Embed Size (px)

Citation preview

JEEViKA-A STUDY OF RURAL LIVELIHOODS PROGRAMME IN BIHAR

2015

Management Development Institute

Gurgaon

JEEViKA Study Page 2

Principal Investigator

Prof. Avanish Kumar

Management Development Institute, Gurgaon

Email: [email protected]

Research Associate

Aman Dewan

JEEViKA Study Page 3

CONTENTS

S.No. Chapter Page No.

Acknowledgment 4

Executive Summary 5-9

1. Introduction 10-14

2. JEEViKA’s Social Inclusion 15-38

3. JEEViKA’s Financial Inclusion 39-55

4. JEEViKA’s Livelihoods 56-66

5. The Way Forward 66-71

6. References

JEEViKA Study Page 4

Acknowledgement

First and foremost, we would like to thank the Ford Foundation for inviting a group of

academicians to work on rural livelihoods under MANTHAN. We would like to thank and

acknowledge financial support from the Ford Foundation especially to Ajit Kanitkar and

Srinivasan Iyer, whose timely guidance helped us in charting our path. Support from the

MANTHAN partners i.e. C. Shambu Prasad, Janat Shah, Dinesh Awasthi, Madhukar Shukla,

Ashwani Kumar, KV Gouri and Kalpana Pant, Joseph Satish, Hemanta provided great pace,

impetus and enthusiasm to the study. We would also like to make most of the opportunity to

express deep gratitude to the Bihar Rural Livelihood Promotion Society for graciously hosting us

and giving us administrative support through the journey of the study, especially the field

survey. It is imperative to make a special mention of Ajit Ranjan, Jay Kumar Palit, Bobby and to

Pramod Kumar, for their immersive, insightful and constant field support. We are also grateful

to all the development experts who provided insights during various consultation and

presentation at JEEViKA, MoRD, XIMB and the World Bank. We thank Amrita Sandhu for her

valuable inputs in the report.

MDI considers it a matter of great honour and privilege to be part of the MANTHAN initiative

and expresses regards towards all those who helped in making this study a fully-thriving reality.

The spirit and energy of this report came from the community that actually engaged with the

initiative. All of them were generous with their time and ever-willing participation in discussions

and conversations spanning hours. They welcomed the chance to contributively participate in

the study and brought large amounts of depth and enthusiasm to it. Our role in this research

study was that of a listener and observer. We hope that with our ear-on-the-ground efforts and

approach, we have been able to paint and distill an accurate stroke of the kind of impact the

initiative has had on the lives of the community.

JEEViKA Study Page 5

Executive Summary

About the Study

This study has been supported by the Ford Foundation and coordinated by the Management

Development Institute, in the capacity of a MANTHAN partner. This project has been geared

towards identifying, distilling and documenting ground-level understanding of JEEViKA in Bihar,

via a participatory approach. The focus of the study was on ‘what works, and why it works’

pertaining to the three thematic areas of social, livelihoods and financial inclusion among the

marginalized. The study tools comprised a detailed household survey with a focus on

livelihood, social and financial inclusion parameters; along with focus group discussions (FGD)

and semi-structured interviews with the community members, beneficiaries, JEEViKA’s

professionals and community workers. The geographic focus of the study was two adjacent

villages in two blocks of Gaya District. These blocks were selected to understand the difference

of impact due to spatial administrative exclusion. Barachatti block is at the periphery of the

Gaya district, bordering with Jharkhand while Bodh Gaya is the administrative hub of the

JEEViKA project.

Key Findings

This report is a compilation of detailed case studies on JEEViKA’s social inclusion model,

financial inclusion model and livelihoods inclusion model.

Social Inclusion

Our findings suggest that social inclusion has happened as a result of the inclusive platform that

JEEViKA has created at the community level. The project has helped in creating an identity for

unknown women and by increasing their unity. Till date, being traditionally a patriarchal

society, norms and values of the society favored the male over the female, thus leading to the

JEEViKA Study Page 6

blocking of their progress. JEEViKA through its micro-finance program and livelihood creation

aims to lower this gap and improve the well being of women.

Data from a survey of 84 women beneficiaries showed that 29.8 per cent of women feel that

now there is no gender bias in health and education seeking behavior in the village, 57 per cent

of the surveyed women attributed this outcome to the functioning of the SHGs.

Identity as a prerequisite to empowerment -The study reveals that an increase in the sense of

identity in the family, community and by institutions like banks increases the avenues for

income generation. Prior to JEEViKA’s intervention, women had representative identity –

mother of …or wife of…, women having an independent identity were not considered desirable.

Identity creation under JEEViKA is universally considered across caste and class of women as an

indispensible asset.

Social networks and Empowerment - A majority of women (57 percent) believe that SHGs

created a positive platform for women’s empowerment. A major shift in the community is

noticeable in the way the program is being currently perceived by the people of the village.

From being reluctant participants in government schemes, an attitudinal shift in men is

observed whereby most men encourage women to join SHG’s. The state and community is

being considered a partner for the first time.

Intergenerational equity Impact - Increase in women’s self respect can be seen as a direct

outcome for the girl child who is now seen as an asset rather than a liability in the village. In the

Focus Group Discussions, women revealed that though the difference between boys and girls

continues to exist, but gender bias is fast fading away.

Financial Inclusion

Loan seeking behavior - Average loan taking by the members was highest in areas of Health

pegged at 32 percent, then Education at 25 percent, followed by asset creation at 21 percent

and marriage. This shows a weak public service delivery in health and education. These

expenses for health and education are key barriers that hinder livelihood creation.

JEEViKA Study Page 7

Improved household Cash flows - JEEViKA has succeeded in removing local moneylenders who

perpetuated a cycle of debt to a great extent. Further loan taking has become professional

through JEEViKA and does not involve loss of dignity and respect. This has implications on

household finances especially related to consumption smoothening.

Improved Community Health - Lower interest rates, especially through the Health risk fund,

which provide micro loans at 1 percent interest has improved accessibility to better quality

treatment. 60 percent of the respondents claim JEEViKA has improved overall health

accessibility in the villages.

Improved financial literacy - The study results show that 70 per cent of the community

members surveyed were aware of insurance, pension and other saving mechanisms. This

establishes the Village organizations’ ability to be a platform for financial literacy, but this

awareness has not translated into practice.

Livelihoods Inclusion

System for Rice Intensification (SRI) – Bihar being primarily an agrarian economy, the report

discusses case histories of individuals impacted by SRI and details their success stories. The case

further discuss on equity implications of SRI among the poor.

Poultry Farming - Amongst the livelihood activities that JEEViKA has taken up in our research

area, the most popular has been poultry farming. It provides quick returns and supply chain has

been instilled by JEEViKA across the area.

The study finds that untrained poultry resource persons and ineffective partnerships lead to

higher than normal chick deaths and that the business model is being rapidly taken up by the

community due to subsidies by the Bihar government.

Ineffective horizontal partnerships - The BRLPS has consistently focused on increasing rural

livelihood opportunities through self-employment, but this leaves out many who lack the ability

to branch out on their own.

JEEViKA Study Page 8

Women’s Livelihood Issues - The loan size, time period, lack of training, inability to market,

inability to get dislocated from the village are many issues that rural women face in crossing

the bridge from financial to livelihood inclusion.

Key Recommendations

Strengthening community workers- The community workers need to be sensitized to gender

conflicts and the ways of approaching their solutions. Gender sensitization workshops for men

showing regular life scenarios in the village are recommended. This could lead to an improved

understanding of avoidable and unjust gender disparity and its importance in the overall

context of development. VOs should be aware of exclusionary indicators of a local area, so that

they can start including members who are being left out. It was found that even in the model

villages few families are left out of JEEViKA.

Strengthening Social Audits- Health and Education costs cause financial distress to the poor,

these costs can be reduced by effective monitoring of the public health and education facilities,

this shall also free up capital for livelihood generation.

Loan Purpose Regulation- Beyond bank linkages, the poor need guidance on the correct

reasons for loan borrowing. If the goal of micro-finance has to be poverty alleviation, active

monitoring of loan purpose by SHGs and Village organizations is needed.

Tapping at the opportune time – 65 per cent of men claim to be supportive of women in

becoming active contributors to the family income. JEEViKA is recommended. The

recommended strategy would be to run programs for skill development, which do not involve

displacement of women from the villages. Even if JEEViKA is not able to deploy resources for

holistic livelihood programs, it has been observed that women have been able to face the task

of SHG formation for improving financial ability. It is expected that skill development will lead

to a change in the ability of women in producing and selling at competitive prices.

