Embed Size (px)

Citation preview

ALIMENTATION COUCHE-TARD INC.ALIMENTATION COUCHE-TARD INC.

Investors Presentation

April 2016

This presentation and the accompanying oral presentation contain forward-looking statements within the meaning of applicable securitieslegislation. Forward-looking statements are typically identified by words such as “projected”, “estimate”, “may”, “anticipate”, “believe”,“expect”, “plan”, “intend” or similar words suggesting future outcomes or statements regarding an outlook. All statements other thanstatements of historical fact contained in these slides are forward-looking statements.

Forward-looking statements involve numerous assumptions, risks and uncertainties. A variety of factors, many of which are beyondAlimentation Couche-Tard Inc.’s (“Couche-Tard”) control, may cause actual results to differ materially from the expectations expressed inits forward-looking statements. These factors include, but are not limited to, the effects of the integration of acquired businesses and theability to achieve projected synergies, fluctuations in margins on motor fuel sales, competition in the convenience store and retail motorfuel industries, foreign exchange rate fluctuations, and such other risks as described in detail from time to time in documents filed byCouche-Tard with securities regulatory authorities in Canada, including those risks described in Couche-Tard’s management’s discussionand analysis (MD&A) for the year ended April 26, 2015. Couche-Tard’s MD&A and other publicly filed documents are available on SEDARat www.sedar.com.

Unless otherwise required by law, Couche-Tard does not undertake to update any forward-looking statement, whether written or oral, thatmay be made from time to time by it or on its behalf. No financial information presented in this presentation as of a date more recent thanApril 26, 2015 has been audited.

While the information contained in this presentation is believed to be accurate, Couche-Tard expressly disclaims any and all liability forany losses, claims or damages of whatsoever kind based upon the information contained in, or omissions from, this presentation or anyoral communication transmitted in connection therewith. In addition, none of the statements contained in this presentation are intended tobe, nor shall be deemed to be, representations or warranties of Couche-Tard and its affiliates. Where the information is from third-partysources, the information is from sources believed to be reliable, but Couche-Tard has not independently verified any of such informationcontained herein.

This presentation is not, and under no circumstances is to be construed as, a prospectus, an offering memorandum, an advertisement or apublic offering of securities. Under no circumstances should the information contained herein be considered an offer to sell or a solicitationof an offer to buy any securities.

FORWARD-LOOKING INFORMATION AND CAUTIONARY LANGUAGE

2

3

Brian Hannasch

President and Chief Executive Officer

Claude Tessier

Chief Financial Officer

Mathieu Descheneaux

Vice President Finance

COMPANY REPRESENTATIVES

1. Company Highlights

2. Financial Highlights

3. Strategy and Value Creation

1. Organic Growth

2. Acquisitions

3. Cost Control

4. Capital Structure & Financial Flexibility

4. Appendix

4

AGENDA

ALIMENTATION COUCHE-TARD INC.

COMPANY

HIGHLIGHTS

Couche-Tard is a Canadian based group and a world leader in the convenience

store sector

• In North America, we are the largest independent convenience store operator in terms of number of company-

operated stores.

• In Europe, Couche-Tard is a leader in convenience store and road transportation fuel retail in Scandinavian and

Baltic countries with a significant presence in Poland and Russia.

• Couche-Tard’s mission is to provide a fast and friendly service offering food, hot and cold beverages, car wash

services, road transportation fuel and other high quality products and services in a clean, welcoming and efficient

environment.

As of January 31, 2016, Couche-Tard’s network comprised:

WHO ARE WE ?

6

North America Europe Rest of World

7,979 convenience stores

throughout North America,

including 6,560 stores offering

road transportation fuel in all 10

Canadian provinces and 41 US

states, and employing about

80,000 people.

Couche-Tard operates 2,218 stores,

comprising a broad retail network across

Scandinavia (Norway, Sweden and

Denmark), Poland, the Baltics (Estonia,

Latvia and Lithuania) and Russia.

Including employees at its branded

franchise stations, about 19,000 people

work in its retail network, terminals and

service offices across Europe.

In addition, about 1,500 stores

are operated by independent

operators under the Circle K

banner in 13 other countries or

regions worldwide which brings to

almost 11,700 the number of sites

in Couche-Tard’s network.

7

• 1980 Start of operations with the opening of a first convenience store located in Laval, Québec.

• 80’s-90’s Consolidation of the Canadian market.

• 2001 First breakthrough of Couche-Tard in the United States : acquisition of the assets of Johnson Oil Company, Inc.,

owner of 225 Bigfoot stores, all located in the U.S. Midwest.

• 2003 Acquisition of The Circle K Corporation from ConocoPhillips Company that operates 1,663 Circle K corporate stores

located in 16 States and has a franchising or licensing relationship with 627 additional stores in the U.S. and

worldwide.

• 2004 Couche-Tard becomes an active player in the US market consolidation.

• 2012 Acquisition of Statoil Fuel & Retail, a leading Scandinavian road transport fuel retailer. Statoil Fuel & Retail operates

a broad retail network across Scandinavia (Norway, Sweden, Denmark), Poland, the Baltics (Estonia, Latvia,

Lithuania), and Russia with approximately 2,300 stores, the majority of which offer fuel and convenience products

while the others are automated (fuel only) stations.

• 2015 Acquisition of The Pantry, Inc., a leading convenience store operator in the southeastern United States and one of

the largest independently operated convenience store chains in the United States. The Pantry operates

approximately 1,500 stores in 13 states under select banners, including Kangaroo Express®, its primary operating

banner.

• 2015 Couche-Tard launches its global Circle K brand, the world’s preferred destination for convenience and fuel.

• 2016 Acquisition of Topaz, the leading convenience and fuel retailer in Ireland, made up of 444 stores. All the Topaz

stores will be rebranded with the new global brand Circle K.

• 2016 Couche-Tard signs an agreement with Imperial Oil to acquire 279 Esso-branded Canadian fuel and convenience

sites. These sites are located in the provinces of Ontario and Québec.

COMPANY HISTORY

1. As of March 4, 2016.

2. Fiscal Year ended 24/04/2015 and Q3 2016 YTD being 40 weeks to 31/01/2016.

3. Includes Couche-Tard’s Company-Owned/Dealer-Operated and Dealer-Owned-Dealer-Operated sites.

4. Long term interest-bearing debt, net of cash and cash equivalents and temporary investments divided by EBITDA adjusted for non-recurring items. Pro forma the acquisition of The

Pantry.

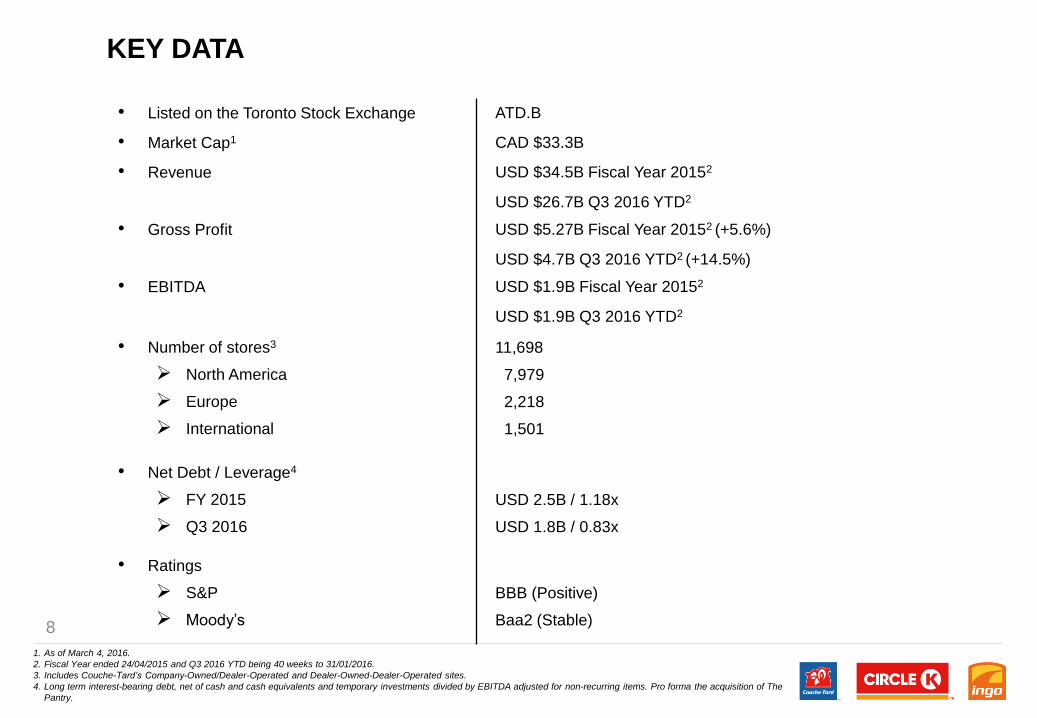

• Listed on the Toronto Stock Exchange ATD.B

• Market Cap1 CAD $33.3B

• Revenue USD $34.5B Fiscal Year 20152

USD $26.7B Q3 2016 YTD2

• Gross Profit USD $5.27B Fiscal Year 20152 (+5.6%)

USD $4.7B Q3 2016 YTD2 (+14.5%)

• EBITDA USD $1.9B Fiscal Year 20152

USD $1.9B Q3 2016 YTD2

• Number of stores3

North America

Europe

International

11,698

7,979

2,218

1,501

• Net Debt / Leverage4

FY 2015

Q3 2016

USD 2.5B / 1.18x

USD 1.8B / 0.83x

• Ratings

S&P

Moody’s

BBB (Positive)

Baa2 (Stable)

KEY DATA

8

9

INVESTMENT HIGHLIGHTS

Couche-Tard

is a

disciplined

c-store

operator and

integrator

Disciplined

Management Culture

• Management team with strong track

record and founders have 23% equity

ownership

• Management and Board need to hold

a multiple of their salary in Shares

• Decentralized operating model

S&P: BBB (Positive)

Moody’s: Baa2 (Stable)

Powerful

Financial Results• Strong and consistent financial

performance throughout all economic

cycles

• Prolific history of positive same-store

comps and 25% ROE

• Significant FCF generation (2010-2015)

CAGR of 29%

Broad Geographic Footprint

with Leading Market Positions

• Leading C-store operator in North America,

Scandinavia and Baltics

• Multiple banners (Couche-Tard, Circle K,

Mac’s, Ingo, and Kangaroo Express) that will

be rebranded to the strong and well-

established Circle K banner (except Couche-

Tard in Québec, Canada) to drive traffic and

sales

• World class Canadian retailer with most

geographically diversified footprint

Attractive

Synergy Potential• Proven ability to extract significant

synergies from acquisitions

• Transferring best practices across entire

platform

Superior

Product Offerings

• Increasing focus on private

label, fresh food products and

famous for concepts

• Industry leading

merchandise gross margin

Attractive

Sector Dynamics

• Steady industry performance

throughout downturns with strong

projected growth

• C-store sector well positioned to gain

share from traditional food retail

• Industry-leading returns in recession

Track Record of Highly Disciplined

Growth and Debt Reduction

• Proven ability to integrate acquisitions (More than 5,550 stores

from more than 50 acquisitions since Circle K in 2003, including

SFR and The Pantry)

• Well positioned to lead further consolidation in fragmented

industry

• Committed to remain investment grade post acquisition

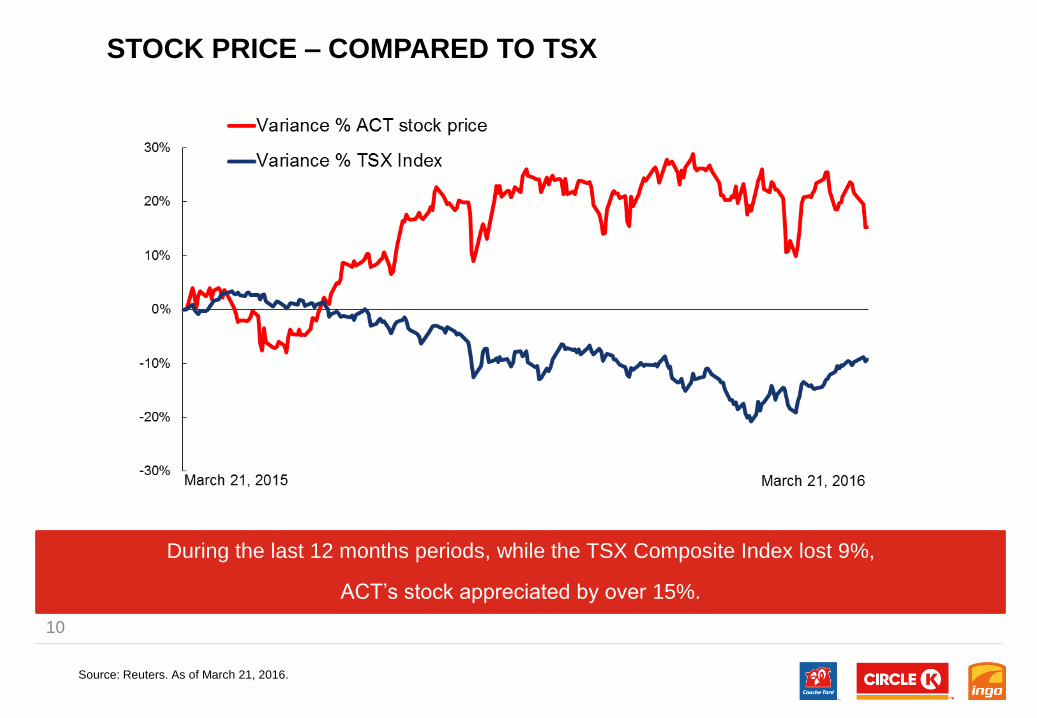

STOCK PRICE – COMPARED TO TSX

10

During the last 12 months periods, while the TSX Composite Index lost 9%,

ACT’s stock appreciated by over 15%.

