Embed Size (px)

DESCRIPTION

Audit experience

Citation preview

Journal of Accounting,Auditing & Finance

2015, Vol. 30(1) 78–100�The Author(s) 2014

Reprints and permissions:sagepub.com/journalsPermissions.nav

DOI: 10.1177/0148558X14544503jaf.sagepub.com

The Effect of Audit Experienceon Audit Fees and AuditQuality

Steven F. Cahan1 and Jerry Sun2

Abstract

Prior research on audit experience focuses on behavioral studies that are conducted byrunning experiments. Although these studies provide evidence on the role of experience incompleting specific audit tasks, they do not shed light on how experience affects a com-plete audit engagement. We conduct an archival study to examine the effect of audit experi-ence on audit fees and audit quality. Using unique data from China, where the signees ofthe audit report can be identified and linked with a government database containing per-sonal information about certified public accountants, we find that experience is positivelyassociated with audit fees and negatively associated with absolute discretionary accruals.Furthermore, we extend the research on personal characteristics of audit partners by con-sidering the incremental effects of gender, education, engagement tenure, industry speciali-zation, and client importance after controlling for overall audit experience. Overall, ourresults suggest that the auditors’ personal characteristics may serve as a signal of the levelof care that will be exercised during the audit process. Our results also have implicationsfor China’s recently announced regulation that would require localization of Big 4 offices inChina.

Keywords

audit experience, individual auditors, audit fees, audit quality, audit partners

Introduction

We examine the effect of an individual’s overall audit experience on audit fees and audit

quality using unique archival data. Prior behavioral research examines the relationship

between individual auditors’ audit experience and audit judgments (e.g., Bonner, 1990;

Libby & Frederick, 1990; Moeckel, 1990; Simnett, 1996). These behavioral studies argue

that experienced auditors have greater knowledge and more developed memory structures

than inexperienced auditors, which leads to more accurate judgments by experienced audi-

tors, but the results of these studies are mixed. Bonner (1990) contends that the mixed

1The University of Auckland, New Zealand2University of Windsor, Ontario, Canada

Corresponding Author:

Jerry Sun, Odette School of Business, University of Windsor, 401 Sunset Ave., Windsor, Ontario, Canada N9B

3P4.

Email: [email protected]

Article

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

findings could result from a failure to incorporate task-specific knowledge in the test instru-

ment, suggesting that the results may be sensitive to the experimental design. Moreover,

behavioral research focuses on manipulated specific audit tasks rather than the body of

audit work completed for a client. To complement this stream of behavioral research, we

examine the effects of audit experience using an archival approach.

Archival research based on individual auditors’ personal characteristics is extremely rare

because of limited data availability. The difficulty of using individual auditors’ data in

archival research usually arises for two reasons: (a) the audit partner’s name is not dis-

closed in the audit report, and (b) even where the partner’s name is disclosed in the audit

report, information about the personal characteristics of that partner has not been publicly

available. A few studies focus on audit partner tenure (e.g., Carey & Simnett, 2006; C. Y.

Chen, Lin, & Lin, 2008; Manry, Mock, & Turner, 2008). These studies use the number of

years for which a partner has served as the engagement partner for the same company.

However, strictly speaking, audit partner tenure for a particular company is not a personal

characteristic of the partner; rather, it is an engagement characteristic. In this study, we

focus on the audit partner’s overall experience, that is, the number of years that an individ-

ual has been engaged in audit work, using unique data from China.

The Chinese audit context is unique because regulations require that the names of the

two Certified Public Accountants (CPAs) who sign the audit report be disclosed and

because it is possible to obtain some personal information about individual auditors from

the Chinese Securities Regulatory Commission (CSRC), which oversees the licensing of

auditors who audit listed companies. Thus, we are able to examine the effect of an auditor’s

overall audit experience (as opposed to engagement experience) on audit fees and audit

quality after controlling for gender, education, industry experience, engagement tenure, and

client importance. We document a positive association between audit fees and the aggre-

gate audit experience of the two signee auditors, suggesting that clients pay fee premiums

to have their audits led by more experienced CPAs. As the audit fee reflects the hours and

billing rates of the entire audit team, it is unlikely that this result is merely reflecting the

higher charge out rate of more experienced lead auditors. More important, we find that cli-

ents of more experienced CPAs have lower absolute discretionary accruals than clients of

less experienced CPAs, suggesting that experienced auditors are better able to constrain

earnings management. Combined, this suggests that more experienced lead auditors can

conduct higher quality audits and that clients are willing to pay a premium for this quality.

Overall, our results suggest that the lead auditors’ personal characteristics may proxy for

the level of care that will be exercised during the audit process, and thus may help mitigate

information problems in a setting where the client cannot fully observe the quality of the

audit.

Our study complements the work of Gul, Wu, and Yang (2013) who also use data from

individual auditors in China. They focus on estimating individual auditor fixed effects and

find that including these fixed effects significantly improves the explanatory power of

regression models that seek to explain differences in audit quality (e.g., abnormal accruals,

small profits). However, they find that only a small portion of the individual auditor fixed

effects can be explained by demographic characteristics related to the auditor. Rather than

focus on individual auditor fixed effects, we focus on the average effect of auditor experi-

ence. That is, we are not interested in how the auditor experience-audit quality relation dif-

fers between individual auditors; instead, we are interested in whether auditor experience is

related to audit quality at a general level. Furthermore, while Gul et al. (2013) consider

auditor experience specifically, they define it based on the number of years of Big N

Cahan and Sun 79

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

experience. We define experience as overall auditor experience which is important because,

as Gul et al. (2013) note, the Big N have relatively small market shares in China. Finally,

we also consider how auditor experience affects the price of an audit while Gul et al.

(2013) do not.

Our study contributes to the literature in two additional ways. First, our research com-

plements the behavioral research on audit experience. The behavioral studies document

mixed evidence on the relationship between audit experience and audit judgments. As these

studies were conducted by designing specific audit tasks, they are unable to test the effect

of audit experience on the complete audit engagement. Thus, unlike behavioral research,

we are able to examine the implications of audit experience in a broader context. Second,

our study extends a small but important stream of archival research that focuses on individ-

ual audit partners. Prior studies focus on engagement tenure rather than overall audit expe-

rience. The effects of a longer engagement tenure should mainly reflect the auditor’s

client-specific knowledge. By controlling for engagement tenure as well as auditors’ indus-

try experience, we are able to isolate the role of overall experience—a measure of general

knowledge—from client-specific knowledge and industry knowledge. We find evidence

that greater general knowledge can reduce earnings management and increase audit quality.

Our research has also practical importance. In May 2012, the Ministry of Finance in

China regulated that foreign partners in a Big 4 Chinese office should be not more than

20% by 2017, and the chief partner of the office should be a Chinese citizen. This regula-

tion was announced 1 day after the Securities and Exchange Commission (SEC) charged

Deloitte’s Shanghai office for failing to produce audit documents for a Chinese client, a

violation of the Sarbanes–Oxley Act that requires the Public Company Accounting

Oversight Board (PCAOB) to inspect non-U.S. auditors who audit U.S.-listed firms (e.g.,

‘‘Accounting in China,’’ 2012). Together, these events raise questions about the quality and

experience of Chinese auditors. Our results suggest that audit quality increases with overall

audit experience, which suggests that increasing Chinese auditor involvement in Big 4

offices in China is unlikely to diminish audit quality in the long run as Chinese auditors

gain greater experience as a result of the new regulation. Whether audit quality will suffer

in the short term is outside the scope of our study, but is an interesting issue for future

research.

The rest of the article is organized as follows. ‘‘Institutional Background’’ section intro-

duces the institutional background. ‘‘Literature Review’’ section reviews the literature.

‘‘Hypotheses’’ section develops the hypotheses. ‘‘Research Design’’ section designs the

research. ‘‘Empirical Results’’ section reports the results. ‘‘Conclusion’’ section concludes.

Institutional Background

On December 25, 1995, the Chinese Ministry of Finance issued the first batch of indepen-

dent audit standards since the People’s Republic of China (PRC) was established in 1949.1

These standards became effective on January 1, 1996. No. 7 Independent Audit

Standards—Audit Report regulated the practices of CPAs issuing audit reports. According

to the standards, CPAs issuing audit reports were required to sign and stamp their individ-

ual names, and to also stamp their accounting firm’s name on the audit report.

Nevertheless, there were no specific requirements on whose names or how many CPAs’

names should be signed and stamped on the audit report.

