Embed Size (px)

Citation preview

������� ���������������������������

JASDAQ

New Listing GuidebookTokyo Stock Exchange

Table of ContentsIntroduction

- 1 -

Table of Contents

Introduction ······································································································· 1

Legend·············································································································· 2

Ⅰ About Listing ································································································· 3

1. Benefits of Listing ·························································································3

(1) Smooth and Diversified Fundraising ··························································3

(2) Enhance Corporate Value ·······································································3

(3) Improve its Internal Management System and Enhance Employees’ Motivation ···3

2. Mechanism for Initial Listing ············································································4

(1) Mechanism for Initial Listing ····································································4

(2) Composition of Market ···········································································5

3. Parties Involved in Listing and Their Roles ·························································7

(1) Securities Companies ············································································7

(2) Certified Public Accountants (Auditing Firms) (CPAs) ····································7

(3) Shareholder Services Agent ····································································8

4. Steps to be Taken Before Listing ······································································9

(1) Before the Listing Application································································· 12

(2) Preliminary Review ············································································· 13

(3) Listing Application ··············································································· 15

(4) Listing Examination ············································································· 18

(5) After TSE’s Listing Approval ·································································· 21

(6) Follow-ups after Listing ········································································ 22

II Formal Requirements (relating to Rule 216-3 and Rule 216-6 of the Regulations)···26

Criteria for JASDAQ Standard ············································································· 29

1. Share Distribution ······················································································· 29

2. Market Capitalization of Tradable Shares ························································· 34

3. Net Asset Value ························································································· 40

4. Profits or Market Capitalization ······································································ 42

5. False Statement or Adverse Opinion and Audit by a Listed Company Audit Firm ········ 45

6. Establishment of a Shareholder Services Agent ················································· 49

7. Share Unit and Classes of Stock ···································································· 50

8. Restrictions on Transfer of Shares ·································································· 53

9. Handling by the Designated Book-Entry Transfer Institution ·································· 54

Criteria for JASDAQ Growth················································································ 55

III Listing Examination (relating to Rule 216-5 and Rule 216-8 of the Regulations) ·····56

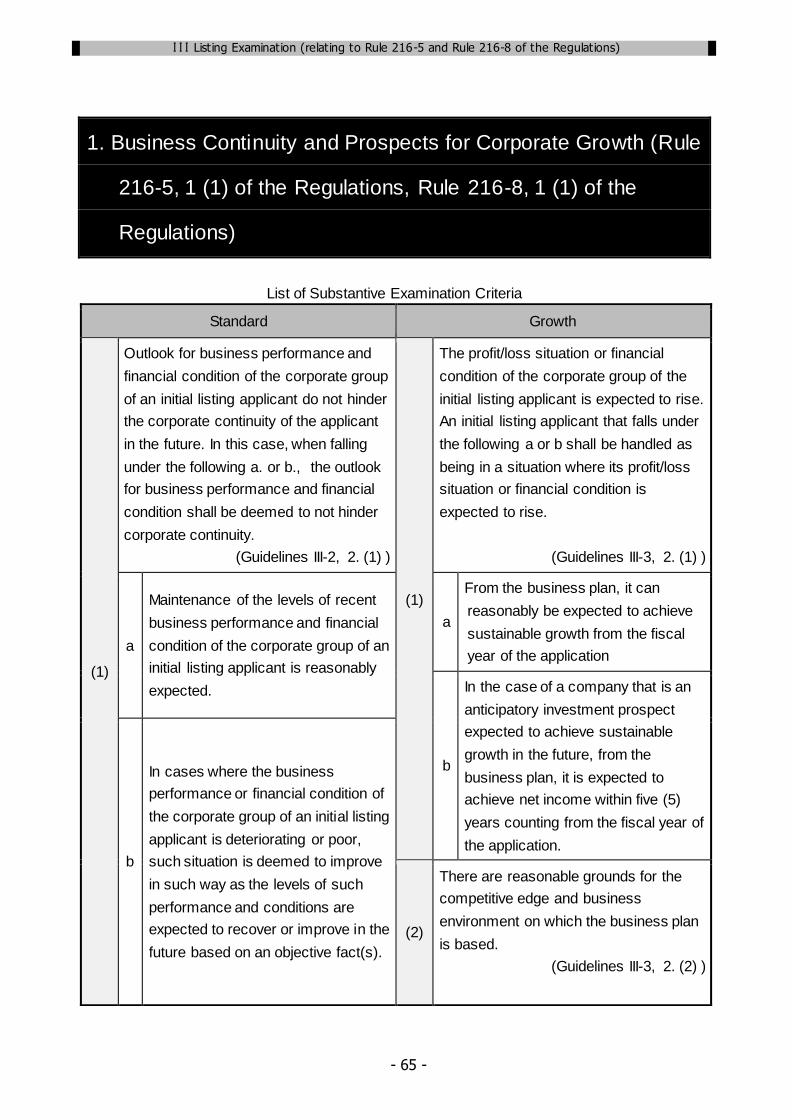

1. Business Continuity and Prospects for Corporate Growth (Rule 216-5, 1 (1) of the

Regulations, Rule 216-8, 1 (1) of the Regulations) ·············································· 65

2. Establishment of Sound Corporate Governance and Internal Management System

Corresponding to Stage of Growth (Rule 216-5, 1 (2), Rule 216-8, 1 (2) of the

Regulations) ······························································································ 79

Table of ContentsIntroduction

- 2 -

3. Reliability of Corporate Actions (Rule 216-5, 1 (3) of the Regulations, Rule 216-8,1 (3)

of the Regulations) ······················································································ 93

4. Appropriateness of Disclosure of Corporate Details, etc. (Rule 216-5, 1 (4) of the

Regulations, Rule 216-8, 1 (4) of the Regulations) ············································ 120

5. Other Matters Deemed Necessary by the Exchange from the Viewpoint of the Public

Interest or Investor Protection (Rule 216-5, 1 (5) of the Regulations, Rule 216-8, 1 (5) of

the Regulations) ······················································································· 140

IV Checklists Before Applying for Listing on JASDAQ··········································· 170

JASDAQ Standard ·························································································· 170

1. Has the Business Plan been Reasonably Developed in Consideration of Future

Business Developments? ··········································································· 170

2. Have Business Management Organizations Effectively Functioned?····················· 172

(1) Board of Directors ············································································· 172

(2) Company Auditors ············································································ 173

(3) Independent Directors / Auditors ·························································· 173

(4) Accounting Advisors ·········································································· 174

(5) Internal Audits ·················································································· 174

(6) Internal Managements and Regulations ················································· 175

(7) Operating Results Management ··························································· 176

(8) Other Considerations for the Management·············································· 176

3. Have you Prepared Yourself for Timely and Appropriate Disclosures of Corporate

Information? ···························································································· 177

(1) Internal Systems··············································································· 177

(2) Disclosure Documents ······································································· 178

(3) Disclosure of Operating Results ··························································· 179

(4) Accounting Processing······································································· 179

(5) Change of Business Year (Accounting Period and Balance Sheet Date) ········ 180

(6) Management of Company Information ··················································· 180

4. Has not the Soundness of Corporate Management been Impaired due to Transactions

with Company Related Parties, etc.? ····························································· 181

5. Have You Properly Addressed Other Considerations in Filing a Listing Application? · 183

(1) Parent Company, etc. ········································································ 183

(2) Other ····························································································· 184

6. Have You Completed Necessary Preparations for Interviews with JPXR or Answers to

Questions Made by JPXR in Writing? ···························································· 185

(1) Reasons Why the Applicant Decided to List its Stock································· 185

(2) Business Lines················································································· 185

(3) Status and Conditions of the Industry where the Applicant Operates ············· 185

(4) Growth Plan Going Forward ································································ 186

(5) Details of the Business Lines ······························································· 186

(6) Business Plan ·················································································· 186

(7) Use of Proceeds from Public Offering at Listing ······································· 187

Table of ContentsIntroduction

- 3 -

(8) Announcement of Future Forecast Information such as Prospectus for Operating

results for the Period in which the Listing Applicant is Filed ························ 187

(9) Design and Implementation of Management Control System and Internal Audit

System ·························································································· 187

(10) Design and Implementation of Timely Disclosure System, etc.····················· 188

(11) Relationship with Parent Company, etc., and Status of Corporate Group········ 188

(12) Transactions, etc. with Related Parties, etc. ············································ 189

(13) Legal Actions, Disputes and Violation of Laws and Regulations ··················· 189

(14) Other ····························································································· 190

JASDAQ Growth ···························································································· 191

1. Has the Business Plan been Reasonably Developed in Consideration of Future

Business Developments? ··········································································· 191

2. Have Management Control Organizations Effectively Functioned? ······················· 192

(1) Board of Directors ············································································· 192

(2) Company Auditors ············································································ 193

(3) Independent Directors/Auditors ···························································· 193

(4) Accounting Advisors ·········································································· 194

(5) Internal Audits ·················································································· 194

(6) Internal Managements and Regulations ················································· 195

(7) Operating Results Management ··························································· 196

(8) Other Considerations for the Management·············································· 196

3. Have you Prepared Yourself for Timely and Appropriate Disclosures of Corporate

Information? ···························································································· 197

(1) Internal Systems··············································································· 197

(2) Disclosure Documents ······································································· 200

(3) Disclosure of Operating Results ··························································· 201

(4) Accounting Processing······································································· 201

(5) Change of Business Year (Accounting Period and Balance Sheet Date) ········ 202

(6) Management of Company Information ··················································· 202

4. Has not the Soundness of Corporate Management been Impaired due to Transactions

with Company Related Parties, etc.? ····························································· 203

5. Have You Properly Addressed Other Considerations in Filing a Listing Application? · 202

(1) Parent Company, etc. ········································································ 202

(2) Other ····························································································· 203

6. Have You Completed Necessary Preparations for Interviews with JPXR or Answers to

Questions Made by JPXR in Writing? ···························································· 204

(1) Reasons why the Applicant Decided to List its Stock ································· 204

(2) Business Lines················································································· 205

(3) Status and Conditions of the Industry where the Applicant Operates ············· 205

(4) Business Plan which Demonstrates Growth Potential ································ 206

(5) Details of the Business Lines ······························································· 206

(6) Business Plan ·················································································· 206

Table of ContentsIntroduction

- 4 -

(7) Use of Proceeds from Public Offering at Listing ······································· 207

(8) Announcement of Future Forecast Information such as Prospectus for Operating

Results for the Period in which the Listing Applicant is Filed ······················· 207

(9) Design and Implementation of Management Control System and Internal Audit

System ·························································································· 207

(10) Design and Implementation of Timely Disclosure System, etc.····················· 208

(11) Relationship with Parent Company, etc., and Status of Corporate Group········ 208

(12) Transactions, etc. with Related Parties, etc. ············································ 209

(13) Legal Actions, Disputes and Violation of Laws and Regulations ··················· 209

(14) Other ····························································································· 209

V Listing Examination Q&A ··············································································· 210

1. Relating to “Corporate Continuity of Domestic Companies” Listed on JASDAQ Standard

············································································································ 210

(1) Items for which Profit Level is Assessed ················································· 210

(2) Confirmation of Progress of Performance during the Period Pertaining to the

Listing Application ·············································································211

(3) Application of “Accounting Standards for Accounting Changes and Correction of

Errors”····························································································211

2. Relating to Checklists Before Applying for Listing on JASDAQ ···························· 213

(1) Business Plan (Checklists No.1)··························································· 213

