Embed Size (px)

Citation preview

INTEGRATED PLAN

PART A – OVERVIEW

Contents Page

Part A: Overview

Section 1: Strategic Context and Key Decisions 4 - 15

Section 2: Revenue Budget Funding 15 - 20

Section 3: Risk Management, Uncertainties, Contingency and Sensitivity Analysis

20 - 27

Section 4: Capital Programme 28 - 29

Appendix A: Summary Budget Movements & Funding Statement 30 - 31

Appendix B: Local Government Act 2003 - S25 Report of the Director of Finance

32 - 36

Part B: Strategic Direction and Financial Consequences

1. Adult Care & Health portfolio 37 – 64

2. Children, Young People & Families portfolio 65 – 90

3. Community Safety & Waste Management portfolio 91 - 118

4. Education, Libraries & Localism portfolio 119 – 145

5. Growth, Infrastructure, Planning & the Economy portfolio 146 – 161

6. Highways & Environment portfolio 162 - 188

7. Public Health & Prevention portfolio 189 - 198

8. Resources & Performance (including Central Items) portfolio 199 - 233

9. Education, Libraries & Localism portfolio – Schools 234 - 245

Part C: Capital Strategy 246 - 293

Part D: Treasury Management Strategy 294 - 328

Part E: Insurance and Risk Strategy 329 - 343

Part F: Equalities Impact Assessment 344 - 352

Part G: Supporting Technical Information & Summary Tables 353 - 387

Guide to using the Integrated Plan pack

The Integrated Plan is a multi–part pack and each section forms a standalone document. Each part includes summary and detailed tables and commentary to explain them. It includes: Parts A and B (supported by the detailed schedules at Part G), set out the overall revenue and capital budget position and a detailed narrative for each Portfolio’s budget proposals.

• Part A provides an overview of the proposed revenue budget and capital programme, including a review of the budget estimates and adequacy of reserves. It also includes the legal declaration of the Director of Resources/s151 officer on the robustness of the estimates provided.

• Part B sets out, for each Cabinet Portfolio, the Strategic Direction and Financial Consequences. These set out the future service direction and priorities, including details of revenue budget movements (pressures and savings) and capital programme proposals. They also include benchmarking comparisons and an assessment of key risks in delivering services within the IP.

Parts C to E provide the detailed strategies that support the Council’s financial processes. Part F summarises the equalities impact assessment. Part G provides supporting detailed schedules.

• the Capital Strategy (part C), including changes arising from updated guidance, and detailing how the Council will invest in its property and infrastructure assets and use its resources to deliver financial returns and service efficiencies;

• the Treasury Management Strategy (Part D), a statutory requirement setting out the Council’s approach to borrowing and financial investments, including changes arising from new guidance;

• the Insurance and Risk Strategy (Part E), sets out the Council’s approach to risk management and insurance;

• the Equalities Impact Assessment is also included (Part F), which considers the cumulative equality impact of IP proposals; and

• Detailed supporting schedules provide other technical information and financial summaries, and these are included in Part G.

IP Part A: Overview 3

1 Introduction – Strategic Context and Key Decisions

1.1 The Integrated Plan (IP) sets out the Council’s plans for service delivery within available funding. It brings together services’ key priorities and plans for delivering these, alongside the strategies that shape how the Council manages its resources.

1.2 These plans have been set in the context of a year like no other. The pandemic has

had a huge impact on communities, the Council and its finances. The future impact on the public and the organisation is still very uncertain. This is compounded further by existing operational challenges that the council faces, including:

• Increasing demand for services from our growing and ageing population

• Increasing complexity of needs of existing service users, for example within social care related services;

• Significant savings already delivered by the Council since 2010.

1.3 Additionally, the process to prepare the IP for 2021 has been marked by an

unusually high level of uncertainty. As was the case last year, and the year before, councils were expecting in the year ahead:

• A new spending review outlining public spending plans for the coming years;

• Key changes to local government funding including Business Rates Retention and the Fair Funding review.

Given the impact of the pandemic, these key financial reviews have been delayed once again, increasing the uncertainty for Councils.

Investing in Hertfordshire

1.4 Despite these challenges, the Council remains determined that Hertfordshire

continues to be a county where people have the opportunity to live healthy, fulfilling lives in thriving, prosperous communities.

1.5 Prudent financial and operational management has helped the Council tackle some of the challenges outlined above. This, coupled with a financial settlement in the Spending Review that has listened to the concerns of Councils, means that it is possible to consider investing in key services. This Integrated Plan includes significant investment in the following portfolio areas:

• Adult Care and Health: o The budget proposes that the Council will take advantage of the flexibility

in council tax for adult social care, but will spread this across 2 years as follows:

▪ 2021/22 – an extra 2% ▪ 2022/23 – an extra 1%

o It is felt that this approach strikes a balance between minimising the council tax burden for residents, whilst enabling investment in critical services.

o The ASC council tax increase will enable investment in the following areas:

IP Part A: Overview 4

▪ Funding for additional numbers of people needing support and to cover increases in the National Living Wage

▪ Funding to enable care worker pay increases to be extended to include those working in residential, nursing and supported living establishments across disability and older people’s services

▪ Support to the Voluntary Sector, including an enhanced package next year to support COVID recovery, building on the excellent support these partnerships have provided to communities this year

▪ Investment in safeguarding – providing additional practitioners to ensure this critical service has the right level of resource to be able to support the most vulnerable

▪ Providing permanent funding for the Domestic Violence Service, enabling it to respond to new national initiatives with certainty

▪ Funding to support the transformation in disability services in the coming years

• Highways and Environment: o £10m of investment as part of our Climate Change response, providing

additional capital funding to improve drainage in response to highways flooding brought about by increasing and changing rainfall patterns

o £7m of investment to move forward roll out of 20 mph speed limits, in line with the Speed Management strategy approved by Cabinet in December 2020

o £3m of investment in active travel schemes o Extra funding for Winter Maintenance to help keep the county moving

• Sustainable Herts: o £10m of capital investment in sustainable projects to significantly drive

forward delivery of the Sustainable Hertfordshire strategy approved by

Cabinet in March 2020 with an action plan approved in December 2020,

including £1.5m earmarked for pilot projects in schools energy initiatives.

It will also enable the council to seek external funding, providing matched

funding where needed, to maximise funding available to support the

strategy

o Creating a £2m revenue investment fund to drive forward the action plan, and doubling project capacity to £600k per year

• Growth, Infrastructure, Planning and the Economy: o Creating a £2m investment fund to support driving forward Growth and

Infrastructure work in the county, including development work and studies to put the Council at the forefront of being able to bid for government and other external funding

• Investing in tackling inequality o Creating a £11.5m investment fund over the life of the IP to bring forward

proposals to help tackle some of the longer term issues of inequality. This includes, but not limited to, economic recovery, investment in skills, support families and children’s wellbeing and education

IP Part A: Overview 5

• Community Safety and Waste Management: o Investment in our waste infrastructure, including at our recycling centres

with equipment to minimise the environmental impact and cost of waste

transfer

o To deliver against, the 2019-23 Integrated Risk Management Plan (IRMP)

so that appropriate Fire Prevention, Protection and Response resources

are provided in Hertfordshire

• Children, Young People and Families o Investment in prevention, supporting diversion work that aims to avoid

children becoming looked after o Ensuring there is sufficient contingency in the budget to meet post COVID

demand, both in terms of staffing and support for children needing care

• Education, Libraries and Localism: o £53m of investment in new Special Schools and specialist resource

provision to enable delivery of the SEND strategy approved by Cabinet in

December 2020

• Resources and Performance: o Investment in technology to ensure the organisation can modernise and

take advantage of new ways of working

• Public Health and Prevention:

o To support in the recovery from Covid-19 additional funding of £1.5m will

be invested into Health Inequalities, Healthy Places and Mental Health

1.6 There are other more detailed proposals contained throughout the IP document, including within the individual Portfolio strategic Direction statements (Part B). Future Financial Position

1.7 The summary IP position shows a balanced position for 2021/22, but with rising

budget gaps in later years (£5.4m rising to £25.6m). This is essentially because the demand and cost of services is increasing faster than our funding levels. At the same time, after many years of identifying and delivering savings is proving harder and harder to identify and achieve efficiency savings.

1.8 Securing a balanced financial plan for 2021/22 proved more challenging than was originally expected. This is due to significant financial and operational implications caused by the pandemic, and especially due to the uncertainty of the levels of funding available.

1.9 The impact of the recession on finances of the local population and its businesses are very difficult to model and forecast accurately. It is clear that predicting levels of council tax and business rates will be difficult over the medium term. Furthermore, overlaying potential changes in funding from government and existing operational challenges will make the formulation of the 2022/23 budget even more challenging.

