Embed Size (px)

Citation preview

The past week has been nothing less than eventful. Qatar Central Bank’s surprise directive to cease Islamic banking windows by the end of the year has caught industry players off guard. Many are still reeling from the announcement, trying to make sense of the impact on the banking world, both Islamic and conventional, while the central bank keeps mum on the matter.

India too threw a curveball when the Kerala High Court dismissed a petition challenging the setting up of Islamic banks in India, taking the country one step closer to making Shariah banking a reality despite its current law and lack of regulation. Whether or not it does take off remains to be seen. We examine the issues for Qatar and India in our IFN reports.

While industry players in both Qatar and India may well be occupied with assessing the impact and opportunities that lie ahead, Advent Software has been doing the same with regards to the Islamic Financial Reporting Standards (IFRS). In the current scenario, convergence is not yet a reality within the Islamic fi nancial community. While some opt for IFRS and a convergence of standards, some do not permit them, and others implement them with local adaptations, says Advent in its report.

IFRS is in fact issued by the International Accounting Standards Board (IASB). It seems that the IASB and AAOIFI, both standard setting organizations, have entirely different priorities, according to Mohammed Amin, Islamic fi nance consultant and former head of Islamic fi nance at PwC (UK). He suggests in his report that each leverage on the other’s strengths to the extent of partnering and exchanging roles. He even questions the

appropriateness of AAOIFI’s role with regards to accounting standards.

Speaking of roles, the Bermuda Monetary Authority comes to the fore with the potential to be largely instrumental in the growth of Takaful in the offshore jurisdiction, according to law fi rm Conyers Dill & Pearman. Their report considers the various structures available for Takaful and re-Takaful operators in Bermuda, and the various opportunities that lie beneath.

Before opportunities can be explored in Tanzania, the country needs to address the challenges that stand in the way for Islamic fi nance, based on a report by Stanbic Bank Tanzania. The bank gives an overview of the situation in the country, stating that Islamic banking faces two main challenges — lack of capacity and low levels of awareness, before the industry can fi rmly take root in Tanzania.

A growth in the level of awareness for Islamic fi nance will surely bring with it confi dence in exploring and accepting its products as an alternative to conventional funds. At least, that is what Christina Tung, managing director of Mayfair Pacifi c Financial Group looks forward to. Tung, who is featured in Meet the Head this week, heads a fi rm that has been appointed by the government in the Ningxia Hui autonomous region, China to promote Islamic investments.

In Termsheet this week, you will fi nd details of LBS Bina Group’s third issuance of US$6.6 million of its US$44.46 million notes program. LBS is the fi rst issuer to issue Sukuk with the assistance of Malaysia’ fi rst fi nancial guarantee insurer Danajamin.

Vol 8 Issue 5 9th February 2011

T h e W o r l d ’ s G l o b a l I s l a m i c F i n a n c e N e w s P r o v i d e r

In this issue

IFN Rapid ..................................................... 2

Islamic Finance News ................................ 3

Takaful News ............................................... 6

Moves ........................................................... 6

Ratings News .............................................. 7

IFN Reports:Qatar shuts the door on Islamic windows .................................................... 8

Islamic bank in India – Almosta reality ..................................................... 8

Mixed signals in the UAE ....................... 9

Articles:Bermuda: Crossroads for Takaful Opportunities ..........................................10

Which Accounting Standards? .............14

AAOIFI’s Proper Accounting Standards Role ..........................................................16

Meeting Changing Banking Needs in Africa........................................................18

Meet the Head ..........................................19Christina Tung, managing director of Mayfair Pacifi c Financial Group

Termsheet ..................................................20LBS Bina Group US$6.6 million Sukuk

Deal Tracker ..............................................21

Eurekahedge Funds Tables .....................22

REDmoney Indexes ..................................23

S&P Shariah Indexes ...............................24

Dow Jones Shariah Indexes ....................25

Dealogic League Tables ...........................26

Thomson Reuters League Tables ...........29

Events Diary...............................................32

Company Index .........................................33

Subscription Form ....................................33

Impact versus opportunity

Job Search For Islamic Finance ProfessionalsTo find out more about Barakat Jobs, logon to

www.BarakatJobs.com today, and reach your potential.

Page 2© 9th February 2011

www.islamicfi nancenews.comA round-up of all this week’s news IFN RAPID

• Egyptian crisis rings fear for investors and market participants, say fund managers

• Country to launch Islamic banking soon, says governor of Central Bank of Nigeria

• First Community Bank launches Shariah compliant unit trust fund

• Bank Muamalat Indonesia plans to quadruple Shariah debt

• The IDB takes 10% stake in Sri Lanka’s Amana Bank

• Bank Kerjasama Rakyat Malaysia and Mastercard Worldwide launch One Retail Cash Islamic Debit

• QSR Brands increases interest in Al-‘Aqar KPJ REITs to 4.77 million shares

• Kerala High Court approves Shariah compliant Al Baraka Financial Services to start operations as India’s fi rst Islamic bank

• More investments to come from the UAE, says Luxembourg’s minister of fi nance

• National Bank of Kuwait Group announces US$1.07 billion in profi ts for 2010

• National Bank of Abu Dhabi profi t up by 22% in 2010

• Ajman Bank charts US$1.1 million in net profi t for its fi nancial year ending on the 31st December 2010

• Bahrain Financial Exchange launches online trading platform for Murabahah transactions

• Abu Dhabi Islamic Bank launches 97% capital protected BRIC Currency Notes

• Qatar Central Bank orders conventional banks to close their Islamic banking windows

• Saudi Telecom seals deal with Samba Financial Group and HSBC Bahrain to provide US$280 million fi nancing to VIVA Bahrain

• Two Dubai properties of American International Group taken over by consortium of banks

• Syria International Islamic Bank and MasterCard Worldwide launch credit and debit cards

• Jordan Dubai Islamic Bank signs agreement with Visa Jordan to provide Shariah compliant charge cards

• Unicorn Investment Bank cancels plan to buy Dubai Group’s 40% stake in Bank Islam Malaysia

• BMI Bank launches new tag line to reinforce position as customer centric bank

• The Saudi British Bank signs US$533 million in Islamic fi nance deals with Abdul Latif Jameel Group

• National Leasing Holding Company charts a net profi t of US$59 million in 2010

• SHUAA Capital halves losses in 2010 to US$61 million

• Qatar International Islamic Bank plans to issue at least US$500 million Sukuk by mid year

• Gulf Bank returns to profi t in 2010 by posting a net income of US$68.4 million

• Barwa Bank completes acquisitions of The First Investor, First Finance Company and First Leasing Company

TAKAFUL• Mitsui Sumitomo Insurance eyes

35% stake in Malaysian Takaful operator Hong Leong Tokio Marine Takaful

• Amana Takaful (Maldives) applies to be listed on the Maldives Stock Exchange

• Takaful industry may see mergers and acquisitions, says CEO of Takaful Ikhlas

• Department of Shariah affairs and Takaful Brunei Am ink deal to provide Takaful to enforcement offi cers

• Al Khaleej Takaful Insurance and Reinsurance announces US$20 million profi ts for 2010

RATINGS• Fitch assigns individual rating of

‘C/D’ to Dubai Islamic Bank

• MARC affi rms ‘AAAID’ rating on Kwantas SPV’s outstanding US$26 million class ‘A’ Sukuk

• PACRA upgrades Askari Islamic Income Fund’s stablility rating to ‘AA-(F)’ from ‘A+(f)’

• Shariah Quality Rating of ‘AA’ for Jordan Islamic Bank by Islamic International Rating Agency maintains

MOVES• Al Baraka Bank Pakistan appoints

Adnan Ahmed Yousif as chairman of the board of directors

• Al-Amanah Islamic Investment Bank of the Philippines appoints Enrique D Bautista Jr as chairman and CEO

NEWS

Disclaimer: Islamic Finance news invites leading practitioners and academics to contribute short reports each week. Whilst we have used our best endeavors and efforts to ensure the accuracy of the contents we do not hold out or represent that the respective opinions are accurate and therefore shall not be held responsible for any inaccuracies. Contents and copyright remain with REDmoney.

NEW SERVICE

We’re not just a Weekly but also a Daily news provider

Register now for RSS Feeds on www.islamicfinancenews.com

Page 3© 9th February 2011

www.islamicfi nancenews.comNEWS

AFRICACrisis stirs concernEGYPT: Average yields for Sukuk have plummeted in the Gulf after seven weeks of turmoil in Egypt.

Investors are being cautious and the turmoil may have long-term effects on Islamic markets in the Middle East if not resolved soon, said Muhammad Asad, chief investment offi cer at Al Meezan Investment Management.