Brand Creation and Market linkages- Local market supply chains are essential if enterprise

development has to be given primary importance, the presence of a mere market is not the

solution, the solution lies in building holistic supply chains, where the producer at the village

JEEViKA Study Page 9

level is able to find a guaranteed buyer, the poor are not always able to find a market for their

produce, further the problems lie in extracting the correct amount for their produce, and this

should be fixed independently by an outside agency. It is recommended that JEEViKA starts

with marketing products in the tourist spot of Bodh Gaya under its own brand as a pilot

exercise.

JEEViKA Study Page 10

1. Introduction to JEEViKA

The government of Bihar has initiated a project on rural livelihood promotion with support

from the World Bank. This initiative is implemented through a Society registered with

Government of Bihar by the name of Bihar Rural Livelihoods Promotion Society (BRLPS). BRLPS

through the Bihar Rural Livelihoods Project, also known as JEEViKA, aims to improve rural

livelihood options and works towards social and economic empowerment of the rural poor and

women. The BRLP intervenes with the community through the following four themes or

JEEViKA Study Page 11

programmes: institution and capacity building, social development, microfinance and

livelihood.

The Objectives of JEEViKA

The objectives of JEEViKA are:

1. Creating self managed community institutions of participating households.

2. Enhancing income through sustainable livelihoods.

3. Increasing access to social protection including food security by enabling the rural poor

to articulate a more effective voice in the implementation of such schemes.

Strategy

According to the BRLPS mission, the core strategy of the JEEViKA programme is to build vibrant

and bankable women's community institutions in the form of self help groups (SHGs), who

through member savings, internal loaning and regular repayment become self sustaining

organizations. The groups formed would be based on self savings and revolving fund and not on

a single dose of community investment fund (CIF) funds for association given as a subsidy. The

primary level SHGs would next be federated at the village, by forming village organizations

(VOs), then at a cluster level, to become membership based, social service providers, business

entities and valued clients of the formal banking system. Such community organizations would

also partner a variety of organizations for provided back end services for different market

institutions such as correspondents for banks and insurance companies, procurement

franchises for private sector corporations and delivery mechanisms for a variety of government

programmes.

Working and structure of JEEViKA-

State Level- The State Project Management Unit (SPMU) oversees and manages various

functions of JEEViKA project at the state level with support from various functional specialists

such as state project managers and project managers under the leadership of the chief

executive officer (CEO) of JEEViKA. At the state level the society focuses on designing policy,

JEEViKA Study Page 12

planning interventions and framing operational strategies. The Executive Committee

compromises of senior government officials and representative members from civil society

organizations as its members. Its main function is to guide the project and approve policy

framework. The development commissioner is the president and BRLP CEO is the member

secretary of the council.

District Level- The District Project Coordination unit (DPCU) is responsible for coordinating,

implementing and managing project activities across the district under the guidance of the

district programme manager. The DPCU is now functional with thematic positions and

supported by the finance and administrative staff.

Block Level- The Block Project Implementation Unit (BPIU) is a key unit of the project. It is the

quality and effectiveness of this unit that determines how effectively the project rolls out in the

field with the partnership of community institutions. The Block programme manager (BPM) is

the functional head of this unit, he is supported by area coordinators (AC) who in turn are

supported by community coordinators (CC). BPIU builds strong community institutions of the

poor and subsequently intervene with well designed social and livelihood activities.

Introduction to the Report

This report is an outcome of the Ford Foundation supported initiative to conduct a field study

of JEEViKA in Bihar. The project was anchored by Prof. Avanish Kumar at Management

Development Institute, Gurgaon as a MANTHAN partner. Livelihoods MANTHAN is a collective

effort of management and higher educational institutions on rural livelihoods in India. The

project was geared towards participatory identifying, distilling and documenting ground-level

understanding of JEEViKA in Bihar. The focus of the study was on ‘what works, and why it

works’ on issues of social, livelihoods and financial inclusion among the marginalized. The study

was conducted in two phases; initially a team had four thematic discussions with the team of

JEEViKA at Patna. The team comprised of Ajit Kanitkar (Ford Foundation), KV Gouri (Livelihood

School), Kalpana Pant (Chaitanya) and Avanish Kumar (MDI). The second phase was intensive

fieldwork carried out by Aman Dewan and Avanish Kumar of MDI. The study employed a

JEEViKA Study Page 13

participatory multi-pronged approach while covering four villages across in two blocks of Gaya

district in Bihar. Gaya is part of the intensive districts from the time of conception, while the

two adjacent villages in two blocks are Bodh Gaya and Barachatti. These blocks were selected

to understand the difference of impact due to spatial administrative exclusion. Barachatti block

is at the periphery of the district Gaya, bordering Jharkhand while Bodh Gaya is a centre of

JEEViKA project administration. The study tools comprised a detailed household survey with a

focus on livelihood, social and financial inclusion parameters; along with focus group

discussions (FGD) and semi-structured interviews with the community members, beneficiaries,

JEEViKA’s professionals and community workers. The study was carried out with the

administrative and technical support of JEEViKA.

The specific objectives of this study were to understand the genesis and conditions that

promoted rural livelihood programme, JEEViKA in Bihar, further to analyze the role of

stakeholders (CSO, Community, Funding agencies) in promoting JEEViKA’s objectives, and to

identify direct and indirect impact of JEEViKA in the lives of the rural poor in order to

recommend issues that require attention in future for communities managing the strategic

process of their internal resources to the emerging demands for sustainability.

This study is focused on understanding of lessons and learning. The findings are expected to

broaden the understanding towards inclusive pathways of state to society models on

promoting rural livelihoods among the poorest of the poor.

This report includes three cases, they are

1. The Social Inclusion Model

2. The Financial Inclusion Model

3. The Livelihood Inclusion Model

The need of the report lay in the positive context that the state of Bihar is being cited as an

example that redressed some of the barriers that lead to inclusion, and that it is moving toward

inclusive development, through strengthening the development of institutions for the poor, as

well as helping the poor have a voice in civic engagement . In this direction, it is pertinent to

JEEViKA Study Page 14

understand the programme, identify learning and comprehend lessons. With five years of

implementation, JEEViKA provides opportunities to understand experiential models of

promoting collective action and rural livelihoods.

These learning in the context of Bihar are expected to improve understanding on the policies

and programs in the context of rural livelihood development across the country and how the

lessons that need to be kept in mind to ensure development and inclusion go hand in hand.

JEEViKA Study Page 15

2. JEEViKA’s SOCIAL INCLUSION

Social Inclusion

According to the official Mandate of the Bihar Rural Livelihoods Programme (BRLP), social

inclusion is a result of social development and institutional and capacity building. According to

BRLP, the poor suffer from an acute shortage of access to basic public health, education

services and other public schemes. As a result, they incur high cost debt to smoothen

consumption needs, especially with regard to health. The specific objectives of Social

Development are

1. Improve access to preventive and reproductive health care.

JEEViKA Study Page 16

2. Provide opportunities for primary and secondary education.

3. provide for social risk funds at the Village Organization (VO) for use by members to

overcome debilitating risks, and

4. Finance the skill development of health, nutrition and gender activists appointed by the

VO.

The main thrust of institutional and capacity building according to BRLP is towards

1. Creating awareness regarding livelihood options and approaches

2. Transparent, participatory and accountable institution building process is the key

for sustainability of the community institutions initiated.

Training Cluster Coordinators (CCs) and Community Resource Persons (CRPs) to introduce

issues of social and economic empowerment for discussion at the CBOs is critical. The project

would also enable the capturing and dissemination of experiences and learning at the CBOs

based on these social and economic interventions.

Bihar is the most densely populated state (Census, 2011) with approximately 83 million

population, which accounts for one-seventh of the Below Poverty Line (BPL) population of

India. With 9 out of every 10 person in Bihar living in villages, poverty in Bihar is significantly a

rural phenomenon. According to the World Bank report titled - Bihar Towards a Development

Strategy, the challenge of development in Bihar are persistent poverty, rigid social

stratification, poor infrastructure and weak governance. Main problem identified is service

delivery, particularly in services that affect the poor and where the role of the government is

crucial (World Bank, 2005).

The need for the creation of Rural livelihoods in Bihar has been due to the neglect of small land

holder agriculture. Agriculture is the main stay of the Indian population with sixty five percent

involved in it. The contention is that being employed in agriculture itself, does not lead to

poverty but under employment, low productivity, lack of irrigation facilities do ultimately lead

to poverty (Ministry of Rural Development, 2011).

JEEViKA Study Page 17

The (World Bank, 2005) reports that “agriculture in Bihar has been performing poorly and that

productivity was going down by 2 percent per annum in the early 90’s and has been growing at

less than 1 percent since 1995, thus reducing in terms of per-capita growth, with 80 percent of

the work force, employed in agriculture, poverty in Bihar becomes the norm for the populace”.

