Embed Size (px)

Citation preview

NGX Secure Trading & ClearingAn Introduction to Commodities Clearing

Executive Summary

• NGX is an established electronic Natural Gas & Crude Oil Exchange and Clearinghouse

– Over 200+ contracting parties (members) across North America

– Clearing over $8 billion monthly of physical gas, crude and financial power

– Delivering over 14 Bcf of physical gas & 400,000 bpd

– Capital structure includes full margining, settlement bank credit facility and emergency fund

– Owned by TMX Group Inc., combination of Toronto Stock Exchange and Montreal Exchange

– Clearing bank and regulatory oversight

– Zero-default history

• NGX’s value proposition is twofold– For Traders: optimize counterparty access, maintain anonymity

– For Risk Managers: reduce overall risk, maximize capital and operational efficiency

• NGX’s ‘direct’, non-mutualized clearing model is ideally suited to the trading and clearing of physical energy commodities

2

Sections

• Overview

• Clearing Structure

• Risk Management

• Contacts

3

Introduction to NGX

• Business Concept:– Provide electronic trading and clearing services to North

American energy market participants– NGX is a service provider and therefore does not trade or

take positions

• Headquartered in Calgary, Alberta, Canada

• Incorporated in 1993, began trading operations in Feb 1994

• Ownership History– Initial Ownership by Westcoast Energy Inc.– Acquired by OM on Jan 1, 2001– Acquired by TSX Group March 1, 2004– Acquired NetThruPut on May 1, 2009

4

NGX Core Competencies

• Clearinghouse Operations– Physically and financially settled over 1,400,000 trades– Zero-default history

• Liquidity Development– Focus on customers and quality of service– Commitment to the reduction of trading impediments

• Electronic Trading & Clearing– Over 15 years of experience developing and operating high-

reliability, high-performance electronic trading and clearing systems

– Trading now available through the InterContinental Exchange (ICE) leading-edge trading platform

5

NGX Services

• Exchange– Centralized electronic trading– Standardized contracts– Pipeline balancing instruments– Cleared and bilateral trading – Market advocacy (facilitating transactions)– Market agency (facilitating order entry)– Real-Time Price Index Generation

• Clearing House– Assured performance– Trade and counterparty netting– Centralized collateral management– Centralized risk management

6

Operational & Clearing Statistics

• Currently 200+ NGX Contracting Parties– All “Member” firms eligible to transact through the Exchange and/or clear through the

Clearing House

• 2008 Gas Trading Statistics:– Volume = 14.46 Tcf– Transactions = 286,729

• Average Daily Gas Deliveries in Excess of 14.0 Bcf

• Cleared Transactions – Notional value of transactions consummated through NGX is in excess of CAD $80

Billion annually

• Margin– Over 200 corporate margin accounts held by NGX– Manage margin accounts in excess of CAD $4.0 Billion in cash and letters of credit

• Settlement– Settlement of $US and $CAD cash streams– Monthly settlement values over CAD $2 Billion processed by the clearing house

