Embed Size (px)

Citation preview

INSTITUTIONAL EQUITY RESEARCH

Page | 1 | PHILLIPCAPITAL INDIA RESEARCH

NBFC Sector Rising above challenges INDIA | NBFC

5 March 2015

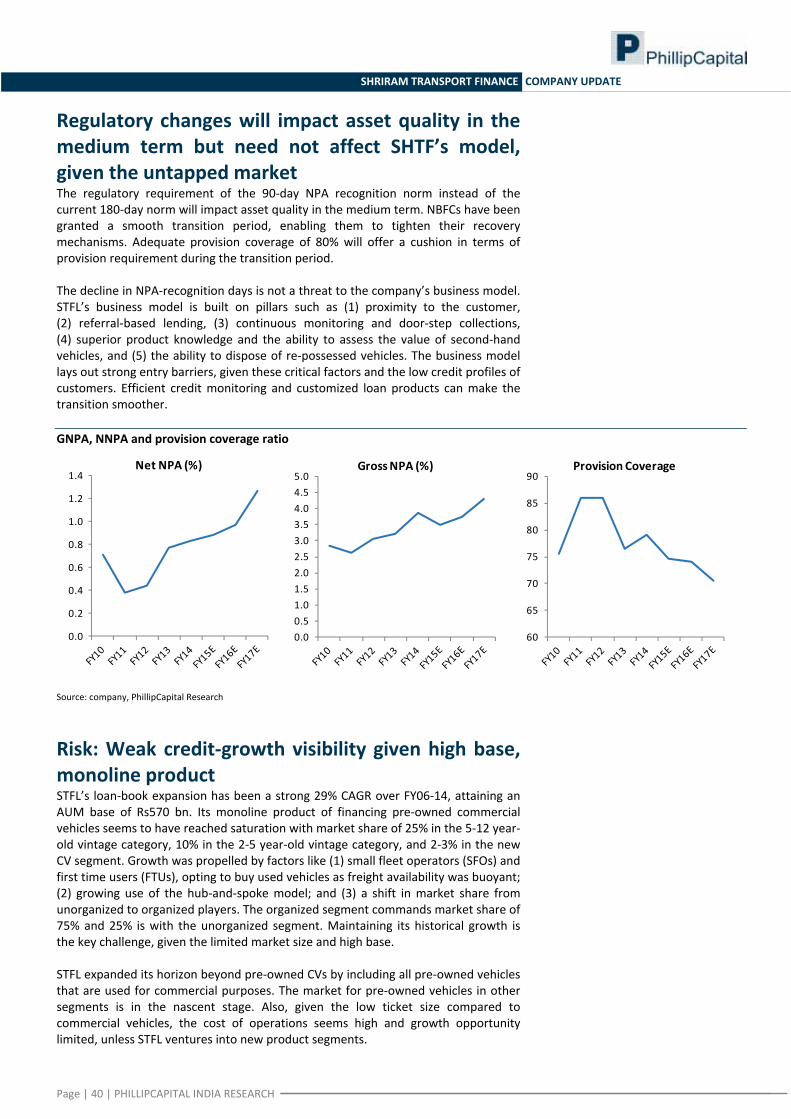

Recovery in M&HCV and passenger vehicle augurs well for financiers; LCV remains a drag The Auto finance market witnessed moderation in line with downward trending industry volume in last couple of years. The slowdown in auto volumes can be attributed to factors like declining economic activity; low disposable income; high fuel prices etc. Medium & heavy commercial vehicle (M&HCV) & passenger vehicle (cars & utility vehicle) segment witnessed some rebound in growth driven by reversal of the said factors. However the LCV segment remains under stress. Nonetheless, the LCV market remains under penetrated at just 2.15 per M&HCV compared to global average of 6 per M&HCV. With the improvement in demand for M&HCV, the demand for LCV will follow but with a lag of 3‐4 quarters. Economic downturn in rural geography had been with a lag; revivals will also be delayed A sharp deceleration in economic activity over FY12‐14 had immediate bearing on urban regions but the rural economy continued to do well, helped by good monsoons, high MSPs and government welfare schemes. However last two years have not been good , as rural economy is facing slow down driven by moderate growth in MSPs; declining sowing acreage; lack of employment opportunity and stagnation in rural wage. We believe that NBFCs with larger dependency on rural economy to remain under pressure. Increased focus towards longer term assets; making balance sheet more stable All the four NBFCs viz CIFC, MMFS, SHTF, SCUF we have covered in the report have diversified portfolio spanning across Vehicle finance, LAP, SME, Gold. However one thing which is common among most of the NBFCs is their rising focus towards longer term assets. NBFC like Chola and SCUF have increased their portfolio share in LAP/ SME to 28%/ 53% from 24% each in FY11. An average Vehicle finance loan has tenure of 2 years, whereas SME loan or LAP goes upto 5 years. A longer term assets bring stability to balance sheet, as the repayment is spread over a longer time frame. Interest rates trending down; huge benefit on the cost front The large part of these NBFCs borrowing is comprised of bank loan followed by bonds. While around 75‐90% of the bank loans are linked to base rate across NBFCs, bonds issuances normally done at a spread of 50‐100bps over 10 year GSec. While GSec yields have come down by 100bps since the beginning of the year, bank base rate have been stable at 10‐10.25%. With interest rates trending down, NBFCs will get benefit in the range of 60‐90bps on their cost of funds over FY16/17. The emerging trends in NBFC business suggests a favorable operating environment which translate into improved return ratio. We maintain BUY on SHTF – a play on liability re‐pricing, revival of Used ‐ CV demand and easing pressure on asset quality. We Initiate coverage on CIFC & SCUF with Buy rating – given favorable interest rate environment; demand revival and improving efficiency. We also initiate coverage on MMFS with NEUTRAL rating, as demand in rural economy remains weak and recovery still far away.

Companies CHOLAMANDALAM INVESTMENT & FINANCE Reco BUY CMP, Rs 595 Target Price, Rs 750 Upside (%) 26 MAHINDRA & MAHINDRA FINANCE Reco NEUTRAL CMP, Rs 257 Target Price, Rs 220 Upside (%) ‐14 SHRIRAM TRANSPORT FINANCE Reco BUY CMP, Rs 1209 Target Price, Rs 1470 Upside (%) 22 SHRIRAM CITY UNION FINANCE Reco BUY CMP, Rs 2015 Target Price, Rs 2450 Upside (%) 22 Pradeep Agrawal (+ 9122 6667 9953) [email protected] Manish Agarwalla (+ 9122 6667 9962) [email protected]

Peer Valuation CMP Reco Target MCAP _______RoA (%)_______ _______RoE (%)_______ _______ABV (Rs)_______ _______P/ABV (x)_______(Rs) Price (Rs) Rs bn FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E

CIFC 595 BUY 750 92 1.8 2.0 2.4 15.3 15.7 18.8 193.8 206.4 246.8 3.1 2.9 2.4MMFS 257 NEUTRAL 220 145 2.3 2.5 2.8 14.1 14.7 16.5 80.4 87.3 105.1 3.2 2.9 2.4STFC 1209 BUY 1470 274 2.2 2.3 2.6 14.0 15.6 17.8 394.6 452.7 523.8 3.1 2.7 2.3SCUF 2015 BUY 2450 133 3.3 3.6 3.6 16.5 16.3 17.7 605.3 674.1 760.7 3.3 3.0 2.6

Source: Company, PhillipCapital India Research

Page | 2 | PHILLIPCAPITAL INDIA RESEARCH

NBFC SECTOR

Table of Contents INDUSTRY ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 3

Companies Section Cholamandalam Investment & Finance ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 9

M&M Financial Services ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 20

Shriram Transport Finance ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 33

Shriram City Union Finance ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 44

Page | 3 | PHILLIPCAPITAL INDIA RESEARCH

NBFC SECTOR

Industry Firm recovery in M&HCV and passenger vehicle segment augurs well for the financing market; LCV remains a drag The Auto finance market witnessed moderation in line with downward trending industry volume in last couple of years. The slowdown in auto volumes can be attributed to factors like declining economic activity; low disposable income; high fuel prices etc. Medium & heavy commercial vehicle (M&HCV) & passenger vehicle (cars & utility vehicle) segment witnessed some rebound in growth driven by reversal of factors mentioned above but the LCV segment remains under stress. M&HCV sales grew by 13% in 9MFY15 after nine consecutive quarters of negative growth whereas passenger vehicle reported a 4% growth over same period. But LCV sales declined by 12.4% in 9MFY15. LCV which has started witness stress with a lag compared to M&HCV will take time to recover. The LCV market remains under penetrated at 2.15 per M&HCV compared to global average of 6 per M&HCV. With the improvement demand for M&HCV, the demand for LCV will follow but with a lag of 3‐4 quarters. Growth in M&HCV & LCV finance market (percent)

Source: PhillipCapital India Research

Growth in Passenger vehicle, tractor & used vehicle finance market (percent)

Source: PhillipCapital India Research

‐40‐30‐20‐100102030405060

2008

‐09

2009

‐10

2010

‐11

2011

‐12

2012

‐13

2013

‐14

2014

‐15e

2015

‐16e

2016

‐17e

M&HCV LCV

‐20

‐10

0

10

20

30

40

2008

‐09

2009

‐10

2010

‐11

2011

‐12

2012

‐13

2013

‐14

2014

‐15e

2015

‐16e

2016

‐17e

CAR & UV tractor Used Vehicle segment

Page | 4 | PHILLIPCAPITAL INDIA RESEARCH

NBFC SECTOR

Within the auto financing segment, M&HCV & passenger vehicle market are expected to witness strong CAGR of 23 % & 19% respectively over FY14‐17. However other segments like LCV & tractors is expected to grow at ‐1 % & 10% respectively over same period of time. Used CV segment to witness 16% growth over same period of time. Product wise auto financing market (Rs bn)

Source: PhillipCapital India Research Economic downturn in rural geography had been with a lag; revivals will also be delayed A sharp deceleration in economic activity over FY12‐14 had immediate bearing on urban regions but the rural economy continued to do well, helped by (1) good monsoons, (2) high MSPs and (3) government welfare schemes. The Central Government’s pro‐rural policies over FY07‐13 led to a sharp improvement in rural cash flows (1) The introduction of NREGS in FY07, and (2) ~15% CAGR in MSPs over FY07‐13 and (3) higher credit to the agriculture sector helped rural economy flourish. However last two years have not been good as MSPs increased by just 5%/1.3% in FY13/14 respectively and output was lower. According to the Second Advance Estimates, food grain production in FY15 is estimated at 257.07 mn tonnes, down 3.2% yoy. Food grain production is down due to poor monsoons in the Kharif season and low Rabi acreage. While the southwest monsoon was 12% deficient, total area coverage as on February 13, 2015 under Rabi crops declined to 61.6 mn hectares from 65.9 mn hectares in FY14. Lower agricultural production, falling yields and crop prices are impacting rural cash flows. Non‐agricultural demand pull has also been subdued as infrastructure and construction failed to pick up. Movement of MSP & Change in sowing acreage

