Embed Size (px)

Citation preview

Jack van der MerweCEO: Gautrain Management Agency / President UATP

06 October 2016

‘Unlocking the Economy with Public Transport’

A: The Global Environment we Operate in

Global Environment

• Globally we are driven by the following three “C”’s:• Change, we are living in a world that is continuously

changing (now and in the future).• Complexity, we are living in a world that is extremely

complex, with an overload of data & information and very few traditional methods of addressing problems and issues are still applicable.

• Competition, we are living in an competitive global village where processes and procedures must be upgraded continuously to ensure growth and survival.

B: Future Cities(A case for Public Transport)

How Will Cities Look in 2025?

• By 2025, almost 60% of the world’s population will be living in urban areas

• Rapid urbanisation & economic development will increase the demand for the movement of people, goods & services

• Global trend is towards private vehicles as the preferred mode of transport

• 6.2 billion private motorised trips will be made every day in cities worldwide

• Gridlock, pollution, road traffic accidents & greater dependency on fossil fuels

• If left unchecked by 2025 worldwide transport related greenhouse gas emissions will be 25% higher than 2005 levels, this will:

• Put us firmly on the path towards potential catastrophic climate change

• Transport energy bills will skyrocket• Higher levels of energy consumption could pose a threat to global

energy security• Traffic congestion will bring cities worldwide to a standstill• Half a million people will be killed in road traffic accidents every year• Potentially catastrophic climate change

How Will Cities Look in 2025?

UITP

• International Association of Public Transport (UITP) is an international network for public transport authorities and operators, policy decision makers, scientific institutions, consultants, operators and the public transport support and service industry

• UITP brings together 3400 members (companies, firms of organisations) from 92 countries around the world

• (UATP is the Africa chapter of the UITP)

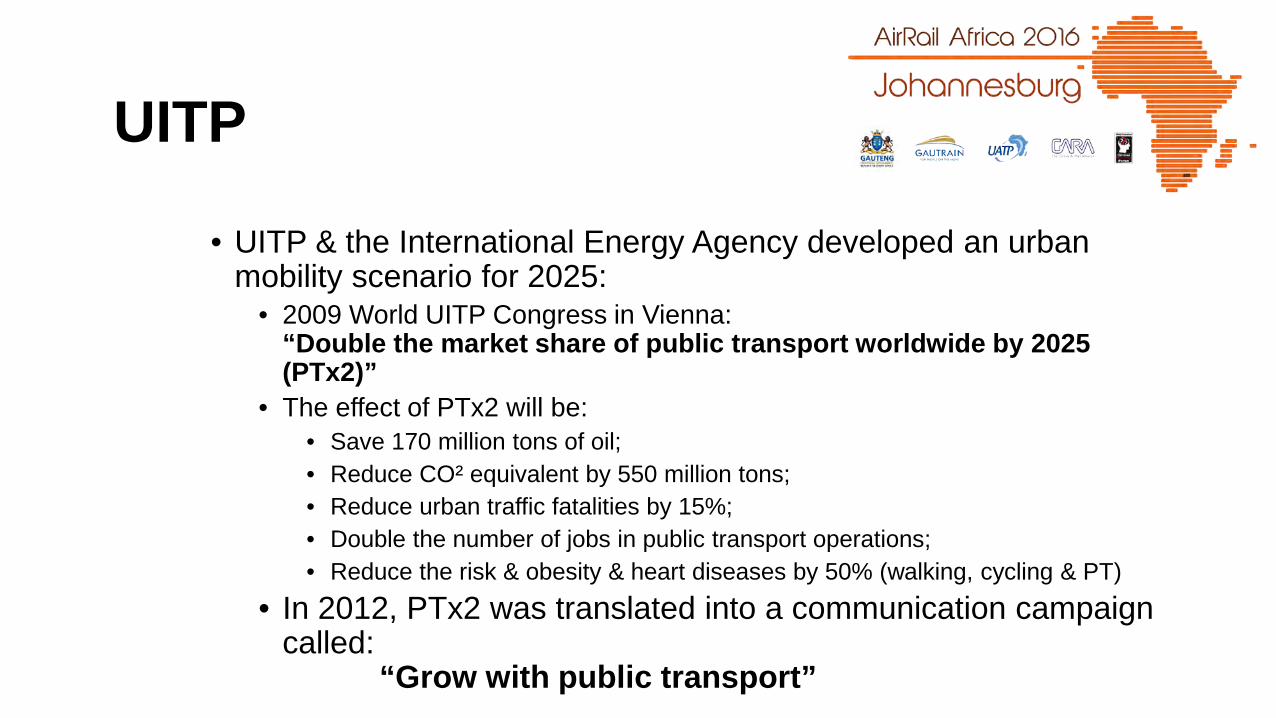

• UITP & the International Energy Agency developed an urban mobility scenario for 2025:

• 2009 World UITP Congress in Vienna:“Double the market share of public transport worldwide by 2025 (PTx2)”

• The effect of PTx2 will be:• Save 170 million tons of oil;• Reduce CO² equivalent by 550 million tons;• Reduce urban traffic fatalities by 15%;• Double the number of jobs in public transport operations;• Reduce the risk & obesity & heart diseases by 50% (walking, cycling & PT)

• In 2012, PTx2 was translated into a communication campaign called:

“Grow with public transport”

UITP

C: Long Term Transport Planning for Gauteng

(A case for Public Transport)

25-YEAR INTEGRATED TRANSPORT MASTER PLAN(ITMP25)

Best Practice in Public Transport -Africa for Africa: UATP Workshop 2015

22 October 2015

Transport Planning

Current –Status Quo

Predicted –Future State

Population Growth –(Number of workers)

Land-use Patterns –(Where will the People live)

Economic Growth –(type, location, labour requirements)

13 (GTIP5) & 10 (ITMP25) Major Interventions* or “do nothing”*

Enablers*** or “do nothing”

2012

2037

External Factors**

“The Cost of Doing Nothing”

• Analysis of the transport situation in 25-years’ time, shows that the consequences or “cost of doing nothing” will be severe, i.e. if current trends continue

• Vehicle population predicted to grow from 3.65 mil. to 6.57mil.• Peak hour person trips to grow from 2.2mil. to 3.9mil.• Weighted average peak hour road network speed will reduce from

48km/h to below 10km/h• Weighted public transport travel speed decline from 38km/h to

below 14km/h• Congestion nightmare, with the transport network, the economy

and the natural environment eventually choking• Major interventions and management of travel choices and

demand will be required to avoid this scenario

7%9%

30%53%

Base Year

9%

11%

31%

48%

2025 Demand on Base Year Network

39%

17%

22%

23%

2037 Demand on Base Year Network

0 - 20 km/h

20 - 40 km/h

40 - 60 km/h

> 60 km/h

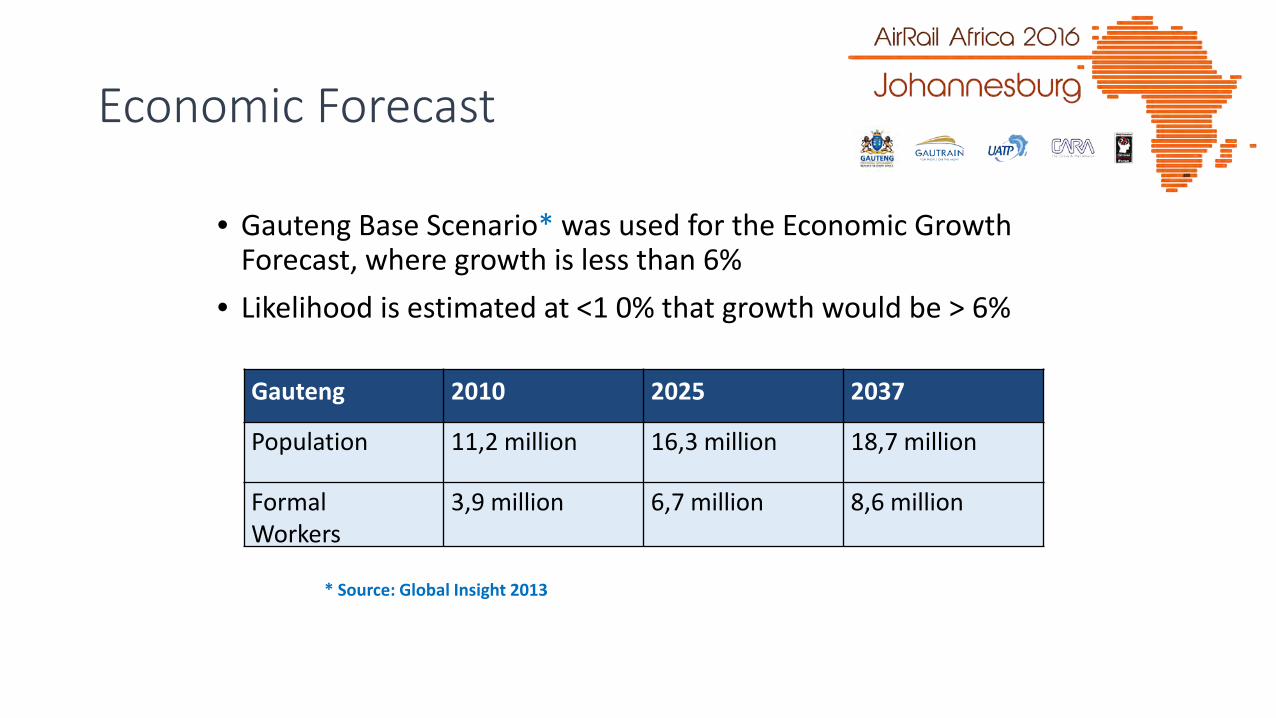

Economic Forecast

• Gauteng Base Scenario* was used for the Economic Growth Forecast, where growth is less than 6%

• Likelihood is estimated at <1 0% that growth would be > 6%

Gauteng 2010 2025 2037

Population 11,2 million 16,3 million 18,7 million

FormalWorkers

3,9 million 6,7 million 8,6 million

* Source: Global Insight 2013

Job Opportunities: Formal Workers

Key focus areas:

• Priority public transport corridors• Strategic modal transfer nodes and interchanges• Freight routes and logistics centres• Rail as the backbone of an integrated public transport system• Protection of future priority corridors, future road networks, passenger

and freight rail networks, and airports.