7

Sections

• Overview

• Clearing Structure

• Risk Management

• Contacts

8

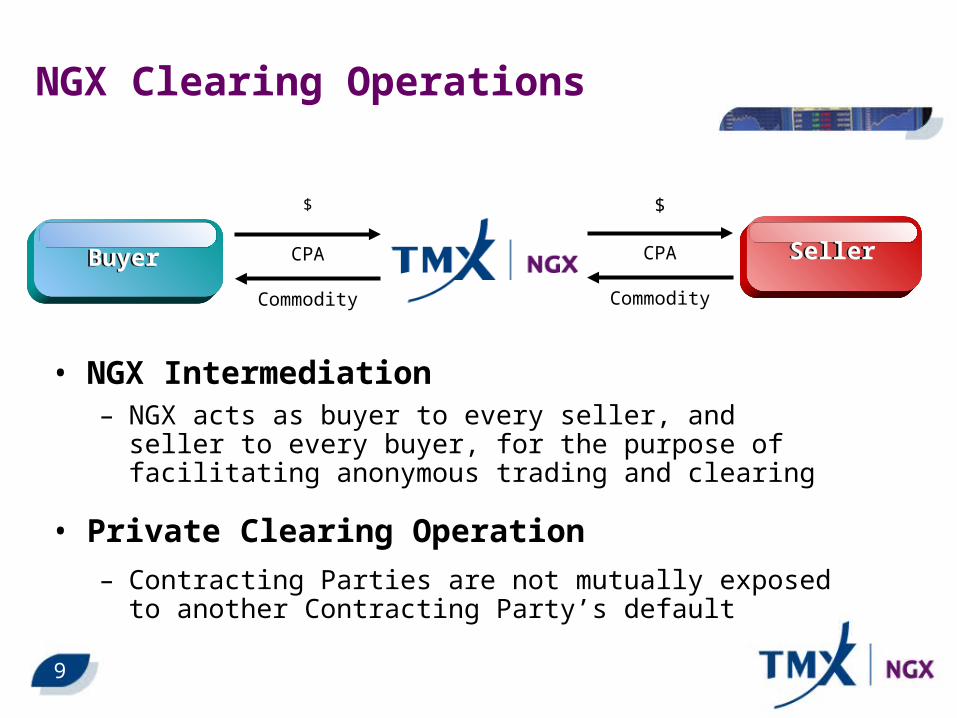

NGX Clearing Operations

• NGX Intermediation– NGX acts as buyer to every seller, and seller to every buyer,

for the purpose of facilitating anonymous trading and clearing

• Private Clearing Operation

– Contracting Parties are not mutually exposed to another Contracting Party’s default

$

Commodity

CPA

$

Commodity

CPABuyerBuyer SellerSeller

9

How is Counterparty Risk Mitigated?

• Standard Rules– All Contracting Parties are subject to the same rules and

regulations as set forth in the CPA– Contracting Parties must meet minimum creditworthiness test and

meet credit requirements on an ongoing basis

• Collateral Provisions– The requirement for liquid collateral to be placed on deposit with

NGX in advance and in excess of margin requirements provides the security against default

• Liquidation Rights– NGX has a number of rights if a Contracting Party default occurs,

including the ability to close-out (or accelerate) all forward positions for the defaulting party

– Collateral is utilized to cover any liquidated damages

10

How is Counterparty Risk Mitigated?

• Backstopping– Delivery risks are mitigated through the use of backstopping

services provided by various market participants, including storage facilities, large shippers, and pipeline operators

– Backstopping is typically an arrangement for immediate provision of supply/market at a pre-determined price (usually based on index)

• Settlement Bank– The settlement bank daylight and overdraft facilities provide for

clearing operation liquidity during a default situation and assist in managing timing issues on settlement day

• Guarantee Fund– NGX provides a USD $100 million trust fund for Contracting Parties

to access in the event of an exchange default

11

NGX Clearing Structure

Physical Backstopping

Settlement Banking Credit Facility

Defaulting Party Collateral (100% Coverage Under NGX Exposure Model)

NGX Cash Reserves

NGX Guarantee Fund (USD$100MM CIBC Mellon Trust)

