Embed Size (px)

Citation preview

In Search of a Fresh Start:Can Credit Counseling Help Debtors

Recover from Bankruptcy?

NFCC WebinarMay 12, 2010

Introductions

Dr. Angela LyonsAssociate Professor University of Illinois(217) [email protected]

Shawn HowardStatisticianMoney Management International(713) [email protected]

2

Why bankruptcy counseling?

• 2005 Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA).

• Two educational requirements. Pre-filing credit counseling session. Pre-discharge financial education course.

• Reasons behind legislation. Help debtors make an informed choice

about bankruptcy. Provide debtors with the financial skills necessary to

better manage their money and avoid future financial problems.

3

4

The Big Debate:Does credit counseling work?

Opponents:

“The counseling places undue hardship on debtors who are already overwhelmed financially. It’s an administrative obstacle to those who really have no other option but to file for bankruptcy.”

Proponents: “The counseling has educational value. Repealing this requirement would prevent debtors from getting the knowledge and skills they need to better manage their finances and build future financial security.”

5

Key Questions

1. Do the counseling and education requirements have educational value?

2. Do debtors learn something?

3. Do debtors improve their financial behaviors?

4. What happens to debtors after the bankruptcy process?

5. Do debtors benefit from both the counseling and education? Is one requirement more effective than the other?

6

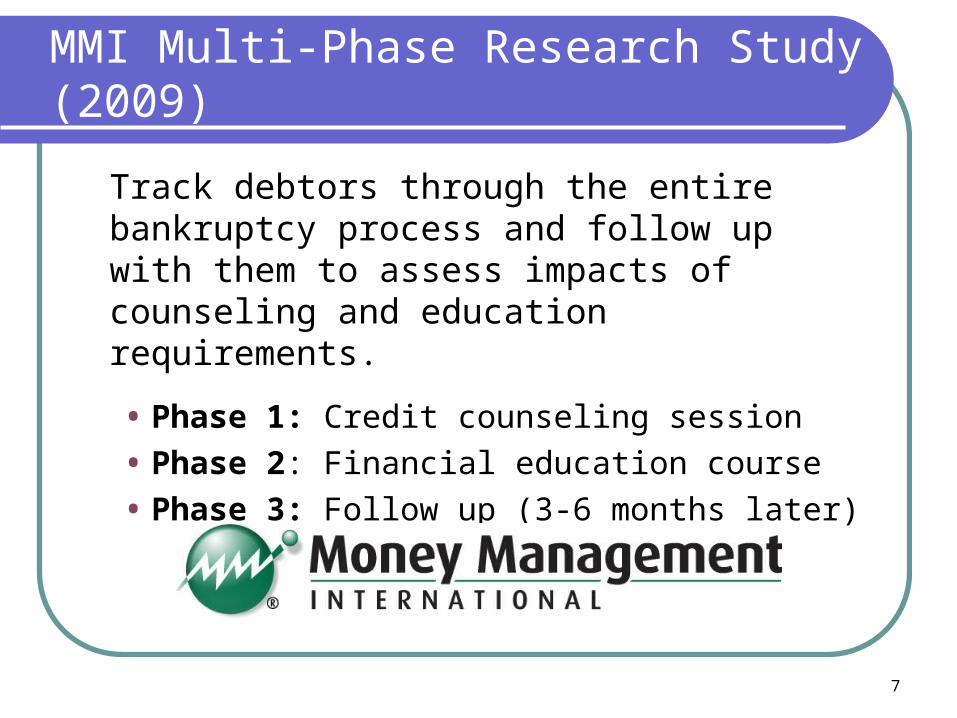

MMI Multi-Phase Research Study (2009)

Track debtors through the entire bankruptcy process and follow up with them to assess impacts of counseling and education requirements.

• Phase 1: Credit counseling session

• Phase 2: Financial education course

• Phase 3: Follow up (3-6 months later)

7

Focus of Today’s Webinar

Phase I: Credit Counseling Session

To measure and quantify the educational value of the counseling experience.

To identify specific groups of debtors who benefited more/less from the counseling.

8

Background Information

Consumers who seek out credit counseling generally fall into one of three categories:

1. Those who are able to help themselves out of financial trouble and are looking for solutions to handle debt on their own.

2. Those who need a DMP to help them consolidate and repay their debts.

3. Those whose financial situation is so severe that bankruptcy may be their best, and perhaps only, option.

9

What Do We Already Know?

General Credit Counseling

Socio-psychological researchKim, Garman, and Sorhaindo (2006), Xiao, Sorhaindo, and Garman (2006), Xiao and Wu (2006).