Source: PhillipCapital India Research

146

372

175

329

48124 145 142

260

503 474

758

74

180236

436

80131 149

197214

392460

724

0

100

200

300

400

500

600

700

800

2008‐09 2011‐12 2013‐14 2016‐17e

MHCV LCV CAR Utility Vehicle Tractor Used Vehicle segment

0

10

20

30

40

50

1996

‐97

1997

‐98

1998

‐99

1999

‐00

2000

‐01

2001

‐02

2002

‐03

2003

‐04

2004

‐05

2005

‐06

2006

‐07

2007

‐08

2008

‐09

2009

‐10

2010

‐11

2011

‐12

2012

‐13

2013

‐14

2014

‐15

Kharif MSP yoy Rabi MSP yoy

‐8

‐6

‐4

‐2

0

2

4

6

8

10

2010‐11 2011‐12 2012‐13 2013‐14 2014‐15

Karif crop Rabi crop

Page | 5 | PHILLIPCAPITAL INDIA RESEARCH

NBFC SECTOR

Empirical data suggest that the rural economy facing slow down due to moderate growth in MSPs; declining sowing acreage; lack of employment opportunity due to slow down in construction activity in rural area and stagnation in rural wage. The passenger car sales volume data of Maruti Suzuki suggest a recovery in urban sales volume whereas rural volume reports moderation. Similarly, Indian market Research Bureau (IMRB) data suggest that rural consumption, which had propelled FMCG firms' growth in CY2013, slowed in CY2014. Household FMCG consumption volume (all categories) grew by 4% in CY2014 compared to ‐3% in CY2013. Similarly, rural volume growth declined 3% in CY2014, versus zero growth in CY2013. Household consumption trends were similar in value terms, too. For urban India, growth in 2014 stood at 6%, compared to 2% in CY2013. For rural India's the same number stood at 3% in CY2014 Vs 4% in CY2013. Geography wise passenger vehicle volume growth (Maruti)

Source: MSIL, PhillipCapital India Research

‐20

‐15

‐10

‐5

0

5

10

15

20

25

FY12 FY13 FY14 FY15YTD

Rural Sales Growth (%) Urban Sales Growth (%)

Page | 6 | PHILLIPCAPITAL INDIA RESEARCH

NBFC SECTOR

NBFC, play on interest rate cycle; lower interest rates to drive benefit on the cost front The large part of these four NBFCs borrowing is comprised of bank loan followed by bonds. While around 75‐90% of the bank loans are linked to base rate across NBFCs, bonds issuances are normally done at a spread of 50‐100bps over 10 year GSec. While GSec yields have come down by 100bps since the beginning of the year, bank base rate have been stable at 10‐10.25%. This has provided limited benefit on cost front, as more than 50% of borrowing is from banks. However as RBI has cut repo rate by 50bps in the last three months, we expect the banks to also bring down their base rate starting from Q1FY16 onwards. With interest rates trending down, NBFCs will get benefit in the range of 60‐90bps on their cost of funds spread over FY16/17. NBFC historically have shown strong correlation to interest rates as they tend to benefit significantly in term of lower cost, which leads to improvement in their Margins. In the last downward interest rate cycle of FY09‐FY11, these four NBFC saw more than 100bps decline in their cost of funds. Average 1 Year Fwd p/ABV also improved to 2.3x in March 2011 from 1.2% in March 2009. In the current downward cycle which started from Sept 2013, average valuations of these four NBFCs have increased from 2x to 2.9x. With further downtrend in interest rates the average valuation of these NBFC is expected to move up further. We expect the downward interest rate cycle to be more prolonged and will continue till FY17. Our Economist expect around 100bps further cut in interest rate in FY16/17. 1 Year Fwd P/ ABV Chart Vs Interest rate – Downward rate cycle drive valuation higher

Source: PhillipCapital India Research NBFC stock Price movement Vs Interest rate – strong correlation

Source: PhillipCapital India Research

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

4/26/2008 4/26/2009 4/26/2010 4/26/2011 4/26/2012 4/26/2013 4/26/2014

CIFC SHTF MMFS SCUF AA Corp Bond 3 Yr Repo rates

0

2

4

6

8

10

12

14

0

200

400

600

800

1000

1200

1400

1600

3/16/2006 3/16/2007 3/16/2008 3/16/2009 3/16/2010 3/16/2011 3/16/2012 3/16/2013 3/16/2014

CIFC SHTF MMFS SCUF Repo rate 3 yr AA Corp Bond yield

Page | 7 | PHILLIPCAPITAL INDIA RESEARCH

NBFC SECTOR

Increased focus towards longer term assets; making balance sheet more stable All the four NBFC CIFC, MMFS, SCUF, STFC, covered in the report have diversified portfolio spanning across Vehicle finance, LAP, SME, and Gold. However one thing which is common among most of the NBFCs is their increased focus on longer term assets. NBFC like Chola and SCUF have increased their portfolio share in LAP/ SME to 28%/ 53% from 24% each in FY11. An average Vehicle finance matures in of 2‐3 years, whereas SME loan or LAP goes upto 4‐5 years. A longer term assets bring stability to balance sheet, as the repayment is spread over a longer time frame. As a result CIFC and SCUF AUM has grown at a higher CAGR of 29‐36% over FY10‐14. We expect the share of longer maturity portfolio to increase further to 35%/60% for CIFC and SCUF respectively. As a result the AUM will also grow at higher pace than peers at 24‐26% CAGR over FY15‐17. AUM breakup % of portfolio SCUF CIFC MMFS SHTF HCV 8 4 63 LCV 19 9 29 Mini LCV‐3W & SCV 6 Cars & MUV 8 10 53 Used Vehicles 20 15 Tractors 7 19 5 Home Equity 28 Gold 17 1 MSME 53 1 Home Loans 1 2 Wheeler 18 Personal Loans 4 Total AUM (Rsmn) 161,770 247,363 365,023 570,713

Source: PhillipCapital India Research Rising share of longer duration products driving higher growth

___Higher maturity portfolio share___ __________AUM CAGR__________

FY11 9MFY15 FY17E FY10‐14 FY15‐17E

CIFC 24% 28% 35% 36% 26%MMFS NA NA NA 35% 11%STFC NA NA NA 16% 21%SCUF 24% 53% 60% 29% 24%

Source: PhillipCapital India Research

Page | 8 | PHILLIPCAPITAL INDIA RESEARCH

NBFC SECTOR

Compa

nies Sectio

n

INSTITUTIONAL EQUITY RESEARCH

Page | 9 | PHILLIPCAPITAL INDIA RESEARCH

Cholamandalam Investment & Finance (CIFC IN) Multiple levers to drive RoA to the next level INDIA | NBFCs | Initiating coverage

5 March 2015

Optimised product mix & economies of scale to boost profitability ratios. The company is in a sweet spot as the confluence of several levers will drive RoA to the next level. Factors such as a rising share of the LAP book, recovery in the CV cycle and a decline in opex ratio will boost RoA, by about 50 bps, to 2.4% over the next two years. With a recovery in the CV cycle, the credit cost in the vehicle‐finance segment will moderate to 1.5% by FY17 from 1.9% in 9MFY15. Investment in technology and economies of scale will drive a 30 bps cut in opex/asset ratio. Besides, as LAP share (higher RoA business) increases in the portfolio it will have a positive impact on aggregate RoA. These factors will drive RoA to 2.4% by FY17 from 1.8% in FY14. Under‐penetration, structural factors to drive medium to long‐term growth. The recovery of the CV cycle augurs well for CV financiers like Cholamandalam, which has almost 35% of its AUM in the new CV segment and 15‐20% in the used‐CV segment. M&HCV growth is on the uptrend and growth in the LCV segment is likely to pick up with a lag of 3‐4 quarters. The long‐term growth potential for the LCV segment is intact, given (1) the low penetration of LCVs, (2) emergence of a hub‐and‐spoke model for transport and (3) increased urbanisation. These factors will drive 17% CAGR in vehicle finance over FY14‐17E. Sticky LAP book offers stability to the balance sheet. CIFC home equity portfolio (LAP), is the company’s second‐largest product segment, after vehicle finance, accounting for 27% of assets under management. Disbursement CAGR over FY12‐14 was 20% but with longer‐tenure loans, LAP grew by a higher 38% CAGR. The home equity portfolio has lent stability to the balance sheet as it is a longer‐tenure product with average tenure of 4‐5 years against two years in the vehicle‐finance segment. Average ticket size is also higher, at Rs5 mn, against 0.4‐0.5 mn in the vehicle‐finance segment. We expect AUM under LAP to post 27% CAGR over FY14‐17. Strong risk management limits asset‐quality deterioration. Cholamandalam’s asset quality, with GNPA ratio of 2.8%, compares favourably with most of its peers. Companies like Mahindra Finance and Shriram Transport Finance, which operate mainly in the vehicle‐finance space, have a significantly higher GNPA ratio of 7.1% and 3.6% respectively. Strong understating of borrowers’ cash flow and robust credit appraisal systems underpin the company’s better asset quality. Although the downtrend in CV cycle contributed to a gradual rise in GNPA ratio over the past two years, the deterioration has been less than that of peers. With the start of the uptrend in the CV cycle, asset‐quality pressure will subside gradually. By FY17, we expect the GNPA ratio to ease to 2.3%. Valuation and recommendation Cholamandalam is expected to deliver strong earnings CAGR of 26% over FY14‐17, driving sharp improvement in RoAs and RoEs. RoA will improve by 50 bps to 2.4% and RoE to 18.8% by FY17. Improving operating matrix and profitability ratios, to result in further re‐rating in the stock. We value CIFC at 3x FY17ABV arriving at a price target of Rs750. We initiate coverage with a BUY rating.

BUY CMP RS 595 TARGET RS 750 (+26%) COMPANY DATA O/S SHARES (MN) : 144MARKET CAP (RSBN) : 86MARKET CAP (USDBN) : 1.452 ‐ WK HI/LO (RS) : 607 / 229LIQUIDITY 3M (USDMN) : 1.8PAR VALUE (RS) : 10 SHARE HOLDING PATTERN, % PROMOTERS : 57.7FII / NRI : 20.9FI / MF : 13.0NON PROMOTER CORP. HOLDINGS : 2.9PUBLIC & OTHERS : 5.6 PRICE PERFORMANCE, %

1MTH 3MTH 1YRABS 7.0 27.1 157.9REL TO BSE 5.2 24.2 119.4 PRICE VS. SENSEX

Source: Phillip Capital India Research KEY FINANCIALS Rs mn FY15E FY16E FY17ENet Income 17,577 20,425 24,510% growth 18 16 20Net Profit 4,145 5,258 7,313% growth 13.9 26.8 39.1EPS (Rs) 28.9 33.8 47.0PER (x) 20.7 17.7 12.8Book value (Rs) 218.9 229.9 270.8P/BV (Rs) 2.7 2.6 2.2Adj. book value (Rs) 193.8 206.4 246.8P/ABV (Rs) 3.1 2.9 2.4

Source: PhillipCapital India Research Est. Pradeep Agrawal (+ 9122 6667 9953) Manish Agarwalla (+ 9122 6667 9962)

