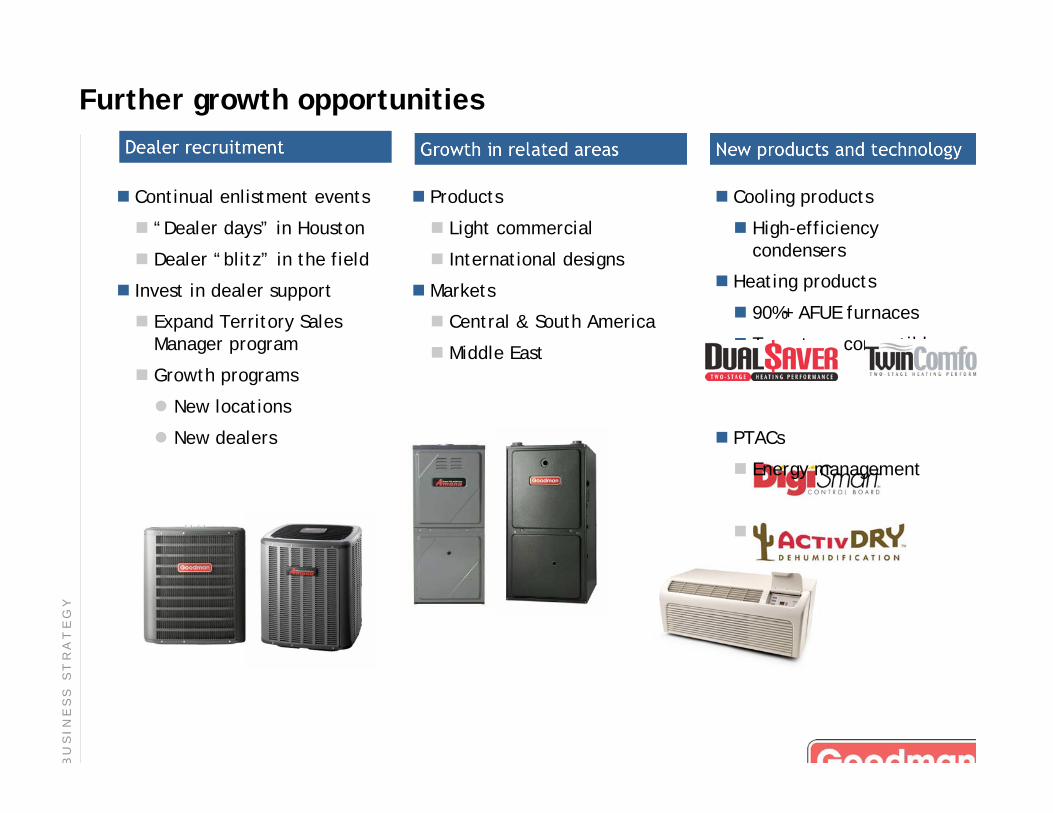

Cooling products

High-efficiencycondensers

Heating products

90%+ AFUE furnaces

Two-stage convertibles

PTACs

Energy management

Comfort control

Further growth opportunities

Growth in related areas New products and technologyDealer recruitment

Continual enlistment events

“Dealer days” in Houston

Dealer “blitz” in the field

Invest in dealer support

Expand Territory SalesManager program

Growth programs

New locations

New dealers

Products

Light commercial

International designs

Markets

Central & South America

Middle East

B U

S I N

E S

S S

T R

A T

E G

Y

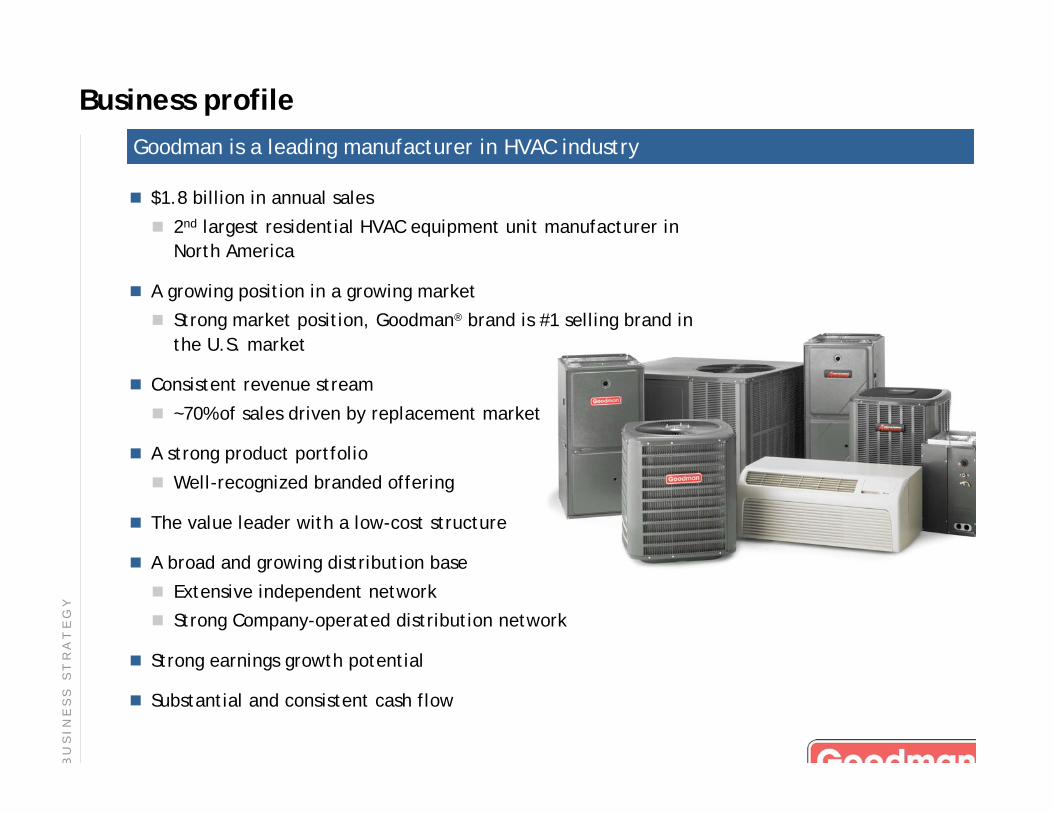

Business profile

$1.8 billion in annual sales

2nd largest residential HVAC equipment unit manufacturer in

North America

A growing position in a growing market

Strong market position, Goodman® brand is #1 selling brand in

the U.S. market

Consistent revenue stream

~70% of sales driven by replacement market

A strong product portfolio

Well-recognized branded offering

The value leader with a low-cost structure

A broad and growing distribution base

Extensive independent network

Strong Company-operated distribution network

Strong earnings growth potential

Substantial and consistent cash flow

Goodman is a leading manufacturer in HVAC industry

B U

S I N