Poverty and social exclusion are complimentary processes and JEEViKA through its intervention

is trying to correct both the evils of poverty and exclusion. The adherence to social norms, and

the maintenance of social order requires the involvement of the subaltern in the growth

paradigm, the failure to do this, has adverse effects on both the community living in these

areas, as well as for the country. At the macro level, the marginalization of the subaltern, raises

doubts in the minds of the youth regarding the role of India as the nation state in their minds.

This structured form of alienation leads to rebellion. In her article, Chitralekha (2010) mentions

that the youth of Bihar and Jharkhand, who are not able to join the formal system, due to lack

of opportunities, get influenced to join the MCC1 outfit of the Naxals, in order to secure a better

future and lives for themselves and their families, this cadre that joins for money and lack of

opportunity in the main stream are termed as “Drifters”. This youth does not share the Naxal

ideology strongly, but they support it for their own personal benefit, this group is vastly

different from the ‘committed cadre’, which shares the pro poor Marxist ideology, and from the

‘opportunists’, who look at naxalism as a means of acquiring and exercising power.

The need for social inclusion arises as a way to tackle rebellions within and against the state. It

becomes important to give the youth opportunities for the channelization of their energies,

while also ensuring that equity is made a virtue of development, and the barriers of caste , class

, gender are transcended at each given opportunity. It is interesting to note that a majority of

the Naxal cadre fall in the Drifter category, showing a direct correlation with lack of

development and the rise of communism. Moving beyond the aspect of conflict, through a

rights based approach, social inclusion is considered to be a necessary condition for poverty

reduction, as it brings about participation and access. Here it must be noted that poor people

have the right to participate in their development plans, and access regular information

regarding their plans(Cornwall & Musembi, 2004). JEEViKA’s strategy to build institutions of the

1 Maoist Communist Center

JEEViKA Study Page 18

poor is an appropriate strategy, to work from a rights based perspective, because the

enforcement of rights requires strong institutional structures, which the poor do not have

access to. From the perspective of vulnerabilities we see that in the Tonle Sap lake area,

Cambodia which is characterized by high floods , it is found that the community’s ability to

adapt to unpredictable climate is restricted due to homogenous livelihood, inequality

experienced by minorities in the political discourse, and the lack of capacity building needed to

help in livelihood diversification( Varis,2010).

Thus a holistic approach to social inclusion i.e. building capacities of the people and giving

voice to the marginalized in political discourse and linking it to livelihood development is

imperative to improve resilience of the poor people from a vulnerability perspective.

Introduction to Social Inclusion in the context of BRLPS2

The main focus of the BRLPS is on mobilizing the poor around livelihoods and to enable them to

develop institutions that can sustain their engagement with the newly introduced business

models by JEEViKA. To achieve this, it in turn endeavours to develop collectives of empowered

group of poor people. These groups of people are expected to be fully enabled to assert access

and utilize their entitlements over natural, physical, human, social and financial assets. They are

also able to manage their transactions through negotiation, peer pressure and advocacy(Bihar

Rural Livelihood Program Society, u.d., p. 10). The process of development is seen to be linear,

thus social inclusion of the vulnerable is a prerequisite for the development of new livelihoods.

Thus, the initiative considers social inclusion to not be an end, but an ongoing activity.

JEEViKA, is focused on inducing livelihoods through the process of micro-credit disbursement,

the main target group is women from poverty ridden households, thus the impact on gender is

a key to understand social inclusion in the context of JEEViKA.

2 Bihar rural livelihood program society

JEEViKA Study Page 19

Observations and Findings:

Social Inclusion as a process is aimed to achieve empowerment as its goal. Here we define

empowerment as “the ability to feel useful and important”. Our finding suggests that social

inclusion has happened as a result of the inclusive platform that JEEViKA has created at the

community level. The project has helped in creating an identity for the unknown women and by

increasing their unity.

The women interviewed commonly remarked that “hum jeevika ke pehele kissi ka naam

nahi jante the, pati ke naam se ya bete ke naam se jane jate the”(before JEEViKA we did

not know any woman by name , we were called by our husband’s or son’s name”). A

name is an essential part of building an identity, which is a prerequisite to be able to feel

important. Absence of identity was considered as absence of desire and dream for a

woman in the village. Rekha said, ham aaj apne astitva ko banana chahete hain, hamari

aaj ek pehchan hai. (We nurture our identity, today we are recognized).

SHG meetings happening once a week became a platform for interaction amongst the women,

and also led to a deeper understanding of the common issues that they faced. Beyond the

activities of saving and detailing the books of records, the key reason for them feeling

empowered is the ability to associate and discuss their lives amongst their peer group.

Inclusion should be seen in the larger social context under which it is embedded. Unlike past

when women in Bihar women decision to cook was also influenced by the choice of the male in

the family, today women are taking decision in family and are participating in village level

development.

Women of the different SHGs in village came together to decide on the place for boring

for water. Woman members at home are part of the collective decision making on

issues of crop to plough, sell and decide on their children’s education and health seeking

behaviour. The collective of women has reduced gender specified culturally defined

roles and responsibilities. There are rare families who still discriminate in sending girls

and boys to different schools. Sunita Devi said, “while observing us in the meeting our

daughters ask us why there is an incidence of bias between a boy and a girl”. Though

JEEViKA Study Page 20

boys and girls are sent to school, but bias was observed at the time of private tuition.

Boys were sent for private tuition, while girls were expected to study on their own.

Sending girls to government school and boys to private school is a past phenomena,

Chandni devi3 remarked “that our group members will ask the reason if anyone does

such a thing”. The original idea of self help groups as a collective for peer accountability

to repay loan on time, is reaping social inclusion as interest.

We first start with understanding the groups which suffer from social exclusion and the reason

behind it. Traditionally speaking, women, the scheduled tribes, the lower castes and the poor

people are the ones who get excluded from the development paradigm. Though the economic

marginalization among the upper caste is not the same as lower caste, but among the poor,

caste as a barrier for multi-caste SHGs is abridged.

Literature suggests that the feminist authors (Thampi & Devika,2007) are still critical of micro-

finance as the key to women emancipation, they argue that women empowerment is

dependent on a number of factors like water and sanitation, healthcare, food insecurity, power

structures, lack of basic education and the effort to consider micro-finance as the sole

technique to overcome these bottlenecks is fairly utopian(Sengupta, 2013).

The exclusion of women from the paradigm of development has been due to a variety of

reasons. Being traditionally a patriarchal society, norms and values of society favored the male

over the female, thus leading to the blocking of their progress. The specific issues that the

patriarchal and caste based society led to are a lower level of education, a restriction to be

engaged in gainful employment, an inability to access healthcare, and a lack of freedom of

choice and opportunity. Stratification based on caste and patriarchy is a social construction

which has over time encouraged that women be submissive, it has conditioned women to

exercise least amount of power and progress, in the areas of male dominance. The compliance

of unequal non competing roles between male and female gives stability to societies but roles

which are inherently based on exploitation for a particular gender cannot be sustainable in the

long run.

3 Name changed

JEEViKA Study Page 21

Programme Strategy of Social Inclusion

The BRLPS aims to institutionalize inclusion by the process of making women groups in the form

of SHG’s. The self help groups are created on a basis of affinity, homogeneity and proximity of

location. The logic is to develop strong social ties, and this is done by reinforcing the already

existing ties in the village rather than creating a whole new relationship pattern(Pramod, 2014).

In terms of homogeneity, it is more important that similarity in economic class be present

rather than the caste similarity. The strategy is to form SHGs more on spatial proximity. It

leverages the administrative efficiency of SHG management and social capital of neighborhoods

makes it more sustainable as a group in the village. However, in areas where a particular caste

is present in large numbers, it is preferred to form a same caste SHG. In areas where not

enough members of one caste are out of SHG fold, multi-caste groups are formed. The strategy

is to prioritize spatial and social overlap as a strategy of group formation.

Through these two lenses; caste and location, BRLPS aims to create SHGs and thus induce

social inclusion, in the form of collective bargaining and empowerment. The strategy of spatial

and social overlap strengthens unity towards common cause of the area and their social cause.

Affinity amongst the group was present as a result of their proximity of households, but

considerable work was needed to convince women to save money in the SHG and that the

money would remain in their hands only, and that BRLPS will not have access to their

money.(Pramod, 2014).

JEEViKA Study Page 22

Programme structure at the community level-

The process of social mobilization and creating women collectives requires a definite strategy.

JEEViKA team member upon entry into the village, starts with a social activity, like a village

cleanliness drive, they then take up residence with the poorest families, to show their clean

intentions and build trust amongst the community as a partner, thus by showing the poor

dignity and respect, and through this mechanism JEEViKA wins people’s trust(Pramod, 2014).

