Embed Size (px)

Citation preview

RESULTS PRESENTATIONFOR THE PERIOD ENDED

30 SEPTEMBER 2019

INVESTEC PROPERTY FUND

2

Glossary

CCS Cross currency swaps

CGT Capital gains tax

Edcon Edcon Holdings Limited

EV Enterprise value

GAV Gross asset value

GBF General banking facility

HFS Held for sale

IAPF Investec Australia Property Fund

Ingenuity or ING Ingenuity Property Investments Limited

IPF or The Fund Investec Property Fund Limited and its subsidiaries

IRS Interest rate swaps

Izandla or Izandla Property Fund Izandla Property Fund Proprietary Limited

MTM Mark to market

NAV Net asset value

NPI Net property income

PEL Pan-European logistics

PELI Pan-European light industrial

UK Fund Nestor Investment Holdings Limited

WALE Weighted average lease expiry

3

1. Six months in review

2. Financial review

3. Balance sheet management

4. SA property portfolio

5. Projects

6. Capital expenditure and sustainability

7. SA investments

8. Offshore investments

9. Capital allocation

10. Looking ahead

11. Annexures

Contents

SIX MONTHS IN REVIEW

5

Key highlightsFor the first half of the FY2020 year

New leadership settled• Complementary skills with similar philosophies and aligned behind a common purpose and strategy

• Supported by an experienced board of directors comprised of both property and financial / business skills

SA portfolio is resilient and maintained positive growth despite local headwinds• 1.3% base NPI growth

› 3.6% if Edcon rental rebate and tenant failures excluded

• Focus on letting – 89% of space expiring within the period re-let

• Low vacancy maintained – marginally up from 2.4% (March 2019) to 3.9%

• Total net cost to income increased to 20.9% (March 2019: 18.8%)

› Remains flat if Edcon and abnormal bad debts excluded

PEL platform continues to bolster portfolio performance• Further €21.5m invested

› 8 properties acquired (Netherlands, France and Poland) – GAV of €151m

• €106m deployed to date (€44m remaining)

• Current investment return of 11.9% in EUR (12.3% in ZAR); capital uplift since initial investment of 20.2% in EUR

• 20.1% total return for the period (in EUR)

• Letting activity ahead of business plan – 100% of total expiries let at positive reversion of 8.2%

• Portfolio vacancy of 1.2% – reduced from 5.1% at March 2019

• Initial €10m investment into PELI platform to acquire 25% interest – €54.5m remaining

6

Key highlightsFor the first half of the FY2020 year (continued…)

Further investment in UK Fund represents attractive enhancement to initial investment• Increased stake in UK Fund from 10% to 32.5% – £25m investment

• Acquired a portfolio of 3 retail warehouses for £14.7m (net initial yield of 7%)

• Expected to generate annualised total return of c.10% (in GBP)

Sell down of IAPF to facilitate successful ASX listing• Decreased stake from 20.9% to 9.9% to support ASX listing in May 2019 – R584m proceeds• 27.4% total shareholder return for the period

Capital recycling and investment activity implemented on an earnings enhancing basis• Sold R843m assets across SA and Australia and raised R519m debt to fund expansion

› Blended yield of 7.0%

• Exited minority Ingenuity position• Redeployed into Europe and UK

› Average return of 8.3%, higher returns generated on a risk-adjusted basis

• Balance used to fund local expansion and refurbishment / capital expenditure

Balance sheet strength further enhanced with sufficient capacity for growth• Gearing at 37.3% (March 2019: 35.9%) – marginal increase due to offshore activity

› SA cost of funding remains flat at 9.1%

• All balance sheet metrics enhanced› Hedging increased to 94% (March 2019: 84%)› Swap and debt maturity increased to 3.7 and 3.6 years respectively

• Balance sheet remains significantly unencumbered • Limited liquidity risk for the next 12 months

7

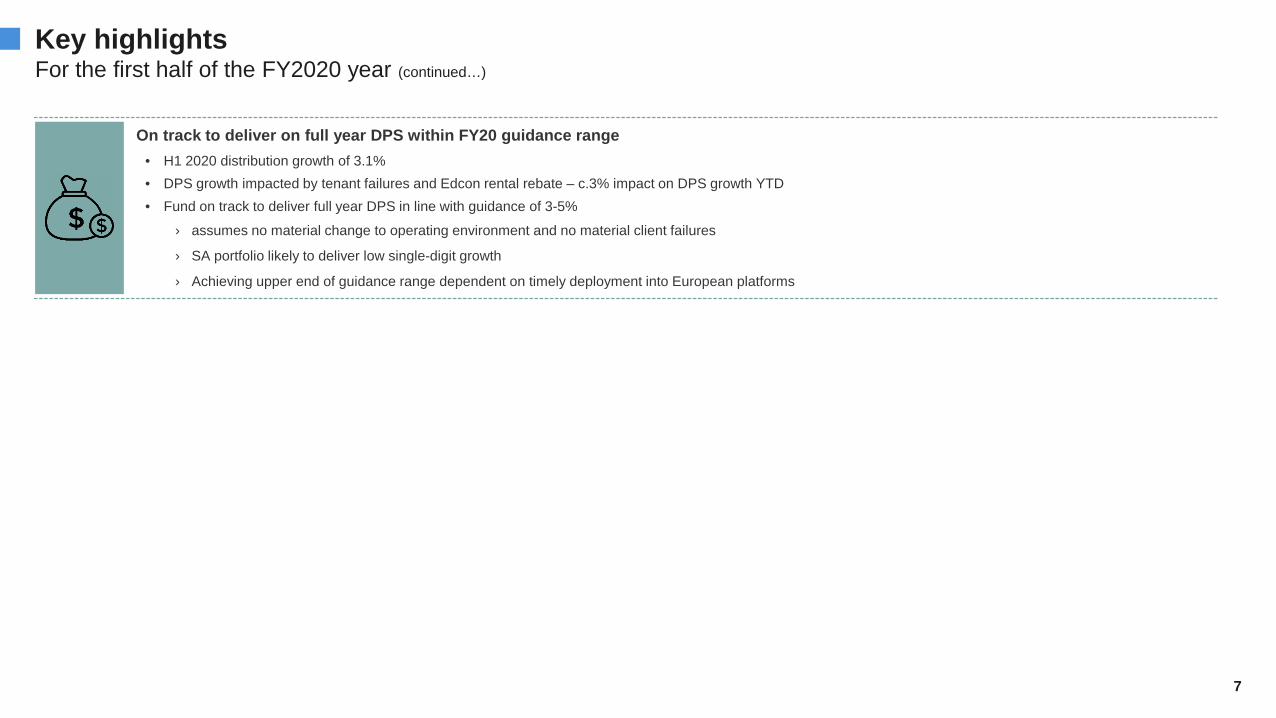

Key highlightsFor the first half of the FY2020 year (continued…)

On track to deliver on full year DPS within FY20 guidance range• H1 2020 distribution growth of 3.1%• DPS growth impacted by tenant failures and Edcon rental rebate – c.3% impact on DPS growth YTD• Fund on track to deliver full year DPS in line with guidance of 3-5%

› assumes no material change to operating environment and no material client failures

› SA portfolio likely to deliver low single-digit growth

› Achieving upper end of guidance range dependent on timely deployment into European platforms

8

Key metrics – H1 2020Good performance in a challenging environment

8

1.3%like-for-like net propertyincome growth

(Sep 2018: 1.7%)

2.9 yearsWeighted averagelease expiry

(Mar 2019: 2.8 years)70.9 cps(Sep 2018: 68.8 cps)

3.1%half year distribution growth

89.0%of space expired in the period renewed or re-let

(Mar 2019: 94.2%)

20.9%total cost to income ratio

(Mar 2019: 18.8%)

3.9%vacancy

(Mar 2019: 2.4%)1

SA portfolio in focus

94.0% interest rate exposure hedged (Mar 2019: 84.0%)

Swap expiry extended to 3.7 yrs (Mar 2019: 3.4 yrs)

7.1%all-in cost of funding decreased

(Mar 2019: 7.9%)

1.5%increase in NAV driven by performance of offshore investments

37.3% gearingTarget below 35%

(Mar 2019: 35.9%)

Balance sheet metrics

Offshore performance

Balance sheet composition

81.4% South Africa 18.6% Offshore

11.9% investment return8.2% capital uplift

EUR 20.1%total return from PEL YTD

GBP 10%anticipated total return from UK Fund

27.4%total shareholder return from IAPF YTD

13.0% including strategic development vacancy

(Mar 2019: 84.8%) (Mar 2019: 15.2%)

9

Operational strategyLiving the strategy in the Fund’s H1 2020 accomplishments…

Focus onlong-term value

creation

M&A- remain

opportunistic

Strategicoffshoreplatforms

Peopleon the ground

Propertypurists

Disciplinedapproach to

capital allocationand assetrecycling

Balance sheetmanagement

9

• Strive to differentiate ourselves through:› Best of breed assets› Client experience and creating an out-

of-the-ordinary experience for tenants› Unlocking the potential of space

• Targeted initiatives:› To anticipate and mitigate leasing risk through

early lease renewals and higher tenant retention

› Guerrilla tactics to source and secure

• Focused on repositioning SA assets:› Extracting value from existing assets› Positioning old / non-core assets for sale› Making hold / invest / sell decisions› Identifying ‘core-plus’ assets where

we can work on unlocking value• Operational efficiencies

• Explored opportunities in SA:› across asset classes – industry

consolidation› in unlisted space

• Assessed M&A opportunities to the value of ±R24bn in SA but turned them down

• Disposal of non-core and under-performing assets› more efficiently allocate capital

• Active balance sheet and treasury management• Well-positioned balance sheet

• Further deployment into UK and European platforms• Investment into new PELI platform

• PEL has gained scale • Performance is supporting overall IPF portfolio growth

• Offshore investments provide optionality

• Review of minority positions• Exited Ingenuity investment

• Sold down IAPF holding• Disposed of 4 properties - non-core

FINANCIAL REVIEW

11

1. Total NPI decreased due to sale of 4 properties (this was offset by savings in funding costs)2. Decreased due to disposal of 2 buildings in H2 2019 and 4 buildings in H1 20203. Includes income from IAPF (R37.9m), UK Fund (R8.8m), PEL portfolio (R86.1m) and Izandla (R16.6m), change in composition of investments4. Comprise fund expenses and asset management fee. Management fee increased as the EV increased and the Zenprop discount reduced

6. Interest from Izandla not serviced is not distributed, however more has been serviced in FY20 – in line with business plan7. Withholding tax on IAPF dividend and CGT on partial disposal of investment in IAPF

5. Decreased due to proceeds received on sale of buildings and IAPF shares used to pay down debt, offset by deployment into European platforms and UK Fund

Distribution statement3.1% H1 2020 DPS growth, in line with guidance

11

ActualSep 2019

Rm

Prior yearSep 2018

Rm±

%Net property income (excl. straight lining)¹ 701.2 720.7 (2.7)Base net property income 679.6 670.6 1.3Acquisitions and disposals2 21.6 50.0 (56.7)Income from investments3 149.4 135.1 10.6 Notional cost of Ingenuity funding 4.4 4.4 -Other operating expenses4 (50.2) (46.1) (9.0)Net finance costs5 (275.8) (300.3) 8.2 Izandla JPIK interest not received6 (1.3) (6.0) 78.1 Antecedent dividend - 1.55 (100.0)Taxation (net of deferred tax and CGT)7 (5.5) (2.7) (107.8)Net distribution income 522.2 506.6 3.1 Number of shares 736.3 736.3 -Total distribution per share (cents) 70.9 68.8 3.1