Rohit Chawdhry, portfolio manager at Bahrain Islamic Bank, said market participants fear that the contagion may spread in the Middle East causing an oil price hike which would impact global economic growth.

Shariah banking soonNIGERIA: Islamic banking will soon begin in Nigeria, said Sanusi Lamido Sanusi, governor of the central bank.

Sanusi urged Nigerians to help make the Islamic banking initiative a success as it will help to develop the country’s economy.

New Islamic unit trust fundKENYA: First Community Bank has received approval from the Capital Markets Authority to introduce an Islamic unit trust fund. The fund will make selective investments in equities, government bonds and real estate options that are Shariah compliant.

Nathif Adam, the CEO said the bank sees this move as strengthening its portfolio of Islamic fi nancial services.

He added that many Muslims are unable to buy bonds or stocks because the products are not structured according to Shariah values.

ASIAOptimistic targetINDONESIA: Bank Muamalat Indonesia is planning to quadruple its Shariah compliant debt holdings from IDR500 billion (US$55.4 million) to IDR2 trillion (US$222 million) in 2011, said Hendiarto, its chief fi nancial offi cer.

He added that with a current asset base of IDR20.4 trillion (US$2.27 billion), the bank is targeting asset growth of 50% in 2011 compared to 32% last year.

IDB buys 10% stakeSRI LANKA: The Islamic Development Bank (IDB) has acquired a 10% stake in Amana Bank.

Amana Bank received fi nal approval from the minister of fi nance in January to operate as the fi rst Islamic bank in Sri Lanka.

New Islamic debit cardMALAYSIA: Bank Kerjasama Rakyat Malaysia and Mastercard Worldwide has launched a debit card called One Retail Cash Islamic Debit (Orchid Card) based on the concept of Wakalah and Ujrah.

According to Kamaruzaman Che Mat, its managing director, cardholders will not be required to pay any membership fee. They only need to pay the RM8 (US$2.64) annual fee from the second year onwards.

Page 4© 9th February 2011

www.islamicfi nancenews.comNEWS

Stake expansionMALAYSIA: Investment holding fi rm QSR Brands has increased its interest in Al-‘Aqar KPJ REITs to 4.77 million shares, worth RM5.11 million (US$1.68 million) by acquiring an additional 2.82 million units of the hospital REIT.

QSR purchased 2.27 million shares last month and 553, 200 shares on the 21st July 2010.

EUROPEWidening revenue streamsLUXEMBOURG: Luxembourg is eyeing more investments from the UAE, said Luc Frieden, minister of fi nance. He highlighted plans to open an embassy in Abu Dhabi later this year to facilitate regional investments.

In Luxembourg’s various investment funds, AED2.485 billion (US$676 million) come from UAE investors, said Frieden.

He also added that the country is a prime location for Islamic fi nance with 16 Sukuk listed on the Luxembourg Stock Exchange, and a treaty with the UAE to avoid double taxation.

MIDDLE EASTProfi t increaseKUWAIT: National Bank of Kuwait Group has reported profi ts of KWD301.7 million (US$1.075 billion) for last year, an increment of 14% compared to 2009.

Total assets stood at KWD12.9 billion (US$46 billion) and shareholder’s equity at KWD2.1 billion (US$7.4 billion).

The bank recommended a cash dividend of 40 fi ls (14.3 US cents) per share and a 10% bonus share distribution.

Profi ts soarUAE: National Bank of Abu Dhabi has reported a profi t of AED3.68 billion (US$1 billion) for 2010, an increment of 22% compared to AED3.02 billion (US$822.2 million) in the previous year

Total assets grew by 7.4% to AED211.4 billion (US$57.55 million) while deposits increased 6.5% to AED123.1 billion (US$33.51 billion).

e-Tayseer launchedBAHRAIN: Bahrain Financial Exchange (BFX) has started operations with e-Tayseer, an online trading platform for the sale and purchase of underlying assets for Murabahah transactions.

BFX, the fi rst multi asset exchange in the Middle East and North Africa will initially deploy e-Tayseer with its Islamic division Bait Al Bursa and fi ve banks, said Arshad Khan, managing director and CEO.

Arshad said the bourse is targeting by year end to tap 30% of global Murabahah transactions which has a volume of between US$8 billion and US$10 billion daily.

Making progressUAE: Ajman Bank has posted AED4 million (US$1.1 million) in net profi t for its fi nancial year ending the 31st December 2010, an increase from the marginal profi t of AED1.1 million (US$299,474) in 2009.

The bank’s income rose 84% to AED144 million (US$39 million), while customer deposits went up 157% to AED2 billion (US$544.5 million).

New BRIC notesUAE: Abu Dhabi Islamic Bank has launched a 97% capital protected BRIC Currency Notes, which is based on Murabahah principles.

The notes will enable investors to obtain a return of up to 22% at maturity by investing

in the currencies of four BRIC countries — Brazil, Russia, India and China, for two years.

Subscription will be on a fi rst come fi rst served basis and is available until the 3rd March, with a minimum subscription of US$30,000.

Major deal for VIVA BahrainBAHRAIN: Saudi Telecom (STC) has signed an agreement with Samba Financial

continued...

First Islamic bank INDIA: The Kerala High Court has given approval to Shariah compliant Al Baraka Financial Services to start operations as India’s fi rst Islamic bank with Kerala State Industrial Development Corporation as an investor.

The Kerala High Court also dismissed the petitions of Janata Party leader Subramanian Swamy and others fi led against the Kerala state government’s decision to establish the Islamic bank.

(See IFN Report on page 8)

Islamic windows shutdownQATAR: Qatar Central Bank (QCB) announced the termination of Islamic banking services offered by conventional banks, and has given a grace period until the 31st December this year for the banks to close their Islamic windows.

The local conventional banks involved are Qatar National Bank, Commercial Bank of Qatar, Doha Bank and International Bank of Qatar.

The order gives no direction on whether banks can apply for separate Islamic banking licences and suggests a lack of transparency in the country, say bankers.

John Sfakianakis, chief economist at Banque Saudi Francais, said that the vague directive creates an unlevel playing fi eld for investors and those observing the Qatar economy.

On the other hand, Doha Bank does not expect a major fi nancial impact as approximately 89% of the bank’s books are conventional, said Raghavan Seetharaman, its group CEO.

Mohd Daud Bakar, CEO of Amanie Business Solutions said QCB’s decision is in accordance with Malaysia’s development model for its Islamic banking sector, and is a positive step in terms of competition for Islamic banking.

The local conventional banks as well as HSBC Amanah are currently in talks with the central bank for a workable solution.

(See IFN Report on page 8)

Page 5© 9th February 2011

www.islamicfi nancenews.comNEWS

Group and HSBC Bahrain to provide a seven-year US$280 million Islamic fi nancing facility for STC’s wholly owned subsidiary, mobile telecommunications operator VIVA Bahrain.

The facility consists of US$100 million from HSBC and US$180 million from Samba Financial Group.

“STC is keen to expand its international operations,” said Ameen Al-Shiddi, its vice president of fi nance.

New MastercardsSYRIA: Syria International Islamic Bank in collaboration with MasterCard Worldwide has launched four credit and debit card programs.

They are MasterCard Al Mas Platinum and MasterCard Zhahab Gold credit cards; MasterCard Fiddhah and MasterCard Zomorod debit cards.

Islamic Visa cardsJORDAN: Jordan Dubai Islamic Bank has signed an agreement with Visa Jordan to provide Shariah compliant charge cards to the bank’s customers.

The card has a JOD15,000 (US$21,156) charge limit.

Unicorn scraps plan BAHRAIN: Bahrain based Unicorn Investment Bank has cancelled its plan to buy the 40% stake in Bank Islam Malaysia currently

owned by Dubai Group, said Ikbal Daredia, acting chief executive of Unicorn.

Unicorn has also effectively repaid a three-year US$125 million Murabahah facility involving more than 20 banks, settling Unicorn’s long-term debt, said Ikbal.

Rebranding programBAHRAIN: BMI Bank has launched its new tag line ‘Better, Together’ to strengthen its position as a customer centric bank.

The bank also plans to soon embark on a rebranding exercise.

US$533 million in fi nancingSAUDI ARABIA: The Saudi British Bank has signed Islamic fi nance agreements worth SAR2 billion (US$533 million) with Abdul Latif Jameel Group.

The agreements include three securitization deals for the benefi t of the group’s installment wing, United Installment Sales, and a stock fi nance Murabahah agreement.

Profi ts riseQATAR: National Leasing Holding Company (NLHC) has posted a net profi t of QAR179.83 million (US$59 million) for 2010, from QAR90.21 million (US$29.7 million) in the previous year.

