Embed Size (px)

Citation preview

International Auditing and Assurance Standards Board

Communication with Those Charged with Governance

ISA Implementation Support Module

Prepared by IAASB Staff

October 2009

• Introduction

• Two-Way Communication

• The Communication Process

• Matters to be Communicated

Overview

2

• The context for revising the standard

• New standard provides overarching framework for communication with TCWG

• Standard applies regardless of entity’s governance structure or size

• Specific considerations where TCWG and management are the same

Introduction

Introduction

3

• Old standard focused on communication of audit matters arising from the audit with TCWG

– Essentially a one-way communication from auditor to TCWG

• New standard imposes specific obligation on auditor to promote effective two-way communication

– Auditor now has specific responsibility to take steps to achieve effective two-way communication, or failing that, to take further appropriate action

• Emphasis on effective two-way communication recognized in the objectives

Two-Way Communication

Two-Way Communication

4

• Why is it important?

– Assists in developing constructive working relationship between auditor and TCWG

– Sets clear expectations between auditor and TCWG regarding communication of matters of audit relevance

– Recognizes that TCWG are an important element of control environment

– Assists TCWG in fulfilling their oversight responsibility for financial reporting process

– Recognizes that TCWG are an important source of information for conduct of effective audit

Two-Way Communication

Two-Way Communication

5

• Standard does not mandate two-way communication

– TCWG cannot be required to communicate with auditor

• However, auditor required to evaluate whether two-way communication has been adequate

• If two-way communication not adequate

– May affect auditor’s assessment of risks of material misstatement

– May affect auditor’s ability to obtain sufficient appropriate audit evidence

– Standard provides guidance on possible auditor actions

Two-Way Communication

Two-Way Communication

6

• Communicate form, timing, and expected general content of communications

– Provides basis for constructive dialogue

• Helps to explain or clarify such matters as

– Purpose of communications

– Which person(s) on each side will be the point contacts

– The auditor’s expectation that the communication will be two-way

– How the feedback mechanism will work between the parties

The Communication Process

The Communication Process

7

• Will not be the same as in a larger entity audit– Process will vary with entity’s size and

governance structure, among other things

• Formal communications may be more appropriate in a larger entity audit– Greater formality may be necessary with greater

size and complexity of entity

Communication Process in an SME Audit

The Communication Process

8

• Less structured approach often more suitable in an SME audit

– Consistent with lack of formality in management and governance practices in SMEs

• Often, oral communication may be all that is needed in an SME audit

– Especially if auditor has ongoing contact and dialogue with TCWG

Communication Process in an SME Audit

The Communication Process

9

• If all TCWG are involved in managing the entity, matters communicated with them in a management capacity need not be re-communicated with them in a governance role

– Common situation in owner-managed entities

• However, make sure that communication with individuals with management responsibilities informs all of those in a governance role

The Communication Process

The Communication Process

10

• New standard is much more specific about matters that should be communicated

– Auditor’s responsibilities in relation to the audit

– Planned scope and timing of the audit

– Significant findings from the audit

• Objectives recognize importance of these matters

• Intended to increase consistency of communication practices

• Will enhance quality and effectiveness of auditor’s communication with TCWG

Matters to be Communicated

Matters to be Communicated

11

• Helps TCWG better understand the audit and what to expect from it

• Opportunity for TCWG to identify any specific areas where they may ask auditor to perform additional work

• Assists auditor in better understanding the entity and its environment through dialogue with TCWG, consistent with the two-way communication principle

• Care needed not to compromise effectiveness of audit

Communicating Planned Scope and Timing of Audit

Matters to be Communicated

12

• Significant qualitative aspects of accounting practices– E.g., accounting policies, accounting estimates, and

disclosures

• Significant difficulties encountered during audit

• Unless all TCWG and management are the same– Significant matters discussed with management

