Embed Size (px)

Citation preview

“International Finance and Payments”

Lecture V

“Cost of International Capital”

Lect. Cristian PĂUNLect. Cristian PĂUN

Email: Email: [email protected]

URL: http://www.finint.ase.roURL: http://www.finint.ase.ro

Academy of Economic Studies

Faculty of International Business and Economics

Course 2: International Financial Markets and Institutions 2

International portfolio theory - review

• the difference between certainty, risk and uncertainty in international financing;

• investment decision is based on risk and return profile;

• investors expectations in terms of return are based on their risk assessment (direct relationship);

• investors associate an utility function to their expected returns;

• we have different risk attitudes;

• modern portfolio theory:

• Markovitz – efficient frontier

• CAPM (W. Sharpe) – beta and market portfolio

• APT (S. Ross) – arbitrage and market equilibrium

• active and passive portfolio management.

Course 2: International Financial Markets and Institutions 3

Interest rate and market equilibrium• interest rate = compensation required by the investors because they lend money for a determined period of time;

• interest rate = market equilibrium between demand and supply of money;

Supply curveDemand curve950 $ 5.3%

900 $ 11.1%

i=RET=(FV-P)/P

Quantity of bonds

750 $ 33 %

100 bil. 500 bil.

850 $ 17.6%E

300 bil.

Interest rateSecurity price

Course 2: International Financial Markets and Institutions 4

Shifts in the demand for bonds• Wealth;

• Expected returns on bonds relative to alternative assets;

• Expected inflation

• Risk of bonds relative to alternative assets;

• Liquidity of bonds relative to alternative assets.

Shifts in the supply for bonds• Expected profitability of investment opportunities (increase);

• Expected inflation (real cost of financing is falling down);

• Government activities (public deficits).

Fisher effect: when expected inflation rises, interest rates will rise

Liquidity preference framework: BD+MD=BS+MS (Keynes)(no real assets)

Course 2: International Financial Markets and Institutions 5

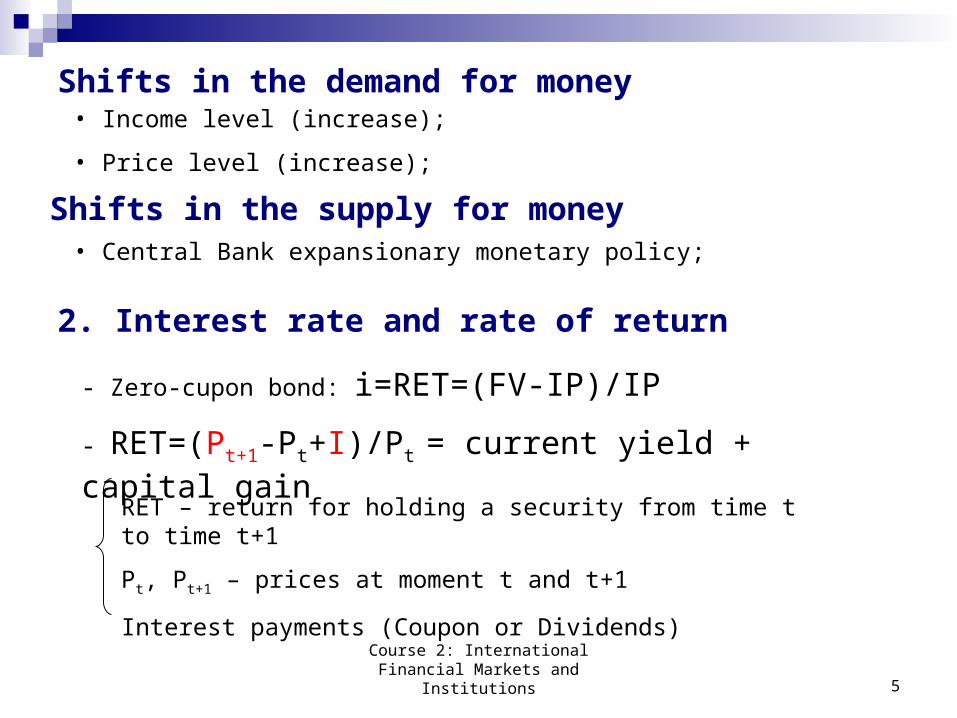

Shifts in the demand for money• Income level (increase);

• Price level (increase);

Shifts in the supply for money• Central Bank expansionary monetary policy;

2. Interest rate and rate of return

- Zero-cupon bond: i=RET=(FV-IP)/IP

- RET=(Pt+1-Pt+I)/Pt = current yield + capital gain

RET – return for holding a security from time t to time t+1

Pt, Pt+1 – prices at moment t and t+1

Interest payments (Coupon or Dividends)

