Embed Size (px)

Citation preview

2

Important information

The information, statements and opinions contained in this document do not constitute a recommendation to

buy or sell financial instruments issued by the bank or in connection with the bank.

Certain sections in this document contain “forward-looking statements” regarding the bank’s future business

development and economic performance. There are a number of known and unknown risks and uncertainties

which may have an impact on the future business development or may influence future performance.

There are several factors which may influence operations, financial conditions, liquidity and banking sector

activity, and therefore future performance may be altered from present projections.

These factors include, but are not limited to: general market, macroeconomic, regulatory changes; b)

movements in local and international financial markets, currency exchange rates and interest rates; c)

competitive pressures; d) technological developments; e) changes in the financial position or credit

worthiness of our clients.

The information contained in this presentation must be read in conjunction with all other publicly available

documents and financial statements published by the Bank. The Bank will not be held responsible for any

transactions made on the basis of this presentation.

3

Agenda

what we’ve planned for today

I. Carpatica Overview II. The Immediate Future III. People and Service Excellence IV. Sales V. Financial Performance VI. Conclusions & Final Remarks

4

I. Carpatica Overview

1. Brief Profile

Johan Gabriëls, Chief Executive Officer

5

Established in 1999, head office – Sibiu (Transylvania)

Back to profit in 2012

National presence in all regions in Romania through 139 branches and

agencies

2004 listed on the Bucharest Stock Exchange

Full banking license

Regulated by the National Bank of Romania

~15,000 SME & Corporate and ~150,000 retail clients

Offers various banking products to SME, Corporate and Retail clients

SME / Corporate are the biggest contributor (>85%) to the loan portfolio

I.1 Carpatica Brief Profile

6

II. The Immediate Future

A glimpse at what is next to come

1. Capsule of BCC Current Status 2. Shareholders structure as at 30th of June 2013 3. Stock Price Evolution 4. Capsule of BCC Immediate Future 5. Our Clear Vision

Johan Gabriëls, Chief Executive Officer

7

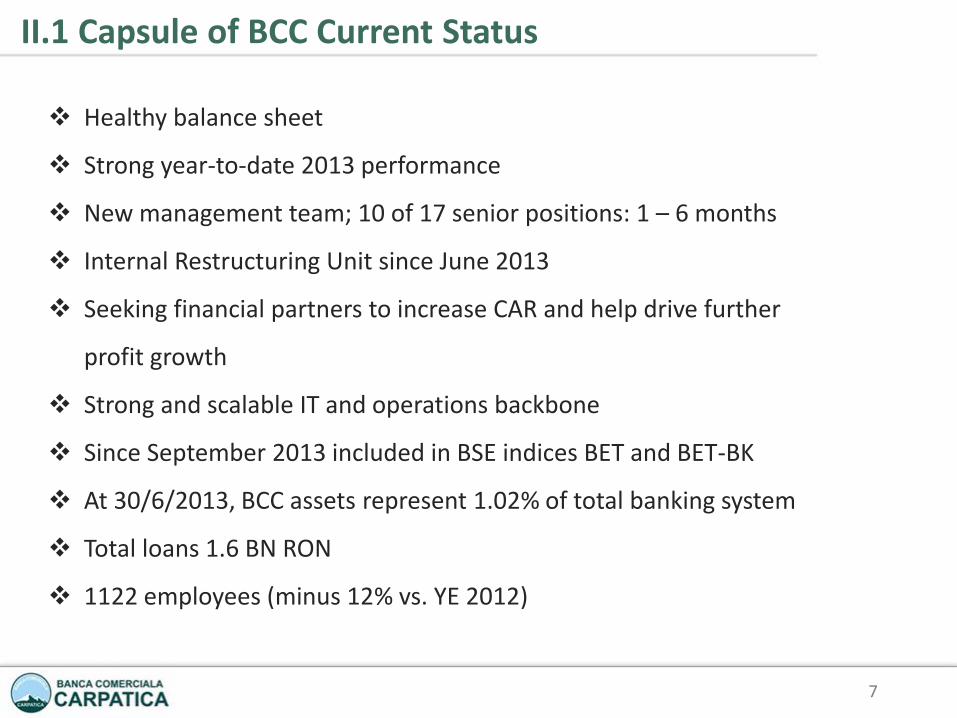

Healthy balance sheet

Strong year-to-date 2013 performance

New management team; 10 of 17 senior positions: 1 – 6 months

Internal Restructuring Unit since June 2013

Seeking financial partners to increase CAR and help drive further

profit growth

Strong and scalable IT and operations backbone

Since September 2013 included in BSE indices BET and BET-BK

At 30/6/2013, BCC assets represent 1.02% of total banking system

Total loans 1.6 BN RON

1122 employees (minus 12% vs. YE 2012)

