Embed Size (px)

Citation preview

Infrastructure Needs Assessment for Distribution of FrozenProcessed Potato Products in Southeast Asian Countries

Final Report on Cooperative Agreement #5599-109To Foreign Agricultural Service, Emerging Markets Program,

U.S. Department of Agriculture

by

Catherine L. ViatorWu-yi (Dennis) FangJennifer L. Hadley

Wipon (Marty) Aiew

Under the direction ofDr. Victoria SalinDr. Rodolfo Nayga

Department of Agricultural EconomicsTexas A&M University

December 2000

Contact information:Dr. Victoria SalinDepartment of Agricultural EconomicsTexas A&M University2124 TAMUCollege Station, Texas [email protected]: 979-845-8103Full report available at http://agecon.tamu.edu/faculty/salin/research/aptapg.htm

Executive Summary

As U.S. food trade increasingly includes high-value fresh or processed products that require coldstorage to maintain their quality, there will be a need to develop infrastructure to support thedistribution and storage of chilled and frozen foods. This report addresses cold chaininfrastructure in the Philippines and Thailand, and includes a preliminary study of Vietnam. Thestudy was prepared with the American Potato Trade Alliance (APTA), with support from theForeign Agricultural Service, U.S. Department of Agriculture. The purpose of this project is toassess the commercial feasibility of investments in cold chain infrastructure improvement neededto distribute frozen foods in and beyond major cities in these emerging markets. The exploratorystudy of business culture and the investment climate in Vietnam will provide the foundation for apossible follow-up effort.

The objectives of this project were to:

(1) Develop pilot projects illustrating business opportunities with commercial potential in theinfrastructure needed for transportation and handling of frozen foods to secondary cities inthe Philippines and Thailand; and

(2) Draw conclusions about feasibility of projects, using risk analysis based on economicconditions and institutional constraints.

A research team visited the capital cities and major secondary cities in the Philippines andThailand during May and June 2000. Representatives of approximately 80 companies wereinterviewed including cold storage businesses, transportation service companies (shipping linesand trucking and railway cargo service companies), port authorities, frozen food companies,quick service restaurants, banks, and government officials.

Philippines

Insufficient quality cold storage is the main issue facing companies that distribute frozenprocessed potato products in the Philippines, especially in secondary cities such as Bacolod andCebu. Cold storage business is seasonal, with monthly utilization rates ranging from 60 percentto 100 percent. Expensive inter-island shipping from Manila to secondary cities on the southernislands is another bottleneck. Freight rates for inter-island shipping are higher than internationalshipping charges. For example, the cost from Hong Kong or Japan to Manila is about $1,500 per40-foot container, while from Manila to Cebu the cost is $1,800 to $2,000 per 40-foot container.Furthermore, although Manila and Cebu have modern seaports, the port in Bacolod is incapableof handling 40-foot containers. Because the seafood industry in Bacolod is declining, coldstorage and port facilities have not been developed. It was also noticed that traffic congestion isa serious problem in Manila and makes inter-city deliveries more difficult.

The proposed pilot project in the Philippines was to build medium-sized cold storage warehousesin designated secondary cities. Two scenarios were used to assess commercial feasibility of theproposed new cold storage. The first is a “worst-case” scenario that assumes that the newwarehouse is not used at full capacity utilization. The project would break even if it is filled to63 percent of capacity, on average. This result assumes a 15 percent discount rate, 300 pesos per

ii

cubic meter per month in storage charges, and a 15,000 cubic meter facility. These and otherbaseline assumptions are based on information provided in interviews conducted in thePhilippines. Annual net income is 4.5 million pesos and the Net Present Value of the 10-yearproject is 340,550 pesos, when discounted at 15 percent. This is a modestly attractive investmentopportunity given these pessimistic assumptions.

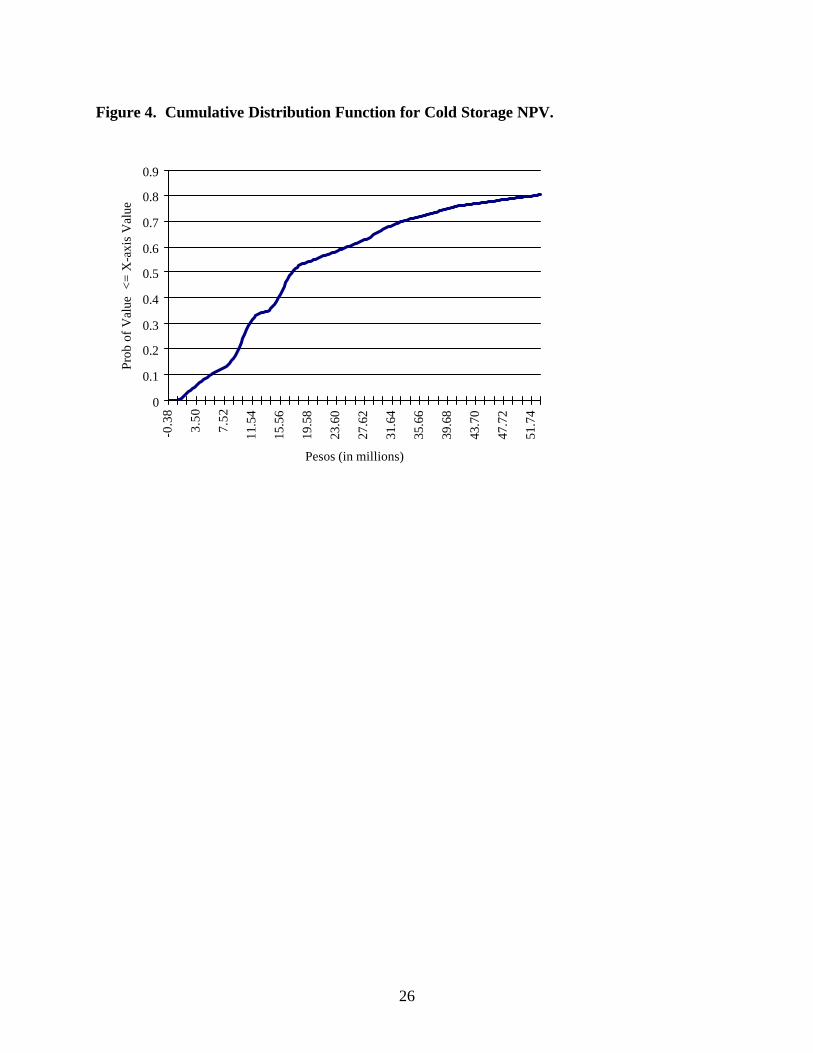

Most cold storage facilities in the Philippines described a seasonal pattern of demand for theirservices. These businesses operate at full capacity utilization in the fall and winter, leading up tothe holiday season. To model the seasonal variation, the utilization rate was simulated to followan empirical distribution developed according to the usage patterns described by officials of coldstorage companies in the Philippines. All other assumptions were the same as in the previous setof financial statements. The average annual capacity utilization rate is 78 percent, according tothe simulation. The expected Net Present Value (NPV) for the project is positive, at 22.3 millionpesos, discounted at 15 percent. Thus, a new cold storage facility that experiences variation inits business similar to those warehouses now in the market appears to be an attractive investment.If an investor has a higher discount rate, the simulated project was found to break even at 27percent.

The project team feels that the market for frozen french fries is well developed and will continueto expand in the Philippines. Investment in cold storage warehouses in Cebu City and Cagayande Oro will be feasible given declining tariffs, the favorable market situation, and the absence ofcompetition at the moment. A caution is the effect of recent political issues on future economicgrowth and the capital market in the Philippines.

Thailand

Compared with the Philippines, Thailand has less severe problems in distributing frozenprocessed potato products from ports to secondary cities. Ports in Bangkok and Laem Chabanghave good facilities to handle imports and exports of frozen food products. Thailand has a well-built highway system connecting the Bangkok ports to secondary cities. Private cold storagefacilities (owned by frozen food exporters and importers, including an importer of french fries)are modernized and can meet strict quality standards. In addition, the capacity is enough tosatisfy current demand. However, there is only one public cold storage facility available in theBangkok area and none in the other cities visited. Thus if the market for frozen and chilled foodswere to grow rapidly, the limited amount of cold storage could present a barrier in the future.