IP Part A: Overview 6

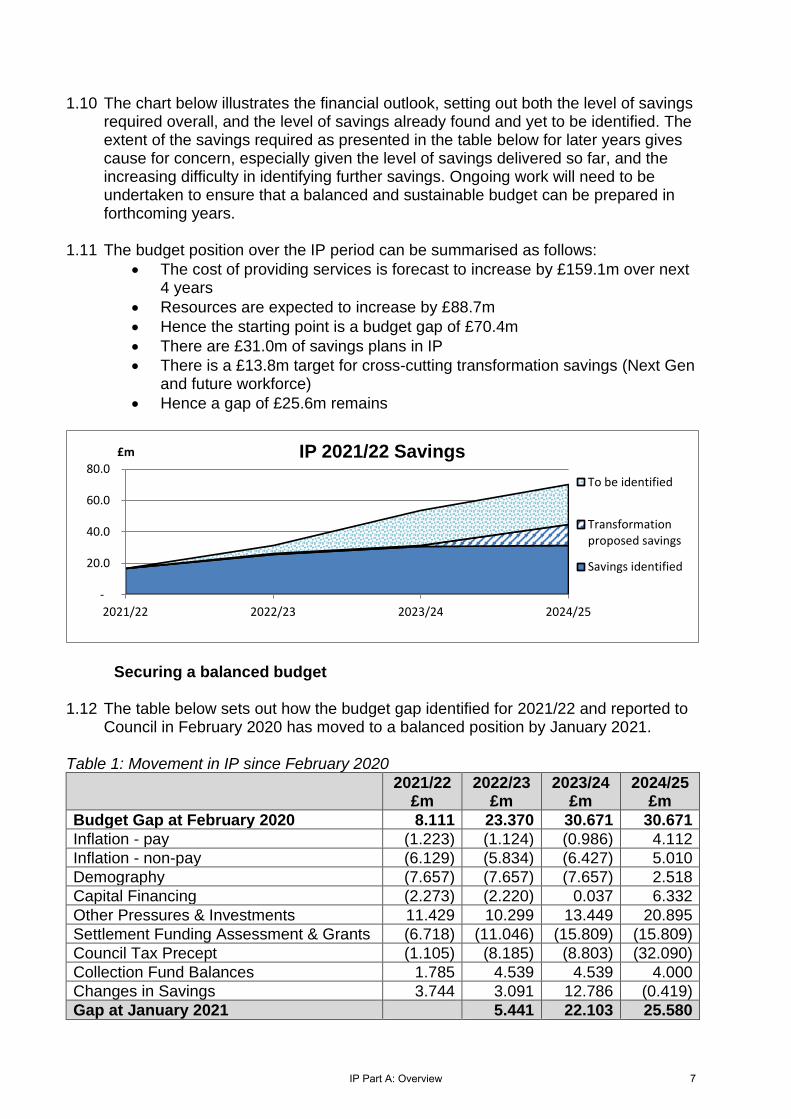

1.10 The chart below illustrates the financial outlook, setting out both the level of savings required overall, and the level of savings already found and yet to be identified. The extent of the savings required as presented in the table below for later years gives cause for concern, especially given the level of savings delivered so far, and the increasing difficulty in identifying further savings. Ongoing work will need to be undertaken to ensure that a balanced and sustainable budget can be prepared in forthcoming years.

1.11 The budget position over the IP period can be summarised as follows:

• The cost of providing services is forecast to increase by £159.1m over next 4 years

• Resources are expected to increase by £88.7m

• Hence the starting point is a budget gap of £70.4m

• There are £31.0m of savings plans in IP

• There is a £13.8m target for cross-cutting transformation savings (Next Gen and future workforce)

• Hence a gap of £25.6m remains

Securing a balanced budget

1.12 The table below sets out how the budget gap identified for 2021/22 and reported to

Council in February 2020 has moved to a balanced position by January 2021. Table 1: Movement in IP since February 2020

2021/22 £m

2022/23 £m

2023/24 £m

2024/25 £m

Budget Gap at February 2020 8.111 23.370 30.671 30.671

Inflation - pay (1.223) (1.124) (0.986) 4.112

Inflation - non-pay (6.129) (5.834) (6.427) 5.010

Demography (7.657) (7.657) (7.657) 2.518

Capital Financing (2.273) (2.220) 0.037 6.332

Other Pressures & Investments 11.429 10.299 13.449 20.895

Settlement Funding Assessment & Grants (6.718) (11.046) (15.809) (15.809)

Council Tax Precept (1.105) (8.185) (8.803) (32.090)

Collection Fund Balances 1.785 4.539 4.539 4.000

Changes in Savings 3.744 3.091 12.786 (0.419)

Gap at January 2021 5.441 22.103 25.580

-

20.0

40.0

60.0

80.0

2021/22 2022/23 2023/24 2024/25

£m IP 2021/22 Savings

To be identified

Transformationproposed savings

Savings identified

IP Part A: Overview 7

1.13 It can be seen from the table above that pressures and investments were presented

over and above those already included in IP 2020 (including through capital bids and other pressures and investments). This position was further worsened by a drop in council tax income and the delay in the achievement of existing savings. This position was offset by a significant one-off fall in social care demand caused by the pandemic, lower than forecasted inflation and interest rates and an enhanced level of government funding.

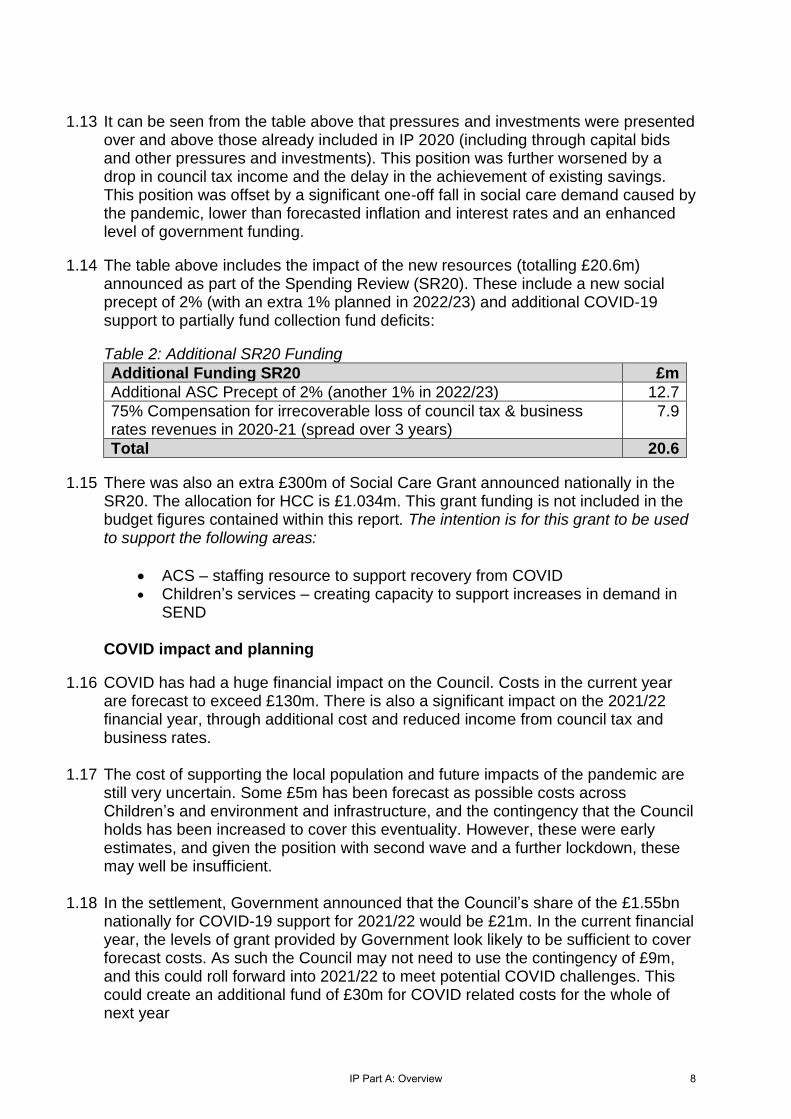

1.14 The table above includes the impact of the new resources (totalling £20.6m) announced as part of the Spending Review (SR20). These include a new social precept of 2% (with an extra 1% planned in 2022/23) and additional COVID-19 support to partially fund collection fund deficits:

Table 2: Additional SR20 Funding

Additional Funding SR20 £m

Additional ASC Precept of 2% (another 1% in 2022/23) 12.7

75% Compensation for irrecoverable loss of council tax & business rates revenues in 2020-21 (spread over 3 years)

7.9

Total 20.6

1.15 There was also an extra £300m of Social Care Grant announced nationally in the SR20. The allocation for HCC is £1.034m. This grant funding is not included in the budget figures contained within this report. The intention is for this grant to be used to support the following areas:

• ACS – staffing resource to support recovery from COVID • Children’s services – creating capacity to support increases in demand in

SEND

COVID impact and planning

1.16 COVID has had a huge financial impact on the Council. Costs in the current year are forecast to exceed £130m. There is also a significant impact on the 2021/22 financial year, through additional cost and reduced income from council tax and business rates.