(2) Board of Directors (Checklists No. 2(1) ) ················································ 214

(3) Company Auditors (Checklists No. 2(2) ) ················································ 217

(4) Independent Directors/Auditors (Checklists No. 2 (3) ) ······························· 218

(5) Accounting Advisors (Checklists No. 2 (4) ) ············································· 219

(6) Internal Audits (Checklists No. 2 (5) )····················································· 219

(7) Internal Managements and Regulations (Checklists No. 2 (6) ) ···················· 220

(8) Operating Results Management (Checklists No. 2 (7) ) ······························ 221

(9) Other Considerations for the Management (Checklists No. 2 (8) ) ················ 222

(10) Internal Systems (Checklists No. 3 (1) ) ················································· 224

(11) Disclosure of Operating Results (Checklists No. 3 (2) ) ······························ 225

(12) Disclosure of Operating Results (Checklists No. 3 (3) ) ······························ 225

(13) Change of Business Year (Accounting Period and Balance Sheet Date)

(Checklists No. 3 (5) )12) ································································· 229

(14) Transactions with Company Related Parties, etc. (Checklists No. 4) ············· 231

(15) Parent Company, etc. (Checklists No. 5 (1)) ············································ 237

(16) Change in shareholders before the listing ··············································· 237

(17) Examination of Business Plan (Checklists No. 6 (6) ) ································ 239

(18) Other ····························································································· 241

VI Receipt or Transfer of Stocks, etc. Before Listing and Allotment, etc. of Offered

Stocks Through Third Party Allotment ····························································· 243

1. Receipt or Transfer of Shares, etc. before Listing ············································· 244

(1) Descriptions Concerning the Status of Changes in Shares before Listing ······· 244

Table of ContentsIntroduction

- 5 -

(2) Retention, etc. of the Record of Changes in Ownership of Stocks, etc. Before

Listing ··························································································· 245

2. Allotment of Offered Stocks by Third Party Allotment, etc. Before Listing ················ 246

(1) Regulations on Allotment of Offered Stocks by Third-Party Allotment, etc. ······ 246

(2) Regulations on Allotment and Holding of Offered Subscription Warrants by Third

Party Allotment, etc.·········································································· 255

(3) Regulations on Allotment and Holding of Subscription Warrants as Stock Option

···································································································· 258

(4) Descriptions of the Status of Offered Allotment of Shares, etc. by Third Party

Allotment ······················································································· 264

VII Public Offering or Secondary Offering before Listing ······································· 266

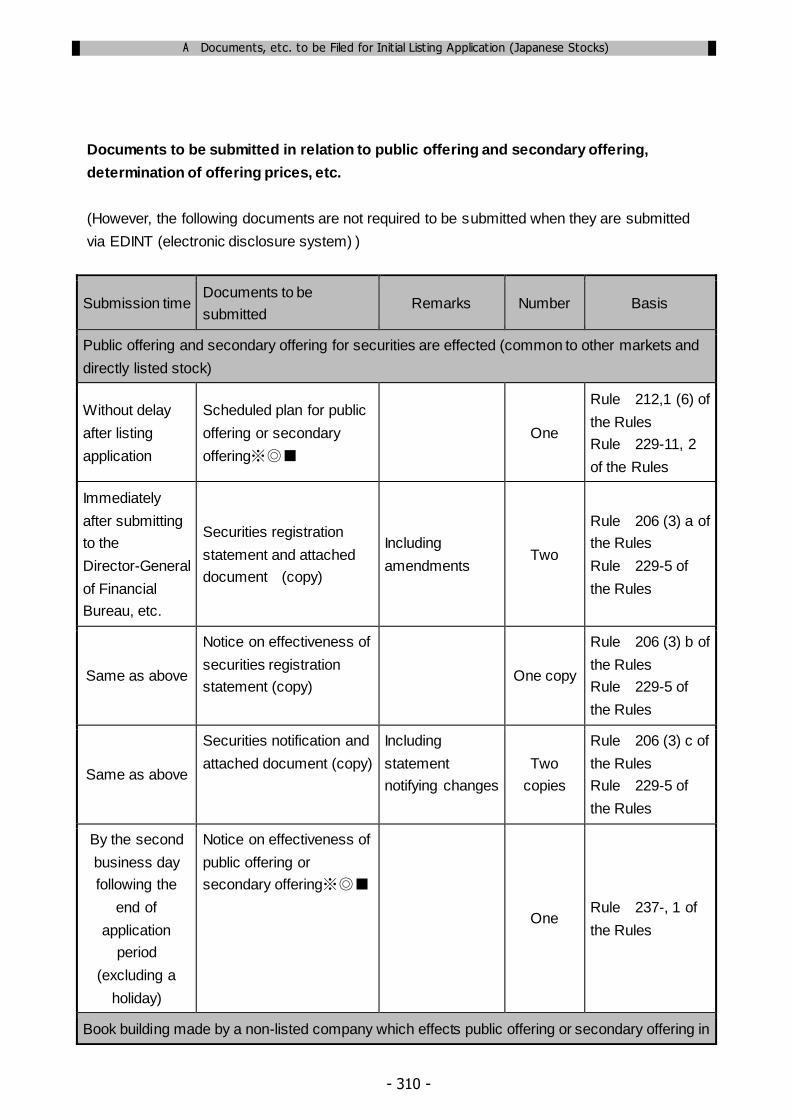

(1) Submission of Scheduled Plan for Public Offering or Secondary Offering ······· 266

(2) Procedures for Public Offering, etc. Before Listing ···································· 266

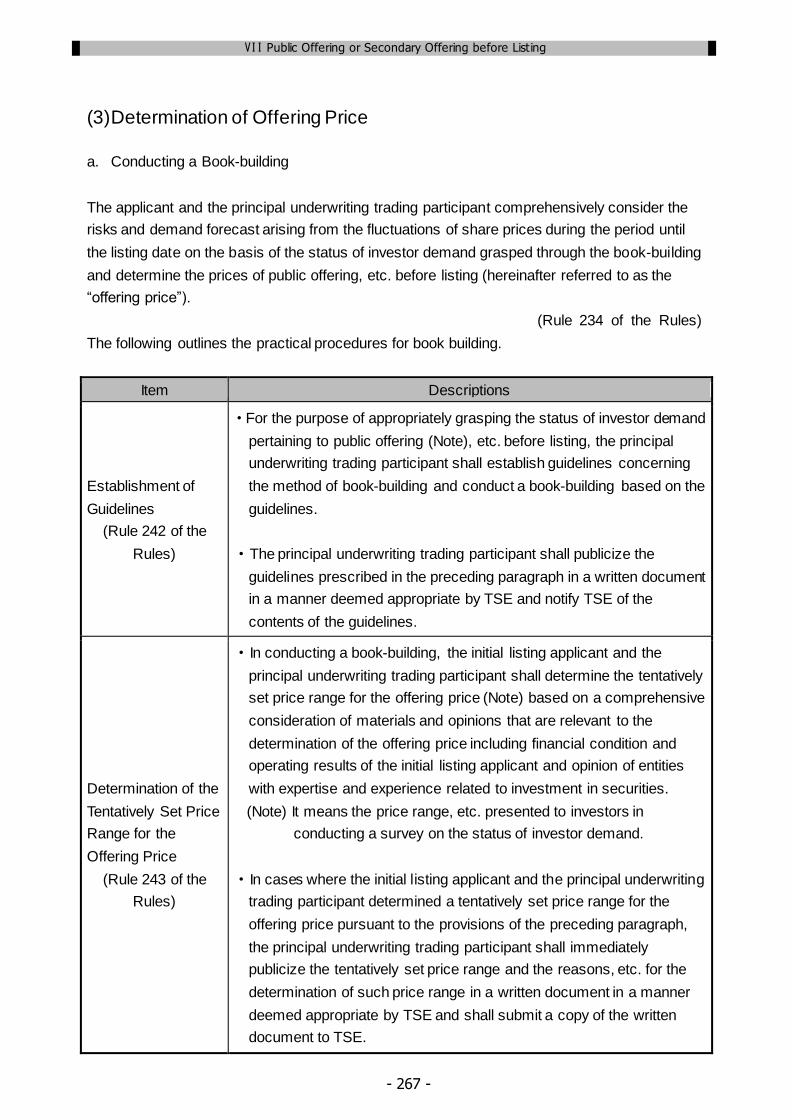

(3) Determination of Offering Price ···························································· 267

(4) Allocation Pertaining to Public Offering, etc. Before Listing ························· 269

(5) Submission of Notice of Execution of Public Offering or Secondary Offering, etc.

···································································································· 270

(6) Other ····························································································· 271

VIII Handling of Corporate Reorganization Event················································· 273

a. Handling of corporate reorganization for the purpose of examination ······················· 274

1. Merger ··································································································· 274

2. Becoming a Holding Company····································································· 276

3. Stock Swap ····························································································· 278

4. Company Split-up, Receipt of Business ························································· 280

b. Documents required to be submitted when a significant effect is given ····················· 283

IX Listing Fees ································································································ 286

1. Listing Examination Fees ··········································································· 286

2. Initial Listing Fees····················································································· 287

3. Fees to be Paid by Listed Companies ··························································· 288

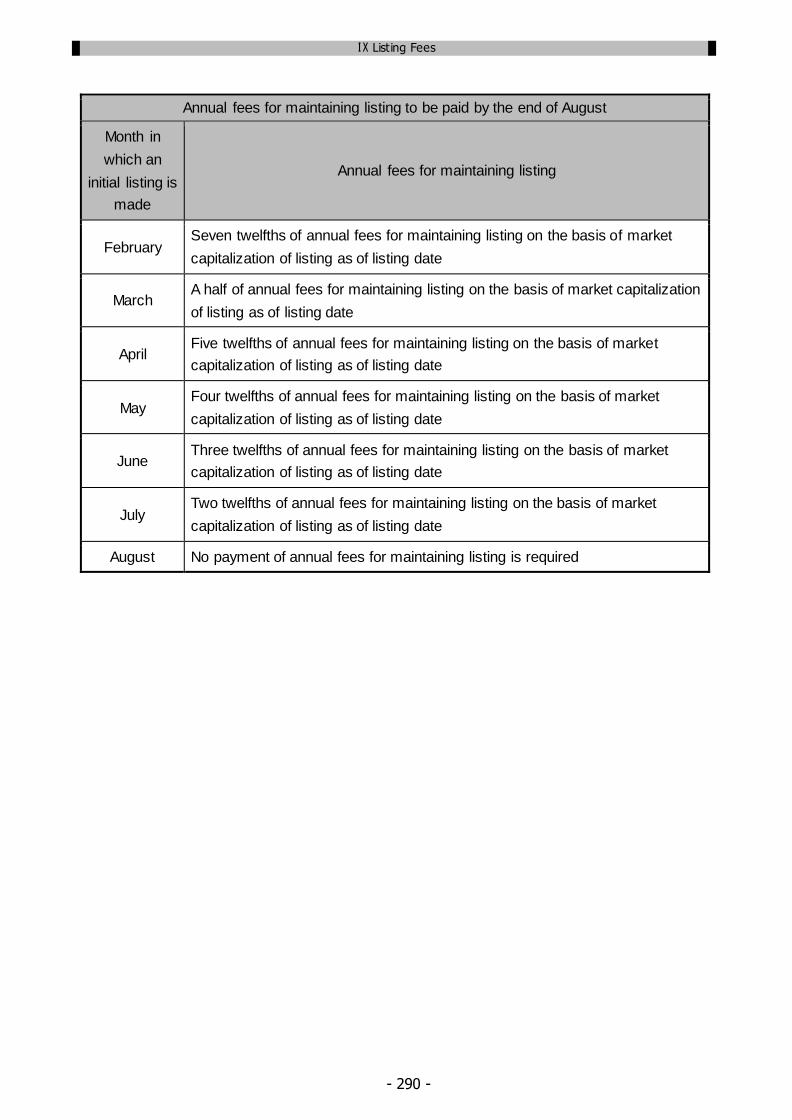

(1) Annual Fees for Maintaining Listing······················································· 288

