Embed Size (px)

Citation preview

ed: CK / sa:MA, PY

Benign competition may turn sour

Telkomsel has launched aggressive data-pricing in Java

while lowering voice pricing outside Java

Downgrade XL to HOLD after the stock rose 70% YTD;

likely to be impacted by slower industry growth;

Downgrade Indosat to HOLD due to its higher reliance

on Java and potential loss of revenue share.

Prefer Sarana Menara Nusantara (TOWR) as proxy to

mobile data growth and Link Net (LINK) as pure proxy

to fixed broadband growth in Indonesia.

Telkomsel’s data-only promotions in Java are 60% cheaper

than peers. Our checks indicate that Telkomsel has launched

data-only starter-packs in Java around July which are ~60%

cheaper than those offered by its competitors. It seems that

Telkomsel is targeting XL’s data-savvy customers. This has

halted the data-pricing hike cycle which had started in 4Q16-

1Q17. Indosat (ISAT) and XL (EXCL) derive ~90% and ~70% of

their revenue from Java respectively vs ~35% for Telkomsel

and may react if Telkomsel does not take-off these promotions

soon. Telkomsel has also lowered its voice-tariff by 30-60%

outside Java selectively to defend its customer base. We lower

FY17F/18F industry growth to 6.5%/6.3% (from 7%/6.8%) on

the back of these promotions.

Downgrade XL to HOLD as we see limited gains after the

recent rally (up 70% YTD). EXCL’s stock price has done well

due to revenue share gains in 1H17. With an aggressive

Telkomsel now, EXCL’s revenue share gains in 2H17F will rely

on ISAT’s network improvement. EXCL may barely meet

consensus EBITDA of Rp4.6tr in 2H17F vs only Rp3.9tr EBITDA

in 1H17. We also think that XL’s consensus FY18F EBITDA of

Rp9.7tn could be cut by 3% due to slower industry growth.

Downgrade Indosat (ISAT) to HOLD due to potential

revenue share loss. ISAT has been the biggest beneficiary of

benign competition in Java, which is not the case anymore.

ISAT also faces network quality issues due to low network

capex. We expect ISAT to lag the industry growth rate in

FY17F/18F, whereby consensus EBITDA could be cut 3%/6%.

Mantain HOLD on TLKM due to rich valuations amid slower

growth. TLKM’s 9.1x adjusted FY18F EV/EBITDA (+2SD) does

not leave room for disappointment. Consensus FY16-19F

EBITDA CAGR of 10% needs non-Telkomsel business to deliver

an aggressive 20% EBITDA CAGR.

JCI : 5,884.60

Analyst Sachin MITTAL +65 6682 3699 [email protected]

EXCL gained 800 basis points revenue share in 1H17, forcing

Telkomsel to react in July 2017

Source: Companies, DBS Bank

Stabilising data-yields may resume downward journey in

2H17F

Source: Companies, DBS Bank

DBS Group Research . Equity 20 Sep 2017

Indonesia Industry Focus

Telecom Sector

Refer to important disclosures at the end of this report

STOCKS

12-mth

Price Mkt Cap Target Performance (%)

Rp US$m Price Rp 3 mth 12 mth Rating

PT Link Net Tbk 5,200 1,194 6,000 2.0 10.6 BUY PT Sarana Menara Nusantara

4,420 3,402 5,100 15.7 11.1 BUY Telekomunikasi Indonesia 4,710 35,818 4,800 4.9 15.2 HOLD XL Axiata 3,850 3,104 3,900 18.8 45.3 HOLD Indosat 6,300 2,583 6,800 (2.3) 17.2 HOLD Tower Bersama Infrastructure

6,575 2,248 6,200 (4.4) 13.9 HOLD

Source: DBS Bank, Bloomberg Finance L.P.

Closing price as of 19 Sep 2017

Page 1

Industry Focus

Telecom Sector

Telkomsel is disrupting the status quo

Telkomsel getting aggressive in Java. Our channel checks

indicate intensifying competition on the data front in the Java

region. Telkomsel has reportedly slashed pricing on its high-end

data packages, currently offering a 25GB starter pack with a 90-

day validity for just Rp55,000-45,000.

Internet packages offered by EXCL and ISAT

Source: Companies, DBS Bank

XL and Indosat had been cutting bonus data under their

packages since 4Q16-1Q17 as Indonesia data yields are among

the lowest in the region. Indonesian data yields declined nearly

50% from 2Q16 to 2Q17, with usage jumping 120% from

~260MB to 1.2GB over the same period.

Stabilising data yields may see downward trend again

Source: Companies, DBS Bank

This implies a discount of over 60% to similar data packages on

offer by Indosat and EXCL. This promotion is not mentioned

anywhere on Telkomsel’s website but dealers are offering this

promotion on the ground. Telkomsel appears to be keen on

snatching heavy data users in Java, who are mostly with EXCL,

to compensate for subscriber losses outside Java.

We believe that it is possible for Telkomsel to keep this

promotion ongoing for an extended period of time, leading ISAT

and EXCL to resort to lowering data prices. This would disrupt

the duos’ efforts in 4Q16-1Q17 to lift up data prices. Indosat

may also be facing some capacity constraint in our view due to

lower addition of 3G/4G base stations.

India and Indonesia have lowest data yields in the region

Source: M1, Maxis, Digi.com, Celcom Axiata, Bharti Airtel, idea Cellular,

Telkom, XL Axiata, Indosat, AIS,, DBS Bank

Page 2

Industry Focus

Telecom Sector

Data usage on the rise in India and Indonesia supported by

low prices

Source: M1, Maxis, Digi.com, Celcom Axiata, Bharti Airtel, idea Cellular,

Telkom, XL Axiata, Indosat, AIS,, DBS Bank

Telkomsel’s voice prices have been slashed ~ 30%-60% in

FY17

General tariffs on prepaid packages.

Source: Telkomsel, DBS Bank

Revenue share gains by EXCL likely to lose steam as Telkomsel

fires back in the ex-Java region. EXCL made steady gains in

revenue market share over the past two quarters, snatching ex-

Java market share from Telkomsel. Telkomsel lost nearly 0.9%

revenue market share over the last two quarters, of which over

0.8% was grabbed by EXCL. However, our industry checks

indicate that Telkomsel is retaliating against EXCL outside Java,

beefing up its data offerings and slashing voice prices. Since the

beginning of the year Telkomsel has slashed its voice prices by

~30%-60% in certain ex-Java regions that overlap with EXCL’s.

With the price adjustments, Telkomsel has ousted EXCL from

being the cheaper provider of legacy services ex-Java. Higher

legacy pricing of EXCL and Telkomsel’s superior network quality

outside Java may reduce the pace of EXCL’s ex-Java subscriber

acquisitions. Intensifying competition on the data front in Java,

which remains a stronghold of EXCL, could also lead to an

increase in subscriber churn. Accordingly, we believe that the

pace of revenue share gains by EXCL will likely reduce over

2H17F.

EXCL gained 800bps revenue share over 1H17, forcing

Telkomsel to react in July 2017

Source: Companies, DBS Bank

Telkomsel closes the gap on voice pricing with EXCL

Source: Companies, DBS Bank

Page 3

Industry Focus

Telecom Sector

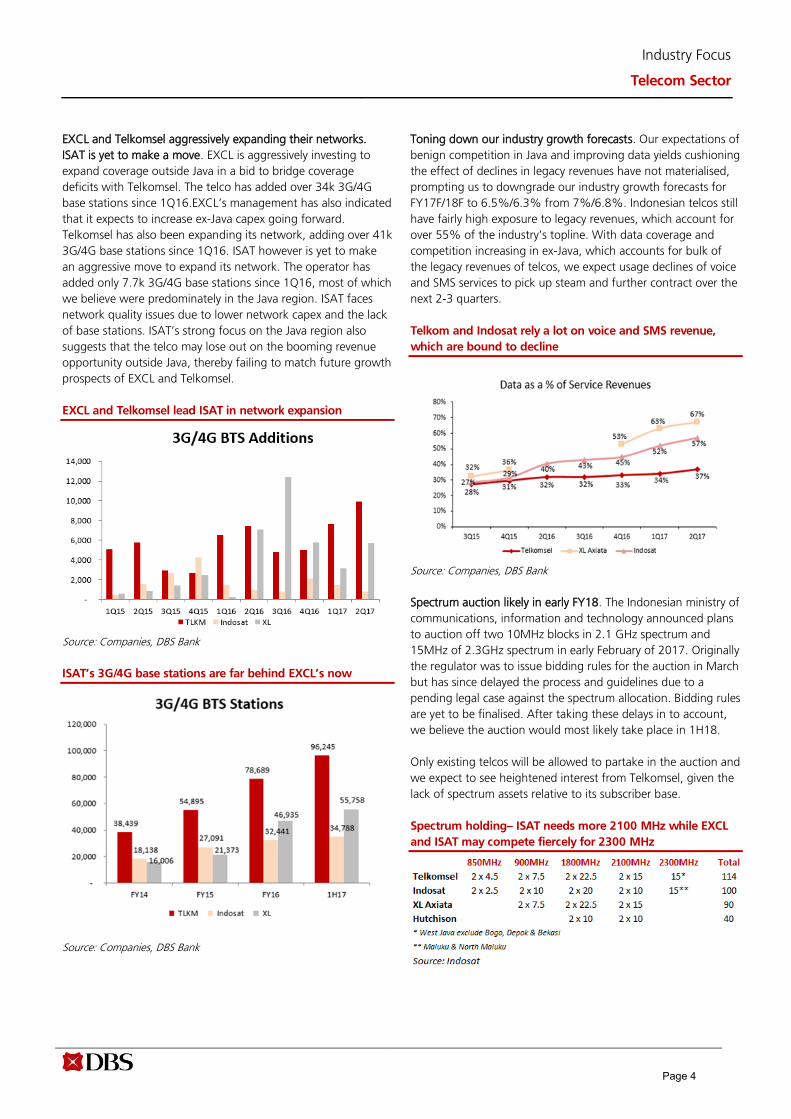

EXCL and Telkomsel aggressively expanding their networks.

ISAT is yet to make a move. EXCL is aggressively investing to

expand coverage outside Java in a bid to bridge coverage

deficits with Telkomsel. The telco has added over 34k 3G/4G

base stations since 1Q16.EXCL’s management has also indicated

that it expects to increase ex-Java capex going forward.

Telkomsel has also been expanding its network, adding over 41k

3G/4G base stations since 1Q16. ISAT however is yet to make

an aggressive move to expand its network. The operator has

added only 7.7k 3G/4G base stations since 1Q16, most of which

we believe were predominately in the Java region. ISAT faces

network quality issues due to lower network capex and the lack

of base stations. ISAT’s strong focus on the Java region also

suggests that the telco may lose out on the booming revenue

opportunity outside Java, thereby failing to match future growth

prospects of EXCL and Telkomsel.

EXCL and Telkomsel lead ISAT in network expansion

Source: Companies, DBS Bank

ISAT’s 3G/4G base stations are far behind EXCL’s now

Source: Companies, DBS Bank

Toning down our industry growth forecasts. Our expectations of

benign competition in Java and improving data yields cushioning

the effect of declines in legacy revenues have not materialised,

prompting us to downgrade our industry growth forecasts for

FY17F/18F to 6.5%/6.3% from 7%/6.8%. Indonesian telcos still

have fairly high exposure to legacy revenues, which account for

over 55% of the industry’s topline. With data coverage and

competition increasing in ex-Java, which accounts for bulk of

the legacy revenues of telcos, we expect usage declines of voice

and SMS services to pick up steam and further contract over the

next 2-3 quarters.

Telkom and Indosat rely a lot on voice and SMS revenue,

which are bound to decline

Source: Companies, DBS Bank

Spectrum auction likely in early FY18. The Indonesian ministry of

communications, information and technology announced plans

to auction off two 10MHz blocks in 2.1 GHz spectrum and

15MHz of 2.3GHz spectrum in early February of 2017. Originally

the regulator was to issue bidding rules for the auction in March

but has since delayed the process and guidelines due to a

pending legal case against the spectrum allocation. Bidding rules

are yet to be finalised. After taking these delays in to account,

we believe the auction would most likely take place in 1H18.

Only existing telcos will be allowed to partake in the auction and

we expect to see heightened interest from Telkomsel, given the

lack of spectrum assets relative to its subscriber base.