12

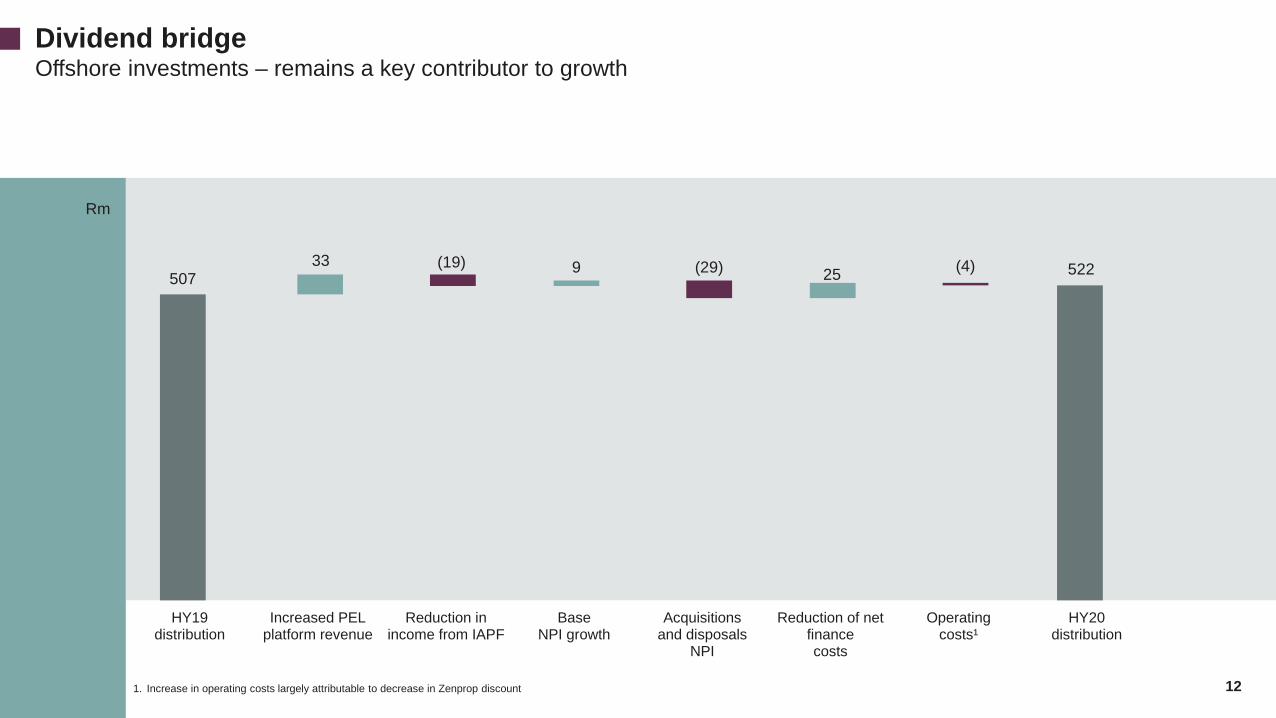

Dividend bridgeOffshore investments – remains a key contributor to growth

507 52233 9 25(19) (29) (4)

HY19distribution

Increased PELplatform revenue

Reduction inincome from IAPF

BaseNPI growth

Acquisitionsand disposals

NPI

Reduction of netfinancecosts

Operatingcosts¹

HY20distribution

Rm

1. Increase in operating costs largely attributable to decrease in Zenprop discount

13

Summarised income statementSignificant fair value gains achieved on IAPF investment

13

ActualSep 2019

Rm

Prior yearSep 2018

Rm±

%Net property income(incl. straight line adjustment) 689.6 744.3 (7.3)

Other operating expenses (50.2) (46.1) (9.0)Fair value adjustments 251.8 367.2 (31.4)

Mark to market – derivatives1 (94.6) 10.5 (1 001.2)Foreign exchange translation2 31.5 (42.5) 174.1 Mark to market – investment property (0.3) (51.7) 99.4 Mark to market – investments3 169.9 220.4 (22.9)Mark to market – PEL portfolio4 143.5 (39.1)(Loss)/profit on sale of investment property 1.8 (5.0) 135.9

Net finance costs5 (275.8) (300.2) 8.1 Income from investments6 177.0 133.0 33.1 Taxation7 (51.6) (7.2) (617.1)Accounting profit after tax 740.8 891.0 (16.9)

1. Negative MTM on derivatives is largely driven by negative MTM on IRS book due to flattening of the IRS curve and on CCS due to ZAR weakness2. Movements in the EUR and GPB exchange rate, relating to foreign debt and investments3. Comprises IAPF increase of R183.8m (increase in share price from R12.86 to R15.72) and Ingenuity decrease of R13.9m (closing price R1.05)4. Marginal tightening of cap rate on underlying property portfolio5. Lower due to proceeds received on sale of buildings and IAPF shares – offset by deployment into PEL6. Includes income received from IAPF (R70.5m), UK Fund (R6.1m), PEL portfolio (R86.1m) and Izandla (R14.3m)7. Deferred tax on IAPF

14

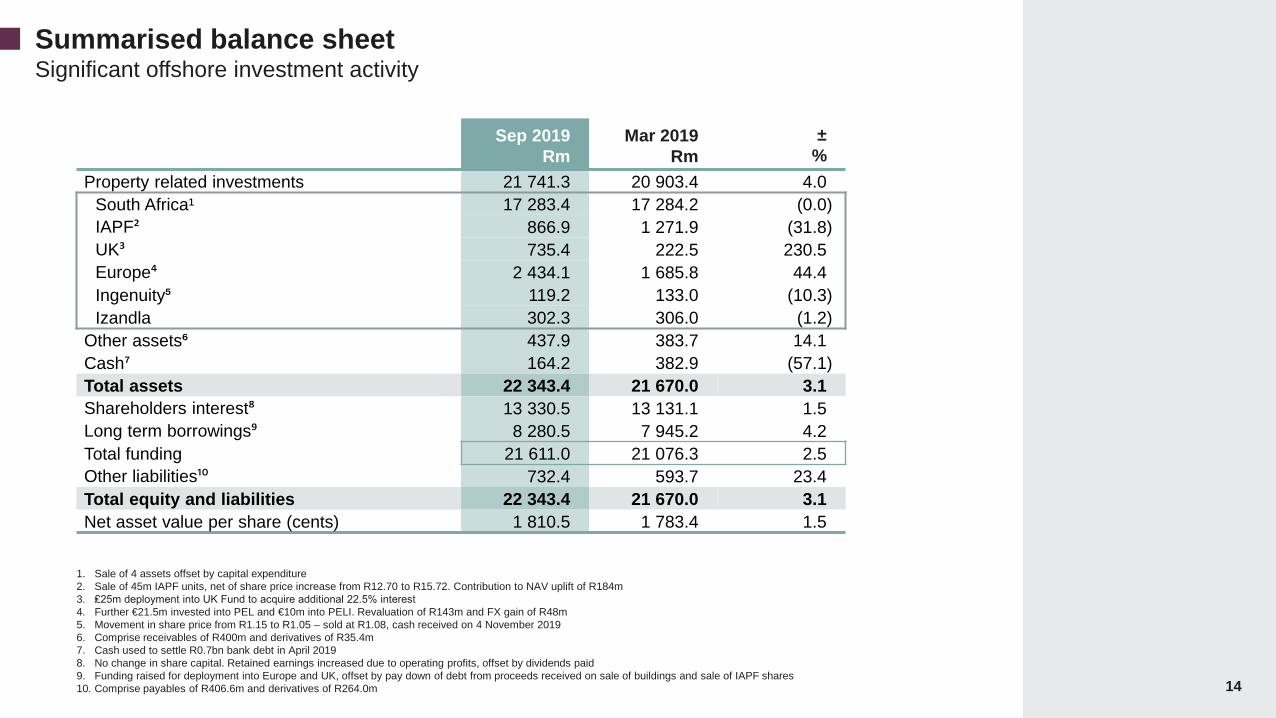

Summarised balance sheetSignificant offshore investment activity

14

1. Sale of 4 assets offset by capital expenditure2. Sale of 45m IAPF units, net of share price increase from R12.70 to R15.72. Contribution to NAV uplift of R184m3. ₤25m deployment into UK Fund to acquire additional 22.5% interest4. Further €21.5m invested into PEL and €10m into PELI. Revaluation of R143m and FX gain of R48m5. Movement in share price from R1.15 to R1.05 – sold at R1.08, cash received on 4 November 20196. Comprise receivables of R400m and derivatives of R35.4m7. Cash used to settle R0.7bn bank debt in April 20198. No change in share capital. Retained earnings increased due to operating profits, offset by dividends paid9. Funding raised for deployment into Europe and UK, offset by pay down of debt from proceeds received on sale of buildings and sale of IAPF shares10. Comprise payables of R406.6m and derivatives of R264.0m

Sep 2019Rm

Mar 2019Rm

±%

Property related investments 21 741.3 20 903.4 4.0 South Africa¹ 17 283.4 17 284.2 (0.0)IAPF² 866.9 1 271.9 (31.8)UK³ 735.4 222.5 230.5 Europe⁴ 2 434.1 1 685.8 44.4 Ingenuity⁵ 119.2 133.0 (10.3)Izandla 302.3 306.0 (1.2)

Other assets⁶ 437.9 383.7 14.1 Cash⁷ 164.2 382.9 (57.1)Total assets 22 343.4 21 670.0 3.1 Shareholders interest⁸ 13 330.5 13 131.1 1.5 Long term borrowings⁹ 8 280.5 7 945.2 4.2 Total funding 21 611.0 21 076.3 2.5 Other liabilities¹⁰ 732.4 593.7 23.4 Total equity and liabilities 22 343.4 21 670.0 3.1 Net asset value per share (cents) 1 810.5 1 783.4 1.5

15

Sep 2019Rm % of total

Mar 2019Rm % of total

SA investment property 17 283.4 79.5 17 284.1 82.7Ingenuity 119.2 0.5 115.8 0.6 Izandla 302.3 1.4 278.5 1.5 South African assets 17 704.9 81.4 17 678.4 84.8IAPF 866.9 4.0 1 251.8 6.1 UK Fund 735.4 3.4 222.5 1.1 European portfolio 2 434.1 11.2 1 379.0 8.0Offshore assets 4 036.4 18.6¹ 2 853.4 15.2 Total Investments 21 741.3 100.0 20 531.8 100.0

Balance sheet constructRemain committed to SA

1. Increased by 2.9% from year end as a result of deployment into UK Fund, PEL and PELI platforms, offset by sell down of IAPF

South Africa

UK

Australia

PEL

PELI

Return

Risk

Asset risk vs. return profile• Investment strategy progressing towards assets

that offer higher risk-adjusted returns

• Balance sheet remains diversified across SA & developed markets (82% SA focused)

Represents asset size / investment value

15

161. Additional deployment into PEL of €21.5m, initial investment into PELI of €10m, revaluation of the underlying portfolio amounting to R153m, income accrual and forex gains of R80m2. Deployment of additional £25m to increase stake to 32.5%3. Sale of 45m units in IAPF of R584m, offset by positive MTM on revaluation of R183m4. Debt drawn to fund acquisition activity, offset by proceeds from sales

Net asset value bridgeGrowth from investments (IAPF and PEL) offset by negative fair value movements on swap book