To reinforce the accountability of CPAs who issue audit reports, the Ministry of Finance

released a supplementary regulation on the signing and stamping CPAs’ names on audit

80 Journal of Accounting, Auditing & Finance

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

reports on July 2, 2001. This regulation, Notice of the Ministry of Finance on Related

Issues of CPAs’ Signature and Seal on Audit Reports, required that the audit report should

be signed and sealed by two CPAs who are licensed to issue the related audit report2 and

should be sealed by the accounting firm of the two CPAs. More specifically, the regulation

requires that the signers should include the audit partner, chief CPA or an entrusted deputy

chief CPA, who makes the final review of the audit, and another CPA who is in charge of

the daily work on the audit.

On April 13, 2003, the Ministry of Finance issued a revised version of No. 7

Independent Audit Standards—Audit Report, which became effective on July 1, 2003.

Similar to the original version, the revised version states that audit reports should be signed

and sealed by CPAs, and also sealed by the accounting firm. In addition, the revised ver-

sion provided a template for the audit reports, which indicated that two CPAs were required

to sign and stamp their names.

On February 15, 2006, the Ministry of Finance issued No. 1501 Audit Standards of

Chinese CPAs—Audit Report to replace No. 7 Independent Audit Standards—Audit Report.

This batch of audit standards became effective from January 1, 2007. With respect to the

requirements on the signature and seal of CPAs on audit reports, it is identical to the prior

audit standard revised in 2003. The specific requirements on who should sign and seal

audit reports are still the same as set out in the Ministry’s Notice that was issued in 2001.

Thus, China has a relatively long history of requiring signatures of the two key auditors on

an engagement.

Literature Review

Audit Experience

Prior research on audit experience was generally conducted by designing experiments or

cases to examine the effect of audit experience on individual auditors’ judgments. Farmer,

Rittenberg, and Trompeter (1987) document that experienced auditors are less likely to

agree with the client’s preferred accounting treatment than inexperienced auditors, whereas

Abdolmohammadi and Wright (1987) find a negative relation between audit experience

and the likelihood of proposing an audit adjustment or qualified opinion. Biggs, Mock, and

Watkins (1988) compare the analytical review of two audit managers with 7 years of audit

experience and two senior auditors with 3 years of audit experience in a case study. They

find that the senior auditors increased workload throughout the revenue cycle, while the

audit managers did so more selectively. Libby and Frederick (1990) investigate the relation

between error frequency knowledge and audit experience.3 Their findings indicate that per-

ceptions about the source of the financial statement error are more accurate for experienced

auditors than for inexperienced auditors.

Moeckel (1990) examines the effect of audit experience on the frequency of two types

of memory errors including failure to integrate and reconstruction.4 She finds that inexper-

ienced auditors fail to integrate more often than experienced auditors, whereas experienced

auditors reconstruct more often than inexperienced auditors. As reconstructions impair

experienced auditors’ ability to integrate and to detect the integration failures of their sub-

ordinates, Moeckel indicates that her findings challenge the intuition that experienced audi-

tors will perform better at all aspects of work paper review. Bonner (1990) notes that the

mixed results on the effect of audit experience on audit judgments may have arisen because

some studies did not consider the role of task-specific knowledge in experimental designs.

Cahan and Sun 81

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

In a study of the effect of information selection, information processing, and task com-

plexity on predictive accuracy of auditors, Simnett (1996) finds that audit experience can

mitigate some of the limitations arising from information selection, but not from informa-

tion processing. Davis (1996) examines whether audit experience affects auditors’

approaches to selecting relevant information and whether selection of more relevant infor-

mation improves auditors’ judgment performance for preliminary control risk assessments.

By comparing new audit seniors and experienced audit seniors from a non-Big 6 account-

ing firm, he finds that experienced senior auditors exhibited a higher level of selective

attention to relevant information than new senior auditors. Moreover, experienced senior

auditors exhibited more consistency between the selected relevant information and the con-

trol risk assessment response, selected fewer cues, and made judgments in less time. In

sum, these experimental studies provide valuable insights about the effects of experience in

specific settings. We complement this research by examining the role of experience on the

overall audit engagement.

Audit Fees and Audit Quality

Although there is a vast literature on audit fees, prior research has not considered how the

personal characteristics of the lead auditors might affect the fee that is charged to clients.

Instead, the prior research focuses on characteristics of the client firm, characteristics of the

audit firm delivering the service, or characteristics of the specific engagement. In a meta-

analysis, Hay, Knechel, and Wong (2006) find significant support for a Big 8/6/5/4

premium based on 85 different studies. Just as the Big N premium is due to reputational

inferences made by investors, detailed knowledge of the personal characteristics of lead

members of the audit team may influence the reputational inferences made by the client

firm.

Audit Partner Tenure

Audit firm size and industry specialization are organization-level variables. Recently, sev-

eral archival studies have focused on audit partner tenure, which is a partner/engagement-

level variable. That is, it reflects the partner’s experience on a particular audit, but says

nothing about the partner’s other clients or overall work experience. Still, these studies

shed light on the value of partner rotation, which is an important issue from a regulatory

perspective.

Carey and Simnett (2006) examine the relation between audit partner tenure and audit

quality. They measure audit partner tenure as the number of years for which a partner has

served as the engagement partner for the sample company. Using an Australian sample,

they document that financial distressed firms with long audit partner tenure are less likely

to receive a going-concern audit opinion. They also document some evidence that firms

with long audit partner tenure are more likely to just beat earnings benchmarks, but no evi-

dence on the association between audit partner tenure and discretionary working capital

accruals. Using data from Taiwan, where audit reports of public companies should be certi-

fied by two audit partners whose names must be disclosed in the audit report, C. Y. Chen

et al. (2008) identify audit partner tenure, and find that firms with long audit partner tenure

have lower absolute discretionary accruals, inconsistent with the argument that long tenure

audit partners provide lower quality services.

82 Journal of Accounting, Auditing & Finance

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

Manry et al. (2008) examine the association between audit partner tenure and discretion-

ary accruals based on the data from multiple U.S. offices of three large international

accounting firms. They find that audit partner tenure is negatively associated with discre-

tionary accruals. Furthermore, they find that the significant and negative association

between audit partner tenure and discretionary accruals is only for small clients with part-

ner tenure of more than 7 years. Bedard and Johnstone (2010) investigate the relation

between audit partner tenure and audit planning and pricing in United States. They find no

association between audit partner tenure and planned audit hours, and a positive association

between audit partner tenure and planned realization rates.5

Hypotheses

Behavioral auditing research suggests that audit experience affects the accuracy of auditors’

judgments. When auditors make judgments, they need to recall information necessary to

perform tasks from memory (Bonner, 1990). The judgment accuracy depends on how much

recalled information is matched to the task requirement (Libby & Frederick, 1990). As

experienced auditors have developed vast and complex memory structures, they are able to

use more adequate information in decision making, resulting in more accurate judgments.

Moreover, these memory structures are precursors as they interpret the meaning and impli-

cations of domain-specific information, and thus affect auditors’ selection, understanding,

and reaction to the task environment (Gibbins, 1984; Waller & Felix, 1984). Audit experi-

ence also affects the selection and weighting of information cues. Experienced auditors

have knowledge structures that enable them to identify the particular information cues that

should be selected and appropriately weighted to form their judgments (Bonner, 1990).

Thus, audit experience can lead to more accurate audit judgments.

Signees of the audit report are audit partners or chief CPAs of accounting firms who are

responsible for the final review of the audit, or CPAs who are in charge of the audit proj-

ect. In a field experiment, Pratt and Jiambalvo (1981) find that in-charge auditors’ beha-

viors significantly affect the performance of audit teams supervised by those auditors.

More experienced audit team leaders are more likely to behave in a way to increase audit

team performance. These team leaders have more knowledge and expertise to effectively

guide and monitor subordinates’ work.

The importance of personal characteristics can be linked to the economic theory of

auditing. Auditing is a credence good because the client cannot determine the amount of

service required ex ante and because the client cannot determine the quality of the service

ex post (e.g., Causholli & Knechel, 2012; Emons, 1997). In such a setting, Dye (1993)

expects that observable characteristics, such as the auditor’s wealth, will proxy for the

unobserved audit quality. An auditor’s wealth is important because wealthy auditors have

more to lose if they are sued for a substandard audit. DeAngelo (1981) makes a similar

argument for audit firm size but focuses on quasi-rents. In our setting, the personal charac-

teristics of the auditor may serve as an observable signal of the level of care that will be

exercised during the audit process. Thus, knowledge of the lead auditors’ personal charac-

teristics may mitigate information problems for the client firm.