The plan further includes a vision to support and strengthen the Gauteng Global City Region. Geographical Information Systems and Intelligent Transport Systems form a practical basis for the plan.

Sustainable Transport

• Reduce travel:• Change travel patterns

• Regularity & extent of travel in peak periods, trip lengths, etc.

• Shift in modes:• Shift from: Motorised Non-motorised transport• Shift from: Private Public transport• Shift from Road Rail

• Technology:• Environmentally friendly technologies• Intelligent Transport Solutions (ITS)

D: Ekurhuleni Aerotropolis(A case for Public Transport)

WHAT IS AN

AEROTROPOLIS?

An Aerotropolis has an airport city at its core and is surrounded by clusters of industry-related enterprises that gain a competitive advantage by utilizing the synergistic capabilities of its respective location.

~ Dr. John Kasarda

BackgroundThe development of an Aerotropolis is a process not a

project

An Aerotropolis will develop around an international airport spontaneously, but if the development is planned and properly structured one can maximise the benefits to the area and the country.

The Ekurhuleni Aerotropolis is not competing with Johannesburg or Tshwane, its competing with Schiphol, Memphis, Denver, Hong Kong, etc.

THE AEROTROPOLIS OPPORTUNITY

Produce and Export

Value Add

Import and Distribute

Transshipment

Service provider

CONNECTING THROUGH ECONOMIC FACILITATION

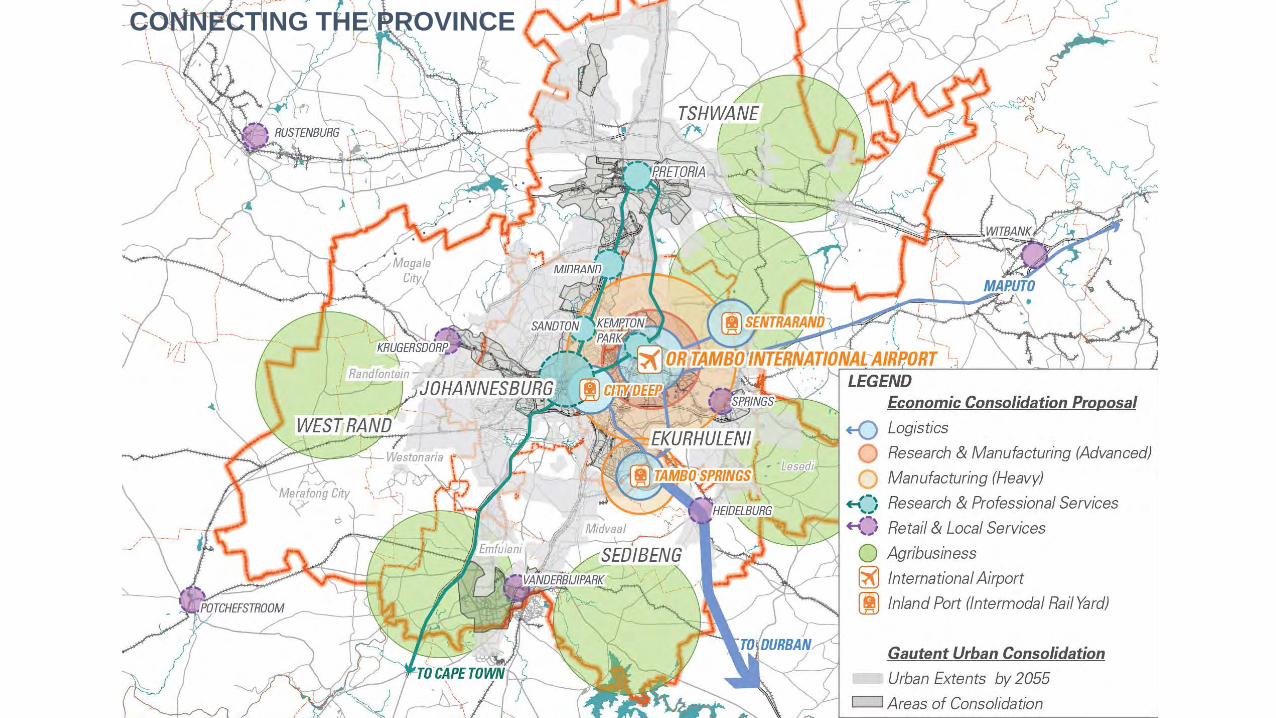

CONNECTING THE PROVINCE

CONNECTING SOUTH AFRICA TO ITS NEIGHBOURS

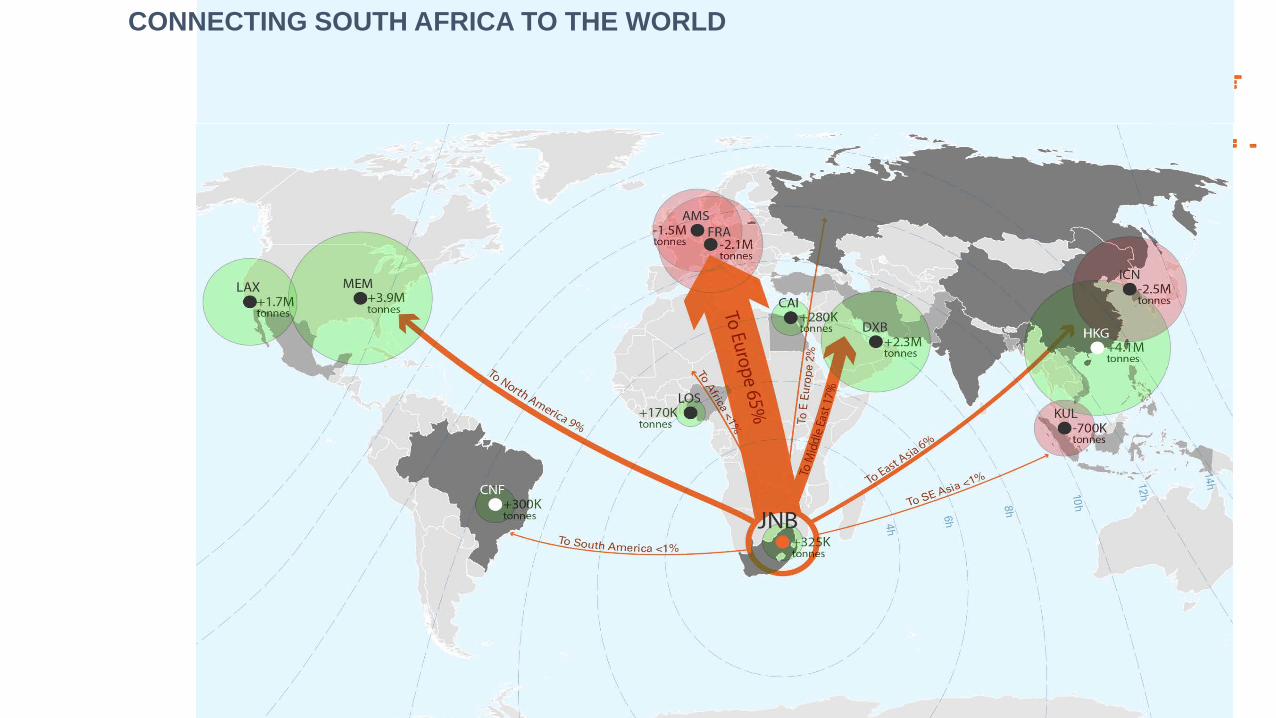

CONNECTING SOUTH AFRICA TO THE WORLD

ENABLING & CATALYST PROJECTS

ENABLING PROJECTS

• Four types of enabling projects:• Commercial Catalytic Projects;• Urban Regeneration Projects;• Economic Enabling Infrastructure Projects; and• Development (Mega) Projects.

Aerospace Manufacturing &

Aviation

Manufacturing and High Tech

Logistics & Distribution

Health & Life Sciences

Agri – Business & Food Processing

Natural Resources & Energy

Education & Skills Training

Tourism & Culture

Retail

Professional Services & Public

Admin

KEY ECONOMIC CLUSTERS

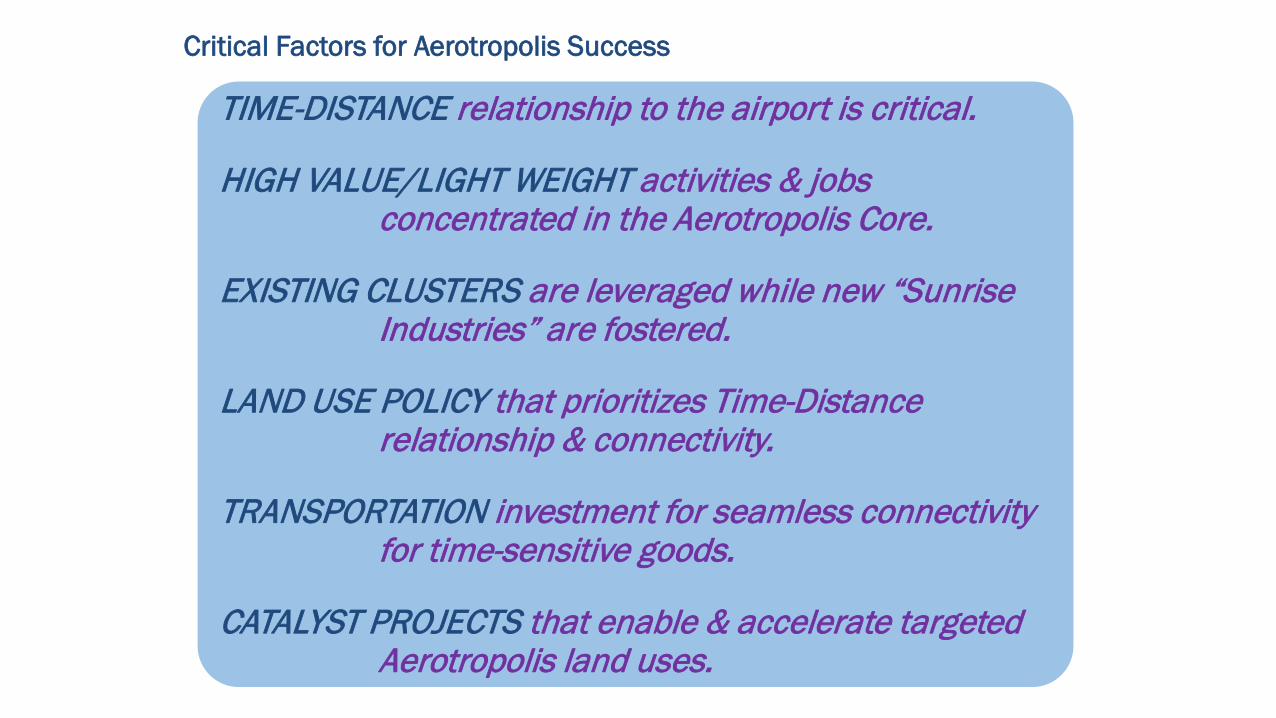

TIME-DISTANCE relationship to the airport is critical.

