Embed Size (px)

Citation preview

Institutional PresentationItaú Unibanco Holding S.A.

2Q20

ITUB

NYSELISTED LEVEL 1

BM&FBOVESPACDP

2Q20

This presentation contains forward-looking statements regarding Itaú Unibanco Holding, its subsidiaries and affiliates - anticipated synergies, growth plans, projected results and future strategies. Although theseforward-looking statements reflect management’s good faith beliefs, they involve known and unknown risks and uncertainties that may cause the Company’s actual results or outcomes to be materially different fromthose anticipated and discussed herein. These statements are not guarantees of future performance. These risks and uncertainties include, but are not limited to our ability to realize the amount of the projected synergiesand the timetable projected, as well as economic, competitive, governmental and technological factors affecting Itaú Unibanco Holding’s operations, markets, products and prices, and other factors detailed in ItaúUnibanco Holding’s filings with the Securities and Exchange Commission which readers are urged to read carefully in assessing the forward-looking statements contained herein. Itaú Unibanco Holding undertakes in dutyto update any of the projections contained herein. This presentation contains managerial numbers that may be different from those presented in our financial statements. The calculation methodology for thosemanagerial numbers is presented in Itaú Unibanco Holding’s quarterly earnings report. To obtain further information on factors that may give rise to results different from those forecast by Itaú Unibanco Holding, pleaseconsult the reports filed with the Brazilian Securities and Exchange Commission (Comissão de Valores Mobiliários - CVM) and with the U.S. Securities and Exchange Commission (SEC), including Itaú Unibanco Holding’smost recent Annual Report on Form 20F.

AgendaCorporate

profileStrategicagenda

Corporategovernance

Our businesses

0413

3152

Economiccontext

Capital andrisk management

6276

Financial highlights 81

Additionalinformation92

Corporate profile

4

Corporate profile

About us?

Market Value³US$45.9 bn

Total assets3

R$2,075.1 bnCredit portfolio3

R$811.3 bnROE4

13.5%Net income4

R$4.2 bnTier I Capital 3

12.1%

Universal bank | 95 years of history | largest bank in Latin America¹

(1) Largest bank in market value; (2) 2019 Interbrand Ranking ; (3) June 2020 (4) In 2Q20. (5) April 2020.

Brazil’s most valuable² brand

R$33.5 billion

Approximately

We are present in 18 countries

434 kdirect shareholders

4.5 kbranches and PABs

97 kemployees

56 million5

Retail clients

46 kATMs

Key

Multiple Bank1 Corporate & Investment Banking 2 Asset Management 3 Private BankingOther operations

5

Rest of the World

Argentina

Brazil

Chile

ColombiaMexicoPanamaParaguayPeru

Uruguay

Latin America

1

1

GermanBahamasCaymanSpainUnited StatesFrancePortugalUnited KingdomSwitzerlandReino UnidoSuíça

1

1

1

1

1 2

3

2 3

1

1 2 3

1

3

Corporate profile

What do we do?

Personal

Cards

Working capital

Real estate

Micro credit

Vehicles

Rural

Current accounts

Cards and acquiring

Consórcio

Brokerage

Premium Bonds

Payment means

Capital markets

Life

Homeowners insurance

Auto

Dental

Card protection

Travel

Healthcare

Smartphone protection

Investments Guarantee insurance

Payroll loans

Imports/Exports

Pension plans

Full offering of products and services | diversified client base | solid brand

ServicesCredit InsuranceA completephysical and digital bank

The Retail Bank includes retail clients, high-income clients and very small and small businesses, in addition to products and services for non-account holders.

The Wholesale Bank is responsible for high net

worth clients (private banking), the units in Latin

America, banking for middle market and large

companies and corporations through Itaú

BBA, the unit responsible for corporate clients and

for its role as an investment bank.

Open platformInvestment and insurance products sold on open platforms.

$

$

$

$

$

$

$$

$

Main brands and commercial partners

Other productsOther products Other products...... ...

6

Corporate profile

How have we evolved?

First stepsCasa Moreira Salles opens in 1924, and Banco Central de Créditoin 1943.

Paths to growthMarked by mergers, acquisitions and business alliances that enabled the growth and consolidation of both institutions.

An historic mergerIn 2008, Itaú andUnibanco united to create Brazil’s largest private bank.

Focus onLatin AmericaOur international presence has evolved year after year. Today, Itaú is present in 18 countries.

A bank with a purposeWe believe that people have the power to transform the world, and that the bank can promote this transformation.

1929 1945 1983 1985 1990 2006 2016 2020

Adaptable culture | innovation | transparency in business

1930 1950 1960 1980 1984 2002 2014 2020

We have witnessed important changes around the world...

NY Stock Exchange crisis

First overseas branch of Itaú

First version of Windows appears

First Internet providers

World War IIends

Itaú on the NY Stock Exchange.

First checks with client’s name

First in-branch calculators

FirstATMs

Mobile Banking in Brazil

First debit and credit cards

Banking automation begins

... and in Brazil

Britain decides to leave the European Union (Brexit)

7

World Health Organization declares coronavirus pandemic

Fintechsstart to gain strength

Central Bank launches PIX

To change leagues and compare ourselves with the world’s best companies in client satisfaction

Corporate profile

What are we seeking?

Our WayOur culture

PurposeOur Promoting people’s power

of transformation

Simple. Always

People mean everything to us

Ethics are non-negotiable

It’s only good for us if it’s good for the client

Passionate about performance

The best argument is the one that matters

We thinkand act like owners

Positive impact

Strategic agenda

Commitments to a Responsible investment

Financing for sectors with a

positive impact

Inclusion and entrepreneurship

Financial citizenship

Transparency in communication

Ethics in relationships and

business

Inclusive management

Responsible management

8

Clientcentricity

Our ambition is to be one of the world's best companies in client satisfaction.

Digital Transformation

We must have the best products, in less time and higher flexibility.

People

Our business is providing services and that is why people is a vital issue. We invest to provide a more open and diverse environment.

Efficiency

Price is of paramount importance customer satisfaction. We can only have competitive prices if we are efficient.

Carta Empresarial pelo Direitos Humanos e pela Promoção do Trabalho

Decente

Red Mujer Emprendedora

Corporate profile

A responsible bank

Financing for sectors with a positive impactTo increase our financing and services in those sectors.

Responsible investmentTo expand our offering and distribution of products and services for an economy that is more responsible and with a positive impact.

Inclusion and entrepreneurshipTo increase financial inclusion for entrepreneurs.

Financial citizenshipTo promote client satisfaction, as well as their financial lives.

Transparency in the communicationTo strengthen our transparency, demonstrating the value created for our stakeholders.

Ethics in relationships and businessEthics are non-negotiable. Promote the creation of an intimate and ethical financial ecosystem.

Inclusive managementTo enhance our employees’ experience and to foster a working environment that is diverse, inclusive and healthy.

Responsible managementTo improve the performance of our operations and to foster sustainable practices across our supply chain.

Our commitments to apositive impact

Main pacts, initiatives and voluntary commitmentsWe believe that people have the power to transform the world, and that a bank can promote this transformation.

Ethics is present in our business and results in transparency, respect and honesty in our relationships with our stakeholders, in the quality of our products and services and in our concern with financial performance and socioenvironmental responsibility.

9

Respect and diversity

Sustainable development

Responsible banking

Transparency in the communication

Climate change

Ethics and integrity

Contribuição Empresarial para a Promoção da Economia Verde e Inclusiva

Corporate profile

A responsible bank | ESG

10

ESG aspects have been integrated into the Bank's management for over two decades

We reported 12 of the 14 indicators of the Sustainability Accounting Standards Board in our Integrated Annual Report 2019.

We adopted the SASB indicatorsWe follow the main global framework of the climatechange agenda - Task Force on Climate-relatedFinancial Disclosures.

100% adherent to the TCFD until 2022ESG management and transparency practices

Environmental conservation and development of a bioeconomy

Investment in sustainable infrastructure

Guarantee of the basic rights for the population

Together with the banks Bradesco and Santander, we announced 10concrete measures targeting 3 areas considered top priority for the region:

The three banks are working together on specifying the initiatives and setting clear objectives, goals and metrics.

1999

Dow Jones Sustainability

Index(DJSI)

2008

Principles for Responsible Investment

(PRI)

2017

Bloomberg's Gender

Equality Index

2005

B3’s Corporate Sustainability

Index(ISE)

2004

Equator Principles

2019

Principles for Banking

Responsibility(UN)

2018

Sustainable Development

Goals(SDG)

2009

Global Reporting Initiative

Standards (GRI)

Integrated plan to promote sustainable development of the Amazon

2020

Since 2012We offset 100%

of our direct emissions (scope 1)1

Since 2017We offset 100%

of our indirect emissions (scope 2)2

2010

Carbon Disclosure

Project (CDP)

(1) Scope 1: Direct greenhouse gas (GHG) emissions from sources that are owned or controlled by Itaú Unibanco. (2) Scope 2: Indirect GHG emissions from the acquisition of electricity that is consumed by Itaú Unibanco.

