Embed Size (px)

Citation preview

Investor Fact Sheet

Unit Linked Insurance Plans - Individuals February, 2012

A Joint Venture of

Monthly Market Report February, 2012 Economy

Q3 FY-12 GDP at 6.1 percentage Q3FY-12 real GDP growth came at 6.1 percentage y-o-y due to continued slow growth on the manufacturing side. Farm sector posted 2.7 percentage growth, good enough considering the high base (11 percentage in Q3 FY-11). The manufacturing sector, one of the key drivers of the economy, grew 0.4 percentage. Mining contracted 3.1 percentage due to regulatory and environmental hurdles. While electricity, gas and water supply grew at a robust 9 percentage, construction activity also picked up during the quarter, growing at a healthy 7.2 percentage. Services sector growth at 8.9 percentage y-o-y although relatively lower than previous quarters, remains the axle around which the economy can achieve 6 percentage+ overall growth. Notably, among services, growth in the finance and insurance sectors has moderated to 9.0 percentage y-o-y against 10.5 percentage in the previous quarter.

IIP continues to remain volatile IIP continues to remain volatile as it fell down to 1.8 percentage for December vs 5.9 percentage reported for November 2011. The main reason for the fall was the sharp deterioration in the manufacturing sector growth which plunged to 1.8 percentage Vs 6.6 percentage growth number reported in the previous month. Mining industry continues to post the negative growth as it posted a de-growth of 3.7 percentage y-o-y for the month of December. Capital Goods also followed the trend as it posted a y-o-y de-growth of 16.5 percentage. Given the reduction in the CRR, the interest rate in the economy is expected to reduce which may improve the investments in the economy. This could see a turnaround in the capital goods sector and the overall IIP

Inflation at two year low The inflation for the January came at 6.55 percentage, lowest in the last 26 months. The fall is in line with RBI’s expectation of reducing inflation since the start of the CY2012. Food inflation contracted 0.52 percentage in January on the back of falling vegetable prices, compared with a 0.74 percentage rise a month ago.

January Trade Deficit stands at USD14.8bn The trade deficit continues to inch higher on the back of strong growth in the imports and sluggish growth on the export. For the month of January, the trade deficit stands at USD14.8bn on the back of 20.3 percentage growth in Imports and mere 10.4 percentage y-o-y growth in the exports. The surge in import was contributed by huge OIL import bill which stood at three and half year high of USD12.3bn. The elevated rupee dollar rate may help in reducing the import in near future and can help to reduce the trade deficit

USD/INR exchange rate The Indian Rupee exchange rate for February 2012 averaged at 49.1900 INR to USD. The high was 49.50 while the low for the month was 48.6950.

Debt Market Update The benchmark 10-year G-sec yield has begun the month at 8.27 percentage and ended the month at 8.21 percentage. The market was range bound and stable during the month.

Equity Market Update Equity market continued their positive performance in February month on the back of the positive investor sentiments in the markets. The Sensex gained approx 3.25 percentage for the month while nifty too posted a gain of 3.5 percentage for the same period. The investor sentiment continued to remain buoyant and the same has been reflected in the FII money flow which has remained positive for the last two months. The other positive highlights on the domestic side were the inflation which came at 26 month low and also appreciation of rupee against dollar. The reduction in the inflation has further resurfaced the talk of RBI cutting rate as early as in the March midterm policy review. On the global front, the Greece bailout added to the positive sentiments.

On the sectoral front, most of the indices have seen positive gains and outperformed the major indices. The highest gainer was Realty (14.5 percentage), Auto (8.15 percentage) and Capital Goods (5.7 percentage)

discounting this much earlier. Despite recent run-up, equity markets are still trading at valuations at ~13 times FY13 earnings, much below the long-term averages. Short term volatility and marginal downward correction cannot be ruled out. However, it is a good time to increase the exposure to equity with an investment horizon of at least 3 years. Market Valuations: At the current levels of ~17677 the Sensex with an expected EPS of 1260 for FY-13E trades at a PE of ~13x 1-year forward. The valuation multiple has rebounded from its bottom level but they are still below their historical averages. One can expect the market to reach its mean multiples of 15-16 times in the next 1 yr. period.

Fund Flows: Foreign Institutional investors (FIIs) were turned net buyers to the tune of Rs.24,694cr, while domestic institutional investors (DIIs) were net sellers to the tune of Rs.2171cr worth of shares in the month.

Sectoral Update Oil and Gas: The Government has again increased both diesel and petrol prices to pass-on the high crude prices which may help to reduce the under-recovery of the oil marketing companies. This should be a positive step towards profitability of Oil marketing companies as well as upstream companies. We also expect clarity on subsidy sharing and de-regulation in the Oil& Gas sector in the next 3-6 months.

Information Technology: IT- Majors maintained their volume growth guidance for FY-12 and sees an increase in spending budget in FY13 onwards. This coupled with weakening rupee augur well for the sector. However, Euro-zone issues and fear of double-dip recession in US continue to dampen sentiments. Also, non-extension of the Sec 10A/B and bringing of SEZ facilities under MAT regime may act as a sentiment dampener for short-term.

Auto: Auto sales numbers are continue to remain at comfortable level and are expected to inch up in the next fiscal once the interest rates in the system starts going down. New launches, both in two wheeler and three wheeler will keep the demand in momentum and augur well for the auto and auto ancillary companies.

Banking: The banking sector got affected mainly due to RBI tightening interest rates mainly to curb inflationary pressures. However, we are near the rate-hike cycle and this would augur well for the banking sector in the longer-term.

We expect the sectors such as IT, Pharma, Banking and Oil & Gas would outperform and will maintain an overweight stance in these sectors. We continue to be cautious on Metals due to slow down in China and global weakness.

Market Outlook: Global market continued their upward journey during the month on the back of improved investor sentiments and strong FII flows. Most of the major global indices posted monthly returns in the range of 2 percentage - 5 percentage. The major trigger were the finalisaiton of the Greece bailout and the second round of LTRO funding by the European central bank. These events has eased the liquidity in the system and prompted investors to again look back to the riskier investments. Cues from the US also remained positive as the unemployment rate fell to 4 year low and sales of new homes in the U.S. came in at a higher than expected level in January.

The domestic market too continued its upward journey which started early in January on the back of the strong FII flow and improvement in the macroeconomic trends. On the global side, strong weekly sales and job data from US, some stability in the Euro zone were the important positive factors. On the domestic side, the continued moderation in the inflation has sparked a talk of the reduction in the interest rate by RBI. The results of the UP election are also expected to be out in the sometime and the consensus view is that the congress will be able to consolidate its position and increase its strength in the parliament. Improvement in the IIP, core industry and an adoption of expansionary monetary policy by RBI may emerge as the key positive factors for the equity markets. Going ahead; the UP election results, Union Budget, RBI monetary policy, crude prices and Europe and US situation will determine the direction of the markets. We expect the up-move to resume post a consolidation phase for a month or two.

The policy initiatives, such as removing the restrictions on interest paid on NRE Deposits, allowing any foreign national to buy Indian equities directly from the secondary / primary market, increasing the debt limits for subscription by FIIs (both G-Sec & Corporate debts), proposals on allowing PSUs to buy the other PSU stocks, persuading cash rich PSUs to pay more dividends, allowing promoters to sell their equity holdings by auction mechanism through stock exchanges etc, needs to be closely watched as they could be game changers. We expect some of these measures to work towards reducing the high fiscal deficit, arresting steep rupee depreciation and also reduce the burden of high Govt. borrowings. This in turn can soften the inflation and interest rates, there-by putting the economy back on the growth path. The results will not be immediate but may take a few months – but the stock market as it generally does, may start

14.5%

8.8% 8.1%6.1% 5.7% 5.1% 4.8%

3.6% 3.3% 2.5%

0%

4%

8%

12%

16%

Rea

lty

Mid

cap

Aut

o

Sm

allC

ap

Cap

ital G

oods

Ban

kex

Met

al

Nift

y

Sen

sex

OIL

Features of our Funds Nature of the Fund Equity Fund/Equity Pension Fund Name of the Fund Equity Growth Fund - Primarily invested in equity.

Investment Objective To provide high growth opportunities with an objective of long term capital appreciation through investments primarily in equity and equity related instruments.

Fund Positioning This fund is positioned as a highly diversified equity fund aiming to provide a stable and sustainable relative out performance vis-à-vis the benchmark. The fund will stick to the theme of discipline, diligence and dividend yield while selecting equity stocks. It will invest at least 70 percentage of its exposure to equity in large cap stocks (from S&P CNX Nifty Index or BSE 100 Index) and the remaining may be invested in mid/small-cap equity stocks.