HIGH VALUE/LIGHT WEIGHT activities & jobs concentrated in the Aerotropolis Core.

EXISTING CLUSTERS are leveraged while new “Sunrise Industries” are fostered.

LAND USE POLICY that prioritizes Time-Distance relationship & connectivity.

TRANSPORTATION investment for seamless connectivity for time-sensitive goods.

CATALYST PROJECTS that enable & accelerate targeted Aerotropolis land uses.

Critical Factors for Aerotropolis Success

Employment Projection-Driven Land Demand Forecasting

Targeted Economic

Sectors Allocated into

Statistical Categories

Building Typology Statistics &

Densities & Site Coverage

20,868,890 m2

Gross Floor Area projected

AGRICULTUREAgri- Business & Food processing 100%

MININGNatural Resources 100%

MANUFACTURINGAerospace Manufacturing & Aviation 40%Manufacturing & High-Tech 60%

ELECTRICITYNatural Resources & Energy 100%

TRADERetail 75%Tourism & Culture 25%

TRANSPORTLogistics & Distribution 100%

FINANCEProfessional Services 90%Public Administration 10%

COMMUNITY SERVICESEducation & Skills Training 25%Health & Life Sciences 75%

2040Baseline

Employment Projection

2040Aerotropolis

Multiplier Scenarios

87.25 km2

land demand projected

AEROTROPOLIS ECONOMIC DEVELOPMENT WORK STREAM

AEROTROPOLIS LAND USE PLANNING WORK STREAM

ECONOMIC CLUSTER STRATEGY

TIME-DISTANCE STRATEGY

LAND USE ALLOCATION

CATALYST PROJECT STRATEGY

Drive-Time Distance by Economic Activity

VALUE-ADD

MANUFACTURINGADVANCED

MANUFACTURING

ICT REPAIR

RENEWABLE ENERGY

0 - 5 Minutes

5 -10 Minutes10 - 15 Minutes

15+ Minutes

FAST-CYCLE LOGISTICS

BIO - LIFE SCIENCES &

DIAGNOSTICS

AEROSPACE

AVIATION

BIO-LOGISTICS

RETAIL FULFILLMENT

SPORTS & RECREATION

ARTISAN TRAINING

LOGISTICS

PROFESSIONALSERVICES

AGRI-BUSINESS

RETAIL FULFILLMENT

R & D

EDUCATION & SKILLS TRAINING

TOURISM& CULTURE

R & D

INTEGRATOR / CEP

Education Skills & Training

Public Admin City

Aviation Industry College

TVET College

RetailTourism &

Culture

Heavy Equipment

AuctionSports City

Int’l Conference

Center

Outlet MallAuto-Mall of Africa

Hotel & Dining District

SA Trade Mart

Aerospace & Advanced

Manufacturing

Denel Aerospace

Manufacturing Hub

Recycling & Renewable Energy Hub

Human Settlements Factory-Built Housing Hub

Air Cargo Logistics &

DistributionBio-Life Sciences

ICT R&D

Value-Add Food

Processing Hub

Medical City Africa

Digital City Business

Park

Discovery R&D

Business Park

Air Cargo Logistics

Hub

Post Office e-commerce

Integrator

Temperature-Controlled Cold Chain

Village

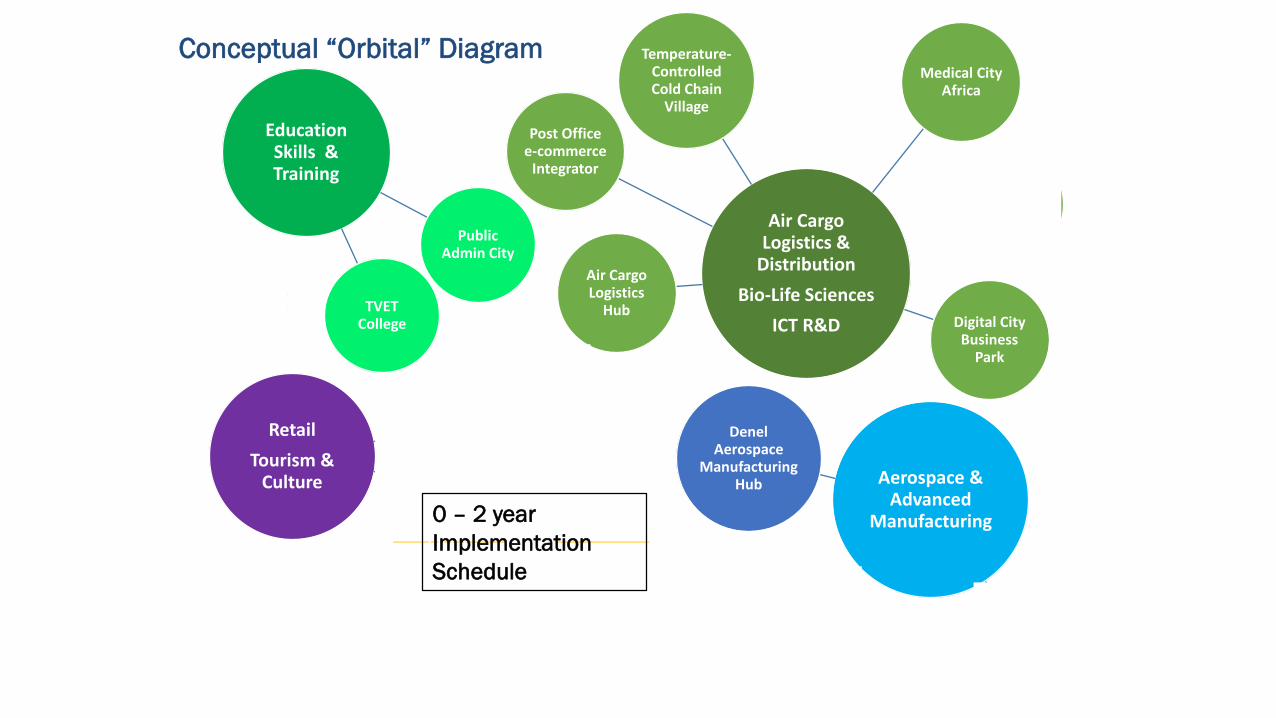

Conceptual “Orbital” Diagram

0 – 2 year ImplementationSchedule

Education Skills & Training

Public Admin City

Aviation Industry College

TVET College

RetailTourism &

Culture

Heavy Equipment

AuctionSports City