Corporate profile

2020 | Support for clients during the crisis

11

R$1.6 billionin emergency credit for payrollsto finance salaries of more than 660 thousand employees in the last months

1st private bankto offer the Pronampe²credit lineR$ 3.6 billion - all available volume –for about 36 thousand very small and small companies

Participation in government initiatives

R$2.9 billion subscribed by Itaú Unibanco in the initiative between CCEE³ and banksof a total of R$ 15.2 billion, to support energy generators, distributors and concessionaires

(1) Includes emergency credit for payroll financing and the Pronampe² credit line; (2) Pronampe is a national support program for very small and small companies; (3) Chamber of Commercialization of Electric Energy

R$13.2 billion

middle-market companies

large companies

R$52.4billion

very small and small companies

R$17.1¹billion

individualsR$14.1billion

New credits were grantedMarch 16 to July 17, 2020

R$96.8 billionThis unprecedented initiative aims to address indebtedness using a structured approach, providingclients with some respite and ensuring that they enjoy sustainable conditions over time.The range of customized solutions includes grace periods, extended loan terms and additional credit offer.

Term extension of up to6 years for individuals

5 years for very small and small companies

Grace period of up 120 days for individuals

180 days for very small and small companies

Better interest rate conditions

~1.8 millionindividuals

It has already benefited:

~200 thousandvery small and small companies

R$52 billion in loan portfolio reprofilingIn June 30, 2020

Corporate profile

2020 | Todos pela saúde

12

From R$1.2 billion donated to date, more than $1 billion has already been allocated to 4 areas of activity.Next, check out some of the main achievements in these 90 days.

Campaigns to clarify and raise awareness among the population and guidance on the proper use of protective masks

to informR$94 million

to protectR$347 million

Test Centers operations begins on the 31st of July in Rio de Janeiro city and on the 7th of August in the Ceará state

+ 25,000 tests per day

Support for epidemiological research and for the treatment of covid-19

to prepare R$222 million

and caregivers in more than 600 institutions

to careR$396 million

serving all cities in Brazil105,000 oximeters

Implementation of Reception Centers in vulnerable areas

1,000 units of hospital equipment

~ 175 million people society to resume social activities as normal

support to 50,000 elderly people

Distributed to the elderly, users of public transport, residents of communities, indigenous people and homeless people

14 million masks

330,000 health professionals and 172,000 patientsBenefited by the distribution of more than 50 million protective equipment

Investment in the new vaccine manufacturing plants of Fiocruz and Instituto Butantã

and awareness initiatives for truck drivers44,000 tests

Strategic agenda

13

Strategic agenda

Strategic agenda

Following a collective thought process, we defined our strategic agenda in order to achieve consistent and quality results in the years ahead.

Client centricity

Efficiency

Digital Transformation

People

14

Customer centricity is the central piece supported by three fundamental pillars: digital transformation, people and efficiency.

Our ambition is to be one of the world's best companies in client satisfaction.

We must have the best products, in less time and higher flexibility.

Our business is providing services and that is why people is a vital issue. We invest to provide a more open and diverse environment.

Price is of paramount importance customer satisfaction. We can only have competitive prices if we are efficient.

Strategic agenda

Client Centricity

We want our clients to have the best experienceThat is why we are continually and tirelessly striving to improve our client’s experience each time they engage with the bank

56 million clients

between 18 and over 80 years of age;

from low-income to the Private segment;

present throughout Brazil, both in the capital cities and hinterland, and overseas;

companies: from very small companies, to major corporate conglomerates.

We challenge ourselves daily to serve this very heterogeneous universe.

Satisfied clients create more valuePresent Value of R$/client net income, 5-year forecast (base 100)

10xThe difference between the present value created by a client who advocates for the Itaú Branches segment, against the value generated by one who knocks it

Universal Bank

15

100

468

950

ItaúBranches

5x

2x

Strategic agenda

Client Centricity

We want to be the benchmark in satisfaction, transforming our culture so that the client is at the center of everything. Our actions, including digital transformation and the efforts involving people management, are designed for our clients’ satisfaction, a key metric for the entire organization.

Lessons learned from client feedbacks to enhance their

experience.

Active contact to understand our clients’ experience.

+4 k meetings per month¹

+60 k feedbacks per month¹

We want to be compared to the world’s best companies in client satisfaction

Comparable companies

Satisfied clients create higher value

Global NPS

16

+ 8 points

+ 17 points

+ 27 points

2020 vs 2018(Jun-20 vs Aug-18)

2021 vs 2018 2023 vs 2018

1: Period: Jan-20 to Mar-20

Strategic agenda

Client Centricity

3,8Updated in Jun-20

1st bank offering bank account opening by mobile phone

1st bank offering a leanersmartphone app

Card receivables control by phone

APP ITAÚ(INDIVIDUALS)

APP ITAÚ EMPRESAS

4,4

APP LIGHT

APP REDE

APP ABRE CONTA

APP ITAUCARD

APP ITAÚ EMPRESAS

APP PERSONNALITÉ

Continuous updates for a better experience

17

4.4 4.7

4.5

4.5 4.6

4.7 4.7

4.3 4.8

4.4 4.0

4.3 4.7

Our apps are among the best rated in app stores

App Store

Play Store

14.7 MM of individual and corporate account holders using our digital channels

56on the mobilechanel

More than half new users have been our customers for over 1 year

47% of new entrants are over 50 years old: 17 p.pincrease over the period before the pandemic

Newfeatures

Strategic agenda

Client Centricity

Juros pós-fixados Juros prefixados

Inflação Multimercado

Carteira em 26/08/2019Nível de risco: Moderado

Retorno esperado (em % CDI): 114.5% a.a.

Nível de risco: Arrojado

Retorno esperado (em % CDI): 133.9% a.a.

DIAGNÓSTICO DA SUA CARTEIRA

Sua carteira atual Carteira personalizada

07

Investment recommendationsWhat is the best way to invest my money?

Data only Itaú has:

Expected results from 28,000 financial products and assets 1,200,000 possible portfolio combinations 10,000 scenarios for market behavior

Testing 12 billion different scenariosfor all client profiles

Optimization in the client context (current portfolio, earnings and new investments)

2.5 minutesto generate arecommendation

+0.80 to 3.00 pp additional annualportfolio profitabilitybased on the recommendation

The most advantageous combination possible for each client, according to their profile and moment in life

Customized expert evaluation

Solution

Identifiedneed:

18

Tendências de novas tecnologias:

cloud

artificial Intelligence andmachine learning

big data and analytics

APIs

blockchain

What are they for?Identifying possible application

opportunities

Let’s testPilots and tests in lateral situations,

which do not compromise

client’s realneeds

New technology radar:

cloud

artificial Intelligence and machine learning

big data and analytics

APIs

blockchain

+

Technology applied to solve real problems,enabling measurement of value created

Expenditure Time Expenditure Time

$ $ $ $ $ $

Strategic agenda

Digital Transformation

19

Supply perspective x Demand perspective

Traditional model: supply perspective Tendências de novas tecnologias:Modern model: demand perspective

New technology trends:

We find an applicationMore investment for

updating

time data customization

Client Bank

Market research

Solutiondevelopment

Data+ research

+ experimenting

time data customization

Bank

Client

Client

Before

Now

Strategic agenda

Digital Transformation

To achieve digital transformation, we need to change the way we develop services and products