Cold chain infrastructure in Thailand is basically sufficient to meet the current distribution needsof frozen processed potatoes. Thai consumer acceptance of western-style quick servicerestaurant foods is lower than the level observed in the Philippines. However, it is possible thattrucking fleets near ports could help improve the efficiency of distribution if the demandincreases in the near future.

The proposed pilot project in Thailand was to establish a refrigerated trucking company to helpmove frozen food products between Bangkok and secondary cities. The trucking fleet wouldconsist of twenty refrigerated vans. The initial scenario reported reflects conditions as ofOctober 2000, with fuel costs relatively high (14.58 baht per liter). Based on this “worst-case”

iii

scenario, the trucking fleet is an attractive investment. The Net Present Value of the five yearproject is 8.7 million baht using a 15 percent discount rate. Variation in fuel costs couldsignificantly affect investment outcomes, and is thus simulated from an empirical probabilitydistribution. The simulation shows the pressure on current profits from the prospect of higherfuel costs. Annual profits are expected to be 9.9 million baht under the stochastic model.However, the expected fuel cost in the simulation reflects 18 months of historical data on retailfuel costs and is more favorable to the investment than the most recently observed oil prices.Given the market demand for trucking services, current competitiveness in the industry,operational and financial risks, and profitability of the proposed pilot project, the research teambelieves it is commercially viable.

Vietnam

Operating a business in Vietnam can be difficult; however, infrastructure improvements andincreasing demand for frozen potato products makes investing increasingly more feasible.Current infrastructure is limited and consumer demand for frozen foods is modest. Only 10quick service restaurants operated in Vietnam as of summer 2000, and total imports of frozenpotatoes were approximately a container load per year. The possibility of normalized traderelations between Vietnam and the U.S. could help to improve the economy and enhance theprospects for investing in the cold chain infrastructure.

iv

Table of Contents

Executive Summary..........................................................................................................................iIntroduction..................................................................................................................................... 1

Objectives..................................................................................................................................... 2Literature Review......................................................................................................................... 2

Field Studies ............................................................................................................................. 3Academic Studies ..................................................................................................................... 4

The Philippines................................................................................................................................ 7Geographic Environment ............................................................................................................. 7

Major Cities .............................................................................................................................. 7Ports.......................................................................................................................................... 8

Business Environment ................................................................................................................. 9Income Distribution.................................................................................................................. 9Urbanization/Westernization.................................................................................................... 9Macroeconomic Conditions.................................................................................................... 10Capital Markets in the Philippines ......................................................................................... 11Bank Regulation and Reforms................................................................................................ 12Financial Assistance Programs ............................................................................................... 12

Issues Identified in Interviews ................................................................................................... 14Shortage of Cold Storage Capacity in Outlying Provinces.................................................... 14High Cost of Inter-Island Shipping ........................................................................................ 15

Proposed Projects....................................................................................................................... 18QSR Market Growth............................................................................................................... 19Industry and Competition....................................................................................................... 19Business and Operation.......................................................................................................... 19

Conclusions ................................................................................................................................ 22Thailand......................................................................................................................................... 38

Geographic Environment ........................................................................................................... 38Major Cities ............................................................................................................................ 38Ports........................................................................................................................................ 39

Business Environment ............................................................................................................... 39Urbanization/Westernization.................................................................................................. 40Macroeconomic Conditions.................................................................................................... 40Capital Markets in Thailand ................................................................................................... 41Financial Assistance Programs ............................................................................................... 42

Issues Identified in Interviews ................................................................................................... 43Inadequate Cold Storage in the South.................................................................................... 43Lack of Refrigerated Truck Fleets.......................................................................................... 44

Proposed Projects....................................................................................................................... 45Frozen/Chilled Food Transportation Market.......................................................................... 45Industry Analysis .................................................................................................................... 45Business and Operation.......................................................................................................... 46

Conclusions ................................................................................................................................ 48Vietnam......................................................................................................................................... 61

Geographic Environment ........................................................................................................... 61

v

Major Cities ............................................................................................................................ 61Ports........................................................................................................................................ 62

Business Environment ............................................................................................................... 62Urbanization/Westernization.................................................................................................. 62Macroeconomic Conditions.................................................................................................... 63

Issues Identified in Interviews ................................................................................................... 64References ..................................................................................................................................... 66

List of Figures

Figure 1. Shaded Relief Map of the Philippines. ........................................................................ 24Figure 2. Cumulative Distribution Function for Cold Storage Utilization. ................................ 25Figure 3. Cumulative Distribution Function for Cold Storage Net Income................................ 25Figure 4. Cumulative Distribution Function for Cold Storage NPV. ......................................... 26Figure 5. Shaded Relief Map of Thailand................................................................................... 50Figure 6. Volume of Traffic Handled in Bangkok Port and Laem Chabang Port....................... 51Figure 7. Cumulative Distribution Function for Trucking Diesel Price. .................................... 51Figure 8. Cumulative Distribution for Trucking Net Income. .................................................... 52Figure 9. Cumulative Distribution Function for Trucking NPV. ................................................ 52Figure 10. Shaded relief map of Vietnam. .................................................................................... 65

List of Tables

Table 1. Number and Length of Bridges in the Philippines, 1990-1996. .................................. 27Table 2. Distance in Nautical Miles Between Major Cities in the Philippines.......................... 27Table 3. Passenger and Cargo Volume Handled at Philippine Ports, January – June 1999. ..... 28Table 4. Projected Population, 2000 and 2005, and 1997 Average Income in the Philippines, by Region. ................................................................................................ 29Table 5. Total Number of Families by Income Class, 1997. ..................................................... 29Table 6. Number of McDonalds Units in Major Cities of the Philippines, 2000. ..................... 30Table 7. Eating Establishments in the Philippines, 1996-1997.................................................. 30Table 8. Summary of Macroeconomic Indicators for the Philippines, 1990-2001.................... 31Table 9. Performance Measures for Commercial Banks in the Philippines............................... 31Table 10. Philippine National Bank and Subsidiaries Consolidated Statement of Income for the Year Ended December 31................................................................................. 32Table 11. Number of Banks in the Philippines at the End of 1998.............................................. 32Table 12. Summary of Door-to-Door Freight Rates from Manila to Secondary Cities............... 33Table 13. Sales Volume and Earnings for Jollibee Foods............................................................ 33Table 14. Assumptions for Cold Storage Income Statements...................................................... 34Table 15. Income Statement for Deterministic Cold Storage Model. .......................................... 35Table 16. Income Statement for Stochastic Cold Storage Model. ............................................... 36Table 17. Descriptive Statistics for Stochastic Cold Storage Model. .......................................... 37Table 18. NPV for Cold Storage Deterministic Model, Under Various Discount Rate Assumptions................................................................................................................. 37

vi

Table 19. Major Cities/Provinces in Thailand, 2000, Population and Distance from Bangkok. ...................................................................................................................... 53Table 20. Comparison of Main Thailand Port Facilities.............................................................. 53Table 21. Comparison of Major QSRs in Thailand Versus the Philippines, 2000. ..................... 53Table 22. Thailand Macroeconomic Indicators, 1990-2000. ....................................................... 54Table 23. Bangkok Bank Financial Statements for the Year Ended, Dec. 31. ............................ 55Table 24. Assumptions for Trucking Project Income Statement. ................................................ 56Table 25. Income statement for deterministic trucking model..................................................... 57Table 26. Cash Flows and NPV for Deterministic Trucking Model, Assuming Various Discount Rates.............................................................................................................. 58Table 27. Income Statement for Stochastic Trucking Model....................................................... 59Table 28. Descriptive Statistics for Stochastic Trucking Model.................................................. 60Table 29. Cash Flows and NPV under Different Discount Rates. ............................................... 60

1

Infrastructure Needs Assessment for Distribution of FrozenProcessed Potato Products in Southeast Asian Countries

Introduction

Infrastructure is a critical component that supports international trade in food and agriculturalproducts. There is a need for the development of infrastructure that is suited for distribution andstorage of chilled and frozen foods, as trade in food products increasingly includes high-value,processed and prepared foods.

