Embed Size (px)

Citation preview

Individual Equity Return Data From Thomson Datastream: Handle with Care!

December 2003

PRELIMINARY (Please do not quote without permission)

* PO Box 117168, 321 Stuzin Hall, Gainesville, FL 32611-7168. Email: [email protected] and [email protected]. Phone: (352) 392-8928. We would like to thank Ralf Elsas.... for their many helpful comments. Any remaining errors remain ours alone.

1

Abstract

We compare individual equity return data from Thomson Datastream (TDS) for one large national equity market, the United States, to the source most often used by academics, the Center for Research in Security Prices (CRSP) for the period 1975-2002 in order to evaluate the suitability of TDS for use in studies involving large numbers of individual equities in markets outside the U.S. We discover important issues of coverage, classification, and data integrity and find that naive use of TDS data can have a large impact on economic inferences, particularly early in the sample period and among smaller stocks. We show that after careful screening of the TDS data that although differences remain, inferences drawn from TDS data are similar to those drawn from CRSP.

2

I. Introduction

International asset pricing occupies a prominent position in the finance literature.

From a U.S. perspective, non-U.S. equity markets provide an opportunity to verify results

from tests using U.S. data. The study of all markets is also interesting in its own right.

Studies of market integration, market comovement, the benefits from international

diversification etc., add to our understanding of finance in an important way. A

necessary condition for conducting such research is the availability of high quality equity

return data. There exist many sources for non US equity return data including that

maintained by the Pacific-Basin Research Center (PACAP) for eight Asian markets

beginning in 1975 as well as the individual markets themselves. Alternatively, many

researchers have used Thomson Datastream (TDS) for its broad and deep coverage. We

know of no current alternative to TDS in terms of number of markets covered and stocks

covered in each market.

We evaluate the use of Thomson Datastream data for academic research by

comparing TDS data for U.S. equities to the "standard" academic source, The Center for

Research in Securities Prices (CRSP). The CRSP data is maintained specifically for

research of US equity markets so is an appropriate standard. We are not evaluating TDS

vs. CRSP per se; rather we use the comparison between the two databases to identify

issues that may be relevant in the use of TDS data for non-U.S. equities. In all of what

follows we never use CRSP to make corrections to TDS, rather we screen the TDS data

independently then compare the results to CRSP to see how well our proposed screens

perform. Since users of international TDS equity data rarely have an independent source

available, the procedures we develop must not require an independent data source in

order to be of practical use.

To our knowledge, this is the first formal examination of the TDS equity return data

as a research database even though several papers make use of worldwide equity return

data from this source. Examples include Griffin, Ji, and Martin (2003) and Naranjo and

Porter (2003) who examine the interaction between country neutral momentum strategies,

Griffin (2002) who examines whether country-specific or global versions of Fama and

3

French's three factor model better explain time-series variation in international stock

returns, and Porter (2003) who investigates the interaction between market-wide liquidity

shocks in national equity markets. Many authors use Thomson Datastream to compile

samples of all stocks traded within a national market. Examples include Clare and

Priestley (1998) for Malaysian stocks, Brooks, Faff, and Fry (2001) for Australia,

Pinfold, Wilson and Li for New Zealand, Hiller and Marshal (2002) in the U.K., Lau,

Lee, and McInish (2002) for Singapore and Malaysia, and Elsas (2003) for Germany.

We focus on issues of coverage, classification, and data integrity. We begin by

downloading price, shares outstanding, and total return data for all equities traded in the

U.S. and included by TDS in their research lists and lists of equities that are no longer

traded (dead) for the period 1975-2002. We compare this data to the CRSP universe

during the same time period.

Our investigation reveals several problems with using TDS data for research

involving broad market coverage. Most troubling is the inability to easily distinguish

between the various types of securities traded on equity exchanges. We also find that

classification variables often reflect only the most current values. For example, a security

that begins trading on the Nasdaq NMS and later delists and begins trading on the non-

Nasdaq OTC market would be classified as a non-Nasdaq OTC security by TDS

throughout the sample period. We also identify several issues with calculating total

returns using return variables provided by TDS.

Most of the problems identified in this paper are concentrated among the smaller size

deciles calculated using NYSE breakpoints. We illustrate the effects of these problems

on inferences by reporting sample statistics on size decile portfolios and by reporting the

profits from simple momentum strategies. It is well known that portfolios short recent

losers and long recent winners will be concentrated in smaller stocks since small stocks

tend to have higher variance; therefore data problems with calculating returns of small

stocks will likely show up in momentum portfolio returns. We find that the well

documented momentum effect in returns is not detectable in the raw TDS data.

4

We screen the TDS data in two steps. First we attempt to identify the non-common

equity securities included in our TDS sample. Second we run a series of screens to

identify 'unusual' return patterns and either replace the returns in question using

information contained in other TDS variables or drop the observations from our sample.

Although we develop our rules for screening observations using only information from

TDS, we verify using CRSP that our screens do not drop valid observations.

We give an overview of the Thomson Datastream data in Section II, and document

our extraction methods. Section III compares the coverage of TDS and CRSP in the U.S.

Section IV identifies idiosyncratic problems with using TDS return data, Section V

compares dividend data from CRSP and TDS and Section VI summarizes our findings

and concludes.

II. Datastream Overview

Thomson Datastream (TDS) has price, volume, market capitalization and dividend

data for approximately 50,000 equities covering 64 developed and emerging markets with

up to 25 years of data. There is also considerable accounting, fixed income, index,

commodity, macroeconomic time series, interest rate, and exchange rate data available,

although none of this is discussed in this paper.

To download security data we make use of constituent lists. TDS constituent lists are

maintained by TDS and contain all firms in an industry, sector or market. Each list

contains the TDS identification numbers of all firms that are part of the list. We use lists

FAMERA – FAMERZ (one list for each letter of the alphabet) for equities currently

trading in the U.S. and DEADUS1 – DEADUS6 for equities that are no longer traded.

We download daily data for all days between 1/1/1975 and 12/31/2002 and create

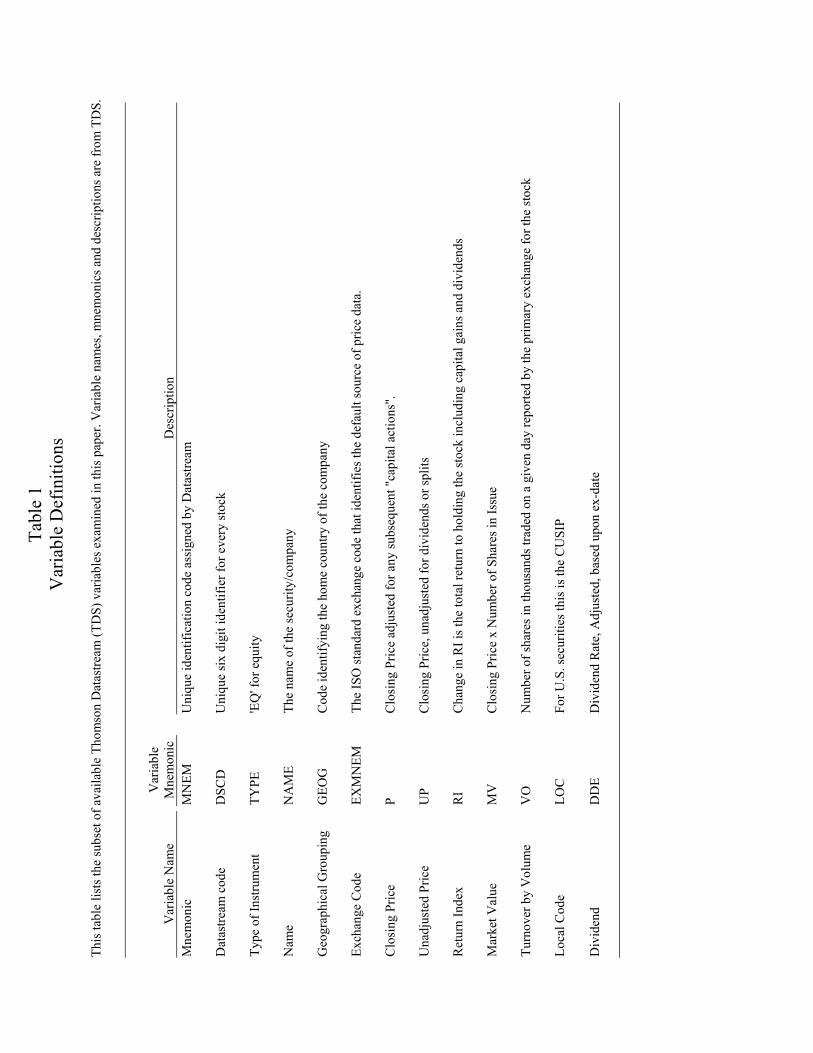

monthly returns from end-of-month daily data1. Table 1 lists the TDS variables we use

and their definitions. For comparison we use the entire CRSP universe for the same time

period including delisting returns and partial period data.

1 This yields exactly the same return series as requesting monthly frequency data. We request the more detailed data to help us in developing rules to screen the data.

5

Extracting a large volume of data from TDS can take many days due to limitations on

how much data can be extracted in a day. The length of time required along with the

constant updating nature of the data can cause some difficulties. For example, we

download the current data first followed by the dead equities, otherwise a firm that ceases

trading while the data is being extracted will be lost.

The approach used by TDS and CRSP when a user requests data after a firm ceases

trading is different. CRSP will report no data whereas TDS reports the last valid data

point. TDS pads the time period after the firm ceases trading with constant values equal

to the last month (or day) that the firm traded. To identify and eliminate these dummy

records we delete all monthly observations from TDS from the end of the sample to the

first non-zero return. We realize that a small number of valid zero return observations

may be lost at the end of the sample2.

Table 2 provides summary statistics on the data from the two sources with non-

missing return data. We have 22,832 unique permnos (CRSP Permanent Issue Number)

and 2,256,605 monthly observations from CRSP and 21,245 unique TDS identifiers and

2,048,255 observations from Thomson Datastream. Of the CRSP observations,

1,941,744 or 86% are share code 10 and 11 defined as common equity of U.S. based

companies. Most market studies using CRSP data restrict themselves to these share

codes. Of the TDS observations, 2,002,459 or 98% have TYPE equal to EQ (Equity).

Within common stock, CRSP has 503,107 monthly NYSE observations compared to

TDS with 946,940, or almost twice as many as CRSP. As we will show, most of this

discrepancy is due to the inclusion of non-common equity securities by TDS that are

traded on the NYSE. Somewhat surprisingly, there are fewer TDS observations

associated with AMEX (124,521) and Nasdaq (472,398) than CRSP observations on the

same exchanges (230,497 and 1,208,137 respectively).

