Embed Size (px)

DESCRIPTION

Investments and International Operations. Chapter. 15. Basics of Investments. Motivation for Investments. Companies transfer excess cash into investments to produce higher income. Some companies are setup to produce income from investments. Companies make investments for strategic reasons. - PowerPoint PPT Presentation

Citation preview

McGraw-Hill/Irwin1

15-1

© The McGraw-Hill Companies, Inc., 2006

Investments and International Operations

Chapter

1515

McGraw-Hill/Irwin2

15-2

© The McGraw-Hill Companies, Inc., 2006

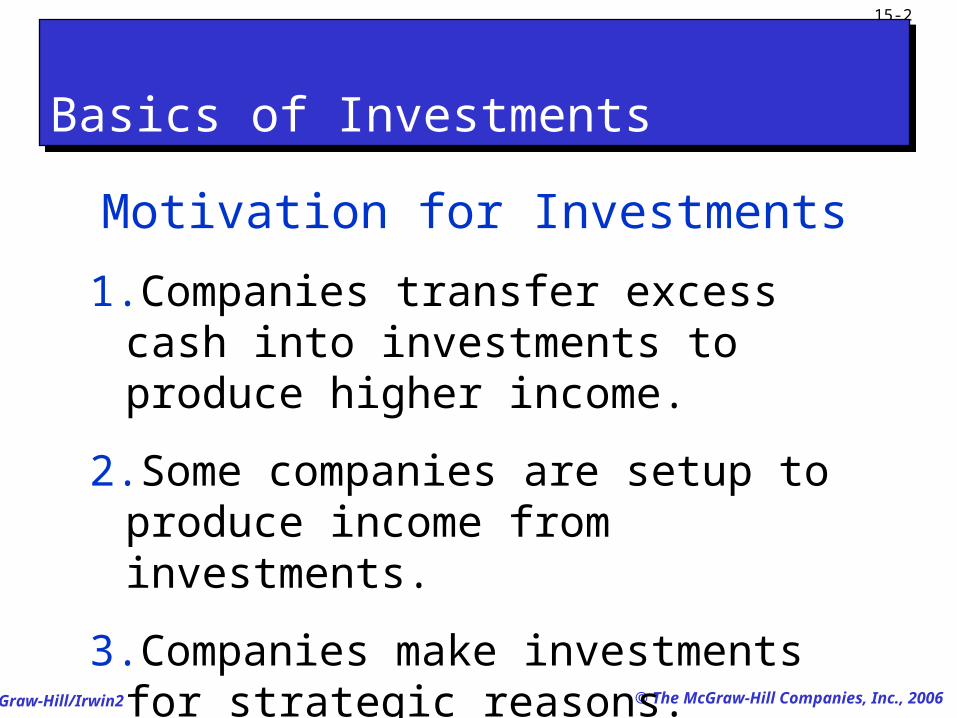

Basics of InvestmentsBasics of Investments

1.Companies transfer excess cash into investments to produce higher income.

2.Some companies are setup to produce income from investments.

3.Companies make investments for strategic reasons.

Motivation for Investments

McGraw-Hill/Irwin3

15-3

© The McGraw-Hill Companies, Inc., 2006

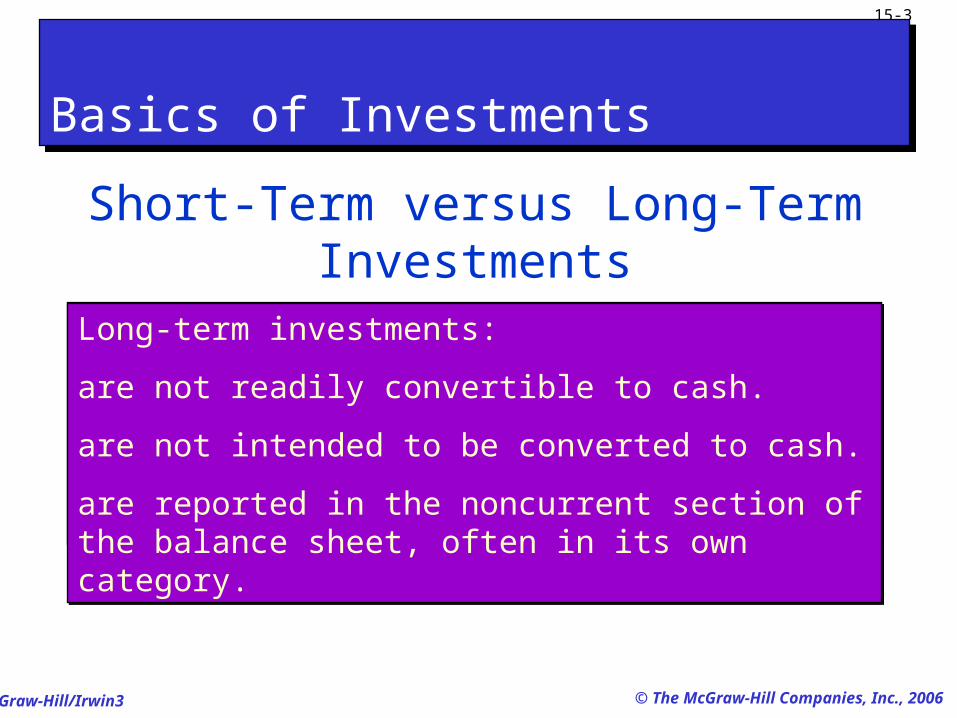

Basics of InvestmentsBasics of Investments

Short-Term versus Long-Term Investments

Short-term investments:

are securities that management intends to convert to cash with one year or the operating cycle, whichever is longer.

are readily convertible to cash.

Short-term investments:

are securities that management intends to convert to cash with one year or the operating cycle, whichever is longer.

are readily convertible to cash.

