Embed Size (px)

Citation preview

Introduction to Financial Engineering

Aashish Dhakal

Week 5: The Greek Letter

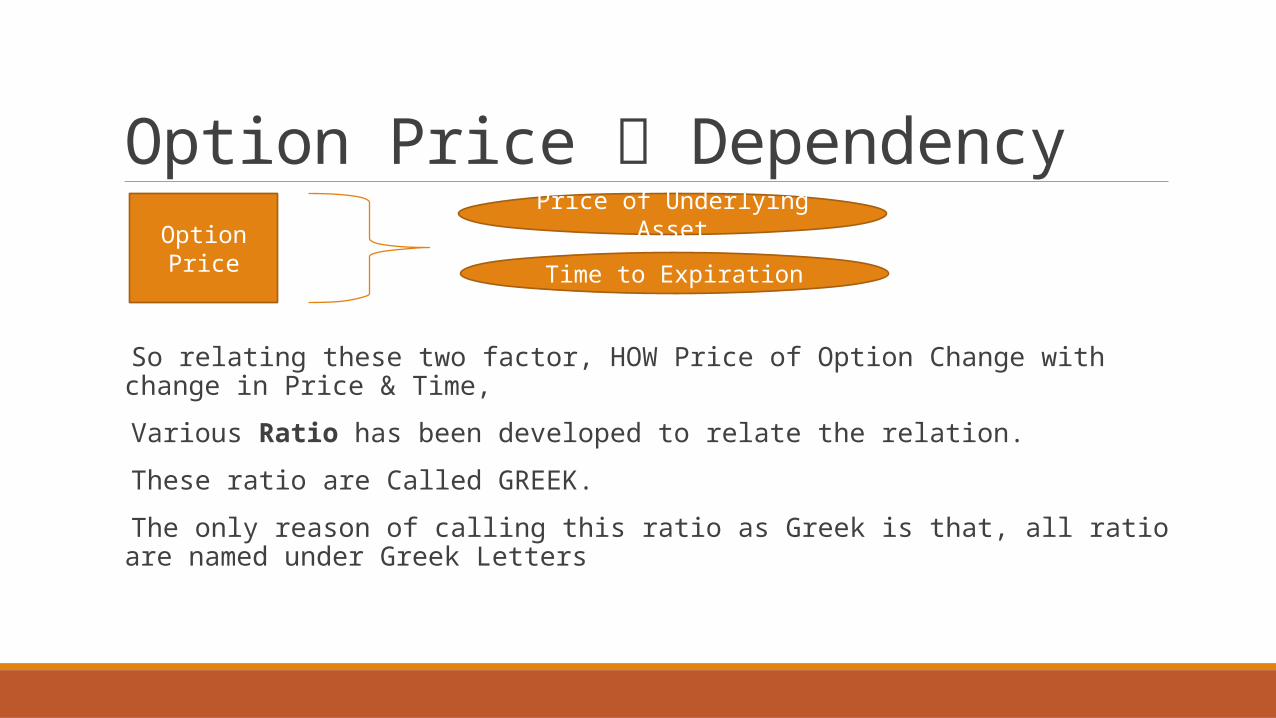

Option Price Dependency

So relating these two factor, HOW Price of Option Change with change in Price & Time,

Various Ratio has been developed to relate the relation.

These ratio are Called GREEK.

The only reason of calling this ratio as Greek is that, all ratio are named under Greek Letters