Deposit Agreement

$

Commodity

$

Commodity

PayerPayer PayeePayee

Deposit Agreement

12

Value Proposition of Clearing

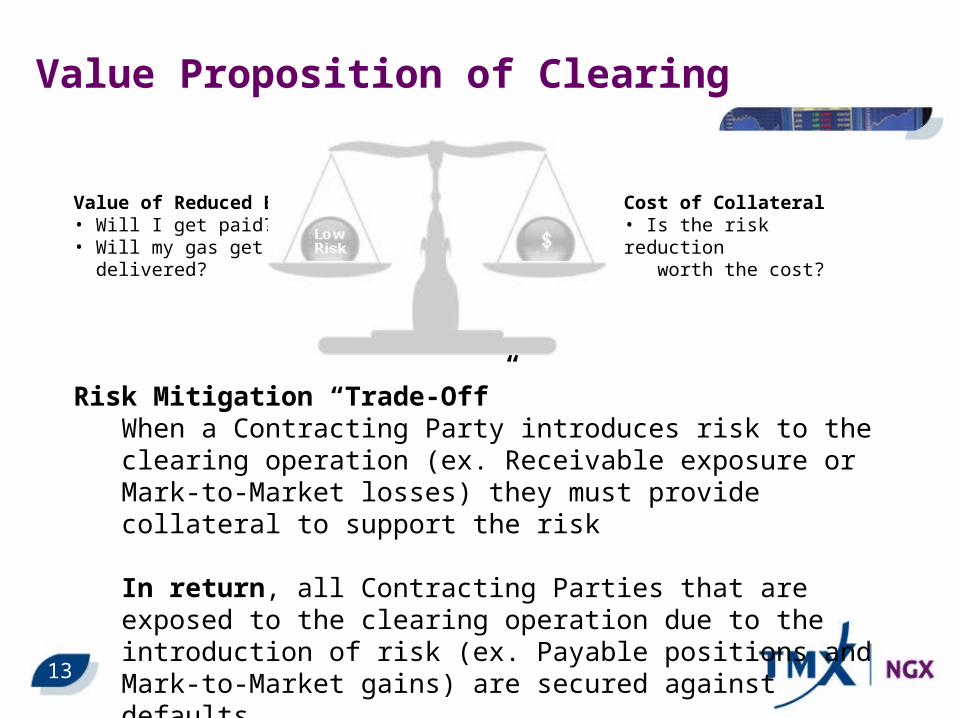

Value of Reduced Exposure • Will I get paid?• Will my gas get delivered?

Cost of Collateral • Is the risk reduction worth the cost?

Risk Mitigation “Trade-Off”When a Contracting Party introduces risk to the clearing operation (ex. Receivable exposure or Mark-to-Market losses) they must provide collateral to support the risk

In return, all Contracting Parties that are exposed to the clearing operation due to the introduction of risk (ex. Payable positions and Mark-to-Market gains) are secured against defaults

13

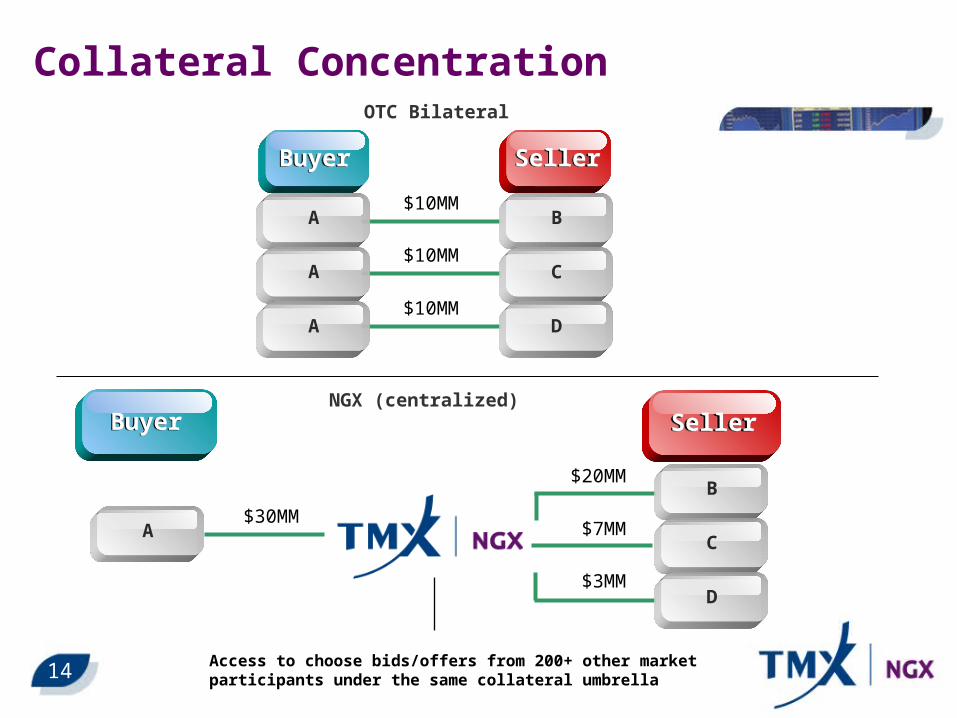

Collateral Concentration

NGX (centralized)

$3MM

$20MM

$30MM$7MM

OTC Bilateral

$10MM

$10MM

$10MM

A

A

A

B

C

D

B

C

D

A

BuyerBuyer SellerSeller

BuyerBuyer SellerSeller

Access to choose bids/offers from 200+ other market participants under the same collateral umbrella14