1.17 The cost of supporting the local population and future impacts of the pandemic are still very uncertain. Some £5m has been forecast as possible costs across Children’s and environment and infrastructure, and the contingency that the Council holds has been increased to cover this eventuality. However, these were early estimates, and given the position with second wave and a further lockdown, these may well be insufficient.

1.18 In the settlement, Government announced that the Council’s share of the £1.55bn

nationally for COVID-19 support for 2021/22 would be £21m. In the current financial year, the levels of grant provided by Government look likely to be sufficient to cover forecast costs. As such the Council may not need to use the contingency of £9m, and this could roll forward into 2021/22 to meet potential COVID challenges. This could create an additional fund of £30m for COVID related costs for the whole of next year

IP Part A: Overview 8

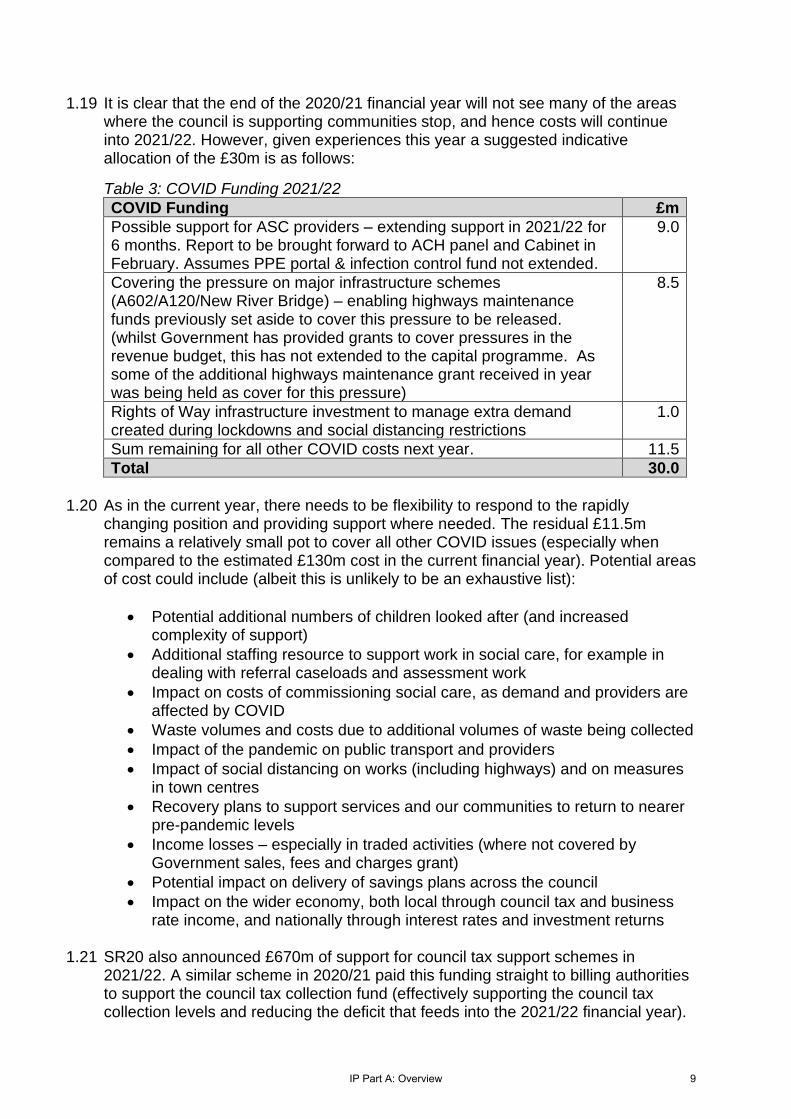

1.19 It is clear that the end of the 2020/21 financial year will not see many of the areas where the council is supporting communities stop, and hence costs will continue into 2021/22. However, given experiences this year a suggested indicative allocation of the £30m is as follows:

Table 3: COVID Funding 2021/22

COVID Funding £m

Possible support for ASC providers – extending support in 2021/22 for 6 months. Report to be brought forward to ACH panel and Cabinet in February. Assumes PPE portal & infection control fund not extended.

9.0

Covering the pressure on major infrastructure schemes (A602/A120/New River Bridge) – enabling highways maintenance funds previously set aside to cover this pressure to be released. (whilst Government has provided grants to cover pressures in the revenue budget, this has not extended to the capital programme. As some of the additional highways maintenance grant received in year was being held as cover for this pressure)

8.5

Rights of Way infrastructure investment to manage extra demand created during lockdowns and social distancing restrictions

1.0

Sum remaining for all other COVID costs next year. 11.5

Total 30.0

1.20 As in the current year, there needs to be flexibility to respond to the rapidly

changing position and providing support where needed. The residual £11.5m remains a relatively small pot to cover all other COVID issues (especially when compared to the estimated £130m cost in the current financial year). Potential areas of cost could include (albeit this is unlikely to be an exhaustive list):

• Potential additional numbers of children looked after (and increased complexity of support)

• Additional staffing resource to support work in social care, for example in dealing with referral caseloads and assessment work

• Impact on costs of commissioning social care, as demand and providers are affected by COVID

• Waste volumes and costs due to additional volumes of waste being collected

• Impact of the pandemic on public transport and providers

• Impact of social distancing on works (including highways) and on measures in town centres

• Recovery plans to support services and our communities to return to nearer pre-pandemic levels

• Income losses – especially in traded activities (where not covered by Government sales, fees and charges grant)

• Potential impact on delivery of savings plans across the council

• Impact on the wider economy, both local through council tax and business rate income, and nationally through interest rates and investment returns

1.21 SR20 also announced £670m of support for council tax support schemes in

2021/22. A similar scheme in 2020/21 paid this funding straight to billing authorities to support the council tax collection fund (effectively supporting the council tax collection levels and reducing the deficit that feeds into the 2021/22 financial year).

IP Part A: Overview 9

The £670m will effectively have the same effect for collection in 2021/22 – and reduce the potential deficit that would otherwise hit the Council in 2022/23. This time however the Government is paying the grant directly to all councils, rather than into the collection fund. An indicative allocation for HCC is in the region of £10.3m. Whilst District Councils will have made some estimate as to the possible levels of council tax support in setting the taxbase, the actual levels in next financial year are very uncertain. As such it is recommended that this funding is held to cover the position for the 2022/23 financial year – effectively doing the same as the approach in the current year. This position may need to be reviewed in year if the COVID financial impact is more significant than expected and cannot be contained within the grant position in 1.19 to 1.20 above.

1.22 The SR20 also included a pay ‘pause’ for the majority of public sector workers for 2021/22. The exception being health staff, and an uplift of at least £250 for all workers earning under £24,000. Whilst the Chancellors statement is not binding on local government, and the position remains subject to national negotiations that the council will adhere to, it is likely to impact on the level of pay. In light of this uncertainty, the budget includes cover for 1.5% cost.

1.23 The council continues to invest to deliver services more efficiently and with better outcomes for users. We will continue to prioritise frontline services – the vast majority of new savings proposed are from efficiencies rather than policy changes impacting service delivery.

Planning assumptions

1.24 As in the previous IP, revenue and capital plans have been set for a four year period which is now extended out to 2024/25. However, while core government funding for 2021/22 is covered by the SR20 announcements, revenue funding beyond this is uncertain (as discussed earlier).

1.25 For the IP period, in line with pre-2020/21 trends, services will face a return to

demand pressures from population changes, not only from the growing elderly population but more significantly from learning disability and children looked after and special education needs transport. This higher demand has impacted the market for social care, increasing prices for specialist care.

1.26 Revenue budgets (the net running costs of the Council’s services) are based on the

current year budget, which is then adjusted for inflation, for any unavoidable changes (for example population increases) and any new legal and statutory responsibilities. Any avoidable changes are challenged. This has been a key feature of this year’s IP, with any increases already included in 2021/22 as part of the previous IP round being reviewed. Once complete, the resulting costs are compared to forecast overall funding, with the difference – the budget gap – to be met by making savings.

1.27 The Council has also considered where investment will help significantly improve services, or to drive forward the corporate plan and priorities.

1.28 The Council has further developed its Capital and Investment strategies to make best use of these resources, recognising the impact of capital spend on the revenue

IP Part A: Overview 10

budget, and the opportunities to add value and generate income streams from this investment. The proposed Capital Programme also invests in the infrastructure that will be needed for a rising population and to support economic growth.

Key decisions in IP 2021

1.29 Key decisions in this Integrated Plan include

• To raise council tax by 1.99% in 2021/22;

• To include a social care precept at 2% in 2021/22 and 1% in 2022/23; i.e. a total council tax increase of 3.99% in 2021/22 and 2.99% in 2022/23.

• Planned efficiency savings to be delivered in all years;

• Provision for specific inflation on spending budgets where there are contractual or statutory increases, but otherwise requiring services to absorb non pay inflation within existing budgets (part G refers);

• Continuing to review pay levels for care staff;

• Proposed levels of capital investment, and the planned funding to achieve this;

• The requirement to provide forward funding for schools expansion schemes where developer contributions are only expected to be received at a late stage in the construction process;

• Use of planned capital receipts based on specific properties and opportunities to support the capital programme and reduce borrowing costs, whilst also earmarking surplus sites for operational use, or for development to generate enhanced future receipts and/or income streams; and

• Setting out principles for the disposal of specific assets to fund new capital projects, where there is a reliable business case.

