Embed Size (px)

Citation preview

Sustainable finance Investment and financing needed for Switzerland to reach net zero by 2050

August 2021

Swiss Bankers Association (SBA) and Boston Consulting Group

Swiss Bankers Association · Sustainable finance 3

Contents

Foreword 4

Executive Summary 9

1 Background and methodology 13

1.1 Aim of the study 13

1.2 Climate mitigation vs. climate adaptation 14

1.3 Methodology 15

2 Measures and investment volumes needed up to 2050 17

2.1 Emissions reduction per sector 17

2.2 Measures and investment volumes per sector 20

3 Assessment of potential financing sources 28

3.1 Presentation of basic decision logic and categorisation 28

3.2 Suitability of possible funding sources for necessary measures 29

4 Framework conditions for the Swiss financial centre 33

4.1 General location factors 35

4.2 Financingneedsthatthefinancialcentreisalreadyabletomeet 36

4.3 Financingneedsnotadequatelymetbythefinancialcentretoday 40

4.4 Public initiatives and major projects 43

4.5 General approaches and accompanying measures 48

Bibliography 50

Appendix 54

Swiss Bankers Association · Sustainable finance4

Foreword

TheFederalCouncilseessustainablefinanceasagreatopportunityfortheSwissfinancialcentreandasa

relevantcompetitivefactorinsustainablegrowth1.TheSwissfinancialcentreshouldbealeadingglobal

locationforsustainablefinancialservices.TheFederalCouncilthereforeintendstoshapetheframework

conditionsinsuchawaythattheSwissfinancialsectorcanmake“aneffectivecontributiontosustaina-

bility”inlinewiththeUN’s2030Agenda.ThiswasthepathsetbytheFederalCouncilbackinJune2020.

TheSwissBankersAssociation(SBA)fullysupportsthegovernment’sobjectivesandisconfident

thattheSwissfinancialcentrecanmakeasignificantcontributiontotheclimatetransitionofthenational

economyasawhole.

MostoftheSBA’sworkin2020wasconcentratedoninvestmentbusiness.2Thisyearweplantofocus

moreonbanks’financingactivityandthecontributionstheymaketowardssustainability.Amongthe

mostpressingissuesherearehowtheSwisseconomycanachievethenetzerotargetsetbytheFederal

Council3,thescaleoftheinvestmentsrequired,andhowtheywillbefinanced.Thisiswherethebanks

canmakeaneffectivecontribution,andourstudyexploreshowtheycandoso.

1 https://www.sif.admin.ch/dam/sif/en/dokumente/dossier/int_finanz-waehrungsfragen/int_waehrungszusammenarbeit/bericht_sustainable_finance.pdf.download.pdf/24062020-Nachhaltigkeit%20Bericht%20Executive%20Summary-EN.pdf.

2 https://www.swissbanking.ch/_Resources/Persistent/5/9/3/b/593b75d1d479ddc70fff20a76991deffd9ca4bab/SBA_Guidelines_for_the_integration_of_ESG_considerations_into_the_advisory_process_for_private_clients_EN.pdf.

https://www.swissbanking.ch/_Resources/Persistent/3/3/e/7/33e7c9a474c72717e1cd19bc547b6f048a020b56/SBA_Sustainable-Finance_2020_EN.pdf.

3 https://www.admin.ch/gov/en/start/documentation/media-releases.msg-id-76206.html.

“Banks can make an effective contribution towards achieving the net zero target.”

Swiss Bankers Association · Sustainable finance 5

Foreword

TheSwisseconomywillhavetoundergoaradicaltransformationifitistoreduceitsGHGemissions.

Thistransitionhasdifferentconsequencesforthevariouseconomicsectors.Takenasawhole,however,

italsopresentsafantasticopportunityfortheSwisseconomy,byopeningupnewmarketsinwhich

ourcountrycanbecomealeadingplayer.Atthesametime,achievingthesegoalswillrequireconsiderable

extrainvestmentstorolloutgreentechnologiesandfindsubstitutesforhigh-emissionactivities.

TakingtheglobalstudybyBCGandGFMA4asastartingpoint,wehaveexploredpotentialmeasures

forreducinggreenhousegasemissionsin10Swisssectorsthattogetheraccountforanestimated

87 percentofnationalemissions.Wehavealsoquantifiedthecorrespondinginvestmentvolumerequired

andanalysedthepotentialsourcesoffundingfortheseinvestments.Thetypesoffinancingstudied

rangefrommortgagelendingtovehicleleasing,SMEloansandthecapitalmarketasawhole.Herewe

considerthevariousinitiativesalreadytakenbySwitzerland’sbankstoapplysustainablecriteriato

theirfinancingactivities.

Suitableincentivesandframeworkconditionsarealsoneededforclimatetransition–anditsfinancing–

inordertomoveforwardsasswiftlyandsmoothlyaspossibleandthusbenefitourdomesticeconomy.

AppropriateincentiveswillencouragemarketforcesthatofferveryeffectivesupportinreducingGHG

emissions.FollowingtherejectionoftheCO₂ActinJune2021,policymakershavetoredefinethe

necessaryapproachesandframeworkconditions.

Thankstoacombinationofexperience,financialexpertise,familiaritywithtechnologicalsolutionsanda

dynamicimplementationdrive,theSwissfinancialcentrealreadycommandsastrongpositioninthefield

ofsustainablefinance.Swissbanksareacutelyawareoftheirresponsibilityhere,andsustainable

financeisaccordinglyatoppriorityfortheSwissBankersAssociation.Wefocusparticularlyontheroleof

investment,financingandcapitalmarkets,aseachonecanmakedifferent,butsignificant,contributions

towardsclimatechangeandsustainability.AstheumbrellaassociationforSwissbanks,weactively

campaignfortheremovalofexistingregulatoryhurdlesforsustainablefinancialinstrumentsinSwitzerland

andforoverallimprovementstotheframeworkconditionsforsustainablefinancialflows.

4 https://www.gfma.org/policies-resources/gfma-and-bcg-report-on-climate-finance-markets-and-the-real-economy/.

Christian SchmidManaging Director and Senior PartnerBostonConsultingGroup

AugustBenzDeputyCEOSwissBankersAssociation

Swiss Bankers Association · Sustainable finance6

“The Swiss economy will have to undergo a radical transformation if it is to reduce its greenhouse gas emissions.”

Swiss Bankers Association · Sustainable finance 7

Imprint

Authors SBA

AugustBenz

Hans-RuediMosberger

ThomasRühl

AlexandreRoch

About the SBA

AstheumbrellaassociationofSwissbanks,the

SwissBankersAssociation(SBA)representsthe

Swissfinancialcentre’sinterestsvis-à-vispoliti-

cians, the authorities and the general public.

Wearecommittedtoentrepreneurialfreedomand

openmarketsandworktowardsanenvironment

inwhichaninnovativeanddiversebankingsector

cangrow.Weareaforward-thinkingknowledge

hub,settingtheagendaandsteeringtheindustry

towardsasuccessfulfuture.

Furtherinformation:www.swissbanking.ch

Authors BCG

Daniel Kessler

Christian Schmid

JannikLeiendecker

DominicReiterlehner

About Boston Consulting Group

BostonConsultingGrouppartnerswithleadersin

businessandsocietytotackletheirmostimportant

challenges and capture their greatest opportuni-

ties.BCGwasthepioneerinbusinessstrategywhen

itwasfoundedin1963.Today,weworkclosely

withclientstoembraceatransformationalapproach

aimedatbenefitingallstakeholders—empowering

organizationstogrow,buildsustainablecompeti-

tive advantage, and drive positive societal impact.

Ourcontinuingsuccessisdrivenbyacombination

ofdigitalandhumanskills.Ourdiverse,global

teamsbringdeepindustryandfunctionalexpertise

andarangeofperspectivesthatsparkchange.

BCGdeliverssolutionsthroughleading-edgeman-

agement consulting, digital technology and

analytics, innovative business models and a clear

understandingofcompanyvalues.Weadopta

uniquelycollaborativemodelacrossthefirmand

throughoutalllevelsoftheclientorganization,

fueled by the goal of helping our clients thrive.

BCGhasofficesinover90citiesandmorethan

50 countries.Itsglobalworkforceof22,000 em-

ployeesgeneratedrevenuesofUSD8.6billion

in 2020.

Furtherinformation:www.bcg.ch

Swiss Bankers Association · Sustainable finance8

“Thanks to a combination of experience, financial expertise, familiarity with technological solutions and a dynamic imple-mentation drive, the Swiss financial centre already com-mands a strong position in the field of sustainable finance.”

Swiss Bankers Association · Sustainable finance 9

Executive Summary

The growing global importance of sustainability and climate protection affects Switzerland as much as any other nation: with total greenhouse gas (GHG) emissions of 46.2 megatonnes (million metric tonnes, Mt) CO₂ equivalents (CO₂e), our country is responsible for 0.1 percent of global emissions and 1 percent of all European emissions. The ten sectors with the highest emissions in Switzerland produce 40.4 Mt CO₂e, equating to around 87 percent of the Swiss economy’s total emissions. Swiss industry must therefore make a considerable effort to reach its net zero target.

Annual investments of around CHF 12.9 bn up to 2050

Switzerland’stransitiontoalow-carboneconomywillrequiretotalinvestmentsofCHF387.2bnover

thenext30years,thebulkofwhich(anestimated77percent)willbeconcentratedinthe2020sand

2030s.Theseinvestmentswillfundtheroll-outofmeasuresneededtoreduceGHGemissionstoachieve

the2050netzerotargetforSwitzerland’stensectorswiththehighestemissions.Toputthisincontext,

therequiredlevelofdomesticinvestmentamountstoapproximately0.2percentoftheglobalinvestment

volumeofaroundUSD178trillion.Switzerland’s

investmentvolumeisthereforealmosttwice

ashighcomparedwithitsshareofCO₂emissions

(0.1percent).Around58percentoftheCHF 12.9 bn

annualinvestmentvolumeisearmarkedforre-

placingexistingsolutions,whilearound42 per-

centisdestinedfornewinvestments.Alarge

part of the investments required are concentrated

onthesectorsLightRoadTraffic,BuildingsandHeavyRoadTraffic.Acomparisonwiththeaverageannual

increaseinmortgagevolumeofCHF 30.1 bnshowsthat,althoughtheadditionalinvestmentrequiredfor

thebankingsystem’stransitionisquitesubstantial,itdoesnotthreatenstabilityandisnotbeyondreach.

TheannualinvestmentneededtoachieveclimatetargetsworksoutataroundtwopercentofSwitzerland’s

grossdomesticproduct(2019:CHF727bn).

“The traditional offering of Swiss banks can cover 83 percent of the investment requirement.”