(2) Fees for Listing of Shares of New Stock ················································· 291

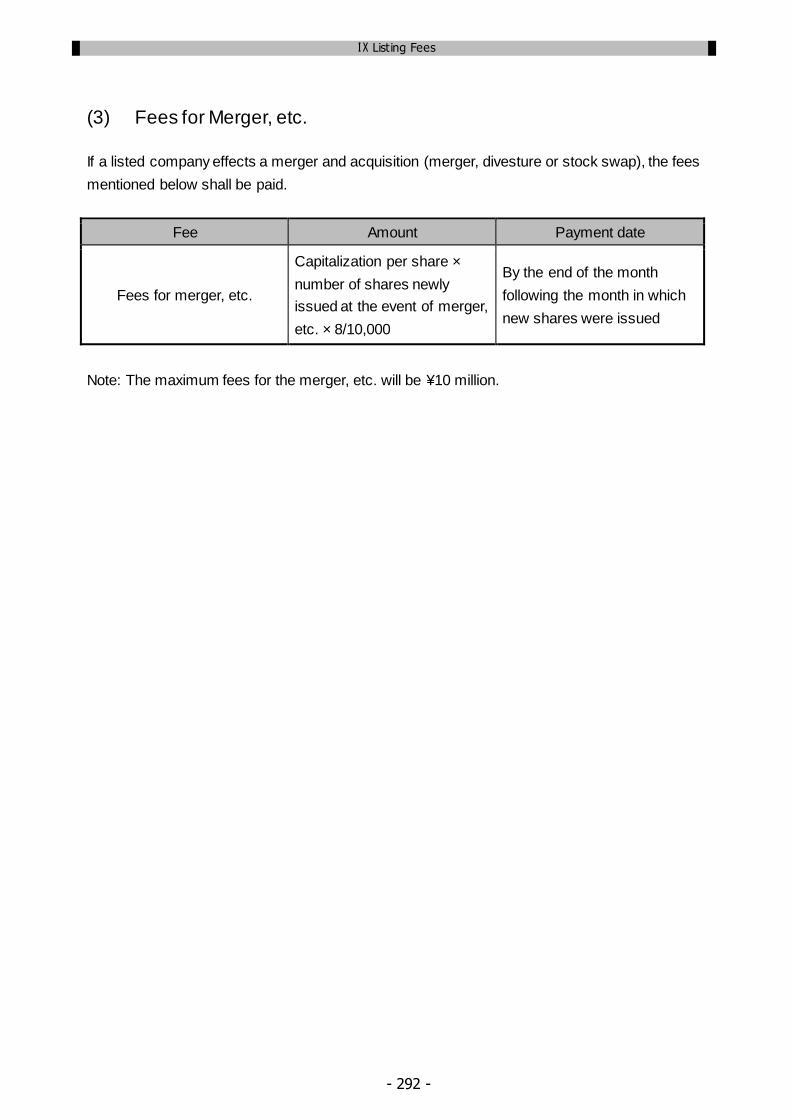

(3) Fees for Merger, etc. ········································································· 292

X IPO Center (Support Given to Prospective Issuers) ·········································· 293

1. Assistance Activities through Visits to Individual Companies and Consultation········· 293

2. Seminars for Prospective Issuers ································································· 293

3. Mail Magazine ························································································· 293

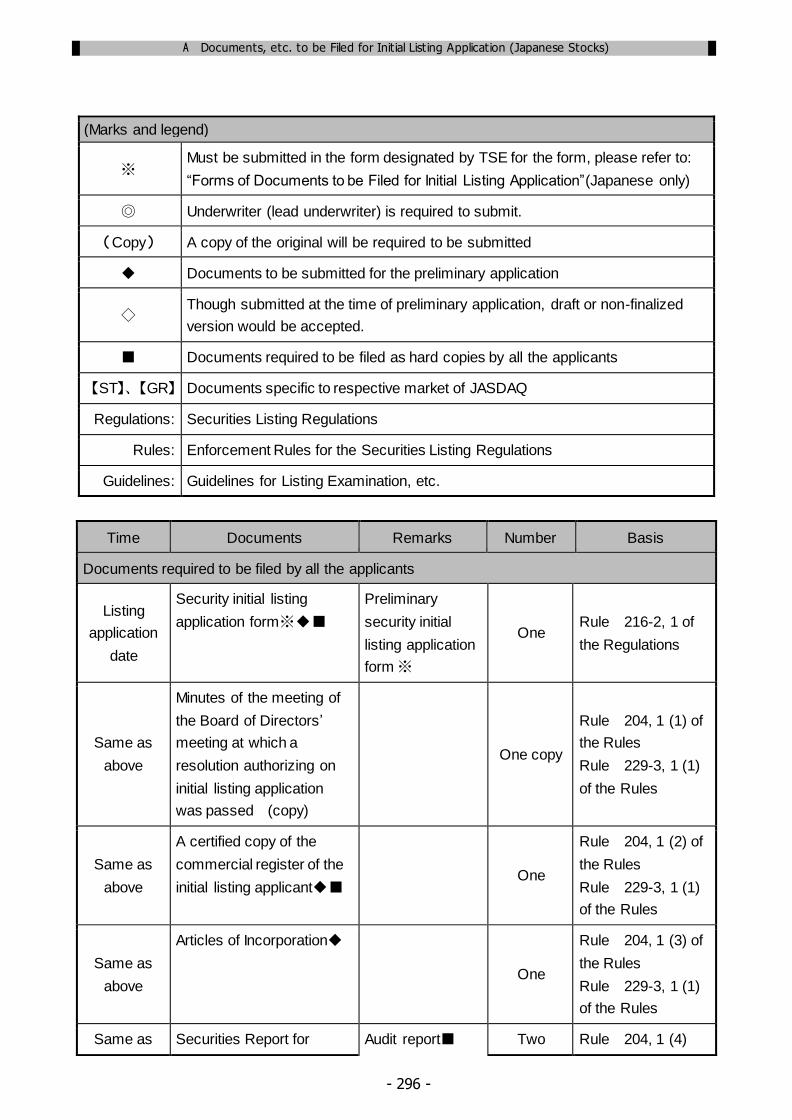

A Documents, etc. to be Filed for Initial Listing Application (Japanese Stocks) ······ 294

1. List of Documents, etc. to be Filed for Initial Listing Application (Japanese Stocks)··· 294

(1) Documents, etc. to be Filed for Initial Listing Application (Japanese Stocks)···· 294

(2) Securities Report for Initial Listing························································· 319

(3) JASDAQ Listing Application Report ······················································· 321

2. Guide to Completing the “JASDAQ Listing Application Report” ···························· 322

Introduction

- 1 -

Introduction

JASDAQ, which took over the over-the-counter registration system launched by the Japan

Securities Dealers Association (JSDA) in 1963, was turned into a market operated by Osaka

Securities Exchange (OSE) under the brand of OSE JASDAQ, when the Nippon New Market

“Herclues” operated by OSE and “JASDAQ” and “NEO” operated by JASDAQ were

consolidated in October 2010. On July 16, 2013, then, Tokyo Stock Exchange and Osaka

Securities Exchange conducted a business combination and Tokyo Stock Exchange took over

the operation of JASDAQ from OSE and the market was newly emerged as “TSE JASDAQ.”

A company can benefit from listing its stock on TSE JASDAQ as it can gain access to smooth

and diversified fundraising, enhanced credit quality and profile of companies, etc. On the other

hand, listing of stock means that the company will be a choice of investments by a large number

of investors, including individual investors.

Thus Tokyo Stock Exchange, Inc. requires a company which applies for listing to meet certain

eligibility criteria for listing of its stock from the perspective of investors’ protection, and will

implement the examination of listing application in accordance with standards for listing

examination.

Any company which considers listing its stock on TSE JASDAQ is required to fully understand

the standards for listing examination and to prepare itself for meeting criteria for listing by

improving internal management and control system before filing the listing application.

This booklet is issued in order to help any company considering the listing of its stock on TSE

JASDAQ and other parties involved in the listing to fully understand the standards for listing

examination as it illustrates key points of standards for listing examination and procedures

related to the listing examination in a way that is very understandable. We strongly hope that

this booklet will be useful when you consider the listing of your shares on TSE JASDAQ. If any

regulations and rules are revised after this booklet is issued, we will update the “Guidelines for

Listing on TSE JASDAQ” with comparison table between previous and revised regulations on

our website (http://www.jpx.co.jp/equities/listing-on-tse/new/guide/02.html).

October 2019

Tokyo Stock Exchange, Inc.

Legend

- 2 -

Legend

TSE: Tokyo Stock Exchange

JPXR: Japan Exchange Regulation

Regulations: Securities Listing Regulations

Rules: Enforcement Rules for Securities Listing Regulations

Guidelines: Guidelines for Listing Examination, etc.

Copyright 2019, Tokyo Stock Exchange, Inc. ALL RIGHTS RESERVED. The contents of this

booklet are protected under the Copyright Act. No reproduction, copy, transmission,

modification or sales of all or a part of the contents shall be permitted without prior written

permission. Doing so is regarded as the breach of the copyright retained by TSE. In addition,

the contents may be modified or abolished without any prior notice.

Ⅰ About Listing

- 3 -

Ⅰ About Listing

1. Benefits of Listing

By listing on Tokyo Stock Exchange (TSE), your company can:

(1) Smooth and Diversified Fundraising

Once listed on JASDAQ, your company will have a direct access to financing and capital

increase by issuing shares of stock at a market price through publicly offered stock or issuing

subscription warrants, corporate bonds with subscription warrants, etc. Our highly liquid market

can offer more efficient and diverse fund-raising capacity for your company to develop and grow

further.

(2) Enhance Corporate Value

A company can enhance its social recognition and establish its status as a company with future

growth potential by becoming a listed company. Coverage by media, including market news of

newspapers, will allow your company to enhance its corporate reputation in Japan. The

company will also be able to retain and attract excellent human resources as well.

(3) Improve its Internal Management System and Enhance Employees’ Motivation

Corporate disclosure will allow investors and other third parties to examine your company’s

corporate management. Therefore, your company has obligations to continue to improve and

strengthen its management system as well as its internal control. Becoming a public company

will also help boost the morale of the officers and employees of the company.

Please keep in mind that since securities issued by a listed company will be a choice of

investment by a large number of public investors, going public also involves taking on new

social responsibilities and duties for the purpose of protection of investors. It will be required,

among other things, to disclose earnings information and corporate information in an

appropriate and timely manner.

Ⅰ About Listing

- 4 -

2. Mechanism for Initial Listing

(1) Mechanism for Initial Listing

Listing of stock is effected on the basis of application filed by a company issuing the stock

(hereinafter referred to as an “applicant”). When the stock is listed, it will be an investment

choice for a large number of general investors. Thus, TSE (Note) will examine whether an

applicant is eligible for listing on TSE from the perspective of investor protection. TSE has

developed and set forth various regulations and rules for initial listing. The listing examination

will be conducted by assessing whether the requirements in the regulations and rules are

satisfied. (“Securities Listing Regulations” and “Enforcement Rules for Securities Listing

Regulations,” etc.) by which the examination will be conducted. When the examination results

reveal that the applicant is eligible for listing, TSE will approve and announce the listing of

applicant, following which the stock will eventually be listed on TSE.