Total assets rose 13% to QAR2.03 million (US$669 million), while total revenue increased 113% to QAR458 million (US$151 million).

Mixed performanceUAE: SHUAA Capital halved its losses in 2010 to AED223.6 million (US$61 million), from AED529.8 million (US$144 million) in 2009.

In the same period, the bank’s income decreased by 29.7% to AED188.4 million (US$51 million), while total assets lowered 32.5% to AED1.92 billion (US$522 million), and total liabilities slid 61% to AED704 million (US$191.7 million).

QIIB Sukuk to come QATAR: Qatar International Islamic Bank (QIIB) is planning to issue a benchmark-sized Sukuk of at least US$500 million by the middle of this year.

No banks have yet been mandated on the deal.

Swinging back to profi tKUWAIT: Gulf Bank has returned to profi t in 2010 by posting a net income of KWD19.1 million (US$68.4 million), compared to a loss of KWD28.1 million (US$100.3 million) in 2009.

Ali Abdul Rahman Al Rashaid Al Bader, its chairman attributed the performance to recovery in Kuwait’s economy, increase in public infrastructure projects, new business strategy, growth in credit facilities and expansion in banking services.

Takeover fi nalizedQATAR: Barwa Bank has completed the acquisitions of The First Investor, First Finance Company and First Leasing Company.

The bank has also announced the distribution of share certifi cates for Barwa Bank to shareholders, to replace those of the three entities.

continued...

Double takeoversUAE: Two Dubai properties of American International Group (AIG) have been taken over by a consortium of banks after a breach of valuation covenant.

The properties were acquired by AIG under an Ijarah agreement from the consortium comprising of Noor Islamic Bank, National Bank of Abu Dhabi, Abu Dhabi’s First Gulf Bank, United Arab Bank and United Bank.

The outstanding amount for the facility is AED430 million (US$117 million).

(See IFN Report on page 9)

Too many pieces in the puzzle?

Let IFN put ittogether for you…

SUBSCRIBE TOIFN TODAY

www.IslamicFinanceNews.com

Page 6© 9th February 2011

www.islamicfi nancenews.comTAKAFUL NEWS

ASIAAttractive Islamic InsuranceJAPAN: Mitsui Sumitomo Insurance, a unit of Japan’s property-casualty insurance fi rm MS&AD is eyeing a 35% stake in Malaysian Takaful operator Hong Leong Tokio Marine Takaful (HLTMT), which is currently owned by Japanese insurer Tokio Marine & Nichido.

Tokio Marine & Nichido, a unit of Tokio Marine Holdings, recently expressed a desire to divest of its stake in HLTMT and sell it back to Hong Leong Financial Group, before the Group sells it on to Mitsui Sumitomo.

Signifi cant applicationMALDIVES: Amana Takaful (Maldives), a subsidiary of Sri Lanka’s Amana Takaful Insurance, has applied to be listed on the Maldives Stock Exchange.

According to the bourse, the local Takaful operator is the fi rst foreign owned Shariah compliant company which has applied for the listing.

Takaful consolidationMALAYSIA: The Malaysian Takaful industry may see a wave of mergers and acquisitions following the implementation of proposed risk based capital framework, said Syed Moheeb Syed Kamarulzaman, president and CEO of Takaful Ikhlas.

He highlighted that under the framework, the required capital will change signifi cantly.

According to industry players, the proposed framework may be implemented this year and could lead to consolidation among Takaful operators to meet the capital requirements.

Takaful for Shariah offi cersBRUNEI: The department of Shariah affairs and Takaful Brunei Am have signed an agreement to provide a one-year personal accident cluster Takaful scheme coverage to the department’s enforcement offi cers.

The scheme will provide coverage in the event of death and permanent disablement, due to accident or illness occurring within 12 months.

MIDDLE EASTSteady progressQATAR: Al Khaleej Takaful Insurance and Reinsurance has reported a profi t of QAR72.84 million (US$20.04 million) for 2010, a rise of 7% from 2009. The company has proposed a cash dividend of 30%.

Total investments and other income had a 58% growth of QAR117.4 million (US$32.29 million) compared to 2009. Total expenses stood at QAR30.87 million (US$8.49 million).

The shareholders’ defi cit was QAR610,000 (US$170,000) from Takaful operations compared with a QAR33.31 million (US$ 9.17 million) surplus last year.

Total assets stood at QAR976.54 million (US$268.65 million).

AL BARAKA BANK PAKISTANPAKISTAN: Adnan Ahmed Yousif has been elected chairman of the board of directors of Al Baraka Bank Pakistan.

He is also the president and CEO of Al Baraka Banking Group.

AL-AMANAH ISLAMIC INVESTMENT BANK OF THE PHILIPPINESPHILIPPINES: Al-Amanah Islamic Investment Bank of the Philippines has appointed Enrique D Bautista Jr as its new chairman and CEO.

He replaces Armando O Samia who has rejoined the marketing department of state-owned Development Bank of the Philippines.

MOVESSection Sponsor

IFN

= INDEPENDENT= FACTUAL= NEUTRAL

For more information, visit www.islamicfinancenews.com

DON’T YOU THINK YOU SHOULD BE

SUBSCRIBING?

Page 7© 9th February 2011

www.islamicfi nancenews.comRATINGS NEWS

ASIAStrong backing

UAE: Fitch Ratings has assigned Dubai Islamic Bank a long-term foreign currency issuer default

rating (IDR) of ‘A’ with a stable outlook, short-term IDR of ‘F1’, individual rating of ‘C/D’ and support rating fl oor of ‘A’. The support rating has been affi rmed at ‘1’.

The long- and short-term ratings are based on the support from the UAE government. The individual rating refl ects the strong franchise, earning power and satisfactory liquidity position of the bank.

Sturdy fi nancial supportMALAYSIA: Malaysian Rating Corporation (MARC) has affi rmed its ‘AAAID’

rating on Kwantas SPV’s outstanding RM80 million (US$26 million) class ‘A’ Sukuk with a stable outlook.

The move is based on the satisfactory net operating income from the company’s securitized plantation estates.

The estates’ consolidated net operating income of RM49.9 million (US$16 million) for 2010 was 78% higher than MARC’s assessed sustainable revenue of RM28 million (US$9.2 million).

Moving up PAKISTAN: The Pakistan Credit Rating Agency (PACRA) has upgraded the stability rating of Askari Islamic Income Fund to ‘AA-(F)’ from ‘A+(f)’.

The move is based on Askari Investment Management’s capacity to manage the fund’s returns.

MIDDLE EASTDominant power

JORDAN: Islamic International Rating Agency has maintained the Shariah Quality Rating of ‘AA’ for

Jordan Islamic Bank.

According to the agency, the rating is supported by the bank’s highly qualifi ed Shariah supervisory board and a vibrant Shariah audit department.

3rd - 5th October, Kuala Lumpur

Page 8© 9th February 2011

www.islamicfi nancenews.comIFN REPORTS

Qatar shuts the door on Islamic windows

Qatar Central Bank (QCB), in a surprise move issued a circular last week ordering conventional banks in the country to shut down their Islamic window operations by the 31st December 2011. This move came without warning or market player consultation. Nor has the central bank given any indication that the conventional banks involved will be allowed to apply for separate Islamic banking licences to circumvent a loss of revenue stream.

The circular affects seven conventional banks including Qatar National Bank (QNB), Commercial Bank of Qatar, Doha Bank, International Bank of Qatar, HSBC, al khaliji Bank and AhliBank. Some are now lobbying for a workable solution with QCB.

“This is likely to have a signifi cant impact on the Islamic fi nance industry in Qatar as it will effectively reduce the number of Islamic fi nancial service providers by over half within 10 months,” said Amjad Hussain, partner at Doha based law fi rm Eversheds.

Speculation has it that the seven conventional banks may be asked to sell off their Islamic assets to their fully fl edged Islamic competitors, which are Qatar Islamic Bank, Qatar International Islamic Bank, Masraf Al Rayan and Barwa Bank.

If so, the current four Islamic banks stand to benefi t from enhanced revenue streams from Shariah sensitive customers who will be seeking alternative channels to place their money. With this possibility and a potential widening of customer base, shares of Islamic banks have soared in recent days, with Masraf Al Rayan’s up 10% and Qatar Islamic Bank’s rising to 9.4%.

Qatar’s Islamic banking sector began with the opening of Qatar Islamic Bank in 1983. It was not until 2005 when QCB allowed conventional banks to open Islamic windows, a move that has since attracted almost 100,000 customers.

To date, the Islamic banking sector has grown to four Islamic banks and seven Islamic windows, and has achieved an overall market share of 20% of the banking industry.

