Embed Size (px)

Citation preview

INSURANCEThe Ultimate Risk Solution

2 CorpAssurance, Vol. 1, No. 3

Foreword

Dear Sir/Madam,

WHILE MANAGING RISK, REMEMBER INSURANCE

WHILE MANAGING RISK REMEMBER INSURANCE TO AVOID UNEXPECTED MONETARY LOSS

Managing Risk Is a ‘risky’ business. It moves between the two ends of compulsion and choice. It is difficult to manage an enterprise without getting exposed to certain types of risks.Going back to the basics, there are four techniques of Risk Management :a. Avoidanceb. Loss Prevention and Reductionc. Retention d. Transfer(Insurance) Insurance is a very important tool of managing risk. Money is collected by way of premium from many to be disbursed to a few who get saddled with claims.Insurance thrives on fortuity. If an insurance buyer were sure that there would be no claim, he would not buy a policy while by the same token if a seller were to feel that there was certainty about the claims being prohibitively high, he would not provide insurance. It is the element of Uncertainty which brings the two together. And yet insurance does not cover speculative risks. The risks covered are ‘pure’ in nature whereby in the event of the occurrence of a fortuitous incident, the monetary loss is imminent. Just as Risk Management is an integral part of an enterprise, Insurance should likewise be treated as integral to the Risk Management. Thus, as an EPC Contractor, our concerned project team should ensure that all the insurance policies are properly taken as per the Insurance Clauses of the contract with the Owner and also keeping in view the exposure which may go beyond the minimum requirements given in the said Clauses. Project policy whether taken by the Owner or the Contractor should have adequate covers commensurate with the exposure to different types of perils as in the event of a loss usually it is the contractor who bears the monetary brunt of failure of the policy to respond effectively to a claim. Even with regard to the usual sale and purchase of the items, one should be careful that the agreement is clear about the apportionment of responsibilities in regard to the purchase of insurance policies. If the responsibility is of the other party, it is advisable to sight the policy/ies and be sure of the correctness of the same. One should also be careful about the monetary- limit and the extent of the time- period for which the exposure remains. It is important to check-up the insurance requirements while working at the customer’s site. Risks are also related to the individuals as human beings. Therefore, it is necessary to ensure that the employees remain properly covered under the policies for mediclaim, life- term cover and personal accident. Going by the past experience one may safely state that all these policies come in very handy for the employee or his family members. Hence, we need to pro-actively evaluate our risks, more so in a highly diverse company as ours, and use Insurance as a risk transfer mechanism.

With best wishes,

Pradeep SinhaHead-Corporate Insurance

CorpAssurance, Vol. 1, No. 3 3

In Focus

Nature is benign and bountiful, but her vagaries can be devastatingly disruptive. Weather-borne risks are today the most lethal ones faced by the economy in particular and mankind in general. A World Economic Forum survey cites weather-borne risk as the most impactful risk confronting business. Climatic and weather changes have been common phenomena for millions of years. Change in these patterns has been gradual, and their impact imperceptible. Enter the Industrial Revolution. The widespread use of fossil fuels. The galloping use of minerals and metals. Automated transportation, industrial production. Massive deforestation. All this has led to an increased momentum in the process of the climatic change. The recent IPCC Report states that the earth’s temperature

has increased by 0.85 Centigrade since 1880. Of this increase, 95% can be attributed to carbon emissions from man-made activities. The process of climate change is expected to accelerate further over the next 20 years. Fast-increasing warmer temperatures will lead to an increase in the severity and frequency of weather disasters. We can look forward to fast-melting glaciers and rising seas, as well as shifts in rainfall patterns and climatic zones (for example, Maharashtra experienceing the weather of Rajasthan, and Mumbai being completely submerged by the sea). Leading global reinsurer Munich Re has ranked cities under the threat of natural disasters. New York was identified as the U.S. city most exposed to storm surges, with just over a million people at risk. China’s Pearl River Delta ranked No. 1 globally, with 5.3

million people said to be in harm’s way. “In U.S.A., there is a spread of approximately $10 trillion of insurable assets along the sea-coasts, and as deliberated at the World Climate Congress, the vast majority of these assets is designed to withstand climatic events of the past, not that of the future.”

Risks from climate and climate change are related to:• Theextentanddurationofweatherand climate events (see diagram below);• The type, relevance and skill of information that is available about the risks (e.g., current monitoring forecasts, outlooks, scenarios);• Thevulnerabilitysuchchangesmay expose the economy to in general and to agriculture in particular