Asset Allocation Equity Debt Money market

Minimum 80 0 0

Maximum 100 10 20

Chief Investment Officer A. K. Sridhar

Fund Manager Prasanna Pathak

Date of Launch 25th November, 2009

Net Asset Value Declared every business day

Fund's Fact Sheet Published monthly

Benchmark Index - Composition

S & P CNX Nifty - 90 percentage weight CRISIL - CBLO Index Index - 10 percentage weight

Nature of the Fund Debt Fund/Debt Pension Fund Name of the Fund Primarily invested in debt instruments.

Investment Objective To generate a good level of income and prospects for capital growth through diversified investment in corporate debt instruments, government securities and money market investments.

Fund Positioning This fund is positioned as a pure debt oriented fund, with asset allocation pattern providing a good opportunity to provide consistent and sustainable returns. The debt portfolio will comprise of high rated debt instruments with a low to moderate liquidity, government securities and money market investments with very high safety and easy liquidity. The asset allocation between corporate debt and government securities/money market investments and the portfolio duration of the fund, will follow a macro level economic scenario while the individual corporate debt investments will follow with a micro level credit worthiness and debt servicing capacity of companies.

Asset Allocation Equity Debt Money market Minimum 0 70 0

Maximum 0 100 30

Chief Investment Officer A. K. Sridhar

Fund Manager Poonam Tandon

Date of Launch 25th November, 2009

Net Asset Value Declared every business day

Fund's Fact Sheet Published monthly

Benchmark Index - Composition

CRISIL Composit Bond Fund Index - 85 percentage Weight CRISIL - CBLO Index - 15 percentage Weight

Nature of the Fund Balanced Fund/Balanced Pension Fund Name of the Fund Balanced Fund with exposure to equity and debt

investments. Investment Objective To provide higher growth with reasonable security, by

investing primarily in equity instruments and moderate allocation in debt securities/bonds.

Fund Positioning This fund is positioned as a balanced mix of debt and equity, with the asset allocation pattern providing a good opportunity to provide consistent and sustainable returns. The equity portion will have a highly diversified portfolio with high liquidity while the debt portion will comprise of high rated debt instruments with low to moderate liquidity. The asset allocation will follow a macro level market scenario and the individual stock selection will be with micro level performance expectations of the stocks and securities.

Asset Allocation Equity Debt Money market Minimum 50 30 0 Maximum 70 50 20 Chief Investment Officer

A. K. Sridhar

Fund Manager Prasanna Pathak and Poonam Tandon Date of Launch 25th November, 2009 Net Asset Value Declared every business day Fund's Fact Sheet Published monthly Benchmark Index - Composition

S & P CNX Nifty - 60 percentage Weight CRISIL Composit Bond Fund Index - 30 percentage weight CRISIL - CBLO Index - 10 percentage Weight

Nature of the Fund Liquid Pension Fund Name of the Fund Investment in liquid and money market instruments.

Investment Objective To provide capital protection with growth at short-term interest rates while providing a high level of liquidity.

Fund Positioning This Fund is positioned as a pure debt oriented short term liquid fund with the asset allocation pattern giving a reasonable opportunity to provide consistent and sustainable returns, with very high liquidity. The investment portfolio will primarily comprise of high rated short term money market investments with very high safety and easy liquidity. The maturity profile and the portfolio duration will follow a macro level economic scenario and the expected liquidity needs of the fund.

Asset Allocation Equity Debt Money market

Minimum 0 80 0

Maximum 0 100 20

Chief Investment Officer

A. K. Sridhar

Fund Manager Poonam Tandon

Date of Launch 25th November, 2009

Net Asset Value Declared every business day

Fund's Fact Sheet Published monthly

Benchmark Index – Composition

CRISIL - CBLO Index - 100 percentage Weight

Features of our Funds Nature of the Fund Value Fund

Name of the Fund Growth Fund.

Investment Objective To provide high growth opportunities with an objective of long term capital appreciation through investments primarily in equity and equity related instruments

Fund Positioning This fund will be positioned as a multi-cap pure value fund with clearly defined investment criteria for investing in value stocks.The fund will invest in stocks that are relatively undervalued to their intrinsic value and will create wealth for investors in the medium to long term.

Asset Allocation Equity Debt Money market

Minimum 70 0 0

Maximum 100 0 30

Chief Investment Officer

A. K. Sridhar

Fund Manager Prasanna Pathak

Date of Launch 16th September, 2010

Net Asset Value Declared every business day

Fund's Fact Sheet Published monthly

Benchmark Index - Composition

BSE 100 Index - 90 percentage Weight CRISIL - CBLO Index - 10 percentage Weight

Nature of the Fund Index Tracker Fund Name of the Fund Equity Index Fund.

Investment Objective The principal investment objective of the scheme is to invest in stocks of companies comprising S&P CNX Nifty Index and endeavour to achieve return equivalent to Nifty by "passive" investment

Fund Positioning This will be a passively managed Fund, by investing the major portion of the fund, only in 50 equity stocks comprised in the S&P Nifty Index, in a proportion that is as close as possible to the weightages of these stocks in the index. The exposure/weightages of investment stocks will , however be subject to regulatory investment guidelines and exposure norms.

Asset Allocation Equity Debt Money market

Minimum 90 0 0

Maximum 100 0 10 Chief Investment Officer

A. K. Sridhar

Fund Manager Sandeep Shirsat

Date of Launch 22nd September, 2010

Net Asset Value Declared every business day

Fund's Fact Sheet Published monthly

Benchmark Index – Composition

S & P CNX Nifty - 95 percentage Weight CRISIL - CBLO Index - 5 percentage Weight

Nature of the Fund Dynamic Asset Allocation Fund Name of the Fund Equity Fund- proportion varies with P/E model

Investment Objective To provide long-term capital appreciation with relatively lower volatility by dynamically adjusting the capital allocation between equity and fixed income instruments

Fund Positioning This Fund would be positioned as a dynamic equity fund aiming to provide a stable and sustainable relative out performance vis-à-vis the benchmark. The asset allocation between equity and fixedincome instruments will be based on the PE level of the index (Sensex).

Asset Allocation Equity Debt Money market

Minimum 0 0 0

Maximum 100 100 20

Chief Investment Officer

A. K. Sridhar

Fund Manager Prasanna Pathak

Date of Launch 22nd September, 2010

Net Asset Value Declared every business day

Fund's Fact Sheet Published monthly

Benchmark Index – Composition

S & P CNX Nifty - 95 percentage Weight CRISIL - CBLO Index - 5 percentage Weight

# S&P CNX NIFTY/BSE 100 Index Equity Fund, Equity Fund Pension, Balanced Fund, Balanced Fund Pension and Index Tracker Fund are benchmarked to S&P CNX Nifty Index which is not sponsored endorsed, sold or promoted by India Index Services & Products Limited (IISL). IISL is nor responsible for any errors or omissions or the results obtained from the use of such index and in no event shall IISL have any liability to any party for any damages of whatsoever nature (including lost profits) resulted to such party due to purchase or sale or otherwise of such product benchmarked to such index.

“Standard & Poor’s® and “S&P® are trademarks of The McGraw-Hill Companies, Inc. and have been licensed for use by India Index Services & Products Limited (IISL). The S&P CNX Nifty is not compiled, calculated or distributed by Standard & Poor’s and Standard & Poor’s and IISL make no representation regarding the advisability of investing in products that utilize any such Index as a component. All rights in the SENSEX/BSE 100 vest in Bombay Stock Exchange Ltd. (“BSE”). BSE and SENSEX are trademarks of BSE and are used by IndiaFirst Life Insurance Company Limited. BSE shall not be liable in any manner whatsoever (including in negligence) for any loss arising to any person whosoever out of use of or reliance on the SENSEX by any person.

CRISIL Composite Bond Fund Index and CRISIL - CBLO Index CRISIL has taken due care and caution in compilation of data for CRISIL Composite BondFund Index and CRISIL - CBLO Index. Information has been obtained by CRISIL from sources it considers reliable. However, CRISIL does not guarantee the accuracy, adequacy or completeness of the information and is not responsible for any errors or omissions or for the results obtained from the use of such information. CRISIL is not responsible for any errors in data reproduction. CRISIL especially states that it has no financial liability whatsoever to the subscribers/users/transmitters/distributors of this bulletin.