Alternatively, it would be faster and easier for the conventional banks to set up subsidiaries in the form of separate Islamic banks, if allowed, rather than fully converting into an Islamic institution. It would also allow the conventional banks to retain their Shariah sensitive customers.

Another motivation for QCB’s decision may be the possible mixing of conventional and Islamic funds, which poses a threat to the Shariah compliance of Islamic banking windows. Amjad believes that the preferred method of operation for a regulator is to have clarity, with one set of rules for Islamic banks and another for conventional banks.

“However, the concern that the Islamic fi nance industry has is the lack of proper industry and stakeholder-wide consultation as well as the timescale in which the changes are coming into force. This may deter foreign investors at a time when Qatar needs to bring them in the most,” said Amjad.

Bankers have voiced that the decision has brought about confusion, highlighting a lack of transparency and an unlevel playing fi eld for investors and players following the Qatari economy. The real effect that this decision carries for banks is still vague, with analysts projecting

QNB as the most severely impacted if it is forced to exit Islamic banking. Doha Bank does not expect a major fi nancial impact as its Islamic window operations account for only 11% of the total asset book. The fi nancial markets and investors have shown a more intense reaction to the news with QNB’s shares plummeting by 4.8% following the news.

How QCB plans to deal with existing long term Shariah compliant fi nancing by conventional banks is still unclear. “These changes, if they are to have an immediate impact, may constitute a material change in law under existing facilities and this may, depending upon terms, lead to the acceleration of re-payment obligations,” added Amjad.

Ashar Nazim, executive director and MENA head of Islamic fi nancial services group at Ernst & Young, believes that many more central banks may take their cue from Qatar. If central banks start tightening the screws on Shariah governance and auditing, Islamic banks may have an advantage over conventional banks in maintaining stricter control over Shariah compliance, said Ashar.

Islamic bank in India – Almost a reality

Last week, the Kerala High Court dismissed a petition objecting to the creation of an Islamic fi nancial institution, bringing India much closer to the reality of developing Islamic banking within its shores. While this has given Al Baraka Financial Services (Al Baraka) the approval it needs to start operations as the country’s fi rst Islamic bank, the high court did however caution that the bank was to work in accordance with the fi nancial laws of the country.

The ruling by the Kerala High Court may give constitutional validity to an Islamic bank in India, but the hurdle of the lack of regulatory framework and law still stands, at least as far as the Reserve Bank of India (RBI) is concerned. The stand that the RBI has thus far taken is that Shariah banking is not possible given the present regulation.

“With this court ruling, the government may consider giving some relaxation for Shariah compliant banks. Things will start moving, but it will still take time,” said Ali M Shervani, director at investment advisory fi rm Miftah Advisory India.

Al Baraka was set up with an authorized capital of INR10 billion (US$220 million) with the aim of starting up an Islamic bank in 2009, an initiative from Dr TM Thomas Isaac, state minister for fi nance and the non-resident Indian community.

The initial proposal also contains the appointment of an advisory body, comprising Islamic scholars to ensure Shariah compliance of the fi nancial entity. Once formed, the Kerala State Industrial Development Corporation is to hold an 11% stake in Al Baraka.

The interest in the proposed institution has been strong. Shri Elamaram Kareem, state minister for industries highlighted that immediately after the plan was drawn up, a large corporation with interest in multiple domains sought 74% stake in it. Doha Bank also expressed a desire to pick up a 46% equity.

Ali emphasizes the fact that a cautious approach needs to be taken with regards to Islamic banking in India, and “it would be of crucial importance to see which players take the lead in developing this industry”.

continued...

Page 9© 9th February 2011

www.islamicfi nancenews.comIFN REPORTS

He further added that a need is there for major fi nancial institutions like HSBC and Standard Chartered with vast experience in Islamic fi nance globally to step into the Indian market, to capitalize on their expertise, establish infrastructure and Islamic product lines.

This victory of sorts follows from a year long battle with the courts, in which the fi nal verdict by the Kerala High Court was to dismiss a petition fi led in January 2010 by Subramanian Swamy, former law minister and Janata Party chief, and RV Babu, head of Hindu Aikyavedi, claiming that the state government’s participation in the creation of an Islamic bank violates the principle of secularism in the Indian constitution.

The decision marks another positive sign for the world’s largest Muslim minority of 160 million. Recent efforts which have exposed the Indian market to Shariah compliant fi nance and investment options include the successful launch of the BSE TASIS Shariah 50 Index by the Bombay Stock Exchange and Taqwaa Advisory and Shariah Investment Solutions.

The launch of an Islamic bank will assist the economy and have wide reaching economic impact for Kerala as well as the country. According to the Centre for Development Studies, INR250 billion (US$5.5 billion) to INR280 billion (US$6.17 billion) is remitted by Keralans into the state.

The major chunk of the remittance is invested in real estate and gold. The introduction of Islamic banking in Kerala can contribute to channeling these funds to more productive use.

Mixed signals in the UAE

The UAE economy is expected to grow by more than 3% in 2011, a slight increase from the estimated 2.3% in 2010, as the banking

sector grapples with fi nancial diffi culties this year. Economic progress is positive based on rising oil prices and the fi nalization of Dubai World’s US$25 billion restructuring plan in September last year. But contrasting signals are being sent from the real estate business, with two major developments last week. In a strong move from the UAE banks, two commercial properties in the UAE have been taken over from the real estate arm of insurance giant American International Group (AIG). The strong action came after AIG’s refusal to pay more to cover its creditors’ risk. The properties have been on the seller’s market since early 2009 without much success. This was a part of AIG’s plan to dispose of assets in order to raise funds for the repayment of the US government’s rescue fund.

The move came about when AIG violated a valuation covenant in an Islamic leasing agreement (Ijarah).The properties had been acquired under Ijarah in 2008 via a consortium of banks including Noor Islamic Bank, National Bank of Abu Dhabi, First Gulf Bank, United Arab Bank and United Bank. The outstanding amount of the Ijarah facility is understood to be AED430 million (US$117 million).

The second development includes property giant Dubai World narrowly avoiding default on US$3.52 billion debt, and its overseas arm Istithmar World recently breaching a loan to value ratio covenant on debt against the Adelphi building in London worth US$427 million. The asset revaluation last month put the loan to value ratio at 89.48% in breach of contractual limit of 80%.

According to a statement from Indus Holding, the vehicle that issued the notes for the Adelphi debt, US$341 million is still outstanding against the property. All surplus rent on the property is now being used to pay off the debt, which is due to mature later this year. This default may well lead to the sale of the building.

Register to secure yor FREE seat now!

www.ifnroadshow.com

ww!!w!!

Free to attend, although all delegates will bescreened before qualifyingFocusing on markets which are developing in theslamic nance world

Particular focus on that market with international participationStandard format ensuring everyone knows exactlywhat to expect from each eventPlenary sessions – no sales pitchesShort one-day events – senior individuals don’thave the time to attend lengthier eventsTargeting between 125 and 250 for each eventCooperation and participation from local regulatorsPractitioner led, with some Shariah scholarsproviding the perfect mixConclusions will be delivered at the end of each eventIssuers and investors will be in attendance– not just the intermediaries