Weathering the Weather

4 CorpAssurance, Vol. 1, No. 3

In Focus

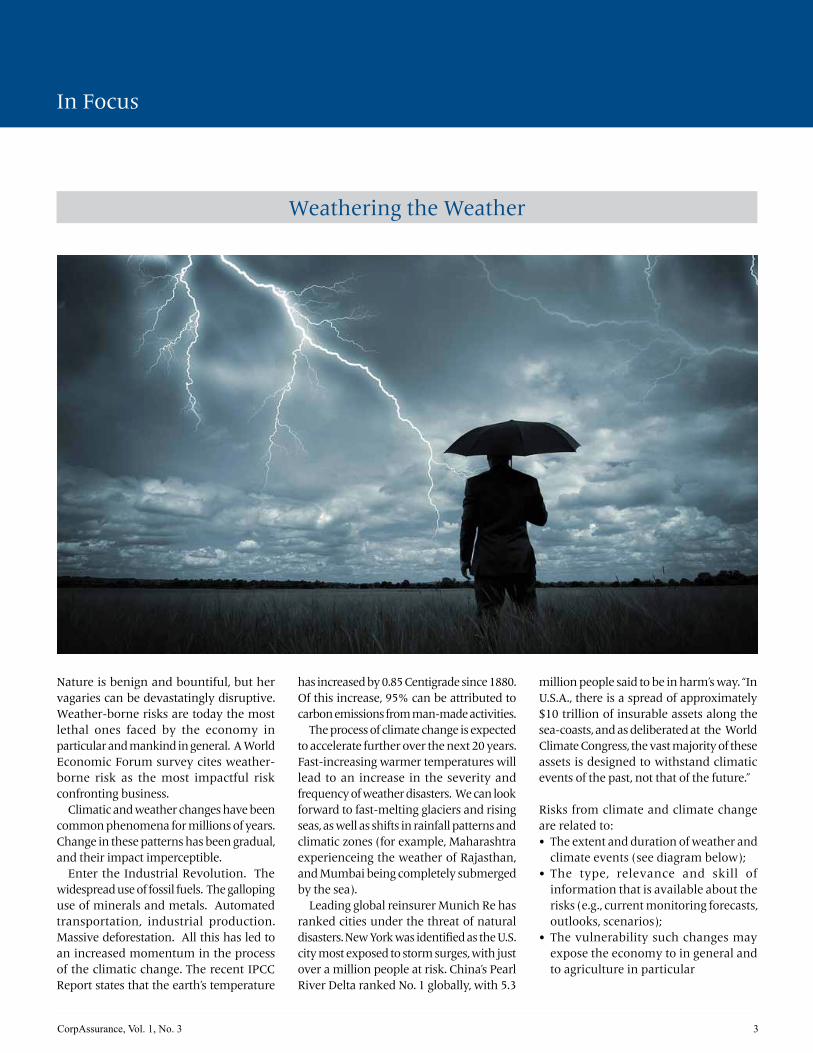

Doing the MathIt has always been a challenge to quantify the losses due to climatic change. Various models have been designed, tested and applied to real-life situations.The model developed by Swiss Re touches upon the following parameters:• Hazard: Severity and frequency of the hazard for different climate change scenarios :H• Asset Module: Geographically distributed value of assets, incl. incomes :A• Vulnerability : Vulnerability for different assets based on hazard severity :V Expected Loss per Climate Change

Scenario: H*A*V It has estimated that globally different locations on the surface are exposed to 1-12% loss of GDP due to climate-related factors Generally, weather-borne risks take the form of gyration in pressure, precipitation and general temperature. Weather risks are different from other classes of risk as they tend to play out at diverse timeframes, i.e. from short-term to long-term and extend for varying expanses – from a few kilometers to a landmass of an entire continent.

Natural CalamitiesThe massive devastation of calamitous

‘Acts of God’ – like floods, cyclones and storms – are perils caused by wildly erratic atmospheric factors. An earthquake is the culmination of geo-thermal dynamics operating under the surface of the earth. Natural calamities are always caused by atmospheric factors, but atmospheric factors do not always result in a natural calamity, e.g. a normal monsoon is a boon. Calamities impair capital assets while atmospheric fluctuations (which are milder) cause the loss of earnings. Nature’s calamitous effects can be brought under the ambit of a conventional insurance policy. All property insurance policies offer insurance against Acts of God, i.e. perils like floods, earthquakes and

In Focus

CorpAssurance, Vol. 1, No. 3 5

cyclones. In some policies, these covers are in-built, while in others they are optional. The policies on the above-mentioned lines cover the impairment of assets. It is pertinent to note that, in a conventional Asset Insurance Programme, 80% of the total premium goes towards risk-pricing of the Acts of God Perils.

Combating Nature’s Negative Impact on AgricultureThe segment of the economy most vulnerable to nature’s vagaries is agriculture. For example, excessive rain may delay the sowing or damage the standing crop, hampering farmers’ earnings. In Maharashtra, the expected annual loss from drought stands at a whopping US$24 Billion – equivalent to 2.5% of the agricultural output. With the projected climatic change, the total annual potential loss can rise to US$57 Billion – that is , 45% of the total agricultural production. The Economics of Climate

Adaption (ECA) Working Group had estimatede that in Maharashtra, a specific event of magnitud such as a drought once in 25 years – may affect up to 30% of the regional population, which also includes 15 million small and marginal farmers. The same event would reduce 14% of the agricultural output and 30% of the food-grain production. It would increase the indebtedness of the farmers by 96%. In India, crop insurance as a risk management tool has been in practice, in diverse formats, for quite some time. It covers the loss of crops due to factors arising from inclement weather. The loss of the crop for each farmer is separately assessed and settled. The loss is measured in terms of the difference between the projected output and actual output, converted into monetary terms. It hase been noted that crop with inshurans the process of setalment is long-drawn-out and fraught with ambiguous. An alternative approach has been

Weather Insurance. In this case, weather event parameters have been indexed, based upon the historical data. In case the parameters waver from the predefined range, the pay-out follows. The larger the divergence from the range, the larger will the pay-out be – and vice-versa. The rainfall is the common parametric event in the India scenario. The concept of index-based contracts for broad-based natural disaster in place of crop insurance has been gaining in prominence in most of the geographies of the world. Apart from agriculture, weather insurance can be a major risk management solution for other businesses also, particularly those associated with agriculture, such as agrochemicals and agricultural equipment.

Article contributed by Mr Ajit VermaSr DGM, Corporate Insurance

Tapan Singhel, MD & CEO, Bajaj Allianz General Insurance, speaks to CorpAssurance on the impact of liberalization of India’s insurance sector.