2 TDS lists a variable "TIME" defined as "date of last equity price data", however a random check of several securities shows this variable to be uninformative for U.S. equities. In many cases the variable value is #N/A (for example: Integrated Silicon Systems) or the value does not coincide with actual return data available on both TDS and CRSP (see EMS Systems whose value for the TDS variable TIME is 12/29/1989 but has valid CRSP and TDS data through May (CRSP) and April (TDS) of 1990.)

6

We show the potential impact on inferences by calculating equal-weighted market

returns, equal-weighted returns by exchange, size decile returns, and the returns to two

momentum trading strategies. Our CRSP dataset for this exercise contains all equities

with share code equal to 10 or 11 (common equity) and that are traded on the NYSE,

AMEX, or Nasdaq exchanges. The TDS dataset contains all securities of type 'EQ'

(equity) and have an exchange identifier of NYSE, AMEX, Nasdaq-NMS, or Nasdaq-

nonNMS. No other data screens or checks have been used. Table 3 presents the results.

The TDS equal-weighted average market return of 2.40% per month is 72% higher

than the comparable CRSP average return of 1.41% per month. The time series

correlation of the equal-weighted market return series is 0.66. The value-weighted

market returns are more similar with nearly identical mean returns and a time series

correlation of 0.998, implying the differences between the two datasets is concentrated

among smaller issues.

Comparing equal-weighted returns by market we see that the biggest difference is

among AMEX firms, although as we will see later this is due in large part to errors in the

return data. Mean returns calculated from TDS are also much higher than those

calculated from CRSP for both NYSE and Nasdaq firms. The NYSE return series have a

correlation of 0.84 and the Nasdaq series have a correlation of 0.93. Comparing size

decile returns we see the largest differences in the smaller deciles.

The momentum trading strategy results are consistent with the large disparity in the

smaller decile returns between the two data sources. Using CRSP data, a strategy long

the top 10% of firms ranked on average return over months t-2 through t-12 and short the

bottom 10% and held for one month before rebalancing, referred to in the table as a 1090

strategy, earns an average monthly return of 1.13% with an associated t-statistic of 2.86.

A comparable strategy using TDS data results in an average of 0.26% per month and we

cannot reject the null that the average return is zero. The results from a 3070 strategy are

even more different with the return calculated from CRSP data equal to and average of

0.95% per month with an associated t-statistic of 3.65 while the average return calculated

from TDS is negative.

7

It is clear that there are important differences between the two data sources and that

these differences are concentrated in the smaller size deciles. In the next section we

explore differences in coverage between the two data sources and discuss a method of

screening the TDS database for securities that researchers may wish to exclude.

III. Coverage

To isolate the differences in coverage between the two data sources we match the

databases security by security using the last firm observation in each year between 1975

and 2002. We link securities using combinations of CUSIP, ticker symbol, and name.

We manually verify a sample of matching firms and nonmatching firms to confirm the

quality of our matching process.

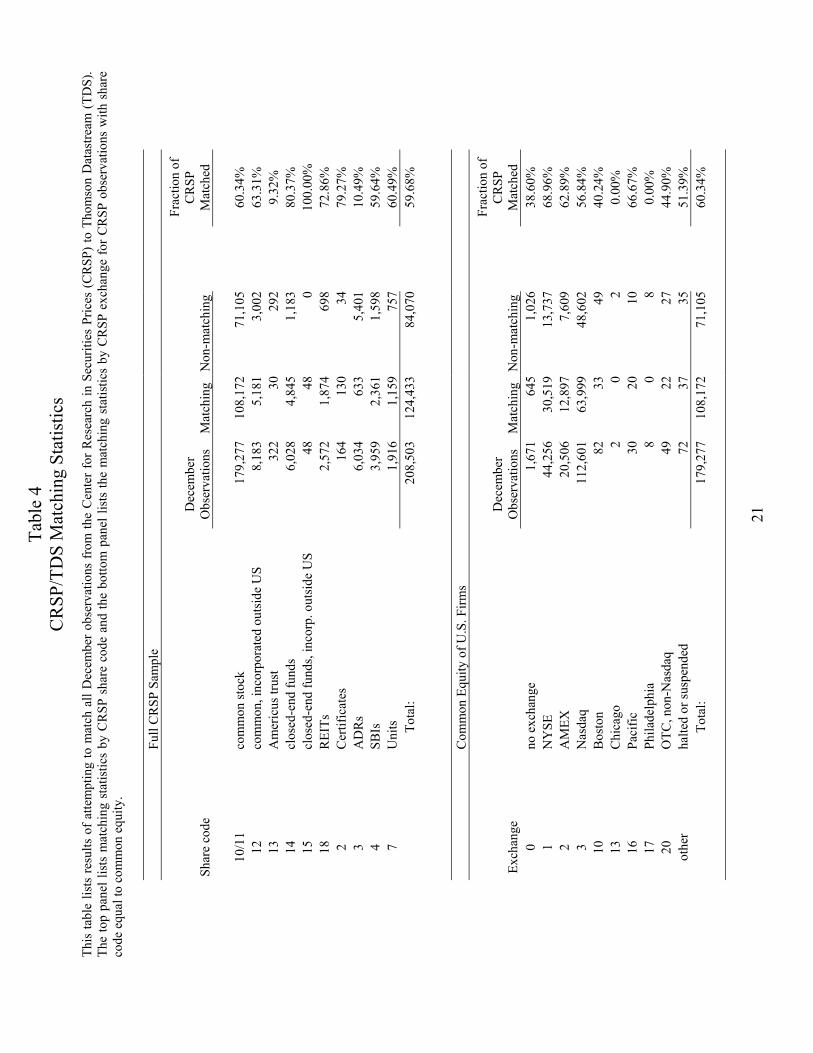

Table 4 summarizes the results of our matching exercise. We are able to match 60%

of December CRSP observations with share code 10 and 11 to December TDS

observations. The rate at which we match CRSP NYSE common equity (69%) is slightly

higher than for either AMEX (63%) or Nasdaq (57%). The matching is much better later

in the sample period than in earlier years.

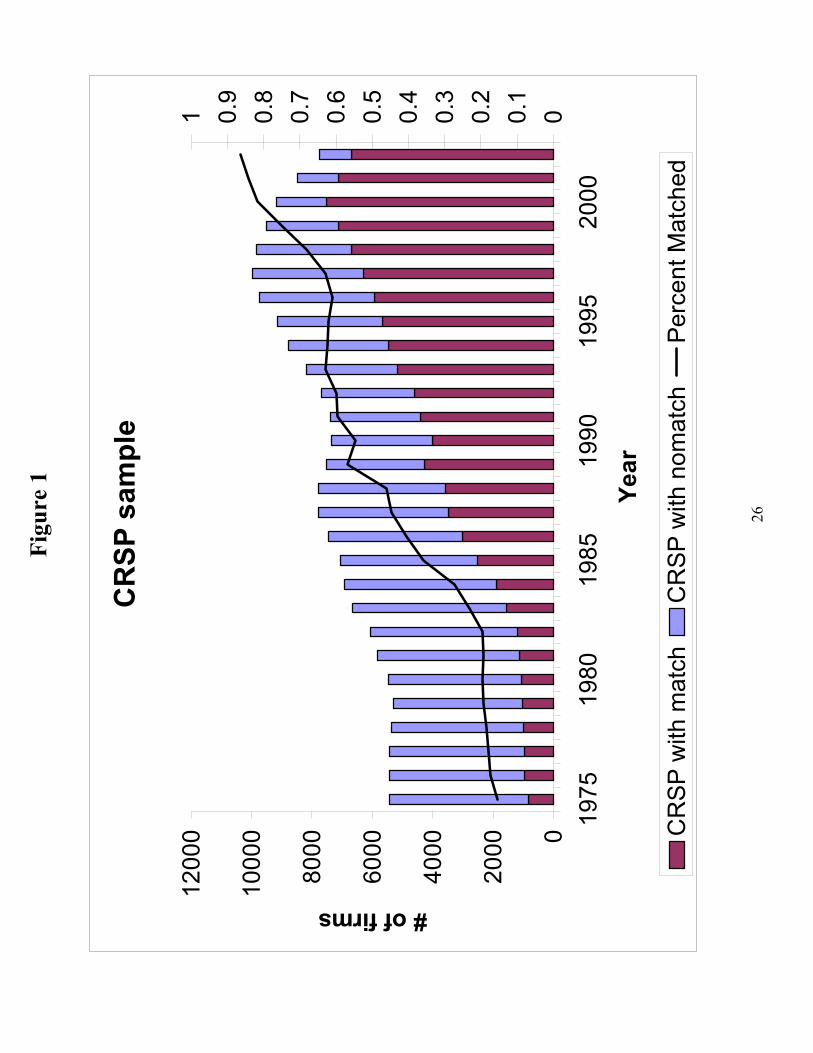

Figure 1 summarizes the fraction of CRSP permnos that are also found in TDS in

December of each year. Approximately 20% of the CRSP sample is also in TDS in

December of 1975 and this fraction rises steadily throughout the sample reaching almost

90% by December of 2002. Of the December 2002 CRSP observations that we are

unable to match to TDS, approximately half are ADRs (share codes 30 through 39 for

which TDS maintains separate constituent lists) and the remainder are firms that are

either absent from the TDS constituent lists or exist on TDS with different CUSIP

numbers than on CRSP.

We are surprised that not all firms that cease trading are included on the TDS

constituent lists of inactive firms, DEADUS1 through DEADUS6, and therefore do not

appear in our sample. Using the TDS interactive utility, Advance Version 4.0, we are

able to locate several large firms that have ceased trading and are not included on the

8

dead constituent lists. Examples include such well known names such as Atlantic

Richfield Co., GTE Corp, and Honeywell.