Page 10© 9th February 2011

www.islamicfi nancenews.comCOUNTRY REPORT

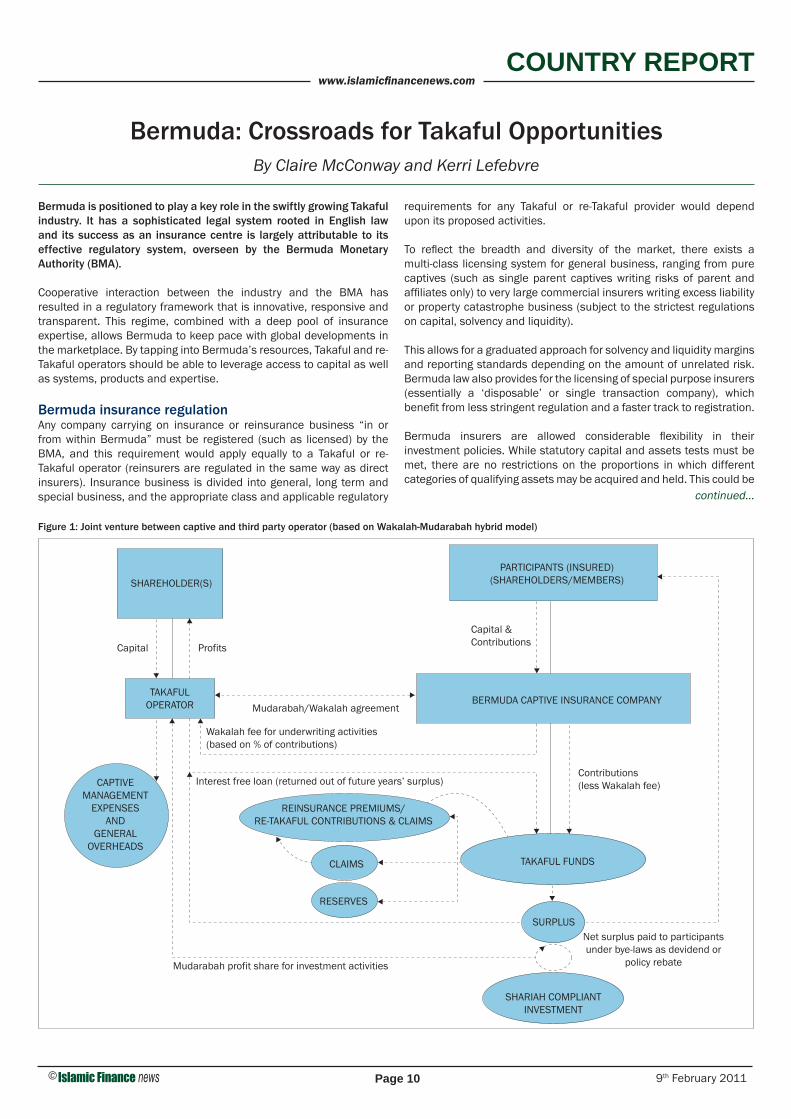

Bermuda is positioned to play a key role in the swiftly growing Takaful industry. It has a sophisticated legal system rooted in English law and its success as an insurance centre is largely attributable to its effective regulatory system, overseen by the Bermuda Monetary Authority (BMA).

Cooperative interaction between the industry and the BMA has resulted in a regulatory framework that is innovative, responsive and transparent. This regime, combined with a deep pool of insurance expertise, allows Bermuda to keep pace with global developments in the marketplace. By tapping into Bermuda’s resources, Takaful and re-Takaful operators should be able to leverage access to capital as well as systems, products and expertise.

Bermuda insurance regulationAny company carrying on insurance or reinsurance business “in or from within Bermuda” must be registered (such as licensed) by the BMA, and this requirement would apply equally to a Takaful or re-Takaful operator (reinsurers are regulated in the same way as direct insurers). Insurance business is divided into general, long term and special business, and the appropriate class and applicable regulatory

requirements for any Takaful or re-Takaful provider would depend upon its proposed activities.

To refl ect the breadth and diversity of the market, there exists a multi-class licensing system for general business, ranging from pure captives (such as single parent captives writing risks of parent and affi liates only) to very large commercial insurers writing excess liability or property catastrophe business (subject to the strictest regulations on capital, solvency and liquidity).

This allows for a graduated approach for solvency and liquidity margins and reporting standards depending on the amount of unrelated risk. Bermuda law also provides for the licensing of special purpose insurers (essentially a ‘disposable’ or single transaction company), which benefi t from less stringent regulation and a faster track to registration.

Bermuda insurers are allowed considerable fl exibility in their investment policies. While statutory capital and assets tests must be met, there are no restrictions on the proportions in which different categories of qualifying assets may be acquired and held. This could be

Bermuda: Crossroads for Takaful OpportunitiesBy Claire McConway and Kerri Lefebvre

SHAREHOLDER(S)

TAKAFULOPERATOR

Capital Profits

Mudarabah/Wakalah agreement

Wakalah fee for underwriting activities(based on % of contributions)

Interest free loan (returned out of future years’ surplus)

Mudarabah profit share for investment activities

Net surplus paid to participantsunder bye-laws as devidend or

policy rebate

Contributions(less Wakalah fee)

Capital &Contributions

CAPTIVEMANAGEMENT

EXPENSESAND

GENERALOVERHEADS

REINSURANCE PREMIUMS/RE-TAKAFUL CONTRIBUTIONS & CLAIMS

CLAIMS

RESERVES

SHARIAH COMPLIANTINVESTMENT

SURPLUS

TAKAFUL FUNDS

BERMUDA CAPTIVE INSURANCE COMPANY

PARTICIPANTS (INSURED)(SHAREHOLDERS/MEMBERS)

Figure 1: Joint venture between captive and third party operator (based on Wakalah-Mudarabah hybrid model)

continued...

Page 11© 9th February 2011

www.islamicfi nancenews.comCOUNTRY REPORT

Bermuda: Crossroads for Takaful Opportunities (continued)

advantageous for Takaful operators, which by defi nition have more restrictive investment policies than conventional insurers.

It also should be noted that certain categories of assets which do not automatically qualify as “relevant assets” for general business (such as unquoted equities and real estate) may on successful application to the BMA by the insurer be designated as relevant. This provides considerable scope for focus on Shariah compliant asset classes.

Dividends may be declared and paid by Bermuda insurance companies provided that relevant liquidity and solvency margins are met and the solvency requirements under Bermuda company law are satisfi ed. As a consequence, Bermuda companies enjoy greater freedom to declare dividends than their counterparts in many other jurisdictions.

Bermuda structures for Takaful operationsAs with conventional insurance, Takaful participants vary from corporations to individuals. There is no “one size fi ts all” approach, but it is likely that elements of traditional captive and third party insurance arrangements may facilitate Takaful arrangements.

CaptivesCaptives are privately owned insurance companies, and range from single member captives to group or association captives, which have more than one owner, and from pure captives (which insure only risks emanating from their parent and affi liates) to captives which also underwrite a limited amount of third party risk.

Conventional captive management is typically outsourced by all but the largest of businesses, and specialist Takaful captive management services could also be sub-contracted where necessary. With the exception of single member captives (which would lack the necessary element of mutuality), captives are well suited to Takaful arrangements.

The majority of captives in Bermuda are set up as companies limited by shares, although a small number of multi-owner captives are set up as mutuals (often cited as the conventional counterpoint to Takaful).

These are companies without share capital authorized to carry on insurance or reinsurance business on the mutual principle, meaning that their members, who are exposed to some contingency, contribute premiums on the basis that if the contemplated contingency befalls any member he will receive a compensatory payment.

Since the solidarity principle is already built into the structure, it is easy to see how the mutual concept aligns to Takaful. Commonly used in Bermuda for groups of ship owners or professional fi rms, a mutual structure could be used by any group of persons sharing similar exposure.

In general, captives are best suited to operations with a relatively small number of participants, as the operation cannot exist until the founders have come together and pooled their contributions. The use of captives in Takaful business is therefore likely to attract smaller groups of participants with access to signifi cant capital reserves.

Bermuda law allows captives to be capitalized through equity, debt or contributed surplus, which in the case of a Shariah compliant captive, would need to be structured subject to the usual Shariah considerations.

To the extent that further capital is necessary and is unavailable from the owner-participants, a Shariah compliant captive would need to access capital by way of a Qard through a Takaful operator or through some form of Islamic fi nancing arrangement.

In this regard, an independent conventional insurer could potentially enter into a joint venture with a Shariah compliant captive. The relevant joint venture agreement could provide for remuneration in respect of the management, licensing, underwriting and investment activities to be carried on.

The parties also could agree on the establishment of a Qard facility or some other form of Shariah compliant capital, provided that any issues of corporate benefi t that may arise in this regard are addressed.

While there are a number of possibilities for such a structure, the chart in Figure 1 shows how a captive might work in such a joint venture. In the example given, the captive remains the owner of the Takaful fund which is managed on its behalf by an operator on the basis of Wakalah/Mudarabah.

Third party arrangementsA conventional non-captive insurer is not owned by the policyholder(s), and underwrites mainly or exclusively the risks of third parties. While conventional non-captive insurance contracts typically contravene Shariah principles, what such arrangements have in common with most commercial Takaful schemes is the lack of an ownership interest by the policyholders in the insurance company or operator.

In both cases, the policyholder (or Takaful participant) pays money to an unrelated insurance company (or Takaful operator), and in return, is entitled to make a claim for his loss should the covered risk materialize. In the case of Takaful, Shariah compliance typically is achieved through the relevant contractual arrangements and appropriate provisions in the operator’s constitutional documents.

It should be possible to set up third party re-Takaful arrangements in Bermuda along the lines of what is done in other jurisdictions that have embraced Takaful. The Takaful operator might be an established (re)insurer in Bermuda, or a newly licensed overseas (re)insurer or re-Takaful operator.

In a joint venture situation, the operator might be the vehicle for a partnership between an established conventional (re)insurer with access to capital resources, and an overseas re-Takaful operator with

continued...