Swiss Bankers Association · Sustainable finance10

Executive Summary

Swiss financial centre and government can meet almost all of the funding required

ThetraditionalofferingofSwissbankscancoverthelion’sshare(83percent)oftheinvestmentrequire-

ment.OntopofCHF 10.7 bninbankloans,anotherCHF1.0bn(8 percent)couldbefinancedbytheSwiss

capitalmarket.Thebankloansneededforclimatetransitionwouldthereforemakeup10.8percentof

theCHF99bninmortgagesandbusinessloansissuedeveryyearbySwissbanks.Ontheonehand,this

createsnewbusinessopportunitiesforthebanks.Ontheotherhand,thefinancialindustrywillhave

to address the logistical challenges presented by the considerable volume and diversity of these loans,

whileatthesametimeworkingwithinexistingregulatoryconstraints.Bycontrast,thecapitalmarket

financingofaroundCHF1.0bnneededforclimatetransitionwouldonlyaccountforasmallproportion

(1.6percent)oftotalannualbondissuesontheSwissexchange(2019:CHF62bn).Around7percent

(CHF0.9bn)ofinvestmentsrelatetopublicgoodssuchastheexpansionofpublictransport,whichis

traditionallysupportedbystatesubsidies.TheremainingCHF0.3bn(2percent)presentcertain

challenges because the technologies required, such as carbon sequestration and storage, are relatively

immatureandneedspecialattention.Approachessuchasblendedfinanceorpublic-privatepartnerships

can provide solutions for these investments.

Switzerland’sfinancialcentrehasanimportantroletoplayinachievingthegovernment’snetzerotarget

fortheSwisseconomy.AsdemonstratedbythelendingprogrammetoSMEsduringthecoronavirus

crisis,Swissbanks’physicalproximityandlong-standingclientrelationshipsprovideanidealplatformfor

deliveringefficientfinancesolutions.Thesupportofthewholesector–fromregionalbanksthroughto

cantonalandthelargeSwissbanks–togetherwiththeirentireofferingofproductsandservices(including

mortgages,SMEloans,vehicleleasingandcapitalmarkettransactions)arenecessarytoensureoptimal

coverage of individual funding requirements.

Net zero target achievable through funding from the banks’ own initiatives and favourable framework conditions

Toperformitsroleeffectivelyandtothenecessaryextent,theSwissfinancialcentrerequiresacombina-

tionofowninitiativesbyfinancialinstitutionsandsuitableframeworkconditions.Manyinstitutionshave

alreadysigneduptoglobalinitiativessuchasthePrinciplesforResponsibleBanking(PRB).Manyalso

report climate compatibility indicators, such as TCFD or testing of climate alignment goals by the Federal

OfficefortheEnvironment(FOEN).Somehavecreateddedicatedofferingsforfinancingclimate-orient-

edinvestments.Asfarasframeworkconditionsareconcerned,additionalrestrictionsonfundingactivity

havebeensuccessfullyavoidedtodate.Onlyastrongfinancialcentrewillbeinapositiontoplayakey

roleinsupportingSwitzerland’stransitiontoalow-carboneconomy.Inaddition,theregulatorcancreate

regulatoryincentivesforclimate-orientedfinancing,aspartofa“greensupporting”approach.

Executive Summary

Swiss Bankers Association · Sustainable finance 11

Switzerland’s commitment to climate transition can have a signalling effect

ThegoaloftheSwissgovernmentandfinancialcentreistomakeSwitzerlandaleadingglobalhubfor

sustainablefinance.Financingandachievingnetzerocarbonemissionsby2050isakeycomponentof

thisandwillstrengthenthecompetitivenessbothofSwitzerland’seconomyanditsfinancialcentre.

ByworkingtogetherwiththeSwisseconomyinthismanner,banksalsomakeaneffectivecontributionto

sustainabilityandtoclimateprotectionasanimportantpublicgood.Asanaffluentandtechnologically

advancedsociety,Switzerland’sclimatetransitioncanprovideaclearsignallingeffectforothercountries.

Thisstudymakesafact-basedcontributiontothistransitionandsuggestswaysoffinancingit.

Swiss Bankers Association · Sustainable finance12

“Implementing the various CO₂ reduction measures will require significant efforts across all sectors.”

Swiss Bankers Association · Sustainable finance 13

Aim of the study 1.1

1 Background and methodology

If Switzerland is to achieve its goal of becoming carbon neutral (net zero) by 2050, its economy must switch to activities with lower emissions. This will require the implementation of numerous technical and behavioural measures capable of reducing GHG emissions. The pricing of external effects (in the form of a carbon tax, for example) is very important, as climate protection then becomes not just a global and long-term public good, but also a private good. This provides a financial incentive for companies and private households to reduce their emis-sions. In industry especially, these reductions are associated with investments in new plant and equipment that need to be financed through own funding or external capital. Other investments focus on the development of new, greener technologies, which often tend to be long term and high risk.

1.1 Aim of the study

ImplementingthevariousCO₂reductionmeasureswillrequiresignificanteffortsacrossallsectors.On

theonehand,thisentailsanadjustmentintheuseofenergyandresources,whichinturnchangesthe

structureofcompanies’runningcosts.Ontheotherhand,itinvolvestheuseofnewtechnologiesand

modifiedprocesses,supportedbythenecessarylevelofinvestment.TheSwissfinancialcentreplays

akeyroleasthemainsourceoffinancingforsuchinvestments.Thefocusofthisstudyisthereforeon

· outliningthetransitionpathwaysandthenecessarymeasuresatsectorlevelinordertodeterminethe

investmentvolumeneededtofundSwitzerland’sGHGreductiontargetsupto2050(seeChapter2)

· discussing the possible sources of funding and their suitability for the sector-level measures identified

previously(seeChapter3)

· definingtheframeworkconditionsrequiredforsuitablefundingthroughtheSwissfinancialcentre

(seeChapter4)

Swiss Bankers Association · Sustainable finance14

1.2 Climate mitigation vs. climate adaptation

1.2 Climate mitigation vs. climate adaptation

Thisstudydistinguishesbetweenclimatemitigationandclimateadaptation.Climatemitigationrefersto

theactivereductionofGHGemissionsthroughsuitabletechnicalandbehaviouralmeasures,andis

oftenreferredtoas“climateprotection”.Climatemitigationisverydistinctfromadaptation,whichthe

IPCCdefinedasfollowsin2001:“Inhumanornaturalsystems,theprocessofadjustmenttoactualor

expectedclimatechangeanditseffects,inordertomoderateharmorexploitbeneficialopportunities”

(IPCC2001).Inotherwords,itisaresponsetochangingclimaticconditions,suchastheexpansionof

flooddefences.

Whendeterminingthemeasuresandtherelevantinvestmentvolumesneededtoachievenetzeroin

Switzerland,thisstudydidnotincludethepotentialcostsofclimateadaptation.However,itisimportant

tonotethatthereisastrongconnectionbetweenclimatemitigationandadaptation:ifnoactionis

takenintheareaofclimatemitigation,worseningclimateconditionsandextremeweathereventswillresult

inhigherclimateadaptationcosts.Conversely,loworineffectiveclimateadaptationleadstohigher

climate-relatedlosses,whichinturnpushesupinsurancecosts.Higherinsurancepremiumswouldalsohave

adirectimpactonthecreditworthinessofmitigation-relatedinvestments.Becauseofthisinterde-

pendence, climate mitigation is becoming an increasingly important means of containing consequential

losses.

Mitigationandadaptationalsodifferwithregardtophysicalscale,however:althoughclimatechangeis

aninternationalconcern,thebenefitsofadaptationarepredominantlylocal,whiletheadvantagesof

mitigationareglobal.Thedifferencealsoextendstothetimedimensionandthebusinesssectorsaffected.

Whendiscussingtheframeworkconditionsforfinancingthetransition,wethereforeneedtoview

adaptationandmitigationfromasocietal(andconsequentlypolitical)perspectiveaswell.Intheeyesof

policymakers,climateadaptationismainlyalocal,privategood,oftenwithclearandimmediatebenefit.5

Climatemitigation,ontheotherhand,isaglobal,publicgoodwithfar-reachingbenefit.Thisisexactlywhy

theverydiverseformsoffundingcannotbeconsistentlyplacedinalocal,privatecontext.Established

formsoffundingarenotalwayscapableofmeetingthechallengesofmitigationfinancing.Itistherefore

importanttocheckwhetheradditionalsolutionsandframeworkconditionsexisttoplugfinancinggaps.

5 Incontrasttoprivategoods,publicgoodsarecharacterisedbytheirnon-excludabilityandnon-rivalryinconsumption.

Swiss Bankers Association · Sustainable finance 15

Methodology 1.3

1.3 Methodology

InDecember2020,theGlobalFinancialMarketAssociation(GFMA)andBostonConsultingGroup(BCG)

publishedajointstudy:“ClimateFinanceMarketsandtheRealEconomy”.Basedonthetensectors6

withthehighestGHGemissionsglobally,thediscussionfocusedonthemeasuresrequiredforclimate

transition,leadingtoanestimateoftheinvestmentvolumeneededovertheperiod2020–2050(exclud-

ingprivateinvestments).GlobalinvestmentswereestimatedtobeintheregionofUSD100–150 tril-

lion7,withEuropeaccountingforUSD21trillion.Ourstudytakesasimilarapproachwhenestimatingthe

investmentvolumeneededfortheSwisseconomy(supplementedbyprivatefunding),basedonthe

GHGemissionsofthesametensectors.Inthiscontext,however,noexplicitconsiderationwasgivento

the potential consequences of climate mitigation for running costs. To ensure adequate validation of

thestudy’sfindings,therewasfullconsultationwithrepresentativesfromindividualindustryassociations

tomakeallowancesforthespecificcharacteristicsofSwitzerland’seconomy.

Forthepurposesofthisstudy,thefocuswasontheSwisseconomy’stotalgreenhousegasemissions,

basedonthecurrentFOENdefinition.Asaresult,thefollowingemissions,whichareonlypartiallylinked

toSwissclimatetargetsortheSwissfinancialcentre,arenotconsideredfurther:

· EmissionsofcompaniesdomiciledabroadbutfinancedbySwissbanks,

· EmissionsgeneratedbySwisscompaniesoperatingabroad,

· CO₂emissionsofimportedgoods(In2018theseso-called“grey”emissionscametoaround74Mt8,

equivalentto1.6timesthedomesticemissionsoftheSwisseconomy.Nofurtherconsiderationis

giventotheseemissions,astheyarealreadyincludedintherelevantcountryoforigin’sCO₂statistics,

andSwissbankspresumablyplayonlyaminimalroleinfinancingthesecompanies),

· GHGbalanceofsubstitutioninvestments,inotherwords,theclimateimpactsofdisposingofdecom-

missioned plant and equipment, the climate impacts of the production of substitution investments,

and the effects of potentially reduced substitution cycles.

6 Hereasectorreferstoanareaofbusinesswhereundertakings,companiesorprivateindividualssharethesameorarelatedproduct or service.

7 Source:GFMA/BCGstudy“ClimateFinanceMarketsandtheRealEconomy”(December2020).8 Source:FederalStatisticalOffice–EnvironmentalAccounts2020(GHGemissionsbasedonSwissenddemand).

Swiss Bankers Association · Sustainable finance16

1.3 Methodology

TherepresentationoftherespectiveclimatepathwayswasbasedontheplannedSwissclimatetargets

persector.Wheresuchasector-specificclimatetargetwasunavailable,alinearannualreductionwas

assumedtoachievea50percentsavingby2030comparedwith1990levels,andnetzerocarbonby

2050.Inaddition,GHGemissionsfor2019weretakenasabasisforsubsequentcalculationsinorder

toavoidpotentialdistortionscausedbytheeffectsofthecoronaviruspandemic.