R’000

1 2

3

13,131 13,331

Opening NAV InvestmentPEL & PELI

InvestmentUK Fund

Sale of IAPF Movement indebt & cash

Working capital Movement inMTM & other

Closing NAV4

748

513 (405)

(554)

10 (112)

BALANCE SHEET MANAGEMENT

18

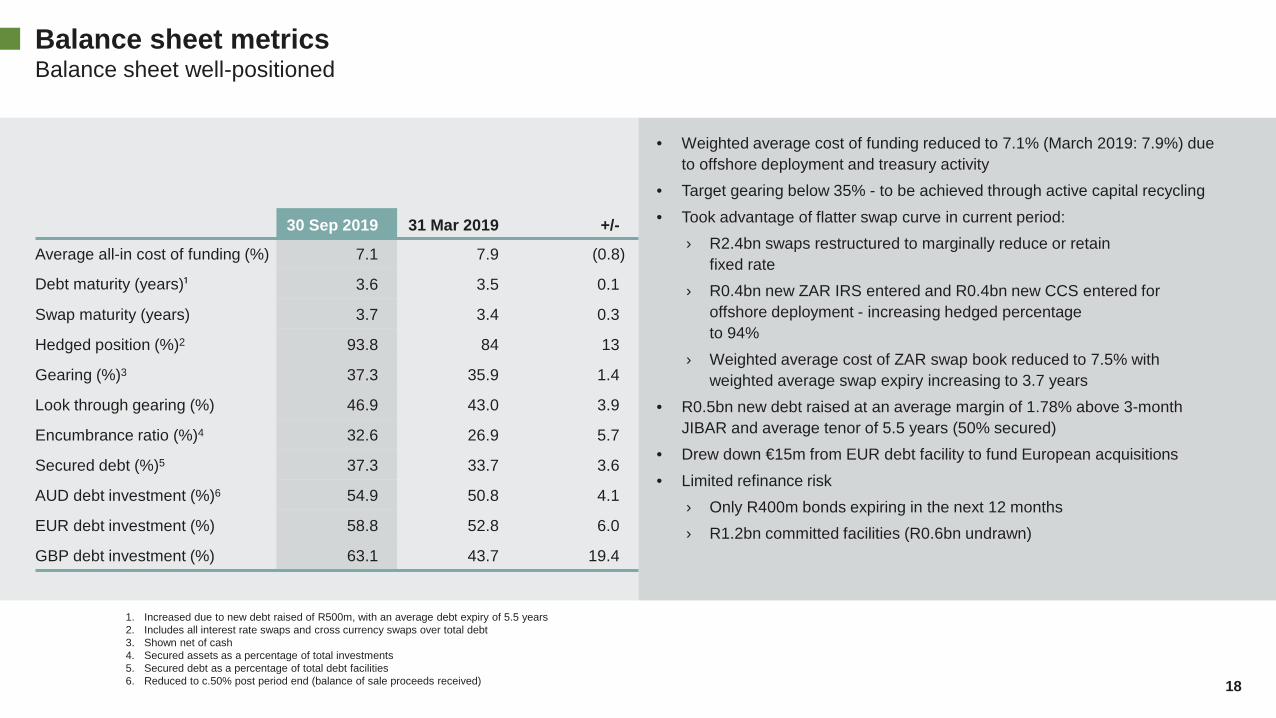

1. Increased due to new debt raised of R500m, with an average debt expiry of 5.5 years2. Includes all interest rate swaps and cross currency swaps over total debt3. Shown net of cash4. Secured assets as a percentage of total investments5. Secured debt as a percentage of total debt facilities6. Reduced to c.50% post period end (balance of sale proceeds received)

Balance sheet metricsBalance sheet well-positioned

30 Sep 2019 31 Mar 2019 +/-

Average all-in cost of funding (%) 7.1 7.9 (0.8)

Debt maturity (years)¹ 3.6 3.5 0.1

Swap maturity (years) 3.7 3.4 0.3

Hedged position (%)2 93.8 84 13

Gearing (%)3 37.3 35.9 1.4

Look through gearing (%) 46.9 43.0 3.9

Encumbrance ratio (%)4 32.6 26.9 5.7

Secured debt (%)5 37.3 33.7 3.6

AUD debt investment (%)6 54.9 50.8 4.1

EUR debt investment (%) 58.8 52.8 6.0

GBP debt investment (%) 63.1 43.7 19.4

• Weighted average cost of funding reduced to 7.1% (March 2019: 7.9%) due to offshore deployment and treasury activity

• Target gearing below 35% - to be achieved through active capital recycling• Took advantage of flatter swap curve in current period:

› R2.4bn swaps restructured to marginally reduce or retainfixed rate

› R0.4bn new ZAR IRS entered and R0.4bn new CCS entered for offshore deployment - increasing hedged percentageto 94%

› Weighted average cost of ZAR swap book reduced to 7.5% with weighted average swap expiry increasing to 3.7 years

• R0.5bn new debt raised at an average margin of 1.78% above 3-month JIBAR and average tenor of 5.5 years (50% secured)

• Drew down €15m from EUR debt facility to fund European acquisitions• Limited refinance risk

› Only R400m bonds expiring in the next 12 months› R1.2bn committed facilities (R0.6bn undrawn)

19

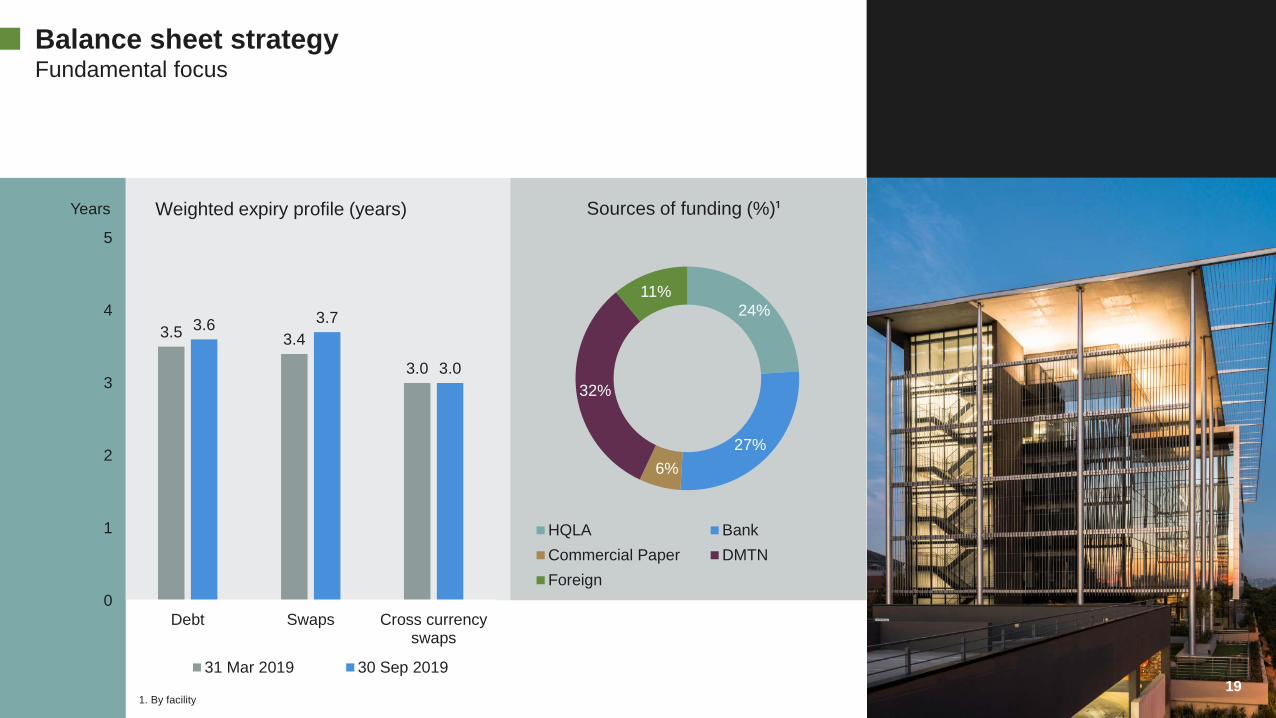

Balance sheet strategyFundamental focus

19

24%

27%6%

32%

11%

HQLA BankCommercial Paper DMTNForeign

3.5 3.4

3.0

3.6 3.7

3.0

0

1

2

3

4

5

Debt Swaps Cross currencyswaps

31 Mar 2019 30 Sep 2019

Sources of funding (%)¹Weighted expiry profile (years)

1. By facility

Years

20

Balance sheet strategyLooking forward

¹R400m bonds expiring, R452m commercial paper. IPF has sufficient committed facilities in the event investors choose not to roll²³Bank facilities of R300m (R160m drawn)R590m bonds - ample backstop facilities in place

2%9%

14%

28%33%

14%

0% 0%

16%10%

19%15%

19%14%

4% 3%0%

10%

20%

30%

40%

FY20 FY21 FY22 FY23 FY24 FY25 FY26 FY27Total swaps Total debt

Debt and swap expiry (%)

7%3%

15%

0% 0% 0% 0% 0%0% 0% 0%

12%

0% 0% 0% 0%

9%7%

4% 3%

8%4% 4%

0%0% 0% 0% 0%

11% 10%

0%3%

0%

5%

10%

15%

20%

FY20 FY21 FY22 FY23 FY24 FY25 FY26 FY27ZAR bank Foreign bank DMTN HQLA

Debt expiry (%)

¹

²³

R1.2bn committed facilitiesof which R0.6bn is undrawn (excluding GBF)

covers all imminent refinance risk

SA PROPERTY PORTFOLIO

221. Including legal tenants 3.6% (Sep 2018: 3.1%)2. Including strategic development vacancy 3.0%

SA property portfolioNPI growth despite macro-economic challenges

Property portfolio

• SA portfolio remains under pressure – positive letting performance and marginal uptick in vacancy, offset by increase in bad debts resulting from business failures and poor economy

• Total NPI decreased due to sale of 4 assets in H1 2020 and 2 assets in H2 2019. Base NPI growth subdued due to negative reversions, void periods and increased bad debts

• Cost to income ratio increased – key drivers as follows:› Low core rental growth of 0.4%, Edcon rental rebate, voids and negative reversions in prior and current year› Slight increase in variable costs – letting related costs due to increased letting activity› Significant increase in bad debts due to business failures and liquidations (4 large clients)› Fixed costs increased by 2.9% – well controlled, below inflation› Increase in net utility costs and net rates primarily due to void periods and council revaluations

• Vacancy increased 1.5% since March 2019 due to uptick in industrial off very low base• 89% of total expiries let YTD (full year – 84%)

ActualSep 2019

Rm

Prior yearSep 2018

Rm±

%Gross income 850.9 828.1 2.8

Net expense (171.3) (157.4) (8.8)

Base net property income 679.6 670.6 1.3Acquisitions and disposals 21.6 50.0 (56.7)Net property income(excl. straight lining) 701.2 720.6 (2.7)