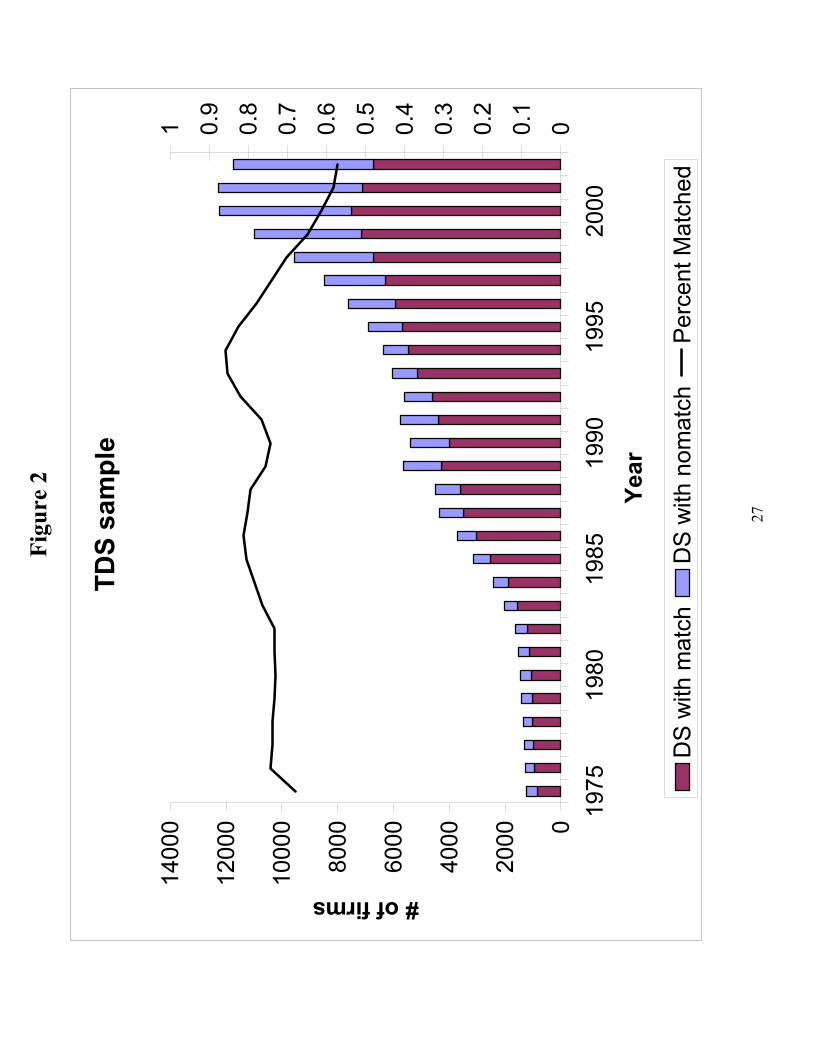

Figure 2 summarizes the fraction of TDS identifiers with TYPE equal to 'EQ' that are

also found in CRSP in December of each year. Approximately 70-80% of the TDS

sample is also on CRSP until the mid 1990s when the fraction steadily falls until only

55% of the TDS sample is also on CRSP in December of 2002.

The large number of TDS identifiers with no corresponding CRSP permnos,

especially late in the sample period, is due in large part to the fact that TDS includes

many securities with a type indicator of "equity" that are not common stock of U.S. firms.

Such securities include stock of firms incorporated outside the U.S., closed end funds,

REITs, ADRs (although there are very few ADRs on the TDS equity lists since there are

specific TDS constituent lists for ADRs), Shares of Beneficial Interest, and traded

partnership units. Researchers using CRSP data commonly restrict the sample to share

codes 10 and 11, however there is no simple method for performing the same screen with

TDS.

Since the only other source of information about the security is the variable NAME,

we search the NAME variable for key words or phrases that may indicate the security is

not common equity. Our procedure is to search the name field for key phrases, create a

candidate list of firms for removal by extracting all observations containing those

phrases, and then review the list of observations for any firms which should not be

removed from the sample. For example, we search for the letter combinations 'pf' and

'pref' to identify preferred stock, but explicitly prevent removing 'Pfizer'. We use the

TDS variable GEOG to remove any firm incorporated outside the U.S and the EXMNEM

variable to exclude any firm not traded on the NYSE, AMEX, or Nasdaq. Our screening

process reduces the number of TDS observations from 2,002,459 to 1,267,218, a

reduction in sample size of 37%. We repeat our calculation of market portfolio returns

and momentum portfolio returns using the TDS screened sample and compare the results

to our CRSP sample. The third set of columns of Table 3 reports our results. The results

are similar to the unscreened sample implying that the large differences in market returns,

9

size decile returns, and momentum returns are not due solely to the inclusion of securities

other than common equity by TDS.

IV. TDS Data Issues

Our goal is to develop methods for identifying data errors in TDS than can be used in

markets outside the U.S. for which an alternative data source is not readily available to

the researcher. In developing these rules we make extensive comparisons of CRSP and

TDS matched data but we take great care that no screen or correction we develop would

require the use of such an outside source.

Several TDS data errors we identify would be difficult, if not impossible to identify

without an alternative data source. For example, in June of 1992 Big O Tires, Inc

(permno=92508) conducted a 1:5 reverse stock split that is reflected in the shares

outstanding and closing price from CRSP. The unadjusted price series in TDS matches

that in CRSP, including the large rise in price level in 6/1992, however the change in

shares outstanding and adjusted price is in 6/1990 resulting in an incorrect return index

and return in June of 1990 and 1992 and an incorrect shares and market value for the full

two year period.

To be fair, TDS often does a better job than CRSP in reflecting capital structure

changes. For example, TDS will often reflect a seasoned equity offering on or very near

the day of the offering, however CRSP will not reflect the additional shares or the change

in market capitalization until the end of the quarter or fiscal year3. For example,

Nashville Country Club, Inc (now known as TBA Entertainment, CRSP permno=80256)

offered shares in a seasoned offering in April of 1996 but the additional shares are not

reflected in CRSP until 12/27/1996. The TDS data reflects the additional shares in May

of 1996. Since market value is derived from shares outstanding, the CRSP market

capitalization for this firm is incorrect for the eight month interval.

There are other differences in which it is not clear which data source is 'correct'. The

closing prices used by each source often do not agree. For example, according to CRSP, 3 Thank-you to Jay Ritter for providing an alternative source of SEO offer dates and share quantities.

10

Apogee Technology Inc, closed in May of 1990 at $4.625 and in June at $9.75 for a

return of 110.81%. The same firm is listed in TDS closing in May at $4.00 and in June at

$9.50, for a return of 137.50%, a difference of 26.69%. Note also that CRSP maintains

prices in increments as small as 1/64 while TDS rounds all prices to the nearest penny

resulting in differences in return, particularly for low priced stocks. Both CRSP and TDS

report closing price as a bid/ask average on days in which the stock does not trade.

To check for errors in return calculated from changes in the total return index, we

calculate returns using price and dividend data and compare it to the percentage change in

the return index. We only compare the two returns in months in which the ratio of

adjusted price to unadjusted price is the same as the previous month in order to prevent

differences in the two return calculations from being due to a capital structure change.

The TDS practice of rounding prices to the nearest penny can cause non trivial

differences in the calculated return when prices are small, so we drop all observations in

both TDS and CRSP when the end of previous month price is less than $1.00.

A related problem is the discreetness of the TDS total return index. The return index

is reported to the nearest tenth so when the return index is very small, discreetness

becomes important. To see why this is true, consider Firepond Inc. in October and

November of 2001. According to TDS, Firepond closed at $4.70 in September, $7.89 in

October and $8.00 in November. The corresponding values of the total return index are

0.5, 0.8, and 0.8. No dividends or capital changes occurred in this period. The returns

calculated from price changes are 67.87% and 1.39% whereas the returns calculated from

the return index changes are 60.00% and 0.00%. In these cases we substitute return

calculated directly from prices for returns calculated from the return index.

Suspension of trading is handled differently by the two sources. CRSP reports

missing values for prices and daily returns, however while monthly returns are reported

as missing if trading is suspended at the end of the month, the return for the first month

after trading resumes is calculated using the last available end of month price, even if the

intervening time interval is long, and without accounting for the multiperiod nature of the

return. For example, Ormand Industries (permno=34905) stopped trading on 5/31/1990

11

and resumed trading on 9/19/1990. The September return is calculated from the end of

month price, 0.68750 and the last valid end of month price, 4/30/1990, of 0.43750,

resulting in a simple 1-month reported return for September of 57.14%. TDS reports

sporadic trades during this period with changing prices. The way in which CRSP

calculates returns after the resumption of trading and the difficulty of identifying trading

halts on TDS can cause large difference in monthly returns between the two sources.

Since we are unable to identify trading suspensions using only TDS data, we make no

corrections for this problem.

We identify many instances of data errors. According to TDS, in the first eight

months of 1995, Magellan Petroleum Corp never has a daily closing price above $2.38

but the closing prices for 7/31, 8/1, and 8/2 are all above $13.60. On 8/3 the price reverts

to $1.88. The closing prices on the three days in question on CRSP are 1.9375, 1.8750,

and 1.9375. The resulting monthly TDS return for July is 626.69% vs. a CRSP reported

return of 0.00%. We screen for such occurrences by setting any return above 300% that

is reversed within one month to missing.

After screening the TDS equity data for non common equity securities and searching

for data errors as described above we recalculate the portfolio returns for the same

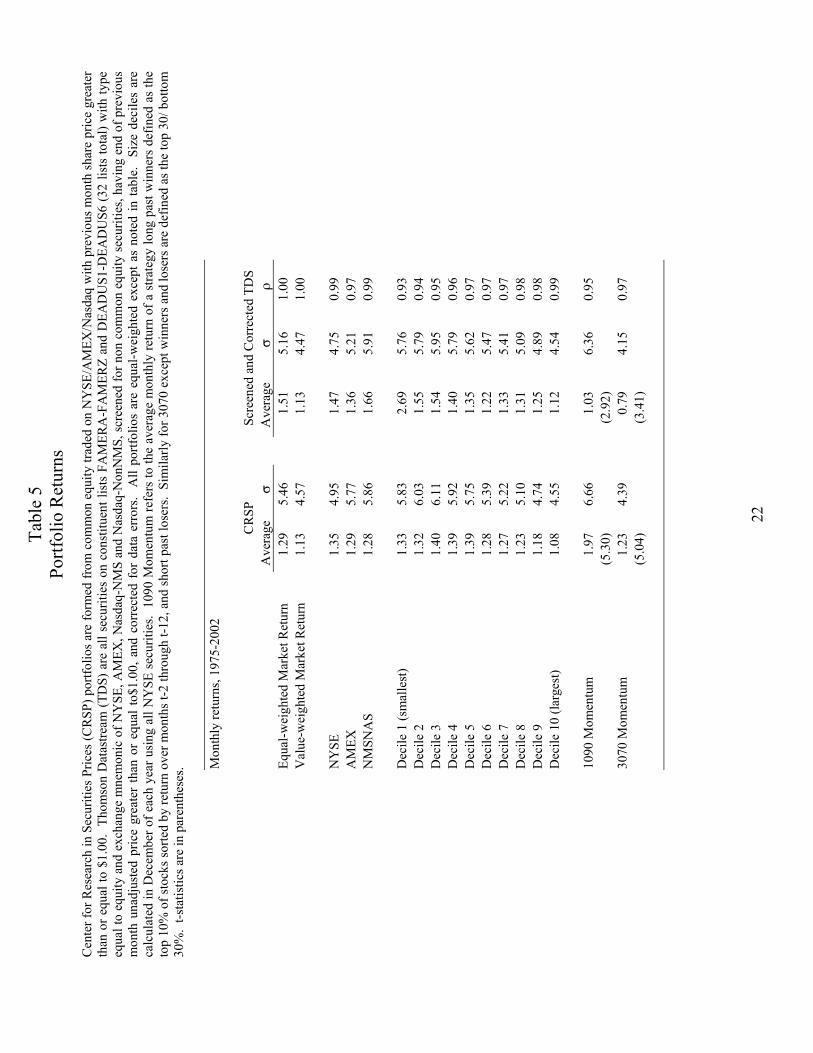

portfolios reported in Table 3. The results are reported in Table 5. We report revised

CRSP results as well because we have dropped CRSP observations with previous month

price less than $1.00. In calculating momentum returns we only enforce the price

restriction during the portfolio formation period and not during the holding period.