Prior research (e.g., Francis, 1984; Palmrose, 1986) indicates that auditors charge higher

fees on higher quality audits. If experienced auditors make better decisions as the experi-

mental research suggests, they may increase audit fees to better reflect the higher quality of

their audits. This quality differential may result in the higher audit fees charged by experi-

enced signees. On the contrary, more experienced auditors may be able to conduct the

Cahan and Sun 83

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

audit more efficiently. However, the audit firm may not pass these cost savings on to

clients.

Consequently, we examine two hypotheses. First, we examine whether there is a positive

association between signees’ audit experience and audit fees. Second, to the extent experi-

enced auditors charge higher fees, we consider whether the higher fees are due to experi-

enced auditors providing higher audit quality. More formally, we test the following two

hypotheses:

Hypothesis 1 (H1): Audit fees are positively associated with signees’ audit

experience.

Hypothesis 2 (H2): Audit quality is positively associated with signees’ audit

experience.

Research Design

Data Collection

We begin to select sample firms from the CSMAR-Audit Opinion database, which provides

the data including audit fees of auditing the annual financial statements, the names of

CPAs who signed the audit report, and the name of the audit firm, from all companies

listed on both the Shanghai Stock Exchange and the Shenzhen Stock Exchange for the

years 2007 to 2010.6 Using the data for years 1990 to 2010 from the CSMAR-Audit

Opinion database, we identify the audit tenure of both signees and the audit firm.

We then manually collect the data on signees’ audit experience, gender, and education

background from the official website of the CSRC (i.e., www.csrc.gov.cn), which is the

government agency to regulate the Chinese securities markets.7 To be allowed to audit

Chinese listed companies, audit firms and their CPAs must have a license from the CSRC.

The CSRC provides the basic information of licensed audit firms and their individual

licensed CPAs on its website including the number of years for which an individual CPA

has been engaged in audit work, which is used in this study to measure the individual

CPA’s audit experience.

Next, we manually collect the data on the number of each company’s business segments

and the number of each company’s consolidated subsidiaries from the annual report, which

is downloaded from the official websites of the Shanghai Stock Exchange and the

Shenzhen Stock Exchange (i.e., www.sse.com.cn and www.szse.cn). We also acquire the

data on each audit firm’s total revenue publicly released by the Chinese Institute of

Certified Public Accountants (CICPA). Finally, we collect the data of financial statements

from the Compustat Global database to compute other variables used in the statistical

analysis. After the exclusion of firms with missing data and firms not covered by the

databases, the final sample consists of 1,917 firm-year observations over the period 2007 to

2010.

Table 1 reports the breakdown of the final sample across 50 two-digit Standard

Industrial Classification (SIC) industries, of which chemicals and allied products (18.36%),

electrical and electronic equipment (10.12%), machinery and computer equipment (8.50%),

primary metal industries (5.89%), transportation equipment (5.32%), and electric, gas, and

sanitary services (5.32%) are the most representative industries in the sample.

84 Journal of Accounting, Auditing & Finance

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

Models

We test the first hypothesis by estimating the following regression model:

AFEE =a0 +a1SEXP +a2SFM +a3SEDU +a4STEN +a5SIS +a6AFTEN +a7AFIS

+a8AFSIZE +a9AFINT +a10SIZE +a11ROA+a12DEBT +a13LOSS +a14NSEG

+a15NSUBS +a16REC +a17INV +a18AUOP + industry dummies + e,

ð1Þ

where AFEE = audit fees, measured as the natural logarithm of audit fees for auditing the

company’s annual financial statements; SEXP = signee audit experience, measured as the

natural logarithm of the sum of years for which two signees have engaged in audit work;

SFM = female signees, coded ‘‘2,’’ ‘‘1,’’ and ‘‘0’’ if both signees, one of the two signees,

and no signees are female, respectively; SEDU = signee education, measured as the sum of

two signees’ education level, which is coded ‘‘3,’’ ‘‘2,’’ and ‘‘1’’ if a signee has a PhD

degree, master’s degree, and undergraduate degree or others, respectively; STEN = signee

tenure, measured as the natural logarithm of the sum of years for which the two signees

have audited the client; SIS = signee industry specialization, measured as the sum of the

two signees’ industry specialization, which is the ratio of the sales of the clients of a signee

Table 1. Sample Breakdown by Industry.

Two-digit SIC code Industry description Frequency %

12 Coal mining 25 1.3016 Heavy construction contractors 28 1.4620 Food and kindred products 75 3.9122 Textile mill products 74 3.8626 Paper and allied products 28 1.4628 Chemicals and allied products 352 18.3630 Rubber and miscellaneous plastics products 32 1.6732 Stone, clay, glass, and concrete products 55 2.8733 Primary metal industries 113 5.8935 Machinery and computer equipment 163 8.5036 Electrical and electronic equipment 194 10.1237 Transportation equipment 102 5.3238 Measuring and analyzing instruments 22 1.1544 Water transportation 26 1.3647 Transportation services 40 2.0948 Communications 20 1.0549 Electric, gas, and sanitary services 102 5.3250 Wholesale trade-durable goods 40 2.0951 Wholesale trade-non-durable goods 37 1.9353 General merchandise stores 52 2.7173 Business services 50 2.6199 Nonclassifiable establishments 37 1.93

Others 250 13.04Total 1,917 100.00

Note. SIC = Standard Industrial Classification.

Cahan and Sun 85

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

in a two-digit SIC industry to the total sum of the sales of all companies in that industry;

AFTEN = audit firm tenure, measured as the natural logarithm of the maximum number of

years for which the audit firm has audited the client; AFIS = audit firm industry specializa-

tion, measured as the ratio of the sales of the clients of the audit firm in a two-digit SIC

industry to the total sum of the sales of all companies in that industry; AFSIZE = audit firm

size, measured as the natural logarithm of the total revenue of the audit firm; AFINT =

audit firm international alliance, coded ‘‘1’’ if the audit firm is a member of an interna-

tional audit firm alliance, and ‘‘0’’ otherwise; SIZE = client size, measured as the natural

logarithm of total assets; ROA = return on assets, measured as the ratio of income before

extraordinary items to total assets; DEBT = debt ratio, measured as the ratio of long-term

debt to total assets; LOSS = loss making, coded ‘‘1’’ if income before extraordinary items

is negative and ‘‘0’’ otherwise; NSEG = segment, measured as the natural logarithm of the

number of business segments; NSUBS = subsidiary, measured as the natural logarithm of

the number of consolidated subsidiaries; REC = receivables intensiveness, measured as the

ratio of receivables to total assets; INV = inventory intensiveness, measured as the ratio of

inventory to total assets; AUOP = audit opinion, coded ‘‘1’’ if a modified audit opinion is

issued, and ‘‘0’’ otherwise.

In Equation 1, the coefficient on SEXP is expected to be positive and significant if the

first hypothesis is supported.8 Because we use the panel data for years 2007 to 2010, stan-

dard errors are clustered by year.

We include control variables for other personal characteristics that might affect audit

fees or quality. Numerous studies examine the role of gender in business settings. For

example, Adams and Ferreira (2009) find that gender-diverse boards devote more effort to

monitoring, and prior research (e.g., Lund, 2008; Nguyen, Basuray, Smith, Kopka, &

McGulloh, 2008) suggests that women may be more ethical and effective than men. In an

audit context, a few experimental studies examine the effect of gender on audit judgments.

Estes and Reames (1988) find that female auditors differ from male auditors in terms of

confidence in their materiality decisions. J. Chung and Monroe (2001) find that women

auditors outperform male auditor in an inventory valuation task. Gold, Hunton, and Gomaa

(2009) find that female auditors are less likely to be swayed by unverified client-provided

explanations, but are more (less) likely to be persuaded by male (female) clients when com-

pared with male auditors. To control for gender effects, we include SFM in the model.

As education level reflects an individual’s knowledge and skill base (Hambrick &

Mason, 1984), we control for SEDU in the model. Very few studies examine the effects of

education on auditor’s decision making. Estes and Reames (1988) find no difference in

auditors’ material decisions based on various measures of education. Grant, Ciccotello, and

Dickie (2002) find the 150-hr rule adopted in many U.S. states had only marginal impact

on student’s CPA exam success. In a survey, Ethridge and Heminway (1993) find only

31% of respondents thought individuals with an accounting master’s degree perform better

than individuals with an accounting bachelor’s degree.