Switzerland’s “grey” emissions (imports 74 Mt)

CO₂ emissions of foreign companies

Rest of the world

(global: 53,000 Mt)

CO₂ emissions of Swiss companies

Switzerland(46 Mt)

Potential CO₂ emissions of Swiss and foreign companies financed by

Swiss banks or the Swiss capital market

Note: all scaling is indicative onlySource: ownrepresentation,FederalOfficefortheEnvironment,UNFCCCGHGDatainterface

Figure 1

In focus: Swiss economy’s greenhouse gas emissions

Focus of the Study:

Domestic CO₂ emissions of

the Swiss economy

Swiss Bankers Association · Sustainable finance 17

Emissions reduction per sector 2.1

2 Measures and investment volumes needed up to 2050

2.1 Emissions reduction per sector

In2019globalgreenhousegasemissionsamountedto53,000Mt9(measuredinCO₂equivalents,CO₂e),

withEuropecontributing5,000Mt.Switzerland’stotaloutputof46.2Mt10makesup0.1percentofglobal

emissions,or1percentofEuropeanemissions.ThetensectorswiththehighestemissionsinSwitzerland

produced40.4Mt,equivalenttoaround87percentoftheSwisseconomy’stotalemissions(atthe

globallevel,theGFMA/BCGstudyestimatedthecontributionofthese10sectorsat75percentoftotal

emissionsworldwide).Thefollowingsectionthereforeprovidesmorein-depthanalysis.

9 Source:UNFCCCGHGDataInterface.10 Source:FederalOfficefortheEnvironment(FOEN).

46.2

11.1

6.5

3.4

3.32.8 1.4

0.4 0.1 0.1

5.8 5.7

11.2

Figure 2

CO₂ emissions per sector

SwissGHGemissionsbysector,2019

[MtCO₂e]

Tota

l

LightRoad

Traffic

Buildings

Agr

icul

ture

HeavyRoad

Traffic

Ener

gy

Cem

ent

Che

mic

als

Met

al a

nd S

teel

Do

mes

tic

Air

Tra

vel

Ship

ping

Others

International

Air

Tra

vel

Source: FederalOfficefortheEnvironment

87 %

Swiss Bankers Association · Sustainable finance18

2.1 Emissions reduction per sector

ThebiggestemittersinSwitzerlandarethesectors“LightRoadTraffic”(11.2MtCO₂e)and“Buildings”

(11.1MtCO₂e),withacombinedshareofalmost48percent.Thefractionproducedbybothsectorsis

disproportionatelyhighbyEuropeanstandards.Bycomparison,thesetwosectorsonlyaccountforjust

under26percentoftotalCO₂emissionsinEurope.

Thehighfigurefor“LightRoadTraffic”canbeexplainedbythestrongerpurchasingpowerinSwitzerland

andthepopularityofhigh-performanceprivatecars–everyothernewvehicleinSwitzerlandisanSUV11

producinghigheremissionsthanmorecompactmodels.Thiswillrequiremeasurescoupledwithsubstantial

investment in order to meet the planned climate target of a 25 percent reduction in emissions by 2030

comparedwith1990levels,equivalenttoacutfrom11.2MtCO₂eatpresenttoaround8.6MtCO₂ein

2030.

Thecurrentproportionofoil-firedheatingintheSwissbuildingsectoristhehighestinEurope12.Over

twothirds13ofbuildingsinSwitzerlandareheatedwithfossilfuelsandmorethanamillion14 homes

requireenergyefficiencyimprovements.Thecurrentrateofrefurbishmentisonlyaroundonepercent15,

but that rate has to be at least doubled to achieve national climate targets. The emissions reduction

goalsetforthebuildingsectorrequiresasavingof65percentby2030comparedwith1990levels.Asa

result,thecurrentlevelof11.1MtCO₂emissionsneedstobecuttoaround5.8Mtby2030.Anational

buildingprogrammewaslaunchedbackin2010,andaprogrammeoffederalsubsidiesaddedin2017.

Additionalstepsarestillneeded,however,andthesewillbeexploredinmoredetailinthenextchapter

asweidentifythemeasuresrequiredatsectorlevel.

TheagriculturalsectoristhethirdhighestemitterinSwitzerland,withannualgreenhousegasemissions

ofaround6.5MtCO₂e.Farmingaccountsfor14percentofSwitzerland’sGHGemissions(including

nitrousoxideandmethane),afigureroughlyinlinewiththerestofEurope(12percent).Thesector’sworst

emitterislivestockfarming–especiallycattle.Furthermore,thebulkofammoniagasemittedinSwitzer-

landoriginatesfromslurry(liquidmanure),sosomeoftheemissionsproducedthroughfarmingarevery

difficulttoavoid.Toallowforthespecificattributesoftheagriculturalsector,andtoensureasecure

food supply, the climate target set for the sector is therefore a reduction of only 20 percent by 2030, or

acutofonethirdby2050comparedwith1990levels.Atthesametime,itisimportantthatclimate

protectionmeasuresdonotresultinproductionconstraintsoracompetitivedisadvantageforSwiss

farming.

11 Source:Auto-Suisse“Newpassengercarregistrations2020”.12 Source:Eurofuel“Energysourcesforheatingbuildings”.13 Source:SwissFederalOfficeofEnergy(FFOE).14 Source:FederalOfficefortheEnvironment(FOEN)–“Thefederalandcantonalbuildingsprogramme”.15 Source:SwissNationalScienceFoundation(SNSF).

Swiss Bankers Association · Sustainable finance 19

Emissions reduction per sector 2.1

Inthecaseof“Domesticairtravel”16,theGHGemissionsreportednationallybytheFederalOfficefor

theEnvironment(FOEN)areminimal.Bycontrast,emissionsfrominternationalairtravel(notcountedin

thenationalfigure17)arefarmorerelevant,at5.7MtCO₂e.Comparedwithneighbouringcountries,the

Swisstaketotheairtwiceasoften,withover80percent18ofSwisspassengersflyingtoEuropeandestina-

tions.Forthe“Internationalairtravel”sector,alinearreductioninthecurrentlevelofgreenhousegas

emissions(5.7Mt),withaninterimtargetof3.8Mt(2030),issetastheclimategoalfor2050.

TheenergysectoristhebiggestemitteratEuropeanlevel,witha26percentshareofCO₂emissions.It

alsoaccountsforasimilarpercentageofCO₂emissionsonagloballevel.InSwitzerlandthefigureisjust

7 percent.Thisisduetothefactthat,eversinceelectrificationbegan,Switzerlandhassourcedenergy

fromrenewablessuchashydroelectricpower,benefitingfromthecountry’stopographyandplentiful

rainfall.In2019,almost57percentofSwisselectricityconsumptioncamefromhydroelectricplants.

Inaddition,thecountry’sfournuclearpowerplantsplayakeyroleinprovidingacomparativelyeco-

friendlypowersupply,accountingforaroundathird 19oftheelectricityproducedinSwitzerland.20

Thetargetsetfortheenergysectorenvisagesa50percentcutinCO₂emissionsby2030comparedwith

1990levels,orareductionfrom3.3Mt(2019)to1.3Mtin2030.

TheremainingCO₂emissionsarespreadacrossthesectors“HeavyRoadTraffic”,“Cement”,“Chemicals”,

“MetalandSteel”and“Shipping”,allofwhichareexpectedtoworktowardsanetzerotargetby2050,

withonlyminordeviationsfromthe2030targets.

16 Includingtheimpactofmilitaryandhelicopterflights.17 AccordingtotheguidelinesoftheUnitedNationsFrameworkConventiononClimateChange(UNFCCC),thenationaltotal

doesnottakeintoaccountgreenhousegasemissionsfrominternationalairtravel;undertheUNFCCC,eachcountryrecordsbothdomesticandinternationalflightsaccordingtotheamountofaviationfuelconsumedinthecountry–thiscorrespondstotheamountoffuelrequiredforallflightsdepartingfromtheirowncountrytothedestination.

18 Source:FederalStatisticalOffice(FSO).19 Source:NuclearpowerstationKernkraftwerkGösgen-DänikenAG(KKG).20TheEnergyStrategy2050adoptedbytheFederalCouncilprescribesawithdrawalfromnuclearpower,amongstotherthings.

Theresultingenergyproductiongapistobefilledbyrenewables.

“ThebiggestGHGemittersinSwitzerlandarethesectorsLightRoadTrafficandBuildings, withacombinedshareofalmost 48 percent.”

Swiss Bankers Association · Sustainable finance20

2.2 Measures and investment volumes per sector

2.2 Measures and investment volumes per sector

Thetransitiontoalow-carboneconomywillrequiresubstantialinvestmentsoverthecomingyearsto

supporttheroll-outoftherequiredmeasures.AverageannualinvestmenttothetuneofCHF12.9bn

(includinginternationalairtravel)isneededtoreduceemissions,mainlyconcentratedonthesectors

“LightRoadTraffic”,“Buildings”and“HeavyRoadTraffic”.21

Tomeetemissionreductiontargets,Switzerlandwillthereforeneedatotalinvestmentvolumeof

CHF387.2bn(includinginternationalairtravel).22Theleveloffundingwillbehigherbothduringthe

2020s,whentheaverageannualinvestmentvolumewillbeCHF16.6bn(withCHF10.3bnspenton

substitution),andthe2030satCHF13.2bn(CHF7.2bnsubstitution),whichequatesto77.1percentof

21 Theinvestmentrequiredisbasedonalevelpopulationandunchangedeconomicstructure.Theeffectsofgrowth,changesin demand and structural change are not considered here.

22 The spread of investments over time is based on assumptions about future innovation developments and price trends for the relevant technologies.

12,9005,708

2,144

170

1,8861,233

99290

16198 156 0

1,008

Tota

l

LightRoadTraffic

Buildings

Agr

icul

ture

HeavyRoadTraffi

c

Ener

gy

Cem

ent

Che

mic

als

Met

al a

nd S

teel

Do

mes

tic

Air

Tra

vel

Ship

ping

Others

International

Air

Tra

vel

Figure 3

Investments per sector

Swissnetzeroinvestmentvolumesp.a.,2020–2050

[CHFm]

Note: the spread of investments over time is based on assumptions about future innovation developments and price trends for therelevanttechnologies(seeAppendix).Source: ownestimate

Swiss Bankers Association · Sustainable finance 21

Measures and investment volumes per sector 2.2

totalinvestments.Bycontrast,theaverageinvestmentvolumeinthe2040swillbelower,atCHF8.8bn

(CHF5.0bnsubstitution).Thevariationovertimeismainlyduetothetechnicalavailabilityofselected

measures.Thesubstitutioneffectisexpectedtoincreaseovertime–inotherwords,investmentsthat

wouldhavebeennecessaryirrespectiveofclimatetransition,suchasthemodernisationoftruckfleets–

and is mainlylinkedtotheacquisitionofnewcommercialvehiclesandaircraft.Herethesubstitution

effectdropsfromaround62percentinthe2020stoaround57percentinthe2040s.