In order to extend its coverage, the program uses Community Resource Persons (CRPs)4 to help

in formation of SHGs and VOs5. CRP’s are members of the community who were in the same

situation as the current intended beneficiary but now are in a better social and financial

situation due to JEEViKA. Thus, the CRPs are able to influence more members to form and join

SHG’s due to their personal history. Expansions happen through the CRP’s and village

organizations. Village organizations are a group of ten-twelve SHGs who come together to form

a larger group with a different set of responsibilities. Initially when a group of SHGs make a VO,

4 Community resource person 5 Village organization

Block Levek Federation

•Three members from each VO in a block join the block level federation•Main role is to strenghten the VO's and liaison on behalf of the community for better public services and help in avaling of pro-poor schemes

Village organization(VO)

•10 SHGs come together to form a Village Organization•VO is the organization head of the Social Audit Comittee ,Bank Linkage Commitee,Social Action Comittee and Repayment Committee

Self Help Group

•Groups of 8- 10 women made on the basis of affinity, who come together as a a collective to access micro finance services

•Governed by five rules- weekly meeting, weekly savings, regular lending and borrowing, timely repayment of loan, maintaining books of record acccurately

JEEViKA Study Page 23

their handholding is done for a period of six months JEEViKA, after which the VO becomes

independent. The main role of the village organization is to make the poorest members of the

community join, and make sure that no household is left out. Thus, village saturation is to be

left to the VO, which makes it extremely important to build on the capacities of the VO.

The other important responsibility with the VO is that if any member has any problem based on

caste, VO directly engages in dialogue with the offender, this is a key reason to improving inter-

caste relations, as VO is a major deterrent against caste exploitation. VO’s also tie themselves

with the government schemes like pension, insurance, etc.

Data Analysis

The study focused on the changes that JEEViKA had brought about in terms of social inclusion of

the disadvantaged group, with a particular focus on women. A survey of 84 women

beneficiaries was conducted using a semi structured interview and focus group discussions. It

was to come up with a set of issues which the women of the village consider success and

identify hindrances in the movement of women in moving towards gender equality and social

cohesion. The key identified issues were unequal educational status and need, unequal health

needs and access to care and cure, unequal independence from domestic roles and family

restrictions. Analysis of the data showed that 29.8 per cent of women feel that there is no

gender bias in health and education seeking behavior in the village, 57 per cent of the

surveyed women supported this outcome to the functioning of the SHGs. However, 27 per cent

of the women felt SHGs made an impact but gender bias is still present though they consider

the situation to be continuously improving and they felt that women are marching towards

increased freedom and empowerment. The problems that the women face were considered to

be unequal independence followed by uneven education and healthcare access. See table 1 for

details.

JEEViKA Study Page 24

Table 1: Social Inclusion

Issues Frequency Percent

Uneven education 15 17.9

Unequal health care 13 15.5

Unequal independence 24 28.6

Family restrictions 7 8.3

No disadvantage 25 29.8

Total 84 100.0

Figure 1: Five Key Reasons for Inequality

On being asked, how they thought women were treated unfairly in comparison to men, the highest percentage of women felt (30 percent) that no disadvantage in the community was present. Unequal independence which is a result of patriarchal norms was given importance by a similar 28 percent of women. The other reasons cited for inequality were uneven education and healthcare.

JEEViKA Study Page 25

Identity as a prerequisite to empowerment

In this section, we look at an understanding of empowerment based on the notion of self, we

theorize that for a group or gender to be empowered at various levels like at the household

level, community level, and at the political level, the first prerequisite is to create a strong

notion of self, which we understand as personal empowerment.

This pattern of empowerment is not dependent on others and is an internal process that

women develop and strengthen(Rowlands, 1997). The ability to have their own voice in

matters, was related to the ability to think for their own selves, and their aspirations, like Sonu

Devi commented “ JEEViKA ne hume aapna pehchan or sapne dekhne ka mauka diya hai”

(JEEViKA , has given us a personal identity , as well as the ability to dream for ourselves”)

Identity and income help in reducing insecurity, we show this through the following figure

JEEViKA Study Page 26

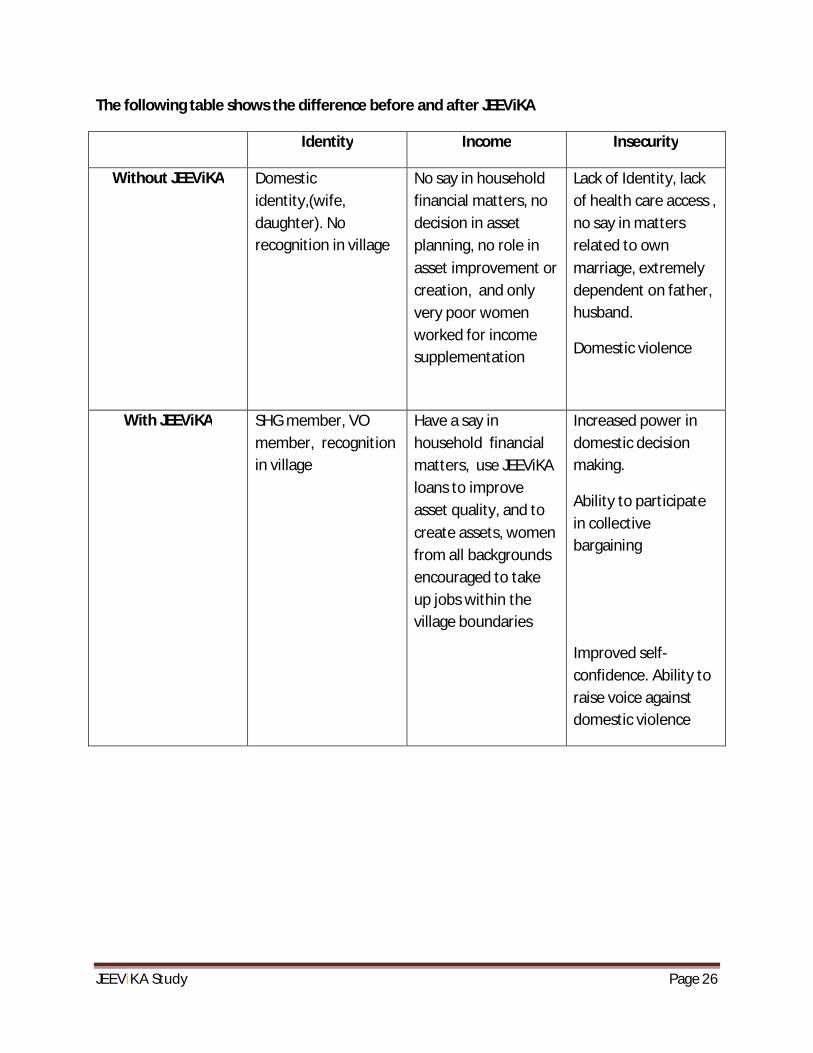

The following table shows the difference before and after JEEViKA

Identity Income Insecurity

Without JEEViKA Domestic identity,(wife, daughter). No recognition in village

No say in household financial matters, no decision in asset planning, no role in asset improvement or creation, and only very poor women worked for income supplementation

Lack of Identity, lack of health care access , no say in matters related to own marriage, extremely dependent on father, husband.

Domestic violence

With JEEViKA SHG member, VO member, recognition in village

Have a say in household financial matters, use JEEViKA loans to improve asset quality, and to create assets, women from all backgrounds encouraged to take up jobs within the village boundaries

Increased power in domestic decision making.

Ability to participate in collective bargaining

Improved self-confidence. Ability to raise voice against domestic violence

JEEViKA Study Page 27

Multiple identities are created, woman as a self, identity of the group with reference to SHG

that they belong to and part of JEEViKA, often called as ‘JEEViKA ki didi’.

Figure 2: Multiple Identity of a woman in JEEViKA

In our study nearly all respondents echoed the thought that “Hum Samuh banne se pehele ek

dusri didi ka naam bhi nahi jaante the, ab hamari ek pehchan hai”. (we did not know the name

of other women before joining the SHGs.)

This quotation reflects the lack of identity women suffered from in the villages of our study in

Bihar. The respondents mention that a woman had no identity, she was referred with reference

to dominant male of the family. The unmarried girls were referred to as “daughter of father’s

name” while married woman were referred as “wife of husband’s name”. Prior to JEEViKA’s

intervention, having an independent identity was not desirable. The notion of self is an

ingredient of empowerment; while self is an amalgamation of identity, income and insecurity.