20

Strategic agenda

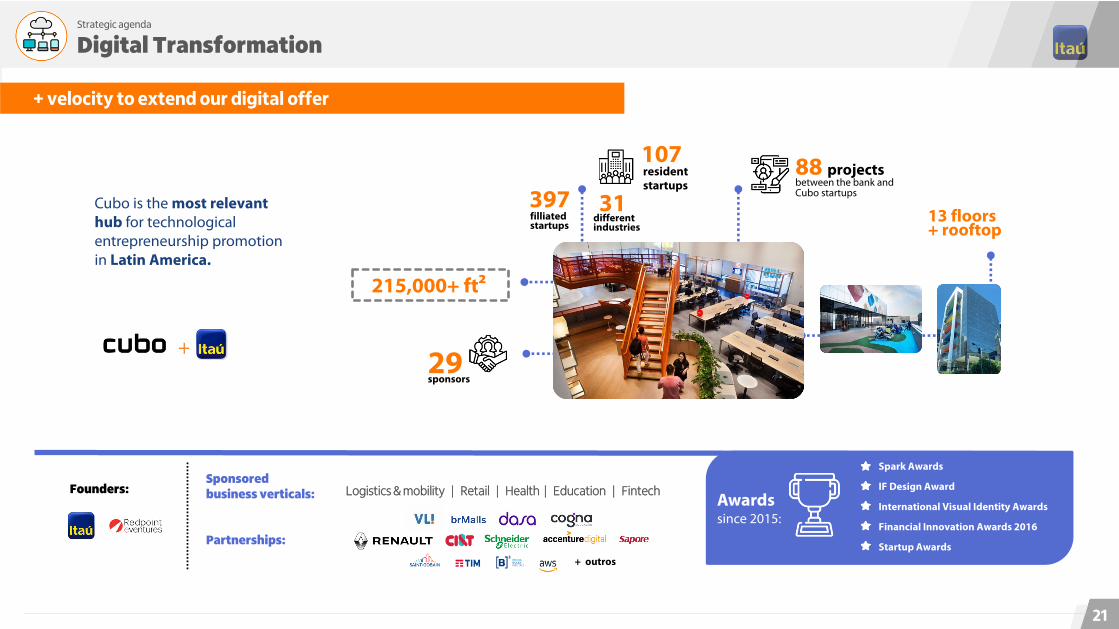

Digital Transformation

21

+

Sponsoredbusiness verticals:Founders:

Spark Awards

Financial Innovation Awards 2016

Startup Awards

Awardssince 2015:

International Visual Identity Awards

+ velocity to extend our digital offer

IF Design Award

Cubo is the most relevant hub for technologicalentrepreneurship promotion in Latin America.

Logistics & mobility | Retail | Health | Education | Fintech

Partnerships:

+ outros

88 projectsbetween the bank and Cubo startups

13 floors+ rooftop

29sponsors

215,000+ ft2

397filliatedstartups

residentstartups

107

31differentindustries

Higher productivity

22

Reduction of customers who had problems with major transactions on the internet and mobile channels:

More availability

Now99.6% of ourclientsfind no problems when using the main transactions on these channels

Data base 100

2Q2019 2Q2020

More technology solutions

Greater number of solutions delivered Reduction in the delivery time of technology solutions

New work methods lead to superior results

Strategic agenda

Digital Transformation

- 57%

15%2Q2019 2Q2020-30%

2Q2019 2Q2020

130 MM calls/year

The right service, for the right client at the right moment

One of the world’s largest voice transcription operations

Traditional monitoring

Calls monitored by people.<0.5% followed up

Capture client’s satisfaction limited to one sample

Transcription of 100% of the calls and analysis of the texts

client attendant

“I would like to increase my

limit.”

• Map opportunities

• Capture intentions without having to ask

• Channel efficiency

• Measure the satisfaction of 100% of our clients

In the past

Speech analytics

Today

Strategic agenda

Digital Transformation

Analytics: “listening to” 360,000 calls every day

23

Audio signal

Call content

Client´s data

Transactions

Geolocation

Interactions indigital channels

Voice data

Biometrics

Image data

Text data

Data: the bank’s new capital

Strategic agenda

Digital Transformation¹

24

70petabytes

(1) Data base Jul-20.

+State-of-the-artalgorithms

Data andanalytics

Data scientists+

+ Resultado

+485% of value captured in projects in analyticsData base: 2017 to Jul-20

Strategic agenda

Digital Transformation

Focus on efficiency while continually investing in technology

25

11%Inflation (IPCA) accumulated in the period

Technology investments

45.3 46.4 47.6 45.5

100122

130154

100 101 106 109

2016 2017 2018 2019

Efficiency Ratio (%) Technology investments (Base 100) Non-interest Expenses (Base 100)

Strategic agenda

Digital Transformation

26

Digital dashboard

Quality

Virtual stores(Itaú Varejo app, end of period)

Availability -%Share of customers with normal service on the main digital functionalities in June 2020.

99.0%

99.6%

Jan-19 Jun-20

App Store

Play store Jun-19

Mar-20

Jun-20

4.3

4.4

4.4

Jun-19

Mar-20

Jun-20

4.7

4.7

4.7

4.4 of 5

4.7 of 5+1 m reviews

+1 m reviews

Digital solutions

Transfers

Payments

Investments

Personal loan

97%85%

46%40%

For individualsShare of digital channels in 2020 (%)

For companies

R$3.6 billion²through Itaú Empresas appPronampe³ emergency credit line, directly through smartphone1st private bank to offer Pronampe.

R$1.6 billionthrough the internetLine of credit for payroll expenseswith implementation in record time.

Usability

~ 1 million accounts opened through Abreconta app in 2020(thousand)

Annual increase of 17.1% of digital clients in 2020¹

XX,X

1H18

218

987+131%

1H20 vs. 1H19

+353%1H20 vs. 1H181H201H19

426

5.56.6

8.2

IndividualsCompaniesCredit card holders

10.3

11.9

13.5

1.1 1.2 1.2

(1) Considers account holders (individuals and companies) and digital credit card holders; (2) In July 2020; (3) National Support Program to Micro and Very Small businesses.

Jun-18 Jun-19 Jun-20

14%

Employees²in Brazil and overseas

41.5%

58.5%

Men

Women

1%

3%

7%

5%

83%

OfficersManagersAdministrationOperationsTraineesInterns

Apprentices

0.1%15.0%38.8%38.6%

0.2%5.4%1.8%

86% 14%48% 52%50% 50%

30% 70%59% 41%

47% 53%31% 69%

Approximately

NorthNortheastCenter-WestSoutheastSouth

4.2%

People with disabilities

22.9%Afro-Brazilians

By gender

By age bracket By region

43.2%

51.4%

5.4%45.5 k people30-50 years38.3 k peopleup to 30 years

4.7 k people> 50 years

By hierarchical level Inclusion and diversity

27

97 thousand

(1) December 2019 - For information relating to employees, we only consider information from Itaú Unibanco companies under the management of the Human Resources department, except for International Units. (2) June 2020.

Strategic agenda

People1

Employee’s experience

An innovative and inspiring environment.

VoU cOmO sOu

Home-office

IU Conecta

New work methods

Rendering our dress code flexible, respecting our employees and our strategic agenda..

We offer more flexible options that encourage employee autonomy.

A new platform for our employees’ day-to-day. A social network with several administrative tools.

Collaborative environments, delivery communities and focal space aiming for greater synergy, communication and integration among the teams.

Greater freedom for employees to reconcile their working hours with their personal life.

Flexibility

Is Itaú Unibanco a good place to work?

73e-NPS

78%

18%

5%

Advocates

Neutrals

Knockers

In our employees’ eyes

(Scores 9-10)

(Scores 7-8)

(Cores 0-6)

Our challenge is to be increasingly attractive to all generations and to engage and develop our talent pool. To do so, we have consistently invested in disseminating our purpose and what we refer to as Our Way– a strong culture rooted in collaboration,meritocracy, ethics and total and unbridled respect for the individual.

Attraction and retention of employees

16.7% turnover rate

86% Up to 30 years’ old

14% Over 30 years old

49% Women

51% Men

Strategic agenda

People¹

28

13.6 kadmissions

(1) Data base 2019.

In the market view

2018

12.1% Involuntary

4.7% Voluntary

Strategic agenda

People¹

The program takes into account the priorities of the year, the results obtained and the manner in which those results are delivered, since although it is important to achieve objectives, our values must underpin all actions.

Incentive Model

Over than 1,000,000 live and online training sessions.

Courses and training

On average, 13 hours of live and online training per employee.

Hours of training

6.1 k scholarships, postgraduate and language courses.

Scholarships

72% of the employees have a supplementary plan.

Supplementary pension schemes

A bank that recognizes, values and encourages people development.

Investment in personnel

29

Partners’ and Associates’ ProgramTo align the interests of our officers and employees with those of our shareholders, we run a program for partners and associate intended for managers and employees with a differentiated performance.

Further details on page 60

(1) Data base 2019. Fixed compensations include compensation, social benefits and charges. Variable compensation includes employees´profits sharing and share-based payment.

Evaluation (directors and EDs)

Conversation with DG/VP/DE on the priorities for the year.

Objective indicators related to priorities as support (priorities, results achieved in the previous year and market data - if applicable).

_ performance _ reporting

Behavioral assessment (360º): evaluates whether the executive's behavior is consistent with our moment and our work models.

Results. Career Moment.

Assessment with up to 3 challenges (simpler and more agile).

Evaluation can even be 100% qualitative.

_performance _ Y axis e career committee

Behavioral assessment evaluates whether the employee's behavior is consistent with our moment and our work models.

Career evaluation and development in a collegiate committee (with inputs, Y axis and reporting - if applicable).