Total net cost to income ratio 20.9% 19.3% 1.6%

Arrears % collectibles¹ 2.0% 1.0% 1.0%

22

Sep 2019 Mar 2019No. of properties 99 102

GLA (m²) 1 191 375 1 197 921

Vacancy 3.9% 2.4%²

WALE (years) 2.9 2.8

In-force escalation 7.5% 7.6%

Property asset value R17.3bn R17.3bn

231. Including legal tenants 4.4% (Sep 2018: 2.0%)

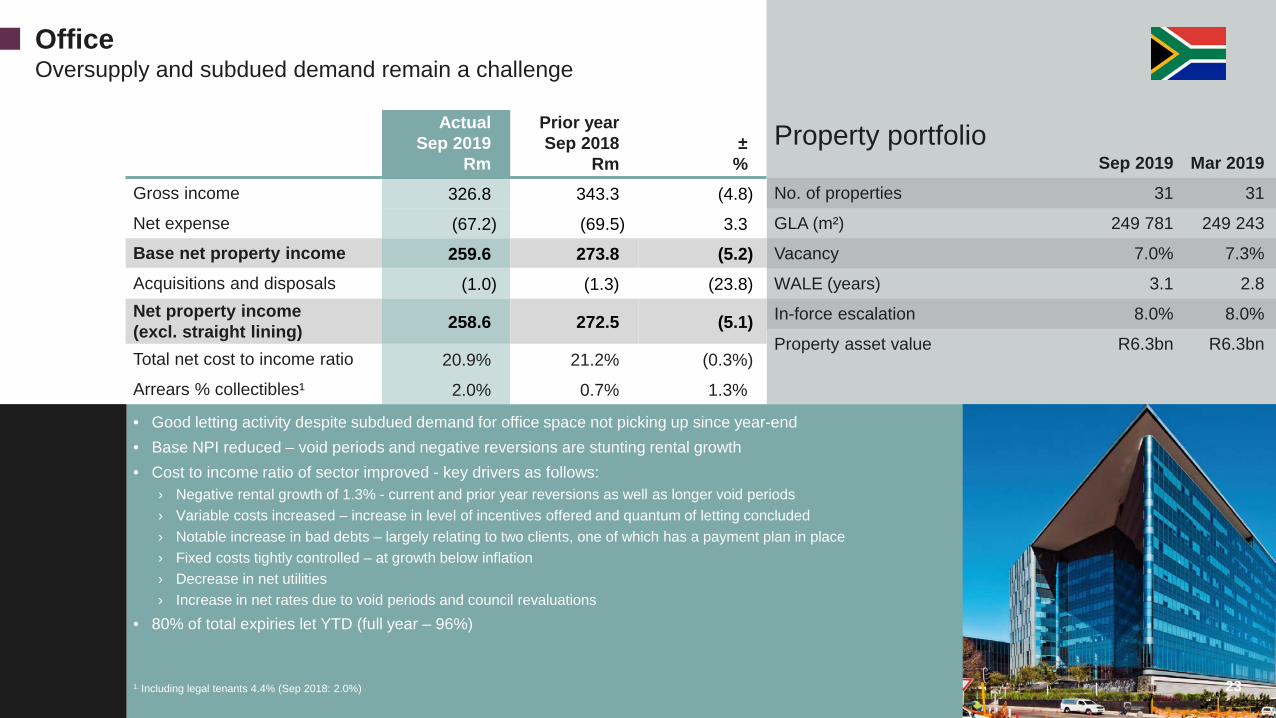

OfficeOversupply and subdued demand remain a challenge

Property portfolio

• Good letting activity despite subdued demand for office space not picking up since year-end• Base NPI reduced – void periods and negative reversions are stunting rental growth• Cost to income ratio of sector improved - key drivers as follows:

› Negative rental growth of 1.3% - current and prior year reversions as well as longer void periods› Variable costs increased – increase in level of incentives offered and quantum of letting concluded› Notable increase in bad debts – largely relating to two clients, one of which has a payment plan in place› Fixed costs tightly controlled – at growth below inflation› Decrease in net utilities› Increase in net rates due to void periods and council revaluations

• 80% of total expiries let YTD (full year – 96%)

ActualSep 2019

Rm

Prior yearSep 2018

Rm±

%Gross income 326.8 343.3 (4.8)Net expense (67.2) (69.5) 3.3 Base net property income 259.6 273.8 (5.2)Acquisitions and disposals (1.0) (1.3) (23.8)Net property income(excl. straight lining) 258.6 272.5 (5.1)

Total net cost to income ratio 20.9% 21.2% (0.3%)Arrears % collectibles¹ 2.0% 0.7% 1.3%

23

Sep 2019 Mar 2019No. of properties 31 31

GLA (m²) 249 781 249 243

Vacancy 7.0% 7.3%

WALE (years) 3.1 2.8

In-force escalation 8.0% 8.0%

Property asset value R6.3bn R6.3bn

241. Including legal tenants 4.1% (Sep 2018: 5.7%)

IndustrialUnder pressure given increase in bad debts and arrears

Property portfolio

• Sector resilient in challenging market – excellent letting• Client base under pressure as evidenced by rise in bad debts and arrears• Base NPI increased – good rental growth from shorter void periods,

offset by increase in bad debts• Cost to income ratio of sector increased – key drivers as follows:

› Good rental growth of 7.8% – shorter void periods in FY20› Variable costs stable year on year› Material increase in bad debts – low volume of tenants but high value in arrears› Fixed costs growth in line with inflation› Slight under recovery of net utilities and net rates to due to void periods

• Vacancy increased 2.8% since March 2019, due to additional vacancy at Riverhorse-IHD and Lerwick Road

• 88% of total expiries let YTD (full year – 84%)

ActualSep 2019

Rm

Prior yearSep 2018

Rm±

%Gross income 183.5 172.7 6.2 Net expense (34.0) (30.3) (12.4)Base net property income 149.5 142.5 4.9 Acquisitions and disposals 3.2 26.3 (87.9)Net property income(excl. straight lining) 152.7 168.8 (9.6)

Total net cost to income ratio 19.2% 17.0% 2.2%Arrears % collectibles¹ 3.8% 3.4% 0.4%

24

Sep 2019 Mar 2019No. of properties 37 38

GLA (m²) 527 723 531 501

Vacancy 4.0% 1.2%

WALE (years) 2.8 2.9

In-force escalation 7.5% 7.7%

Property asset value R3.8bn R3.7bn

251. Including legal tenants 2.8% (Sep 2018: 3.5%)². Including strategic development vacancy 1.8% (Mar 2019: 2.6%)

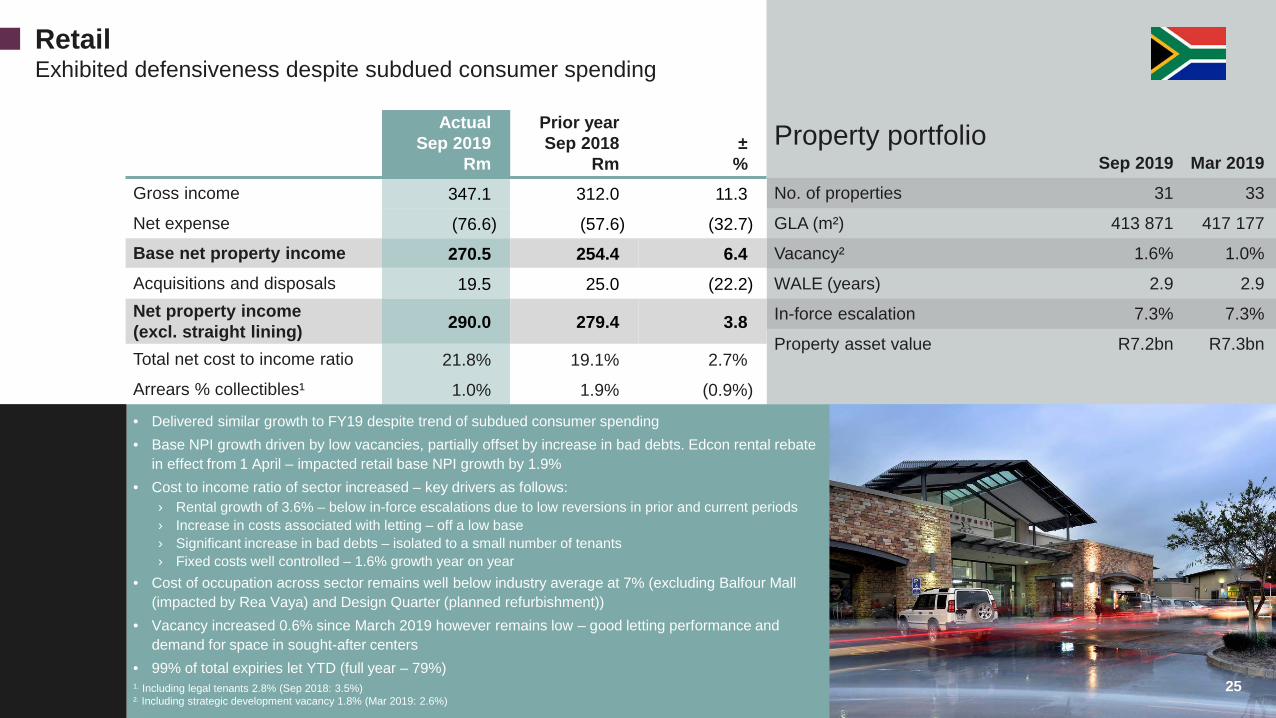

RetailExhibited defensiveness despite subdued consumer spending

Property portfolio

• Delivered similar growth to FY19 despite trend of subdued consumer spending• Base NPI growth driven by low vacancies, partially offset by increase in bad debts. Edcon rental rebate

in effect from 1 April – impacted retail base NPI growth by 1.9%• Cost to income ratio of sector increased – key drivers as follows:

› Rental growth of 3.6% – below in-force escalations due to low reversions in prior and current periods› Increase in costs associated with letting – off a low base› Significant increase in bad debts – isolated to a small number of tenants› Fixed costs well controlled – 1.6% growth year on year

• Cost of occupation across sector remains well below industry average at 7% (excluding Balfour Mall (impacted by Rea Vaya) and Design Quarter (planned refurbishment))

• Vacancy increased 0.6% since March 2019 however remains low – good letting performance and demand for space in sought-after centers

• 99% of total expiries let YTD (full year – 79%)

ActualSep 2019

Rm

Prior yearSep 2018

Rm±

%Gross income 347.1 312.0 11.3 Net expense (76.6) (57.6) (32.7)Base net property income 270.5 254.4 6.4Acquisitions and disposals 19.5 25.0 (22.2) Net property income(excl. straight lining) 290.0 279.4 3.8

Total net cost to income ratio 21.8% 19.1% 2.7%Arrears % collectibles¹ 1.0% 1.9% (0.9%)