We include STEN in the model because, as discussed above, prior research (e.g., Carey

& Simnett, 2006; Ghosh & Moon, 2005; Manry et al., 2008) indicates a positive effect of

audit partner tenure and audit firm tenure on audit quality. We control for STEN so we can

disentangle the effects of the audit partner’s firm-specific knowledge and general

knowledge.

To examine the effects of industry-specific knowledge, we control for industry speciali-

zation for each signees of the audit report. Solomon, Shields, and Whittington (1999) find

that industry-specific knowledge leads to more accurate non-error frequency knowledge.

86 Journal of Accounting, Auditing & Finance

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

Owhoso, Messier, and Lynch (2002) find that industry specialists are better at detecting

errors, and Low (2004) finds that specialists provide superior risk assessment and audit

planning decisions. Thus, SIS and STEN allow us to examine the effect of general audit

experience that is incremental to the lead auditors’ industry-specific knowledge and firm-

specific knowledge.

Consistent with the prior literature, we also include several variables measured at the

audit firm level. Palmrose (1986) documents a positive relationship between audit fees and

audit firm absolute size, and Becker, DeFond, Jiambalvo, and Subramanyam (1998) find

that auditor size is positively associated with audit quality. Thus, AFSIZE is added to the

model. As audit firms develop areas of expertise and can build teams of experts (e.g.,

Cahan, Jeter, & Naiker, 2011), we include AFIS to capture industry specialization at the

audit firm level. As prior research shows an association between audit firm tenure and earn-

ings quality (e.g., Ghosh & Moon, 2005; Myers, Myers, & Omer, 2003), we include

AFTEN. Finally, as audit firms may benefit from being part of an international accounting

firm alliance (e.g., Carson, 2009), we include AFINT. As China is a developing economy,

such alliances may be particularly important in terms of users’ perceptions about audit

quality and reputation.

In addition, we include several client-related variables. SIZE, NSUBS, and REC in the

model as prior research (e.g., Abbott, Parker, Peters, & Raghunandan, 2003; Francis &

Simon, 1987; Simon & Francis, 1988) finds that audit fees are positively associated with

the three variables. As Carcello, Hermanson, Neal, and Riley (2002) indicate that LOSS,

SEG, and INV positively affect audit fees, these three variables are also added to Equation

1. According to Larcker and Richardson (2004), ROA and DEBT are included in the model.

AUOP is used as a control variable in Equation 1 as it is found to be positively related to

audit fees (Francis & Simon, 1987; Simon & Francis, 1988). Finally, industry dummies are

added in the model to control for fixed industry effects.

The second hypothesis is tested by estimating the following regression model:

ADAC =b0 +b1SEXP +b2SFM +b3SEDU +b4STEN +b5SIS +b6SCIM +b7AFTEN

+b8AFIS +b9AFCIM +b10AFSIZE +b11AFINT +b12SIZE +b13ROA+b14DEBT

+b15LOSS +b16SGROW +b17CFO+ industry dummies + e:

ð2Þ

All the variables in Equation 2 have been defined for Equation 1 except for the follow-

ing variables: ADAC = absolute discretionary accruals, measured as the absolute value of

discretionary accruals; SCIM = signee client importance, measured as the sum of the two

signees’ client importance, which is the ratio of the natural logarithm of the client’s total

assets to the sum of the natural logarithm of total assets of all clients audited by a signee;

AFCIM = audit firm client importance, measured as the ratio of the natural logarithm of

the client’s total assets to the sum of the natural logarithm of total assets of all clients

audited by the audit firm; SGROW = sales growth, measured as the annual percentage

change in sales; CFO = cash flow, measured as the absolute value of cash flow from opera-

tions deflated by total assets.

Like prior research (e.g., Becker et al., 1998; Francis, Maydew, & Sparks, 1999), we use

discretionary accruals to measure audit quality. Following S. Chen, Sun, and Wu (2010),

we also use the propensity of issuing modified audit opinions as an alternative measure of

audit quality. To measure discretionary accruals, we estimate the Jones (1991) model

Cahan and Sun 87

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

within each two-digit SIC industry based on the data of all Chinese firms from the

Compustat Global database in each year:

ACC

TA�1=c0

1

TA�1+c1

DSALES

TA�1+ c2

PPE

TA�1+ e, ð3Þ

where ACC = total accruals, measured as income before extraordinary items minus cash

flows from operation; TA21 = total assets at the beginning of the year; DSALES = annual

change in sales; PPE = gross property, plant, and equipment.

After estimating Equation 3 within each two-digit SIC industry in each year, we com-

pute the residual value for each sample firm to measure discretionary accruals.9

In Equation 2, we expect a negative and significant coefficient on SEXP if the second

hypothesis is supported. As discussed for Equation 1, signees’ other characteristics such as

SFM, SEDU, STEN, and SIS, and the audit firm’s characteristics such as AFTEN, AFIS,

AFSIZE, and AFINT are also included in Equation 2. In addition, SCIM and AFCIM are

included in the model because S. Chen et al. (2010) find that auditor client importance

affects audit quality. As Armstrong, Barth, Jagolinzer, and Riedl (2010) suggest that larger

firms have higher earnings quality, SIZE is added in Equation 2. Kothari, Leone, and

Wasley (2005) indicate that earnings performance affects the measurement of discretionary

accruals. Thus, we include ROA in the model. We control for DEBT because financial

leverage may have the twofold effect on corporate governance (Klein, 2002; Jensen &

Meckling, 1976). Francis, LaFond, Olsson, and Schipper (2004) indicate that accrual qual-

ity is lower for loss-making firms. Thus, we add LOSS in the model. As high sales growth

could be associated with lower audit quality (Cahan & Zhang, 2006), SGROW is added in

the model. Like H. Chung and Kallapur (2003), we add CFO to control for the effect of

cash flow from operations on the measurement of discretionary accruals.

We also test the second hypothesis by estimating the following regression:

ARA=d0 +d1SEXP +d2SFM +d3SEDU +d4STEN +d5SIS +d6SCIM +d7AFTEN

+d8AFIS +d9AFCIM +d10AFSIZE +d11AFINT + industry dummies + e,

ð4Þ

where ARA is audit reporting aggressiveness, measured as the difference between predicted

probability from the following logistic model and AUOP (Gul et al., 2013):

AUOP = e0 + e1QUCIK + e2ARINV + e3OTHREC + e4ROA+ e5SIZE + e6DEBT

+ e7LOSS + e, ð5Þ

where QUICK = quick ratio, measured by the sum of cash and short-term investments,

notes receivables, and accounts receivables divided by current liabilities; ARINV = accounts

receivables and inventory, measured by the sum of accounts receivables and inventory

divided by total assets; OTHREC = other receivables, measured by other receivables

divided by total assets.

Higher values of ARA indicate auditors’ lower propensity to issue modified audit opi-

nions, and thus higher audit reporting aggressiveness. If signees with high audit experience

more effectively audit financial statements, their clients are more likely to receive modified

88 Journal of Accounting, Auditing & Finance

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

audit opinions. We expect a negative and significant coefficient on SEXP in Equation 4 if

the second hypothesis is supported.

Empirical Results

All variables are defined in the appendix. The descriptive statistics of variables are reported

in Table 2. The mean and median natural logarithm values of audit fees are 13.219 and

13.122 in RMB yuans, equivalent to RMB U550,730 and RMB U499,818 for the mean and

median audit fees, respectively. The mean and median natural logarithm values of audit

experience are 3.042 and 3.219 years, indicating that the mean and median of the sum of

years for which two signees have engaged in audit work are 21 and 25 years. Table 3 pre-

sents the Pearson correlations of independent variables. The correlation between SIS and

AFIS is extremely high (r = .84). To mitigate this multicollinearity issue, SIS is dropped

from Equations 1, 2, and 4. We find that the results are not substantially changed if SIS is

not dropped from the models.

Table 4 provides the results on audit fees. We find that the coefficient on SEXP is posi-

tive and significant (t statistic = 3.86), consistent with H1. Thus, clients pay audit fee pre-

miums to signees with higher audit experience, suggesting that experienced CPAs conduct

higher quality audits. We also find that the coefficient on SEDU is positive and significant

(t statistic = 4.13), suggesting that signees with graduate degrees receive audit fee

Table 2. Descriptive Statistics.