050

100150200250300350

Apr‐11 Jul‐12 Oct‐13 Jan‐15CholamandalamBSE Sensex

Page | 10 | PHILLIPCAPITAL INDIA RESEARCH

CHOLAMANDALAM INVESTMENT AND FINANCE INITIATING COVERAGE

Optimised product mix, economies of scale to boost RoA Cholamandalam Investment and Finance (CIFC) kept its RoA stable, at 1.7‐1.9 over FY12‐14, despite a 100‐bp decline in RoA in the vehicle‐finance portfolio. The negative impact of Vehicle finance segment was offset by a 70‐bp increase in the LAP RoA and increase in LAP book proportion. We do not expect the LAP RoA to improve further, but continued increase in the LAP book proportion, due to the sticky nature of the loans, will contribute about 10‐bp improvement to aggregate RoA over the next 2‐3 years. Besides, a recovery in the CV cycle will ease credit costs in the vehicle‐finance segment to 1.5% by FY17 from 1.9% in 9MFY15, boosting aggregate RoA by 15 bps. Reduction in the opex ratio will also contribute to RoA expansion. CIFC reduced its opex ratio by 46 bps over FY12‐14 but it still is one of the highest among peers. The management guidance indicated it would reduce it to 2.5‐3% over 3‐5 years as the company has invested in technology and process improvements aimed at enhancing productivity and reducing operating costs. Besides, its home equity branches are located along with vehicle‐finance branches. This cuts operating expenses to a large extent. We expect the opex ratio to fall by 35 bps to 3.1% in FY17. The combined impact of above mentioned three factors will drive about 50 bps improvement in RoA, to 2.4%, by FY17. Higher RoA in LAP compensated for lower RoA in Vehicle finance ____Vehicle finance____ _____Home equity_____ ______Aggregate______As % of assets FY12 FY14 Chng, % FY12 FY14 Chng, % FY12 FY14 Chng, %NIM 7.7 7.1 ‐0.6 5.4 5.6 0.2 7.4 7.7 0.3Expense ratio 4.1 3.5 ‐0.6 2.0 1.6 ‐0.4 4.1 3.4 ‐0.7Provisions 0.5 1.6 1.1 0.3 0.2 ‐0.1 0.6 1.1 0.5RoA 3.1 2.1 ‐1.0 3.1 3.8 0.7 2.7 2.8 0.1AUM share 73.1 73.4 0.3 22.9 25.2 2.3

Source: Company, PhillipCapital India Research Dupont analysis of peers ________FY14 Dupont________ ________FY17 Dupont________ ____Change in FY17 over FY14____ Chola MMFS SCUF SHTF Chola MMFS SCUF SHTF Chola MMFS SCUF SHTFInterest Income 16.3 16.5 19.3 14.6 16.1 16.2 19.7 15.7 (0.2) (0.3) 0.4 1.2 Interest Expense 8.9 7.7 8.3 8.4 8.4 7.3 7.7 8.2 (0.5) (0.4) (0.6) (0.2)Net interest margins 7.3 8.8 11.0 6.2 7.7 8.9 12.0 7.5 0.4 0.1 1.0 1.3 Other income total 0.2 0.8 0.6 2.3 0.2 0.7 0.6 0.2 (0.0) (0.1) (0.0) (2.1)Net Income total 7.5 9.7 11.6 8.4 7.9 9.7 12.6 7.7 0.4 0.0 1.0 (0.7)Operating expenses total 3.3 3.2 4.4 2.1 3.1 3.4 5.0 1.7 (0.2) 0.2 0.5 (0.4)Preprovision profit 4.2 6.5 7.1 6.4 4.8 6.3 7.6 6.0 0.6 (0.2) 0.5 (0.4)Provisions 1.4 1.8 2.4 2.5 1.3 2.2 2.3 2.2 (0.1) 0.4 (0.1) (0.3)Profit before tax and exceptional items 2.8 4.7 4.8 3.9 3.5 4.1 5.4 3.8 0.7 (0.6) 0.6 (0.1)Profit before tax 2.8 4.1 4.8 3.9 3.5 3.5 5.4 3.8 0.7 (0.6) 0.6 (0.1)Tax total 0.9 1.6 1.6 1.2 1.2 1.4 1.8 1.3 0.2 (0.2) 0.2 0.1 Reported Profit after tax 1.8 3.1 3.2 2.7 2.3 2.8 3.6 2.6 0.5 (0.3) 0.4 (0.1)Adjusted Profit after tax 1.8 3.1 3.2 2.7 2.3 2.8 3.6 2.6 0.5 (0.3) 0.4 (0.1)RoAA 1.8 3.1 3.2 2.7 2.3 2.8 3.6 2.6 0.5 (0.3) 0.4 (0.1)Leverage 9.3 6.0 6.3 6.1 8.0 5.8 4.9 7.0 (1.3) (0.2) (1.4) 0.9 RoAE 17.1 18.6 20.2 16.3 18.3 16.1 17.7 17.8 1.2 (2.4) (2.6) 1.5

Source: Company, PhillipCapital India Research

Page | 11 | PHILLIPCAPITAL INDIA RESEARCH

CHOLAMANDALAM INVESTMENT AND FINANCE INITIATING COVERAGE

LCV a drag in near term; under‐penetration, structural factors to drive growth in medium to long term The M&HCV segment is showing signs of recovery following two years of a downtrend, but the LCV segment remains under stress. M&HCV sales grew by 8.6% in Q2FY15 after nine consecutive quarters of negative growth. However LCV sales declined by 9.4% in Q2FY15. We expects the decline in the LCV segment to continue until H1FY16, as the impact of a slowdown in the economy on LCV segment also took place with a lag of 4‐5 quarters. The LCV segment is CIFC’s largest product segment under vehicle finance, contributing 36% to its overall vehicle finance AUM. Consequently, it will weigh on overall growth in the vehicle‐finance portfolio. Nonetheless, other product segments like HCV, refinance and older vehicles, have begun to show good traction, offsetting loss of business in the LCV segment. AUM mix Vehicle‐finance portfolio mix

Source: Company, PhillipCapital India Research The LCV segment might continue to contract for a couple of quarters more but the long‐term growth potential is intact, given (1) low penetration, (2) emergence of a hub‐and‐spoke model for transport, and (3) increased urbanisation. The LCV penetration has doubled over past five years with M&HCV: LCV ratio reaching ~1:2 in FY14 from ~1:1 in FY09. However, it is significantly lower than the 1:6 in developed nations. These factors are expected to help the vehicle‐finance book to post 17% CAGR over FY14‐17. LCV penetration (Industry) MCV/LCV growth in the system

Source: Company, PhillipCapital India Research, SIAM

Vehicle Finance71%

Home Equity27%

Gold/ MSME/

Home Loans2%

HCV11%

LCV28%

Mini LCV9%

Cars/ MUV13%

Refinance15%

Older Vehicles14%

Tractors10%

0.0

0.5

1.0

1.5

2.0

2.5LCV to M&HCV ratio

32.9 31.9

8.0

‐23.1 ‐25.3

1.9

43.5

25.4 27.5

14.1

‐17.7‐14.2

‐30

‐20

‐10

0

10

20

30

40

50

FY10 FY11 FY12 FY13 FY14 YTDFY15

M&HCV LCV

Page | 12 | PHILLIPCAPITAL INDIA RESEARCH

CHOLAMANDALAM INVESTMENT AND FINANCE INITIATING COVERAGE

Home equity (LAP) portfolio gives stability to the balance sheet The CIFC home equity portfolio (LAP) is the company’s second largest product segment after vehicle finance, accounting for 27% of assets under management. The company added this product in FY07 and has since rapidly ramped it up. About 90% of this product portfolio comprises self‐occupied residential property, and the rest of the mix comprises rented, commercial and others. While the CAGR in disbursement over FY12‐14 was 20%, with longer tenure of loans, AUM under LAP grew by a higher 38% CAGR. The home‐equity portfolio has lent stability to company balance sheet as it is a longer tenure product with average tenure of 4‐5 years against the two‐year average maturity in the vehicle‐finance segment. The average ticket size is higher (Rs5 mn) against Rs0.4‐0.5 mn in the vehicle‐finance segment. We expect AUM under LAP to grow at a CAGR of 27% over FY14‐17. LAP is more stable portfolio with higher tenure and ticket size Vehicle Finance Home EquityAUM 174678 64864% of total portfolio 71% 27%Average ticket size (Rsmn) 0.5 5Tenure (Years) 2 4

Source: Company, PhillipCapital India Research Rising share of LAP in the portfolio Advance maturity profile‐ Increase in higher duration loans

Source: Company, PhillipCapital India Research

10

12

14

16

18

20

22

24

26

0

10000

20000

30000

40000

50000

60000

70000

FY09 FY10 FY11 FY12 FY13 FY14

LAP (Rsmn) as % of AUM (RHS)

‐

10

20

30

40

50

FY09 FY10 FY11 FY12 FY13 FY14

% of p

ortfolio

< 1 Year 1‐3 Years 3‐5 Years > 5 Years

Page | 13 | PHILLIPCAPITAL INDIA RESEARCH

CHOLAMANDALAM INVESTMENT AND FINANCE INITIATING COVERAGE

New product lines to drive sustainable, long‐term growth The company has been consistently adding new products to its portfolio to fill gaps in its product offerings. The company started operations as a vehicle financier in FY92 and added LAP in FY07 and gold loans in FY12. It added home loans, rural financing, MSME loans and construction equipment finance to its bouquet of products over FY13‐14. Though the combined AUM of new products added over the past 3‐4 years is less than 2%, we believe with the roll out of these products in more branches the share in the overall AUM will gradually pick up. While this will not only reduce the company’s risk from product concentration, but also act as a catalyst for growth in the medium to long term and help in optimisation of cost ratios. Product details Business Year of

commencement Products Share in

AUM (%)Average tenure (years)

Average yield (%)

LTV (%) Average ticket size

Borrower profile Area of operation

Vehicle finance FY92 New and used M&HCVs, LCVs, SCVs, cars,

MUVs, tractors

70 2 ~17 65‐90 LCVs: Rs0.4‐0.5

mn; M&HCVs:

Rs1.2‐1.3 mn

SME and agri‐based customers account for 65% of disbursements

Tier‐II, III towns

Home equity FY07 Self‐occupied residential property

28 4 ‐5 14‐15 50 Rs5 mn Largely self‐employed individuals

Tier‐I, II towns

Others FY13‐14 Gold and home loans, MSME, rural finance

2 2‐10 NA NA NA Self‐employed individuals, MSME

Tier‐I, II, III towns

Source: Company, PhillipCapital India Research Evenly spread branch network minimises region‐specific risks CIFC has 579 branches, spread across all the four regions, with a slightly higher concentration in South India. South India comprises about 33% of the branch network, followed by North and West India, with 24% each and East India, which has 20% of the branches. Over the past three years, the company has ramped up its branch presence in the eastern region from 56 to 115 branches. The AUM is also well spread across states with no single state contributing more than 12% of the AUM. Maharashtra, Rajasthan, Chhattisgarh, Andhra Pradesh and Madhya Pradesh are the top 5 business generating regions for the company. Evenly spread branch network across regions… ...largely in rural and semi‐urban areas (%)

Source: Company, PhillipCapital India Research

15% 17% 19% 20%

21% 24% 24% 24%

23%24% 24% 24%

40% 35% 33% 33%

375 518 574

0%

20%

40%

60%

80%

100%

FY12 FY13 FY14 Dec‐14

West North South Branches

579

10% 10% 10% 10%

19% 19% 19% 19%

71% 71% 71% 71%

0%

20%

40%

60%

80%

100%

FY12 FY13 FY14 Dec‐14

Urban Semi Urban Rural

Page | 14 | PHILLIPCAPITAL INDIA RESEARCH

CHOLAMANDALAM INVESTMENT AND FINANCE INITIATING COVERAGE

Branch productivity, advanced technology to lower costs Over the past couple of years the company has invested in technology and process improvement, which has helped the company to improve productivity and lower opex. Introduction of higher tenure products helped to improve business per branch/ employee. AUM per branch improved to Rs427 mn from Rs359 mn in FY12 and AUM/employee increased from Rs17 mn to Rs19 mn. We believe that as the company leverages its platform and technology across product categories, productivity ratios will improve. We expect cost ratio to decline from the current 3.5% to 3.1% by FY17. Improving productivity of Branches and Employees FY12 FY13 FY14 9MFY15 Branches 375.0 518.0 574.0 579.00 Employees 8,437 10,919 11,187 12,941 AUM (Rs mn) 145,047 201,779 232,534 247,363 AUM/branch 386.8 389.5 405.1 427.2 AUM/employee 17.2 18.5 20.8 19.1

