Embed Size (px)

Citation preview

BILL DOUGLAS EVP & CFO

JOHN F. BROCK Chairman & CEO

Forward-Looking Statements

INCLUDED IN THIS PRESENTATION ARE FORWARD-LOOKING MANAGEMENT

COMMENTS AND OTHER STATEMENTS THAT REFLECT MANAGEMENT’S

CURRENT OUTLOOK FOR FUTURE PERIODS.

▸ As always, these expectations are based on currently available competitive,

financial, and economic data along with our current operating plans and are

subject to risks and uncertainties that could cause actual results to differ materially

from the results contemplated by the forward-looking statements.

▸ The forward-looking statements in this presentation should be read in conjunction

with the risks and uncertainties discussed in our filings with the Securities and

Exchange Commission (“SEC”), including our Form 10-K for the year ended

December 31, 2012 and other SEC filings.

2

Agenda

▸OPPORTUNITY

▸GROWTH

▸ SHAREOWNER VALUE

▸CRS and KEY TAKEAWAYS

► SOLID FOUNDATION

3

CCE at a Glance

EUROPE

4

► $8.1 billion net sales

► 30 billion servings annually to 170 million consumers

► 17 production facilities

► ~13,000 employees

10-K 2012

Solid Fundamentals

MARKET1 ~$65B NARTD – A Growing Category

CCE NARTD

SHARE POSITION2

Brands Our Consumers Prefer and a

Successful Value & Volume Position

TRACK RECORD

OF GROWTH3

5

LT Targets 3 Yr CAGR 5 Yr CAGR

Net Sales 4 ─ 6% 7% 5%

OI 6 ─ 8% 6% 7%

EPS HSD 12% 10%

1. Non-alcoholic ready-to-drink AC Nielsen FY12 & Canadean FY11 2. AC Nielsen FY12 3. Long-term targets are comparable & currency neutral; comparable CAGRS, base years represents Legacy CCE EU operating segment except EPS which is total company; 2008-2011 includes segment remeasurement

Vision and Global Operating Framework

#1 OR STRONG #2 IN EVERY CATEGORY WE COMPETE

OUR CUSTOMERS’ MOST VALUED SUPPLIER

A WINNING AND INCLUSIVE CULTURE

Be the best beverage sales and

customer service company

VISION 1

2

3

Drive Consistent Long-Term Profitable Growth

6

Commitment to Shareowners

► Achieve long-term targets

► Return cash to shareowners

DRIVE CONSISTENT LONG-TERM

PROFITABLE GROWTH

7

Agenda

▸GROWTH

▸ SHAREOWNER VALUE

▸CRS and KEY TAKEAWAYS

▸ SOLID FOUNDATION

► OPPORTUNITY

8

~$25B NARTD Measured1

~$40B NARTD non-Measured2

Market – Opportunity Overview

SEGMENTS3

CHANNELS Grocery, Take Home,

and On-Premise

Ready-to-Drink: Sparkling,

Still, and Water

All

Channels

Hot Tea/Coffee,

All Alcohol, Dilutables

Liquid Refreshment Beverages (LRB) is a ~$160B Retail Market in CCE’s Territories

~$95B ALL OTHER2

1. AC Nielsen FY12 2. Canadean FY11 3. Excludes tap/bulk water & dairy

9

RETAIL SIZE

NARTD – Category Growth Opportunity

▸~$65B NARTD Retail Value with a 6+% 3 year CAGR

▸GROW NARTD – European consumption is ~0.6x of US

▸GROW SPARKLING – European consumption is ~0.5x of US

LRB PER CAP MIX OPPORTUNITIES

NARTD Sparkling1 NARTD Other2 All Other Bev2

10 1. FY12 AC Nielsen 2. FY11 Canadean

US CCE Territories

~30% ~15%

~40%

~25%

~30%

~60%

NARTD TOP 5 BRAND OWNERS

NARTD – A Competitive Category

20.2%

6.2%

7.0%

7.0% 2.3%

24.1%

33.2%

Private Label

Other Brand Owners

Orangina/Schweppes

Nestle

Danone

Pepsi

Coca-Cola

VOLUME

28.2%

9.3%

4.2% 3.9% 3.3%

26.5%

24.6%

VALUE

AC Nielsen FY12; Private Label and Other Brand Owners individual companies have value share < 3% 11