The study reveals that increase in identity in the family, community and by institutions such as

bank increases options for income. Rise in identity and income reduces insecurity promoting

empowerment. Studies at various levels have considered that a strong sense of self within a

Member of JEEViKA

(Programme and Purpose Identity)

Member of the VO (Organlisation and

Income + Community

Identity)

Member of the SHG (Group and

Solidarity Identity)

Woman as a Self

JEEViKA Study Page 28

collective milieu is what leads to personal empowerment.(Lord, 1997). Traditionally women of

the villages, without their identity, suffered from acute powerlessness due to their inability to

create independent social space. The study reveals that the ability and desire to follow one’s

own needs and wants constitute the critical component of empowerment. However, it can only

happen when individual identity of the self is created. A notion of self linearly leads to an ability

to bargain for the self.

Social networks and Empowerment

JEEViKA’s engagement over the past few years in the village is seen by the community as a

major milestone towards their emancipation. A major shift in the community is noticeable in

the way the program is being currently perceived by the people of the village. From being

reluctant to participate in government schemes, today most men encourage their women to

join SHG’s. It is for the first time that the state and the community are considered as partners.

The state often considered the community as patron, but never reached the marginalized. Sita

said, “sarkar pehli bar samaj ke beech hai. Pehle ham sarkar ke paas jate the, aaj sarkar hamare

paas aati hai” (It is for the first time the State is within the society. Earlier we use to go to the

State, today the State comes to us).

Social networks create a sense of belonging for a certain group of people. By seeing their lives

through the eyes of their peers, a new level of awareness is achieved. As they see their lives

from the perspective of others, by routinely discussing issues which they otherwise would not

have spoken of women realize if they are going through any unfair practices at home or if the

girl child in their house is being treated unfairly

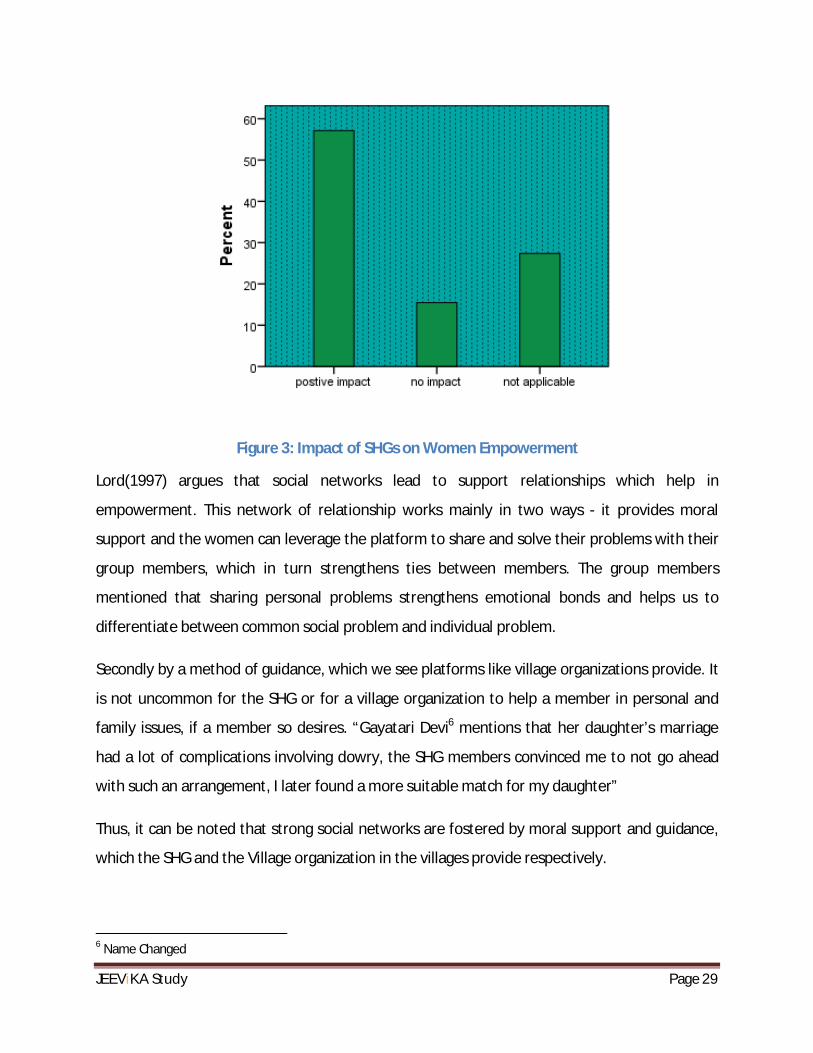

Figure 2 below shows the impact as perceived by the women. A majority at 57 percent believe

that SHGs created a positive platform for women’s empowerment. (The responses stated in the

graph below were answers to the question posed to women – what was the impact of the

formation and engagement of SHGs on your empowerment levels? Here “Not applicable” is

used for those women who see no difference between men and women empowerment, thus

do not consider SHGs to be a changing force.

JEEViKA Study Page 29

Figure 3: Impact of SHGs on Women Empowerment

Lord(1997) argues that social networks lead to support relationships which help in

empowerment. This network of relationship works mainly in two ways - it provides moral

support and the women can leverage the platform to share and solve their problems with their

group members, which in turn strengthens ties between members. The group members

mentioned that sharing personal problems strengthens emotional bonds and helps us to

differentiate between common social problem and individual problem.

Secondly by a method of guidance, which we see platforms like village organizations provide. It

is not uncommon for the SHG or for a village organization to help a member in personal and

family issues, if a member so desires. “Gayatari Devi6 mentions that her daughter’s marriage

had a lot of complications involving dowry, the SHG members convinced me to not go ahead

with such an arrangement, I later found a more suitable match for my daughter”

Thus, it can be noted that strong social networks are fostered by moral support and guidance,

which the SHG and the Village organization in the villages provide respectively.

6 Name Changed

JEEViKA Study Page 30

Collective Bargaining and Social Networks

Collective bargaining has traditionally been used in trade union studies(Jerry, 1985). In context

of this study, the ability to form a group and use the group platform to collate voices for the

betterment of public good and to create opportunity for self is considered to be collective

bargaining. The male respondents in our study villages mentioned that there has been a

marked shift in the way the voices of women are being heard within the family and in the

village. This voice is not limited to empowerment of the self or the group. It is used to demand

better services from PDS7 fair price shops (FPS) , and other services. Thus the benefits are

accrued to the whole village members . Collective bargaining has lead to women taking control

of management of FPS in the villages of Bhagair and Sekhwada, peaceful demonstrations have

been ongoing in the village of Bara, but the results are yet to be awaited.

The Public Distribution System in these villages was marked with a high level of corruption, the

respondents mentioned that they were able to access their rightful monthly ration only three

to four times a year. Similar situation still exists in Bara village, thus actions are being taken by

the community members by using peaceful demonstrations as a tool for advocacy. In the

villages where this change has already taken place, the effectiveness of the PDS has gone up as

the poor women form the village organizations and take charge of it.

For the men, this comes as great respite from the resistance that they met earlier when they

visited the higher government officials. A proud husband of one of the woman leaders

exclaimed - “Hum aadmi jaate toh yahi baat mahine tak chalti. Hum toh ek do karke alag alag

jaakar milte the, kabhi saath mein ikatha hokar toh gaye nahin, isliye hamari baat bhi kabhi

suni nahin gayi. Mahilaon ke ekatrit hokar kaam karne se hi toh hamari itni tarraki hui hai.” (If

we men used to one by one on our own then no one ever paid heed to what we were

demanding. Moreover, the men never thought of going as a group. By the women getting

together as a unified force we have seen such prosperity – had it been left to the abilities of the

men, the same thing would have taken much longer).

7 Public distribution system

JEEViKA Study Page 31

There has also been a very positive impact on the nature of the community’s relationship with

the government. Namita Devi8 expresses “We all have learnt the benefits of collaborative

partnership with the government. From being reactive and rigid, men folk from the village

fought regularly with government officials, we have now shown how we can peacefully and

legally bargain through collectives in front of authorities and get our work done.”

Access and Control

Access and control experienced by women in the villages is an important indicator to study

their empowerment. Access refers to the ability to use a certain product or service, and control

refers to the ability to decide and make informed decisions regarding issues concerning daily

life. Rural women had access to limited goods and services and lack of ability to control

resources within and outside family. The conditioning of women towards a set gender role

formed by society leads to a situation where many key aspects of their life fell beyond their

control (Dube 2001). Women’s decision making roles related to matters of assets and property

are crippled, due to patriarchal society with an over-emphasis on dowry , and an under-

emphasis on education and productive work. The current study understands how women are

viewed by their families as adding to their family expense pressure, while completely ignoring

their capability of income generation. How women’s role and recognition beyond cooking,

caring in family has changed due to JEEViKA. Our study indicates that the nature of gender

relations has started to change with the advent of JEEViKA, due to entitlement to access loan at

two percent interest rates, which are far lower than interest rates of money lenders. Though

income generation is still the priority of males, women do control its success and failure.