Equity Fund (SFIN: ULIF001161109EQUITYFUND143) Fact Sheet for February, 2012

Investment Objective To provide high growth opportunities with an objective of long term capital appreciation through investments primarily in equity and equity related instruments.

Name Date of Inception NAV as on 29th February, 2012 Equity Fund 25-Nov-09 `10.91

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 80 100 86 Debt Securities and Bonds 0 10 0 Cash and Money Market Investments 0 20 14

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning This Fund is positioned as a highly diversified equity fund aiming to provide a stable and sustainable relative out performance vis-à-vis the benchmark. The fund will stick to the theme of discipline, diligence and dividend yield while selecting equity stocks. It will invest at least 70 Percentage of its exposure to equity in large cap stocks (from S&P CNX Nifty Index or BSE 100 Index ) and the remaining may be invested in mid/ small-cap equity stocks.

Asset Allocation Pattern as on 29th February, 2012

Industry -wise Exposure

Portfolio Scheme: Equity Fund

Nature of Security

Security Name Holding

Percentage Equity Shares

Reliance Industries Limited 7.52 Infosys Limited 7.26 ITC Limited 5.64 ICICI Bank Limited 5.63 Housing Development Finance Corporation Limited 4.40 State Bank Of India 3.89 Larsen & Toubro Limited 3.68 Tata Consultancy Services Limited 3.52 HDFC Bank Limited 3.31 Hindustan Unilever Limited 2.83 Bharti Airtel Limited 2.47 Oil & Natural Gas Corporation Limited 2.11 Bharat Heavy Electricals Limited 2.04 Axis Bank Limited 1.90 National Thermal Power Corporation Limited 1.83 Mahindra & Mahindra Limited 1.79 Tata Steel Limited 1.68 GAIL (India) Limited 1.58 Tata Motors Limited 1.37 Dr. Reddys Laboratories Limited 1.19 Other Equity 20.39

86.03 Debt 0.00 Money Market Investments 13.97 Net Assets 100.00

Industry-wise Exposure Industry Percentage Banking and Finance Services 15.02 CBLO 13.98 Computer Software 11.59 Refinery 7.77 Tobacco Products 5.64 Housing Finance Sector 4.84 Industrial Construction 3.68 Drugs & Pharmaceuticals 3.42 Steel 3.27 Electricity Generation 3.24 Others* 27.55 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3 percentage

Quantitative Indicators

Std Dev (Annualised) : 22.30 Sharpe Ratio :- 0.16 Portfolio Beta: 0.87

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception

Equity Fund 10.72 7.11 1.53 3.91 Composite Benchmark** 10.51 7.33 1.65 2.73

** Refer "Features of our Funds" for Details

Equity Debt Money Market

Banking and Finance ServicesCBLO

Computer Software

RefineryTobacco Products

Housing Finance SectorIndustrial Construction

Drugs & Pharmaceuticals

SteelElectricity Generation

Others*

Equity Fund (SFIN: ULIF001161109EQUITYFUND143) Fact Sheet for February, 2012

Fund Manager's Comments In the month of February, The domestic market too continued its upward journey which started early in January on the back of the strong FII flow and improvement in the macroeconomic trends. The major event during the month was the Greece bailout and the second round of LTRO (Long term Refinancing Operations) funding by the European central bank. These events has eased the liquidity in the system and prompted investors to again look back to the riskier investments. On the domestic side, the continued moderation in the inflation has sparked a talk of the reduction in the interest rate by RBI. Going ahead; the UP election results, Union Budget, RBI monetary policy, crude prices and Europe and US situation will determine the direction of the markets. We expect the consolidation phase for the domestic markets to continue for a few more months. During the month, we continued to be over-weight on Oil & Gas, Pharma, Banking, Auto and other consumption themes. Going ahead, we would tactically reduce cash levels to deploy in good stories at attractive levels. The exposure to equity will be tilted towards low beta stocks that are having attractive value proposition.

Equity1 Fund (SFIN : ULIF009010910EQUTY1FUND143) Fact Sheet for February, 2012

Investment Objective To provide high growth opportunities with an objective of long term capital appreciation through investments primarily in equity and equity related instruments.

Name Date of Inception NAV as on 29th February, 2012 Equity1 Fund 15-Sep-10 ` 9.44

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 80 100 86 Debt Securities and Bonds 0 10 0 Cash and Money Market Investments 0 20 14

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning This Fund is positioned as a highly diversified equity fund aiming to provide a stable and sustainable relative out performance vis-à-vis the benchmark. The fund will stick to the theme of discipline, diligence and dividend yield while selecting equity stocks. It will invest at least 70 Percentage of its exposure to equity in large cap stocks (from S&P CNX Nifty Index or BSE 100 Index ) and the remaining may be invested in mid/ small-cap equity stocks.

Asset Allocation Pattern as on 29th February, 2012

Industry -wise Exposure

Portfolio Scheme: Equity1 Fund

Nature of Security

Security Name Holding

Percentage Equity Shares

Reliance Industries Limited 6.34 ICICI Bank Limited 6.23 ITC Limited 5.72 Infosys Limited 5.55 Housing Development Finance Corporation Limited 4.94 HDFC Bank Limited 4.35 State Bank Of India 3.96 Larsen & Toubro Limited 3.44 Hindustan Unilever Limited 2.88 Tata Consultancy Services Limited 2.69 Axis Bank Limited 2.51 Oil & Natural Gas Corporation Limited 2.47 Bharti Airtel Limited 2.43 National Thermal Power Corporation Limited 2.33 Power Grid Corporation of India Limited 1.50 GAIL (India) Limited 1.46 Mahindra & Mahindra Limited 1.39 Bharat Heavy Electricals Limited 1.32 Tata Steel Limited 1.29 Tata Motors Limited 1.28 Other Equity 21.60

85.67 Debt 0.00 Money Market Investments 14.33 Net Assets 100.00

Industry-wise Exposure Industry Percentage Banking and Finance Services 18.00 CBLO 14.33 Computer Software 9.25 Refinery 6.95 Tobacco Products 5.72 Housing Finance Sector 5.22 Drugs & Pharmaceuticals 5.04 Electricity Generation 3.50 Industrial Construction 3.44 Others* 28.55 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3 percentage

Quantitative Indicators

Std Dev (Annualised) : 21.81 Sharpe Ratio : -0.12 Portfolio Beta: 0.85

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception

Equity1 Fund 10.51 7.36 2.15 -3.90

Composite Benchmark** 10.51 7.33 1.65 -4.35

** Refer "Features of our Funds" for Details

Equity Debt Money Market

Banking and Finance Services

CBLO

Computer Software

Refinery

Tobacco Products

Housing Finance Sector

Drugs & Pharmaceuticals

Electricity Generation

Industrial Construction

Others*

Equity1 Fund (SFIN : ULIF009010910EQUTY1FUND143) Fact Sheet for February, 2012 Fund Manager's Comments In the month of February, The domestic market too continued its upward journey which started early in January on the back of the strong FII flow and improvement in the macroeconomic trends. The major event during the month was the Greece bailout and the second round of LTRO (Long term Refinancing Operations) funding by the European central bank. These events has eased the liquidity in the system and prompted investors to again look back to the riskier investments. On the domestic side, the continued moderation in the inflation has sparked a talk of the reduction in the interest rate by RBI. Going ahead; the UP election results, Union Budget, RBI monetary policy, crude prices and Europe and US situation will determine the direction of the markets. We expect the consolidation phase for the domestic markets to continue for a few more months. During the month, we continued to be over-weight on Oil & Gas, Pharma, Banking, Auto and other consumption themes. Going ahead, we would tactically reduce cash levels to deploy in good stories at attractive levels. The exposure to equity will be tilted towards low beta stocks that are having attractive value proposition.

Equity Pension Fund (SFIN: ULIF002161109EQUFUNDPEN143) Fact Sheet for February, 2012

Investment Objective To provide higher growth with reasonable security, by investing primarily in equity instruments and moderate allocation in debt securities/ bonds.