• An initial estimate COVID-19 costs and funding have been included in the enhanced contingency within the budget. Beyond this the current assumption is that there is sufficient funding within the allocation from Government outlined above. Further risks around this are covered within the CFO’s statement.

Budget 2021/22

1.30 The proposed 2021/22 revenue budget is £877.185m. Table 1 in Appendix A at the

end of Part A summarises the movements from the 2020/21 original budget over the Integrated Plan period 2021/22 to 2024/25; the budget by department is shown in Table 4 in Part G (Other Technical Information).

1.31 Key movements from the previous IP are set out in the table below. This table

shows how the budget for 2020/21 was in balance (1 – net revenue budget 2020/21) and moves to a balanced position for 2021/22 (4- net revenue budget 2020/21).

1.32 What is apparent is that whilst total savings planned for next year are high at

£16.5m, the majority of these were already planned and approved as part of the 2020/21 IP, and only just over £3m is new savings. This indicates how difficult is it becoming to identify new savings, and the approach followed in this IP to balance the budget has been more about challenging the budget increases planned and looking to reduce those where possible.

IP Part A: Overview 11

Table 4: Analysis of the overall Budget Movement between 2020/21 and 2021/22

£m £m £m

Expenditur

e Income Net

1) Net Revenue Budget 2020/21 858.568 (858.568) 0.000

Pressures on budget:

Inflation – pay 3.602 3.602

Inflation – non pay 6.062 6.062

Pressures – demography 2.819 2.819

Pressures and investments – other:

Adult Care Services 10.000 10.000

Children's Services 2.897 2.897

Environment & Infrastructure 3.824 3.824

Resources 3.819 3.819

Other 5.573 5.573

Increased Capital Financing Costs 3.292 3.292

Increase to Contingency 4.078 4.078

Reduction in New Homes Bonus 0.912 0.912

Impact of Reduced Taxbase 3.795 3.795

Collection Fund Balances (net of 75% funding)

5.287 5.287

2) Increase in pressures 45.966 9.994 55.960

Met by:

Inflation – income (1.828) (1.828)

Reversal of one-off items from 2020/21

(11.159) (11.159)

Existing savings / policy choices (13.377) (13.377)

New efficiency savings (2.764) (2.764)

New policy choice savings (0.380) (0.380)

Technical Adjustments and Savings (29.508) 0.000 (29.508)

Public Health Grant 2.159 (2.159) 0.000

Business Rates Retention Scheme (0.592) (0.592)

Other Central Grants (0.370) (0.370)

Council Tax 1.99% Band D increase (12.753) (12.753)

ASC 2% Precept (12.738) (12.738)

Funding 2.159 (28.611) (26.452)

3) Mitigation of pressures (27.349) (28.611) (55.960)

4) Net Revenue Budget 2021/22 877.185 (877.185) 0.000

1.33 The movement from 2020/21 to 2021/22 shows increased pressures on the budget, with an overall increase in pressures of £55.960m, made up of £45.966m of proposed increases to spending and £9.994m of decreases in income items (2 – increase in pressures). This includes the £5.287m of reduced Collection Fund

IP Part A: Overview 12

balances and a £3.795m impact on the reduced taxbase due to an increase in Council Tax claimants and reduced collection rates.

1.34 These pressures were mitigated through a combination of technical adjustments

that reverse previous one-off expenditure items and increases in savings, totalling £27.349m, and increased income items of £28.611m (chiefly the planned increase in Council Tax and Adult Social Care Precept).

1.35 Key movements from the previous IP, set out in the table above, are described in

more detail below.

• Inflation: o As noted above pay inflation is modelled at 1.5% for 2021/22 (2% for

2022/23 onwards). These give a total cost of £3.6m for 2021/22 (£4.9m pa thereafter).

o Standard non-pay expenditure inflation has been frozen again for 2021/22, with only exceptional service specific inflation applied where, for example, contracts stipulate a requirement to uplift prices by inflation. Full detail can be found in Part G.

• Pressures and investments: Demographic change in the elderly and child populations, together with growth in Learning Disability and other social care client groups, continues to generate the greatest pressures over the medium term. These forecasts have been subject to detailed review and challenge. For 2021/22 there is a one-off fall in Demography caused by the pandemic in the Older People service area. This is a one-off base reduction with the normal upward trend applying to all future years.

In addition, investments are continuing in services. These are summarised in para 1.5 above, with more detail included in the individual portfolio sections.

• Grant Reductions: A legacy year of New Homes Bonus has dropped out of the scheme creating a £0.9m reduction in funding. This reduction has been partially offset by marginal increases in other central grants for2021/22.

• Collection Fund: The collection fund reflects the year-to-year differences between estimated and actual collection of Council Tax and Business Rates, due to changes in collection rate and levels of base-growth. The impact of the pandemic has generated a deficit for 2020/21 of £10.4m. The financial impact has been offset a Government commitment to fund 75% of the 2020/21 deficit, and a statutory allowance to spread deficits over a three period. The spreading allowance will reduce the annual charge General Fund to £3.5m p.a. This will then be offset by the 75% government funding, which we have forecasted to be £7.9m. Once spread over the three years this will result in a final annual deficit charge of £0.9m p.a. A 2019/20 residual surplus of £1.6m will be released in 2021/22 creating a net surplus of £0.7m (the 2020/21 comparable was a surplus of £6.0m).

• Reversal of One-Off items & Technical adjustments: This figure represents the reversal of items included in the budget for 2020/21 as one-off values

IP Part A: Overview 13

(which therefore need to be removed from the 2021/22 base budget). This primarily reflects the removal of a contribution of £11.1m to the Invest to Transform Reserve made in 2020/21.

• Savings: Existing savings options have been reviewed to confirm they are deliverable, and deferred where this is not possible (mainly due to the impact of COVID on plan). Some new efficiency savings have been identified. Officers will continue to monitor delivery of savings during 2021/22, and report on any issues in the quarterly Finance monitor.

• Business Rates Retention Scheme: Inflationary increases in the Settlement Funding Assessment agreed by Government is forecasted to be marginally greater than the reduction in the number of companies paying rates. The economic impact of the pandemic on business and business rates is still not fully known and will be an area of risk for 2021/22 and the medium term.

• Council tax / ASC Precept: A forecasted reduction in the taxbase across the county has generated a £3.7m reduction in billing for 2021/22. The impact of the pandemic has created an uplift in the number of Council Tax Support (CTSS) claimants and an increase in the provision of uncollected debts. These reductions in the taxbase have been partially offset by new houses, but it has still created a 0.6% reduction between years. The anticipated increases in the Band D rate of 1.99% on the general bill and an additional 2.00% for the ASC Precept has created an estimated net £21.7m increase in revenues for the council.

Investing in tackling inequality

1.36 Additional funding provided by the final information from district councils gives the

Council the opportunity to create a budget that can be used to tackle inequality.

1.37 The council has responded rapidly during the pandemic to support communities, including initially through operation shield to deliver essentials to vulnerable families, and then developing this further through operation sustain to support those in need through provision of grants, essentials and other support in conjunction with the voluntary sector. This is on top of existing support arrangements including the money advice unit.

1.38 As our thinking moves beyond the immediate response, it is clear that the pandemic will have longer term impacts, including on inequality. This is being driven through a number of factors, including the impact on the economy and schools.

1.39 Research from the Institute of Fiscal Studies, has outlined:

• The coronavirus pandemic is affecting our social, economic and family lives dramatically and in widely-varying ways, and its potential for impacts on inequalities not only now but in the longer term is huge

• Excluding key workers, most people in the bottom tenth of the earnings distribution are in sectors that have been forced to shut down, and 80% are either in a shut-down sector or are unlikely to be able to do their job from home – compared with only a quarter of the highest-earning tenth.

IP Part A: Overview 14

• About 30% of low-income households pre-crisis said that they could not manage a month if they were to lose their main source of household income.

• We came into the crisis with female employment at record highs, but school and nursery closures removed the childcare provision that had made much of that possible

• School shutdowns are likely to accentuate the socio-economic divide in educational attainment

• But it will bring opportunities too. An increase in remote working could be especially helpful for mothers’ careers. Widespread working from home may reduce the dominance of London.

• Policymakers have rightly been consumed by the immediate response to the crisis, but attention should already be turning to the longer-term effects.

1.40 The additional funding will be used to create the following budgets:

• 2021/22 - £5.5m (utilising all additional funding available)

• 2022/23 to 2024/25 - £2m per year to enable initiatives to continue, but recognising that currently budget gaps still remain in those years

1.41 Establishing this budget will enable the council to bring forward proposals to help tackle some of these longer term issues of inequality, including (but not limited to):

• Support for economic recovery

• Investment in skills

• Support for families

• Children’s wellbeing and education 1.42 The Council will work with partners, including the voluntary sector, in developing

these initiatives.