Evaluation (team)

R$ 22 bi

Total compensation1

Fixed compensation

Variable compensation

R$ 17 billionRecognizes a professional’s competence and seniority.

R$ 5 billionRecognizes the level of individual performance, the financial result attained by the bank and its

sustainability in the short, medium and long terms. Each employee has targets to be

achieved, which are linked to the strategy of each area which, in turn, reflects our global

strategy.

Strategic agenda

Efficiency

Our challenge is to continually improve the efficiency of our operations by maintaining clients at the center of our decisions, through strategic cost management and investment in technology and new ways of working in order to boost the use of our resources, whileefficiently managing the allocation and cost of capital.

Key principles of ourStrategic Cost Managementweekly reported to the Executive Committee

Automation and digitalization

Focus in technology

Consolidation, reorganization and redesign of operations

Optimization of service channels

+802 employeeshired by the Technology area in the quarter+1,327 employees in the last 12 months.

Zup1,448 employees incorporated in the quarter

3.7% 2.4% 1.8%-0.7%

0.4% -0.5%-2.5%

-4.0%

2Q19 3Q19 4Q19 1Q20 2Q20

Non-interestexpensesgrowing at a slower pacethan inflation

Non-interest expenses growthyear over year

Non-interest expenses growthcompared to the same period of the previous year (deflated by IPCA)

-9.0%

-6.8%

30

Our business

31

Our business

Who are our clients?

Through our Retail and Wholesale Banking segments we offer a wide range ofproducts and services tailored to each client profile.

Personnalité>R$10 thousand or >R$100 thousand in total investments

Uniclass>R$4 thousand up to R$10 thousand

Retailup to R$4 thousand

Private Bank>R$5 million in total investment

;;;;;;;

; Middle between R$30 million up to R$500 million

Largebetween R$500 million up to R$4 billion

Ultra over R$4 billion

Very Small and Small Companiesup to R$30 million

Client profileby segment in Brazil

RETAIL

WHOLESALE

Individuals Companies

32

Our business

Retail Banking

Our distribution network comprises¹4 , 0 0 6 B R A N C H E S A N D C S B s I N B R A Z I L

3 %North

8 %Northeast

7 %Midwest

67 %Southeast

15 %South

MainResults 2Q20

Serving a client base of over

56 million clients

MORE THAN 45,000ATMsin Brazil

Efficiencyratio

Return onallocatedcapital

Consolidatedprofitsharing

Net income R$1.8billion

42%

15.3 %

51.8 %

(1) In June 2020. Does not include branches and CSBs in Latin America and Itaú BBA. 33

Retail Banking NPS

+8 points Dec-19 vs. Aug-18

DigitalBranches(Brazil)

Brick and Mortar Branches and PABs

Branches and PABs

4,7224,488

Jun-19 Jun-20

196

4,292

196

4,526

234(Jun-20 vs Jun-19)

Our business

Retail Banking

The use of our digital channels significantly increased over the last years. Our digital branches alsoincreased to serve clients who almost do not use brick and mortar branches.

196 digital branchesfor over 2.3 millionclients

More than335,000 companies4

servedbymanagers withmobility, usingsmartphone, tablet andvideoconference

Use of digital channels¹

Total current account holders (in millionpeople)

Jun-18 Jun-19 Jun-20

10.3 11.9 13.4

1.1 1.2

individuals

companies

% of transactionsthrough digital channels

Investiments²

Credit²

Payments²

46%

25%

85%

41%

18%

72%

1H20 1H19

(1) Internet, mobile and SMS in Retail Banking; (2) Share of digital channels in the total volume of transactions (R$) in the Retail Banking; (3) Share of digital channels in the total volume (R$) of transactions in the Retail Bank segment; (4) Includes Emp3 and Emp4; (5) Includes only Emp4.

ExtendedhoursDifferentiatedservice

18 digital branches for107,000 microentrepreneurs5

HighlightDigital branches

34

Transfers³ 97% 91%

1.2

Account openings through the Abreconta app The availability of digital channels remains high, at the highest level ever

99.6%of the clientsdid not have any impact on the mainfunctionalities.(June 2020)

99.0%

99.6%

Jan-19 Jun-20

127 205

645

2Q18 2Q19 2Q20

Our business

Retail Banking | Support for clients during the crisis

This unprecedented initiative aims to address indebtedness using a structured approach, providing clients with some respite and ensuring that they enjoy sustainable conditions over time.

35

0.8 1.0 1.0

0.6 0.4 0.3

03/16 to04/17

04/18 to05/01

05/02 to05/15

05/16 to05/29

05/30 to06/12

06/13 to 06/26

March 16 to June 30, 2020

37.6 IndividualsVery small and small companies

Reprofiled portfolio by product (in R$ billions)

16.1Mortgage loans

12.9Personal loans

4.7Vehicle loans

2.8Cards

Reprofiled volume per working day (in R$ billions)

14.6

12.1Working capital

2.5Vehicle loans

R$52 billionin loan reprofiling for individuals, very small and small businesses

58% are collateralized

90% in ratings AA to C

93% individuals

83% very small and small companies

1.0Payroll loans

100% up to date in February

Our business

Wholesale Banking

Our sales channels reach institutional clients in 18 countries.

Mainproducts and services

MainResults 2Q20Only in Brazil, We serve approximately

21,000 corporate groups andinstitutional

Efficiencyratio

Return onallocatedcapital

Consolidatedprofit sharing

Net income R$825 million

20 %

5.6 %

48.9 %

ParaguayArgentina

PeruColombiaUruguayPanamaMexicoUSABahamasCayman Chile

EnglandPortugalSpainGermanyFranceSwitzerlandCorporate

Institutional Clients

Private Banking

CreditsolutionsNationalandforeigncurrency

Service solutionsR$3.3 bnfixed incomedistributionR$585 mnequitiestransactionsin LatinAmericaR$757 mn total volume of Mergerand AcquisitionR$7.4 bnfinancing of infrastructure projects in different sectors

Solutionsin WMSR$1,405 bn under local custodyR$113 bn under internationalcustodyR$720 bn¹ under assetmanagement

$

36

2020 maininitiativesLatAm –ClientCentricity

(1) Source: ANBIMA (Brazilian Financial and Capital Markets Association) – June 2020. Considers Itaú Unibanco and Intrag.

WholesaleBanking NPS

+8 points Dec-19 vs. Aug-18

• Accelerating the digitization of customer experiences and journeys • Evolution of the digital technological platform

• Increasein 100% digital customeracquisition• Implementation of NPS System for 3Q20

36% 38% 39% 40% 41% 41% 42% 44% 44%

64% 62% 61% 60% 59% 59% 58% 56% 56%

46.5 44.6 44.8 44.4 45.4 46.7 49.1 49.4 50.4

Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19 Jun-20

Rede de Agências Itaú Consignado S.A.

31.4 31.0 32.2 32.8 34.6 36.5 38.8 39.0 40.2

10.5 9.2 8.2 7.0 5.9 5.1 4.5 3.9 3.54.6 4.4 4.3 4.7 4.9 5.1 5.8 6.5 6.646.5 44.6 44.8 44.4 45.4 46.7 49.1 49.4 50.4

Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19 Jun-20

INSS Setor Público Setor Privado

Personal loans

Money in the accountThe money is immediatelycredited, including on theweekends.

PurposeThe loan does not have to bejustified.

Payroll loans

Reduced ratesInterest rates are lower than for other types of loans.

Easier repaymentFixed installments are deducteddirectly from the payroll of theborrower.

Payment conditionsFirst installment in up to 90 days.

Origination channels of payroll loans

Other personal loans

Payroll loans

(In R$ billion)

Evolution of personal loans portfolio

(In R$ billion)Composition of the payroll loans portfolio

(In %)

The payroll loans portfolio accounts for 58% of total operations in personal loans.

The portfolio of the personal loans accounts for 42% of total operations in personal loans.

58%

42%

$

$

Our business

Personal Loans and Payroll Loans$

Public SectorINSS Private Sector Itaú Consignado S.A.Branches

37

28.2 25.8 25.4 25.3 27.3 28.2 31.9 33.7 36.4

46.5 44.6 44.8 44.4 45.4 46.7 49.1 49.4 50.4

74.7 70.5 70.2 69.8 72.7 74.9 81.0 83.1 86.8

Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19 Jun-20

77.0% 78.4% 80.0% 82.6% 85.1% 87.0% 89.3% 91.4% 90.8%

23.0% 21.6% 20.0% 17.4% 14.9% 13.0% 10.7% 8.6% 9.2%

Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19 Jun-20

Pessoas Físicas Pessoas Jurídicas

Our business

Mortgage Loans$

Mortgage loans portfolio Products and sales channels

Environmental and social assessment on mortgage loans

Client focused

Quick and efficient process withcredit analysis in up to one hour for operations of up to R$1 million.

possibility of digitally contracting.

specialized consultants providingsupport throughout the process.