Spectrum holding– ISAT needs more 2100 MHz while EXCL

and ISAT may compete fiercely for 2300 MHz

Page 4

Industry Focus

Telecom Sector

Telkomsel would be keen on both the spectrum blocks given

its already high no. of subscribers serviced per MHz

Source: Companies, DBS Bank

We have used a 40%/80% premium to the 2.1GHz/2.3GHz

spectrum auction held in India recently (per MHz per

population) to arrive at a 5MHz spectrum pricing of ~US$43m

for the 2.1GHz band and ~US$15m for the 2.3GHz band. We

attach a higher premium to the 2.3GHz band as we expect to

see more interest on this spectrum, which reportedly would

be used for 4G services. We assume that Telkomsel will

acquire spectrum assets in both bands. We also expect to see

ISAT acquiring one 10MHz block in the 2.1GHz spectrum and

EXCL and ISAT both acquiring 5 MHz each in the 2.3GHz

spectrum band (Assuming that the 2.3GHz band will be

auctioned in 5MHz blocks). This results in spectrum capex of

Rp1.3tr for ISAT and Rp196bn for EXCL. We have not

factored in any upside to earnings from the additional

spectrum resources.

Historical 12-month forward EV/EBITDA multiples

Telkom’s non-adjusted + 2SD EV/EBITDA is not justified with

fixed-line compensating for slower mobile growth

Source: DBS Bank

EXCL may trade below the historical average as mobile

competition intensifies

EXCL may trade below the historical average as mobile

competition intensifies

Source: DBS Bank

ISAT may trade below the historical average due to potential

revenue share loss

Source: DBS Bank

Page 5

Industry Focus

Telecom Sector

Regional Peer Table

Source: DBS Bank; DBS Vickers

Mkt Price 12-mth CA GR

Company F YE Cap S$ Target Price % 16-18

(US$m) 18/9/2017 LCL Upside Rcmd (%) 17F 18F 16A 17F 16A 17F 17F 18F

China / Hong Kong SHCOMP Index 3,363

China Mobile Dec 212,440 81.10 114.00 41% BUY 4 12.4 11.8 3.5% 7.8% 1.4x 1.4x 3.3x 3.0x

China Telecom Dec 7,030 3.96 5.10 29% BUY 8 13.5 12.7 2.8% 3.1% 0.9x 0.8x 3.6x 3.4x

China Unicom Dec 34,251 11.18 11.30 1% HOLD nm 45.6 23.8 0.0% 0.8% 1.0x 1.0x 3.9x 3.4x

Smartone Telecom Jun 1,318 9.32 7.50 -20% FV -8 15.1 14.8 6.4% 6.4% 2.3x 2.2x 5.1x 4.9x

Hutchison Telecom Dec 1,769 2.87 3.30 15% HOLD -1 20.4 20.0 3.8% 3.7% 1.2x 1.2x 7.1x 6.8x

HKT Trust Dec 9,541 9.85 12.80 30% BUY 0 15.7 15.3 6.3% 6.4% 1.9x 1.9x 8.7x 8.5x

Malay sia KLCI Index 1783.66

Digi.Com Dec 9,038 4.87 4.20 -14% FV -4 25.7 25.2 4.3% 3.9% 72.9x 72.9x 13.9x 13.7x

Maxis Bhd Dec 10,701 5.74 5.15 -10% HOLD 0 22.7 21.9 3.5% 3.8% 9.1x 6.8x 11.8x 11.8x

Telekom Dec 5,741 6.40 7.10 11% BUY 9 27.9 24.0 3.4% 3.2% 3.1x 3.1x 7.5x 7.0x

Axiata Group Dec 10,846 5.05 4.75 -6% HOLD 1 35.4 31.3 1.6% 1.4% 1.9x 1.9x 8.0x 7.6x

Singapore ST I Index 3241.85

M1 Dec 1,235 1.79 1.78 0% FV -12 13.1 14.4 7.2% 6.1% 4.1x 4.1x 6.9x 7.5x

Starhub Dec 3,348 2.61 2.33 -11% FV -12 17.0 17.6 7.7% 6.1% 23.1x 27.1x 8.8x 9.3x

Thailand SET Index 1670.2

Advanced Info Serv ice Dec 17,430 194.00 162.00 -16% HOLD 6 19.5 17.0 5.2% 3.6% 13.5x 11.8x 10.0x 9.1x

Total Access Comm. Dec 4,132 57.75 37.90 -34% SELL 19 80.5 37.7 0.7% 0.3% 5.1x 4.9x 5.8x 5.7x

Indonesia J CI Index 5884.611

Indosat Dec 2,580 6,300 8,500 35% BUY nm 19.1 nm 0.0% 0.0% 2.6x 2.3x 3.8x 3.2x

PT Telekom Dec 35,775 4,710 4,800 2% HOLD 18 19.9 17.5 2.9% 3.5% 5.6x 5.3x 7.6x 7.1x

XL Axiata Dec 3,197 3,970 4,000 1% BUY nm 422.0 93.2 0.5% 0.1% 2.0x 2.0x 6.3x 5.7x

PT Sarana Menara Dec 3,398 4,420 5,100 15% BUY nm 19.5 17.8 0.0% 1.6% 4.2x 3.7x 10.5x 9.6x

Tower Bersama Dec 2,245 6,575 6,200 -6% HOLD -2 33.3 25.3 0.9% 3.3% 19.1x 20.5x 14.2x 13.1x

A v erage 47.7 24.0 7.8 7.4

EV /EBITDAPE (x) Div idend Y ield (%) P/BV

Page 6

Industry Focus

Telecom Sector

COMPANY GUIDES

Page 7

ed: CK / sa:MA, PY

HOLD (Downgrade from BUY)

Last Traded Price ( 18 Sep 2017): Rp6,300 (JCI : 5,884.60)

Price Target 12-mth: Rp6,800 (8% upside) (Prev Rp8,500)

Analyst Sachin MITTAL +65 6682 3699 [email protected]

What’s New Market may be underestimating the impact of rising

competition in Java which accounts for 90% of ISAT’s

revenue

FY17F/18F EBITDA may be cut 3%/6% due to lower

growth as network quality remains a concern

Downgrade to HOLD with a lower TP of Rp6,800

Price Relative

Forecasts and Valuation FY Dec (Rp m) 2016A 2017F 2018F 2019F

Revenue 29,185 30,321 30,611 31,091 EBITDA 12,778 13,079 12,967 13,046 Pre-tax Profit 1,795 2,134 1,920 1,737 Net Profit 1,105 1,306 1,137 989 Net Pft (Pre Ex.) 1,105 1,306 1,137 989 Net Pft Gth (Pre-ex) (%) nm 18.2 (12.9) (13.1) EPS (Rp) 203 240 209 182 EPS Pre Ex. (Rp) 203 240 209 182 EPS Gth Pre Ex (%) (184) 18 (13) (13) Diluted EPS (Rp) 203 240 209 182 Net DPS (Rp) 0.0 0.0 0.0 182 BV Per Share (Rp) 2,457 2,697 2,906 2,984 PE (X) 31.0 26.2 30.1 34.6 PE Pre Ex. (X) 31.0 26.2 30.1 34.6 P/Cash Flow (X) 3.5 3.2 2.9 3.4 EV/EBITDA (X) 4.5 4.0 3.9 3.7 Net Div Yield (%) 0.0 0.0 0.0 2.9 P/Book Value (X) 2.6 2.3 2.2 2.1 Net Debt/Equity (X) 1.5 1.1 0.9 0.7 ROAE (%) 8.6 9.3 7.5 6.2

Earnings Rev (%): (27) (52) (66) Consensus EPS (Rp): 355 487 624 Other Broker Recs: B: 27 S: 0 H: 3

Source of all data on this page: Company, DBS Bank, Bloomberg Finance L.P

Worse-off from rising competition in Java

Share price could be range-bound due to potential revenue

share losses. ISAT was the biggest beneficiary of benign

competition in Java due to its higher reliance on Java, which is

not the case anymore. Our checks indicate that Telkomsel is

offering data-only starter packs at over 60% discount in Java

since July-Aug 2017. ISAT offers limited upside potential after

factoring potential revenue share loss and incorporating the

potential spectrum auction price of ~Rp1.3tr in FY18F.

Where we differ? Our FY17F/18F EBITDA estimates are 3%/6%

below consensus estimates. Consensus is overestimating the

impact of stabilising data yields pre-maturely and ignoring

network quality issues at ISAT which may take a few months to

resolve. We believe that despite efforts by ISAT and EXCL to

improve data yields, aggressive competitive behaviour by

Telkomsel in the Java region is likely to reverse this trend.

Potential catalyst – significant change in network quality. ISAT

needs to ramp up its capex significantly to have enough

capacity to encourage data usage. We expect ISAT to catch up

with its peers in terms of network quality by 2H18F.

Valuation:

Downgrade to HOLD with a lower target price of Rp6,800. As

we cut FY17F/18F EBITDA by 2%/2.5%, nudge up FY18F/19F

capex and factor in the potential spectrum auction price of

~Rp1.3tr, our TP drops to Rp6,800. Our DCF-based TP assumes

a WACC of 9.4% and 1% terminal growth rate. ISAT’s

valuation is cheap but gaining revenue share is a critical factor

for the stock price to perform well.

Key Risks to Our View:

Benign competition in Java. If Telkomsel reverts back to uphold

the trend of increasing data yields within Java and thereby

cooling down competition, ISAT could record faster growth in

revenues and higher-than-expected EBITDA.

DBS Group Research . Equity 20 Sep 2017

Indonesia Company Guide

Indosat Version 6 | Bloomberg: ISAT IJ | Reuters: ISAT.JK Refer to important disclosures at the end of this report

Issued Capital (m shrs) 5,434

Mkt. Cap (Rpbn/US$m) 34,234 / 2,580

Major Shareholders (%)

Ooredoo Asia (%) 65.0

Govt of Indonesia (%) 14.3

Oredoo Asia Pte Ltd 65.00%

Free Float (%) 20.7

3m Avg. Daily Val 0.28

ICB Industry : Telecommunications / Telecommunications

Page 8

Company Guide

Indosat

CRITICAL DATA POINTS TO WATCH

Critical Factors

ISAT to be impacted the most from tightening competition in

Java. ISAT, which generates close to 90% of revenues in the

Java region is likely to be impacted the most with tightening

competitive dynamics in Java. ISAT was among the first telcos to

curtail promotions on data, which was soon followed by EXCL.

However, with Telkomsel disrupting this trend, we believe ISAT

would have no choice but to revert back to offering discounts

on data packages to prevent a loss of market share to the

incumbent. As a result, we revise our cellular revenue growth

forecasts to only 5.8%/5.5% from 7.3%/5.8%, leading us to

cut EBITDA by 2%/2.5%.

Lack of investments in and out of Java could hurt future

revenue growth. ISAT’s lack of expansions in and out of Java

could lead to the operator trailing EXCL and Telkomsel on

future growth in topline. Indosat was the least active in

expanding its network, adding over 7.7k 3G/4G BTS stations

(predominately in Java) since 1Q16 vs. 41k/34k by Telkomsel

and EXCL. Our industry checks also indicate that the operator is

facing network quality and capacity restrictions amid rising

usage of data in Java. This could result in ISAT losing data heavy

subscribers to EXCL. Restricting operations to Java and rising

network issues could result in ISAT losing revenue market share,

leading to muted growth in future revenues.

ISAT lags EXCL and Telkomsel in 3G/4G base stations

Source: Companies, DBS Banks

Reducing exposure to USD debt could bring predictability to the

bottomline. ISAT's earnings will be more predictable as it now

has lesser exposure to foreign currency debt. ISAT’s USD debt

outstanding is only 5% (2Q17) of the total outstanding debt,

lower than its historical level of ~50%. We estimate that 60%

of the outstanding USD debt is expected to mature within the

next 12 months, which should minimise forex impact on

profitability further. This should allow the counter to post

predictable stable net profit in the short to medium term.