Course 2: International Financial Markets and Institutions 6

Real and Nominal Interest Rate

Simple and Compounded Interest Rate

Risk Free Interest Rate

Inominal=Ireal+Inflation

(1+Inominal)=(1+Ireal)x(1+p) - Fisher Effect

RFR=(FVT-Bills-IPT-Bills)/IPT-Bills

100 USD = IP 110 USD = FV

1)Per

D(1D Persimple

compounded

Course 2: International Financial Markets and Institutions 7

Risk Structure of Interest Rate

- Default risk = the chance that the issuer of the bond will be unable to make interest payments or pay off the face value at the maturity;

Aaa Baa Caa (Moody’s)

AAA BBB CCC D (S&P)

Ex:

B Companies: Mariott, Revlon

AA Companies: McDonalds, Mobil Oil

AAA Companies: General Electric, Wisconsin Bell

- Liquidity = the capacity of a security to be cheaply and quickly converted into cash

- Income Tax Consideration: in case of Municipal Bonds vs. T-Bonds

Course 2: International Financial Markets and Institutions 8

Term Structure of Interest Rate

- Securities with identical risk, liquidity and income tax characteristics may have different interest rates because the maturity is different

- Yield Curve plots the yields on bonds with different terms to maturity but identical risk, liquidity and tax characteristics

US Treasury Yield Curve / November 2004Date 1 mo 3 mo 6 mo 1 yr 2 yr 3 yr 5 yr 7 yr 10 yr 20 yr

11/01/04 1.79 1.99 2.20 2.34 2.61 2.89 3.36 3.76 4.11 4.84

11/02/04 1.86 1.97 2.19 2.33 2.60 2.86 3.34 3.75 4.10 4.84

11/03/04 1.83 1.96 2.18 2.32 2.60 2.85 3.35 3.74 4.09 4.83

Maturity

Yield

Yield CurveSecurities with longer maturities usually have a higher yield. If short term securities offer a higher yield, then the curve is said to be inverted.

Course 2: International Financial Markets and Institutions 9

Cost of International Capital

International Financing Plan

Credit Years Payoffs Interest An RemainKValue 200000 euro 1 0 0 0 220000Interest Rate 10% 2 0 0 0 242000Maturity 5 years 3 80667 24200 104867 161333Reimboursement equally 4 80667 16133 96800 80667

5 80667 8067 88733 0290400

Current Yield = period

1

C

CA

0

0n

Current Yield = 9.04%

Step 1: Determine the proportions of each source to be raised as capital.

Step 2: Determine the marginal cost of each source.

Step 3: Calculate the weighted average cost of capital.

Course 2: International Financial Markets and Institutions 10

Cost of International Capital – Time Value of Money

- Translating a value back in time

-- referred to as discounting --

requires determining what a

future amount or cash flow is

worth today.

A1A2 A3 A4 A5

Financing Decision Moment

EX: 1000 USD 1100 USD after 1 y

Inflation rate of 20%

1100 USD = 1100 / (1+p) = 916.6.

USD in present

Course 2: International Financial Markets and Institutions 11

Present Value, Net Present Value, Internal Rate of Return

(4) k)(1

CFPV

nn

M

1nn

nfinancing

M

1nn

ninvestment

)k1(

ACNPV

)k1(

AINPV

IRR = k NPV = 0

• Inflation rate

• Interest rate

• Estimated profit for an investment project

Discounted rate

Expectations in terms of

Course 2: International Financial Markets and Institutions 12

Present Value, Net Present Value, Internal Rate of ReturnBonds

Value 500000 euroInterest Rate 10% 10%Maturity 5 years 9%Reimboursement equally 8.89%Face Value 10 euro 551234Issuing Price 9 euro -51234Maturity Price 11 euro 17.80%Number of Bonds 50000

Years Nb NV Cupons P An Krem Drate Disc An1 10000 100000 50000 10000 160000 400000 0.9174 1467892 10000 100000 40000 10000 150000 300000 0.8417 1262523 10000 100000 30000 10000 140000 200000 0.7722 1081064 10000 100000 20000 10000 130000 100000 0.7084 920955 10000 100000 10000 10000 120000 0 0.6499 77992

700000 551234

Net present valueIRR

Interest rateDiscount RateCurrent YieldPresent Value

Conclusion 1:

Internal Rate of Return is the best measure for the marginal cost of international financing (real cost is 17.80 instead 10% or 8.89%)

