Embed Size (px)

Citation preview

Investing and Money Management Basics

Ways to make money work for you

We all have things we’d like to accomplish during our lifetime, and many of them cost money. But

the truth is, unless we learn how to manage money and make it work for us, it will be hard to accomplish all the

things we’d like. Although it may seem like it sometimes, managing money is not a mystery—but it does involve

some time and effort. Learn the basics of budgeting, saving and investing, and you’ll be on your way to realizing

your goals and, perhaps, your dreams.

Table of Contents

Start With a Budget . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Look With a Critical Eye . . . . . . . . . . . . . . . . . . . . . . . 4

Establish Savings Goals . . . . . . . . . . . . . . . . . . . . . . . 4

Matching Budget With Savings Needs . . . . . . . . . . . 5

Putting Your Savings to Work . . . . . . . . . . . . . . . . . . 5

Types of Savings Vehicles . . . . . . . . . . . . . . . . . . . . . 6

How Much Risk Is Too Much? . . . . . . . . . . . . . . . . . . 6

Assessing Your Risk Tolerance . . . . . . . . . . . . . . . . . . 6

Types of Investments . . . . . . . . . . . . . . . . . . . . . . . . . 7

Retirement Investment Plans and Arrangements . . . 10

For More Information . . . . . . . . . . . . . . . . . . . . . . . . 12

Compliments of:

Life Advice

Ezra LittonFinancial Services RepresentativeFinancial Advisor5400 Lyndon B Johnson Frwy S1100Dallas, TX 75240(972) [email protected]

2

Start With a BudgetWhat’s a budget? A budget is an itemized listing of money that will come in (e.g., paycheck) and money that will be paid out (e.g., bills), over a specified period of time—usually monthly. In a personal or family budget, all sources of income are identified and expenses are planned with the intent of matching expenses to income. By creating and following a budget, you can have the money for the things you want.

Many people don’t know where their money goes; all they know is it’s gone too soon. Understanding where your money goes each month will help you develop a workable budget—the first step to financial security. If you’re like most people, incoming funds are fairly predictable and easily documented—your paycheck and earnings on savings and investments. Money going out, however, is often harder to keep track of.

Start by making a list of all the items you spend money on each month: rent or mortgage payment, utilities, transportation and so on. Keep a daily record of all expenses. Document every purchase by getting a receipt for everything you buy, from the cup of coffee at the drive-up window on Monday morning to the movie tickets on Saturday night. You might want to keep a pocket notepad handy to record items. Note everything, including how you pay for things: cash, credit card or check.

At the end of the month, make an expense record. First, list all of your expenses for the month, then think about items you pay less often (e.g., semi-annual car insurance payments). For items you pay just once or twice a year, divide the payment by the number of months it covers and write that amount on the monthly record.

The Monthly Expense Record example that follows is a starting point. Some items on the list may not apply to you, and you may need to add others.

This Life Advice booklet, Investing and Money Management Basics, was produced by the MetLife Consumer Education Center and reviewed by the Financial Planning Association.