Various rules concerning initial listing comprise “Securities Listing Regulations,” “Enforcement

Rules for Securities Listing Regulations” and “Guidelines for Listing Examinations, etc.”

The standards for listing examination specified by various rules provide for “Formal

Requirements” which specify quantitative requirements for the number of shareholders, amount

of profit, etc. and standards for “Substantive Examination Standards” which represent the

qualitative criteria for assessing disclosure systems, corporate governance practices and so on.

Please refer to “II Formal Requirements” and “III Listing Examination,” respectively, in this

booklet.

As a result of listing examination, when an applicant is determined to meet the eligibility for

listing, TSE will approve and announce the listing of the applicant. Subsequently the applicant

will be listed through the process of public offering or secondary offering.

Note: Actual examination will be conducted by JPXR to which the role of examination is

delegated by TSE.

Ⅰ About Listing

- 5 -

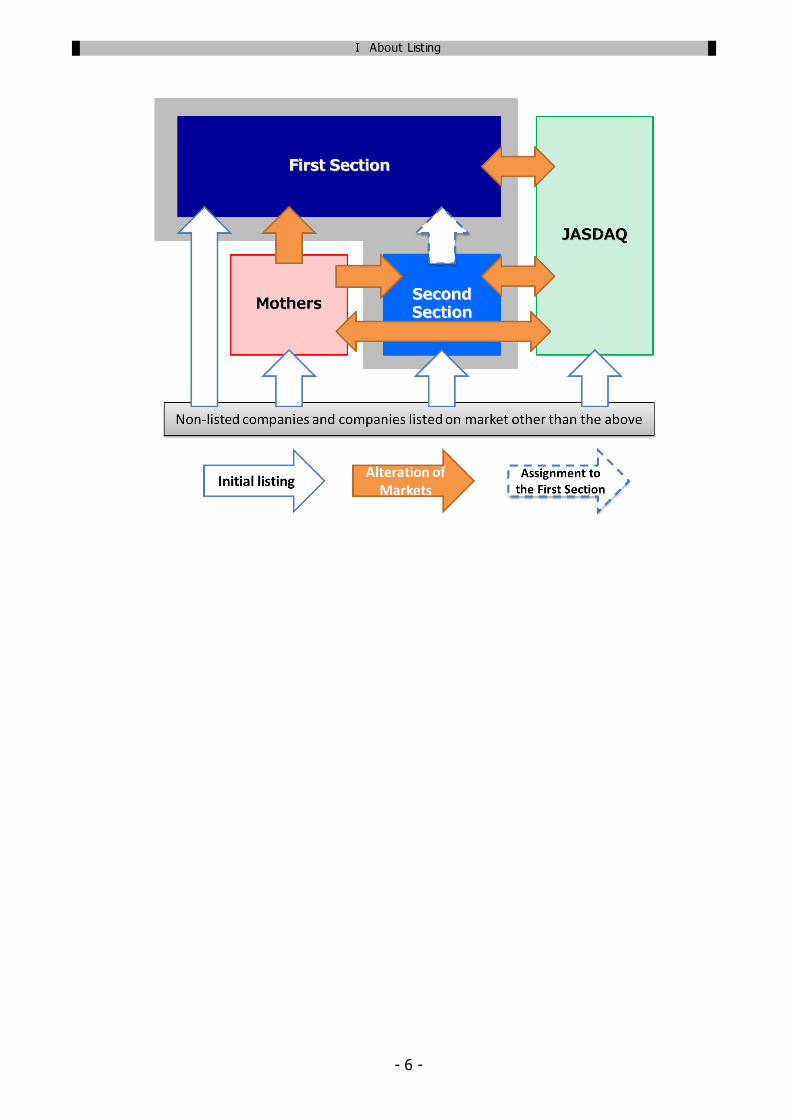

(2) Composition of Market

TSE operates five markets of the First Section, Second Section, Mothers, JASDAQ and

TOKYO PRO Market.

1) First Section and Second Section

The First and Second Sections represent the main boards of TSE where leading large and

second tier Japanese and foreign companies are listed. Especially the First Section is viewed

as one of the top rank markets in terms of the size and liquidity, as foreign investors account for

a large portion of equity trading. The First and Second Sections are collectively referred to as

the “Main Markets.”

2) Mothers

Mothers offers a trading market for companies with growth potential which aim to be reassigned

to the First Section in near future. Thus TSE requires applicants to demonstrate high growth

potential. Whether an applicant has growth potential or not shall be assessed and determined

by lead underwriters on the basis of its business model or business environment. As the

objective of Mothers is to offer financing opportunities for many companies with growth potential,

Mothers has no restrictions on the size or business category of applicants. After successfully

listing their stock on Mothers, many have satisfied the criteria for reassignment to the First

Section and listed their stock on the First Section.

3) JASDAQ

JASDAQ is a market characterized by the three concepts of (1) reliability, (2) innovativeness

and (3) region and internationalization. JASDAQ is split into the “Standard” market for growth

companies with a certain size and business performance and the “Growth” market for

companies with stronger future growth potential and unique technologies or business models.

* Please refer to the “Guidebook for Initial Listing on First and Section Second” for listing on the

First and Second Sections and the “Guidebook for Initial Listing on Mothers” for initial listing

on Mothers.

Furthermore, any company which successfully lists its stock can change its listed market

according to the stage of business development and growth after initial listing as follows.

Ⅰ About Listing

- 6 -

Ⅰ About Listing

- 7 -

3. Parties Involved in Listing and Their Roles

(1) Securities Companies

There are a number of tasks that need to be completed by a securities company before listing.

At the stage of preparation for listing, the securities company will provide advice to the applicant

on capital policy and internal systems and also carry out the examination of the corporate

information of the applicant to determine whether the securities company can perform the

required listing procedures and underwrite the public offering or secondary offering

(underwriting examination). When the securities company decides to underwrite the public

offering or secondary offering, it has to implement a series of tasks according to the listing

schedule. Even after the applicant successfully lists their shares on the market, it will assist the

applicant in various aspects, including raising secondary funds and investor relations or IR

activities.

The securities companies that assist the applicant in carrying out various tasks for listing

procedures are called “underwriters” (If the securities company is a TSE member, it is also

called a “trading participant”). The main underwriter among them is called the “lead underwriter

(lead trading participant)”. A securities company which enters into a prime contract for

underwriting for public offering, etc. with the applicant is called the “prime underwriter (prime

trading participant).”

(2) Certified Public Accountants (Auditing Firms) (CPAs)

Certified public accountants (auditing firms) express their audit opinion on the applicant’s

financial statements to be submitted to TSE, in compliance with the Securities Listing

Regulations. They will also advise the applicant on its accounting practices and internal control.

For the purpose of Securities Listing Regulations, the applicant is required to submit an audit

report on financial statements attached to “Securities Report for Initial Listing Application (Part I)

“hereinafter referred to as “Part I” documents) as prescribed in the Financial Instruments and

Exchange Act.

Ⅰ About Listing

- 8 -

(3) Shareholder Services Agent

A shareholder services agent is an entity which is required to be appointed in order to

implement smooth services related to shareholders. Their services include preparation of a

shareholders registry, and handling various rights granted to shareholders including voting

rights and dividend payments to shareholders. The applicant is required to outsource services

related to shareholders to a shareholder services agent or to receive preliminary consent to the

acceptance of services provided to shareholders from a shareholder services agent by the date

when the listing application is filed (please refer to section 6 “Establishment of a Shareholder

Services Agent” at II Formal Requirements.

Ⅰ About Listing

- 9 -

4. Steps to be Taken Before Listing

In general, the following steps will be taken before the successful listing of stock on JASDAQ.

The following outlines the steps to be taken at each stage from the application to approval of

listing.

[Model schedule from listing application entry to listing approval]

<First part>

Ⅰ About Listing

- 10 -

1 Sun 1 Wed

2 Mon 2 Thu

3 Tue 3 Fri

4 Wed 4 Sat

5 Thu 5 Sun

6 Fri 6 Mon

7 Sat 7 Tue

8 Sun 8 Wed

9 Mon 9 Thu

10 Tue 10 Fri

11 Wed 11 Sat

12 Thu 12 Sun

13 Fri 13 Mon

14 Sat 14 Tue

15 Sun 15 Wed

16 Mon 16 Thu

17 Tue 17 Fri

18 Wed 18 Sat

19 Thu 19 Sun

20 Fri 20 Mon

21 Sat 21 Tue

22 Sun 22 Wed

23 Mon 23 Thu

24 Tue 24 Fri

25 Wed 25 Sat

26 Thu 26 Sun

27 Fri 27 Mon

28 Sat 28 Tue

29 Sun 29 Wed

30 Mon 30 Thu

31 Tue 31 Fri Third presentation of questions

Receipt of answers to the second questions

Interview

Physical inspection

Preliminary review related to listing

application

Second presentation of questions

Listing application entry

Holiday

Receipt of answers to the first questions

Interview

First presentation of questions

Month X One month after month X

Listing application, Receipt of “Part I”

documents and JQ Report

Interview, Schedule coordination

At

eig

ht

bu

sin

ess d

ay

s in

terv

al

At

fou

r b

usin

ess d

ay

s in

terv

al

Ap

pro

xim

ate

ly

two

we

eks

On

e w

ee

k

Ⅰ About Listing

- 11 -

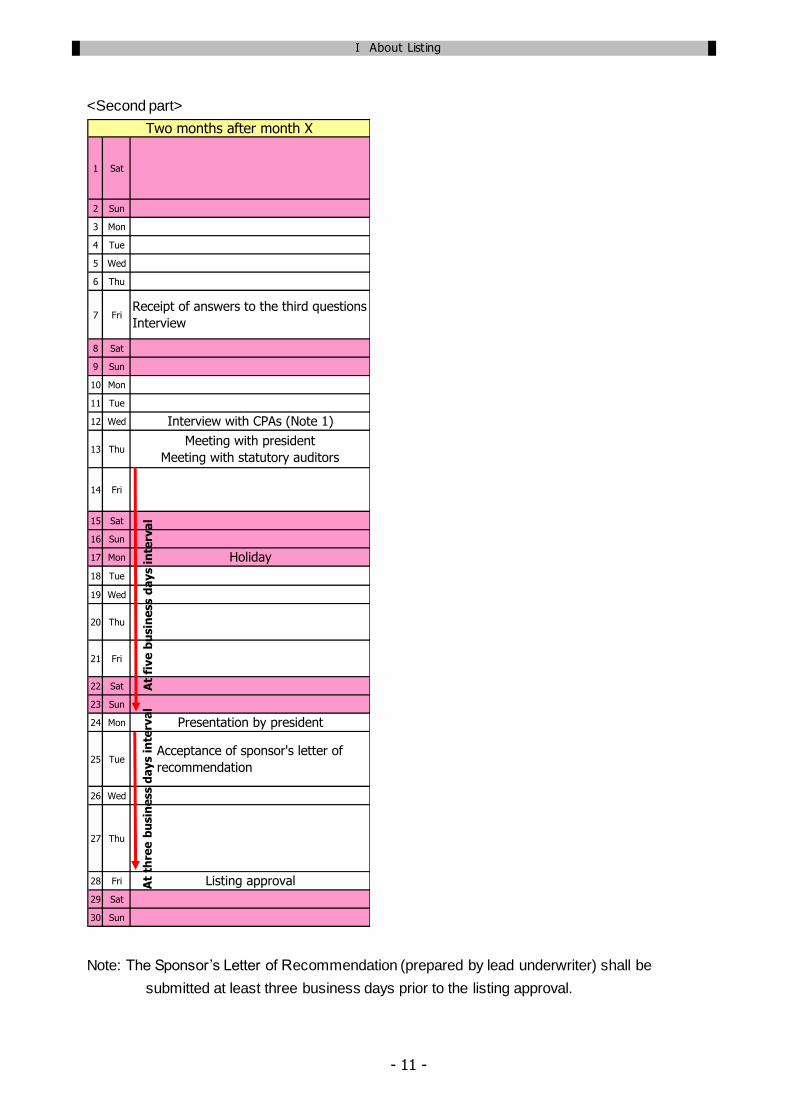

<Second part>

1 Sat

2 Sun

3 Mon

4 Tue

5 Wed

6 Thu

7 Fri

8 Sat

9 Sun

10 Mon

11 Tue

12 Wed

13 Thu

14 Fri

15 Sat

16 Sun

17 Mon

18 Tue

19 Wed

20 Thu

21 Fri

22 Sat

23 Sun

24 Mon

25 Tue

26 Wed

27 Thu

28 Fri

29 Sat

30 Sun

Listing approval

Presentation by president

Acceptance of sponsor's letter of

recommendation

Holiday

Interview with CPAs (Note 1)