Subscribers (m)

Blended ARPU (Rp k)

EBITDA Margin %

Capex (Rp tn)

EBITDA (Rpbn)

Source: Company, DBS Bank

Page 9

Company Guide

Indosat

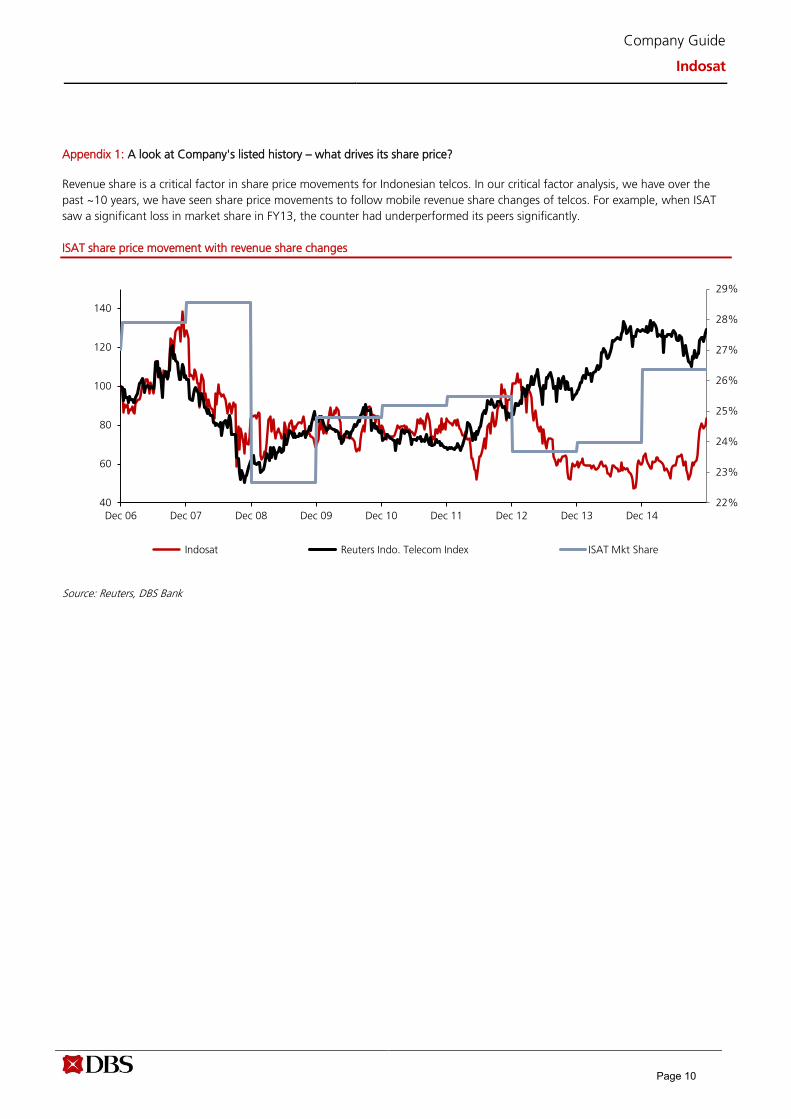

Appendix 1: A look at Company's listed history – what drives its share price?

Revenue share is a critical factor in share price movements for Indonesian telcos. In our critical factor analysis, we have over the

past ~10 years, we have seen share price movements to follow mobile revenue share changes of telcos. For example, when ISAT

saw a significant loss in market share in FY13, the counter had underperformed its peers significantly.

ISAT share price movement with revenue share changes

Source: Reuters, DBS Bank

22%

23%

24%

25%

26%

27%

28%

29%

40

60

80

100

120

140

Dec 06 Dec 07 Dec 08 Dec 09 Dec 10 Dec 11 Dec 12 Dec 13 Dec 14

Indosat Reuters Indo. Telecom Index ISAT Mkt Share

Page 10

Company Guide

Indosat

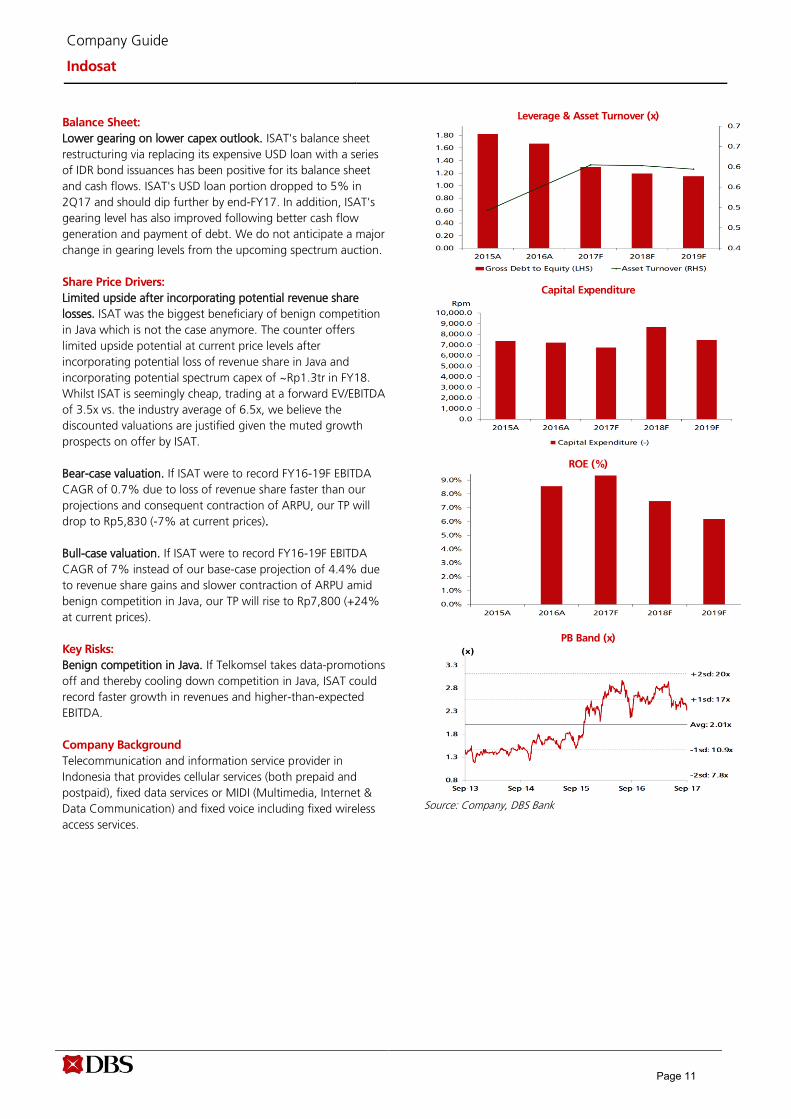

Balance Sheet:

Lower gearing on lower capex outlook. ISAT's balance sheet

restructuring via replacing its expensive USD loan with a series

of IDR bond issuances has been positive for its balance sheet

and cash flows. ISAT's USD loan portion dropped to 5% in

2Q17 and should dip further by end-FY17. In addition, ISAT’s

gearing level has also improved following better cash flow

generation and payment of debt. We do not anticipate a major

change in gearing levels from the upcoming spectrum auction.

Share Price Drivers:

Limited upside after incorporating potential revenue share

losses. ISAT was the biggest beneficiary of benign competition

in Java which is not the case anymore. The counter offers

limited upside potential at current price levels after

incorporating potential loss of revenue share in Java and

incorporating potential spectrum capex of ~Rp1.3tr in FY18.

Whilst ISAT is seemingly cheap, trading at a forward EV/EBITDA

of 3.5x vs. the industry average of 6.5x, we believe the

discounted valuations are justified given the muted growth

prospects on offer by ISAT.

Bear-case valuation. If ISAT were to record FY16-19F EBITDA

CAGR of 0.7% due to loss of revenue share faster than our

projections and consequent contraction of ARPU, our TP will

drop to Rp5,830 (-7% at current prices).

Bull-case valuation. If ISAT were to record FY16-19F EBITDA

CAGR of 7% instead of our base-case projection of 4.4% due

to revenue share gains and slower contraction of ARPU amid

benign competition in Java, our TP will rise to Rp7,800 (+24%

at current prices).

Key Risks:

Benign competition in Java. If Telkomsel takes data-promotions

off and thereby cooling down competition in Java, ISAT could

record faster growth in revenues and higher-than-expected

EBITDA.

Company Background

Telecommunication and information service provider in

Indonesia that provides cellular services (both prepaid and

postpaid), fixed data services or MIDI (Multimedia, Internet &

Data Communication) and fixed voice including fixed wireless

access services.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

PB Band (x)

Source: Company, DBS Bank

Page 11

Company Guide

Indosat

Key Assumptions

FY Dec 2015A 2016A 2017F 2018F 2019F

Subscribers (m) 66.5 77.8 77.9 81.7 83.4

Blended ARPU (Rp k) 28.7 28.4 27.4 27.0 26.5

EBITDA Margin % 42.2 43.8 43.1 42.4 42.0

Capex (Rp tn) 7.30 7.20 6.70 8.70 7.50

EBITDA (Rpbn) 11,297 12,778 13,079 12,967 13,046

Segmental Breakdown

FY Dec 2015A 2016A 2017F 2018F 2019F

Revenues (Rpbn)

FWA & IDD 1,119 959 940 921 902

Cellular 21,896 24,095 25,003 25,224 25,633

MIDI 3,754 4,131 4,378 4,466 4,555

Others 0.10 0.10 0.10 0.10 0.10

Total 26,769 29,185 30,321 30,611 31,091

Income Statement (Rpbn)

FY Dec 2015A 2016A 2017F 2018F 2019F

Revenue 26,769 29,185 30,321 30,611 31,091

Cost of Goods Sold (24,100) (25,238) (26,076) (26,747) (27,411)

Gross Profit 2,669 3,946 4,246 3,863 3,680

Other Opng (Exp)/Inc 0.0 0.0 0.0 0.0 1.00

Operating Profit 2,669 3,946 4,246 3,863 3,680

Other Non Opg (Exp)/Inc (1,844) (6.3) 0.0 0.0 0.0

Associates & JV Inc 0.0 0.0 0.0 0.0 0.0

Net Interest (Exp)/Inc (2,611) (2,145) (2,112) (1,944) (1,944)

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0

Pre-tax Profit (1,786) 1,795 2,134 1,920 1,737

Tax 622 (520) (640) (576) (521)

Minority Interest (147) (171) (188) (206) (227)

Preference Dividend 0.0 0.0 0.0 0.0 1.00

Net Profit (1,310) 1,105 1,306 1,137 989

Net Profit before Except. (1,310) 1,105 1,306 1,137 989

EBITDA 11,297 12,778 13,079 12,967 13,046

Growth

Revenue Gth (%) 11.1 9.0 3.9 1.0 1.6

EBITDA Gth (%) 29.4 13.1 2.4 (0.9) 0.6

Opg Profit Gth (%) 312.6 47.9 7.6 (9.0) (4.7)

Net Profit Gth (Pre-ex) (%) 34.9 nm 18.2 (12.9) (13.1)

Margins & Ratio

Gross Margins (%) 10.0 13.5 14.0 12.6 11.8

Opg Profit Margin (%) 10.0 13.5 14.0 12.6 11.8

Net Profit Margin (%) (4.9) 3.8 4.3 3.7 3.2

ROAE (%) (10.1) 8.6 9.3 7.5 6.2

ROA (%) (2.4) 2.1 2.6 2.2 1.9

ROCE (%) 6.2 6.8 7.6 6.9 6.5

Div Payout Ratio (%) N/A 0.0 0.0 0.0 100.0

Net Interest Cover (x) 1.0 1.8 2.0 2.0 1.9

Source: Company, DBS Bank

Higher capex on spectrum assets

Lower revenue growth forecasts

Page 12

Company Guide

Indosat

Quarterly / Interim Income Statement (Rpbn)

FY Dec 2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

Revenue 7,129 7,583 7,660 7,290 7,823

Cost of Goods Sold (6,271) (6,552) (6,449) (6,458) (6,403)

Gross Profit 858 1,030 1,211 832 1,420

Other Oper. (Exp)/Inc 0.0 0.0 0.0 0.0 0.0

Operating Profit 858 1,030 1,211 832 1,420

Other Non Opg (Exp)/Inc 11.0 134 (239) 5.80 (1.3)

Associates & JV Inc 0.0 0.0 0.0 0.0 0.0

Net Interest (Exp)/Inc (519) (545) (516) (528) (513)

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0

Pre-tax Profit 350 619 456 309 906

Tax (104) (170) (130) (97.9) (247)

Minority Interest (35.0) (32.1) (65.4) (37.3) (47.8)

Net Profit 211 417 260 174 610

Net profit bef Except. 211 417 260 174 610

EBITDA 3,080 3,425 3,398 3,100 3,574

Growth

Revenue Gth (%) 4.6 6.4 1.0 (4.8) 7.3

EBITDA Gth (%) 4.0 11.2 (0.8) (8.8) 15.3

Opg Profit Gth (%) 1.2 20.1 17.6 (31.3) 70.7

Net Profit Gth (Pre-ex) (%) (2.9) 97.9 (37.7) (33.2) 250.9

Margins

Gross Margins (%) 12.0 13.6 15.8 11.4 18.2

Opg Profit Margins (%) 12.0 13.6 15.8 11.4 18.2

Net Profit Margins (%) 3.0 5.5 3.4 2.4 7.8

Balance Sheet (Rpbn)