E S

S S

T R

A T

E G

Y

2007 outlook & long-term objectives

Business strategy

Company review

Appendix

2006 results & 2007 outlook

$1,318

$1,565

$1,795

2004 2005 2006 2007F

$226

$194

$164

2004 2005 2006 2007F

22.7%

23.1% 23.1%

2004 2005 2006 2007F

Net sales ($ millions) Adjusted gross margin (% sales) Adjusted EBITDA ($ millions)

$255 - $265

Outsold the industry

Revenues increased 15%

Adjusted gross margins held at23.1%

13-SEER transition benefits

Operating efficiencies

Commodity cost increases

Adjusted SG&A expense ratioimproved 20 bp

Sales per employee increased 10%

Complete transition to 13+ SEER

Decline in residential newconstruction

2006 price increases

Copper and aluminum costincreases

Productivity gains

Investment in growing distributionnetwork and dealer recruitment

EBITDA

$255 million to $265 million

Earnings per share

$1.30 to $1.40

Excluding gain on property sale

Debt reduction

Approx. $120 million

2 0

0 7

O

U T

L O

O K

&

L

O N

G -

T E

R M

O

B J

E C

T I V

E S

2006 results 2007 outlook 2007 forecast

1Q’07 results: A good start

$268

$296

$381 $380

1Q'04 1Q'05 1Q'06 1Q'07

$26

$29

$41

$32

1Q'04 1Q'05 1Q'06 1Q'07

22.5% 22.3% 22.6%

20.3%

1Q'04 1Q'05 1Q'06 1Q'07

Net sales ($ millions) Adjusted gross margin (% sales) Adjusted EBITDA ($ millions)