Name Date of Inception NAV as on 29th February, 2012 Equity Pension Fund 25-Nov-09 `10.92

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 80 100 87 Debt Securities and Bonds 0 10 0 Cash and Money Market Investments 0 20 13

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning This Fund is positioned as a highly diversified equity fund aiming to provide a stable and sustainable relative out performance vis-à-vis the benchmark. The fund will stick to the theme of discipline, diligence and dividend yield while selecting equity stocks. It will invest at least 70 Percentage of its exposure to equity in large cap stocks (from S&P CNX Nifty Index or BSE 100 Index ) and the remaining may be invested in mid/ small-cap equity stocks. Asset Allocation Pattern as on 29th February, 2012

Industry -wise Exposure

Portfolio Scheme: Equity Pension Fund

Nature of Security

Security Name Holding

Percentage Equity Shares

Infosys Limited 7.96 Reliance Industries Limited 7.36 ITC Limited 5.85 ICICI Bank Limited 5.51 Housing Development Finance Corporation Limited 4.72 Tata Consultancy Services Limited 3.92 HDFC Bank Limited 3.74 Larsen & Toubro Limited 3.66 State Bank Of India 3.64 Hindustan Unilever Limited 2.40 Bharat Heavy Electricals Limited 2.03 Tata Motors Limited 2.02 Oil & Natural Gas Corporation Limited 1.91 Axis Bank Limited 1.87 Mahindra & Mahindra Limited 1.78 GAIL (India) Limited 1.69 Bharti Airtel Limited 1.67 National Thermal Power Corporation Limited 1.64 Cipla Limited 1.40 Maruti Suzuki India Limited 1.38 Other Equity 20.66

86.79 Debt 0.00 Money Market Investments 13.21 Net Assets 100.00

Industry-wise Exposure Industry Percentage Banking and Finance Services 15.42 CBLO 13.22 Computer Software 12.39 Refinery 8.20 Tobacco Products 5.85 Housing Finance Sector 5.10 Drugs & Pharmaceuticals 3.86 Industrial Construction 3.66 Electricity Generation 3.23 Passenger Cars & MUVs 3.16 Others* 25.93 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3 percentage

Quantitative Indicators

Std Dev (Annualised) : -22.01 Sharpe Ratio : 0.14 Portfolio Beta: 0.86

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception

Equity Pension Fund 10.88 7.07 1.77 3.98

Composite Benchmark** 10.51 7.33 1.65 2.73

** Refer "Features of our Funds" for Details

Equity Money Market

Banking and Finance ServicesCBLO

Computer Software

RefineryTobacco Products

Housing Finance SectorDrugs & Pharmaceuticals

Industrial Construction

Electricity GenerationPassenger Cars & MUVs

Others*

Equity Pension Fund (SFIN: ULIF002161109EQUFUNDPEN143) Fact Sheet for February, 2012

Fund Manager's Comments In the month of February, The domestic market too continued its upward journey which started early in January on the back of the strong FII flow and improvement in the macroeconomic trends. The major event during the month was the Greece bailout and the second round of LTRO (Long term Refinancing Operations) funding by the European central bank. These events has eased the liquidity in the system and prompted investors to again look back to the riskier investments. On the domestic side, the continued moderation in the inflation has sparked a talk of the reduction in the interest rate by RBI. Going ahead; the UP election results, Union Budget, RBI monetary policy, crude prices and Europe and US situation will determine the direction of the markets. We expect the consolidation phase for the domestic markets to continue for a few more months. During the month, we continued to be over-weight on Oil & Gas, Pharma, Banking, Auto and other consumption themes. Going ahead, we would tactically reduce cash levels to deploy in good stories at attractive levels. The exposure to equity will be tilted towards low beta stocks that are having attractive value proposition.

Balanced 1 Fund (SFIN: ULIF011010910BALAN1FUND143) Fact Sheet for February, 2012

Investment Objective

To provide higher growth with reasonable security, by investing primarily in equity instruments and moderate allocation in debt securities/ bonds.

Name Date of Inception NAV as on 29th February, 2012 Balanced 1 Fund 14-Sep-10 ` 9.88

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 50 70 54 Debt Securities and Bonds 30 50 32 Cash and Money Market Investments 0 20 14

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning This Fund is positioned as a balanced mix of debt and equity, with the asset allocation pattern providing a good opportunity to provide consistent and sustainable returns. The equity portion will have a highly diversified portfolio with high liquidity while the debt portion will comprise of high rated debt instruments with a low to moderate liquidity. The asset allocation will follow a macro level market scenario and the individual stock selection will be with micro level performance expectations of the stocks and securities.

Asset Allocation Pattern as on 29th February, 2012

Credit Profile of Debt and Money Market Investments Nature Percentage

GSEC & T Bills 5.69 AAA & P1+ & PR1+ & A1+ 50.99 AA+ & LAA+ 10.93 AA 0.00 Fixed Deposits with Banks 4.70 CBLO/ Other Money Market Investments 27.69 Grand Total 100.00

Industry-wise Exposure

Portfolio Scheme: Balanced 1 Fund

Nature of Security

Security Name Holding

Percentage Equity Shares Reliance Industries Limited 4.23

ITC Limited 4.12 Infosys Limited 3.87 ICICI Bank Limited 3.79 Housing Development Finance Corporation Limited 3.35 HDFC Bank Limited 3.07 State Bank Of India 2.38 Larsen & Toubro Limited 2.30 Tata Consultancy Services Limited 2.22 Hindustan Unilever Limited 1.79 Bharti Airtel Limited 1.58 Axis Bank Limited 1.39 National Thermal Power Corporation Limited 1.13 Oil & Natural Gas Corporation Limited 1.05 Tata Motors Limited 0.98 Sun Pharmaceutical Industries Limited 0.96 Bharat Heavy Electricals Limited 0.91 Mahindra & Mahindra Limited 0.83 GAIL (India) Limited 0.82 Maruti Suzuki India Limited 0.79 Other Equity 12.23

53.79 Debt Sundaram Finance Limited 3.50

Tata Sons Limited 2.98 Rural Electrification Corporation Limited 2.36 Sovereign 2.30 Infrastructure Leasing & Financial Services Limited 2.24 Other Debt 18.91

32.30 Money Market Investments 13.91 Net Assets 100.00

Industry-wise Exposure Industry Percentage Banking and Finance Services 16.59 CBLO 13.12 Computer Software 7.52 Infrastructure Finance Services 7.32 Housing Finance Sector 7.20 Refinery 6.79 Electricity Generation 4.36 Tobacco Products 4.12 Investment Services 4.02 Drugs & Pharmaceuticals 3.02 Others* 25.94 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3percentage

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception Balanced 1 Fund 7.14 5.59 4.01 -0.79 Composite Benchmark** 7.94 6.38 3.85 -0.11

** Refer "Features of our Funds" for Details

Equity Shares Debt Money Market Investments

Banking and Finance ServicesCBLO

Computer Software

Infrastructure Finance ServicesHousing Finance Sector

RefineryElectricity Generation

Tobacco Products

Investment ServicesDrugs & Pharmaceuticals

Others*

Balanced 1 Fund (SFIN: ULIF011010910BALAN1FUND143) Fact Sheet for February, 2012

Maturity Profile of Debt Portfolio Period Percentage 0-3 months 17.62 3-12 months 17.21 1- 3 year 33.46 3 -5 year 12.45 5- 10 year 19.26 > 10 year 0.00 Grand Total 100.00

Fund Manager's Comments In the month of February, The domestic market too continued its upward journey which started early in January on the back of the strong FII flow and improvement in the macroeconomic trends. The major event during the month was the Greece bailout and the second round of LTRO (Long term Refinancing Operations) funding by the European central bank. These events has eased the liquidity in the system and prompted investors to again look back to the riskier investments. On the domestic side, the continued moderation in the inflation has sparked a talk of the reduction in the interest rate by RBI. Going ahead; the UP election results, Union Budget, RBI monetary policy, crude prices and Europe and US situation will determine the direction of the markets. We expect the consolidation phase for the domestic markets to continue for a few more months. During the month, we continued to be over-weight on Oil & Gas, Pharma, Banking, Auto and other consumption themes. Going ahead, we would tactically reduce cash levels to deploy in good stories at attractive levels. The exposure to equity will be tilted towards low beta stocks that are having attractive value proposition. The GDP growth has dipped further to 6.1 percentage for the third quarter. The IIP data has slowed to 1.8 percentage in December 2011. The inflation for the month of January 2012 dipped to 6.55 percentage on the back of a decrease in food prices and primary articles. All these data are conducive for an interest rate cut by the RBI. However, crude prices have increased significantly and will impact inflation negatively in the future. Therefore the RBI may not cut the rates in the March 2012 policy, although the RBI has stated that the interest rates have peaked. The 10 year G-sec has been range bound in the 8.15 percentage - 8.25 percentage in the month of February 2012. The market is also worried about high government borrowing programme which is expected to be announced in the month of March. We have elongated duration and will continue to do so whenever there is an increase in the yields.