Women mention that overtime there has been a positive co-relation between SHG’s and their

decision making pertaining to household expenses, deciding their children’s marriages, their

ability to access health care, and their ability to make decisions regarding family assets. It is

important to note that amongst the elderly women, a majority of the decisions regarding assets

are still being made by the men, but the rise of decision making space amongst the younger age

group has expanded drastically. On enquiry about relocation due to income option outside

8 Name Changed

JEEViKA Study Page 32

village, husband of Rani said “hum bina apni patni ke nahi kah sakte hain” (we can only decide

after discussing with my wife).

However, women empowerment is not merely presence or absence of participation in

economic activities. It should be understood with as a choice or compulsion. It is noted that

women belonging to very poor families have to work in order to meet the income requirements

of the family. It is more out of necessity rather than choice, it does not necessarily mean

empowerment. It does not replace her roles within the household, but increases the

responsibility outside family too.

Thus we understand that productive employment of its own is not necessarily an indicator of

women empowerment, the ability to choose is an important factor to remember.

The figure 4. below shows that in terms of access and control most women have the ability to

decide over families expenses, this is also partly due to the fact that the pressure to run the

kitchen and manage household necessities is on the shoulders of women. It is important to see

that a extremely high majority of women are being able to have important role in matters

related to marriage. Although women decision making has increased in some key areas, but

areas such as asset and income still depicts inequality. 60 per cent of women still consider

themselves to have a say in matter related to family assets, but when seen in comparison with

access and control in other areas of life, this figure seems to be low.

Figure 4: Gender Empowerment at Household Level

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

Household expenditure

Own and Children marrige decisions

Family Assets

Ability to be active income contributor

JEEViKA Study Page 33

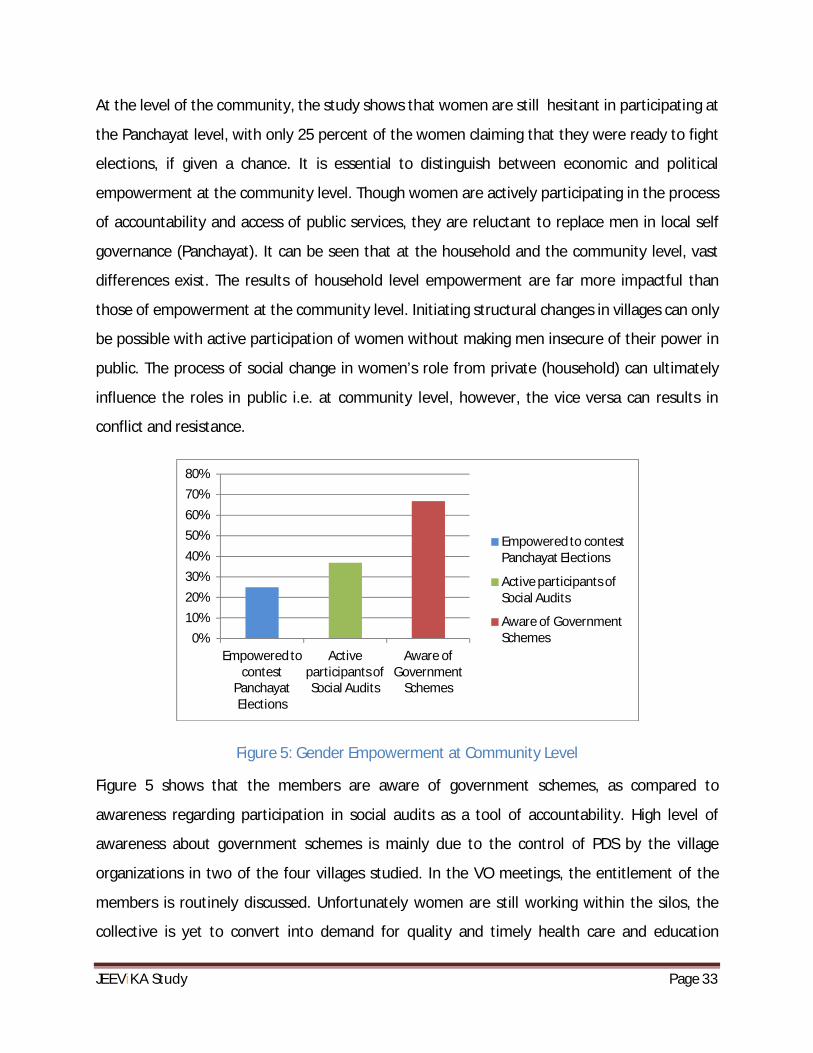

At the level of the community, the study shows that women are still hesitant in participating at

the Panchayat level, with only 25 percent of the women claiming that they were ready to fight

elections, if given a chance. It is essential to distinguish between economic and political

empowerment at the community level. Though women are actively participating in the process

of accountability and access of public services, they are reluctant to replace men in local self

governance (Panchayat). It can be seen that at the household and the community level, vast

differences exist. The results of household level empowerment are far more impactful than

those of empowerment at the community level. Initiating structural changes in villages can only

be possible with active participation of women without making men insecure of their power in

public. The process of social change in women’s role from private (household) can ultimately

influence the roles in public i.e. at community level, however, the vice versa can results in

conflict and resistance.

Figure 5: Gender Empowerment at Community Level

Figure 5 shows that the members are aware of government schemes, as compared to

awareness regarding participation in social audits as a tool of accountability. High level of

awareness about government schemes is mainly due to the control of PDS by the village

organizations in two of the four villages studied. In the VO meetings, the entitlement of the

members is routinely discussed. Unfortunately women are still working within the silos, the

collective is yet to convert into demand for quality and timely health care and education

0%

10%

20%

30%

40%

50%

60%

70%

80%

Empowered to contest

Panchayat Elections

Active participants of Social Audits

Aware of Government

Schemes

Empowered to contest Panchayat Elections

Active participants of Social Audits

Aware of Government Schemes

JEEViKA Study Page 34

through social audit. Only 35 percent of the members are active participants of social audits. It

was observed that women collective are yet to confront the rural elites. Panchayat represented

by powerful families and other public services are in connivance. As a result, women are unable

to impact upon the poor services of health and education. It will be possible when impetus to

resist is orchestrated by JEEViKA.

The Role of SHGs in Promoting Inter-Generational Social Equity

To incorporate the effect that JEEViKA’s programs, the study tried to understand the liberal

future for the girl child in the study villages. As social inclusion is an ongoing process, it is

important to understand the effect of JEEViKA on future generations, by analyzing the

worldview of the current generation.

A common but silent preference for boys exists. This preference is believed to arise due to the

ability of boys to contribute to family income and take care of parents in their old age and girls

being considered a weaker gender due to increased burden of dowry without the ability to add

income of the household. This culture of gender discrimination is ingrained in the thought

processes of women too. A discussion with the beneficiaries of JEEViKA brought about the

insight that female oppression is not merely a phenomenon due to the male members of the

society. Mohini Devi9 expresses “earlier women used to make high demands for dowry and

preferred to educate their sons, a mother was the daughter’s biggest enemy”.

An accepted behaviour or thought process that becomes a part of the dominant culture starts

to be seen as a norm in the society. In Baradi, the women feel that a change in attitudes has

started taking place and the SHGs of JEEViKA are seen as the catalyzing force for this change. In

the villages of Barachatti Block, borrowing money was primarily men’s prerogative. In the

initial phase, there was apprehension about the need of women to build such savings group

and enter a primarily male bastion. Also the increased mobility of women out of the household

was a cause of concern. The interest rate differentials offered by micro-finance was the original

attraction, which made men agree to this addition of roles to the women’s work load. In about

9 Name changed

JEEViKA Study Page 35

a year’s time, the change in the way women saw themselves started to arise. Mohini Devi10 a

health worker with a local NGO exclaims that the SHG was a key reason due to which my

husband allowed me to go outside the village to work. “Earlier it was not just his traditional

mindset, but fear that I would not be able to work in the outside world”.

Many such important cases point to the fact that women are now taking responsibilities

beyond their traditional roles. This confidence on self for the ability to perform is an important

process of empowerment in the current context. Women now mention in a majority of the

Focus group discussions, that the difference between boys and girls although exists, but gender

bias is fast fading away. They attribute it to the change in the mindsets of women more than it

is to do with male oppression.

Caste

The formations of SHG’s group identity along with the rising identity the women have led to the

thinning of caste barriers. This should be considered an indirect effect, for reasons explained

below.