The equipment and processes used to protect chilled and frozen foods are referred to as the "coldchain." The integrity of the cold chain must be preserved from the point of production andprocessing, through the transport phases -- loading, unloading, handling, and storage -- to storageat the consuming household or restaurant. There may be several different points at whichloading and storage is required. Potential problems may result from the size of shipments,reliability of equipment, and ownership transfers of products moving through the system. Inorder to unlock the vast emerging markets of Southeast Asia for U.S. frozen food exports, the"cold chain" infrastructure must be strengthened. Both U.S. exports and within-countrycommerce will depend on efficient infrastructure systems, including facilities owned by publicagencies and private commercial interests.

The United States is a major supplier of frozen processed potato products in Southeast Asia. Thecountries in the Asia-Pacific Economic Community (APEC) purchased nearly 80 percent of allU.S. frozen processed potatoes in 1998, which accounted for 1.5 billion pounds of potatoesgrown by U.S. farmers or an estimated 10 percent of the U.S. crop. The value of U.S. frozenprocessed potato exports increased by 140 percent from 1992 to 1997. Export expansion isexpected to continue, especially to the industry's priority growth markets of the Philippines,Thailand, and Vietnam. However, the infrastructure supporting frozen processed potato productsis a limiting factor in supplying markets in and beyond major cities and hampers U.S. exportgrowth potential in the region. As trade barriers decline through the WTO process, the logisticalissues linked with expanded shipments will take on more prominence for U.S. exporterstargeting these emerging markets in Southeast Asia. Primary competition will come from otherthird country producers (the Netherlands, Canada, and Australia) because none of the SoutheastAsian countries have local production of frozen processed potatoes.

This report focuses on the linkages needed to extend the cold chain for distribution of frozenfoods between major capital cities, where most imports arrive, and important secondarypopulation centers throughout the Philippines and Thailand. These two countries represent mostof the diverse transportation situations of Southeast Asia, including archipelagic nations,mountainous conditions, congested cities, and heavy traffic of many types of vehicles onsecondary roads. The study built on previous efforts to develop the cold chain, and focused on adetailed examination of investment conditions and prospects for specific projects that might havecommercial potential and enhance the cold chain.

The following report will outline the objectives of the project and review literature from previousstudies on the subject. Furthermore, an overview of the geographic and business environments,as well as the cold chain logistics for the Philippines and Thailand will be considered. Pilot

2

projects will be developed for both countries as a means of improving the cold chaininfrastructure. The term “infrastructure” encompasses a wide range of facilities and equipment,from roadways and railcars to ports and harbors. This study focuses on the type of infrastructureinvestments that can be commercially viable in the private sector, rather than large public sectorfacilities. Thus, the pilot projects are evaluated using standard business decision rules forinvestments, supplemented with simulations to reflect major uncertainties in the economicenvironment. Conclusions and recommendations for further research are drawn from the pilotproject feasibility assessments. Also included is a brief look at the conditions in Vietnam.

Objectives

The purpose of this project was to assess the commercial feasibility of investments in cold chaininfrastructure improvement needed to distribute frozen foods from ports in major cities intosecondary population centers in the target countries.

Major objectives were to:

(1) Develop pilot projects illustrating business opportunities with commercial potential in theinfrastructure needed for transportation and handling of frozen foods for marketing in thesecondary cities of the Philippines and Thailand; and

(2) Draw conclusions about feasibility of the projects, using risk analysis based on economicconditions and institutional constraints.

There are a great deal of potential benefits for all parties involved. Due to the recent economicdownturn in Asia, it is expected that government investments in major infrastructureimprovements will not be rapidly forthcoming. However, the cold chain infrastructureencompasses many smaller-scale projects, such as refrigerated transportation equipment, that arelikely to be commercially viable for private investment. Therefore, the goal of the research wasto focus less on major public infrastructure, such as ports or roads, than on recommendations forcommercial projects. Nevertheless, basic knowledge of the entire cold chain for imports, fromports to final consuming locations, was necessary. The primary research method was tointerview business and government officials who are involved with food and trade business on aregular basis.

In beginning this study, it was necessary to review some of the major research already publishedon the subject of the cold food chain infrastructure in Southeast Asia.

Literature Review

This review of literature consists of two parts -- field studies and academic studies. While thefindings of this literature search indicate that information on food distribution in Asia,specifically the Philippines and Thailand, is available, there has been limited research on fooddistribution outside of the capital cities. Very little, if any, financial analysis concerning capitalinvestments in the distribution system has been published. In addition, this study providesrelevant geographical and macroeconomic background information on both countries, which was

3

excluded from other reports. Thus, this research serves to add the perspectives of business andeconomic factors to the infrastructure assessments that have previously been available.

Field Studies

The Foreign Agricultural Service and Agricultural Marketing Service conducted two separate butrelated studies in 1998 and 1999, respectively. The purpose of these studies was to expand U.S.agricultural exports that are constrained by cold chain impediments in the Philippines andThailand. Winrock International also completed two studies on the cold chain in Asia, althoughtheir focus was on Indonesia. These four studies established the necessary framework for thisresearch project.

The first USDA study (Beasley) assessed the current state of the cold chain in both countries,and had a broad focus on all U.S. perishable food products. The study presented detailedfindings on distribution from the U.S. to the capital cities of Metro Manila and Bangkok, but didnot evaluate distribution systems within secondary cities. The researchers focused on thetechnical aspects of maintaining the cold chain, such as the use of humidity control, ethyleneoxidizers to prevent premature fruit ripening, proper air circulation in chiller rooms, regulardefrost cycles, and automated cold storage inventory control techniques. In addition, aqualitative demand analysis for perishable foods was done. As a follow-up to the USDA study,educational seminars were conducted to inform those involved in cold chain distribution aboutproper transportation, handling and storage of specific products. Over 200 representatives werein attendance at each country's seminar, and because of the positive response generated, moreseminars are being planned for the future.

The second USDA study (Caron et. al) examined shipments of containerized U.S. agriculturalproducts, including frozen vegetables, to both countries. It primarily discussed internationalshipments into the capital cities, and briefly mentioned within-country shipments. Specificlogistical data was provided, such as the major ocean carriers, refrigerated container rates forvarious Asian ports, and specific time requirements for shipments from the capital city tosecondary cities. Other relevant data in the AMS study includes the following:

• In 1998, only 4 percent of agricultural products were shipped from the U.S. directly to thePhilippines and only 14 percent were shipped directly to Thailand. Reasons cited includeinsufficient port depth and lack of Philippine and Thailand bound cargo per ship.

• The Cebu port in the Philippines, in the southern Visayan Islands, does not have roll-on/roll-off facilities for containers. The Songkhla port in southern Thailand has no cranes and mustrely on the ship's equipment to load and unload containers.

Information on cold storage warehouses was not included in this report. Additionally, neitherstudy mentioned specific business opportunities for improving the cold chain, nor did theyprovide financial analysis for potential investors.

Winrock International completed two studies on infrastructure development for fresh fruitdistribution in eastern Indonesia. The primary goal of their first project was to make guaranteedsoft loans available to local businesses in the shipping and food transportation industries. These

4

loans were for the acquisition of transportation and refrigeration equipment. Another goal of theresearch project was to provide training programs for the recipients of the loans and theiremployees to educate them on fruit handling technology. This training program was part of theloan approval criteria. Winrock discovered that the major infrastructure needs for fruitdistribution in eastern Indonesia were cold storage warehouses, refrigeration units for boats andtrucks, and packing sheds in or near fruit production areas. The researchers also compared costsof air and sea distribution, and of domestic and international shipping. Results indicate that it isabout six times less expensive to ship apples from the U.S. West Coast to eastern Indonesia thanto ship between two ports within eastern Indonesia. As expected, air freight was much moreexpensive than ocean freight. However, the major limitation in air freight was not the cost, butrather the lack of capacity to handle large tonnage.