Quantitative Indicators (Equity) Std Dev (Annualised) Sharpe Ratio Portfolio Beta

13.74 -0.09 0.89

Quantitative Indicators (Debt) Average Maturity Modified Duration

2.06 Years 1.50 Years

Balanced Pension Fund (SFIN: ULIF006161109BALFUNDPEN143) Fact Sheet for February, 2012

Investment Objective To provide higher growth with reasonable security, by investing primarily in equity instruments and moderate allocation in debt securities/ bonds.

Name Date of Inception NAV as on 29th February, 2012 Balanced Pension Fund

25-Nov-09 ` 11.05

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 50 70 54 Debt Securities and Bonds 30 50 34 Cash and Money Market Investments 0 20 12

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning This Fund is positioned as a balanced mix of debt and equity, with the asset allocation pattern providing a good opportunity to provide consistent and sustainable returns. The equity portion will have a highly diversified portfolio with high liquidity while the debt portion will comprise of high rated debt instruments with a low to moderate liquidity. The asset allocation will follow a macro level market scenario and the individual stock selection will be with micro level performance expectations of the stocks and securities.

Asset Allocation Pattern as on 29th February, 2012

Credit Profile of Debt and Money Market Investments Nature Percentage GSEC & T Bills 5.74 AAA & P1+ & PR1+ & A1+ 56.10 AA+ & LAA+ 5.23 AA 0.00 Fixed Deposits with Banks 6.32 CBLO/ Other Money Market Investments 26.60 Grand Total 100.00

Industry -wise Exposure

Portfolio Scheme: Balanced Pension Fund

Nature of Security Security Name

Holding Percentage

Equity Shares Infosys Limited 5.20 Reliance Industries Limited 4.85 ITC Limited 3.54 ICICI Bank Limited 3.11 Housing Development Finance Corporation Limited 2.91 Tata Consultancy Services Limited 2.46 State Bank Of India 2.30 Larsen & Toubro Limited 2.09 HDFC Bank Limited 1.93 Bharat Heavy Electricals Limited 1.65 Axis Bank Limited 1.47 Tata Motors Limited 1.44 Oil & Natural Gas Corporation Limited 1.21 Mahindra & Mahindra Limited 1.16 Hindustan Unilever Limited 1.13 GAIL (India) Limited 1.01 Tata Steel Limited 0.97 Bharti Airtel Limited 0.96 Maruti Suzuki India Limited 0.89 Hero Motocorp Limited 0.84 Other Equity 13.24

53.55 Debt Tata Sons Limited 4.51

Rural Electrification Corporation Limited 3.07 Housing Development Finance Corporation Limited 3.01 LIC Housing Finance Limited 2.92 Tech Mahindra Limited 2.83 Other Debt 17.17

33.50 Money Market Investments 12.14 Net Assets 100.00

Industry-wise Exposure Industry Percentage Banking and Finance Services 12.56 CBLO 12.14 Computer Software 10.97 Housing Finance Sector 9.10 Refinery 7.05 Investment Services 6.57 Infrastructure Finance Services 6.12 Electricity Generation 4.64 Tobacco Products 3.54 Others* 27.30 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3 percentage

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception

Balanced Pension Fund 7.64 6.17 4.66 4.53 Composite Benchmark** 7.94 6.38 3.85 3.84

** Refer "Features of our Funds" for Details

Equity Debt Money Market Investments

Banking and Finance Services

CBLO

Computer Software

Housing Finance Sector

Refinery

Investment Services

Infrastructure Finance Services

Electricity Generation

Tobacco Products

Others*

Balanced Pension Fund (SFIN: ULIF006161109BALFUNDPEN143) Fact Sheet for February, 2012

Maturity Profile of Debt Portfolio Period Percentage 0-3 months 13.83 3-12 months 20.26 1- 3 year 39.35 3 -5 year 13.85 5- 10 year 12.71 > 10 year 0.00 Grand Total 100.00

Fund Manager's Comments In the month of February, The domestic market too continued its upward journey which started early in January on the back of the strong FII flow and improvement in the macroeconomic trends. The major event during the month was the Greece bailout and the second round of LTRO (Long term Refinancing Operations) funding by the European central bank. These events has eased the liquidity in the system and prompted investors to again look back to the riskier investments. On the domestic side, the continued moderation in the inflation has sparked a talk of the reduction in the interest rate by RBI. Going ahead; the UP election results, Union Budget, RBI monetary policy, crude prices and Europe and US situation will determine the direction of the markets. We expect the consolidation phase for the domestic markets to continue for a few more months. During the month, we continued to be over-weight on Oil & Gas, Pharma, Banking, Auto and other consumption themes. Going ahead, we would tactically reduce cash levels to deploy in good stories at attractive levels. The exposure to equity will be tilted towards low beta stocks that are having attractive value proposition. The GDP growth has dipped further to 6.1 percentage for the third quarter. The IIP data has slowed to 1.8 percentage in December 2011. The inflation for the month of January 2012 dipped to 6.55 percentage on the back of a decrease in food prices and primary articles. All these data are conducive for an interest rate cut by the RBI. However, crude prices have increased significantly and will impact inflation negatively in the future. Therefore the RBI may not cut the rates in the March 2012 policy, although the RBI has stated that the interest rates have peaked. The 10 year G-sec has been range bound in the 8.15 percentage - 8.25 percentage in the month of February 2012. The market is also worried about high government borrowing programme which is expected to be announced in the month of March. We have elongated duration and will continue to do so whenever there is an increase in the yields.

Quantitative Indicators (Equity) Std Dev (Annualised) Sharpe Ratio Portfolio Beta 13.79 0.02 0.90

Quantitative Indicators (Debt) Average Maturity Modified Duration 1.97 Years 1.44 Years

Debt Fund (SFIN: ULIF003161109DEBTFUND00143) Fact Sheet for February, 2012

Investment Objective To generate a good level of income and prospects for capital growth through diversified investment in corporate debt instruments, government securities and money market investments.

Name Date of Inception NAV as on 29th February, 2012 Debt Fund 25-Nov-09 `11.52

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 0 0 0 Debt Securities and Bonds 70 100 87 Cash and Money Market Investments 0 30 13

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning This Fund is positioned as a pure debt oriented fund, with asset allocation pattern providing a good opportunity to provide consistent and sustainable returns. The debt portfolio will comprise of high rated debt instruments with a low to moderate liquidity, government securities and money market investments with very high safety and easy liquidity. The asset allocation between corporate debt and government securities/ money market investments and the portfolio duration of the fund, will follow a macro level economic scenario while the individual corporate debt investments will follow with a micro level credit worthiness and debt servicing capacity of companies.

Asset Allocation Pattern as on 29th February, 2012

Credit Profile of Debt and Money Market Investments Nature Percentage GSEC & T Bills 4.25 AAA & P1+ & PR1+ & A1+ 65.96 AA+ & LAA+ 13.65 AA 0.00 Fixed Deposits with Banks 6.84 CBLO/ Other Money Market Investments 9.30 Grand Total 100.00

Portfolio Scheme: Debt Fund

Nature of Security

Security Name Holding

Percentage Debt

MRF Limited 8.20 Housing Development Finance Corporation Limited 8.10 LIC Housing Finance Limited 7.77 Power Grid Corporation of India Limited 5.53 Reliance Industries Limited 5.02 Other Debt 52.10

86.72 Money Market Investments 13.28 Net Assets 100.00

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception

Debt Fund 10.31 8.93 9.26 6.46 Composite Benchmark** 11.06 8.87 8.22 6.05

** Refer "Features of our Funds" for Details

Industry-wise Exposure Industry Percentage Housing Finance Sector 17.47 Banking and Finance Services 13.30 Infrastructure Finance Services 11.30 Short Term Deposits 10.82 CBLO 9.30 Investment Services 8.75 Tyres and Tubes 8.20 Electricity Distribution 5.53 Refinery 5.36 Sovereign 4.25 Electricity Generation 3.88 Others* 1.86 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3%

Quantitative Indicators Average Maturity Modified Duration

3.55 Years 2.42 Years

Industry -wise Exposure

Debt Money Market

GSEC & T Bills

AAA & P1+ & PR1+ & A1+

AA+ & LAA+

AA

Fixed Deposits with Banks

CBLO/ Other Money Market Investments

Housing Finance SectorBanking and Finance ServicesInfrastructure Finance ServicesShort Term DepositsCBLOInvestment ServicesTyres and TubesElectricity DistributionRefinerySoveriegnElectricity GenerationOthers*

Debt Fund (SFIN: ULIF003161109DEBTFUND00143) Fact Sheet for February, 2012

Maturity Profile of Debt Portfolio Period Percentage 0-3 months 21.33 3-12 months 6.78 1- 3 year 26.87 3 -5 year 12.34 5- 10 year 29.90 > 10 year 2.78 Total 100.00

0-3 months

3-12 months

1- 3 year

3 -5 year

5- 10 year

> 10 year

Fund Manager's Comments The GDP growth has dipped further to 6.1 percentage for the third quarter. The IIP data has slowed to 1.8 percentage in December 2011. The inflation for the month of January 2012 dipped to 6.55 percentage on the back of a decrease in food prices and primary articles. All these data are conducive for an interest rate cut by the RBI. However, crude prices have increased significantly and will impact inflation negatively in the future. Therefore the RBI may not cut the rates in the March 2012 policy, although the RBI has stated that the interest rates have peaked. The 10 year G-sec has been range bound in the 8.15 percentage - 8.25 percentage in the month of February 2012. The market is also worried about high government borrowing programme which is expected to be announced in the month of March. We have elongated duration and will continue to do so whenever there is an increase in the yields.