Int’l Conference

Center

Outlet MallAuto-Mall of Africa

Hotel & Dining District

SA Trade Mart

Aerospace & Advanced

Manufacturing

Denel Aerospace

Manufacturing Hub

Recycling & Renewable Energy Hub

Human Settlements Factory-Built Housing Hub

Air Cargo Logistics &

DistributionBio-Life Sciences

ICT R&D

Value-Add Food

Processing Hub

Medical City Africa

Digital City Business

Park

Discovery R&D

Business Park

Air Cargo Logistics

Hub

Post Office e-commerce

Integrator

Temperature-Controlled Cold Chain

Village

Conceptual “Orbital” Diagram

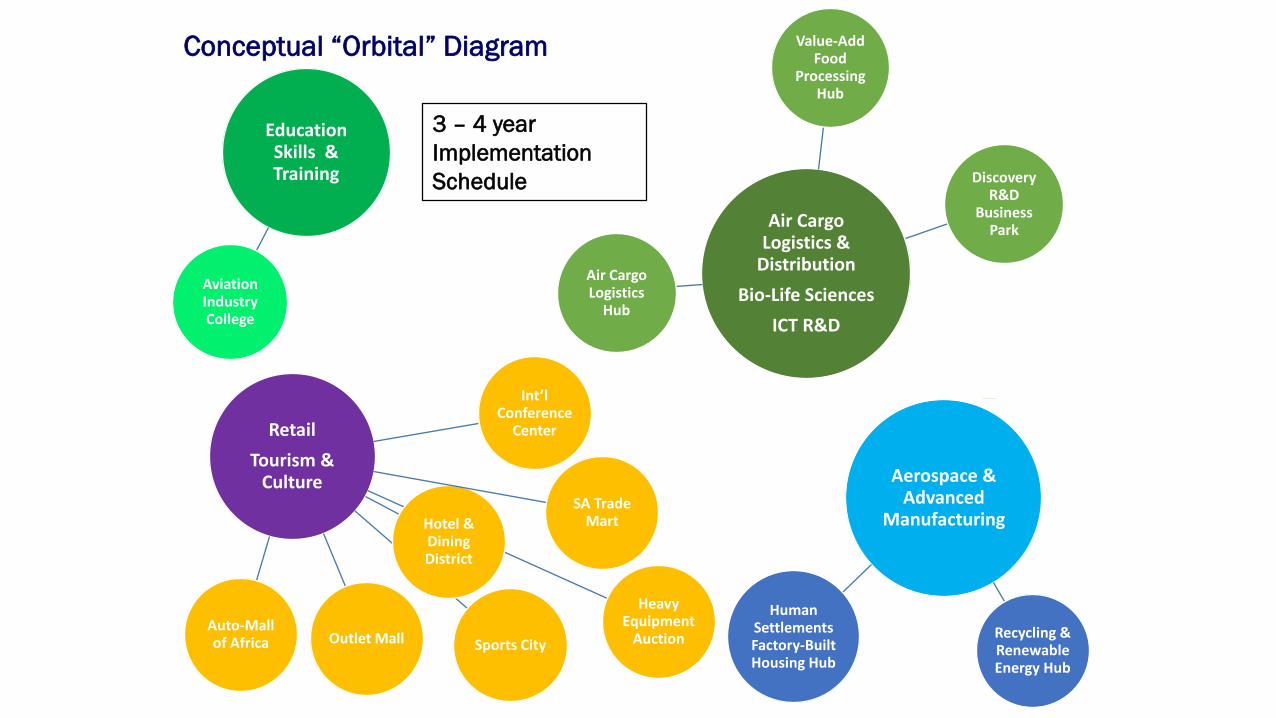

3 – 4 year ImplementationSchedule

Education Skills & Training

Public Admin City

Aviation Industry College

TVET College

RetailTourism &

Culture

Heavy Equipment

AuctionSports City

Int’l Conference

Center

Outlet MallAuto-Mall of Africa

Hotel & Dining District

SA Trade Mart

Aerospace & Advanced

Manufacturing

Denel Aerospace

Manufacturing Hub

Recycling & Renewable Energy Hub

Human Settlements Factory-Built Housing Hub

Air Cargo Logistics &

DistributionBio-Life Sciences

ICT R&D

Value-Add Food

Processing Hub

Medical City Africa

Digital City Business

Park

Discovery R&D

Business Park

Air Cargo Logistics

Hub

Post Office e-commerce

Integrator

Temperature-Controlled Cold Chain

Village

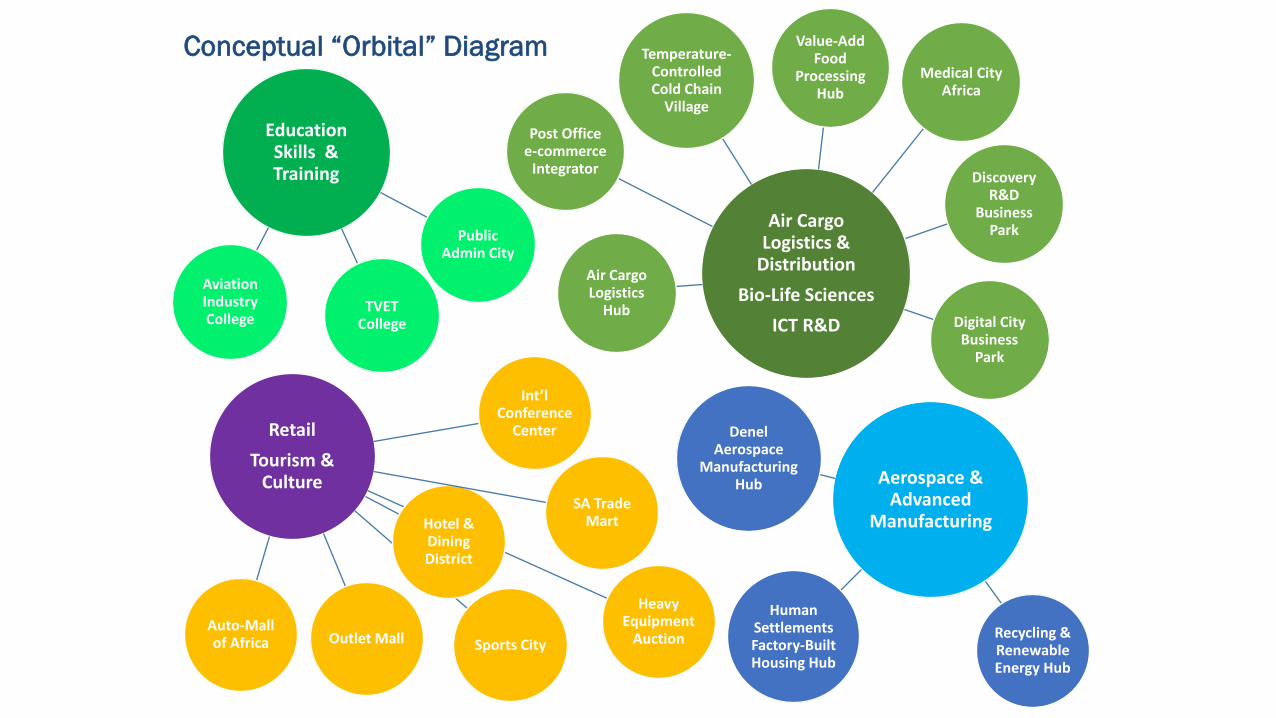

Conceptual “Orbital” Diagram

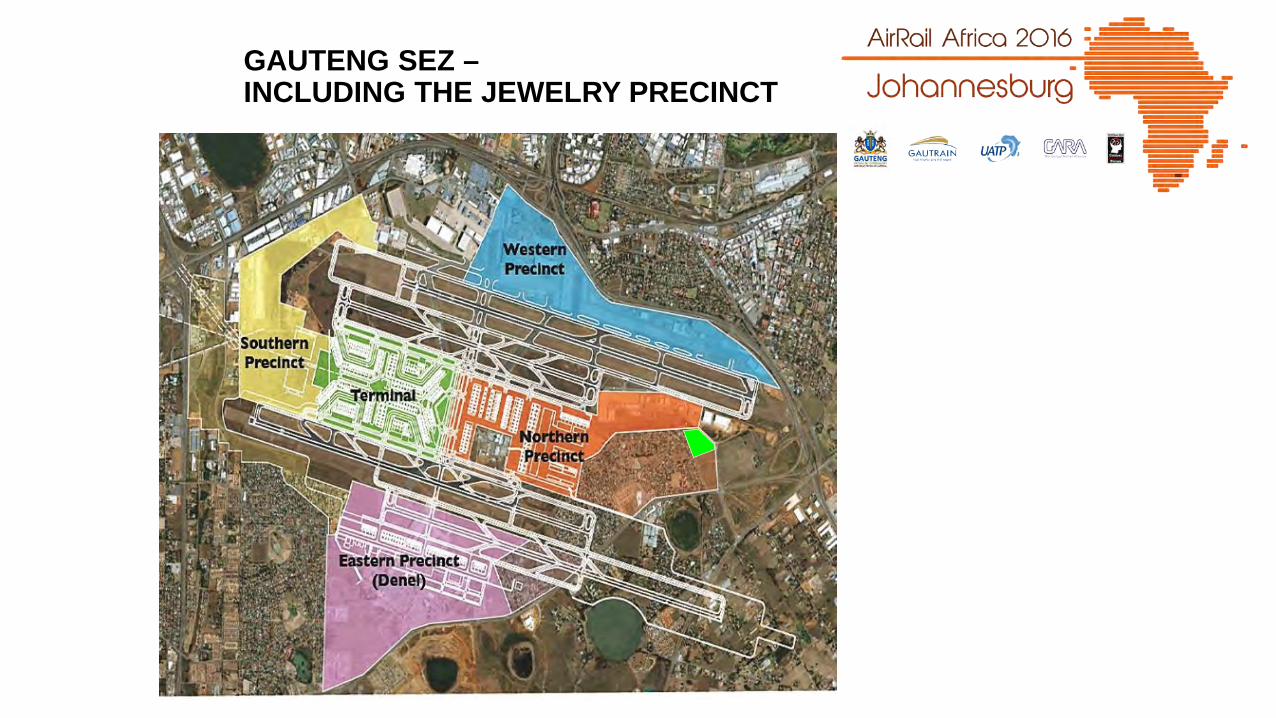

GAUTENG SEZ –INCLUDING THE JEWELRY PRECINCT

Advanced Manufacturing

3D Printing

Smart Textiles & Fabrics

Sunrise Industries

Opportunity: Foster a Nanotech manufacturing sectorthrough R&D-Commercialisation support, with afocus on the export of products by air.

Nanotechnology

Opportunity: Encourage the commercialisation of 3D Printingbreakthroughs for use in the Aerospace,advanced manufacturing, & mining sectors.

Opportunity: Support incorporation of Smart Fabrics into SAtextile sector through R&D and support for start-up advanced manufacturing businesses.

ICT

Big Data

Cloud-Based Computing

“Internet of Things”

Opportunity: Support R&D-Commercialisation of “Big Data”computing with a focus on Social and EconomicDevelopment applications in emerging markets.

Opportunity: Foster a low-cost mobile-computing environmentand R&D-Commercialisation ecosystem. PositionEkurhuleni as home for South Africa’s datacentres.

Opportunity: Position Ekurhuleni as the “Silicon Valley ofAfrica” for R&D-Commercialisation of internet-enabled devices for emerging markets.

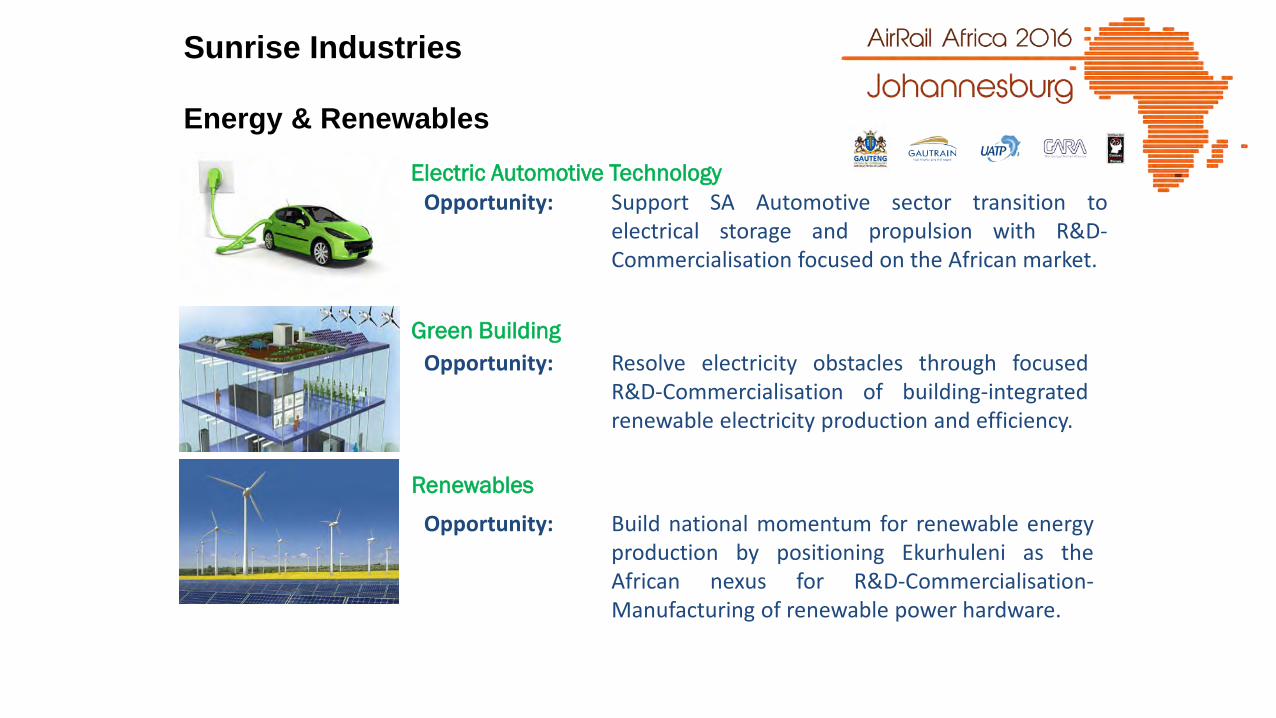

Sunrise Industries

Energy & RenewablesElectric Automotive Technology

Green Building

Renewables

Opportunity: Support SA Automotive sector transition toelectrical storage and propulsion with R&D-Commercialisation focused on the African market.