Intercaste acceptance of food has been a recent phenomena. VO meetings, weddings are major

melting pots, although at the personal level there is still some hesitation in accepting “kaccha”

(unoiled) food from lower caste. Fried foods are accepted in most settings but it is difficult to

say if this is an outcome of SHG formation or schooling, and other common sources of

interaction. However, SHGs have played a major role in reducing caste barriers. JEEViKA’s

strategy is more based on poverty and proximity of location. According to an interview with

JEEViKA Staff, SHG making is done on the basis of proximity of locations, the preference from

JEEViKA is to form homogenous caste group SHG. In case a single caste is not concentrated in a

geographical location then, a heterogeneous group of similar economic status are considered,

reinforcing the caste alliance. This strategy of social mobilization initially instills horizontal

cohesion within the caste followed by inter-caste integration between the SHGs resulting in a

cohesive community (Pramod, 2014).

10 Name changed

JEEViKA Study Page 36

In terms of religion, in Bhagair village Muslims are also present. Their SHGs are of the same

community as their settlement pattern is also clustered as caste settlements. Challenges of

poor Muslim women into collectives are different due to wide segregation in roles and

expectations from women and high community cohesion. Thus it can inferred that inter-caste

integration has increased more than the inter-religious. It is also important to note that caste

still plays an important role as an identity, even after reduction in untouchability/oppression of

lower castes especially in marriage. Marriage outside caste is unacceptable. Intra-village

marriage is also considered taboo as village is thought of as one large family.

The Current Situation, Challenges and Ways Out

The exposure and experience of the women of JEEViKA has made them find a place of dignity

for themselves in society. Women remark, “JEEViKA has truly helped us in gaining a voice and

we are no longer afraid of demanding action from Sarpanch, BDO or police inspector. Earlier we

were extremely scared of government officials, they used to speak extremely rudely with us,

now we had a meeting with the Chief Minister of Bihar. Our belief in ourselves has increased

many times. People like you and from foreign countries also come to visit us”. Women

experience greater autonomy and higher participation in decision making at the household

level. At the village level also participation in decision making has increased as women have

taken control of PDS. There is still a lot left to be desired out of the situation at the community

level and in empowerment for better access and utilization of basic public services.

The knowledge regarding tools like social audit, is fairly limited and the awareness regarding

new government schemes is below the expected level. Women’s participation in social audit

needs to be strengthened.Village segregated data points to the fact that at 40 percent

awareness and participation, Sekhwara and Bara village have a higher degree of participation in

social audits, than the villages of Bhagair and Baradi, where awareness and participation of

social audits is a mere 15 percent.

In Mahatma Gandhi National Rural Employment Guarantee Scheme, studies argue that the

process leading to the social audit and the follow-up after the social audit are as important as

the audit itself, and as social audits are a qualitative process, they need immense efforts at

JEEViKA Study Page 37

grass root mobilization and preparation of the community to understand the process of social

audit and the needs it shall fulfill (Ambasta & Shah, 2008). Organizing trainings for the VO which

in turn shall train the SHGs would be the advisable way forward. This training should not be a

one off event but a continuous process till the audits start becoming successful. Guidelines

from JEEViKA in this direction will add pace to the process and participation of women in

improving the accountability of public services through social audit.

While looking at the fact that there is an increase in the voice and visibility of women in the

community, we should remember there is a long way to go in removing the limitations to their

growth as empowered individuals.

It first needs to be clearly stated that empowerment like social inclusion is a means and not an

end to livelihoods and empowerment. Every benchmark of success today becomes the baseline

for tomorrow. Therefore, at no point it can be said that women have achieved “full” or

“absolute” empowerment. The quest for women empowerment is a journey, not a destination.

Gender roles have not changed over time, and additional duty of groups and micro finance, has

been added to the existing responsibilities of women. Women in the study area are responsible

for all domestic duties as well as collecting fodder and water for the household and livestock,

this stagnancy in gender roles show that micro-finance within itself, is not capable of changing

these predefined roles. Issac (2002) states that micro credit or micro enterprise building can

facilitate the process but the real challenge lies in creating awareness and societal

implementation of more gender neutral roles. Paterson (2008) in his study of women

empowerment in Balochistan emphasizes the role of recreating every day roles of men and

women through specific training programs. However, as a strategy, income generation for

women can only be successful when it allows her to perform her traditional role. Women

indicated that income generation options ideally suited are the ones that are located in

physical proximity to their households. Relocation is a possible option for men with high

income gain; women’s preference is to opt for income generation options not involving

permanent relocation in order to avoid role conflicts.

JEEViKA Study Page 38

For mainstreaming the poorest of the poor, capacities of the VO should be built, in terms of

social inclusion through participatory poverty assessment. VOs should be aware of exclusionary

indicators of a local area, thus members being left out, will also start getting included. It was

found that even in the model villages few families are left out of JEEViKA.

In the section Access and control it was stated that women had more access to productive

labour, especially in cases where the family situation demanded money. This leads to a

gendered understanding of women’s labour. Interviews with the respondents and FGDs lead to

the understanding that the ability of women to spend money on their own self is extremely

limited. The earnings of the women are meant for the family, and thus societal expectation of

self sacrifice from women does not let her escape from the poverty she faces on account of

being a woman. However, women collective do provide a venue for social collateral to change

the status of inter generational inequality by reducing bias against the girl child.

Another major challenge for social inclusion is the lack of toilet coverage in the village. The total

sanitation campaign provided a certain number of toilets in the village but the inability of SHGs

to convince the men in the community to build toilets combined with the reduction in open

defecation space, shows that a lot needs to improve in terms of women empowerment.

We conclude by saying that SHG formation has brought in collective bargaining, now specific

strategies need to be developed for men and women groups separately.

It is imperative for the community to understand the gender roles being played in daily life

while aiming for a more egalitarian society through gender guided workshops and training

programs.

The community mobilizers need more training in helping solve issues of gender conflict, and

specific sensitization workshop for men can be recommended. Social inclusion has taken place

due to the aim of financial inclusion, its time that empowerment of women is looked into

separately as a key to social development. The rise of mobilization entails rise of linear upward

movement, without government institutional design to make system gender neutral, the

process may not achieve sustainable outcome.

JEEViKA Study Page 39

3. Financial Inclusion

The Context- Practice and Policy

The assumption that poor can come out of poverty, if they were organized as a social collateral

and given the opportunity for financial inclusion through formal institution such as banks and

Micro Finance Institutions (MFIs) led to the rise of the micro finance movement. The successful

implementation of this model by the Grameen Bank in Bangladesh has resulted in wide spread

experimentation across the world. By definition , microfinance aims to provide “permanent

access to an appropriate range of high quality financial services, including not just credit but

also savings, insurance and fund transfer” (Christern & Rosenberg, 2004). According to

JEEViKA Study Page 40

Sinclair(2001), micro finance has emerged as a solution to financial exclusion. A widely

accepted definition of financial exclusion is "the inability to access necessary financial services

in an appropriate form" (Sinclair 2001).

In India financial inclusion has been a priority for the Reserve Bank of India. In 1977, the Indian

central bank policy made it mandatory for banks to open four rural branches in unbanked

locations for every new branch in an already banked location(Burgess & Pandey, 2005). Though

the policy lasted till 1990, it led to a major expansion of rural banking network. Despite clear

policy direction, it unfortunately did not achieve the desired goal. In the 2006-2007 budget the

then Finance Minister of India P. Chidambaram mentioned in his speech that just 22 percent of

the Indian population received financial services from the formal sector(Dev, 2006). The goal of

financial inclusion through formal banks could not be achieved for a number of reasons-

vulnerability of small and marginal farmers, the lack of education of the borrowing group, the

inability to provide any form of collateral the indifferent attitude of the bank staff and high

consumption of loan in non-income related activities such as health, education and marriage. In

2005 the Rangarajan committee declared that rural banking must be friendly to the vulnerable

and marginal farmers. It stated that rural banking needs to be differentiated from commercial

banking. Since it is a mix of social and commercial development, the work ethos of rural banks

must be developed accordingly (Rangarajan 2005). Recognizing the increase in need of banking

services and change in policy and practices, banks have started to follow a more inclusive

approach to the financial sector. This is also supported by the RBI introducing no frills, zero

balance bank accounts in 2005. A good example would be states like Bihar , as they have

arrived at an agreement with the banks to provide a loan of a minimum amount of Rs. 50,000/-

irrespective of the consumers paying capacity.

One of the poorest states in India, Bihar is characterized by a high incidence of rural poverty,

which at 41.1% is far higher than the rate of urban poverty at 24.7%.(World Bank, 2005). The

lack of institutions for the poor to organize themselves has also inhibited their economic

growth. Rural savings in the context of Bihar were characterized by unscrupulous chit fund

JEEViKA Study Page 41

operators, which despite being officially banned, continue to operate in various guises

throughout the state, further increasing people’s lack of trust in investing, or parting with their

money.