Debt 1 Fund (SFIN: ULIF010010910DEBT01FUND143) Fact Sheet for February, 2012

Investment Objective To generate a good level of income and prospects for capital growth through diversified investment in corporate debt instruments, government securities and money market investments.

Name Date of Inception NAV as on 29th February, 2012 Debt 1 Fund 17-Sep-10 `11.13

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 0 0 0 Debt Securities and Bonds 70 100 88 Cash and Money Market Investments 0 30 12

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning This Fund is positioned as a pure debt oriented fund, with asset allocation pattern providing a good opportunity to provide consistent and sustainable returns. The debt portfolio will comprise of high rated debt instruments with a low to moderate liquidity, government securities and money market investments with very high safety and easy liquidity. The asset allocation between corporate debt and government securities/ money market investments and the portfolio duration of the fund, will follow a macro level economic scenario while the individual corporate debt investments will follow with a micro level credit worthiness and debt servicing capacity of companies.

Asset Allocation Pattern as on 29th February, 2012

Credit Profile of Debt and Money Market Investments Nature Percentage GSEC & T Bills 5.76 AAA & P1+ & PR1+ & A1+ 63.93 AA+ & LAA+ 13.04 AA 0.00 Fixed Deposits with Banks 7.23 CBLO/ Other Money Market Investments 10.04 Grand Total 100.00

Portfolio Scheme: Debt 1 Fund

Nature of Security

Security Name Holding

Percentage Debt

Housing Development Finance Corporation Limited 8.84 LIC Housing Finance Limited 7.01 Rural Electrification Corporation Limited 6.72 MRF Limited 6.50 Sovereign 5.76 Other Debt 53.11

87.94 Money Market Investments 12.06 Net Assets 100.00

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception

Debt 1 Fund 11.79 9.24 9.19 7.66 Composite Benchmark** 11.06 8.87 8.22 7.07

** Refer "Features of our Funds" for Details

Industry-wise Exposure Industry Percentage Housing Finance Sector 16.58 Infrastructure Finance Services 14.09 Banking and Finance Services 11.38 CBLO 10.04 Short Term Deposits 9.25 Investment Services 7.75 Electricity Generation 6.72 Tyres and Tubes 6.50 Sovereign 5.76 Crude Oil & Natural Gas 4.33 Refinery 4.29 Others* 3.31 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3 percentage

Quantitative Indicators Average Maturity Modified Duration

4.55 Years 3.03 Years

Industry -wise Exposure

Debt Money Market Investments

GSEC & T Bills

AAA & P1+ & PR1+ & A1+

AA+ & LAA+

AA

Fixed Deposits with Banks

CBLO/ Other Money Market Investments

Housing Finance SectorInfrastructure Finance ServicesBanking and Finance ServicesCBLOShort Term DepositsInvestment ServicesElectricity GenerationTyres and TubesSoveriegnCrude Oil & Natural GasRefineryOthers*

Debt 1 Fund (SFIN: ULIF010010910DEBT01FUND143) Fact Sheet for February, 2012

Maturity Profile of Debt Portfolio Period Percentage 0-3 months 9.51 3-12 months 2.97 1- 3 year 35.34 3 -5 year 10.38 5- 10 year 37.35 > 10 year 4.44 Total 100.00

0-3 months

3-12 months

1- 3 year

3 -5 year

5- 10 year

> 10 year

Fund Manager's Comments The GDP growth has dipped further to 6.1 percentage for the third quarter. The IIP data has slowed to 1.8 percentage in December 2011. The inflation for the month of January 2012 dipped to 6.55 percentage on the back of a decrease in food prices and primary articles. All these data are conducive for an interest rate cut by the RBI. However, crude prices have increased significantly and will impact inflation negatively in the future. Therefore the RBI may not cut the rates in the March 2012 policy, although the RBI has stated that the interest rates have peaked. The 10 year G-sec has been range bound in the 8.15 percentage - 8.25 percentage in the month of February 2012. The market is also worried about high government borrowing programme which is expected to be announced in the month of March. We have elongated duration and will continue to do so whenever there is an increase in the yields.

Debt Pension Fund (SFIN : ULIF004161109DEBFUNDPEN143) Fact Sheet for February, 2012

Investment Objective To generate a good level of income and prospects for capital growth through diversified investment in corporate debt instruments, government securities and money market investments.

Name Date of Inception NAV as on 29th February, 2012 Debt 1 Fund 25-Nov-09 `11.43

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 0 0 0 Debt Securities and Bonds 70 100 90 Cash and Money Market Investments 0 30 10

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning This Fund is positioned as a pure debt oriented fund, with asset allocation pattern providing a good opportunity to provide consistent and sustainable returns. The debt portfolio will comprise of high rated debt instruments with a low to moderate liquidity, government securities and money market investments with very high safety and easy liquidity. The asset allocation between corporate debt and government securities/ money market investments and the portfolio duration of the fund, will follow a macro level economic scenario while the individual corporate debt investments will follow with a micro level credit worthiness and debt servicing capacity of companies.

Asset Allocation Pattern as on 29th February, 2012

Credit Profile of Debt and Money Market Investments Nature Percentage GSEC & T Bills 5.37 AAA & P1+ & PR1+ & A1+ 72.94 AA+ & LAA+ 9.94 AA 0.00 Fixed Deposits with Banks 5.12 CBLO/ Other Money Market Investments 6.62 Grand Total 100.00

Portfolio Scheme: Debt 1 Fund

Nature of Security

Security Name Holding

Percentage Debt

Housing Development Finance Corporation Limited 8.76 Rural Electrification Corporation Limited 8.72 Tata Sons Limited 8.22 MRF Limited 7.76 LIC Housing Finance Limited 7.58 Other Debt 49.13

90.16 Money Market Investments 9.84 Net Assets 100.00

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception

Debt Pension Fund 9.62 8.38 8.59 6.10 Composite Benchmark** 11.06 8.87 8.22 6.05

** Refer "Features of our Funds" for Details

Industry-wise Exposure Industry Percentage Housing Finance Sector 18.85 Infrastructure Finance Services 16.46 Investment Services 15.19 Electricity Generation 8.72 Short Term Deposits 8.34 Tyres and Tubes 7.76 Banking and Finance Services 6.33 Sovereign 5.37 Computer Software 4.61 CBLO 6.62 Others* 1.76 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3%

Quantitative Indicators Average Maturity Modified Duration

3.74 Years 2.62 Years

Industry -wise Exposure

Debt Money Market Investments

GSEC & T Bills

AAA & P1+ & PR1+ & A1+

AA+ & LAA+

AA

Fixed Deposits with Banks

CBLO/ Other Money Market Investments

Housing Finance SectorInfrastructure Finance Services

Investment Services

Electricity GenerationShort Term Deposits

Tyres and TubesBanking and Finance Services

Soveriegn

Computer SoftwareCBLO

Others*

Debt Pension Fund (SFIN : ULIF004161109DEBFUNDPEN143) Fact Sheet for February, 2012