Variable M Median SD Q1 Q3

AFEE 13.219 13.122 0.585 12.821 13.527ADAC 0.063 0.044 0.062 0.019 0.086ARA 20.001 0.003 0.164 0.000 0.018SEXP 3.042 3.219 0.650 2.833 3.466SFM 0.547 0.000 0.647 0.000 1.000SEDU 2.252 2.000 0.501 2.000 2.000STEN 1.547 1.609 0.556 1.099 1.946SIS 0.108 0.027 0.241 0.010 0.074SCIM 1.176 1.192 0.503 0.728 1.498AFTEN 1.307 1.386 0.811 0.693 2.079AFIS 0.087 0.036 0.141 0.013 0.091AFCIM 0.034 0.023 0.041 0.013 0.038AFSIZE 9.827 9.887 0.993 9.073 10.354AFINT 0.364 0.000 0.481 0.000 1.000SIZE 7.780 7.664 1.156 7.015 8.474ROA 0.032 0.029 0.064 0.010 0.058DEBT 0.063 0.016 0.098 0.000 0.087LOSS 0.114 0.000 0.318 0.000 0.000NSEG 0.751 0.693 0.627 0.000 1.099NSUBS 1.838 1.792 0.860 1.386 2.398REC 0.136 0.116 0.102 0.054 0.190INV 0.157 0.136 0.123 0.067 0.214SGROW 0.172 0.138 0.314 20.007 0.303CFO 0.058 0.053 0.075 0.015 0.096

Note. All variables are defined in the appendix.

Cahan and Sun 89

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

Tab

le3.

Pear

son

Corr

elat

ions.

Var

iable

SFM

SED

UST

EN

SIS

SCIM

AFT

EN

AFI

SAFC

IMAFS

IZE

AFI

NT

SIZ

ERO

AD

EBT

LOSS

AUO

PN

SEG

NSU

BS

REC

INV

SGRO

WCFO

SEX

P.0

9***

2.1

0***

.14***

.02

2.0

2.1

1***

.04

.03

2.1

5***

2.0

1.0

8***

.06**

.01

2.0

6**

2.0

5**

.02

.07***

2.0

02

.02

.05**

2.0

3

SFM

2.1

1***

2.0

0.0

7***

.04*

.04

.04

.01

2.0

1.0

6**

.02

.01

.01

2.0

22

.03

.01

.05**

2.0

2.0

3.0

1.0

1

SED

U2

.05**

2.0

2.0

02

.05**

2.0

4.0

7***

.06**

.08***

2.0

22

.03

2.0

32

.04

.04

.00

2.0

4*.0

12

.03

.04*

.02

STEN

.02

2.1

8***

.56***

.01

2.0

12

.01

.03

.12***

.02

.11***

2.0

4*

2.1

3***

.12***

.05**

2.1

5***

.03

2.0

1.0

9***

SIS

.01

.03

.84***

2.0

3.0

9***

.09***

.31***

.05**

.03

2.0

7***

2.0

4*.1

1***

.19***

.02

2.0

2.0

8***

.06**

SCIM

2.0

9***

.02

.25***

2.0

2.0

2.0

9***

.05**

.02

2.0

6**

.03

.04

.03

2.0

12

.03

.03

2.0

1

AFT

EN

.01

.05*

2.0

2.0

0.1

4***

.03

.07***

2.0

6**

2.0

8***

.09***

.03

2.1

5***

2.0

4*

.01

.06**

AFI

S2

.14***

.13***

.11***

.31***

.02

.08***

2.0

5*

2.0

7***

.08***

.18***

.01

2.0

4*

.09***

.03

AFC

IM2

.15***

2.0

2.0

32

.01

.01

2.0

4.0

2.0

1.0

2.0

0.0

4.0

2.0

1

AFS

IZE

.37***

.12***

.02

.00

2.0

02

.03

2.0

1.0

6**

2.0

3.0

3.0

1.0

6**

AFI

NT

.08***

.00

.02

2.0

0.0

1.0

0.0

1.0

3.0

12

.01

2.0

5*

SIZ

E.1

3***

.38***

2.1

7***

2.2

4***

.05**

.26***

2.1

7***

.02

.22***

.06**

RO

A2

.08***

2.6

8***

2.3

0***

2.0

4*2

.02

.06**

2.0

1.3

0***

.34***

DEBT

.00

2.1

0***

.03

.02

2.3

2***

2.2

1***

.07***

2.0

2

LOSS

.31***

.01

2.0

12

.08***

2.0

4*

2.2

4***

2.1

6***

AUO

P.0

1.0

2.0

5**

2.1

0***

2.1

8***

2.1

1***

NSE

G.3

3***

2.0

7***

2.0

02

.03

2.0

4*

NSU

BS

.00

.04

.01

.00

REC

.13***

.03

2.1

6***

INV

.03

2.1

8***

SGRO

W.0

9***

Not

e.A

llva

riab

les

are

def

ined

inth

eap

pen

dix

.

***,**,an

d*

den

ote

sign

ifica

nce

at1%

,5%

,an

d10%

leve

l,re

spec

tive

ly(t

wo-t

aile

dte

sts)

.

90

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

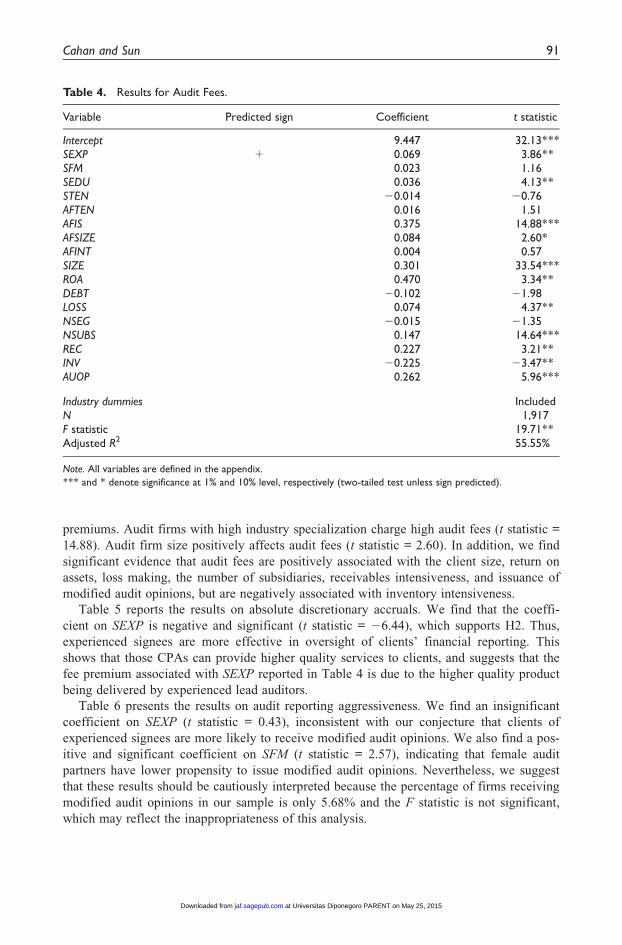

premiums. Audit firms with high industry specialization charge high audit fees (t statistic =

14.88). Audit firm size positively affects audit fees (t statistic = 2.60). In addition, we find

significant evidence that audit fees are positively associated with the client size, return on

assets, loss making, the number of subsidiaries, receivables intensiveness, and issuance of

modified audit opinions, but are negatively associated with inventory intensiveness.

Table 5 reports the results on absolute discretionary accruals. We find that the coeffi-

cient on SEXP is negative and significant (t statistic = 26.44), which supports H2. Thus,

experienced signees are more effective in oversight of clients’ financial reporting. This

shows that those CPAs can provide higher quality services to clients, and suggests that the

fee premium associated with SEXP reported in Table 4 is due to the higher quality product

being delivered by experienced lead auditors.

Table 6 presents the results on audit reporting aggressiveness. We find an insignificant

coefficient on SEXP (t statistic = 0.43), inconsistent with our conjecture that clients of

experienced signees are more likely to receive modified audit opinions. We also find a pos-

itive and significant coefficient on SFM (t statistic = 2.57), indicating that female audit

partners have lower propensity to issue modified audit opinions. Nevertheless, we suggest

that these results should be cautiously interpreted because the percentage of firms receiving

modified audit opinions in our sample is only 5.68% and the F statistic is not significant,

which may reflect the inappropriateness of this analysis.

