Embed Size (px)

Citation preview

Infrastructure investment and bioincubation-the UK model

GENESIS Plenary presentation, December 1st, 2011

www.stevenagecatalyst.com

Presentation Outline

• The UK scene - issues and challenges

• The UK Bioincubator Forum

• The pharma/incubation landscape

• Stevenage Bioscience Catalyst

Rejuvenation of the UK biotech sector

• The UK biotech sector is underweight and underinvested – Despite the rich academic and pharmaceutical environment here – Research ecosystem needs to be restructured so biotech can thrive

• The pharmaceutical sector faces its own challenges – Patent cliffs, increased regulatory burden, lack of innovation – Increased focus on sources of external innovation – Pfizer 25%, Sanofi-Aventis 55%

• The UK Government is very supportive of the science agenda – Protected £4.6bn science budget, – Strong charities prepared to invest and drive research – CRUK, the Wellcome Trust, MRC – the Crick Institute

• Open innovation at SBC – To enable smaller companies to access big pharma expertise – Strong focus on networking

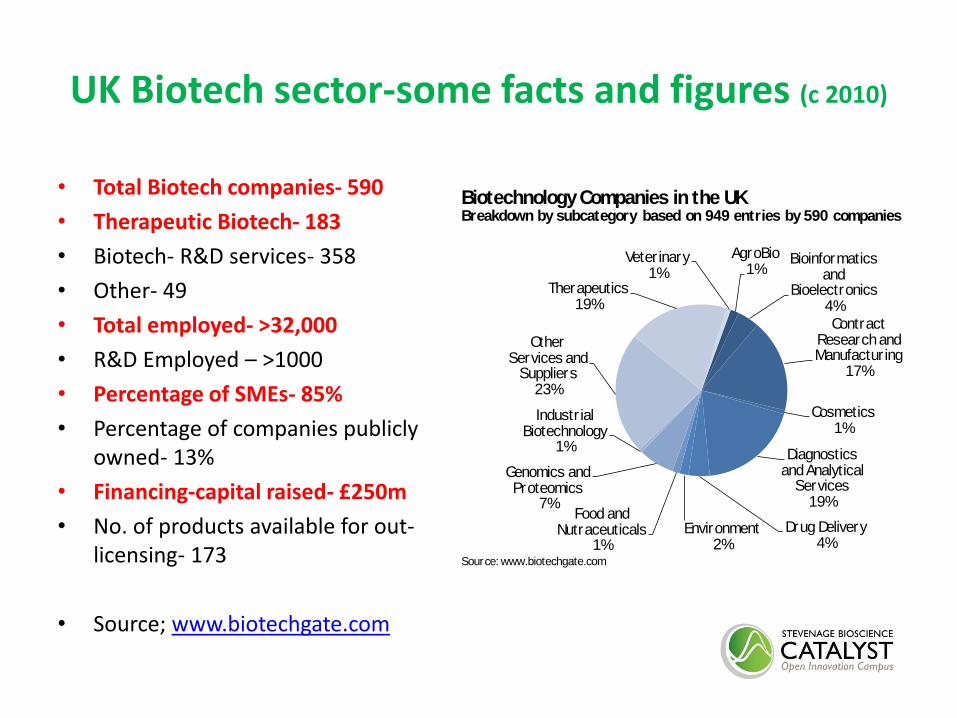

UK Biotech sector-some facts and figures (c 2010)

• Total Biotech companies- 590

• Therapeutic Biotech- 183

• Biotech- R&D services- 358

• Other- 49

• Total employed- >32,000

• R&D Employed – >1000

• Percentage of SMEs- 85%

• Percentage of companies publicly owned- 13%

• Financing-capital raised- £250m

• No. of products available for out-licensing- 173

• Source; www.biotechgate.com

AgroBio 1%

Bioinformatics and

Bioelectronics 4%Contract

Research and Manufactur ing

17%

Cosmetics 1%

Diagnostics and Analytical

Services 19%

Drug Delivery 4%

Environment 2%

Food and Nutraceuticals

1%

Genomics and Proteomics

7%

Industr ial Biotechnology

1%

Other Services and

Suppliers 23%

Therapeutics 19%

Veterinary 1%

Source: www.biotechgate.com

Biotechnology Companies in the UKBreakdown by subcategory based on 949 entries by 590 companies