Winrock’s second study was done in collaboration with the U.S. Agricultural Trade Office inJakarta, and had three major objectives. They were 1) to identify weaknesses in the cold chaininfrastructure that hinder sales of quality U.S. foods in eastern and northeastern Indonesia, 2) tomake technical and economic recommendations to vendors and transportation companies, and 3)to build a network that will develop into a Cold Chain Association. One finding that deals withfrozen french fries is their acceptance into major supermarkets, but the lack of freezer storageand refrigerated trucks or vans (generally referred to as reefers) hinders their expansion intosecondary cities. The researchers also discovered that reefers are mainly used for the exportationof seafood, and that reefer containers are usually backhauled empty. This procedure addssignificantly to transportation costs. There is also a problem with temperature management dueto lack of monitoring of reefers at the ports and to non-functioning data recorders. To deal withthe problem of pilferage and vandalism, the study made the following recommendations:

• Use smaller vehicles to transport reefers, such as a truck with 20-foot containers.• Hire shippers with the best reputation; avoid shippers with known problems.• Hire forwarding agents that have experience dealing with paperwork and port procedures.

Recommendations were also made to help solve the problem of inadequate cold storage, whichincluded building a warehouse that is locally situated, perhaps shared by several companies thatare interested in food distribution. This warehouse would ideally have four rooms, one of whichto store frozen foods and the remainder for different types of fresh fruits and vegetables.

The Winrock International studies were very technical in nature, suggesting specific mechanicaland chemical techniques to improve the cold chain. Again, detailed financial analysis ofpotential improvements was not done in either of these studies.

Academic Studies

Ashley and Epperson (1989) identified several barriers to exporting commodities, which include1) increased transportation difficulties, 2) lack of current and/or accurate information, 3)differences in international currency exchange rates, 4) language and labeling differences, 5)varying governmental policies and restrictions, and 6) cultural acceptance. The objective of theirstudy was to identify the barriers, opportunities, and factors influencing the internationalmarketing of vegetables. Data were obtained from a survey of companies in the vegetablebusiness from 22 countries, of which Hong Kong and Japan represented Asia.

5

Half of the companies surveyed were in the vegetable business; one-fourth were retailers; andprocessors and distributors were each 12.5 percent of the sample. Key findings are:

• 98.8 percent of all U.S. processed vegetables are transported to Asia via sea vessel,• 71.4 percent of Asian importers always prefer the elimination of tariffs, duties, and

government regulations; and• 66.6 percent of Asian importers perceived an increasing demand for potatoes in their country,

while 33.3 percent perceived constant demand for potatoes.

The authors concluded that Asia has the most potential for growth in the export market forvegetables. Reasons cited include 1) a high percentage of Asian firms predicting an increase inimport levels of vegetables compared with firms in other regions, 2) lack of emphasis on theprice of vegetable imports by Asian importers, 3) expected ability of U.S. agribusinesses to adoptsuggested changes of Asian importers - specifically greater market knowledge and interest andhigher quality standards, 4) apparent inability of exporters to decrease the price of vegetables asdesired by European and Latin American importers, and 5) a greater commitment to internationalmarkets by Asian importers.

Lanclos, Devadoss, and Guenthner (1997) examined the factors that affect the export demand forU.S. frozen potatoes, such as advertising, foreign investments, income, and prices. Fourcategories of importers were studied from 1978 to 1993 based on 1993 import volume: Japan,Mexico, the Philippines, and Thailand. Geweke's Bayesian estimation procedure was used toestimate the per-capita demand equations for the four countries. Prices of substitutes andcomplements, exchange rates, and the percentage of young people in the population wereeliminated due to low significance and little contribution to the explanatory power of the models.

The results show that the Philippine and Thailand markets for frozen potatoes are very priceinelastic (-0.13 and -0.02, respectively). The Philippines has the highest income elasticity (2.50),while Thailand has the lowest (0.04). The effectiveness of U.S. Potato Board advertising has aninverse relationship with the degree of market development of the country. Third partyadvertising is ten times more effective than Potato Board advertising in the Philippines andThailand. Conventional economic factors, such as prices and income, may become moreimportant as the market becomes more established, as was the case in Japan. Advertising andfood service industry investments primarily influence the import demand of smaller, newermarkets.

As the composition of agricultural and food trade shifts from bulk agricultural commodities tomore processed food products, more knowledge is needed about Asian food safety regulations.The objective of Wang and Caswell's (1998) study was to compare the levels of food safetyregulations of three U.S.-Asian trading groups, in which the third group was developingcountries. The developing countries included China, India, Thailand, and the Philippines.

Food safety, as defined by the authors, includes quality attributes such as foodborne pathogens,heavy metals, pesticide residues, food additives, naturally occurring toxins, and veterinaryresidues.

6

In 1995, of all U.S.-Asian food and agricultural trade, 25 percent of U.S. exports were directedtowards the developing countries, while 87 percent of U.S. imports were from developingcountries. Probably due to the high percentage of imports, the authors focused on the food safetyregulations that these countries need to meet to gain greater access to the U.S. market, rather thanwhat the regulations should be for the U.S. to gain greater access to export markets.

Of all the developing countries, Thailand supplied the greatest volume of imports to the U.S. in1995, and had the lowest number of import detentions. This suggests that Thailand has morefood safety regulations than the other developing countries. Developing countries in Asia havebeen criticized for poorly established food safety laws, primarily in the areas of pesticideresidues, packaging and labeling, and government inspection.

Finally, one study by researchers at the University of the Philippines offered important detail ontransportation within the country. Garsuta (1995) completed a study on urban goods movementin Metro Manila in which a survey was conducted of traffic enforcers, truckers, foodmanufacturers and producers, and merchants. This research was limited to food distribution withboth the origin and destination within the Metro Manila area. Survey results indicate thefollowing:

• Trucks represent only 6.2 percent of the total traffic in Metro Manila. The low relativevolume of truck traffic resulted in its exclusion from the urban planning process.

• Almost 60 percent of firms that use trucks for delivery do not follow a scheduling plan.• Over 80 percent of trucks failed to arrive on scheduled time.• 89 percent of trucks are backhauled empty.• 64 percent of trucking firms do not have a terminal or garage facility.

Garsuta also mentioned that traffic congestion is a severe problem near the port areas. This isdue to peaked and irregular demand generated by the arrival of vessels, the truck ban whichresults in delays to trucks which are sent to pick up cargo, and the presence of squatters on thestreets.

The previous research available offered a useful foundation regarding the role of cold chaininfrastructure in trade between the U.S. and Asia. To build on the prior efforts, this studyfocused on economic conditions and financial feasibility of specific cold chain improvements. Inorder to form conclusions about the feasibility of projects, it was necessary to consider thegeographic and business environments and the cold chain logistics of the target countries. Thisprovided an insight into the overall economic conditions and institutional constraints, which wasimportant in achieving the objectives of the project. The following section includes a review ofthe physical and business environments for the Philippines, followed by a parallel presentationabout Thailand.

7

The Philippines

The Philippines has seen many economic and political changes in the 1980s and 1990s. Afterthe Marcos regime was overthrown in 1986, a vigorous economic reform program was adopted.This included privatization of many government enterprises, tariff reductions, liberalized foreignexchange and investment policies, and infrastructure modernization.

The following section outlines the geographic information that is important in assessing thefeasibility of commercial projects. Following the review of physical conditions andinfrastructure, economic indicators are presented.

Geographic Environment

The Philippines is an archipelago country in Southeast Asia, located between the Philippine Seaand the South China Sea (Figure 1). Total land area includes 298,170 km, with 334,539 km ofcoastline (CIA). It extends 1,850 km north to south, and 1,100 km east to west (De Villa). In1998, there were 199,950 km of roads, of which 39,590 km were paved (CIA). The number andlength of existing bridges in the Philippines is listed in Table 1. Although the number of bridgeshas remained stable, the length of the bridges increased by more than eight percent from 1990 to1996. The terrain is mostly mountainous with narrow to extensive coastal lowlands, which isprone to volcanoes and earthquakes. The climate is tropical marine, with typhoons and flashfloods common during the rainy season (May-November).