Source: Company, PhillipCapital India Research Strong risk management limits asset‐quality deterioration CIFL’s asset quality, with GNPA ratio of 2.8%, compares favourably with most of its peers. Companies like Mahindra Finance and Shriram Transport Finance, which are predominantly in the vehicle‐finance space, operate at significantly higher delinquency ratios of 7.1% and 3.8% respectively. A strong understanding of borrowers’ cash flows, robust credit‐appraisal systems and less exposure to the M&HCV segment have made for better asset quality for the company. Though with a downtrend in the CV cycle the GNPA ratio increased to 2.8% in Q3FY15 from 0.9% in FY12. But the deterioration has been limited compared to peers. With an uptrend in the CV cycle, asset quality is likely to improve to 2.3% by FY17. GNPA better than most of the peers (%)

Source: Company, PhillipCapital India Research

7.1

3.63.0 2.8

2.4

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

MMFS STFS SCUF CHOLA SUNDF

Page | 15 | PHILLIPCAPITAL INDIA RESEARCH

CHOLAMANDALAM INVESTMENT AND FINANCE INITIATING COVERAGE

Borrowing skewed to bank loans; falling rates to reduce costs Almost 56% of the company’s borrowings are in the form of bank loans, followed by debentures (18%). Almost 97% of the bank borrowings are linked to the base rate, and hence any cut by the banks in the base rate will correspondingly cut costs of borrowings. We expect 100‐125 bps cut in the base rate by banks over FY16‐17, and hence expect a significant decline in companies’ borrowing costs over FY16‐17. 90%+ bank borrowing linked to base rate

_____Amount (Rsmn) _____ ________% Share________(Rs mn) FY14 FY13 FY14 FY13Base rate 41830 30883 45.9 44.5Base rate + average spread of 1% 46133 27450 50.6 39.6Fixed rate 3250 11000 3.6 15.9Total 91213 69333 100.0 100.0

Source: Company, PhillipCapital India Research On the debentures side, about 30% of the borrowings, raised at an average cost of 10.75 ‐11.25%, will mature in FY16‐17. The company borrowed at 9.75‐10.5% in H2FY15. With a cut in benchmark rates by the RBI, the cost will come down further. We expect further reduction in bond yields over FY16‐17, which is likely to drive reduction in bond raising costs. On the overall book, including bank borrowings, we expect 60‐90 bps reduction in borrowing costs over FY16‐17. Borrowing profile (%)‐ skewed towards banks Bonds maturity year wise (Rsbn)

Source: Company, PhillipCapital India Research

Banks56%

CP13%

Debentures18%

Tier II Capital13%

Banks CP Debentures Tier II Capital

16.1

10.0

6.0

3.3

5.4

3.0 3.5 3.6 3.82.9

0

2

4

6

8

10

12

14

16

18

FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 FY24

Maturity

Page | 16 | PHILLIPCAPITAL INDIA RESEARCH

CHOLAMANDALAM INVESTMENT AND FINANCE INITIATING COVERAGE

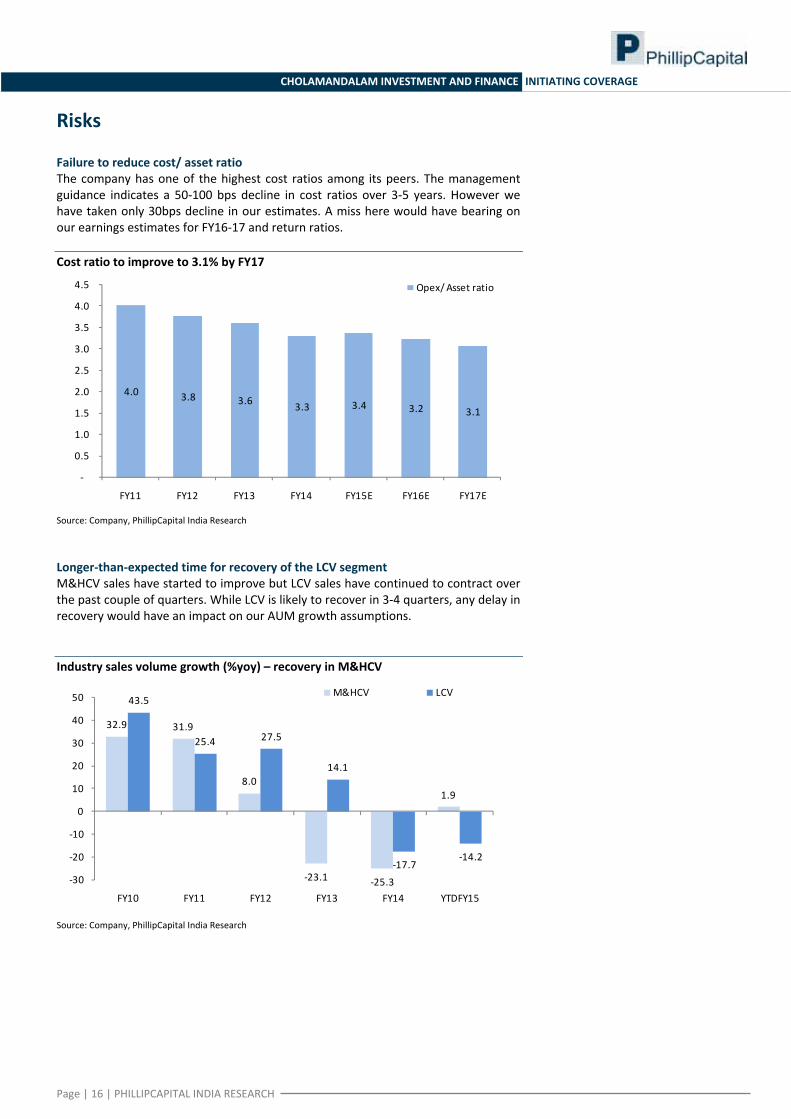

Risks Failure to reduce cost/ asset ratio The company has one of the highest cost ratios among its peers. The management guidance indicates a 50‐100 bps decline in cost ratios over 3‐5 years. However we have taken only 30bps decline in our estimates. A miss here would have bearing on our earnings estimates for FY16‐17 and return ratios. Cost ratio to improve to 3.1% by FY17

Source: Company, PhillipCapital India Research Longer‐than‐expected time for recovery of the LCV segment M&HCV sales have started to improve but LCV sales have continued to contract over the past couple of quarters. While LCV is likely to recover in 3‐4 quarters, any delay in recovery would have an impact on our AUM growth assumptions. Industry sales volume growth (%yoy) – recovery in M&HCV

Source: Company, PhillipCapital India Research

4.0 3.8 3.6 3.3 3.4 3.2 3.1

‐

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

Opex/ Asset ratio

32.9 31.9

8.0

‐23.1 ‐25.3

1.9

43.5

25.4 27.5

14.1

‐17.7‐14.2

‐30

‐20

‐10

0

10

20

30

40

50

FY10 FY11 FY12 FY13 FY14 YTDFY15

M&HCV LCV

Page | 17 | PHILLIPCAPITAL INDIA RESEARCH

CHOLAMANDALAM INVESTMENT AND FINANCE INITIATING COVERAGE

Valuation Our investment thesis for Cholamandalam Finance is based on a sharp improvement in its profitability ratios, aided by levers like the CV‐cycle recovery, lower opex and low credit costs. A gradual pick‐up in growth, aided by recovery in the CV cycle and an increasing share of the higher duration LAP book in the portfolio will drive NII CAGR of 18% over FY14‐17. Moreover, reduction of opex ratio by 30 bps over FY15‐17E, (helped by increased adoption of technology) and decline in credit costs will enhance RoA. We expect the company to improve RoA to 2.4% from 1.8% and RoE to 18.8% on a sustainable basis. Improving operating matrix and profitability ratios, to drive further re‐rating in the stock. We value CIFC at 3x FY17ABV arriving at a price target of Rs750. We initiate coverage with a BUY rating. 1 year Fwd P/ ABV Band

Source: Company, PhillipCapital India Research

0

100

200

300

400

500

600

Apr‐09Jul‐09Oct‐09

Jan‐10Apr‐10Jul‐10Oct‐10

Jan‐11Apr‐11Jul‐11Oct‐11

Jan‐12Apr‐12Jul‐12Oct‐12

Jan‐13Apr‐13Jul‐13Oct‐13

Jan‐14Apr‐14Jul‐14Oct‐14

Jan‐15

0.5x

1.3x

2.0x

2.7x

Page | 18 | PHILLIPCAPITAL INDIA RESEARCH

Cholamandalam Investment and Finance Ltd INITIATING COVERAGE

Annexure: 1

Background Cholamandalam Investment and Finance Company (CIFC) was incorporated in 1978 as the financial services arm of the Murugappa Group. It commenced business as an equipment‐financing company and has emerged as a comprehensive financial services provider, offering vehicle finance, home loans, home equity loans and SME loans. Chola operates from over 579 branches in India with assets under management of Rs247 bn. Subsidiaries include Cholamandalam Securities (CSEC) and Cholamandalam Distribution Services (CDSL).

Management Mr. M.B.N. Rao, Chairman. He is a graduate in agriculture, an Associate of the Chartered Institute of Bankers, London, a Certified Associate of the Indian Institute of Bankers and a Fellow of the Indian Institute of Banking & Finance. He holds a diploma in computer studies from the University of Cambridge and the National Centre for Information Technology, United Kingdom. He used to be the chairman and managing director of Canara Bank and Indian Bank. Has over 40 years of varied experience in the fields of banking, finance, economics, technology, human resources, marketing, treasury and administration. Has over nine years of international banking experience in Singapore and Indonesia. He is a member of the Singapore Institute of Management, was chairman of Indian Banks Association and a member of various committees constituted by the RBI, MoF, SEBI and the National Institute of Bank Management. He is on the boards of various reputed companies including E.I.D. Parry (India), Ramco Cements and Taj GVK Hotels and Resorts. He joined the Board of CIFC in July 2010. Mr. Vellayan Subbiah, Managing Director. He is a Bachelor of Technology in civil engineering from IIT Madras and holds a Masters in Business Administration from the University of Michigan. He worked with McKinsey and Company, Chicago, 24/7 Customer Inc. and Sundaram Fasteners and was managing director of Laserwords, Chennai, between January 2007 and August 2010. He is a director on the boards of SRF and certain other Murugappa Group companies. He joined the Board of CIFC in August 2010. Key Shareholders

Numbers (mn) % of total Promoters 82.8 57.66 Tube Investments Of India Ltd. 72.2 50.3 Ambadi Investments Pvt Ltd. 7.2 5.03 Others 0.0 2.33Other key shareholders Norwest Venture Partners X Fii ‐ Mauritius 7.1 4.93 Creador I Llc 6.6 4.61 Amansa Holdings Private Limited 6.2 4.29 International Finance Corporation 5.9 4.12 Multiples Private Equity Fii I 4.8 3.33 HSBC Bank (Mauritius) Limited A/C Jwalamukhi Investment Holdings 3.1 2.17 Apax Viii Gp Co. Limited A/C Cornalina Acquisition(Fii) Limited 3.0 2.06 Aquarius Investments Ltd 2.7 1.85 Multiples Private Equity Fund 1.9 1.34Total 120.7 86.4