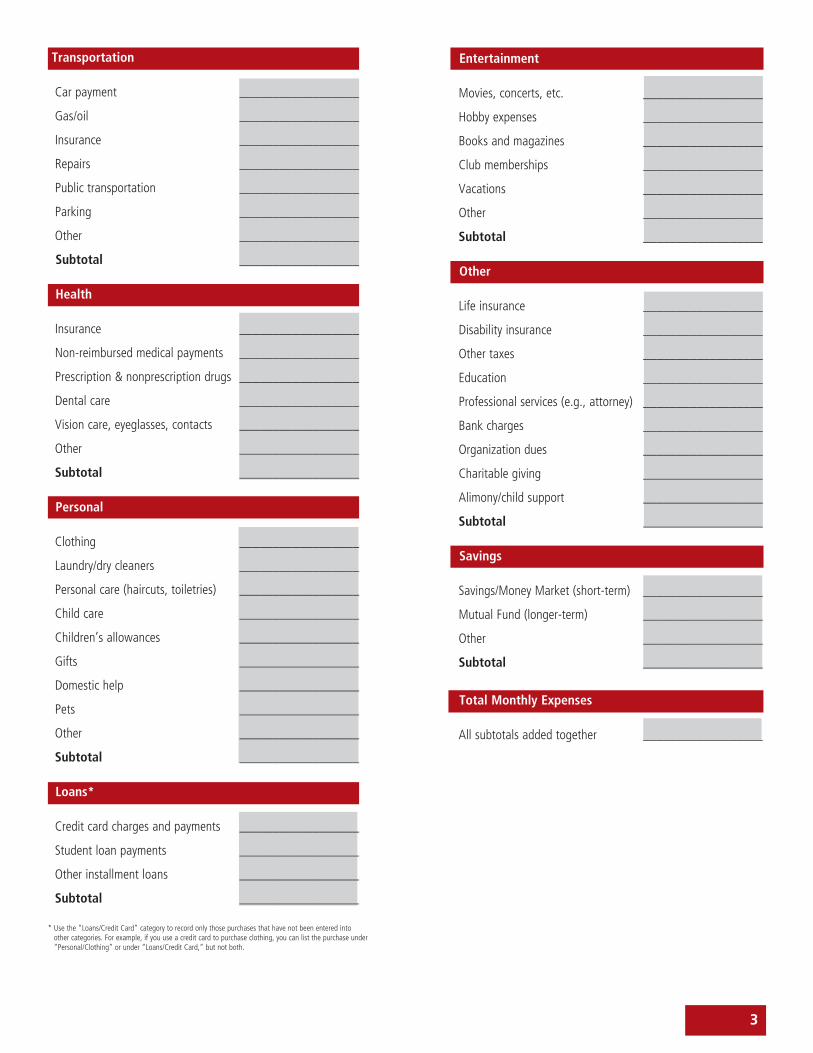

Monthly Expense Record

Housing

Rent or mortgage __________________

Insurance __________________

Property taxes __________________

Utilities (gas, oil, electric, water) __________________

Telephone __________________

Home repairs __________________

Cleaning __________________

Furniture and appliances __________________

Other __________________

Subtotal __________________

Food

Groceries __________________

Restaurants __________________

Other __________________

Subtotal __________________

LIFE ADVICE®

3

* Use the “Loans/Credit Card” category to record only those purchases that have not been entered into other categories. For example, if you use a credit card to purchase clothing, you can list the purchase under “Personal/Clothing” or under “Loans/Credit Card,” but not both.

Entertainment

Movies, concerts, etc. __________________

Hobby expenses __________________

Books and magazines __________________

Club memberships __________________

Vacations __________________

Other __________________

Subtotal __________________

Other

Life insurance __________________

Disability insurance __________________

Other taxes __________________

Education __________________

Professional services (e.g., attorney) __________________

Bank charges __________________

Organization dues __________________

Charitable giving __________________

Alimony/child support __________________

Subtotal __________________

Savings

Savings/Money Market (short-term) __________________

Mutual Fund (longer-term) __________________

Other __________________

Subtotal __________________

Total Monthly Expenses

All subtotals added together __________________

Transportation

Car payment __________________

Gas/oil __________________

Insurance __________________

Repairs __________________

Public transportation __________________

Parking __________________

Other __________________

Subtotal __________________

Health

Insurance __________________

Non-reimbursed medical payments __________________

Prescription & nonprescription drugs __________________

Dental care __________________

Vision care, eyeglasses, contacts __________________

Other __________________

Subtotal __________________

Personal

Clothing __________________

Laundry/dry cleaners __________________

Personal care (haircuts, toiletries) __________________

Child care __________________

Children’s allowances __________________

Gifts __________________

Domestic help __________________

Pets __________________

Other __________________

Subtotal __________________

Loans*

Credit card charges and payments __________________

Student loan payments __________________

Other installment loans __________________

Subtotal __________________

4

Look With a Critical Eye Using the monthly expense categories you’ve identified, try to reconstruct your expenses for the past few months. You may be surprised to find that you actually spent more money in those months than you can account for. You’ll have a record of your credit card expenditures and your checks, but cash often seems to just disappear.

To get an even better picture, continue to record expenses for several months as you develop your budget. When you review your expenses, you’ll probably see areas where you can reduce spending and increase your savings. You’ll also get a good idea of which expenses you can’t change. Understanding and changing your spending habits is the key to successful budgeting.

Now, take a blank copy of your expense record and label it “Budget.” Instead of recording actual expenses, list what you expect to spend in each category. Start by listing constant expenses—such as rent or mortgage and car payments—that don’t change from month to month. Then, use the information you’ve gathered over the past several months to set reasonable limits on the items that fluctuate, such as food and clothing, and those where you have the most flexibility, such as entertainment. Setting the limits isn’t hard—the trick is living within them.

