Embed Size (px)

Citation preview

Intro to Budgeting

Shana McClellandSponsored Projects Administrator, Principal

Sponsored Projects ServicesSeptember 16, 2016

TODAY’S AGENDA

2

Where do we start?

Mechanics of budget building

Preparing the budget

Math and Stuff

Q&A

3

WHERE DO WE START?

Read the announcement!

Sponsor deadline

Total/annual dollar limits

Cost sharing

Required items of cost

Unallowed items of cost

Indirect cost limitations

Format

Submission details

Who else is involved?

Lead or a subaward? Prime?

Multiple UA PIs? Co-Is?

Other units?

Indirect cost waiver?

What is our timeline?

Have we done this before?

4

UNIVERSITY 3 DAY DEADLINE

Requests for Indirect Cost Waivers should be submitted to Sponsored Projects eight business days prior to our sponsor’s deadline

All proposals, paper and electronic, should be submitted to Sponsored Projects in final form three business days prior to our sponsor’s deadline

http://rgw.arizona.edu/sites/researchgateway/files/three_day_deadline.pdf

5

REALISTIC TIMELINES

Are we applying directly to the funding entity?

Are we a subaward? Who is the Prime Sponsor?

How many PIs, CoIs, and Units are involved?

How large or complex is the budget?

Does it require an Indirect Cost Waiver?

Are there other items of complexity?

http://rgw.arizona.edu/administration/proposal-preparation#Timeline

6

MECHANICS OF BUDGET BUILDING

Budget and Budget Justification or Narrative should make sense when read along with the science

Should follow the guiding principles set forth for federal awards

Should follow any specific Sponsor requirements or exclusions as set forth in the funding announcement

Are required for internal review even when not required by the sponsor

7

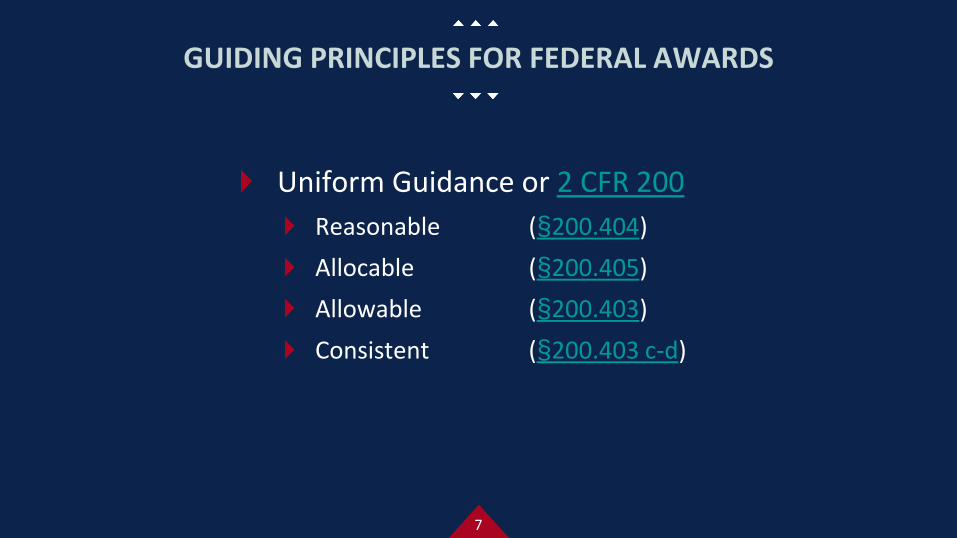

GUIDING PRINCIPLES FOR FEDERAL AWARDS

Uniform Guidance or 2 CFR 200

Reasonable (§200.404)

Allocable (§200.405)

Allowable (§200.403)

Consistent (§200.403 c-d)

8

CATEGORIES OF COSTS

Direct Costs

Identifiable with a particular sponsored project (§200.413)

Indirect Costs

Facilities & Administrative costs (§200.414)

Costs incurred for common or joint objectives that cannot be readily and specifically identified with a particular sponsored project

Administrative expenses (staff, office supplies, toner, copy paper)

Utilities

Building renovations, maintenance

Depreciation, debt service, central administration

9

DIRECT vs. INDIRECT

Costs must be treated consistently and in “like manner” - either as a direct cost or as an F&A cost

Institution’s DS-2 (Cost Accounting Disclosure Statement) often details which costs will be viewed as direct costs vs. indirect costs

UA Direct/Indirect Cost guidance -http://rgw.arizona.edu/administration/build-budget/budget-categories

10

DIRECT COSTS

UA PersonnelSalaries

Fringe Benefits/Employee Related Expenses (ERE)

Capital Equipment

Travel

Other Direct CostsMaterials and Supplies (includes non-capital equipment

Publications

Subawards/Contractual/Services

Tuition Remission

11

INDIRECT COSTS

Facilities & Administrative (F&A) costs, also known as indirect costs oroverhead costs, are defined by the Office of Management and BudgetUniform Guidance 2 CFR, Part 200.56 as "those costs incurred for acommon or joint purpose benefitting more than one cost objective, andnot readily assignable to the cost objectives specifically benefitted,without effort disproportionate to the results achieved."