+ 9.2 %vs Jun-19

+ 13.0 %vs Jun-18

Real Estate

Brokers

29%High

Income Branches

32%Partnerships

17%Regular Branches

21%

(In R$ billion) (In %)

CompaniesIndividuals

38

Building site visit gatheringof information

Enterprise and region data

• Levantamento de Indícios de Contaminação (LIC)

• Enterprise Environmental and Social Form;

• Building site photos;

• Document analysis;

• Consultation of the Contaminated Areas Register; and

• Consultation of Google Maps.

No Environmental

License?

Indication ofcontamination?

Environmental and Social Department + Environmental and Social Legal Department +

Compliance

• Technical analysis of evidence;

• Analysis of site contamination documentation; and

• Preparation of contractual clauses and conditions for release of funds.

Risksmitigated

Operation approved

Technical analysis for construction financing

47.1 48.6 47.8 48.1 47.6 48.3 49.2 50.3 53.8

Developers0.4%

Our business

Mortgage Loans¹

Loan to Value

Average Ticket and Average Origination Term²,³

$

(Em %)

+ 3.4 p.pvs Jun-19

- 0.4 p.p.vs Jun-19

Vintage (quarterly average) Mortgage Loan Portfolio

Average operation period (in months)Value of the Property (R$ mn) Financing Average Ticket (R$ mn)

(1) Includes only Individuals. (2) Average Operation Period for new developers’ contracts; (3) Value determined using monthly financing average ticket and quarterly average LTV. Production source: ABECIP.

39

Vintage (quarterly average)

Mortgage Loan Portfolio

+ 0.5 %vs Jun-19

+ 0.4 %vs Jun-19

Average operation period

Average value of the Property

Financing Average Ticket

- 4.4 %vs Jun-19

54.9% 54.6% 54.5% 54.7% 57.3% 58.4% 59.7% 62.1% 63.1%

41.8% 41.8% 40.9% 40.2% 39.9% 38.7% 38.7% 38.6% 38.3%

Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19 Jun-20

296 306 305 294 302 315 328 314 313

312 312 311 318 322 322 323 324 325

584 561 554 537 523 538 546 500 548

Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19 Jun-20

1.8 2.3 1.8 2.5 2.6 2.9 3.0 3.5 2.1

0.3 0.4 0.5 0.8 1.0

1.6 1.9 2.5

1.1 2.1

2.6 2.3 3.2 3.6 4.5 4.8

6.0

3.2

2Q16 4Q16 2Q17 4Q17 2Q18 4Q18 2Q19 4Q19 2Q20

PF PJ

16.7 15.4 14.1 14.1 14.7 15.9 17.2 19.0 19.53.6 2.9 2.3 2.6 3.2 4.3 6.0

9.1 10.120.3 18.3 16.4 16.7 17.8 20.2 23.2 28.1 29.5

Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19 Jun-20

PF PJ

Our business

Vehicles$

40

13.2 thousand sales points;

Sale of light and heavy vehicles:

• 83% of contracts are made in stores and dealers;

• 91% to individuals;

28% made in Digital Channels;

85% of financing are made up to 48 months.

Contracting

Average Ticket (individual)

R$37.6 thousand

LTV (individual)

61%

Loan portfolio by client profile(In R$ billion)

Credit origination by client profile¹(In R$ billion)

CompaniesIndividuals

CompaniesIndividuals

(1) Includes Finame in Companies

90-day NPL Ratio ( Individuals – Vehicles)

40

(Base 100)

100

54 49

43 35 38 42

2012 2015 2016 2017 2018 2019 2Q20

+ 27.0 %

- 33.6 %

Resumption of production

11 19

31

Abril Maio Junho

Contracts - thousand

April May June

100 111

147

2018 2019 2Q20

Evolution of financing proposals on the iCarros platform:(Base 100)

Our business

Vehicles$

$

iCarros Portal

Main commercial partnerships

41

21 mn access/month 87% mobileMain products and services

Facial RecognitionSimple and safe contracting process.

ConectCarPayment of tolls and parking without queuing.

InsurancesProtection to the car and tranquility in financing.

Lead ManagerDealer platform to manage leads in one place.

Knowledge GarageDistance learning platform to training theprofessionals from the sector.

9

75

8

6

10

11

4

1

2

3 Digital ContractingIntegrated to iCarros and other digital environments, like dealers’ websites andothers e-commerces.

Credline 2.0 New proposal origination platform, with simple and renewed digital experience.

Floor PlanCredit lines for partner dealers.

iCarrosVehicle Marketplace with technologicalsolutions, that brings buyers and sellerstogether.

Eletronic signatureDigital and simple experience for the customer and the dealer.

Digital AssistantOnline credit analysis and approval platform, without additional cost for the dealer.

We are leaders in the creditcard segment in Brazil, totaling around 33.0 million credit cards and 29.8 million debit cards (both in numberof accounts).

Our credit card options serve current account holders and non-current account holders

Main brandsTo individuals, very small, small and middle-market companiesand corporate segment.

Commercial partnershipsMain partnerships with retailers and traders.

Digital portfoliosIncreased comfort and convenience to our clients.

Convenience to clientsFinancial services through credit cards.

$

$

Personalcredit

Payment of bills ininstallments

Debt renegotiation

Consumer credit

42

Our business

Credit Card

Itaucard App Benefits to our clients

Digital billing statements: Paperless. More environmentally friendly.

Timeline: To follow up consumption.

Loyalty program: Points and reward program.

Virtual card: Added security for online purchases.Virtual cards generated (2Q19 = Base 100)

1002Q19

2Q20 238

2.4x

78.6%

67.9%

10.1%

10.2%

11.3%

22.0%Transactor

Installment with Interest

Revolving Credit + Overdue Loans

13.5%¹ of total sales are carriedout using digital channels

33.4%Market ShareWe are leaders in theBrazilian credit cardMarketData base: Mar-20

40.3%² in 1Q20 + 3.6 pp vs 1Q19of household consumptionare card expenses

SFN whithout

Itaú

+2 points CustomersatisfactionGlobal NPS - Business

Composition of credit balance

2Q20

R$101.3 billions- 21.8% (vs. 1Q20)- 19.8% (vs. 2Q19)

Credit- 22.2 % (vs. 1Q20)- 20.5 % (vs. 2Q19)

Debit- 20.6% (vs. 1Q20)- 17.6% (vs. 2Q19)

Transaction Volume

43

Our business

Credit Card

(1) Considers only credit cards issued to current account holders of Branches, Uniclass e Personnalité. (2) Consider only credit and debit cards.Note: Data base refers to Jun-20 except household comsuptiom.

Debit

Credit

Total

Jun-20 vs. Aug-18

95.368 97.40375.826

30.947 32.114

25.509

126.316 129.517

101.335

2Q19 1Q20 2Q20

Our business

Acquiring services

Acquiring service revenues(R$ million)

2Q20

R$102.5 billions- 15.9% (vs. 1Q20)- 10.1% (vs. 2Q19)

credit- 18.9% (vs. 1Q20)- 16.2% (vs. 2Q19)

debit- 10.7% (vs. 1Q20)+ 1.2% (vs. 2Q19)

Transaction VolumeOur brands

accepted by Rede machines

25 brandsMore than de

+33 pointsCustomersatisfactionGlobal NPS - Business

837 thousand

Clients

1.4 mnPOS number

44

Debit

Credit

Total

1,226 1,177 1,2521,106

964 932 908737

528

2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20

Note: Data base refers to Jun-20.

Jun-20 vs. Aug-18

74.095 76.575 62.092

39.959 45.28240.429

114.055121.858

102.521

2Q19 1Q20 2Q20

58.3% 61.9% 60.6% 60.4% 57.1%

52.7% 55.2% 53.8% 52.6% 50.5%

2Q19 3Q19 4Q19 1Q20 2Q20

Combined Ratio Extended Combined Ratio

Revenue from insurance operations/GDP (%)

Our business

Insurance

We offer a wide range of insurance products related to life, personal accidents, vehicles and property credit and travel. Ourinsurance core activities, which include our 30% interest in Porto Seguro, consist of mass-market insurance products related to lifeand property, and credit.

Ranking¹,²

Potential growth in the sector8

Combined Ratio – Recurring Activities Insurance

(1) Source SUSEP, date: May-20, includes our 30% interest in Porto Seguro. Doesn´t consider Health and VGBL is consider in Pension Plans; (2) Insurance = Earned Premiums; Pension Plans = Provision for Benefits to be Granted and Premium Bonds = Revenues from Premium Bonds; (3) Recurring insurance activities and other activities; (4) Recurring insurance activities include: Personal Insurance (Life, Personal Accidents, Unemployment, Funeral Allowance, Serious Diseases, Random Events, Credit Life), Housing, Homeowners, Multiple Peril and Travel; (5) Considers only Porto Seguro numbers; (6) Other activities include: Extended Warranty, Large Risks, DPVAT and IRB; (7) The sale of this portfolio has been concluded on October 31, 2014. (8) Sector growth potential figures for Chile, USA and South Korea refer to 2018.