Source: Reuters. As of March 21, 2016.

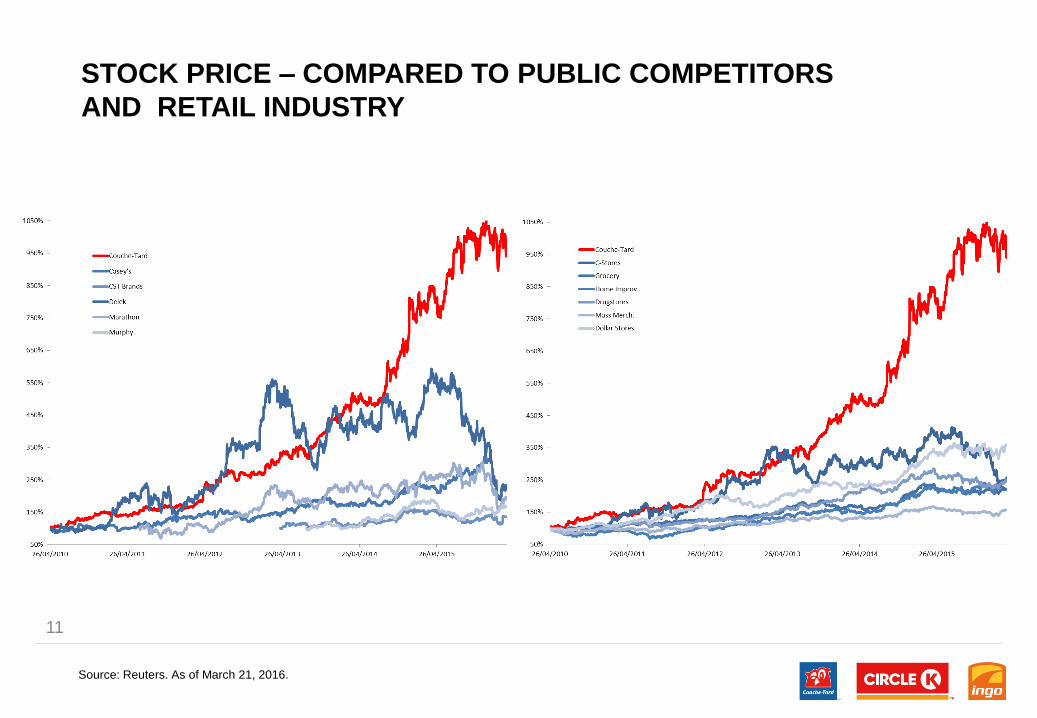

STOCK PRICE – COMPARED TO PUBLIC COMPETITORS

AND RETAIL INDUSTRY

11

Source: Reuters. As of March 21, 2016.

Merchandise and services

63%

Motor fuel37%

Gross Profit: $3,872M

US65%

Canada12%

Europe23%

Merchandise and services

27%

Motor fuel58%

Other15%

$1,357M

US61%

Canada6%

Europe33%

$24,002M

Merchandise and services

57%

Motor fuel39%

Other4%

$34,690M

Merchandise and services

79%

Motor fuel21%

$735M

US7%

Europe93%

$727M

US72%

Canada17%

Europe11%

Revenue: $9,961M

US

OtherMerchandise and services Motor Fuel

EuropeCanada

Gross Profit By

Geography

LTM Q3 2016(1)

Gross Profit By

Products

LTM Q3 2016(1)

Total

Total

Couche-Tard is a leading global convenience store operator with pro-forma EBITDA of $2.2 billion

• Well diversified

• Merchandise and services represent 57% of gross profits

• Focus on growing high margin categories

COUCHE-TARD – WORLD LEADER

(1) Pro Forma The Pantry acquisition.

$5,964M

12

13

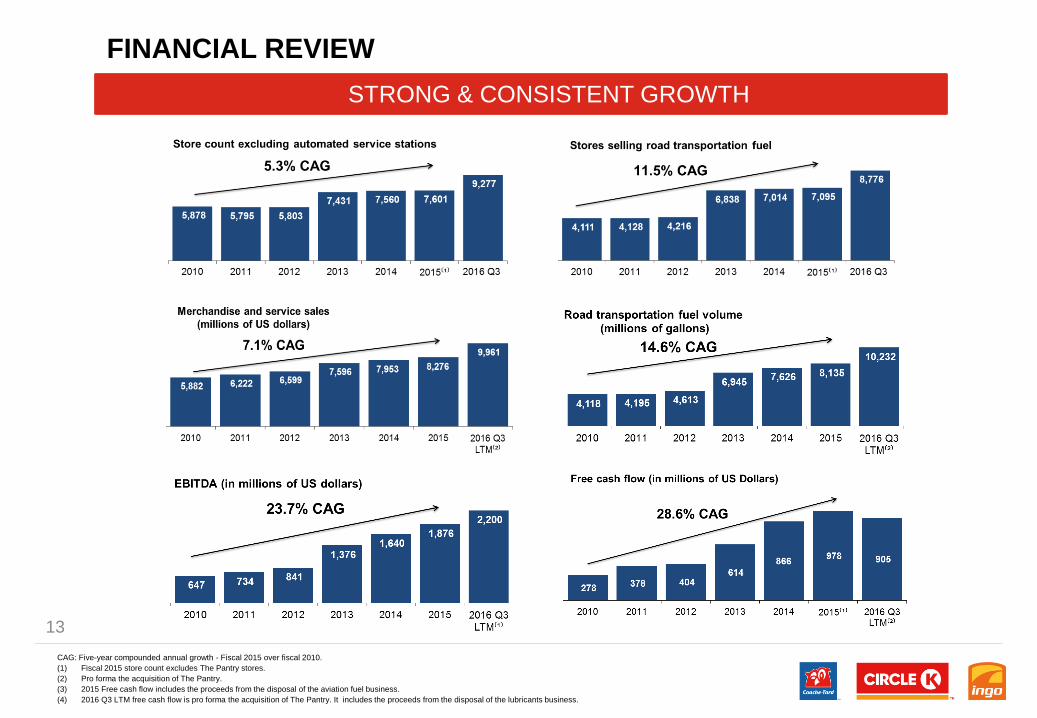

FINANCIAL REVIEW

STRONG & CONSISTENT GROWTH

CAG: Five-year compounded annual growth - Fiscal 2015 over fiscal 2010.

(1) Fiscal 2015 store count excludes The Pantry stores.

(2) Pro forma the acquisition of The Pantry.

(3) 2015 Free cash flow includes the proceeds from the disposal of the aviation fuel business.

(4) 2016 Q3 LTM free cash flow is pro forma the acquisition of The Pantry. It includes the proceeds from the disposal of the lubricants business.

14

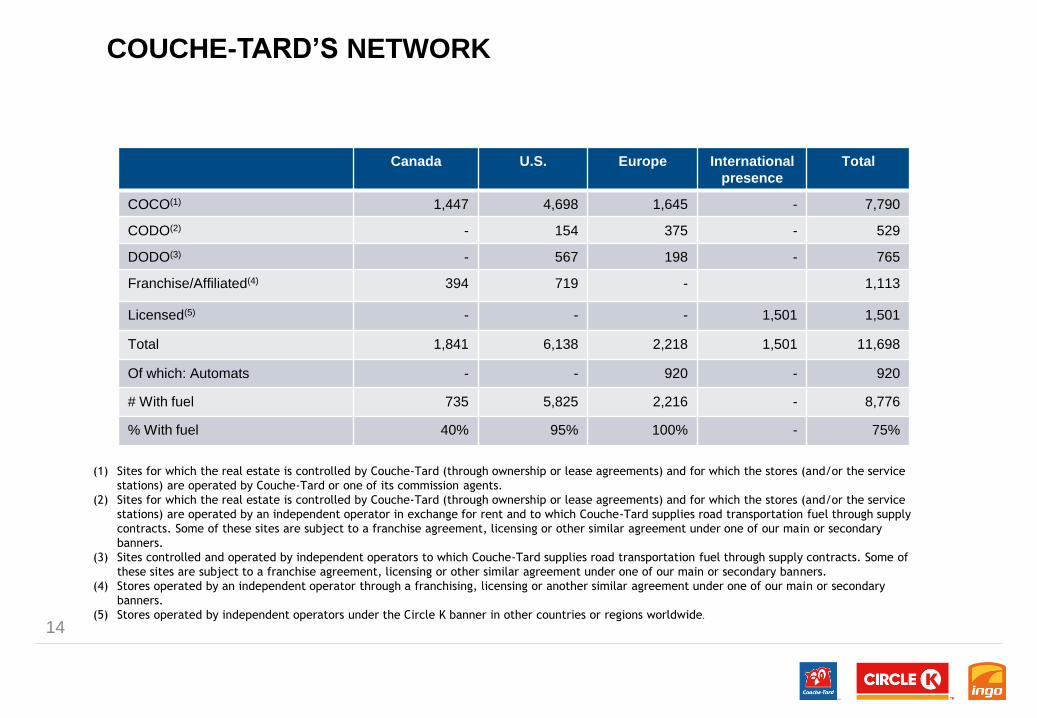

COUCHE-TARD’S NETWORK

Canada U.S. Europe International

presence

Total

COCO(1) 1,447 4,698 1,645 - 7,790

CODO(2) - 154 375 - 529

DODO(3) - 567 198 - 765

Franchise/Affiliated(4) 394 719 - 1,113

Licensed(5) - - - 1,501 1,501

Total 1,841 6,138 2,218 1,501 11,698

Of which: Automats - - 920 - 920

# With fuel 735 5,825 2,216 - 8,776

% With fuel 40% 95% 100% - 75%

(1) Sites for which the real estate is controlled by Couche-Tard (through ownership or lease agreements) and for which the stores (and/or the service

stations) are operated by Couche-Tard or one of its commission agents.

(2) Sites for which the real estate is controlled by Couche-Tard (through ownership or lease agreements) and for which the stores (and/or the service

stations) are operated by an independent operator in exchange for rent and to which Couche-Tard supplies road transportation fuel through supply

contracts. Some of these sites are subject to a franchise agreement, licensing or other similar agreement under one of our main or secondary

banners.

(3) Sites controlled and operated by independent operators to which Couche-Tard supplies road transportation fuel through supply contracts. Some of

these sites are subject to a franchise agreement, licensing or other similar agreement under one of our main or secondary banners.