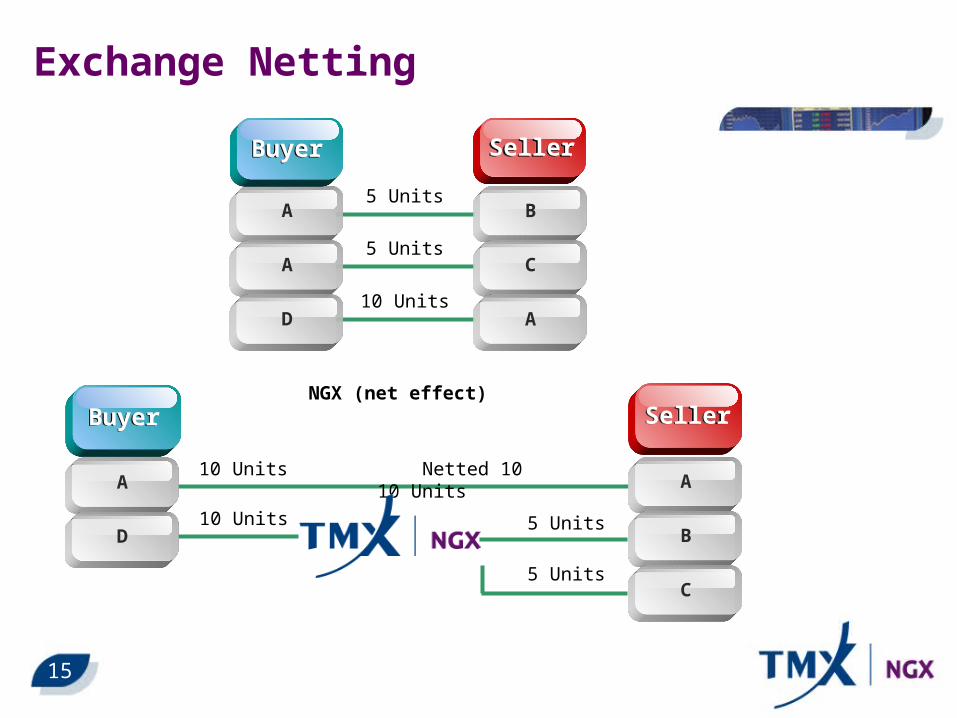

Exchange Netting

5 Units

5 Units

10 Units

A

A

D

B

C

A

NGX (net effect)

5 Units

10 Units Netted 10 10 Units

10 Units 5 Units

A

B

C

A

D

BuyerBuyer SellerSeller

BuyerBuyer SellerSeller

15

Sections

• Overview

• Clearing Structure

• Risk Management

• Contacts

16

Performance Risks

• Failure to Make/Take Delivery– NGX is exposed to the price at which an alternative supply/market can be

found – Risk is managed with backstopping contracts, penalty mechanisms,

collateral requirements and credit policy

• Failure to Pay– NGX is exposed to receivables risk on settlement dates– Risk is managed with penalty mechanisms, collateral requirements and

credit policy

• Failure to Provide Collateral– NGX is exposed to the risk that Contracting Parties will not provide sufficient