NESTA Research: the potential to improve cross-sector

collaboration in the UK biomedical industry

• Collaboration can be impactful as well as productive

• Biomedical papers with industry & academic authors have greater citation impact than purely academic papers

• There is potential to improve the way the UK system works together

• Companies, charities, the NHS and universities are all vital parts of the system

• Collaboration is needed for all life sciences

• for research, for access to patients, for delivery

• Collaboration & partnership is increasingly important for pharmaceutical and biotech companies

GSK now does 50% of drug discovery externally

•Hub and satellite bioincubators

•Creating an interacting web of support to promote early stage bioventures

http://www.ukbioincubation.com/

New Activities – Incubator Pharma Parks

• Pfizer Discovery Park (Sandwich)

• Charnwood- MRCT/China Development

• Stevenage Bioscience Catalyst

An opportunity for engagement, interaction and collaboration across the UK

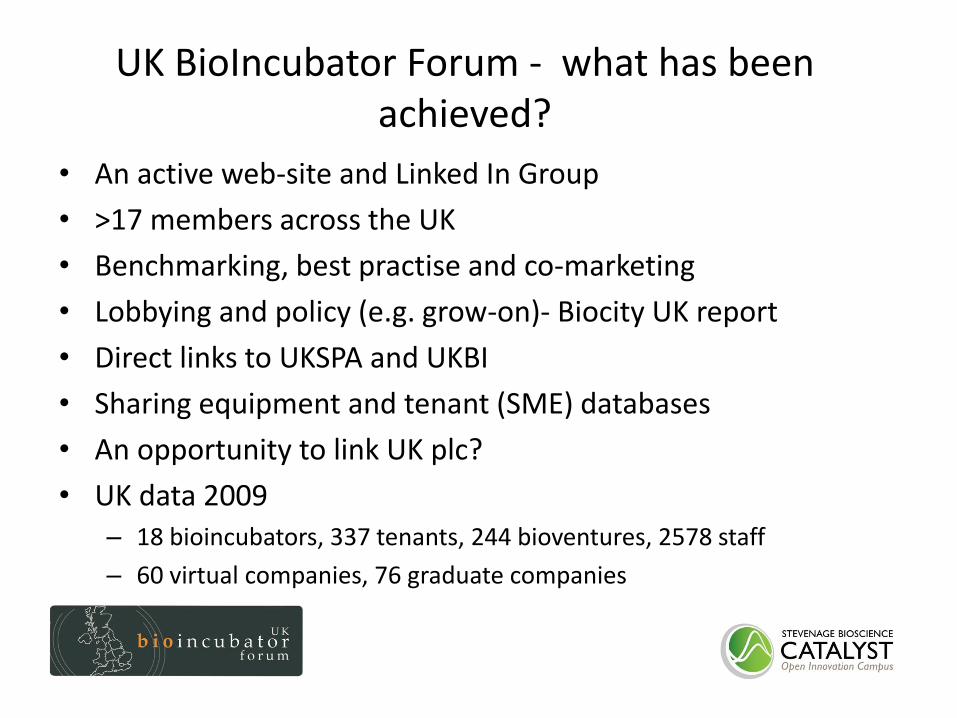

UK BioIncubator Forum - what has been achieved?

• An active web-site and Linked In Group

• >17 members across the UK

• Benchmarking, best practise and co-marketing

• Lobbying and policy (e.g. grow-on)- Biocity UK report

• Direct links to UKSPA and UKBI

• Sharing equipment and tenant (SME) databases

• An opportunity to link UK plc?

• UK data 2009 – 18 bioincubators, 337 tenants, 244 bioventures, 2578 staff

– 60 virtual companies, 76 graduate companies

Moving forwards

• Greater coordination of activities (UK plc)

• “Open” collaboration and partnerships across the UK

• Development of a UK “super cluster” to compare with global centres (Boston, Singapore etc.)