Establish Savings Goals Once it’s clear how your money is being spent, you can establish goals for saving money. Identify shorter-term goals for expenses such as home improvement or a vacation, and longer-term goals for things like a college education or retirement account. Write down exactly what you’re saving for, and keep the list handy for extra motivation. Set up savings to be as automatic as possible, using direct deposit from your bank account or direct payroll deductions.

Start with the following chart, and personalize it to reflect your goals. Prioritize every item on the list and assign each a time frame—weeks, months or years—to help gauge your progress. Ideally, you want to save at least 10 percent of your earnings, but no amount is too small. Even a dollar a day adds up to $365 a year.

Goal Priority Amount Time Frame

Pay off bills ____ __________ _________

Emergency cash reserve ____ __________ _________

Savings ____ __________ _________

New car ____ __________ _________

Buy a home ____ __________ _________

Gifts ____ __________ _________

College ____ __________ _________

Wedding ____ __________ _________

Vacation ____ __________ _________

Retirement ____ __________ _________

Other ____ __________ _________

5

Matching Budget With Savings Needs Now compare your living expenses and your savings goals. While it’s likely that the expense side will need some work, most who undertake this exercise find that a surprising amount of cash is unaccounted for. Ask yourself where you can spend less without drastically cutting your standard of living. And start a “pay yourself first” program by automatically setting aside an amount each month. This amount can then be increased if you get a raise or pay off an installment loan. Here’s a list of suggestions to help you cut corners and stick to your budget:

• Don’tbuyanythingonimpulse.

• Payoffcreditcardseachmonth;chargeitemsonlyforconvenience.

• Takeyourlunchandsnackstowork.Avoidvendingmachines.

• Buyinbulk;usecoupons.

• Ifyousmoke,quit.It’sgoodforyourhealthandyourbudget.

• Entertainathomeinsteadofgoingtoarestaurant.RentaDVDinsteadofatriptothetheater.

• Putsomemoneyintosavingseverypayperiod.Ifyourcompanyorbankhasanautomaticsavings plan, sign up.

While all of these suggestions will help control expenses, many people find that it’s actually easier to tackle the big items. Look at the big expenses in your budget and think about how you might cut them. Consider buying a less expensive car, for example (your car payment and your car insurance will be less). Or consider buying a used car instead of a new one.

If you’ve trimmed and cut, but still can’t meet your savings goals, reevaluate your goals. Perhaps if you change the time frame you can meet the goal—delay the trip to Rome for a year or two, and take a less expensive vacation closer to home. Sometimes, though, you’ll have to adjust the goal itself.

Putting Your Savings to WorkOnce saving becomes part of your budget and spending routine, money will begin to accumulate. It’s important to take advantage of financial tools that can help your savings earn interest and grow in value. The dollar-a-day savings example illustrates the power of compound interest. If you invest the $365 saved in a year in an account earning a 4 percent return, compounded daily, here’s how that money will grow*:

Savings + Amount Saved 4% Interest

One Year $365 $372

Five Years $1,825 $2,021

Ten Years $3,650 $4,492

Thirty Years $10,950 $21,195

*Note that the savings plus interest accumulations above do not reflect any tax liability that might be incurred. Returns mentioned are hypothetical, and are not intended to reflect any actual investments.