Net sales:

HVAC industry’s best reportedsales performance

Significant decline in residentialnew construction market

Carryover of 2006 price increases

Further 13 SEER transition

Benefit from dealer recruitmentand promotional activities

3 Yr CAGR: 12%

Gross margin:

13 SEER transition benefits

Copper and aluminum costincreases above price increases

Factory productivity

Continued investments indistribution network and dealerrecruitment

1Q’07, adjusted for $10mm, net,commodities impact

Adj’d gross margin = 22.9%

Adj’d EBITDA = $42 million

C diti h d i l

Cash flow:

Improved inventory levels

Capital spending in line

Debt well below prior year level

2 0

0 7

O

U T

L O

O K

&

L

O N

G -

T E

R M

O

B J

E C

T I V

E S

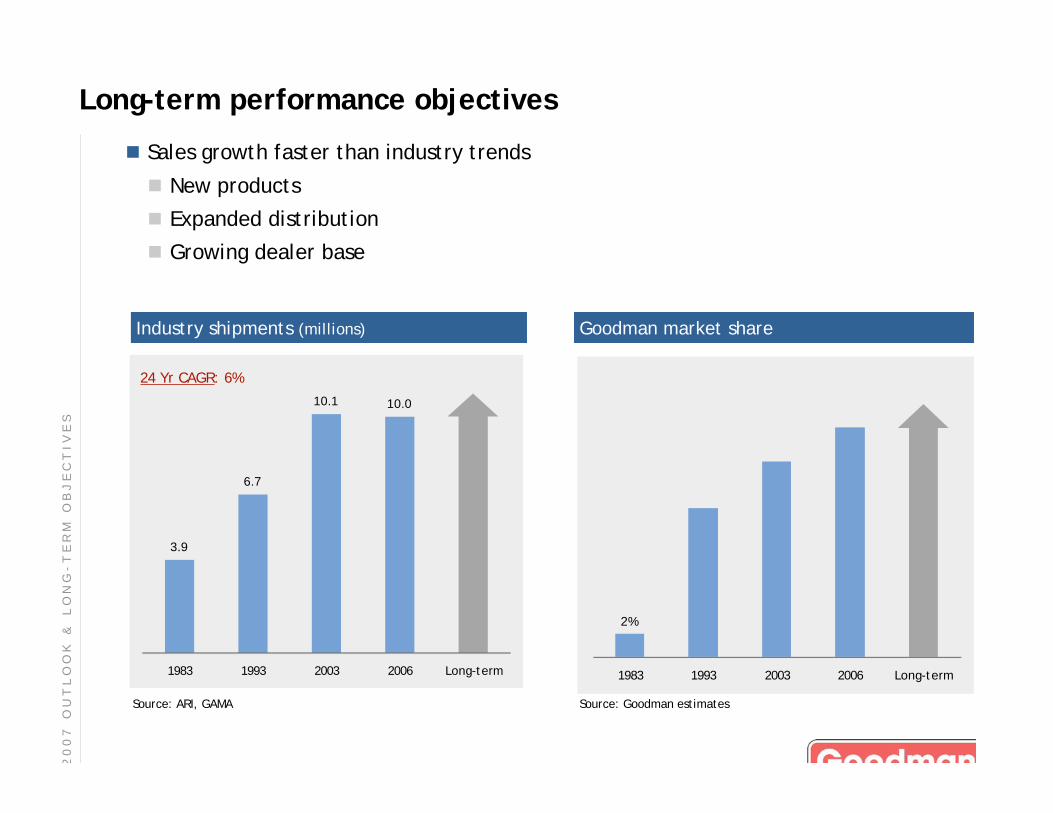

Long-term performance objectives

Sales growth faster than industry trends

New products

Expanded distribution

Growing dealer base

2%

1983 1993 2003 2006 Long-term

Goodman market share

3.9

6.7

10.1 10.0

1983 1993 2003 2006 Long-term

Industry shipments (millions)