Table 4. Results for Audit Fees.

Variable Predicted sign Coefficient t statistic

Intercept 9.447 32.13***SEXP + 0.069 3.86**SFM 0.023 1.16SEDU 0.036 4.13**STEN 20.014 20.76AFTEN 0.016 1.51AFIS 0.375 14.88***AFSIZE 0.084 2.60*AFINT 0.004 0.57SIZE 0.301 33.54***ROA 0.470 3.34**DEBT 20.102 21.98LOSS 0.074 4.37**NSEG 20.015 21.35NSUBS 0.147 14.64***REC 0.227 3.21**INV 20.225 23.47**AUOP 0.262 5.96***

Industry dummies IncludedN 1,917F statistic 19.71**Adjusted R2 55.55%

Note. All variables are defined in the appendix.

*** and * denote significance at 1% and 10% level, respectively (two-tailed test unless sign predicted).

Cahan and Sun 91

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

Table 5. Results for Absolute Discretionary Accruals.

Variable Predicted sign Coefficient t statistic

Intercept 0.119 2.75*SEXP 2 20.004 26.44***SFM 20.000 21.95SEDU 0.001 0.21STEN 20.005 21.91SCIM 20.003 21.40AFTEN 20.001 20.52AFIS 20.008 20.44AFCIM 0.064 1.46AFSIZE 0.001 0.76AFINT 20.004 22.10SIZE 20.008 22.84*ROA 0.098 1.38DEBT 20.022 22.45*LOSS 0.043 4.91**SGROW 0.015 2.54*CFO 0.032 0.42Industry dummies Includedn 1,600F statistic 74.85***Adjusted R2 9.61%

Note. All variables are defined in the appendix.

***, **, and * denote significance at 1%, 5%, and 10% level, respectively (two-tailed test unless sign predicted).

Table 6. Results for Audit Reporting Aggressiveness.

Variable Predicted sign Coefficient t statistic

Intercept 20.113 21.75SEXP 2 0.004 0.43SFM 0.007 2.57*SEDU 0.001 0.12STEN 0.014 1.39SCIM 20.011 21.74AFTEN 0.006 0.91AFIS 20.028 21.22AFCIM 0.028 0.24AFSIZE 0.007 1.49AFINT 20.013 21.63Industry dummies Includedn 1,600F statistic 3.93Adjusted R2 3.45%

Note. All variables are defined in the appendix.

***, **, and * denote significance at 1%, 5%, and 10% level, respectively (two-tailed test unless sign predicted).

92 Journal of Accounting, Auditing & Finance

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

We conduct additional analyses as follows. First, we test the hypotheses by controlling

for experienced signees’ self-selection bias. Based on the auditor selection model used in

prior research (e.g., Khurana & Raman, 2004), we estimate the following logistic model:

SEXPI =f0 +f1SHORT +f2LONG +f3PE +f4ISSUE +f5SIZE +f6DEBT +f7LOSS + e,

ð6Þ

where SEXPI = an indicator variable of experienced signees; SHORT = absolute value of

short-term accruals in income deflated by sales; LONG = absolute value of long-term

accruals in income deflated by sales; PE = ratio of price to earnings per share; ISSUE =

new equity issue, coded ‘‘1’’ if change in equity is greater than 10% and ‘‘0’’ otherwise.

The indicator variable is coded ‘‘1’’ if the sum of the first and second signees’ audit

experience is greater than 32 years, which is the 75th percentile of the distribution of the

two signees’ audit experience. We use the fitted value from Equation 6 to compute the

inverse Mills ratio. Then, we include the inverse Mills ratio in Equations 1, 2, and 4 to cor-

rect for the self-selection bias (Heckman, 1979).

Table 7 includes the results after controlling for the self-selection bias. From Equation

1, we find that the audit experience is positively associated with audit fees (t statistic =

3.37). From Equation 2, we find that audit experience is negatively associated with absolute

discretionary accruals (t statistic = 23.12). Thus, the results after allowing for the experi-

enced signees’ self-selection bias still support H1 and H2. From Equation 4, we find that

there is an insignificant association between audit experience and the issuance of modified

audit opinions (t statistic = 0.64), which is consistent with the findings without controlling

for the experienced signees’ self-selection bias.

Second, we estimate Equation 2 by using income-increasing or income-decreasing dis-

cretionary accruals as the dependent variable separately. Like the results on absolute discre-

tionary accruals, we find that the coefficient on SEXP remains negative and significant for

income-increasing discretionary accruals (non-tabulated t statistic = 23.35). The coefficient

on SEXP is positive and insignificant for income-decreasing discretionary accruals (non-

tabulated t statistic = 0.81). Overall, our results still support H2 when signed discretionary

accruals are used as the dependent variable in Equation 2; in particular, more experienced

auditors are more likely to constrain aggressive income-increasing accruals.

Third, we separate SEXP into SEXP1 and SEXP2 in the equations, where SEXP1 is the

first signee’s audit experience and SEXP2 is the second signee’s audit experience.10 From

Equation 1, we find that the coefficients on SEXP1 and SEXP2 are positive and significant

(non-tabulated t statistics = 3.59 and 2.92, respectively), consistent with H1. From

Equation 2, we find that the coefficients on SEXP1 and SEXP2 are negative and significant

(non-tabulated t statistics = 23.34 and 24.21, respectively), consistent with H2. From

Equation 4, we find negative and insignificant coefficients on SEXP1 and SEXP2 (non-

tabulated t statistics = 20.43 and 0.29, respectively). Thus, the results are inconsistent with

the results on SEXP.

Fourth, we re-run the analyses by measuring SEXP as the maximum value of the first or

second signees’ audit experience. Similar to the results on the sum of the first and second

signees’ audit experience, the maximum value of SEXP1 or SEXP2 is positively associated

with audit fees (non-tabulated t statistic = 2.93), and is negatively associated with absolute

discretionary accruals (non-tabulated t statistic = 23.37). Likewise, clients’ likelihood of

Cahan and Sun 93

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

Tab

le7.

Res

ults

Aft

erC

ontr

olli

ng

for

Self-

Sele

ctio

nB

ias.

Var

iable

Audit

fees

Abso

lute

dis

cret

ionar

yac

crual

sA

udit

report

ing

aggr

essi

venes

s

Pre

dic

ted

sign

Coef

ficie

nt

tst

atis

tic

Var

iable

Pre

dic

ted

sign

Coef

ficie

nt

tst

atis

tic

Var

iable

Pre

dic

ted

sign

Coef

ficie

nt

tst

atis

tic

Inte

rcep

t9.3

37

27.0

3***

Inte

rcep

t0.1

10

2.2

0In

terc

ept

20.1

15

21.8

1SE

XP

+0.0

67

3.3

7**

SEX

P2

20.0

04

23.1

2**

SEX

P2

0.0

07

0.6

4SF

M0.0

13

0.7

2SF

M2

0.0

01

21.0

7SF

M0.0

06

1.6

7SE

DU

0.0

31

1.5

8SE

DU

20.0

01

20.3

7SE

DU

0.0

05

0.5

0ST

EN

20.0

10

20.6

3ST

EN

20.0

04

21.7

7ST

EN

0.0

19

1.8

7AFT

EN

0.0

19

1.7

7SC

IM2

0.0

03

21.0

1SC

IM2

0.0

22

24.6

2**

AFI

S0.4

02

14.8

6***

AFT

EN

20.0

01

20.3

0AFT

EN

20.0

02

20.4

0AFS

IZE

0.0

93

2.5

2*

AFI

S2

0.0

13

20.5

6AFI

S2

0.0

17

20.9

4AFI

NT

20.0

10

20.8

8AFC

IM0.0

64

2.3

9*

AFC

IM0.0

49

0.5

6SI

ZE

0.3

05

26.0

9***

AFS

IZE

0.0

02

0.8

8AFS

IZE

0.0

05

1.1

4RO

A0.3

68

2.6

4*

AFI

NT

20.0

04

21.6

8AFI

NT

20.0

03

20.6

5D

EBT

20.1

26

21.5

7SI

ZE

20.0

06

21.6

7IM

R2

0.0

01

20.2

6LO

SS0.0

97

4.0

5**

RO

A0.0

46

0.5

9N

SEG

20.0

15

20.9

7D

EBT

20.0

32

22.5

6*

NSU

BS

0.1

53

10.0

3***

LOSS

0.0

41

4.0

1**

REC

0.2

14

2.6

8*

SGRO

W0.0

13

1.5

1IN

V2

0.1

93

22.3

4CFO

0.0

80

1.3

0AU

OP

0.2

27

3.1

4*

IMR

20.0

01

22.7

0*

IMR

0.0

11

1.9

1In

dust

rydu

mm

ies

Incl

uded

Indu

stry

dum

mie

sIn

cluded

Indu

stry

dum

mie

sIn

cluded

n1,7

32

n1,4

51

n1,4

51

Fst

atis

tic

20.9

1**

Fst

atis

tic

21.2

1**

Fst

atis

tic

4.2

8A

dju

sted

R2

56.1

9%

Adju

sted

R2

9.6

2%

Adju

sted

R2

4.7

7%

Not

e.A

llva

riab

les

are

def

ined

inth

eap

pen

dix

.