Source: Company, PhillipCapital India Research

Page | 19 | PHILLIPCAPITAL INDIA RESEARCH

CHOLAMANDALAM INVESTMENT AND FINANCE LTD INITIATING COVERAGE

Financials Profit and loss (Rs mn) Balance sheet (Rs mn)(Year Ending Mar 31) FY14 FY15E FY16E FY17E (Year Ending Mar 31) FY14 FY15E FY16E FY17E

Net interest income 14,587 17,202 19,988 24,001 Equity 1,433 1,433 1,555 1,555Other income 331 375 436 510 Reserves 21,515 29,921 34,211 40,560Net Income 14,918 17,577 20,425 24,510 Net worth 22,947 31,354 35,766 42,115Operating expenses 6,582 7,715 8,450 9,573 Borrowings 180,932 196,237 233,636 284,569Preprovision profit 8,335 9,862 11,975 14,938 Current liabilities & others 11,589 12,160 12,267 12,385Provisions 2,833 3,596 4,027 4,129 Total liabilities 215,468 239,751 281,669 339,070Profit before tax 5,502 6,266 7,947 10,808 Net block 729 758 822 936Tax 1,862 2,120 2,689 3,495 Investments 824 710 710 710Tax rate 33.8 33.8 33.8 32.3 Loans 194,281 218,650 260,503 317,790Adjusted Profit after tax 3,640 4,145 5,258 7,313 Current assets & others 19,634 19,634 19,634 19,634 Total assets 215,468 239,751 281,669 339,070

Dupont (as % of Assets) Key ratios(Year Ending Mar 31) FY14 FY15E FY16E FY17E (Year Ending Mar 31) FY14 FY15E FY16E FY17E

Interest Income 16.3 16.2 16.1 16.1 NIM (%) 7.3 7.6 7.7 7.7Interest Expense 8.9 8.7 8.5 8.3 NIM (%) ‐On AUM 6.9 7.1 7.1 6.7Net Interest Income 7.3 7.6 7.7 7.7 Cost/ Income (%) 44.1 43.9 41.4 39.1Other income total 0.2 0.2 0.2 0.2 Credit cost (%) 1.4 1.6 1.5 1.3Net Income total 7.5 7.7 7.8 7.9 RoA(%) 1.8 1.8 2.0 2.4Operating expenses total 3.3 3.4 3.2 3.1 RoE (%) 17.1 15.3 15.7 18.8Preprovision profit 4.2 4.3 4.6 4.8 Leverage (x) 9.3 8.4 7.8 8.0Provisions 1.4 1.6 1.5 1.3 Tier I (%) 10.9 12.9 12.6 11.8Profit before tax and exc. items 2.8 2.8 3.0 3.5 CAR (%) 17.2 20.9 19.0 17.9Profit before tax 2.8 2.8 3.0 3.5 No of shares (mn) 143.3 143.3 155.5 155.5Tax total 0.9 0.9 1.0 1.1 Gross NPA (%) 1.9 2.8 2.6 2.3 Profit after tax 1.8 1.8 2.0 2.4 Net NPA (%) 0.8 1.5 1.3 1.1 Provision coverage (%) 59.7 46.4 50.0 52.2

Growth (%) Valuation ratios(Year Ending Mar 31) FY14 FY15E FY16E FY17E (Year Ending Mar 31) FY14 FY15E FY16E FY17E

Net interest income 31.7 17.9 16.2 20.1 EPS (Rs) 25.4 28.9 33.8 47.0Net Income total 30.3 17.8 16.2 20.0 PER (x) 23.6 20.7 17.7 12.8Preprovision profit 44.9 18.3 21.4 24.7 Book value (Rs) 160.2 218.9 229.9 270.8Profit before tax 22.1 13.9 26.8 36.0 P/BV (Rs) 3.7 2.7 2.6 2.2Profit after tax 18.7 13.9 26.8 39.1 Adjusted book value (Rs) 148.9 193.8 206.4 246.8Loan 16.9 12.5 19.1 22.0 P/ABV (Rs) 4.0 3.1 2.9 2.4Disbursement 8.2 ‐5.0 19.0 22.0 P/ PPP 2.8 3.2 3.0 2.8AUM 22.4 9.1 23.4 28.4 Dividend yield (%) 0.6 0.6 0.6 0.6

INSTITUTIONAL EQUITY RESEARCH

Page | 20 | PHILLIPCAPITAL INDIA RESEARCH

M&M Financial Services (MMFS IN)

In the midst of a cyclical downturn INDIA | NBFCs | Initiating coverage

5 March 2015

MMFS is in midst of asset‐quality deterioration cycle: MMFS’ asset quality is a reflection of rural economic growth. As the economic slowdown percolates into rural India, MMFS’ asset quality has come under severe pressure. An analysis of historical trends suggests a business cycle for MMFS normally lasts eight years—the first four years being an up‐cycle followed by four years of a down‐cycle. From FY14 MMFS entered a down‐cycle with agricultural growth slowing. This impacted MMFS’ asset quality with the GNPA ratio rising from 3% in FY13 to 4.4% in FY14 and to 7.1% in M9FY15. The company is running into its second year of a down‐cycle and asset quality is likely to deteriorate further with GNPA ratio expected to increase to 8.4% in FY16, before moderating in FY17. AUM/branch close to optimum, limits growth prospects: MMFS’ AUM per branch increased from Rs166 mn in FY07 to a peak of Rs463 mn in Q3FY14, before moderating to Rs338 mn in Q2FY15. The moderation was largely driven by a steep increase of 54% in the branch network over the past four quarters. However, 90% of these branches are pure recovery centers and do not generate business. So, effectively AUM per “business‐generating branch” is Rs473 mn. MMFS’ branches can handle 2,800‐3,000 customers, and with an average ticket size of Rs200,000, each branch can manage AUM of Rs550‐600 mn. With 1.7 mn live customers, on average, each branch handles 2,500 customers, close to the maximum capacity of MMFS branches. With pressure on asset quality and lack of growth drivers, AUM is expected to grow moderately at 10% CAGR over FY14‐17 as compared to 31% CAGR over FY11‐14. Rural economy on the back foot; a poor monsoon can worsen the situation: With 80% of MMFS branches concentrated in rural areas, it’s’ fortunes are directly linked to the rural economy. A sharp deceleration in economic activity over FY12‐14 had immediate impact on urban regions, but the rural economy continued to do well, helped by (1) a good monsoon, (2) higher MSPs and (3) government welfare schemes. Moderate increase of just 5%/1.3% in MSP in FY13/14, coupled with lower farm production in FY15, is affecting rural cash flows. As the cash flows of MMFS customers are already stretched due to a slow rural economy, another year of poor rains can worsen an already poor asset‐quality situation. Banks gain ground in rural areas—is that a threat to MMFS? Banks have made significant inroads into rural areas over the past 3‐4 years as is evident from a sharp rise in the number of bank outlets. The outlets (branches plus business correspondents or BCs) in villages increased from 67,694 in FY10 to 383,804 in FY14, but only 12% were in the form of brick‐and‐mortar branches, with 88% being BCs and other modes. BCs are used mainly for liability‐based transactions (deposits and payments‐related) and play a limited role in credit growth. While the banks’ deposit‐account penetration has more than doubled, from 33 accounts per 100 rural adults in FY01 to 68 in FY13, credit penetration increased from 5.7% to just 8.9%. Valuation and recommendation: MMFS’ earnings will post a muted 7% CAGR over FY14‐17, as weak AUM growth, higher opex and steep provisioning will weigh on profitability. Asset quality to remain under pressure in FY16 as rural economy slows down further. At its current market price, the stock trades at 2.9x/2.4x FY16E/FY17E ABV with average RoA and RoE of 2.6%/15.4% over FY16/17. We initiate coverage with a NEUTRAL rating and price target of Rs220.

NEUTRAL CMP Rs257 TARGET Rs220 (‐14%) COMPANY DATA O/S SHARES (MN) 569MARKET CAP (Rs BN) 145MARKET CAP (US$ BN) 2.352 ‐ WK HI/LO (Rs) 345 / 230LIQUIDITY 3M (USDMN) 10.1PAR VALUE (Rs) 10 SHARE HOLDING PATTERN, % PROMOTERS 52.0FII/NRI 41.7FI/MF 1.7NON‐PROMOTER CORP. HOLDINGS 0.6PUBLIC & OTHERS 3.9 PRICE PERFORMANCE, %

1MTH 3MTH 1YRABS ‐1.8 ‐21.6 4.7REL TO BSE ‐3.5 ‐24.4 ‐33.9 PRICE VERSUS SENSEX

Source: Phillip Capital India Research KEY FINANCIALS Rs mn FY15E FY16E FY17ENet Income 29,976 33,337 37,228% growth 8 11 12Net Profit 7,518 8,715 10,934% growth ‐15.3 15.9 25.5EPS (Rs) 13.3 15.5 19.4PER (x) 19.2 16.6 13.2Book value (Rs) 99.4 110.4 125.0P/BV (Rs) 2.6 2.3 2.0Adj. book value (Rs) 80.4 87.3 105.1P/ABV (Rs) 3.2 2.9 2.4

Source: PhillipCapital India Research estimates Pradeep Agrawal (+ 9122 6667 9953) Manish Agarwalla (+ 9122 6667 9962)

0

50

100

150

200

250

Apr‐11 Apr‐12 Apr‐13 Apr‐14

Mah Finance BSE Sensex

Page | 21 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

Focus on recovery; growth takes back seat • The company is in its second year of the down‐cycle, and is likely to see another

year of pain before showing signs of recovery in asset quality • MMFS has opened more than 400 branches over the past five quarters, 90% of

which are pure recovery centres, putting pressure on cost ratios • With 1.7 mn live customers, on average, each business‐generating branch