• A real focus on “Biotech”- new therapies, new drugs

• Making connections between

– Academia

– Biotech

– Pharma

– Help to improve the connections

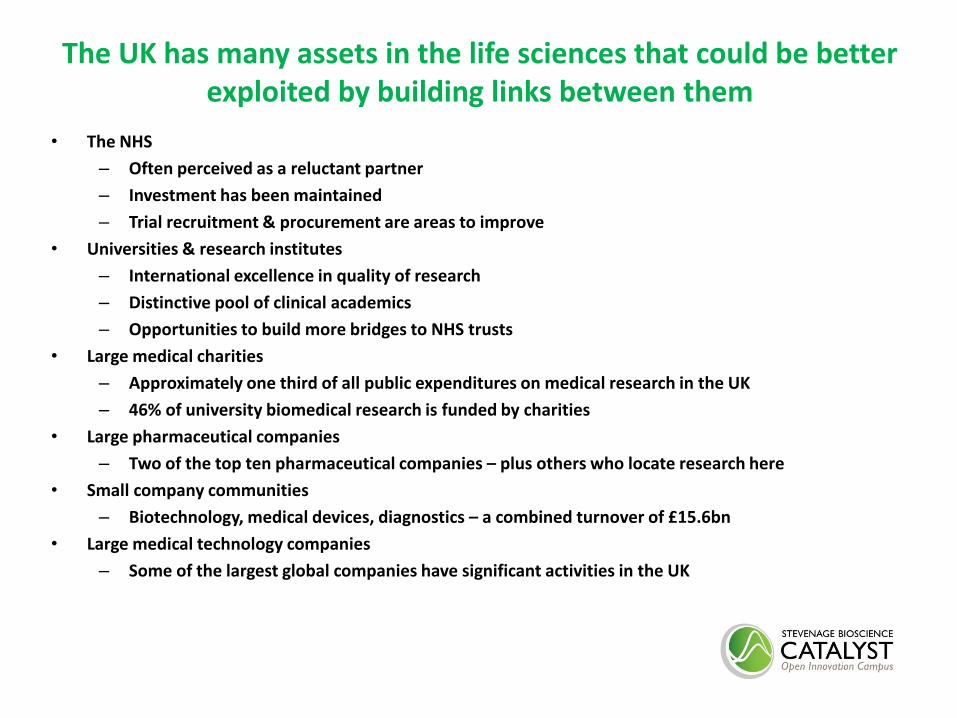

The UK has many assets in the life sciences that could be better exploited by building links between them

• The NHS

– Often perceived as a reluctant partner

– Investment has been maintained

– Trial recruitment & procurement are areas to improve

• Universities & research institutes

– International excellence in quality of research

– Distinctive pool of clinical academics

– Opportunities to build more bridges to NHS trusts

• Large medical charities

– Approximately one third of all public expenditures on medical research in the UK

– 46% of university biomedical research is funded by charities

• Large pharmaceutical companies

– Two of the top ten pharmaceutical companies – plus others who locate research here

• Small company communities

– Biotechnology, medical devices, diagnostics – a combined turnover of £15.6bn

• Large medical technology companies

– Some of the largest global companies have significant activities in the UK

Stevenage Bioscience Catalyst

The UK Bioscience sector

• SBC will ensure that the biomedical research ecosystem is fed by all three partners; academia, big pharma and biotech – Biotech in SE England is currently underweight and underinvested in comparison to

academia and big pharma, which is harming the ecosystem. • Translational nature of SBC will create a workforce whose skills and expertise will be

transferable across sectors • Develop a supportive environment and ‘open innovation’ model that works in a large pharma

setting and sets SBC apart from other Science Parks. – Enable smaller companies to access big pharma expertise resulting in the sharing of

ideas and knowledge and ultimately increased R&D productivity – Help the UK develop a biotechnology industry consistent with its strength of science

base and able to compete in the long term GSK

• Co-location offers our staff the opportunity to forge direct links with biotechs and increase our chances of external partnerships

• SBC will help to ensure that GSK continues to be a pioneer in the shift to collaborative working, – It will accelerate entrepreneurial thinking and the cultural changes required by the

R&D organisation

An exciting new concept that aims to develop a world class environment for engagement between academia, pharma and biotech