6

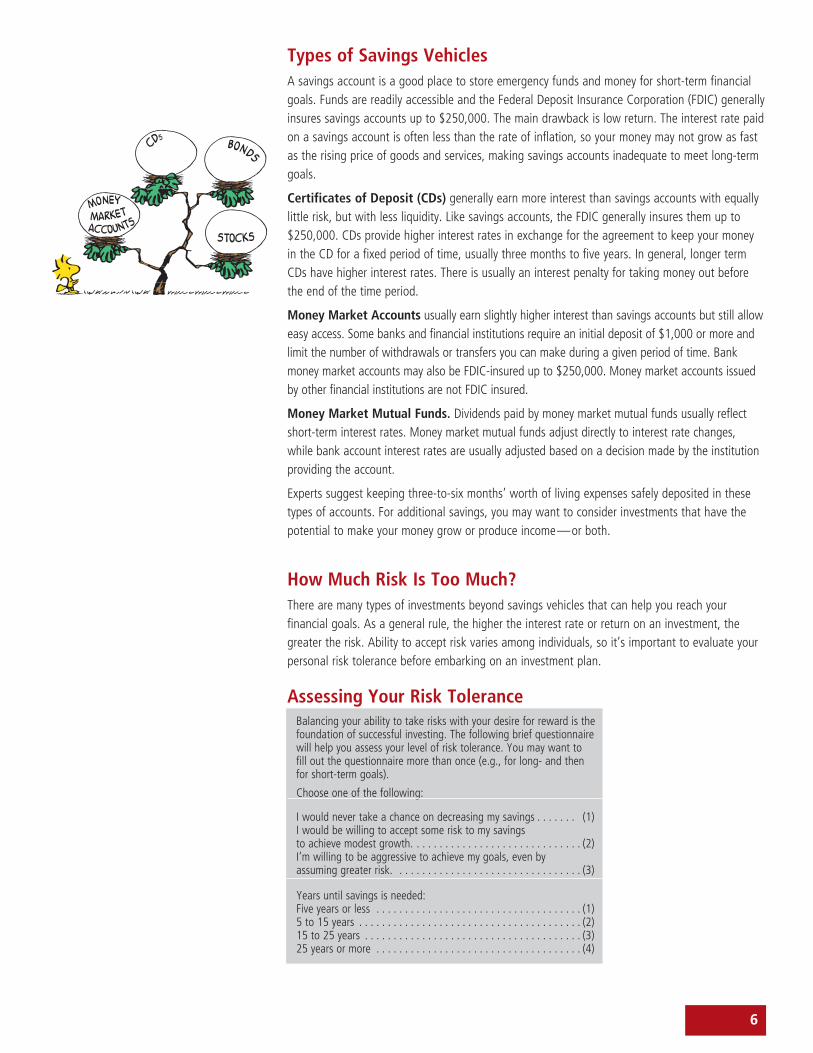

Types of Savings VehiclesA savings account is a good place to store emergency funds and money for short-term financial goals. Funds are readily accessible and the Federal Deposit Insurance Corporation (FDIC) generally insures savings accounts up to $250,000. The main drawback is low return. The interest rate paid on a savings account is often less than the rate of inflation, so your money may not grow as fast as the rising price of goods and services, making savings accounts inadequate to meet long-term goals.

Certificates of Deposit (CDs) generally earn more interest than savings accounts with equally little risk, but with less liquidity. Like savings accounts, the FDIC generally insures them up to $250,000. CDs provide higher interest rates in exchange for the agreement to keep your money in the CD for a fixed period of time, usually three months to five years. In general, longer term CDs have higher interest rates. There is usually an interest penalty for taking money out before the end of the time period.

Money Market Accounts usually earn slightly higher interest than savings accounts but still allow easy access. Some banks and financial institutions require an initial deposit of $1,000 or more and limit the number of withdrawals or transfers you can make during a given period of time. Bank money market accounts may also be FDIC-insured up to $250,000. Money market accounts issued by other financial institutions are not FDIC insured.

Money Market Mutual Funds. Dividends paid by money market mutual funds usually reflect short-term interest rates. Money market mutual funds adjust directly to interest rate changes, while bank account interest rates are usually adjusted based on a decision made by the institution providing the account.

Experts suggest keeping three-to-six months’ worth of living expenses safely deposited in these types of accounts. For additional savings, you may want to consider investments that have the potential to make your money grow or produce income—or both.

How Much Risk Is Too Much?There are many types of investments beyond savings vehicles that can help you reach your financial goals. As a general rule, the higher the interest rate or return on an investment, the greater the risk. Ability to accept risk varies among individuals, so it’s important to evaluate your personal risk tolerance before embarking on an investment plan.

Assessing Your Risk ToleranceBalancing your ability to take risks with your desire for reward is the foundation of successful investing. The following brief questionnaire will help you assess your level of risk tolerance. You may want to fill out the questionnaire more than once (e.g., for long- and then for short-term goals).

Choose one of the following:

I would never take a chance on decreasing my savings . . . . . . . (1)I would be willing to accept some risk to my savings to achieve modest growth. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (2)I’m willing to be aggressive to achieve my goals, even by assuming greater risk. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (3)

Years until savings is needed: Five years or less . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (1) 5 to 15 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (2) 15 to 25 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (3) 25 years or more . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (4)

7

My priority is to: Preserve savings and earn a modest return . . . . . . . . . . . . . . . . (1) Generate potentially higher returns with limited risk . . . . . . . . . . (2) Grow my savings assuming moderate risk . . . . . . . . . . . . . . . . . . (3) Aggressively grow savings despite significant risk . . . . . . . . . . . . (4)

My emergency savings would cover expenses for: Six months or more . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (3) A few months . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (2) A few weeks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (1) No emergency savings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (0)

