Embed Size (px)

Citation preview

IMA Clearing House Day

ICE Clear Europe12 November 2013

CONFIDENTIAL – NOT FOR DISTRIBUTION

Legal Disclaimer

Forward-Looking Statements

This presentation may contain “forward-looking statements” made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Statements regarding our business that are not historical facts are forward-looking statements that involve risks, uncertainties and assumptions that are difficult to predict. These statements are not guarantees of future performance and actual outcomes and results may differ materially from what is expressed or implied in any forward-looking statement. For a discussion of certain risks and uncertainties that could cause actual results to differ from those contained in the forward-looking statements see our filings with the Securities and Exchange Commission (the "SEC"), including, but not limited to, the "Risk Factors" in our Annual Report on Form 10-K for the year ended December 31, 2012, as filed with the SEC on February 6, 2012. SEC filings are also available in the Investors & Media section of our website. All forward-looking statements in this presentation are based on information known to us on the date hereof, and we undertake no obligation to publicly update any forward-looking statements.

CONFIDENTIAL – NOT FOR DISTRIBUTION

Introduction and overview of ICE Clear Europe

Corporate Governance and Capital

Scope of clearing services: Type of Contract Client Account Options

Treasury Management: Collateral and Banking; CCP Investment Policy

Risk Management: Margin and Collateral Default Rules and Procedures

EMIR Trade Reporting

Agenda

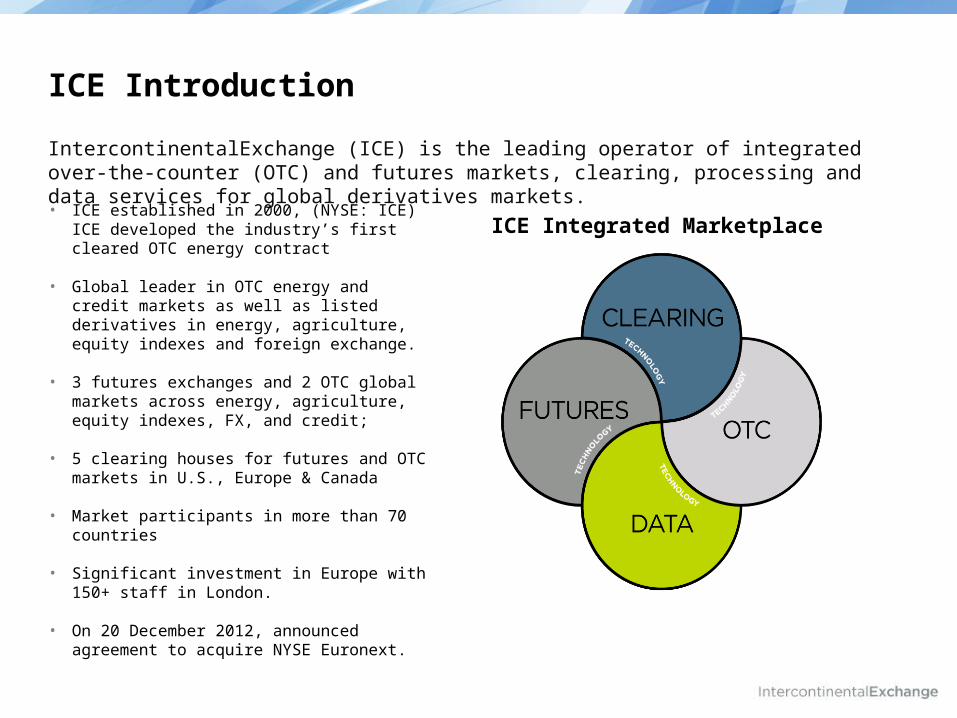

IntercontinentalExchange (ICE) is the leading operator of integrated over-the-counter (OTC) and futures markets, clearing, processing and data services for global derivatives markets.

ICE Introduction

• ICE established in 2000, (NYSE: ICE) ICE developed the industry’s first cleared OTC energy contract

• Global leader in OTC energy and credit markets as well as listed derivatives in energy, agriculture, equity indexes and foreign exchange.

• 3 futures exchanges and 2 OTC global markets across energy, agriculture, equity indexes, FX, and credit;

• 5 clearing houses for futures and OTC markets in U.S., Europe & Canada

• Market participants in more than 70 countries

• Significant investment in Europe with 150+ staff in London.