The official language of the country is Filipino (based on Tagalog), but English is widely used incommercial and legal transactions. The Philippines is the world's third-largest English-speakingcountry in terms of population, after the United States and the United Kingdom. There are alsoover 100 regional dialects.

Major Cities

The 880 inhabited islands of the Philippines are divided into three main regions: Luzon, Visayas,and Mindanao. Luzon is the largest and northernmost island, Visayas is comprised of the centralislands, and Mindanao is the southernmost island. The capital city of Manila and surroundingcities comprise Metro Manila, the most populous area in Luzon as well as the entire country.Other major cities include Cebu City and Bacolod City in Visayas, and Davao City and Cagayande Oro in Mindanao. The distance between the major cities in the Philippines can be seen inTable 2. Population data for each city was not available.

Cebu City is the country's oldest city, having been named the capital by the Spaniards in 1565.Today it is a bustling trade port. Bacolod City is the capital of the Negros Occidental province,and lies in the northwestern part of the province. Twenty-five percent of the province'spopulation lives in Bacolod City. The province's major crop grown is sugarcane. One of theworld's largest cities in terms of land area is Davao City, comprising 244,000 hectares. It isconsidered Mindanao's center for education and commerce, and accounts for the majority ofsouthern Mindanao's exports and imports. Davao exports various agricultural goods such asbananas and crude and refined coconut oil, as well as furniture and processed foods. Cagayan deOro is also becoming an educational and commerce center as the capital of the Misamis Oriental

8

province. This city has many large manufacturing companies which process goods for both localand export markets.

Ports

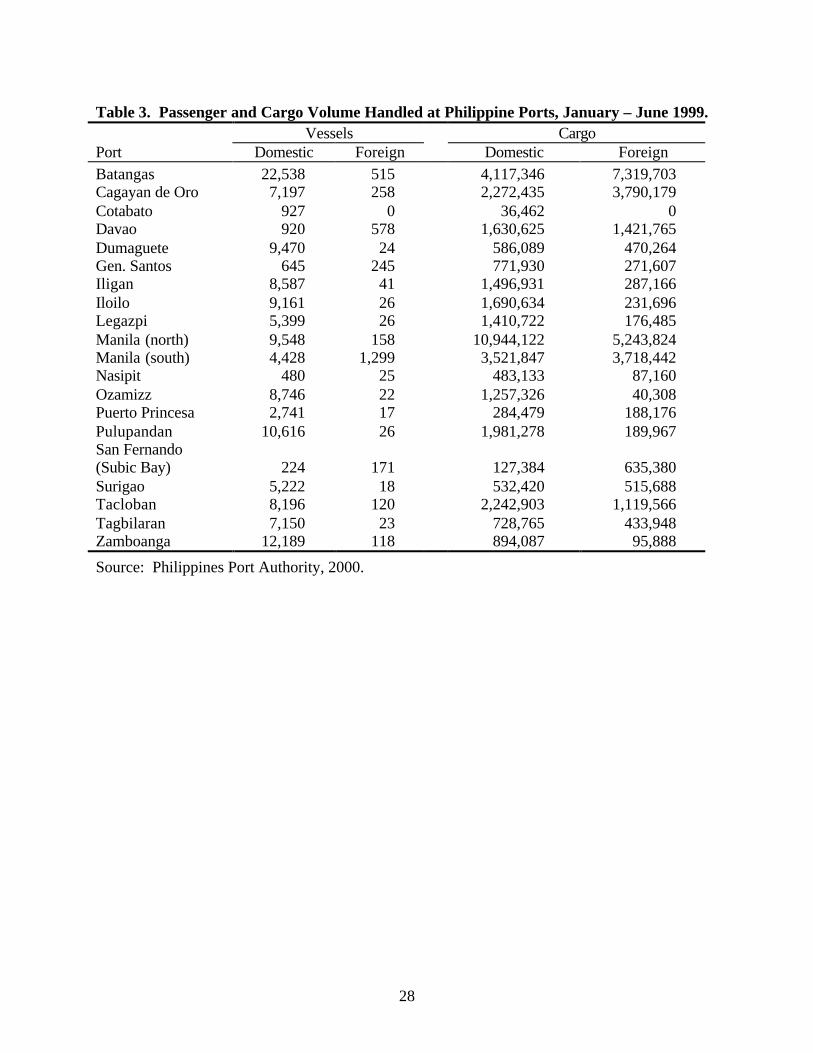

The main international seaports are located in Manila, Subic, and Cebu City. The ports handlealmost 98 percent of materials and products imported and exported by the Philippines (PhilippinePort Authority). Shipping statistics for the ports operated by the Philippine Port Authority arelocated in Table 3. International Container Terminal Services Incorporated (ICTSI) manages thecontainer terminal yard at the Manila international port. The ICTSI is responsible for loadingand unloading containers from vessels, as well as temporarily storing containers. They handle alittle less than 60 to 70 percent of all imports that come into the Philippines. The ManilaInternational Container Terminal (MICT) was once government operated, but was privatizedwith the signing of a 25-year BOT (Build-Operate-Transfer) contract with ICTSI. According toofficials at ICTSI, the terminal capacity is 1.5 million TEU's (twenty-foot equivalent units); in1999 the volume handled exceeded 800,000+ TEU's. ICTSI prefers to operate at 60 percentcapacity because they can be more efficient at this level. If the containers are stacked, morecontainers must be handled to move the bottom container. The capacity for reefer containers is730 slots, including 100 temporary slots that were recently added. ICTSI monitors thetemperature requirements. The average dwell time is five days for dry goods and 2.5 days forchilled or frozen goods. All customers are charged handling fees, and customers who own reefercontainers are charged for electricity (minimum six hour charge). There is an additional chargewhen containers are stored at the terminal for more than five days. The Philippine PortAuthority regulates the rates.

Ports in outlying provinces are variable in capacity and quality. The port in Cebu is comparableto that in Manila, based on visits by the research team, although it is smaller. Oriental Port &Allied Services Corporation (OPASCOR) is a private firm that manages the international port inCebu. They have had a contract with the Cebu International Port (CIP), a government agency, tooperate the port since 1990. In 2001 they will renegotiate the contract for 15 to 20 years. Theport that OPASCOR manages handles foreign vessels only; the domestic carriers load andunload vessels at the domestic port next door to the international port. Sixty percent of thecontainers handled at CIP are 20-footers, according to the officials interviewed, while fortypercent are 40-footers. The CIP has the capacity to berth two foreign vessels at one time.Inbound containers can remain in the yard for six days with no charge, and outbound containersare allowed two days without charge. Reefer containers are typically only at the port for oneday, according to OPASCOR representatives. There are 25 reefer outlets at this port, which isjust enough to handle the amount of reefer container volume that they currently have. The CebuPort Authority (CPA) can add more reefer outlets if OPASCOR requests it; the port has landcapacity for 100-150 more outlets. The international port has two forty-year old gantry cranesand 10 transtainers, but does not have roll-on/roll-off capabilities.

Bacolod port includes a public section operated by the Philippine Port Authority (PPA) and aprivate section operated by Negros Navigation Company, Inc. The facilities are not capable ofhandling 40-foot containers, and no reefer plugs were visible in the container yard visited byresearchers.

9

The port at Cagayan de Oro is managed by the PPA. According to information gathered fromtheir website, this is an advanced, modern port. The total area is 191,400 square meters, withopen storage areas in Phase 1 of 15,232 square meters, and Phase 2 of 31,460 square meters. Ithandles foreign and domestic containerized cargo and has approximately 36 reefer outlets, aswell as roll-on/ roll-off capabilities.

Business Environment

Another important factor in considering the feasibility of a commercial project is the businessenvironment of the target country. The following section establishes a picture of thisenvironment through discussions of the income distribution, urbanization and westernization,and the macroeconomic and banking situations of the Philippines.