Long-term investments:

are not readily convertible to cash.

are not intended to be converted to cash.

are reported in the noncurrent section of the balance sheet, often in its own category.

Long-term investments:

are not readily convertible to cash.

are not intended to be converted to cash.

are reported in the noncurrent section of the balance sheet, often in its own category.

McGraw-Hill/Irwin4

15-4

© The McGraw-Hill Companies, Inc., 2006

Classes of and Reporting for InvestmentsClasses of and Reporting for Investments

Held-To-MaturityHeld-To-Maturity

Available-For-Sale

Available-For-Sale

Significant Influence

Significant Influence

Controlling Influence

Controlling Influence

ConsolidateConsolidateEquityMethodEquity

MethodMarket Value

MethodMarket Value

Method

TradingTrading

AmortizedCost

AmortizedCost

Class of Investment

Reporting

McGraw-Hill/Irwin5

15-5

© The McGraw-Hill Companies, Inc., 2006

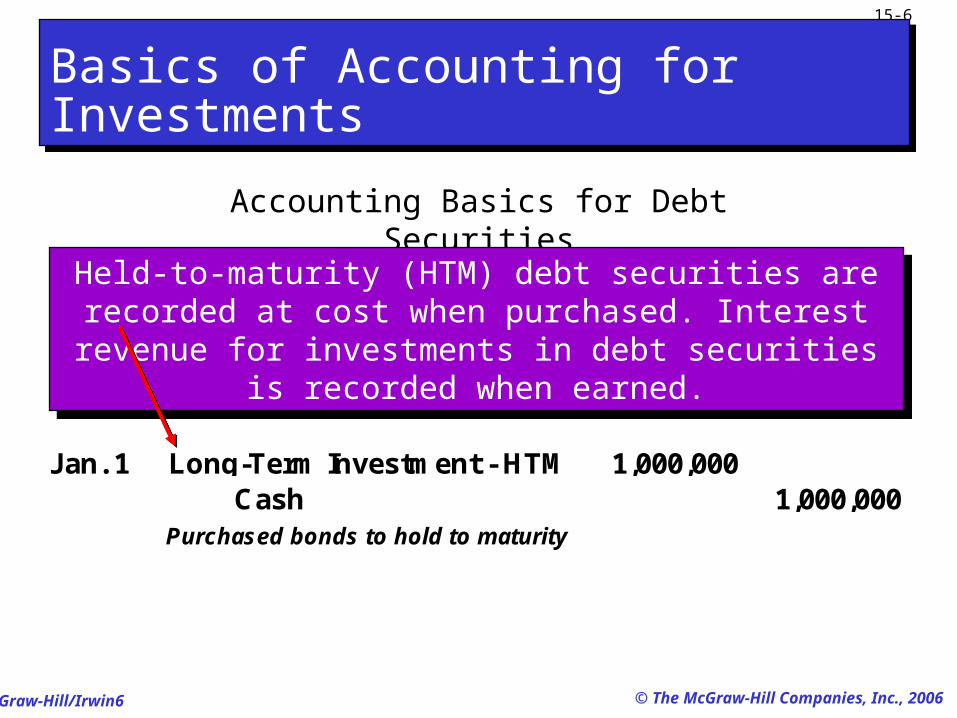

Basics of Accounting for InvestmentsBasics of Accounting for Investments

Accounting Basics for Debt Securities

Debt securities are recorded at cost when purchased. Interest revenue for investments in debt securities is

recorded when earned.

Debt securities are recorded at cost when purchased. Interest revenue for investments in debt securities is

recorded when earned.

On January 1, 2005, Matrix, Inc. purchased $1,000,000 in bonds of Debt, Inc. Matrix paid $975,000 for the

bonds and $25,000 in brokerage fees. The two-year bonds have a stated rate of 6% annually. Interest is paid semi-annually on June 30 and December 31.

On January 1, 2005, Matrix, Inc. purchased $1,000,000 in bonds of Debt, Inc. Matrix paid $975,000 for the

bonds and $25,000 in brokerage fees. The two-year bonds have a stated rate of 6% annually. Interest is paid semi-annually on June 30 and December 31.

McGraw-Hill/Irwin6

15-6

© The McGraw-Hill Companies, Inc., 2006

Basics of Accounting for InvestmentsBasics of Accounting for Investments

Accounting Basics for Debt Securities

Held-to-maturity (HTM) debt securities are recorded at cost when purchased. Interest revenue for investments in debt

securities is recorded when earned.

Held-to-maturity (HTM) debt securities are recorded at cost when purchased. Interest revenue for investments in debt

securities is recorded when earned.