45

2.9 2.9 3.0 3.2 3.3 3.43.7 3.8 3.8 3.6 3.8

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

jan-may/20 jan-may/19 Model

Total Insurance 3 4th 4th

Recurring Insurance Activities 4 4th 5th

Life & Personal Accidents 2nd 2nd Bancassurance

Credit Insurance 6th 6th Bancassurance

Pension Plan 3rd 3rd Bancassurance

Premium Bonds 5th 4rd Bancassurance

Porto Seguro 3rd 3rd

Vehicles 5 Leader: Porto Seguro Leader: Porto Seguro Broker

Residential 5 Leader: Porto Seguro Leader: Porto Seguro Broker

Other Insurance Activities 6 6th 5th

Large Risks 7

Health Insurance

we do not offer this product.

we do not offer this product.

Chile: 4.7USA: 11.3South Korea: 10.5

Benefits Products OfferedMulti-channel BrokerSales Force

Our business

Insurance | Insurance Open Platform

Multi-channel distributionFocused on commissions and fees

Specialized sales force

Excellence in post-sales

Easy access and convenience to clients

Insurance consultants

Insurance Shop

Manager

Cashier

Internet Banking/Mobile

ATM

Call Center

NAC/Partners

Corban

Inte

rnal

Exte

rnal

Multi-channelBroker Platform

Retention Post-Sales Analytics

SatisfactionMarketing Client service

Relationship withclients

Vehicles

Life

Health (Companies)

Full Life

Credit Life

Dental (Individuals and Companies)

Protected Card

Premium Bonds

Mortgage

Travel

Smartphone protection

Homeowners

Corporate lines

46

Guarantee Insurance

+

Auto, Moto, Home and Pet Assistance

Our business

Pension plan

Open platform

Funds carefully selectedalways keeping the client in mind

+ 5.7% (vs. 2Q19) + 2.8% (vs. 2Q19)+ 5.1% (vs. 2Q19) VGBLPGBLTraditional

Technical Provisions

Concept 1,3,6,9: How much does the client have tosave to enjoy a peaceful retirement?

47

Retirement

Future expenses

Children education

Tax planning

Financial return

Enable easychanging of plan

Successionplanning

Reasons to invest:

1

2

3

4

5

6

7

Years of salary accumulated Age1 353 456 559 65

R$ Billion

6.6 6.8 7.0 7.0 7.2 7.3 7.4 7.5 7.7

38.1 39.2 40.6 41.7 42.8 43.5 44.9 43.8 45.0

140.4 144.0 149.0 151.6 154.8 158.1 161.4 156.5 159.2

185.2 190.0 196.6 200.4 204.8 208.9 213.6 207.8 211.8

2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20

Main products

Zero-fee products:

Our business

Services | Investments

SavingsPension PlanFixed incomeFunds Equities Treasury Direct

Variable Income Pension Plan Fixed Income Real Estate Fund Treasury Direct

Zero custody feefor shares of Itaú Corretora and thestock exchange

Zero initial andfinal contributionfees

Zero custody fee for third party FI via Itaú Corretora

Zero brokerage andcustody fee on digital channels

Zero custodyfee - Itaú Corretora

Real Estate Funds COE

Itaú Asset ManagementThe largest private asset manager in Brazil in figures:

R$720 billlion¹assets under management

+ 60 yearsin investment management

11 timesbest fund manager by “Exame” magazine

We incorporate ESG issues intoour investment process.

Responsibleinvestments

48(1) Source: ANBIMA (Brazilian Financial and Capital Markets Association) – June - 2020. Considers Itaú Unibanco and Intrag. (2) CDB - Certificates of Banks Deposits. LCA - Agricultural Credit Bonds. LCI - Real Estate Credit Bonds

Investment Open PlatformThird-party products offered

Funds Fixed income2

Fixed IncomeMultimarketEquityPension Plan

CDBLCALCI

MiddleAnnual revenues from R$30 mn to R$500 mn

“Focused on clients with the best ratings, with 95% of the credits being rated B3 or better, and with operations in diversified services, such as Cash Management, Foreign

Exchange, Investment Banking and Funding."

Corporate BankingAnnual revenues over R$500 mn

“We offer a broad portfolio of banking products and services, ranging from“ cash management ”to structured

transactions and transactions in the Capital Market. We serve around 3,317 large business groups (includes

Agrobusiness) in addition to serving more than 240 financial institutions.”

Investment BankingLeadership position and client recognition

Markets, Products & PlanningTreasury operations for the conglomerate.

LatAmPresence in all banking segments in Latin America.

49

AgrobusinessLarge and Regional (medium size + producers)

“We serve more than 1,200 customers in the integrated agribusiness chain, from plants to rural producers, with an emphasis on Targeted products and Foreign Currency, in a

portfolio of more than R$30 billion.”

Our business

Services | Wholesale Banking

Fixed incomeWe took part in local operations with debentures, promissory notes and securitization, which totaled R$3,338 million up to June 2020, taking the second place in the ANBIMA (Brazilian Financial and Capital Markets Association) ranking.

EquitiesWe undertook 8 offerings in South America in the first semester of 2020, which totaled US$585 million, taking the second place in the Dealogic ranking.

Mergers and AcquisitionsIn the first half of 2020, we provided financial advisory on 18 transactions in South America, totaling US$757 million and maintaining the leadership position in the Dealogic ranking.

Project FinanceIn the first half of 2020, we served as advisor and/or creditor of approximately R$7.4 billion in financing to 25 different infrastructure projects in different sectors.

Ranking 2Q20 2019 2018

M&A¹ 1st 1st 1st

Local ECM¹ 2nd 1st 1st

Local DCM² 2nd 1st 1st

International DCM¹ 2nd 3rd 6th

Derivatives Total3 1st 1st 1st

(1) Source Dealogic; (2) Source ANBIMA – Brazilian Financial and Capital Markets Association. Information from Jun-20; (3) Source: Cetip. Information from Jun-20.

Our business

Services | Wholesale Banking

WMSLarge range of customized wealth management and

investments solutions

Local Custody: we ended June with R$1,404.5 billion under custody (practically stable from the same period of 2019).

International Custody: we ended June with R$112.8 billion under custody (-36.4% from the volume under custody in the same period of 2019).

Corporate Solutions: we are leaders in the bookkeeping of shares, providing services to 189 companies listed on B3, representing 58.2% of the total market, and in the bookkeeping of debentures, we work as a bookkeeper for 342 (28.9%) used.

Securities Services

With a full global wealth management platform, leadership position in Brazil.We have been recognized by the world’s top international Private Banking market publications:

Private Banker International• Outstanding Global Private Bank - Latin America, 2019

PWM / The Banker• Best Private Bank in Brazil, 2019

Private Banking

Investment Product management for the conglomerate and a full range of investment options to Retail Banking.

Evolution of Assets Under Administration1

50

752 801 883

946 1,025

1,107 1,176

1,363 1,299

Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19 Jun-20

R$ million

(1) Includes only Brazil (ex-Latam).

Our business

Services | Wholesale Banking

KineaIt is an independent platform of management of differentiated investments. With R$61.1 billion in assets as of June 2020, it operates in the segments of Multi-Markets, Real Estate, Pension Plan and Private Equity, Stock and Infrastructure.

Asset ManagementIn June 2020, we reached R$720.21 billion in assets under management.Over 60 years in investment management and 11 times best fund manager by “Exame” magazine.

Itaú Asset Management integrates ESG issues in the investment process:

51

Asset Management

Timeline of IAM responsible investment practices

(1) Source: ANBIMA (Brazilian Financial and Capital Markets Association) – June 2020. Considers Itaú Unibanco and Intrag.

2004

2008

2009

2010

2013

2014

2015

2016

2017Itaú Asset

Management launchesits Itaú Social

Excellence Fund (FIES)

Signatory toProprietary model to

incorporate ESG issuesinto the analysis of

funding fixed income

ESG issuesincorporated intothe Proxy Voting

policy

White paper on theincorporation of ESG

issues into the analysisof funding

Internal study aboutESG issues and

sovereign bonds

White paper on theincorporation of ESG

into the analysis ofcorporate securities

Launching of AMEC Stewardship Code /

Latin America

Carbon footprintcalculator for funds

2018

White paper onresponsible investment

through the SDGs lenses(image below).