Meeting with president

Meeting with statutory auditors

Receipt of answers to the third questions

Interview

Two months after month X

At

five

bu

sin

ess d

ays i

nte

rva

lA

t th

ree

bu

sin

ess d

ays i

nte

rva

l

Note: The Sponsor’s Letter of Recommendation (prepared by lead underwriter) shall be

submitted at least three business days prior to the listing approval.

Ⅰ About Listing

- 12 -

(1) Before the Listing Application

Having its stock listed on a stock market means that a company will be a choice of investment

by a large number of investors.

It is therefore important for an applicant to prepare itself for the prospective IPO by

strengthening its revenue base and improving its management system, etc. The applicant is

primarily responsible for this preparation process and implements the process with necessary

assistance and advice offered by the applicant’s lead underwriter and audit firms.

Should you have any questions regarding examination standards, eligibility, etc., please contact

New Listings of TSE or the Listing Examination Division of JPXR either directly or via your lead

underwriter before the listing application (Note 1).

When all the required preparation work is complete, the lead underwriter makes an entry for the

listing application at least two weeks prior to the listing application (for the purpose of the entry,

the lead underwriter sends e-mail to TSE with the “Listing Application Entry Sheet” attached

including the descriptions of the trade name of the applicant; contact of the lead underwriter;

expected listing schedule (listing application date, listing approval date, listing date) and other

necessary matters (Note 2).

Note 1: TSE will express its view on your questions in consideration of facts and circumstances

disclosed to TSE at the time of consultation. Therefore, if any fact not disclosed at the

time of consultation emerges or changes in conditions of the applicant or environment

surrounding the applicant including any revision to the criteria for listing, takes place

subsequent to the consultation, some views derived from the listing examination would

likely be different from the views expressed by TSE at the time of consultation.

Note 2: If TSE (i.e., New Listings of TSE or the Listing Examination Division of JPXR) is

concerned that some significant issues may take place in terms of substantive listing

examination criteria before the listing application, TSE believes that the applicant must

stand ready to clearly address these issues before the listing application.

Ⅰ About Listing

- 13 -

(2) Preliminary Review

When JPXR is satisfied with the explanations of the lead underwriter of matters related to (1)

appropriate instructions and advice on going public (2) no ties or relationship with any

anti-social forces, and (3) listing schedule, JPXR will accept the application for listing on

JASDAQ. The preliminary review takes place between the person in charge of the listing

application at the lead underwriter and the officials in charge of the examination at JPXR at

least one week prior to the acceptance of listing application.

1) JASDAQ (“Standard” and “Growth”)

JPXR will confirm which market an applicant intends to list its stock on, Standard or Growth.

In practice JASDAQ Standard is suitable for companies with a certain size and business

performance, which are expected to further expand its business, while JASDAQ Growth is for

companies with stronger future growth potential and unique technologies or business models.

2) Report related to the contents of instructions on going public and underwriting examination

The lead underwriter reviews any matters considered during the process of instructions on

going public or underwriting examination carried out by the lead underwriter by the time of

listing application on the basis of the descriptions (draft permitted) included in the “Report

Related to the Contents of Instructions on Going Public and Underwriting Examination."

Practically the lead underwriter is requested to discuss the matters of special consideration in

light of factors specific to the applicant such as lines and category of business and the growth

stage of the company and any other matters on which the lead underwriter focused its

considerations (e.g., design and implementation of significant internal management system,

adoption of special accounting treatment, existence of material breach of laws and regulations)

on the basis of the descriptions included in this report.

JPXR may request the lead underwriter explain the reasons why it commenced its instructions

on going public and the timing thereof (the background why the lead underwriter began

contacting the applicant and its timing).

3) Ties with anti-social forces

In evaluating any ties with any anti-social forces, JPXR will review the following points on the

basis of the “Sponsor’s Letter of Confirmation,” as attached (draft permissible) including the

descriptions of items to be investigated and the method of investigations, and the “Draft of

Declaration of No Association with Anti-Social Forces” to the effect that the applicant has no ties

with any anti-social forces (attached separately).

Ⅰ About Listing

- 14 -

a. Scope of related persons for whom the lead underwriter checked their personal records

and backgrounds and attributes (board members, executive officers, corporate auditors,

shareholders and trading partners); the contents if the lead underwriter considered the

background for founding the initial listing applicant and its customers, suppliers and

other trading partners, and industry and trading conventions specific to the applicant;

and

b. Contents and nature of investigations to ensure that the applicant has no ties with any

anti-social forces (including the contents of investigations of assessments of any

customers, suppliers and other trading partners with initial listing applicant, if any)

4) Review of listing schedule

While the lead underwriter presents the listing and finance schedule of the applicant, JPXR will

propose the examination schedule from the listing application to listing approval.

The lead underwriter is encouraged to appropriately develop and coordinate a schedule which

will not lead to any irrational schedule in consideration of the routine and ordinary business of

the applicant.

Note 1: The two month period is usually defined as the standardized period subject to the

examination. However, in consideration of size of the applicant group, seasonality of

its business or routine businesses, a response period which is different from the

standardized period may be determined or the number of interviews might be adjusted.

As a result of adjustment, the overall period subject to the examination may change. In

addition, the standard examination period has been determined under the assumption

that no specific issues would be identified in the due course of examination. If any

issues or problems are identified during the examination process or any fact which

was not known is revealed by some news or information provided by external media,

the examination period may be extended.

Note 2: For any applicants expected to significantly influence the market or investors, the

Listing Examination Division of JPXR will reach a conclusion on the listing after making

several rounds of discussions at the Board of Directors. For example, such applicants

include:

- Privatized enterprise applicants;

- Applicants adopting any scheme requiring considerations in terms of corporate

governance such as the use of class stocks with voting rights;

- Re-listing applicant;

- Applicants concerned with compliance as a company of the applicant group or those for

which the management of the applicant committed a serious incident or breached laws

and regulations in the past;

- Other applicants requiring considerations for other issues; or,

- Applicants with an expected market capitalization of 100 billion yen or more at the time

Ⅰ About Listing

- 15 -

of listing.

For such applicants, a large number of issues must be discussed and assessed during

listing examination. Therefore TSE would request the applicants to allow for one month or

more in addition to the standard listing examination period.

Note 3: Should you have any questions or uncertainty concerning examination schedule,

including cases of Notes 1 and 2 above, please contact JPXR via your lead

underwriter following the consultation with it.

Meanwhile, in case of preliminary review, the applicant is requested to submit the draft of any

pages in “JASDAQ Listing Application Report responding to the questions made at the time of

acceptance of application before interviews at the time of listing application. In practice, the lead

underwriter will submit such draft.

(3) Listing Application

At the meeting for the purpose of listing application, JPXR will accept the listing application and

examination officers will brief the applicant on the prospective listing examination and overview

of listing examination as well as practical procedures for examination (written schedule and

examination items will also be provided).

Then the applicant is requested to explain the reasons for listing application, lines of businesses,

business environment, and business model. For actual questions, please refer to “Questions at

Interview (at the time of Listing Application)” at section 6 of IV Checklists Before Applying for

Listing on JASDAQ.

An application will ordinarily be made after the completion of the general shareholders’ meeting

for the previous year. Presidents (CEO), officers in charge of listing application and persons in

charge of contact of the applicant as well as officers of the lead underwriter in charge of listing

application will attend the meeting for the acceptance of listing application.

[Questions Concerning Listing Application]

Q1: Consistent with the application for listing on the First and Second Sections, and Mothers,

can we make listing application before the accounts for the immediate preceding year

are finalized and settled as the general meeting of shareholders completes?

A1: You may file the application before the accounts for the previous year are finalized and

settled (hereinafter referred to as “Preliminary Application”). However, as “Part I”

documents will be made available for the public inspection when TSE approves the listing

and publicly announces the approval thereof and they include the presentation of financial

statements for the previous year, the approval of listing (and public announcement) by

TSE will be after the completion of general meeting of shareholders where financial

statements are finalized and fair opinion on the financial statements is expressed by the

Ⅰ About Listing

- 16 -

relevant audit firm in the audit report.

In case of listing on JASDAQ, JPXR will carry out the examination on the basis of “Part I”

documents and “JASDAQ Listing Application Report.” So if you file a Preliminary

Application, the examination will be made based on the documents submitted for the

Preliminary Application (Preliminary Security Listing Application Form for Securities

Listing, and draft documents commonly required for the listing application).

When you file a Preliminary Application, you will be required to reapply for the listing when

all the documents necessary for listing application (financial statements authorized at the

general meeting of shareholders, Part I documents with audit report attached, and so on)

are prepared.

Ⅰ About Listing

- 17 -

Q2: What is the timing of filing an application for listing on JASDAQ?

A2: JPXR requests an applicant to file an application for listing so that the listing would be

made within application year, consistent with the First and Second Sections, and Mothers.

However an expected application may be made when the end of the business year

approaches due to the underwriter’s examination of revenue trend.

Therefore, if in light of JASDAQ concepts, the applicant may determine the listing

schedule which may allow the listing date to be before the completion of general meeting

of shareholders by considering the following, JPXR may accept the listing application.

1) Listing application does not straddle the end of business year (the listing application is

made within the year described in the listing application);

2) Accounts information for application year is additionally included in Part I documents;

and

3) Movements of monthly operating results assure that the applicant will not meet any

delisting criteria in the business year following the application year.

In the meantime, in the event that the listing proves not to be made at latest by the date

preceding the general meeting of shareholders, the applicant is required to make the

reapplication for listing.

Ⅰ About Listing

- 18 -

(4) Listing Examination

Actual listing examination will be implemented as follows:

a. Interviews

The examiners will assess the degree of satisfaction of requirements of the standards for listing

examination (II Formal Requirements (those relating to Rule 216, 3 of Regulations or Rule 216,

6 of Regulations) on the basis of the documents submitted at the time of listing application.

Then the examiners will conduct interviews mainly based on “Part I” documents or “JASDAQ

Listing Application Report” in order to examine the contents described in “III Listing Examination

(relating to Rule 216-5 and Rule 216-8 of the Regulations).”

