Embed Size (px)

Citation preview

Investor DayLondon, 16th May 2019

1© National Bank of Greece

Investor Presentation – May 2019

Disclaimer

This corporate presentation has been prepared by National Bank of Greece S.A. (the Bank) for the Investor Day held by the Bank on 16/05/2019, in order to present the strategic objectives of the Bank for the period 2019 – 2022. It

is not and should not be construed as a disclosure of regulated information as defined in Directive 2004/109.

Not an Offer to Sale

The information contained herein is not and must not be construed to be an offer to sale or to purchase or an invitation or any type of solicitation or a recommendation or an advice to invest in any way on the shares or any other

security issued or to be issued by the Bank. It has not been prepared to assist prospective investors in making their own evaluation of the Bank and does not purport to be all-inclusive or complete or to contain all of the information

a prospective or existing investor may need or want to have. As such, the information contained in this presentation cannot and should not be relied upon as advice to buy or sell or hold such securities or as an offer to sell such

securities. This presentation does not take into account nor does it provide any tax, legal or investment advice or opinion regarding the specific investment objectives or financial situation of any person. In all cases, any interested

person should conduct his or her own investigation and analysis of the Bank and the data set forth in this presentation. The Bank makes no representation or warranty as to the accuracy or completeness of the information contained

in this presentation and shall not have any liability for any statements or representations (expressed or implied) made herein and information contained herein, or for any omissions from, this information. Neither the Bank nor any of

our representatives shall have any liability whatsoever, under contract, tort, or otherwise, to any person resulting from the use of the information in this presentation.

The Bank does not assume any liability to update any of the information included or statement made herein. The Bank reserves the right to amend or replace the information contained herein, in part or entirely, at any time, without

undertaking the obligation to formally inform investors that such amendment or replacement has been made. Additionally, the Bank undertakes no obligation to comment on the expectations of, or statements made by, third parties

in respect of the matters discussed in this presentation. In any case all readers of this presentation are invited to read it in the future in combination with all future announcements made by the Bank on material events and inside

information, in general, pursuant to applicable legislation.

Strategic objectives and Financial Targets included in the Presentation

This presentation does not contain any projections or forecasts for the period 2019 – 2022. It outlines the most important strategic objectives and financial targets of the Bank’s management as of the date of the presentation. Such

strategic objectives and targets, as well as other statements made herein regarding the Bank’s business and operations, results of operation, financial condition and capital adequacy and risk management practices are based on the

opinions, estimates and reasonable assumptions of the Bank’s management regarding, inter alia, the relevant macroeconomic conditions, at the date the statements are made and as reasonably anticipated based on available data at

that date. Such opinions, estimates and assumptions are inherently subjective and uncertain, and the relevant target and future statements contained in the presentation are subject to a variety of risks and uncertainties and other

factors, most of which are outside the control of the Bank, that could cause actual events or results to differ materially from the targeted performance of the Bank as expressed or implied in this presentation. Although we believe

that such targets are reasonable, there can be no assurance that such targets will materialize in the future as described in this presentation in all material respect. We cannot guarantee future results, level of activity, performance or

achievements and there is no representation that the actual results will be the same, in whole or in part, as those set out in the presentation. It is also noted that past performance of similar actions undertaken does not guarantee

future results. Important factors that could cause actual results to differ materially from the targets set and future statements included in this presentation, are, inter alia:

– the heavily regulated industry in which the Bank pursues its business activity, including capital adequacy rules and the relevant loan portfolio, capital and liquidity tests and reviews as well conducted by national and

supranational regulatory authorities;

– the relevant market conditions, including the macroeconomic environment in Greece and the European Union;

– our ability to manage risks inherent in the Bank’s operations;

– the restrictions to which the Bank’s operational autonomy is subject as a recipient of state aid and shareholder expectations and special rights of the HFSF, a 40% shareholder.

Readers are cautioned that this list of factors should not be construed as exhaustive. All targets and future statements contained in this presentation are expressly qualified by this cautionary statement. Except as and to the extent

required by law, the Bank undertakes no obligation to update or revise publicly any such statement, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect

the occurrence of unanticipated events.

2© National Bank of Greece

Investor Presentation – May 2019

AGENDA

Introduction Costas Michaelides | Chairman

Strategic objectives 2019–2022Pavlos Mylonas | Chief Executive Officer

Financial targets

Clean-up the balance sheet Fotini Ioannou | Head of Troubled Assets Group

Boost revenue generationChristina Theofilidi | Head of Retail Banking

Vassilis Karamouzis | AGM Corporate & Investment Banking

Enablers: people, technology, processesEvi Hatzioannou | Head of Human Resources

Stratos Molyviatis | Chief Information Officer

Ethniki180: Transformation Program Ernestos Panayiotou | Chief Transformation Officer

Q&A

3© National Bank of Greece

Investor Presentation – May 2019

AGENDA

Introduction Costas Michaelides | Chairman

Strategic objectives 2019–2022Pavlos Mylonas | Chief Executive Officer

Financial targets

Clean-up the balance sheet Fotini Ioannou | Head of Troubled Assets Group

Boost revenue generationChristina Theofilidi | Head of Retail Banking

Vassilis Karamouzis | AGM Corporate & Investment Banking

Enablers: people, technology, processesEvi Hatzioannou | Head of Human Resources

Stratos Molyviatis | Chief Information Officer

Ethniki180: Transformation Program Ernestos Panayiotou | Chief Transformation Officer

Q&A

4© National Bank of Greece

Investor Presentation – May 2019

Key remarks

Our team: a new management team, fully aligned to the strategy, with clear roles and responsibilities3

Our starting point: large client base, trusted brand and the strongest asset quality and liquidity in the

Greek market2

Our strategic priorities: broad alignment on the challenges and a transformation plan developed

bottom-up to address them4

Our NBG in 2022: a clean and profitable bank - the Greek bank of choice6

Our operating environment: macroeconomic tailwinds and recovery of the banking fundamentals1

Our delivery engine: a unique, bank-wide transformation program with clear accountabilities and strong

execution discipline5

5© National Bank of Greece

Investor Presentation – May 2019

Macroeconomic tailwinds and recovery of banking fundamentals

2020

19.3

2018

17.7

20212019

16.515.5 14.8

2022

2.01.9

2018 2021

1.8

20202019

1.8 1.7

2022

2022

106109

2018

100103

20202019 2021

112

373296 293 301 311

20202018 20212019 2022

20222018 2019 2020 2021

3.6

1.9

3.9 3.5 3.2

20212018 20193 2020 2022 2023

-13.5

11.55.9 6.2 6.4 6.6

1. Operating environment

Greek 10yr

sovereign bond

spread over G.

Bund2

(bps)

Unemployment

rate (%)1

GDP growth (%)1

Gross fixed

capital formation

excl. residential

(nominal,

yoy growth)

Private sector

disposable

income

(nominal,

yoy growth)

Sources: ELSTAT, Focus Economics Consensus, NBG - Economic Analysis Division estimates

Sources: Bank of Greece, NBG - Economic Analysis Division estimates

Sources: Focus Economics, NBG - Economic Analysis Division estimates

House Price Index

(rebased to 2018)

Sources: ELSTAT, Focus Economics Consensus, NBG - Economic Analysis Division estimates

Sources: ELSTAT, Focus Economics Consensus, NBG - Economic Analysis Division estimates

Sources: ELSTAT, Focus Economics Consensus, NBG - Economic Analysis Division estimates

1. Average annual | 2. Average of quarterly spreads | 3. 2019 Fixed capital formation based on NBG economic analysis estimates, accounting for a positive base effect and transfer of public investments from 2018 to 2019

6© National Bank of Greece

Investor Presentation – May 2019

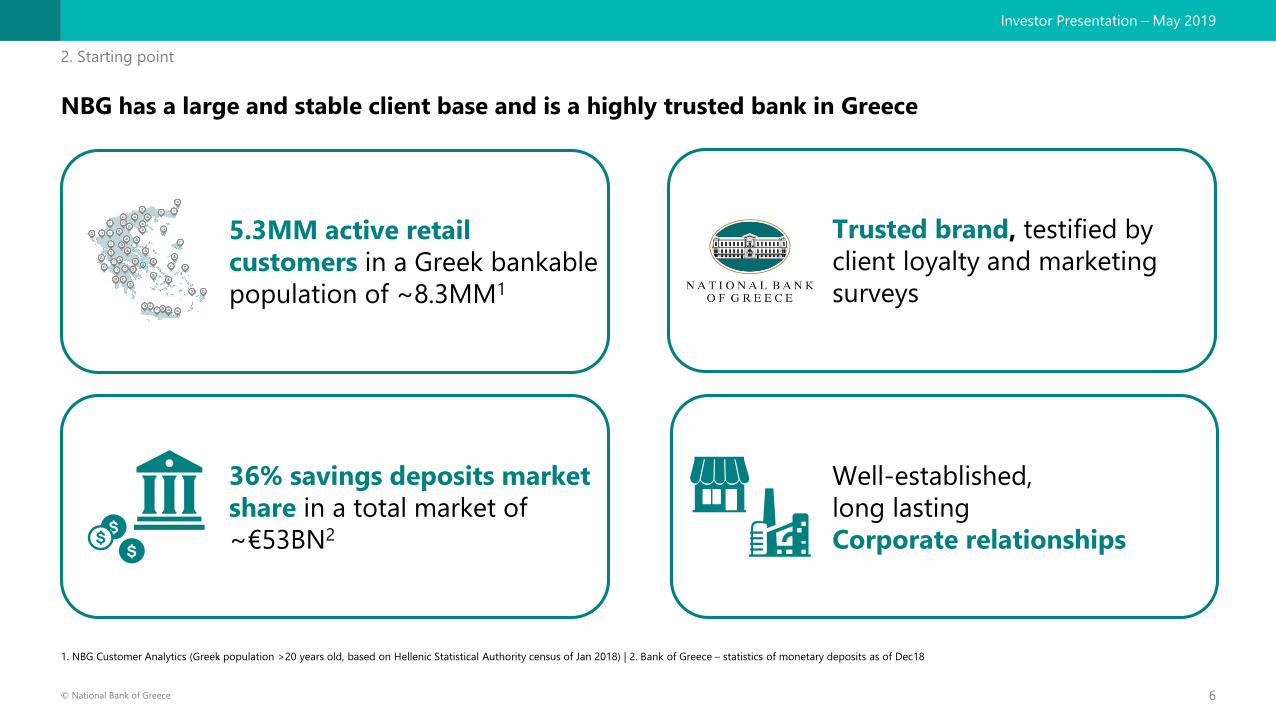

NBG has a large and stable client base and is a highly trusted bank in Greece

2. Starting point

36% savings deposits market

share in a total market of

~€53BN2

Well-established,

long lasting

Corporate relationships

5.3MM active retail

customers in a Greek bankable

population of ~8.3MM1

Trusted brand, testified by

client loyalty and marketing

surveys

1. NBG Customer Analytics (Greek population >20 years old, based on Hellenic Statistical Authority census of Jan 2018) | 2. Bank of Greece – statistics of monetary deposits as of Dec18