The TDS portfolio returns are now much closer to those calculated from CRSP. The

average CRSP equal-weighted market return is 1.29% per month compared to the TDS

equal-weighted market return of 1.51%. The correlation between the two equal-weighted

market indexes is 0.995 and the correlation between value-weighted indices is 0.998.

The individual market return means and standard deviations are also similar and the

correlations are high. The momentum returns that for TDS were insignificant and

sometimes negative are now positive, significant, and highly correlated with the

12

momentum returns calculated from CRSP4. In unreported results, we delete all

observations not common to both datasets and calculate all of the portfolio returns.

Although differences remain, they are generally quite small.

There are several reasons why we should not expect the CRSP and TDS results

reported in Table 5 to be identical. First is the issue of coverage. Not only will this

affect the average market returns but also the NYSE size breakpoints. In addition, the

issue of classification errors will induce a survivorship bias in a TDS sample of

NYSE/AMEX/Nasdaq firms. Since firms with poor returns are more likely to be delisted

and TDS captures only the most recently available exchange information, firms that delist

from the major exchanges and trade over-the-counter will be excluded from the TDS

sample raising the average return of the firms that remain.

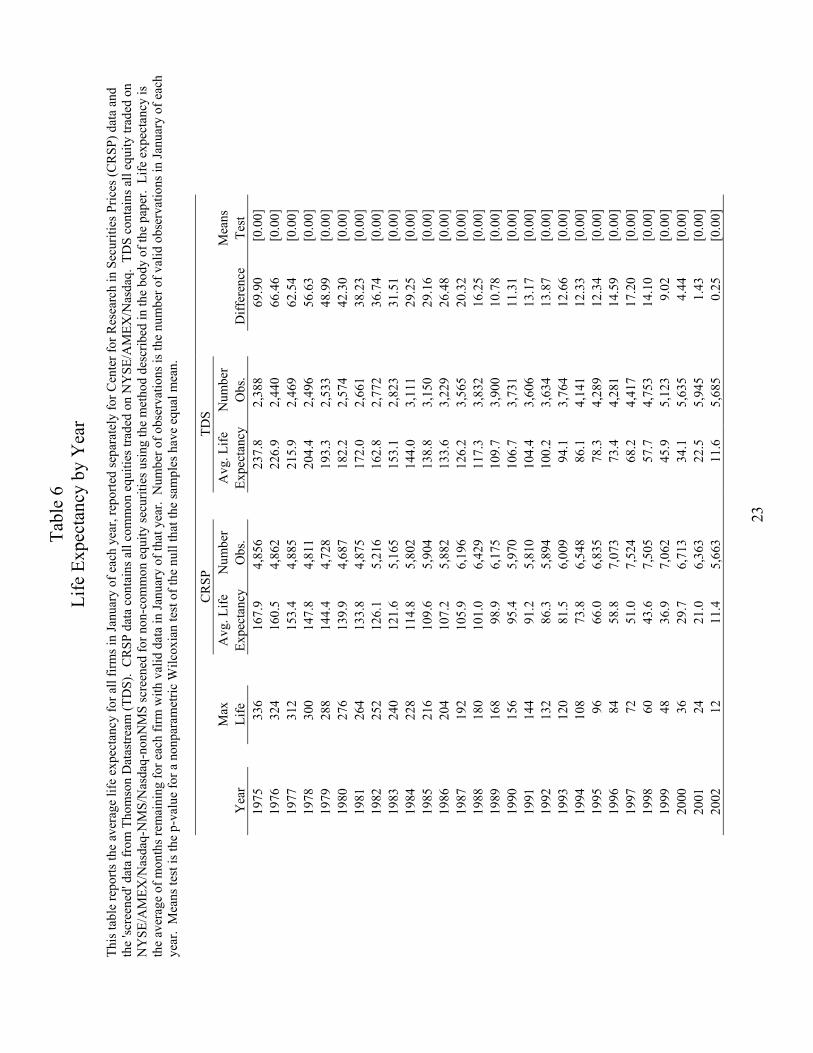

We illustrate the survivorship issue by calculating life expectancy for every year in

each sample. In January of each year, for all firms with valid observations in that month,

we estimate the life expectancy of a firm by averaging the number of months that each

firm remains in the sample. The 'life' of a firm has a maximum value equal to the number

of months remaining before December of 2002. Panel A of Table 6 reports the results.

In every year the average number of months remaining is larger for TDS than for CRSP

implying that firms that delist are less likely to be included in the TDS sample. A

nonparametric Wilcoxian rank-sum test for difference in mean easily rejects in every

year.

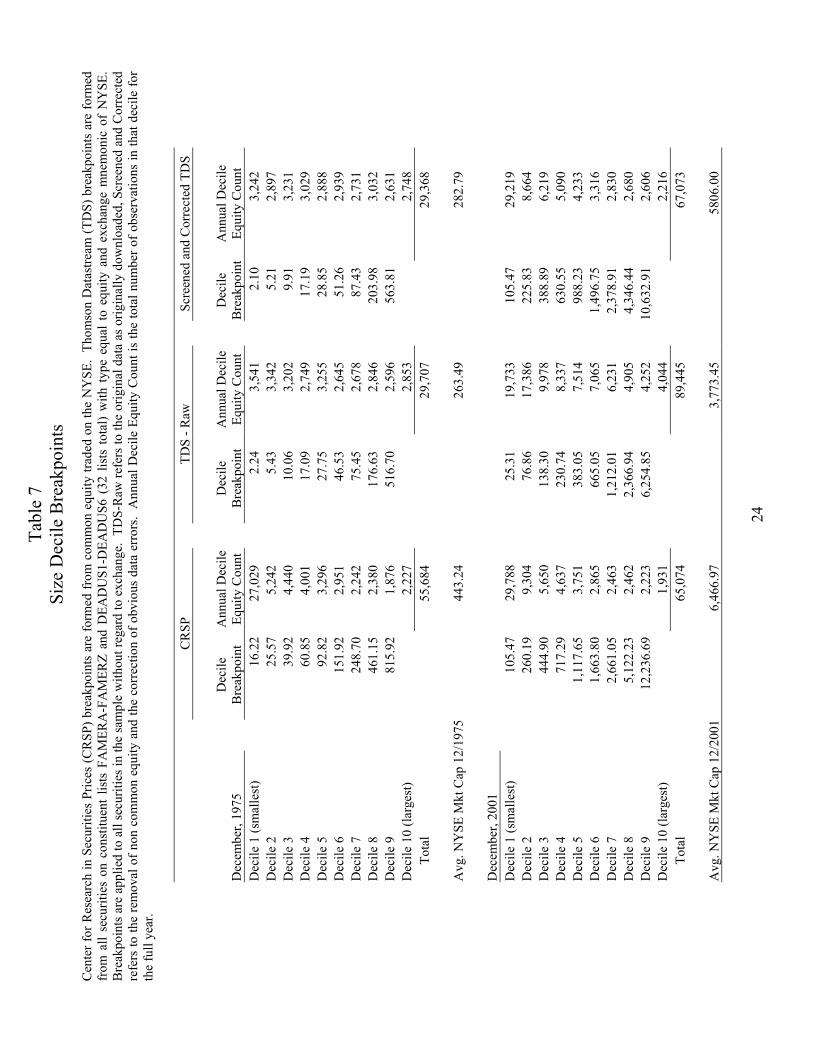

In addition, the issue of classification makes it difficult to identify NYSE firms from

which the breakpoints are calculated, particularly early in the sample period. Table 7 lists

the breakpoints calculated at the end of 1975 and 2001 calculated for stocks classified as

trading on NYSE for each of TDS and CRSP. The first set of columns list breakpoints

and the number of firms/month observations falling in each decile using CRSP, the

second set of columns list breakpoints and observations calculated from the 'raw' TDS

4 The CRSP 1090 momentum return of 1.97% per month is very high by the standards of the literature, however this value is not due only to dropping firm with prices less than $1.00 during the portfolio formation period. Restricting the sample to observations that exist on both CRSP and TDS lowers the CRSP 1090 momentum return to 1.38% per month.

13

data and the third set of columns refer to the TDS data after screening for non U.S. and

non common equity securities.

In December of 2001, the CRSP and screened TDS size decile breakpoints and equity

counts are very similar. The difference in breakpoints between the raw and screened

TDS samples show that most of the screened securities have very small market

capitalization. This is also reflected in the average market capitalization figures. The size

breakpoints are very different between the samples in December of 1975. Interestingly,

the number of firms from which the breakpoints are calculated is higher for the screened

and corrected TDS sample (2044) than for the CRSP sample (1429). The smaller average

NYSE market capitalization figure combined with the larger number of observations and

the smaller breakpoints implies that the additional firms are quite small. We believe this

is due to stale exchange information. For CRSP, the ratio of the number of observations

in decile 1 to the number of observations in decile 2 for 1976 is over 5:1 because the

average Nasdaq/AMEX firm is much smaller than the average NYSE firm. The

comparable ratio for TDS for 1976 is only 1.1:1. Taken together, these facts suggest that

the TDS size breakpoints have not been calculated only from stocks that traded on the

NYSE at the end of 1975. By the last year of the sample period the breakpoints and

distribution of firms by decile are much more similar.