(4) Stores operated by an independent operator through a franchising, licensing or another similar agreement under one of our main or secondary

banners.

(5) Stores operated by independent operators under the Circle K banner in other countries or regions worldwide.

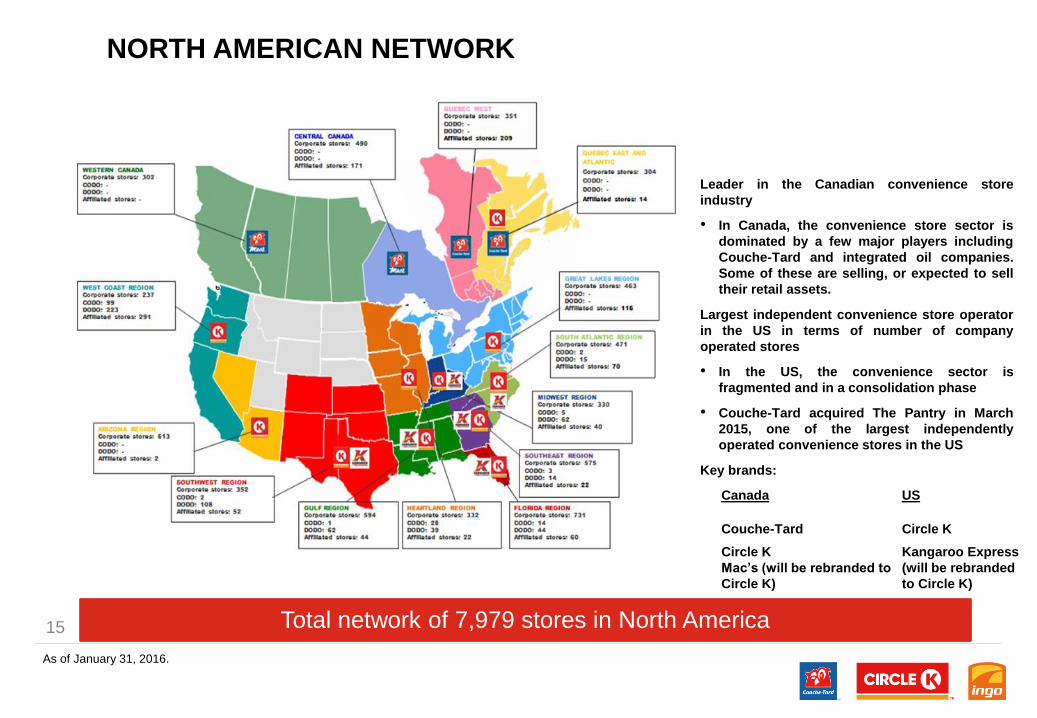

Leader in the Canadian convenience store

industry

• In Canada, the convenience store sector is

dominated by a few major players including

Couche-Tard and integrated oil companies.

Some of these are selling, or expected to sell

their retail assets.

Largest independent convenience store operator

in the US in terms of number of company

operated stores

• In the US, the convenience sector is

fragmented and in a consolidation phase

• Couche-Tard acquired The Pantry in March

2015, one of the largest independently

operated convenience stores in the US

Key brands:

As of January 31, 2016.

Total network of 7,979 stores in North America

NORTH AMERICAN NETWORK

Canada US

Couche-Tard Circle K

Circle K

Mac’s (will be rebranded to

Circle K)

Kangaroo Express

(will be rebranded

to Circle K)

15

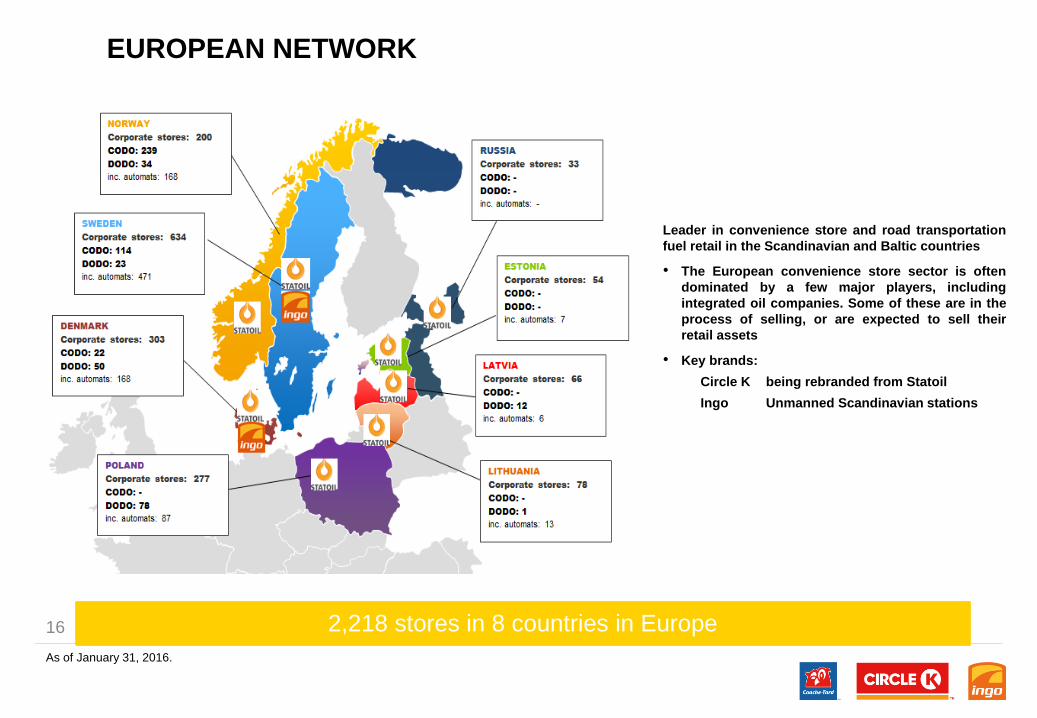

Leader in convenience store and road transportation

fuel retail in the Scandinavian and Baltic countries

• The European convenience store sector is often

dominated by a few major players, including

integrated oil companies. Some of these are in the

process of selling, or are expected to sell their

retail assets

• Key brands:

Circle K being rebranded from Statoil

Ingo Unmanned Scandinavian stations

As of January 31, 2016.

2,218 stores in 8 countries in Europe

EUROPEAN NETWORK

16

Around 1,500 licensed Circle K stores in Asia, Costa Rica, Egypt, Honduras, Mexico,

and U.A.E

As of January 31, 2016.

INTERNATIONAL PRESENCE

17

• Convenience stores

operated by

independent operators

• Under the Circle K

brand

18

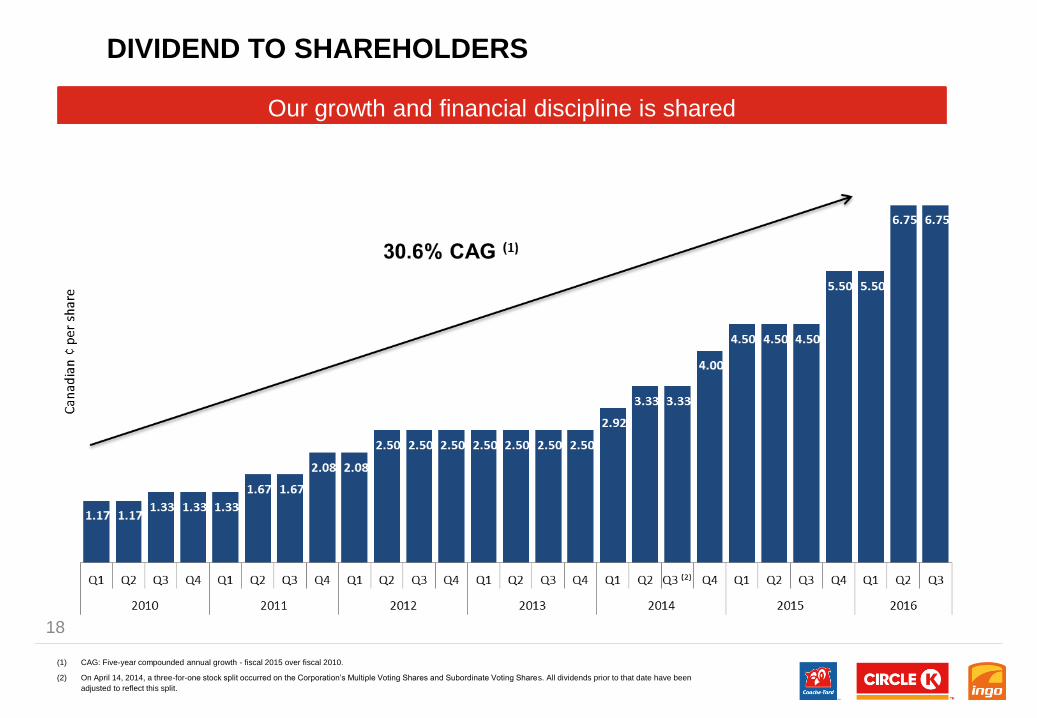

DIVIDEND TO SHAREHOLDERS

(1) CAG: Five-year compounded annual growth - fiscal 2015 over fiscal 2010.

(2) On April 14, 2014, a three-for-one stock split occurred on the Corporation’s Multiple Voting Shares and Subordinate Voting Shares. All dividends prior to that date have been

adjusted to reflect this split.

Our growth and financial discipline is shared

ALIMENTATION COUCHE-TARD INC.

FINANCIAL

HIGHLIGHTS

20

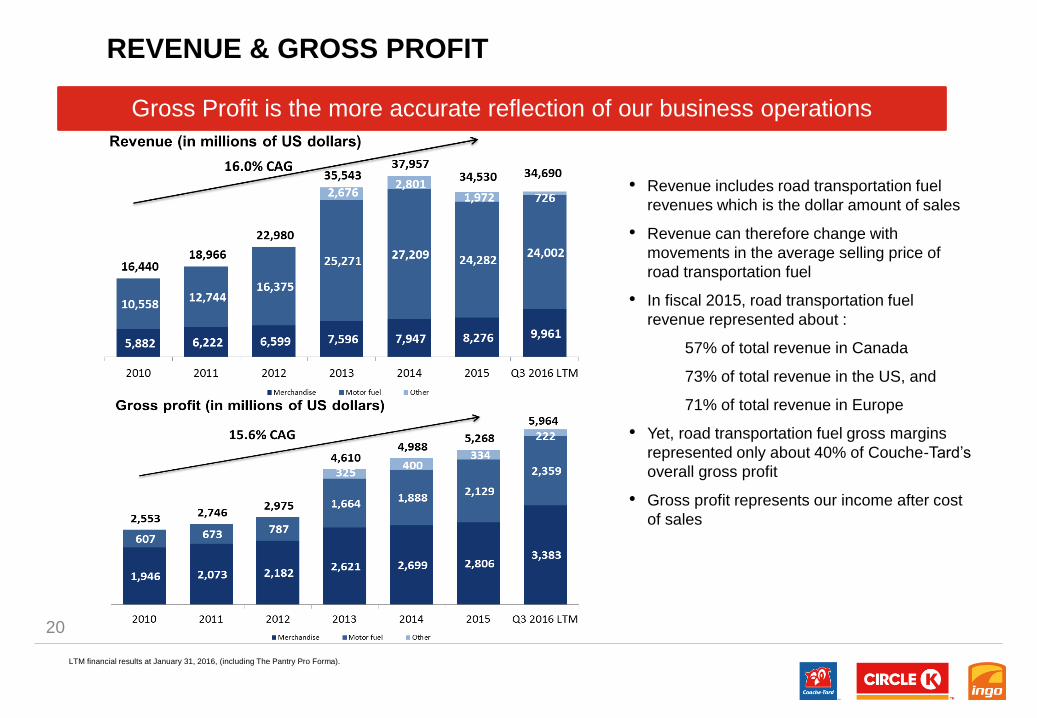

REVENUE & GROSS PROFIT

• Revenue includes road transportation fuel

revenues which is the dollar amount of sales

• Revenue can therefore change with

movements in the average selling price of

road transportation fuel

• In fiscal 2015, road transportation fuel

revenue represented about :

57% of total revenue in Canada

73% of total revenue in the US, and

71% of total revenue in Europe

• Yet, road transportation fuel gross margins

represented only about 40% of Couche-Tard’s

overall gross profit

• Gross profit represents our income after cost

of sales

LTM financial results at January 31, 2016, (including The Pantry Pro Forma).