Opportunity: Resolve electricity obstacles through focusedR&D-Commercialisation of building-integratedrenewable electricity production and efficiency.

Opportunity: Build national momentum for renewable energyproduction by positioning Ekurhuleni as theAfrican nexus for R&D-Commercialisation-Manufacturing of renewable power hardware.

Sunrise Industries

Life Sciences & HealthcarePersonalised Medicine

Innovative Agri-Business

Sunrise Industries

Opportunity: Support R&D-Commercialisation of individualisedgene therapy as part of positioning Ekurhuleni asthe Medical Tourism hub for Sub-Saharan Africa.

Opportunity: Leverage innovations in agronomy, cropsciences, and food processing to evolve the Agri-Business sector and create new export products.

ENABLING PROJECTS

• Urban Regeneration Projects:• Rhodesfield Master Plan;• Tembisa Urban Regeneration project;• Kempton Park Urban Regeneration Project; and• Germiston Precinct Urban Regeneration Project.

ENABLING PROJECTS

• Development (Mega) Projects:• Development of the Gibela Prasa Rolling Stock

Manufacturing Facility;• Development of the Tambo Springs Intermodal

Facility; and• Redevelopment of the Sentrarand Inland Port.

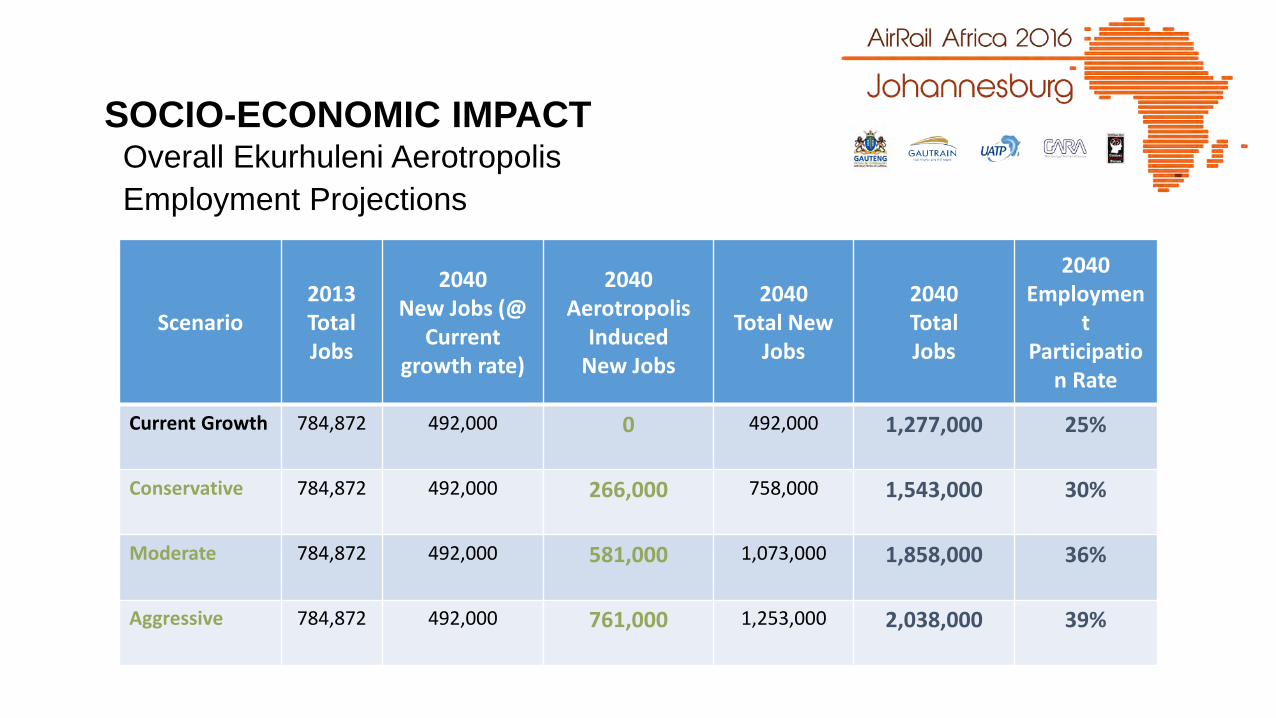

SOCIO-ECONOMIC IMPACTOverall Ekurhuleni Aerotropolis Employment Projections

+ ++ =

Scenario2013Total Jobs

2040New Jobs (@

Current growth rate)

2040 Aerotropolis

InducedNew Jobs

2040Total New

Jobs

2040TotalJobs

2040Employmen

t Participatio

n Rate

Current Growth 784,872 492,000 0 492,000 1,277,000 25%

Conservative 784,872 492,000 266,000 758,000 1,543,000 30%

Moderate 784,872 492,000 581,000 1,073,000 1,858,000 36%

Aggressive 784,872 492,000 761,000 1,253,000 2,038,000 39%

SOCIO-ECONOMIC IMPACTOverall Ekurhuleni Aerotropolis Employment Projections

784,872 784,872 784,872 784,872

492,000 492,000 492,000 492,000

266,000581,000 761,000

0

500000

1000000

1500000

2000000

2500000

Status Quo Conservative Moderate Aggressive

2013 Total Jobs 2040 Status Quo New Jobs 2040 Aerotropolis-Induced New Jobs

1,277,0001,543,000

1,858,0002,038,000

SOCIO-ECONOMIC IMPACTProject Socio-economic Effects

8,1 billion ZAR per annum*

Catalyst project effect on Gauteng GDP

(+0.67% annual contribution to the Gauteng GDP)*Estimated Gauteng GDP (current 2013 prices)

E: The Gautrain Rapid Rail Link Project(A case for Public Transport)

Implementation Process• Four pillars

• Political will & commitment• Viable project (base case design)

• Technical• Financial• Legal/Institutional

• Funding (for Infrastructure & Operations)• Government’s portion• Private Sector’s portion

• Community acceptance & buy-in• Socio-economic benefits• Power of expropriation

F: Objectives of the Gautrain Project

The Gautrain will promotePublic Transport

SMME & BBBEE DevelopmentTourism

Business development

The project stimulatesEconomic growth

Local & Foreign Investment New development

Job creation

Design toRestructure urban areasReduce travel distances,

time and costImprove city sustainability

Gautrain: More than Just Another Transport Project

G: PPP Requirements

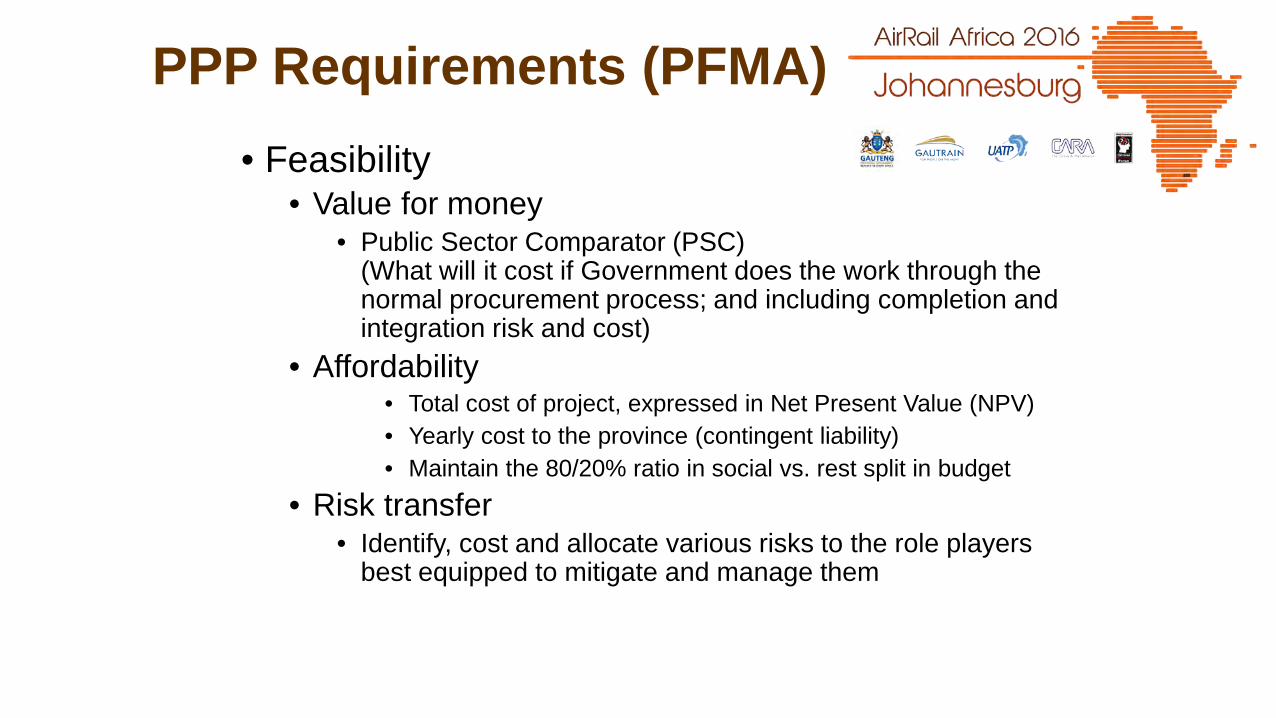

PPP Requirements (PFMA)• Feasibility

• Value for money • Public Sector Comparator (PSC)