19.2%

6.3%

6.8%

7.0% 2.2%

25.0%

33.5%

1

1

1

3

4

NARTD – CCE Category and Segment Rank

CCE STRATEGY

NARTD

Colas

Sparkling Flavors

Energy

Stills

SELECTIVELY GROW VALUE SHARE

VALUE VOLUME

1

1

1

3

5

GROW SEGMENTS

AC Nielsen FY12 12

3%

CCE – Focused on High Value Segments

2 1 1

CATEGORY & CCE MIX

CCE participates in the highest value segments that drive favorable profit mix

1. AC Nielsen FY12 2. 10-K 2012 13

Sparkling Still Water

NARTD Volume NARTD Value CCE Volume

39% 17%

24%

37%

11%

37% 46%

86%

Agenda

14

▸ SHAREOWNER VALUE

▸CRS and KEY TAKEAWAYS

▸ SOLID FOUNDATION

▸OPPORTUNITY

► GROWTH

Capturing the Growth Opportunities

15

OUTSTANDING

MARKETING & EXECUTION

GREAT PEOPLE

SUCCESSFUL BRANDS

COCA-COLA TRADEMARK

SPARKLING FLAVORS AND ENERGY

STILLS

Successful Brand Portfolio

68%

MIX

18%

MIX

14%

MIX

16 10-K 2012

Sparkling – Coca-Cola Trademark

PACKAGE INNOVATION

► MyCoke 1.75 ltr , 375ml & 250ml

BRAND INNOVATION & EXPANSION

► Coke Zero Cherry

► Vanilla Coke

#1 IN VOLUME AND VALUE COLA SHARE IN EVERY TERRITORY

17 AC Nielsen FY12

COKE ZERO VOLUME 12.6% 3YR

CAGR

2009 2010 2011 2012

Sparkling – Flavors

#1 IN VOLUME AND VALUE FLAVORS SHARE

PACKAGE

INNOVATION BRAND INNOVATION &

EXPANSION

► Fanta 1 ltr

► Fanta Fridgepack

► Fanta Peach Apricot

► Sprite w/ Stevia

► Schweppes Summer Punch

18 AC Nielsen FY12

Sparkling – Energy

Energy

Segment

CCE

Brands

Volume 8% 19%

Value 9% 16%

PACKAGE INNOVATION

► Relentless 250/500ml can

► Burn 500ml

BRAND INNOVATION & EXPANSION

► Monster line extensions

► Relentless & Burn Lemon

SWEETENER INNOVATION

► Burn Sugar Free

2012 SEGMENT GROWTH

AC Nielsen FY12 19

CCE OUTPERFORMED THE SEGMENT IN 2012

Stills

PACKAGE INNOVATION

BRAND INNOVATION & EXPANSION

SWEETENER INNOVATION

► Oasis 2 ltr

► Nestea can & 1 ltr

► Oasis Mango &

Lemonade

► VitaminWater

Sunshine

► Ocean Spray

► Nestea

Lemon Stevia

► Oasis Citrus

Punch Light

20

2013 Marketing Calendar

“COKE WITH MEALS”

2013 GROWTH WILL BE DRIVEN BY ‘CORE’ BRANDS

21

Commercials

22

Procurement, Production, and Logistics Excellence

► Pan European scale with global procurement capability

► Flexible & responsive to customers

► Cost efficient & expandable infrastructure

► Responsible & sustainable

23

CUSTOMER CENTRIC SUPPLY CHAIN

Flexible and Efficient Distribution

93%

99%

62%

99%

99%

58%

7%

1%

38%

1%

1%

42%

Indirect Direct

ROUTES TO MARKET

INDIRECT ~90%

DIRECT ~10% through CCE

through customer,

wholesalers, or

3rdparty

Norway mix estimate of EOY13 run rate; included in total company mix 24

CUSTOMER VALUE-CREATION MODEL

Revenue Growth Management (RGM) Excellence

25

► Value-creating selling capabilities

► Investing in technology

► On-line & digital shopping

Optimize Sales and Marketing Structure

CHANNEL-CENTRIC MODEL TO BETTER ALIGN CENTRAL & FIELD SALES

IMPROVE OUR OPERATING MODEL AND PLATFORM

FOR DRIVING SUSTAINABLE FUTURE GROWTH

26

► Best practice evolution

► Proven results in Benelux

► More aligned to customer needs

► Better position to capitalize on opportunities

Hard Discount Channel Opportunity

27

► Large and important consumer channel

► One of the fastest growing channels

► Expanding our business with tailored offerings to better address consumer and customer needs