1. Following the liberalization of the insurance sector in the early years of this century, what have been the changes in the insurance landscape of India?The idea behind opening up the insurance sector was to create awareness and improve penetration in the country. In the last 15 years, the industry has seen immense action. The number of insurers has grown to over 50 today. Besides capital, liberalization brought in significant changes in the product portfolio, channel mix and operational efficiencies that brought transformative reduction in customer service TATs. All these changes were driven by digital and technological enablers that changed the rules and disrupted the traditional value chains. Post- liberalization, the regulator was also ringing in new changes in the industry to streamline the sector. It was imperative for companies to quickly learn to anticipate change and allow flexibility in plans, strategies, systems and processes to respond faster. Some of the key developments that made a significant impact on the insurance landscape were de-tariffication, formation of a third-party pool, emergence of bancassurance as a significant distribution arm and rise of standalone health companies. The insurance industry is undergoing yet another transformation today. Digitalization has opened up major opportunities for us. It has given a breakthrough to deal with the challenges that we have been battling for over decades. It has affected all areas of operations of an insurer, including employees, customers and business partners. For instance, it has not only

helped us reach out to unrepresented geographies, but has also enabled the industry to provide ease of transaction and real time solutions to the customers. What continues to be a cause of concern is the unsustainable premium rates post de-tariffication and the insurance penetration in the country. De-tariffication was deemed as a logical step in the evolution of the general insurance sector in India. However, de-tariffing triggered a price war among the insurance providers, which we believe is not sustainable for the industry in the long term and needs immediate corrective measures. The intense competition without a simultaneous reduction in claims has led to a drop in profits. Despite various initiatives the penetration of General Insurance has not seen a significant improvement. It has moved to 0.7% from 0.5% in the last 15 years. The industry and its various stakeholders must collectively work towards taking insurance footprints to every corner of the country while ensuring a profitable and sustainable growth.

2. For many of the policies, for example, operational assets and projects, there is a reluctance in the market to provide comprehensive covers that commensurate with the exposure to hazards. Do you think that the market competition should also take into insurance covers along with premium rates?There are comprehensive covers available in the market, and they have evolved over time with the changing risk landscape. The Indian insurance market has adequately responded to these changes and rise of new-age risks. For instance, looking at the rising incidences of Natural catestrophic losses in the country, a new add-on cover called ‘Denial Access’ has been introduced recently under the business

interruption policy for business entities. Today, insurers do provide tailor-made policies and are open to providing add-on covers, looking at the specific needs of the client and the exposure the entity is subject to. The insurance industry and its various stakeholders need to sensitize the customers on why it is essential for the insured to look at and understand the covers being offered under the plan, along with the premium, before choosing an insurance provider. Premium should not be the single most important enabler for deciding on an insurance plan.

3. How will the coming of the Lloyd’s and the International Reinsurer in the Indian insurance market affect it?This is a welcome change for the industry because these international players will bring in international expertise and covers, which will lead to dynamic changes in the product and service offerings in the sector. Besides, this will give access to quality international capacity locally.

6 CorpAssurance, Vol. 1, No. 3

Tête-à-Tête

In Conversation with Mr. Tapan Singhel

Tête-à-Tête

CorpAssurance, Vol. 1, No. 3 7

4. With the risks becoming transnational like these related to cyber or D&O, what should the Indian insurance market do to eliminate the time lag in the introduction of such new policies in the western market and the Indian Insurance market.The regulator has addressed this through the revised product guidelines. The use-and-file system is a welcome move towards a self-regulatory environment, which will help the industry to come out with innovative products that meet our customers’ requirements much quicker. This will definitely aid us in launching more products in the near

future depending on the demand from our customers.

5. Do you foresee the Indian Insurance market hardening the premium rates? Why it has remained soft for so long?It is high time that the Indian general insurance industry realizes the challenges arising due to the unsustainable pricing and its repercussions in the long run. The industry collectively must start working towards right pricing to improve the industry’s revenue, combined ratio and – most importantly – bring in profitability. Risk-based pricing and not succumbing to market pressure will be beneficial for

both the industry and the customers. We are hopeful that this trend will be reversed in the coming quarters. One of the reasons for softening of premium rates was the mismatch in the capacity available and the demand. With more and more insurers companies entering the Indian market, the capacities have increased, however the market potential remained stagnant due to lack of awareness in the country. Besides, the constant flow of new companies with their focus only on growth also added to pricing pressures.

In conversation withMr Ajit Verma, Sr DGM

Insurance Company

Buyer Share percentageConsideration(Rs in Crores)

Enterprise Value(Rs in Crores)

Holding After Merger

ICICI Lombard Fairfax 9% 1,650 17,225 Fairfax:35%

ICICI Prudential Life

Tamasaek 2 650 48,000 Prudential:26%

HDFC Standard Standard 9 1700 30,000 Standard:35%

HDFC Ergo Ergo 22.9 1122 4900 Ergo:49%

Birla Sun Life Sunlife 23 1700 7,400 Sunlife:49%

Reliance Nippon Nippon 26 3,062 11,500 Nippon:49%

Max Bupa Bupa 23 190 826 Bupa:49%

Recent Merger and Acquisition Deals in India Insurance Market

8 CorpAssurance, Vol. 1, No. 3

Insight

Gas-based Combined Cycle Power Plants are an important source of electrical energy, as they offer certain advantages over the coalbased thermal power plants. The capital cost is low, energy efficiency high and are less polluting. In the combined cycle plant, waste gas is extracted from the turbine exhaust. This heat is used to generate steam to drive the steam turbine generator and generate additional electricity. This enhances the fuel-to-energy efficiency to over 50% as against energy-efficiency of 40-45% of the supercritical thermal power plants. Despite all the benefits provided by gas turbines and the increasing normalisation of this leading-edge technology achieved through numerous technical developments, certain risks are associated with these plants.