Jan. 1 Long-Term Investment - HTM 1,000,000 Cash 1,000,000

Purchased bonds to hold to maturity

McGraw-Hill/Irwin7

15-7

© The McGraw-Hill Companies, Inc., 2006

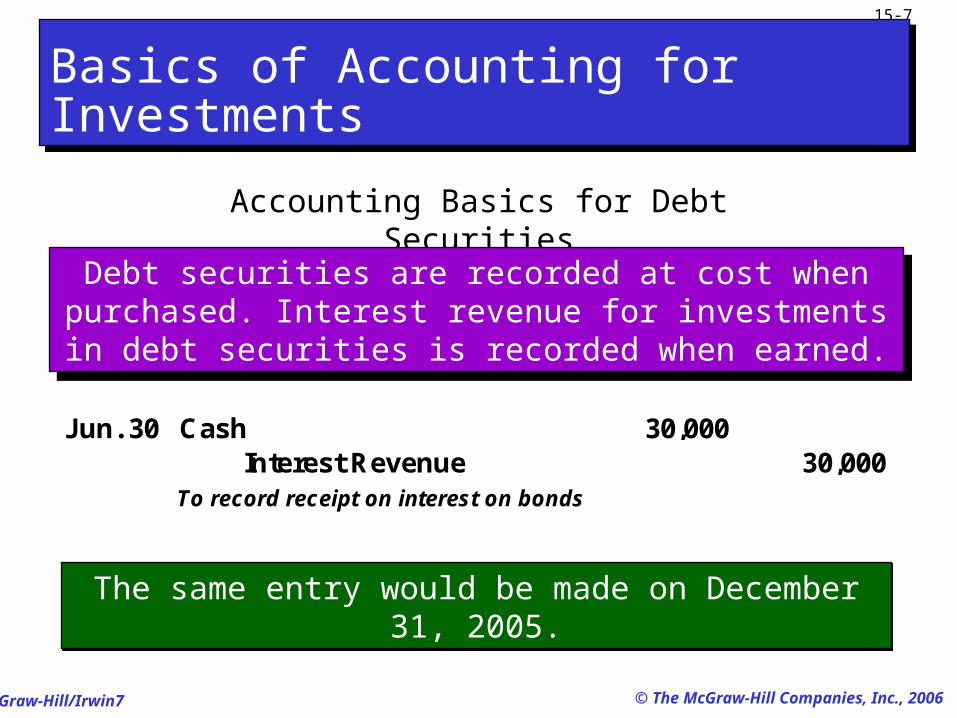

Basics of Accounting for InvestmentsBasics of Accounting for Investments

Accounting Basics for Debt Securities

Debt securities are recorded at cost when purchased. Interest revenue for investments in debt securities is

recorded when earned.

Debt securities are recorded at cost when purchased. Interest revenue for investments in debt securities is

recorded when earned.

Jun. 30 Cash 30,000 Interest Revenue 30,000

To record receipt on interest on bonds

The same entry would be made on December 31, 2005.The same entry would be made on December 31, 2005.

McGraw-Hill/Irwin8

15-8

© The McGraw-Hill Companies, Inc., 2006

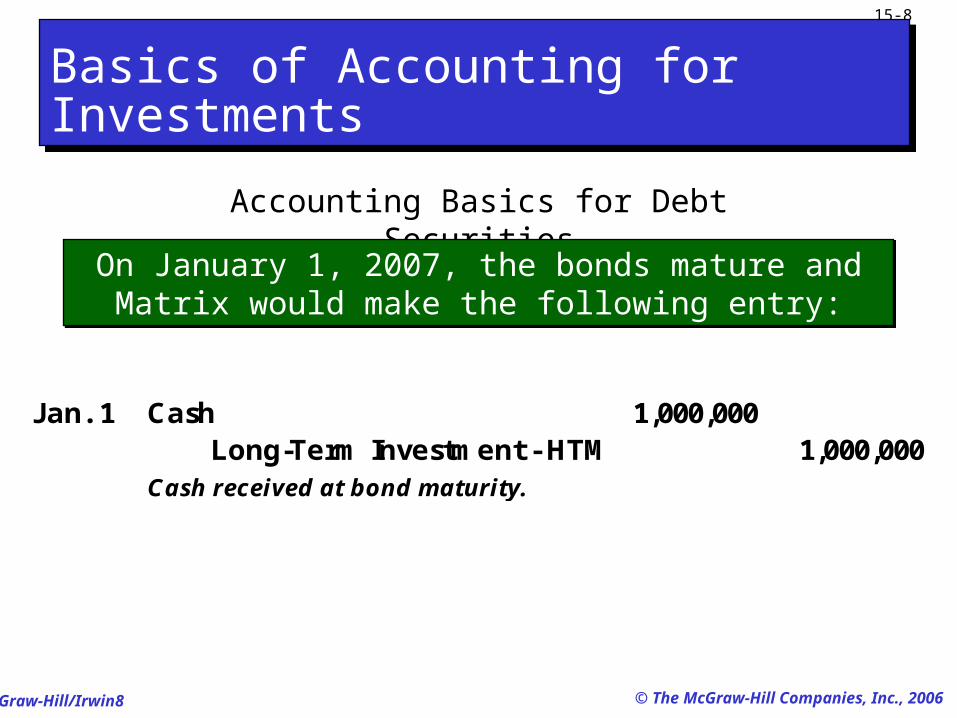

Basics of Accounting for InvestmentsBasics of Accounting for Investments

Accounting Basics for Debt Securities

Jan. 1 Cash 1,000,000 Long-Term Investment - HTM 1,000,000

Cash received at bond maturity.

On January 1, 2007, the bonds mature and Matrix would make the following entry:

On January 1, 2007, the bonds mature and Matrix would make the following entry:

McGraw-Hill/Irwin9

15-9

© The McGraw-Hill Companies, Inc., 2006

Accounting Basics for Equity SecuritiesAccounting Basics for Equity Securities

Equity securities are recorded at cost when acquired, including commissions or brokerage fees paid. Any cash dividends received are credited to Dividend

Revenue and reported in the income statement. When the securities are sold, sales proceeds are compared

with cost, and any gain or loss is recorded.

Equity securities are recorded at cost when acquired, including commissions or brokerage fees paid. Any cash dividends received are credited to Dividend

Revenue and reported in the income statement. When the securities are sold, sales proceeds are compared

with cost, and any gain or loss is recorded.