• On 20 December 2012, announced agreement to acquire NYSE Euronext.

ICE Integrated Marketplace

Introduction and overview of ICE Clear Europe

› ICE Clear Europe was established in 2008 and launched on 05 November 2008.

› ICE Clear Europe (ICE Clear) regulatory status is as follows:• Recognised Clearing House and systemically important payment system supervised by the Bank of England;• Designated under the Settlement Finality Directive;• Derivatives Clearing Organisation supervised by the U.S. Commodity Futures Trading Commission; and • Securities Clearing Agency supervised by the U.S. Securities and Exchange Commission.

› ICE Clear currently offers clearing and settlement services to:• ICE Futures Europe and ICE Futures US Energy Division contracts;• ICE Endex derivatives markets;• NYSE Liffe London derivatives markets; and • iTraxx Europe indices and Single Name OTC CDS contracts

› ICE Clear Europe has also developed a clearing service for OTC FX (focusing initially on NDFs) – this service has not yet gone live.

› ICE Clear Europe submitted an application for authorisation under EMIR to the Bank of England ahead of the deadline on 15 September 2013. The application is now subject to the necessary confidential regulatory process.

Introduction and overview of ICE Clear Europe

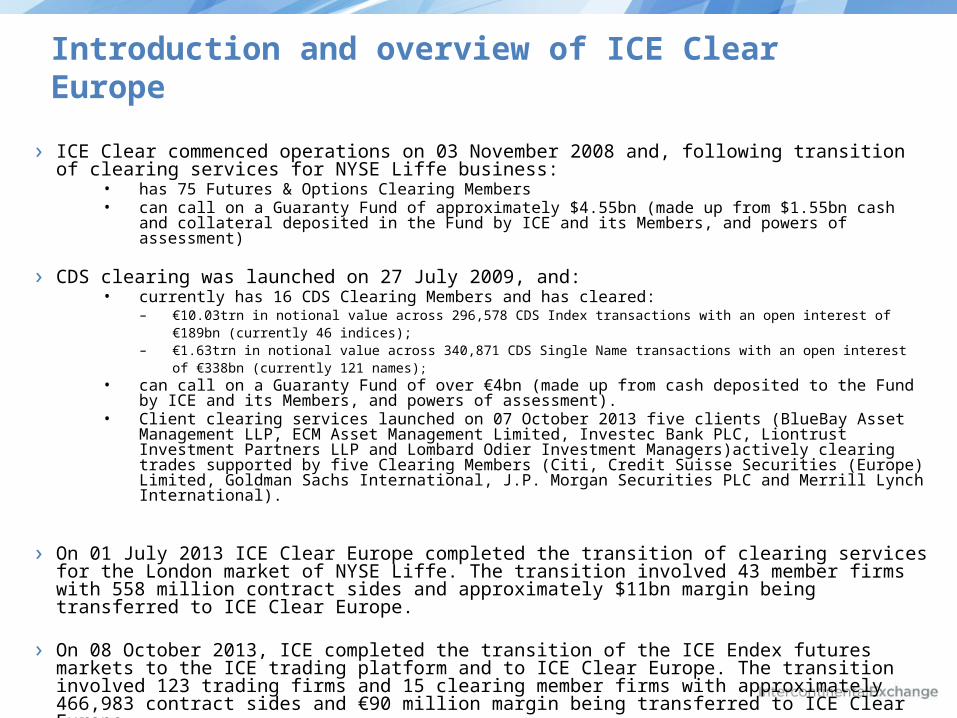

› ICE Clear commenced operations on 03 November 2008 and, following transition of clearing services for NYSE Liffe business:

• has 75 Futures & Options Clearing Members• can call on a Guaranty Fund of approximately $4.55bn (made up from $1.55bn cash and collateral deposited in

the Fund by ICE and its Members, and powers of assessment)

› CDS clearing was launched on 27 July 2009, and:• currently has 16 CDS Clearing Members and has cleared:

– €10.03trn in notional value across 296,578 CDS Index transactions with an open interest of €189bn (currently 46 indices);– €1.63trn in notional value across 340,871 CDS Single Name transactions with an open interest of €338bn (currently 121 names);

• can call on a Guaranty Fund of over €4bn (made up from cash deposited to the Fund by ICE and its Members, and powers of assessment).