Major components of a Combined Cycle Plant

Gas Turbines (GT)Gas turbines are generally fired by natural gas/naphtha. The gas turbines convert thermal energy of the fuel air mixture to mechanical energy to drive a generator, which in turn generates electricity. A diverting damper attached to the turbine directs the hot combustible gases from the gas turbine to the HRSG or boiler.

GT has following Major Systems

Combustion ChamberThe gas turbine system consists of a combustion chamber where the fuel air mixture is burned. The inlet air is filtered and admitted through the air filter banks. The fuel is fed by the fuel system, and is atomised using air. Atomising air is supplied from auxiliary air compressors. Supplying purge air does the removal of superfluous fuel from the lines downstream of the fuel control valves.

Lubricating Oil SystemAs the gas turbines operate at very high speeds and temperatures, they need an efficient lubrication system. In many plants, the lube oil is stored in a reservoir, and pumped to bearing header, gears, generator and hydraulic supply system. The lube oil system is fitted with a trip system so that in case of reduction in oil pressure, fuel stop valves automatically stop supply of fuel to gas turbines.

Starting SystemThis provides the necessary cranking and turning power for starting the turbine. It is necessary that the gas turbine is operated at about 100 to 200 RPM prior to start-up and also during the cooling period after unit shut-down. Heat Recovery Steam Generator (HRSG)The function of the HRSG is to utilise the waste heat of the gas turbine exhaust gases to generate high-pressure steam. The HRSG harnesses this energy, and uses it to generate additional electricity, thus increasing the unit’s efficiency. The water for steam generation is supplied from the DM plant. This high pressure and high temperature steam is then used to drive the steam turbine. Exhaust steam from the turbine is then condensed in the water-cooled condenser and again fed to the boiler. Thus the cycle is a closed cycle.

Steam Turbine The steam turbine converts the thermal energy of steam into mechanical energy, which in turn, is used to drive the generator and produce electrical energy. A steam turbine consists of two sections, viz., high pressure and low pressure. High-pressure steam is supplied from the common main steam header from all the three HRSGs through two stop and control valves and low-pressure steam is supplied from the common low-pressure main

steam header through a one-stop control valve. A turning gear arrangement keeps the steam turbine rotor continuously turning during shutdown.

Balance of Plant Equipment (major)

TransformerPower evacuation is done using transformers. These transformers step up the voltage from 11kV to 220 kV for transmission to the grid.

The Raw Water SystemSupplies water to the water pretreatment plant. In the pre-treatment plant the water is softened prior to sending it for condensor cooling.

Demineralised Water PlantThe water is treated for removing dissolved contaminants such as salts and silica, and is sent to feed the water supply to the HRSG. In the pre-treatment plants, chemicals are used to improve the water condition.

Loss ExposuresDue to the rapid technological advancements discussed above, Combined Cycle Power Plants have been exposed to various risks. These include metallurgical challenges, failures in start- up and operating procedures, poor maintenance practices and failures resulting from air / fuel contamination.

Typical loss exposure scenarios are discussed below.

Risk Management in Combined Cycle Power Plants

Insight

CorpAssurance, Vol. 1, No. 3 9

Mechanical ProblemsAs the plants have become more sophisticated in design and efficient in operations, many difficulties have arisen as regards their mechanical integrity following the increased workload imposed on components. Manufacturers have moved towards the installation of fewer rotor bearing points, putting additional demands on rotors and components, which in turn have been subject to stress cracking, distortion and rubbing. Such issues have led to failures and significant downtime whilst repairs take place. Many of these failures often occur at the very early stages of operation. In all cases that have appeared so far, redesign and modifications have addressed such deficiencies, but this has still led to extensive downtime, additional inspection frequencies and hence loss of capacity and diminished productivity.

Thermal ProblemsThe use of increased firing temperatures has led to use of advanced metallurgy, thermal barriers and advanced cooling techniques. Manufacturers have encountered problems with all three of these techniques, ranging from failure of thermal barriers and their attachment systems, to insufficient blade cooling leading to thermal distress. Again, redesign and modifications have addressed such problems in many machines. Cleanliness of the fuel supply is of utmost importance, as impurities within the fuel supply can lead to chemical and physical degradation of internal surfaces. As such, purification and filtration systems are provided within fuel supply systems. Quality control is also vital, as even trace quantities of certain elements can cause long-term problems e.g. corrosion associated with sulphur.

Burner HummingIn a drive to reduce emissions, all modern gas turbine machines feature Dry Low NOx or Dry Low Emission-type burners. Many plants have encountered the phenomenon known as combustion chamber, or burner-humming. This vibration-induced noise is brought about by flame instabilities within the burner area of the combustion chamber. Though burner humming is not generally a short-term threat to the operation of the machine, it could lead to long-term damage as a result of excessive vibrations.

Combustion FlashbacksCombustion flashbacks occur when the burner flame front moves back from its intended location towards the burner front. The repositioned flame then impinges on those components not designed to accommodate high temperatures, causing them to melt and become detached. The molten metal can then pass through the turbine, causing extensive damage.

Steam Turbine Losses The majority of the large losses that are reported in respect of steam turbine are due to damage to blades caused by vibration cracking and corrosive deposits due to poor water conditioning. Other causes include damage resulting from protection facilities not functioning properly and damage to bearings due to faults in the supply of lubricating oil.

HRSG LossesUnburnt gases can explode in boilers. Faulty erection and operations that are carried out without proper controls and protection facilities can also lead to major damage. These events are more likely to happen when operations switch over from single-gas turbine to combined-cycle operations.

Generator LossesShort circuits in stator and rotor windings and faulty rotor insulation are the main causes of such damage. Important loss prevention and loss minimization measures are diligent control of the operating parameters and an electrical generator protection system which should be checked regularly to make sure that it is functioning properly.