Option PricePrice of Underlying Asset

Time to Expiration

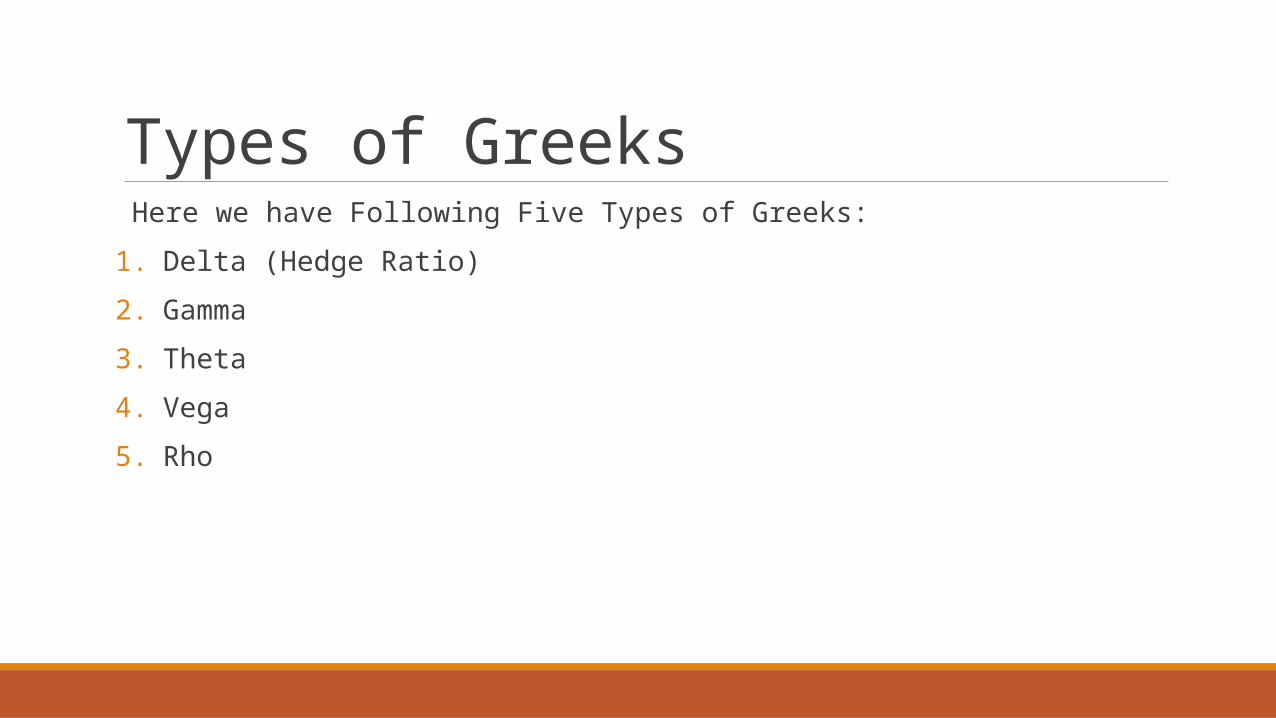

Types of Greeks Here we have Following Five Types of Greeks:

1. Delta (Hedge Ratio)

2. Gamma

3. Theta

4. Vega

5. Rho

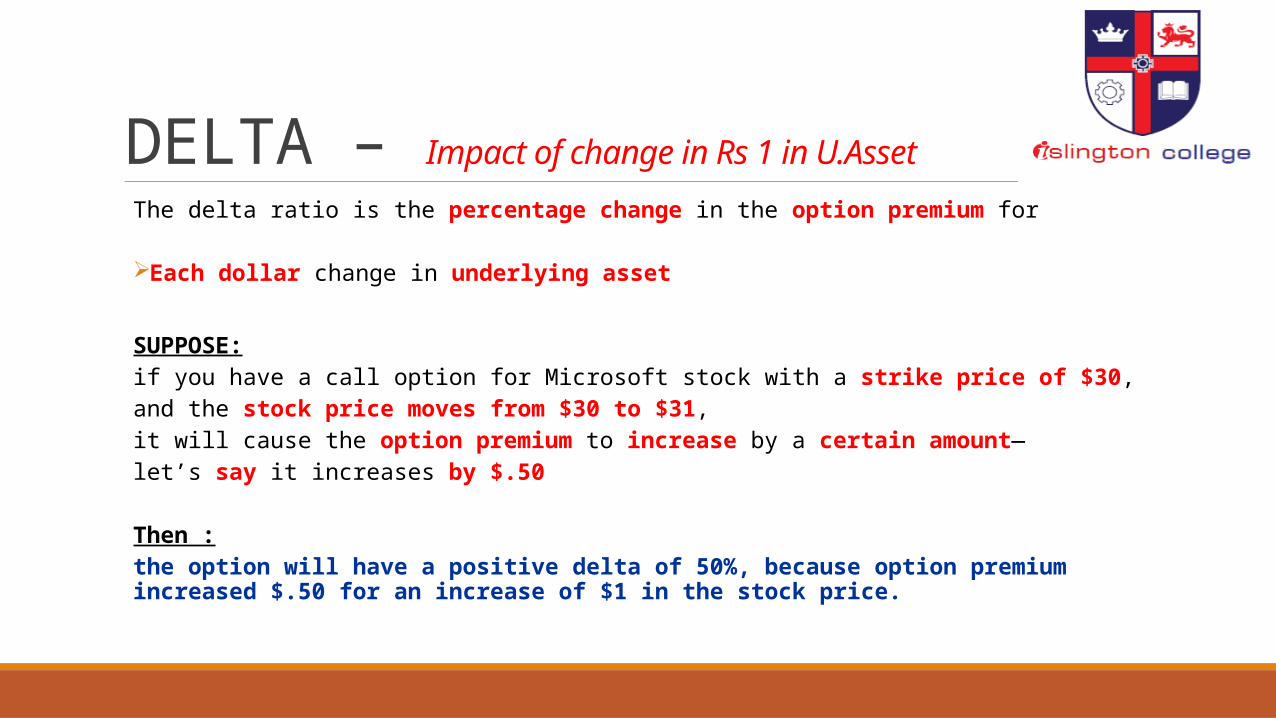

DELTA – Impact of change in Rs 1 in U.Asset

The delta ratio is the percentage change in the option premium for

Each dollar change in underlying asset

SUPPOSE:if you have a call option for Microsoft stock with a strike price of $30, and the stock price moves from $30 to $31, it will cause the option premium to increase by a certain amount—let’s say it increases by $.50

Then :the option will have a positive delta of 50%, because option premium increased $.50 for an increase of $1 in the stock price.

DELTA – Impact of change in Rs 1 in U.AssetDENOTED By WHOLE NOS:delta is often denoted by a whole number.so if an option has a 50% delta, then it will often be denoted as "50 delta“

NOTE:Put option with the same strike price will decline in price by almost the same amount, and will therefore have a negative delta.

Use:Delta HedgingEstimating Probability of option moneyless: a stock with a delta of 85% is deemed to have an 85% chance of finishing in the money. However, delta does not measure probability per se.

Gamma – Impact of Change in Rs 1 price of underlying asset on delta

Gamma is the change in delta for each unit change in the price of the underlying.

Gamma changes in predictable ways.

As an option goes more into the money, delta will increase until it tracks the

underlying dollar for dollar; however, delta can never be greater than 1 or less than -1.

When delta is close to 1 or -1, then gamma is near zero, because delta doesn’t

change much with the price of the underlying. Gamma and delta are greatest when

an option is at the money—when the strike price is equal to the price of the

underlying.

Gamma – Impact of Change in Rs 1 price of underlying asset on delta

The change in delta is greatest for options at the money, and decreases as the option goes

more into the money or out of the money.

Theta- Impact of Time value per Day

The option premium consists of a time value,

that continuously declines as time to expiration nears, with most of the decline occurring near

expiration.

Theta:

Theta is a measure of this time decay

is expressed as the loss of time value per day

Explanation:

theta of -.1 indicates that the option is losing $.10 of time value per day.

Theta- Impact of Time value per Day

Theta measures changes in value of options or a portfolio that is due to the passage of time.

The holding of options has a negative position theta.

The net of the positive and negative position thetas is the total position theta of the portfolio.

VEGA- Impact of change in 1% volatility

Vega is often used to measure the change in implied volatility.

Volatility is the variability in the price of the underlying over a given unit of time.

Vega measures the change in the option premium due to changes in the volatility of the

underlying, and is always expressed as a positive number.

Because volatility only affects time value, vega tends to vary like the time value of an option

—greatest when the option is at the money and least when the option is far out of the money

or in the money.

Vega measures how much an option price will change with a 1% change in implied volatility.

RHO – Impact of Change in 1% Risk free rate

Rho is the amount of change in premiums due to a 1% change in the prevailing risk-free interest rate.

Thus, a rho of 0.05 means that the theoretical value of call premiums will increase by 5%, whereas the

theoretical value of put premiums will decrease by 5%, because put premiums move opposite to

interest rates.

The values are theoretical because it is market supply and demand that ultimately determines prices.

Interest Rate & Risk Premium:

higher interest rates correspond to lower present values, leading to higher call prices.

Call Premium Put Premium

BEST REGARDS