Gross Profit is the more accurate reflection of our business operations

21

FUEL GROSS MARGIN VS AVERAGE SELLING PRICE

• No clear correlation between fuel selling price

and margins;

• Our margins are not directly impacted by

lower fuel selling prices;

• Lower fuel prices leave customers more

money in their pockets for their in-store

shopping.

U.S. Fuel Margins (CPG) Canadian Fuel Margins (CPL)

22

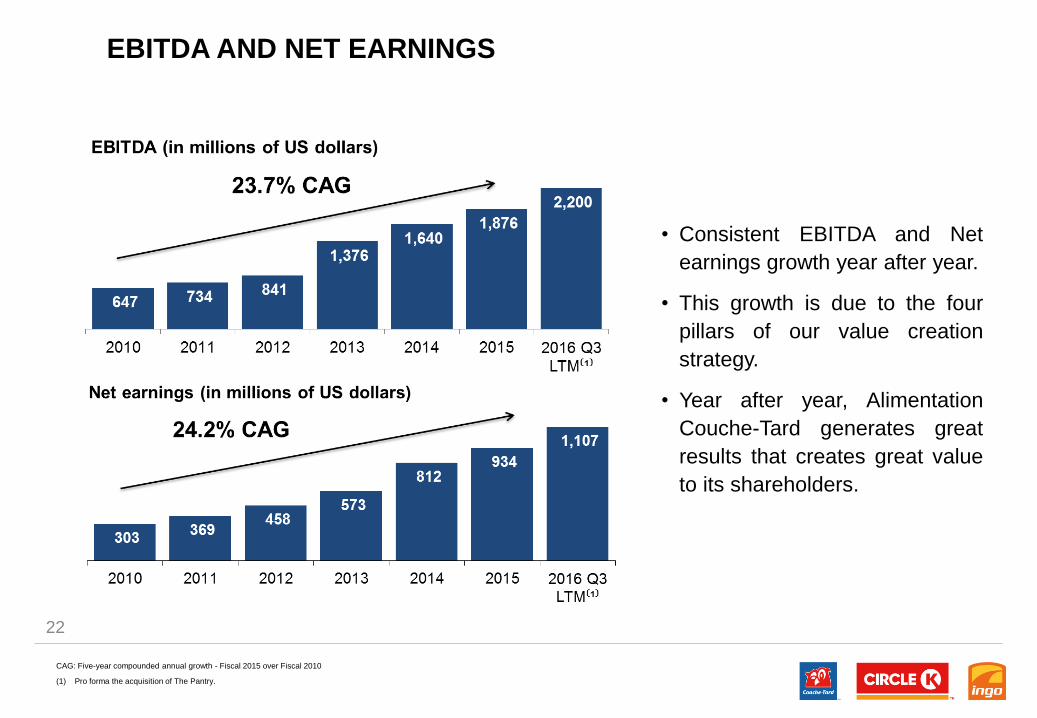

EBITDA AND NET EARNINGS

CAG: Five-year compounded annual growth - Fiscal 2015 over Fiscal 2010

(1) Pro forma the acquisition of The Pantry.

• Consistent EBITDA and Net

earnings growth year after year.

• This growth is due to the four

pillars of our value creation

strategy.

• Year after year, Alimentation

Couche-Tard generates great

results that creates great value

to its shareholders.

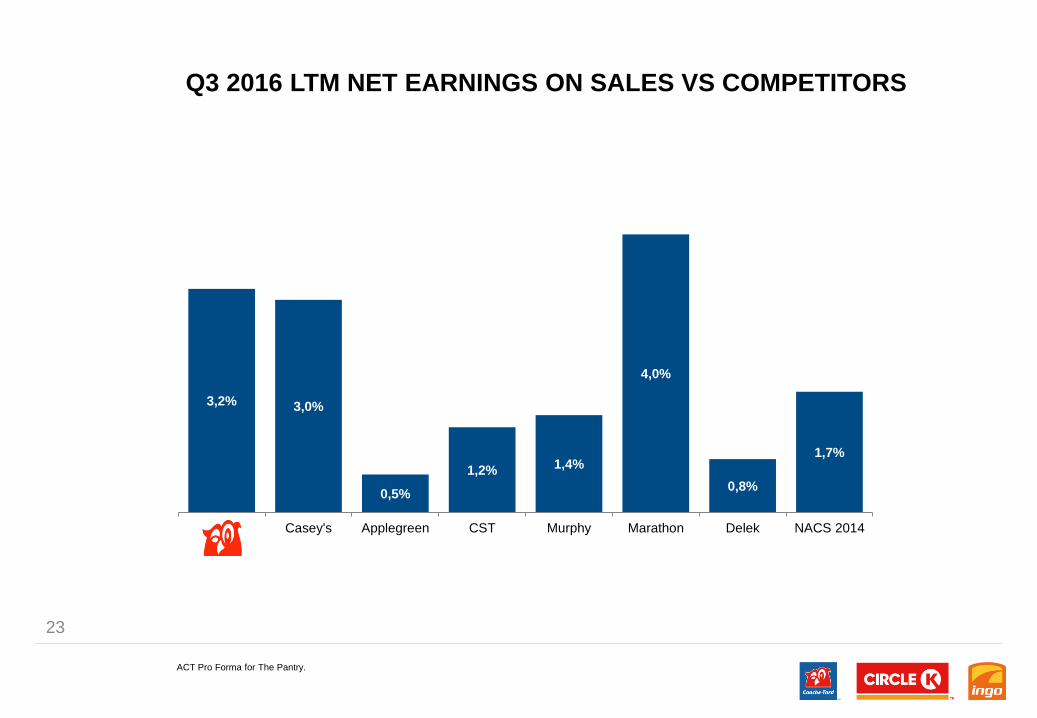

3,2% 3,0%

0,5%

1,2% 1,4%

4,0%

0,8%

1,7%

Casey's Applegreen CST Murphy Marathon Delek NACS 2014

Q3 2016 LTM NET EARNINGS ON SALES VS COMPETITORS

23

ACT Pro Forma for The Pantry.

24

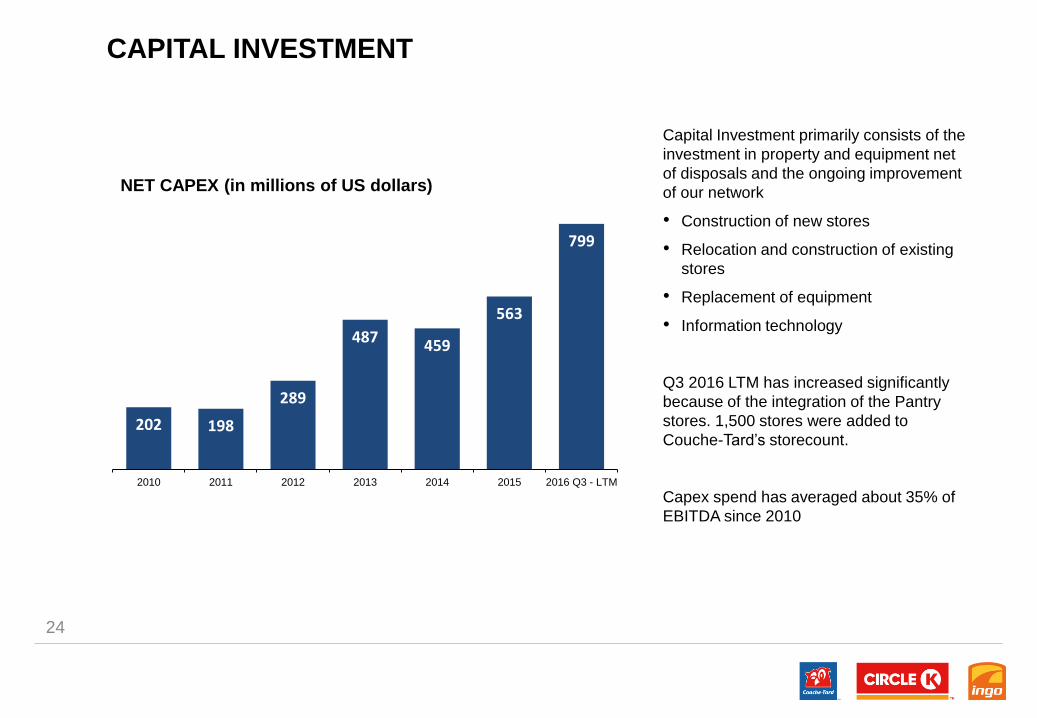

CAPITAL INVESTMENT

Capital Investment primarily consists of the

investment in property and equipment net

of disposals and the ongoing improvement

of our network

• Construction of new stores

• Relocation and construction of existing

stores

• Replacement of equipment

• Information technology

Q3 2016 LTM has increased significantly

because of the integration of the Pantry

stores. 1,500 stores were added to

Couche-Tard’s storecount.

Capex spend has averaged about 35% of

EBITDA since 2010

202 198

289

487 459

563

799

2010 2011 2012 2013 2014 2015 2016 Q3 - LTM

NET CAPEX (in millions of US dollars)

25

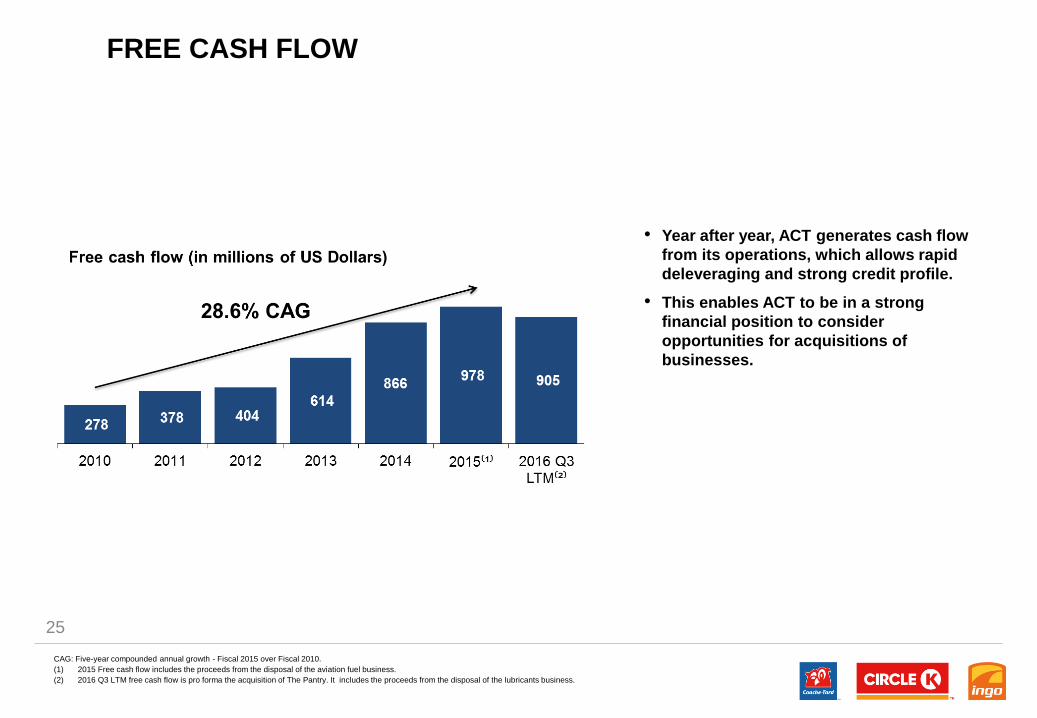

FREE CASH FLOW

CAG: Five-year compounded annual growth - Fiscal 2015 over Fiscal 2010.

(1) 2015 Free cash flow includes the proceeds from the disposal of the aviation fuel business.

(2) 2016 Q3 LTM free cash flow is pro forma the acquisition of The Pantry. It includes the proceeds from the disposal of the lubricants business.

• Year after year, ACT generates cash flow

from its operations, which allows rapid

deleveraging and strong credit profile.