Risk Management Recommendations

OperationModern plants are operated with modern DCS systems which send out various alarms in case of equipment malfunctions, as well as shut down automatically in case of an emergency. It is vital to operate these machines in the correct way. Many problems have been caused by poor procedures, leading to (or resulting from) failure in communications and important steps of operations being skipped. Cooling air valves have been left in the incorrect position after maintenance activities, lubrication systems have been left out of service prior to start-up and pre-start

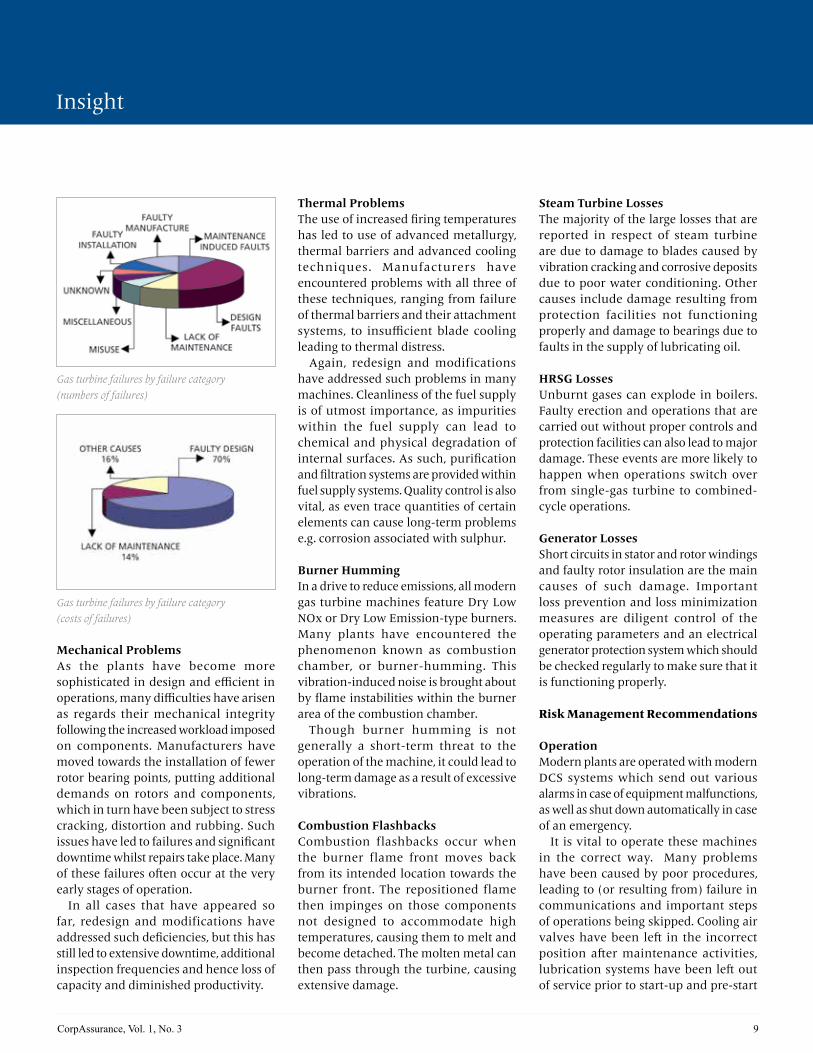

Gas turbine failures by failure category

(numbers of failures)

Gas turbine failures by failure category

(costs of failures)

Insight

Inside Insurance

10 CorpAssurance, Vol. 1, No. 3

Know Your Policy: Mediclaim Policy

Hospitalization is becoming increasingly expensive. As the general ailments are increasing and treatments becoming more invasive, the hospital expenses are becoming unaffordable to the large segment of the population. Medical Insurance is one effective way to meet this expenses. However Medical Insurance comes with its own set of challenges. No Insurance would be available if the person is sick or likely to be hospitalised undergo hospitalization. So it is better to “have a policy when you do not want it otherwise it is possible that you would not get the policy when you want it”.

Coverage under MediclaimHospitalisation Expenses following injury or disease. The coverage would include– Consultation Charges– Surgical Procedure– Diagnostic Expenses– Medicines– 30 days Pre-Hospitalisation Expenses– 60 days Post-Hospitalisation ExpensesCoverage without geting admited is admissible for certain ailment like Cataract, Dialysis, Chemotherapy, Radiotherapy, Eye surgery etc. It is to be noted that the hospitalization on account of general wellness programme and non-

theuropatic reasons are not covered under Mediclaim.

Major Exclusions– Circumcision, vaccination, Cosmetic Treatment, Plastic Surgery– Cost of Spectacles, Lenses, Hearing Aids, Dental Treatment– Diagnostic Test & Routine CheckupSettlement of Claims on Cashless BasisMany insurance companies have outsourced and appointed the Third Party Administrators (TPA) to process the claims relating to the medical insurance. The TPA have entered into the tie-up with

checks have been carried out incorrectly.

MaintenanceUse of correct components and properly designed spare parts are of equal importance during maintenance. The manufacturer’s guidelines should be properly adhered to. Improperly controlled maintenance activities can also lead to problems. Bolts can be left untightened, tools can be left in the machine and auxiliary systems may not be re-commissioned correctly. Maintenance activities must be strictly monitored. All debris or foreign objects or loose components should be removed and kept away from the turbine. Gas turbine internals are relatively fragile; a single tiny foreign particle can have catastrophic consequences.

Quality AssuranceQuality assurance of component parts and materials is extremely important as gas turbines operate at high speed in high temperatures and pressures confine and low tolerances between blades and veins. Failure of a relatively minor component within the machine can cause extensive damage.