• Client clearing services launched on 07 October 2013 five clients (BlueBay Asset Management LLP, ECM Asset Management Limited, Investec Bank PLC, Liontrust Investment Partners LLP and Lombard Odier Investment Managers)actively clearing trades supported by five Clearing Members (Citi, Credit Suisse Securities (Europe) Limited, Goldman Sachs International, J.P. Morgan Securities PLC and Merrill Lynch International).

› On 01 July 2013 ICE Clear Europe completed the transition of clearing services for the London market of NYSE Liffe. The transition involved 43 member firms with 558 million contract sides and approximately $11bn margin being transferred to ICE Clear Europe.

› On 08 October 2013, ICE completed the transition of the ICE Endex futures markets to the ICE trading platform and to ICE Clear Europe. The transition involved 123 trading firms and 15 clearing member firms with approximately 466,983 contract sides and €90 million margin being transferred to ICE Clear Europe.

CCP Governance and Capital

› ICE Clear Europe is a wholly-owned subsidiary of ICE Inc. and has an independent board which is chaired by Sir Bob Reid.

› ICE Clear has established separate Product Risk Committees for CDS, FX and Futures & Options. A Board Risk Committee will be established with representatives of customers in order to meet EMIR requirements.

› The Product Risk Committees are comprised of up to 15 participants and operate on delegated powers from the Board, including responsibility to:

– ensure that the Clearing House maintains and implements procedures, processes and controls which are designed to:• protect the integrity of the Guaranty Fund; • manage and mitigate credit and market risks;

– advise the clearing house in relation to its investment risk polices and the appropriateness of varying investment types;

– consider applications for membership; and– review the clearing of new products.

› ICE Clear Europe’s capital was $256mn at 31 December 2012 (made up from a combination of called-up share capital and reserves).

› ICE has entered into a senior unsecured loan facility which can provide $150mn to ICE Clear Europe for liquidity or required financial resources purposes.

EMIR Account Structure models

8

“H” Position Account1

HOUSE

SEGREGATED CLIENT ACCOUNTS(FCA Client Money Clients)

NON-SEGREGATED CLIENT ACCOUNTS(Title Transfer Collateral Arrangement – TTCA)

ICE CLEAR EUROPE

EU CLEARING MEMBER A4 SPONSORED PRINCIPAL

SP POSITIONS3

SP MARGIN3

SP ASSETS3

EMIR ARTICLE 39(3) COMPLIANT

“H” Margin Account

“H” Asset Account

SPONSOR

“S” Position Account

(Futures & Options)

“S” Margin Account

(Futures & Options)

“S” Position Account

(CDS)

“S” Margin Account

(CDS)

“S”Asset Account

(Futures & Options)

“S” Asset Account (CDS)

Individual Segregated

Position Account2

Individual Segregated

Margin Account2

Individual Segregated

Asset Account2

EMIR ARTICLE 39(2) COMPLIANT

EMIR ARTICLE 39(3)

COMPLIANT (SUBJECT TO

LEGAL ANALYSIS)

“T” Position Account

(Futures & Options)

“T” Margin Account

(Futures & Options)

“T” Position Account

(CDS)

“T” Margin Account

(CDS)

“T”Asset Account

(Futures & Options)

“T” Asset Account (CDS)

Individual Segregated

Position Account2

Individual Segregated

Margin Account2

Individual Segregated

Asset Account2

EMIR ARTICLE 39(2) COMPLIANT

EMIR ARTICLE 39(3)

COMPLIANT (SUBJECT TO

LEGAL ANALYSIS)

Key:Net margined

Gross margined

Notes:1. Multiple Position Accounts will be provided (H, G, L and U).2. Positions, Margin and Assets will be recorded on a per client basis.3. SP may be able to have additional administrative accounts in due course4. FCM Clearing Members will have alternative accounts (e.g. W, F and Z)5. CDS and Energy Accounts will be differentiate by different Clearing Member Mnemonics (e.g. ABC (Energy) and 123 (CDS))

CUSTOMER SPONSORED PRINCIPAL

Available Q2/3 2014

9

Omnibus Client Segregation (Gross Margin)

› Clearing Member is principal to the trade.

› Customer positions and assets are segregated from those of the firm (i.e. House).

› Customer positions are identified by customer legal entity via the Desk set up process.

› Margin is determined on a Customer-by-Customer basis and margin collected from the Clearing Member on a Gross basis.