“Dividends may be declared and paid by Bermuda insurance companies provided that relevant liquidity and solvency margins are met and the solvency requirements under Bermuda company law are satisfi ed”

Page 12© 9th February 2011

www.islamicfi nancenews.comCOUNTRY REPORT

Bermuda: Crossroads for Takaful Opportunities (continued)

the requisite technical expertise. Such partnerships with established conventional (re)insurers are often cited as a potential solution to the thorny issue of capitalization.

In order to conform to the requirements of Takaful, the operator would not be entitled to all of the profi ts from the operation, but neither would it bear all the risk. Under the Wakalah/Mudarabah hybrid model, the operator would be entitled to its Wakalah underwriting fees and/or its Mudarabah profi t share, and against the possible need for draw down under the Qard facility, the right to recover any advances out of future years’ profi ts.

The diagram in Figure 2 shows how such a model might work in Bermuda. This has been structured so that the company which holds the Takaful fund is incorporated as a subsidiary of the operator, but this might not be necessary depending on the circumstances (such as if the operator is already established and licensed in Bermuda).

Bermuda law allows for a variety of arrangements that might be considered in connection with the re-Takaful fund. For example, it might be held on a ring fenced basis that is purely contractual, through a trust or in a segregated accounts company. Care would need to be taken to ensure the arrangement remains Shariah compliant even on a dissolution or winding up of the operator, since surplus in the re-Takaful fund must not revert to the operator or any liquidator of the operator (other than to settle amounts to which the operator is contractually entitled).

Additional structuring optionsThe Segregated Accounts Companies Act 2000 (SAC Act) sets out rules governing the operation of segregated accounts. While separate accounts to manage risk may be created contractually, SACs are an increasingly popular option for insurers who need to differentiate between categories of risk and accordingly register under the SAC Act.

Figure 2: Third party arrangement (based on Wakalah-Mudarabah hybrid model)

Capital Profits

Wakalah fee for underwritingactivities (based on % ofcontributions)

Interestfree loan (returned out of future years’ surplus)

Mudarabah profitshare forinvestmentactivities

Net surplus paid to participantsunder Mudarabah agreement

Contributions(less Wakalah fee)

Contributions

SHAREHOLDER(S)

TAKAFUL OPERATOR

CAPTIVEMANAGEMENT

EXPENSESAND

GENERALOVERHEADS

REINSURANCEPREMIUMS/RE-TAKAFUL

CONTRIBUTIONS

CLAIMS

RESERVES

SHARIAH COMPLIANT INVESTMENTS

TAKAFUL FUNDS

BERMUDA INSURANCECOMPANY

PARTICIPANTS (INSURED)

SURPLUS

Contributions madeon terms of “policy”(Mudarabah/Wakalahagreement)

continued...

Page 13© 9th February 2011

www.islamicfi nancenews.comCOUNTRY REPORT

Bermuda: Crossroads for Takaful Opportunities (continued)

Given that the Takaful fund must be kept entirely separate from the funds belonging to the operator and there can be no cross contamination of assets and liabilities, a SAC could be a useful Takaful structuring tool. A SAC could be used wholly for Takaful business, or by a conventional (re)insurer who wishes to operate a Takaful or re-Takaful window without having to incorporate and license a new entity.

Since Takaful operators receive fee income which will by defi nition be Shariah compliant, operators may wish to diversify by offering Shariah compliant securities, which would give them the option of accessing the Islamic capital markets. Such instruments could play a part in an increasingly diversifi ed Islamic capital market. The potential to operate SACs may be advantageous in this regard.

In addition, while we do not consider that Bermuda’s existing legal and regulatory framework would pose any substantive obstacles to Takaful, it is worth noting that it is possible to petition the Bermuda Parliament for private bespoke legislation to give enhanced fl exibility, and a number of Bermuda reinsurers and fi nancial institutions are governed by private act.

Additional issues arisingShariah complianceThe requirement to ensure compliance with Islamic principles arises in every Takaful structure. While contractual and constitutional documents will be subject to any secular laws which may apply (by choice or by operation of law), they also must conform to Shariah. The BMA is of course a secular regulator.

Even in Islamic countries the regulator typically does not determine whether an arrangement accords with Shariah. Rather, this requirement is devolved to a Shariah board established by the Takaful operator. The regulator requires the operator to provide evidence that the board has been established and has signed off on the arrangement. It is to be expected that the BMA would impose a similar requirement.

EnforcementAs a self governing overseas territory of the UK, Bermuda’s legal system is based upon that of the UK, and decisions of the English and other Commonwealth courts are highly persuasive. The Supreme Court of Bermuda is the fi rst instance court in Bermuda, exercising unlimited jurisdiction. An appeal lies as of right to the Court of Appeal for Bermuda and thereafter, in more limited circumstances, to the Privy Council.

The question arises as to how the Bermuda courts might deal with disputes involving Takaful contractual arrangements, a point highlighted by the recent English High Court ruling on an appeal from

summary judgment in The Investment Dar Company (TID) versus BLOM Development Bank [2009].

A lesson learned from the TID case applicable to Takaful operations is that one should not rely solely on the approval of a Shariah board to establish compliance. While obviously not unique to Takaful or Islamic fi nance matters, it is key to ensure that the transaction is within the objects of the relevant company and conforms to other provisions in its constitutional documents, although additional steps should be taken, including requiring parties to waive any defence of non-compliance and/or to obtain independent Shariah advice.

It should be noted that substantive contracts involved in setting up and operating a Takaful arrangement involving a Bermuda entity (in-cluding the Wakalah and/or Mudarabah contracts and the Qard loan facility) generally need not be governed by Bermuda law, other than in relation to matters such as capacity, which are of necessity governed by local law.

The Bermuda courts generally recognize the validity of foreign choice of law provisions and submission to the jurisdiction of overseas courts and tribunals. To the extent that judicial resolution of disputes may be inappropriate, the parties could provide for arbitration. It stands to reason that only tribunals with Takaful expertise should hear cases involving potential default in Takaful arrangements based on Shariah principles.

The way forwardDespite the growth predictions for Takaful, it has suffered during the downturn alongside the rest of the global insurance industry. Nonetheless, projections suggest that Takaful is set to remain the fastest growing area of insurance in the world, including in Western countries.

As a jurisdiction with a potentially advantageous legal and regulatory framework, an established captive insurance and reinsurance market and an interest in opening up to Islamic capital markets, Bermuda provides a unique opportunity for the re-Takaful industry — and vice versa.

The authors gratefully acknowledge the kind assistance of Peter Hodgins, partner at Clyde & Co, Dubai in reviewing the article. This article is not intended to be a substitute for legal advice or a legal opinion. It deals in broad terms only and is intended to merely provide a brief overview and give general information.

Claire McConwayAssociateConyers Dill & PearmanEmail: [email protected] Prior to joining Conyers, Claire spent fi ve years in the London offi ce of US fi rm King & Spalding where she advised on the corporate aspects of Shariah compliant fi nance transactions and investment structures.

Kerri LefebvreDirectorConyers Dill & PearmanEmail: [email protected] has advised issuers and underwriters in connection with IPOs and follow on offerings of debt and equity listed on the NYSE, the Nasdaq, the LSE and other exchanges.

“A lesson learned from the TID case applicable to Takaful operations is that one should not rely solely on the approval of a Shariah board to establish compliance”

Page 14© 9th February 2011

www.islamicfi nancenews.comSECTOR REPORT

The wake up call of the fi nancial crisis has made the need for global accounting and fi nancial reporting standards more pertinent than ever before, as investor and regulator demands for transparency, disclosure and demonstrating best practices increase. As a consequence of globalization and the growing role of Islamic fi nance within the wider fi nancial services industry, players within the Islamic fi nance arena have been active parties in the undertaking to reinforce and homogenize accounting and reporting standards.

Many countries and institutions did not wait for the crisis to start developing common accounting and reporting standards. As early as 1997 the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) was created with this aim. It currently has over 200 members across 46 countries adhering to its guidelines.

Similarly, the International Accounting Standards Board (IASB) has been working towards global convergence of accounting standards for over ten years, proposing the now widely applied International Financial Reporting Standards (IFRS). Since 2008, at the initiative of China, Japan and Korea, the Asian-Oceanian Standard-setters Group (OSG) has been taking part in the IFRS debate, representing the viewpoints of the region on the evolution of those standards. In particular, this group has been closely looking at technical fi nancial reporting issues relating to Islamic fi nance.

As a matter of fact, there is much to gain in using common standards in fi nancial accounting and reporting for both Islamic and conventional fi nance, in terms of increased transparency and comparability of the reporting for regulators and investors worldwide. Moreover, IFRS’s standards are principles based rather than legal based, which makes them applicable to Islamic fi nance, provided that concerned states issue the appropriate complementary guidelines and obligations.