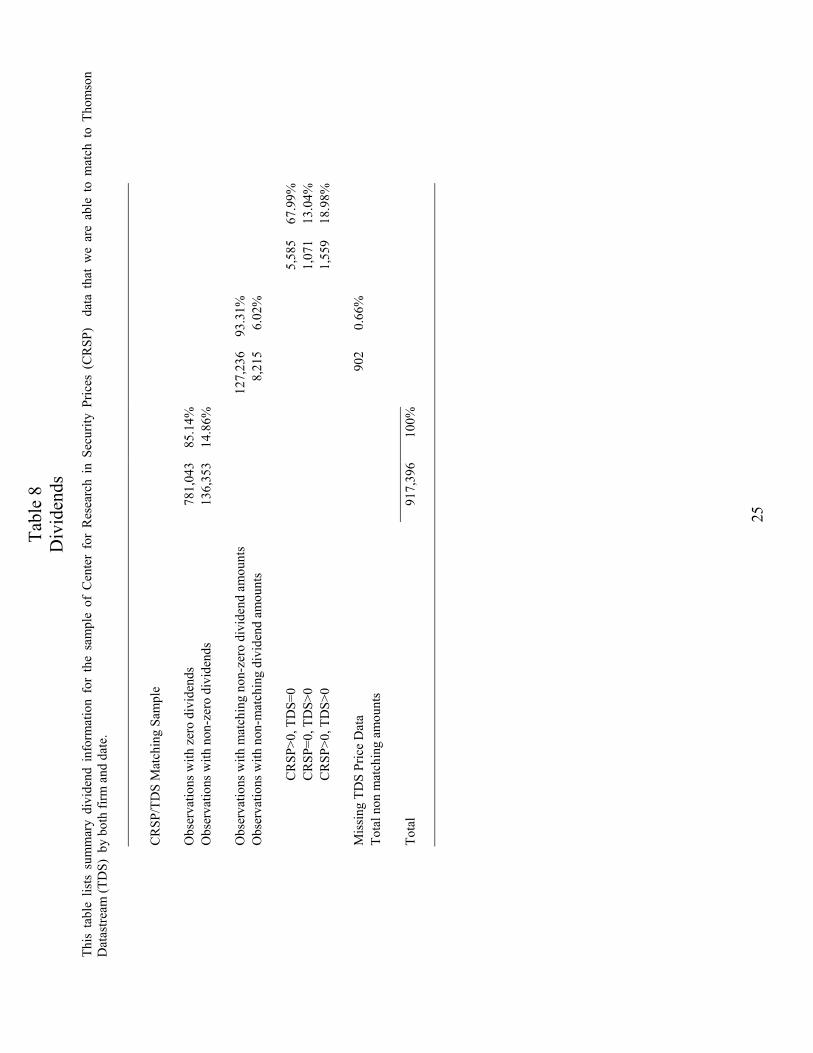

V. Dividends

We also compare the dividend information provided by CRSP and TDS. We

compare CRSP dividends coded as ordinary or liquidating cash dividends to all TDS

dividends. We use the TDS dividend adjusted for capital changes and recover the

original dividend amount by multiplying the adjusted dividend by the ratio of unadjusted

price to adjusted price.

First we examine the common set of observations and find that of 136,353 firm

months in which either CRSP or TDS show a dividend payment, 127,236 or 93.31% of

the firm months show identical dividend amounts from each source. 8,215 dividend

observations or 6.03% disagree by the dividend payment amount and 902 observations or

0.66% have non zero values for TDS dividends but unadjusted prices are missing so

14

dividends before any capital changes cannot be calculated. Of the 8,215 observations

that disagree as to the dividend amount, 68% have positive dividends payments according

to CRSP and zero according to TDS. 13% have zero dividends according to CRSP and

positive according to TDS with the remainder showing positive dividends on each source

but disagreeing on the dividend amount.

Many of the observations that show positive dividends on CRSP and zero dividends

on TDS are for firms paying regular dividends. For example, the NYSE listed firm

American Can Co., later renamed Primerica Corporation (CRSP permno=10241) paid a

quarterly dividend every quarter from 1Q75 through 3Q88 in per share amounts from

$0.40 to $0.725 per share, however the first dividend reflected in TDS is in January of

1987.

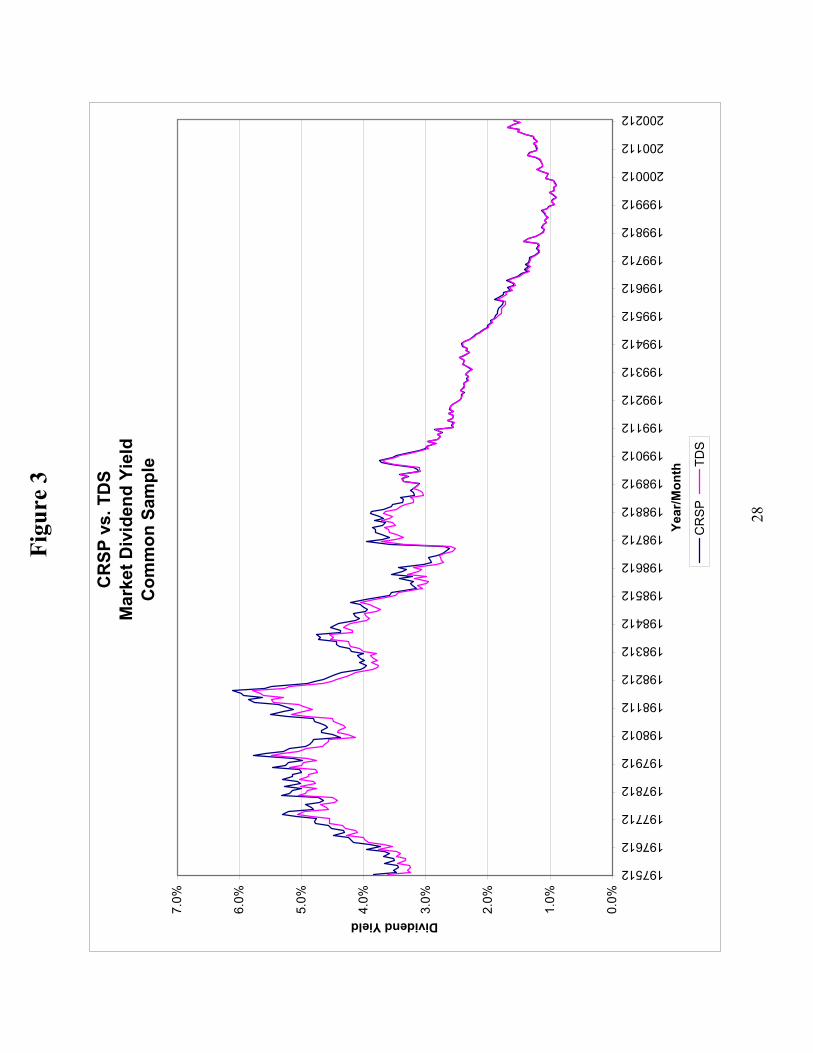

We calculate market dividend yields as the sum of all dividends paid during the

previous year calculated as per share dividend times shares outstanding computed from

market value and price, divided by the sum of all firm's market values. Figure 3 plots the

monthly dividend yields for the combined NYSE/AMEX/Nasdaq sample. Although the

time series of the two dividends yields is similar throughout the sample period, the fit is

better in the latter half. The common sample dividends yields have a correlation of 0.996.

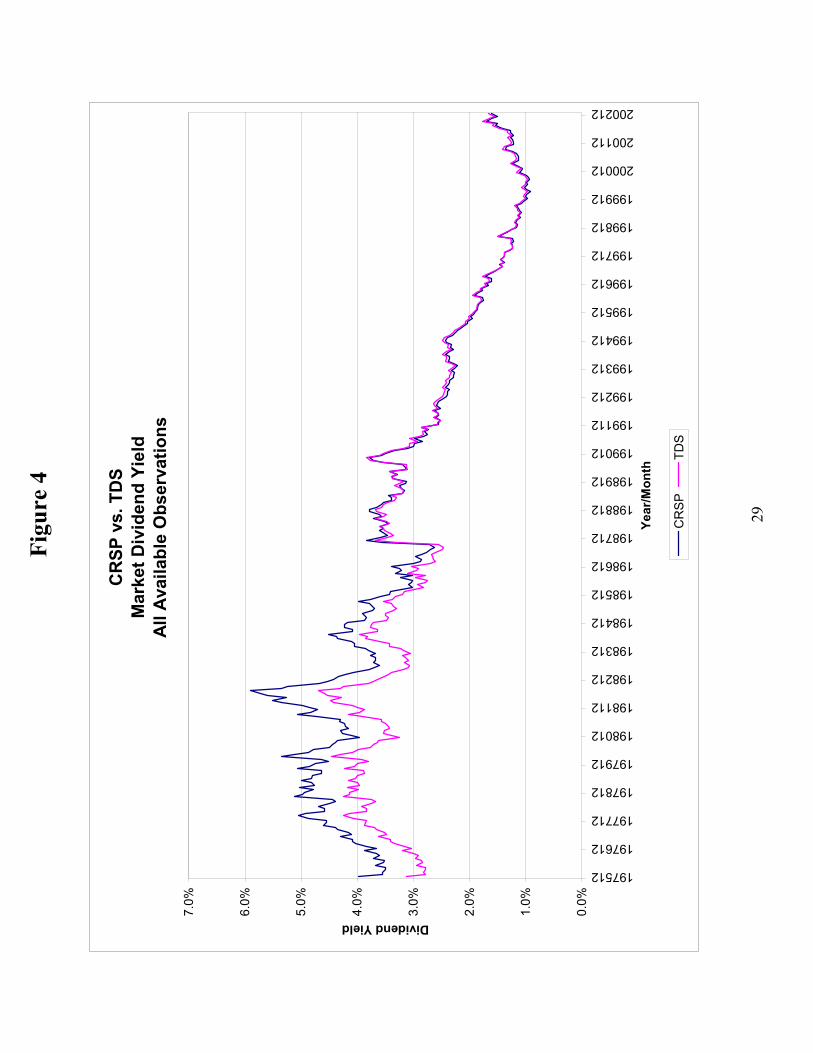

We recalculate market dividend yields without restricting the sample to matched

observations. Figure 4 plots the results. The CRSP dividend yield is higher than the TDS

dividend yield in the first half of the sample although they do move together. In the

second half there appears to be little difference in the two measures. The correlation of

the two measures of the market dividend yield is 0.982.

VI. Conclusion

Thomson Datastream is a rich data source containing equity return data for

approximately 50,000 equities in 64 developed and emerging markets with up to 25 years

of data; however, issues of classification, coverage, and data integrity require that care be

used. We compare Thomson Datastream (TDS) data for U.S. equities to data from the

15

Center for Research in Securities Prices (CRSP) in order to identify features of the TDS

data that might cause errors in inference for the unwary researcher.

We find that TDS includes data for many securities with type equal to 'EQ' (equity)

that the researcher may wish to exclude from her sample. Examples of such securities

include preferred stock, traded warrants, REITs, closed-end funds, exchange traded

funds, and shares of beneficial interest, however to the best of our knowledge there is no

simple method for classifying these securities. By scanning the security name field for

clues as to the security type, we are able to identify over 35% of the monthly

observations as not being common equity.

We also find several errors related to the country constituent lists maintained by TDS.

We identify several examples of large firms for which TDS maintains data but that are

not included on the appropriate constituent list and hence will not be downloaded by the

researcher. Since we can only check for missing firms manually, by identifying firms

that exist on CRSP and are not in the data we download from TDS, we are not sure how

common this problem is, however we do not have trouble finding several large firms that

are not on the TDS lists of non-traded (dead) firms. We also have no way of knowing

how common this problem is in other markets.