› Gross Margin is computed at EOD* and CM meets any increase day over day; where one customer requirement goes up this may be netted against another customer’s requirements reducing.

› Customers share “fellow customer risk”: At Clearing House, collateral/assets not legally attributed to

Customer in terms of asset or value; Margin provided in respect of one customer can offset that on

another’s positions and gains or losses; one customer margin decrease may offset another’s increase;

Gross margin of customer account is potentially subject to mutualisation; Gross minus net amount is currently subject to enhanced protections;

Initial Margin (IM) calls, Variation Margin (VM) calls/pays are “netted” to a single call or pay per currency - Net VM payable to the CM can be used to cover increased margin requirements.

› Clearing Member can maintain “excess” buffer at Clearing House to “anticipate” changes in margin etc., but this is not attributable to individual clients.

* End of Day

Sponsored Principal Model – Key Features

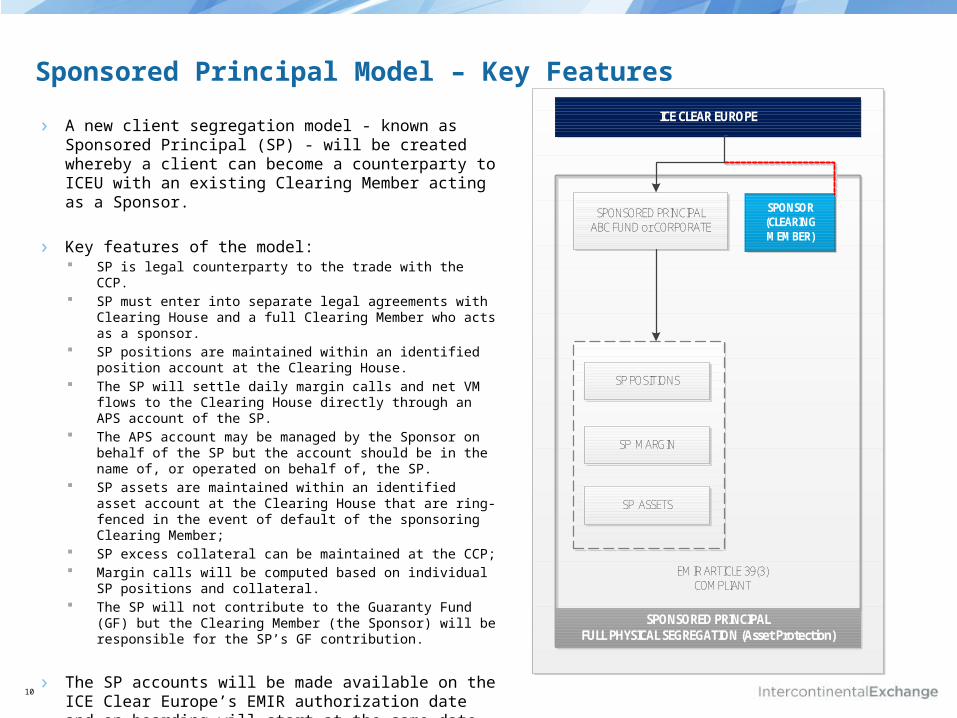

› A new client segregation model - known as Sponsored Principal (SP) - will be created whereby a client can become a counterparty to ICEU with an existing Clearing Member acting as a Sponsor.

› Key features of the model: SP is legal counterparty to the trade with the CCP. SP must enter into separate legal agreements with Clearing House

and a full Clearing Member who acts as a sponsor. SP positions are maintained within an identified position account at

the Clearing House. The SP will settle daily margin calls and net VM flows to the Clearing

House directly through an APS account of the SP. The APS account may be managed by the Sponsor on behalf of the

SP but the account should be in the name of, or operated on behalf of, the SP.

SP assets are maintained within an identified asset account at the Clearing House that are ring-fenced in the event of default of the sponsoring Clearing Member;

SP excess collateral can be maintained at the CCP; Margin calls will be computed based on individual SP positions and

collateral. The SP will not contribute to the Guaranty Fund (GF) but the

Clearing Member (the Sponsor) will be responsible for the SP’s GF contribution.

› The SP accounts will be made available on the ICE Clear Europe’s EMIR authorization date and on-boarding will start at the same date.