• This enables ACT to be in a strong

financial position to consider

opportunities for acquisitions of

businesses.

26

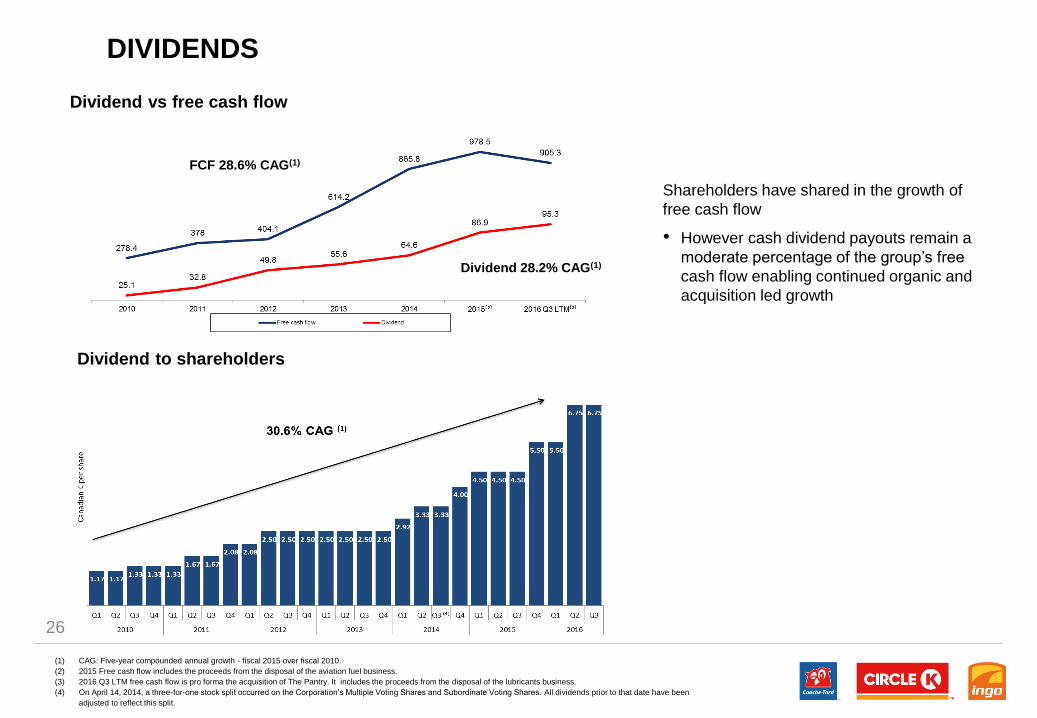

DIVIDENDS

(1) CAG: Five-year compounded annual growth - fiscal 2015 over fiscal 2010.

(2) 2015 Free cash flow includes the proceeds from the disposal of the aviation fuel business.

(3) 2016 Q3 LTM free cash flow is pro forma the acquisition of The Pantry. It includes the proceeds from the disposal of the lubricants business.

(4) On April 14, 2014, a three-for-one stock split occurred on the Corporation’s Multiple Voting Shares and Subordinate Voting Shares. All dividends prior to that date have been

adjusted to reflect this split.

Shareholders have shared in the growth of

free cash flow

• However cash dividend payouts remain a

moderate percentage of the group’s free

cash flow enabling continued organic and

acquisition led growth

Dividend to shareholders

Dividend vs free cash flow

FCF 28.6% CAG(1)

Dividend 28.2% CAG(1)

27

CAPITAL STRUCTURE

(1) Pro Forma The Pantry

Couche-Tard’s debt fluctuates primarily

with acquisitions, followed by strong

cash flow paying down debt

• Adjusted debt / adjusted EBITDAR

ratio includes lease obligations

• Couche-Tard’s term revolving

unsecured credit facilities include

financial covenants for :

Leverage – the ratio of net debt to

EBITDA for the four most recent

quarters

Interest Coverage – the ratio of

EBITDA to total interest paid for

the four most recent quarters

• Couche-Tard is in compliance with

these covenants

ADJUSTED NET DEBT/ ADJUSTED EBITDAR

TOTAL CAPITALIZATION

28

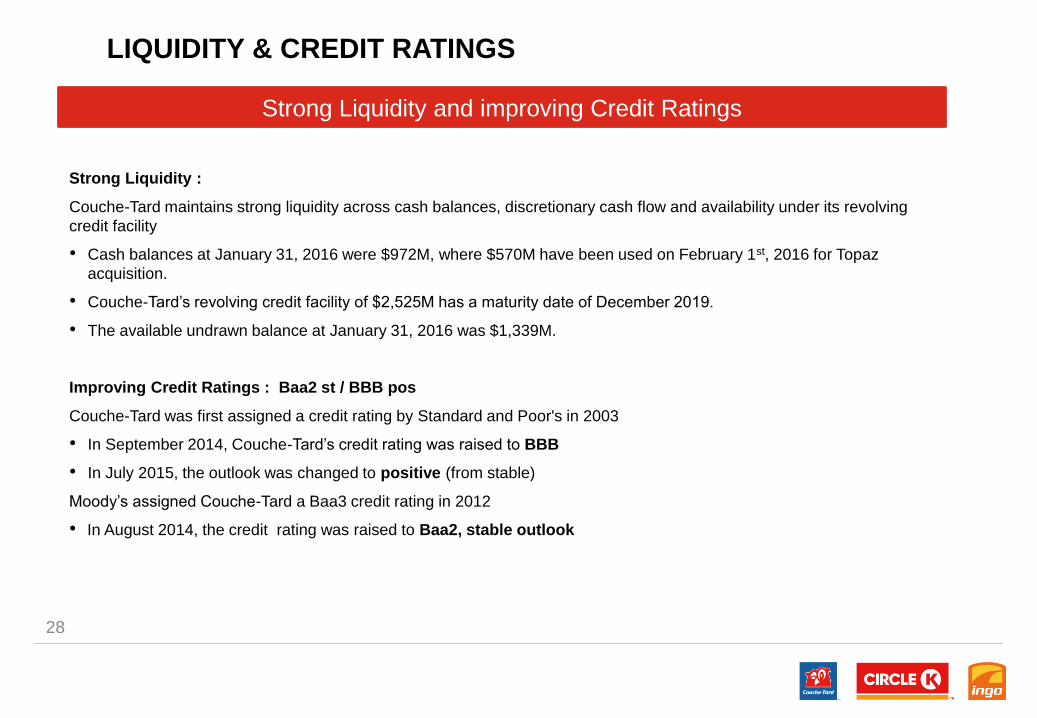

LIQUIDITY & CREDIT RATINGS

Strong Liquidity :

Couche-Tard maintains strong liquidity across cash balances, discretionary cash flow and availability under its revolving

credit facility

• Cash balances at January 31, 2016 were $972M, where $570M have been used on February 1st, 2016 for Topaz

acquisition.

• Couche-Tard’s revolving credit facility of $2,525M has a maturity date of December 2019.

• The available undrawn balance at January 31, 2016 was $1,339M.

Improving Credit Ratings : Baa2 st / BBB pos

Couche-Tard was first assigned a credit rating by Standard and Poor's in 2003

• In September 2014, Couche-Tard’s credit rating was raised to BBB

• In July 2015, the outlook was changed to positive (from stable)

Moody’s assigned Couche-Tard a Baa3 credit rating in 2012

• In August 2014, the credit rating was raised to Baa2, stable outlook

Strong Liquidity and improving Credit Ratings

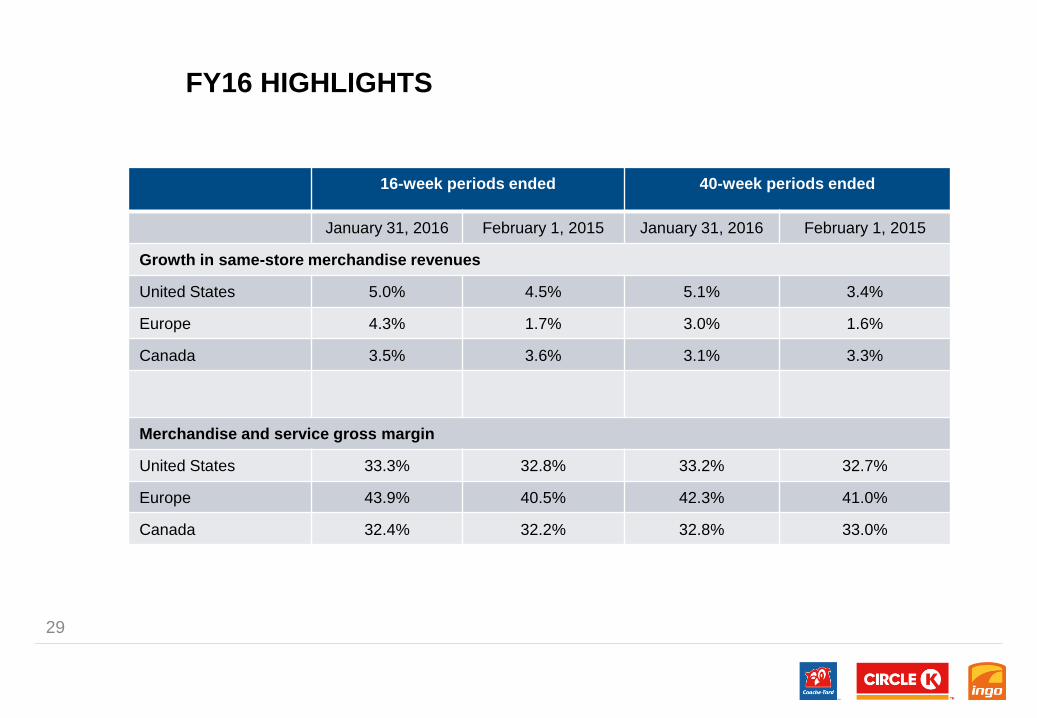

FY16 HIGHLIGHTS

29

16-week periods ended 40-week periods ended

January 31, 2016 February 1, 2015 January 31, 2016 February 1, 2015

Growth in same-store merchandise revenues

United States 5.0% 4.5% 5.1% 3.4%

Europe 4.3% 1.7% 3.0% 1.6%

Canada 3.5% 3.6% 3.1% 3.3%

Merchandise and service gross margin

United States 33.3% 32.8% 33.2% 32.7%

Europe 43.9% 40.5% 42.3% 41.0%

Canada 32.4% 32.2% 32.8% 33.0%

FY16 HIGHLIGHTS

30

16-week periods ended 40-week periods ended

January 31, 2016 February 1, 2015 January 31, 2016 February 1, 2015

Same-store motor fuel volume growth

United States 6.2% 2.8% 7.5% 2.3%

Europe 2.9% 2.1% 3.1% 2.0%

Canada (0.5%) (0.5%) 1.4% (0.5%)

Total motor fuel volume

United States (millions of

gallons)

2,177.6 1,491.3 5,557.8 3,720.3

Europe (millions of litres) 2,544.1 2,455.1 6,551.8 6,400.0

Canada (millions of litres) 918.8 904.1 2,399.8 2,326.4

Motor fuel gross margin

United States (US cents per

gallon)