2019Incorporation of ESG issues

into the analysis of more than 95% of assets under

management (AuM) of IAM

2020

White paper aboutresponsible investment in

the days of COVID-19

Corporate governance

52

Corporate governance

History of our Governance

We believe that a sound and meritocracy-based governance, guided towards long-term value creation, adds value to our business, facilitates access to capital and contributes to business continuity.

53

20081996APIMECsmeetings andRoadshows

2000Corporate Code of EthicsIndependent Fiscal Council

1999APIMECs meetings

Inclusion in the DowJones Sustainability Index

2005Trading Committee and Policy

Inclusion in the CorporateSustainability Index

1997Level III ADR

2002DisclosureCommitteeand Policy

2001Stock Option Plan

Level I of Corporate Governance of B3

2003Election of Independent Members

2007Certification under section404 of Sarbanes-Oxley Act

Merger

Highlights

2018-XP Investimentos (XP)CADE’s approval of the acquisition of a minority interest, reaffirming the independence of management – ItaúUnibanco acquired 49.9% of the capital, with 30.1% of the common shares- First woman elected on the Board of Directors- 21 years on the NYSE- 50% stock splitwith a 50% increase in dividends paid monthly;- Encouraging diversity and new Vou Como Soudress code;- Board of Directors;- General Data Protection Law as a Priority for Itaú Unibanco- 10 years of merger between Itau and Unibanco

2019- Changes in the composition of the Executive Committee:Caio Ibrahim David assumed the position of General Director of the Wholesale department and Milton Maluhy assumed the position of Vice-President of Risks and Finance, being part of the Executive Committee- The creation of the Social Responsibility Committee Approved on January 31, 2019

2020- Disclosure of the Management Members’ Compensation Policy

2017Policy for Nomination ofExecutives: minimum 30% ofindependent members in C.A.

Inclusion in the BloombergEquality Index

2008CorporateGovernancePolicy

2007Voluntary adherenceto Abrasca’s Manual forMaterial InformationControl and Disclosure

2006Certification under section404 of Sarbanes-Oxley Act

Internal Regulation of theBoard of Directors

2004Audit Committee

Creation of Dividendreinvestment program

2001Level I of CorporateGovernance of B3

Election of IndependentBoard Members

1999Inclusion in the DowJones Sustainability Index

1995Stock Option Plan

2013

Related Party Committee

2011Voluntary adherence to the Abrasca’sCode of Self-regulation and Bestpractices of Publicly-Held Companies

Remuneration Committee

2009Strategy Committee

Risk and CapitalManagement Committee

Nomination and CorporateGovernance Committee

Personnel Committee

2012Digital Assembly

2010Partners and AssociatesProgram

2015Inclusion in the SustainabilityVigeo EIRIS Index – Emerging 70

New Management Structure ofItaú Unibanco Holding

2005Nominating and Compensation Committee

Inclusion in the Corporate Sustainability Index

2002Disclosure and Trading Committee

Level II ADR Program

Tag Along

Highly diversifiedshareholder base

Corporate governance

Our governance structure

Family control, with long-term vision

ON51.71%

PN0%

ON39.21%

PN0.004%

ON7.76%

PN99.59%

Free Float

ON36.73%

PN81.87%

Free Float*

74%

Traded on B3

26%Traded on NYSE

51% Brazilians49% Foreigners

100% Foreigners

Itaú Unibanco participações

(IUPAR)ITAÚSA

Itaú Unibanco Holding S.A.

Non-voting shares (PN)4.8 billion of shares

66.5%

33.47%

33.64%

ON63.27%

PN18.13%

familyMoreira

Salles

Cia. E. Johnston de Participações66.36%

26.15% 52.95%19.91%

100%

familyEgydio de

Souza Aranha

ON50.00%

PN0%

Note: ON = Common Shares; PN = Non-voting Shares; (*) Excluding shares held by majority owners and treasury shares.54

Corporate governance

Pillars of our Governance

Family control ensuring long-term strategic vision

Responsible for value creation by means of strategicdefinition

Focus on decision-making, resolving upon high impact topicsfor the company’s destiny

• Alignment among shareholders• Defines group’s vision, mission and values• Assesses significant mergers and acquisitions• Nominates executives to the Board of Directors• Evaluation of performance and admission of family members• Discusses and approves long-term strategies

IUPAR

Itaú Unibanco Holding S.A.

Shareholders’ General Meeting

Board of Directors

Fiscal Council

Executive Committee

Committees

Disclosure and Trading Committee

Professional management with the implementation ofstrategy and day-to-day management

decisions made ona collective basis

management alignedwith meritocracy-basedculture

Focus on performance and value creation

55

Our Board of Directors consists of professionals with exceptional knowledge and expertise in different areas of expertise, some of the key differentials of our management.

Corporate governance

Board of Directors

• Defining and monitoring the strategy;• Assessing mergers and acquisitions; • Monitoring the Executive Committee performance; • Appointing officers (meritocracy);• Approving the budget;• Defining and supervising risk appetite and policies for capital use;• Defining and monitoring incentive andcompensation models and establishing goals; • Supervising the technology strategy; • Defining meritocracy policies;• Supervising the business operation.

The evaluation process of the Board of Directors iscarried out by a third-party. Each director evaluatesthemselves, the other directors and of the organ as a collegiate ”.

1

2

4

7

Risk and Capital Management

Social Responsibility Committee

3

5

6

8 Compensation Committee

Strategy Committee

Board of DirectorsCommittees

Main duties

Audit Committee

Personnel Committee

Related Parties Committee

Nomination and Corporate Governance Committee

56

2 Co-chairmenPedro Moreira SallesRoberto Egydio Setubal

9 Members, being 6 Independent membersAlfredo Egydio SetubalAna Lúcia de Mattos Barretto VillelaJoão Moreira Salles

2 4 72 4 7

Fábio Colleti BarbosaGustavo Jorge Laboissière Loyola José GallóMarco Ambrogio Crespi Bonomi Pedro Luiz Bodin de MoraesFrederico Trajano Inácio Rodrigues

2 3 4 7

24 5

3 5 8

5 8

2 4 7 86

6

6

6

3 81

1 Vice-presidentRicardo Villela Marino 6

Check Point of Executive Committee + 7

Institutional Crisis Management Committee and Check Point of Risks

Febraban and Retail War Rooms and Wholesale Committee

People, Legal, Marketing, IT, CRM and Service channels War Rooms

Executive Committee agenda

Retail War RoomMonitoring and adjusting operations in real time.

Wholesale CommitteeConsolidates the treasury, credit and ECM war rooms and monitors and adjusts their operations in real time.

Febraban* War RoomCoordination between banks and alignment with public authorities and regulators.

Check Point of Risks Closing day. Market, credit, liquidity and operational risks monitoring.

Institutional Crisis Management Committee Morning Calls. Operation monitoring. Decisions coordination. Risks and contingencies mitigation.

57

Corporate governance

COVID-19 Governance Committee

Responsible for monitoring the crisis and its impacts, deliberations and institutional positioning.

* Febraban is the Brazilian Federation of Banks.

Our committees report directly to the Board of Directors.

Corporate governance

Board of Directors Committees

since 2009

Risk and Capital Management100% of the members are non-executive12 meetings in the year

Supports the Board of Directors; establishes the riskappetite; evaluates the cost of capital x the minimum return expected; allocates capital; oversees risk management and control; improves riskculture and complies withregulatory requirements

since 2004

Audit100% of the members are independent60 meetings in the year

Ensures the integrity of thefinancial statements; complies with legal andregulatory requirements; and ensures the efficiency ofinternal controls and riskmanagement

since 2011

Compensation100% of the members are non-executive5 meetings in the year

Promotes discussions onincentive and compensationmodels; developscompensation policies for management members and employees; and establishes goals

since 2009

Nomination andCorporate Governance100% of the members are non-executive3 meetings in the year

since 2009

Personnel100% of the members are non-executive4 meetings in the year

Establishes policies for attracting and retaining talented professionals; proposes guidelines for recruiting and training employees; and presents long-term incentive programs and monitors the culture of meritocracy

since 2009

Strategy100% of the members are non-executive5 meetings in the year

Proposes budgetary guidelines; provides inputs for decision-making processes; recommends strategic guidelines and investment opportunities; and internationalizes and creates new business areas.

since 2013

Related Parties100% of the members are independent12 meetings in the year

Manages transactions between related parties; and ensures equality and transparency for these transactions

since 2018

LATAM StrategyCouncil

Assesses the outlooks for the world economy; adoptsinternationally accepted trends, codes and standards; andprovides guidelines for the Board of Directors to analyze opportunities

since 2017

Digital AdvisoryBoardProposes technologicaldevelopments; assessesclient’s experience; andfollows world trends

since 2019 NEW

Social Responsibility4 meetings in the year

Defines strategies tostrengthen our social responsibility; monitors theperformance and defines theallocation process of theRouanet Law

8committees

Strategic committees

The Board ofDirectors isresponsible for electing themembers of thecommittees for one-year terms ofoffice.