Income Distribution

Population projections for the Philippines by region for the years 2000 and 2005 are listed inTable 4, as well as the average income by region for 1997. Thirty-seven percent of thepopulation ranges from 0-14 years, while fifty-nine percent range from 15-64 years. This issignificant because it is the younger generation that typically frequents quick service restaurants(QSRs) where many frozen potatoes reach the final consumer. However, a 1997 estimate statesthat 32 percent of the population lives in poverty (CIA). The total number of families by incomeclass is listed in Table 5. In 1997, 45.6 percent of Filipinos derived their income source fromwages and salaries, 26.2 percent from entrepreneurial activities, and 28.2 percent from othersources, such as net share of crops, receipts from abroad, and family sustenance activities(Philippines National Statistics Office).

Urbanization/Westernization

The Philippines is one of the most westernized countries in Southeast Asia, due to the fact that itwas under U.S. political administration from 1898 to 1946. During this time period, the U.S.introduced their system of education, style of government, and commercial products (De Villa).Many U.S. companies, particularly QSRs, have subsidiaries in the Philippines, includingMcDonalds, Pizza Hut, KFC, Shakey's, Dunkin' Donuts, Subway, Dairy Queen, TGI Fridays,etc. There are currently 228 McDonalds outlets in the Philippines, of which 161 are in the majorcities. By the end of 2000 there will be 240 total McDonalds outlets (Cochico). There are 23outlets in the Visayas and Mindanao regions, with the remainder in Luzon (Table 6).

"Malling" is a popular pastime, in which Filipinos spend hours at a mall shopping, walking,watching movies, playing games, and eating. Refreshment stands, kiosks, and counters arecommonly found in shopping malls, with many serving processed potato products such asflavored french fries, potato rosettes, and hash browns. The number of restaurants, fast foodcenters, refreshment stands, and kiosks increased between five to six percent from 1996 to 1997(Table 7).

Despite the high degree of urbanization and westernization, there is still less than completeconsumer acceptance of frozen foods. A common thought is that only leftover foods are frozen.For example, many Filipinos refer to frozen seafood as "double dead." Shopping at open-air wet

10

markets is common, where consumers purchase what they consider "fresh" meats and seafood,some of which may have been un-refrigerated all day. This mentality carries over to thesupermarkets, where many consumers are reluctant to purchase frozen vegetables for homeconsumption. Adding to this problem is the lack of refrigerators in many rural homes.

The changes in income and urbanization present potential market opportunities for businessesinvolved in frozen foods. At the same time, the growth in urban sectors presents challenges indistribution. Due to the rapid pace of urbanization in Metro Manila, there has been a significantincrease in traffic volume in recent years and there is severe traffic congestion in many parts ofthe metropolitan area. Garsuta (1995) also attributes the heavy traffic congestion to theunplanned industrial developments, the undisciplined behavior of both drivers and pedestrians,and the way in which truck movements have been allowed to grow in the past. In addition, theseventeen local government units (LGUs) of Metro Manila all have their own traffic regulationsand enforcement agencies. Failure to coordinate among the various LGUs compounds theproblem of traffic congestion (Garsuta). On a country-wide basis, there was a 10 percentincrease in the number of motor vehicles registered and a nine percent increase in the number ofdrivers licenses issued in only one year, 1996 to 1997 (Road Handbook in the Philippines ‘98).While secondary cities are smaller than Manila, visits by the research team to Cebu indicate thattraffic congestion may be a growing problem.

Macroeconomic Conditions

The economy of the Philippines has improved over the past ten years, with only a few setbacks(Table 8). Of the six principal macroeconomic indicators (nominal and real Gross DomesticProduct, average lending rate of banks, inflation rate, exchange rate, and unemployment rate),only the exchange rate and unemployment rate situation worsened. This was primarily due to theAsian financial crisis in 1997, which began when the Thai government floated its currency. Thevalue of the Thai Baht fell by 15 percent on July 2, 1997, and the Philippine Peso declinedshortly thereafter (Coyle, McKibbin, Wang, and Lopez). Although the Asian financial crisisseverely affected the economy of the Philippines, the effect was less severe than in otherSoutheast Asian countries (U.S.-ASEAN Business Council, Inc.(b), 2000).

On the demand side, nominal GDP increased every year over the past ten years, showing a 178percent improvement from 1990 to 1999. Furthermore, GDP is expected to increase in 2000 and2001 by eight to twelve percent each year. It is predicted that services will be the fastestgrowing segment in 2000. Real GDP, which is adjusted for inflation, has also improved over thepast ten years, showing decreases in only two years, 1991 and 1998. The unemployment ratehovered between eight and ten percent during the 1990s. It was showing an improvement whenthe financial crisis hit, causing unemployment to rise again to the ten percent level. It appears asif unemployment is now decreasing to the level that it was at in the mid-1990's.

More signs of the recent recession are visible in the credit and money indicators. The averagelending rate of banks has decreased by 14 percent since 1990, with the largest decrease in 1999.In 1994, 1997, and 1998, the lending rate increased marginally, but the large decreases over theten-year time period more than offset this. The inflation rate also decreased significantly, fromdouble-digit numbers in the early 1990s to a low of 3.5 percent for the beginning of 2000. Smallincreases in the inflation rate were realized in 1994 and 1996, with a larger increase in 1998

11

during the Asian financial crisis. Inflation in the food sector decreased from 7.8 percent in thesame quarter/month last year to 0.20 percent this year, and in Metro Manila inflation decreasedfrom 6.7 percent to 2.8 percent. The Philippines National Economic and Development Authoritypredicts that the inflation rate will remain between five and six percent for the years 2000 and2001. As previously stated, the foreign exchange rate is the only macroeconomic indicator thathas not shown an improvement. Until 1997, the foreign exchange rate fluctuated in the mid- toupper- twenties. However, there was a dramatic decrease in the value of the peso in 1998, to40.89 pesos/U.S. Dollar. The exchange rate has been in this range ever since.

According to the Philippines National Economic and Development Authority (2000), 1999 was arecovery year for the Philippines. The general outlook for 2000 is one of stronger growth, lowerinflation, fiscal consolidation, and an acceleration of the reform process.

Capital Markets in the Philippines

The macroeconomic data presented in the previous section suggest solid economic fundamentalsand modest growth for the Philippines. In spite of the signs of economic strength, there is a needto continue to improve the financial system to ensure recovery from the effects of the Asiancrisis (Buenaventura).

Banks have undergone some shaky times and face challenges in the current depressed businessenvironment. Measures of banks’ performance suggest several positives (Table 9), althoughthere is continued concern about the shrinking of bank lending. The overhang of non-performingdebt continues to constrain banks’ ability and willingness to lend. Table 10 is the balance sheetand income statement for a major Philippine bank, and it shows the constraints on banks due tothe need for provisioning (loan loss reserves).

Bank officials interviewed for this research indicated that lending terms were relatively strict inorder to prevent future problems with repayment. One leading bank required that net incomeafter debt service be at least 30 percent of sales revenues before lending based on cash flows.Collateral was also required, with loan amounts restricted to no more than 60 percent ofcollateral asset value. Interest terms offered were for annually adjustable rates, with 13.75percent reported as a typical rate available to commercial borrowers in May 2000. These termswere similar to those reported by a competing large bank.

Major commercial banks typically do not lend to very small businesses, except occasionally onthe basis of a personal loan secured with a home or other personal property. The number ofbanks by business type is shown in Table 11. The Development Bank of the Philippines wasconsidered a potential source of credit for start-up concerns that cannot obtain loans fromcommercial banks.

While the evidence suggests that banks have tightened up lending policies, it is not entirely clearif Philippine businesses face serious credit constraints. Some sources indicate that debt capitalis an important source of funds for small and medium sized businesses in the Philippines.Reported typical leverage ratios exceeded 2:1, sometimes as high as 5:1. These high leverageratios could be the result of past generous credit terms or they could indicate falling assetvaluations.

12

While interest rates have fallen below those in the market at the peak of the Asian crisis, (Table8), the real cost of funds has remained relatively high as inflation has fallen. Policies of theBangko Sentral ng Pilipinas (BSP, the Philippine Central Bank) in response to broader pressureshave contributed to the high cost of funds. The Philippine currency is extremely sensitive tochanges in U.S. interest rates, so during the tightening of U.S. monetary policy in spring 2000,the BSP increased its overnight rates repeatedly to prevent the peso from depreciating furtheragainst the U.S. Dollar. The overnight rate was 10 percent for borrowing and 12.25 percent forlending in mid-May 2000. Higher rates are an effort to keep funds in pesos rather than in foreignexchange. The military conflict in Mindanao has also contributed to capital flight and leads torelatively high interest rates in the Philippines.