FY Dec 2015A 2016A 2017F 2018F 2019F

Net Fixed Assets 41,822 39,078 36,835 36,279 34,234

Invts in Associates & JVs 0.0 0.0 0.0 0.0 0.0

Other LT Assets 3,648 3,687 3,546 3,405 3,264

Cash & ST Invts 3,623 1,850 2,601 5,819 8,318

Inventory 39.3 79.3 79.3 81.1 83.0

Debtors 2,730 2,707 2,813 2,840 2,884

Other Current Assets 3,526 3,437 3,590 3,664 3,738

Total Assets 55,389 50,839 49,464 52,088 52,521

ST Debt 7,586 8,366 5,000 5,000 5,000

Creditor 764 845 905 926 948

Other Current Liab 11,703 9,875 10,313 11,572 11,337

LT Debt 16,607 15,309 15,309 15,309 15,309

Other LT Liabilities 5,465 2,266 2,266 2,266 2,266

Shareholder’s Equity 12,483 13,350 14,656 15,794 16,213

Minority Interests 781 827 1,015 1,221 1,448

Total Cap. & Liab. 55,389 50,839 49,464 52,088 52,521

Non-Cash Wkg. Capital (6,171) (4,497) (4,736) (5,914) (5,579)

Net Cash/(Debt) (20,569) (21,824) (17,708) (14,489) (11,991)

Debtors Turn (avg days) 32.9 34.0 33.2 33.7 33.6

Creditors Turn (avg days) 17.2 17.9 18.5 18.9 19.0

Inventory Turn (avg days) 1.0 1.3 1.7 1.7 1.7

Asset Turnover (x) 0.5 0.5 0.6 0.6 0.6

Current Ratio (x) 0.5 0.4 0.6 0.7 0.9

Quick Ratio (x) 0.3 0.2 0.3 0.5 0.6

Net Debt/Equity (X) 1.6 1.5 1.1 0.9 0.7

Net Debt/Equity ex MI (X) 1.6 1.6 1.2 0.9 0.7

Capex to Debt (%) 30.4 30.4 33.1 42.8 36.7

Z-Score (X) 1.2 1.5 1.9 2.1 2.2

Source: Company, DBS Bank

Lower interest costs after balance sheet restructure

Page 13

Company Guide

Indosat

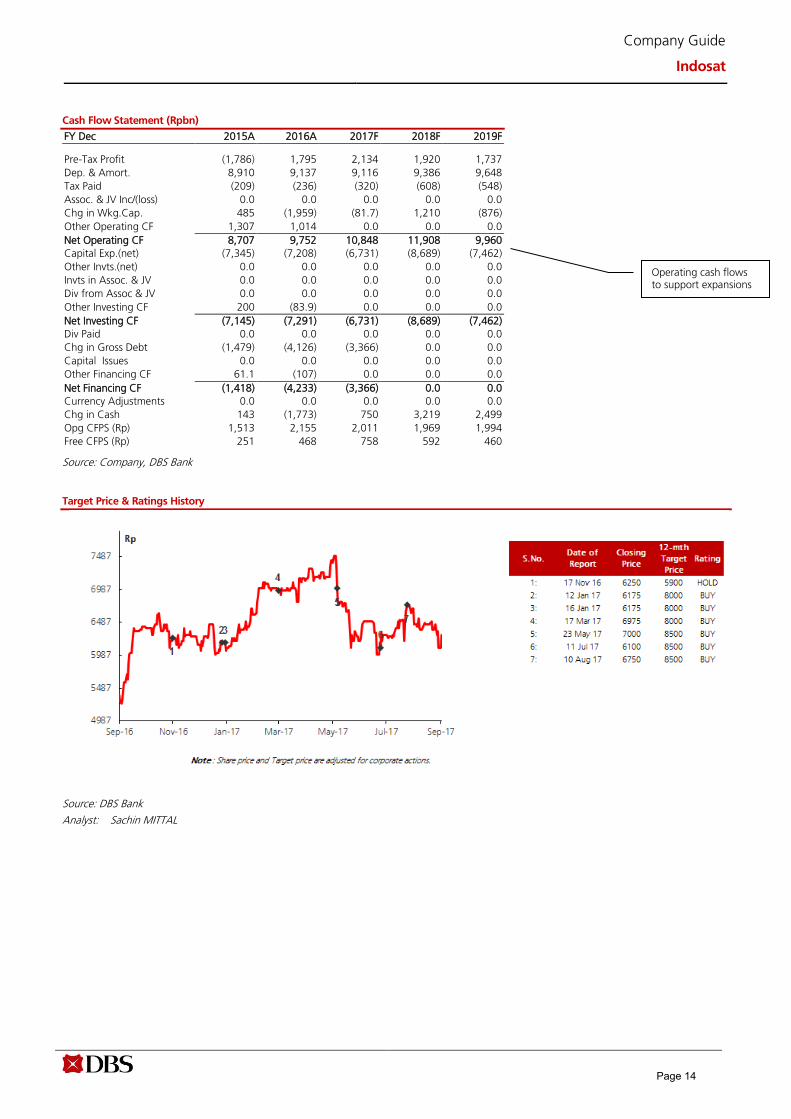

Cash Flow Statement (Rpbn)

FY Dec 2015A 2016A 2017F 2018F 2019F

Pre-Tax Profit (1,786) 1,795 2,134 1,920 1,737

Dep. & Amort. 8,910 9,137 9,116 9,386 9,648

Tax Paid (209) (236) (320) (608) (548)

Assoc. & JV Inc/(loss) 0.0 0.0 0.0 0.0 0.0

Chg in Wkg.Cap. 485 (1,959) (81.7) 1,210 (876)

Other Operating CF 1,307 1,014 0.0 0.0 0.0

Net Operating CF 8,707 9,752 10,848 11,908 9,960

Capital Exp.(net) (7,345) (7,208) (6,731) (8,689) (7,462)

Other Invts.(net) 0.0 0.0 0.0 0.0 0.0

Invts in Assoc. & JV 0.0 0.0 0.0 0.0 0.0

Div from Assoc & JV 0.0 0.0 0.0 0.0 0.0

Other Investing CF 200 (83.9) 0.0 0.0 0.0

Net Investing CF (7,145) (7,291) (6,731) (8,689) (7,462)

Div Paid 0.0 0.0 0.0 0.0 0.0

Chg in Gross Debt (1,479) (4,126) (3,366) 0.0 0.0

Capital Issues 0.0 0.0 0.0 0.0 0.0

Other Financing CF 61.1 (107) 0.0 0.0 0.0

Net Financing CF (1,418) (4,233) (3,366) 0.0 0.0

Currency Adjustments 0.0 0.0 0.0 0.0 0.0

Chg in Cash 143 (1,773) 750 3,219 2,499

Opg CFPS (Rp) 1,513 2,155 2,011 1,969 1,994

Free CFPS (Rp) 251 468 758 592 460

Source: Company, DBS Bank

Target Price & Ratings History

Source: DBS Bank

Analyst: Sachin MITTAL

Operating cash flows to support expansions

Page 14

ed: CK / sa:MA, PY

HOLDLast Traded Price ( 18 Sep 2017): Rp4,710 (JCI : 5,884.60)

Price Target 12-mth: Rp4,800 (2% upside)

Analyst Sachin MITTAL +65 6682 3699 [email protected]

What’s New Telkomsel’s growth to slow sharply in FY17F;

Corporate and Fibre broadband to support fixed

segment revenue

Ex-Java competition from EXCL is a concern

Maintain HOLD with unchanged TP of Rp4,800

Price Relative

Forecasts and Valuation FY Dec (Rp m) 2016A 2017F 2018F 2019F

Revenue 116,333 127,316 136,997 145,442 EBITDA 59,498 66,266 71,560 76,066 Pre-tax Profit 38,189 45,069 48,729 51,284 Net Profit 19,352 23,634 26,816 28,868 Net Pft (Pre Ex.) 19,352 23,634 26,816 28,868 Net Pft Gth (Pre-ex) (%) 24.9 22.1 13.5 7.7 EPS (Rp) 194 237 269 289 EPS Pre Ex. (Rp) 194 237 269 289 EPS Gth Pre Ex (%) 25 22 13 8 Diluted EPS (Rp) 194 237 269 289 Net DPS (Rp) 137 166 188 202 BV Per Share (Rp) 845 890 934 972 PE (X) 24.3 19.9 17.5 16.3 PE Pre Ex. (X) 24.3 19.9 17.5 16.3 P/Cash Flow (X) 10.0 9.6 7.8 6.9 EV/EBITDA (X) 8.3 7.6 7.1 6.7 Net Div Yield (%) 2.9 3.5 4.0 4.3 P/Book Value (X) 5.6 5.3 5.0 4.8 Net Debt/Equity (X) 0.0 0.0 CASH CASH ROAE (%) 24.3 27.3 29.5 30.4

Earnings Rev (%): 0 0 0 Consensus EPS (Rp): 235 265 297 Other Broker Recs: B: 25 S: 0 H: 9

Source of all data on this page: Company, DBS Bank, Bloomberg Finance L.P

Premium valuation suggests high

expectations Premium valuation warrants high growth from Non-Telkomsel

business. We project Telkomsel revenue to grow below 7%

(versus 14% last year) implying that Non-Telkomsel revenue

needs to grow 20% in FY17F (versus 12% last year) to meet

consensus expectations. TLKM’s rich multiple of 9.1x adjusted

FY18F EV/EBITDA does not leave any room for disappointment

Where we differ? We see some room for disappointment to

ours and consensus’ FY17F/18F EBITDA forecasts. Voice & SMS

revenue of Telkomsel grew 4.5% in FY16 but is likely to decline

from FY17F onwards due to rising competition outside Java and

higher smartphone penetration. While 1H17 Non-Telkomsel

revenue jumped c.24% y-o-y to Rp19tn, we are not sure about

the sustainability of such growth. The growth mainly came from

sale of customer premises equipment for ICT solutions.

Potential catalyst. We see a potentially sharp slowdown in the

Telkomsel business in 2H17F with rising competition and

smartphone penetration approaching 30% plus in the non-Java

region. As Telkomsel generates 63% of its revenues from voice

and SMS services (vs 33% for EXCL and 43% for ISAT), it is

likely to be impacted more over the next 2-3 years.

Valuation:

Maintain HOLD. The counter is trading at a relatively high

adjusted Fy18F EV/EBITDA of 9.1x, with EBITDA CAGR of 7%

over FY17-19. Our DCF-based (WACC 9.1%, terminal growth

1%) TP is Rp4,800.

Key Risks to Our View:

Disruption of its strong presence outside Java. We have not

factored any network sharing between EXCL and ISAT in our

model. Any network sharing arrangement could hurt TLKM

quite badly outside the Java region where people do not have

much choice other than Telkomsel currently.

At A Glance Issued Capital (m shrs) 100,800 Mkt. Cap (Rpbn/US$m) 474,768 / 35,775 Major Shareholders (%) Govt. of Indonesia (%) 51.0

Free Float (%) 49.0 3m Avg. Daily Val (US$m) 24.0 ICB Industry : Telecommunications / Telecommunications

DBS Group Research . Equity 20 Sep 2017

Indonesia Company Guide

Telekomunikasi Indonesia Version 6 | Bloomberg: TLKM IJ | Reuters: TLKM.JK Refer to important disclosures at the end of this report

Page 15

Company Guide

Telekomunikasi Indonesia

CRITICAL DATA POINTS TO WATCH

Critical Factors

Telkomsel growth hampered by legacy decline. Telkomsel was

the key growth driver over the past few years with 14% top line

growth in FY16. Telkomsel has been able to avoid decreases in

its legacy services due to its presence outside Java. However, we

believe the industry dynamics are at a tipping point which

would drastically reduce Telkomsel’s growth in the immediate

future. The company is already witnessing steep drops in SMS

revenues while voice usage levels are also in steady decline.

Voice revenues, which have been sustained through bundling

and cluster base pricing, are unlikely to sustain at these levels in

our view, due to increasing competition outside Java and overall

drop in voice demand. As a result, we expect the Indonesian

mobile segment to expand at 6.5%, despite the strong mobile

data growth, down from 11% last year. Telkomsel generates

66% of its revenues from legacy services, compared to 37% for

EXCL and 48% for ISAT. Hence, we do not expect Telkomsel to

outperform the market like it did in previous years, despite its

strong market position.

Corporate segment to offset Telkomsel slowdown. We expect

TLKM’s corporate segment growth to remain strong in FY17

with higher revenues being booked through ICT solutions and

managed services. The corporate segment saw its external

revenues increase by 15% in FY16 while the segment’s higher

ICT solution due to increases due to a revenue jump from

Customer Premise Equipment revenue was the key contributor

to the 23% q-o-q bump in 1Q17 TLKM fixed segment revenues.

IndiHome will support overall growth, but still early days.

