Embed Size (px)

Citation preview

Insolvency Insolvency Outcomes:Outcomes:Research Research FindingsFindings

Dr Sandra Frisby Dr Sandra Frisby Baker & McKenzie Lecturer in Company and Baker & McKenzie Lecturer in Company and

Commercial LawCommercial LawUniversity of Nottingham University of Nottingham

27 July 200627 July 2006

The Research ProgrammeThe Research Programme• 2063 Companies

– 953 companies in administrative receivership– 1110 companies in administration

• Procedures entered into between September 2001 and September 2004– Comparison between pre- and post-Enterprise

Act outcomes

• 27 Interviews– Bankers and Insolvency Practitioners– Telephone contact with receivables financiers

The DatabaseThe Database

Trends Relating to Trends Relating to Companies Companies

• Business Sectors– High incidence of printing firms

• Locations– 14% of all companies located in London– 11% of companies located in

Manchester, Birmingham, Leeds, Bristol or Nottingham• No significant variation from general

incorporation trends

Appointment Trends: Appointment Trends: Administrative Receivership Administrative Receivership

Receivership Appointors

40%

20%

17%

12%

5%4% 2%

Major Clearing Bank

IndependentFactor/ Invoice Discounter

Other Bank or CreditInstitution/OverseasBank

Corporate Charge Holder

Venture Capital Provider

Individual Charge Holder

Bank Invoice Discounter

Appointment Trends: Appointment Trends: Administration Administration

• Method of Appointment – 58% Company/Director appointment (para.22)– 30% Court appointment (para.12)– 12% Charge Holder appointment (para.14)

• Going behind the figures– Para.22 appointments may be charge holder

driven• Non-interventionist stance from charge holders

– Para.14 appointments: trusted practitioners – Para.12 appointments: Additional ‘legitimacy’?

Firms Appointments: Entire Firms Appointments: Entire SampleSample

Firms

29%

9%

5%

5%5%

3%

3%

3%

3%

3%

3%

3%

3%

3%

2%

2%

2%

2%

2%1%

1%1%

1%1% 1% 1%1% 1%1%

Other

Begbies Traynor

Pricew aterhouseCoopers

BDO Stoy Hayw ard

KPMG

Baker Tilly

Kroll

Grant Thornton

Poppleton & Appleby

Tenon Recovery

HKM Harlow Khandhia Mistry

Mazars

RSM Robson Rhodes

Ernst & Young

Smith & Williamson

PKF

DTE Leonard & Curtis

Hacker Young

Deloitte

Rothman Pantall & Co

Casson Beckman & Partners

Numerica

Cranf ield Recovery

Thompson Shaw Associates

Fisher Curtis

Moore Stephens

P & A Partnership

David Rubin & Partners

Geof f rey Martin & Co

New Entrants Post-New Entrants Post-Enterprise Act Enterprise Act

• 69 new firms taking administration appointments – 21.8% of the 710 post-Enterprise Act

administrations

• Comparison with entire sample– 63% Company/Director appointment– 31% Court appointment – 6% Charge Holder appointment

• Absence of charge holder?• Comfortably secured charge holders?

Duration of Procedures: Duration of Procedures: ComparisonComparison

• Significantly longer duration in administrative receivership – Average of 558 days as compared to

average of 377 days in administration– The Brumark effect

• Similar impact on both procedures?

Pre- and Post-Enterprise Act Pre- and Post-Enterprise Act DurationsDurations

• All Administrative Receiverships– 17% of cases lasting over 3 years– 15% of cases lasting over 2 years– 48% of cases lasting over 1 year– 20% of cases lasting less than one year

• All Administrations – 6% of cases lasting over 3 years– 3% of cases lasting over 2 years– 22% of cases lasting over one year– 69% of cases lasting less than one year