McGraw-Hill/Irwin10

15-10

© The McGraw-Hill Companies, Inc., 2006

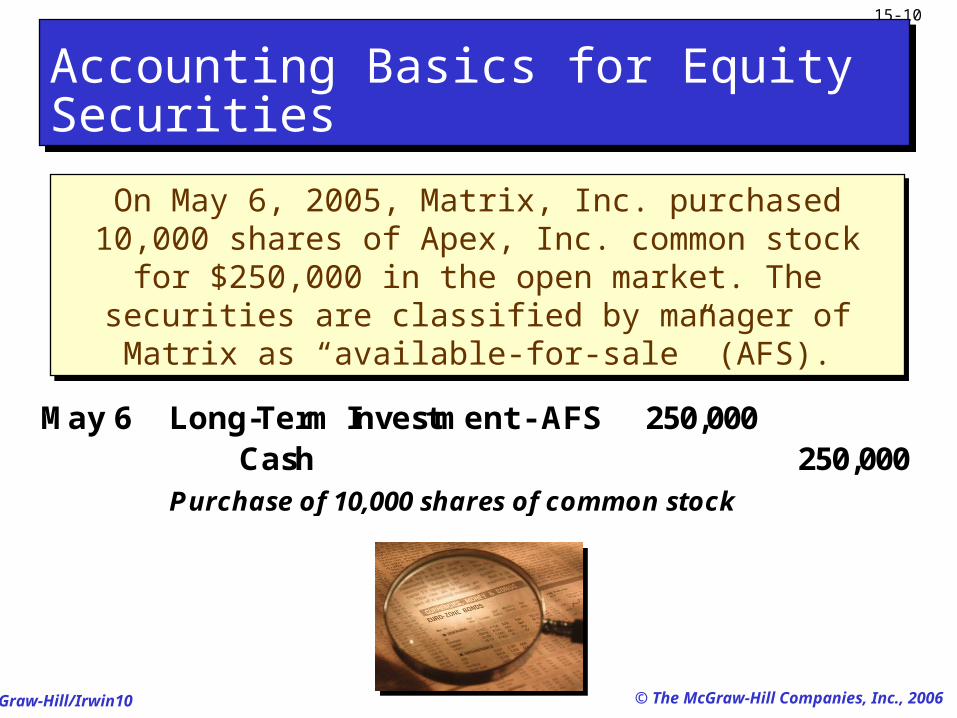

Accounting Basics for Equity SecuritiesAccounting Basics for Equity Securities

On May 6, 2005, Matrix, Inc. purchased 10,000 shares of Apex, Inc. common stock for $250,000 in the open market.

The securities are classified by manager of Matrix as “available-for-sale” (AFS).

On May 6, 2005, Matrix, Inc. purchased 10,000 shares of Apex, Inc. common stock for $250,000 in the open market.

The securities are classified by manager of Matrix as “available-for-sale” (AFS).

May 6 Long-Term Investment - AFS 250,000 Cash 250,000

Purchase of 10,000 shares of common stock

McGraw-Hill/Irwin11

15-11

© The McGraw-Hill Companies, Inc., 2006

Accounting Basics for Equity SecuritiesAccounting Basics for Equity Securities

On June 30, Apex pays a quarterly dividend to Matrix, Inc. of $0.50 per share. Matrix receives a dividend check for $5,000.On June 30, Apex pays a quarterly dividend to Matrix, Inc. of $0.50 per share. Matrix receives a dividend check for $5,000.

Jun 30 Cash 5,000 Dividend Revenue 5,000

Received dividend of $0.50 per share

McGraw-Hill/Irwin12

15-12

© The McGraw-Hill Companies, Inc., 2006

Accounting Basics for Equity SecuritiesAccounting Basics for Equity Securities

On December 18, Matrix, Inc. sells 1,000 shares of Apex, Inc. in the open market for $30 per share.

On December 18, Matrix, Inc. sells 1,000 shares of Apex, Inc. in the open market for $30 per share.

Dec. 18 Cash 30,000 Long-Term Investment - AFS 25,000 Gain on Sale of Investment 5,000

Sold 1,000 Apex shares

$250,000 ÷ 10,000 shares = $25 per share cost

McGraw-Hill/Irwin13

15-13

© The McGraw-Hill Companies, Inc., 2006

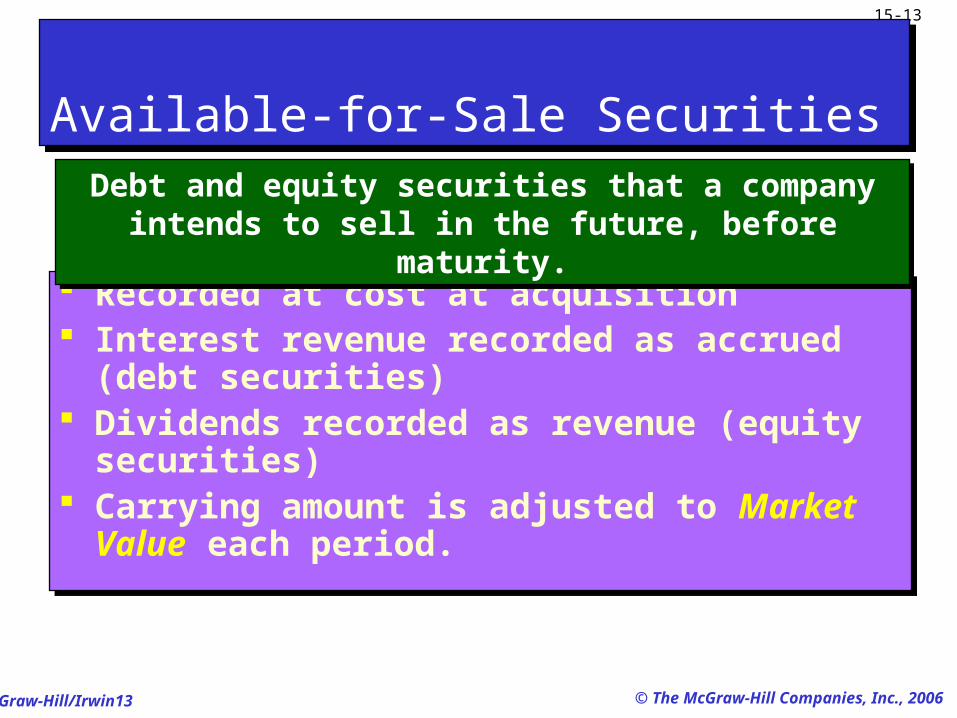

Recorded at cost at acquisition Interest revenue recorded as accrued (debt

securities) Dividends recorded as revenue (equity

securities) Carrying amount is adjusted to Market Value

each period.