***,**,an

d*

den

ote

sign

ifica

nce

at1%

,5%

,an

d10%

leve

l,re

spec

tive

ly(t

wo-t

aile

dte

stunle

sssi

gnpre

dic

ted).

94

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

receiving modified audit opinions is not associated with the maximum value of SEXP1 or

SEXP2 (non-tabulated t statistic = 0.83).

Fifth, we measure discretionary accruals using the performance-matched discretionary

accruals developed by Kothari et al. (2005). For absolute discretionary accruals, we find a

negative but insignificant coefficient on SEXP (non-tabulated t statistic = 20.70). The coef-

ficient on SEXP is negative and significant for income-increasing discretionary accruals

(non-tabulated t statistic = 24.65), and is insignificant for income-decreasing discretionary

accruals (non-tabulated t statistic = 0.13), consistent with the results of non-performance-

matched discretionary accruals. The coefficient on SEXP1 is negative and significant

(non-tabulated t statistic = 21.71), whereas the coefficient on SEXP2 is insignificant (non-

tabulated t statistic = 20.00). Overall, we still find some evidence to support H2. Recently,

Keung and Shih (2014) show that the performance matching approach significantly under-

estimates discretionary accruals and increases the frequency of Type II errors.

Sixth, in the spirit of Teoh and Wong (1993), we examine whether audit experience

affects the association between stock returns and accounting earnings by running the fol-

lowing regression:

RET =g0 +g1DE +g2SEXP +g3DE3SEXP +g4SFM +g5DE3SFM +g6SEDU

+g7DE3SEDU +g8STEN +g9DE3STEN +g10SIS +g11DE3SIS +g12SCIM

+g13DE3SCIM +g14AFTEN +g15DE3AFTEN +g16AFIS +g17DE3AFIS

+g18AFCIM +g19DE3AFCIM +g20AFSIZE +g21DE3AFSIZE +g22AFINT

+g23DE3AFINT + industry dummies + e:

ð7Þ

In Equation 6, RET is annual stock returns. DE is measured as the annual change in

income before extraordinary items deflated by the beginning of year market value of

common equity. If investors view unexpected earnings of firms with more experienced

auditors as being more credible, the coefficient g3 (i.e., the earnings response coefficient)

will be positive and significant.

We find an insignificant coefficient on DE 3 SEXP (non-tabulated t statistic = 21.51),

suggesting that investors either do not recognize or appreciate the higher quality audit of

experienced individual auditors. However, we caution that such a test is a joint test of audit

quality and market efficiency. Thus, an alternative explanation for the insignificant coeffi-

cient is that the Chinese stock market is inefficient because of its speculative nature and sus-

ceptibility to rumors and investor sentiment. Groenewold, Wu, Tang, and Fan (2004) and

others provide evidence of inefficiency, although the overall evidence is mixed. Chong, Lam,

and Yan (2012) find that while the efficiency of the Chinese stock market has improved over

time, some trading rules remain profitable in the latest period they examine (2009-2010).

Conclusion

We conduct an archival study to examine the effect of audit experience on audit fees and

audit quality. Using the unique data from China, we find that the overall audit experience

of two signees of the audit report is positively associated with audit fees, and is negatively

associated with absolute discretionary accruals after controlling for other personal charac-

teristics of the lead auditors, audit firm characteristics, and client characteristics. Our

Cahan and Sun 95

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

findings suggest that more experienced CPAs provide higher quality audit services than

less experienced CPAs.

Prior research on audit experience focuses on behavioral studies that are conducted by

running experiments. These studies only provide experimental and task-based results.

Based on those results, it is not possible to determine how audit experience affects the com-

plete audit engagement. Thus, archival evidence could complement the prior behavioral

studies in an important way, but obtaining personal characteristics of auditors in a large

sample has been difficult. Using unique data from China, we are able to help fill this void

in the literature. Furthermore, we extend the research on audit partners by considering the

incremental effects of gender, education, engagement tenure, industry specialization, and

client importance after controlling for overall audit experience. Overall, our results suggest

that the lead auditors’ personal characteristics may serve as a signal of the level of care

that will be exercised during the audit process. In this way, personal characteristics help

mitigate adverse selection problems for the client in a setting where audit quality is not

fully observable, that is, a credence good.

Our study complements the work of Gul et al. (2013). Although they examine the effects

of demographic characteristics of Chinese auditors at an individual level, we focus on the

average effect across individual auditors. Finally, our study has implications for the

recently announced Chinese regulation that would require the localization of Big 4 offices

in China. Our results suggest that audit quality increases with the experience of Chinese

auditors. Thus, giving Chinese auditors more experience by increasing their involvement in

Big 4 offices will benefit auditing in China in the long run.

Appendix

Variable Definition for Tables

AFEE = audit fees, measured as the natural logarithm of audit fees for auditing the com-

pany’s annual financial statements;

ADAC = absolute discretionary accruals, measured as the absolute value of discretionary

accruals;

ARA = audit reporting aggressiveness, measured as the difference between predicted prob-

ability from the logistic regression (i.e., Equation 5) and actual modified audit opinion

(AUOP), which is a dummy coded ‘‘1’’ if a modified audit opinion is issued, and ‘‘0’’

otherwise;

SEXP = signee audit experience, measured as the natural logarithm of the sum of years for

which two signees have engaged in audit work;

SFM = female signees, coded ‘‘2,’’ ‘‘1,’’ and ‘‘0’’ if both two signees, one of the two sign-

ees, and no signees are female, respectively;

SEDU = signee education, measured as the sum of two signees’ education level, which is

coded ‘‘1’’ if a signee has a postgraduate degree and ‘‘0’’ otherwise;

STEN = signee tenure, measured as the natural logarithm of the sum of years for which the

two signees have audited the client;

SIS = signee industry specialization, measured as the sum of the two signees’ industry spe-

cialization, which is the ratio of the sales of the clients of a signee in a two-digit SIC

industry to the total sum of the sales of all companies in that industry;

96 Journal of Accounting, Auditing & Finance

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

SCIM = signee client importance, measured as the sum of the two signees’ client impor-

tance, which is the ratio of the natural logarithm of the client’s total assets to the sum of

the natural logarithm of total assets of all clients audited by a signee;

AFTEN = audit firm tenure, measured as the natural logarithm of the number of years for

which the audit firm has audited the client;

AFIS = audit firm industry specialization, measured as the ratio of the sales of the clients

of the audit firm in a two-digit SIC industry to the total sum of the sales of all compa-

nies in that industry;

AFCIM = audit firm client importance, measured as the ratio of the natural logarithm of

the client’s total assets to the sum of the natural logarithm of total assets of all clients

audited by the audit firm;

AFSIZE = audit firm size, measured as the natural logarithm of the total revenue of the

audit firm;

AFINT = audit firm international alliance, coded ‘‘1’’ if the audit firm is a member of an

international accounting firm alliance, and ‘‘0’’ otherwise;

SIZE = client size, measured as the natural logarithm of total assets;

ROA = return on assets, measured as the ratio of income before extraordinary items to total

assets;

DEBT = debt ratio, measured as the ratio of long-term debt to total assets;

LOSS = loss making, coded ‘‘1’’ if income before extraordinary items is negative and ‘‘0’’

otherwise;

NSEG = segment, measured as the natural logarithm of the number of business segments;

NSUBS = subsidiary, measured as the natural logarithm of the number of consolidated

subsidiaries;

REC = receivables intensiveness, measured as the ratio of receivables to total assets;

INV = inventory intensiveness, measured as the ratio of inventory to total assets;

SGROW = sales growth, measured as the annual percentage change in sales;

CFO = cash flow, measured as cash flow from operations deflated by total assets;

IMR = inverse Mills ratio, computed using the fitted value from Equation 6.