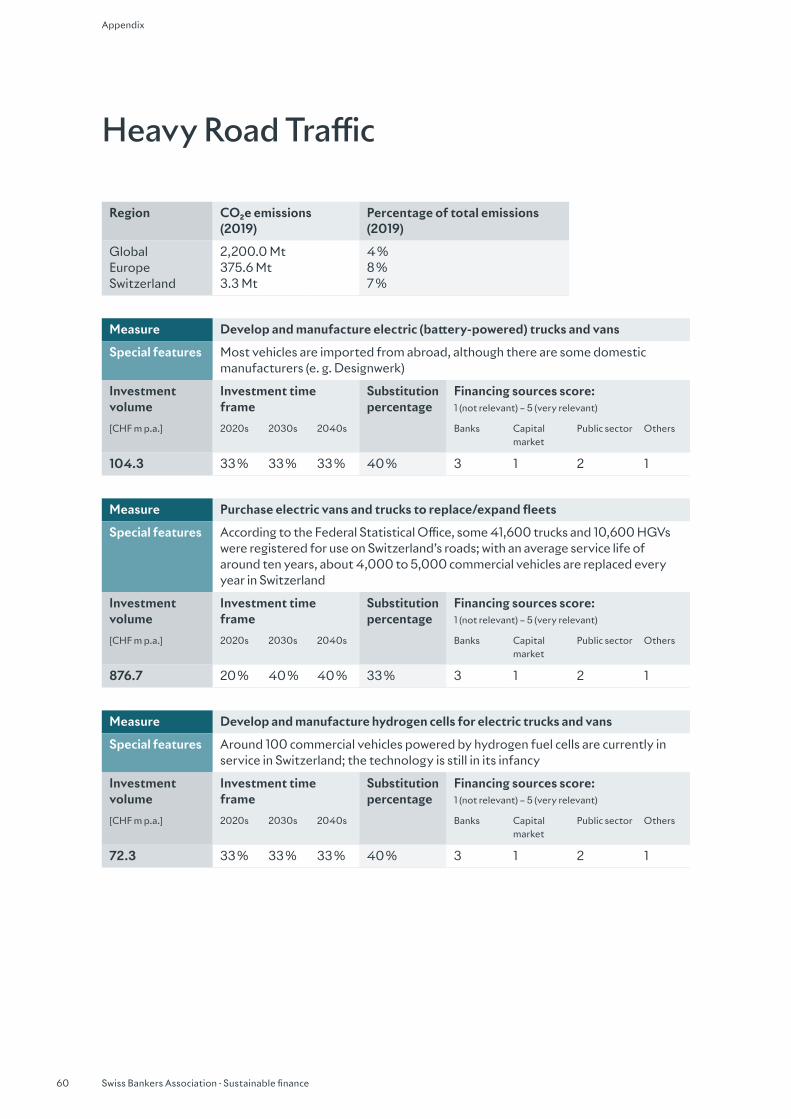

The climate transition of the “Heavy Road Traffic” 23sectorwillrequireaverageannualinvestmentsof

CHF1.9bnupto2050.Thefocusherewillbeonthesubstitutionorexpansionofexistingtransport

fleetsthroughthepurchaseofelectriccommercialvehiclespoweredbybatterypacksorhydrogencells.

In2020,around41,600trucksand10,600articulatedlorrieswereregisteredforuseinSwitzerland24.

23 Vehiclesweighingmorethan3.5tonnes.24Source:FederalStatisticalOffice(FSO)“FahrzeugeundTransportmittelbeständedesGüterverkehrs”(Jan.2021,Germanonly).

CHF131.9bn

CHF166.9bn

CHF88.4bn

Note: the spread of investments over time is based on assumptions about future innovation developments and price trends for the relevanttechnologies(seeAppendix).Source: ownestimate

2020s 2030s 2040s Year

Figure 4

Investments over time, including substitution effect

Swisseconomy’stotalinvestmentrequirementovertime

[CHFbn]

Newinvestments

Substitution investments

2021

2022

2023

2024

2025

2026

2027

2028

2029

203

0

203

1

203

2

203

3

203

4

203

5

203

6

2037

203

8

203

9

204

0

204

1

204

2

204

3

204

4

204

5

204

6

204

7

204

8

204

9

2050

Swiss Bankers Association · Sustainable finance22

2.2 Measures and investment volumes per sector

FreighttransportwithinSwissnationalbordersisbyfarthedominantsegmentwithinheavyroadtraffic.

In2019,domesticfreightaccountedforjustundertwothirds(65 percent)oftotaltransportvolume.Export

andimporttrafficmadeup26 percentandtransittrafficjust9 percent25. Essentially, inland transport is

onlycarriedoutbydomesticcommercialvehicles,asforeigncommercialvehiclesarenotpermittedfor

roadconsignmentswithinSwitzerlandduetotheso-calledcabotageban.

Bycontrast,foreigntrucksandarticulatedlorriesdominatetransittraffic,aswellasimportsandexports.

Thepriceofagreenprototypetruckiscurrentlyaroundthreetimeshigherthanaconventionalmodel,

whichcostsaroundCHF100,000onaverage.Withanaverageservicelifeofabout10years,between

4,000 and 5,000 commercial vehicles are typically replaced every year. This requires average annual

investmentsintheregionofCHF1.5bn,with33percentofthissumattributabletosubstitution.Atthe

sametime,around80percentofinvestmentswillonlytakeplaceinthe2030sand2040s,ascurrent

technologyisstillinitsinfancy.Ontopofthat,thebroaderuseofbiofuelsorsyntheticfuelsplaysan

importantrole.Theramp-upofhydrogenproduction,alongwiththeexpansionofinfrastructure

forhydrogensupply,willrequireannualinvestmentsofCHF200minordertosignificantlyincreasethe

numberofhydrogenfillingstationsacrossthewholecountry.Theseareentirelynewinvestments

thatwillbenecessaryinthe2020sand2030s.Otherinitiativestopromotealternativefreighttransport

systems,suchasrailtraffic,arealreadyrelativelywelladvancedinSwitzerland(suchasthesystemfor

routinggoodsthroughtheNEATtunnel).

AverageannualinvestmentsofCHF1.2bnareneededtosupportclimatetransitioninthe“Energy”

sector.Asmentionedpreviously,Switzerlandisalreadyextremelywellpositionedinrenewablescom-

paredwithothercountries.Evenso,fargreateruseofrenewablesisneededinordertoachieve

netzerocarbonemissionsandthegoalsofthegovernment’sEnergyStrategy2050.Around650 hydro-

electricpowerstations26produceenoughelectricitytomeetasignificantproportionofSwitzerland’s

dailyelectricityneeds,althoughtheyproducemorepowerinsummerthaninwinter(asdosolarplants).

Thiscreatesacertaindependenceonimportedelectricityinthewintermonths.Windpowercanfillthis

gap,asaroundtwothirdsofwindfarms’annualoutputisgeneratedinwinter,hencethewintermonths

arethemostproductive.Althoughtherearemanysuitablelocationsforwindturbinesacrossthe

country,barelyonepercentofSwisselectricitycomesfromwindfarms.Switzerlandlagsbehindtherest

ofEuropeintheareaofwindpower,andfurtherexpansionshouldbeconsidered.27 To push ahead

withthedevelopmentoftheseandotherrenewableswillrequireaverageannualinvestmentsofaround

CHF740m.Improvingtheflexibilityandreliabilityofthenationalgrid,especiallywithregardtonew

connectionsorenergystoragemedia,isanotherimportantleverthatwillcostCHF390mperyear,with

30 percentofthisspentonsubstitution.Bothmeasureswilltakeplacemainlyinthe2020sand2030s.

The Buildings sectorwillneedaninvestmentvolumeofCHF2.1billionoverthenext30years.Thekey

measures to reduce heating and cooling demand in both commercial and residential buildings include

25 Source:FederalStatisticalOffice(FSO)“Goodstransportbyroad”.26 Source:FederalOfficeforEnergy(FOE)“WasserkraftSchweiz:Statistik2018”(Germanonly).27 Source:EnergieSchweiz“WinterstromfürdieSchweiz”(Germanonly).

Swiss Bankers Association · Sustainable finance 23

Measures and investment volumes per sector 2.2

improveddesignofthebuildingshellandreplacingconventionalheatingwithmoreadvancedlow-carbon

technologyandelectrification.Around67percentoftheinvestmentsneededforthesemeasures

wouldinvolvesubstitution.

The Light Road Traffic sectorwillrequireaverageannualinvestmentsofCHF5.7bn,withthelion’sshare

(CHF4.6bn)goingtowardsfundingthefirstprivatepurchaseofe-models.Giventhatthemanufacture

ofdiesel/petrol-fuelledvehiclesisscheduledtoendinthe2030s,itispredictedthataround80 %

ofregisteredprivatevehicleswillbeelectricallypoweredby2050.Inaddition,hardlyanyothercountry

hassuchadenseandwell-developedpublic

transportsystem.Itsshareofthemovementof

peoplebyroadandrailhasrisenfrom17 per-

centin2000to21 percentin201928. Further

expansionthroughadditionalfundingwouldbe

relativelyeasytoachievecomparedwithother

countries.Theshiftinfavouroflocalpublic

transport–especiallythecontinuingexpansionofthenetworkaswellasitselectrification–requires

anaverageofCHF 625 millionperyear.Anotherimportantleverinthe“LightRoadTraffic”sectoris

thegrowingshifttoelectricvehiclesandtheinstallationofthenecessarycharginginfrastructure.The

EUrecommendsatargetofatleastonechargingpointforeverytenelectricvehicles.Switzerland

alreadyhasarelativelydensenetworkofchargingpointstocaterforthe29,000electricvehiclescurrent-

lyregisterednationwide:18ofthebiggestchargingnetworkoperatorsinSwitzerlandalreadyprovide

around 5,000 public charging stations.29IftheelectrificationofSwisspassengertransportcontinues

(estimates30 forecast up to a million purely electric vehicles in 2030 against an overall total of 4.7 m

registered private cars31),however,thereislikelytobeaspikeindemandforpublicchargingstations

(100,000pointsby2030)andprivatechargingstations(1,000,000by2030).Thecorresponding

expansionofthepublicandprivatecharginginfrastructurewillcostaroundCHF440mperyear,with

most of this investment being required during the 2020s.

The “International Air Travel” sector32willneedaverageannualinvestmentsofaroundCHF1.0bnupto

2050forclimatetransition.AsofMay2021,forexample,thefleetofthenationalairlineSwissincluded

92aircraftwithanaverageageof9.9years33. There is still potential for further improvements and

renewals.Inthewakeoftheglobalpandemicandthecollapseindemandforairtravel,withmanyairlines

cuttingbackontheroutestheyserve,Swissalsoplanstoreduceitsfleettoaround85aircraft,with

26 deployedforinternationaland59forEuropeanflights.34Swissownsmostofitsfleet–onlyafew

planesareleased.Commissioningaircraftfittedwithnext-generationpropulsiontechnologieswill

requireadditionalinvestmentsofsomeCHF790mperyearonaverage.However,thereisnosignof

suchinnovativetechnologiesbeingrolled-outintheforeseeablefuture.Thereisstillalongwayto

28 Source:FederalStatisticalOffice(FSO)“Publictransport”.29 Source:TCSMobilitätsberatung“Ladeinfrastruktur:AnzahlLadepunkteinderSchweiz”(Germanonly).30Source:AccordingtoaninterviewinthenewspaperNZZwiththepresidentofImporteursvereinigungAuto-Schweiz.31 Source:FederalStatisticalOffice(FSO)“Vehicles”

https://www.bfs.admin.ch/bfs/en/home/statistics/mobility-transport/transport-infrastructure-vehicles/vehicles.html.32 In2019SwissInternationalAirLinesaccountedfor54.7percentofairtrafficatZurichairport,followedbyEdelweissAirwith

6.6 percent.ThismakesitreasonabletoassumethattheemissionsapportionedtoSwitzerlandfrominternationalairtravelcanbe allocated directly to these airlines.