ICE CLEAR EUROPE

SPONSOR (CLEARING MEMBER)

EMIR ARTICLE 39(3) COMPLIANT

SPONSORED PRINCIPALFULL PHYSICAL SEGREGATION (Asset Protection)

SP POSITIONS

SP MARGIN

SP ASSETS

SPONSORED PRINCIPALABC FUND or CORPORATE

10

Individually Segregated Margin-flow Co-mingled Account (“ISOC”)

› ICE Clear Europe is also developing an Individually Segregated Margin-flow Co-mingled Account model - known as ISOC.

› In this model, the Clearing Member continues to act as principal to the positions but the Clearing House keeps a separate record of positions and assets at individual customer level.

› The proposed ISOC model seeks to leverage the LSOC workflow implemented in US for CFTC’s Dodd Frank requirements by enabling the separation of the process of asset deposit and withdrawal. Margin is attributed to each account, ultimate model will depend on outcome of current regulatory and industry deliberations: Option 1: accept only one class of asset (e.g. USD only), allowing all

customer accounts to have actual assets allocated based on value. Option 2: Clearing House asset reporting (once and if available) Option 3: Clearing Member’s own asset reporting. Option 4 (if CM asset report is invalid / incorrect): deemed allocation across

customers.

› In order to implement this model, ICE Clear Europe will require identification of trades on a per client basis as part of the clearing workflow.

› Please note that the ISOC model development is still in progress. Further detail describing all aspects of the model will be published when the model is finalized.

11

CLEARING MEMBER 2

EMIR ARTICLE 39(3) COMPLIANCE SUBJECT TO LEGAL ANALYSIS

HOUSE ACCOUNT

CLIENT ACCOUNT(S)

Client 2 POSITIONS

Client 1 POSITIONS

Client 1 MARGIN

Client 2 MARGIN

ASSETS (=Client 1 (including excess) + Client 2 + Client 3 + FIRM BUFFER + Unallocated Excess)

INDIVIDUALSEGREGATION MARGIN-FLOW CO-MINGLED (Asset Protection)

Client 3 POSITIONS

Client 3 MARGIN

ICE CLEAR EUROPE

Valuation and Margining

› In relation to its Futures & Options business:– ICE has entered into a licensing agreement with the Chicago Mercantile Exchange for the

use of SPAN. ICE Clear Europe uses the current version of SPAN (SPAN 4) for margin calculation purposes;

– ICE Clear manages market risk through Margin (Original, Variation and Intra-day) and through the F&O Guaranty Fund. The F&O Guaranty Fund is calibrated to meet Cover 2 requirements;

– ICE Clear offers inter-commodity margin offsets where appropriate and in line with the risk policies approved by the F&O Risk Committee;

– Segregation of client and house accounts fully supported.

› In relation to its CDS clearing business:– Dynamic Stress-Based Regime Specifically designed for CDS– Portfolio margining methodology (Index Decomposition) to provide capital efficiencies

between Index and Single Name contracts; and– EOD settlement process based on price submissions subject to execution ensuring fidelity of

quotes; – Margin Calculator provides transparency and detailed analysis of requirements– Guaranty Fund covers simultaneous default of 2 largest Clearing Members (Cover 2).

13

Risk Management Framework and Waterfall

*CM Default Related to Client Positions

1 Use of ‘net’ client account margin will be subject to further rulebook restrictions for LSOC

Membership Criteria

Initial Margin Requirement

Mark-To-Market Margin Requirement

Guaranty Fund

Intra-day Risk Monitoring Special Margin Call Execution

Additional Assessment Rights

Ensure CM has sufficient financial resources, operational capabilities and risk management

experience

Daily margin call based on dynamic stress test regime

Daily MTM based on EOD settlement prices

Additional margin can be called unusual market fluctuations

Additional collateral to mutualise losses under extreme market scenarios

Oblige Clearing Members to contribute additional default funding

Layers of Protection

1. Close-out gains

2. Customer Account net margin

3. Defaulting CM’s Guaranty Fund

4. Surplus collateral and ‘gross minus net’ margin of out-of-the money customers

8. Assessment contributions of CM’s

7. Non-defaulting CM’s GF / ICE pro rata GF

6. ICE Priority Guaranty Fund (GF)

Application of Assets in Net Sum Calculation*

5. Defaulting CM’s House account margin surplus

If the net sum represents a shortfall …

If the net sum represents a shortfall …

13

Treasury Management

› ICE Clear Europe has appointed JPMorgan Chase Bank NA (JPMorgan) and Citi as its consolidation banks which perform transaction processing, investment management and safe custody services. The Bank of England is used for pounds sterling (GBP) concentration of funds.

