Embed Size (px)

Citation preview

Introduction to OHADA law and latest update on OHADA company and security law

Yves Baratte Taous Mabed

8 January 2015

2 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

Introduction to OHADA Law

3 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

OHADA: What is it?

OHADA is the acronym for Organisation pour l'Harmonisation en Afrique du Droit des Affaires (Organisation for the Harmonisation of Business Law in Africa)

Before OHADA, business law in the OHADA Member States was governed by outdated post-colonial codes

The OHADA treaty (the “Treaty”) was adopted on 17 October 1993. The objective was to implement a modern harmonised legal framework for business law in order to address legal and judicial uncertainty by:

Creating a uniform and modern business law for Member States

Promoting arbitration as a conflict resolution process

Improving the training and the expertise of judges

The Treaty was revised in 2008. It is today one of the most advanced harmonised legal systems and prevails over national law

Doc ID: L_LIVE_EMEA2:7298229v1 © Simmons & Simmons 2009

OHADA Member States

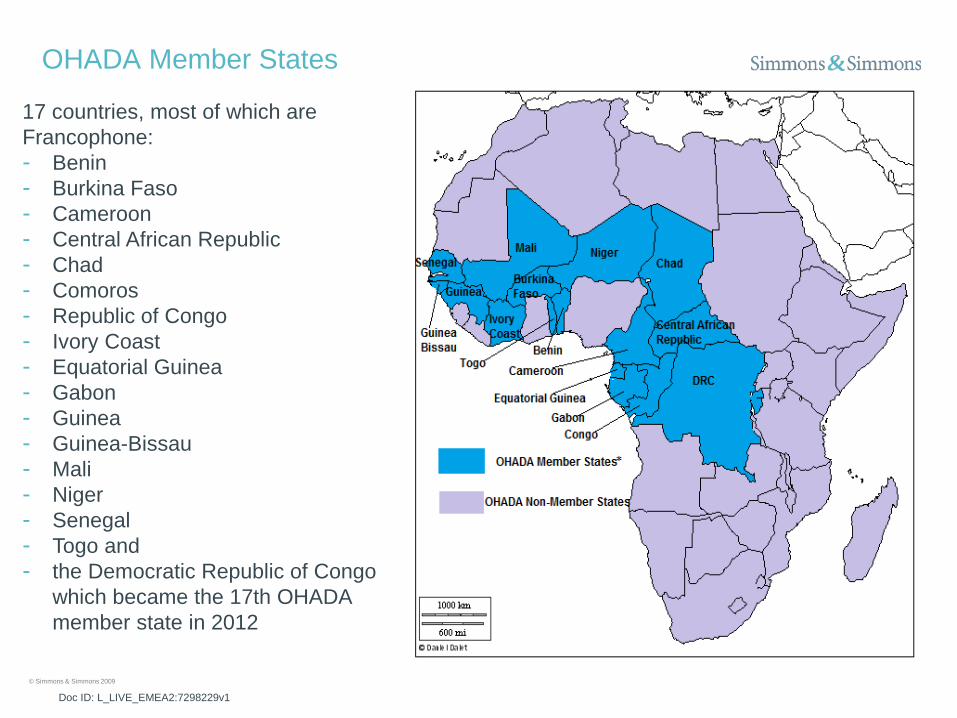

17 countries, most of which are Francophone: - Benin - Burkina Faso - Cameroon - Central African Republic - Chad - Comoros - Republic of Congo - Ivory Coast - Equatorial Guinea - Gabon - Guinea - Guinea-Bissau - Mali - Niger - Senegal - Togo and - the Democratic Republic of Congo

which became the 17th OHADA member state in 2012

5 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

OHADA: How does it work?

OHADA promotes both domestic and foreign investment, through consistency of regulation and interpretation

A treaty and 9 Uniform Acts have created modern business law governing: Insolvency (1998) Collective proceedings for the wiping up of debts (1999) Arbitration (1999) Accountancy (2001-2002) Contracts for the carriage of goods by road (2004) Cooperative companies (2011) General commercial law (1998, revised in 2011) Security interests (1998, revised in 2011) Company law (1998, revised in 2014)

Future uniformity envisaged in areas such as labor, contract, competition, intellectual property, banking

Exclusively business related and based on a modernised French legal model

6 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

The governing bodies of the OHADA

A legislative body: the Council of Ministers Legislative function: approval of the annual business law harmonisation

program and of the Uniform Acts (instead of the legislative bodies of the Member States)

Legal and administrative function: approval of the budgets of the CCJA and of the Permanent Secretariat, nomination of the CCJA Judges, approval of the OHADA annual accounts, approval of implementing decrees, etc.