IndiHome added ~150k subscribers in 1Q17 though a majority

of the subscribers were upgrading from their existing fixed

broadband packages. Management expects the IndiHome

uptake to accelerate as the year progresses which should

support fixed home segment (voice, broadband, pay TV)

growth. With voice services contracting, we expect the

segment’s growth to add ~Rp1.5tr to the topline, or around

~1% to the overall TLKM’s revenue in FY17.

GSM Subscribers (m)

Data revenue

EBITDA Margin %

Net Capex (Rp tr)

EBITDA (Rptn)

Source: Company, DBS Bank

Page 16

Company Guide

Telekomunikasi Indonesia

Appendix 1: A look at company's listed history – what drives

its share price?

Market share a critical factor in share price movements for Indonesian telcos. In our critical factor analysis we have over the

past ~10 years, we have seen share price movements to follow mobile revenue share changes of telcos. This has held true for all telcos including TLKM, which derives a majority of its revenues from Telkomsel.

TLKM share price movement with Telkomsel revenue share changes

Source: Reuters, DBS Bank

50%

51%

52%

53%

54%

55%

56%

57%

58%

59%

40

60

80

100

120

140

160

Dec

06

Dec

07

Dec

08

Dec

09

Dec

10

Dec

11

Dec

12

Dec

13

Dec

14

PT Telkom Reuters Indo. Telecom Index TLKM Mkt Share

Page 17

Company Guide

Telekomunikasi Indonesia

Balance Sheet:

No exposure to foreign debt. TLKM has the strongest balance

sheet among peers because of zero exposure to foreign debt,

and the lowest gross debt to equity ratio of 0.25x. The low

leverage also means TLKM has better flexibility to acquire digital

or other businesses. TLKM's capex will be sustainable at 23-

25% of revenue, at Rp31tr in FY17. Capex will be focused on

mobile and fixed broadband investments.

Share Price Drivers:

Limited upside despite fixed line growth. Telkomsel which

accounts for ~75% of topline is under threat from voice and

SMS cannibalisation and an aggressive EXCL. The counter is

trading at a relatively high adjusted EV/EBITDA of 9.7x with an

average EBITDA CAGR of 8% over FY16-FY19. Our DCF-based

(WACC 9.15%, Terminal growth 1%) TP of Rp4,800 indicates

3% potential upside with c.3% yield.

Bear-case valuation. TLKM were to see FY16-19F EBITDA grow

at 5% versus our base case CAGR of 8% due to slower fixed

line growth coupled with 5% EBITDA CAGR at Telkomsel, our

TP will drop to Rp4100.

Bull-case valuation. If TLKM were to see FY16-19F EBITDA grow

at 11% versus our base case CAGR of 8% due to faster fixed

line growth coupled with 7% EBITDA CAGR at Telkomsel, our

TP will rise to Rp5500.

Key Risks:

EXCL’s cannot gain traction outside Java. If EXCL is not able to

gain traction outside Java, Telkomsel could potentially maintain

its voice revenue growth.

Slowdown in corporate revenues. Despite strong growth in

corporate revenues, the segment relies on new contracts in the

areas of ICT solutions and manage services. A slowdown in

new orders could potentially slow down TLKM

Company Background

TLKM Indonesia is the largest telecommunication and network

provider in Indonesia. The company offers a wide range of

network and telecommunication services, including fixed-line

connection services, cellular services, network and

interconnection services, as well as Internet and data

communication services. TLKM also operates multimedia

businesses such as content and applications, completing its

business portfolio that spans Telecommunication, Information,

Media, Edutainment and Services (TIMES).

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, DBS Bank

Page 18

Company Guide

Telekomunikasi Indonesia

Key Assumptions

FY Dec 2015A 2016A 2017F 2018F 2019F

GSM Subscribers (m) 153 175 182 189 197

Data revenue 47.8 59.0 69.6 79.1 87.6

EBITDA Margin % 50.2 51.1 52.0 52.2 52.3

Net Capex (Rp tr) 27.4 29.4 30.6 31.5 31.7

EBITDA (Rptn) 51.4 59.5 66.3 71.6 76.1

Segmental Breakdown

FY Dec 2015A 2016A 2017F 2018F 2019F

Revenues (Rpbn)

Fixed Line 7,833 7,542 7,240 6,951 6,673

Wireless Voice 37,285 38,497 37,727 36,973 36,233

Interconnection 4,290 4,151 4,027 3,906 3,789

Data/Internet & SMS 47,820 58,971 69,644 79,098 87,562

Others 5,242 7,172 8,679 10,071 11,186

Total 102,470 116,333 127,316 136,997 145,442

Income Statement (Rpbn)

FY Dec 2015A 2016A 2017F 2018F 2019F

Revenue 102,470 116,333 127,316 136,997 145,442

Cost of Goods Sold (51,055) (56,835) (61,050) (65,437) (69,376)

Gross Profit 51,415 59,498 66,266 71,560 76,066

Other Opng (Exp)/Inc (18,534) (18,532) (20,257) (21,980) (23,971)

Operating Profit 32,881 40,966 46,009 49,580 52,094

Other Non Opg (Exp)/Inc (463) (1,771) 0.0 0.0 0.0

Associates & JV Inc (2.0) 88.0 96.8 101 105

Net Interest (Exp)/Inc (1,074) (1,094) (1,037) (953) (915)

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0

Pre-tax Profit 31,342 38,189 45,069 48,729 51,284

Tax (8,025) (9,017) (10,817) (11,695) (12,308)

Minority Interest (7,828) (9,820) (10,618) (10,218) (10,108)

Preference Dividend 0.0 0.0 0.0 0.0 0.0

Net Profit 15,489 19,352 23,634 26,816 28,868

Net Profit before Except. 15,489 19,352 23,634 26,816 28,868

EBITDA 51,415 59,498 66,266 71,560 76,066

Growth

Revenue Gth (%) 14.2 13.5 9.4 7.6 6.2

EBITDA Gth (%) 12.6 15.7 11.4 8.0 6.3

Opg Profit Gth (%) 15.2 24.6 12.3 7.8 5.1

Net Profit Gth (Pre-ex) (%) 7.0 24.9 22.1 13.5 7.7

Margins & Ratio

Gross Margins (%) 50.2 51.1 52.0 52.2 52.3

Opg Profit Margin (%) 32.1 35.2 36.1 36.2 35.8

Net Profit Margin (%) 15.1 16.6 18.6 19.6 19.8

ROAE (%) 21.7 24.3 27.3 29.5 30.4

ROA (%) 10.1 11.2 12.6 13.2 13.1

ROCE (%) 19.4 22.3 22.9 22.5 21.8

Div Payout Ratio (%) 61.0 70.5 70.0 70.0 70.0

Net Interest Cover (x) 30.6 37.4 44.4 52.1 56.9

Source: Company, DBS Bank

Voice starting to decline from FY17

Topline revised upward due to fixed-line business

Page 19

Company Guide

Telekomunikasi Indonesia

Quarterly / Interim Income Statement (Rpbn)

FY Dec 1Q2016 2Q2016 3Q2016 4Q2016 1Q2017

Revenue 27,542 28,912 29,734 30,145 31,022

Cost of Goods Sold (12,887) (14,772) (14,151) (15,025) (14,213)

Gross Profit 14,655 14,140 15,583 15,120 16,809

Other Oper. (Exp)/Inc (4,405) (4,334) (4,618) (5,175) (4,773)

Operating Profit 10,250 9,806 10,965 9,945 12,036

Other Non Opg (Exp)/Inc (663) 520 (557) (983) 472

Associates & JV Inc 0.0 0.0 0.0 0.0 0.0

Net Interest (Exp)/Inc (271) (144) (289) (390) (184)

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0

Pre-tax Profit 9,316 10,182 10,119 8,572 12,324

Tax (2,423) (2,412) (2,613) (1,569) (2,948)

Minority Interest (2,307) (2,430) (2,700) (2,383) (2,688)

Net Profit 4,586 5,340 4,806 4,620 6,688

Net profit bef Except. 4,586 5,340 4,806 4,620 6,688

EBITDA 14,655 14,140 15,583 15,120 16,809

Growth

Revenue Gth (%) 3.0 5.0 2.8 1.4 2.9

EBITDA Gth (%) 2.2 (3.5) 10.2 (3.0) 11.2

Opg Profit Gth (%) 10.1 (4.3) 11.8 (9.3) 21.0

Net Profit Gth (Pre-ex) (%) 16.3 16.4 (10.0) (3.9) 44.8

Margins

Gross Margins (%) 53.2 48.9 52.4 50.2 54.2

Opg Profit Margins (%) 37.2 33.9 36.9 33.0 38.8

Net Profit Margins (%) 16.7 18.5 16.2 15.3 21.6

Balance Sheet (Rpbn)

FY Dec 2015A 2016A 2017F 2018F 2019F

Net Fixed Assets 103,700 114,498 124,882 134,412 142,147

Invts in Associates & JVs 0.0 0.0 0.0 0.0 0.0

Other LT Assets 14,561 17,412 17,469 17,570 17,674

Cash & ST Invts 30,935 31,238 30,195 35,871 47,181

Inventory 528 584 754 809 857

Debtors 7,517 7,363 9,247 9,950 7,272

Other Current Assets 8,932 8,516 12,282 12,748 13,164

Total Assets 166,173 179,611 194,830 211,359 228,295

ST Debt 4,444 5,432 5,877 5,877 5,877

Creditor 13,994 13,518 17,193 18,428 20,813

Other Current Liab 16,975 20,812 17,277 18,445 19,542

LT Debt 30,168 26,367 25,922 25,477 25,032

Other LT Liabilities 7,164 7,938 7,938 7,938 7,938

Shareholder’s Equity 75,136 84,384 88,845 93,198 96,989

Minority Interests 18,292 21,160 31,778 41,996 52,104

Total Cap. & Liab. 166,173 179,611 194,830 211,359 228,295

Non-Cash Wkg. Capital (13,992) (17,867) (12,186) (13,366) (19,061)

Net Cash/(Debt) (3,677) (561) (1,604) 4,517 16,271

Debtors Turn (avg days) 24.9 23.3 23.8 25.6 21.6

Creditors Turn (avg days) 144.9 131.1 137.4 149.6 157.7

Inventory Turn (avg days) 5.6 5.3 6.0 6.6 6.7

Asset Turnover (x) 0.7 0.7 0.7 0.7 0.7

Current Ratio (x) 1.4 1.2 1.3 1.4 1.5

Quick Ratio (x) 1.1 1.0 1.0 1.1 1.2

Net Debt/Equity (X) 0.0 0.0 0.0 CASH CASH

Net Debt/Equity ex MI (X) 0.0 0.0 0.0 CASH CASH

Capex to Debt (%) 79.2 92.2 96.4 100.5 102.6

Z-Score (X) 5.7 5.8 5.8 5.7 5.5

Source: Company, DBS Bank

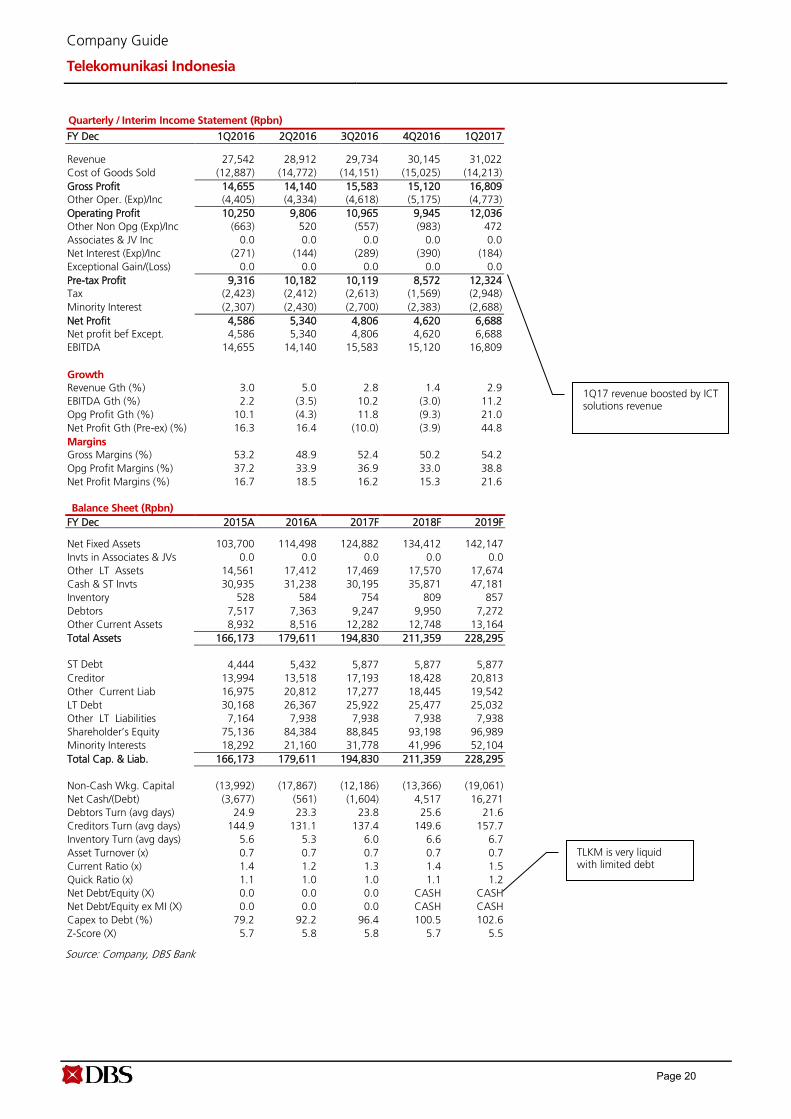

1Q17 revenue boosted by ICT solutions revenue

TLKM is very liquid with limited debt

Page 20

Company Guide

Telekomunikasi Indonesia

Cash Flow Statement (Rpbn)