25

Sep 2019 Mar 2019No. of properties 31 33

GLA (m²) 413 871 417 177

Vacancy² 1.6% 1.0%

WALE (years) 2.9 2.9

In-force escalation 7.3% 7.3%

Property asset value R7.2bn R7.3bn

26

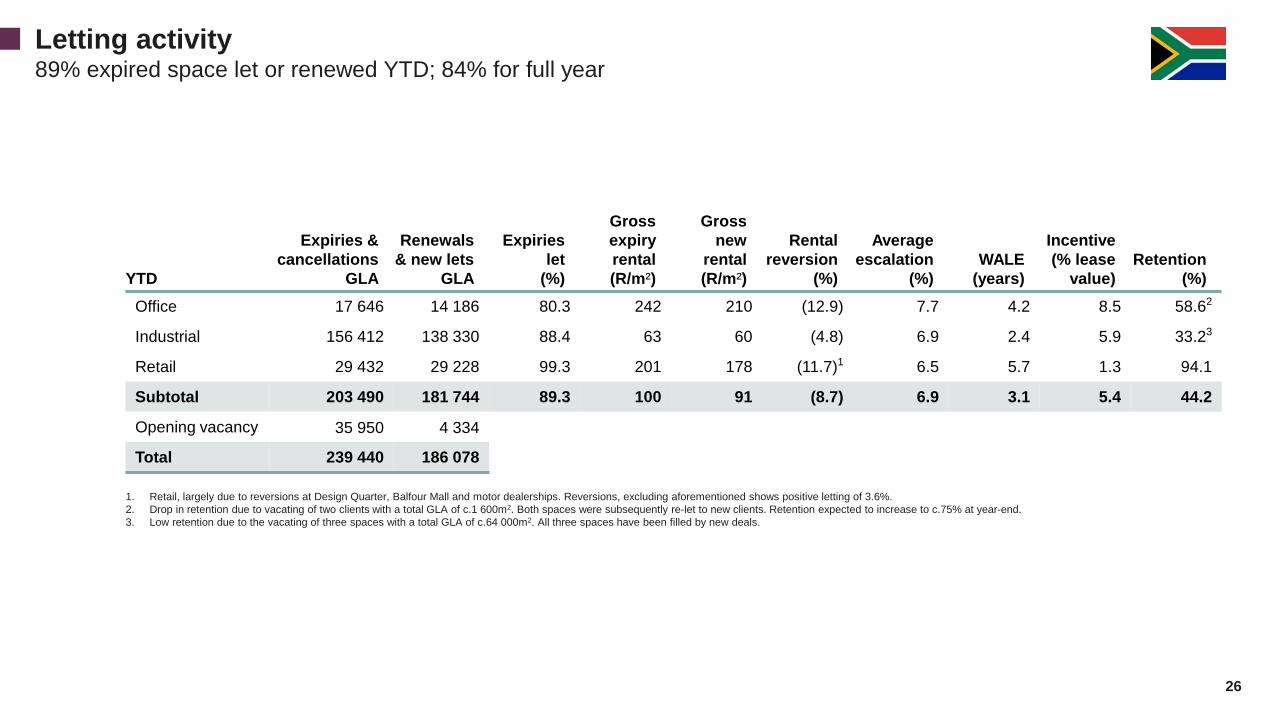

1. Retail, largely due to reversions at Design Quarter, Balfour Mall and motor dealerships. Reversions, excluding aforementioned shows positive letting of 3.6%.2. Drop in retention due to vacating of two clients with a total GLA of c.1 600m2. Both spaces were subsequently re-let to new clients. Retention expected to increase to c.75% at year-end.3. Low retention due to the vacating of three spaces with a total GLA of c.64 000m2. All three spaces have been filled by new deals.

Letting activity89% expired space let or renewed YTD; 84% for full year

YTD

Expiries & cancellations

GLA

Renewals& new lets

GLA

Expiries let

(%)

Gross expiry rental(R/m²)

Gross new

rental(R/m²)

Rental reversion

(%)

Average escalation

(%)WALE

(years)

Incentive(% lease

value)Retention

(%)Office 17 646 14 186 80.3 242 210 (12.9) 7.7 4.2 8.5 58.62

Industrial 156 412 138 330 88.4 63 60 (4.8) 6.9 2.4 5.9 33.23

Retail 29 432 29 228 99.3 201 178 (11.7)1 6.5 5.7 1.3 94.1

Subtotal 203 490 181 744 89.3 100 91 (8.7) 6.9 3.1 5.4 44.2

Opening vacancy 35 950 4 334

Total 239 440 186 078

27

Carrying amount

31 March 2019(Rm)

Revaluation and straight

lining(Rm)

Other capital

movements(Rm)

Directors’ valuation

30 Sep2019(Rm)

Totalchange

(%)

Revaluation and straight

lining(%)

Forward yield

(%)

Prior year yield

(%)Office 6 243.4 4.1 49.3 6 296.8 0.9% 0.1% 9.8% 9.4%Industrial 3 572.0 (0.7) 40.7 3 612.0 1.1% 0.0% 9.4% 9.5%Retail 6 653.5 43.8 66.1 6 763.4 1.7% 0.6% 8.4% 8.4%Total base 16 468.9 47.2 156.1 16 672.2 1.2% 0.3% 9.0% 9.0%Acquisitions - - 52.3 52.3 - - 4.4% 0.0%Held for sale 815.3 (52.3) (204.1) 558.8 (31.5%) (9.4%) 10.5% 8.8%Total portfolio 17 284.2 (5.1) 4.3 17 283.3 0.0% 0.0% 9.1% 9.0%

Property valuationsRealistic forward yield of 9.1%

27

Notes: • Directors’ valuation performed on total portfolio - properties revalued if significant changes in forecast net property income• Cap rates remained stable since year end• Net property income assumptions used are realistic and reflect the challenging environment• Acquisitions refers to 1 small property purchased in the current period

PROJECTS

29Existing

Re-positioning of offices• 96% of customers (office tenants, office clientele and retail customers)

utilise the basement parking• Cradock Avenue access provides thoroughfare for taxi commuters

however, commuters not spending time in the Firs – not our target market therefore negatively impacting first impressions of office lobby

• Plan to close off access to Cradock Avenue – reposition entranceof the offices

• Create sense of arrival in basement and improve reception area

ProjectsThe Firs

What do we expect from this upgrade?• Recognised as premier office space in Rosebank• Command higher than average market rents in Rosebank• Attract users that will remain with us longer than anticipated

- as a result of on-site amenities within walking distance to office space

The Firs• A Rosebank landmark – mixed-use precinct• Phase 1 retail refurbishment – well on its way to being established

as a food destination• Offices generate significant interest for niched office users• Positioning as “Where business-people meet and eat”

Proposed

29

30

• Work in progress for some time – 3-5 years• Has all the location and target market requirements of a

regional mall – IPF has not been able to take full advantage of positioning as a result of changing market dynamics and delays with Rea Vaya (impacting access)

• Have a better understanding of target market – where they come from, catchment area, what customers want

• Positioning mall to meet their needs

ProjectsBalfour Mall

30Existing

Proposed

What will this achieve? • Be the Mall of the people – safe and ‘the place’ to hang out

Acquisition of Highlands Mall - assists in positioning

Allow free flow of feet from Louis Botha Avenue (current taxi rank), general vehicular traffic, and huge volume of pedestrians

Income of Highlands Mall is made up of a complex retail mix – mainly informal and not IPF’s target market

Introduce exciting food and entertainment complex on parking deck with mechanical access from ground floor

Planned repositioning and reconfiguration – aim to retain income but lose a fair portion of current GLA

Community initiative – converting a portion of Standard Bank space into a study center for school children

31

4 Sandown Valley Crescent

ProjectsOther

31

Fleurdal Mall Phase 3

• Extension unveiled on 1 August – bigger, better shopping experience

• Added 6 000m² – increasing size of mall from 24 000m² to 30 000m²

• Launch received significant digital media exposure and featured in print publications

• Presented a brand identity – better access to offices• Improve visibility along Sandown Valley Crescent – give a better sense of arrival

Site used to stress test several client service initiatives – R&D department for office portfolio• Sense of arrival• Basement identity• High tech• Restaurant• Introducing meeting rooms and collaboration space on the ground floor for all tenants in property

CAPITAL EXPENDITURE AND SUSTAINABILITY

33

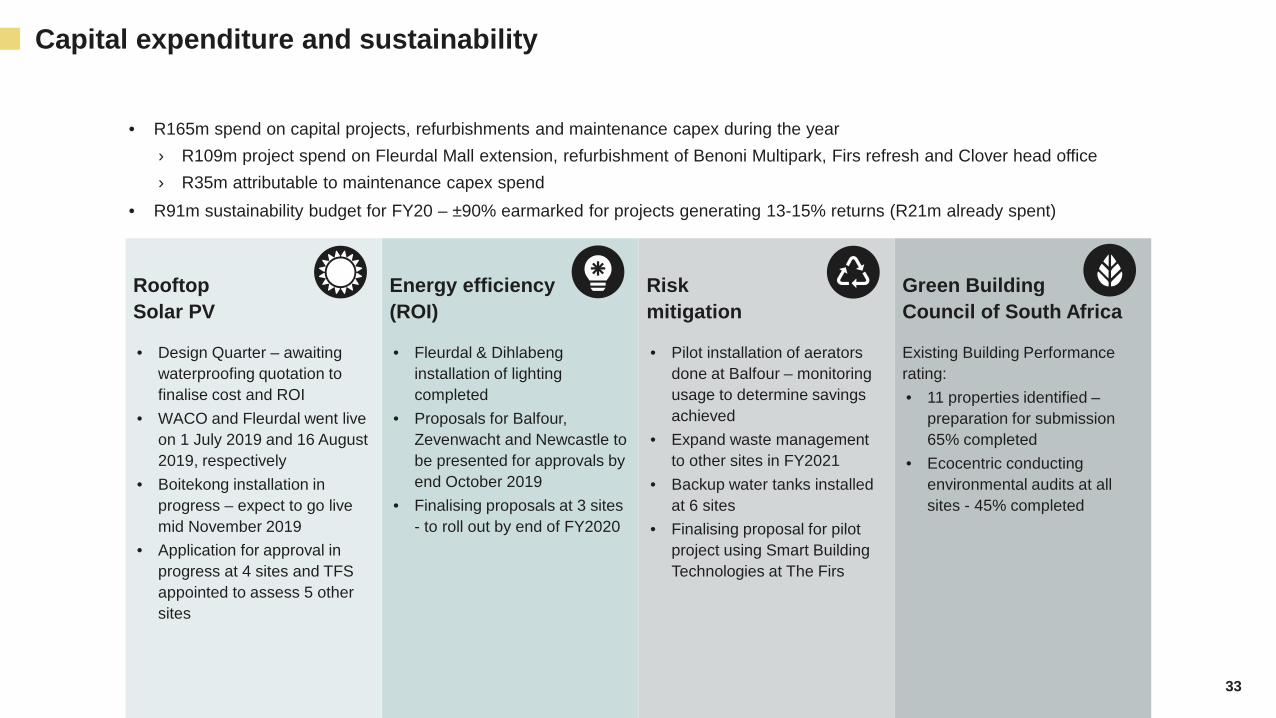

Capital expenditure and sustainability

RooftopSolar PV

• Design Quarter – awaiting waterproofing quotation to finalise cost and ROI

• WACO and Fleurdal went live on 1 July 2019 and 16 August 2019, respectively

• Boitekong installation in progress – expect to go live mid November 2019

• Application for approval in progress at 4 sites and TFS appointed to assess 5 other sites

Energy efficiency(ROI)

• Fleurdal & Dihlabeng installation of lighting completed

• Proposals for Balfour, Zevenwacht and Newcastle to be presented for approvals by end October 2019

• Finalising proposals at 3 sites - to roll out by end of FY2020

Riskmitigation

• Pilot installation of aerators done at Balfour – monitoring usage to determine savings achieved

• Expand waste managementto other sites in FY2021

• Backup water tanks installed at 6 sites

• Finalising proposal for pilot project using Smart Building Technologies at The Firs

Green BuildingCouncil of South Africa

Existing Building Performance rating:• 11 properties identified –

preparation for submission 65% completed

• Ecocentric conducting environmental audits at all sites - 45% completed

• R165m spend on capital projects, refurbishments and maintenance capex during the year› R109m project spend on Fleurdal Mall extension, refurbishment of Benoni Multipark, Firs refresh and Clover head office› R35m attributable to maintenance capex spend

• R91m sustainability budget for FY20 – ±90% earmarked for projects generating 13-15% returns (R21m already spent)

SA INVESTMENTS

35

Izandla

SA investments

• There has been no further investment by IPF intothe empowerment vehicle during the current period