33Source:Planespotters“SwissFleetDetailsandHistory”.34Source:basedonadiscussionwithanexpertatSwiss.

“Demand for public charging points for electric vehicles will rise to around 100,000 by 2030.”

Swiss Bankers Association · Sustainable finance24

2.2 Measures and investment volumes per sector

gobeforetheaviationindustryisabletodeployelectricorhydrogen-poweredenginesinlargeaircraft

becauseofthelowenergyintensityofbatteriesandthetechnicaldifficultyofstoringlargeamounts

ofhydrogen.Thesetechnologiesareonlyexpectedtobecomeavailablefrom2030onwards,atthe

earliest.Therelevantinvestmentsarethereforelikelytobedeferreduntilthe2030sand2040s.To

providesomeperspective:overthepasttenyears,SwisshasspentCHF8bnmodernisingitsfleet.35

Thefutureinvestmentsrequiredforthemeasuresoutlinedpreviouslywillthereforegomainlytowards

replacements(80percent).Anadditionalmeasureinvolvestheuseofsustainablebiofuels,whichwill

costaroundCHF180mperyearonaverage.LufthansaGroup,theparentcompanyofSwiss,views

sustainableaviationfuel(SAF)suchasbiokeroseneasanimportantleverfortheenergytransformation

oftheaviationindustry.Comparedwithconventionalfossilaviationfuels,SAFreducesCO₂emissions

byupto80percent.Undercurrentsafetyregulations,however,nomorethanhalfofaviationfuelcan

come from alternative sources. The cost of sustainable fuels is currently around 10 times higher than

fossilfuels.Coststhereforeneedtocomedownsignificantly,especiallysinceindustryexpertsestimate

thatfuelcostsmakeuparound30percentofairlines’totaloperatingcosts.Ifahigherproportion

ofbiokeroseneweretobeintroduced,forexample,thebusinesswouldnolongerbeprofitable.Ontop

ofthat,therearesomemeasureswhichdonotentailanyinvestmentcostsbutarestillveryeffective

forachievingnetzero.Themostobviousistochangepeople’sflyinghabits.Anotheristointroduce

measuresthatimprovedepartureproceduresandroutemanagement.Industryexpertsestimatethat

everyEuropeanaircrafttravels250kmfurtherthannecessaryoneachflight,whichmakesoptimised

routeplanningextremelyimportantfortheaviationsector.

Achieving the climate transition in the “Chemicals”sectorwillrequireaverageannualinvestmentsof

CHF290mupto2050.Heretheemphasisisontheuseofalternativelow-emissionfuelsandraw

materials,withannualinvestmentsofCHF160m.Theuseofhydrogeninthechemicalsindustrypromises

enormouspotential.Similartootherindustries,suchas“MetalandSteel”and“Cement”,oneproposed

measureistheprovisionofcarboncaptureutilisation&storage(CCUS)technology.Sofar,however,there

have only been mostly pilot projects and there is the possibility of public opposition to the permanent

storageofCO₂.Inaddition,thereareinsufficientstoragecapabilitiesinSwitzerland,andnotransport

infrastructuretocaterforpotentialexport.Thetechnologyitselfisanimportanttoolforindustrial

sectorstoachievethenetzerotarget.AnnualinvestmentsofCHF115mwouldbeneededinthe“Chemi-

cals”sector.Improvingtheprocessandenergyefficiencyofchemicalproductionrequiresinvestments

ofCHF20mperyear.Onemeasuretoimproveenergyefficiency,forexample,wouldbetomodernise

boilerplants.BASFSchweizAGhasmanagedtodojustthis:withthesupportoftheEnergyAgency

oftheSwissPrivateSector(EnAW)ithascuttheCO₂emissionsfromitsKaistenchemicalsplantby

5,000 tonnes per year.36

35 Source:basedonadiscussionwithanexpertatSwiss.36 Source:EnergyAgencyoftheSwissPrivateSector(EnAW).

Swiss Bankers Association · Sustainable finance 25

Measures and investment volumes per sector 2.2

ReducingtheGHGemissionsofthe“Agriculture”sectorwillrequireaverageannualinvestmentsof

CHF170m.Althoughcuttingthenumberofdomesticcattlewouldhelptoreducenationalemissions,

thiswouldbeoffsetbyacorrespondingriseinimportsifdemandisconstant,effectivelyshiftingemis-

sionsabroad.Amoreefficientmeasurewouldthereforebetochangeourdiettowardsalternative

sources of protein such as plant-based meat substitutes and cultured meat. Around a quarter of the

Swisspopulationisnow“flexitarian”37anddemandisgrowingforplant-basedmeatsubstitutes.Asthe

climatic requirements and labour costs are considerable, a substantial amount of these products have

tobeimportedfromabroad,asfluctuatingyieldsmakesuchcropsariskypropositionforSwissfarmers.

Itisthereforequestionablewhetherplant-basedproteincouldbegrownprofitablyinlargequantities

inSwitzerland:becauseofhigherproductioncosts,locallygrowngreenlentilscostmorethantwiceas

much as rival products from Canada.38 Suitable state incentives therefore need to be created. This

wouldrequireannualinvestmenttothetuneofCHF114mupto2050.Toreducetheemissionscaused

byslurry,theFederalCouncilhasalreadyincorporatedtwonewmeasuresinthe2020Ordinanceon

AirPollutionControl(OAPC):first,slurrystoragefacilitiesmustbepermanentlycoveredtopreventthe

releaseofammoniagas;second,itisnowmandatorytoapplytheslurry–wherethetopographyallows

(i.e.primarilyinflatareas)–withdraghosespreadersratherthanbaffleplates,asbefore.39 The further

improvementofslurrymanagementwillrequireannualinvestmentsintheregionofCHF46m.

Furthermore,theadoptionofregenerativeagriculturalpractices,primarilydirectsowingandamoveto

organicfarming,playsanimportantroleaswell.“No-tillfarming”,ordirectsowing,isarelativelynew

methodinSwitzerlandandverylittlescientificresearchhasbeenconductedintotheseapproaches.

37 Source:Swissveg“SurveyofvegetariansandvegansinSwitzerland”.38Source:SchweizerBauer“Pflanzenburger:SchweizerBauernprofitierennicht”(SwissFarmersMagazine,Germanonly).39 Source:FederalOfficefortheEnvironment“LuftreinhaltunginderLandwirtschaft”(Germanonly).

Swiss Bankers Association · Sustainable finance26

2.2 Measures and investment volumes per sector

Becauseofthespecialistknow-howrequired,thisapproachhasonlybeentakenupbyasmallproportion

ofSwissfarmers:estimatesfordirectsowingarejustunderfivepercentoftheSwitzerland’stotal

arablelandarea(275,439hectares).40Improvementsherewillrequireannualinvestmentsofaround

CHF 10 moverthecomingdecades.Thesubstitutioneffectofboththesemeasuresinagricultureis

onlymodest,ataround10–20percent.

Inaddition,annualinvestmentstotallingCHF 470 marerequiredinthesectors“Domestic Air Travel”,

“Shipping”, “Cement” and “Metal and Steel” forahostofmeasuresneededtoachievethenetzero

target(seeAppendixformoredetails).

40Source:LandwirtschaftlicherInformationsdienst(LID)“DersteinigeWegwegvomPflug”(Germanonly).

GDP(2019)

Gross investments

(2019)

Federal budget (spending2019)

AHV(spending2019)

Increaseinmortgage volumes

(2011–2020p.a.)

Fossil fuels (spending2019)

Climate transition

Defence (spending2019)

Figure 5

Comparison of required climate transition investments

ComparisonofSwiss“netzero”investmentvolumesforclimatetransition

[CHFbnp.a.]

Source: FederalStatisticalOffice,SNB,FederalFinanceAdministration,FederalSocialInsuranceOffice

726.9

178.3

71.4

45.3

30.1

17.612.9

4.9

Swiss Bankers Association · Sustainable finance 27

Measures and investment volumes per sector 2.2

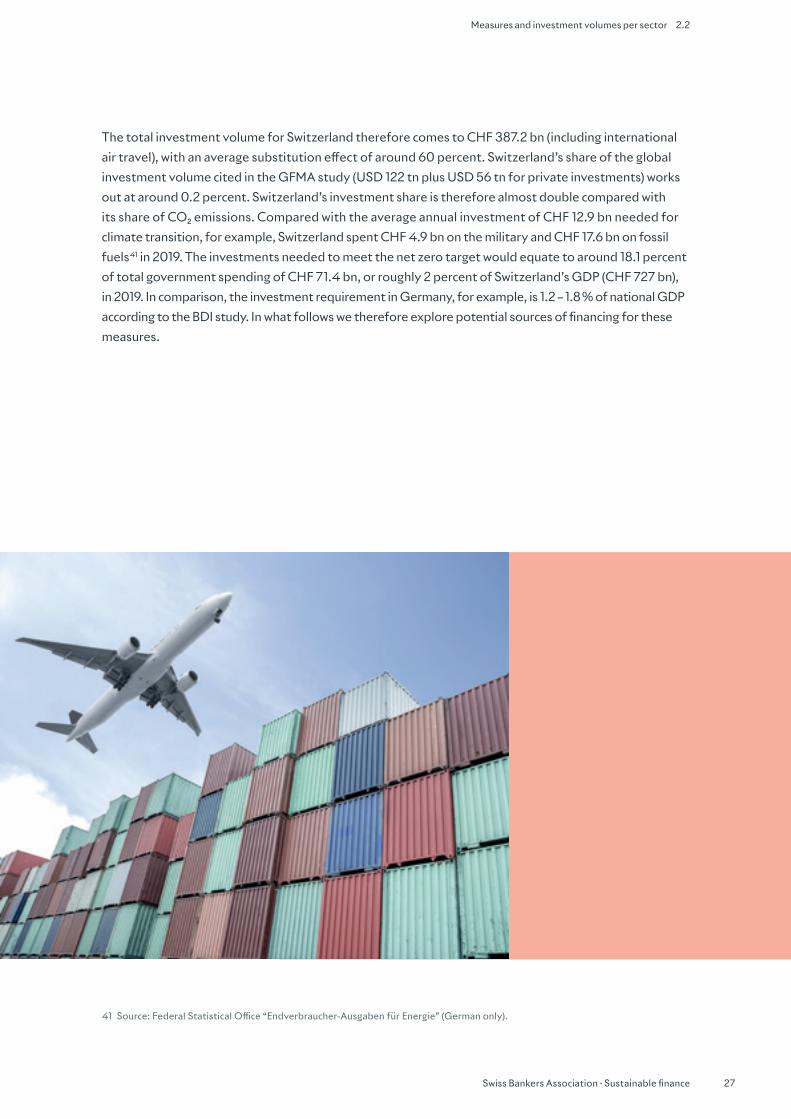

ThetotalinvestmentvolumeforSwitzerlandthereforecomestoCHF387.2bn(includinginternational

airtravel),withanaveragesubstitutioneffectofaround60percent.Switzerland’sshareoftheglobal

investmentvolumecitedintheGFMAstudy(USD122tnplusUSD56tnforprivateinvestments)works

outataround0.2percent.Switzerland’sinvestmentshareisthereforealmostdoublecomparedwith

itsshareofCO₂emissions.ComparedwiththeaverageannualinvestmentofCHF12.9bnneededfor

climatetransition,forexample,SwitzerlandspentCHF4.9bnonthemilitaryandCHF17.6bnonfossil

fuels41in2019.Theinvestmentsneededtomeetthenetzerotargetwouldequatetoaround18.1percent

oftotalgovernmentspendingofCHF71.4bn,orroughly2percentofSwitzerland’sGDP(CHF727bn),

in2019.Incomparison,theinvestmentrequirementinGermany,forexample,is1.2 – 1.8 %ofnationalGDP

accordingtotheBDIstudy.Inwhatfollowswethereforeexplorepotentialsourcesoffinancingforthese

measures.