Recorded at cost at acquisition Interest revenue recorded as accrued (debt

securities) Dividends recorded as revenue (equity

securities) Carrying amount is adjusted to Market Value

each period.

Available-for-Sale SecuritiesAvailable-for-Sale Securities

Debt and equity securities that a company intends to sell in the future, before maturity.

Debt and equity securities that a company intends to sell in the future, before maturity.

McGraw-Hill/Irwin14

15-14

© The McGraw-Hill Companies, Inc., 2006

Matrix, Inc. purchased 1,000 shares of Apex, Inc. at $5 per share during 2005. At December 31, 2005, the shares had increased in value to $9.50 per share.

Matrix, Inc. purchased 1,000 shares of Apex, Inc. at $5 per share during 2005. At December 31, 2005, the shares had increased in value to $9.50 per share.

Valuing and Reporting Available-for-Sale SecuritiesValuing and Reporting Available-for-Sale Securities

Dec. 31 Market Adjustment - AFS 4,500 Unrealized Gain - Equity 4,500

To adjustment AFS securities to market

McGraw-Hill/Irwin15

15-15

© The McGraw-Hill Companies, Inc., 2006

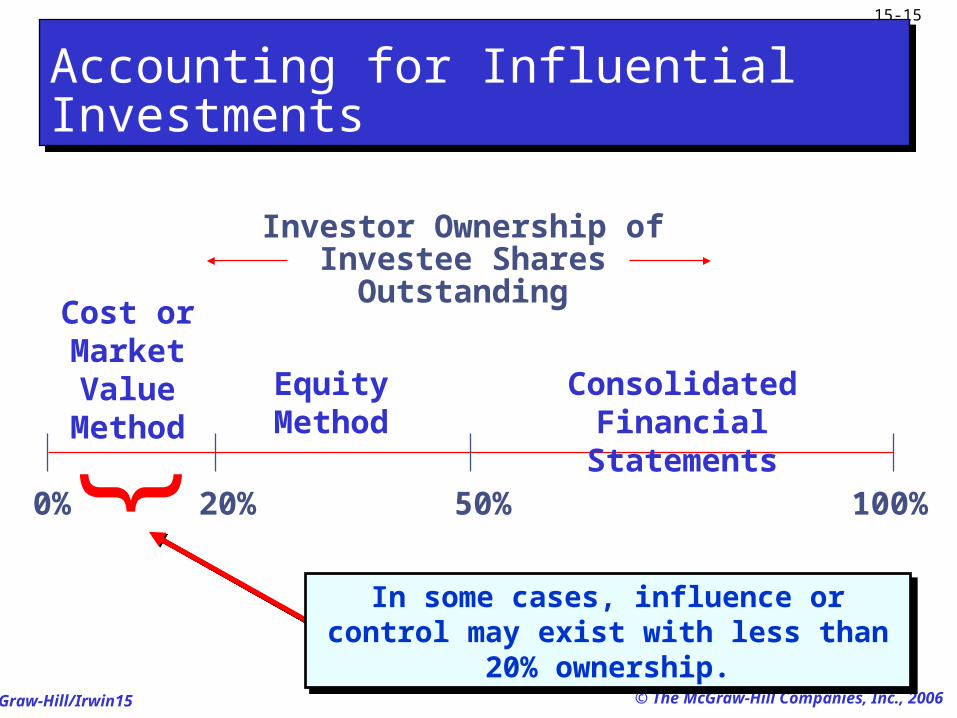

{

In some cases, influence or control may exist with less than 20% ownership.

In some cases, influence or control may exist with less than 20% ownership.

Investor Ownership of Investee Shares

Outstanding

0% 20% 50% 100%

Cost or Market Value

MethodEquity Method

Consolidated Financial Statements

Accounting for Influential InvestmentsAccounting for Influential Investments

McGraw-Hill/Irwin16

15-16

© The McGraw-Hill Companies, Inc., 2006

{Significant influence is generally assumed

with 20% to 50% ownership.Significant influence is generally assumed

with 20% to 50% ownership.