19.90 24.93 21.18 24.15

Europe (US cents per litre) 8.69 9.81 9.26 10.90

Canada (CA cents per litre) 6.29 6.12 6.50 6.39

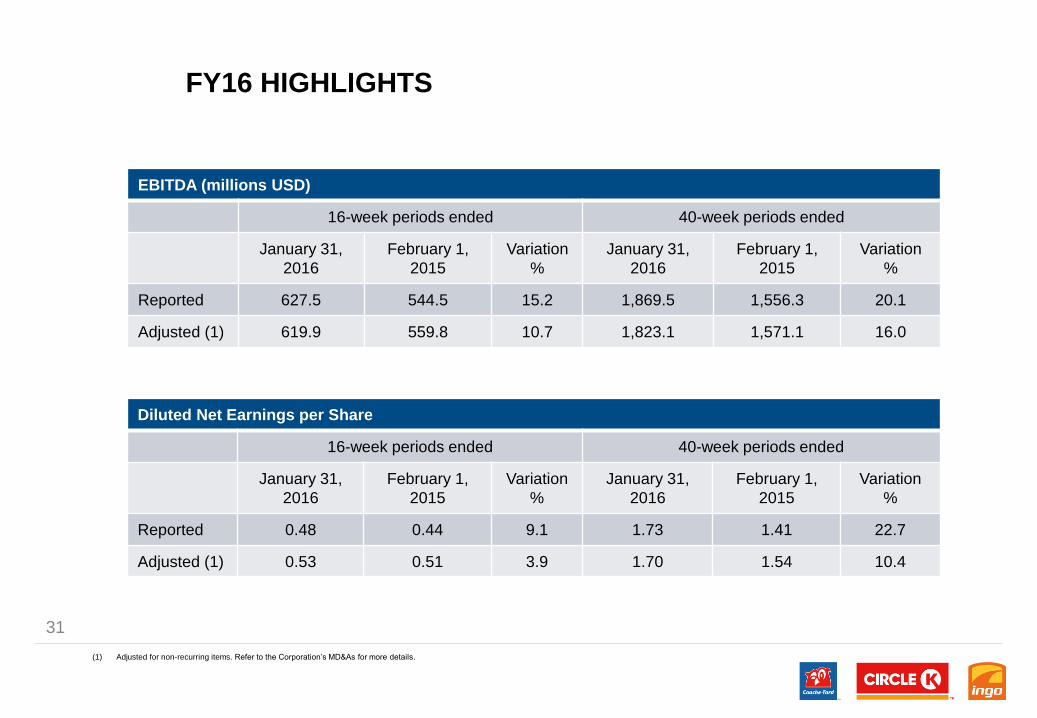

FY16 HIGHLIGHTS

31

Diluted Net Earnings per Share

16-week periods ended 40-week periods ended

January 31,

2016

February 1,

2015

Variation

%

January 31,

2016

February 1,

2015

Variation

%

Reported 0.48 0.44 9.1 1.73 1.41 22.7

Adjusted (1) 0.53 0.51 3.9 1.70 1.54 10.4

(1) Adjusted for non-recurring items. Refer to the Corporation’s MD&As for more details.

EBITDA (millions USD)

16-week periods ended 40-week periods ended

January 31,

2016

February 1,

2015

Variation

%

January 31,

2016

February 1,

2015

Variation

%

Reported 627.5 544.5 15.2 1,869.5 1,556.3 20.1

Adjusted (1) 619.9 559.8 10.7 1,823.1 1,571.1 16.0

FY16 HIGHLIGHTS

32

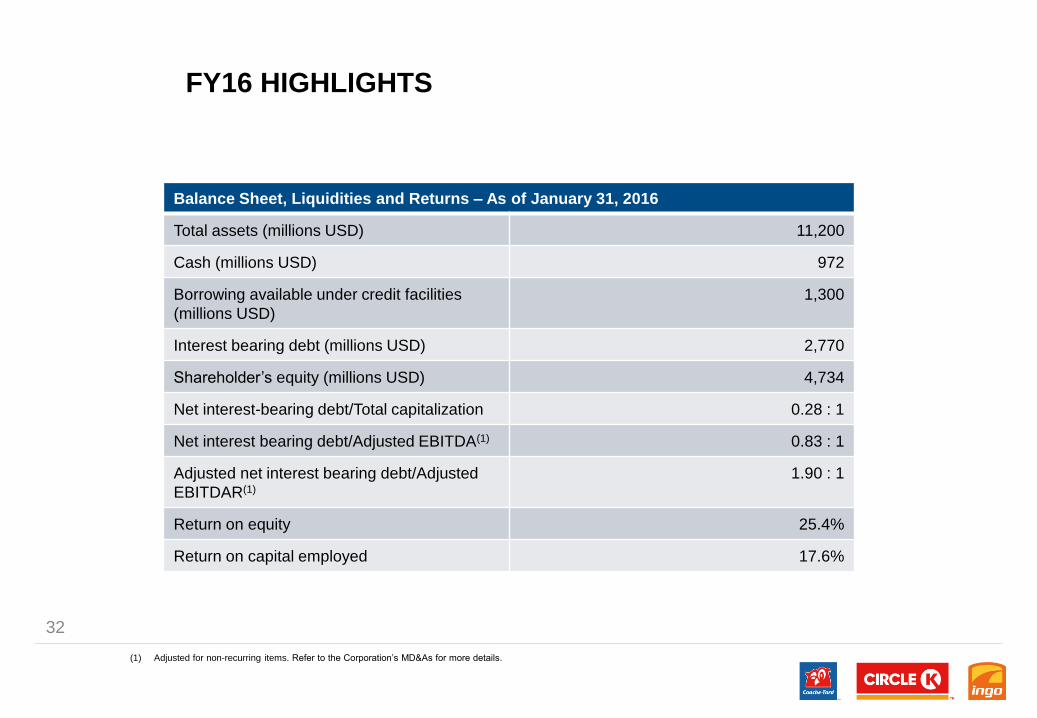

(1) Adjusted for non-recurring items. Refer to the Corporation’s MD&As for more details.

Balance Sheet, Liquidities and Returns – As of January 31, 2016

Total assets (millions USD) 11,200

Cash (millions USD) 972

Borrowing available under credit facilities

(millions USD)

1,300

Interest bearing debt (millions USD) 2,770

Shareholder’s equity (millions USD) 4,734

Net interest-bearing debt/Total capitalization 0.28 : 1

Net interest bearing debt/Adjusted EBITDA(1) 0.83 : 1

Adjusted net interest bearing debt/Adjusted

EBITDAR(1)

1.90 : 1

Return on equity 25.4%

Return on capital employed 17.6%

ALIMENTATION COUCHE-TARD INC.

STRATEGY &

VALUE CREATION

EXPERIENCED MANAGEMENT TEAM

Brian P. Hannasch

President and Chief

Executive OfficerPLACE IMAGE

HERE

Jean Bernier

Group President Fuel

Americas and Operations

North-East

PLACE IMAGE

HERE

Darrell Davis

Senior Vice-President,

OperationsPLACE IMAGE

HERE

President and Chief

Executive Officer since 2014.

Previously Chief Operating

Officer since 2010 and

Senior Vice-President, U.S.

Operations from 2008 to

2010.

Appointed Group President

Fuel Americas and

Operations North-East on

July 30, 2012. He has over 25

years of experience in the

convenience store, fuel and

grocery store sectors of the

retail industry.

Appointed Senior Vice-

President, Operations in

May 2012. Previously, he

had been Vice-President

Operations, Florida since

March 2011.

Geoffrey C. Haxel

Senior Vice-President,

OperationsPLACE IMAGE

HEREAppointed Senior Vice-

President, Operations in

January 2011. He was

formerly Vice-President,

Operations, U.S. Arizona

Region since December

2003.

Hans-Olav Høidahl

Executive Vice-President,

ScandinaviaPLACE IMAGE

HERE

Jørn Madsen

Executive Vice-President,

Central & Eastern EuropePLACE IMAGE

HERE

Alex Miller

Senior Vice President,

Global FuelsPLACE IMAGE

HEREAppointed Executive Vice-

President, Scandinavia on

October 1, 2010. He was

formerly Vice President for

Energy Europe in the Statoil

Group since 2006.

Appointed Executive Vice-

President, Central & Eastern

Europe on October 1, 2010.

He was formerly Vice

President for country

operations in Statoil Energy &

Retail since 2007. He joined

Statoil in 1990.

Appointed Senior Vice-

President Global Fuels on

February 16, 2016.

Previously, he had been Vice-

President North American

Fuels since October 2012.

He joined Couche-Tard in

January 2012 as Director of

Operations Midwest.

Jacob Schram

Group President,

European OperationsPLACE IMAGE

HEREAppointed Group President,

European Operations in

June, 2012. He was

formerly Chief Executive

Officer for Statoil Fuel &

Retail from October 1st,

2010. He joined Statoil in

1996.

Claude Tessier

Chief Financial Officer

PLACE IMAGE

HERE

Dennis Tewell

Senior Vice-President,

OperationsPLACE IMAGE

HERE

Claude Tessier, CPA, CA, is

Couche-Tard’s Chief Financial

Officer since February 2016.

Beforehand, Mr. Tessier was

President of the IGA

Operations Business Unit part

of Sobeys since 2012.

Appointed Senior Vice-

President, Operations in June

2013. Prior to his current

appointment, He held the

position of Vice-President,

Worldwide Franchise as he

joined Couche-Tard in January

2011.

Alain Bouchard

Founder and Executive

Chairman of the BoardPLACE IMAGE

HEREOn September 24, 2014, Mr.

Bouchard stepped down as

President and Chief

Executive Officer and took on

a new role as Founder and

Executive Chairman of the

Board of Directors.

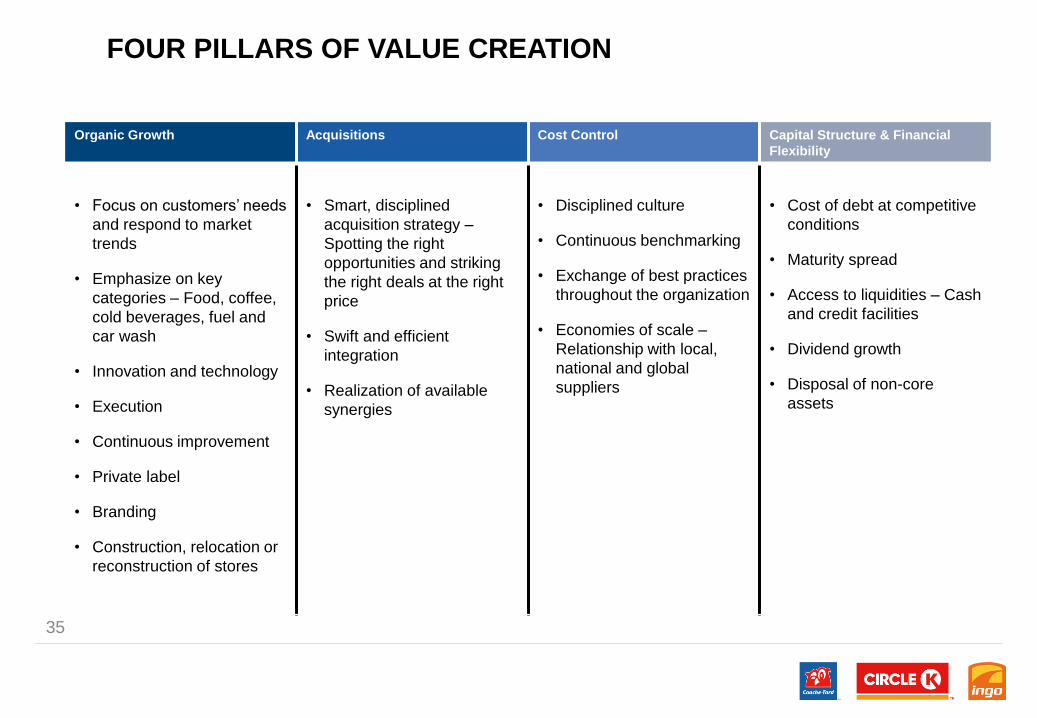

FOUR PILLARS OF VALUE CREATION

35

Organic Growth Acquisitions Cost Control Capital Structure & Financial

Flexibility

• Focus on customers’ needs

and respond to market

trends

• Emphasize on key

categories – Food, coffee,

cold beverages, fuel and

car wash

• Innovation and technology

• Execution

• Continuous improvement

• Private label

• Branding

• Construction, relocation or

reconstruction of stores

• Smart, disciplined

acquisition strategy –

Spotting the right

opportunities and striking

the right deals at the right

price

• Swift and efficient

integration

• Realization of available

synergies

• Disciplined culture

• Continuous benchmarking

• Exchange of best practices

throughout the organization

• Economies of scale –

Relationship with local,

national and global

suppliers

• Cost of debt at competitive

conditions

• Maturity spread

• Access to liquidities – Cash

and credit facilities

• Dividend growth

• Disposal of non-core

assets

ALIMENTATION COUCHE-TARD INC.