www.stevenagecatalyst.com

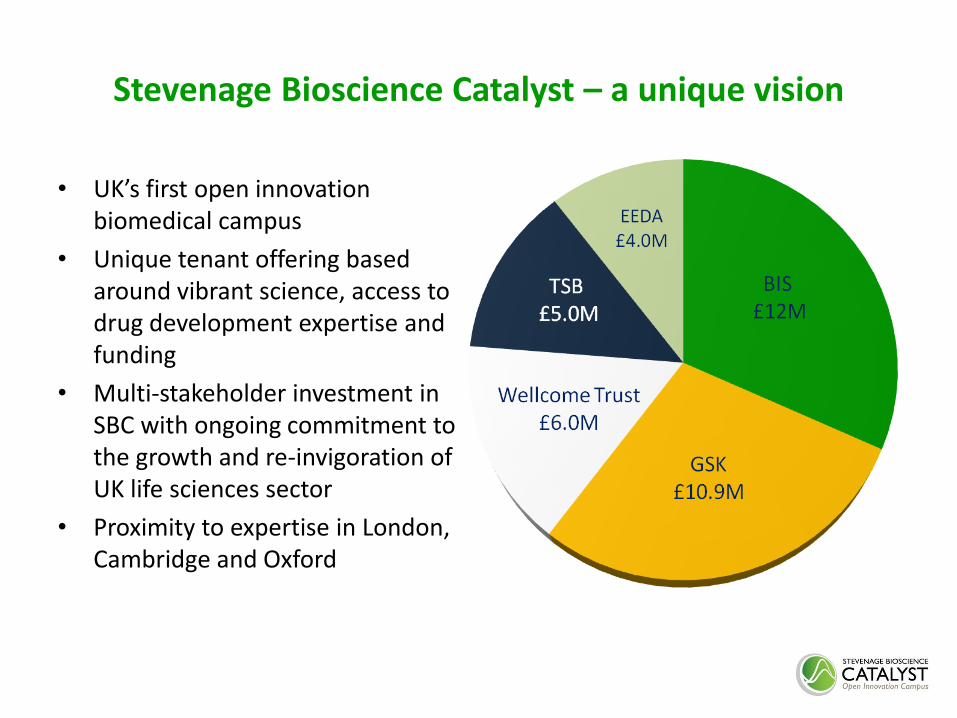

Stevenage Bioscience Catalyst – a unique vision

• UK’s first open innovation biomedical campus

• Unique tenant offering based around vibrant science, access to drug development expertise and funding

• Multi-stakeholder investment in SBC with ongoing commitment to the growth and re-invigoration of UK life sciences sector

• Proximity to expertise in London, Cambridge and Oxford

The benefits of the Catalyst to Life Science Companies • Access to an early stage seed fund – plans being developed

• Access to GSK expertise

–Senior mentoring and GSK networks

• Access to GSK facilities and experience –High value capital equipment and drug discovery and development

consultancy expertise

• Similar synergistic relationships with other stakeholders in development

• Advisory Board with commercial and technical leaders in the sector

• Exploring opportunities for a Healthcare Technology Innovation Centre

– Other central facilities being discussed

SBC Business Model

Mixed model of types of tenants & pipeline

– University spin-outs

– External start-ups or SMEs

– Satellite companies/units

Hot Desk Office Large Unit Unit

Unit

Unit

Grow On Space (e.g.

Accelerator, Science park)

Business development continuum

‘Accelerator’

Virtual

Business Support

Venturepoint

SBC Tenant Offering

• Compelling location

• Access to Scinovo

• Access to SR One funding

• Access to GSK e-journals

• Access to therapeutic expertise at GSK and other stakeholders

• Access to SBC Experts Panel

• Access to a funding network

• Access to an SBC associate network (services in areas such as IP, legal, marketing)

• Access to technical “shared services”

• Development of a web-based SBC community portal (in collaboration with TSB)