Fuels Fuel quality should be of prime order, as fuel impurities can cause deposition, erosion or corrosion of internal parts of the equipment causing major damage. Fuel pulsations as a result of varying fuel quality or irregular supply systems can cause vibrations in combustion systems and turbine areas leading to mechanical disfiguration and dislocations exacerbated

due to exposure to high temperatures. Extremely fine particles in fuel can have an effect similar to a sand blaster on turbine blading or may become embedded within or stuck to blade surfaces, leading to a build-up of material and subsequent machine imbalances.

The Insurance Aspect of Combined Cycle PlantsThe comprehensive insurance policies available for Combined Cycle Plants generally cover all damages emanating from the accidental reasons. However, damages due to corrosion or normal wear and tear are not covered under such policies.

Contributed by Mr Ajoy GangulySr DGM, Corporate Insurance

Inside Insurance

CorpAssurance, Vol. 1, No. 3 11

some hospitals for the cashless settlement. The list of the hospitals with the tie-up are generally available on the website of the respective companies. The Unique Identification Number is allotted to each covered person.

For availing cashless settlement, following procedures are required to be followed:a. The requisite identity card should be presented at the hospital while approaching for the cashless facility b. The requisite form should be filled in and be submitted duly signed and stamped by the concerned hospital and doctorc. The TPA will issue the letter of guarantee to the hospital upto which amount expended would be paid directly to the hospitald. In case the tota l hospita l expenditure exceeds the amount authorized, the hospital will ask for the further authorization and TPA will provide the same depending upon the sum insured and nature of ailment.

Settlement of Claim on Non-Cashless BasisIn case the claimant does not intend to avail the cashless facility ,he can approach the insurer/TPA for the reimbursement of the expenses incurred on hospitalisation and submit the relevant documents. The documents to be submitted would be as follows: • OriginalHospitalBillwithproperbreak- up• DischargeCard(indetail)• Doctors’Prescription(Copywilldo)• DiagnosticReports(copywilldo)• Receiptforpaymentsdone• Chemistbillsformedicines(Invoice/ cash memo)• FIRforaccidentcases

For the sake of good order it is advisable to ensure that all claim related documents should be dated and mention the name of the patient

Major Challenges with the MediclaimWhile L&T has taken most comprehensive cover, employee needs to take certain safeguards to ensure that his claims are admitted and settled without hassle.

HospitalsThe treatment should be undertaken at the hospitals, which comply with the following requirements: • Shouldhaveatleast10/15beds.• Fullyequippedoperation theatre& Qualified Doctor/nursing staff round the clock.• Duly registered with appropriate government authorities.• EstablishmentslikeNaturopathyClinics, Place for Rest-cure, Aged, Alcoholics, Drug Addicts and Ayurvedic Centers are not considered to be the Hospitals.

Process of Identification:First one needs to keep employee ID and Medical Unique Identification Number handy all the time. Procedure for e-print is available on SSC site. It has been observed that 95% of the admissions to hospital are planned and therefore it is necessary to co-ordinate with hospital well in advance of actual admission date. In case of emergency admission, please keep a close follow up with hospital authorities for arranging nessesary document so that sanction for cashless from TPA can be availed timely.

Submission of Proper Claim Related Documents: a. Make a list of documents and attach the same along with the claim. Please

also check that you are attaching what is listed and listing what is attached. This will eliminate the doubt when any of the document gets misplaced during transit.b. Make a list of amounts paid with invoice/bill/receipt details. This will enable you to claim amount properly and also check deductions if any. This document also helps claims processing person to mark for query if any.c. Preferably make a file or staple the documents properly. One should be able to see the document without removing the staple. Documents should not be crumpled and should be folded if necessary. d. Arrange documents serially from the detection of illness to hospitalization to treatment after hospitalization. Your claim is examined by a Doctor also at TPA and this would help him to go thru the documents and see the development date wise. He needs to see the illness report first and then see the line of treatment.e. Make sure all the bills receipts bear the name of the patient. Otherwise bill will not be paid assuming it is not for the patient for whom the claim is lodged.

Group Mediclaim Insurance of L&T EmployeesL&T has taken a Group Medical Employees covering the employees as well as their family numbers on the floater basis.The family includes self, spouse, children and parents.

Contributed by Mr Shrikant AbhyankarDGM, Corporate Insurance

Health is true wealth. Prevention is better than cure. There is no substitute for taking care of yourself and your family. Incorporate healthy practices into your lifestyle – adequate exercise, a balanced diet, good sleep – and you and your family will be healthier and happier for it!