We also find that the exchange information provided by TDS usually applies only to

the exchange on which the security is trading when data is downloaded, or for securities

that are no longer traded, the last available exchange. This causes several problems.

First, if the researcher wished to include only securities traded on the major exchange(s)

of a particular country then the sample may include a survivorship bias. Since poorly

performing firms are those most likely to delist and trade over-the-counter, the remaining

firms are likely to have higher average returns. Second, for countries such as the U.S.

with multiple major exchanges, methods such as the using of NYSE determined size

breakpoints can be problematic, particularly the further back in time you go.

We identify many instances of errors in the return data. We compare returns

calculated from changes in the TDS total return index to returns calculated from price and

16

dividend data and either drop observations in which there is a large discrepancy or

substitute the return we calculate for the return calculated from the change in the return

index.

After screening the data for non-common equity and obvious errors in the data, we

find that market-wide, exchange, and decile portfolio returns are quite similar between

TDS and CRSP. We also find positive profits to momentum trading strategies using both

the CRSP data and the screened and corrected TDS data that are statistically significant

and highly correlated. However, the means are quite different but this is not surprising

considering the large discrepancies in coverage, particularly early in the sample period.

In our final judgment, TDS provides an excellent source of equity return data,

however the researcher must take great care to screen and correct the data. We argue that

failure to do so can result in very misleading inferences being drawn from tests using

these data.

17

References

Brooks, Robert D., Robert W. Faff, and Tim R.L. Fry (2001), GARCH Modeling of

Individual Stock Data: the Impact of Censoring, Firm Size and Trading Volume, Journal

of International financial Markets, Institutions and Money 11, pp. 215-222.

Clare, Andrew D., and Richard Priestley (1998), Risk Factors in the Malaysian Stock

Market, Pacific-Basin Finance Journal 6, pp. 103-114.

Elsas, Ralf (2003), Bank debt vs. public debt of German companies, University of Florida

Working Paper.

Griffin, John M. (2002), Are the Fama and French Factors Global or Country Specific?,

The Review of Financial Studies 15, pp 783-803.

Griffin, John M., Susan Ji, and Spencer Martin (2003), Momentum Investing and

Business Cycle Risks: Evidence from Pole to Pole, The Journal of Finance, December

2003.

Hiller, David and Andrew Marshall (2002), Insider Trading, Tax-Loss Selling, and the

Turn-of-the-year Effect, International Review of Financial Analysis 11, pp. 73-84.

Lau, Sie Ting, Chee Tong Lee, and Thomas H. McInish (2002), Stock Returns and Beta,

Firms' Size, E/P, CF/P, Book-to-market, and Sales Growth: Evidence from Singapore and

Malaysia, Journal of Multinational Financial Management 12, pp. 207-222.

Naranjo, Andy and R. Burt Porter (2003), International Momentum Strategies:

Profitability and Cross-Country Relationships, University of Florida working paper.

Pinfold, John F., William R. Wilson, and Qiuli Li (2001), Book-to-Market and Size as

Determinants of Returns in Small Illiquid Markets: the New Zealand Case, Financial

Services Review 10, pp. 291-302.

Porter, R. Burt (2003), Market-wide Liquidity Shocks in International Markets,

University of Florida working paper.

Tabl

e 1

Var

iabl

e D

efin

ition

s

This

tabl

e lis

ts th

e su

bset

of a

vaila

ble

Thom

son

Dat

astre

am (T

DS)

var

iabl

es e

xam

ined

in th

is p

aper

. Var

iabl

e na

mes

, mne

mon

ics a

nd d

escr

iptio

ns a

re fr

om T

DS.

Var

iabl

e N

ame

V

aria

ble

Mne

mon

ic

D

escr

iptio

n M

nem

onic

M

NEM

Uni

que

iden

tific

atio

n co

de a

ssig

ned

by D

atas

tream

D

atas

tream

cod

e D

SCD

Uni

que

six

digi

t ide

ntifi

er fo

r eve

ry st

ock

Type

of I

nstru

men

t T

YPE

'EQ

' for

equ

ity

Nam

e N

AM

E

The

nam

e of

the

secu

rity/

com

pany

G

eogr

aphi

cal G

roup

ing

GEO

G

C

ode

iden

tifyi

ng th

e ho

me

coun

try o

f the

com

pany

Ex

chan

ge C

ode

EX

MN

EM

Th

e IS

O st

anda

rd e

xcha

nge

code

that

iden

tifie

s the

def

ault

sour

ce o

f pric

e da

ta.

Clo

sing

Pric

e P

Clo

sing

Pric

e ad

just

ed fo

r any

subs

eque

nt "

capi

tal a

ctio

ns".

Una

djus

ted

Pric

e U

P

Clo

sing

Pric

e, u

nadj

uste

d fo

r div

iden

ds o

r spl

its

Ret

urn

Inde

x R

I

Cha

nge

in R

I is t

he to

tal r

etur

n to

hol

ding

the

stoc

k in

clud

ing

capi

tal g

ains

and

div

iden

ds

Mar

ket V

alue

M

V

C

losi

ng P

rice

x N

umbe

r of S

hare

s in

Issu

e

Tu

rnov

er b

y V

olum

e V

O

N

umbe

r of s

hare

s in

thou

sand

s tra

ded

on a

giv

en d

ay re

porte

d by

the

prim

ary

exch

ange

for t

he st

ock

Loca

l Cod

e L

OC

For U

.S. s

ecur

ities

this

is th

e C

USI

P

D

ivid

end

DD

E

Div

iden

d R

ate,

Adj

uste

d, b

ased

upo

n ex

-dat

e

19

Tabl

e 2

Com

para

tive

Stat

istic

s

This

tabl

e lis

ts th

e nu

mbe

r of m

onth

ly o

bser

vatio

ns a

nd u

niqu

e se

curit

y id

entif

iers

ava

ilabl

e in

the

1975

-200

2 da

ta fr

om th

e C

ente

r for

Res

earc

h in

Sec

uriti

es P

rices

(C

RSP

) and

Tho

mso

n D

atas

tream

(TD

S).

The

CR

SP id

entif

ier i

s th

e Pe

rman

ent I

ssue

Num

ber (

perm

no) a

nd th

e D

atas

tream

cod

e (D

SCD

) for

TD

S. W

e do

wnl

oad

all a

vaila

ble

CR

SP d

ata

for t

he ti

me

perio

d an

d lis

t cou

nts

by s

hare

cod

e an

d ob

serv

atio

ns b

y ex

chan

ge fo

r sha

re c

odes

10&

11 (c

omm

on e

quity

). W

e do

wnl

oad

all

avai

labl

e TD

S da

ta u

sing

TD

S co

nstit

uent

list

s FA

MER

A –

FA

MER

Z fo

r cur

rent

ly tr

aded

U.S

. equ

ities

and

DEA

DU

S1-D

EAD

US6

for s

ecur

ities

that

are

no

long

er

trade

d. W

e lis

t cou

nts

by ty

pe a

nd fo

r typ

e eq

ual t

o eq

uity

, by

exch

ange

. Su

bcat

egor

ies

of u

niqu

e id

entif

iers

do

not s

um to

ove

rall

coun

ts b

ecau

se o

f cha

nges

in th

e va

lue

of c

lass

ifica

tion

varia

bles

in th

e tim

e se

ries o

f uni

que

iden

tifie

r.

CR

SP

TD

S

Mon

thly

Obs

. U

niqu

e Id

entif

iers

M

onth

ly

Obs

. U

niqu

e Id

entif

iers

To

tal n

umbe

r of o

bser

vatio

n in

sam

ple

1975

-200

2 2,

256,

605

22,8

32

2,04

8,25

521

,245

Sh

are

Cod

e Sh

are

Cod

e D

escr

iptio

n

TYPE

TY

PE D

escr

iptio

n

10

-11

Com

mon

stoc

k 1,

941,

744

19,3

31

mis

sing

1,43

027

12

Com

mon

, inc

orpo

rate

d ou

tsid

e U

.S.

85,2

331,

141

EQ

Equi

ty

2,00

2,45

920

,394

13

Com

mon

, am

eric

us tr

ust c

ompo

nent

s 3,

196

54

AD

R

Am

eric

an D

epos

itory

Rec

eipt

21,7

6738

214

C

lose

d en

d fu

nds

66,9

2766

4 U

T U

nit T

rust

22

,599

466

15

Clo

sed

end

fund

s, in

corp

. out

side

US

567

3

T

otal

2,

048,

255

21,2

6918

R

EITs

28

,277

293

20-2

4 C

ertif

icat

es

1,84

918

30

A

DR

s 65

,326

764

40-4

8 SB

Is (a

ll)

42,8

4550

0

70

-78

Uni

ts (a

ll)

20,6

4126

3

T

otal

2,

256,

605

23,0

31

Ex

chan

ge

Cod

e Ex

chan

ge C

ode

Des

crip

tion

Mon

thly

Obs

. U

niqu

e Id

entif

iers

Ex

chan

ge

Cod

e Ex

chan

ge C

ode

Des

crip

tion

Mon

thly

O

bs.

Uni

que

Iden

tifie

rs

1NY

SE

503,

107

3,96

6 N

YS

NY

SE

946,

940

7,87

12A

MEX

23

0,49

72,

637

ASE

A

MEX

12

4,52

11,

084

3Nas

daq

1,20

8,13

715

,242

N

MS

Nas

daq/

NM

S 38

3,28

33,

665

0No

exch

ange

list

ed

33

NA

S N

asda

q/no

n N

MS

89,1

1591

7

To

tal

1,94

1,74

421

,848

O

TC

Non

-Nas

daq

OTC

21

1,07

43,

262

X

BQ

O

TC B

ulle

tin B

oard

23

5,72

03,

477

Oth

er U

.S.

1,70

518

Mis

sing

or U

nkno

wn

5,75

712

9

N

on-U

S 4,

344

97

Tot

al

2,00

2,45

920

,520

20

Tabl

e 3

Portf

olio

Ret

urns

Cen

ter

for

Res

earc

h in

Sec

uriti

es P

rices

(C

RSP

) po

rtfol

io a

re c

omm

on e

quity

trad

ed o

n N

YSE

/AM

EX/N

asda

q.

Thom

son

Dat

astre

am (

TDS)

are

all

secu

ritie

s on

co

nstit

uent

list

s FA

MER

A-F

AM

ERZ

and

DEA

DU

S1-D

EAD

US6

(32

lists

tota

l) w

ith ty

pe e

qual

to e

quity

and

exc

hang

e m

nem

onic

of N

YSE

, AM

EX, N

asda

q-N

MS

and

Nas

daq-

Non

NM

S. S

cree

ned

TDS

is T

DS

scre

ened

for n

on-c

omm

on e

quity

sec

uriti

es u

sing

the

proc

edur

e de

scrib

ed in

the

body

of t

he p

aper

. A

ll po

rtfol

ios

are

equa

l-wei

ghte

d ex

cept

as

note

d in

tabl

e.