› ICE Clear Europe has developed the Assured Payment Service (APS) which provides payment finality for transfers between ICE Clear Europe and Clearing Members. The APS has been designated under the Settlement Finality Directive and is a payment system under the U.K. Banking Act 2009 regulated by the Bank of England

› Current acceptable collateral includes:– Cash – EUR, GBP and USD (Initial Margin and Variation Margin);– Cash – CAD, CHF, SEK, JPY, NOKO, DKK, HUF, CZK, PLN, TRY and ZAR (Variation Margin only)– Government Securities – U.S., European and Japanese Governments only;– Letters of Credit / Pass-through Letters of Credit– Gold Bullion– Emissions Allowances– Triparty arrangements through Euroclear.

› ICE Clear Europe’s APS Banks are currently (July 2013):– Bank of America NA (London Branch)– Barclays Bank plc– Brown Brothers Harriman & Co. (New York Branch)– Citibank NA (London Branch)– Deutsche Bank AG (London Branch)– HSBC Bank plc– JP Morgan Chase Bank NA (London Branch)– Skandinaviska Enskilda Banken AB (London Branch)

CCP Investment Policy

› The main objective of our investment policy is to manage the cash balances deposited by Clearing Members ensuring capital preservation, risk diversification and intraday liquidity.

› The Board has approved the Investment Policy.

› Investments are done via two agents: Citibank and JP Morgan.

› Under the terms of the Investment Policy, the main products used are triparty reverse repos, outright purchase of sovereign debt and time deposits. Typically, at least 99% of all our investments are collateralized.

› Collateral is held in ICE Clear Europe accounts at relevant custodian.

› Further information can be found at: https://www.theice.com/clear_europe_treasury.jhtml

EMIR Trade ReportingOverview

› The European Markets Infrastructure Regulation (EMIR) mandates the reporting of derivatives contracts to Trade Repositories (“TRs”).

› All EU counterparties (financial and non-financial counterparties and CCPs).

› All derivative contracts (OTC, cleared swaps, exchange-traded futures and options).

› All asset classes (equities, interest rates, FX, commodities, credit).

› Reporting to TRs no later than one working day following conclusion, modification or termination.

› To fulfil the reporting requirements, counterparties may:

› Report trades to a TR themselves;

› Delegate reporting to the other counterparty to the trade;

› Delegate reporting a third party, including a CCP.

› On 7 November 2013, ESMA announced the registration of the first TR. The registration will take effect on 14 November and, as a result, the reporting obligation will begin on 12 February 2014 (90 calendar days after the registration date).

ICE Trade Vault Europe› ICE Trade Vault will offer a full trade repository service for all cleared derivatives in the commodities, interest rate, CDS and equity asset

classes, and initially, OTC commodities and CDS trades, with other OTC asset classes to follow, all subject to approval by ESMA.

› Application filed with ESMA on 26 March 2013. Now working with ESMA to complete application and have verbal acknowledgement that upon receipt of final documents, ESMA will recommend approval. Therefore, we anticipate that ICE Trade Vault Europe’s trade repository registration could be granted very shortly.

ICE’s Cleared Derivatives Delegated Reporting Services

› ICE intends to provide delegated reporting services for both Clearing Members and market participants:

› Any derivatives (both exchange-traded and OTC) cleared by an ICE Clearing House (ICE Clear Europe, ICE Clear US, ICE Clear Canada and ICE Clear Credit).

› All trades, positions and lifecycle events.

› Daily valuation and collateral updates.

› Historical reporting requirement for Clearing Members1.

› All reporting directly to ICE Trade Vault Europe2.

1 Where market participants would like ICE to fulfil their historical reporting obligations, ICE will work with the market participant and their Clearing Member to achieve this in the most efficient way possible.2 Subject to ESMA authorisation of ICE Trade Vault Europe.

Contacts

Roger BartonBoard Director & Chairman of the Futures and Options Risk CommitteeICE Clear Europe+44 (0)20 7012 [email protected]

Mark Woodward Director, Corporate DevelopmentICE Clear Europe+44 (0)20 7065 [email protected]