Chief Finance Officer assurances 1.43 It is a requirement of every Council budget that the designated s151 officer (Chief

Finance Officer) provides assurances through a ‘Section 25’ Statement on:

• The robustness of the estimates presented to Council, and

• The adequacy of the reserves available to the Council, given the risks and uncertainties it faces.

1.44 The formal statement is provided as Appendix B at the end of Part A.

2 Revenue Budget – Funding

Provisional Finance Settlement

2.1 The provisional local government finance settlement was released on 17 December 2020, through a written ministerial statement. The national levels of Government Grants announced were in line with the Spending Review 2020 in November.

2.2 The Government also calculates authorities’ Spending Power, which includes income from locally raised Council Tax and Adult Social Care Precept. The Council’s Spending Power for 2021/22 is £861.9m, of which £179.9m is funded by central government grants and business rates. Government claims this is a 5.2%

IP Part A: Overview 15

increase. However, this figure does however assume we have applied the full 3% ASC precept in 2021/22, and that the taxbase has increased (whereas in fact it has decreased).

2.3 The graph over the page illustrates the changes in separate elements of the Core Spending Power since 2015/16. There has been a fundamental switch from government funded resources as the Council’s Settlement Funding Assessment has reduced by 45% over the six-year period. Council Tax represents 79.1% of funding sources (66.3% in 2015/16).

2.4 The ministerial statement announced a Spring 2021 consultation on the future of the New Homes Bonus scheme, stating that “It is not clear that the New Homes Bonus in its current form is focused on incentivising homes where they are needed most” and the consultation will “include moving to a new, more targeted approach that rewards local authorities where they are ambitious in delivering the homes we need, and which is aligned with other measures around planning performance”. This was also confirmed in the provisional settlement press release, stating “We will soon be inviting views on how we can reform the scheme from 2022-23 to ensure it is focused where homes are needed most”.

2.5 The further extension of Business Rates Retention, and the implementation of a Fair Funding Review that will re-assess funding need across all authorities are expected to be introduced in 2022/23 at the earliest now. Whilst there may be some transitional protection, these changes may give some significant funding movements.

2.6 The funding position at Appendix A shows the latest estimates of available Central Government funding based on the technical consultation on the financial settlement, together with projections of other income sources including Council Tax and Business Rates Collection Fund balances.

2.7 The provisional settlement outlined the provision for the social care precept to 2022/23, allowing social care authorities to raise the precept by up to 3% across 2021/22 and 2022/23. Additionally, it confirmed referendum threshold for General Council tax increases to be used for 2021/22 as 1.99%.

0

100

200

300

400

500

600

700

800

900

1,000

2015-16 2016-17 2017-18 2018-19 2019-20 2020-21 2021-22

MIL

LIO

NS

Core Spending PowerCouncil Tax (including ASC Precept) Settlement Funding Assessment Other Grants

IP Part A: Overview 16

2.8 The provisional settlement further confirmed the SR20 announcements, where the

Chancellor announced a repeat of new funding announced as part of SR19. Additionally, a £0.3bn amount of a further funding for social care was announced. This is to be divided into an amount to ensure that authorities with low council tax bases are not at detriment (i.e. more properties in the lower council tax bands). This will create a fund of £240m. The balance of £60m is expected to be distributed on the relative needs formula (RNF) basis; the provisional settlement has indicated the Council will receive £1.0m. Other benefits outside this amount include confirmation of Better Care Fund (BCF) funding and the social care support grant being repeated. Notifications on the funding amounts for the following grants are expected soon; Public Health Grant, funding for firefighter pensions costs, as well as a range of smaller grant amounts. For all grants there remains uncertainty about future years.

2.9 Overall, the benefit of these announcements is £21.6m in 2021/22, with the social care precept increase of 2% providing £12.7m of this. The £1m additional Social Care Grant has not been built into the budget at this stage.

2.10 The gap between forecast expenditure and resource funding is widening over the period of this Integrated Plan, as shown in the table below.

Business Rates 2.11 Business Rates income is received as a proportion of income collected by local

District/Borough councils, increased by “top up” from, or reduced by “tariff” to, central government to an assessed baseline level of need. Income increases each year by the nationally set rate (based on September CPI).

2.12 Estimates of business rates income in Hertfordshire for 2021/22 was confirmed at

the end of January by district councils, who act as billing authority.

2.13 Government has invited business rates pools applications for 2021/22, in a similar approach used as 2020/21. It has been confirmed that Hertfordshire will form another pool in 2021/22, similar to that formed for 2020/21, but comprising a different mix of the County Council and 5 districts and boroughs (It is not

800.0

850.0

900.0

950.0

1000.0

2021/22 2022/23 2023/24 2024/25

£mFunding Gap

Total Funding Expenditure forecast

IP Part A: Overview 17

advantageous to include more of the districts otherwise the overall return to Hertfordshire reduces). The final decision to proceed with the pool was taken by the six councils in early January based on a final review of the latest forecasts. Grants

2.14 Table 2 in Appendix A shows the grants provisionally announced for 2021/22. Non-ringfenced grants are available to support all Council services, although where these relate to specific services the relevant service budget is normally increased to reflect the funding.

2.15 Ringfenced grant is received for Public Health responsibilities.

2.16 There are still a number of outstanding Government grant announcements, including some smaller non-ringfenced grants.

Council Tax and Social Care Precept

2.17 The 2020/21 IP assumed a general council tax increase of 1.99% in 2021/22 and in the years thereafter.

2.18 In the Provisional Settlement, the referendum threshold for General Council Tax increases to be used for 2021/22 as 1.99% has been confirmed. Additionally, the Secretary of State allowed Adult Social Care authorities to raise council tax by up to a further 3% across 2021/22 and 2022/23. The budget proposes that the Council will take advantage of the flexibility in council tax for adult social care, but will spread this across 2 years as follows:

▪ 2021/22 – an extra 2% (so 3.99% in total) ▪ 2022/23 – an extra 1% (so 2.99% in total)

It is felt that this approach strikes a balance between minimising the council tax burden for residents, whilst enabling investment in critical services.

1,100.00

1,200.00

1,300.00

1,400.00

1,500.00

1,600.00

Authority (County Councils with Fire Responsibilities)

2020/21 Band D Council Tax

IP Part A: Overview 18

2.19 The Band D Council Tax for Hertfordshire County Council in 2020/21 was

£1,414.20 which compares with a county council with fire responsibilities average of £1,405.06, ranging from £1,285.42 (Northamptonshire) to £1,527.44 (Oxfordshire).

2.20 The final council tax base and collection fund balance estimates for both Council

Tax and Business Rates were provided by districts in late January. These reflect changes in the tax bases for Council Tax and Business Rates, together with the collectability of income, impact of reliefs and business rates appeals (which may have a significant backdated element). The IP presented to January Cabinet is based on information provided by districts during the Autumn.

2.21 The current taxbase position used in the calculation of the 2021/22 Council Tax precept is a 0.6% reduction from the 2020/21 taxbase. There are a number of variables which impact the net taxbase position used for the calculation of Council Tax receipts, but the main movements in variables are explained below:

• Growth in households – a reduced rate of growth has been achieved in the last 12 months due to the impact of the pandemic; and subsequent lockdown and working restrictions which continue to be in place. For the 12 months to September 2020 there has been an increase of 0.8% in billable properties.

• Increase in claimants of Council Tax Support – due to the pandemic, and the impact on the economy and the higher rate of unemployment, more residents qualify for support in paying their Council Tax bill. By Q2 of 2020/21 working age claimants in Hertfordshire had increased by 8.2% over the 12 month period.

• Reduced rates of collection – the forecasted collection rate across all billing authorities has fallen by an average 0.75% to 97.85%.

2.22 Within the financing budgets for 2021/22 the level of Council Tax receipts has

increased by £21.696m between years. This is the net increase which incorporates the 3.99% in Band D (including the 2% ASC precept) offset by the reduction in taxbase. The table below splits the £21.696m increase into the relevant elements.

Element Band D Taxbase Amount

£m Commentary

1.99% Basic Uplift 28.15 453,039.9 12.753 1.99% Band D if taxbase was flat

2% ASC Precept 28.28 450,408.8 12.738 2% Extra billed using the new taxbase

1% Taxbase Reduction 1,442.35 (2,631.1) (3.795) Reduction in taxbase on non-ASC element

Net Movement 21.696

Budget and Council Tax consultation

2.23 In preceding years, the council has consulted and engaged with residents earlier in the Integrated Plan process, using a variety of methods, to seek their views on their broad spending priorities rather than about the financial proposals included within the Integrated Plan.

IP Part A: Overview 19

2.24 Covid-19 affected these timescales and the resourcing for the usual engagement and consultation process. Engagement this year has therefore instead coincided with the publication of the draft Integrated Plan and the proposed budget for 2021/22, necessitating a shorter window for engagement than in previous years. The draft Integrated Plan and proposed budget documents were published in advance of Cabinet’s consideration of the draft Integrated Plan 2021/22 at its meeting on 18 January.