• The shareholder loan granted to Izandla in FY19 to supportdevelopment of a client facility is likely to be refinancedby external funds before the end of the financial year

• Exited minority interest

› Ingenuity repurchased all ING shares held by IPFat R1.08 per share, as part of a general offer to all shareholders to repurchase their shares and de-list the company from the JSE

› Selling price at 29% premium to purchase price

• The disposal is part of IPF’s focused strategy to recycle capital into assets that generate higher risk-adjusted returns

Ingenuity

35

OFFSHORE INVESTMENTS

37

Pan-European logistics portfolioPlatform gaining scale

37

€106m deployed to date• Further €21.5m invested during the period to acquire a further 8 properties

across Netherlands, France and Poland (GAV of €151m)• €106m deployed to date – €44m remaining of €150m commitment• Portfolio comprises assets to the value of c.€671m (March 2019: €516m)• 60% of investment value hedged at average rate of 1.87%• 100% of income over the next 5 years hedged at rates between R16.49 –

R23.41

Performance tracking ahead of business plan (BP)• Strong letting has been concluded at positive average reversions

across the portfolio› 80% of opening vacancy let and 100% of year-to-date expiries let

at average reversion of positive 8.2%• Occupancy level at 98.8% (March 2019: 94.9%)• WAULT improved to 4.9 years (March 2019: 4.5 years)• Investment return on initial portfolio of 11.9% in EUR (12.3% in ZAR) and capital

uplift since initial investment of 20.2% in EUR (8.2% in the current period)• Total return for H1 2020 is 20.1% and since inception is 43.7% (in EUR)

France 184 11Germany 213 10Italy 45 3Netherlands 102 9Poland 91 10Spain 36 2Total 671 45

38

Pan-European logistics portfolio – letting activity100% of expired space let YTD

38

Highlights• 80% opening vacancy let• 100% of YTD expiries let at a reversion of positive 8.2%

Expiries & cancellations

Renewals & new lets Expiries let

Gross expiry rental

Gross new rental

Rental reversion WALE

GLA GLA (%) (€/m²) (€/m²) (%) (years)Netherlands 55 597 55 597 100 50 55 10.0 3.0France 6 010 6 010 100 45 43 (3.0) 3.0Poland 37 937 37 937 100 34 36 6.7 10.0Subtotal 99 544 99 544 100 44 47 8.2 4.7 Opening vacancy 51 211 40 793Total 150 755 140 337

39

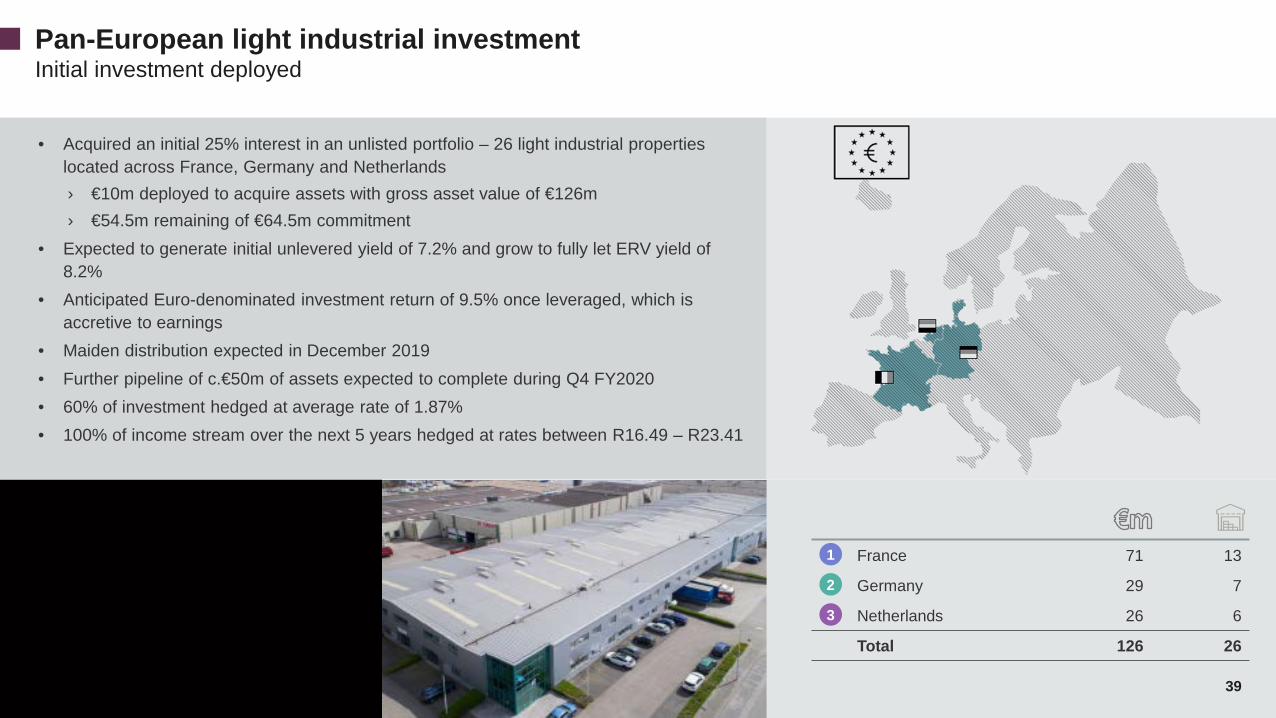

• Acquired an initial 25% interest in an unlisted portfolio – 26 light industrial properties located across France, Germany and Netherlands› €10m deployed to acquire assets with gross asset value of €126m› €54.5m remaining of €64.5m commitment

• Expected to generate initial unlevered yield of 7.2% and grow to fully let ERV yield of 8.2%

• Anticipated Euro-denominated investment return of 9.5% once leveraged, which is accretive to earnings

• Maiden distribution expected in December 2019• Further pipeline of c.€50m of assets expected to complete during Q4 FY2020• 60% of investment hedged at average rate of 1.87% • 100% of income stream over the next 5 years hedged at rates between R16.49 – R23.41

Pan-European light industrial investmentInitial investment deployed

39

France 71 13

Germany 29 7

Netherlands 26 6

Total 126 26

1

2

3

40

Key highlights• IAPF completed ASX listing in May 2019• In conjunction with the listing:

› IAPF undertook a primary capital raise of A$100m› IPF undertook a secondary capital raise and sold down 45m units

raising net proceeds of R584m • Strong demand received and offer was oversubscribed

› Final subscription price of A$1.32, above lower end of offer range• IPF interest reduced from 20.9% to 9.9%

› Further diluted to 9.0% post IAPF accelerated bookbuild offering of A$84m undertaken post interim period end

• Share price today of R16.12 (A$1.56) – 24% uplift since 31 March 2019• As expected, distribution received post ASX listing reduced by 10% on a like-

for-like basis (to align with other ASX listed REITs and best practice in Australia)

› Offset by 4% growth in FEC rate on a ZAR basis• Total return to IPF for the period was 27.4%• IAPF acquired three industrial properties during the period for purchase

consideration of A$81m at initial yield of 7.3%

IAPFASX-listing established and well received

40

Share price performance since ASX listing (A$)

95%

100%

105%

110%

115%

120%

125%

27-May 27-Jun 27-Jul 27-Aug 27-Sep 27-Oct

IAP AU A-REIT Index

19%

2%

Key portfolio metricsSep 2019 Mar 2019

No. properties 31 28

Total value of property AUD 1,180m AUD 1,063m

Value of investment R0.9bn R1.3bn

WALE (years) 4.6 4.7

Vacancy 0.1% 0.6%

NAV per unit AUD 1.33 AUD 1.30

Gearing 26.8% 38.1%

41

Further investment• IPF acquired an additional 22.5% interest in the UK Fund for £25m

increasing its shareholding to 32.5%› Total value of investment in UK Fund at £37.2m› IPF’s influence in the UK Fund has evolved to a position of joint control on

the back of the increased equity stake and shareholder rights

• 63% of investment value hedged at average rate of 2.43%• 100% of income stream over the next five years hedged at rates

between R18.52 and R26.06

Performance• 40% of opening vacancy let and no expiries in the current period• Expected to generate a post-tax income return of c.5% and total return of

c.10% p.a. in GBP

Acquisition activity• In September 2019, the UK Fund acquired a portfolio of 3 freehold retail

warehouse properties valued at £14.7m at net initial yield of 7%› Value on this portfolio can be unlocked by undertaking a conversion

to light industrial

UK FundStrategic investment and provides optionality

Key portfolio metrics

411Increase in vacancy due to tenant insolvency in one asset

UK portfolio Sep 2019 Mar 2019

Total value of property £254.1m £233.8m

Value of investment R721m R680m

Historical income return p.a. 5.4% 5.4%

WALE (years) 9.9 11.7

GLA (m²) 100 840 89 520

Vacancy 3.8%1 2.2%

Number of properties 13 10

9CAPITAL ALLOCATION

43

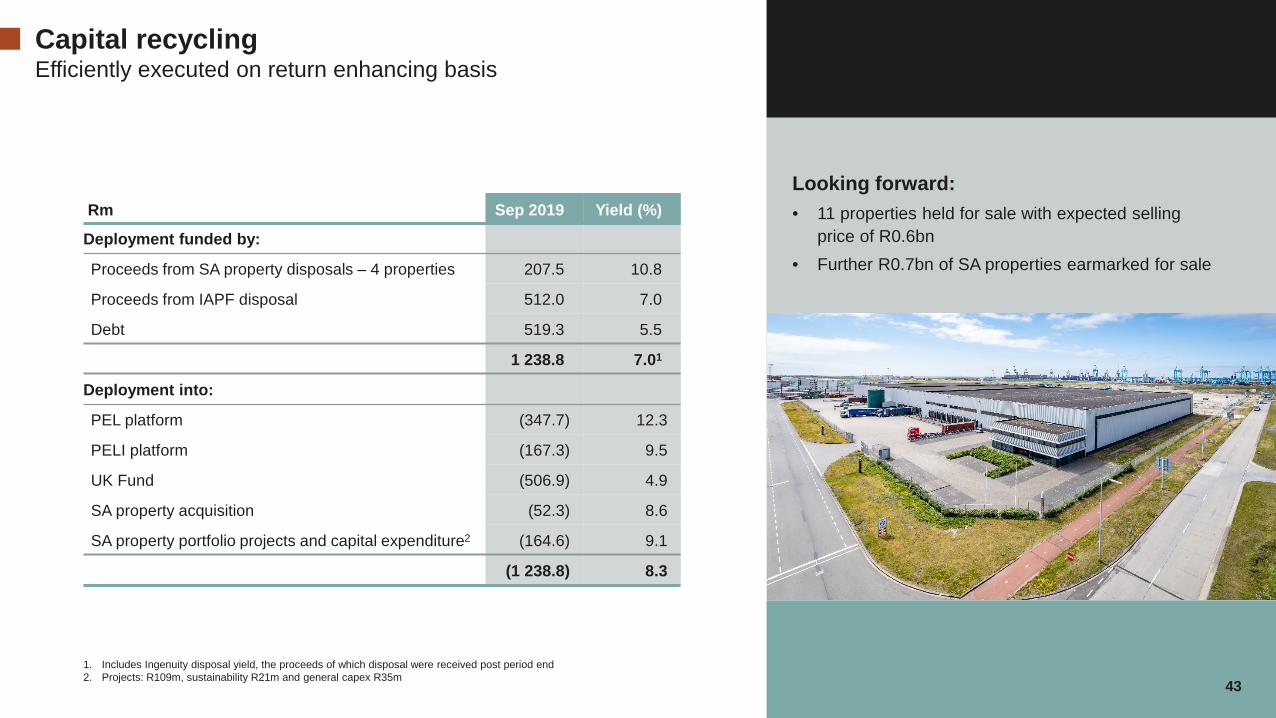

Capital recyclingEfficiently executed on return enhancing basis

43

Rm Sep 2019 Yield (%)