Three rounds of interviews will usually be made not including the one at the time of listing

application. When the third round of interviews completes, if there remain issues to be clarified,

additional interviews may be requested.

b. Field inspection

When an applicant possesses factories or other facilities, the examiners actually visit on-site to

more thoroughly understand the substance of the applicant.

c. Attending e-learning courses

Directors and officers of a listed company are required to have insights on a wide variety of

matters on company management. Especially, they are requested to attend e-learning courses

to help them deepen their understanding of the issues to which they have to pay close attention

during the examination period for a listing application. They include the duties and attitudes of

mind entailed in listing, the need to develop and appropriately operate a management system

meeting all the requirements of a listed company, suitable attitude towards corporate

governance as a listed company, and preventive measures against insider trading,

communication of information and issuance of trading recommendations.

d. Interviews with certified public accountants (CPAs)

The examiners hold interviews with certified public accountants that carry out the audit of the

applicant with a primary focus on the reasons for entering into audit engagement, degree of

communication with management, company auditors and so on, status of design and

implementation of internal management systems, as well as accounting and disclosure systems.

The interviews will be conducted only with the Certified Public Accountants. Timing of execution

of the interviews will not be notified to an applicant and a lead underwriter.

Ⅰ About Listing

- 19 -

e. Meeting with the president (CEO),the company auditors and independent

directors/auditors

For the purpose of meetings with the president (CEO), the examiners will visit the applicant and

meet the president (representative director, chief executives). During the interviews the

examiners will ask the following issues:

- The overview of the company and industry;

- What vision does the president as a manager have for the operation and management of

the company;

- Measures to address investors (shareholders) when it becomes a listed company

(including IR activities);

- A policy, a current organizational framework and a management status regarding corporate

governance and compliance of an applicant; and

- Systems to disclose operating results and ensure control of internal information

During the interviews with company auditors, the examiners will, in principle, ask full time

company auditors of the status of audits they perform and any challenges faced by the

applicant.

In addition, during the interviews with independent directors/auditors, the examiners will, in

principle, ask them of the following:

- Policies, present status and implementation conditions for the corporate governance

practices of the applicant;

- Management’s awareness of compliance issues;

- Status of development and improvement of environments for independent

directors/auditors to execute their duties (provision of information, sufficient time to review,

etc.);

- How they assess the existence of transactions involving the management and check and

balance system over the transactions; and

- How they recognize the roles and functions, etc. expected of them after the listing.

In addition when the examiners find it necessary to have interviews with other officers on any

specific matter, they may have interviews with such other officers. If the applicant appoints

accounting advisors, the examiners may ask them of design and implementation of accounting

organization and their roles.

A three business day interval will be provided between the interview (final round) and the

meetings with the president,company auditors and independent directors/auditors.

f. Presentation by the president

Ⅰ About Listing

- 20 -

JPXR will ask the president (representative directors, chief executives) to visit JPXR and make

a presentation of the company in terms of the characteristics, management policies and

business plans, etc. of the company. Then JPXR will decide to proceed with the final

determination of the listing based on the result of questions and answers session regarding

them. In addition the executive officers of JPXR will ask some questions concerning the

presentation and explain the issues the applicant should consider and the requests to be

satisfied when it becomes a listed company. As issues to be considered and requested to

address may include those related to disclosure system, etc., JPXR will request the chief

information officer (*) of applicant to attend the presentation.

* Listed companies are required to select and appoint the chief information officers from

directors, executives or those in similar capacity and register them with TSE.

The chief information officer shall be responsible for reports in response to inquiries by TSE

and other communication in relation to the disclosure of corporate information. In practice, the

chief information officer will be the person TSE will communicate with and also be responsible

for internal management and disclosures of material information.

f. Internal discussions in TSE

Following the completion of the presentation by the president, JPXR will make the final decision

on the listing and the listing examination process will substantially complete.

After necessary procedures are implemented, TSE will inform the applicant of TSE’s approval

and explain the subsequent procedures to be followed.

Ⅰ About Listing

- 21 -

(5) After TSE’s Listing Approval

a. Announcements to the media, etc.

TSE will announce the approval of listing of the applicant to the press and other media. If any

public offering or secondary offering is effected, listing will be realized about four weeks

thereafter. If no public offering or secondary offering is effected as it has already listed its stock

on another financial instruments exchange, listing will be realized one week after

announcement of the listing.

In the meantime, listing approval may be cancelled if any requirement of standards for the

listing examination is not satisfied as public offering or secondary offering is discontinued.

b. Meetings with TSE’s Listing Department and Market Surveillance and Compliance

Department of JPXR

Between the approval and the actual listing, the TSE Listing Department will meet officers

responsible for the information management and those responsible for communications with

TSE in relation to timely disclosure, etc. following listing and explain various procedures in

terms of timely disclosures and earnings announcements.

In order to prevent any insider trading, the Market Surveillance and Compliance Department of

JPXR will explain the regulations on prevention of insider trading.

c. Public offering and secondary offering

JPXR will assess whether the company meets criteria for liquidity (the number of shareholders,

criteria for shares traded on the secondary market, the number of shares publicly offered and

market capitalization) through the public offering and secondary offering. In addition JPXR

ensures that for a company before listing, public offering, or public offering and secondary

offering have been carried out according to various rules set forth for public offering and

secondary offering, etc.

d. Listing

The Listing Contract entered into by and between the company and TSE requires the company

to comply with various rules set forth for timely disclosure, etc. effective from the listing date. On

the listing date, the recent financial information, etc. will be disclosed through the TDnet as the

“Earnings Release” (including the contents of future forecast information (information related to

the forecast for company’s future performance results and financial position; the same shall

apply hereinafter) if it is disclosed). Alisting ceremony will also be held where TSE will present

the company with a memorial token of listing.

Ⅰ About Listing

- 22 -

(6) Follow-ups after Listing

Given that a newly listed company is required to continuously carry out appropriate business

activities after listing, TSE will continue to follow up the business activities of the listed company

for approximately one year after listing (three years in case of Growth Market). Such follow-ups

will mainly focus on the matters identified by TSE during the process of listing examination.

In practice TSE will continuously follow up material business activities after listing and the status

of matters requested by TSE to be addressed during the process of listing examination on the

basis of timely disclosures. If necessary and appropriate, TSE will make inquiries and

interviews with the listed company and the lead underwriter.

As a result of the follow-ups, if TSE detects any inappropriate business activities after listing or

the some issues identified to be corrected in the listing examination remain uncorrected, TSE

will require improvements and corrections of such matters. In response to such requirements,

the listed company should provide a written response outlining the prospective corrective

measures.

Items to be monitored after listing may include:

[Material business activities after listing (examples)]

- Resignation of chief executive officer (such as president)

- Corporate reorganization through mergers and other transactions (stock swap, share

transfer, merger and split-up)

- Material business partnership or its termination

- Changes in the parent company, changes in controlling shareholders (excluding the parent

company) or changes in other related companies

[Issues detected during the examination process, to be addressed by the listed company

(examples)]

- Appropriate operation of internal management system improved during the period subject to

the examination

- Gradual decrease and elimination of transactions with related parties, which should

eventually be eliminated

[Timely disclosures after listing (examples)]

- Revision of future prospective information including earnings forecast

- Modifications and/or reviews of business plan and medium-term management plan

presented at the listing examination

Listed companies are encouraged to review and update the contents of the securities report, as

appropriate, after listing in consideration of external and internal environments surrounding

them.

Ⅰ About Listing

- 23 -

As a part of TSE’s follow-ups after listing, it will ensure that listed companies have appropriately

reviewed and updated the securities reports filed after listing, especially the section “Risks, etc.

associated with business” in consideration of their specific conditions and environments.

Ⅰ About Listing

- 24 -

[Model schedule form the listing approval to the listing]

1 Sun 1 Wed

2 Mon 2 Thu

3 Tue 3 Fri

4 Wed 4 Sat

5 Thu 5 Sun

6 Fri 6 Mon

7 Sat 7 Tue

8 Sun 8 Wed

9 Mon 9 Thu

10 Tue 10 Fri

11 Wed 11 Sat

12 Thu 12 Sun

13 Fri 13 Mon

14 Sat 14 Tue

15 Sun 15 Wed

16 Mon 16 Thu

17 Tue 17 Fri

18 Wed 18 Sat

19 Thu 19 Sun

20 Fri 20 Mon

21 Sat 21 Tue

22 Sun 22 Wed

23 Mon 23 Thu

24 Tue 24 Fri

25 Wed 25 Sat

26 Thu 26 Sun

27 Fri 27 Mon

28 Sat 28 Tue

29 Sun 29 Wed

30 Mon 30 Thu

31 Tue 31 Fri

Month Y One month after month Y

Listing approval, resolution at the Board

of Directors to issue new shares, filing of

Securities Registration Statement (filing

with the Financial Services Agency by

the applicant)

Payment date and date when new

shares take effect

Listing date

Holiday

Meeting of the Board of Directors to

determine provisional terms and

conditions (payment amounts for the

purpose of the Companies Act)

Filing of (Primary) Amended Registration

Statement (filing with the Financial

Services Agency by the applicant)

Determination of issue prices and

underwriting prices

Date when the registration statements

take effect

Filing of (Secondary) Amended

Registration Statement (filing with the

Financial Services Agency by the

applicant)

Pre

-ma

rke

tin

g p

eri

od

(9 b

usin

ess d

ays)

15

da

ys o

r o

ve

r

Bo

ok

bu

ild

ing

pe

rio

d

(5 b

usin

ess d

ays)

Su

bscri

pti

on

pe

rio

d

(4 b

usin

ess d

ays)

Ⅰ About Listing

- 25 -

Note: The above is given only for reference. Actual financing schedule (pre-marketing period or

book building period, timing of the board meeting on the terms and conditions or the filing

of Securities Registration Report) may differ from one applicant to another.