41 Source:FederalStatisticalOffice“Endverbraucher-AusgabenfürEnergie”(Germanonly).

Swiss Bankers Association · Sustainable finance28

3.1 Presentation of basic decision logic and categorisation

3 Assessment of potential financing sources

Cooperation between the Swiss financial centre, the private sector as a whole and the public sector is key to ensuring that the measures presented previously at sector level can be financed. The private sector applies different criteria to its financing decisions compared to state institutions. This raises questions as to which source of financing appears suitable for the measure concerned, and the best way to structure the interaction between the financial centre, the private sector and the public sector.

3.1 Presentation of basic decision logic and categorisation

Inthecontextofthisstudy,possiblesourcesofexternalfinancing(financingofthenecessaryinvestments

fromownresourceswasnotexplicitlytakenintoaccount)basedonthecategoriesof“Banks”(mainly

financingthroughclassicbankingproductssuchasloans),“Capitalmarkets”(financingthroughthecapital

market,e.g.bondissues),“Publicsector”(measuresfinancedviathepublicsector–theunderlyingcapital

raisingcantakeplacethroughclassicbankloans,appropriatebondsorthestatetreasury)and“Others”

(thisincludesfinancingforwhichnoclearlydefinableformoffinancingiscurrentlyapparent).There-

spectivemeasureswereallocatedtothedifferentcategoriesbyselectingcriteriathatmakefinancing

withinthecategoryconcernedappearlikely.

Whenassessingbankeligibility,thecriteriaofcreditworthiness,potentialcollateral,technologicalmaturity

anddurationwereconsideredindetail.Creditworthinessreferstotheborrower’sabilitytorepaythe

loan,whichdepends,amongotherthings,onthesizeandprofitabilityoftheenterprise.Theavailability

ofloancollateralintheformoftangibleand,whereapplicable,intangibleassetstosecureloanscan

improveabelow-averagecreditrating.Furthermore,project-relatedfactorssuchasthematurityofthe

underlyingtechnologyandtheexpectedpaybackperiodoftheinvestmentalsoplayarole.

Toassesscapitalmarketeligibility,theborrower’saccesstothecapitalmarketwasevaluatedbasedon

thesizeofitsbusinessandthevolumeoffinancelookedfor.Onthewhole,financingvolumesintheform

ofbondissuesfromprivateissuersofatleastCHF20marerequired42.Government-backedcapital

marketfinancingisanotherpossibility.

42AccordingtotheSIXSwissExchange’sBondListingGuide,thenominalamountofabondissuemustbeatleastCHF20m,withatleastCHF100mbeingrequiredforinclusionintheSwissBondIndex(SBI).

Swiss Bankers Association · Sustainable finance 29

Suitability of possible funding sources for necessary measures 3.2

Publicmandates,inthesenseofthegeneralpublic,arecharacterisedinthatthefinancingofthemeasure

isguaranteedbygovernmentfundsandfinancingfromtheprivatesectorislikelytobeunprofitable.

Apublicgoodcanalsobefinancedbythestateorcantonitselfwiththehelpofthecapitalmarket.Hence,

thefinancialcentremayplayasupportingroleinthefinancingofapublicmandate.Therearealsomixed

formsoffinancingsuchaspublic-privatepartnershipsorblendedfinance(seeChapter4).

Afinancinggapexistsiffinancingisneitherbankeligiblenorcapitalmarketeligibleandtheprojectisnot

a public mandate in the form of a public good. Further incentive structures are therefore needed to ensure

asuitableallocationtooneoftheothercategories(forexamplethroughtheguaranteeofgovernment

securities).

Whenassessingthemeasurespresentedaboveatsectorlevelwithregardtofulfilmentofthecriteria,

thesectorsandtheirspecificfeatureswereconsideredindividually.Whenassessingborrowers,the

nationalkeyplayersofthesectorconcernedandthemarketconcentrationweretakenintoconsideration,

inordertoobtainaratingfortheaverageborrowerinthesector.Itwasexpresslydecidedtoassessonly

the measures for the top ten sectors.

3.2 Suitability of possible funding sources for necessary measures

Basedontheunderlyingmeasures,itisexpectedthatannualinvestmentsofCHF10.7bncanbefinanced

throughclassicbankloans.Anexampleinthecommercialbuildingsectorwouldbethereductionofheat-

ing/coolingdemandwithadvancedbuildingenvelopedesign,whereannualinvestmentstotallingaround

CHF 680 mcouldbefinancedbybanks.Anotherexampleistheimprovementofgridflexibilityand

reliability(newconnections,energystorage)intheenergysector.Ontheonehand,theelectricityproduc-

ersandgridoperatorsareestablishedenergycompanieswithadequatecollateraland,ontheother

hand,thisisameasurewithaveryhighdegreeoftechnologicalmaturity.Here,annualinvestmentsof

CHF393mcouldbefinancedthroughtraditionalbankloans.Inthecaseofplantupgradeswithhigh-

er-quality,moreenergy-efficientequipmentinthecementsector,forexample,loansareequallybank-

eligibleinviewoftheexistingindustrialstructureinvolvingwell-establishedinternationalgroups.Here,

annualinvestmentsofCHF22mcouldbefinancedbybanks.Aspecificexampleinthe“MetalandSteel”

sectoristhemodernisationofexistingelectricarcfurnacesinSwisssteelworks.Switzerlandhastwo

steelworks(StahlGerlafingenandSwissSteelEmmenbrücke)withelectricarcfurnaces.Thetwoplants,

builtin1996and1999,werelastmodernisedin2007and2013respectively.Overthenext30years,

renovationworkislikelytobecarriedoutatbothsiteswithatotalinvestmentvolumeof0.4bn.43 These

companiesarewellestablishedinthemarketandentirelybank-eligiblegiventheirgoodcreditrating.

43Source:Accordingtoexpertdiscussions.

Swiss Bankers Association · Sustainable finance30

3.2 Suitability of possible funding sources for necessary measures

AroundCHF1.0bncouldbefinancedthroughthecapitalmarketintheformofbondsorcapitalincreases.

Themeasureshereprimarilyconcernairtravel–Swiss,forexample,isanestablishedcompanywith

accesstothecapitalmarket.Improvingthefleetefficiencyofaircraftandusingplaneswithnext-generation

propulsiontechnologiescanthusbefinancedthroughthecapitalmarketinthelongterm.Thiswould

meanthataround91percentofthetotalinvestmentneededwouldbeprivatelyfinanced(bankeligible

orcapitalmarketeligible).

Themeasuresdescribedas“publicgoods”wouldbefinancedmainlybythestateatanannualcostof

CHF0.9bn.Oneexamplewouldbethefurtherexpansionoflocalpublictransportatanannualinvestment

costofCHF624m.Investmentsinpublictransportaregenerallythedirectorindirectresponsibilityof

thestateandcanpotentiallyalsobefinanceddirectlyviathecapitalmarketthroughgovernmentbonds.

Total Banks Capitalmarket Public goods Others

Figure 6

Overview of financing sources

Financingsourcesfornetzeroinvestments,2020–2050

[CHFbnp.a.]

Source: ownestimate

12.9 10.7

83 %

100 %

8 %

7 %

1.0

0.90.32 %

Swiss Bankers Association · Sustainable finance 31

Suitability of possible funding sources for necessary measures 3.2

Fortheremainingmeasures,wecurrentlyanticipatecertainchallengeswhenusingthefundingsources

outlined above. This is due in particular to the amount of investment required, but also the level of

technologicalmaturity.ThedevelopmentofCCUStechnologiesandtheconstructionofassociated

infrastructuressuchaspipelinesystemsareparticularlyworthmentioninginthisrespect.Atotalof

twopercentoftheannualinvestmentvolume(correspondingtoanannualamountofCHF0.3bn)canbe

allocatedtothiscategory.Toensureappropriatefinancing,certaingovernmentsupportservicesare

needed(seerelevantexplanationsinChapter4).

Toputthesefinancingsumsintoperspective,itisworthcomparingthemwiththeannualvolumesof

investmentandfinancinginSwitzerland.AnnualgrossinvestmentsoftheSwisseconomyamountedto

aroundCHF178bnin2019.44Theannualdomesticnewlendingbusiness45ofallSwissbanksfor2019

wasestimatedatCHF99bn.AccordingtoSNBfigures,mortgagefinancingaccountedforalargeshareof

this,ataroundCHF75bn.Asfortheremainingloans,annualnewbusinessisintheregionofCHF24bn.In

ordertoreduceemissions,thisstudy–aspreviouslyexplained–estimatedanannualinvestmentvolume

forSwitzerlandofCHF12.9bn,ofwhichCHF10.7bncaninprinciplebefinancedbytraditionalbank

loans.Consequently,thiswouldaccountforaround10.8percent(calculation:CHF10.7bn/CHF99bn)of

totalcurrentannualSwissnewlendingbusiness.

44Source:FederalStatisticalOffice(FSO)“Nationalaccounts:grossdomesticproduct”.45ToestimatetheannualnewdomesticloansbusinessofallSwissbanks,acomparisonwasmadeofthedomesticcreditvolumeof

Swissbanks,includingtermstomaturity(source:SNB)overa5-yearhorizonbetween2014and2019.

Figure 7

Overview of financing sources – comparison

Switzerland–AnnualinvestmentandfinancingvolumeinCHFbn,comparativevolumes:

Note: InvestmentscorrespondtothefigureforgrossdomesticcapitalinvestmentreportedintheNationalAccounts.Theseare financedfromvarioussources,suchasequitycapital,externalcapitalandothers.Theamountofdomesticfinancingstudiedhereincludesbankloans,bondsandexchange-listedequitycapitalthatcanbedeployedinSwitzerlandorabroad,andinfutureyears. Thevaluesoftheinvestmentsandfinancingcannotthereforebedirectlycompared. Source: SNB,SIX,FSO

Investments Financing Loans Bonds Equity capital (IPO,capitalincrease,

etc.)