collateral to manage their risks– Risk is managed with liquidation provisions

17

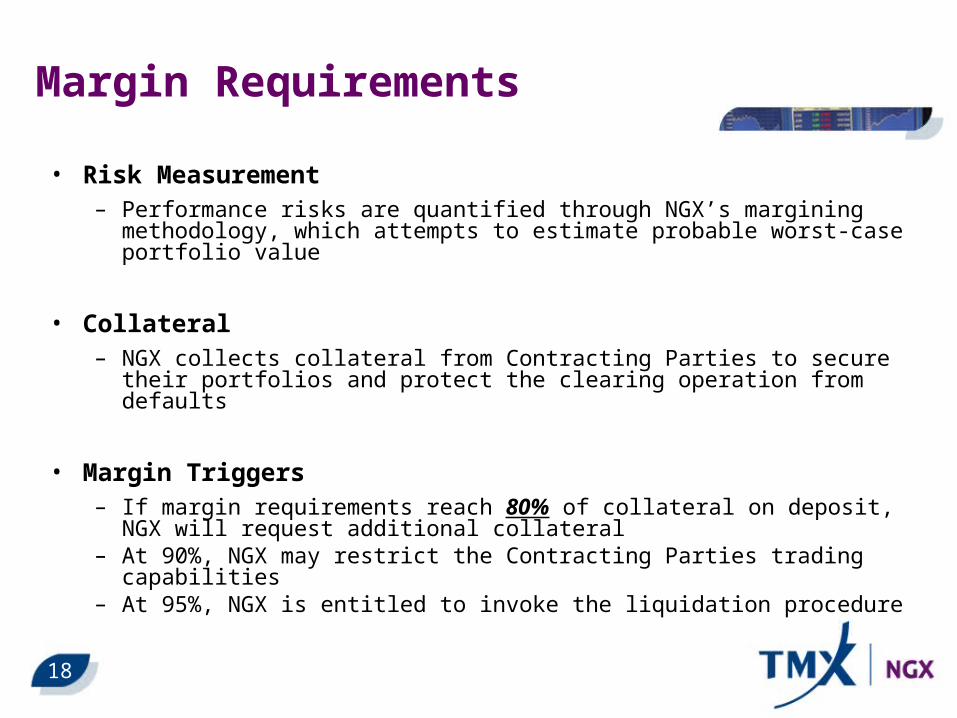

Margin Requirements

• Risk Measurement– Performance risks are quantified through NGX’s margining methodology,

which attempts to estimate probable worst-case portfolio value

• Collateral– NGX collects collateral from Contracting Parties to secure their portfolios

and protect the clearing operation from defaults

• Margin Triggers– If margin requirements reach 80% of collateral on deposit, NGX will

request additional collateral– At 90%, NGX may restrict the Contracting Parties trading capabilities– At 95%, NGX is entitled to invoke the liquidation procedure

18

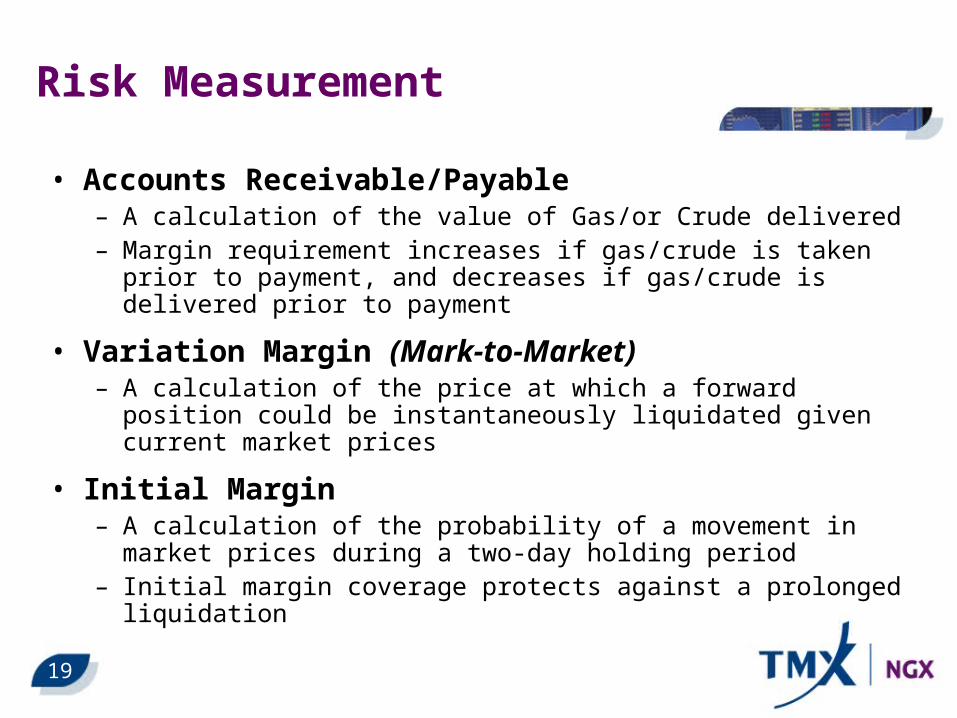

Risk Measurement

• Accounts Receivable/Payable– A calculation of the value of Gas/or Crude delivered– Margin requirement increases if gas/crude is taken prior to

payment, and decreases if gas/crude is delivered prior to payment

• Variation Margin (Mark-to-Market)– A calculation of the price at which a forward position could be

instantaneously liquidated given current market prices

• Initial Margin– A calculation of the probability of a movement in market prices

during a two-day holding period– Initial margin coverage protects against a prolonged liquidation

19

Contacts for Further Information

Dan Zastawny – Vice President, Clearing & Compliance403.974.4335, [email protected]

Matt Frye – Vice President, U.S. 832.978.9835, [email protected]

Janelle Dormaar – Clearing Manager403.974.1763, [email protected]

_____________________Natural Gas Exchange Inc.Suite 2330, 140 - 4th Avenue SWCalgary, AlbertaCanada T2P 3N3

Phone: 403.974.1700Fax: 403.974.1719www.ngx.com