(What will it cost if Government does the work through the normal procurement process; and including completion and integration risk and cost)

• Affordability• Total cost of project, expressed in Net Present Value (NPV)• Yearly cost to the province (contingent liability)• Maintain the 80/20% ratio in social vs. rest split in budget

• Risk transfer • Identify, cost and allocate various risks to the role players

best equipped to mitigate and manage them

PPP Advantages (1)• What each party brings to a PPP

Legislation

Subsidies &Guarantees

Land

Rights of wayLong term vision

Operation &Maintenance

Design &Build innovation

Capital

Access to the market

Financing

Users

Public

SectorConcession

(SPV)

Private

Sector

Revenue

PPP Advantages (2)• What each party gets from a PPP

Social function

PeopleMobility

Taxes

Economic development

Associatedbenefits

Environment protectionTime/cost savingService Quality

Concession

(SPV)

Private

Sector

Users

Public

Sector

Design & Construction Contract

OperationContract

Servicing of Debt

Incomes

Profit

H: Process sequence

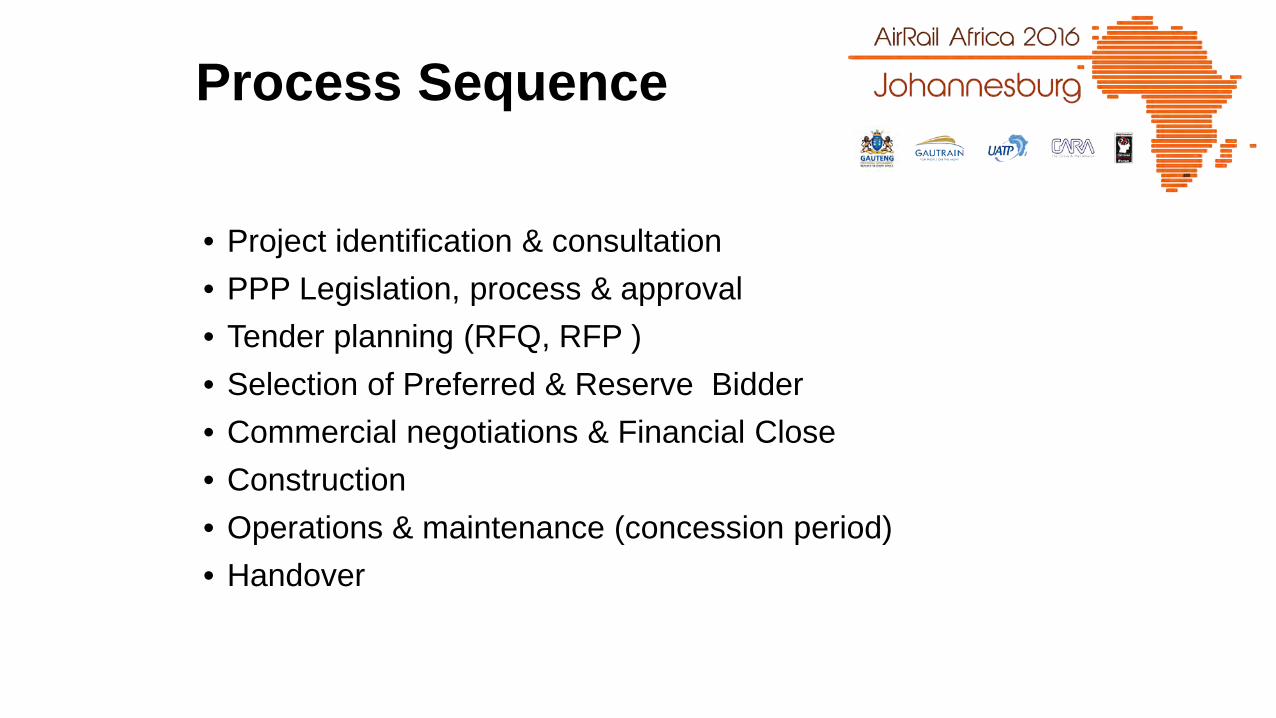

Process Sequence

• Project identification & consultation• PPP Legislation, process & approval• Tender planning (RFQ, RFP )• Selection of Preferred & Reserve Bidder• Commercial negotiations & Financial Close• Construction• Operations & maintenance (concession period)• Handover

Parallel Processes

• Decision making & authorisation (Governance)• Legal processes (Litigation on content & process)• Continuous communication, consultation & public relations• Environmental (EIA) process • Third party involvement, co-operation and buy-in• Socio-economic Development (SED) requirements• External pressures• Land requirements (GTIA process)• Continuous funding – for multiple MTEF periods

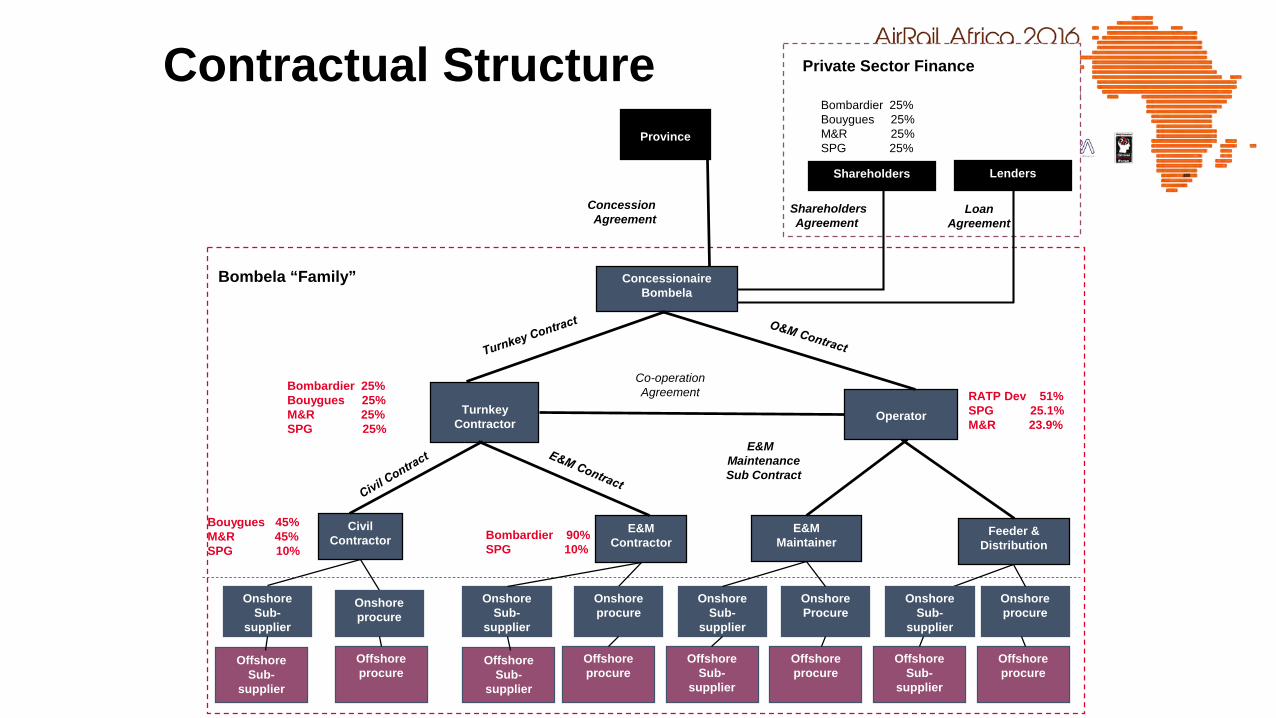

I: The Deal

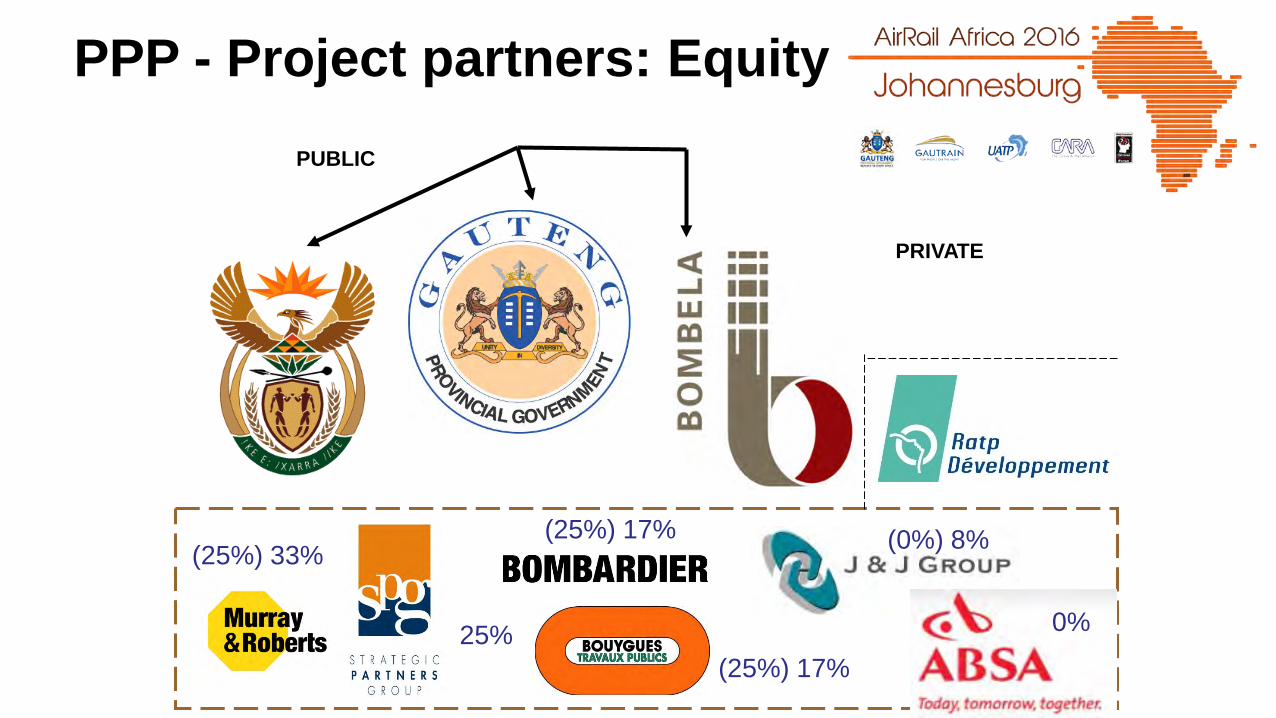

PPP - Project partners: EquityPUBLIC

PRIVATE

(25%) 33%

25%(25%) 17%

(25%) 17% (0%) 8%

0%

Concessionaire Bombela

Turnkey Contractor

Civil Contractor

E&M Contractor

E&MMaintainer

Operator

Contractual Structure

Lenders

Province

ShareholdersAgreement

LoanAgreement

Concession Agreement

E&M MaintenanceSub Contract

Bombardier 90%SPG 10%

RATP Dev 51%SPG 25.1%M&R 23.9%

Bombardier 25%Bouygues 25%M&R 25%SPG 25%

Private Sector Finance

Bombela “Family”