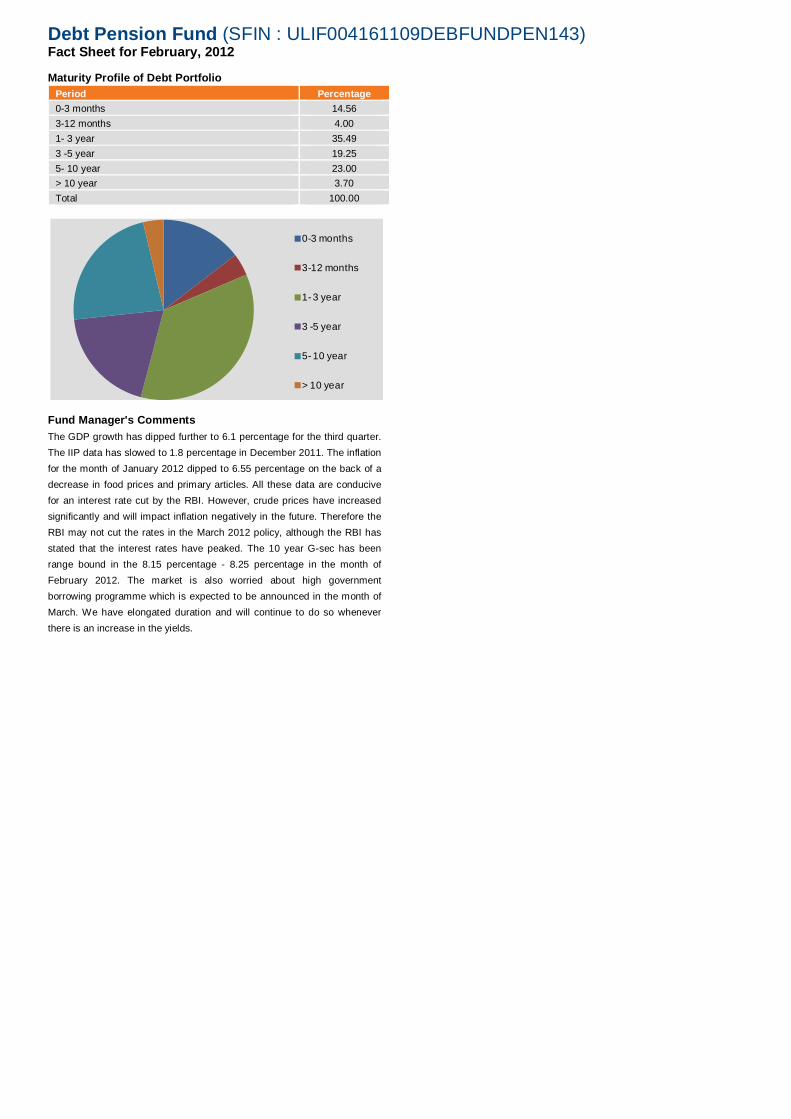

Maturity Profile of Debt Portfolio Period Percentage 0-3 months 14.56 3-12 months 4.00 1- 3 year 35.49 3 -5 year 19.25 5- 10 year 23.00 > 10 year 3.70 Total 100.00

0-3 months

3-12 months

1- 3 year

3 -5 year

5- 10 year

> 10 year

Fund Manager's Comments The GDP growth has dipped further to 6.1 percentage for the third quarter. The IIP data has slowed to 1.8 percentage in December 2011. The inflation for the month of January 2012 dipped to 6.55 percentage on the back of a decrease in food prices and primary articles. All these data are conducive for an interest rate cut by the RBI. However, crude prices have increased significantly and will impact inflation negatively in the future. Therefore the RBI may not cut the rates in the March 2012 policy, although the RBI has stated that the interest rates have peaked. The 10 year G-sec has been range bound in the 8.15 percentage - 8.25 percentage in the month of February 2012. The market is also worried about high government borrowing programme which is expected to be announced in the month of March. We have elongated duration and will continue to do so whenever there is an increase in the yields.

Liquid Pension Fund (ULIF008161109LIQFUNDPEN143) Fact Sheet for February, 2012

Investment Objective To provide capital protection with growth at short-term interest rates while providing a high level of liquidity.

Name Date of Inception NAV as on 29th February, 2012

Liquid Pension Fund 25-Nov-09 ` 11.30

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 0 0 0 Debt Securities and Bonds 0 20 0 Cash and Money Market Investments 80 100 100

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning This Fund is positioned as a pure debt oriented short term liquid fund with the asset allocation pattern giving a reasonable opportunity to provide consistent and sustainable returns, with very high liquidity. The investment portfolio will primarily comprise of high rated short term money market investments with very high safety and easy liquidity. The maturity profile and the portfolio duration will follow a macro level economic scenario and the expected liquidity needs of the fund.

Asset Allocation Pattern as on 29th February, 2012

Industry -wise Exposure

Portfolio Scheme: Liquid Pension Fund

Nature of Security Security Name Holding

Percentage Money Market Investments 100.00 Debt 0.00 Net Assets 100.00

Industry-wise Exposure Industry Percentage CBLO 84.37 Short Term Deposits 15.63 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3 percentage

Credit Profile of Debt and Money Market Investments Nature Percentage GSEC & T Bills 9.44 AAA & P1+ & PR1+ & A1+ 15.63 AA+ & LAA+ 0.00 AA 0.00 Fixed Deposits with Banks 0.00 CBLO/ Other Money Market Investments 74.93 Grand Total 100.00

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception

Liquid Pension Fund 7.13 7.26 7.54 5.53

Composite Benchmark** 8.48 8.39 7.78 6.04

** Refer "Features of our Funds" for Details

Fund Manager's Comments The funds under the Liquid Fund category continued to be invested in highly liquid short term papers having very high safety and liquidity, as per the investment mandates, set out for this fund.

Money Market Investment

CBLO Short Term Deposit

Value Fund (SFIN: ULIF013010910VALUEFUND0143) Fact Sheet for February, 2012

Investment Objective To provide high growth opportunities with an objective of long term capital appreciation through investments primarily in equity and equity related instruments.

Name Date of Inception NAV as on 29th February, 2012 Value Fund 16-Sep-10 ` 9.63

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 70 100 85 Debt Securities and Bonds 0 0 0 Cash and Money Market Investments 0 30 15

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning The Fund will be positioned as a multi-cap pure value fund with clearly defined investment criteria for investing in value stocks. The Fund will invest in stocks that are relatively undervalued to their intrinsic value and which will create wealth for shareholders in the medium to long term.

Asset Allocation Pattern as on 29th February, 2012

Industry -wise Exposure

Fund Manager's Comments The Value Fund invests in stocks which offer better value- proposition vis-a-vis peers based on strategies laid out in the Fund's investment mandate. In the initial phase, the tilt has been more towards large-cap stocks. This conscious short term strategy, has worked well as can be seen by the fund out-performance. We have started to increase the exposure to value and mid-cap stocks, to bring in more of value orientation, as the risk-reward appears to be favourable now.

Portfolio Scheme: Value Fund

Nature of Security

Security Name Holding Percentage

Equity Shares Reliance Industries Limited 6.68 Bharti Airtel Limited 5.80 ICICI Bank Limited 5.74 Larsen & Toubro Limited 5.55 ITC Limited 5.45 HDFC Bank Limited 5.05 Infosys Limited 5.04 Power Grid Corporation of India Limited 3.01 Oil & Natural Gas Corporation Limited 2.60 Housing Development Finance Corporation Limited 2.36 Bajaj Auto Limited 2.29 Hindalco Industries Limited 2.19 Mahindra & Mahindra Limited 2.15 Tata Steel Limited 2.02 Tata Motors Limited 1.97 Cipla Limited 1.73 Kotak Mahindra Bank Limited 1.54 Dr. Reddys Laboratories Limited 1.45 National Thermal Power Corporation Limited 1.40 Tata Consultancy Services Limited 1.37 Other Equity 19.61

84.99 Debt 0.00 Money Market Investments 15.01 Net Assets 100.00

Industry-wise Exposure Industry Percentage CBLO 15.01 Banking and Finance Services 14.68 Computer Software 8.03 Refinery 7.00 Telecommunication Services 5.80 Industrial Construction 5.55 Tobacco Products 5.45 Drugs & Pharmaceuticals 3.66 Electricity Generation 3.32 Copper & Copper Products 3.24 Electricity Distribution 3.01 Others* 25.27 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3 percentage

Quantitative Indicators

Std Dev (Annualised) : 22.06 Sharpe Ratio :-0.01 Portfolio Beta: 0.89

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception

Value Fund 12.06 10.05 3.75 -2.53

Composite Benchmark** 10.92 6.54 1.38 -5.48

** Refer "Features of our Funds" for Details

Equity Debt Money Market

CBLOBanking and Finance ServicesComputer SoftwareRefineryTelecommunication ServicesIndustrial ConstructionTobacco ProductsDrugs & PharmaceuticalsElectricity GenerationCopper & Copper ProductsElectricity DistributionOthers*

Index Tracker Fund (SFIN: ULIF012010910INDTRAFUND143) Fact Sheet for February, 2012

Investment Objective To provide high growth opportunities with an objective of long term capital appreciation through investments primarily in equity and equity related instruments.