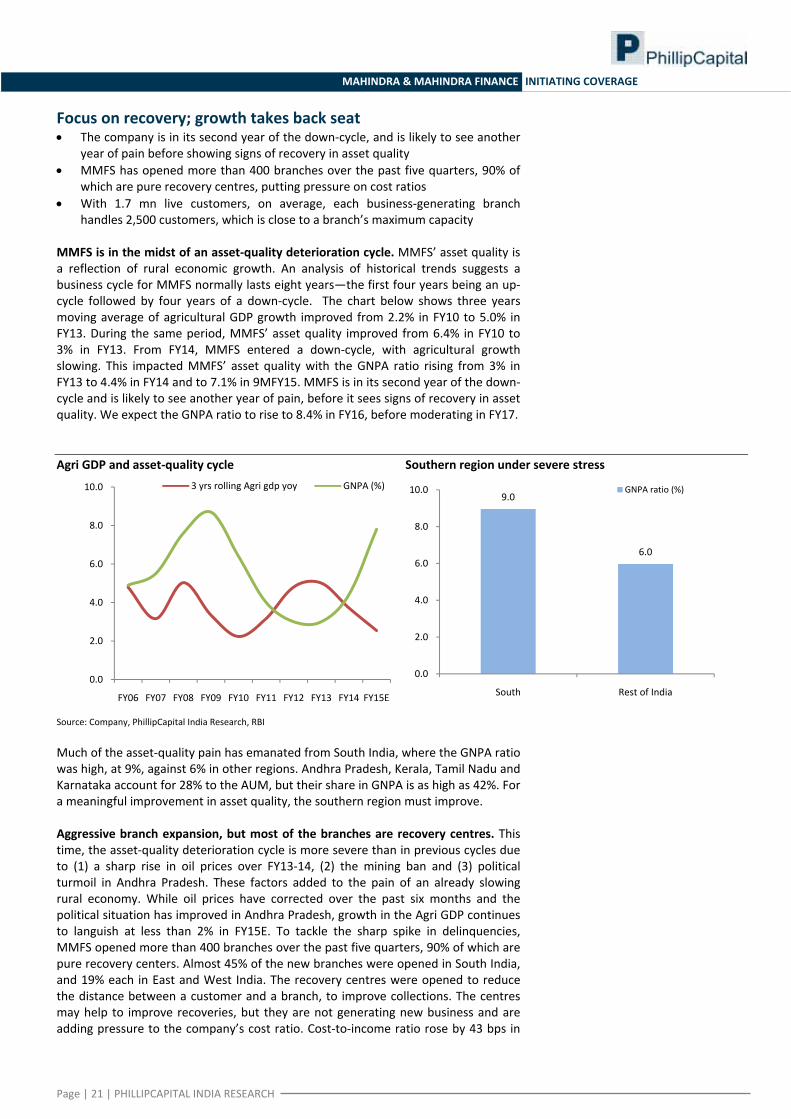

handles 2,500 customers, which is close to a branch’s maximum capacity MMFS is in the midst of an asset‐quality deterioration cycle. MMFS’ asset quality is a reflection of rural economic growth. An analysis of historical trends suggests a business cycle for MMFS normally lasts eight years—the first four years being an up‐cycle followed by four years of a down‐cycle. The chart below shows three years moving average of agricultural GDP growth improved from 2.2% in FY10 to 5.0% in FY13. During the same period, MMFS’ asset quality improved from 6.4% in FY10 to 3% in FY13. From FY14, MMFS entered a down‐cycle, with agricultural growth slowing. This impacted MMFS’ asset quality with the GNPA ratio rising from 3% in FY13 to 4.4% in FY14 and to 7.1% in 9MFY15. MMFS is in its second year of the down‐ cycle and is likely to see another year of pain, before it sees signs of recovery in asset quality. We expect the GNPA ratio to rise to 8.4% in FY16, before moderating in FY17. Agri GDP and asset‐quality cycle Southern region under severe stress

Source: Company, PhillipCapital India Research, RBI Much of the asset‐quality pain has emanated from South India, where the GNPA ratio was high, at 9%, against 6% in other regions. Andhra Pradesh, Kerala, Tamil Nadu and Karnataka account for 28% to the AUM, but their share in GNPA is as high as 42%. For a meaningful improvement in asset quality, the southern region must improve. Aggressive branch expansion, but most of the branches are recovery centres. This time, the asset‐quality deterioration cycle is more severe than in previous cycles due to (1) a sharp rise in oil prices over FY13‐14, (2) the mining ban and (3) political turmoil in Andhra Pradesh. These factors added to the pain of an already slowing rural economy. While oil prices have corrected over the past six months and the political situation has improved in Andhra Pradesh, growth in the Agri GDP continues to languish at less than 2% in FY15E. To tackle the sharp spike in delinquencies, MMFS opened more than 400 branches over the past five quarters, 90% of which are pure recovery centers. Almost 45% of the new branches were opened in South India, and 19% each in East and West India. The recovery centres were opened to reduce the distance between a customer and a branch, to improve collections. The centres may help to improve recoveries, but they are not generating new business and are adding pressure to the company’s cost ratio. Cost‐to‐income ratio rose by 43 bps in

0.0

2.0

4.0

6.0

8.0

10.0

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E

3 yrs rolling Agri gdp yoy GNPA (%)9.0

6.0

0.0

2.0

4.0

6.0

8.0

10.0

South Rest of India

GNPA ratio (%)

Page | 22 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

FY14 and by 123 bps in 9MFY15, to 34.3%. We expect the cost ratio to move up further to ~35% in FY17. Branch expansion over the years Highest incremental addition in FY14/15

Source: Company, PhillipCapital India Research Branches operating closer to full capacity, limiting growth prospects. MMFS’ AUM per branch increased from Rs166 mn in FY07 to a peak of Rs463 mn in Q3FY14, before moderating to Rs338 mn in Q2FY15. The moderation was driven largely by a steep increase of ~60% in the branch network over the past five quarters. More than 90% of these branches are pure recovery centres and do not generate business. So, effectively AUM per “business‐generating branch” is Rs473 mn. MMFS’ branches can handle 2,800‐3,000 customers. With a ticket size of Rs0.2 mn, it can manage an AUM of Rs550‐600 mn. With 1.7 mn live customers, on average, each branch handles 2,500 customers, which is close to the maximum capacity of an MMFS branch. Hence to attain meaningful AUM growth, the recovery branches need to be converted into fully operational branches. However, considering the economic environment and asset‐quality position, we do not expect this in the medium term. AUM and branches AUM per “business‐generating branch”

Source: Company, PhillipCapital India Research

55 59 59 56 59 74 79 107 13174 83 83 86 99 105 111148 162

108 113 113 120 128 136 147173

218

72 74 74 74 88 100 107

128

170

89 100 100 113156

172190

302

370

403 436 436 459547

607657

893

1088

0

200

400

600

800

1000

1200

South North Central West North East East

98

33

0

23

88

6050

236

195

‐25

25

75

125

175

225

275South North Central West North East East

67 78 83 101 143 20

6 279 34

1

365403 436

436

459 54

7 607 657 713

738

0

100

200

300

400

500

600

700

800

AUM (Rsbn) Business generating branches

166 178 191220

262

340

425479 495

0

100

200

300

400

500

600 AUM/ branch (Rsmn)

Page | 23 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

High repayment ratio to keep AUM growth sub‐optimal in FY16. As the average tenure of loans is a little over two years, slowing disbursement growth in FY13/14, which worsened with a decline of 8% in M9FY15, will result in higher repayment rates in FY16/17. While disbursement CAGR was 32% over FY10‐14, repayments CAGR was a relatively lower 24%, resulting in a decline in repayment rates from 68% in FY10 to 50% in FY14. Historically, repayment rates have been in the range of 50‐85%, with the bottom last seen in FY06. Amid rising NPA concerns and a slowdown in rural India, we expect disbursements to decline by 5% in FY15 before showing moderate growth of 10% in FY16. Consequently, repayment rates will increase to 52% in FY16 from ~47% in FY15. As a result of moderate disbursement growth and rising repayment rates, AUM growth will fall to 7% in FY16E from 22.3% growth in FY14. In the last cycle GNPA peaked out with disbursement‐to‐repayment ratio at 1.1; in FY14 it was at a high 1.5x

Source: Company, PhillipCapital India Research

Diversified across vehicle segments – AUM

Source: Company, PhillipCapital India Research

0

2

4

6

8

10

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E

Disbursement (Rsmn) Repayments(Rsmn)

GNPA ratio peaked out at disbursement to repayment ratio

of 1.1x

Disbursement to Repayment ratio stood at a high 1.5x

43% 38% 38% 33% 31% 30% 28% 29% 30%

26%23% 24% 30% 31% 31%

24% 24% 23%

19%25% 25% 23% 23% 20%

19% 19% 19%

9% 7% 7% 8% 9% 12%17% 15% 13%

3% 7% 6% 6% 6% 7% 12% 13% 15%

0%

20%

40%

60%

80%

100%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Auto/ Utility vehicles Cars Tractors Commercial Vehicles Refinance & Others

Page | 24 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

Rural economy falters; poor monsoons can worsen things • MMFS’ performance is directly linked to the fortunes of rural India, as 80% of its

branches are in rural areas • Despite poor economic conditions over FY12‐14, rural India did not see a

slowdown due to (1) good monsoons, (2) high MSPs and (3) government welfare schemes, which helped to keep the rural cash‐flow buoyant

• A fall in agricultural production, lower yields and weakening crop prices in FY15 have started to impact rural cash flows, which is also evident from MMFS’ deteriorating asset quality

A proxy play on the rural economy, MMFS benefits from pro‐rural policies. With 80% of its branches in rural areas, MMFS’ fortune is directly linked to the rural economy. A sharp deceleration in economic activity over FY12‐14 had immediate bearing on urban regions but the rural economy continued to do well, helped by (1) good monsoons, (2) high MSPs and (3) government welfare schemes. The Central Government’s pro‐rural policies over FY07‐13 led to a sharp improvement in rural cash flows, which had a significant positive impact on MMFS’ balance‐sheet growth and asset quality. (1) The introduction of NREGS in FY07, and (2) ~15% CAGR in MSPs over FY07‐13 and (3) higher credit to the agriculture sector helped MMFS directly and indirectly. MMFS did not benefit directly from NREGS, but the scheme improved rural cash flows, from which MMFS benefited. Higher MSPs and a sharp growth in agricultural credit improved the credit profile of customers, which had a direct bearing on vehicle sales and asset quality.

Decline in production/moderating MSPs impact rural cash flow. FY11‐13 were among the best years for the rural economy as the average minimum selling price for all crops posted 16% CAGR against 8% CAGR over past 20 years. Besides, food grain production increased by a healthy 12.2% yoy/6% yoy in FY11/12 respectively, which led to higher cash flow in rural areas. However last two years have not been as good as MSPs increased by just 5%/1.3% in FY13/14 respectively and output was lower. According to the Second Advance Estimates, food grain production in FY15 is estimated at 257.07 mn tonnes, down 3.2% yoy. Food grain production is down due to poor monsoons in the Kharif season and low Rabi acreage. While the southwest monsoon was 12% deficient, total area coverage as on February 13, 2015 under Rabi crops declined to 61.6 mn hectares from 65.7 mn hectares in FY14. Lower agricultural production, falling yields and crop prices are impacting rural cash flows. Non‐agricultural demand pull has also been subdued as infrastructure and construction failed to pick up.

A lot depends on 2015 monsoon: The monsoons are expected to be close to normal in 2015, according to initial forecasts, but meteorologists say it is too early for accurate monsoon predictions. As the cash flow of MMFS customers are stretched due to a slow rural economy, another year of poor rains can have a spiralling effect on MMFS’ already poor asset quality.

Page | 25 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

Banks gain ground in rural areas—is this threat to MMFS? • Banking outlets (branches and bank correspondents) in villages increased from

67,694 in FY10 to 383,804 in FY14, with only 12% being branches • While the banks’ deposit‐account penetration increased significantly from 33

accounts per 100 rural adults in FY01 to 68 accounts in FY13, credit penetration increased from 5.7% to just 8.9%

• In the past three years (FY12‐14) banks opened 27,000 branches across India, 41% of which were in tier‐5 and ‐6 centres.

Bank penetration has increased significantly over the past five years. Banks made significant inroads into rural areas over the past 3‐4 years as is evident from a sharp rise in the number of banking outlets. The banking outlets in villages increased from 67,694 in FY10 to 383,804 in FY14, but only 12% were brick‐and‐mortar branches and 88% were banking correspondents. Business correspondents are used mainly for liability‐based transactions (deposits and payment‐related) and play a limited role in credit growth. Besides, as most borrowers in rural areas do not have a credit profile, banks’ credit penetration in rural areas is low.