7© National Bank of Greece

Investor Presentation – May 2019

Cash coverage and low cost liquidity are our key strengths

Highest NPE coverage in the market Strongest liquidity position

Savings deposits2

€BN

11.4

Greek peers averageNBG

19.3

Loan to deposit ratio

%

70

100

Greek peers averageNBG

Gross NPE

Group, €BN

6.8

12.7

9.5

10.516.3

NBG Greek peers average

23.2

Unprovided

Provided

45%59%Total provision

coverage

1

Yield3 3bps

Market

share36%

LCR

NSFR

144%

108%

2. Starting point

Note: Group level 2018YE figures, except for saving deposits

1. Average of NPE stock for Greek systemic banks (excluding NBG group). Source: 2018YE financial reports | 2. Bank of Greece – statistics of monetary deposits as of Dec18 | 3. Average funding cost on savings deposits

8© National Bank of Greece

Investor Presentation – May 2019

A new management team committed to effect change

Kostas

Adamopoulos

Head of

Strategic

Transactions

Fotini

Ioannou

Head of

Troubled

Assets Group

Christina

Theofilidi

Head of Retail

Banking

Ioannis

Vagionitis

Chief Risk

Officer

Pavlos

Mylonas

Chief Executive

Officer

Chara

Dalekou

Head of

Marketing &

Communi-

cations

Panos

Dasmanoglou

Chief

Governance &

Compliance

Officer

Beate Randulf

Head of

Internal

Controls

Evi

Hatzioannou

Head of Human

Resources

Aris

Divaris

Head of

Operations

Stratos

Molyviatis

Chief

Information

Officer

Christos

Christodoulou

Chief Financial

Officer

Vassilis

Kavalos

Group

Treasurer

Ernestos

Panayiotou

Chief

Transformation

Officer

3. The team

George

Koutsoudakis

AGM Corporate

Banking

Vassilis

Karamouzis

AGM Corporate

& Investment

Banking

9© National Bank of Greece

Investor Presentation – May 2019

Our key challenges The opportunity

Elevated NPE levels Highest coverage in the market and a realistic plan to tackle the issue in place

High legacy cost base Areas of improvement identified and actions to capture efficiency gains planned

Low cross-selling Opportunities to increase fees and NII identified, strong brand and large client

base already in place

Outdated HR managementNew employee value proposition and performance management system expected

to boost productivity

Limited MIS visibility and staff

accountabilityUpgrades to planning and value-based-management infrastructure well under way

Limited digital penetrationInvestments to improve customer experience across channels, modernise

processes and support cost reduction

A

B

C

D

E

F

Our challenges are clear and require rapid and effective action

4. Strategic priorities

10© National Bank of Greece

Investor Presentation – May 2019

Our six strategic priorities for 2019-2022

CLEAN-UP

THE BALANCE

SHEET

MOBILISE OUR

PEOPLE

Front-load NPE clean-up delivering a

~5% NPE ratio

Reward performance and motivate our

people aligning individual objectives to

strategic goalsA D

IMPROVE

VISIBILITY &

CONTROL

ENHANCE

EFFICIENCY

& AGILITY

Complete FTE reductions and G&A

rationalisation supporting C:I drop to

~45%

Enhance client planning and steering tools

enabling value and risk-based decisionsB E

UPGRADE

TECHNOLOGY

INFRASTRUCTURE

BOOST

REVENUE

GENERATION

Improve sales and service orientation

growing non-risk income and shifting

transactions to digital channels

Invest to modernize the technology

infrastructure improving efficiency and

service levels

C F

4. Strategic priorities

11© National Bank of Greece

Investor Presentation – May 2019

NPE stock and coverage

2018YE, Group, €BN

A clean bank with an NPE ratio of ~5% in 2022

Strategic directions

• Material NPE reduction by 2020, driven by

sales in the consumer, SBL and corporate

portfolios

• More concessionary restructurings and

friendlier legal framework to increase

recoverable value in the mortgages portfolio

• Large mortgage securitisations in 2021–22,

when market conditions have further

improved and restructuring efforts have been

explored

• Internal REO platform to cover the entire

value chain from onboarding to

commercialisation, supporting liquidation

targets

NPE evolution targets

Group, €BN

~1.7

~4.7

~2.3

2018

~2.9

~4.4

2019 2020 2021 2022 2022YE

~16.3

~5%

>50%

NPE Ratio

S3 Coverage

FNPEs <90dpd ~€1BN

4. Strategic priorities | A. Clean-up the balance sheet

~50% inorganic reduction 2019-2022

78%

Mortgages

42%89%

Corporate, SME & ShippingConsumer

66%

SBL

60%

Subsidiaries

Total Provisions

~7.0

~1.4~1.9

~4.9

~0.9

12© National Bank of Greece

Investor Presentation – May 2019

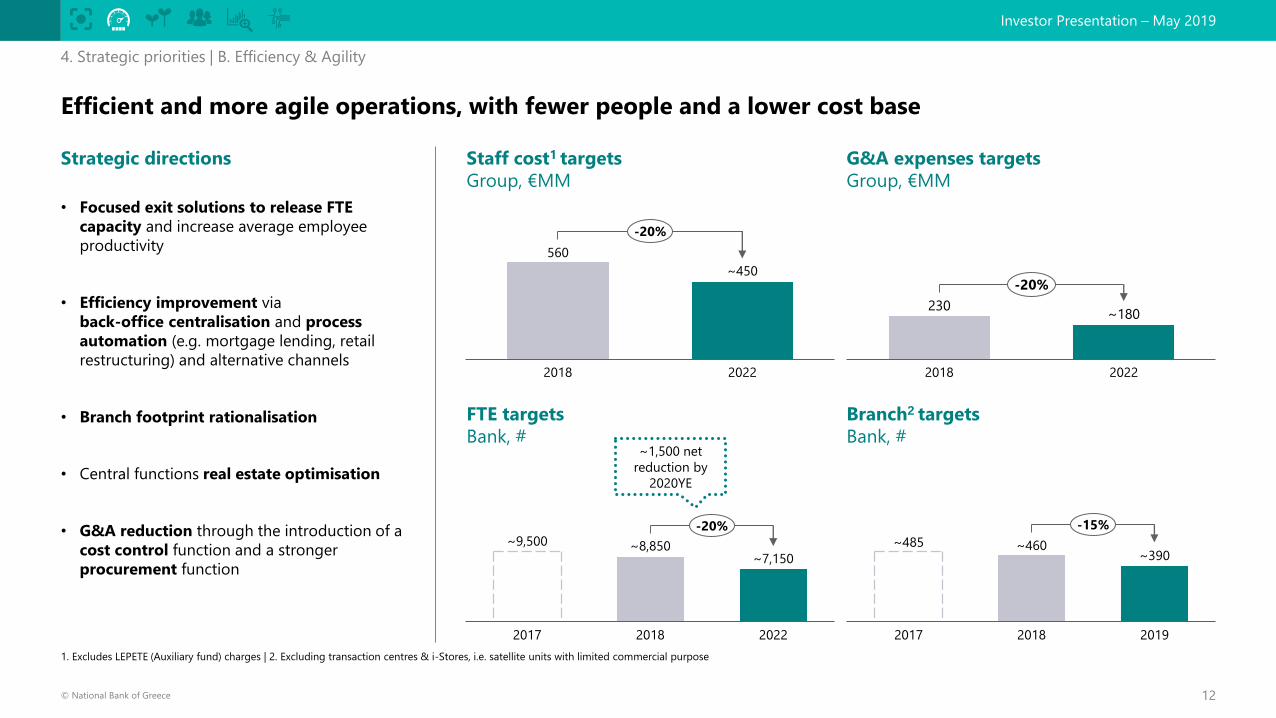

Efficient and more agile operations, with fewer people and a lower cost base

Strategic directions

• Focused exit solutions to release FTE

capacity and increase average employee

productivity

• Efficiency improvement via

back-office centralisation and process

automation (e.g. mortgage lending, retail

restructuring) and alternative channels

• Branch footprint rationalisation

• Central functions real estate optimisation

• G&A reduction through the introduction of a

cost control function and a stronger

procurement function

4. Strategic priorities | B. Efficiency & Agility

Staff cost1 targets

Group, €MM

FTE targets

Bank, #

Branch2 targets

Bank, #

20222017 2018

~9,500 ~8,850~7,150

-20%

~1,500 net

reduction by

2020YE

~485 ~460~390

20192017 2018

-15%

560

2018 2022

~450

-20%

230~180

2018 2022

-20%

G&A expenses targets

Group, €MM

1. Excludes LEPETE (Auxiliary fund) charges | 2. Excluding transaction centres & i-Stores, i.e. satellite units with limited commercial purpose

13© National Bank of Greece

Investor Presentation – May 2019

A retail bank more focused on cross-sell and fee generation

Strategic directions

• Segment-focused RMs for affluent and small

business

• Accelerated migration of transactions

to digital channels to increase time spent

on sales

• Push of fee-generating products and

services, introduction of product bundles

and revamped credit card loyalty scheme

• Stronger performance management and

data analytics

• Simple and engaging digital proposition to

increase usage and onboard new clients

4. Strategic priorities | C. Boost revenue generation

Gross interest income targets

Retail performing loans, €MM

119

20222018

~190

~60%

Consumer3

2022

Mortgages

2018

SB

~0.4

~1.3

~X3.5

Loan origination targets

Retail, €BN

394

20222018

~520

>30%

Fee income targets

Retail, €MM

Key indicators

Δ 2018-2022

Note: Bank level figures

1. Monthly mobile active users | 2. Cross-sell ratio: number of products per retail client | 3. Includes credit cards

Mobile active users1

Cross-sell ratio2

Payment fees

8% ~25%

3 ~3.7

+~50%

14© National Bank of Greece

Investor Presentation – May 2019

A corporate bank with deeper large client relationships and a broader SME base

Strategic directions

• Enhanced service levels through corporate

branches, new RMs, faster processes and

digital offerings

• Further refocusing of relationship

managers’ time, from credit underwriting

activities to sales

• Push on ancillary products and fees (e.g.

treasury, trade finance, insurance)

• Deployment of EVA and account planning

tools to improve client understanding and

sales focus

Gross interest income targets

Corporate performing loans, €MM

80

~120

2018 2022

~50%

20222018

Shipping

SMEs

Corporate1

~2.6~3.0

~15%

Loan origination targets

Corporate, €BN

421

2018 2022

~670

~60%

Fee income targets

Corporate, €MM

Key indicators

Δ 2018-2022

Of which

~50% in

2018Q4

4. Strategic priorities | C. Boost revenue generation

Note: Bank level figures.