If the stock market dropped 15 percent, I would: Cash out to avoid further losses . . . . . . . . . . . . . . . . . . . . . . . . . (1) Reduce the amount invested in equities overall . . . . . . . . . . . . . (2) Do nothing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (3) Buy more stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (4)

Add the points indicated at the end of each statement or choice. If your score is 4, 5 or 6, safety is your priority. You’ll likely be most comfortable with relatively conservative investments that don’t have sudden or extreme fluctuations.If you scored more than 10, your situation may allow you to assume greater risk in your financial choices. In general, the higher your overall score, the more investment risk you are personally able to tolerate. However, this chart is only a guide to determining your risk tolerance. When you’re ready to make investments, a qualified financial advisor can help you choose investments that fit your specific situation.

Types of InvestmentsOnce you have a feel for your risk tolerance, consider what types of investments might be right for you. Following is an overview of some common investment opportunities.

Stocks

When you buy stock, you become part owner of a company. In choosing stocks, you’re looking for companies that you believe will do well over time. If the company does well, you may receive dividends and/or be able to sell your stock at a profit. Conversely, if the company does poorly and its stock price falls, you may lose some or all of the money you invested.

There are two types of stock: common and preferred. As an owner of common stock, you are entitled to attend annual meetings and vote, although for a small investor these entitlements are usually meaningless. Preferred stock generally guarantees fixed dividends. Even if the company does not do well, you will receive dividends before the common stockholders. Shareholders owning preferred stock generally have restricted voting rights, and sometimes no voting rights.

8

Reading Stock Tables

Stock tables, which are in daily newspapers as well as online, can be confusing—a lot of information is presented in an abbreviated form. Once you learn what the abbreviations mean, most of the confusion will disappear.

• Stock—Under this heading is an abbreviated form of the company’s name, also called a symbol. Here, the XYZ Co.’s common stock is listed as XYZ. Not all symbols are easy to decipher. If a stock symbol’s roots are not obvious to you, an online service can help you determine the full company name.

• Div—Dividend is the cash return paid on the stock. This listing shows that the XYZ Co. is paying stockholders an annual cash dividend of $2 per share. A rising dividend may be a signal the company is confident of its future.

• Yld%—Yield is the percentage return paid on the stock. That $2 dividend equals about 3.4 percent of XYZ Co.’s stock price. Though 3.4 percent may be below the rate on a bank CD, investors will accept it because they hope the stock price will go up as well.

• PE—PE (or p/e) is the price-to-earnings ratio. PE is a comparison of the day’s closing stock price to the company’s profit per share over the last year. Here, XYZ Co. sold for 10 times earnings. A hot growth stock may sell at 25 times earnings or even more. A troubled stock will have a low PE.

• Vol 100s—Volume is the number of shares traded that day. Multiply this number by 100 to get the real volume. On this example day, 2.9 million XYZ Co. shares changed hands.

• Hi and Lo—The high and low prices that day. All investors want to buy low and sell high, and many want to know the range during the day. XYZ Co.’s high this day was $59.625. The low was $58.375.

• Close—Close is where the stock ended that day. This is the last price a stock sold for on the day. It’s also the information investors most often seek when they look up a stock in the paper. XYZ Co.’s close was 59, or $59. In some papers, close is called “last.”

• Net chg—Net chg is the price change from the day before. Investors always want to know if a stock finished up or down (i.e., higher or lower) from the previous day. XYZ Co. closed up 1⁄2 point, or 50 cents. Some newspapers use “Chg” instead.

Bonds

Bonds are a form of debt instrument or loan that you make to a corporation, the federal government and its agencies, or a local government. You become a creditor for a set period of time, called a term, and you are paid interest for the use of your money. Bond terms generally range from a few months up to 30 years. If you hold the bond until it matures (i.e., until the end of its term), the issuer promises to return to you the amount you originally paid, plus a fixed rate of interest. It is possible, though, for bond issuers to default, meaning they may be unwilling or unable to pay their debts, including the debt owed to holders of their bonds. Overall, bonds are considered a safer investment than stocks, because bondholders are paid before stockholders, should a company become insolvent. Bonds are not FDIC insured. Independent agencies such as Standard & Poor’s and Moody’s rate bonds in the marketplace according to default risk. Examine the ratings of bonds before you buy.