Pre-Enterprise Act Pre-Enterprise Act Administrations Administrations

Pre- EA Administrations

16%

15%

12%

11%

10%

9%

6%

6%

5%

5%

3%

1%

1%

Over 36

10 to 12

4 to 6

7 to 9

19 to 21

13 to 15

16 to 18

25 to 27

22 to 24

0 to 3

28 to 30

31 to 33

34 to 36 16% over 3 years11% over 2 years30% over 1 year43% under 1 year

Post-Enterprise Act Post-Enterprise Act Administrations Administrations

Post-EA Administrations

65%

9%

8%

8%

7%

2%

1%

0%

10 to 12

13 to 15

16 to 18

7 to 9

4 to 6

0 to 3

19 to 21

22 to 24

18% over 1 year82% under 1 year

Secured Creditors: ProfilesSecured Creditors: Profiles• Fragmentation of Security

– Receivables financiers• Brumark • More effective method of lending

– Hire purchase/leasing– Bondholders/Debt Traders

• Effects– Multiple agendas?– Easier withdrawal?– Incentives to withdraw (termination fees?)

Secured Creditors: ReturnsSecured Creditors: Returns• The Brumark Effect• Administrative receivership

– 100% return in 22.6% of sample– Zero return in 0.7% of sample

• Administration (pre-Enterprise Act)– 100% return in 29.9% of sample– Zero return in 0.9% of sample

• Administration (post-Enterprise Act)– 100% return in 36.8% of sample– Zero return in 0.7% of sample

Preferential CreditorsPreferential Creditors• Average of 11.2% return across entire

sample– Average of 6.7% return in receivership and

15.9% in administration• Absence of secured creditors in some administration

cases

• The Position of the Crown– Loss of minimum £28.5m per annum as a

result of abolition of preferential status– Approach to troubled companies generally

supportive, but inconsistent– No change in approach post-Enterprise Act?– No appearance of monitoring

Unsecured Creditors Unsecured Creditors • Returns

– 3.3% average return– Zero return in 28.9% of cases

• Approach– Interviewee comments

• Passive/Disinterested

• Prescribed Part– 25 cases recorded

• One distribution of 5.8% of total unsecured debt• Average distribution on estimated prescribed part

would be 2.13% of unsecured debt

Insolvency Outcomes: Insolvency Outcomes: General General

• Possible Outcomes– A) Rescue of the company– B) Rescue of part of the company– C) Going concern sale of the business of

the company– D) Going concern sale of part of the

business of the company– E) Asset sale– F) Procedure ongoing

Outcomes in Administration: Outcomes in Administration: Entire SampleEntire Sample