Onshore Sub-

supplier

OffshoreSub-

supplier

Bombardier 25%Bouygues 25%M&R 25%SPG 25%

Shareholders

Bouygues 45%M&R 45%SPG 10%

BombardierSPG

Onshore Sub-

supplier

OffshoreSub-

supplier

Onshore procure

Offshoreprocure

Feeder &Distribution

Co-operation Agreement

Onshore Sub-

supplier

Offshoreprocure

Offshoreprocure

OffshoreSub-

supplier

OffshoreSub-

supplier

Onshore procure

Onshore procure

Onshore Procure

Onshore Sub-

supplier

Offshoreprocure

Complex problems have simple, easy to understand, wrong answers.

No. 4 Grossman’s Misquote

J: Funding

Funding

• Gautrain has 5 sources of funding• DoRA (Division of Revenue Act) money from central

government via the Department of Transport (only for construction - CAPEX)

• MTEF (Medium Term Expenditure Framework) from Gauteng Provincial Government

• Private Sector Equity• Private Sector Borrowing• Provincial Borrowing

Project Financing

MTEF26.1%

DoRA44.2%

Equity1.8%

Private Debt9.5% Provincial

borrowing18.4%

K: Socio-Economic Development

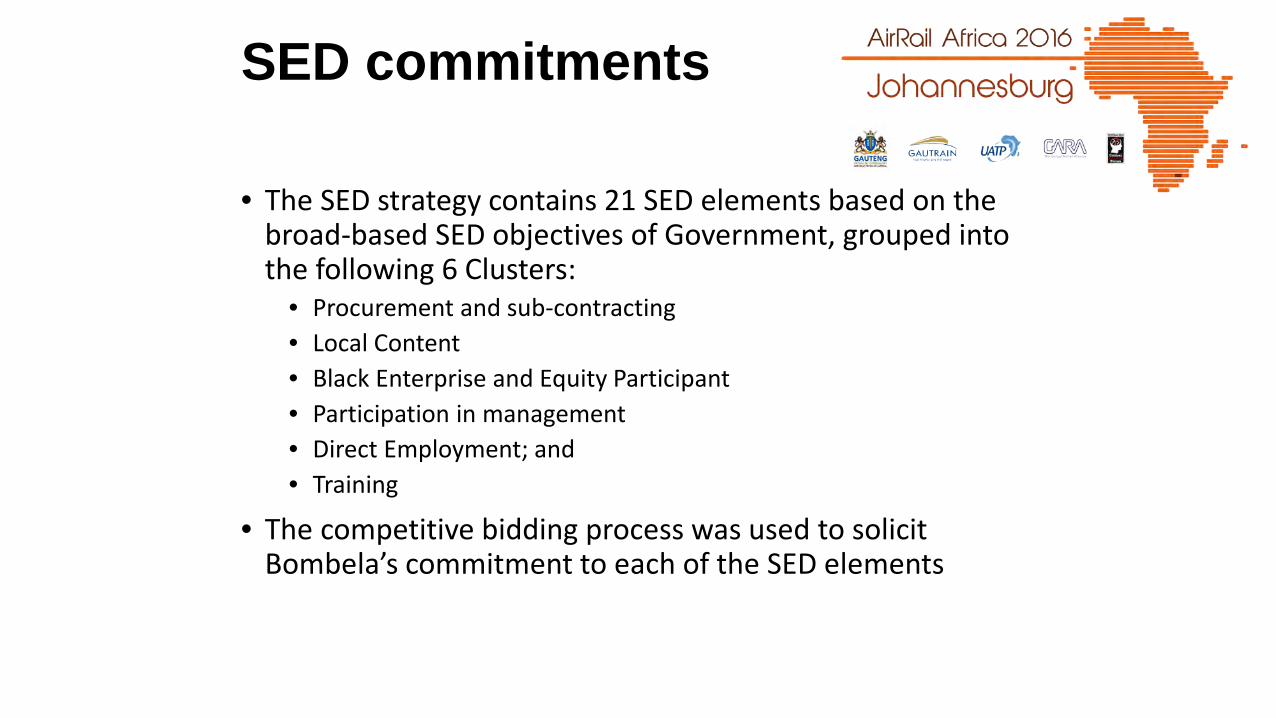

SED commitments

• The SED strategy contains 21 SED elements based on the broad-based SED objectives of Government, grouped into the following 6 Clusters:

• Procurement and sub-contracting• Local Content• Black Enterprise and Equity Participant• Participation in management• Direct Employment; and• Training

• The competitive bidding process was used to solicit Bombela’s commitment to each of the SED elements

166%

98%

117%

127%

225%

215%

411%

397%

266%

216%

124%

186%

176%

190%

180%

411%

197%

223%

179%

119%

100%

0% 50% 100% 150% 200% 250% 300% 350% 400% 450%

EEP08(b):Women Learners employed & mentored

EEP08(a): Women trained & mentored

EEP06:Expenditure on Human Resource Development

EEP05:People with Disabilities employed

EEP04:Women employed

EEP03:HDIs employed

EEP07:HDIs in Occupational Level C

EEP02:Women in Management Positions

EEP01:HDIs in Management Positions

SED13:Procurement from, or Sub-contracting to SPG

SED12:Expenditure by SPG on Plant & and Equipment

SED11:HDI staff seconded by SPG

SED10:Procurement of RSA Plant & Equipment

SED09:Procurement of RSA Materials

SED08:Employment of Local People

SED06:Procurement & sub-contracting to SMMEs

SED05:Procurement & sub-contracting to New BEE

SED04:Sub-contracting to BEE

SED03:Procurement from BEEs/ Black Persons

SED02:Shares held by Black Women

SED01:Shares held by BEEs/ Black Persons

Verified % Compliance

L: Gautrain Operations

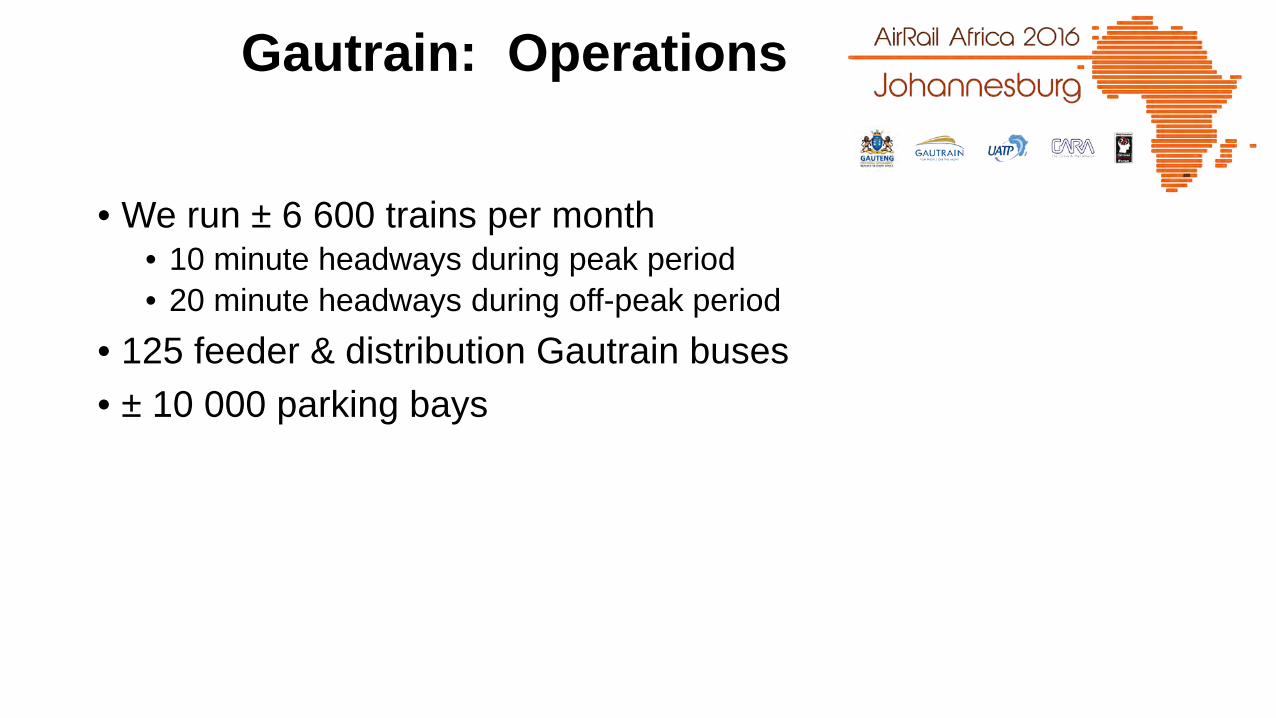

Gautrain: Operations

• We run ± 6 600 trains per month• 10 minute headways during peak period• 20 minute headways during off-peak period