Size

dec

iles

are

calc

ulat

ed in

Dec

embe

r of

eac

h ye

ar u

sing

all

NY

SE s

ecur

ities

. 10

90 M

omen

tum

ref

ers

to th

e av

erag

e m

onth

ly re

turn

of a

stra

tegy

long

pas

t win

ners

def

ined

as

the

top

10%

of s

tock

s so

rted

by re

turn

ove

r mon

ths

t-2 th

roug

h t-1

2, a

nd s

hort

past

lose

rs.

Sim

ilarly

for

30

70 e

xcep

t win

ners

and

lose

rs a

re d

efin

ed a

s the

top

30/ b

otto

m 3

0%.

t-sta

tistic

s are

in p

aren

thes

es.

M

onth

ly re

turn

s, 19

75-2

002

CR

SP

TD

S

Scre

ened

TD

S

Ave

rage

σ

A

vera

ge

σ ρ

A

vera

ge

σ ρ

Equa

l-wei

ghte

d M

arke

t Ret

urn

1.41

5.

69

2.

40

7.53

0.

66

2.

67

9.10

0.

61

Val

ue-w

eigh

ted

Mar

ket R

etur

n 1.

13

4.57

1.14

4.

40

1.00

1.16

4.

49

1.00

N

YSE

1.

35

5.00

2.00

5.

35

0.80

2.24

6.

54

0.74

A

MEX

1.

42

6.16

6.95

88

.90

0.11

8.19

10

6.15

0.

10

NM

SNA

S 1.

45

6.17

2.54

6.

24

0.94

2.55

6.

34

0.94

Dec

ile 1

(sm

alle

st)

1.60

6.

44

7.

15

14.6

9 0.

34

11

.27

76.6

2 0.

12

Dec

ile 2

1.

32

6.06

4.53

50

.30

0.12

1.83

5.

98

0.93

D

ecile

3

1.40

6.

11

1.

53

5.17

0.

91

1.

63

6.05

0.

95

Dec

ile 4

1.

39

5.92

1.39

4.

97

0.94

1.50

5.

84

0.96

D

ecile

5

1.39

5.

75

1.

38

4.98

0.

95

1.

41

5.65

0.

97

Dec

ile 6

1.

28

5.39

1.29

5.

18

0.96

1.28

5.

49

0.97

D

ecile

7

1.27

5.

22

1.

29

5.18

0.

96

1.

38

5.45

0.

97

Dec

ile 8

1.

23

5.10

1.28

5.

06

0.96

1.33

5.

10

0.98

D

ecile

9

1.18

4.

74

1.

27

4.88

0.

97

1.

28

4.91

0.

98

Dec

ile 1

0 (la

rges

t) 1.

08

4.55

1.15

4.

49

0.99

1.14

4.

55

0.99

1090

Mom

entu

m

1.13

7.

13

0.

26

7.99

0.

67

0.

20

8.79

0.

64

(2

.86)

(0.6

0)

(0

.42)

30

70 M

omen

tum

0.

95

4.70

-1.0

2 20

.32

0.21

-1.2

4 25

.40

0.18

(3.6

5)

(-

0.90

)

(-0.

88)

21

Tabl

e 4

CR

SP/T

DS

Mat

chin

g St

atis

tics

Th

is ta

ble

lists

resu

lts o

f atte

mpt

ing

to m

atch

all

Dec

embe

r obs

erva

tions

from

the

Cen

ter f

or R

esea

rch

in S

ecur

ities

Pric

es (C

RSP

) to

Thom

son

Dat

astre

am (T

DS)

. Th

e to

p pa

nel l

ists

mat

chin

g st

atis

tics

by C

RSP

sha

re c

ode

and

the

botto

m p

anel

list

s th

e m

atch

ing

stat

istic

s by

CR

SP e

xcha

nge

for C

RSP

obs

erva

tions

with

sha

re

code

equ

al to

com

mon

equ

ity.

Fu

ll C

RSP

Sam

ple

Shar

e co

de

Dec

embe

r O

bser

vatio

ns

Mat

chin

gN

on-m

atch

ing

Frac

tion

ofC

RSP

M

atch

ed

10

/11

co

mm

on st

ock

179,

277

108,

172

71,1

05

60.3

4%

12

co

mm

on, i

ncor

pora

ted

outs

ide

US

8,18

3 5,

181

3,00

2 63

.31%

13

Am

eric

us tr

ust

322

3029

2 9.

32%

14

clos

ed-e

nd fu

nds

6,02

8 4,

845

1,18

3 80

.37%

15

clos

ed-e

nd fu

nds,

inco

rp. o

utsi

de U

S 48

48

0 10

0.00

%

18

R

EITs

2,57

2 1,

874

698

72.8

6%

2

Cer

tific

ates

16

4 13

034

79

.27%

3

A

DR

s

6,03

4 63

35,

401

10.4

9%

4

SBIs

3,95

9 2,

361

1,59

8 59

.64%

7

U

nits

1,91

6 1,

159

757

60.4

9%

T

otal

:

208,

503

124,

433

84,0

70

59.6

8%

Com

mon

Equ

ity o

f U.S

. Firm

s

Exch

ange

D

ecem

ber

Obs

erva

tions

M

atch

ing

Non

-mat

chin

g

Frac

tion

ofC

RSP

M

atch

ed

0

no e

xcha

nge

1,67

1 64

51,

026

38.6

0%

1

NY

SE

44

,256

30

,519

13,7

37

68.9

6%

2

AM

EX

20

,506

12

,897

7,60

9 62

.89%

3

N

asda

q

112,

601

63,9

9948

,602

56

.84%

10

Bos

ton

82

33

49

40.2

4%

13

C

hica

go

2

02

0.00

%

16

Pa

cific

30

2010

66

.67%

17

Phila

delp

hia

8 0

8 0.

00%

20

OTC

, non

-Nas

daq

49

2227

44

.90%

ot

her

ha

lted

or su

spen

ded

72

3735

51

.39%

Tot

al:

17

9,27

7 10

8,17

271

,105

60

.34%

22

Tabl

e 5

Portf

olio

Ret

urns

Cen

ter f

or R

esea

rch

in S

ecur

ities

Pric

es (C

RSP

) por

tfolio

s are

form

ed fr

om c

omm

on e

quity

trad

ed o

n N

YSE

/AM

EX/N

asda

q w

ith p

revi

ous m

onth

shar

e pr

ice

grea

ter

than

or e

qual

to $

1.00

. Th

omso

n D

atas

tream

(TD

S) a

re a

ll se

curit

ies

on c

onst

ituen

t lis

ts F

AM

ERA

-FA

MER

Z an

d D

EAD

US1

-DEA

DU

S6 (3

2 lis

ts to

tal)

with

type

eq

ual t

o eq

uity

and

exc

hang

e m

nem

onic

of N

YSE

, AM

EX, N

asda

q-N

MS

and

Nas

daq-

Non

NM

S, s

cree

ned

for n

on c

omm

on e

quity

sec

uriti

es, h

avin

g en

d of

pre

viou

s m

onth

una

djus

ted

pric

e gr

eate

r th

an o

r eq

ual t

o$1.

00, a

nd c

orre

cted

for

dat

a er

rors

. A

ll po

rtfol

ios

are

equa

l-wei

ghte

d ex

cept

as

note

d in

tabl

e.

Size

dec

iles

are

calc

ulat

ed in

Dec

embe

r of e

ach

year

usi

ng a

ll N

YSE

sec

uriti

es.

1090

Mom

entu

m re

fers

to th

e av

erag

e m

onth

ly re

turn

of a

stra

tegy

long

pas

t win

ners

def

ined

as

the

top

10%

of s

tock

s sor

ted

by re

turn

ove

r mon

ths t

-2 th

roug

h t-1

2, a

nd sh

ort p

ast l

oser

s. S

imila

rly fo

r 307

0 ex

cept

win

ners

and

lose

rs a

re d

efin

ed a

s the

top

30/ b

otto

m

30%

. t-s

tatis

tics a

re in

par

enth

eses

.

Mon

thly

retu

rns,

1975

-200

2

C

RSP

Scre

ened

and

Cor

rect

ed T

DS

A

vera

geσ

A

vera

ge

σ ρ

Equa

l-wei

ghte

d M

arke

t Ret

urn

1.29

5.

46

1.51

5.

16

1.00

V

alue

-wei

ghte

d M

arke

t Ret

urn

1.13

4.

57

1.13

4.

47

1.00

N

YSE

1.

35

4.95

1.

47

4.75

0.

99

AM

EX

1.29

5.

77

1.36

5.

21

0.97

N

MSN

AS

1.28

5.

86

1.66

5.

91

0.99

D

ecile

1 (s

mal

lest

) 1.

33

5.83

2.

69

5.76

0.

93

Dec

ile 2

1.

32

6.03

1.

55

5.79

0.

94

Dec

ile 3

1.

40

6.11

1.

54

5.95

0.

95

Dec

ile 4

1.

39

5.92

1.

40

5.79

0.

96

Dec

ile 5

1.

39

5.75

1.

35

5.62

0.

97

Dec

ile 6

1.

28

5.39

1.

22

5.47

0.

97

Dec

ile 7

1.

27

5.22

1.

33

5.41

0.

97

Dec

ile 8

1.

23

5.10

1.

31

5.09

0.

98

Dec

ile 9

1.

18

4.74

1.

25

4.89

0.

98

Dec

ile 1

0 (la

rges

t) 1.

08

4.55

1.

12

4.54

0.

99

1090

Mom

entu

m

1.97

6.

66

1.03

6.

36

0.95

(5.3

0)

(2.9

2)

3070

Mom

entu

m

1.23

4.

39

0.79

4.

15

0.97

(5.0

4)

(3.4

1)

23

Tabl

e 6

Life

Exp

ecta

ncy

by Y

ear

This

tabl

e re

ports

the

aver

age

life

expe

ctan

cy fo

r all

firm

s in

Janu

ary

of e

ach

year

, rep

orte

d se

para

tely

for C

ente

r for

Res

earc

h in

Sec

uriti

es P

rices

(CR

SP) d

ata

and

the

'scre

ened

' dat

a fr

om T

hom

son

Dat

astre

am (T

DS)

. C

RSP

dat

a co

ntai

ns a

ll co

mm

on e

quiti

es tr

aded

on

NY

SE/A

MEX

/Nas

daq.