Indeed, while Islamic and conventional fi nance are distinct systems which work differently, in terms of accounting and reporting, the principles are the same, with an aim at accounting for transactions and values.

All states should have a set of standards to ensure the quality and transparency of reporting, and international convergence of these standards can only contribute to greater comparability, and therefore better information, providing for local exceptions and specifi cities.

These specifi cities, however, are still the object of much discussion, and may prove to be a challenge to fi t within the existing framework provided by IFRS to date. Some conventional accounting principles are not necessarily applicable to Islamic fi nancial transactions, nor would they require additional disclosure and explanation.

In addition, for conventional and Islamic fi nancial institutions alike, the adoption of IFRS affects more than just accounting policies and fi nancial reporting. Many aspects of an organization’s business could be affected. The adoption of IFRS may have a transformational impact on fi nancial reporting systems, internal controls, taxes, treasury and cash management with an extended impact on employees, processes, and systems.

Therefore, institutions wishing to implement IFRS or to produce reporting under both IFRS and their national standards may require changes to their operational and technology environments. In many cases, the requirements for IFRS are less specifi c than local standards such as US-GAAP and as such, in many cases treatment under these local standards will work for IFRS.

However, some differences will require different accounting treatment or reporting and therefore have an impact on how fi rms operate and account for their investment activity.

High level considerations include:1. Pricing

Firms that are currently valuing investments using only one type of price under their current standards will need to accommodate additional prices for valuing their assets under IFRS. Depending on how fi rms gather prices and value their investments, this may represent a technology change, as many fi rms are using technology to automate the process of price collection and position valuation.

2. Trade versus settle date representationFirms moving to IFRS who want to report initial recognition of positions as of settle date will need to ensure they are capturing settlement date information. Firms that are tracking positions only based on trade date may not be capturing settle date information today.

3. Transaction costsUnder some accounting standards, transaction costs can be recognized as part of an investment’s cost basis. As such, fi rms may not be tracking these separately from investment cost. Under IFRS, transaction costs may need to be expensed. Firms that are not currently differentiating transaction costs from the investment cost will need to identify transaction costs so that different treatments may be applied.

More specifi cally, IFRS reporting has specifi c requirements that organizations will need to cater for, such as:

1. Statement of cash fl owsThis statement is required for IFRS, and even for fi rms that currently provide it under their local standards, the potential exists for classifi cation differences. In both cases, fi rms will need to capture cash activity with enough detail to generate the statement of cash fl ows and classify appropriately on statements.

2. Classifi cation of investor ownership IFRS requires that investor capital be split between share capital, premium, and surplus. Firms that were not previously tracking different types of ownership may need to do so to report accurately.

Which Accounting Standards? By Kaushiq Kodithodika

continued...

“IFRS’s standards are principles based rather than legal based, which makes them applicable to Islamic fi nance”

Page 15© 9th February 2011

www.islamicfi nancenews.comSECTOR REPORT

Which Accounting Standards? (continued)

3. Recognition of unrealized and realized price and currency gainsUnder some standards such as US-GAAP, fi rms must distinguish between realized and unrealized gains and price and foreign exchange gains. IFRS does not require this. This is an example where a local standard can be more specifi c, and while this may not change current operations for a fi rm adopting IFRS, it may require technology to report both ways without manual effort to combine gains for IFRS.

4. Functional currencyUnder a number of local standards, it is possible for a fund to have different functional currencies. IFRS, on the other hand, does not allow for this. In order to meet IFRS requirements, fi rms therefore need to ensure that additional foreign exchange rates to and from additional functional currencies are captured and must have the ability to restate in multiple currencies.

5. Segment reportingIFRS requires separate sub-reporting for business unit or geographic segments. If they are not already doing this, fi rms will need to start tracking and associating all investment activities to the appropriate segments.

6. Risk reportingIFRS requires disclosures related to the nature and extent of risk exposure of investments. The types of risk that must be reported include liquidity risk, market risk, and currency risk.

Institutions wishing or obliged to cater to IFRS standards, either in addition to local standards or in replacement of these, will therefore not only be faced with the specifi cities of exceptions for Islamic fi nance and the additional rules that may be applied by their national regulator, but will also have to consider whether their current frameworks and systems can carry the strain of these new requirements.

Firstly, the system must allow fi rms to capture any additional data needed to ensure proper treatment and reporting of accounting results.

Secondly, the system must be fl exible enough to apply different sets of accounting rules to the same underlying data sets. And thirdly, the system must be able to present the results in ways that are compliant with both standards without ongoing manual intervention.

In spite of these challenges, IFRS is being applied today in more than 100 countries where its use is either required or permitted. The

major breakthrough occurred in 2002 when the European Union (EU) required all European-listed companies to adopt IFRS by 2005. Since then, several countries outside the EU have followed and IFRS has gained acceptance as a set of global standards specifi cally among multinational organizations.

However, convergence is not yet a reality within the Islamic fi nancial community, with a number of players opting for IFRS and a convergence of standards, some not permitting them, and others implementing them with local adaptations.

For example, IFRS are required for all listed companies in countries like the UAE or Egypt and permitted in Brunei and Yemen, but are not permitted in Indonesia, Iran or Pakistan. Libyan stock market regulations require the use of IFRS for all listed companies and the Libyan Banking Law requires the use of IFRS for all commercial banks, however, it would seem that they have yet to put IFRS in practice.

The Philippines are adopting IFRS as Philippines Financial Reporting Standards (PFRS), after various modifi cations were made. Malaysia has announced a plan to ‘bring Malaysian GAAP into full convergence with IFRS effective the 1st January 2012’.

Therefore, while the debate is still seemingly rife on global accounting standards for Islamic fi nance, the need for such standards has been widely acknowledged. The fi nancial crisis underlined the multiple connections and dependencies of conventional and Islamic fi nancial centres and helped build the momentum of a convergence towards internationally accepted and recognized standards, as a basis for higher quality reporting, transparency and comparability.

Used in conjunction with national standards which will cater to specifi c local practices, these widely recognized standards will in turn reinforce investor confi dence and favour international investments and economic growth.

Kaushiq KodithodikaRegional sales director, MENAAdvent SoftwareEmail: [email protected] Kaushiq Kodithodika has been working in the MENA region for 15 years, collaborating closely with a variety of Islamic fi nancial institutions. In his current position at Advent, his role is to identify clients’ needs and to have an ongoing dialogue with key players in the market and regulatory evolutions which impact clients’ businesses.

“The adoption of IFRS may have a transformational impact on fi nancial reporting systems, internal controls, taxes, treasury and cash management with an extended impact on employees, processes, and systems”

“Therefore, while the debate is still seemingly rife on global accounting standards for Islamic fi nance, the need for such standards has been widely acknowledged”

Page 16© 9th February 2011

www.islamicfi nancenews.comSECTOR REPORT

When most of the world accounts under IFRS, what should be AAOIFI’s role with regard to accounting standards?

At Islamic fi nance events, participants often ask whether Islamic fi nancial institutions should account under International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Boar d (IASB) or under the Financial Accounting Standards issued by the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI). While this question is common, a more fundamental question is “What is the proper role of AAOIFI with regard to accounting standards?”

AAOIFI was established after an agreement signed by various Islamic fi nancial institutions on the 26th February 1990 and was registered in Bahrain as an international autonomous non-profi t making corporate body on the 27th March 1991.

At that time, local country accounting standards were not well established in the Middle East and a need was clearly felt for the establishment of accounting standards for Islamic fi nancial institutions that would be harmonized across countries.

AAOIFI has also established a Shariah board which is highly respected, and is probably the leading global setter of Islamic fi nance Shariah standards. However the organization’s name clearly indicates that it regards its main focus as being accounting and auditing standards setting.

AAOIFI’s limited geographical reachThe 2010 edition of AAOIFI’s “Accounting, Auditing and Governance Standards for Islamic Financial Institutions” shows that AAOIFI’s Accounting and Auditing Standards Board is heavily dominated by the Middle East. The 15 members (ignoring the secretary general) come from only the following countries — Kuwait (1), Bahrain (5), Saudi Arabia (2), Lebanon (1), UAE (2), Jordan (1) and Qatar (1) with only Malaysia (2) from outside the Middle East.

A review of AAOIFI’s membership list published in the same volume shows that it has many member Islamic fi nancial institutions drawn from outside the Middle East. For example, both Kenyan Islamic banks (First Community Bank and Gulf African Bank) are members, and so are two (European Islamic Investment Bank and Gatehouse Bank) of the fi ve Islamic banks established in the UK. However it is striking that the other three UK Islamic banks do not feel any need to join AAOIFI.