Administration Overall

53%

31%

4%

5%

3%3%

1%

0%

0%

E

C

F

D/E

A

C/E

D

B/E

B

53% ‘liquidations’40% business rescue3% corporate rescue 4% unknown

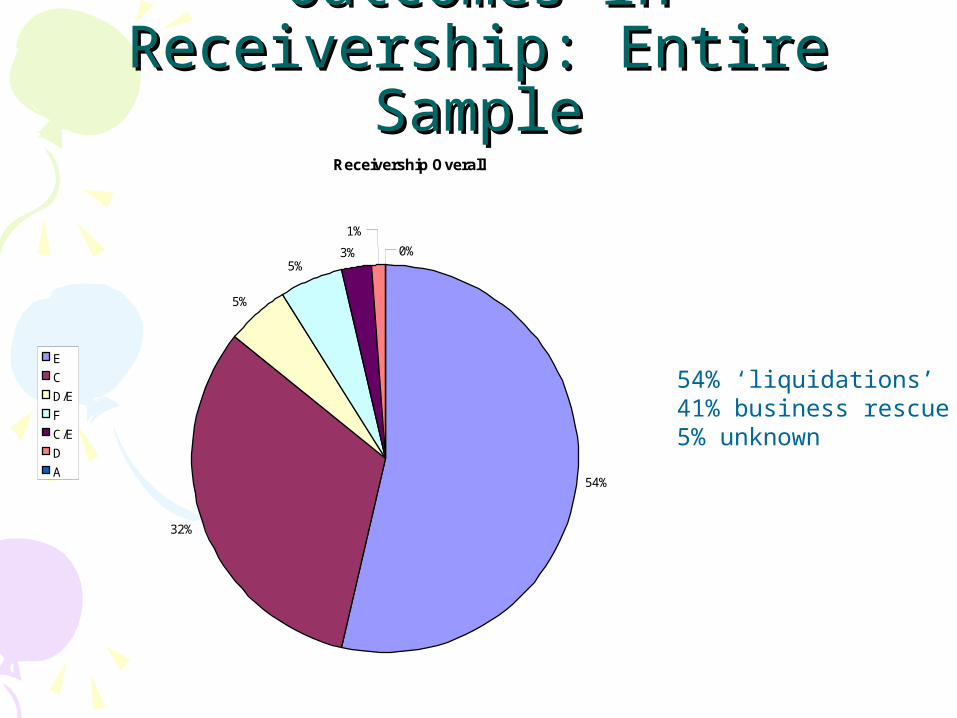

Outcomes in Receivership: Outcomes in Receivership: Entire SampleEntire Sample

Receivership Overall

54%

32%

5%

5%3%

1%

0%

E

C

D/E

F

C/E

D

A

54% ‘liquidations’41% business rescue5% unknown

Pre-Enterprise Act Pre-Enterprise Act Administration OutcomesAdministration Outcomes

Administration Pre-EA

44%

29%

9%

7%

5%4%

2%

0%

E

C

D/E

F

C/E

A

D

B/E

44% ‘liquidations’45% business rescue4% corporate rescue7% unknown

Post-Enterprise Act Post-Enterprise Act Administration OutcomesAdministration Outcomes

Administration Post-EA

56%32%

3%

3%3%

2%

1%

0%

E

C

D/E

F

A

C/E

D

B

56% ‘liquidations’38% business rescues3% corporate rescues 3% unknown

Corporate Rescue: ViewsCorporate Rescue: Views• Informal rescue activity by the banks

– Ongoing, and generally viewed as successful • Use of the CVA

– Viability of proposal • Unworkable proposals may deter future creditors

• How realistic is corporate rescue through formal insolvency?– Attitudes of creditors– Insolvency-related depreciation– Late entry into the procedure – Possibility considered but rarely achievable

Business Rescue: Pre-PacksBusiness Rescue: Pre-Packs• Trends towards pre-packaging

– To independent purchasers – To connected parties

• Advantages of pre-packs– Preservation of goodwill and avoidance of costs– Encouraging a rigorous procedure through accountability– Preservation of employment?– Better realisations?– The ‘second-chance’ ideal?

• Disadvantages of pre-packs– Lack of transparency– The image problem– Subsequent insolvency of Newco?

Administrations as ‘Disguised Administrations as ‘Disguised Liquidations’: The Phenomenon Liquidations’: The Phenomenon • Explaining the higher incidence of asset

sales in post-Enterprise Act administrations

• Using administration instead of CVL– Higher incidence of company/director

appointments – Non-interventionist stance of charge holders– Low barrier to entry into administration: para.

3(1)(b) Schedule B1 Insolvency Act 1986

Disguised Liquidations: Disguised Liquidations: Incentives and EvaluationIncentives and Evaluation

• The Leyland Daf effect– Costs and expenses (including fees) payable out of floating

charge • 55% asset sales pre-Leyland Daf compared to 62% post-Leyland

Daf• But are there significant floating charge assets anyway?

• Securing the appointment– Avoiding the s.98 meeting

• Commercial advantage– Speed– Opportunities for trading– Preservation of contracts

• A New Entrant Phenomenon?– Higher rates of asset sales, but inconclusive

• Do we need the CVL?

Conclusions Conclusions • Significant drop in duration of

administration• Large number of ‘new entrant’ firms• No detrimental effects for secured

creditors• No rise in incidence of corporate rescue• Both administration and receivership

equally likely to result in a business rescue• Trend towards pre-packs• Trend towards ‘disguised liquidations’