II.1 Capsule of BCC Current Status

8

II.2 Shareholders structure – 30th of June 2013

71%

29%

Shareholders by capital origin

Romanian capital Foreign capital

80%

20%

Shareholders by participation type

Individuals Legal Persons

Owner name Number of

shares Value (RON) Stake (%)

Carabulea Ilie 1,299,097,478 129,909,747.80 41.29%

Tanase Corneliu 352,948,364 35,294,836.40 11.22%

SC Atlassib SRL 143,042,518 14,304,251.80 4.55%

SC Safa SRL 278,117 27,811.70 0.01%

Olivo Gian Antonio 150,562,942 15,056,294.20 4.79%

Olivo Lucio 181,426,190 18,142,619.00 5.77%

Individuals 541,092,317 54,109,231.70 17.20%

Corporate 477,842,568 47,784,256.80 15.19%

TOTAL 3,146,290,494 314,629,049.40 100.00%

*according to Central Depository – 30/06/2013

9

Average volume 1.73m Shares outstanding 3.15bn Free float 1.49bn

P/E (TTM) 7.14 Market cap 200m RON EPS (TTM) 0.0089 RO

One year change +66%

II.3 Stock Price Evolution

10

Branch rationalization / incentive plan will further drive profits

Efficiency gains and headcount adjustment in HQ by Qtr1, 2014

Cross selling = another source of increasing profits

New FX and payment activities will add to profit growth

New customers / loan pipeline already at €40 million and growing

Seeking more strategic bank relationships

BCC has opportunity to pick up quality clients as many Romanian SME’s

being abandoned by Western European banks

Romanian banking industry ripe for major consolidation; presents

tremendous opportunity

II.4 Capsule of BCC Immediate Future

11

There is a significant potential supporting Romanians both in their

home country as abroad

We believe in “Service Excellence” as a differentiating factor. As a

small bank, decision taking will be fast

We will drive innovation through strategic partnership

BCC has now the team to create new markets and new services

To become “ The bank of opportunities ”

II.5 Our Clear Vision

12

III. People and Service Excellence Our differentiator

1. One of the Best Teams in the Market 2. Service Excellence as a Differentiator

Ena Badeanu, Chief People Officer (*)

(*) awaiting NBR approval

13

A New Executive Team with right mix of experience, exposure and knowledge

Gheorghe CISMARU

OPERATIONS

12 years with BCC

Johan GABRIELS

EXECUTIVE

6 months with BCC Former RBS / Capital

One

Ion DOBRICA

FINANCE

14 years with BCC

Ena BADEANU

PEOLPLE

6 months with BCC Former RBS / ABN-

Amro

Cosmin BUCUR

SALES

3 months with BCC Former RBS / ABN-

Amro

III.1 One of the Best Teams in the Market

14

Sebastian Bacioiu

Supported by a motivated, competent and highly potential team of directors

4 months with BCC, former Credit Agricole

Doina Dogaroiu

RISK

Irina Neacsu

2 months with BCC, former Erste Bank

Calin Parau

12 years with BCC

RESTRUCTURING

Adrian Fercu

<1 month with BCC, former RBS, ABN-Amro

NETWORK

<1 month with BCC, former RBS, ABN-Amro

SALES

TRANSFORMATION

14 years with BCC

Adrian Chira

4 months with BCC, former Bancpost, HVB

COMMUNICATION

18 months with BCC, former ING, Tiriac Bank

Gabriel Diamandopol

OPERATIONS

Lucian Nicoara

14 years with BCC

TREASURY

Sorin Ionascu

12 years with BCC

RETAIL

Non Credit

IT

Razvan Diaconeasa

6 months with BCC, former RBS, ABN-Amro

2 months with BCC, former RBS, ABN-Amro

Silvana Tataruca

INNOVATION

Adrian Hudulin

III.1 One of the Best Teams in the Market

(*) awaiting NBR approval

(*)

(*)

(*) (*)