FY Dec 2015A 2016A 2017F 2018F 2019F

Pre-Tax Profit 31,342 38,189 45,069 48,729 51,284

Dep. & Amort. 18,534 18,532 20,257 21,980 23,971

Tax Paid (9,509) (14,000) (11,067) (11,475) (12,155)

Assoc. & JV Inc/(loss) 2.00 (88.0) (96.8) (101) (105)

Chg in Wkg.Cap. 3,811 7,297 (5,432) 961 5,541

Other Operating CF (511) (2,699) 0.0 0.0 0.0

Net Operating CF 43,669 47,231 48,731 60,094 68,537

Capital Exp.(net) (27,425) (29,330) (30,641) (31,509) (31,706)

Other Invts.(net) (61.0) 1,307 (1,307) 0.0 0.0

Invts in Assoc. & JV 0.0 0.0 0.0 0.0 0.0

Div from Assoc & JV 0.0 0.0 0.0 0.0 0.0

Other Investing CF 65.0 466 0.0 0.0 0.0

Net Investing CF (27,421) (27,557) (31,948) (31,509) (31,706)

Div Paid (10,427) (10,555) (19,173) (22,463) (25,077)

Chg in Gross Debt 11,778 (3,734) 0.0 (445) (445)

Capital Issues 68.0 3,259 0.0 0.0 0.0

Other Financing CF (7,222) (6,994) 0.0 0.0 0.0

Net Financing CF (5,803) (18,024) (19,173) (22,908) (25,522)

Currency Adjustments 0.0 0.0 0.0 0.0 0.0

Chg in Cash 10,445 1,650 (2,390) 5,676 11,309

Opg CFPS (Rp) 399 400 543 592 631

Free CFPS (Rp) 163 179 181 286 369

Source: Company, DBS Bank

Target Price & Ratings History

Source: DBS Bank

Analyst: Sachin MITTAL

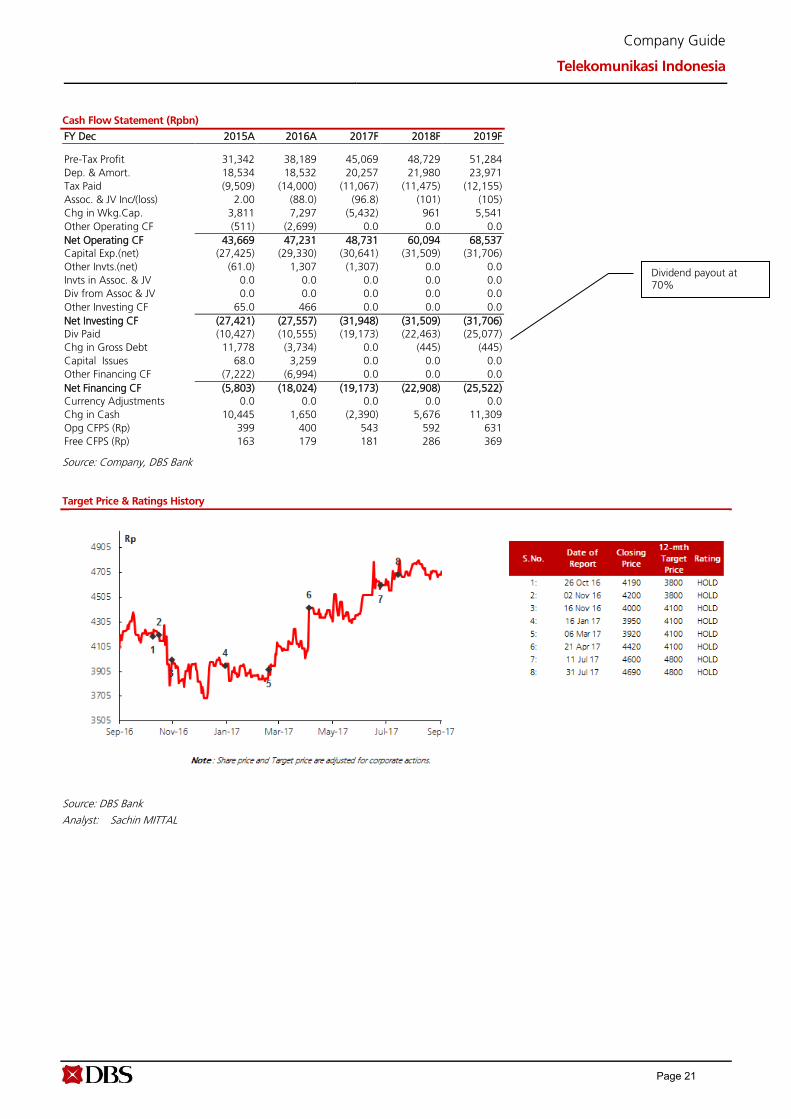

Dividend payout at 70%

Page 21

ed: CK / sa:MA, PY

HOLD (Downgrade from BUY)

Last Traded Price ( 18 Sep 2017): Rp3,970 (JCI : 5,884.60)

Price Target 12-mth: Rp3,900 (-2% downside) (Prev Rp4,000)

Analyst Sachin MITTAL +65 6682 3699 [email protected]

What’s New Limited upside due to recent price gains and tightening

competition in and out of Java

Market seems to be overly optimistic about market

share gains ex-Java

Downgrade to HOLD with a lower TP of Rp3,900

Price Relative

Forecasts and Valuation FY Dec (Rp m) 2016A 2017F 2018F 2019F

Revenue 21,341 22,716 24,365 25,968 EBITDA 8,058 8,404 9,345 10,044 Pre-tax Profit 186 (36.6) 628 1,180 Net Profit 375 (27.4) 471 885 Net Pft (Pre Ex.) 375 (27.4) 471 885 Net Pft Gth (Pre-ex) (%) nm nm nm 87.9 EPS (Rp) 35.1 (2.6) 44.1 82.8 EPS Pre Ex. (Rp) 35.1 (2.6) 44.1 82.8 EPS Gth Pre Ex (%) (1,581) (107) (1,817) 88 Diluted EPS (Rp) 35.1 (2.6) 44.1 82.8 Net DPS (Rp) 21.1 0.0 0.0 0.0 BV Per Share (Rp) 1,984 1,961 2,005 2,088 PE (X) 113.1 nm 90.1 48.0 PE Pre Ex. (X) 113.1 nm 90.1 48.0 P/Cash Flow (X) 5.6 6.2 5.1 4.8 EV/EBITDA (X) 6.8 6.6 5.8 5.1 Net Div Yield (%) 0.5 0.0 0.0 0.0 P/Book Value (X) 2.0 2.0 2.0 1.9 Net Debt/Equity (X) 0.6 0.6 0.5 0.4 ROAE (%) 2.1 (0.1) 2.2 4.0

Earnings Rev (%): (127) 3 (1) Consensus EPS (Rp): 30.3 103 176 Other Broker Recs: B: 21 S: 1 H: 8

Source of all data on this page: Company, DBS Bank, Bloomberg Finance L.P

Limited upside after recent share price surge

Take profit as expectations remain high. The counter has

appreciated ~70% since the beginning of the year and offers

limited upside amid tightening competitive dynamics in and out

of Java. Our checks indicate that Telkomsel is offering data-only

packages in Java at over 55% discount to its original price and

reduced voice prices by ~30%-50% in certain ex-Java regions.

Where we differ? Our FY17F/18F EBITDA estimates are 2%/3%

below consensus estimates. The market appears to be optimistic

about EXCL’s ex-Java expansions, with recent market share

gains underestimating the possibility of Telkomsel’s retaliation.

EXCL may struggle to meet consensus EBITDA of Rp4.6tr in

2H17F vs only Rp3.9tr EBITDA in 1H17. We do think that

consensus FY18F EBITDA of Rp9.7tr is too high – factoring over

8% revenue growth and a 100bps EBITDA margin expansion.

Potential catalyst – changes in revenue market shares over the

next 2-3 quarters. Changes in the composition of revenue

market shares between Telkomsel and EXCL would provide cues

on ex-Java competition and ex-Java execution by EXCL.

Valuation:

HOLD with a revised TP of Rp 3,900. We lower our DCF-based

(WACC 9.4%, Terminal growth 1%) TP to Rp3,900 from

Rp4,000 previously. At the current share price level, the

counter is overvalued by 2%.

Key Risks to Our View:

Change in revenue share gains. If EXCL continues to make

gains at the expense of Telkomsel and Indosat, leading to

FY16-19 EBITDA CAGR of 12% vs our base-case CAGR of 7%,

our TP could rise to Rp4,900. Alternatively, If EXCL were to

register FY16-19 EBITDA CAGR of just 4% due to an

aggressive Telkomsel, our TP could drop to Rp3,250.

At A Glance

Issued Capital (m shrs) 10,688

Mkt. Cap (Rpbn/US$m) 42,431 / 3,197

Major Shareholders (%)

Axiata Group 66.6

Elisalat Intl 13.3

Parkmix Ltd 13.3

Free Float (%) 20.1

3m Avg. Daily Val (US$m) 1.6

ICB Industry : Telecommunications / Mobile Telecommunications

DBS Group Research . Equity 20 Sep 2017

Indonesia Company Guide

XL Axiata Version 6 | Bloomberg: EXCL IJ | Reuters: EXCL.JK Refer to important disclosures at the end of this report

Page 22

Company Guide

XL Axiata

CRITICAL DATA POINTS TO WATCH

Critical Factors

Revenue share gains likely to halt as Telkomsel fires back. EXCL

made steady gains in market share over the past two quarters,

snatching nearly 800bps of revenue market share from

Telkomsel. However, our industry checks indicate that Telkomsel

is retaliating against EXCL outside Java, slashing voice prices by

~30%-60% to oust EXCL as the cheaper provider of legacy

services outside Java. Intensifying competition on the data front

in Java, which remains a stronghold of EXCL, could also lead to

an increase in subscriber churn. This could reduce the pace of

future revenue share gains by the operator. Accordingly, we

revise down our FY17 revenue growth forecasts for EXCL to

6.4% from 8.6% and curtail our EBITDA growth forecasts for

FY17 to 5.7% from 8.1%.

Declining data yields and a data savvy subscriber base may

reduce the pace of growth in data revenues. EXCL boasts a

data-savvy subscriber base with a subscriber on average using

~1.9GB of data per month vs. 900MB at ISAT and Telkomsel.

Data usage also grew at 140% from 2Q16 to 2Q17 vs. ~100%

growth in the industry. While a data heavy subscriber base

cushions potential declines in legacy revenues, EXCL may find it

difficult to post above-industry average growth in revenues if

data yields continue to decline. With data usage already at high

levels, subscribers may remain relatively inelastic to changes in

data pricing, thereby limiting usage growth. Limited usage

growth combined with declining data yields could reduce the

pace of growth in data revenues of EXCL in the future.

Data usage already remains high

Source: Company, DBS Bank

Improving EBITDA margin in FY18. Tower rental renewals, lower

expenses from the managed services contract and stable

interconnection costs are expected to improve EBITDA margin in

FY18. EXCL is expecting up to 50% savings on each tower lease

renewal, with a large chunk of towers being renewed over the

next three years. Managed service contract expenses are also

expected to come down due to lower revenue-sharing going

forward. In addition, interconnection costs are expected to

remain stable despite expansion outside Java due to higher VoIP

use. We believe EXCL would be able to expand its FY18 EBITDA

margin by 60bps from FY16 levels.