Claims Corner 1

12 CorpAssurance, Vol. 1, No. 3

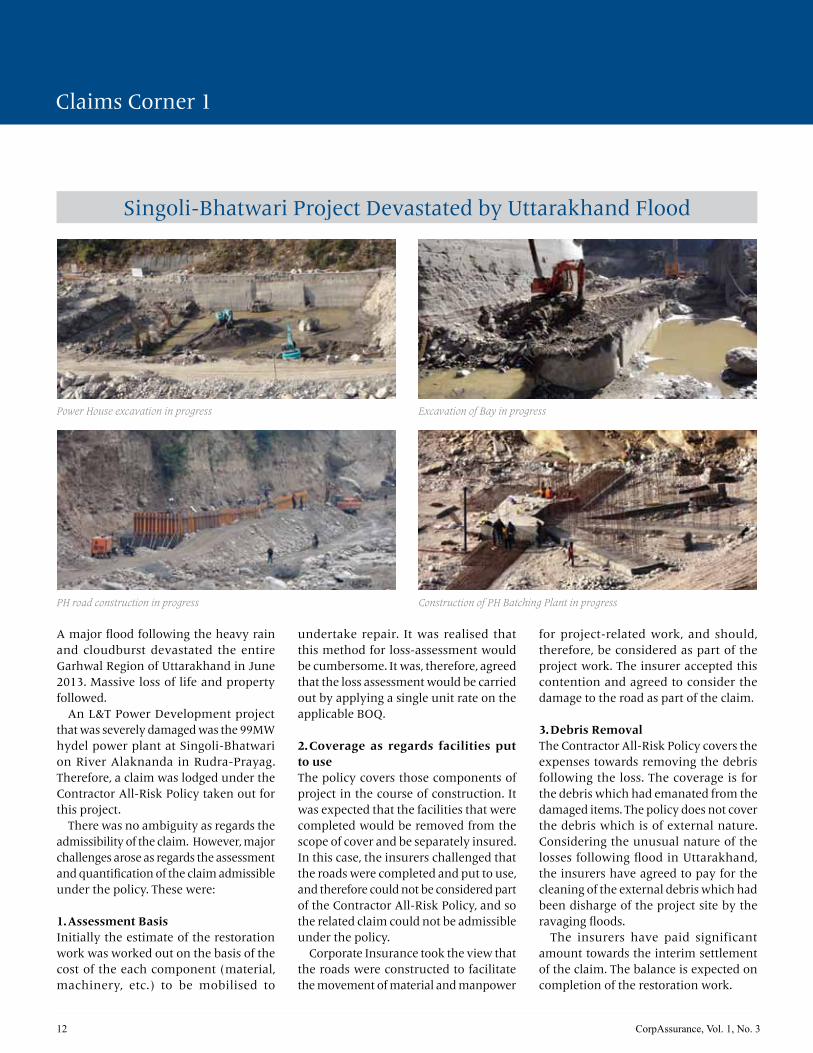

Singoli-Bhatwari Project Devastated by Uttarakhand Flood

A major flood following the heavy rain and cloudburst devastated the entire Garhwal Region of Uttarakhand in June 2013. Massive loss of life and property followed. An L&T Power Development project that was severely damaged was the 99MW hydel power plant at Singoli-Bhatwari on River Alaknanda in Rudra-Prayag. Therefore, a claim was lodged under the Contractor All-Risk Policy taken out for this project. There was no ambiguity as regards the admissibility of the claim. However, major challenges arose as regards the assessment and quantification of the claim admissible under the policy. These were:

1. Assessment BasisInitially the estimate of the restoration work was worked out on the basis of the cost of the each component (material, machinery, etc.) to be mobilised to

undertake repair. It was realised that this method for loss-assessment would be cumbersome. It was, therefore, agreed that the loss assessment would be carried out by applying a single unit rate on the applicable BOQ.

2. Coverage as regards facilities put to useThe policy covers those components of project in the course of construction. It was expected that the facilities that were completed would be removed from the scope of cover and be separately insured. In this case, the insurers challenged that the roads were completed and put to use, and therefore could not be considered part of the Contractor All-Risk Policy, and so the related claim could not be admissible under the policy. Corporate Insurance took the view that the roads were constructed to facilitate the movement of material and manpower

for project-related work, and should, therefore, be considered as part of the project work. The insurer accepted this contention and agreed to consider the damage to the road as part of the claim.

3. Debris RemovalThe Contractor All-Risk Policy covers the expenses towards removing the debris following the loss. The coverage is for the debris which had emanated from the damaged items. The policy does not cover the debris which is of external nature. Considering the unusual nature of the losses following flood in Uttarakhand, the insurers have agreed to pay for the cleaning of the external debris which had been disharge of the project site by the ravaging floods. The insurers have paid significant amount towards the interim settlement of the claim. The balance is expected on completion of the restoration work.

Power House excavation in progress

PH road construction in progress

Excavation of Bay in progress

Construction of PH Batching Plant in progress

Claims Corner 2

CorpAssurance, Vol. 1, No. 3 13

Damage to the Fluid Coupling & Booster Pump at APPDCL Project

Krishnapatnam Thurmal Power project of Andhra Pradesh Power Devlapment Corporation. L&T has been executing an EPC Contract for Turbine & Generator for 2*800 MW Coal Based Thermal Power Project at Krishnapatnam in Andhra Pradesh for Andhra Pradesh Power Development Corporation(APDCL).During the execution phase, there was the major thunder and lightening struck the Fluid Coupling and Booster Pump kept at the storage area of the project-site. This lightening incited the fire and caused damage to the Fluid-Coupling, Booster Pump and Strainers.This claim posed certain major challenges:• Theequipmentswereexternallytoo charred to undertake internal inspection of the damages without risking further damage to the internal components. It was realized that the equipments neither

could be opened at the project site nor were the facilities available to open the and repair the locally. It was finally decided to treat the equipment as total loss and proceed with the fresh procurement from OEM.• Theequipmentswereinitiallyimported under zero-duty Scheme. However the custom duty at the full rate were required to be paid for importing the equipment for the replacement. Initially, the insurer was not agreeable to pay for the custom duties. However after prolonged deliberation, they agreed to pay for the custom duty to be incurred.• Anothermajordisputeasregardstothis claim has been on the applicability of the deductible. As per the policy condition, claims arising due to fire were to attract 20% deductible on the admissible loss amount, while the same

the claim due to Act of God Perils was 10%.The insurance company was of the view that the proximate cause of the loss is Fire and accordingly 20% deductible should be applied on this claim. The corporate insurance department took the stand that the loss had arisen due to lighting, which is an “Act of God” phenomenon. After some reluctance, the insurance company concurred with this interpretation and agreed to settle the claim treating the same to have been emanated from nature-borne phenomenon. This line of interpretation resulted into the additional settlement towards the claim.Finally, the claim was settled for an amount which had been satisfactry to all the parties concerned.