1. Includes large corporate, midcaps and structured finance | 2. Cross-sell ratio: number of products per corporate client | 3. Target achieved by 2019

RM client facing time x 2

Cross-sell ratio2

Branches with

Corporate personnel3

x2

3 ~5

5 ~30

15© National Bank of Greece

Investor Presentation – May 2019

MOBILISE OUR

PEOPLED

IMPROVE

VISIBILITY &

CONTROLE

UPGRADE

TECHNOLOGY

INFRASTRUCTURE

F

Our people, accountability and upgraded technology as key enablers

4. Strategic priorities | People, visibility, technology (D, E, F)

• New people strategy: performance management, transparent career path and development programs for our

core talent

• Redesigned organisation: leaner structure and higher mobility

• Reporting tools to measure performance

• Steering tools to enhance value-based decision making

• Improved data quality and availability to the business

• Investment on the evolution of digital channels

• Reduction of cost through simplification, consolidation of IT infrastructure and process automation

• Upgrade of core systems to improve IT capacity, flexibility and time to market

16© National Bank of Greece

Investor Presentation – May 2019

PURPOSE, VALUES, STRATEGY

CLEAN-UP

THE BALANCE SHEETENHANCE EFFICIENCY

& AGILITY

BOOST REVENUE

GENERATION

MOBILISE OUR PEOPLE IMPROVE VISIBILITY &

CONTROL

UPGRADE TECHNOLOGY

INFRASTRUCTURE

DELIVERY ENGINE

A bank-wide transformation program focused on delivery

• Bank-wide effort: 6 workstreams, 20+ initiatives,

100+ sub-initiatives, 500+ people engaged

• Clear structure and governance led by a top management

transformation committee

• Broad organisational commitment – program developed

bottom-up

• Strong executive accountability with specific ownership of

initiatives and sub-initiatives

• Visibility and delivery discipline through rigorous planning

and monitoring

• A “delivery engine” orchestrated by an empowered

Transformation Program Office

• Leadership development program in place, to support the

new way of working

5. The delivery engine

17© National Bank of Greece

Investor Presentation – May 2019

A clean and profitable bank in 2022 – the Greek bank of choice

6. NBG in 2022

2018 2022 targets

CET1

Cost : Income1

NPE ratio

ROE <0% ~11%

41% ~5%

75% ~45%

16.1% ~15%

Note: Group level figures

1. Excluding restructuring costs

18© National Bank of Greece

Investor Presentation – May 2019

AGENDA

Introduction Costas Michaelides | Chairman

Strategic objectives 2019–2022Pavlos Mylonas | Chief Executive Officer

Financial targets

Clean-up the balance sheet Fotini Ioannou | Head of Troubled Assets Group

Boost revenue generationChristina Theofilidi | Head of Retail Banking

Vassilis Karamouzis | AGM Corporate & Investment Banking

Enablers: people, technology, processesEvi Hatzioannou | Head of Human Resources

Stratos Molyviatis | Chief Information Officer

Ethniki180: Transformation Program Ernestos Panayiotou | Chief Transformation Officer

Q&A

19© National Bank of Greece

Investor Presentation – May 2019

Notes: Group level figures

1. Includes Greek T-Bills, GGBs and Greek sovereign swap | 2. Includes savings and sight deposits

76%

3%

97%

2018

24%

2022

Net PE

Net NPE

30.1 ~30.0

5%

76%

2022

~13.5

19% 12%

2018

64%

24%

8.8

100%

2022

33%

2018

67%0.9

~3.0

Targeting a balance sheet geared towards profit generation

~6.2

2018 2022

~5.0

2022

33% 33%

67%

2018

67%

Time

Core2

43.0

~47.5

Greek sovereign risk1 EU sovereign bonds (non-Greek) Other

Assets

€BN

Deposits Long term debt

Net loans Securities

Accounting equity

Liabilities

and equity

€BN

Senior Debt/Tier 2Covered Bonds

20© National Bank of Greece

Investor Presentation – May 2019

∆ 2018 vs. 2022 target

ROE drivers: top-line growth, cost reduction and CoR normalisation

2018

~ 1,710

2022

1,312

926~ 800

2018 2022

340~ 235

2018 2022

Core

Income

growth

€MM

Cost

reduction

€MM

Normalised

cost of risk

€MM

~ €400MM1

~ €125MM

Core income targets

Opex targets

Impairment targets

Total

~ €105MM

~ €630MM

=

+

+

Note: Group level figure

1. Core income growth excludes trading and other income

21© National Bank of Greece

Investor Presentation – May 2019

Asset class 2018 2022

Corporate 4.2% ~4.3%

SBL 6.6% ~6.8%

Consumer1 8.0% ~10.2%

Mortgage 2.2% ~2.9%

Total 3.8% ~4.4%

Yield assumptions on performing loans

1.3%

• Corporate & SME PE book growth of ~€5.5BN

in 2022 vs. 2018

• GGBs exposure as a result of Titlos transaction

• Deployment of excess liquidity into European sovereign bonds

• Reduced average bond tenor in anticipation of higher interest

rates and to reduce mismatch (IRRBB) risk

2.6%

3.7%

Yields 2022

NII improvement due to portfolio rebalancing to higher yielding assets

Core Income Growth

5%

60%

16%

24%19%

2018

7%

57%

12%

2022

8.8

~13.5

EU sovereign bonds (non Greek)Tbills GGBs Other

Securities targets

Domestic, €BN

Performing loans targets

Domestic, €BN

39%29%

49%58%

6%8%5%

2018

7%

2022

22.3 ~29

MortgagesConsumer1SBLCorporate & SME

1. Includes credit cards

22© National Bank of Greece

Investor Presentation – May 2019

NII growth and quality improvement

NII evolution targets

Domestic, €MM

2018

~380

NPEs

~110

PEs

~220

Swap

arrangement

with Greek state

~120

Securities

~90

Deposits

~70

Non deposit

funding

~30

Other1 2022

1,007

~1,270

Deployment

of excess

liquidity

Includes funding costs

related to issuance of Tier

II and Senior notes to

comply with regulatory

requirements

Assets Liabilities

Core Income Growth

Due to ~€4BN

increase in deposits

and ~20bps increase

in average deposit

yields

1. Includes subsidiaries

PE loans growth driven by

cumulative disbursement of

~€4BN in Retail, ~€12BN in

Corporate and ~€2BN of net curing

23© National Bank of Greece

Investor Presentation – May 2019

Fee income targets driven by new origination, cross-sell and pricing actions

Fee income targets

Domestic, €MM

~25

~40

2018 Lending

related

Digital channels

& payments

Pricing &

bundle offers

Bancassurance

& investments

Non-lending

corporate fees

2022

228

~25

~20

~15 ~350

Core Income Growth

New origination & digital

+ ~€65MM

Cross-sell & pricing

+ ~€60MM

24© National Bank of Greece

Investor Presentation – May 2019

Targeted cost reduction mainly driven by staff cost improvements

Opex evolution targets

Group, €MM

Cost reduction

~35

2022

926

20182

~110

Staff

costs

LEPETE -

Auxiliary fund

~50

G&A

~1

D&A

~800

Cost: Income1

Total reduction3

-17%

75% ~45%

~460

~100

2018 Cumulative

2019-2022

>40%

Capex

Group, €MM

1. Excluding restructuring costs | 2. 2018 Pro forma (Pangaea deconsolidated and adjusted for IFRS 16 implementation) | 3. Excluding LEPETE

Capex related to

transformation

25© National Bank of Greece

Investor Presentation – May 2019

Substantial efficiencies across the bank, combined with a targeted renewal of the workforce

Key actions

• New hires: focused hiring plan until 2022 to

support revenue growth and transformation

needs

• Excess capacity due to network and HQ

restructuring: downsizing of branch network

footprint, discontinuation of discretionary

activities at the Head Office and potential

outsourcing

• Transaction migration to digital: migration

of transactions to digital, reducing capacity

requirements

• Process redesign & organisational

simplification: cross-functional processes

(e.g. optimisation of retail/corporate lending

and retail restructuring), de-layering and

simplification of the organisational structure

Headcount evolution targets

~7,150

350-450

2018 New hires

800-900

Excess capacity

due to network

and HQ

restructuring

800-1,000

Transaction

migration

to digital

Process redesign

& organisational

simplification

Target

headcount

~8,850

300-450

Cost reduction

26© National Bank of Greece

Investor Presentation – May 2019

• Incentives based on age

and tenure

• Cash add-ons and top-ups to

provide “bridge-to-pension” for

older employees

• Children support bonus

• Provision of health insurance

(for 15 years after exit)

• Coverage extended to all

family members

• Maintenance of mortgage terms

• Financial management and family

business development support

towards retirement

Monetary compensation Health insurance Additional support

Cost reduction

Attractive and socially responsible new VES to incentivize exits

Main pillars of the new VES

VES payback period: ~2.1 years

27© National Bank of Greece

Investor Presentation – May 2019

Sustainable savings through tight cost control and stronger procurement processes