Name Date of

Inception NAV as on 29th February,

2012 Index Tracker Fund 22-Sep-10 ` 9.05

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 90 100 98 Debt Securities and Bonds 0 10 0 Cash and Money Market Investments 0 10 2

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning This will be a passively managed Fund, by investing the major portion of the fund, only in 50 equity stocks comprised in the S&P Nifty Index, in a proportion that is as close as possible to the weightages of these stocks in the Index. The exposures / weightages of investment stocks will, however be subject to the regulatory investment guidelines and exposure norms.

Asset Allocation Pattern as on 29th February, 2012

Industry -wise Exposure

Fund Manager's Comments The Fund will be managed passively by investing in all the Nifty 50 Stocks in a proportion that is as close as possible to the weightages of these stocks in the S & P CNX Nifty index. Under Index Funds, tracking error normally occurs due to intraday price movements, cost of transaction, fund management expenses charges, dividend inflows. In addition, limiting the actual exposures to the extent allowed by regulatory norms also contribute to tracking error in certain scrips. The investment strategy is to keep the tracking error low and deliver the returns as close to the returns delivered by the benchmark index. The Fund will optimally use the portfolio re balancing techniques combined with least possible transaction cost to keep the tracking error low.

Portfolio Scheme: Index Tracker Fund

Nature of Security

Security Name Holding Percentage

Equity Shares Reliance Industries Limited 8.30 Infosys Limited 8.27 ITC Limited 6.69 ICICI Bank Limited 6.23 HDFC Bank Limited 5.56 Housing Development Finance Corporation Limited 5.26 Larsen & Toubro Limited 4.21 Tata Consultancy Services Limited 3.71 State Bank Of India 3.45 Tata Motors Limited 2.85 Bharti Airtel Limited 2.51 Oil & Natural Gas Corporation Limited 2.43 Hindustan Unilever Limited 2.34 Mahindra & Mahindra Limited 1.95 Tata Steel Limited 1.89 Axis Bank Limited 1.81 Bharat Heavy Electricals Limited 1.48 Bajaj Auto Limited 1.45 National Thermal Power Corporation Limited 1.39 Jindal Steel & Power Limited 1.35 Other Equity 24.96

98.08 Debt 0.00 Money Market Investments 1.92 Net Assets 100.00

Industry-wise Exposure Industry Percentage Banking and Finance Services 19.04 Computer Software 14.03 Refinery 8.82 Tobacco Products 6.69 Housing Finance Sector 5.26 Industrial Construction 4.21 Drugs & Pharmaceuticals 3.84 Steel 3.61 Electricity Generation 3.40 Crude Oil & Natural Gas 3.24 Others* 27.87 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3 percentage

Quantitative Indicators

Tracking Error : 1.26%

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception

Index Tracker Fund 11.03 7.17 -0.34 -6.72 Composite Benchmark** 10.98 7.51 1.31 -6.42

** Refer "Features of our Funds" for Details

Equity Debt Money Market

Banking and Finance ServicesComputer Software

Refinery

Tobacco ProductsHousing Finance Sector

Industrial ConstructionDrugs & Pharmaceuticals

Steel

Electricity GenerationCrude Oil & Natural Gas

Others*

Dynamic Asset Allocation Fund (SFIN: ULIF015080811DYAALLFUND143) Fact Sheet for February, 2012

Investment Objective To provide higher growth with reasonable security, by investing primarily in equity instruments and moderate allocation in debt securities/ bonds.

Name Date of Inception NAV as on 29th February, 2012 Dynamic Asset Allocation Fund

09-Sep-11 `11.40

Targeted Asset Allocation Pattern in Percentage Minimum Maximum Actual Equity Shares 0 100 86 Debt Securities and Bonds 0 100 0 Cash and Money Market Investments 20 100 14

The actual asset allocation will remain within the 'minimum' and 'maximum' range based on market opportunities and future outlook of the markets.

Fund Positioning This Fund is positioned as a balanced mix of debt and equity, with the asset allocation pattern providing a good opportunity to provide consistent and sustainable returns. The equity portion will have a highly diversified portfolio with high liquidity while the debt portion will comprise of high rated debt instruments with a low to moderate liquidity. The asset allocation will follow a macro level market scenario and the individual stock selection will be with micro level performance expectations of the stocks and securities.

Asset Allocation Pattern as on 29th February, 2012

Credit Profile of Debt and Money Market Investments Industry Percentage GSEC & T Bills 0.00 AAA & P1+ & PR1+ & A1+ 0.00 AA+ & LAA+ 0.00 AA 0.00 Fixed Deposits with Banks 0.00 CBLO/ Other Money Market Investments 100.00 Grand Total 100.00

Industry Wise Exposure

Portfolio Scheme: Dynamic Asset Allocation Fund

Nature of Security

Security Name Holding

Percentage Equity Shares

Larsen & Toubro Limited 7.10 Bharti Airtel Limited 6.78 ICICI Bank Limited 6.57 HDFC Bank Limited 6.18 Infosys Limited 5.26 ITC Limited 4.66 Dr. Reddys Laboratories Limited 3.26 Tata Steel Limited 3.23 Kotak Mahindra Bank Limited 3.12 Bajaj Auto Limited 2.71 Reliance Industries Limited 2.56 Coromandel International Limited 2.53 State Bank Of India 2.51 Tata Power Co. Limited 2.15 Hindalco Industries Limited 2.04 HCL Technologies Limited 1.99 Axis Bank Limited 1.96 Grasim Industries Limited 1.90 National Thermal Power Corporation Limited 1.79 Mahindra Holidays & Resorts India Limited 1.75 Other Equity 15.54

85.61 Debt 0.00 Money Market Investments 14.39 Net Assets 100.00

Industry-wise Exposure Industry Percentage Banking and Finance Services 20.35 CBLO 14.39 Computer Software 8.92 Industrial Construction 7.10 Telecommunication Services 6.78 Drugs & Pharmaceuticals 5.23 Tobacco Products 4.66 Electricity Generation 3.94 Copper & Copper Products 3.73 Steel 3.23 Others* 21.66 Grand Total 100.00

* 'Others' includes all industries having weightage of less than 3 percentage

Returns

Returns in Percentage

3 months 6 months 1 yearSince

Inception

Dynamic Asset Allocation Fund

11.87 NA NA 14.01

Composite Benchmark** 11.45 NA NA 6.44

** Refer "Features of our Funds" for Details

Equity Debt Money Market

Banking and Finance ServicesCBLO

Computer SoftwareIndustrial Construction

Telecommunication ServicesDrugs & Pharmaceuticals

Tobacco ProductsElectricity Generation

Copper & Copper ProductsSteel

Others*

Dynamic Asset Allocation Fund (SFIN: ULIF015080811DYAALLFUND143) Fact Sheet for February, 2012

Fund Manager's Comments In the month of February, The domestic market too continued its upward journey which started early in January on the back of the strong FII flow and improvement in the macroeconomic trends. The major event during the month was the Greece bailout and the second round of LTRO (Long term Refinancing Operations) funding by the European central bank. These events has eased the liquidity in the system and prompted investors to again look back to the riskier investments. On the domestic side, the continued moderation in the inflation has sparked a talk of the reduction in the interest rate by RBI. Going ahead; the UP election results, Union Budget, RBI monetary policy, crude prices and Europe and US situation will determine the direction of the markets. We expect the consolidation phase for the domestic markets to continue for a few more months. During the month, we continued to be over-weight on Oil & Gas, Pharma, Banking, Auto and other consumption themes. Going ahead, we would tactically reduce cash levels to deploy in good stories at attractive levels. The exposure to equity will be tilted towards low beta stocks that are having attractive value proposition.

A Joint Venture of

Toll Free No. 1800 209 8700 SMS <FIRST> to 56677, SMS charges apply. Website: www.indiafirstlife.com Disclaimer: Some of the contents of this document may contain statements / estimates / expectations / predictions, which may be 'forward looking'. The actual outcomes could differ materially from those expressed /implied in this document. These statements, do not intend to provide personal recommendation to any specific individual or any investment needs of an individual. The recommendations / statements / estimates / expectations / predictions are of general in nature and may not take into account the specific investment needs or risk appetite or financial situations of individual clients. Therefore, before acting on any advice or recommendations contained in this document, readers, in their own interest, should consider seeking advice from any authorized and professional investment advisors or financial consultants.'