Economic researchElliehausen, Lundquist, and Staten (2007), Staten and Barron (2009).

Bankruptcy Counseling

Canadian experienceRamsay (2002), Schwartz (2003).

U.S. experienceThorne and Porter (2007), NFCC (2006), Lyons, White, and Howard (2008).

10

Where are the critical gaps?

11

Phase I: Bankruptcy Counseling Course

An overview of MMI’s online course:

10 online modules covering wide range of basic personal finance concepts.

Interactive components (e.g., budgeting activities, financial calculators, checklists, and assessment tools).

Audio track. Available 24/7 for convenience. Course takes about 60 to 90 minutes

to complete. At end of course, clients required to speak

with certified counselor.

12

13

Data Collection

• Data collected from over 32,000 debtors who completed MMI’s online bankruptcy counseling course between February and August 2009.

• Pre- and post-tests built into online course to measure changes in financial knowledge, attitudes, and behavioral intentions.

14

Measuring Financial Knowledge

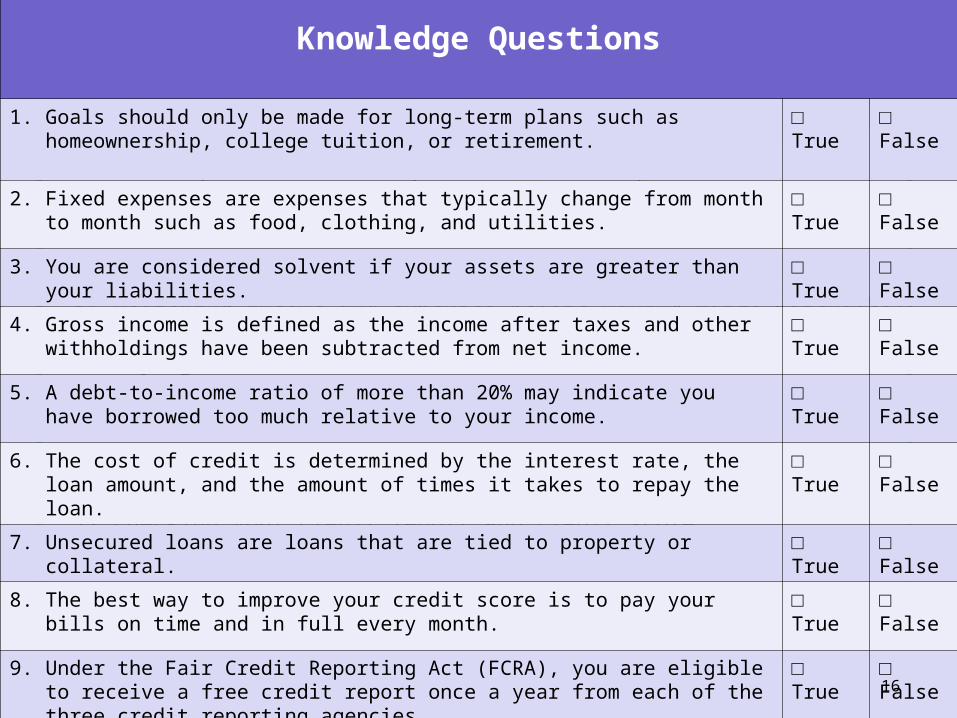

• 10 true/false questions included on both pre- and post-tests.

• Questions test key concepts covered in course.

• Knowledge score calculated for each client based on percentage of questions answered correctly.

• Scores range from 0 to 100 percent.

• Statistical tests show that knowledge score is a reliable measure of clients’ overall level of financial knowledge.

15

1. Setting short- and long-term financial goals.

2. Saving money each month.

3. Tracking income and expenses.

4. Reducing impulse spending and cutting unnecessary expenses.

5. Reviewing income and expenses before making large purchases.

6. Using a filing system to store bills and financial records.

7. Paying bills on time each month.

8. Reviewing bills each month for accuracy.

9. Comparing prices before making purchases.

10. Using less than 50% of your available credit.

11. Keeping your debt-to-income ratio below 20%.

12. Checking your credit report and credit score.

Knowledge Questions

1. Goals should only be made for long-term plans such as homeownership, college tuition, or retirement.

□ True □ False

2. Fixed expenses are expenses that typically change from month to month such as food, clothing, and utilities.

□ True □ False

3. You are considered solvent if your assets are greater than your liabilities. □ True □ False

4. Gross income is defined as the income after taxes and other withholdings have been subtracted from net income.

□ True □ False

5. A debt-to-income ratio of more than 20% may indicate you have borrowed too much relative to your income.

□ True □ False

6. The cost of credit is determined by the interest rate, the loan amount, and the amount of times it takes to repay the loan.