Key priority areas

(Non exhaustive)

• Legal, and other professional

services: review major contracts and

manage demand

• Real estate: optimise space utilization,

rents and maintenance costs

• Insourced personnel: review large

insourced personnel contracts

• Information Technology (IT):

Renegotiate IT support with selected

providers

• Personnel related costs: review

benefit policies

Actions

• Enhance spending monitoring and enforce controls

• Challenge demand and spending from BUs

• Identify saving opportunities through cost-benefit analyses

• Centralise sourcing for >80% of spending

• Standardise sourcing strategy, increase use of competitive tenders

on large contracts

• Install strict purchasing policies

Set-up

Cost Control

Unit

Reinforce

Procurement

Unit

Cost reduction

28© National Bank of Greece

Investor Presentation – May 2019

Relatively low cost of risk throughout the clean-up due to high cash coverage

Cost of risk evolution targets1

Group, bps

113

2018 Avg. 2019-2022 Run rate post 2022

~110

50 – 60

Normalized cost of risk

• High loss budget

until 2022 due to

NPE clean-up

• Run rate cost of

risk of 50-60bps

expected after 2022

~9.0

2018 existing

~1.3

~10.3

2019 - 2022

cumulative impairments

2018-2022

Cumulative provisions1

Group, €BN

1. Including loss budget

29© National Bank of Greece

Investor Presentation – May 2019

~15.0

Cumulative PAT2018

~3.2

Basel IV

~2.1

RWAs expansion1 DTC amortisationSubsidiaries

disposals

~2.2 ~2.1

IFRS9 transitional

adjustment

~0.8

~1.4

2022

16.1

Total capital

Capital evolution targets

Group, %

Planned divestments

of Romania, Cyprus,

Egypt in 2019 and

Ethniki Insurance by

2020

Aiming for robust capital generation throughout the transformation period

16.2 ~17.0

CET1

Including ~€0.8BN TIER II outstanding

Of which non-

recurring losses

with -180-

190bps impact

Organic One-off Regulatory / Accounting

CET1

min

11.0%

OCR

min

14.5%

1. Standardised adoption impact is expected to be fully offset as net NPEs are eliminated

30© National Bank of Greece

Investor Presentation – May 2019

Cost of Risk

CET1 ratio / Total

capital ratio

NPEs GrossCost : Income1

NPE Ratio

2018 2022 targets

ROE

Fees / Total

Assets

Net Interest

MarginNPE Coverage4

2018 2022 targets

PE Loans

290bps ~ 300bps

43bps ~ 60bps

75% ~ 45%

113bps2 ~ 80bps3

<0% ~11%

55.1% >50%

41.0% ~ 5%

€16.3BN ~ €1.7BN

€23.3BN ~€30BN

16.1% / ~15.0% /

16.2% ~17.0%

Profitability Asset Quality, Capital & Liquidity

5% ROE5 in

2020

15.5% CET1

in 2020

Note: Group figures

1. Excluding restructuring costs | 2. Excludes recoveries related to the unsecured portfolio sale in 2018 | 3. Run-rate cost of risk post 2022 at 50-60bps | 4. Stage3 provision coverage | 5. Excluding VES, restructuring costs and sale of Ethniki Insurance

Delivering value for shareholders

31© National Bank of Greece

Investor Presentation – May 2019

AGENDA

Introduction Costas Michaelides | Chairman

Strategic objectives 2019–2022Pavlos Mylonas | Chief Executive Officer

Financial targets

Clean-up the balance sheet Fotini Ioannou | Head of Troubled Assets Group

Boost revenue generationChristina Theofilidi | Head of Retail Banking

Vassilis Karamouzis | AGM Corporate & Investment Banking

Enablers: people, technology, processesEvi Hatzioannou | Head of Human Resources

Stratos Molyviatis | Chief Information Officer

Ethniki180: Transformation Program Ernestos Panayiotou | Chief Transformation Officer

Q&A

32© National Bank of Greece

Investor Presentation – May 2019

Subsidiaries2018

Group

15.4

~3.3

0.9

2018

Bank

~2.5

Liquidations

~0.5

Other

write-offs

Sales

~3.3

Securitisations 2022Debt

forgiveness

~2.0

16.3

New

defaults

~1.6

~1.0

~3.3

Net

curings &

recoveries

Organic and inorganic actions driving NPE targets below €2BN

NPE evolution targets1

Bank, €BN

Inorganic

Organic • Frontloaded sales of highly covered

portfolios

• Accelerated restructurings

capitalising on high cash coverage

and a friendlier legal environment

• Liquidations as a signalling tool for

non-cooperative and non-viable clients

• Large securitisation after

restructuring attempts and front-

loaded sales to address the most

critical part of the NPE portfolio,

balancing value and timing

considerations

CLEAN-UP THE BALANCE SHEET

Outperformance of

SSM targets by

~€1BN in 2016-2018

1. Gross NPEs

33© National Bank of Greece

Investor Presentation – May 2019

A powerful NPE management platform in place to deliver the NPE reduction

NPE management operations

Internal

~700

External2 Total

~500

~1,200

~220

External2Internal3

~50

Total

~270

~240~160

External2Internal

~80

Total

Headcount1

#

• Control over the entire NPE

management lifecycle

• Well-staffed operations, with

experienced and trained personnel

• Flexibility ensured by outsourcing of

non-core activities

• Task force teams to perform large

transactions and resolve complex

restructuring / denouncement cases

Front-office Operations

(Large Corp, SMEs, SBL, Shipping)

Task Force (Investment Bank team,

Denounced Task Force)

Middle & Back Office Operations

Retail

Collections

Special Assets

Unit

(SAU)

Group Real

Estate

REO & Property Management

Asset Valuation

Special Projects & RE advisory

Retail Collections Operations

Delinquent Retail underwriting

Retail Collections Strategy &

Support

Retail NPEs

Corporate NPEs

RE assets

Technical Services

Highlights

1. Does not include supporting shared services | 2. Includes insourced personnel | 3. Does not include internal lawyers and technical experts working on SAU NPE cases

CLEAN-UP THE BALANCE SHEET

34© National Bank of Greece

Investor Presentation – May 2019

NPE reduction strategy designed to maximise portfolio value

NPE targets, Bank solo, €BNSuccessful

restructuring1,2 Liquidations1 Sales /

Securitisations1

Mortgages ~3.2 ~0.9 ~2.6

Consumer ~0.3 - ~1.1

SBL ~0.4 ~0.3 ~1.2

SME ~0.4 ~0.5 ~1.1

Large

Corporates &

Shipping

~1.1 ~0.8 ~0.5

20222018

~1.0

7.0

2018

~0.1

2022

1.4

~0.11.9

20222018

2.8

2018 2022

~0.3

~0.1

2018

2.1

2022

A

B

C D • Restructuring of retail exposures

involving deep debt forgiveness

supported by provision stock and new

legal framework

• Long term restructurings as core

reduction lever for Large Corporates

and Shipping clients

• Cooperation with other banks on

multi-bank exposures via NPL forum

(Large Corporates) and Solar (SMEs)

• Liquidations used as a signalling

tool for non-cooperative / non-viable

debtors

• Front-loaded sales as core reduction

lever for Consumer, SBL & SME

• Large mortgage securitisation in

2021-22

A

B

C

D

CLEAN-UP THE BALANCE SHEET

Note : Bank level figures

1. Excludes other write-offs (not linked to actions): €0.1BN in SBL, €0.1BN in SME, €0.3BN in Large Corp. & Shipping | 2. Includes net recoveries, net curings and debt forgiveness

35© National Bank of Greece

Investor Presentation – May 2019

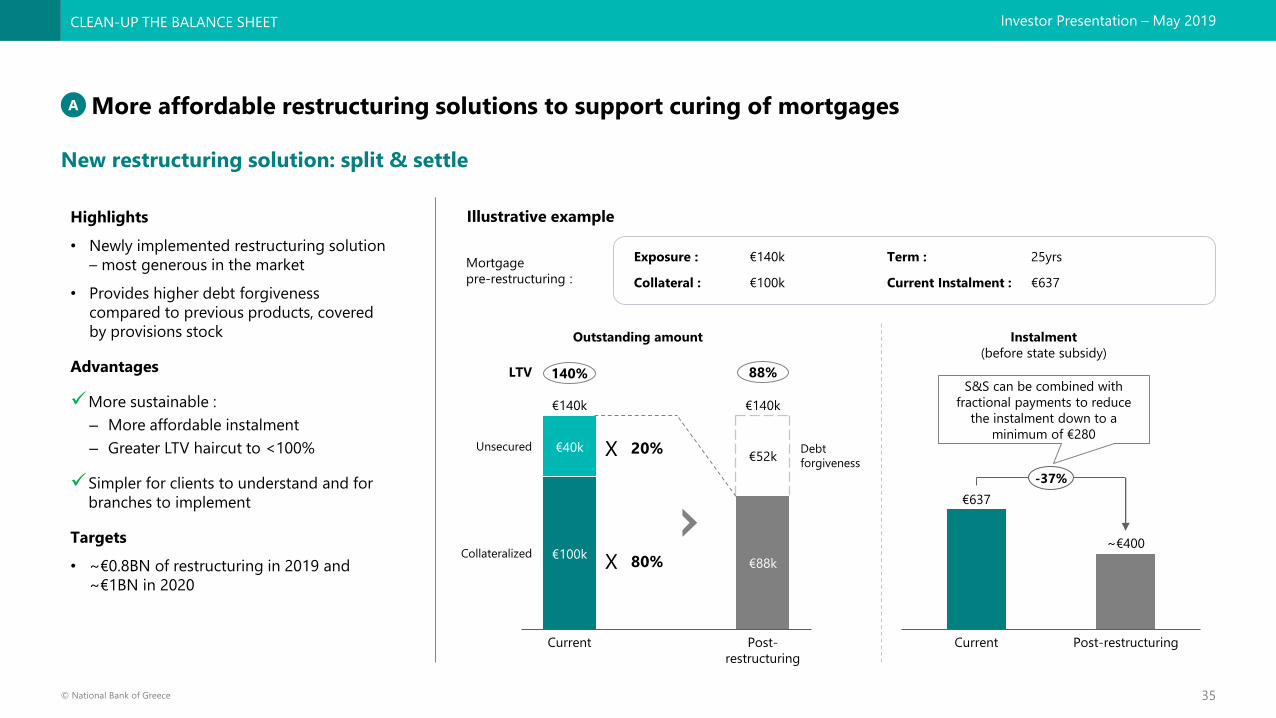

Highlights

• Newly implemented restructuring solution

– most generous in the market

• Provides higher debt forgiveness

compared to previous products, covered

by provisions stock

Advantages

More sustainable :