Investor Ownership of Investee Shares

Outstanding

0% 20% 50% 100%

Equity Method

Consolidated Financial Statements

Accounting for Influential InvestmentsAccounting for Influential Investments

Cost or Market Value

Method

McGraw-Hill/Irwin17

15-17

© The McGraw-Hill Companies, Inc., 2006

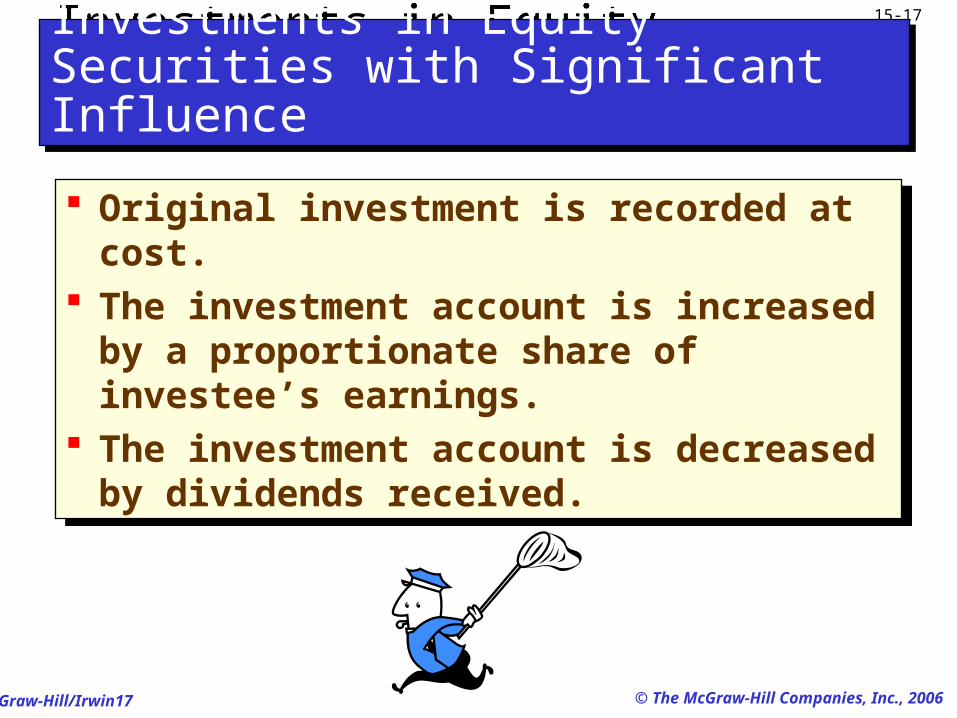

Original investment is recorded at cost. The investment account is increased by a

proportionate share of investee’s earnings.

The investment account is decreased by dividends received.

Original investment is recorded at cost. The investment account is increased by a

proportionate share of investee’s earnings.

The investment account is decreased by dividends received.

Investments in Equity Securities with Significant InfluenceInvestments in Equity Securities with Significant Influence

McGraw-Hill/Irwin18

15-18

© The McGraw-Hill Companies, Inc., 2006

Investment in Equity Securities with Significant InfluenceInvestment in Equity Securities with Significant Influence

On January 1, 2005, Matrix, Inc. buys 20% of the voting common stock of Apex, Inc. for $2,000,000 cash.

Jan. 1 Long-Term Investment - Apex 2,000,000 Cash 2,000,000

To record purchase of Apex common stock

2,000,000

Long-Term Investment - Apex

2,000,000

Cash

McGraw-Hill/Irwin19

15-19

© The McGraw-Hill Companies, Inc., 2006

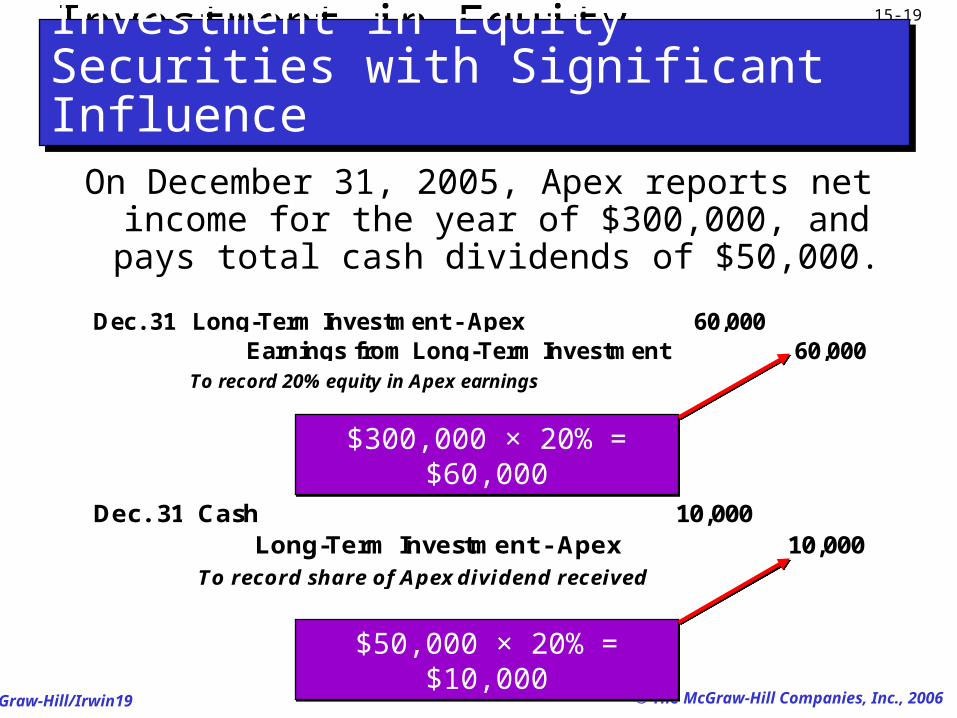

Investment in Equity Securities with Significant InfluenceInvestment in Equity Securities with Significant Influence

On December 31, 2005, Apex reports net income for the year of $300,000, and pays total cash

dividends of $50,000.

Dec. 31 Long-Term Investment - Apex 60,000 Earnings from Long-Term Investment 60,000