□ True □ False

7. Unsecured loans are loans that are tied to property or collateral. □ True □ False

8. The best way to improve your credit score is to pay your bills on time and in full every month.

□ True □ False

9. Under the Fair Credit Reporting Act (FCRA), you are eligible to receive a free credit report once a year from each of the three credit reporting agencies.

□ True □ False

10. All information, including a bankruptcy filing, must be removed from your credit report after 7 years.

□ True □ False16

Measuring Financial Behavior

• Clients asked about current and future intentions to engage in 12 financial practices.

• Pre-counseling: “How often are you currently doing each financial practice?”

• Post-counseling: “How often do you plan to do each financial practice?”

• Responses based on a 5-point scale (1=Never to 5=Always).

• Behavior score calculated by summing responses to the 12 financial practices using the reported values from the 5-point scale.

• Scores range from 12 to 60.

• Statistical tests show that behavior score is a reliable measure of clients’ overall financial behavior.

17

1. Setting short- and long-term financial goals.

2. Saving money each month.

3. Tracking income and expenses.

4. Reducing impulse spending and cutting unnecessary expenses.

5. Reviewing income and expenses before making large purchases.

6. Using a filing system to store bills and financial records.

7. Paying bills on time each month.

8. Reviewing bills each month for accuracy.

9. Comparing prices before making purchases.

10. Using less than 50% of your available credit.

11. Keeping your debt-to-income ratio below 20%.

12. Checking your credit report and credit score.

List of Financial Practices

18

Detailed info also collected on….

Pre-Counseling• Reasons for current financial problems.

• Actions already taken to deal with current financial problems.

• Contact with bankruptcy attorney.

• Willingness to want to improve financial situation.

• Financial portfolio (income, expenses, assets, and debts).

Post-Counseling• Perceived educational impacts of the counseling.

• Overall satisfaction with the counseling.

• Actions likely to take to deal with financial problems.

• What did clients like most/least about the counseling?

• Demographics.

19

Actions taken to deal with financial problems in the past

Previously filed for bankruptcy. 27.1%

Used a credit counseling service. 15.0%

Participated in a DMP. 13.7%

20

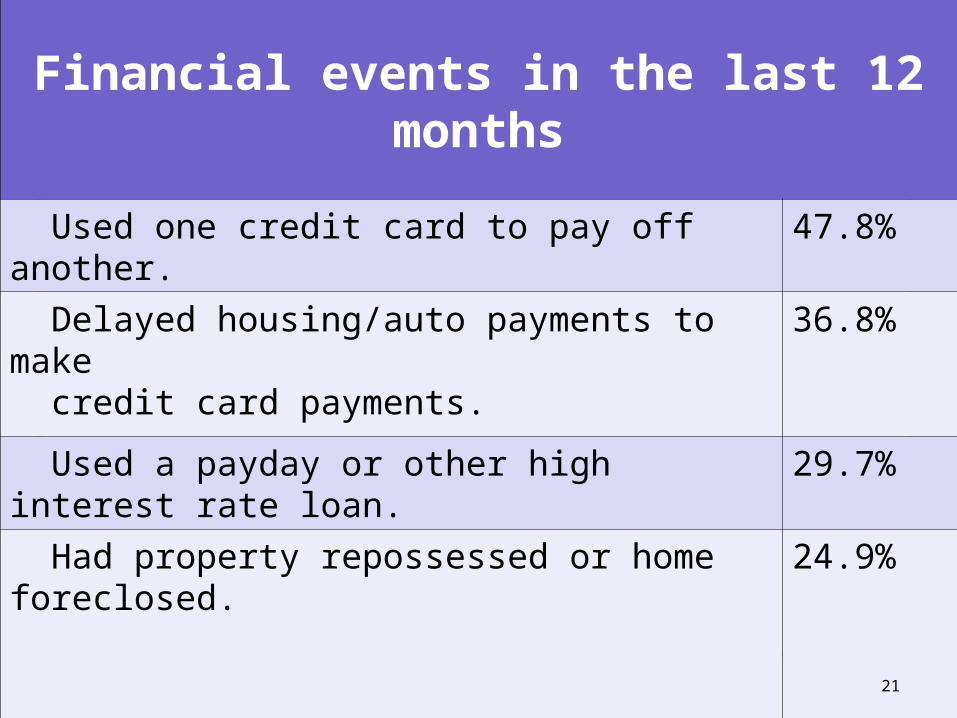

Financial events in the last 12 months

Used one credit card to pay off another. 47.8%

Delayed housing/auto payments to make credit card payments.