– More affordable instalment

– Greater LTV haircut to <100%

Simpler for clients to understand and for

branches to implement

Targets

• ~€0.8BN of restructuring in 2019 and

~€1BN in 2020

More affordable restructuring solutions to support curing of mortgages

New restructuring solution: split & settle

A

Illustrative example

€100k€88k

€40k€52k

Current

Collateralized

Unsecured

Post-

restructuring

Debt

forgiveness

€140k €140k

Exposure : €140k Term : 25yrs

Collateral : €100k Current Instalment : €637

20%

80%X

X

€637

Post-restructuringCurrent

~€400

-37%

Outstanding amount Instalment

(before state subsidy)

Mortgage

pre-restructuring :

140% 88%LTVS&S can be combined with

fractional payments to reduce

the instalment down to a

minimum of €280

CLEAN-UP THE BALANCE SHEET

36© National Bank of Greece

Investor Presentation – May 2019

Legal framework improvements support NPE resolution

‒ Tighter eligibility criteria for law protection limiting NBG

eligible pool to ~€2.2BN

‒ Framework supported by possible state subsidies

The new framework provides several key advantages

‒ Ability to progress quickly to auction for re-defaulting clients

‒ More generous restructuring offers to induce withdrawals from

personal bankruptcy law (L. 3869/10)

‒ Earlier auctions for non-eligible applicants

‒ Faster court process due to better court staffing

Stronger support on NPE reduction through:

– ~40 specialized NPL Hubs

– ~230 dedicated officers

More effective collections enabled by:

– Web-based negotiation tool

– Automated approval and RPA applied to application process

– Improved performance management and incentivisation scheme

for external parties

Supportive legal environment and specialised support from the branch network

Creditor friendly legal framework Specialised support from the branch network

Annual income <€15,550 €15,550 - €31,000

Subsidy on monthly

instalment40–50% 20–30%

Subsidy from state

Based on a family with 2 children

A

NPEs under hubs management >€8BN

NPE

FNPE

FPE

CLEAN-UP THE BALANCE SHEET

37© National Bank of Greece

Investor Presentation – May 2019

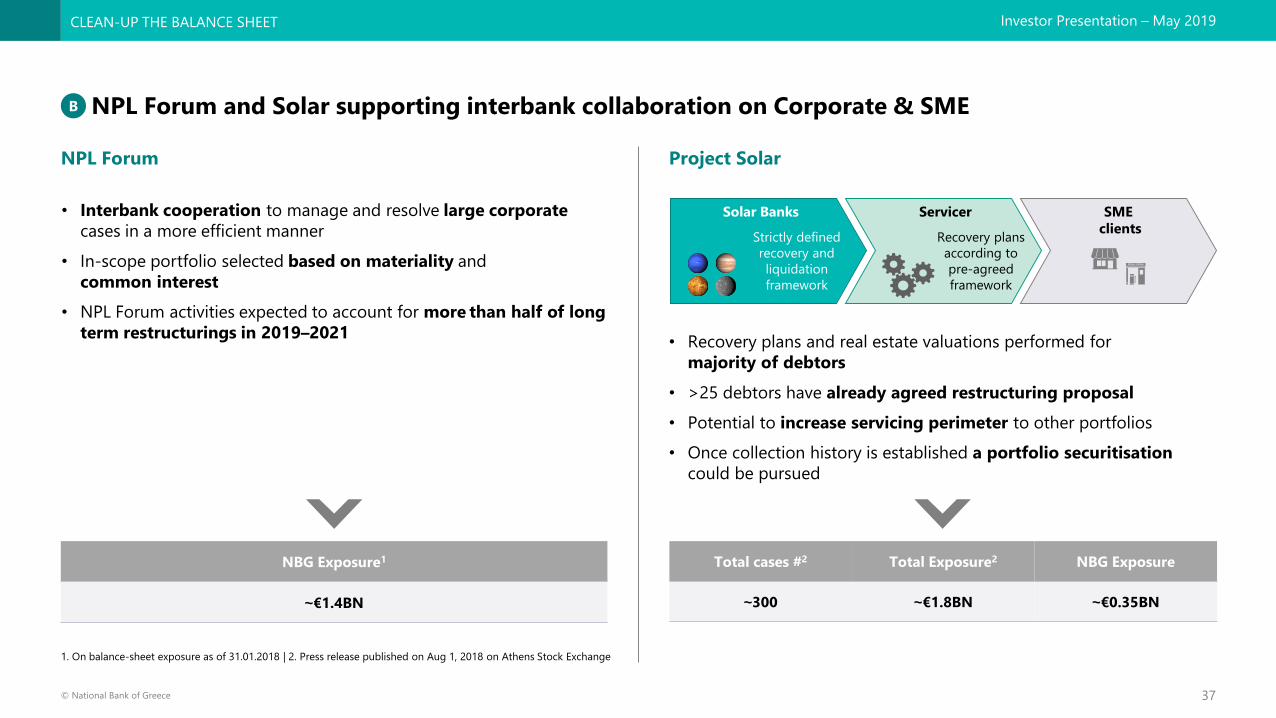

NPL Forum and Solar supporting interbank collaboration on Corporate & SME

NPL Forum Project Solar

NBG Exposure1

~€1.4BN

B

Total cases #2 Total Exposure2 NBG Exposure

~300 ~€1.8BN ~€0.35BN

CLEAN-UP THE BALANCE SHEET

1. On balance-sheet exposure as of 31.01.2018 | 2. Press release published on Aug 1, 2018 on Athens Stock Exchange

• Interbank cooperation to manage and resolve large corporate

cases in a more efficient manner

• In-scope portfolio selected based on materiality and

common interest

• NPL Forum activities expected to account for more than half of long

term restructurings in 2019–2021• Recovery plans and real estate valuations performed for

majority of debtors

• >25 debtors have already agreed restructuring proposal

• Potential to increase servicing perimeter to other portfolios

• Once collection history is established a portfolio securitisation

could be pursued

SME

clients

Servicer

Recovery plans

according to

pre-agreed

framework

Solar Banks

Strictly defined

recovery and

liquidation

framework

38© National Bank of Greece

Investor Presentation – May 2019

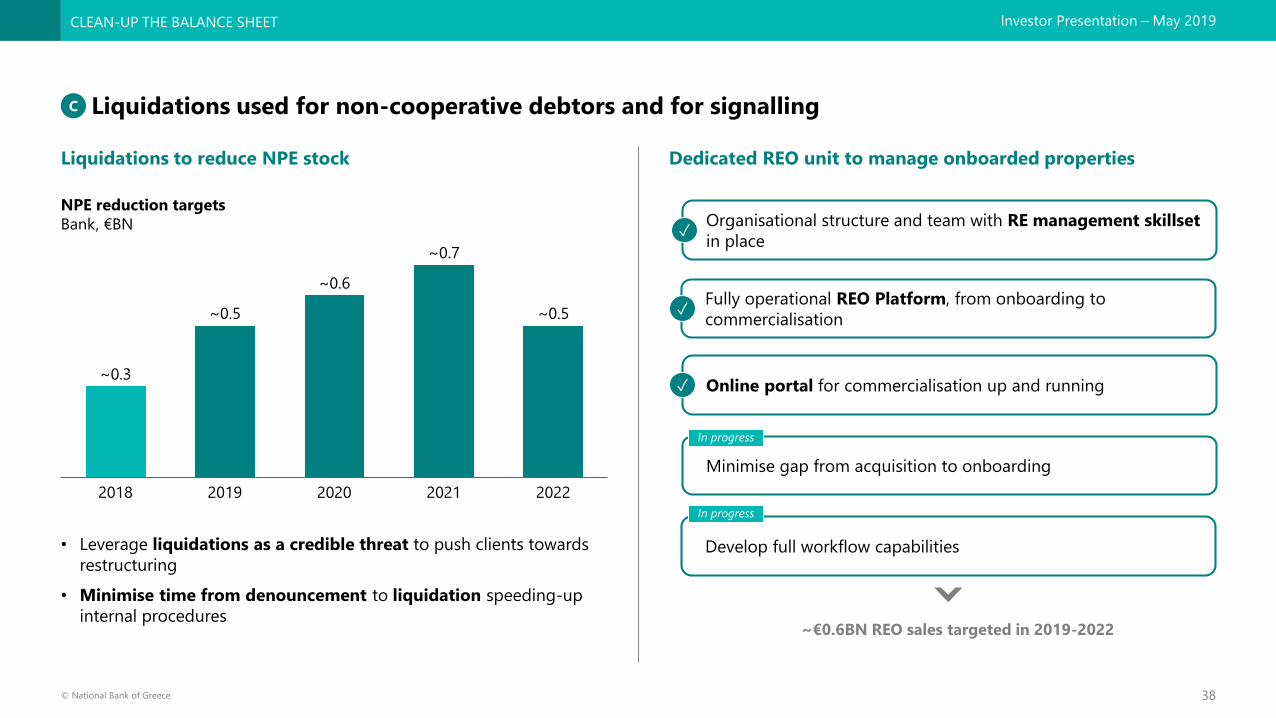

• Leverage liquidations as a credible threat to push clients towards

restructuring

• Minimise time from denouncement to liquidation speeding-up

internal procedures

Liquidations used for non-cooperative debtors and for signalling

Liquidations to reduce NPE stock Dedicated REO unit to manage onboarded properties