178 170,1

24,1

75,0

9,0

62,0

General

Mortgages

Otherloans(SMEsetc.)

Swiss Bankers Association · Sustainable finance32

3.2 Suitability of possible funding sources for necessary measures

Whenitcomestofinancingthroughthecapitalmarket,ontheotherhand,thesituationlooksverydiffer-

ent.SwissfrancdenominatedbondstothevalueofCHF62bnwereissuedin2019(excludingfederal

governmentandcantons).Ofthese,domesticissuersaccountedforCHF42.6bn.46Inaddition,theSwiss

stockexchangerecordedcapitalincreasesofCHF6bn(2020)47andanIPOvolumeofCHF3bn(2019)48.

Here,theCHF1.0bnneededannuallyforcapitalmarketeligiblemeasureswouldbelesssignificant.

46Source:SwissInfrastructureandExchange(SIX)“PrimaryDebtCapitalMarketInformationQ42020–Report”.47Source:SwissInfrastructureandExchange(SIX)“AnnualReport2020”.48Source:SwissInfrastructureandExchange(SIX)“TradingKeyFigures:2019”.

“It is expected that annual investments of CHF 10.7 bn can be financed through classic bank loans.”

Swiss Bankers Association · Sustainable finance 33

4 Framework conditions for the Swiss financial centre

Financing the Sustainable Development Goals and meeting the Paris climate targets cannot be secured with public funds alone: the mobilisation of private funds is imperative. It is therefore becoming increasingly important to align the financial system with these goals – something which is also recognised as a critical factor by international financial bodies. For Switzerland to become an international hub for sustainable finance and thus contribute to the financing of sustainability, proper attention must be devoted to the framework conditions for mobilising private funds.

Accordingtothesubsidiarityprinciple,governmentunitsshouldonlyassumethosetasksthatprivate

actors(especiallythefinancialcentre)arenotcapableofperforming.Thisresultsinthefollowingfunding

hierarchy:

1. Around91percentof‘netzero’investmentscanbecoveredwithaccompanyingmeasuresviaexisting

financialcentrestructures,withfurtheroptimisationoftheframeworkconditions.

2.Forthefinancingofpublicgoods(around7 percentofthetotalvolume),furtherprivatefundscanbe

mobilisedwiththeinvolvementofpublicfundsandpublic-privatepartnerships.Thefocushereison

conceptssuchasmicrofinanceenhancement(seep.41)andblendedfinance(seep.45).

3.Accordingtoourestimate,thisleavesaround2percentoffinancingthatcanhardlybecoveredwiththe

above-mentionedapproaches.Tothisend,wehaveexaminedthemethodpractisedelsewhereof

usingastateinvestmentbank.GiventhecomparativelylowvolumeofaroundCHF300mperannum,

suchaplanisunnecessaryinSwitzerlandandwouldriskcreatingmarketdistortions.

Existing forms of financing and approaches for closing remaining gaps

Inthefirsttwochapters,weshowedthevolumeoffinancinglikelytobeneededtomitigateclimate

changeintheSwisseconomy,particularlytheemissions-intensivesectors.Inordertoactuallyachieve

the climate targets, the necessary funding must therefore be available for this. A goal-oriented policy

requirespatient,long-term,focusedfinancing.

Swiss Bankers Association · Sustainable finance34

4 FrameworkconditionsfortheSwissfinancialcentre

TheSwissfinancialcentrehasawiderangeoffinancingmethodsatitsdisposal.Aswellasmortgagesand

SMEloans,theyalsoincludeotherofferingssuchasleasing,factoringandthecapitalmarket,plusinvest-

mentsfinancedbythepublicsector.Theseprivate-sectorprovidersarecalledupontomaketheneces-

saryvolumesavailable,whichwillbepossiblesincetheyremaincapableofaction.Atthesametime,they

needidealframeworkconditionsandcanalsobeincentivisedtofinanceinvestmentsforclimatechange

mitigation.

Throughappropriateframeworkconditions,theremaininginvestmentprojectscanbemadeeligiblefor

investmentviathefinancialmarketsorfinancedbythestate.Anotherpossibilityistocreatenewforms

offinancingthatarespecificallygearedtowardstheseinvestments.Thefollowingchartisintendedtoshow

whichapproaches(frameworkconditionsandmeasures)couldbeusedtoclosethesefinancinggaps.

Financing the transition – schematic overview

1. General location factors: Sustainablefinanceasalocationadvantage Education and access to talent Legalcertaintyandreliability

Marketaccess Attractiveinvestmentenvironment

2. Already funded via the financial centre

3. Currently underfunded via the financial centre 4. Large-scale financing and overarching aspects

Goal: continue to expand current offering

Raiseawarenessoftheroleoffinancialflowsinthetransition

Expandthefundamentals; disclosure(NFRD,TCFD,etc.) andtaxonomy

Measuresincombinationwithpublic-private partnerships and microfinanceapproaches

Jointinitiativeswiththepublicsector, industry associations and localfinancialserviceproviders

Goal: use targeted measures to make financing possible

Creditworthinessthroughadjustedevaluationmodels(e.g.SMErating)

Establishrelationshipwiththefinancialcentrefortraditionallyself-financedsectors

Formulateaninvestor-appropriateriskprofile Removeobstaclestoinvestment Helpthemarketachievecriticalmass

Goal: encourage and provide solutions for extended financing needs

Improvecapitalmarketappeal (e.g.forgreenbonds,infrastructurefunds,etc.)

Mobilise private investments throughde-riskingandleveragingpublic-sector investments

Createfinancialincentivestofosterinnovation(bothfornewtechnolo-gies,achievingmarketmaturityandalsobroaderscalingeffect)

Support via public-private partnership solutions

Create sustainable perspectives Support via public-private partnership solutions

5. General approaches and support measures:

Integrateintointernationalinitiatives Public/privatesectorcollaboration Consistentdisclosureofclimaterisks Sharing best practice

Promotesignallingeffect Integrateclimatefactorsinengagementandstewardship

Source: SwissBanking

Swiss Bankers Association · Sustainable finance 35

General location factors 4.1

4.1 General location factors

Switzerlandisanattractivelocationforfinancialserviceproviders.However,thisisnotbetakenfor

grantedandmustalsobeensuredinthefuture.Furthermore,theframeworkconditionsmustbesuch

thatthefinancialcentreremainsinnovative,capableofchangeandfullyabletofulfilitsimportant

economicrole.ThisisespeciallytrueinlightoftheupcomingtransitionoftheSwisseconomyandthe

climate targets.

Forthefinancialservicesindustrytoremainattractiveforinvestors,customersandtalents,Switzerland

mustmaintainbusiness-friendlyframeworkconditionsinareassuchastaxlaw,regulation,employment

lawandimmigration.

Thefollowinginitiativeswouldeithersupporttheexistingbusiness-friendlyconditionsordrivechange

toimprovethecompetitivenessoftheSwissfinancialindustryanddomesticserviceprovidersinparticular:

· On24June2020,theFederalCounciladoptedareportandguidelinesonsustainabilityinthefinancial

sector.TheSwissfinancialcentreshouldfurtherstrengthenitspositionasaleadinglocationforsus-

tainablefinancialservices.Theframeworkconditionsmustbedesignedinsuchawaythatthecompeti-

tivenessoftheSwissfinancialcentreiscontinuouslyimprovedandthefinancialsectorcanmakean

effective contribution to sustainability.

· Itisimportanttoensureaccesstoskilledworkersthroughfurtherdevelopmentoftrainingopportu-

nitiesandthemaintenanceofliberalimmigrationlaws.

· Incentivesforinnovationmustbecreatedbydefiningaregulatoryframeworkgearedtothesegoals.

· StampdutyshouldbeabolishedandwithholdingtaxinSwitzerlandreformedtomakethecapital

marketmoreattractiveasafinancingoptionforclimate-orientedinvestments.

· Competitivenessmustbeincreasedandtheexportoffinancialservicesmustbepromotedbyensuring

thatSwissfinancialserviceprovidershaveunrestrictedaccesstointernationalcustomers.

Swiss Bankers Association · Sustainable finance36

4.2 Financingneedsthatthefinancialcentreisalreadyabletomeet

4.2 Financing needs that the financial centre is already able to meet

Theinclusionofenvironmental,socialandgovernance(ESG)criteriainlendingisalreadyafactoflifeata

growingnumberofbanks.Atthesametime,numerousbankshaveannouncedstrategiesonhowtodeal

withexistingfinancingwithharmfulclimateimpacts.Inthisway,banks’loanbooksarebecomingmore

sustainableandclimate-friendly.Severalinternationalinitiativeshaveemergedforthispurpose,which

wewilldiscusslateron.Thereisalsoagreaterfocusonidentifyinganddisclosingtheclimateimpactof

bankingactivities.ThemajorityoftheindustryhasparticipatedintheFederalOfficeoftheEnviron-

ment’s(FOEN)climategoalalignmenttests,andagrowingnumberofbanksarecommittedtotherecom-

mendationsoftheTaskForceonClimate-relatedFinancialDisclosures(TCFD).

InordertosupportthetransitionoftheSwisseconomywithregardtoclimatetargetsandbeableto

meettherelevantfinancingneeds,bankscanpursueadditionalapproachesthataretailoredtothe

respectivefinancialinstrumentsandproductgroups.Inthefollowing,weconsiderwhichapproachescan

helpfinancethetransitioninthedifferentproductcategories.

Mortgage financing

ThereisadirectlinkbetweenCO₂emissionsandthefinancingofbuildings.AccordingtotheFederal

OfficeoftheEnvironment,buildingsmakeasignificantcontributiontoCO₂emissionsinSwitzerland,

accountingforaround24percent.Onlytransporthasanevenlargershare,at32 percent.Itistherefore

obviousinpolicytermstolookforsolutionsviamortgagesorcorporateloans.Thefocushereisonthe

buildingstockandthusthemortgageportfolio.

Thefollowingfourapproachestomortgagelendingaretraditionallyavailableandalreadyusedbyvarious

bankstoday:

· Takingenvironmentalcriteriaintoconsiderationwhensettinginterestrates

· Includingsustainabilitywhenconsideringaffordabilityandotherfinancingcriteria

· Makingthemortgagetermandrepaymentdependentonenvironmentalcriteria

· Promotingawarenessofenvironmentalcriteriaamongbanksandcustomers

Furthermore,bankshaveanimportantroletoplayinhome-owners’financialplanning.Forexample,they

canprovideinformationonthefullcostsofabuilding(maintenance,energycosts,CO₂levies,etc.)as

wellasapplicablelocalclimate-relatedrules(e.g.cantonalbanonoilheating,taxeffectsofrenovations).

Thefinancialadvantagesofclimate-efficientconstructionmethodsorrenovationscanbeimpressed

uponcustomersinthisway.