An executive body: the Permanent Secretariat Proposes to the Council of Ministers’ Chairman an agenda for the Council and the

annual business law harmonisation Drafts the Uniform Acts, present them to the Member States for examination and

request the CCJA’s opinion before their approval Elaborates the final drafts of the Uniform Acts and proposes them for the agenda

of the Council of Ministers Publishes the Uniform Acts in the OHADA Official Journal Proposes candidates for the nomination of the CCJA judges Supervises the ERSUMA (Ecole Régionale Supérieure de la Magistrature de

l'OHADA), the OHADA regional training centre for judges

7 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

The judicial body of the OHADA: the CCJA (Cour Commune de Justice et d'Arbitrage), the common court of justice and arbitration

Based in Abidjan (Ivory Coast) 9 Judges nominated by the Council of Ministers for a non-renewable seven-year

period Written and contradictory procedure Its judicial decisions are directly binding within the Member States, without any

transposition or exequatur Has jurisdiction over final decisions rendered at last instance by national courts Provides opinions for the uniform interpretation and application of the Treaty, its

implementation decrees and the Uniform Acts Arbitration Centre: without settling the dispute itself, it organises and controls the

arbitral proceedings and nominates or confirms the arbitrators

8 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

OHADA: Limitations

Conflicts of laws: where disputes involve OHADA rules and domestic laws, identifying the competent court is not always straightforward and recourse to the CCJA is often only possible after having gone through the national appeal court systems

A full business/investment law is still being developed

OHADA is limited to West and Central, mainly francophone, Africa (for now)

Civil Law based: may slow its spread to Common Law jurisdictions

9 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

The Revised OHADA Uniform Act on Companies

10 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

An OHADA corporate law mainly inspired by French law

Following the independence of African countries, very few of them had a

national legal system. Some of them continued to use the corporate law of the colonial state (Ivory Coast, Niger, Gabon, …), some others passed their own corporate law (Senegal, Mali, Madagascar, …)

The OHADA Uniform Act Relating to Commercial Companies and Economic Interest Group entered into force in 1998. Even if the influence of French law is preponderant, it has brought significant innovations

A Revised Uniform Act on Commercial Companies and Economic Interest Groups (the “New Uniform Act”), was adopted on 30 January 2014 and entered into force on 5 May 2014

The New Uniform Act has brought significant changes, including, in particular, the creation of the “Société par Actions Simplifiée” (SAS), which allows a greater degree of flexibility than the société anonyme (the “SA”, another form of limited liability company), notably in terms of management structure

11 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

A new form of company: the “Société par Actions Simplifiée” (SAS)

The SAS is a limited liability company, whose shareholders have an extended freedom in order to shape the company’s articles of association according to their needs

Management of the company: apart from the obligation to appoint a Chairman (Président), the management structure of the company is freely organised by the company’s articles of association

The articles of association may provide for share transfer restrictions and exclusion clauses

The SAS is authorised to issue a variety of stocks/transferable securities (preference shares, hybrid securities, etc.)

The SAS cannot offer its shares to the public

12 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

Other main innovations of the New Uniform Act (1/5)

An increased control over related party transactions:

The control over transactions between the company and one of its managers (and the transactions in which the manager could be involved), which have to be approved by the board of directors, is extended to the transactions between the company and a shareholder holding 10% or more of the share capital

The possibility to use electronic means of communication in order to convene board and shareholders’ meetings

The possibility to use telecommunications facilities in order to attend board and shareholders’ meetings (videoconference)

The possibility to delegate to the board of directors the power to determine certain terms and conditions of a share capital increase duly authorised by the shareholders

Unless otherwise stated in the articles of association, the board members no longer have the obligation to hold shares of the company

13 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

Other main innovations of the New Uniform Act (2/5)

The possibility to request the appointment of an « Administrateur provisoire » (court appointed receiver) by a judge in a situation where the shareholders or the managers hinder the normal operation of the company

Acknowledgement of the validity of shareholders’ agreements

Extended share transfer restrictions options which can be included in the articles of association:

The former Uniform Act only authorised approval clauses included in the articles of association

Three different types of restrictions are now possible: clauses barring the transfer of shares, approval rights and pre-emption clauses

These restrictions can only be applied to share transfer to third parties and cannot be applied in the event of a succession, divorce or a transfer to a family member

Transfers of shares made in violation of those provisions are null and void

Creation of a new form of abuse of the voting rights: the abuse of equality

14 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

Other main innovations of the New Uniform Act (3/5)

Possibility to create preference shares:

Companies may create shares with specific rights, including voting rights (non-voting shares, double voting rights, …), financial rights (priority dividend, non-proportional dividends, …), or special information rights (mainly used to encourage private investments)

Acknowledgement and creation of new categories of transferable securities:

SA and SAS may now issue hybrid securities and bonds (“valeurs mobilières composées”), convertible into shares (convertible bonds, bonds with share warrants, bond warrants, …). These have been created in order to enable the development of private equity in Africa (mezzanine and subordinated debt, etc.)