• 125 feeder & distribution Gautrain buses• ± 10 000 parking bays

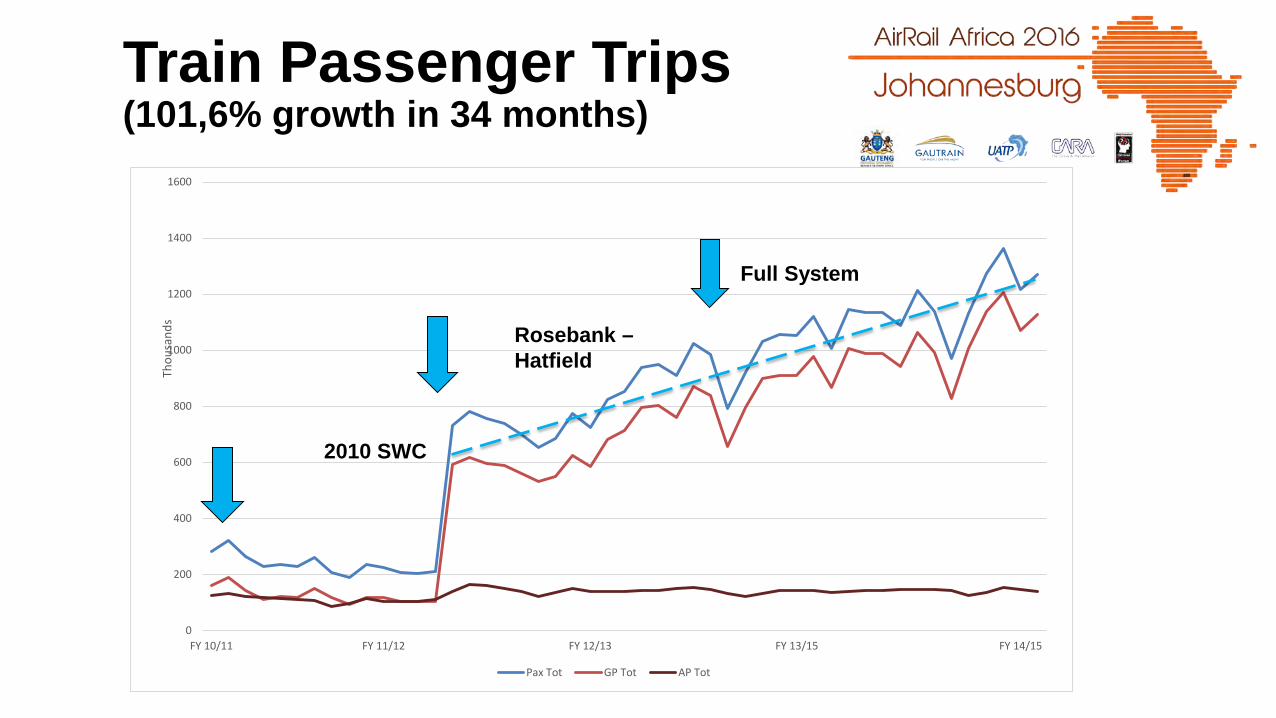

Train Passenger Trips(101,6% growth in 34 months)

Full System

Rosebank -Hatfield

2010 SWC

0

200

400

600

800

1000

1200

1400

1600

FY 10/11 FY 11/12 FY 12/13 FY 13/15 FY 14/15

Thou

sand

s

Pax Tot GP Tot AP Tot

2010 SWC

Rosebank –Hatfield

Full System

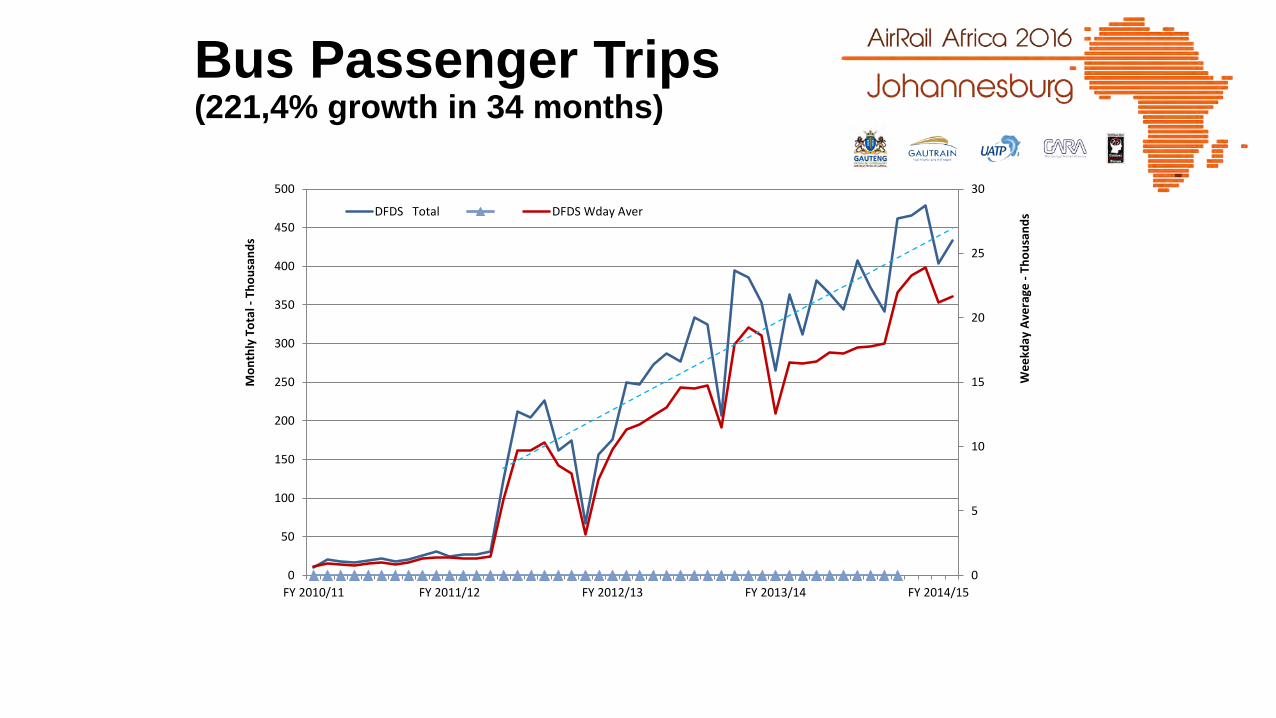

Bus Passenger Trips(221,4% growth in 34 months)

0

5

10

15

20

25

30

0

50

100

150

200

250

300

350

400

450

500

FY 2010/11 FY 2011/12 FY 2012/13 FY 2013/14 FY 2014/15

Wee

kday

Ave

rage

-Th

ousa

nds

Mon

thly

Tot

al -

Thou

sand

s

DFDS Total DFDS Wday Aver

Train Service Levels• Train operational performance in the review period

was above its respective norms of 98.5% and 94%TRAIN SERVICE AVAILABILTY / PUNCTUALITY

Q3 (FY 2013/14) Q4 (FY 2013/14) Q1 (FY 2014/15)

Oct Nov Dec Jan Feb Mar** Apr MaySCHEDULED TRIPS 6661 6301 5953 6424 5946 6389 6103 6305

ACTUAL TRIPS 6639 6263 5921 6413 5930 6353 6090 6303TRIPS CANCELLED 18 31 25 9 14 35 16 2

EARLY STARTS 4 7 7 2 2 1 4 0LATE ARRIVALS 86 57 59 88 89 84 64 65

SERVICE AVAILABILITY* 99.61% 99.29% 99.34% 99.80% 99.70% 99.42% 99.72% 99.97%AVAILABILITY NORM 98.50% 98.50% 98.50% 98.50% 98.50% 98.50% 98.50% 98.50%

SERVICE PUNCTUALITY 98.64% 98.98% 98.89% 98.60% 98.47% 98.66% 98.88% 98.97%PUNCTUALITY NORM 94.00% 94.00% 94.00% 94.00% 94.00% 94.00% 94.00% 94.00%

* Early Starts ( > 190 seconds) not regarded as "available"

Note - Punctuality: Actual Trains operated ≤ 180 seconds at arrival Terminal Station (Destination Station)

M: Gautrain Extensions

HATFIELDPRETORIA

CENTURION

MIDRAND

SANDTON

MARLBORO

PARK

WESTGATE

ROSEBANK

Ultimately four Services:

RED: North – South ServiceBLUE: Naledi – Mamelodi ServiceGREEN: Honeydew – Boksburg ServicePURPLE: Sandton – ORTIA Service

MAMELODI

TSHWANE EAST

IRENE

SUNNINGHILL

FOURWAYS

ROODEPOORT

NALEDI

COSMO

RUIMSIG

BLUE HILLS

SAMRAND

LAKEVIEWRHODESFIELD

BOKSBURG

RANDBURGHONEYDEW

EAST RAND MALL

OR TAMBO

LANSERIA

Environmental Assessment

117

• CoT • 6 new stations

• Incl Samrand

• EMM• 3 new stations

• Incl Rhodesfield 2

• CoJ• 10 new stations

• Incl Modderfontein, Sandton 2

19 New Stations

SANDTON

MARLBORO

MIDRAND

CENTURION

HATFIELD

Metrorail

ROSEBANK

PARK

PRETORIA

RHODESFIELD

O.R. TAMBO

SAMRAND

IRENE

TSHWANE EAST

HAZELDEAN

MAMELODI

OLIEVENHOUTSBOSCH

SUNNINGHILL

FOURWAYS

COSMO

LITTLE FALLS

ROODEPOORT

JABULANI

RANDBURG

LANSERIA

EAST RAND MALL

BOKSBURG

SANDTON 2

LEGEND

North – South Commuter East – West Commuter

Airport

MODDERFONTEIN

Train Operations

N: Closure

The Seven Stages of a PPP Project

• Enthusiasm• Promises & Programmes• Disillusionment• Panic• Hunt for the guilty• Punishment of the innocent• Reward for those who had nothing to do with it

Whatever it is that hits the fan -will not be evenly distributed.

No. 2 Law of Probable Dispersal

Thank You

“The philosophers have only interpreted the world, the point

however is to change it”Karl Marx

“The Future is not for the faint hearted.”

R Reagan