2.25 A full report on the consultation is provided separately on the 22nd February 2021 Cabinet agenda. But in summary:

• 59.9% of total respondents supported an increase in council tax by up to 1.99% to maintain services

• 52.6% support a further 2% increase in Council Tax (through the Social Care Precept) to support adult care services

2.26 In light of this, the council tax proposals remain as per the draft IP, in that the Council will take advantage of the flexibility in council tax for adult social care, but will spread this across 2 years as follows:

▪ 2021/22 – an extra 2% (so 3.99% in total) ▪ 2022/23 – an extra 1% (so 2.99% in total)

2.27 It is felt that this approach strikes a balance between minimising the council tax burden for residents, whilst enabling investment in critical services.

3 Risk Management, Uncertainties, Contingency and Sensitivity Analysis Risk Management

3.1 Service departments have reviewed the risks attached to delivering the 2021/22 budget and reflected any significant risks in the Corporate Risk Register. The Corporate Risk Register is reported regularly to the Audit Committee.

3.2 The Audit Committee advises the Executive on relevant audit matters including the

risk management system and risk related issues. This function has been exercised through regular reports concerning the operation and effectiveness of the Corporate

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Strongly agree or agree Neither agree nordisagree

Strongly disagree ordisagree

No response

% of total respondents

Strongly agree or agree Neither agree nor disagree

Strongly disagree or disagree No response

IP Part A: Overview 20

Risk Process and updates on other risk management activity. To strengthen the Committee’s effectiveness in this oversight role, the Committee also considers, at each meeting, a report that focuses on a risk or risks from the Corporate Risk Register based on a particular theme.

Identified Risks and Uncertainties

3.3 A number of risks and uncertainties exist over the medium term which could potentially increase or decrease costs, including:

• Risk that social care costs escalate above the increases already included within the IP:

- Social care costs typically involve packages of care being arranged dependent on an individual’s needs. Budgets for social care are set based on estimated future levels of activity and average costs for different types of care package. In the event that either costs are greater than anticipated, or demand levels exceed those estimated, overspending can arise.

- This type of risk is especially related to: ▪ adult disability services, ▪ services for older people, ▪ independent placements for children with complex needs and

provision of services for unaccompanied asylum seeking children, and

▪ home to school transport (which is provided for children with complex needs).

- Mitigations are in place to manage these risks, however the volumes of activity, values of budgets involved (more than 50% of net revenue budgets), and level of financial constraints being experienced can mean that a relatively small level of change can lead to significant variations emerging.

- It may be that it is not possible to reduce the cost pressures in a specific area without severe impact. As such the Council often looks across its entire budget to find offsetting savings

• Risk of provider failure (including social care provider failure) - This risk is currently acute in the social care market, and there is a risk to

the Council that a contractor may withdraw from the market with little prior notice, or that a provider may be deeded ‘inadequate’ and so be forced to hand back its contracts. The need to make alternative arrangement may lead to increases in costs.

• Significant uncertainty surrounding the provision and cost of Personal Protective Equipment by the Governmental Portal. If this responsibility falls to the council the cost could be substantial.

• The NHS Winter Plan identified potential legislation around continuing Infection Control procedures for care providers. Funding was given from Central Government for 20/21, however no indication of funding has been given for 21/22, which could fall on HCC to provide.

• Should the Supreme Court overturn a court of appeal ruling on sleep-ins, Adults and Children’s social care providers could request that HCC funds six years of

IP Part A: Overview 21

backdated payments to enable them to pay National Minimum Wages for sleep-ins provided. There is uncertainty regarding the timing or value of the liability which this could generate, but initial estimates are significant.

• Risk of not realising savings as planned, examples include: - time taken to implement new social care strategies in the current

environment - the fragility of the independent care market - realisation of street lighting energy savings

• Tender pricing; the Council is exposed to the risk that wider economic factors may lead to the tenders received for future procurements being significantly higher than anticipated, leading to unexpected budget pressures. This is exacerbated by companies that have got themselves into financial difficulties on public sector contracts e.g. Carillion This is more likely in construction contracts but may also affect contracts for services.

• Risks and uncertainties associated with Brexit. There are a number of risks that have been identified that may arise, with different consequences. Significant uncertainty remains over these risks and the way they may be transpire for the Council. Identified risks will be monitored during the coming months. Key risks include

- workforce availability for the safe delivery of services; - the impact of inflation rate or interest rate volatility on the Council’s

suppliers; the impact of the same changes on the Council’s investments and borrowing costs;

- the impact of relative economic buoyancy or sluggishness on the local population and businesses and the consequent impact upon business rates receipts and wider local prosperity;

- the possibility that any impact from Brexit may also be different between the short and medium term impact

• Risk to contributions from Clinical Commissioning Groups for protection of adult social care and funding of children’s services.

• Highways maintenance: risk of road repairs due to severe winter weather and potential exceptional maintenance, including special requirements for coal tar disposal.

• Potential income from business rates growth; impact of business rate appeals following revaluation and changes to the appeals system.

• The Collection Fund balance and council tax base for future years, as well as council tax support schemes and wider council tax reforms.

• Inflation: non-pay inflation including exceptional inflation, an example being the potential for higher than expected increases in energy and transport costs; possible impacts on Council suppliers of input price changes arising from Brexit arrangements.

• Volatility in interest rates, impacting on borrowing costs and investment income (e.g. from Brexit decisions, but also from other economic factors); and

IP Part A: Overview 22

• Ability to sell assets and secure capital receipts.

• Following the outcome of the McCloud Firefighter Pension appeal, a settlement is still pending to determine any impact on the service such as backdated employer contributions. It is not known whether any settlement would need to be funded by HCC or whether government funding would be provided.

Contingency 3.4 The figures included in this report provide for a general contingency of £13.2m in

2021/22 based on an assessment of risks and uncertainties, as detailed above. This is an increase of £4.2m on the current contingency and includes an extra £5m of cover for COVID issues arising. This level of contingency has been taken into account when assessing the robustness of estimates and adequacy of reserves.

3.5 The 2021/22 financial year carries a number of significant financial risks which support the need to have a substantial increase to the contingency budget. The key risks are associated with the impact and recovery from the pandemic, the transition from the EU and any potential delay or non-delivery of savings. The contingency is budgeted to reduce back down to £8.5m in 2022/23 as the risks associated with the pandemic and the transition from the EU subside. It does still include some cover for potential COVID impact in future years, that will be reviewed as part of IP 2022.

Sensitivity Analysis

3.6 The Council’s budget is constructed using best estimates for both the levels and

timing of spending, cashable savings and resources. Table 5 below gives an indication of the sensitivity of the overall budget to movements in the assumptions underpinning our budgets.

Table 5: Impact of changes in our assumptions

Cash Impact

Impact on

council tax

Variable Change £’000 %*

1% change in number of SEN pupils requiring transport 180 0.03

1% change in numbers of Children Looked After (10 p.a.) 609 0.09

10% increase in Unaccompanied Asylum Seekers (10 p.a.) 96 0.01

1% change in older people client numbers (20 in residential/nursing care per annum)

684 0.10

1% change in Adult Care home care hours (16,534 p.a.) 390 0.06

1% change in Disability Services client numbers (9 in residential/nursing care per annum)

743 0.11

1% change in Disability Services client numbers (11 in supported living per annum)

582 0.09

1% increase in waste management spending 457 0.07

10 extra precautionary salting service outings for bad weather 300 0.05

IP Part A: Overview 23

Cash Impact

Impact on

council tax

Variable Change £’000 %*

10% change in emergency repairs needed on highways (cat 1) 854 0.13

1% increase in operational fire and rescue response activities 271 0.04

1% change in pay inflation 2,401 0.36

1% change in standard/income price inflation 1,041 0.16

+1% change in interest rates on borrowing (additional cost) 1,049 0.16

+1% change in interest rates on investments (additional inc.) 400 0.06

-1% change in interest rates on borrowing (reduced cost) 511 0.08

-1% change in interest rates on investments (reduced income) 299 0.05

1% change in Business Rates Retention Scheme 1,332 0.20

1% change in other non-ringfenced grants 316 0.05

£1 million change in collection fund balance 1,000 0.15

1% change in Council Tax 6,624 1.00 * This is shown only to quantify the theoretical impact in the context of council tax. It does not presume that if there were any such movement that it would be passed on through increased council tax.

Reserves 3.7 The Council retains reserves to respond to specific issues, and to protect the

Council, services and residents against risk. Council reserves fall into two main categories as follows:

• General Balances – this is the Councils main reserve for any unforeseen events. This is currently £31.6m, less than 3.7% of our annual net budget.

• Earmarked reserves – as the name suggests, these are established or held for specific purposes, or on behalf of other bodies.

3.8 The general fund balance is low at 3.7% of the budget. It should also be noted that

benchmark data indicates that Hertfordshire has one of the lowest levels of reserves in the country among county councils.