Unlike the situation in 1990, by 2011 IFRS have become almost universally accepted in Europe, Asia, Oceania, Africa, Latin America and the Caribbean.

The only signifi cant country that still clings to its domestic accounting standards is the US, but the US accounting standards setter,

the Financial Accounting Standards Board (FASB) has signed a memorandum of understanding with the IASB with the purpose of converging FASB standards and IFRS. The goal of convergence is that well before the end of this decade US companies should account under IFRS.

Islamic fi nancial institutions are required to use the system of accounting standards which is mandated by the fi nancial services regulator of the country in which they are based.

Accordingly, Islamic fi nancial institutions based in the US must use FASB accounting standards, while almost everywhere else they account under IFRS, although limited time and the variable quality of English language information disclosure makes exhaustive verifi cation of this impractical.

However it is practical to review the position in the countries closest to AAOIFI’s base, namely the countries of the Gulf Cooperation Council (GCC). A review of published accounts for 2009 shows the following:

Country Islamic fi nancial institutions reviewed

Accounting standards used

Kuwait Kuwait Finance House IFRS

Bahrain Al Salam Bank-Bahrain AAOIFI

Qatar Qatar Islamic Bank AAOIFI

Saudi Arabia Al Rajhi Banking and Investment Corporation

IFRS

UAE (Dubai) Dubai Islamic Bank IFRS

UAE (Abu Dhabi) Abu Dhabi Islamic Bank IFRS

The writer understands that Oman does not have any Islamic banks (none are members of AAOIFI) although some websites list certain entities as offering Islamic fi nancial services. The accounts of one Omani bank, Oman Arab Bank SAOC, were reviewed. It accounts under IFRS although there is no indication from the accounts that it is an Islamic Financial Institution.

Accordingly, even within the GCC, AAOIFI accounting standards are used by only two countries, Bahrain, the country where AAOIFI is established, and its neighbor Qatar. All other GCC countries use IFRS. While both Bahrain are important countries for Islamic fi nance, they only represent a small minority of the global Islamic fi nancial services industry.

The purpose of accountingBefore drawing any conclusions from the almost universal non-use of AAOIFI’s accounting standards, it is helpful to consider the purpose of accounting. Both standard setting organizations have set out their views.

AAOIFI’s “Statement of Financial Accounting No. 1: Objectives of Financial Accounting for Islamic Banks and Financial Institutions” was published in 1993. The introduction to that statement says: “Financial accounting in Islam should be focused on the fair reporting of the entity’s fi nancial position and results of its operations, in a manner that would reveal what is halal (permissible) and haram (forbidden).

Section 6/2 of the standard sets out the objectives of fi nancial reports in six paragraphs of which the fi rst is “6/2(a) Information about the

AAOIFI’s Proper Accounting Standards RoleBy Mohammed Amin

continued...

“The two standard setting organizations have entirely different priorities”

Page 17© 9th February 2011

www.islamicfi nancenews.comSECTOR REPORT

AAOIFI’s Proper Accounting Standards Role (continued)

Islamic bank’s compliance with the Islamic Shariah and its objectives and to establish such compliance; and information establishing the separation of prohibited earnings and expenditures, if any, which occurred, and of the manner in which these were disposed of.”

In 2001 the IASB adopted its “Framework for the Preparation and Presentation of Financial Statements.” Paragraph 12 states: “The objective of fi nancial statements is to provide information about the fi nancial position, performance and changes in fi nancial position of an entity that is useful to a wide range of users in making economic decisions.”

These quotations demonstrate that the two standard setting organizations have entirely different priorities.

In the writer’s opinion, a key criterion for accounting is comparability; two organizations that carry out transactions which have identical economic effects should account for the transactions in the same way. Comparability breaks down when AAOIFI requires transactions to be accounted for differently from IFRS standards.

One simple example is leasing in cases where the asset is to be transferred to the lessee by a gift, Ijarah Muntahia Bittamleek, covered in AAOIFI’s FAS No 8 paragraph 2/2(a). AAOIFI requires the leased asset to be held on the lessor’s balance sheet and depreciated.

IFRS would clearly regard such a transaction as a fi nance lease, removing the asset from the lessor’s balance sheet and instead accounting only for a fi nance lease receivable.

What should AAOIFI be doing with regard to accounting?It is pointless for AAOIFI to continue to issue accounting standards in competition with the IASB, when those standards are going to be ignored outside a few countries.

This represents a waste of limited resources, and also reduces the comparability of Islamic fi nancial institutions’ accounts since AAOIFI accounts are not directly comparable with IFRS accounts.

AAOIFI’s accounting resources would be more usefully directed to collaborating with the IASB. The following goals come to mind immediately, although as the collaboration developed other goals would also most likely emerge:

1. Islamic banks accounting under IFRS will of course show the same numbers in their fi nancial statements and balance sheets as would conventional banks undertaking identical transactions. However Islamic investors need additional

information which is not mandated by IFRS, for example the amount on which they should pay zakat in respect of their shares. In most cases Islamic fi nancial institutions accounting under IFRS are likely to provide this information voluntarily; for example in its 2009 accounts the UK’s European Islamic Investment Bank provided a fi gure computed using AAOIFI’s standards. It would be desirable to have IFRS mandate a standard method of calculation for IFRS accounting entities that wished to make such a disclosure.

2. Muslims represent a growing proportion of the investor base of conventional non-fi nancial companies that account under IFRS. It would be desirable for such companies to give a voluntary disclosure in their accounting notes regarding the amount of their dividends that arise from sources that are regarded as impure by Shariah scholars, computed in a standardized way.

To conclude, while it may appear radical for AAOIFI to cease issuing accounting standards, this would enable it to become globally relevant by partnering with the IASB.

Mohammed AminIslamic fi nance consultantEmail: [email protected] Mohammed Amin MA FCA AMCT CTA (Fellow) was previously UK head of Islamic fi nance at PricewaterhouseCoopers.

“While it may appear radical for AAOIFI to cease issuing accounting standards, this would enable it to become globally relevant by partnering with the IASB”

MODERN FINANCIAL TECHNIQUESFOR ISLAMIC BANKING & FINANCE

www.IslamicFinanceTraining.com

KUALA LUMPUR11th – 13th April

8th - 10th MayCAIRO

14th - 16th JuneDUBAI

20th - 22th June

LAGOS

Page 18© 9th February 2011

www.islamicfi nancenews.comMARKET REPORT

Banking in Africa is becoming increasingly customer driven, with banks moving to tailor their products and services to meet the needs of people who have specifi c banking requirements. Nowhere is this truer than in Tanzania where Stanbic Bank, a subsidiary of the Standard Bank Group, has been proactively structuring new offerings to adhere to Islamic religious teachings.

In order to respond to the call for appropriate banking products from its Muslim community, Stanbic Bank Tanzania has conducted wide ranging research and cooperated with Islamic religious authorities, says Bashir Awale, the bank’s managing director. According to Awale, each new service and product developed involves an intensive process that begins within the bank where a committee meets regularly with Islamic scholars who are authorities in the interpretation of Shariah law as it applies to fi nancial services. “Shariah law governs the way in which Muslims follow their faith, conduct their lives and utilize their day-to-day fi nancial products, so the provision of banking facilities to the Muslim community must strictly conform to this system.”

At the base of the Shariah law is a requirement that is totally opposite to the way that Western banking has been conducted for hundreds of years. At the foundation was the establishment of a Shariah council, which oversees all operational issues regarding product delivery. This ensures the Shariah compliance of all products and services offered. The next step was to ensure that the most common banking products were developed fi rst. Accordingly, Stanbic examined those products primarily needed on an everyday basis, and so introduced transactional accounts to the Muslim community in Tanzania.

The fi rst product to be delivered was a ‘TransactPlus’, the fi rst transactional and cheque account in Tanzania that totally meets Shariah requirements. With its emphasis on convenience this product offers features such as internet banking, debit cards and the ability to access prepaid cellular phone services.

During the course of the new fi nancial year, Stanbic Bank will focus on developing and introducing a number of additional new products that will meet the diversifi ed needs of the Muslim community, whether they are customers interested only in transactional products or those conducting international businesses that trade across Tanzanian borders.

Although Islamic fi nance is progressively being integrated into the international fi nancial system, there is still a need for supervisory authorities and policy makers in emerging markets to become more involved in the process. Fazal Saib, the director of Shariah and specialized banking at Standard Bank Africa argues that a substantial investment of time will be needed to negotiate and develop an international Islamic fi nancial system.