ORGANIC GROWTH

Value Creation

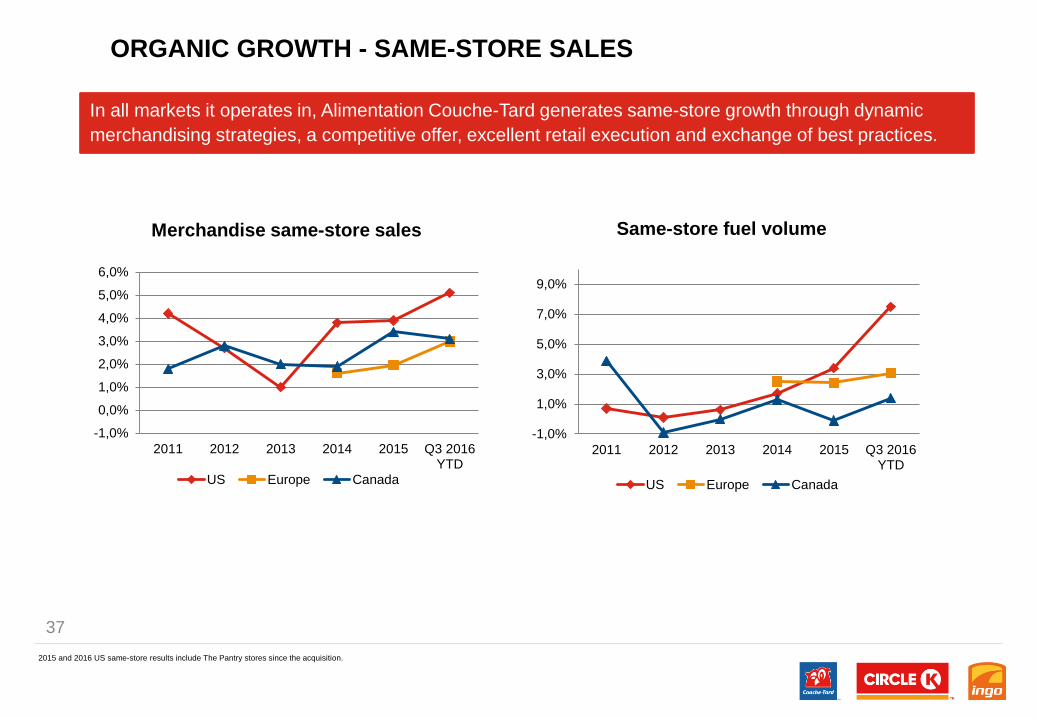

ORGANIC GROWTH - SAME-STORE SALES

In all markets it operates in, Alimentation Couche-Tard generates same-store growth through dynamic

merchandising strategies, a competitive offer, excellent retail execution and exchange of best practices.

2015 and 2016 US same-store results include The Pantry stores since the acquisition.

37

-1,0%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

2011 2012 2013 2014 2015 Q3 2016YTD

Merchandise same-store sales

US Europe Canada

-1,0%

1,0%

3,0%

5,0%

7,0%

9,0%

2011 2012 2013 2014 2015 Q3 2016YTD

Same-store fuel volume

US Europe Canada

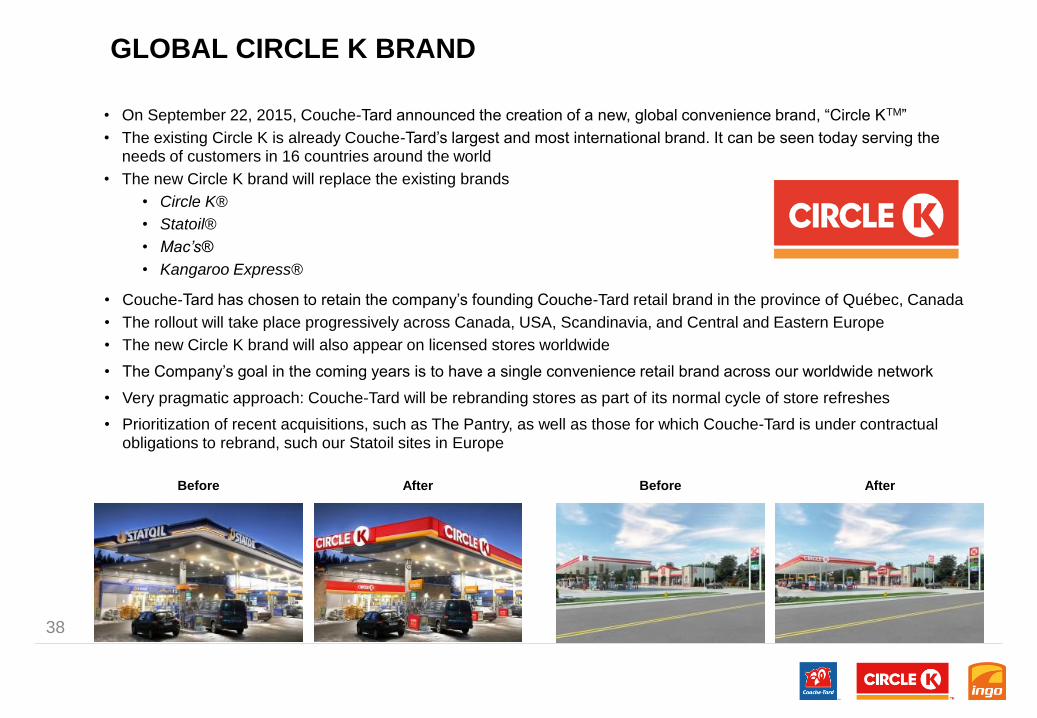

GLOBAL CIRCLE K BRAND

• On September 22, 2015, Couche-Tard announced the creation of a new, global convenience brand, “Circle KTM”

• The existing Circle K is already Couche-Tard’s largest and most international brand. It can be seen today serving the needs of customers in 16 countries around the world

• The new Circle K brand will replace the existing brands

• Circle K®

• Statoil®

• Mac’s®

• Kangaroo Express®

38

• Couche-Tard has chosen to retain the company’s founding Couche-Tard retail brand in the province of Québec, Canada

• The rollout will take place progressively across Canada, USA, Scandinavia, and Central and Eastern Europe

• The new Circle K brand will also appear on licensed stores worldwide

• The Company’s goal in the coming years is to have a single convenience retail brand across our worldwide network

• Very pragmatic approach: Couche-Tard will be rebranding stores as part of its normal cycle of store refreshes

• Prioritization of recent acquisitions, such as The Pantry, as well as those for which Couche-Tard is under contractual obligations to rebrand, such our Statoil sites in Europe

Before After Before After

ALIMENTATION COUCHE-TARD INC.

ACQUISITIONS

Value Creation

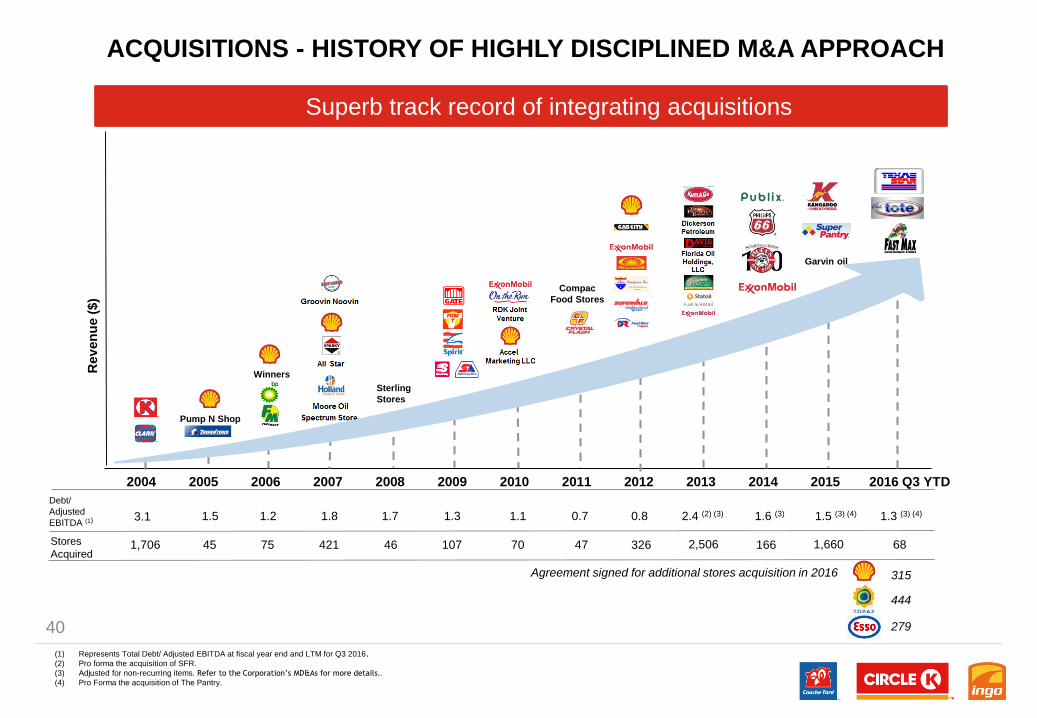

ACQUISITIONS - HISTORY OF HIGHLY DISCIPLINED M&A APPROACH

40

Rev

en

ue (

$)

Debt/

Adjusted

EBITDA (1)

Stores

Acquired

Agreement signed for additional stores acquisition in 2016 315

Superb track record of integrating acquisitions

Pump N Shop

Winners

Sterling

Stores

Compac

Food Stores

Garvin oil

3.1

1,706 45

1.5

75 421 46 107 70 47 326

1.2 1.8 1.7 1.3 1.1 0.7 0.8

2,506

2.4 (2) (3)

166

1.6 (3)

1,660

1.5 (3) (4)

68

1.3 (3) (4)

(1) Represents Total Debt/ Adjusted EBITDA at fiscal year end and LTM for Q3 2016.

(2) Pro forma the acquisition of SFR.

(3) Adjusted for non-recurring items. Refer to the Corporation’s MD&As for more details..

(4) Pro Forma the acquisition of The Pantry.

444

279

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q3 YTD

TOPAZ SNAPSHOT

41

• Leading convenience and fuel retailer in Ireland, made up of 444 stations including its recently acquired Esso station network

• 158 are operated by Topaz and 286 by dealers. Company owns underlying real estate for about 100 sites

• Also commercial fuels operation, with over 30 depots and two owned terminals

• Extensive and attractive convenience and fuel network, with good locations, quality forecourts and stores, an excellent food

offering and very professional teams

• Allows Couche-Tard to expand our geographic footprint into what, today, is one of Europe’s best performing economies

• Great strategic fit for Couche-Tard and it would strengthen its position in Western Europe

• Superior growth anticipated in in-store sales and fuel volume through the improvement of operations; sharing of business

awareness and each company’s best practices; and better supply conditions

• Expected cost reduction synergies from integration into existing European platform

ESSO CANADA SNAPSHOT

• In March 2016, Couche-Tard announced an agreement to acquire 279 Esso-branded fuel and convenience sites in Canada

• 229 sites are located in the province of Ontario, the majority of which in the Greater Toronto Area

• 50 sites are located in the province of Québec, in the Greater Montréal Area, including the south shore of Montréal

• The agreement also includes 13 land banks and two dealer sites, as well as a long-term supply agreement for Esso branded

fuel

• Allows Couche-Tard to expand it’s geographic footprint into the Greater Toronto Area and the Montréal area

• Great strategic fit for Couche-Tard and it would strengthen its position in Canada

42

ALIMENTATION COUCHE-TARD INC.

COST CONTROL

Value Creation

DISCPLINED AND RIGOROUS COST CONTROL

44

Cost leadership is well anchored throughout the organization

(1) Excluding credit card fees. Adjusted for currency translation, impact from acquisitions, acquisition costs as well as, from time to time, for certain non-recurring costs. Refer to the

Corporation’s annual MD&As for more details.

• Cost synergies from major acquisitions :

SFRObjective $150-$200M

Realized $199M

The PantryObjective $85M

Identified $63M

Realized $43M

ALIMENTATION COUCHE-TARD INC.