Bankscanalsodefinestandardsthattheenergyconsumptionofbuildingsmustmeetinorderforthe

mortgagetobeconsideredenergy-efficient.Acorrespondingapproachisbeingpursuedbyaconsortium

ofEuropeanbanksundertheEnergy-efficientMortgagesActionPlan(EeMAP)initiative.49

49https://eemap.energyefficientmortgages.eu/.

Swiss Bankers Association · Sustainable finance 37

Financingneedsthatthefinancialcentreisalreadyabletomeet 4.2

Approachessuchasthese,whichtakesustainabilitycriteriaintoaccountwhengrantingloans,arepursued

voluntarilybybanksandcanaffectthemarginsachievedonthebusinessinquestion.Itmaybepossible

forlegislatorsandregulatorstocontributedirectlytoSwitzerland’sclimategoalsbyaccordingspecial

treatmenttothefinancingofenergy-andclimate-efficientbuildingsintheirregulatoryframeworks.

Thebenefitsandpotentialrisksofa“green-supporting”approachcouldbeexaminedforsuchmortgages.

Forexample:lessstringentequityrequirements,riskweightings,capitalbuffers,valuationandloan-to-

valuecriteria,etc.However,itisstillimportanttoensurethatthecapitalrequirementsareformulatedin

arisk-basedmanner.

Thetransitionofthebuildingsectortowardsimprovedclimateandenergyefficiencyalsofacessocio-

political,fiscalandstructuralobstaclesthatcanbeaddressedbypolicy.Beforeconsideringthequestion

offinancing,itisoftennecessarytolookatotherframeworkconditionswhicharefrequentlycriticalin

termsofthedecisiontorenovate.Theseinclude,forexample,thetaxframework(deductibilityofvalue-

preservingversusvalue-enhancinginvestments),buildingregulationsandstructuralhurdles(site

redevelopment,condominiumownership,dealingwithexistingtenanciesduringrefurbishment,etc.).

Climate-relevantfinancingisanimportantaspect,especiallyfortherenovationofbuildingenvelopes

(butalsophotovoltaics,heatpumps,etc.).Thefocusshouldnotonlybeontherenovationbudgetorthe

increaseinthemortgage,butalsoonmaintainingthevalueofthepropertyasawhole.Theguiding

principleshouldbetolookforthebetterrisk.Arenovatedpropertyislessofariskandshouldtherefore

beconsideredasawhole.Thisapproachcreatesagreaterincentiveforownerswhoarewillingtoreno-

vateandismoreconsistentwiththeassessmentfactorsinmortgagelending.

Loan financing for SMEs

Smallandmedium-sizedenterprises(SMEs)areaveryimportantpartoftheSwisseconomy.Atthesame

time,SMEsarealsoveryheterogeneousandhavestronglocalroots,whichalsoaffectstheirbanking

relationships.Theircreditneedsandthebank’sassessmentofthecreditriskdependontheactivity,size,

profitabilityandothercriteriaoftheindividualenterprise.Securedloans,wherecollateralmaybepledged,

andleasesforvehiclesandequipmentarecommoninSwitzerland.Traditionally,however,financingoutof

thecompany’sownresourcesalsoplaysamajorrole.

Ontheotherhand,particularlyinthecaseofrelativelylargeinvestmentsinconnectionwithclimate

mitigation,financingoutofthecompany’sownresourcesisdifficult,astheseareone-off,largesumsfor

investmentsoverthelongerterm.Fromamacroeconomicperspective,however,suchinvestmentsare

not only desirable but necessary. Failure to invest leads not only to an increasingly poor environmental

performance over time, but also to a loss of competitiveness.

Itisinthebanks’interesttosupportthesecompaniesinthetransitionandtopromotethetransformation

throughincentives.Especiallyinthecaseofthecantonalbanks,thisisoftendoneincompliancewiththeir

mandate.

Swiss Bankers Association · Sustainable finance38

4.2 Financingneedsthatthefinancialcentreisalreadyabletomeet

Morespecifically,theregulatorcancreateincentivesinthiswayor,forexample,helptoclosefinancing

gapswithconditionalguarantees.However,thisisnaturallyveryactivity-specific(e.g.garagebusinesses

andconversiontoelectricmobility).

Thistopicalsohasinternationalrelevance.ThiswasthereasonforcreatingthePrinciplesforResponsible

Banking50.Swissbankswereactivelyinvolvedindefiningtheseprinciplesandhavecommittedthemselves

to observing them51.

Swiss members of the Principles for Responsible Banking, as of May 2021

Bank Date of signing

BankJuliusBär&Co.AG September 2019

Credit Suisse September 2019

GlobalanceBankAG September 2019

J.SafraSarasin September 2019

LombardOdier November2020

RaiffeisenSwitzerland December 2020

Pictet-Gruppe October2019

UBSAG September 2019

Source: UNEPFI

ThesixprinciplesofthePRBweredevelopedbytheUnitedNationsEnvironmentProgrammeFinance

Initiative(UNEPFI)incooperationwith30banksandareintendedtoserveasaframeworktoachievethe

UNSustainableDevelopmentGoalsandtheobjectivesoftheParisClimateAgreement.Underthe

PrinciplesforResponsibleBanking,participatingbanksacknowledgetheirresponsibilitytosupport

companiesintheirtransformationtowardsmoresustainablebusinesspractices.

ThesignatoriesofthePrinciplesforResponsibleBankingundertaketoformulateandpublishtargets

for all major business areas. The principles cover both the strategic and the operational level. The partici-

patingbanksstrivetogiveequalconsiderationtotheinterestsofcustomers,employees,legislators

and investors.

50https://www.unepfi.org/banking/bankingprinciples/.51 https://www.unepfi.org/banking/bankingprinciples/sigs/.

Swiss Bankers Association · Sustainable finance 39

Financingneedsthatthefinancialcentreisalreadyabletomeet 4.2

TheUNEPFI’sNet-ZeroBankingAlliance52 goes one step further. Participating institutions commit to

reducingtheirCO₂emissionsasmuchaspossible.Thegoalistoreducethecarbonfootprintofthe

bank’sentireloanandinvestmentportfoliotonetzeroby2050atthelatest.Thevoluntarynetzero

commitment emphasises the determination to actively shape the sustainable transformation of the

economyandsociety.Thenetzerocommitmentrequiresspecificmeasureswherebythebanksdemon-

strablysupporttheircustomersinreducinggreenhousegasemissions.Initiallythefocusisoncarbon-

intensivesectors.ProgressmustbereportedregularlyaccordingtoUNEPFIguidelines.Portfoliosareto

bemanagedbasedontheapproachdefinedbythe“Science-basedTargets”initiative.ThemajorSwiss

banksaremembersoftheNet-ZeroBankingAlliance.

52 https://www.unepfi.org/net-zero-banking/.

“Financing the Sustainable Development Goals and meeting the Paris climate targets is only possible with the mobilisation of private funds.”

Swiss Bankers Association · Sustainable finance40

4.3 Financingneedsnotadequatelymetbythefinancialcentretoday

4.3 Financing needs not adequately met by the financial centre today

Notallinvestmentscanbefinancedbythefinancialcentre.Thisisthecase,forexample,whenitcomes

toparticularlylong-termorhigh-riskprojects.Inthecaseofunsecuredloans,thecreditworthinessof

theborrowerisalsoveryimportantforthecreditor’sdecision–i.e.theborrower’sabilitytosettleout-

standingaccountsandotherpaymentobligationsreliablyandinaccordancewiththecontract.Banks,

forexample,needtoexerciserestraintandforesightwhenlendingtosmall,youngcompanieswith

unclearprofitability,otherwisetheyincreasetherisksfortheirowncommitments.

Creditworthinessorcreditratingisdeterminedonthebasisofvariousfinancialmarkersbycreditagencies,

ratingagenciesorthebankitself.Themainapproachestoenablingclimate-orientedinvestmentsby

non-creditworthycompaniesareasfollows.

SME sustainability ratings

AchievingthetransitionoftheentireSwisseconomyrequiresnotonlylargecorporationsbutalsosmall

andmedium-sizedenterprises(SMEs)tomakeclimate-orientedinvestments.Currently,around80 per-

centofallbankloansaregrantedtoSMEs.However,basedonourestimatesofmitigationfinancing

needs,thedemandislikelytoincrease.Atthemoment,sustainabilitycriteria,i.e.thenon-financialper-

formanceofSMEs,playhardlyanyroleinthelendingprocess.Onereasonforthisisthelackofsustaina-

bility-oriented assessment tools that are mean-

ingful, suitable and practicable for SMEs. Fur-

thermore, there are currently limited incentives

forSMEstohavetheiractivitiescertifiedwith

regard to sustainability.

InthecontextofSwitzerlandandtheSMElandscape,itisimportanttoconsiderhowtheneedsofthe

financialsectorandtherealeconomycanbesuitablyreconciledwithoneanothersoastoachieveclimate

andsustainabilitygoalstogether,inawaythatbenefitsbothsidesanddoesnotcreateadditional

bureaucracy.

Intheinternationalcontext,variousstandardisationeffortsareunderwayforESGratings/criteria(ISO,

WEF,ValueBalancingAlliance,etc.).However,concreteresultsforstandardisedESGfactorsorstandard-

isedESGratingsforSMEsaretakingtimetomaterialise.StakeholdersinSwitzerland’srealeconomyand

financialsectorthereforehaveitintheirpowertosettheirownstandardforSMEs,withasignallingeffect

beyondthecountry’sborders.

“ESG criteria could soon play a major role in lending practices.”

Swiss Bankers Association · Sustainable finance 41

Financingneedsnotadequatelymetbythefinancialcentretoday 4.3

Financing of micro-enterprises

Bankandcapitalmarketfinancingarecommonfinancingmethodsforlargercompanies.Theyarenotwell

establishedamongsmallerbusinesses,butheretoothereisaneedtoexpandtherangeoffinancingfor

climate-orientedinvestments.Ininternationalparlance,theterm‘microfinanceenhancement’isused.The

aimistosupportenterprisedevelopmentandprosperitybyprovidingshort-andmedium-termfinanc-

ingthroughfinancialinstitutions.Microfinanceandmicro-enterprisesaresupportedthroughadedicated

fund.

The aim of such a fund is to support enterprise development and prosperity by providing short- and

medium-termfinancingthroughfinancialinstitutions.Thefinancialinstitutionssupportsmallandmicro

enterprisesthathavedifficultysecuringfinancing.Inpursuingthisdevelopmentgoal,thefundshould

observetheprinciplesofsustainabilityandcombineadevelopment-orientedwithamarket-oriented

approach.

Theaimofsuchafundistoensurethatmicrofinancestimulatesgrowth,createsjobsand,inparticular,

contributestothetransitioninthismarketsegment.

Bypositioningitselfasanefficientmicrofinancecreditfund,suchfinancinghasanimportantsignaleffect

inthemarketandhelpstostabiliseandstrengthentheprovisionofresponsiblefinancialservices.Alink

withafundfedfromothersourcesiscertainlyanattractivepossibility.

“State support is essential for long-term and high-risk projects.”

Swiss Bankers Association · Sustainable finance42

4.3 Financingneedsnotadequatelymetbythefinancialcentretoday

Role of the capital market in medium-sized companies