It’s important to understand the relationship between interest rates and bonds. When interest rates go up, there is a risk that the market value of bonds will go down. If the market value of a bond you own goes down, and you want to sell before the bond’s maturity date, you may receive less than you originally paid for the bond and/or less than the maturity value of the bond. The interest rate of bonds, however, remains fixed. For example, if you try to resell a bond when interest rates in general

BOND

Stock Div Yld% PE Vol 100s Hi Lo Close Net chg

XYZ Co. 2.00 3.4 10 29062 59.625 58.375 59 +1⁄ 2

9

are higher than the bond’s interest rate, your bond will not be attractive to buyers, and its market value will drop. Conversely, if your bond pays a higher interest rate than the bonds that are currently being sold, your bonds will be desirable to buyers and the price may go up.

There are many types of bonds, including:

Savings bonds, which are principal protected and not subject to interest rate risk.

Municipal bonds (munis), sold by states, cities and other local governments, are generally exempt from federal taxes (i.e., you will pay no federal tax on the interest). Depending on the issuer, muni bonds may be exempt from state and local taxes as well.

Insured bonds generally pay lower interest rates, because a third party guarantees payment of interest and principal. Insured bonds have less risk of default.

Corporate bonds issued by companies, which may include the following types:

• Zero coupon bonds, similar to savings bonds, are bonds that do not pay interest during the life of the bond. You buy zero coupon bonds at a deep discount from their face value. Face value is the amount the bond will be worth when it “matures” or comes due. At maturity, you receive one lump sum equal to the initial investment plus interest that has accrued over the life of the bond.

• Convertible bonds, which can be converted into stock.

• High-yield bonds, commonly referred to as junk bonds, are issued by corporations or governments with low ratings. They have a higher risk of default.

Mutual Funds

A mutual fund is a pool of money, supplied by investors like you, that is invested in various securities such as stocks, bonds, money market instruments or a combination of these investments. The total investments (holdings) of a mutual fund are called its portfolio. Every share of the mutual fund represents a proportion of ownership of the fund’s portfolio as well as a proportion of the income those holdings generate. Typically, the investment portfolios of mutual funds have a professional manager or team of managers making day-to-day and minute-by-minute buy and sell decisions.

By investing in mutual funds, you can diversify your investments and balance risk.

There are many types of mutual funds, and the amount of risk varies widely. The share value of a mutual fund will go up and down as market conditions change — and investors may make or lose money. Mutual funds are not FDIC-insured, even when they are sold through a bank.

Mutual fund companies are required by law to provide you with a prospectus before you invest. A prospectus is a legal document providing detailed information about the mutual fund’s investment strategy, fee structure and operations and is available from your registered representative. Carefully consider investment objectives, risks, charges and expenses before investing. For this and other information about any mutual fund investment, read the prospectus carefully before you invest. Investment return and principal value will fluctuate with changes in market conditions such that shares may be worth more or less than original cost when redeemed. Diversification cannot eliminate risk of investment losses.

10

Your Home

You may not think of a home in investment terms, but it is likely to be the largest single investment you’ll ever make. That’s why it’s important to choose your home with an eye toward long-term value. Keep your home in good repair to maintain or even improve its market value. Market value is based on many factors, including: square footage, house style, location/neighborhood, school district, property tax rates and transportation. Consider as many factors as you can when purchasing. For example, the quality of the school district may seem unimportant to you if your children are grown and gone. When you decide to sell your house, however, potential buyers with children may not want to look in your area.

If you’ve ever shopped for a house, you know that many factors impact price (e.g., good location usually equals higher price). Most people cannot afford to buy a house that is “perfect” for them in every way, and so are forced to make trade-offs. If you find yourself in this position, make sure you’ve gathered and considered as much information as you can before deciding which trade-offs you’re willing to make.

Retirement Investment Plans and Arrangements Financial experts are pretty much in agreement: save for retirement sooner rather than later. It’s never too early to begin saving for retirement. If you don’t already have one, consider establishing a tax-favored retirement account, such as one of the following:

401(k) Plans. If your employer offers a 401(k) plan, it may be one of the best retirement savings vehicles available to you, particularly if the employer matches all or a portion of your contribution. With a 401(k) plan, you may contribute up to a certain percentage of your gross income (i.e., total income before taxes).

Typically, 401(k) plans offer many investment choices, including a variety of mutual funds (e.g., stocks, bonds, money market). Some plans may allow investments in company stock and U.S. Series EE Savings Bonds, as well. You choose how to invest your savings, and you will have the option to change investments at specified times (e.g., quarterly). Typically, you may stop contributions at any time.