LEVERAGE OUR CUSTOMER VALUE-CREATION

SELLING MODEL

New Norway Operating Model

DRIVING VALUE FOR CUSTOMERS, CONSUMERS, AND CCE

► ROUTE TO MARKET CHANGE

Facilitating efficiency and tailoring delivery to match

customer preferences

28

► PACKAGING CHANGE

Unlocking value by creating expanded customer and

consumer options

► ENVIRONMENTAL IMPACT

New model expands recycling capabilities and reduces

the impact of production, packaging, and distribution

CRS is one of the top three employee engagement drivers

Focused on driving diversity

Our People

ATTRACT, DEVELOP AND

RETAIN A HIGHLY

TALENTED AND DIVERSE

WORKFORCE

29

Agenda

30

▸CRS and KEY TAKEAWAYS

▸ SOLID FOUNDATION

▸OPPORTUNITY

▸GROWTH

► SHAREOWNER VALUE

Financial Priorities

CONSISTENT earnings in line with

our long-term objectives

MAXIMIZE free cash flow and

maintain financial flexibility

INCREASE return on invested capital

and drive shareowner value

31

DRIVE

CONSISTENT

LONG-TERM

PROFITABLE

GROWTH

Financial Approach

32

CASH FROM OPS

CAPEX

OPTIMIZE CAPITAL STRUCTURE

M&A

RETURN CASH TO SHAREOWNERS

Achieve long-term targets

Invest prudently

Reach and operate within target leverage

Short Term “use” and long-term “source” of cash

Competitive dividend and share repurchase

─

+

=

+/–

GROWTH

Cash from Operations

NET SALES

OPERATING INCOME

GENERATE SOLID FREE CASH FLOW

ACHIEVE LONG-TERM TARGETS

4% – 6%

6% – 8%

Comparable & Currency Neutral 33

Invest for Long-Term Growth

Operations Cold Drink Equipment IT, Other

58% 28%

14%

2012 CAPITAL MIX CAPITAL HIGHLIGHTS

► LT target ~4.0% – 4.5% of net sales

► 2013 expected to be ~$350M

► ~2/3 supports growth, ~1/3 maintains existing assets

10-K 2012 34

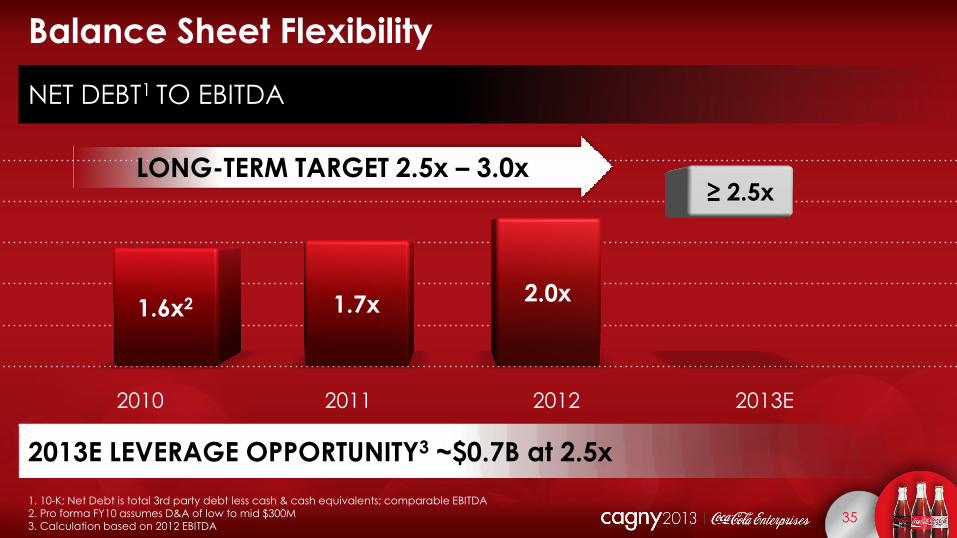

2010 2011 2012 2013E

1.6x2 1.7x 2.0x

≥ 2.5x

Balance Sheet Flexibility NET DEBT1 TO EBITDA

LONG-TERM TARGET 2.5x – 3.0x

2013E LEVERAGE OPPORTUNITY3 ~$0.7B at 2.5x

1. 10-K; Net Debt is total 3rd party debt less cash & cash equivalents; comparable EBITDA 2. Pro forma FY10 assumes D&A of low to mid $300M 3. Calculation based on 2012 EBITDA

35

LONG-TERM DEBT MATURITY ($M)

21201918171615142013

550 525 450 450

250

475

100

600

Balanced Debt Portfolio

10-K; rounded 36

WEIGHTED AVERAGE COST OF DEBT ~3%

OPPORTUNITIES EVALUATED AGAINST ALTERNATIVES,

INCLUDING RETURN OF CASH TO SHAREOWNERS

Investing in High Return Opportunities (including M&A)