– Written representations sought by auditor

• Other matters of significance to oversight of financial reporting process

Communicating Significant Findings

Matters to be Communicated

13

• Why is such communication important?– Helps confirm relevant facts and circumstances

and achieve mutual understanding of the issues

– Recognizes need for open and constructive dialogue on these matters

– Provides opportunity to resolve significant difficulties arising during audit

• Communicate in writing if oral communication would be inadequate

Communicating Significant Findings

Matters to be Communicated

14

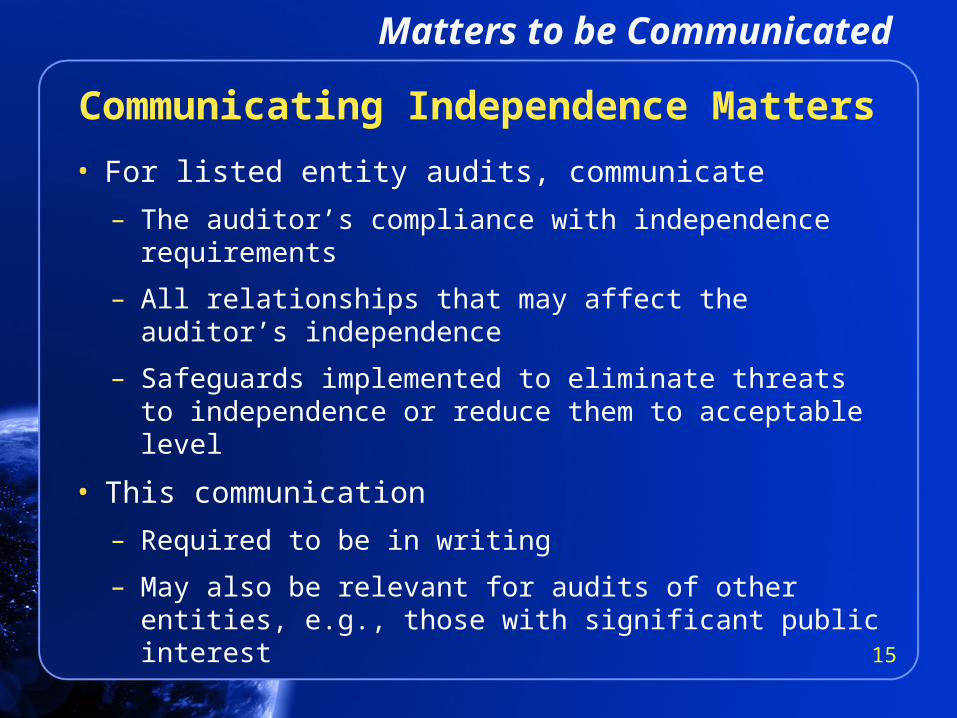

• For listed entity audits, communicate

– The auditor’s compliance with independence requirements

– All relationships that may affect the auditor’s independence

– Safeguards implemented to eliminate threats to independence or reduce them to acceptable level

• This communication

– Required to be in writing

– May also be relevant for audits of other entities, e.g., those with significant public interest

Communicating Independence Matters

Matters to be Communicated

15

Note

This set of support slides does not amend or override the ISAs, the texts of which alone are authoritative. Reading the slides is not a substitute for reading the ISAs. The slides are not meant to be exhaustive and reference to the ISAs themselves should always be made. In conducting an audit in accordance with ISAs, the auditor is required to comply with all the ISAs that are relevant to the engagement.

16

Copyright © October 2009 by the International Federation of Accountants (IFAC). All rights reserved. Permission is granted to make copies of this work provided that such copies are for use in academic classrooms or for personal use and are not sold or disseminated and provided that each copy bears the following credit line: “Copyright © October 2009 by the International Federation of Accountants (IFAC). All rights reserved. Used with permission of IFAC. Contact [email protected] for permission to reproduce, store, or transmit this work.” Otherwise, written permission from IFAC is required to reproduce, store, or transmit, or to make other similar uses of, this work, except as permitted by law. Contact [email protected].

International Federationof Accountants

ISBN: 978-1-60815-043-4

www.ifac.org