A study by BASIX (2007) on the Status of MFI11 highlights that the key reasons for Bihar to be

put on the map of financial inclusion are : :

Presently one bank exists for every 22,224 of the population,where as Punjab,

Maharashtra and West Bengal are much better with a bank existing for every 9000,

11000 and 14000 respectively.

37 blocks of the state don’t have a single branch of commercial banks.

700 to 800 bank branches are functioning with a single person on board.

The credit –deposit ratio is pegged at 32.10% much below the national average of

57%.

High debt due to informal lending and under servicing of the population by banks in Bihar,

coupled with a lack of faith of people in banks regarding formal credit and savings instruments,

are one of the important reasons that lead the Bihar government to initiate a microfinance

program based on mobilization of the poor. The Bihar Rural Livelihood Program Society (BRLPS)

became the corner stone for livelihood generation, by using micro-finance as a stepping stone

for poverty alleviation and alternate livelihood generation.

Strategy

The BRLPS aims to achieve economic mainstreaming of the poor and the vulnerable and to

break the cycle of low investment, low return and low consumption (Bihar Rural Livelihood

Program Society, 2007, p. 7). The use of micro-finance as a weapon is directed towards three

objectives according to the program mandate of BRLPS. The objectives (BRLPS, 2008, p. 14)

state that micro-finance should be able to:

11 Micro Finance Institution

JEEViKA Study Page 42

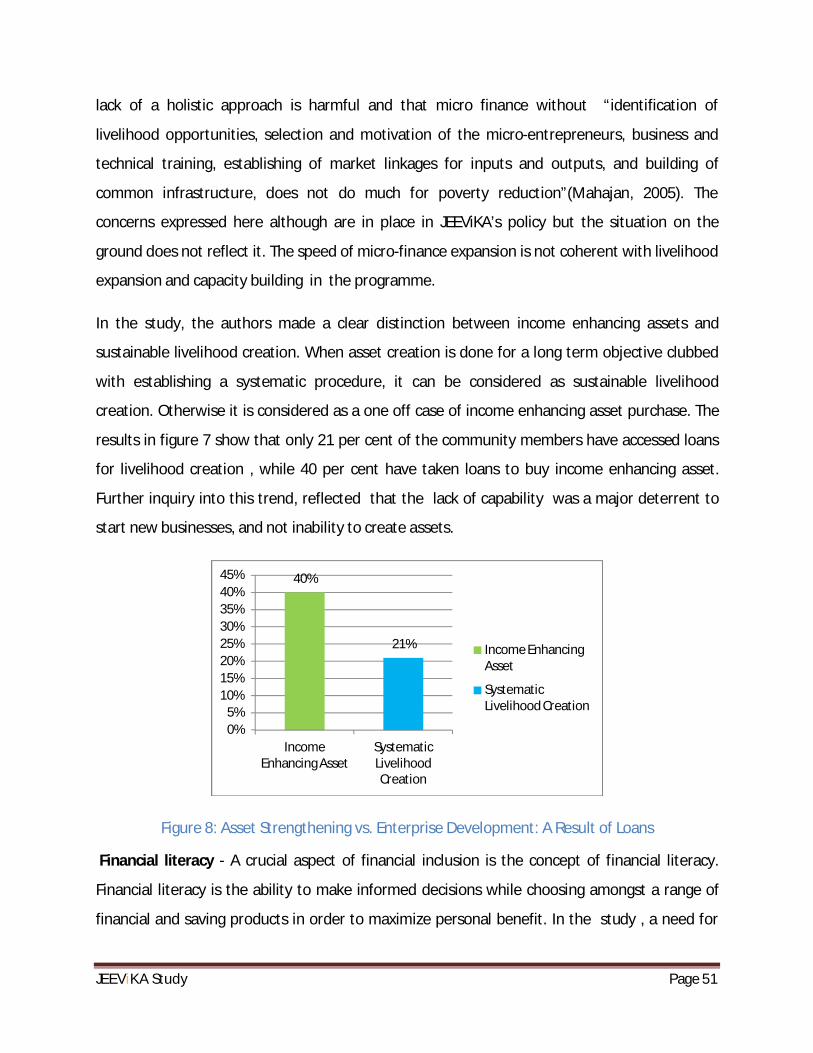

1. ensure that assets are created and incomes are improved for the community based

organizations (CBOs) established or strengthened in the project;

2. facilitate the poor to convert their secure asset base into an economically viable,

improved and sustainable living;

3. facilitate book-keeping and accounting systems for CBOs for promoting transparency,

accountability and ambience of faith for other stakeholders.

Amongst the various forms of micro-finance programs, the BRLP uses a SHG- Bank linkage

model in order to boost financial inclusion. In this model, a group of 10-12 members make one

single SHG, the group members pool savings and indulge in inter-loaning amongst themselves

and they are then linked as a collective to a bank which provides them with loans. The loan

amount in general is limited to four times the cumulative savings of the group. The repayment

in JEEViKA is done on monthly basis, and members take loans based on urgency of needs and by

turn. Once these loans are paid back, the credit rating of the SHGs increase and they in turn get

entitled to a larger loan. The bank and SHG linkages are facilitated by Bank Mitra (Friend of

Bank). She is a member of the community and receives salary based on performance incentives

from the community.

At the level of policy JEEViKA addresses ‘livelihood finance’. It is accepted that micro-finance

can only marginally solve the problem of poverty alleviation and that a complete solution can

only be found if investments are based in the areas of livelihood generation like leveraging

natural resources, capacity building, improving education and skills (Mahajan, 2005).

In our field study in the villages of Bara , Sekhwara, Bhagar and Baradi, the impact that JEEViKA

SHG program had on being able to provide a sound base for the financial progress of its

members has thrown up a list of interesting observations. We also tried to understand the gap

between vision of JEEViKA and the practices on the ground.

Why People Take Loans

The ability to access formal credit in rural areas is dependent on the nature and size of the

assets and the occupation the borrower is involved in(United Nation, 2006). Barman in his

JEEViKA Study Page 43

study argues that informal lending is highest amongst marginal farmers, followed by small and

commercial farmers(Barman & Kalra, 2009). Marginal farmers with extremely small land

holdings could not provide identity and collateral to bank for loans. Marginal farmers along

with their families who were excessively debt ridden became the primary target audience for

BRLP. The program aimed to help them in creating income generating assets and options. Thus,

the program intended to use micro-finance and self help to break the cycle of poverty. The

main reasons for which the poor access loans can be classified under two categories, one is

personal need, the other is social expense. Personal need involves health care emergencies;

money requirement for education, social expense involves money used to celebrate birth of a

child, marriage in the family, and other occasions where a high degree of money is spent

without return. In our understanding the two major common avenues for loan taking were

education in the family with eligible children and health care expenses of family member with

serious or chronic illness, followed by marriages; in this case we study the implications of these.

Average loan taking by the members was highest in areas of Health pegged at 32 percent, then

Education at 25 percent, followed by Asset creation at 21 percent and Marriage. This nature of

loan taking has implications both positive and negative in trying to eradicate poverty. The

positive aspect is that loans taken for education will lead to a creation of sustainable human

capital that will have the potential for creating a better standard of living in the future. In case

of illness or accident requiring health intervention, JEEViKA has introduced the health risk fund.

The fund allows to take money at the rate of one per cent per month. Since public health

facility is not available on time, it is found to be an effective strategy in helping people access

better quality doctors and treatment. Most respondents claim health, education, and marriage

to be their biggest expenses. It is ironical that the debt is caused due to no or lack of public

health facilities not working. Linking effectively with government schemes continues to be an

issue. In those villages where the VOs have not taken over the PDS system, the cost of food and

fuel also becomes a deterrent factor in the expense list of the household. Despite all odds,

members are taking loan for setting up enterprises. Often the choice of the enterprise is an

extension of the existing skill sets and occupation. Like a tailor improves her earning by moving

JEEViKA Study Page 44

away from hand driven stitching machine to motorised machine, while some are into ornament

business. Artificial ornaments are sold in the village and in the local haat (local market).

Figure 6: Distribution of Loan Purposes

A majority of the respondents were financially illiterate when the bank SHG model was

introduced. JEEViKA’s intervention filled the gap by simplification of the process and

partnership with the bank. Over a period of time, the success stories of women in the village

started emerging and with sustained initiative, at the branch and bank level, it led to a

considerable growth in the number of women joining SHGs. JEEViKA then started the practice

of organising a camp where branch representatives are invited and the bank accounts are