OPPORTUNITIES EVALUATION CRITERIA

► Cash flow of existing business

► Incremental value creation by CCE

► Incremental value to CCE’s core business

► Risk, cost, and timeframe

37

► Core business growth

► Adjacent territories and adjacent categories

► Other territories

► New business

LONG-TERM TARGET OF ≥ 20 BPS ANNUAL IMPROVEMENT

After Tax Comparable OI

Average Invested Capital CCE ROIC 14% 2012 Year End = =

Solid Return on Invested Capital (ROIC)

INVEST in High

Return Initiatives Working Capital

TIGHTLY MANAGE

Operating Growth

DRIVE

Average Invested Capital = (Beginning & Ending Net Debt & Equity) / 2 38

Cash Returned to Shareowners – Dividends

10-K 39

ANNUAL DIVIDEND RATE

$0.60

$0.50

$0.40

$0.30

$0.20

$0.10

$0.70

$0.80

1999 00 01 02 03 04 05 06 07 08 09 10 11 12 13E

2013 RATE INCREASE OF 25%

$0.00

$0.2B

$0.8B

$0.8B

≥$0.5B

Cash Returned to Shareowners – Share Repurchases

≥$2.3B of

share repurchases after formation

of new CCE

through 2013E

2010

2011

2012

2013E

10-K; rounded 40

Presented

during our 2011

Investor Event

Progress Report

41

Progress Report – On Track

SEPTEMBER 2011OPPORTUNITY: $4.5B (2H11-2014E)

FREE CASH FLOW OF ~$2.5B BALANCE SHEET ~$2B+

2H11 - FY12 FY13E Balance

42 Free cash flow adjusted for cash restructuring costs, pension contributions in excess of pension expenses, and currency translation; rounded

2H11 - FY12 FY13E Balance

ON TRACK FOR ~$4.5B OPPORTUNITY 2H11 THROUGH 2014E

GROWTH

2013 Outlook

NET SALES

OI

EPS

NEAR TERM, WE EXPECT SOLID BUSINESS RESULTS & SHARE REPURCHASE

TO DRIVE EPS GROWTH ABOVE OUR LONG-TERM OBJECTIVES

2013 GUIDANCE

Mid-Single-Digits

Mid-Single-Digits

~10%

43 Comparable & Currency Neutral

FOCUS ON CONSISTENT LONG-TERM PROFITABLE GROWTH

Key Financial Takeaways

► History of managing the levers of our business to deliver growth

► Favorable and flexible capital structure

► Long-term financial objectives are challenging, yet achievable

► EPS outlook for 2013 exceeds our long-term objectives

44

Agenda

45

▸ SOLID FOUNDATION

▸OPPORTUNITY

▸GROWTH

► CRS and KEY TAKEAWAYS

▸ SHAREOWNER VALUE

CRS Vision and Framework

DELIVER FOR TODAY On our commitments and targets

LEAD THE INDUSTRY In energy and climate change and

sustainable packaging and recycling

INNOVATE FOR THE FUTURE Opportunities for innovation,

collaboration and partnership

STRATEGIC PRIORITIES

We will deliver for today, growing a low carbon, zero waste business, and inspire

and lead change for a more sustainable

tomorrow.

SUSTAINABILITY VISION

DELIVER FOR

TODAY

INSPIRE FOR

TOMORROW

46

CRS Business Benefits

IMPROVE OPERATIONAL EFFICIENCIES AND EFFECTIVENESS

INCREASE EMPLOYEE ENGAGEMENT AND ADVOCACY

EXCEED CUSTOMER EXPECTATIONS

MEET GROWING CONSUMER TRENDS

ENHANCE IMAGE AND REPUTATION

47

► Water – reduced water use ratio

to 1.4 liters/liter

► Carbon – lowest ever carbon footprint

► Packaging – new recycling joint

ventures and residential recycling study

DECREASING ENVIRONMENTAL IMPACT

WHILE REDUCING COSTS

Key Achievements

48

Gaining External Recognition

CARBON

DISCLOSURE

PROJECT Leadership

Index

49

Business Environment Risks

CHALLENGING MACROECONOMIC ENVIRONMENT

VOLATILE COMMODITY COSTS

INCREASING FOCUS ON HEALTH AND WELLBEING

RISK OF INCREASED TAXES

Though

optimistic

about our outlook,

we are realistic

about key business

environment

risks

50

Key Takeaways

CCE IS EXECUTING OUR STRATEGIC PRIORITIES

► History of solid growth

► Financial priorities focused on long-term profitable growth

► Track record of delivering shareowner value

► Operating environment remains challenging

► In position to deliver our 2013 objectives

51

BILL DOUGLAS EVP & CFO

JOHN F. BROCK Chairman & CEO