Earnings in a 401(k) grow tax-deferred until the money is withdrawn—usually after retirement—when you may be in a lower tax bracket. If you withdraw money before you turn age 591⁄2, however, you may be subject to an additional 10 percent IRS penalty. While early withdrawals are generally not permitted, some 401(k) plans permit withdrawals for “hardship” reasons, such as medical emergencies or college tuition. You do pay income tax on the amount withdrawn, and a 20 percent mandatory withholding generally is required from the distribution. Some 401(k) plans may also permit loans against your savings, as well.

403(b) Plans, also known as Tax Sheltered Annuities or TSAs, are retirement plans for nonprofit organizations that are similar to 401(k) plans. Investment options in 403(b) plans include annuities and mutual funds.

Individual Retirement Arrangements (IRAs), are sometimes called “traditional IRAs.” IRAs were established by Congress to encourage people to save for retirement by providing tax advantages. Qualifying individuals may contribute up to $5,000 annually (an additional $1,000 may be contributed if you are over 50) to an IRA. Tax benefits vary depending on your income and whether you contribute to other tax-advantaged savings plans (e.g., a 401(k) plan). In addition to possible tax deduction of IRA contributions, earnings in an IRA grow tax deferred until withdrawals begin. Your money must be designated as an IRA, in an approved account. You have a wide choice of investment options. Funds

11

in an IRA are considered long-term savings and, as with 401(k) plans, you may be subject to a 10 percent IRS penalty as well as to tax liability for premature withdrawals—generally before the age of 591⁄2.Consultaqualifiedtaxprofessionalformorecompleteinformation.

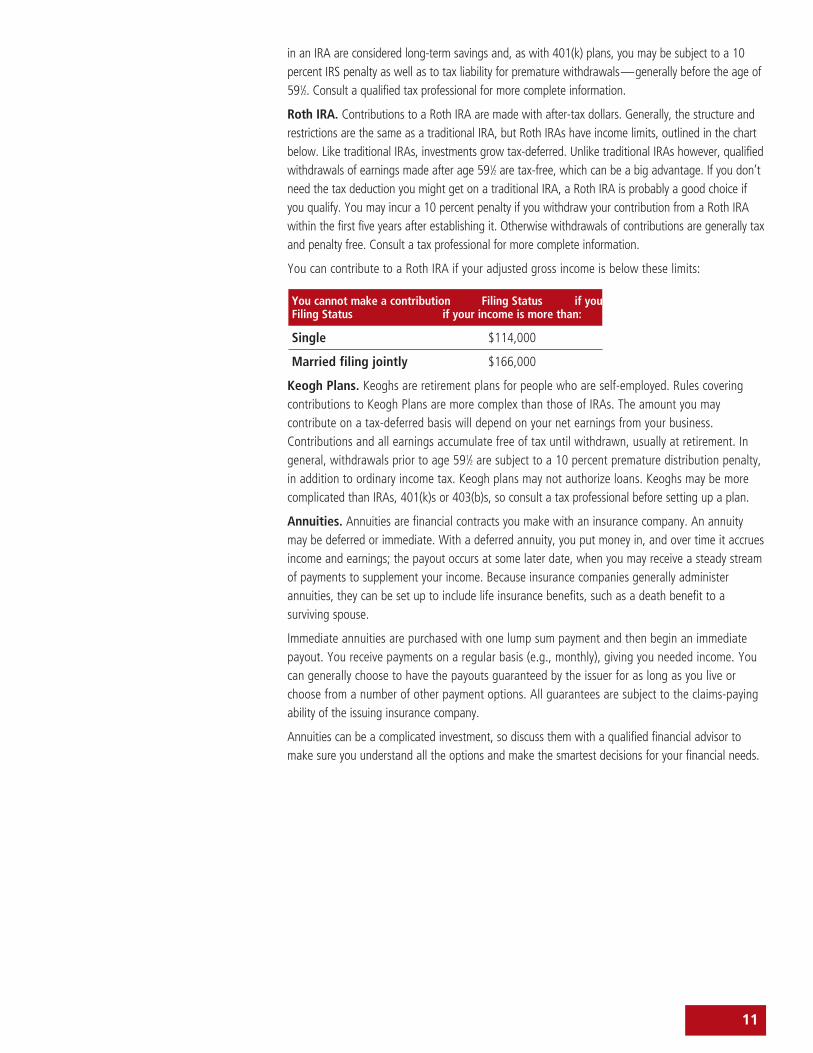

Roth IRA. Contributions to a Roth IRA are made with after-tax dollars. Generally, the structure and restrictions are the same as a traditional IRA, but Roth IRAs have income limits, outlined in the chart below.LiketraditionalIRAs,investmentsgrowtax-deferred.UnliketraditionalIRAshowever,qualifiedwithdrawals of earnings made after age 591⁄2 are tax-free, which can be a big advantage. If you don’t need the tax deduction you might get on a traditional IRA, a Roth IRA is probably a good choice if youqualify.Youmayincura10percentpenaltyifyouwithdrawyourcontributionfromaRothIRAwithin the first five years after establishing it. Otherwise withdrawals of contributions are generally tax and penalty free. Consult a tax professional for more complete information.