They must have proven knowledge in the respective areas of work and technical qualification compatible with their duties.

Periodically reviews the criteria for nomination and succession;provides methodological support for the assessment of the Board of Directors and Chief Executive Officer; nominates members of the Board of Directors and Senior Vice Presidents (Diretores Gerais); and analyzes potential conflicts of interests

58

Corporate governance

Our Executive Committee

• Implementing the guidelines and goals proposed by the Board of Directors;

• Carrying out business and strategies related to products and segments;• Ensuring the best allocation and management of financial, operational

and human resources;• Monitoring market, credit and operational risks; and• Leading the bank in the search for value creation.

Main duties

The Executive Committee is responsible for implementing the strategy and day-to-day management.

59

• Large and Medium Corporates • Asset Management• Institutional Treasury • Private Bank• Custody• Latin America• Investment Banking

• Branches• Cards• Rede• Real Estate• Insurance• Vehicles• Consortia• Payroll

WholesaleCaio Ibrahim David

RetailMárcio de Andrade Schettini

Risks and FinanceMilton Maluhy Filho

Legal and Human ResourcesClaudia Politanski

• IT• Operations• Procurement

• Risks• Finance

• Legal and Internal• Human Resources• Corporate Communication• Institutional and Governmental Relations•Marketing• Sustainability

IT and OperationsAndré Sapoznik

Candido Botelho Bracher• Ombudsman

Chief Executive Officer (CEO)

Senior Vice Presidents (Diretores Gerais) Executive Vice Presidents

Aiming at aligning the interests of our officers and employees with those of our shareholders, we maintain a partner and associate’ program, focused on management members and employees with outstanding performance.

Corporate governance

Partners and Associates Program

Long-term incentivesThe program offers to participants the opportunity to invest in our non-votingshares (ITUB4), receiving a return also in shares, sharing short, medium andlong-term risks.

The partners program may also considerother instruments derived from shares,

as opposed to actual shares.

The share price considered at the grant and delivery dates is calculated on the

seventh business day before of each event, considering the average closing

price in the 30 days prior to the calculation.

Any partners and associates shares not yet received will also be subject to reduction

proportional to a possible reduction in the realized recurring net income of the Issuer

or of the applicable business area.

50%3 year

50%5 years

The investmentmust be retained

for:

Net variablecompensation

PartnersEight-year term of officeEligible to successive reappointmentsPossibility to invest 50% to 100% of net variablecompensation

AssociatesFour-year term of officeEligible to two reappointments (maximum 12-year term)Possibility to invest 35% to 70% of net variable compensation

year 1 year 2 year 3 year 4 year 5 year 6 year 7 year 8

grant year

Shares received will remain unavailablefor sale for five and eight-year term as

from each investment in shares

Partners and associate receive a return on theinvestment in the program

ITUB4

Available for sale

70% associates50% partners

30% associates50% partners

Available for sale

(delivery of 50%)ITUB4

(delivery of theremaining 50%)ITUB4

60

447

363

255259290

Oct-08 Oct-10 Oct-12 Oct-14 Oct-16 Oct-18

ITUB4 - with dividend reinvestmentBank basket with dividend reinvestment¹IBOVESPA IndexDollarCDI

100

Our capital stock is comprised of 9.8 billion common shares (ITUB3) and non-voting shares (ITUB4). Non-voting shares are also traded as depositary receipts (ADR - ITUB ) on the NYSE (New York Stock Exchange).

Corporate governance

Our shares

ITUB3

Stock Exchange

R$24.00Price²

Additional payout4

Tag Along5

Voting right

Priority dividends³

Characteristics of our shares

Jun-20

R$25.45 US$4.69

80% 80% 80%

ITUB4 ITUB

Appreciation of R$ 100 investedon the date before the announcement of the merger(10/31/08) to June 30,2020

Source: Economatica

(1) Simple average of the three largest Brazilian banks ex Itaú Unibanco; (2) Closing price as of 06/30/2020, adjusted for earnings except dividends. Source: Economatica. (3) The non-voting shares will have the right to the priority minimum annual dividend (R$0.022 per share). (4) Additional payments may be made in dividends or interest on capital. ADR holders will be paid by the Custodian Bank, which will be responsible for paying the holders in an average time 10 days as from the payment in Brazil. (5) Mechanism for protecting minority shareholders in the event of a change in the Company’s shareholding control.

61

Capital and risk management

62

Through our internal capital adequacy assessment process (ICAAP), we evaluate our capital adequacy for addressing risks, represented by our regulatory capital for credit, market and operating risks, and the capital required for covering other risks.

Capital adequacy

To ensure our solidness and the availability of capital to support the growth or our business, our Reference Equity remains above the minimum levels required by the Central Bank.

Capital and risk management

Our principles of risk management

The Board of Directors is our main capital management body, responsible for approving our institutional capital management policy and the guidelines involving the institution’s level of capitalization.

preparation of managerial and regulatory reports

preparation of the capital plan, in situations of both normality and stress

We adopt a forward-looking approach when managing our capital, using the following phases:

structuring of the capital contingency and recovery plans

internal capital adequacy assessment

identification of the material risks and the evaluation of additional capital

Main indicators ascertained based on the Prudential Conglomerate on base date June 30, 2020

Basel Ratio13.5%

Reference EquityR$141 billion

Dividends and IOC in 2Q20 R$745 million (net of taxes)

Payout in 2019¹66.2%

63(1) Dividends and net interest on own capital / recurring net income

Capital and risk management

Basel III and Capital structure

Total Capital (10.25% - 12.75%)

Tier I (8.25% - 10.75%)

CET 1 (6.75% - 9.25%)

Jun-20

Additional Tier I Capital (AT1)

4,5%

1.25%

0 – 2.5%

1.5 %

2.0%

Countercyclical²

Conservation4

Common Equity Tier I

1.0 %Systemic³ACP¹

4.5%

Basel III requirement

Tier II

Our current ratio

13.5%

64

10.4%

1.4%

1.7 %

(1) ACP = Additional Principal Capital. (2) Countercyclical ACP: defined by each Central Bank. BACEN and currently set at 0%. (3) Systemic ACP: Requirement required for systemically important banks at domestic (D-SIBs) or global (G-SIBs). For Itaú Unibanco, this requirement is 1.0%. (4) Regulatory change implemented: conservation ACP from 2.5% to 1.25% from April 2020 to March 2021. As of April / 21, the conservation ACP will gradually increase, remaining again at 2.5% in April / 22. (CMN Resolution 4,783).

Capital and risk management

Payout Practice

65

66.2%

The return and growth scenario positioned the percentage to be distributed in the range of 60% to 65%

R$18.8 billionis the net amount paid and provisioned in dividends and interest on own capital in 2019

RWA 9%

2019

23.7%ROE

The percentage to be distributed may change every year based on the company’s profitability and capital demands, always considering the minimum set forth in the Bylaws.

17.5% 20.0%

5.0%

25.0%

10.0%

15.0%

22.5%

RWA growth

ROE

15.0%

65% - 70%

40% -45%

35%

70 - 75%

45 - 50%

35%

75 - 80%

50 - 55%

35 - 40%

80 - 85%

55 - 60%

40 - 45%

85% - 90%

45% - 50%

60% - 65%

Total payout simulation2019

(1) Calculated based on dividends and interest on own capital (IOC) gross of taxes over net income adjusted by the legal revenue reserves.

Dividend yieldPayout

5.5% Dividends and gross interest on own capital / net income¹

2019

2019

Dividends and net interest on own capital / recurring net income

77.6%

Capital and risk management

Capital cost management

Risk and Capital Management

Committee

Board of Directors

The cost of own capital is monitored monthly by a committee that reports to the Board of Directors.

When the monitoring indicators of the CoE exceed the monitoring range, the committee evaluates the indicators and decides whether to propose a revision of the capital cost to the Board of Directors.

Monitoring is based on in-house models, market data and evaluations of the cost of the bank’s capital and

that of the market.

The Board of Directors, then, deliberates on and approves the changes

or the ratification of the cost of own capital

We are continually striving to manage our capital allocation efficiently through an appropriate capital cost.

66

A classical model with three lines of defense: the business areas bear primary responsibility for risk management, followed by the risks area and, lastly, the audit area subordinated to the Board of Directors

Capital and risk management

How are we structured for managing risks?

General Wholesale Office

Caio Ibrahim David

General Retail Office

Marcio Schettini

Legal, Institutional and Personnel Department

Claudia Politanski

Technology and Operations

DepartmentAndré Sapoznik