Subscribers (m)

ARPU (Rp K)

EBITDA margins (%)

Capex (Rp tn)

EBITDA (Rpbn)

Source: Company, DBS Bank

Page 23

Company Guide

XL Axiata

Appendix 1: A look at Company's listed history – what drives its share price?

Revenue share is a critical factor in share price movements for XL. In our critical factor analysis over the past ~10 years, we have seen share price movements to follow mobile market share changes of telcos. This was clearly observable when revenue share dropped in FY15.

Source : Reuters, DBS Bank

15%

16%

17%

18%

19%

20%

21%

22%

23%

24%

25%

30

80

130

180

230

280

330

Dec 06 Dec 07 Dec 08 Dec 09 Dec 10 Dec 11 Dec 12 Dec 13 Dec 14

XL Axiata Reuters Indo. Telecom Index XL Mkt Share

Page 24

Company Guide

XL Axiata

Balance Sheet:

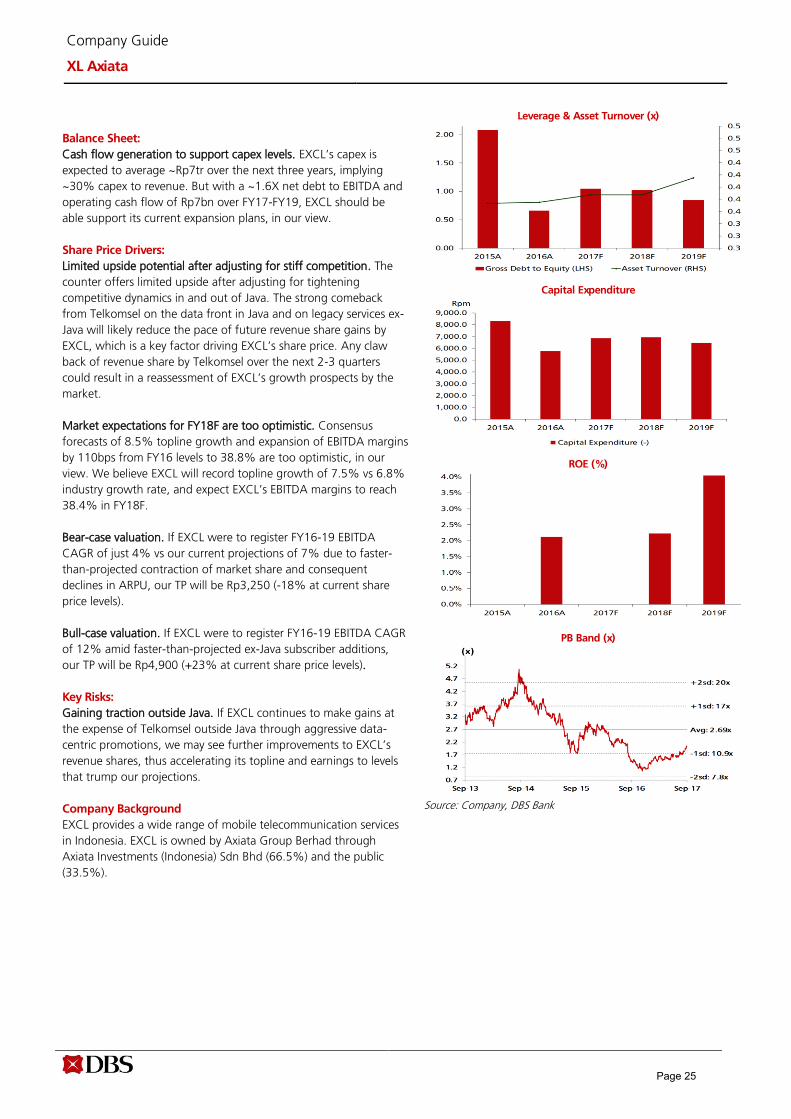

Cash flow generation to support capex levels. EXCL’s capex is

expected to average ~Rp7tr over the next three years, implying

~30% capex to revenue. But with a ~1.6X net debt to EBITDA and

operating cash flow of Rp7bn over FY17-FY19, EXCL should be

able support its current expansion plans, in our view.

Share Price Drivers:

Limited upside potential after adjusting for stiff competition. The

counter offers limited upside after adjusting for tightening

competitive dynamics in and out of Java. The strong comeback

from Telkomsel on the data front in Java and on legacy services ex-

Java will likely reduce the pace of future revenue share gains by

EXCL, which is a key factor driving EXCL’s share price. Any claw

back of revenue share by Telkomsel over the next 2-3 quarters

could result in a reassessment of EXCL’s growth prospects by the

market.

Market expectations for FY18F are too optimistic. Consensus

forecasts of 8.5% topline growth and expansion of EBITDA margins

by 110bps from FY16 levels to 38.8% are too optimistic, in our

view. We believe EXCL will record topline growth of 7.5% vs 6.8%

industry growth rate, and expect EXCL’s EBITDA margins to reach

38.4% in FY18F.

Bear-case valuation. If EXCL were to register FY16-19 EBITDA

CAGR of just 4% vs our current projections of 7% due to faster-

than-projected contraction of market share and consequent

declines in ARPU, our TP will be Rp3,250 (-18% at current share

price levels).

Bull-case valuation. If EXCL were to register FY16-19 EBITDA CAGR

of 12% amid faster-than-projected ex-Java subscriber additions,

our TP will be Rp4,900 (+23% at current share price levels).

Key Risks:

Gaining traction outside Java. If EXCL continues to make gains at

the expense of Telkomsel outside Java through aggressive data-

centric promotions, we may see further improvements to EXCL’s

revenue shares, thus accelerating its topline and earnings to levels

that trump our projections.

Company Background

EXCL provides a wide range of mobile telecommunication services

in Indonesia. EXCL is owned by Axiata Group Berhad through

Axiata Investments (Indonesia) Sdn Bhd (66.5%) and the public

(33.5%).

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

PB Band (x)

Source: Company, DBS Bank

Page 25

Company Guide

XL Axiata

Key Assumptions

FY Dec 2015A 2016A 2017F 2018F 2019F

Subscribers (m) 41.5 45.9 56.1 60.3 64.5

ARPU (Rp K) 34.0 35.0 34.2 34.8 34.8

EBITDA margins (%) 36.7 37.8 37.0 38.4 38.7

Capex (Rp tn) 8.30 5.80 6.90 6.90 6.40

EBITDA (Rpbn) 8,393 8,058 8,404 9,345 10,044

Segmental Breakdown

FY Dec 2015A 2016A 2017F 2018F 2019F Revenues (Rpbn)

GSM Revenue 19,454 18,588 18,866 20,378 21,840

GSM interconnect 2,308 1,744 3,000 3,120 3,245

Other GSM 0.0 0.0 0.0 0.0 0.0

Others 1,115 1,009 850 867 883

Total 22,876 21,341 22,716 24,365 25,968

Income Statement (Rpbn)

FY Dec 2015A 2016A 2017F 2018F 2019F

Revenue 22,876 21,341 22,716 24,365 25,968

Cost of Goods Sold (2,321) (1,926) (2,953) (2,924) (3,064)

Gross Profit 20,555 19,415 19,763 21,441 22,904

Other Opng (Exp)/Inc (19,298) (19,403) (18,200) (19,324) (20,445)

Operating Profit 1,258 12.2 1,562 2,117 2,459

Other Non Opg (Exp)/Inc (808) 1,706 0.0 0.0 0.0

Associates & JV Inc 0.0 0.0 0.0 0.0 0.0

Net Interest (Exp)/Inc (1,080) (1,533) (1,599) (1,489) (1,279)

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0

Pre-tax Profit (631) 186 (36.6) 628 1,180

Tax 605 190 9.10 (157) (295)

Minority Interest 0.0 0.0 0.0 0.0 0.0

Preference Dividend 0.0 0.0 0.0 0.0 0.0

Net Profit (25.3) 375 (27.4) 471 885

Net Profit before Except. (25.3) 375 (27.4) 471 885

EBITDA 8,393 8,058 8,404 9,345 10,044

Growth

Revenue Gth (%) (1.0) (6.7) 6.4 7.3 6.6

EBITDA Gth (%) 2.8 (4.0) 4.3 11.2 7.5

Opg Profit Gth (%) (6.1) (99.0) 12,683.1 35.5 16.1

Net Profit Gth (Pre-ex) (%) 97.9 nm nm nm 87.9

Margins & Ratio

Gross Margins (%) 89.9 91.0 87.0 88.0 88.2

Opg Profit Margin (%) 5.5 0.1 6.9 8.7 9.5

Net Profit Margin (%) (0.1) 1.8 (0.1) 1.9 3.4

ROAE (%) (0.2) 2.1 (0.1) 2.2 4.0

ROA (%) 0.0 0.7 0.0 0.7 1.4

ROCE (%) 2.5 0.0 3.2 3.0 3.6

Div Payout Ratio (%) N/A 60.0 N/A 0.0 0.0

Net Interest Cover (x) 1.2 0.0 1.0 1.4 1.9

Source: Company, DBS Bank

Higher capex on spectrum assets

Revenue growth to slow down amid tightening ex-Java competition

Page 26

Company Guide

XL Axiata

Quarterly / Interim Income Statement (Rpbn)

FY Dec 2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

Revenue 5,237 5,229 5,258 5,266 5,668

Cost of Goods Sold (418) (526) (578) (659) (630)

Gross Profit 4,820 4,704 4,680 4,607 5,037

Other Oper. (Exp)/Inc (4,844) (4,524) (5,143) (4,438) (4,667)

Operating Profit (24.2) 179 (463) 169 371

Other Non Opg (Exp)/Inc 413 108 718 102 78.7

Associates & JV Inc

Net Interest (Exp)/Inc (415) (378) (195) (344) (351)

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0

Pre-tax Profit (26.1) (90.6) 60.8 (72.6) 98.3

Tax 81.6 25.6 155 119 (1.6)

Minority Interest 0.0 0.0 0.0 0.0 0.0

Net Profit 55.5 (65.0) 216 46.5 96.6

Net profit bef Except. 55.5 (65.0) 216 46.5 96.6

EBITDA 2,065 1,979 1,823 1,848 2,073

Growth

Revenue Gth (%) (6.7) (0.2) 0.6 0.1 7.6

EBITDA Gth (%) (5.8) (4.2) (7.9) 1.4 12.1

Opg Profit Gth (%) (107.6) (841.7) (358.0) (136.6) 119.3

Net Profit Gth (Pre-ex) (%) (67.2) (217.2) (431.9) (78.5) 107.8

Margins

Gross Margins (%) 92.0 89.9 89.0 87.5 88.9

Opg Profit Margins (%) (0.5) 3.4 (8.8) 3.2 6.5

Net Profit Margins (%) 1.1 (1.2) 4.1 0.9 1.7

Balance Sheet (Rpbn)

FY Dec 2015A 2016A 2017F 2018F 2019F

Net Fixed Assets 33,427 33,183 33,201 32,919 31,774

Invts in Associates & JVs 0.0 0.0 0.0 0.0 0.0

Other LT Assets 15,266 14,907 14,907 14,907 14,907

Cash & ST Invts 3,312 1,400 9,087 10,394 9,707

Inventory 79.0 161 41.3 44.0 46.7

Debtors 898 637 545 585 623

Other Current Assets 5,863 4,609 4,609 4,609 4,609

Total Assets 58,844 54,896 62,391 63,458 61,667

ST Debt 4,290 3,973 3,973 3,973 3,973

Creditor 5,257 6,503 5,679 6,048 6,430

Other Current Liab 6,201 4,002 4,597 4,823 4,766

LT Debt 25,054 10,024 18,000 18,000 15,000

Other LT Liabilities 3,950 9,186 9,186 9,186 9,186

Shareholder’s Equity 14,092 21,209 20,957 21,428 22,312

Minority Interests 0.0 0.0 0.0 0.0 0.0

Total Cap. & Liab. 58,844 54,896 62,391 63,458 61,667

Non-Cash Wkg. Capital (4,619) (5,098) (5,080) (5,633) (5,916)

Net Cash/(Debt) (26,032) (12,597) (12,885) (11,578) (9,266)

Debtors Turn (avg days) 16.2 13.1 9.5 8.5 8.5

Creditors Turn (avg days) (367.8) (350.7) (571.7) (497.3) (503.7)

Inventory Turn (avg days) (5.9) (7.2) (9.5) (3.6) (3.7)