II Formal Requirements (relating to Rule 216-3 and Rule 216-6 of the Regulations)

- 26 -

II Formal Requirements (relating to Rule 216-3 and

Rule 216-6 of the Regulations)

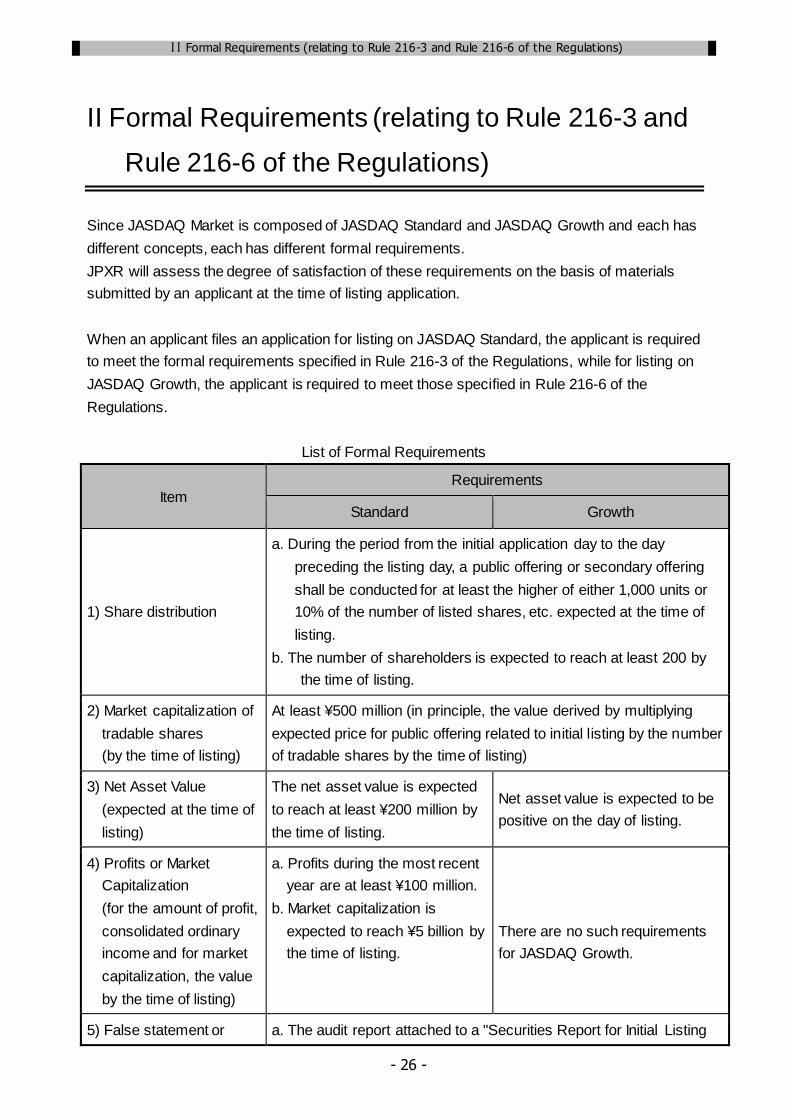

Since JASDAQ Market is composed of JASDAQ Standard and JASDAQ Growth and each has

different concepts, each has different formal requirements.

JPXR will assess the degree of satisfaction of these requirements on the basis of materials

submitted by an applicant at the time of listing application.

When an applicant files an application for listing on JASDAQ Standard, the applicant is required

to meet the formal requirements specified in Rule 216-3 of the Regulations, while for listing on

JASDAQ Growth, the applicant is required to meet those specified in Rule 216-6 of the

Regulations.

List of Formal Requirements

Item Requirements

Standard Growth

1) Share distribution

a. During the period from the initial application day to the day

preceding the listing day, a public offering or secondary offering

shall be conducted for at least the higher of either 1,000 units or

10% of the number of listed shares, etc. expected at the time of

listing.

b. The number of shareholders is expected to reach at least 200 by

the time of listing.

2) Market capitalization of

tradable shares

(by the time of listing)

At least ¥500 million (in principle, the value derived by multiplying

expected price for public offering related to initial listing by the number

of tradable shares by the time of listing)

3) Net Asset Value

(expected at the time of

listing)

The net asset value is expected

to reach at least ¥200 million by

the time of listing.

Net asset value is expected to be

positive on the day of listing.

4) Profits or Market

Capitalization

(for the amount of profit,

consolidated ordinary

income and for market

capitalization, the value

by the time of listing)

a. Profits during the most recent

year are at least ¥100 million.

b. Market capitalization is

expected to reach ¥5 billion by

the time of listing.

There are no such requirements

for JASDAQ Growth.

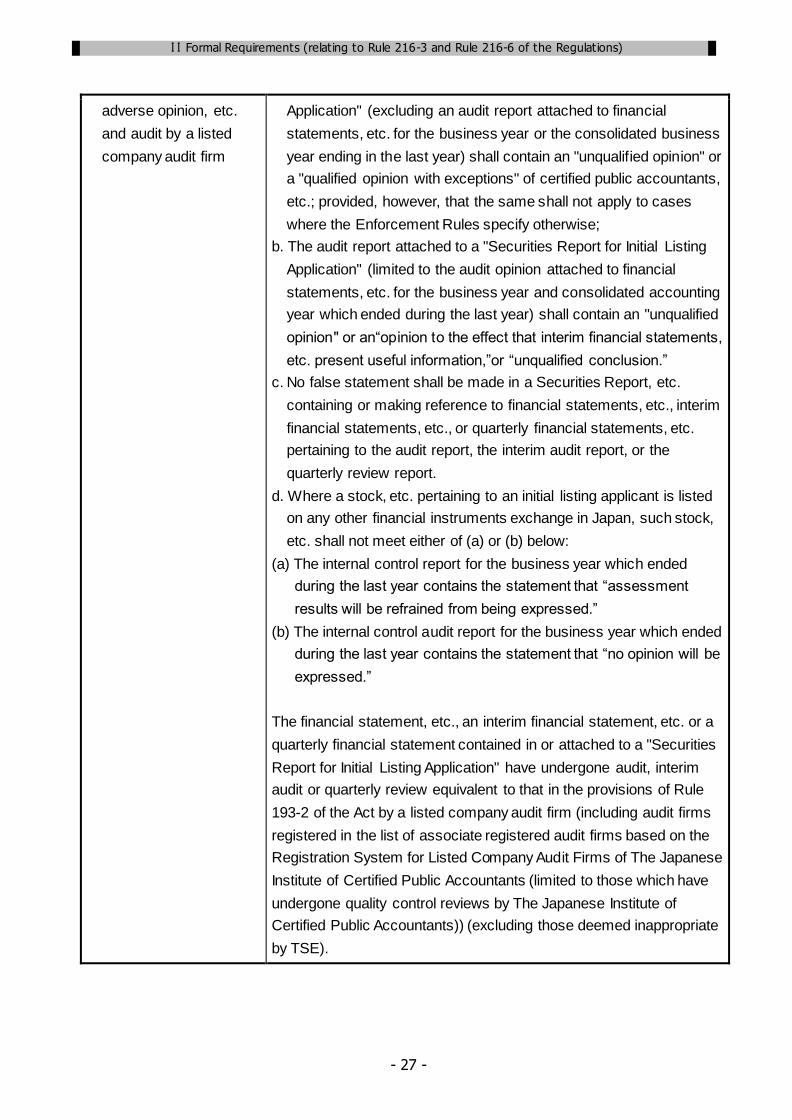

5) False statement or a. The audit report attached to a "Securities Report for Initial Listing

II Formal Requirements (relating to Rule 216-3 and Rule 216-6 of the Regulations)

- 27 -

adverse opinion, etc.

and audit by a listed

company audit firm

Application" (excluding an audit report attached to financial

statements, etc. for the business year or the consolidated business

year ending in the last year) shall contain an "unqualified opinion" or

a "qualified opinion with exceptions" of certified public accountants,

etc.; provided, however, that the same shall not apply to cases

where the Enforcement Rules specify otherwise;

b. The audit report attached to a "Securities Report for Initial Listing

Application" (limited to the audit opinion attached to financial

statements, etc. for the business year and consolidated accounting

year which ended during the last year) shall contain an "unqualified

opinion" or an“opinion to the effect that interim financial statements,

etc. present useful information,”or “unqualified conclusion.”

c. No false statement shall be made in a Securities Report, etc.

containing or making reference to financial statements, etc., interim

financial statements, etc., or quarterly financial statements, etc.

pertaining to the audit report, the interim audit report, or the

quarterly review report.

d. Where a stock, etc. pertaining to an initial listing applicant is listed

on any other financial instruments exchange in Japan, such stock,

etc. shall not meet either of (a) or (b) below:

(a) The internal control report for the business year which ended

during the last year contains the statement that “assessment

results will be refrained from being expressed.”

(b) The internal control audit report for the business year which ended

during the last year contains the statement that “no opinion will be

expressed.”

The financial statement, etc., an interim financial statement, etc. or a

quarterly financial statement contained in or attached to a "Securities

Report for Initial Listing Application" have undergone audit, interim

audit or quarterly review equivalent to that in the provisions of Rule

193-2 of the Act by a listed company audit firm (including audit firms

registered in the list of associate registered audit firms based on the

Registration System for Listed Company Audit Firms of The Japanese

Institute of Certified Public Accountants (limited to those which have

undergone quality control reviews by The Japanese Institute of

Certified Public Accountants)) (excluding those deemed inappropriate

by TSE).

II Formal Requirements (relating to Rule 216-3 and Rule 216-6 of the Regulations)

- 28 -

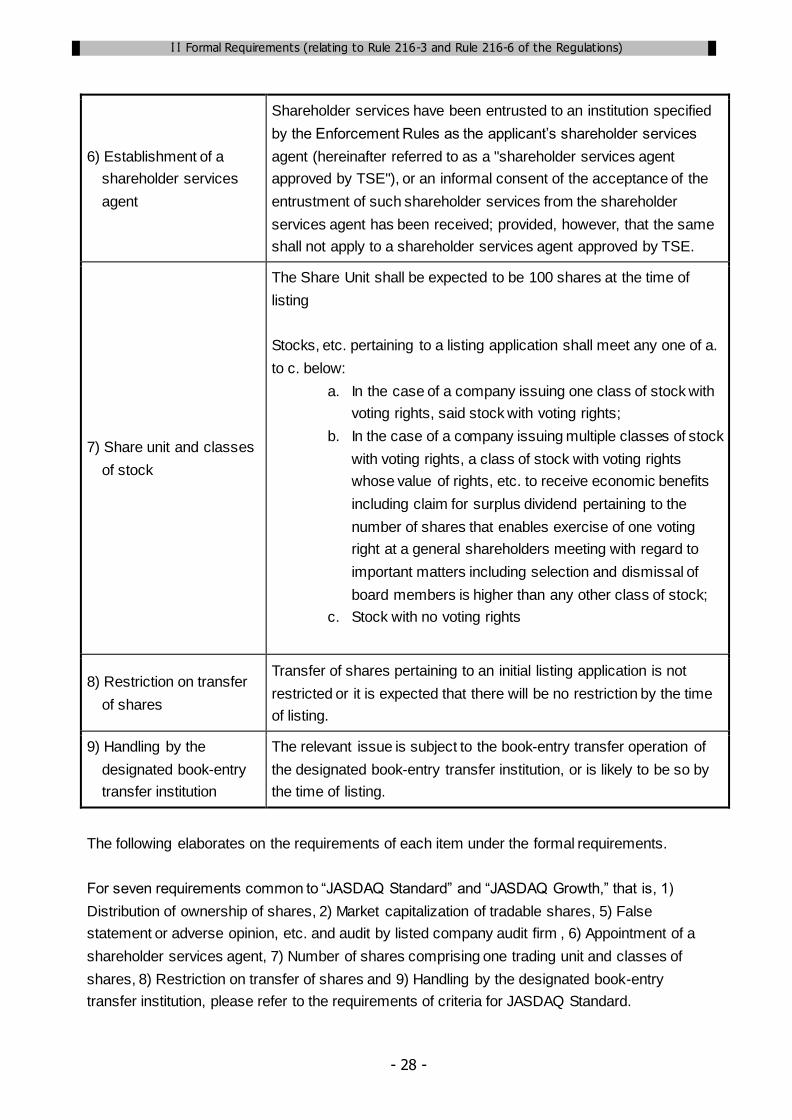

6) Establishment of a

shareholder services

agent

Shareholder services have been entrusted to an institution specified

by the Enforcement Rules as the applicant’s shareholder services

agent (hereinafter referred to as a "shareholder services agent

approved by TSE"), or an informal consent of the acceptance of the

entrustment of such shareholder services from the shareholder

services agent has been received; provided, however, that the same

shall not apply to a shareholder services agent approved by TSE.