All grants, contracts and other sponsored agreements accepted by the University of Arizona are subject to the current federally negotiated F&A rate.

http://rgw.arizona.edu/administration/build-budget/FA-Costs/FA-rates

12

COMMON DIRECT COST QUESTIONS

Can I charge a computer or mobile device to my project?

Can I charge office supplies to my project?

Can I charge administrative assistance to my project?

13

COST SHARING

Anything necessary for the completion of the project that is not directly funded/paid for by the sponsor

Effort

Portion of equipment

Supplies

Indirect Costs

Etc.

14

COST SHARING

General Rule: If it is not specifically required by the program, DO NOT include it.

When required by the program, be sure it is clearly stated in the budget and justifications

15

COST SHARING

Mandatory vs. Voluntary

Committed vs. Noncommitted

Matching funds and In-Kind contributions

“Leveraged Resources”

Cash vs. In-Kind

3rd party contributions

16

PREPARING THE BUDGET

Personnel

Senior/Key Personnel (generally PI, Co-Is, and Key Persons essential to the project)

Other Personnel (generally Postdocs, Other Professionals, Technicians, Administrative, Graduate Students, Undergraduates)

Are they academic or fiscal appointments? (determines how they are budgeted)

Fringe Benefits/ERE rates: http://rgw.arizona.edu/administration/build-budget/budget-categories/Salaries-and-Wages/ERE-Rates

17

PREPARING THE BUDGET

Personnel

Academic Appointment (Faculty and Graduate Students)

Academic salary hourly rates (Salary/1600 academic hours = Academic hourly rate)

Summer salary hourly rates (Salary/3 or Salary *0.00072 = Summer hourly rate)

Fiscal Appointment (Faculty, Researchers, Staff, Postdocs)

Fiscal salary hourly rate (Salary/2088 fiscal hours = Fiscal hourly rate)

Academic appointments consist of 1600 academic hours and 464 possible summer hours for a total of 2,064 hours while Fiscal appointments consist of 2,088 hours.

18

PREPARING THE BUDGET

Personnel costs are the largest portion of most budgets.

Most likely to be restricted:

NSF Senior/Key Personnel Salary – generally restricted to 2 months of regular salary in any one year unless justified/approved

Salary Cap – only applicable if specified by the sponsor

Currently $185,100 effective January 10, 2016 for NIH

Tuition Remission – Smith-Lever Act of 1914 - Indirect costs and tuition remission are unallowable.

19

PREPARING THE BUDGET

Equipment (specifically, capital equipment)

http://rgw.arizona.edu/administration/build-budget/budget-categories/equipment

Defined by our negotiated rate agreement

Tangible, non-expendable, useful life of >1 year

Acquisition cost of $5,000+/unit (includes tax, shipping, installation)

Depending on program and cost of equipment, may require formal quotes or informal quotes as cost-basis

20

PREPARING THE BUDGET

Travel - http://www.fso.arizona.edu/travel

Specifically for UA project personnel

Project-related conferences, required grant meetings, subrecipient site visits, project-related collaboration, field work, etc.

Transportation, lodging, per diem, parking, etc.

Cost basis must be provided and may be based on

Online searches for fares/rates (airline, rental car, etc.),

Historical costs for conferences (fees, hotel, etc.)

Lodging and per diem rates are mandated

Domestic rates – State of Arizona (https://gao.az.gov/travel/welcome-gao-travel)

International rates – U.S. Dept. of State (https://aoprals.state.gov/web920/per_diem.asp)

21

PREPARING THE BUDGET

Participant Support

OMB 2 CFR §200.75 extends Participant Support to all Federal sponsors

Direct costs for items such as stipends or subsistence allowances, travel allowances, and registration fees paid to or on behalf of participants or trainees (not employees) in connection with conferences or training projects

Typically excluded from indirect cost calculations

Not Subject Pay/Incentives

Group meals and coffee breaks not allowed in this category

Speaker fees, honorariums, and travel not allowed in this category

When in doubt, ask early! Participant support is a restricted category that usually does not allow rebudgeting.