You can contribute to a Roth IRA if your adjusted gross income is below these limits:

You cannot make a contribution Filing Status if your Filing Status if your income is more than:

Single $114,000

Married filing jointly $166,000

Keogh Plans. Keoghs are retirement plans for people who are self-employed. Rules covering contributions to Keogh Plans are more complex than those of IRAs. The amount you may contribute on a tax-deferred basis will depend on your net earnings from your business. Contributions and all earnings accumulate free of tax until withdrawn, usually at retirement. In general, withdrawals prior to age 591⁄2 are subject to a 10 percent premature distribution penalty, in addition to ordinary income tax. Keogh plans may not authorize loans. Keoghs may be more complicated than IRAs, 401(k)s or 403(b)s, so consult a tax professional before setting up a plan.

Annuities. Annuities are financial contracts you make with an insurance company. An annuity may be deferred or immediate. With a deferred annuity, you put money in, and over time it accrues income and earnings; the payout occurs at some later date, when you may receive a steady stream of payments to supplement your income. Because insurance companies generally administer annuities, they can be set up to include life insurance benefits, such as a death benefit to a surviving spouse.

Immediate annuities are purchased with one lump sum payment and then begin an immediate payout. You receive payments on a regular basis (e.g., monthly), giving you needed income. You can generally choose to have the payouts guaranteed by the issuer for as long as you live or choose from a number of other payment options. All guarantees are subject to the claims-paying ability of the issuing insurance company.

Annuitiescanbeacomplicatedinvestment,sodiscussthemwithaqualifiedfinancialadvisortomake sure you understand all the options and make the smartest decisions for your financial needs.

12 12

For More Information

Free Publications

The quarterly Consumer Information Center Catalog lists more than 200 helpful federal government publications. Obtain a free copy by calling 888-8-PUEBLO or on the Internet at www.pueblo.gsa.gov.

Helpful Web Sites

www.betterinvesting.org The National Association of Investors Corporation Web site offers self-guided courses on stocks and mutual funds as well as an archive of educational articles.

www.irs.gov Internal Revenue Service Web site offers detailed information about the tax implications of various investment and retirement plans.

www.aaii.com The American Association of Individual Investors offers articles and guidance on stock investing, mutual funds, bonds, retirement planning and more.

LIFE ADVICE®

For information about other Life Advice topics,

go to www.metlife.com/lifeadvice

To order up to three free Life Advice booklets,

call 800-METLIFE (800-638-5433).

Pursuant to IRS Circular 230, MetLife is providing you with the following notification:

The information contained in this booklet is not intended to (and cannot) be used by any-one to avoid IRS penalties. This booklet does not support the promotion and marketing of any particular MetLife product. You should seek advice based on your particular circum-stances from an independent tax advisor.

MetLife does not give legal or tax advice. This booklet, as well as any recommended reading and reference material mentioned, is for general informational purposes only, and is issued as a public service. Always consult a qualified tax or legal professional for spe-cific, up-to-date information.

Current tax law is subject to interpretation and legislative change. Tax results and the appropriateness of any product for any specific taxpayer may vary depending on the particular set of facts and circumstances. You should consult with and rely on your own independent legal and tax advisors regarding your particular set of facts and circumstances.

Metropolitan Life Insurance Company (MLIC), New York, NY 10166. Securities products offered by MetLife Securities, Inc. (MSI)(member FINRA/SIPC), New York, NY 10166. MLIC and MSI are affiliates.

13

LIFE ADVICE®

For more information call 1-800-METLIFE or contact your local MetLife representative.

Text may be reproduced with written permission only. Reproduction of any graphical image, trademark or servicemark is prohibited.

LIFE ADVICE®

1003-1134 LAV05(0308) © 2010 METLIFE, INC. L0310097193(exp1212)(All States)(DC)PEANUTS © 2010 Peanuts Worldwide

Metropolitan Life Insurance Company200 Park AvenueNew York, NY 10166 www.metlife.com