CAPITAL STRUCTURE

& FINANCIAL

FLEXIBILITY

Value Creation

46

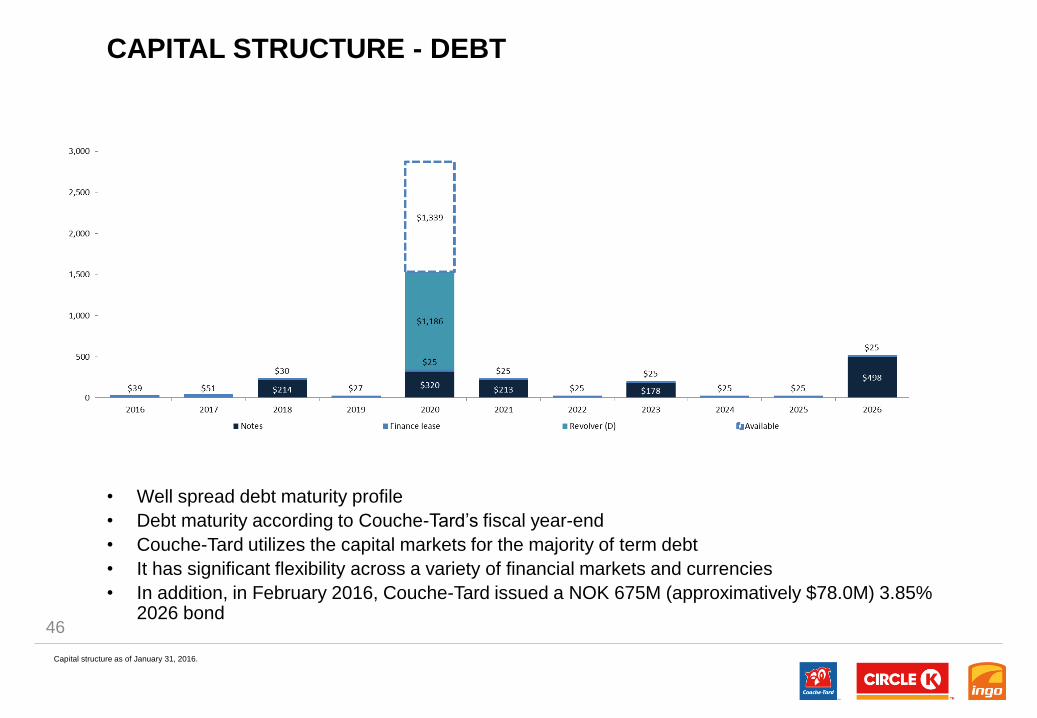

• Well spread debt maturity profile

• Debt maturity according to Couche-Tard’s fiscal year-end

• Couche-Tard utilizes the capital markets for the majority of term debt

• It has significant flexibility across a variety of financial markets and currencies

• In addition, in February 2016, Couche-Tard issued a NOK 675M (approximatively $78.0M) 3.85% 2026 bond

CAPITAL STRUCTURE - DEBT

Capital structure as of January 31, 2016.

AVERAGE INTEREST RATE ON DEBT

47

Competitive and attractive cost of debt

Based on latest Q4 information except for ACT which is as per January 31, 2016.

48

CAPITAL STRUCTURE – ADJUSTED NET DEBT/EBITDAR

• Our growth strategy is supported by our commitment to a strong capital structure

• Acquisitions are undertaken with the objective of rapid deleveraging

• Our credit ratings were raised to Baa2 / BBB in Q3 2014 and S&P revised to positive outlook in July 2015

(1) Pro Forma The Pantry.

Strong Capital Discipline

Industry Average

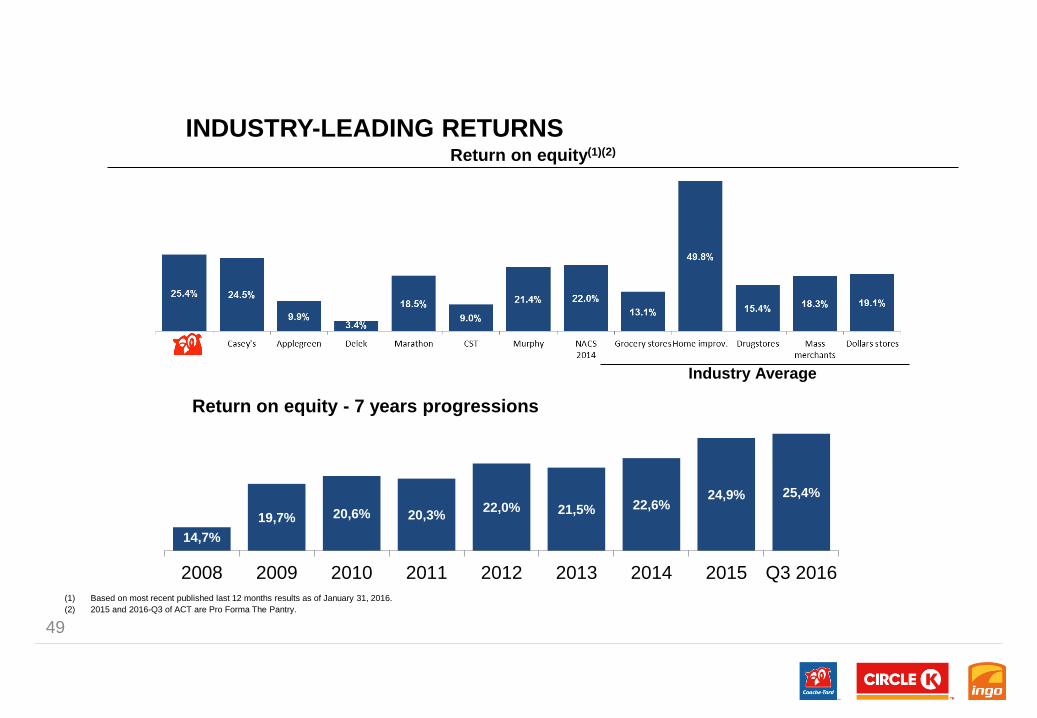

INDUSTRY-LEADING RETURNS

49

Return on equity(1)(2)

(1) Based on most recent published last 12 months results as of January 31, 2016.

(2) 2015 and 2016-Q3 of ACT are Pro Forma The Pantry.

14,7%

19,7% 20,6% 20,3%22,0% 21,5% 22,6%

24,9% 25,4%

2008 2009 2010 2011 2012 2013 2014 2015 Q3 2016

Return on equity - 7 years progressions

50

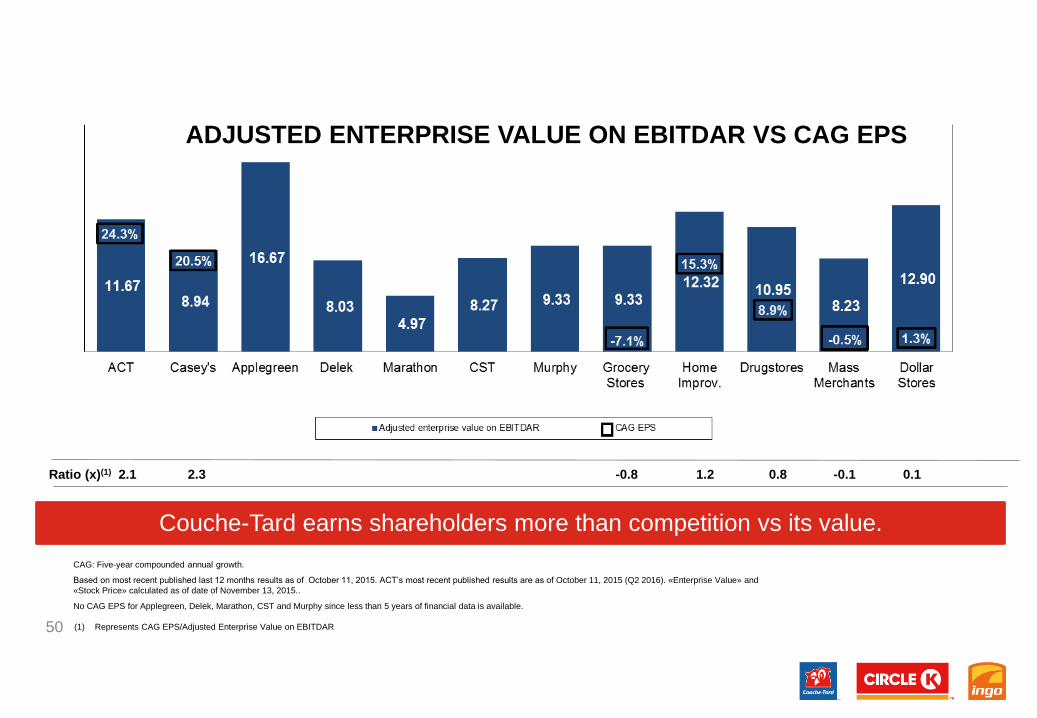

ADJUSTED ENTERPRISE VALUE ON EBITDAR VS CAG EPS

Couche-Tard earns shareholders more than competition vs its value.

CAG: Five-year compounded annual growth.

Based on most recent published last 12 months results as of October 11, 2015. ACT’s most recent published results are as of October 11, 2015 (Q2 2016). «Enterprise Value» and

«Stock Price» calculated as of date of November 13, 2015..

No CAG EPS for Applegreen, Delek, Marathon, CST and Murphy since less than 5 years of financial data is available.

(1) Represents CAG EPS/Adjusted Enterprise Value on EBITDAR

Ratio (x)(1) 2.1 2.3 -0.8 1.2 0.8 -0.1 0.1

ALIMENTATION COUCHE-TARD INC.

APPENDIX

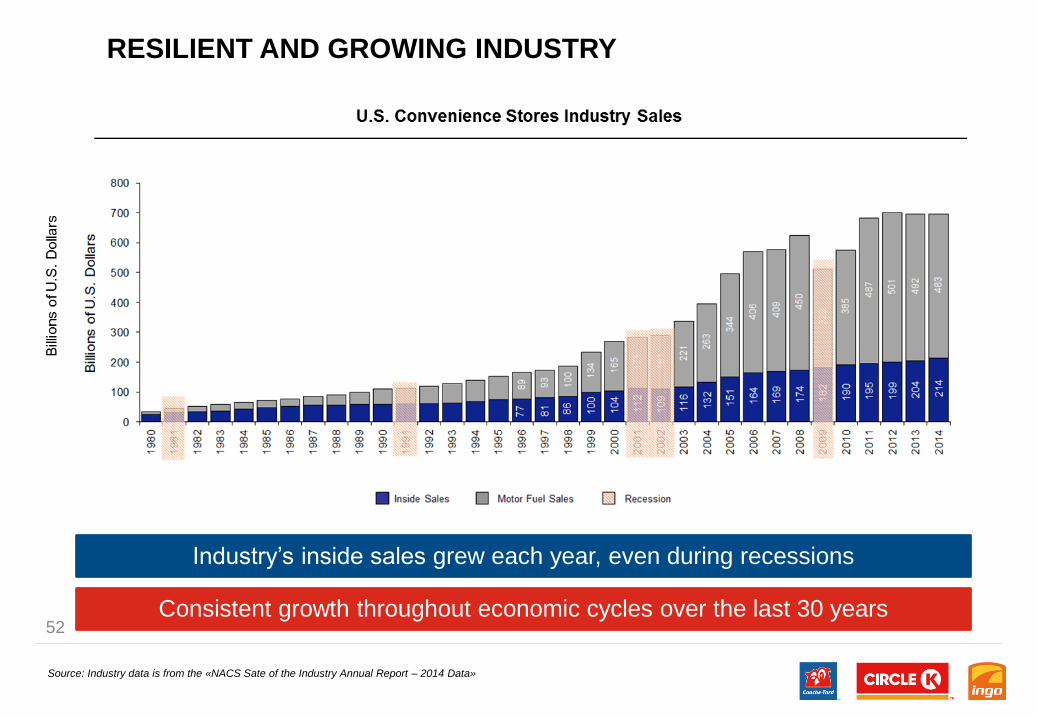

RESILIENT AND GROWING INDUSTRY

52

Industry’s inside sales grew each year, even during recessions

Consistent growth throughout economic cycles over the last 30 years

Source: Industry data is from the «NACS Sate of the Industry Annual Report – 2014 Data»