22

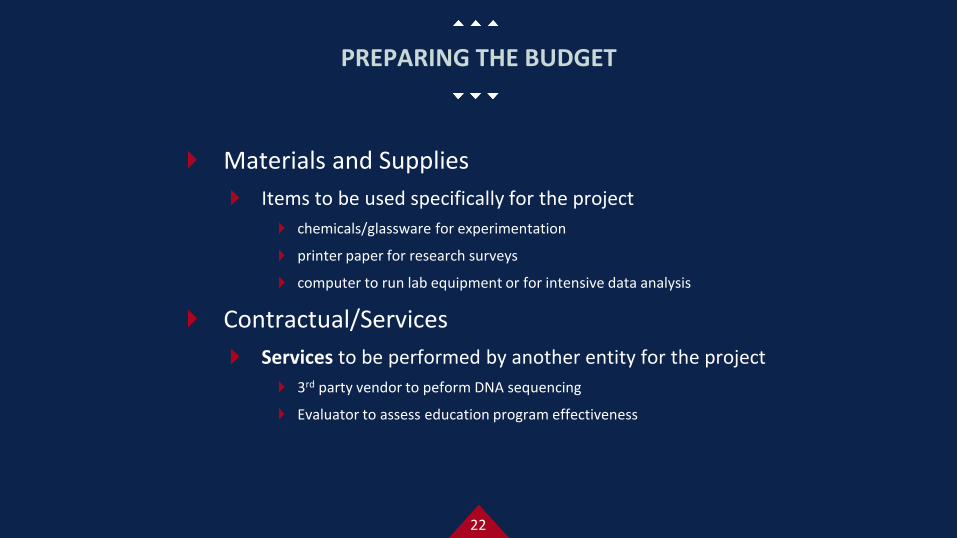

PREPARING THE BUDGET

Materials and Supplies

Items to be used specifically for the project

chemicals/glassware for experimentation

printer paper for research surveys

computer to run lab equipment or for intensive data analysis

Contractual/Services

Services to be performed by another entity for the project

3rd party vendor to peform DNA sequencing

Evaluator to assess education program effectiveness

23

PREPARING THE BUDGET

Subawards

Collaborators from another institution

Distinguished from contractual/services by intellectual contribution to project outcome

Requires SOW, budget, budget justification at time of proposal

Single line on our budget

Subaward budget must comply with sponsor guidelines, subrecipient institution policies, and all federal regulations

F&A only charged on first $25,000 of each subaward

24

PREPARING THE BUDGET

Tuition Remission

http://rgw.arizona.edu/administration/build-budget/budget-categories/other-costs#TuitionRemission

No longer percentage of Fringe Benefits/ERE

Direct charged as “Other Direct Costs”

FY2016/2017 rate is $11,372 for a full (0.50 FTE) graduate student ($5,686/semester)

Tuition and Fees Calculator: http://bursar.arizona.edu/students/fees

25

PREPARING THE BUDGET

Indirect Costs (F&A)

Applies to costs specified in our Federally Negotiated Indirect Cost Rate Agreement (NICRA)

We are a Department of Health and Human Services (DHHS) institution

Default = Modified Total Direct Costs (MTDC)

Excludes tuition, capital equipment, patient care, off-site rentals, scholarships, fellowships, and all subaward costs exceeding $25,000

26

PREPARING THE BUDGET

Sponsor stipulations & F&A Waivers

Stipulations

Unless exclusions are specified by the sponsor, reduced indirect cost rates are calculated at a Total Direct Costs (TDC) base rather than our DHHS Modified Total Direct Costs Base (MTDC)

Watch for odd language that may imply Total Costs (TC) instead (30% of total funds)

Waivers

Required if reduced IDC is not stipulated by sponsor and our regular rate is not used

http://rgw.arizona.edu/administration/build-budget/F-A-Costs#FAWaiverProcess

27

MATH! AND STUFF

If a sponsor limits the project/annual budget total to $200,000 with no IDC stipulations…

AND the project budgets no exclusions (equipment, tuition, etc.)

How much money is available for direct costs?

Total / (1 + F&A Rate) = Direct Cost

Direct - $200,000/1.535 = $130,293

Indirect - $130,293 * 53.5% = $69,707

Total - $130,293 + $69,707

28

MATH! AND STUFF

If a sponsor stipulates indirect costs at 15% of the total annual grant amount of up to $400,000 per year

How much money is available for direct costs?

What F&A rate do you enter into UAccess Research?

Annual - (Annual * TC Rate) = Direct Cost

$400,000 - ($400,000 * 15%) = $340,000

$400,000 * 15% = $60,000

$340,000 + $60,000 = $400,000

TC Rate/(100 - TC Rate) = F&A Rate

15/(100-15) = 17.647% TDC

$340,000 * 17.647% = $60,000 (rounded)

$340,000 + $60,000 = $400,000

29

QUESTIONS?

?