IP Part A: Overview 24

3.9 Whilst the general fund balance is low at 3.7%, the Council’s Chief Finance Officer (Section 151) has previously determined that the level of General Balances is acceptable when underpinned by the Earmarked Reserves in place (albeit that the original purpose for holding those reserves could no longer be met if they had to be used).

3.10 Reserve levels are reviewed as part of the Integrated Planning Process. This year this consideration has included:

• Assessing whether the level of General Fund Balances is sufficient given the level of risk and uncertainty faced in coming years

• Whether the commitments in some earmarked reserves remain appropriate – or if they are effectively being held as cover for a low level of general fund balance, should this be addressed

• The huge level of uncertainty on the financial position for future years, and that further support may be needed to cushion the impact in those years

• The need to support key priorities moving forward

3.11 The review has determined the following self-financing transfers are recommended for inclusion during the 2020/21 financial year:

Table 6: Reserves Review

Reserve Name

Projected Balance

Reviewed £000

Amount Released

£000

Amount Contributed

£000

Revised Balance

£000

Business Rates Equalisation (4,023) 4,023 0

Business Rates Retention Pilot (1,527) 1,527 0

General Contingency Reserve (2,123) 2,123 0

LAMS reserve (2,109) 2,109 0

Waste PFI reserve (6,000) 6,000 0

Investment Reserve (19,250) 14,250 (5,000)

Bad Debt Reserve (2,583) (1,600) (4,183)

Capital Financing Reserve (1,322) (2,000) (3,322)

Invest to Transform (20,792) (2,000) (22,792)

Sustainable Herts Fund 0 (2,000) (2,000)

Growth and Infrastructure Fund 0 (2,000) (2,000)

Capacity Review total 30,032 (9,600)

General Fund Reserve (31,568) (20,432) (52,000)

Overall Transfers 30,032 (30,032)

3.12 This enables the following:

• Creation of new investment funds of £2m each to support the Sustainable Hertfordshire strategy and to help support Growth and Infrastructure plans

• Removes funding from a number of earmarked reserves and enables the general fund balance to be at a more sensible level of 6% (effectively formalising the practice that has developed in recent years)

• Ensuring that there is sufficient cover for risks in the coming years, especially around COVID and the uncertainty over funding from April 2022

IP Part A: Overview 25

3.13 For the two new funds (Sustainable Hertfordshire strategy and to help support Growth and Infrastructure plans), proposals will be developed and subject to approval by the following:

• Relevant service portfolio Executive Member

• Director of Environment and Infrastructure

• Executive Member for Resources and Performance

• Director of Resources

3.14 These reserves are described in Table 10 in Part G of the Integrated Plan, together with estimated opening and closing balances. A summary of this is shown over the page.

Table 6: Reserves Summary

Reserves Summary

Balance at 1 April 2020 £000

Forecast at 31 March

2021 £000

Forecast at 31 March

2022 £000

Balances held on behalf of Schools (82,291) (61,918) (37,374)

Other reserves held for other parties (11,893) (9,877) (8,514)

Subtotal – Non-HCC Controlled reserves

(94,184) (71,795) (45,888)

Earmarked - Commitment (61,929) (39,317) (30,518)

Earmarked - Grant Funding (41,779) (9,111) (6,171)

Earmarked - Risk Management (39,176) (34,548) (33,798)

ITT - Invest to Transform (20,792) (21,881) (16,218)

Subtotal – HCC Controlled reserves (163,676) (104,857) (86,705)

Balances - General Fund (31,568) (52,000) (52,000)

3.15 In reviewing reserves, the following should be noted:

• A number are held on behalf other bodies and are not available for general Council use, including schools (£61.9m), the Local Enterprise Partnership (LEP) (£6.4m) and the Business Rates Pilot Fund Reserve (£2.6m);

• A further £105m are earmarked for specific purposes, which are split into four categories above:

o Grant Funding – non-ringfenced grant allocations from government being held to meet the desired outcomes of the funding agreements. The mains sums at the start of 2020/21 relate to COVID grants paid in 2019/20, but being used in 2020/21

o Commitment - these are reserves held for specific purposes or other commitments identified when establishing them. A key example is:

Insurance Reserve – used to provide self-insurance where cover is not available in the market or is uneconomic to secure. Also cover the excess cost for claims. The sums held are in line with independent advice from an actuary, and further detail is included in Part E: Insurance and Risk strategy

o Risk Management - these help provide cover for risks. The main reserve here is the transition reserve (circa £19m) that we have been contributing to in recent years to help cushion against future funding shortfalls.

IP Part A: Overview 26

Holding this reserve has been pivotal in enabling us to respond to COVID and support our communities, even when there was a substantial gap between the cost of those interventions and the grant received. This reserve continues to be essential in mitigating against the general uncertainty of future funding, and especially the short period between the settlement dates and the start of each financial year;

o Invest to transform Fund – used to invest in projects to transform services and generate savings. In the numbers above the forecasted balance at the end of 2020/21 is at £21.9m. Whilst the reserve forecast initially looks healthy, much of this reflects the timing of drawing down committed funds (i.e funds that have been approved, but not yet drawn down still show in the reserve balance). If all of the commitments were made this financial year there would be a residual balance of £13.2m. Increasingly in recent years, the scale of transformation needed requires significant investment to deliver. For example, some of recent approvals from ITT have included the Next Generation project at £4.1m, and the Children Looked After transformation programme at £2.4m

o Moving forward, we would expect further bids to support transformation, including to support new ways of working after the pandemic

• Balances are held for emergency purposes, and once used are gone.

4 Capital Programme, Funding and Financing Charges

4.1. The capital investment programme and the revenue cost of this is set out in the table below:

Table 7: Capital Programme and associated revenue costs

2021/22 £'000

2022/23 £'000

2023/24 £'000

2024/25 £’000

Capital Programme 366,703 361,074 279,812 204,568

Borrowing Requirement 185,212 168,028 139,330 83,559

Revenue Cost of Capital 30,066 38,698 48,756 55,188

4.2. As can be seen, the size of the capital programme and resultant borrowing results in a significant increase in borrowing costs for the council, from £30m to over £55m by year 4.

4.3. A breakdown by Portfolio of the proposed capital investment programme for IP 2020 set out in the table over the page, along with the planned sources of funding.

Table 8: Summary Proposed Capital Programme 2021/22 – 2024/25

2021/22 £’000

2022/23 £’000

2023/24 £’000

2024/25 £’000

Adult Care & Health 28,182 35,455 31,054 20,146

Children, Young People and Families 2,860 3,002 100 100

Community Safety & Waste Management 24,348 23,733 24,912 8,998

Education, Libraries & Localism 106,439 111,694 93,984 47,515

Growth, Infrastructure, Planning & Economy 47,395 67,560 31,485 32,260

Highways & Environment 94,897 89,580 86,408 85,691

IP Part A: Overview 27

2021/22 £’000

2022/23 £’000

2023/24 £’000

2024/25 £’000

Resources & Performance 48,688 30,050 11,869 9,858

Capital Investments 13,895 - - -

Total 366,703 361,074 279,812 204,568

Financed by: Borrowing 185,212 168,028 139,330 83,559

Capital receipts 25,969 15,528 13,642 10,750

Grant 137,130 138,850 93,241 92,191

Contribution 15,630 36,668 33,149 17,460

Reserves 2,763 2,000 450 608

Total 366,703 361,074 279,812 204,568

4.4. The Council continues to invest significantly in its infrastructure and assets. The

proposed capital programme in 2021/22 is £366.7m, of which £185.2m is funded from borrowing (i.e. HCC funded). In developing the refreshed four year capital programme, the Council has taken the existing programme and reviewed to ensure emerging issues and policy developments can be driven forward. This includes:

• £53m of investment in new Special Schools and specialist resource provision to enable delivery of the SEND strategy approved by Cabinet in December 2020

• £10m of investment in sustainable projects significantly drive forward delivery of the Sustainable Hertfordshire strategy approved by Cabinet in March 2020 with an action plan approved in December 2020, including £1.5m earmarked for pilot projects in schools energy initiatives. It will also enable the council to seek external funding, providing matched funding where needed, to maximise funding available to support the strategy

• £10m of investment for our Climate Change Response, providing additional capital funding to improve drainage in response to highways flooding brought about by increasing and changing rainfall patterns.

• £7m of investment to move forward roll out of 20 mph speed limits • £3m of investment in active travel schemes

• Investment in our waste infrastructure, including at our recycling centres with

equipment to minimise the environmental impact and cost of waste transfer

• Investment in technology to ensure the organisation can modernise and take advantage of new ways of working

4.5. In the early part of the last decade, the Council has used revenue contributions, one-off underspends and Capital Receipts to sustain the capital programme while minimising the need for new borrowing, thus avoiding the costs of interest and of Minimum Revenue Provision (MRP – the amount the Council is required to set aside in its revenue budget for debt repayment). As these sources are no longer available, during the latter part of the decade this has shifted to borrowing, and this trend continues to increase. This causes the significant increase in borrowing costs outlined in para 4.1 above.