Course 2: International Financial Markets and Institutions 13

Comparing credits in different currencies using NPV€ USD 9.0% 7.0%

Year An An €/USD k(euro) k(USD)1 160000 160000 1.2 0.91743 0.9345792 150000 150000 1.3 0.84168 0.8734393 140000 140000 1.4 0.77218 0.8162984 130000 130000 1.5 0.70843 0.7628955 120000 120000 1.6 0.64993 0.712986

TOTAL 700000 700000 1.4

Method I:

- Estimating k(euro)

- Estimating k(USD)

- NPVeuro x spot0 = NPVeuroUSD

€ USD10% 10%7% 8%

579565 565109-129565 -115109

Present ValueNet present value

Interest rateDiscount Rate

Course 2: International Financial Markets and Institutions 14

Comparing credits in different currencies using NPV€ USD 9.0% 7.0%

Year An An €/USD k(euro) k(USD)1 160000 160000 1.2 0.91743 0.9345792 150000 150000 1.3 0.84168 0.8734393 140000 140000 1.4 0.77218 0.8162984 130000 130000 1.5 0.70843 0.7628955 120000 120000 1.6 0.64993 0.712986

TOTAL 700000 700000 1.4

Method II:

- Estimating k(euro)

- Estimating exchange rate

- Transforming An from USD in €

- Comparing NPV

10% 10%7% 8%

579565 510088-129565 -60088

Discount RatePresent ValueNet present value

Interest rate

Course 2: International Financial Markets and Institutions 15

Comparing credits in different currencies using NPV€ USD 9.0% 7.0%

Year An An €/USD k(euro) k(USD)1 160000 160000 1.2 0.91743 0.9345792 150000 150000 1.3 0.84168 0.8734393 140000 140000 1.4 0.77218 0.8162984 130000 130000 1.5 0.70843 0.7628955 120000 120000 1.6 0.64993 0.712986

TOTAL 700000 700000 1.4

Method III (best accuracy):

- Estimating k(euro)

- Estimating k(USD)

- Estimating an average FX rate

- Transforming NPV from USD in €

- Comparing NPV

€ USD10% 10%7% 8%

579565 565109-129565 -100375Net present value

Interest rateDiscount RatePresent Value

Course 2: International Financial Markets and Institutions 16

Comparing credits in different currencies using IRR

€ USDAn An €/USD

160000 144000 0.9150000 142500 0.95140000 121800 0.87130000 107900 0.83120000 97200 0.81700000 613400 0.872

€ USDYear An An €/USD

1 160000 160000 0.92 150000 150000 0.953 140000 140000 0.874 130000 130000 0.835 120000 120000 0.81

TOTAL 700000 700000 0.872

Method I: Comparing IRR obtained on initial An expressed in different currencies

Method II: Transforming An from USD to Euro and calculating IRR

We have the same IRR (= 17.8%)

We have different IRR:

€ USDIRR 17.80% 12.25%NPV -129565 -100375

Course 2: International Financial Markets and Institutions 17

NPV Criteria in International Financing

- Easier to be calculated than IRR

- It is difficult to estimate different discount rates for different financial markets;

- We should take into consideration the exchange rate when we compare different NPVs;

- NPV encourage big investment projects and discourage big financing projects.

IRR Criteria in International Financing

• Independent from FX rate;

• It is quite complicated to be estimated;

• In some cases we can’t calculate it (symmetric annuities, positive annuities).

CONCLUSION 2: When compare different financing alternatives we should use both two criteria: NPV and IRR

Course 2: International Financial Markets and Institutions 18

Cost of Equity

M

1nM

Mn

n

)k1(

NP

)k1(

DivNNIPNPV

Scenario A:

- Buy – back of stocks after 5 years:

NPV = 0 Kstocks

Scenario B: no buy - back

1n

nn

)k1(

DivNNIPNPV

Kstocks = (D0/IP)+g (Gordon – Shapiro Model)

Course 2: International Financial Markets and Institutions 19

International Financing Plan - summary

Capital Structure Value Weight CostCredit 200000 20% 10%Bonds 500000 50% 17.80%Stocks 300000 30% 11.53%

EquityEquityDEBTDebt kWk)T1(WWACC

WACC = 13.27%

Course 2: International Financial Markets and Institutions 20

Global CAPM and WACC

Rf

Rm

Ei

Betaβi=1

Risk premium

Securities with a higher risk than market risk

Securities with a lower risk than market risk

2M

iMi

)r,R(Cov

Note: the company has the same risk as the global market has

WACC

Rm

Course 2: International Financial Markets and Institutions 21

Capital Structure Optimization

• trying to find new financing resources with a lower cost according to the risk level of the borrower

• modifying the credit condition in terms of reimbursement,

• renouncing to the no – payment periods;

• modifying the capital structure;

• different maturities;

• diversifying international your financing;

• search to issue more fixed income instruments.