Possibility to distribute free shares

15 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

Other main innovations of the New Uniform Act (4/5)

Limitation of the use of branches in favour of the use of autonomous local subsidiaries

Creation of the representation office, which role is limited to a representation of the company in a foreign market (no legal personality and no management autonomy)

Simplification of the process in order to modify the articles of association of the company (a Member State may now decide that the use of a notary for the modification of the articles of association is optional)

Clarification of the nullity regime for the articles of association provisions and the corporate decisions

16 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

Other main innovations of the New Uniform Act (5/5)

Definition of the nature, terms and conditions of the contribution of professional or technical skills or services (apport en industrie) to the company in addition to cash or in kind contributions

The par value of the shares can now be freely determined

Creation of a new exception for rules relating to the offer of securities to the public: the accredited investor

Possibility to create companies with a variable share capital

17 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

How should the Revised Uniform Act changes be applied?

Updates to be made to the articles of association of existing companies

Deadline for the update: 2 years from the entry into force of the Revised Uniform Act i.e. 5 May 2016

18 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

The revised OHADA Uniform Act on security law

19 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

Revised OHADA Uniform Act on security law

• Revised OHADA Uniform Act on security law adopted on 15 December 2010 and effective on 16 May 2011

• Introduces welcome improvements and flexibility: more creditor-friendly regime

• Introduces important changes to security interests and limited changes to personal guarantees

• But still no equivalent to an English floating charge

20 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

A new, clarified general framework for pledges (1/2)

Former rules based on the dispossession of the pledged asset: costly and inefficient for some forms of pledges and useless for certain professional creditors such as credit institutions

Pledges no longer based on dispossession, but on the publicity of the pledge at the Trade and Personal Property Credit Registry (“RCCM”)

Difference between the assignment and the pledge no longer based on dispossession, but on the nature of the pledged asset: tangible (pledge: “gage”) or intangible (assignment: “nantissement”)

Simplification for professional creditors: dispossession is no longer mandatory but only a possibility for the parties

The RCCM rules were modified by the Revised Uniform Act Relating to General Commercial Law (2011) in order to simplify the registration of pledges and to reduce its cost, mostly through a computerisation of the RCCM

21 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

A new general framework for pledges (2/2)

Future assets can now be pledged

New forms of pledges explicitly acknowledged: the pledge of bank account balances, the pledge of intellectual property rights and the pledge of securities accounts

22 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

New security interests based on ownership (1/2)

Most efficient security interests since the creditor is the legal owner of the secured asset: the creditor only has to request the possession of the asset in case of default of the debtor

Three new forms of securities based on ownership:

assignment of receivables for security purposes (“cession simplifiée de créance”)

fiduciary transfer of sums of money (“transfert fiduciaire de sommes d'argent”); and

reservation of title clause (“clause de réserve de propriété”)

23 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

The creation of securities based on ownership (2/2)

Assignment of receivable for security purposes: the receivable is the secured asset, which will be transferred to the creditor in the event of a default of the debtor. Relevant for existing and future receivables and extends to its accessories. Only a credit institution may benefit from it

Fiduciary transfer of money: the secured asset is a sum of money placed in a blocked account opened in a bank in the name of the creditor. The debtor has no power on the account and the money is directly transferred to the creditor in the event of default

Retention of title clause: under the former Uniform Act, there was no specific regime governing the retention of title clause, under which the seller of an asset remains the legal owner as long as the price is not paid

24 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

Improved enforcement (1): the contractual attribution clause

Self-appropriation was prohibited under the former Uniform Act: judicial proceedings were required, either for a forced sale at a public auction or for a court-attribution of the pledged assets to the creditor

The Revised Uniform Act on Security Law allows the debtor and the creditor to agree upon a contractual attribution clause allowing the creditor to become the owner of the pledged asset, if this asset is a sum of money or if its price has an official quotation.

If the debtor is a professional debtor, the contractual attribution clause may be provided for all types of tangible assets, provided the price of the asset is determined by an independent expert

25 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

Improved enforcement (2): The security agent

In charge of the creation, registration, management and enforcement of security interests or guarantees in its own name but on behalf of all the creditors

Must be a credit institution or a financial institution

Security interests segregated from the security agent’s own assets

No modification to be filed in case of modification of the identity of the creditors, as the security interest is registered under the name of the security agent

Goes beyond French law

26 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

Yves Baratte, Partner [email protected] +33 1 53 29 17 33 Taous Mabed, Managing Associate [email protected] +33 1 53 29 17 17 Please join our next African webinar on Risk Management: Thursday 29th January 09-09:30am GMT To register please contact Alexandria Gould

27 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

Simmons’ Offices around the World

28 / L_LIVE_EMEA2:10913059v1 Doc ID : L_LIVE_EMEA2 :3199468v1 © Simmons & Simmons 2009

simmons-simmons.com elexica.com