Rise in banking outlets in the last four years Banking correspondents form 88 % of the outlets

Source: RBI Deposit penetration up sharply but credit penetration is low in rural areas. While banks’ deposit‐account penetration increased significantly from 33 accounts per 100 rural adults in FY01 to 68 accounts in FY13, credit penetration increased from 5.7% to just 8.9%. This was mainly due to (1) lack of credit worthiness of rural borrowers due to irregular cash flows, (2) a long time taken by banks to sanction loans and (3) large distances between branches and customers. Deposit penetration increases sharply, credit penetration increase marginal Penetration (%) FY01 FY10 FY11 FY12 FY13

Deposit accounts/100 people All INDIA >19 yrs 76.2 105.5 113.6 123.6 139.7Rural > 19 yrs 33.4 48.5 52.9 58.4 67.6Urban > 19yrs 176.9 217.9 233.2 252.2 281.9Credit accounts/100 people All India > 19yrs 9.3 17.0 16.9 17.9 17.1Rural > 19 yrs 5.7 7.8 8.3 8.5 8.9Urban > 19yrs 17.9 35.2 34.0 36.5 33.5

Source: RBI

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

10‐Mar 11‐Mar 12‐Mar 13‐Mar

Banking Outlets in Villages >2,000 popolation

Banking Outlets in Villages <2,000 population

33,378 34,811 37,471 40,837 46,126 48,12634,17480,802

141136221341

328,678387,626

142595

3,146

6,276

9,000

11,000

0

100,000

200,000

300,000

400,000

500,000

10‐Mar 11‐Mar 12‐Mar 13‐Mar FY14 H1FY14

Banking Outlets in Villages ‐Branches Banking Outlets in Villages ‐BCs Banking Outlets in Villages ‐Other Modes

Page | 26 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

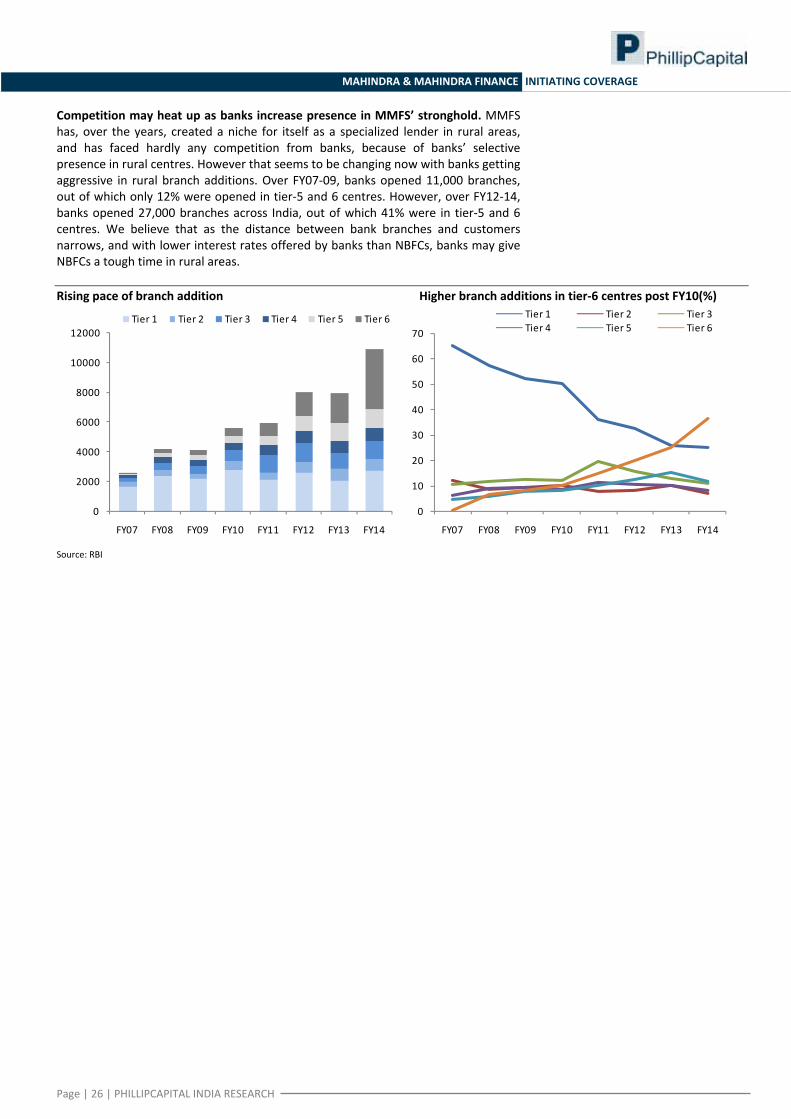

Competition may heat up as banks increase presence in MMFS’ stronghold. MMFS has, over the years, created a niche for itself as a specialized lender in rural areas, and has faced hardly any competition from banks, because of banks’ selective presence in rural centres. However that seems to be changing now with banks getting aggressive in rural branch additions. Over FY07‐09, banks opened 11,000 branches, out of which only 12% were opened in tier‐5 and 6 centres. However, over FY12‐14, banks opened 27,000 branches across India, out of which 41% were in tier‐5 and 6 centres. We believe that as the distance between bank branches and customers narrows, and with lower interest rates offered by banks than NBFCs, banks may give NBFCs a tough time in rural areas. Rising pace of branch addition Higher branch additions in tier‐6 centres post FY10(%)

Source: RBI

0

2000

4000

6000

8000

10000

12000

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Tier 1 Tier 2 Tier 3 Tier 4 Tier 5 Tier 6

0

10

20

30

40

50

60

70

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Tier 1 Tier 2 Tier 3Tier 4 Tier 5 Tier 6

Page | 27 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

Favourable interest rate climate to lead to lower costs • MMFS’ borrowing profile is largely dominated by bank borrowing, which

constitutes 49% of the book, followed by bonds (19%) and fixed deposits (16%), commercial paper (9%) and securitisation (7%)

• Around 83% of the borrowings will benefit from lower bond yields and base rates in FY16/17. A 1% change in borrowing cost in FY16/17 will drive 50‐60 bps reduction in overall cost of borrowings over FY16‐17

• With a favourable spread of 125‐200 bps in bonds over bank loans, the company is incrementally going for bond issuance. We expect the bond proportion in total borrowing to increase to 25‐30% in FY16.

Banks dominate the borrowing profile. MMFS’ borrowing profile is largely dominated by banks, which constitute 49% of the book, followed by bonds (19%) and fixed deposits (16%), commercial paper (9%) and securitisation (7%). Prior to FY09, bonds used to contribute almost 60% to the total borrowing, with bank loans being the second largest source of borrowing, at 26%. However due to adverse international developments and some domestic factors, liquidity conditions tightened significantly between mid‐September and October 2008, resulting in pressure on money markets, which in turn resulted in huge redemptions for mutual funds. As mutual funds were the leading source of borrowings for the company (contributing 41% to the total borrowing), the company had to shift to banks and insurance companies. As a result, the share of bonds in total borrowing declined from 60% in FY08 to 19% in FY11. As the interest rate environment remained tight until FY14, bond borrowing has been 20‐25% since FY11. Sources of borrowing – instrument wise Sources of borrowing – lender wise

Source: Company, PhillipCapital India Research Bank borrowing dominates the borrowing profile with wt. avg cost of ~10%

___________FY13___________ ___________FY14___________

Proportion in

total borrowings Weighted

average costProportion in

total borrowingsWeighted

average costBonds 28.9 9.9 24.4 9.8Banks 58.2 9.8 60.3 10.2Fixed Deposit 12.3 9.7 15.1 9.7Commercial paper/ ICD 0.5 9.2 0.2 9.5Total 100.0 9.8 100.0 10.0

Source: Company, PhillipCapital India Research

0%

20%

40%

60%

80%

100%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Bonds Bank Term Loans SecuritisationFixed Deposit Commercial Paper

0%

20%

40%

60%

80%

100%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Insurance Cos Mutual Fund Banks Others

Page | 28 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

Falling bond yields to boost bond borrowings; cut cost by 60‐70 bps over FY16‐17. While bond yields have eased considerably from a high of 9% in January 2014 to 7.8% now, banks’ base rates remain stable at 10‐10.25%. This has created a favourable spread of ~200 bps in bonds over bank loans. In FY13/14 MMFS’ bank borrowing and bond borrowing cost was almost at par at 9.8‐10.2%. Benefiting from falling bond yields, MMFS has, over the past few months, been borrowing mainly through the bond market. The company issued bonds at 8.5‐9% yield in November. We expect the bond proportion in total borrowing to increase to 25‐30% in FY16 and bank borrowing to fall by equal proportion. Around 30% of the total borrowings (with blended cost at 10.1%) will mature in FY15, out of which 26% comprises bond borrowings, 61%, bank borrowings and 12%, FD and commercial paper. Assuming MMFS replaces 50% of the total maturing borrowings in FY15 by bonds (at an average yield on 9.1%) it will drive 7‐8 bps improvement in cost in FY15. The larger benefit of the repricing will come in FY16/17 when 56% of the borrowings will mature. Besides, 27% of the total borrowings have a reset clause with the bank. So, in total, around 83% of the borrowings will benefit from lower bond yields and base rate in FY16/17. We expect a 60‐70 bps reduction in overall cost of borrowings over FY16‐17. 80%+ borrowings will get reprice at lower rates in FY16/17

Proportion of total borrowings

(%) Maturity profile of borrowings (On book)

Wt Avg Cost(%)

Total Borrowing (Rsbn)

Bank borrowing

Non Bank borrowing

Maturity beyond 5 years 10.00 7 0.0 3.0Maturing between 3 years to 5 years 10.25 28 9.0 2.5Maturing between 1 year to 3 years 9.94 134 33.2 22.9Maturing within 1 year 10.13 70 18.1 11.3Grand Total 10.02 239 60.3 39.7

Source: Company, PhillipCapital India Research

Falling interest rate to drive improvement in cost of funds

Source: Company, PhillipCapital India Research

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Mar‐05 Mar‐07 Mar‐09 Mar‐11 Mar‐13 Mar‐15