15

III.2 Service Excellence as differentiator

A bank where the client is king and our employees are the first brand ambassadors

We are building a culture of excellence

Dedicated business unit of service excellence

Process redesign

Corporate credit flow (Qtr3, 2013)

Client on-boarding process (Qtr4, 2013)

We are creating a (new) corporate identity

Employees as brand ambassadors

Re-branding

Step change in the way we communicate

We are transforming the bank towards a client centric organisation

16

IV. Sales

A platform for future growth

Cosmin Bucur, Chief Commercial Officer (*)

(*) awaiting NBR approval

1. Overview 2. Strategic Focus

17

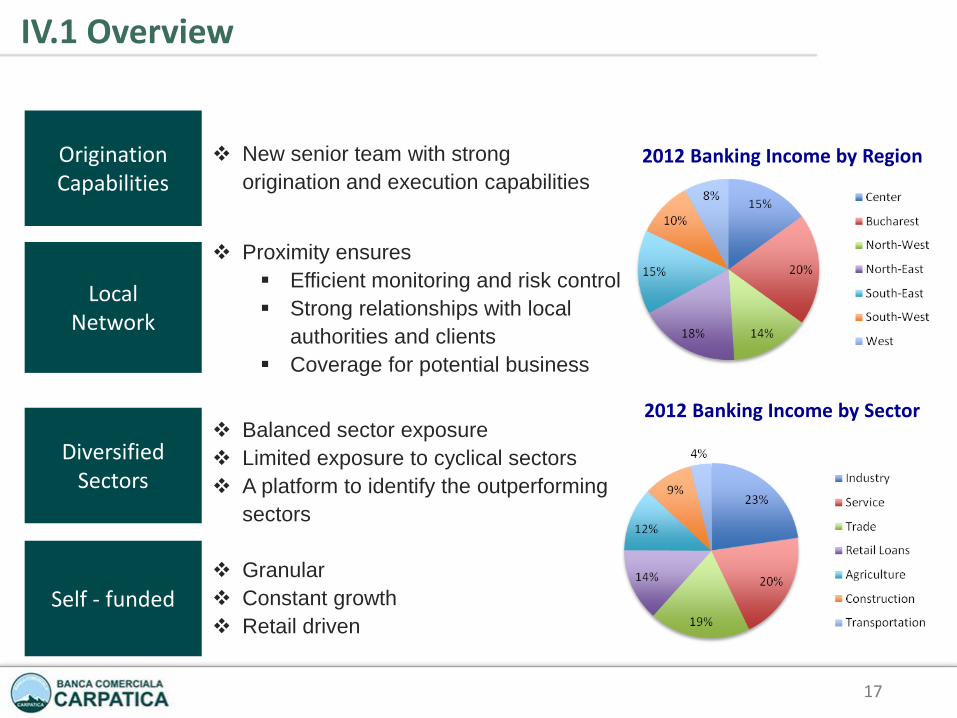

IV.1 Overview

Origination Capabilities

Local Network

Diversified Sectors

Self - funded

New senior team with strong

origination and execution capabilities

Proximity ensures

Efficient monitoring and risk control

Strong relationships with local

authorities and clients

Coverage for potential business

Balanced sector exposure

Limited exposure to cyclical sectors

A platform to identify the outperforming

sectors

Granular

Constant growth

Retail driven

2012 Banking Income by Region

2012 Banking Income by Sector

18

IV.2 Strategic Focus

Cross Sell

Clients & Prospects

People & Culture

Product Innovation

New Treasury Sales and Transaction Banking departments

Key growth drivers: FX platform (H2, 2013) and Commodities (2014)

Focus on International payments

Tailored Cash Management & Trade products for each client segment

Expand wallet on existing clients

Heightened focus on GDP driver (i.e. Agriculture, pharma and energy)

Increase penetration in Top 1000 large local and SME companies

From de-risking to risk management

Proactive identification of early warning signals

Comprehensive reporting, sales tools & client segmentation

Recruit, develop key talent and improve performance

Bring product and service excellence at best in class levels

Transparent performance management process

Focus on Internet Banking, Virtualization and Branch Automation

Deliver innovative solutions for a younger client segment

Creative Alternative Channels and marketing campaigns

19

V. Financial Performance

Towards Financial Strength

1. Healthy Balance Sheet Structure 2. Back to Profit 3. Strong year-to-date Performance

Ion Dobrica, Chief Finance Officer

20

BCC’s balance sheet compares favourably to the Romanian banking sector

BCC Banking system

Source: BCC/ NBR supervision reports

Loans (gross) to Deposits (%) (3)