24 Yr CAGR: 6%

2 0

0 7

O

U T

L O

O K

&

L

O N

G -

T E

R M

O

B J

E C

T I V

E S

Source: Goodman estimatesSource: ARI, GAMA

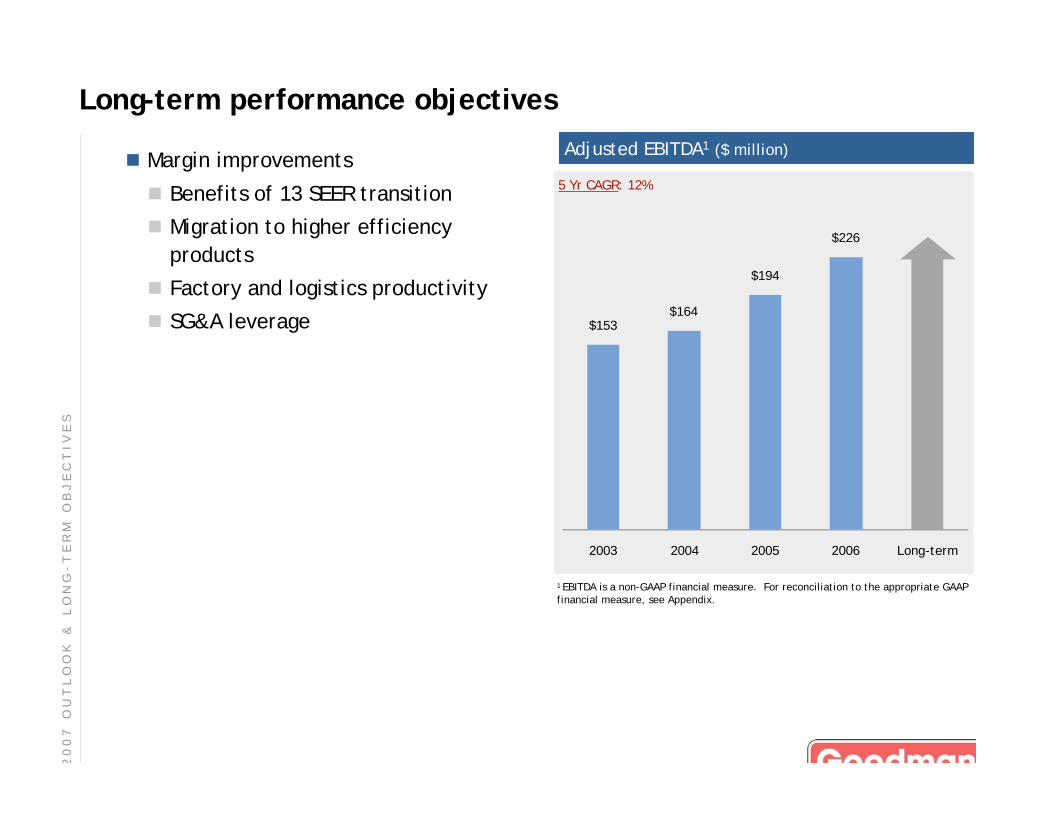

Long-term performance objectives

Margin improvements

Benefits of 13 SEER transition

Migration to higher efficiency

products

Factory and logistics productivity

SG&A leverage

Adjusted EBITDA1 ($ million)