TD

S co

ntai

ns a

ll eq

uity

trad

ed o

n N

YSE

/AM

EX/N

asda

q-N

MS/

Nas

daq-

nonN

MS

scre

ened

for n

on-c

omm

on e

quity

secu

ritie

s usi

ng th

e m

etho

d de

scrib

ed in

the

body

of t

he p

aper

. Li

fe e

xpec

tanc

y is

th

e av

erag

e of

mon

ths r

emai

ning

for e

ach

firm

with

val

id d

ata

in Ja

nuar

y of

that

yea

r. N

umbe

r of o

bser

vatio

ns is

the

num

ber o

f val

id o

bser

vatio

ns in

Janu

ary

of e

ach

year

. M

eans

test

is th

e p-

valu

e fo

r a n

onpa

ram

etric

Wilc

oxia

n te

st o

f the

nul

l tha

t the

sam

ples

hav

e eq

ual m

ean.

CR

SP

TD

S

Max

Avg

. Life

N

umbe

r

Avg

. Life

N

umbe

r

M

eans

Y

ear

Li

fe

Ex

pect

ancy

Obs

.

Expe

ctan

cy

Obs

.

Diff

eren

ceTe

st

1975

336

16

7.9

4,85

6

237.

8 2,

388

69

.90

[0.0

0]

1976

324

16

0.5

4,86

2

226.

9 2,

440

66

.46

[0.0

0]

1977

312

15

3.4

4,88

5

215.

9 2,

469

62

.54

[0.0

0]

1978

300

14

7.8

4,81

1

204.

4 2,

496

56

.63

[0.0

0]

1979

288

14

4.4

4,72

8

193.

3 2,

533

48

.99

[0.0

0]

1980

276

13

9.9

4,68

7

182.

2 2,

574

42

.30

[0.0

0]

1981

264

13

3.8

4,87

5

172.

0 2,

661

38

.23

[0.0

0]

1982

252

12

6.1

5,21

6

162.

8 2,

772

36

.74

[0.0

0]

1983

240

12

1.6

5,16

5

153.

1 2,

823

31

.51

[0.0

0]

1984

228

11

4.8

5,80

2

144.

0 3,

111

29

.25

[0.0

0]

1985

216

10

9.6

5,90

4

138.

8 3,

150

29

.16

[0.0

0]

1986

204

10

7.2

5,88

2

133.

6 3,

229

26

.48

[0.0

0]

1987

192

10

5.9

6,19

6

126.

2 3,

565

20

.32

[0.0

0]

1988

180

10

1.0

6,42

9

117.

3 3,

832

16

.25

[0.0

0]

1989

168

98

.9

6,17

5

109.

7 3,

900

10

.78

[0.0

0]

1990

156

95

.4

5,97

0

106.

7 3,

731

11

.31

[0.0

0]

1991

144

91

.2

5,81

0

104.

4 3,

606

13

.17

[0.0

0]

1992

132

86

.3

5,89

4

100.

2 3,

634

13

.87

[0.0

0]

1993

120

81

.5

6,00

9

94.1

3,

764

12

.66

[0.0

0]

1994

108

73

.8

6,54

8

86.1

4,

141

12

.33

[0.0

0]

1995

96

66

.0

6,83

5

78.3

4,

289

12

.34

[0.0

0]

1996

84

58

.8

7,07

3

73.4

4,

281

14

.59

[0.0

0]

1997

72

51

.0

7,52

4

68.2

4,

417

17

.20

[0.0

0]

1998

60

43

.6

7,50

5

57.7

4,

753

14

.10

[0.0

0]

1999

48

36

.9

7,06

2

45.9

5,

123

9.

02

[0.0

0]

2000

36

29

.7

6,71

3

34.1

5,

635

4.

44

[0.0

0]

2001

24

21

.0

6,36

3

22.5

5,

945

1.

43

[0.0

0]

2002

12

11

.4

5,66

3

11.6

5,

685

0.

25

[0.0

0]

24

Tabl

e 7

Size

Dec

ile B

reak

poin

ts

C

ente

r for

Res

earc

h in

Sec

uriti

es P

rices

(CR

SP) b

reak

poin

ts a

re fo

rmed

from

com

mon

equ

ity tr

aded

on

the

NY

SE.

Thom

son

Dat

astre

am (T

DS)

bre

akpo

ints

are

form

ed

from

all

secu

ritie

s on

con

stitu

ent

lists

FA

MER

A-F

AM

ERZ

and

DEA

DU

S1-D

EAD

US6

(32

lis

ts t

otal

) w

ith t

ype

equa

l to

equ

ity a

nd e

xcha

nge

mne

mon

ic o

f N

YSE

. B

reak

poin

ts a

re a

pplie

d to

all

secu

ritie

s in

the

sam

ple

with

out r

egar

d to

exc

hang

e. T

DS-

Raw

refe

rs to

the

orig

inal

dat

a as

orig

inal

ly d

ownl

oade

d, S

cree

ned

and

Cor

rect

ed

refe

rs to

the

rem

oval

of n

on c

omm

on e

quity

and

the

corr

ectio

n of

obv

ious

dat

a er

rors

. A

nnua

l Dec

ile E

quity

Cou

nt is

the

tota

l num

ber o

f obs

erva

tions

in th

at d

ecile

for

the

full

year

.

CR

SP

TD

S - R

aw

Sc

reen

ed a

nd C

orre

cted

TD

S

Dec

embe

r, 19

75

D

ecile

B

reak

poin

t A

nnua

l Dec

ileEq

uity

Cou

nt

Dec

ile

Bre

akpo

int

Ann

ual D

ecile

Equi

ty C

ount

Dec

ile

Bre

akpo

int

Ann

ual D

ecile

Eq

uity

Cou

nt

Dec

ile 1

(sm

alle

st)

16

.22

27,0

29

2.

24

3,54

1

2.10

3,24

2 D

ecile

2

25

.57

5,24

2

5.43

3,

342

5.

212,

897

Dec

ile 3

39.9

24,

440

10

.06

3,20

2

9.91

3,23

1 D

ecile

4

60

.85

4,00

1

17.0

9 2,

749

17

.19

3,02

9 D

ecile

5

92

.82

3,29

6

27.7

5 3,

255

28

.85

2,88

8 D

ecile

6

15

1.92

2,95

1

46.5

3 2,

645

51

.26

2,93

9 D

ecile

7

24

8.70

2,24

2

75.4

5 2,

678

87

.43

2,73

1 D

ecile

8

46

1.15

2,38

0

176.

63

2,84

6

203.

983,

032

Dec

ile 9

815.

921,

876

51

6.70

2,

596

56

3.81

2,63

1 D

ecile

10

(larg

est)

2,

227

2,85

3

2,74

8

Tot

al

55

,684

29

,707

29,3

68

A

vg. N

YSE

Mkt

Cap

12/

1975

443.

24

263.

49

28

2.79

Dec

embe

r, 20

01

Dec

ile 1

(sm

alle

st)

10

5.47

29,7

88

25

.31

19,7

33

10

5.47

29,2

19

Dec

ile 2

260.

199,

304

76

.86

17,3

86

22

5.83

8,66

4 D

ecile

3

44

4.90

5,65

0

138.

30

9,97

8

388.

896,

219

Dec

ile 4

717.

294,

637

23

0.74

8,

337

63

0.55

5,09

0 D

ecile

5

1,

117.

653,

751

38

3.05

7,

514

98

8.23

4,23

3 D

ecile

6

1,

663.

802,

865

66

5.05

7,

065

1,

496.

753,

316

Dec

ile 7

2,66

1.05

2,46

3

1,21

2.01

6,

231

2,

378.

912,

830

Dec

ile 8

5,12

2.23

2,46

2

2,36

6.94

4,

905

4,

346.

442,

680

Dec

ile 9

12,2

36.6

92,

223

6,

254.

85

4,25

2

10,6

32.9

12,

606

Dec

ile 1

0 (la

rges

t)

1,

931

4,04

4

2,

216

T

otal

65

,074

89

,445

67

,073

Avg

. NY

SE M

kt C

ap 1

2/20

01

6,46

6.97

3,

773.

45

5806

.00

25

Tabl

e 8

Div

iden

ds

Th

is t

able

lis

ts s

umm

ary

divi

dend

inf

orm

atio

n fo

r th

e sa

mpl

e of

Cen

ter

for

Res

earc

h in

Sec

urity

Pric

es (

CR

SP)

dat

a th

at w

e ar

e ab

le t

o m

atch

to

Thom

son

Dat

astre

am (T

DS)

by

both

firm

and

dat

e.

CR

SP/T

DS

Mat

chin

g Sa

mpl

e

Obs

erva

tions

with

zer

o di

vide

nds

781,

043

85.1

4%

O

bser

vatio

ns w

ith n

on-z

ero

divi

dend

s

136,

353

14.8

6%

Obs

erva

tions

with

mat

chin

g no

n-ze

ro d

ivid

end

amou

nts

127,

236

93.3

1%

O

bser

vatio

ns w

ith n

on-m

atch

ing

divi

dend

am

ount

s

8,

215

6.02

%

C

RSP

>0, T

DS=

0

5,

585

67.9

9%

CR

SP=0

, TD

S>0

1,07

113

.04%

C

RSP

>0, T

DS>

0

1,

559

18.9

8%

Mis

sing

TD

S Pr

ice

Dat

a

90

20.

66%

Tota

l non

mat

chin

g am

ount

s

Tota

l

91

7,39

610

0%

26

Figu

re 1

CR

SP s

ampl

e

0

2000

4000

6000

8000

1000

0

1200

0

1975

1980

1985

1990

1995

2000

Year

# of firms

00.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

CR

SP

with

mat

chC

RSP

with

nom

atch

Perc

ent M

atch

ed

27

Figu

re 2

TDS

sam

ple

0

2000

4000

6000

8000

1000

0

1200

0

1400

0

1975

1980

1985

1990

1995

2000

Year

# of firms

00.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

DS

with

mat

chD

S w

ith n

omat

chP

erce

nt M

atch

ed

28

Figu

re 3

CR

SP v

s. T

DS

Mar

ket D

ivid

end

Yiel

dC

omm

on S

ampl

e

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%197512

197612

197712

197812

197912

198012

198112

198212

198312

198412

198512

198612

198712

198812

198912

199012

199112

199212

199312

199412

199512

199612

199712

199812

199912

200012

200112

200212

Year

/Mon

th

Dividend Yield

CR

SP

TDS

29

Figu

re 4

CR

SP v

s. T

DS

Mar

ket D

ivid

end

Yiel

dA

ll A

vaila

ble

Obs

erva

tions

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

197512

197612

197712

197812

197912

198012

198112

198212

198312

198412

198512

198612

198712

198812

198912

199012

199112

199212

199312

199412

199512

199612

199712

199812

199912

200012

200112

200212

Year

/Mon

th

Dividend Yield

CR

SP

TDS