C

Online portal for commercialisation up and running

Organisational structure and team with RE management skillset

in place

Minimise gap from acquisition to onboarding

✓

Fully operational REO Platform, from onboarding to

commercialisation

NPE reduction targets

Bank, €BN

Develop full workflow capabilities

✓

✓

In progress

In progress

~€0.6BN REO sales targeted in 2019-2022

2019

~0.5

2018 2022

~0.6

2020 2021

~0.3

~0.5

~0.7

CLEAN-UP THE BALANCE SHEET

39© National Bank of Greece

Investor Presentation – May 2019

NPE sales in 2019 followed by securitisations in 2020-2022

€MM (on B/S)2 Symbol Mirror Secured Corporate

Consumer - ~750 -

SBL ~450 ~200 ~300

Large - - ~100

SME ~300 ~50 ~ 350

Total GBV ~750 ~1,000 ~750

D

NPE cash coverage1

2018YE, %

Mortgages Consumer

42%

89%

SBL Corporate

78%66%

45% 45%

66% 32%

NPE

ratio

NPE

ratio

Project Symbol

Sale of secured

SBL/SME portfolio

~€0.75BN

Project Mirror

Sale of a ~€1BN

unsecured retail,

SB and small SME

portfolio

2020 -22

Sale of a

~€0.75BN

Secured SBL /

Corporate &

SME portfolio

Project Solar

Securitisation of a

~€0.3BN SME

portfolio

Securitisation of

a ~€3BN

mortgages and

Consumer / SBL

portfolio

H1 2019 H2 2019

Sale of a

~€0.7BN

portfolio of

Consumer, SBL

and Corporate

Targeted sales and securitisations

Note : Bank level figures

1. Total provisions coverage | 2. Approximate figures based on current perimeter assessment

CLEAN-UP THE BALANCE SHEET

40© National Bank of Greece

Investor Presentation – May 2019

Targeted NPE reduction achieved without dilution for shareholders

NPE stock evolution targets

Group, €BN

NPE reduction coverage

Group, €BN

7.3Net NPEs

~1.8

9.0

2018

~0.8

2022

provisions1

~0.9

2022

Stage3

provisions

16.3

~1.7

-14.7

41% ~5%NPE ratio

%

Total coverage

~9.7

NPE reduction

target

9.0

~1.3

14.7

Related collateral3Provisions

10.3

~20.0

Total Capital

2020

16.1%

2018

~15.5%

2022

~15.0% CET1

16.2% ~16.5% ~17.0%

Capital evolution targets

Group, %

2018

New2

CLEAN-UP THE BALANCE SHEET

1. Total provisions | 2. Cumulative impairments 2019-2022 | 3. Total collateral coverage at current valuations

41© National Bank of Greece

Investor Presentation – May 2019

AGENDA

Introduction Costas Michaelides | Chairman

Strategic objectives 2019–2022Pavlos Mylonas | Chief Executive Officer

Financial targets

Clean-up the balance sheet Fotini Ioannou | Head of Troubled Assets Group

Boost revenue generationChristina Theofilidi | Head of Retail Banking

Vassilis Karamouzis | AGM Corporate & Investment Banking

Enablers: people, technology, processesEvi Hatzioannou | Head of Human Resources

Stratos Molyviatis | Chief Information Officer

Ethniki180: Transformation Program Ernestos Panayiotou | Chief Transformation Officer

Q&A

42© National Bank of Greece

Investor Presentation – May 2019

NBG is a reference bank for Greek households

Large customer base Strong deposit base

A brand trusted by Greek customers Solid multichannel proposition

BOOST REVENUE GENERATION – RETAIL

8.3 M

5.3 M

Greek bankable population

NBG active customers

NBG deposits

€BN

~440 branches2

~1,475 ATMs

~1,650 Pay spots3

3.9

3.3Greek peers avg.

#1 mobile app rating

19%

36%

~20 ~22

~19~19

2017

Other (sight and time)

2018

~38

Savings

~42

+9%Market share1

Extensive, nation-wide coverage Strong digital offering

NBG

Sources: NBG analysis. Greek population >20 years old, based on Hellenic Statistical Authority census of Jan 2018

Sources: Android ratings as of March 2019, GooglePlay

Trusted brand, testified by client loyalty and

marketing surveys

1. Bank of Greece – statistics of monetary deposits as of Dec18 | 2. 2019Q1 branches excluding transaction centres & i-Stores, i.e. satellite units with limited commercial purpose | 3. Payment facilities in collaboration with local businesses offering

payment services

43© National Bank of Greece

Investor Presentation – May 2019

Clear market opportunities and untapped growth potential

Market opportunities to capture Untapped potential

71%

25%

Greece

~40%

Southern

Europe3

4%

~35%

~25%

Investments

Insurance

Cash

35

912

18 19 20 20

201620152014 2017

EU

GR

1419

25 27

46 49 51 54

20182015 20172016

GR

EU

Private consumption

Greece, yoy % growth

Financial assets of households

%, 2016

Greece catching up in payments and digital penetration

30%

70%

Registered

Non

registered

Card payments value / GDP

%

Internet banking use

% population

Digital touchpoint increase a key objective

Majority of customers not yet

registered on digital

Transaction migration on

electronic channels

69% 75%

31% 25%

2016 2018

Physical

Electronic2

20162014 2018 20222020

0.1%-0.3%

2.1%

0.9%1.0%

1.6%1.8%

1.5%

Lending, investments and bancassurance expected to increase Low product penetration1, cross-selling can be improved

Sources: ELSTAT, AMECO & NBG estimates Sources: NBG Retail (countries involved include Italy and Germany)

Sources: ECB Payment Statistics (countries involved include all members of the European Union)

Sources: OECD National Account Statistics

BOOST REVENUE GENERATION – RETAIL

1. % of active customers holding at least one product of the indicated type | 2. Includes transactions at ATMs | 3. Including Italy, Portugal, Spain, France

European peersNBG

Credit cards

Bancassurance

5% 20 – 40%

5% 10 – 20%

Mortgages

Consumer loans

4% 15 – 25%

10% 10 – 30%

NBG customers registered on digital

channels,%

NBG transactions by channel,%

44© National Bank of Greece

Investor Presentation – May 2019

The transformation of our retail bank is based on three pillars

• Migrate transactions from branches to digital channels

• Drive engagement through attractive day-to-day services

• Sell basic products and onboard new customers

C. Leverage digital to

better serve our clients

• Leverage analytics to understand customer needs, predict and drive front-office activity

• Strengthen the service model through RMs, tailoring to segments that drive value leveraging ‘myNBG’

CRM platform

• Tailor product offering: new fee-generating and lending products, faster delivery and revamp of

loyalty scheme

A. Deploy a customer

centric model to drive

revenue generation

from our customer base

• Complete branch model transition: optimise footprint, standardise “look & feel” and tailor to

segment needs

• Redesign our branch processes to achieve simplicity and improved customer experience

• Redeploy workforce towards customer facing activities, upgrade CRM tools and actively manage

performance

B. Mobilise our network

to deliver results

BOOST REVENUE GENERATION – RETAIL

45© National Bank of Greece

Investor Presentation – May 2019

• Dedicated RMs to service value-generating customer segments in

the branches

• Mass segment needs addressed through systematic targeted

campaigns based on behavioural models

• myNBG platform to facilitate targeting, sales and service capability

• Network activation team for on-the-job training and support

A. Deploy a customer centric model to drive revenue generation from our customer base

• Automated credit application to support purpose-based lending from

partner merchants

• Redesigning customer journeys to enable faster time to money

• Revamp and modernization of Go4More loyalty program

• Introduction of product bundles to generate fees

Strengthen the service model

Leverage analytics to understand customer needs, predict and drive front-office activity

Tailor product offering

• Upgrade data and analytics used for modelling of customer needs and behaviours (e.g. segmentation, churn, propensity)

• Deployment of a Next Best Action engine to drive front-office activity

• “myNBG” in-house CRM platform available in all channels enabling delivery

Cross – sell ratio1Premium and business customers per RM

~200

2018 2022

~280

-28%

BOOST REVENUE GENERATION – RETAIL

~3.0~3.7

2018 2022

+20%

1. Number of products per Retail client

46© National Bank of Greece

Investor Presentation – May 2019

B. Mobilise our network to deliver results

• Optimise footprint to focus on areas with growth potential

• Re-design and modernise branch topology (size, layout, staffing)

• Branch layout to reflect strategy with self service areas for mass and RM service

for premium and business segments

• Introduce paperless processes and expand usage of digital signature

• Simplify and standardise all activities to minimise operations

• Transition from an inconsistent experience to predictable, branded

experience across all touchpoints

• Refocus effort of network on sales and advisory, supported by transaction

migration and elimination of back office tasks

• New CRM platform with management tools for optimising capacity and effort

i.e. client meeting scheduling module

• Network activation team to ensure alignment with targets and systematic

performance management framework

Reduction of time spent on low-value

activities in the branch

Proactive daily customer meetings per RM

Redesign in-

branch

processes

Complete

branch model

transition

Redeploy effort

and manage

performance

Branch network evolution targets

Teller transactions ~30%

Branch support ~35%

Administrative ~45%

2022

2018

4%

46%47%

49% 48%

2017

~3906%7%

52%

40%

2019

460

Corporate1

Full2

Retail

485

1. Branches with Corporate RMs | 2. Branches with premium and corporate RMs

BOOST REVENUE GENERATION – RETAIL

~1.3

2018 2022

~2.6

X2

47© National Bank of Greece

Investor Presentation – May 2019

C. Leverage digital to better serve our clients

• Wide set of basic services available in a single app

• Mobile first strategy

• Enhanced card management features

• ERP integration for SBs

• Personalised notifications

• Day-to-day spending support (PFM)

• Instant payments

• POS management for merchants

• Business Finance Management for SBs and Professionals

• Full digital onboarding

• Digital signature

• Digital sales of simple credit, investment and insurance products

Mobile monthly connections per active user

Products accessible on digital channels

Drive

engagement

Migrate

transaction

Sell basic

products

Mobile monthly active users

BOOST REVENUE GENERATION – RETAIL

8%

2018 2022

~25%

x3

17

2018 2022

~20

+18%

2018 2022

0

~10

48© National Bank of Greece

Investor Presentation – May 2019

Income growth targeted via cross-sell of lending and fee generating products

Retail loan disbursements targets

Bank, €MM

Retail fee income targets

Bank, €MM

New origination

spread avg.