$153$164

$194

$226

2003 2004 2005 2006 Long-term

1 EBITDA is a non-GAAP financial measure. For reconciliation to the appropriate GAAPfinancial measure, see Appendix.

5 Yr CAGR: 12%

2 0

0 7

O

U T

L O

O K

&

L

O N

G -

T E

R M

O

B J

E C

T I V

E S

Long-term performance objectives

Strong cash flow

Modest capital spending needs

Working capital leverage

Cash tax benefit

Declining debt levels

2.0

3.7

4.8

6.2

1.4

2003 2004 2005 2006 Long-term

Net debt to adjusted EBITDA ratio

Apollo

Acquisition

3.0

2 0

0 7

O

U T

L O

O K

&

L

O N

G -

T E

R M

O

B J

E C

T I V

E S

Cash redeployment

Fund core growth

Product development

Growth capacity

Distribution expansion

Dividends / stock repurchases / debt reduction

Debt-to-EBITDA between 2.0x and 3.0x

Acquisitions

Low priority

2 0

0 7

O

U T

L O

O K

&

L

O N

G -

T E

R M

O

B J

E C

T I V

E S

Summary

Attractive industry structure

Strong and improving market position

Consistent revenue stream driven by non-cyclical replacement demand

Extensive and growing distribution network

Expanding dealer base

The low-cost, value leader with industry leading EBIT margins

Significant opportunities for continued sales and earnings growth

Substantial and consistent cash flow

2 0

0 7

O

U T

L O

O K

&

L

O N

G -

T E

R M

O

B J

E C

T I V

E S

2007 outlook & long-term objectives

Business strategy

Company review

Appendix

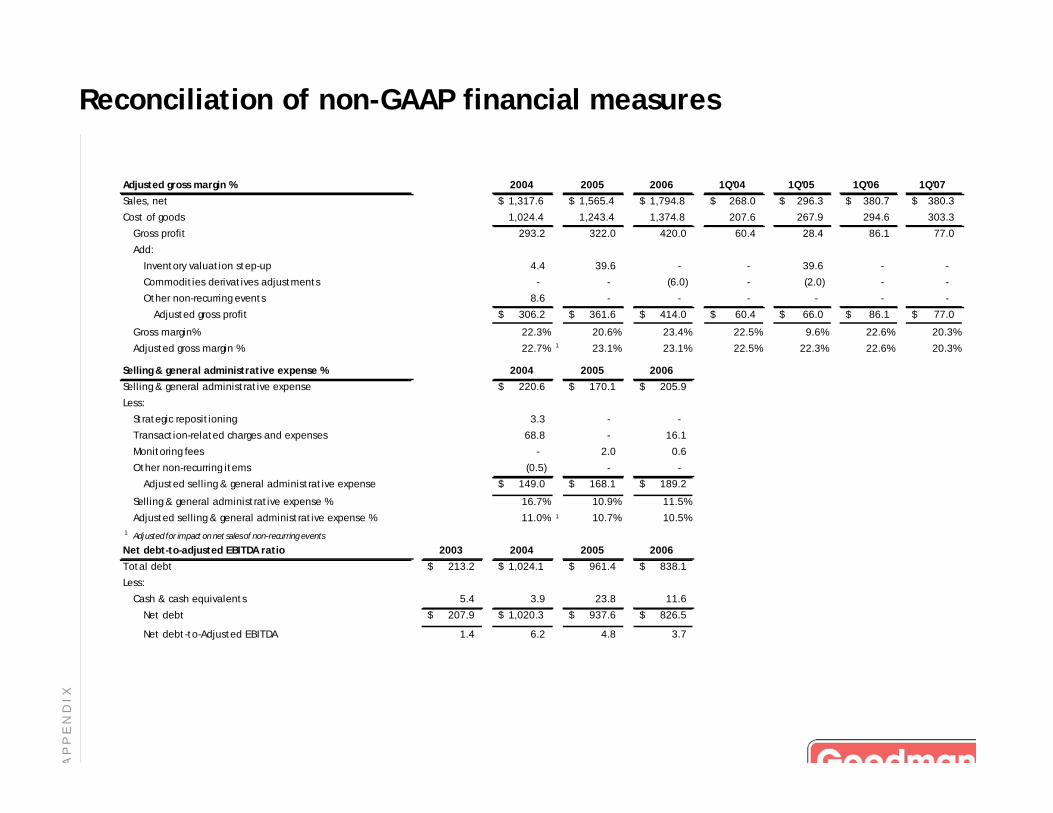

Reconciliation of non-GAAP financial measures

A P

P E

N D

I X

EBITDA & Adjusted EBITDA 2003 2004 2005 2006 1Q'04 1Q'05 1Q'06 1Q'07

Net Income 87.4$ 47.7$ 24.9$ 64.2$ 17.2$ (21.0)$ 8.4$ 4.6$

Add:

Provision for income taxes 1.7 (5.1) 15.8 34.2 (0.3) (12.8) 4.9 2.4

Interest expense, net 26.1 12.5 74.2 77.8 3.2 18.2 19.7 16.9

Depreciation and amortization expense 14.8 18.9 37.7 32.6 4.0 6.6 7.5 8.3

EBITDA 130.0$ 74.0$ 152.6$ 208.8$ 24.1$ (9.0)$ 40.5$ 32.2$

Add:

Strategic repositioning 4.2 3.3 - - 0.4$ -$ -$ -$

Inventory valuation step-up - 4.4 39.6 - - 39.6 - -

Transaction-related charges and expenses - 68.8 - 16.1 - - - -

Monitoring fees - - 2.0 0.6 - 0.5 0.6 -

Gain on commodities derivative - - - - - (2.0) - -

Gain on sale of property - - - - - - - (0.6)

Other non-recurring items 18.7 13.8 - - 1.4 - - -

Adjusted EBITDA 152.9$ 164.3$ 194.2$ 225.5$ 25.9$ 29.1$ 41.1$ 31.6$

Reconciliation of non-GAAP financial measures

A P

P E

N D

I X

Adjusted gross margin % 2004 2005 2006 1Q'04 1Q'05 1Q'06 1Q'07

Sales, net 1,317.6$ 1,565.4$ 1,794.8$ 268.0$ 296.3$ 380.7$ 380.3$

Cost of goods 1,024.4 1,243.4 1,374.8 207.6 267.9 294.6 303.3

Gross profit 293.2 322.0 420.0 60.4 28.4 86.1 77.0

Add:

Inventory valuation step-up 4.4 39.6 - - 39.6 - -

Commodities derivatives adjustments - - (6.0) - (2.0) - -

Other non-recurring events 8.6 - - - - - -

Adjusted gross profit 306.2$ 361.6$ 414.0$ 60.4$ 66.0$ 86.1$ 77.0$

Gross margin% 22.3% 20.6% 23.4% 22.5% 9.6% 22.6% 20.3%

Adjusted gross margin % 22.7% 1 23.1% 23.1% 22.5% 22.3% 22.6% 20.3%

Selling & general administrative expense % 2004 2005 2006

Selling & general administrative expense 220.6$ 170.1$ 205.9$

Less:

Strategic repositioning 3.3 - -

Transaction-related charges and expenses 68.8 - 16.1

Monitoring fees - 2.0 0.6

Other non-recurring items (0.5) - -

Adjusted selling & general administrative expense 149.0$ 168.1$ 189.2$

Selling & general administrative expense % 16.7% 10.9% 11.5%

Adjusted selling & general administrative expense % 11.0% 1 10.7% 10.5%

1Adjusted for impact on net sales of non-recurring events

Net debt-to-adjusted EBITDA ratio 2003 2004 2005 2006

Total debt 213.2$ 1,024.1$ 961.4$ 838.1$

Less:

Cash & cash equivalents 5.4 3.9 23.8 11.6

Net debt 207.9$ 1,020.3$ 937.6$ 826.5$

Net debt-to-Adjusted EBITDA 1.4 6.2 4.8 3.7

Forward looking statements

This presentation contains forward-looking statements. The words “believe,” “expect,” “anticipate,” “intend,”“estimate” and other expressions that are predictions of or indicate future events and trends and that do not relate tohistorical matters identify forward-looking statements. Forward-looking statements also include statements about thefollowing subjects:

• changes in weather patterns and seasonal fluctuations;

• changes in customer demand related to the 13 SEER federally mandated minimum efficiency standard;

• the maturation of our new company-operated distribution centers;

• increased competition and technological changes and advances;

• increases in the cost of raw materials and components;

• our relations with our independent distributors; and

• damage or injury caused by our products.

Although forward-looking statements reflect management’s good faith beliefs, they involve known and unknown risks,uncertainties and other factors, which may cause the actual results, performance or achievements to differ materiallyfrom anticipated future results, performance or achievements expressed or implied by such forward-looking statements.We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of newinformation, future events, changed circumstances or otherwise. These forward-looking statements are subject tonumerous risks and uncertainties, including, but not limited to, the impact of general economic conditions in the regionsin which we do business; general industry conditions, including competition and product, raw material and energy prices;the realization of expected tax benefits; changes in exchange rates and currency values; capital expenditurerequirements; access to capital markets and the risks and uncertainties described under “Risk Factors” in our recent SECfilings.

A P

P E

N D

I X

J P M O R G A N H V A C C O N F E R E N C E