To record 20% equity in Apex earnings

Dec. 31 Cash 10,000 Long-Term Investment - Apex 10,000

To record share of Apex dividend received

$300,000 × 20% = $60,000$300,000 × 20% = $60,000

$50,000 × 20% = $10,000$50,000 × 20% = $10,000

McGraw-Hill/Irwin20

15-20

© The McGraw-Hill Companies, Inc., 2006

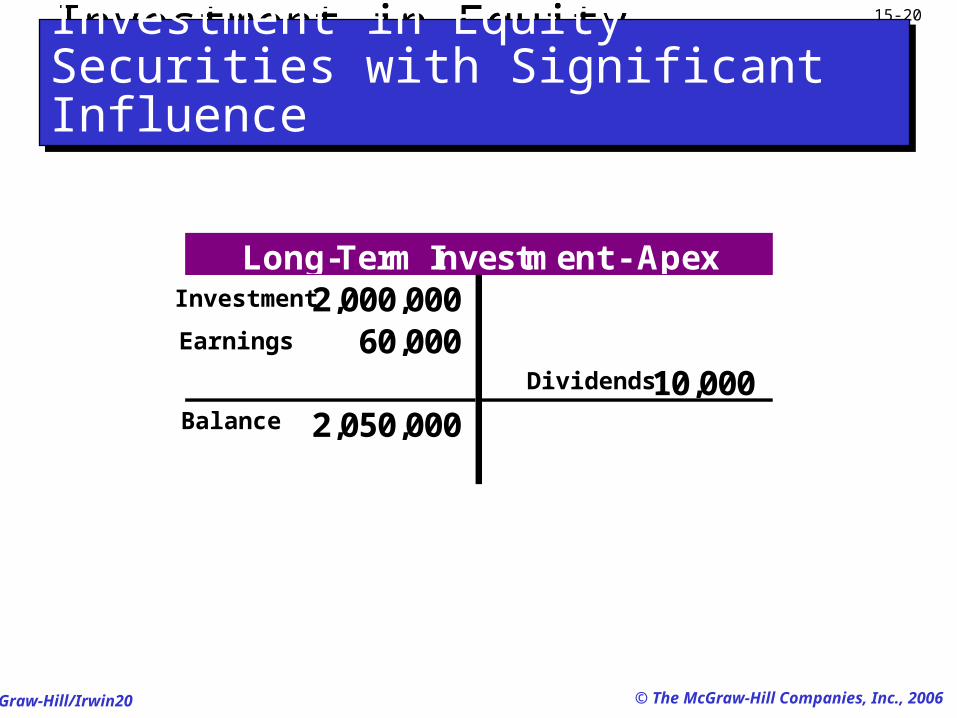

Investment in Equity Securities with Significant InfluenceInvestment in Equity Securities with Significant Influence

2,000,000 60,000

10,000 2,050,000

Long-Term Investment - ApexInvestment

Earnings

Dividends

Balance

McGraw-Hill/Irwin21

15-21

© The McGraw-Hill Companies, Inc., 2006

Investment in Equity Securities with Controlling InfluenceInvestment in Equity Securities with Controlling Influence

o Required when investor’s ownership exceeds 50% of investee.

o Equity Method is used.

o Consolidated financial statements show the financial position, results of operations, and cash flows of all entities under the parent’s control.

McGraw-Hill/Irwin22

15-22

© The McGraw-Hill Companies, Inc., 2006

Accounting Summary for Investments in SecuritiesAccounting Summary for Investments in Securities

Class of Investment Securities Accounting Method

Short-Term I nvestment in Securities

Held-to-maturity (debt securities) Cost (without discount/premium amortization)

Trading (debt and equity) securities Market value (with market adjustment to income)

Available-for-sale (debt and equity) securities Market value (with market adjustment to equity)

Long-Term I nvestment in Securities

Held-to-maturity (debt securities) Cost (with discount/premium amortization)

Available-for-sale (debt and equity) securities Market value (with market adjustment to equity)

Equity securities with significant influence Equity method

Equity securities with controlling influence Equity method (with consolidation)