Equity capital is a potential source of liquidity and investment funds, and reportedly equity hasgrown to partly compensate for the weakness in bank credit in Asian countries (Sender). Thekey role of equity funds was underscored in personal interviews with several firms in the coldchain businesses in the Philippines. National equity markets are a potential resource, but thePhilippine stock market has reportedly been stagnant (Booth and Hilsenrath). Few of the firmsinterviewed for this research were publicly traded corporations. Thus the primary source ofequity capital for small and medium enterprises wishing to expand in businesses related to thecold chain appears to be personal or family savings, or through affiliations with closely heldenterprises. Interlocking relationships among major businesses are a common characteristic inthe Philippine business community. Often important families control the linked businesses.While it is important to consider the potential for equity from these important conglomerates,there is no published information available on this topic.

Bank Regulation and Reforms

Philippine President Joseph Estrada signed a new law widening the supervisory powers of theBSP, to take effect in June 2000 (Philippine Star). The Revised General Banking Act (RA 8791)also opens the banking sector to more foreign investment. A foreign bank may now own theentire voting stock of an existing local bank, whether distressed or healthy.

This reform program was prompted by several bank failures and related runs on banks bynervous depositors. The Philippines has a deposit insurance system, but the coverage limit of100,000 pesos was insufficient for many of the failed banks’ customers, according to pressreports.

The BSP requires a capital adequacy ratio of 10 percent, which is higher than the eight percentstandard recommended by the Bank for International Settlements. There is a restriction oncommercial bank loans to the property sector of no more than 20 percent of the portfolio, inorder to limit the exposure to volatile real estate loans.

Financial Assistance Programs

The review of financial markets in the Philippines indicates some recovery, but lingeringproblems from the severe economic downturn of 1997. In addition to in-country sources offinancing, investors in cold chain infrastructure may consider U.S. export assistance programs

13

that cover equipment related to handling exports. This section introduces the Export-ImportBank and USDA programs that may be relevant to cold chain investments.

The Export-Import Bank of the U.S. in the Philippines.

The Export-Import Bank of the U.S. (EX-IM Bank) is an independent U.S. Government agencythat helps finance the overseas sales of U.S. goods and services. It provides guarantees ofworking capital loans for U.S. exporters, guarantees the repayment of loans or makes loans toforeign purchasers of U.S. goods and services. EX-IM Bank also provides credit insurance thatprotects U.S. exporters against the risks of non-payment by foreign buyers for political orcommercial reasons.

Two different programs, according to an interview with an EX-IM officer in Houston (Crilley),are applicable to exporters from the U.S. and importers from overseas:

1) Short-term credit: EX-IM bank will guarantee the receivables, from oversea importers, viaexporters’ banks in the U.S., therefore the default risk is transferred to EX-IM bank. Whenexporters obtain the receivables from importers, the exporters will use them as collateral for aline of credit from banks in the U.S. However, EX-IM bank must credit the receivables fromimporters. This service has reportedly been used for frozen french fry exports.

2) Medium-term credit: This service is applied for refrigeration equipment and vehicles. Thepayment terms are up to five years. The amount of loan has no restriction in “improving theexisting cold storage chain”, or “building a new facility”, but the equipment must be made orassembled in the U.S. The seller of the equipment will receive a promissory note from theoverseas importer. EX-IM bank will guarantee up to 85 percent of the CIF value.1 Once theseller of the equipment presents the promissory note to banks in the U.S., the EX-IM bank willtake over the responsibility for default risk due to non-payment by the overseas importer.

U.S. Department of Agriculture Facility Guarantee Program in the Philippines

The Commodity Credit Corporation's (CCC) Facility Guarantee Program (FGP) providespayment guarantees to facilitate the financing of manufactured goods and services exported fromthe U.S. to improve or establish agricultural related facilities in emerging markets. By supportingsuch facilities, the FGP is designed to enhance sales of U.S. agricultural commodities andproducts to emerging markets where the demand for such commodities and products may beconstrained due to inadequate storage, processing, or handling capabilities (United StatesDepartment of Agriculture).

Although other government and multi-national programs finance export sales of manufacturedgoods and services, the FGP is aimed initially at financing moderate sized agricultural projects—including small businesses that may be overlooked by other export credit programs thatpredominately support projects unrelated to agriculture.

1 CIF is cargo value inclusive of charges, insurance and freight.

14

During interviews with business officers in various companies in the Philippines and Thailand,most of the business officers were aware of the FGP, but none of them used or plan to use FGPto finance their projects related to manufactured goods and services exported from the U.S.Most of officers do not know the application process. A couple of officers mentioned that theprocess is too complicated or involves extensive paper work.

The preceding review of the geography and economy of the Philippines illustrated the potentialmarket for frozen foods and the broad financial constraints to improving the cold chaininfrastructure. The next section shifts to the specific comments of the business personnelinterviewed in the Philippines. Based mainly on those discussions, specific improvements willbe proposed.

Issues Identified in Interviews

A team of four researchers traveled to the Philippines from May 18, 2000 to June 10, 2000.Approximately half of the time was spent in Metro Manila, while the remaining time was spentin Bacolod City and Cebu City. A trip to Davao City was planned but cancelled upon arrival inManila as a safety precaution due to the political unrest in southern Mindanao. Forty interviewswere conducted to determine the bottlenecks to distributing frozen foods in the Philippines.Persons interviewed consisted of four government officials, and responsible officials at threebanks, nine cold storage warehouses, ten shippers, brokers, and port management officials, threeimporters, four retailers and QSRs, and seven others involved in food distribution.

The main issues identified related to the cold storage facilities and inter-island shippingindustries.

Shortage of Cold Storage Capacity in Outlying Provinces

Two factors are creating a greater demand for cold storage warehouses in the Philippines -Filipinos are becoming more quality conscious and westernized as incomes slowly rise. This isevidenced by the near-full capacity level of most warehouses, particularly during the peak seasonof November and December. In Manila, capacity levels range from 66 percent to 99 percentduring the off-peak season.

In Bacolod, there is only one public cold storage warehouse that was built for the purpose ofleasing space, and this is at full capacity. Other warehouses in Bacolod were built for the privateuse of seafood processing companies, but are now being leased because of the decline in thedemand for seafood storage. These warehouses are not at full capacity due to quality issues. InCebu, there are three public cold storage warehouses, but only one that can reach a temperaturelevel that is adequate for frozen french fries.

If extra capacity is needed at a warehouse, the manager may opt to rent a reefer container totemporarily store product. The cost for this is 2,000 pesos per day, which includes rental andelectricity costs. The reefer container can usually be delivered within one day of the order.Customers will also use ice chests to temporarily store frozen or chilled products when all of thepublic cold storage warehouses are full. Many food processors discussed plans to build privatecold storage warehouses to overcome the shortage in the south.

15

The QSR chains have strict quality guidelines, which many of the cold storage warehousesoutside of Manila cannot meet. Poor quality at a warehouse was defined as the following:variable or high temperatures, dial temperature gauges rather than digital, no racks and perhapsno pallets, lack of ante-rooms, insulation, and loading docks, and no mechanization. As oneQSR representative stated, "The cold storage facilities in the provinces cater to the seafoodindustry, rather than the QSRs." One of the QSR chains requires all of its retail stores in theprovinces to have a large enough freezer to accommodate a 20-foot container so that they do nothave to rent space in cold storage facilities.

Most of the cold storage warehouses in the Philippines require their customers to rent an entireroom and require yearly contracts. Some are starting to partition rooms to accommodatecustomers with smaller volume, although the customers must agree on the room temperature asdifferent products have different temperature requirements. Rates in Manila range from 8.10pesos per cubic meter per day (not inclusive of pallet rental, handling charges, etc.) to 60 pesosper pallet per day (inclusive of inventory maintenance, loading/unloading, etc.). It is common inthe provinces to charge by the room, for instance 120,000 pesos per room per month is theamount that one facility in Bacolod charges. However, one representative in Cebu mentionedthat it is not effective to charge by the room because the customer may overstock the freezer,which can cause maintenance problems. This particular representative charges five centavos perkilo per day plus electricity by the hour when a customer plugs in a reefer container.