Acknowledgment

We thank Bharat Sarath (the editor), Matthew Reidenbach, two anonymous reviewers, and participants

at the 2012 American Accounting Association (AAA) Annual Meeting for their valuable comments.

We appreciate Huanwen Jiao, Siwen Li, Hong Zhao, and Ya Zhou for their research assistance.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/

or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this

article.

Notes

1. In China, only the Ministry of Finance can issue accounting and audit standards. The Chinese

Institute of Certified Public Accountants (CPAs) is actually a government agency under the

Ministry of Finance, which is responsible for developing audit standards.

Cahan and Sun 97

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

2. For example, some CPAs do not have a license to issue audit reports on listed companies.

3. Error frequency knowledge is the knowledge of the base rates associated with error occurrences.

4. Failure to integrate is defined as failure to make mental connections between separately received

pieces of information. Reconstruction is defined as altering the mental representation of informa-

tion to be consistent with existing knowledge or memories.

5. The planned realization rate is the ratio of the planned audit fee to the sum of planned labor

hours times the standard billing rate.

6. We use 2007 as the first year of the sample period because China adopted International

Financial Reporting Standards (IFRS) in that year. We want to ensure that the financial state-

ments during our sample period are prepared using a consistent set of accounting standards. 2010

is the last year in our sample period because data about individual signees were not available in

the CSMAR-Audit Opinion database after 2010. All firms in our sample have December 31

fiscal year ends.

7. The Chinese Securities Regulatory Commission (CSRC) has not disclosed information on indi-

vidual auditors since 2012, which adds to the uniqueness of our data.

8. All continuous variables in the regression models are winsorized at 1% and 99% levels.

9. There are at least 20 firms in each two-digit Standard Industrial Classification (SIC) industry to

estimate the Jones model.

10. The first signee is an individual auditor whose signature is placed on the left side of the audit

report, whereas the second signee is an individual auditor whose signature is placed on the right

side of the audit report.

References

Abbott, L. J., Parker, S., Peters, G., & Raghunandan, K. (2003). The association between audit com-

mittee characteristics and audit fees. Auditing: A Journal of Practice & Theory, 22, 17-32.

Abdolmohammadi, M., & Wright, A. (1987). An examination of the effects of experience and task

complexity and audit judgments. The Accounting Review, 62, 1-13.

Accounting in China: Internal controls. (2012, May 19). The Economist, p. 74.

Adams, R., & Ferreira, D. (2009). Women in the boardroom and their impact on governance and per-

formance. Journal of Financial Economics, 94, 291-309.

Armstrong, C. S., Barth, M. E., Jagolinzer, A. D., & Riedl, E. J. (2010). Market reaction to the adop-

tion of IFRS in Europe. The Accounting Review, 85, 31-61.

Becker, C., DeFond, M., Jiambalvo, J., & Subramanyam, K. (1998). The effect of audit quality on

earnings management. Contemporary Accounting Research, 16, 1-24.

Bedard, J. C., & Johnstone, K. M. (2010). Audit partner tenure and audit planning and pricing.

Auditing: A Journal of Practice & Theory, 29, 45-70.

Biggs, S. F., Mock, T. J., & Watkins, P. R. (1988). Auditors use of analytical review in audit program

design. The Accounting Review, 63, 148-161.

Bonner, S. E. (1990). Experience effects in auditing: The role of task-specific knowledge. The

Accounting Review, 66, 72-92.

Cahan, S. F., Jeter, D. C., & Naiker, V. (2011). Are all industry specialists the same? Auditing: A

Journal of Theory & Practice, 30, 191-222.

Cahan, S. F., & Zhang, W. (2006). After Enron: Audit conservatism and ex-Andersen clients. The

Accounting Review, 81, 49-82.

Carcello, J. V., Hermanson, D. R., Neal, T. L., & Riley, R. A., Jr. (2002). Board characteristics and

audit fees. Contemporary Accounting Research, 19, 365-384.

Carey, P., & Simnett, R. (2006). Audit partner tenure and audit quality. The Accounting Review, 81,

653-676.

Carson, E. (2009). Industry specialization by global audit firms networks. The Accounting Review, 84,

355-382.

98 Journal of Accounting, Auditing & Finance

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

Causholli, M., & Knechel, W. R. (2012). An examination of the credence attributes of an audit.

Accounting Horizons, 26, 631-656.

Chen, C. Y., Lin, C. J., & Lin, Y. C. (2008). Audit partner tenure, audit firm tenure, and discretionary

accruals: Does long auditor tenure impair earnings quality? Contemporary Accounting Research,

25, 415-445.

Chen, S., Sun, S. Y. J., & Wu, D. (2010). Client importance, institutional improvements, and audit

quality in China: An office and individual auditor level analysis. The Accounting Review, 85,

127-158.

Chong, T. T.-L., Lam, T.-H., & Yan, I. K.-M. (2012). Is the Chinese stock market really inefficient?

China Economic Review, 23, 122-137.

Chung, H., & Kallapur, S. (2003). Client importance, nonaudit services, and abnormal accruals. The

Accounting Review, 78, 931-955.

Chung, J., & Monroe, G. (2001). A research note on the effects of gender and task complexity on an

audit judgment. Behavioral Research in Accounting, 13, 111-125.

Davis, J. (1996). Experience and auditor’s selection of relevant information for preliminary control

risk assessments. Auditing: A Journal of Practice & Theory, 15, 16-37.

DeAngelo, L. (1981). Auditor size and auditor quality. Journal of Accounting & Economics, 1,

183-199.

Dye, R. A. (1993). Auditing standards, legal liability, and auditor wealth. Journal of Political

Economy, 101, 887-914.

Emons, W. (1997). Credence goods and fraudulent experts. RAND Journal of Economics, 28,

107-119.

Estes, R., & Reames, D. D. (1988). Effects of personal characteristics on materiality decisions: A

multivariate analysis. Accounting & Business Research, 18, 291-296.

Ethridge, J. R., & Heminway, J. R. (1993). Industry’s view of the 150-hour requirements. The CPA

Journal, 63, 67-69.

Farmer, T. A., Rittenberg, L. E., & Trompeter, G. M. (1987). An investigation of the impact of eco-

nomic and organizational factors on audit independence. Auditing: A Journal of Practice &

Theory, 7, 1-14.

Francis, J. R. (1984). The effect of audit firm size on audit prices: A study of the Australian market.

Journal of Accounting & Economics, 6, 133-151.

Francis, J. R., LaFond, R., Olsson, P. M., & Schipper, K. (2004). Costs of equity and earnings attri-

butes. The Accounting Review, 79, 967-1010.

Francis, J. R., Maydew, E., & Sparks, H. (1999). The role of Big 6 auditors in the credible reporting

of accruals. Auditing: A Journal of Practice & Theory, 18, 17-34.

Francis, J. R., & Simon, D. T. (1987). A test of audit pricing in the small client segment of the U.S.

audit market. The Accounting Review, 62, 145-157.

Ghosh, A., & Moon, D. (2005). Auditor tenure and perceptions of audit quality. The Accounting

Review, 80, 585-612.

Gibbins, M. (1984). Propositions about the psychology of professional judgment in public accounting.

Journal of Accounting Research, 22, 103-125.

Gold, A., Hunton, J., & Gomaa, M. (2009). The impact of client and auditor gender on auditors’ judg-

ments. Accounting Horizons, 23, 1-18.

Grant, C. T., Ciccotello, C. S., & Dickie, M. (2002). Barriers to professional entry: How effective is

the 150-hour rule? Journal of Accounting and Public Policy, 21, 71-93.

Groenewold, N., Wu, Y., Tang, S. H. K., & Fan, X. M. (2004). The Chinese stock market: Efficiency,

predictability and profitability. Cheltenham, UK: Edward Elgar.

Gul, F. A., Wu, D., & Yang, Z. (2013). Do individual auditors affect audit quality? Evidence from

archival data. The Accounting Review, 88, 1993-2023.

Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: The organization as a reflection of its top

managers. Academy of Management Review, 9, 193-206.

Cahan and Sun 99

at Universitas Diponegoro PARENT on May 25, 2015jaf.sagepub.comDownloaded from

Hay, D., Knechel, W., & Wong, N. (2006). Audit fees: A meta-analysis of the effect of demand and

supply attributes. Contemporary Accounting Research, 23, 141-191.