McGraw-Hill/Irwin23

15-23

© The McGraw-Hill Companies, Inc., 2006

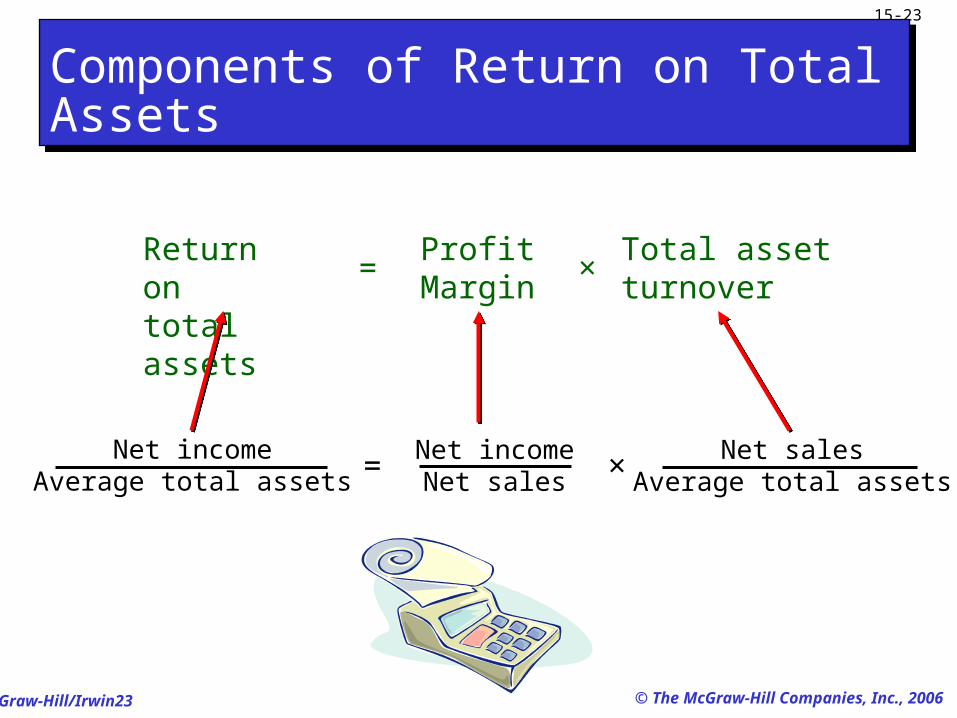

Components of Return on Total AssetsComponents of Return on Total Assets

Return ontotal assets

=ProfitMargin

×Total assetturnover

Net incomeAverage total assets = ×

Net incomeNet sales

Net salesAverage total assets

McGraw-Hill/Irwin24

15-24

© The McGraw-Hill Companies, Inc., 2006

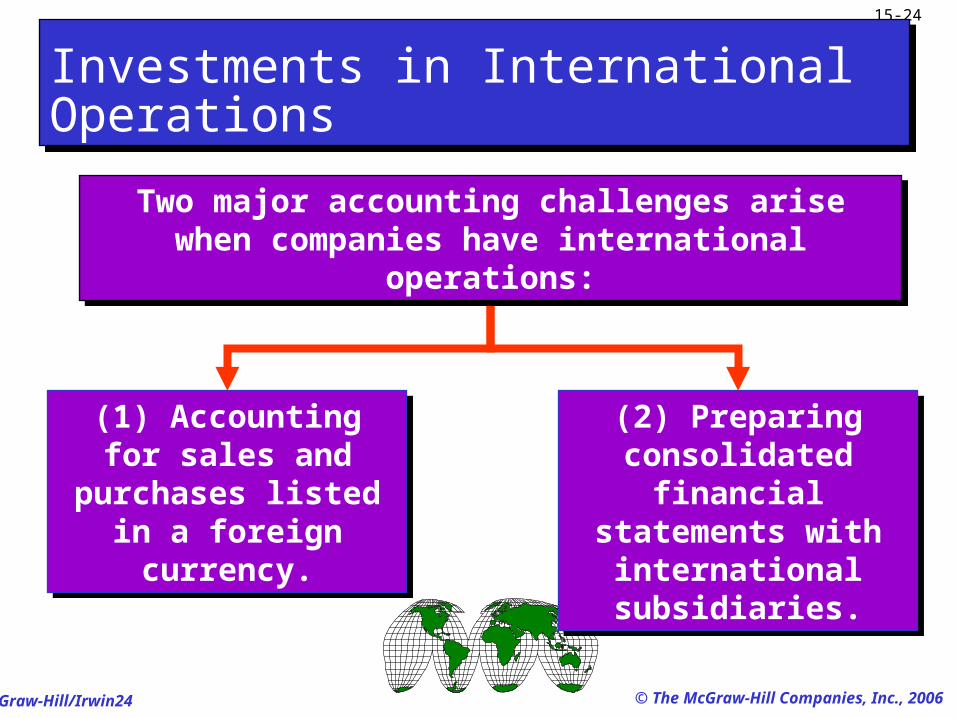

Investments in International OperationsInvestments in International Operations

(1) Accounting for sales and purchases

listed in a foreign currency.

(1) Accounting for sales and purchases

listed in a foreign currency.

(2) Preparing consolidated financial

statements with international subsidiaries.

(2) Preparing consolidated financial

statements with international subsidiaries.

Two major accounting challenges arise when companies have international operations:

Two major accounting challenges arise when companies have international operations:

McGraw-Hill/Irwin25

15-25

© The McGraw-Hill Companies, Inc., 2006

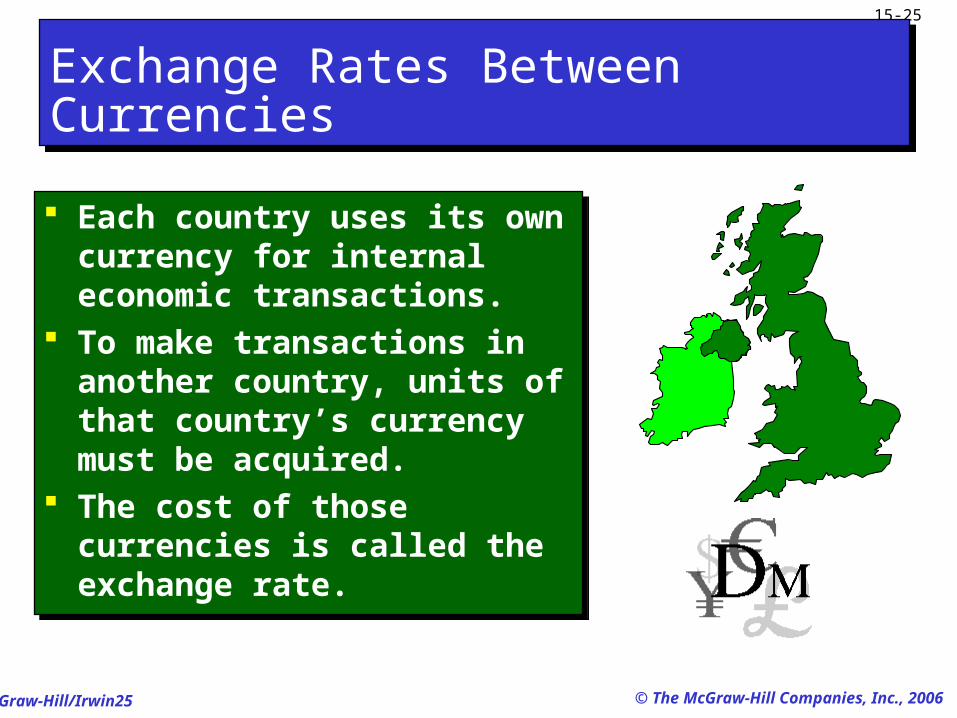

Each country uses its own currency for internal economic transactions.

To make transactions in another country, units of that country’s currency must be acquired.

The cost of those currencies is called the exchange rate.

Each country uses its own currency for internal economic transactions.

To make transactions in another country, units of that country’s currency must be acquired.

The cost of those currencies is called the exchange rate.

Exchange Rates Between CurrenciesExchange Rates Between Currencies

McGraw-Hill/Irwin26

15-26

© The McGraw-Hill Companies, Inc., 2006

Homework for Chapter 15Homework for Chapter 15

Ex 15-4

McGraw-Hill/Irwin27

15-27

© The McGraw-Hill Companies, Inc., 2006

End of Chapter 15End of Chapter 15