High electricity costs were consistently rated as the number one problem that the cold storagefacilities face. The representatives attribute the high rates to the government owned and operatedenergy companies. Energy costs comprise between 30 and 50 percent of total costs at coldstorage facilities in Manila and Bacolod. One representative in Cebu stated that energy costscomprise between 80 and 90 percent of the budget. Electricity rates in secondary cities are 5 to25 percent higher than in Manila, depending on which city is chosen for the project. Cebu hasthe highest energy costs in the country; they have risen from 3.0 to 4.7 pesos per kilowatt hourover the past few years. Another problem in Cebu is erratic electricity voltage, ranging from190-250 volts. This causes compressors to wear out quickly.

To maintain efficient use of energy, the cold storage owners and operators should limit thenumber of freezer door openings as well as perform preventative maintenance on equipment andinsulation.

Another major cost for cold storage warehouses is labor. Labor costs comprise 30 percent of onecold storage warehouse's variable costs. Labor costs are higher in Manila than in the provinces.Labor unions are strong in the Philippines, so one warehouse in Bacolod hires the majority of itsemployees through temp agencies. Labor laws in the Philippines dictate that employees whohave worked for more than six months must be treated as full-time regular employees. To avoidthis labor law, the cold storage facility often hires someone for less than six months.

High Cost of Inter-Island Shipping

There are three major inter-island shipping companies in the Philippines - Negros NavigationCompany, Inc., Sulpicio Lines, Inc., and WG&A. WG&A is the result of a recent merger

16

between three inter-island shipping companies. Although this industry was deregulated a fewyears ago, sources state that the government still allows shippers to confer like a cartel and theshipping lines all charge the same rate.

All three shipping lines transport both passengers and cargo, with cargo representing between 33and 50 percent of their revenues. Of the cargo that is handled, only a small portion isrefrigerated or frozen. The shipping lines offer either pier-to-pier or door-to-door services fortheir customers. They also offer other services, such as providing the reefer containers andloading and unloading of product into the containers. Their customers are primarily brokers whohandle all of the details and negotiations for the food processors or QSRs. One broker allows itsclients to have the container for 48 hours to load or unload without charge; the client is chargedbetween 1,000 and 2,000 pesos per day after this time. The client is also charged between 300and 400 pesos per day for use of the chassis.

High inter-island freight rates were viewed as the largest problem to distributing frozen foods inthe Philippines. See Table 12 for a summary of rates from Manila to the secondary cities.Companies cited many examples to show that it costs more to ship from Manila to another portin the Philippines than to ship from Manila to another port in Asia. It is also less expensive foran importer to ship directly to Cebu or Davao from the U.S. West Coast than it is to transshipthrough Manila. Inter-island freight rates increased by more than 30 percent between December1999 and May 2000. Several reasons were given for the high freight rates. The shipping linesaccredit some of this increase to increasing fuel prices. The government allows them to pass thison to their customers if the increase is greater than 10 percent. Effective August 2, 2000, therates listed in Table 12 will increase by six to seven percent as a result of the latest increase infuel. One representative attributes the high freight rates to pilferage from the containers either onthe ship or at the port. Clients can file claims against the shipping line for missing products, butthe cost is ultimately passed to the customer. Another representative stated that governmentpolicies protect the industry and allow the high rates. Many of those interviewed stated thatmore shipping lines should enter the market to make the industry more competitive. It was alsosuggested that the government allow foreign carriers to ship goods from Manila to secondaryports in the Philippines.

Inadequate reefer outlet plugs on vessels is also seen as a problem to distributing frozen food inthe Philippines, although the shipping lines feel that more outlets are not needed. Onerepresentative in the reefer container industry stated that the shipping lines do not realize a profitwhen transporting reefer containers, therefore it is not a high priority to increase the number ofoutlets. In addition to inadequate number of outlets, there are concerns about the voltageconstraints on some vessels. One carrier's vessels have a voltage range of only 220 to 240 volts,but a 40-foot reefer container requires 440 volts. To overcome this problem, some 40-footcontainers have dual voltage systems that allow one container to be plugged into two 220-voltoutlets.

One of the major industry players explains that the access to ship space and reefer containers isnot a problem. The costs of shipping are high, but they reflect the pressure on prices fromalternative business opportunities in passenger traffic.

17

While 40-foot containers are primarily used in international shipping, 20-foot containers areprimarily used in inter-island shipping of chilled or frozen foods. Reasons for this include lackof market demand for 40-foot volume, inadequate facilities at secondary ports to load and unload40-foot containers, voltage constraints (as discussed above) and narrow roads, which do notaccommodate 40-foot container truck transport. Some french fry importers in Manila do notbreak up the loads of 40-foot containers; therefore their customers must order in 40-footquantities. When a city does not have the demand for this amount of volume or if it cannotaccommodate a 40-foot container, the importer will not service the area.

The inadequate number of 20-foot reefer containers was cited as a major problem to distributingfrozen foods within the country, although some representatives explained that it is theavailability and positioning of the reefer containers that presents the real problem. Moreproducts are shipped from Manila than to Manila; therefore empty reefer containers stay in thesecondary cities waiting to be filled and then shipped. Otherwise they must be shipped backempty. One broker stated that only 20 percent of reefer containers are backhauled from Bacolodto Manila with product inside. Another example is that an average of 60 reefer containers areshipped from Manila to Cebu per month, while only 40 reefer containers are shipped from Cebuto Manila per month. One broker has plans to purchase additional reefer containers to deal withthis problem, at a cost of 500,000 pesos per container (brand new). Reefer containers have anaverage useful life of 20 years depending on the maintenance. One broker who has a 50 percentmarket share in reefer container usage owns approximately 200 reefer containers, of which 70percent are new and 40 percent have a digital temperature recording system.

Alternatives to Shipping Via Sea Carrier

The problems of high freight rates and inadequate reefer outlets associated with sea carriers hasprompted some in the Philippines to utilize alternate distribution systems. Although thePhilippines consists of a group of islands, it is physically possible to truck goods from thenorthernmost island to the southernmost island with the aid of only two ferries. The total triptime from Manila to Davao City is 37 hours, by road. The costs for the two methods ofdistribution are similar, at 34,685 pesos for shipping via sea vs. 48,000 pesos for shipping viatruck. There are two problems, however, with shipping frozen foods for such a long distance viatruck. The first is that the frequency of the ferry crossings is not reliable, and the second is thatthe long drive is too stressful on the driver.

Instead of trucking frozen foods from Manila to Mindanao, some are using trucks for shorterdistances, for instance from Cebu to Bacolod. One source stated that the length of time is thesame, and it is less expensive. Another source, a food manufacturer in Bacolod City, plans tobegin trucking shipments to the capital of Negros Oriental, a four-hour drive with good roadconditions. A food distributor in Cebu City delivers thirty percent of orders via truck tosurrounding cities. The stores that obtain products via truck receive a lower volume more often,but the product is fresher. Each of their stores have a freezer capacity for one week of product.Since the store manager pays for the shipping costs, they are responsible for making thedecisions regarding delivery times and quantities. Still others will place an entire refrigeratedtruck on a vessel to travel from Cebu to Mindanao so that it can be driven around Mindanaoupon arrival.

18

Delivery trucks have an average useful life of between five and fifteen years, depending on themaintenance and the damage they receive from poor road conditions. The refrigerationequipment attached to the truck usually lasts longer than the actual truck. A new refrigeratedtruck costs two million pesos. To overcome this large expense, many purchase used or surplustrucks from Japan for between 300,000 and 400,000 pesos. One company is assembling theirown trucks, saving 30 to 40 percent by using second-hand cabs, chassis and compressors. Asavings of 20 percent would be realized if new cabs and chassis were used.