Asset Turnover (x) 0.4 0.4 0.4 0.4 0.4

Current Ratio (x) 0.6 0.5 1.0 1.1 1.0

Quick Ratio (x) 0.3 0.1 0.7 0.7 0.7

Net Debt/Equity (X) 1.8 0.6 0.6 0.5 0.4

Net Debt/Equity ex MI (X) 1.8 0.6 0.6 0.5 0.4

Capex to Debt (%) 28.3 41.2 31.2 31.6 33.9

Z-Score (X) 1.0 1.1 1.2 1.2 1.3

Source: Company, DBS Bank

Declining network costs support growth in EBITDA

Page 27

Company Guide

XL Axiata

Cash Flow Statement (Rpbn)

FY Dec 2015A 2016A 2017F 2018F 2019F

Pre-Tax Profit (631) 186 (36.6) 628 1,180

Dep. & Amort. 7,135 8,046 6,842 7,228 7,585

Tax Paid (15.5) 361 (167) (73.9) (226)

Assoc. & JV Inc/(loss) 0.0 0.0 0.0 0.0 0.0

Chg in Wkg.Cap. 513 (1,001) 158 470 214

Other Operating CF 0.0 0.0 0.0 0.0 0.0

Net Operating CF 7,002 7,591 6,797 8,252 8,753

Capital Exp.(net) (8,317) (5,762) (6,860) (6,945) (6,440)

Other Invts.(net) 0.0 1,054 0.0 0.0 0.0

Invts in Assoc. & JV 0.0 0.0 0.0 0.0 0.0

Div from Assoc & JV 0.0 0.0 0.0 0.0 0.0

Other Investing CF 0.0 0.0 0.0 0.0 0.0

Net Investing CF (8,317) (4,708) (6,860) (6,945) (6,440)

Div Paid 0.0 0.0 (225) 0.0 0.0

Chg in Gross Debt (2,360) (13,348) 7,976 0.0 (3,000)

Capital Issues 35.8 6,721 0.0 0.0 0.0

Other Financing CF 0.0 1,831 0.0 0.0 0.0

Net Financing CF (2,325) (4,796) 7,751 0.0 (3,000)

Currency Adjustments 0.0 0.0 0.0 0.0 0.0

Chg in Cash (3,639) (1,912) 7,688 1,307 (687)

Opg CFPS (Rp) 607 804 621 728 799

Free CFPS (Rp) (123) 171 (5.9) 122 216

Source: Company, DBS Bank

Target Price & Ratings History

Source: DBS Bank

Analyst: Sachin MITTAL

Strong operating cash flows to support expansions

Page 28

Industry Focus

Telecom Sector

DBS Bank recommendations are based an Absolute Total Return* Rating system, defined as follows:

STRONG BUY (>20% total return over the next 3 months, with identifiable share price catalysts within this time frame)

BUY (>15% total return over the next 12 months for small caps, >10% for large caps)

HOLD (-10% to +15% total return over the next 12 months for small caps, -10% to +10% for large caps)

FULLY VALUED (negative total return i.e. > -10% over the next 12 months)

SELL (negative total return of > -20% over the next 3 months, with identifiable catalysts within this time frame)

Share price appreciation + dividends

Completed Date: 20 Sep 2017 07:36 (SGT) Dissemination Date: 20 Sep 2017 08:00 (SGT)

Sources for all charts and tables are DBS Bank unless otherwise specified.

GENERAL DISCLOSURE/DISCLAIMER

This report is prepared by DBS Bank Ltd. This report is solely intended for the clients of DBS Bank Ltd, its respective connected and associated

corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii)

redistributed without the prior written consent of DBS Bank Ltd.

The research set out in this report is based on information obtained from sources believed to be reliable, but we (which collectively refers to DBS

Bank Ltd, its respective connected and associated corporations, affiliates and their respective directors, officers, employees and agents (collectively,

the “DBS Group”) have not conducted due diligence on any of the companies, verified any information or sources or taken into account any other

factors which we may consider to be relevant or appropriate in preparing the research. Accordingly, we do not make any representation or

warranty as to the accuracy, completeness or correctness of the research set out in this report. Opinions expressed are subject to change without

notice. This research is prepared for general circulation. Any recommendation contained in this document does not have regard to the specific

investment objectives, financial situation and the particular needs of any specific addressee. This document is for the information of addressees

only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate independent legal or financial

advice. The DBS Group accepts no liability whatsoever for any direct, indirect and/or consequential loss (including any claims for loss of profit)

arising from any use of and/or reliance upon this document and/or further communication given in relation to this document. This document is not

to be construed as an offer or a solicitation of an offer to buy or sell any securities. The DBS Group, along with its affiliates and/or persons

associated with any of them may from time to time have interests in the securities mentioned in this document. The DBS Group, may have

positions in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and

other banking services for these companies.

Any valuations, opinions, estimates, forecasts, ratings or risk assessments herein constitutes a judgment as of the date of this report, and there can

be no assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk assessments.

The information in this document is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed, it may

not contain all material information concerning the company (or companies) referred to in this report and the DBS Group is under no obligation to

update the information in this report.

This publication has not been reviewed or authorized by any regulatory authority in Singapore, Hong Kong or elsewhere. There is no planned

schedule or frequency for updating research publication relating to any issuer.

The valuations, opinions, estimates, forecasts, ratings or risk assessments described in this report were based upon a number of estimates and

assumptions and are inherently subject to significant uncertainties and contingencies. It can be expected that one or more of the estimates on

which the valuations, opinions, estimates, forecasts, ratings or risk assessments were based will not materialize or will vary significantly from actual

results. Therefore, the inclusion of the valuations, opinions, estimates, forecasts, ratings or risk assessments described herein IS NOT TO BE RELIED

UPON as a representation and/or warranty by the DBS Group (and/or any persons associated with the aforesaid entities), that:

(a) such valuations, opinions, estimates, forecasts, ratings or risk assessments or their underlying assumptions will be achieved, and

(b) there is any assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk

assessments stated therein.

Page 29

Industry Focus

Telecom Sector

Please contact the primary analyst for valuation methodologies and assumptions associated with the covered companies or price targets.

Any assumptions made in this report that refers to commodities, are for the purposes of making forecasts for the company (or companies)

mentioned herein. They are not to be construed as recommendations to trade in the physical commodity or in the futures contract relating to the

commodity referred to in this report.

DBSVUSA, a US-registered broker-dealer, does not have its own investment banking or research department, has not participated in any public

offering of securities as a manager or co-manager or in any other investment banking transaction in the past twelve months and does not engage

in market-making.

ANALYST CERTIFICATION

The research analyst(s) primarily responsible for the content of this research report, in part or in whole, certifies that the views about the

companies and their securities expressed in this report accurately reflect his/her personal views. The analyst(s) also certifies that no part of his/her

compensation was, is, or will be, directly or indirectly, related to specific recommendations or views expressed in the report. The research analyst (s)

primarily responsible for the content of this research report, in part or in whole, certifies that he or his associate1 does not serve as an officer of the

issuer or the new listing applicant (which includes in the case of a real estate investment trust, an officer of the management company of the real

estate investment trust; and in the case of any other entity, an officer or its equivalent counterparty of the entity who is responsible for the

management of the issuer or the new listing applicant) and the research analyst(s) primarily responsible for the content of this research report or

his associate does not have financial interests2 in relation to an issuer or a new listing applicant that the analyst reviews. DBS Group has

procedures in place to eliminate, avoid and manage any potential conflicts of interests that may arise in connection with the production of

research reports. The research analyst(s) responsible for this report operates as part of a separate and independent team to the investment

banking function of the DBS Group and procedures are in place to ensure that confidential information held by either the research or investment

banking function is handled appropriately. There is no direct link of DBS Group's compensation to any specific investment banking function of the

DBS Group.

COMPANY-SPECIFIC / REGULATORY DISCLOSURES

1. DBS Bank Ltd, DBS HK, DBS Vickers Securities (Singapore) Pte Ltd (''DBSVS''), DBSV HK or their subsidiaries and/or other affiliates have a

proprietary positions in the China Mobile, China Telecom, China Unicom, SmarTone, Hutchison Telecom, HKT Trust, M1, StarHub,

Advanced Info Service, Total Access Communication recommended in this report as of 31 Aug 2017.

2. Neither DBS Bank Ltd, DBS HK nor DBSV HK market makes in equity securities of the issuer(s) or company(ies) mentioned in this Research

Report.

3. DBS Bank Ltd, DBS HK, DBSVS, DBSV HK, their subsidiaries and/or other affiliates have a net long position exceeding 0.5% of the total issued

share capital in M1 recommended in this report as of 31 Aug 2017.

Compensation for investment banking services:

4. DBS Bank Ltd, DBS HK, DBSVS, DBSV HK, their subsidiaries and/or other affiliates of DBSVUSA have received compensation, within the past

12 months for investment banking services from StarHub, Indosat, XL Axiata, PT Sarana Menara Nusantara, Tower Bersama Infrastructure

as of 31 Aug 2017.

5. DBS Bank Ltd, DBS HK, DBSVS, their subsidiaries and/or other affiliates of DBSVUSA have managed or co-managed a public offering of

securities for from StarHub, Indosat, XL Axiata, PT Sarana Menara Nusantara, Tower Bersama Infrastructure as of 31 Aug 2017.

6. DBSVUSA does not have its own investment banking or research department, nor has it participated in any public offering of securities as a

manager or co-manager or in any other investment banking transaction in the past twelve months. Any US persons wishing to obtain further

information, including any clarification on disclosures in this disclaimer, or to effect a transaction in any security discussed in this document

should contact DBSVUSA exclusively.

1 An associate is defined as (i) the spouse, or any minor child (natural or adopted) or minor step-child, of the analyst; (ii) the trustee of a trust of which the analyst, his spouse, minor child (natural or adopted) or minor step-child, is a beneficiary or discretionary object; or (iii) another person accustomed or obliged to act in accordance with the directions or instructions of the analyst.

2 Financial interest is defined as interests that are commonly known financial interest, such as investment in the securities in respect of an issuer or a new listing applicant, or financial accommodation arrangement between the issuer or the new listing applicant and the firm or analysis. This term does not include commercial lending conducted at arm's length, or investments in any collective investment scheme other than an issuer or new listing applicant notwithstanding the fact that the scheme has investments in securities in respect of an issuer or a new listing applicant.

Page 30

Industry Focus

Telecom Sector

Directorship/trustee interests

7. Nihal Vijaya Devadas Kaviratne CBE, a member of DBS Group Holdings Board of Directors, is a Director of Starhub as of 30 Jun 2017.

Disclosure of previous investment recommendation produced:

8. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd (''DBSVS''), their subsidiaries and/or other affiliates may have published other

investment recommendations in respect of the same securities / instruments recommended in this research report during the preceding 12

months. Please contact the primary analyst listed in the first page of this report to view previous investment recommendations published by

DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd (''DBSVS''), their subsidiaries and/or other affiliates in the preceding 12 months.

RESTRICTIONS ON DISTRIBUTION

General This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Australia This report is being distributed in Australia by DBS Bank Ltd. (“DBS”) or DBS Vickers Securities (Singapore) Pte Ltd (“DBSVS”). DBS holds Australian Financial Services Licence no. 475946.

DBSVS is exempted from the requirement to hold an Australian Financial Services Licence under the Corporation Act 2001 (“CA”) in respect of financial services provided to the recipients. DBSVS is regulated by the Monetary Authority of Singapore under the laws of Singapore, which differ from Australian laws.

Distribution of this report is intended only for “wholesale investors” within the meaning of the CA.

Hong Kong This report has been prepared by a person(s) who is not licensed by the Hong Kong Securities and Futures Commission to carry on the regulated activity of advising on securities in Hong Kong pursuant to the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong). This report is being distributed in Hong Kong and is attributable to DBS Vickers Hong Kong Limited, a licensed corporation licensed by the Hong Kong Securities and Futures Commission to carry on the regulated activity of advising on securities pursuant to the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong).

For any query regarding the materials herein, please contact Paul Yong (CE. No. ASE988) at [email protected].

Indonesia This report is being distributed in Indonesia by PT DBS Vickers Sekuritas Indonesia.

Malaysia This report is distributed in Malaysia by AllianceDBS Research Sdn Bhd ("ADBSR"). Recipients of this report, received from ADBSR are to contact the undersigned at 603-2604 3333 in respect of any matters arising from or in connection with this report. In addition to the General Disclosure/Disclaimer found at the preceding page, recipients of this report are advised that ADBSR (the preparer of this report), its holding company Alliance Investment Bank Berhad, their respective connected and associated corporations, affiliates, their directors, officers, employees, agents and parties related or associated with any of them may have positions in, and may effect transactions in the securities mentioned herein and may also perform or seek to perform broking, investment banking/corporate advisory and other services for the subject companies. They may also have received compensation and/or seek to obtain compensation for broking, investment banking/corporate advisory and other services from the subject companies.

Wong Ming Tek, Executive Director, ADBSR