IP Part A: Overview 28

4.6. The capital strategy and treasury management strategy are both included in the IP

pack in the usual way.

0

50000

100000

150000

200000

250000

300000

350000

400000

2015/16 2016/17 2017/18 2018/19 2019/20 2020/21 2021/22 2022/23 2023/24 2024/25

Capital funding sources 2015-2025 (£000)

Capital receipts Grants and contributions Borrowing Revenue contributions & reserves

IP Part A: Overview 29

APPENDIX A

Table 1: Summary Budget Movement Statement

Table 1: Summary Budget Movement Statement (2021/22 – 2024/25)

2020/21 £m

2021/22 £m

2022/23 £m

2023/24 £m

2024/25 £m

818.743 Original Budget 858.568 858.568 858.568 858.568

(16.213) Technical Adjustments 2.159 2.159 2.159 2.159

12.783 Inflation 7.837 24.022 40.559 57.093

815.313 Base Budget 868.564 884.749 901.286 917.820

Pressures for change:

(5.343) Reversal of time limited expenditure (11.159) (11.159) (11.159) (11.159)

11.757 Demography 2.819 13.618 24.634 34.809

5.597 Legislative 3.377 6.540 10.289 13.982

3.156 Capital Financing 3.292 11.339 19.876 26.228

45.225 Other 26.814 27.921 32.260 36.013

60.392 Total Pressures for Change 25.143 48.259 75.900 99.873

875.705 Subtotal 893.706 933.008 977.186 1,017.693

Savings:

(8.629) Existing Efficiencies (12.827) (21.464) (26.895) (40.057)

(0.779) Existing Policy Choices (0.550) (1.200) (1.200) (1.200)

(7.729) New efficiencies (2.764) (2.906) (3.150) (3.193)

- New Policy Choice (0.380) (0.380) (0.380) (0.380)

(0.000) Further savings required 0.000 (5.441) (22.103) (25.580)

(17.137) Total Savings (16.521) (31.391) (53.729) (70.410)

858.568 Resultant Budget 877.185 901.617 923.457 947.283

IP Part A: Overview 30

Table 2: Funding Statement

Table 2: Funding Statement (2021/22 – 2024/25)

2020/21 £m

2021/22 £m

2022/23 £m

2023/24 £m

2024/25 £m

49.255 Business Rates Retention Scheme: Business Rates Income 49.618 49.618 49.618 49.618

74.312 Top-up grant 74.312 74.312 74.312 74.312

9.079 Tax Loss Re-imbursement 9.307 9.307 9.307 9.307

0.396 Collection Fund Balance (0.433) (1.859) (1.859) (1.500)

133.041 132.804 131.377 131.377 131.737

Council Tax:

584.970 Council Tax Income 594.251 615.023 636.628 658.957

55.719 Council Tax Social Care Precept 68.133 75.693 76.639 77.597

5.606 Collection Fund Balance 1.148 (0.179) (0.179) -

646.295 663.532 690.537 713.088 736.554

Non-ringfenced Grants:

1.921 Revenue Support Grant 1.932 1.932 1.932 1.932

7.063 Social Care Support Grant 7.063 7.063 7.063 7.063

14.643 Social Care Support Grant 20/21 14.643 14.643 14.643 14.643

2.770 New Homes Bonus 1.858 0.711 - -

1.944 Independent Living Fund 1.944 1.944 1.944 1.944

2.197 Fire Pension Grant 2.197 2.197 2.197 2.197

0.200 Teacher's Pension Grant 0.398 0.398 0.398 0.398

1.405 Other non-ringfenced grants 1.567 1.567 1.567 1.567

32.143 31.602 30.455 29.744 29.744

Ringfenced Grants:

47.089 Public Health Grant 49.248 49.248 49.248 49.248

47.089 49.248 49.248 49.248 49.248

858.568 TOTAL 877.185 901.617 923.457 947.283

IP Part A: Overview 31

APPENDIX B Local Government Act 2003: Section 25 Report of the Director of Finance 1. Introduction

1.1. The Local Government Act 2003 (Section 25) requires that when a local authority

is agreeing its annual budget and Council Tax requirement, the Section 151 Officer must report to it on the following matters:

• the robustness of the estimates made for the purposes of the calculations, and;

• the adequacy of the proposed financial reserves.

1.2. The Council is required to set a balanced budget and must have due regard to the advice of the Director of Resources (s151 officer). The following paragraphs therefore provide a commentary on the robustness of the budget and the reserves in place to support the Council.

2. National context

2.1. The extraordinary position caused by the COVID pandemic has been outlined in this document already. This has also in turn exacerbated high level of uncertainty in both political and public spending terms.

2.2. Beyond 2021/22 there remains considerable uncertainty over public finances generally, and for Councils more specifically as follows:

• A new Spending Review was expected during 2020. This was to outline overall levels of public expenditure from 2021/22 onwards. Due to COVID, this became a single year settlement for many areas of the public sector (only health, education and the armed forces had multi-year settlements). It is not yet known when the next spending review will be, or for what period it will cover

• COVID has led to significant increases in Government borrowing. It is not yet clear what the impact will be of this on public spending – and especially for those areas of the public sector, including Councils, who only have funding confirmed for one year.

• Government is still reviewing two major aspects of how funds are allocated to Councils:

o The fair funding review is proposing changes to how the total pot of government grant is allocated to councils

o The business rate review is looking at whether councils should retain a greater proportion of business rate income in their areas

2.3. In view of this there is a high level of uncertainty regarding the level of funding the Council can expect through government post April 2022. The position may only likely to be clear when the 2022/23 Settlement is announced in December 2021. Budget planning for this financial year will need to take into account the potential

IP Part A: Overview 32

risk and uncertainty around only knowing the grant position around 3 months before the start of the 2022/23 financial year.

2.4. The impact of COVID on our communities, finances and the economy remains extremely difficult to predict.

3. Local context

3.1. The Council has successfully delivered significant efficiency savings and, where necessary service reductions since 2010. Hertfordshire County Council has delivered nearly £2bn of savings overall in this period, and the current budget is some £334m lower than it otherwise would have needed to have been if those savings had not been made.

3.2. The Council has a proactive approach to financial planning and management, and a good track record of delivery. This is underpinned through the following processes, including:

• A robust budget setting and medium term financial planning process, including risk analysis and challenge on assumptions and estimates.

• monthly reporting to Senior Management Board on budget monitoring forecasts including any remedial management action required and formal reporting on delivery of savings; with further quarterly reports being provided to Cabinet.

• the operation of a robust risk management approach;

• the council’s internal control framework, including the financial regulations and the Scheme of Delegation for Financial Management which provides the framework for delegated budget management;

• the sustaining of good working relations with the external auditor (EY);

• the operation of the internal audit function and its role in assessing controls and processes to highlight any major weaknesses and advise on best practice.

• This practice has been demonstrated in the 2019/20 financial year, where an initial forecast overspend of £6.9m (which would have consumed all the contingency and required a draw down on reserves) was reduced through management action across the council, to a level of £2m that could be contained within the contingency

3.3. The position for future years continues to be challenging. The Council faces significant financial pressures from the continued impact of COVID and increases in demand for services, in particular, but not exclusively, for social care. Indeed in future years this increased demand is potentially a greater issue in terms of impact on the budget gap than grant reductions. Also it is apparent that further efficiencies have become harder to achieve and realise, and will require more resource and investment to achieve through complex transformation programmes and service re-design.

3.4. The 2021/22 Budget has been through the process outlined above. A range of potential risks are outlined in Part A of the IP documentation. Clearly the most

IP Part A: Overview 33

significant risk remains the impact of COVID on the Council’s budget. In the current financial year, the forecast additional cost to the council is in the region of £130m. For next year the level of additional cost remains very uncertain. To prepare for this the following approach has been undertaken:

• Initial forecasts of the COVID impact, both in terms of potential additional costs and lost income were included in the initial budget forecasts for planning purposes

• Departments have flagged areas where there may well be COVID related costs next year (including CLA, staffing pressures, works costs etc)

• Given the uncertainty, additional provision has been made in the Council’s contingency budget – increasing this to £13m next year

• The Council will also make a provisional outline for use of the initial COVID grant funding provided for next year – principally covering pressures in supporting adult social care providers and major infrastructure works

• Strong financial management in the current year, coupled with the level of grant funding received, means that the Council has not had to resort to using reserves in the 2020/21 financial year. These have been reviewed as part of the budget setting, to ensure they remain sufficient to meet potential risks ahead

3.5. In light of these steps, despite the uncertainty, overall it is the Chief Finance Officers opinion the budget is considered robust and deliverable.

3.6. Over the medium term the Council faces further financial pressures, as outlined in para 3.3 above. This means that the Council still has the following budget gaps in future years

2021/22 2022/23 2023/24 2024/25

£m £m £m £m

Savings to be found - 5.4 22.1 25.6

3.7. It is also important to consider how this has moved in recent years. This is