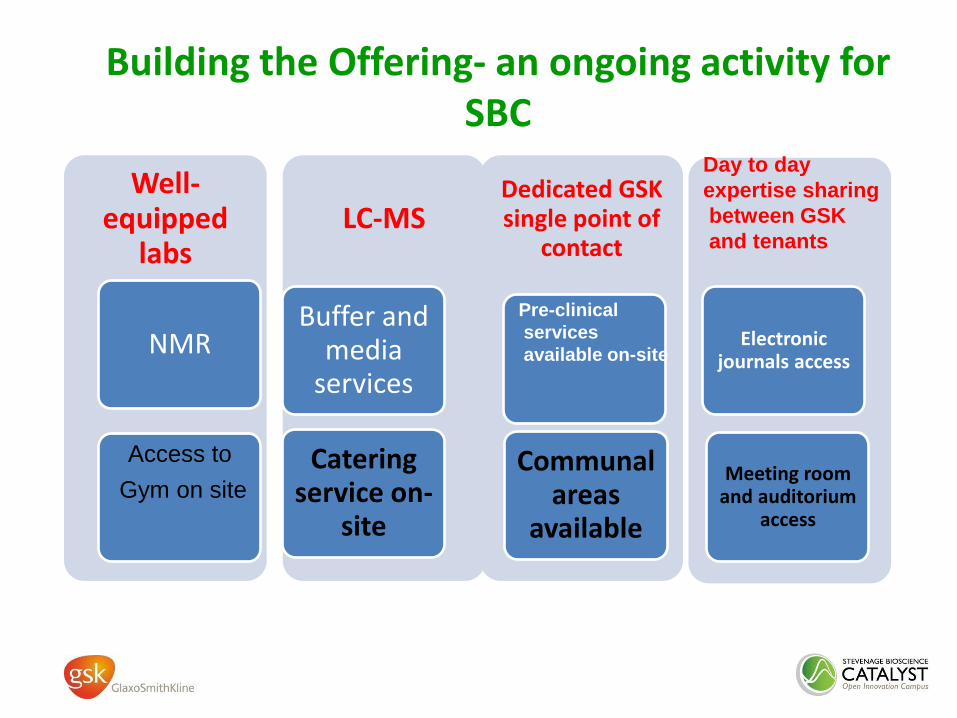

Well-equipped

labs

NMR

LC-MS

Buffer and media

services

Catering service on-

site

Dedicated GSK single point of

contact

Communal areas

available

Building the Offering- an ongoing activity for SBC

Meeting room and auditorium

access

Electronic journals access

Access to

Gym on site

Day to day

expertise sharing

between GSK

and tenants

Pre-clinical

services

available on-site

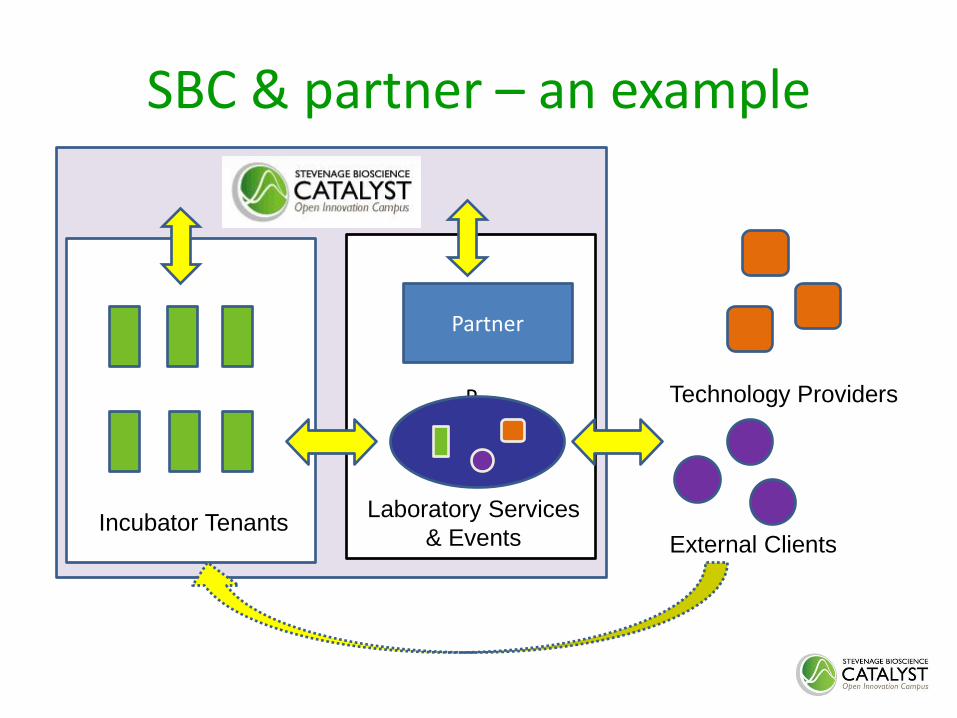

SBC & partner – an example

P

Incubator Tenants Laboratory Services

& Events External Clients

Technology Providers

Partner

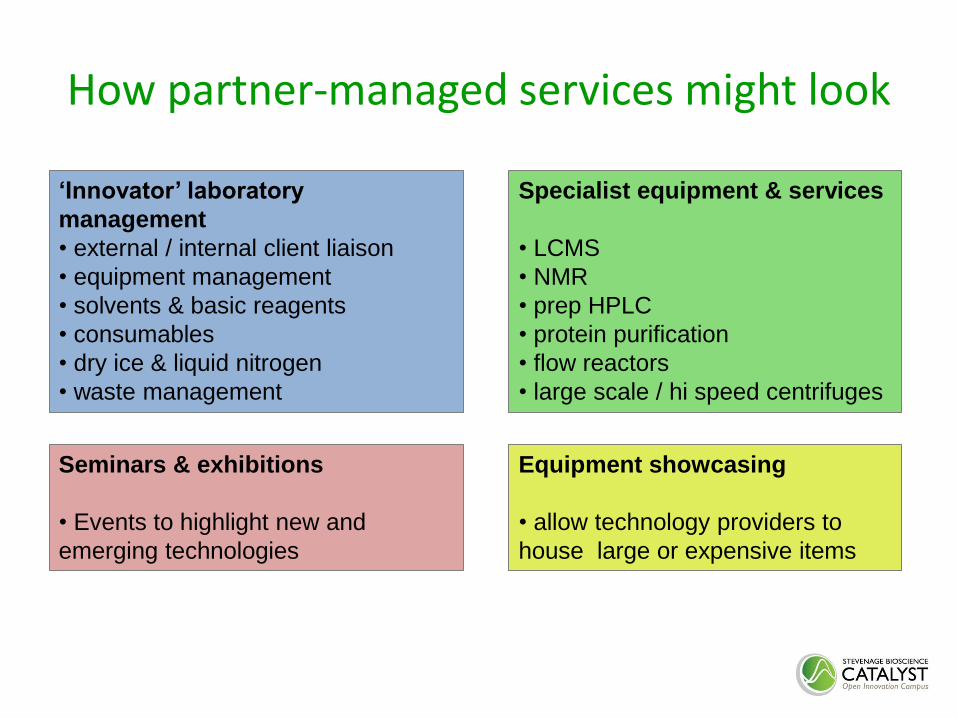

How partner-managed services might look

‘Innovator’ laboratory

management

• external / internal client liaison

• equipment management

• solvents & basic reagents

• consumables

• dry ice & liquid nitrogen

• waste management

Specialist equipment & services

• LCMS

• NMR

• prep HPLC

• protein purification

• flow reactors

• large scale / hi speed centrifuges

Seminars & exhibitions

• Events to highlight new and

emerging technologies

Equipment showcasing

• allow technology providers to

house large or expensive items

What is Open Innovation?: the SBC definition

Open Innovation is about bridging internal and external resources via collaboration at any point in the innovation process. It is characterised by:

• highly effective use of connections and networks to exchange knowledge, expertise and ideas

• external partners being involved at any stage, not just idea-generation

• equitable win-win business relationships where issues are tackled together

• openness towards new business models to maximise the value of IP and other assets