Deployment funded by:

Proceeds from SA property disposals – 4 properties 207.5 10.8

Proceeds from IAPF disposal 512.0 7.0

Debt 519.3 5.5

1 238.8 7.01

Deployment into:

PEL platform (347.7) 12.3

PELI platform (167.3) 9.5

UK Fund (506.9) 4.9

SA property acquisition (52.3) 8.6

SA property portfolio projects and capital expenditure2 (164.6) 9.1

(1 238.8) 8.3

Looking forward:• 11 properties held for sale with expected selling

price of R0.6bn• Further R0.7bn of SA properties earmarked for sale

1. Includes Ingenuity disposal yield, the proceeds of which disposal were received post period end2. Projects: R109m, sustainability R21m and general capex R35m

10LOOKING AHEAD

45

Focus on navigating the SA portfolio through the economic slow down…• Continue repositioning the portfolio

› Support performing assets and sell underperforming ones› Focus on property fundamentals ahead of anything else

• Proactive asset management› Extract value from existing assets› Anticipate and mitigate leasing risk› Monitoring of arrears and continual client engagement to manage bad debts› Guerilla leasing tactics› Timing of capex

• Investing in customer relationship management

• Continue to explore opportunistic M&A activity

… with further deployment into offshore platforms where growth is emerging• Continue to support and grow platforms

• Seek to increase offshore exposure beyond 20%

• Provides optionality – intention to gain control over time

• Continued deployment into Pan-European platforms

H2 2020 prioritiesWhat to expect over the next 6 months

45

Focus on client experience • 4 Sandown Valley Crescent• The Firs• Balfour• Zevenwacht

45

46

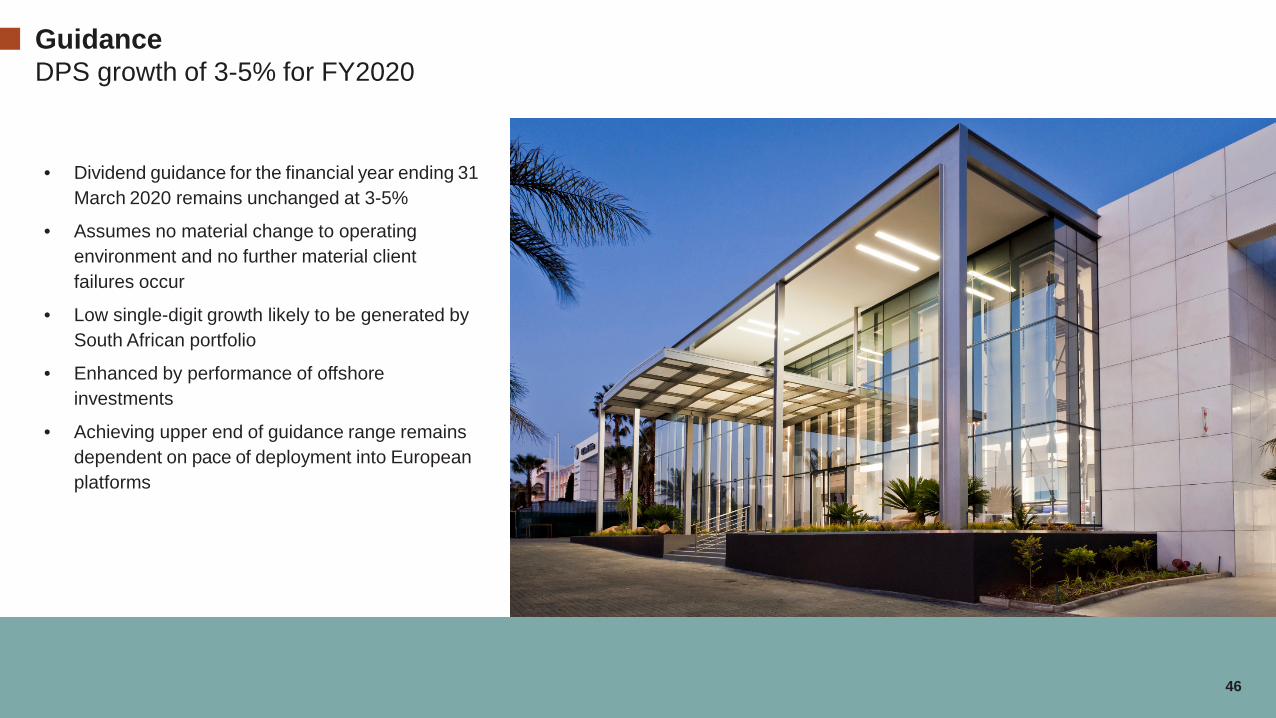

• Dividend guidance for the financial year ending 31March 2020 remains unchanged at 3-5%

• Assumes no material change to operating environment and no further material client failures occur

• Low single-digit growth likely to be generated by South African portfolio

• Enhanced by performance of offshore investments

• Achieving upper end of guidance range remainsdependent on pace of deployment into Europeanplatforms

GuidanceDPS growth of 3-5% for FY2020

46

47

• Good performance in H1 2020

• South Africa – excellent letting statistics have been marred by an increase in bad debts

• Positive capital allocation in terms of deployment and disposal activity improving the quality of the balance sheet

• PEL platform continues to drive distribution growth

• Guidance remains unchanged

Conclusion

47

11ANNEXURES

49

AppendixStrategic pillars Deliver sustainable long-term returns by…

…ensuring best of breed assets

…focusing onclient experience

as a key differentiator

…unlockingthe potential of space

Revenue securityand growth

Client serviceexcellence

Value add asset management andcapital allocation

Cost efficiencyand systemoptimisation

• Early engagement• Solutions based• Proactive asset

management

• Delivering an out-of-the-ordinary experience

• Differentiating IPF in a commoditised environment

• Understanding of and delivering on client needs

• Best of breed assets• Positioning the portfolio

for growth• Active capital recycling• Proactive balance sheet

management• Diversified investment

base• Maximise returns on a

long-term risk-adjusted basis

• Speed and agility• Margin preservation• Controllable costs tightly

managed

49

50

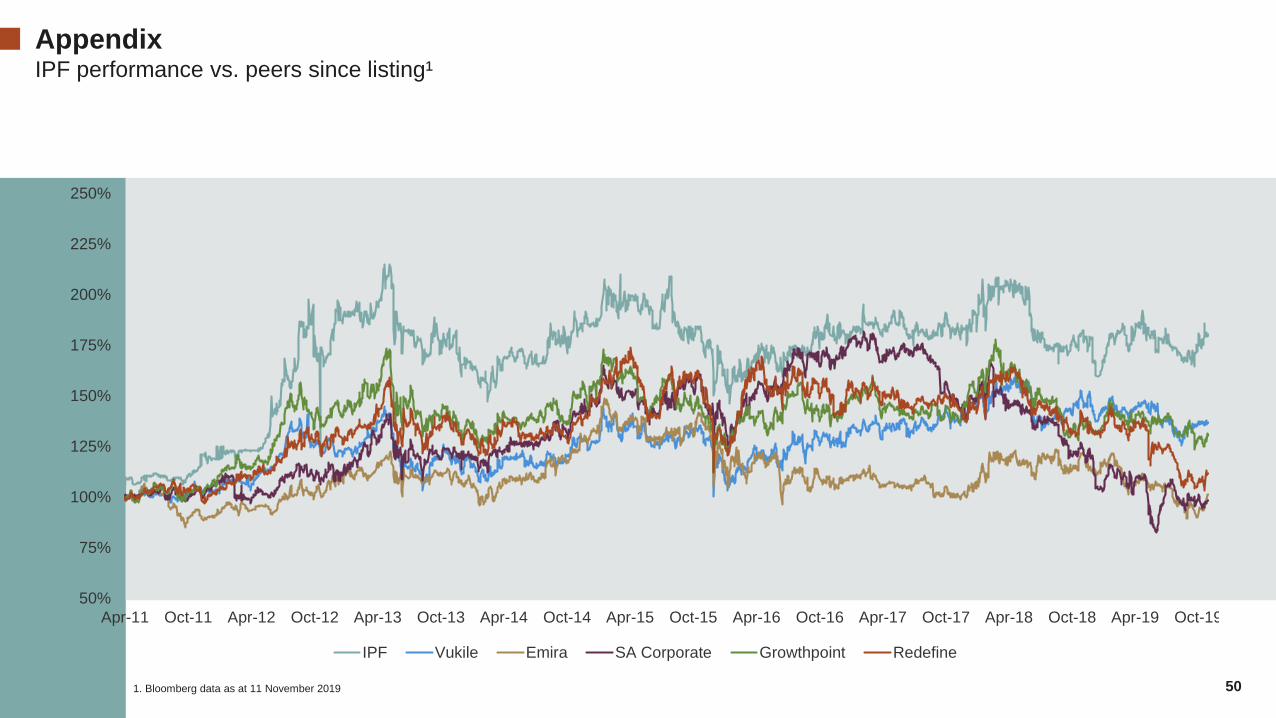

Appendix IPF performance vs. peers since listing¹

1. Bloomberg data as at 11 November 2019

50%

75%

100%

125%

150%

175%

200%

225%

250%

Apr-11 Oct-11 Apr-12 Oct-12 Apr-13 Oct-13 Apr-14 Oct-14 Apr-15 Oct-15 Apr-16 Oct-16 Apr-17 Oct-17 Apr-18 Oct-18 Apr-19 Oct-19

IPF Vukile Emira SA Corporate Growthpoint Redefine

51Source: Bloomberg as at 22 July 2019 and 1 November 2019; Rebosis removed from graph as it distorts it with discount of 40.5% in April 2019Note: Market capitalisation shown for shares with 2 classes is the combined market capitalisation (i.e. Dipula, Fortress, Gemgrow and Rebosis)

Sector forward yieldsTrend of negative sentiment in the market continues – yields slightly pushed out since year end

IAPF

Atta

cq

Equi

tes

Fortr

ess

A

Res

ilient

Stor

-Age

Libe

rty 2

Deg

rees

Gro

wth

poin

t

Vuki

le

Exem

plar

IPF

Dip

ula

A

Tran

scen

d

Hyp

rop

Fairv

est

Safa

ri

Arro

whe

ad A

Spea

r

Oct

odec

SA C

orpo

rate

Emira

Red

efin

e

Hos

pita

lity

Tow

er

Fortr

ess

B

Indl

upla

ce

Arro

whe

ad B

Text

on

Dip

ula

B

Acce

lera

te

Del

ta

Gearing 27% 36% 27% 32% 27% 25% 16% 36% 39% 36% 37% 42% 43% 35% 27% 13% 41% 38% 38% 37% 36% 44% 16% 34% 32% 30% 41% 47% 42% 39% 44%

Market cap (R'bn) 9.9 9.7 11.5 34.5 26.6 5.9 6.3 66.9 18.3 2.9 11.3 3.7 0.9 15.1 1.9 1.4 5.1 1.9 4.2 7.9 6.5 43.9 4.4 1.7 34.5 1.5 5.1 1.1 3.7 1.9 0.7

5.3% 7.