Fluid Coupling and TD Booster Pumps

Booster Pumps

Fluid Coupling and CEP Strainers

BFP Strainers

14 CorpAssurance, Vol. 1, No. 3

Industry Update

In India, defective property title and related issues are the major challenges in the real estate related transaction in India. To protect the buyers from this risk, Insurance Regulatory and Development Authority of India (IRDAI) has proposed introducing ‘Title Insurance’in India. With this objective, IRDA has constituted 7-member working group and the Group has been asked to submit report in two months. Once launched, Title insurance would protect financial interest

of real estate owners as well as lenders against defect in the title to a property, liens or other related issues. This product has been quite prevalent in OECD Countries. In India, the launch of the product was delayed as the land records are not properly documented. But with the with the progress in digitalisation of the land records, the launch of Title Insurance is becoming a commercially viable option.

Proposed Listing of Government owned Non-Life Insurance Companies in India

Launching of ‘Title Insurance’ in India

The PMFBY is a new crop insurance scheme launched by the government which is aimed to take forward the crop insurance scheme that was present. It has come in effect from June, 2016, which also happens to be the Kharif season. The crops that will be considered eligible for crop insurance under this scheme would be Horticultural crops, Commercial crops, Rabi Crops and Kharif Crops. The applicable premium rate would be 2% for Kharif, 1.5% premium for Rabi ,and 5% for Horticulture Crops to be paid by the insured. The rest of the premium rates will be shared equally by the central and state

governments. In the earlier Crop Insurance Policies, the premium was high and the benefit was capped. In this scheme there is no capping. Unlike earlier schemes, current scheme will also cover covers local perils like landslide, hailstorm, inundation etc. To make the process of assessment of the claims faster, drones are proposed to be utilized. A quick drone survey will estimate the crop loss and fasten the entire process. Apart from this, the usage of smart phones and remote sensing are to be encouraged.

What is the Pradhan Mantri Fasal Bima Yojana (PMFBY)?

The Government of India is planning to list the public sector non-life insurance companies in India. The announcement to this intent was made by the Finance Minister in the last budget proposal. The modalities in this regard is being worked out and lot of action on that front is expected in the next few months. The four companies that are likely to be listed are New India Assurance Company, National Insurance Company, Oriental Insurance Company, United India Insurance Company and

General Re. IRDA has also come out with the guidelines as regards the public issue and listing of the insurance companies in India. As of now, only one insurance company is in state-owned are listed. ICICI Prudential has come out with public issue and many other insurance companies have shown intent to tap the IPO route and get listed.

Glossary

CorpAssurance, Vol. 1, No. 3 15

Subrogation is the right for an insurer to legally pursue for the recovery from another party following the settlement of the particular claim. Subrogation in literal sense means the act of one person or party to put itself in the position of another person or party for enforcing certain rights and obligations. In insurance, the insurer acquires the subrogation rights following the settlement of the claim.. It is expected that the insured will keep the recovery right protected and will not take any action which would dilute the recovery right, without the prior permission of the insurer. The insurance works on the concept of indemnity, whereby the insurer undertakes to compensate the insured following the loss in such a way as to put him in the condition, where he was prior to the loss. This is to ensure that the insured receives the rightful compensation for the losses and is not compensated more than what he has lost. If this condition is not enforced strictly, the insured may get into the position whereby he profits from the loss. This may induce him to become lax in protecting the

interest .This may cause loss and damage. The underlying idea is that the insured should act with prudence and conduct himself as if he is not insured. If the recovery right is not subrogated, then the insured may pursue and realise the recovery from the erring third party as well. This will result into the total settlement received being more than the loss suffered by the insured as a claimant. This is not the desired state of affair. In case the insured fails to protect the right of recovery, the claim may become prejudiced. The insurer may penalise the insured for not protecting the recovery right by making deduction from the claimable amount. However, the insurer may agree to waive his subrogation right against certain identified entity. It is advisable to obtain the waiver of the subrogation right by obtaining prior confirmation of the insurer and attaching suitable attachment to the policy document.

What is ‘Subrogation’

Zinged!

Goings-on

Mr. Vinit Prabhu has joined Corporate Insurance as Deputy Head. Mr Prabhu is a mechanical engineer from S.P.C.E, Mumbai and MBA from IIM, Lucknow. He has worked in diverse industries with market leading organisations like Blue Star, Maruti Suzuki, Times of Money.com and ICICI

Lombard General Insurance. At ICICI Lombard, he led various departments such as Reinsurance, Broking, Specialised Industries Group (Aviation, Energy and Construction), Strategic Initiatives.

Corporate Insurance arranged an Insurance Workshop at Nabha Power on salient features of Property (Mega) All risk Policy. The salient issues relating to the claims were also deliberated in the workshop.

Welcome Aboard

Insurance Workshop at Nabha Power

Overview on Political Risk Insurance Congratulations to Mrs. Apoorva Surve

Edited by Pradeep Sinha /Ajit Verma for Larsen & Toubro Limited, Corporate Insurance, L&T House, Ballard Estate, Mumbai 400001, CIN : L99999MH1946PLC004768.

The views expressed in this magazine are not necessarily those of the Management of Larsen & Toubro Limited. The contents of this magazine should not be

reproduced without the permission of the Editor. Not for sale - for circulation among the employees of various Insurance Departments in L&T Group of companies.

One insurance Workshop was conducted at Powai Campus for various Business Units of L&T. The workshop was conducted by Ms.Mellica Chai ,Head Underwriter of Political risk Insurance of AIG International.

25 Years of Ms. Apoorva Surve of Corporate Insurance in L&TMs. Apoorva Surve was facilitated on 17-7-2016 on completing 25 years in the service of L&T. She joined L&T and has since then an invaluable team-member of Corporate Insurance Department.