2019 - 2022

Fees /

Net Loans

BOOST REVENUE GENERATION – RETAIL

72

177

117

~470~450

Consumer1Mortgages

~400

Small Business

2018

2022

~350bps ~1,200bps ~675bps

119

2018 2022

~190

+60%

• Overall loan disbursements to increase significantly as we

capture market growth

• Competitive position enhanced through improved lending

process and selective launch of new products

• New production at low risk levels as internal controls and risk

management capabilities are strengthened

• Core retail fees growth driven by payments, bancassurance and

investments related fees

• Gradually bridging fee-generation gap with Southern

European peers

~100bps ~170bps

1. Includes cards

49© National Bank of Greece

Investor Presentation – May 2019

AGENDA

Introduction Costas Michaelides | Chairman

Strategic objectives 2019–2022Pavlos Mylonas | Chief Executive Officer

Financial targets

Clean-up the balance sheet Fotini Ioannou | Head of Troubled Assets Group

Boost revenue generationChristina Theofilidi | Head of Retail Banking

Vassilis Karamouzis | AGM Corporate & Investment Banking

Enablers: people, technology, processesEvi Hatzioannou | Head of Human Resources

Stratos Molyviatis | Chief Information Officer

Ethniki180: Transformation Program Ernestos Panayiotou | Chief Transformation Officer

Q&A

50© National Bank of Greece

Investor Presentation – May 2019

Leveraging NBG’s unique position, we have embarked on a transformation journey towards becoming the best Corporate Bank in the market

BOOST REVENUE GENERATION – CORPORATE

Longest track-record in Greece

Loyal client base

Experienced personnel

Full spectrum of products and services

Strong brand name

Portfolio in growth trajectory

Young talent

New Corporate & Investment Banking platform

51© National Bank of Greece

Investor Presentation – May 2019

+12%

Initiatives launched in 2017-18 have already delivered significant results

Key initiatives FY2018 results

Corporate loan disbursements

yoy growth, %

SME loan book

yoy% growth

Corporate fees

Accounting

yoy% growth

New production rating

2018 production vs. stock

• Established a uniform Corporate & Investment Banking platform

• Reorganized the Large Groups structure, intensifying coverage

• Revamped our Structured Finance unit, covering the full spectrum of

services

• Created a mid-caps segment, offering premium coverage for mid-sized

companies

• Created a Business Development unit, enhancing business intelligence

capabilities

Corporate

Bank

reorganisation

• Led the majority of large structured finance transactions (>€100MM),

capturing sponsor-led investment activity

• Improved profitability by offering niche product / service capabilities in

large groups and mid-caps

• Increased penetration in SMEs for second consecutive year, targeting

export-oriented firms and domestic consolidators

• Expanded presence in traditional mid-sized Greek shipping companies

segment

Strategic focus

Improvement in

avg. risk rating

+4%

2 notches

+~70%

+7%

Corporate loan book

yoy% growth

Corporate fees

Cash basis

yoy% growth

+12%

BOOST REVENUE GENERATION – CORPORATE

52© National Bank of Greece

Investor Presentation – May 2019

Initiatives launched alongside favourable market conditions provide a solid foundation for growth

Market business loans growth1

yoy delta, gross loans, €BN

• Broader recovery expected for SMEs as domestic demand improves

• Growth in International Trade activities for businesses

• Significant sectoral growth potential in infrastructure, energy,

transportation & logistics, pharma and hospitality

Focus per segment

202020182017

-0.8

2019 2021 2022

0.3

3.44.4 4.7 4.8

Large

groups

• Maximise share of wallet and cross-sell focusing

on profitability

Structured

finance

• €2BN credit expansion pipeline identified for

2019-2022 with high degree of conversion

expected

Mid-caps• Selectively expand by offering tailor-made

solutions and premium coverage

SME • Tap into SME market growth

Shipping

• Grow in mid-sized shipping companies

segment, taking advantage of the void left by

international banks

Corporate market evolution drivers

Import-export growth

yoy growth, %

2017 20222018

6.9

2020

3.3

2019

7.4

2021

2.9

8.8

4.7 5.33.8 4.6 3.7 4.1

2.9

ExportsImports

Source : ELSTAT & Focus Economics Consensus forecasts

Source: Bank of Greece, NBG economic office analysis

Source: NBG Economic Research

1. Including Small Businesses (legal entities) and NPEs; excluding shipping and adjusting for write-offs

BOOST REVENUE GENERATION – CORPORATE

53© National Bank of Greece

Investor Presentation – May 2019

Through our transformation journey we will focus more on how to maximise value for our clients and our shareholders

• Refocus corporate coverage teams from credit underwriting to sales

• Grow business with our product partners’ support

• Leverage business intelligence capabilities to effectively manage portfolio

A. Value-driven

client coverage

• Reduce time-to-money through fast credit processes

• Offer premium services through corporate branches

• Enhance digital channels

B. Service

excellence

BOOST REVENUE GENERATION – CORPORATE

54© National Bank of Greece

Investor Presentation – May 2019

A. Strengthen value-driven client coverage

• Reduce RM administrative work load, simplifying credit process and

developing middle office capabilities

• Re-define frontline team roles, shifting focus from credit underwriting to

relationship management

• Provide advanced client planning tools to enhance RM productivity

• Strengthen dedicated product specialist teams to effectively support client

coverage

• Set common targets and incentives with RMs at product level per segment

• Launch targeted product campaigns

• Capitalize on business intelligence toolkit to effectively steer the business

• Enhance and expand the use of EVA and pricing models in commercial

strategy

• Embed advanced analytics capabilities to optimise SME portfolio management

Cross-sell ratio1

BI Toolkit

• New Corporate CRM

• Referral platform

• New EVA and pricing tools

• Commissions platform

• Next best product and churn prediction

models

Grow business

with our product

partners

Refocus

corporate

coverage teams

Redeploy effort

and manage

performance

RM time spent on client facing activities

1. Number of products per Corporate client

BOOST REVENUE GENERATION – CORPORATE

3

2018 2022

~5

<30%

>60%

2018 2022

55© National Bank of Greece

Investor Presentation – May 2019

B. Achieve service excellence

• Streamline credit approval process by reducing application burden, leveraging

on available technology options

• Centralise and automate middle and back office activities

• Corporate branch model offering local service in areas with significant business

presence

• Offer premium services through dedicated corporate teams across the

country

• Introduce new online “self-service” functionalities

• Migrate transaction volume from physical to digital channels

Corporate network

# of locations with dedicated personnel

New self-service functionalities

• e-factoring & invoicing

• e-trade

• Online legalisation

• Online revolving line usage

• API capabilities

Corporate

branches

Faster credit

processes

Enhanced

digital

channels

Fast track credit application

BOOST REVENUE GENERATION – CORPORATE

5

2018 2019

~30

35% of cases

Perimeter

Reduction in

process time

~30%

56© National Bank of Greece

Investor Presentation – May 2019

Interest income expansion and fee growth targeted over 4 years

Corporate loan disbursements1

Bank, €BN

Corporate fee income targets

Bank, €MM

~3.0

2017 2018

~1.5

2022

~2.6

+~70%+15%

• Structured Finance pipeline and large deals in large groups will

support credit expansion

• While significant contribution from higher margin/ recurring business

in 2020-22 (SMEs, Midcaps) as corporate banking platform is enhanced

• Core lending fee growth driven by new origination and large

structured finance deals

• Ancillary fees growth leveraging new coverage/ service model for

corporate & SMEs, account planning tools and target-setting at RM

level

59

85

21

35

2022

Core lending3

2018

Ancillary products

and services2

80

~120

+50%421 ~670PE gross interest

income, €MM

1. Excluding revolving line roll-overs | 2. Including Investment banking, Import/ export, trade finance, cash management etc. | 3. Core lending fees include loans, guarantees; exclude factoring

BOOST REVENUE GENERATION – CORPORATE

57© National Bank of Greece

Investor Presentation – May 2019

AGENDA

Introduction Costas Michaelides | Chairman

Strategic objectives 2019–2022Pavlos Mylonas | Chief Executive Officer

Financial targets

Clean-up the balance sheet Fotini Ioannou | Head of Troubled Assets Group

Boost revenue generationChristina Theofilidi | Head of Retail Banking

Vassilis Karamouzis | AGM Corporate & Investment Banking

Enablers: people, technology, processesEvi Hatzioannou | Head of Human Resources

Stratos Molyviatis | Chief Information Officer

Ethniki180: Transformation Program Ernestos Panayiotou | Chief Transformation Officer

Q&A

58© National Bank of Greece

Investor Presentation – May 2019

Our people: a priority for NBG and the core enabler of our transformation

Key actions

Deploy a new people strategy

- Offer a new employee value proposition

- Identify and grow our talent

- Manage performance and incentives

Redesign our organisation

- More efficient structure (“Right size”)

- More agile organisation (“Right shape”)

- Having the correct skills (“Right skills”)

- Mobilising our talent (“Right place”)

A

B

• Outdated HR management model

• Hierarchical organisation

• Need to embrace change

• Need for a refreshed employee value

proposition and a talent growth program

Current situation

• Efficiency: Optimise resources and improve

organisational efficiency

• Alignment: Align people to the objectives of

the transformation and manage performance

• Modernisation: Enhance our people strategy

and employee proposition

Strategic priorities – what we are enabling

PEOPLE

59© National Bank of Greece

Investor Presentation – May 2019

We are modernising and upgrading our people strategy

Manage performance and incentives

• Develop a strong performance management model based on:

- Balanced scorecards to measure specific targets

- Competency-based model to measure behaviours

• Link employee compensation model with performance

Identify and grow our talent

• Launch a talent management program to identify high

performers

• Deploy new career paths and training programs to

develop our talent

Modernise our employee value proposition

• A new employee proposition based on agreed key

attributes: trustworthy, meritocratic and fair

PEOPLE STRATEGY

Compensation

and benefits

Talent Development

Employee

value

proposition

Performance

management

A

PEOPLE

60© National Bank of Greece

Investor Presentation – May 2019

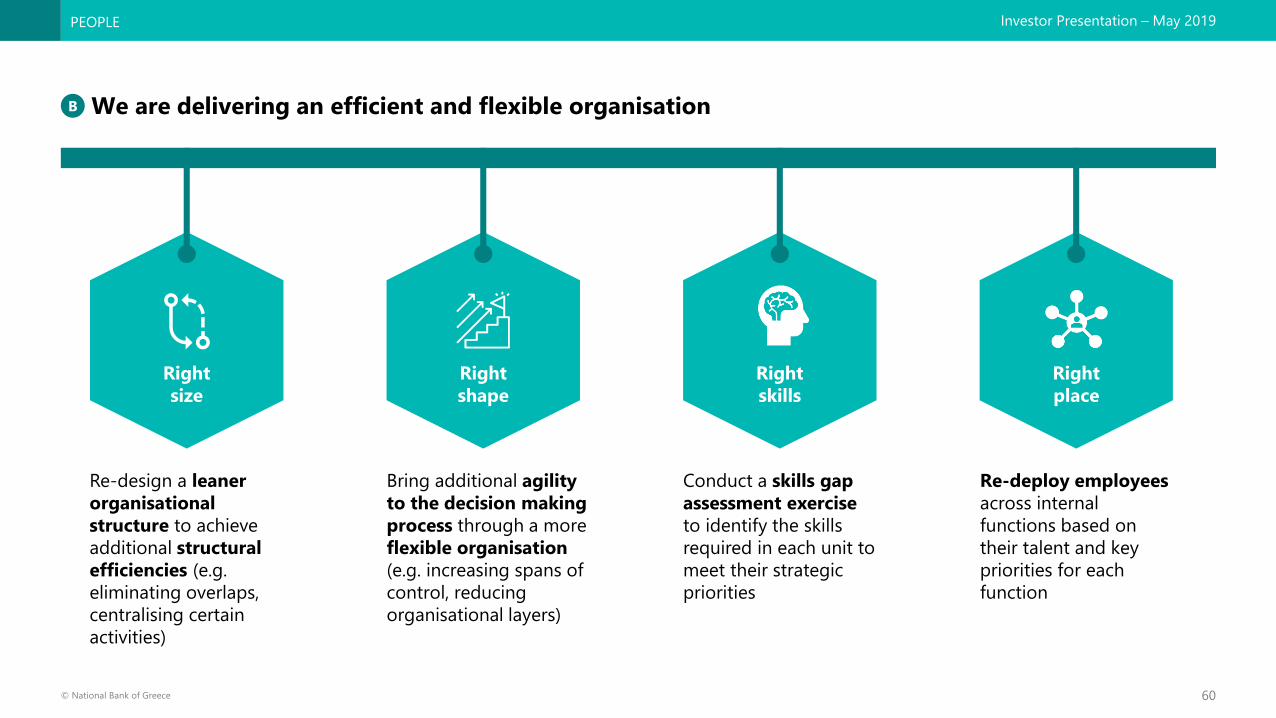

Right

shape

We are delivering an efficient and flexible organisation

Re-design a leaner

organisational

structure to achieve

additional structural

efficiencies (e.g.

eliminating overlaps,

centralising certain

activities)

Bring additional agility

to the decision making

process through a more

flexible organisation

(e.g. increasing spans of

control, reducing

organisational layers)

B

Conduct a skills gap

assessment exercise

to identify the skills

required in each unit to

meet their strategic

priorities

Right

size

Right

skills

Right

place

Re-deploy employees

across internal

functions based on

their talent and key

priorities for each

function

PEOPLE

61© National Bank of Greece

Investor Presentation – May 2019

AGENDA

Introduction Costas Michaelides | Chairman

Strategic objectives 2019–2022Pavlos Mylonas | Chief Executive Officer

Financial targets

Clean-up the balance sheet Fotini Ioannou | Head of Troubled Assets Group

Boost revenue generationChristina Theofilidi | Head of Retail Banking

Vassilis Karamouzis | AGM Corporate & Investment Banking

Enablers: people, technology, processesEvi Hatzioannou | Head of Human Resources

Stratos Molyviatis | Chief Information Officer

Ethniki180: Transformation Program Ernestos Panayiotou | Chief Transformation Officer

Q&A

62© National Bank of Greece

Investor Presentation – May 2019

Simplify, consolidate &

strengthen IT landscapeDigitise products and services

1

Focus on core

banking renewal

3

Introduce new technologies

and innovate

42

1 Focus on digital distribution

channels1 Streamline the back

end engine1 Extended deployment of RPAs

for back and front office1 Cost reduction through

consolidation of assets

2 Rich and simple

customer interaction2 Decrease Time-to-Market for

new products & services 2 Introduce AI &

machine learning

2 Revamped architecture

with smaller footprint

3 Integration with 3rd parties for

a new market place creation3 Lower future TCO 3 Self service management for

business intelligence and

analytics

3 Opportunities for outsourcing

and cloud deployments

4 Strengthened security

Enriched customer experience

Security and Regulatory Compliance

Data insightSimplification

IT strategy is built around four pillars serving transformation objectives

TECHNOLOGY & PROCESSES

63© National Bank of Greece

Investor Presentation – May 2019

IT evolution milestones

Total IT Capex related to transformation initiatives estimated at ~€170MM1, increasing Capex dedicated

to change from ~30% to ~50% of total

TECHNOLOGY & PROCESSES

Transformation journey Continuous evolution

2019

• Renewed mobile/internet banking

• New card management system

• Enterprise data warehouse full deployment

• Robotic process automation for back office

2020

• Enhanced branch and CRM platform

• Omni-channel architecture for digital

• Core banking renewal initiation

2023

• Fully deployed digital IT architecture

2021

• Data analytics and big data for business

• AI and machine learning deployment

• Hybrid cloud model

3

4

2 1

3

31

1. Capex up to 2023 including full Core Banking system renewal

64© National Bank of Greece

Investor Presentation – May 2019

Increased capacity

requirements from

transformation initiatives

Necessity to optimise

cost of IT platform

1

2

3yr targetCurrent state

Application development

Infrastructure operations

Operations in-house/outsourced

Flexible delivery model to optimise costs over a 3-year period

Requirements from business evolution Transition towards a flexible delivery model

10-15%

productivity gain

~€5MM annual saving1

40%

60%NBG

External

NBG

75%

External

25%

95%

NBG

Cloud

5%

75%

NBG

Cloud

25%

External

30%

70%

NBG90% NBG

10%

External

Flexible delivery model to deliver ~€20MM total annual savings from 2020, reallocated to Transformation

~€15MM annual saving1

TECHNOLOGY & PROCESSES

1. Targeted annual cost savings achieved from 2020 onwards

65© National Bank of Greece

Investor Presentation – May 2019

“Simplify the retail

restructuring

process”

• Centralised and automated loan administration (RPAs)

• New restructuring channels and tools

• Reduce process time by ~80%

• Achieve >50% FTE efficiency gain on back office

activities

• Increase applications from alternative channels

“Enable corporate

growth”

• Centralized loan administration

• Digital corporate lending capabilities

• Standardised credit approval documentation

• Credit process automations (incl. workflow system)

• Reduce process time by ~20% for loan admin

• Achieve ~45% FTE efficiency gain for loan

admin

“Improve customer

experience”

• Faster and simpler process from mortgage application

to disbursement

• Centralised and automated loan administration

• Digital lending capabilities

• Reduce process time by ~50%

• Achieve ~20% FTE efficiency gain

Retail NPL

restructuring

Corporate

lending

Retail

lending

Process optimization under way changing how we work and serve our clients

Process Targets

Target is to deliver 250+ FTE efficiency gains (equivalent to €13MM+ p.a.) by 2021

TECHNOLOGY & PROCESSES

Actions

66© National Bank of Greece

Investor Presentation – May 2019

AGENDA

Introduction Costas Michaelides | Chairman

Strategic objectives 2019–2022Pavlos Mylonas | Chief Executive Officer

Financial targets

Clean-up the balance sheet Fotini Ioannou | Head of Troubled Assets Group

Boost revenue generationChristina Theofilidi | Head of Retail Banking

Vassilis Karamouzis | AGM Corporate & Investment Banking

Enablers: people, technology, processesEvi Hatzioannou | Head of Human Resources

Stratos Molyviatis | Chief Information Officer

Ethniki180: Transformation Program Ernestos Panayiotou | Chief Transformation Officer

Q&A

67© National Bank of Greece

Investor Presentation – May 2019

We have launched a unique transformation program that is focused on delivery

Clear program structure and governance

• 6 workstreams led by ExCo members

• 20+ initiatives and 100+ sub-initiatives all led by line managers

• Transformation Program Office with 20+ specialist managers

Broad engagement and transparency

• Initiatives developed bottom-up, with full involvement of the

organisation

• 50+ managers going through leadership development program

• 500+ colleagues actively involved in delivery

Strong cadence and execution discipline

• Weekly CEO updates on priority topics

• Bi-weekly steering by Transformation Committee

• Monthly oversight by Board Strategy Committee

PURPOSE, VALUES, STRATEGY

CLEAN-UP

THE BALANCE SHEETENHANCE EFFICIENCY

& AGILITY

BOOST REVENUE

GENERATION

MOBILISE OUR PEOPLE IMPROVE VISIBILITY &

CONTROL

UPGRADE TECHNOLOGY

INFRASTRUCTURE

DELIVERY ENGINE

68© National Bank of Greece

Investor Presentation – May 2019

The program is on track to deliver impact in the first months; ~90% of objectives for Season 2 are expected

to be achieved

Our focus is on ensuring a disciplined and programmatic new way of working

Objectives

Objectives (KPIs and

milestones by initiative)

validated

bottom-up

Enablers

Full alignment with IT, HR

and communications; cross-

functional teams

Scoring

“Score” for each initiative;

transformation part of

executives’ scorecards

Seasons

6-month periods with

specific objectives;

“Ceremony” at the end of

each Season

1

5

9

2

6

10

3

7

11

4

8

12

69© National Bank of Greece

Investor Presentation – May 2019

AGENDA

Introduction Costas Michaelides | Chairman

Strategic objectives 2019–2022Pavlos Mylonas | Chief Executive Officer

Financial targets

Clean-up the balance sheet Fotini Ioannou | Head of Troubled Assets Group

Boost revenue generationChristina Theofilidi | Head of Retail Banking

Vassilis Karamouzis | AGM Corporate & Investment Banking

Enablers: people, technology, processesEvi Hatzioannou | Head of Human Resources

Stratos Molyviatis | Chief Information Officer

Ethniki180: Transformation Program Ernestos Panayiotou | Chief Transformation Officer

Q&A