36.8%

Used a payday or other high interest rate loan. 29.7%

Had property repossessed or home foreclosed. 24.9%

21

Factors contributing to current financial problems

Unexpected expenses. 74.1%

Loss of employment. 52.1%

Unnecessary spending. 49.8%

Health problems / injury / illness. 36.4%

Business loss / excessive business expenses. 25.9%

Divorce or separation. 21.8%

Death of a spouse or other loved one. 6.7%

22

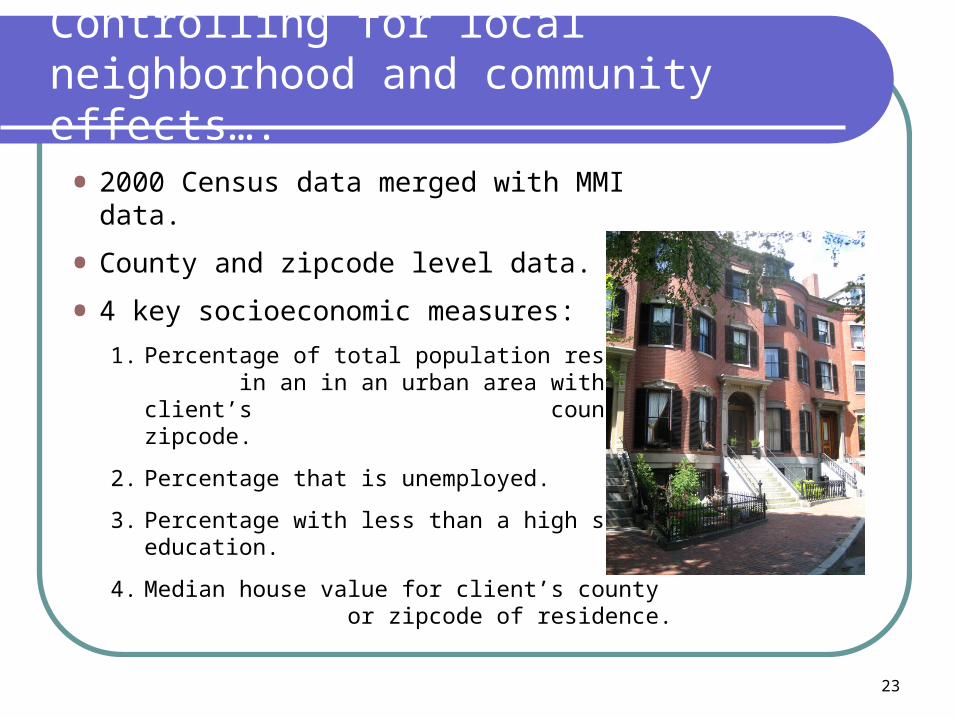

Controlling for local neighborhood and community effects….

• 2000 Census data merged with MMI data.

• County and zipcode level data.

• 4 key socioeconomic measures:

1. Percentage of total population residing in an in an urban area within client’s county or zipcode.

2. Percentage that is unemployed.

3. Percentage with less than a high school education.

4. Median house value for client’s county or zipcode of residence.

23

Methods Used to Analyze Data

24

Methods Used to Analyze Data (cont.)

Step 1: Descriptive Analysis

• Demographic overview.

• Financial profile.

• Financial knowledge pre- and post-counseling.

• Financial practices pre-counseling.

• Intended financial practices post-counseling.

• Perceived educational impacts.

• Overall satisfaction levels.

25

Methods Used to Analyze Data (cont.)

Step 2: Regression Analysis

Which clients were more likely to score higher on the financial knowledge test?

Which clients were more likely to engage in more positive financial practices?

26

Methods Used to Analyze Data (cont.)

Variables included in regression models:

Prior financial knowledge or prior financial behavior. General demographics (age, gender, marital status,

race/ethnicity, education, income, homeownership, employment status).

Willingness to makes changes. Reasons for financial problems (poor health, unemployment,

unnecessary spending). Financial events in last 12 months (used payday or other high

interest loan, delayed house/auto payments to pay credit cards, had property repossessed or home foreclosed).

Previously filed bankruptcy (i.e., repeat filer). Census information.

27

Key Findings

1. Increased knowledge

• Pre- and post-tests showed that most debtors were financially knowledgeable prior to counseling.