10 Yr Gsec Yield (%) 3 Year AA Corp Bond yield Repo rate (%)

Page | 29 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

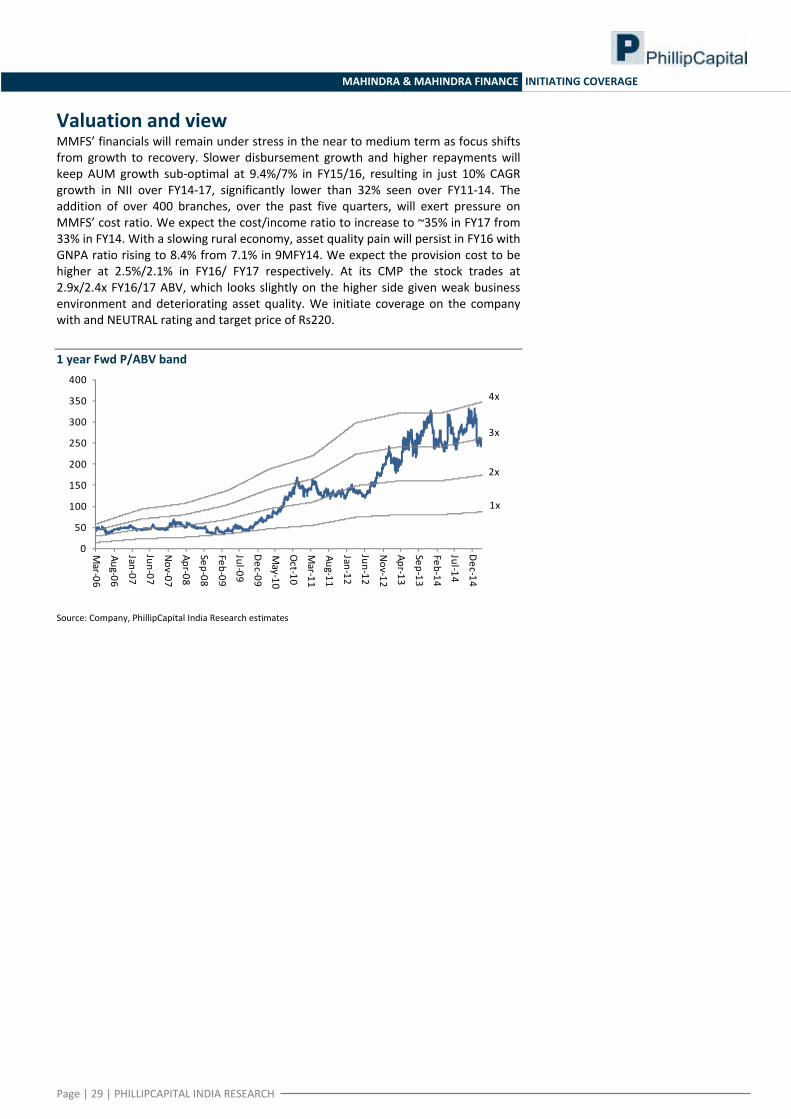

Valuation and view MMFS’ financials will remain under stress in the near to medium term as focus shifts from growth to recovery. Slower disbursement growth and higher repayments will keep AUM growth sub‐optimal at 9.4%/7% in FY15/16, resulting in just 10% CAGR growth in NII over FY14‐17, significantly lower than 32% seen over FY11‐14. The addition of over 400 branches, over the past five quarters, will exert pressure on MMFS’ cost ratio. We expect the cost/income ratio to increase to ~35% in FY17 from 33% in FY14. With a slowing rural economy, asset quality pain will persist in FY16 with GNPA ratio rising to 8.4% from 7.1% in 9MFY14. We expect the provision cost to be higher at 2.5%/2.1% in FY16/ FY17 respectively. At its CMP the stock trades at 2.9x/2.4x FY16/17 ABV, which looks slightly on the higher side given weak business environment and deteriorating asset quality. We initiate coverage on the company with and NEUTRAL rating and target price of Rs220. 1 year Fwd P/ABV band

Source: Company, PhillipCapital India Research estimates

0

50

100

150

200

250

300

350

400

Mar‐06

Aug‐06

Jan‐07

Jun‐07

Nov‐07

Apr‐08

Sep‐08

Feb‐09

Jul‐09

Dec‐09

May‐10

Oct‐10

Mar‐11

Aug‐11

Jan‐12

Jun‐12

Nov‐12

Apr‐13

Sep‐13

Feb‐14

Jul‐14

Dec‐14

1x

2x

3x

4x

Page | 30 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

Annexure: 1

MMFS: Background and business model Company background. Mahindra & Mahindra Financial Services, a subsidiary of Mahindra & Mahindra, is the second largest asset‐finance NBFC with assets under management of Rs365 bn. The company was incorporated in 1991 as a captive financier for M&M tractors and UVs. However since FY02 MMFS diversified its portfolio to other OEM products as well, which now constitute more than 50% of its AUM. MMFS also diversified its product portfolio to other vehicle categories such as commercial vehicles and cars. It ventured into insurance broking, mutual fund distribution and rural‐housing finance. MMFSL has a pan‐India presence, with 1,088 branches, of which almost 80% are in rural and semi‐urban areas. MMFS has two key subsidiaries engaged in insurance broking and rural housing finance. Well diversified portfolio. Since incorporation in 1991, until 2002, MMFS was the captive financier for its parent’s tractors and UVs. However after 2002 the company not only started financing other OEMs’ vehicles, but expanded its product portfolio to cars and commercial vehicles. Now, no single product segment contributes more than 30%, with highest contribution being from UVs (30%), followed by cars/tractors (23%/19%). Commercial vehicle/refinance, into which MMFS entered late, comprise 13%/15% of the product portfolio. The management is not expecting the product mix to change dramatically from here, but it expects the CV share to improve in the next 2‐3 years as the recovery plays out. Deeper rural penetration the backbone of the company’s business model. MMFS has been a major player in rural areas with almost 80% of its branches catering to rural customers. While the company is present in most of the districts (576 districts out of 676 districts in India), it has gone deeper into the rural hinterland as the distance between two branches has come down to 55 kms in H1FY15 from 104 kms in FY06. MMFS has penetration of as high as 45% in South India and 36‐38% in North and West India. With aggressive branch expansion distance between branches declined to 60kms

Source: Company, PhillipCapital India Research

0

20

40

60

80

100

120

0

200

400

600

800

1,000

1,200

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E

No of Branches Distance between branches (km)

Page | 31 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

Management Mr. Bharat Doshi, Chairman. Mr. Doshi joined Mahindra & Mahindra as an executive in 1973 and was elevated to the Board of the Company as Executive Director in 1992. In November 2013, he transited from his position as Executive Director & Group CFO to Non‐Executive Director. Mr. Doshi holds a Master's degree in law from Bombay University. He is a fellow member of the Institute of Chartered Accountants of India and the Institute of Company Secretaries of India. He also participated in the Program for Management Development (PMD) at Harvard Business School. Mr. Doshi was a Member of the Reserve Bank of India (RBI) constituted Working Group to examine emerging issues pertaining to regulation of the NBFC sector. He is a member of the RBI‐constituted Committee on Comprehensive Financial Services for Small Businesses and Low‐Income Households (CCFS). Mr. Ramesh Iyer, Managing Director. He has been the Managing Director of the company from April 30, 2001 and has been associated with the company since its inception. He holds a Bachelor's degree in Commerce and a Master's degree in Business Administration. He has vast experience in matters relating to business development, finance and marketing. He is also a member of the Group Executive Board of Mahindra & Mahindra, the holding company, and is on the boards of various Mahindra Group companies. Mr. Iyer is a member of the Banking & Finance Committee of the Bombay Chamber of Commerce and Industry, the core committee of Finance Industry Development Council (FIDC) and the Task Force of NBFCs of Federation of Indian Chambers of Commerce and Industry (FICCI). He is also co‐Chairman of the Group on Finance & Leasing and Insurance of the Council of Economic Affairs set up by Society of Indian Automobile Manufacturers (SIAM). Mr. V. Ravi, Chief Financial Officer. Mr. V. Ravi has been associated with the company since its inception. Mr. Ravi is also on the Board of other Mahindra Group Companies like Mahindra Rural Housing Finance Company, Mahindra Business and Consulting Services and Mahindra Finance USA LLC. He served with Mahindra Ugine Steel Company (MUSCO) for nine years on treasury, finance and diversification projects prior to his induction in Mahindra & Mahindra Financial Services. He is a member of the FICCI Committee on Corporate Finance. He has also been a member of the Asia Council of the Conference Board, USA, and the Informal Advisory Group of the Reserve Bank of India. Key Shareholders Number (mn) % of total

Mahindra & Mahindra Ltd 291 51.2 Cartica Capital Ltd 44.6 7.85 JP Morgan Sicav Investment Company (Mauritius) Ltd 6.2 1.08 JP Morgan Funds ‐ Emerging Markets Equity Fund 7.0 1.23 Government of Singapore 7.5 1.32 Aranda Investment (Mauritius) Pvt Ltd 10.8 1.91 Total 367.3 64.6

Source: Company, PhillipCapital India Research estimates, BSE

Page | 32 | PHILLIPCAPITAL INDIA RESEARCH

MAHINDRA & MAHINDRA FINANCE INITIATING COVERAGE

Financials

Profit and loss (Rs mn) Balance sheet (Rs mn) (Year Ending Mar 31) FY14 FY15E FY16E FY17E (Year Ending Mar 31) FY14 FY15E FY16E FY17E

Net interest income 25,231 27,552 30,697 34,344 Equity 1,127 1,127 1,127 1,127

Other income 2,419 2,424 2,635 2,868 Reserves 49,815 54,889 61,064 69,329

Net Income 27,650 29,976 33,332 37,211 Net worth 50,942 56,016 62,191 70,456

Operating expenses 9,134 10,180 11,441 12,889 Borrowings 239,306 263,474 273,412 309,927

Pre‐provision profit 18,516 19,796 21,891 24,322 Current liabilities & others 26,409 26,211 26,306 26,435

Provisions 5,058 8,576 8,888 8,376 Total liabilities 316,657 345,700 361,909 406,818

Profit before tax 13,458 11,221 13,003 15,946 Net block 1,195 1,029 894 798

Tax 4,585 3,703 4,291 5,023 Investments 8,692 8,691 8,691 8,691

Tax rate(%) 34.1 33.0 33.0 31.5 Loans 296,170 325,880 342,223 387,228

Adjusted Profit after tax 8,872 7,518 8,712 10,923 Current assets & others 10,601 10,100 10,100 10,100

Total assets 316,657 345,700 361,909 406,818

Dupont (as % of Assets) Key ratios (Year Ending Mar 31) FY14 FY15E FY16E FY17E (Year Ending Mar 31) FY14 FY15E FY16E FY17E

Interest Income 16.5 15.9 16.0 16.2 NIM (%) 8.8 8.3 8.7 8.9

Interest Expense 7.7 7.6 7.3 7.3 NIM (%) ‐On AUM 8.1 7.7 7.9 8.0

Net Interest Income 8.8 8.3 8.7 8.9 Cost/ Income (%) 33.0 34.0 34.3 34.6

Other income total 0.8 0.7 0.7 0.7 Credit cost (%) 1.8 2.6 2.5 2.2

Net Income total 9.7 9.1 9.4 9.7 RoA(%) 3.1 2.3 2.5 2.8

Operating expenses total 3.2 3.1 3.2 3.4 RoE (%) 18.6 14.1 14.7 16.5

Preprovision profit 6.5 6.0 6.2 6.3 Leverage (x) 6.0 6.2 6.0 5.8

Provisions 1.8 2.6 2.5 2.2 Tier I (%) 15.5 15.6 15.5 15.6

Profit before tax and ex items 4.7 3.4 3.7 4.2 CAR (%) 18.0 17.3 17.8 18.2

Profit before tax 4.7 3.4 3.7 4.2 No of shares (mn) 563.5 563.5 563.5 563.5

Tax total 1.6 1.1 1.2 1.3 Gross NPA (%) 4.4 7.8 8.4 6.5

Profit after tax 3.1 2.3 2.5 2.8 Net NPA (%) 1.9 3.3 3.8 2.9

Provision coverage (%) 59.1 58.0 55.0 55.0

Growth (%) Valuation ratios (Year Ending Mar 31) FY14 FY15E FY16E FY17E (Year Ending Mar 31) FY14 FY15E FY16E FY17E

Net interest income 23.0 9.2 11.4 11.9 FDEPS (Rs) 15.7 13.3 15.5 19.4

Net Income total 21.5 8.4 11.2 11.7 PER (x) 16.3 19.2 16.6 13.2

Preprovision profit 20.7 6.9 10.6 11.2 Book value (Rs) 90.4 99.4 110.4 125.0

Profit before tax 5.2 ‐16.6 15.9 22.7 P/BV (Rs) 2.8 2.6 2.3 2.0

Profit after tax 0.5 ‐15.3 15.9 25.5 Adjusted book value (Rs) 80.2 80.4 87.3 105.1

Loan 23.2 10.0 5.0 13.2 P/ABV (Rs) 3.2 3.2 2.9 2.4

Disbursement 6.5 ‐5.0 10.0 20.0 P/ PPP 7.8 7.3 6.6 5.9

AUM 22.3 9.4 7.0 15.0 Dividend yield (%) 1.5 1.5 1.6 1.6

INSTITUTIONAL EQUITY RESEARCH

Page | 33 | PHILLIPCAPITAL INDIA RESEARCH

Shriram Transport Finance (SHTF IN) On the cusp of recovery INDIA | NBFCs | Company update

5 March 2015