7) Share unit and classes

of stock

The Share Unit shall be expected to be 100 shares at the time of

listing

Stocks, etc. pertaining to a listing application shall meet any one of a.

to c. below:

a. In the case of a company issuing one class of stock with

voting rights, said stock with voting rights;

b. In the case of a company issuing multiple classes of stock

with voting rights, a class of stock with voting rights

whose value of rights, etc. to receive economic benefits

including claim for surplus dividend pertaining to the

number of shares that enables exercise of one voting

right at a general shareholders meeting with regard to

important matters including selection and dismissal of

board members is higher than any other class of stock;

c. Stock with no voting rights

8) Restriction on transfer

of shares

Transfer of shares pertaining to an initial listing application is not

restricted or it is expected that there will be no restriction by the time

of listing.

9) Handling by the

designated book-entry

transfer institution

The relevant issue is subject to the book-entry transfer operation of

the designated book-entry transfer institution, or is likely to be so by

the time of listing.

The following elaborates on the requirements of each item under the formal requirements.

For seven requirements common to “JASDAQ Standard” and “JASDAQ Growth,” that is, 1)

Distribution of ownership of shares, 2) Market capitalization of tradable shares, 5) False

statement or adverse opinion, etc. and audit by listed company audit firm , 6) Appointment of a

shareholder services agent, 7) Number of shares comprising one trading unit and classes of

shares, 8) Restriction on transfer of shares and 9) Handling by the designated book-entry

transfer institution, please refer to the requirements of criteria for JASDAQ Standard.

II Formal Requirements (relating to Rule 216-3 and Rule 216-6 of the Regulations)

- 29 -

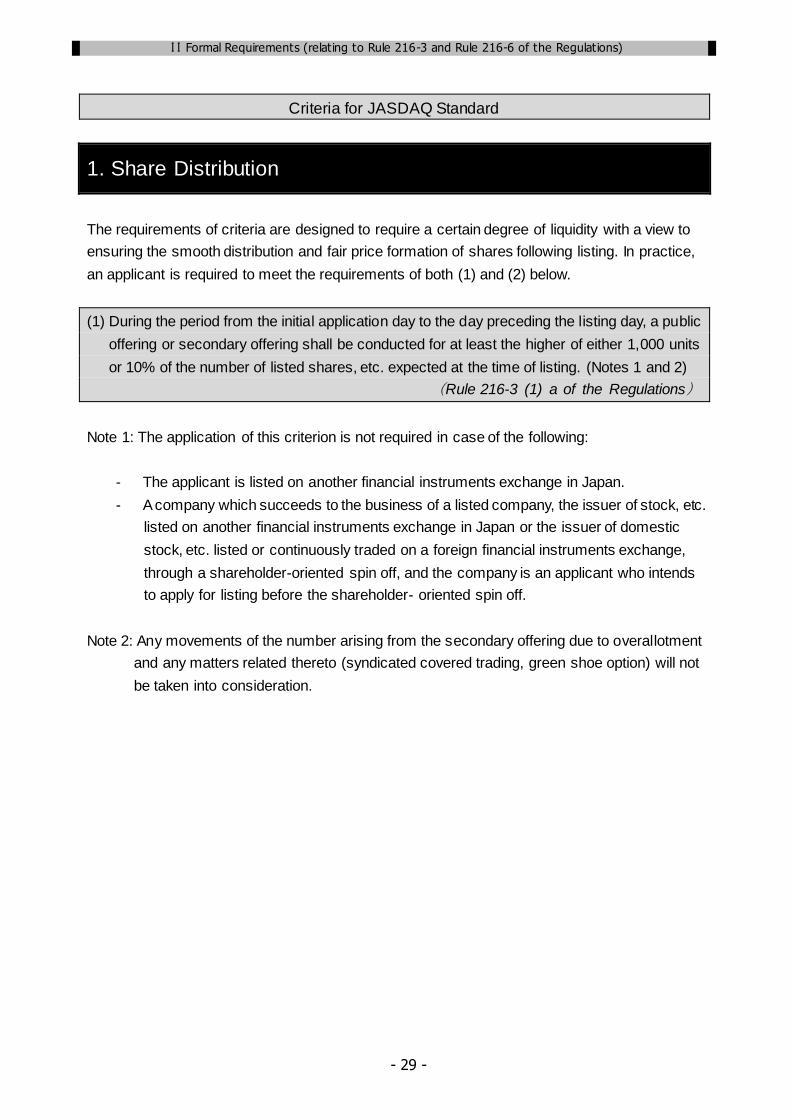

Criteria for JASDAQ Standard

1. Share Distribution

The requirements of criteria are designed to require a certain degree of liquidity with a view to

ensuring the smooth distribution and fair price formation of shares following listing. In practice,

an applicant is required to meet the requirements of both (1) and (2) below.

(1) During the period from the initial application day to the day preceding the listing day, a public

offering or secondary offering shall be conducted for at least the higher of either 1,000 units

or 10% of the number of listed shares, etc. expected at the time of listing. (Notes 1 and 2)

(Rule 216-3 (1) a of the Regulations)

Note 1: The application of this criterion is not required in case of the following:

- The applicant is listed on another financial instruments exchange in Japan.

- A company which succeeds to the business of a listed company, the issuer of stock, etc.

listed on another financial instruments exchange in Japan or the issuer of domestic

stock, etc. listed or continuously traded on a foreign financial instruments exchange,

through a shareholder-oriented spin off, and the company is an applicant who intends

to apply for listing before the shareholder- oriented spin off.

Note 2: Any movements of the number arising from the secondary offering due to overallotment

and any matters related thereto (syndicated covered trading, green shoe option) will not

be taken into consideration.

II Formal Requirements (relating to Rule 216-3 and Rule 216-6 of the Regulations)

- 30 -

(2) The number of shareholders is expected to reach at least 200 by the time of listing. (It

represents the number of shareholders holding share unit (Note 1); the same shall apply

hereinafter).

(Rule 216-3 (1) b of the Regulations)

For the purpose of this criterion, the number of shareholders is determined on the basis of the

number of shareholders as of the last record date. The objective of this criterion is to ensure

smooth distribution and fair price formation of shares. If this criterion is not met as of the last

record date, the satisfaction thereof by the time of listing will suffice.

Note 1: Where an applicant adopts the number of shares per Share Unit, one unit means the

number of shares, and if the applicant does not adopt any number, one unit refers to

one share.

Note 2: When Depository Receipts (DRs) representing the rights, etc. attached to shares are

issued, shareholders who hold DRs representing rights attached to the number of

shares comprising the one trading unit or more can be included in the number of

shareholders.

Note 3: “Record date” represents the record date as prescribed in the Companies Act or

Preferred Equity Contribution Act or the date when a depository institution prescribed in

Rule 2, Paragraph 2 of the Law Concerning Central Securities Depository and

Book-Entry Transfer of Corporate Bonds and Share Certificates (hereinafter referred to

as the “Book-Entry Transfer Law”) (including cases where the Rule applies mutatis

mutandis to Rule 235) issues the notice to all the shareholders in accordance with

Rule 151, Paragraph 1 or Paragraph 8 of the same law.

Note 4: When an applicant does not understand the status of shareholders, etc. as of the record

date, the number of shareholders will be determined based on the conditions of

shareholders as of the last record date when the applicant has understood the status of

shareholders, etc.

When an applicant purchases its own stocks after the last record date under the resolution at

the Board of Directors to authorize the purchaser an applicant resolves at the Board of Directors

to authorize the disposal of its treasury stock, the number of shareholders will be determined in

the following manner.

1) An applicant Purchases its Own Stocks

The number of shareholders reduced as a result of such purchase will be deducted from the

number of shareholders as of the last record date.

II Formal Requirements (relating to Rule 216-3 and Rule 216-6 of the Regulations)

- 31 -

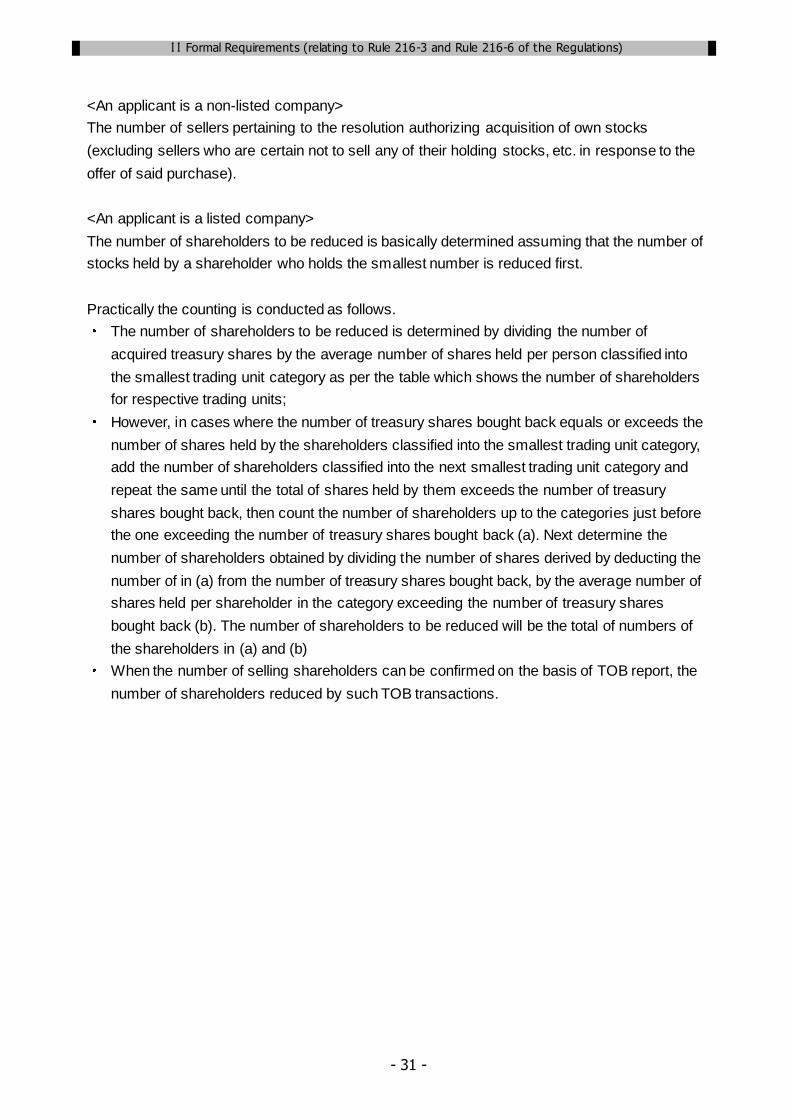

<An applicant is a non-listed company>

The number of sellers pertaining to the resolution authorizing acquisition of own stocks

(excluding sellers who are certain not to sell any of their holding stocks, etc. in response to the

offer of said purchase).

<An applicant is a listed company>

The number of shareholders to be reduced is basically determined assuming that the number of

stocks held by a shareholder who holds the smallest number is reduced first.

Practically the counting is conducted as follows.

The number of shareholders to be reduced is determined by dividing the number of

acquired treasury shares by the average number of shares held per person classified into

the smallest trading unit category as per the table which shows the number of shareholders

for respective trading units;

However, in cases where the number of treasury shares bought back equals or exceeds the

number of shares held by the shareholders classified into the smallest trading unit category,

add the number of shareholders classified into the next smallest trading unit category and

repeat the same until the total of shares held by them exceeds the number of treasury

shares bought back, then count the number of shareholders up to the categories just before

the one exceeding the number of treasury shares bought back (a). Next determine the

number of shareholders obtained by dividing the number of shares derived by deducting the

number of in (a) from the number of treasury shares bought back, by the average number of

shares held per shareholder in the category exceeding the number of treasury shares