• Yet, still see significant improvement overall in financial literacy post-counseling.

• On average, debtors scored 77.1% correct on pre-test and 85.9% on post-test.

• An increase of 11.4% in knowledge.

28

Key Findings (cont.)

2. Increased financial confidence

• Over 97% of debtors felt more knowledgeable about the bankruptcy process and options available to deal with their financial problems.

• Over 91% felt their overall ability to manage their finances had improved.

29

Key Findings (cont.)

3. Improved attitudes and behavioral intentions

• Debtors experienced significant and positive changes in financial attitudes and behavioral intentions.

• By the end of the counseling, debtors were at a “teachable moment.”

• More aware of current financial practices.

• Motivated to take action and improve their financial situation.

30

Key Findings (cont.)

4. Prior knowledge and behaviors are important.

• Debtors with a more solid foundation in personal financial management demonstrated more significant improvements in knowledge and behavior post-counseling.

• However, they may not have had as much room to improve because they started at a higher level to begin with.

31

Key Findings (cont.)

5. Socioeconomic status matters

• Those with higher incomes and education were more likely to experience improvements in knowledge, attitudes, and behavioral intentions.

• Higher-income clients were less likely to report positive financial practices prior to counseling, but more likely to report positive (intended) practices after counseling.

• Why? Indebtedness among high-income clients was primarily the result of poor financial management rather than unfortunate events.

32

Key Findings (cont.)

6. Positive outcomes for those with poor financial management practices

• Half of all debtors reported that their financial situation was due to unnecessary spending.

• These debtors were more likely to become financially knowledgeable than those whose financial situation was not due to financial mismanagement.

• They were also more likely to indicate they would engage in positive financial behaviors post-counseling.

33

Key Findings (cont.)

7. Assistance for those in unfortunate circumstances

• Those whose financial problems were due to unfortunate circumstances such as illness and unemployment also benefited from the counseling.

• Improvements in knowledge and behavior, though, were similar to those whose financial problems were unrelated to an unfortunate event.

• This suggests that on average debtors benefited from the counseling regardless of whether their indebtedness resulted from unfortunate circumstances or from poor financial decisions.

34

Key Findings (cont.)

8. Minorities tended to fair worse

• Minority groups, especially African-Americans and Hispanics, were significantly less likely than Whites to experience improvements in knowledge and behavior.

• Potential explanations: Language barrier. Inadequate controls for neighborhood and

community effects. Inadequate controls for socialization,

attitudinal, and cultural differences.

35

Overall Satisfaction with Counseling

• Debtors were very satisfied with their bankruptcy counseling experience.

• Over 99% found the counseling course helpful.

• About 97% indicated they would be likely to seek counseling again in the future.

Almost all debtors seemed to appreciate the educational value of the counseling and did not feel that the requirement had been a burden or an administrative obstacle.

36

A few limitations to note….

Findings reflect behavioral intentions and not actual behavior change.

Difficult to design objective measures of success or failure that are acceptable to the entire field of financial education.

Methods and measures used were selected taking into account the content of the counseling, the bankruptcy process, administrative constraints, available resources, and debtors’ attributes.

May not be capturing key pieces of information (e.g., cultural and psychological factors).

Data collected from a single credit counseling agency.

37

Implications for Public Policy

Is the counseling requirement serving its intended purpose?

Is it assisting debtors in making an informed choice about bankruptcy?

Is it providing debtors with the financial skills necessary to better manage their money and avoid future financial problems?

38

Implications for Education

Debtors were fairly knowledgeable about basic financial management concepts.

Course content could be tweaked to provide a “fresh start” program to help debtors get back on their feet and rebuild their credit.

Debtors with more severe deficiencies may require more intensive education and motivational support. One counseling session may not be enough.

Online counseling appears to be an effective means of delivery.

A “one-size-fits-all” approach may not be ideal for all debtors.

39

Phase I: Release of Findings1. Research paper2. Research brief3. PowerPoint

http://www.cefe.illinois.edu/research/reports

40

Preview of Coming Attractions(Phases II and III)

What happens after bankruptcy?

• Does the counseling help debtors get a “fresh start” financially?

• Are they able to actually put into practice what they’ve learned?

41

Phases II and III (cont.)

• Follow up data have been collected.

• Preliminary analysis points to marked improvement in debtors’ financial management skills and practices.

• Implication: Credit counseling may be a viable mechanism to help debtors deal with their financial situation and obtain a fresh start.

• Results are scheduled for release later this year. Will be presented at NFCC Conference in October.

42

Questions

43