Deposits to Total Assets (%)

Liabilities (1)

Liquid Assets = Bonds / Total Assets (%)

Loans to Total Assets (%) (2)

Assets (1)

Notes (1) Local GAAP. All data as of December 2012 (2) Loans to total assets = gross loans (pre-provisions) to total assets (pre-provisions) (3) Loans to deposits = gross loans (pre-provisions) to deposits

56

4035 36

29 29

6359 59 59 61

10

30

50

70

2008 2009 2010 2011 2012

6562

65

5348

55 56 56 56

20

40

60

80

2008 2009 2010 2011 2012

BCC Banking system

55 6051 49

59

122113 113 117 120

0

35

70

105

140

2008 2009 2010 2011 2012

56

16

V.1 Healthy Balance Sheet Structure

21

After 3 years of losses, BCC recorded a profit for 2012 Return on Assets (ROA) (%)

Profitability (1)

-1

-0.5

0

0.5

1

2011 2012

Notes (1) Based on local GAAP results. All data as of December 2012 (2) Cost to income ratio = operating expenses / banking income (3) Credit risk rate = exposure classified as doubtful or loss / total loans (pre-provisions) (4) NIM = net interest income / interest earning assets

Return on Equity (ROE) (%)

-15

-10

-5

0

5

10

2011 2012

Cost to Income Ratio (%) (2)

Cost (1)

40

60

80

100

2011 2012 Credit Risk Rate (%) (3)

15

25

35

45

55

2011 2012

Net Interest Margin (%) (4)

Revenues (1)

0

1

2

3

4

2011 2012

BCC Banking system

Source: BCC/ NBR supervision reports

V.2 Back to Profit

22

BCC’s net profit of 16.1 M RON, up 75% on H1, 2012

Balance sheet

Notes (1) All numbers except ROE are based on IFRS financial statements

43.7 42.0 30.5

M RON 2012 2013 H1 %

Total Assets 4726 3608 (24)

Loans (net) 1183 1300 +10

Financial Assets 2652 1530 (42)

Total Liabilities 4362 3232 (26)

Deposits 2514 2620 +4

Equity 364 383 +5

Performance

M RON 2012 H1 2013 H1 %

Total Banking Income 96 118 +24

Total Cost (77) (82) +7

Pre-provision profit 19 36 +88

Provisions (7) (26) ++

Profit before Tax 12 10 (16)

Net Profit 9 16 +75

Credit Risk Rate (%)

2012 H1 2013 H1 2013

53.3 72.5 60.7 Deposits / Total Assets (net) (%)

59.1 61.7 114 Loans (gross) to Deposits (%)

BCC Banking system

2.1 2.4 Net Interest Margin (%)

2012 H1 2013 H1 2013

84 69 Cost to Income Ratio (%)

6.0 12.0 6.0 ROE (%)

V.3 Strong year-to-date Performance

10.7 10.6 14.7 Capital Adequacy Ratio (%)

23

VI. Conclusions and Final Remarks

1. Key Investment Highlights 2. Potential Upside

Johan Gabriëls, Chief Executive Officer

24

New, highly experienced and motivated team with excellent reputation

Access to skilled staff within BCC

One of the best teams in the market 1

International network and projects The bank of opportunities Cross-sell potential Deleveraging by non-Romanian banks

Untapped opportunities 2

Full Romanian banking license Opportunity to passport to all EU countries

Regulatory 3

Operations and IT proven to be flexible Speed to market delivery

Flexible business model 4

Towards Sustainable financial strength

Healthy balance sheet structure

Self-funded business

Service excellence as differentiating factor

VI.1 Key Investment Highlights

25

Optimise Loan Expansion / Risk Appetite

Current loan to deposit ratio ~ 60% … target 80% - 90% … major upside for

additional lending potential based on current deposit base

Many foreign owned Romanian banks reducing lending activities =

opportunities for Carpatica to pick up SME and large local customers

Optimise Client and Product Strategies

Carpatica developing / implementing new products / services

Partnership with brokers outside Romania

Remittances solutions

Treasury sales

Online trading

New online payment solutions

Commodities

Optimise Operating Efficiencies

VI.2 Potential Upside