0% 7.4%

7.6%

8.6%

8.3%

8.9% 10

.1%

10.6

%

10.6

%

10.4

%

11.6

%

11.4

%

11.4

%

12.9

%

12.5

%

11.8

%

11.9

%

13.3

%

13.3

%

12.8

%

14.9

%

15.8

%

15.4

%

17.5

%

18.9

%

21.5

%

19.3

% 24.7

%

28.8

%

55.8

%

5.7%

6.6% 7.3%

7.4%

8.7%

8.4%

8.9% 9.5%

10.0

%

10.0

%

9.9% 10.6

%

12.8

%

11.3

%

12.5

%

12.3

%

12.0

%

9.6% 10

.8%

12.6

%

11.9

%

11.7

%

11.9

% 17.1

%

14.2

%

18.4

%

15.3

%

18.1

%

14.1

%

14.9

%

26.4

%

0%

20%

40%

60%

IAPF

Atta

cq

Equi

tes

Fortr

ess

A

Res

ilient

Stor

-Age

Libe

rty 2

Deg

rees

Gro

wth

poin

t

Vuki

le

Exem

plar IPF

Dip

ula

A

Tran

scen

d

Hyp

rop

Fairv

est

Safa

ri

Arro

whe

ad A

Spea

r

Oct

odec

SA C

orpo

rate

Emira

Red

efin

e

Hos

pita

lity

Tow

er

Fortr

ess

B

Indl

upla

ce

Arro

whe

ad B

Text

on

Dip

ula

B

Acce

lera

te

Del

ta

Friday, 1 November 2019 Monday, 22 July 2019Friday, 1 November 2019 Monday, 22 July 2019

10.6%10.2%

52Source: Bloomberg as at 11 October 2019

Price/NAVInvestec relative to peers

1.23

1.23

1.21

1.08

1.07

1.04

0.97

0.95

0.89

0.87

0.84

0.83

0.80

0.75

0.74

0.73

0.71

0.66

0.63

0.61

0.57

0.56

0.56

0.54

0.46

0.46

0.46

0.46

0.44

0.40

0.19

0.09

0.03

1.18

1.25

1.12

1.06

1.03

1.24

0.61

0.96

0.96

0.88

0.86

0.92

0.85

0.89

0.87

0.72

0.60

0.78

0.68

0.73

0.57

0.64

0.52

0.91

0.53

0.41

0.75

0.59

0.45

0.63

0.42

0.20

0.06

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Stor

-Age

Equi

tes

IAPF

Dip

ula

A

Arro

whe

ad A

Fortr

ess

A

Res

ilient

Vuki

le

Gro

wth

poin

t

Fairv

est

IPF

Exem

plar

Fortr

ess

B

Spea

r

Red

efin

e

Libe

rty 2

Deg

rees

Tran

scen

d

Emira

SA C

orpo

rate

Hyp

rop

Atta

cq

Oct

odec

Safa

ri

Tow

er

Hos

pita

lity

Text

on

Reb

osis

A

Arro

whe

ad B

Indl

upla

ce

Dip

ula

B

Acce

lera

te

Del

ta

Reb

osis

B

Friday, 11 October 2019 Monday, 22 July 2019

Discount increased to 16% to NAV

53

Portfolio composition

40%

38%

22%

RetailOfficeIndustrial

Sectoral spread by revenue

42%

36%

22%

RetailOfficeIndustrial

Sectoral spread by asset value

53

35%

21%

44%

RetailOfficeIndustrial

Sectoral spread by GLA

54

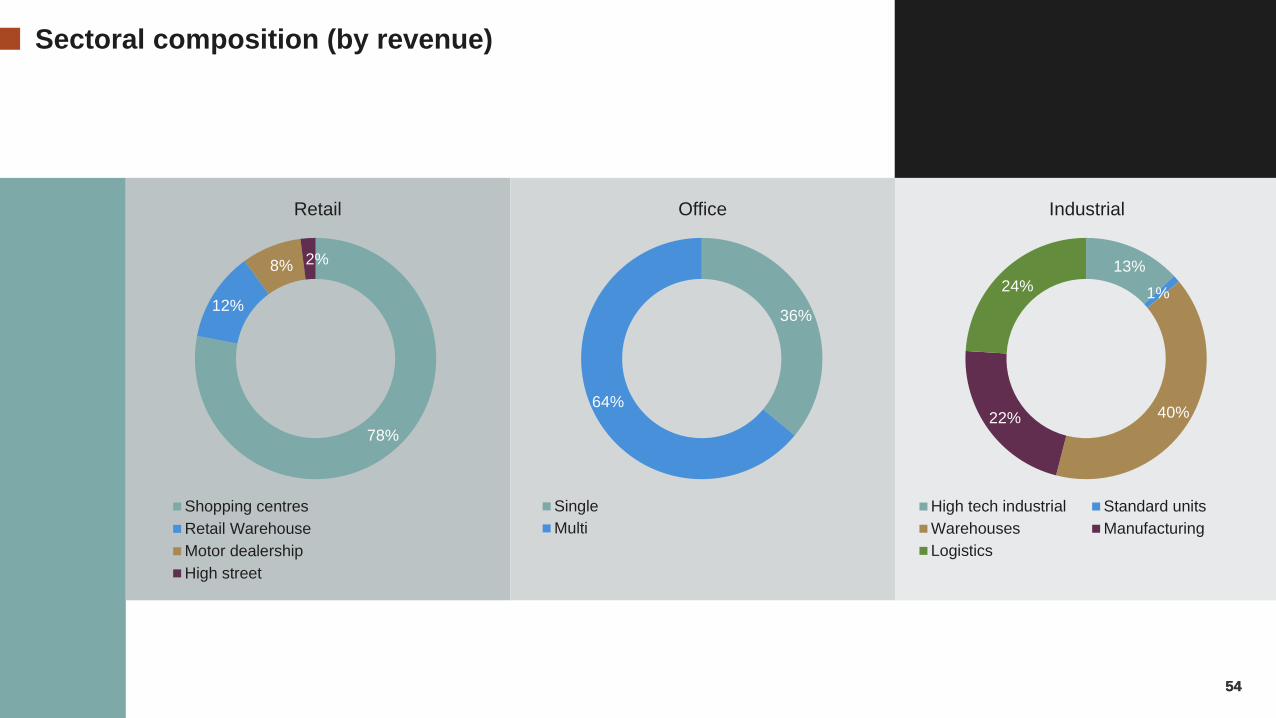

Sectoral composition (by revenue)

78%

12%

8% 2%

Shopping centresRetail WarehouseMotor dealershipHigh street

Retail

36%

64%

SingleMulti

Office

54

13%1%

40%22%

24%

High tech industrial Standard unitsWarehouses ManufacturingLogistics

Industrial

55

2%

5%

9%8%

14%

4% 4%

1%

6%7%

5%

8%6%

10%12%

10%

17%16%

23%

34%

0%

10%

20%

30%

40%

2020 2021¹ 2022 2023 April 2023 Onwards

Office Industrial Retail Portfolio

Lease expiry (by revenue)89% of YTD expiries already let and 89% for full year

56

• Average density of R2 370/m² (excluding Design Quarter and Balfour)• Amongst top 3 in chosen peer group – trading density growth of 2%

including Design Quarter and Balfour Mall (3.5% excluding) • Peer group trading density growth ranged from 2.8% (Vukile) to 0.8%

(Hyprop). Redefine and Growthpoint growing at 1.6% and 1.9% respectively

RetailTrading performance

• Positive growth in a tough environment – only Balfour Mall and Design Quarter showing negative growth

• Balfour trade expected to improve with Rea Vaya and precinct development plan

• Design Quarter – potential redevelopment plan in place• Dihlabeng flat growth – strategy to refresh tenant mix. Excluding

vacant stores, trade of remaining stores in line with past performance

• Long term growth expected to be in line with long term wage growth (4%-4.5%)

• Centers resilient in a difficult market, holding onto market share• Newcastle taking market share back from nearby competitors as a

result of improved tenant mix

7.9% 6.1% 5.4% 5.1%

(0.2%)(3.4%) (4.4%)

Fleurdal Kriel Zevenwacht Newcastle Dihlabeng Design Quarter Balfour

56

Retail – Average annual turnover growth (%)

5.8% 6.0%5.2% 5.3% 5.0%

4.3% 4.1% 4.1% 4.5% 4.4% 4.7% 4.7%

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

Average like-for like turnover excluding Design Quarter and Balfour Mall (%)

1,630

2,370

1,7702,140 2,290

2,6702,200 2,310 2,340 2,370

Balfour BoitekongMall

DesignQuarter

Dihlabeng Fleurdal Great NorthRoad Plaza

Kriel Musina Newcastle Zevenwacht

Average trading density by centre (R/m²)

2019 2020

57

Top 10 tenants

Tenant name %Investec 5.4

Cliffe Dekker Hofmeyr 4.7

Woolworths 2.8

Innovation 2.4

Nedbank Group 1.9

Fluxmans Attorneys 1.8

Samsung Electronics Co. Ltd 1.4

Clover 1.2

Bigen Africa 1.1

ELB Engineering 1.1

Tenant name %Altron Ltd 2.2

Kevro Trading (Pty) Ltd 1.7

RT Group (Pty) Ltd 1.5

General Electric Ltd 1.4

Adcock Ingram Healthcare 1.1

Tiger Brands Ltd 0.9

Martin & Martin (Pty) Ltd 0.9

Waco International 0.9

AGCO Corporation 0.7

Naspers Limited 0.5

Tenant name %Massmart 5.8

Shoprite Checkers Group 3.0

Bidvest 2.1

Edcon Group 1.7

Mr Price Group 1.6

Foschini Group 1.4

Pick 'n Pay Group 1.3

Woolworths 1.2

Pepkor Group 1.0

Zenth Park Trading 0.8

OfficeGross revenue% of total portfolio

IndustrialGross revenue% of total portfolio

RetailGross revenue% of total portfolio

58

The information contained herein is for information purposes only and readers should not rely on such information as advice in relation to a specific issuewithout taking financial, banking, investment or professional advice. Although information has been obtained from sources believed to be reliable, InvestecProperty Fund Limited (Reg. No.2008/011366/06) and or any affiliates (collectively “Investec Property”), do not warrant its completeness or accuracy. Opinionsand estimates represent Investec’s view at the time of going to print and are subject to change without notice.

Past performance is not indicative of future returns. The information contained herein does not constitute an offer or solicitation of investment, banking orfinancial services by Investec Property. Neither Investec Property nor Investec Bank Limited shall be held liable in respect of any claim, damages or loss ofwhatever nature arising in connection with such information. Investec Property accepts no liability for any loss or damage of whatsoever nature including butnot limited to loss of profits, goodwill or any type of financial or other pecuniary or direct or special indirect or consequential loss however arising, whether innegligence or for breach of contract or other duty as a result of use of or reliance on the information contained in this document whether authorised or not.

This document/publication may not be reproduced in whole or in part or copies distributed without the prior written consent of Investec Property.

Disclaimer

![[ SHEESHAM WOOD FURNITURE ] - MakeShop · 02 SHEESHAM WOOD FURNITURE 03 IAPF-305 size :W60D30H95 price: 38,000+TAX IAPF-306 size :W90D30H70 price: 42,000+TAX PRAH1053 size :W73D43H50](https://img.dokumen.tips/doc/110x75/605a686faa18fd0c01437c2b/-sheesham-wood-furniture-makeshop-02-sheesham-wood-furniture-03-iapf-305-size.jpg)