Open Innovation: what it means to us

• SBC is well-positioned to become a national resource for biomedical open

innovation

• SBC is uniquely positioned to boost collaboration at a business-to-business level,

alongside academic-business interactions

• SBC is one part of a wide-ranging commitment to open innovation by GSK. Sister

initiatives include Tres Cantos; pricing policy on diarrhoea vaccines; and publicly

available data on 1000s of potential anti-malaria compounds.

We want everyone

to be at higher risk of having a great idea

and making it work...

... biotechs, pharma, stakeholders, and UK plc

Open Innovation: works through a strong community of shared interests

Charities/public sector

eg CRUK, MRC Academia and

technology transfer

offices

Professional

service firms

eg VCs, angels

SBC as an incubator

Big pharma

Bioscience SMEs

Tenant Referrals Stakeholders:

Wellcome Trust

GSK, BIS, TSB, EEDA

SBC milestones and targets

Milestones

• Stevenage Bioscience Catalyst

announced, Oct 2009

• Start of construction, Nov 2010

• SBC topping-out ceremony with

Rt Hon David Willetts MP,

Minister for Universities and

Science , July 2011

• Practical completion Phase 1–

Dec 2011

Targets

• Planning for Phase 2 , End 2011-

2012

• First tenants, H1 2012

• Praxis/UniCo spin-out conference,

1 March 2012

• SBC opening event, Q3/4 2012

• Open Innovation event-Q4 2012

Development of Phase 1 - Incubator and Accelerator

January 2011 July 2011 September 2011

Stevenage Bioscience Catalyst

Infrastructure investment and bioincubation-the UK model

GENESIS Plenary presentation, December 1st, 2011

www.stevenagecatalyst.com